The Impact of Foreclosures on Economic Recovery in Virginia

|

|

|

- Marian Cannon

- 5 years ago

- Views:

Transcription

1 The Impact of Foreclosures on Economic Recovery in Virginia February, 2012 Brian Koziol Housing Policy and Research Analyst Where you live makes all the difference

is Virginia s premier fair housing organization offering a variety of programs and services designed to ensure equal access to housing for all Virginians.")

2 About Housing Opportunities Made Equal (HOME) HOME's mission is to ensure equal access to housing for all people. Housing Opportunities Made Equal of Virginia, Inc. (HOME) is Virginia s premier fair housing organization offering a variety of programs and services designed to ensure equal access to housing for all Virginians. For the past 40 years, HOME has worked to unlock doors closed by housing discrimination. HOME is a 501(c)(3) nonprofit corporation and a HUD approved housing counseling agency. HOME s Center for Housing Leadership produces high quality public policy analysis and research to evaluate housing opportunity in Virginia. Research at the Center for Housing Leadership is made possible by a grant from Wells Fargo. HOME was founded in 1971 to fight discrimination in housing access. By working to promote financial literacy and the proper use of credit, HOME helps create responsible consumers. By ensuring that the fair housing laws are enforced, HOME helps give businesses the confidence that housing will be available for all their employees. By working to give every family access to good neighborhoods and good schools, HOME helps create a well educated workforce for the future. And by helping to prevent foreclosures and giving families the tools they need to be long term sustainable homeowners, HOME helps to avoid disruptions in the workplace and to create a stable workforce. 626 East Broad Street, Suite 400 Richmond, VA HOME s research is made possible in part by the financial support of Wells Fargo

3 Executive Summary From 2010 to 2011, the total number of foreclosures declined 32% (64,975 to 43,637). This is the first decrease since the collapse of the housing market in However, foreclosures remain 1,000% greater than in 2006 before the recession. (Page 2) The percentage of subprime mortgages resulting in foreclosure continues to increase. Subprime loans account for the majority of loans that are 90 or more days delinquent. Between the third quarter of 2010 and the third quarter of 2011, this segment of foreclosures increased by 51%, accounting for over 12% of all foreclosures in Since minorities and lower income households were specifically targeted for subprime mortgages, the economic outlook for these households is further marginalized. (Page 3) From 2000 to 2010, residential vacancies increased 30%. Vacant properties accounted for 9% of the total housing stock in Foreclosures have created an excess supply of vacant properties which have driven down the value of homes. The foreclosure crisis, particularly the resulting surplus of vacant properties, continues to be a major obstacle to the recovery of the housing market. In the last two years alone, Virginia homeowners who lived in close proximity to a vacant property lost $26 billion in home equity. (Page 2) Declining property values have placed numerous homeowners underwater, or owing more on their mortgage than their home is currently worth. Approximately 23 percent of Virginians with a mortgage are underwater. The median sale price for homes has decreased 21% from $280,000 in the first quarter of 2006 to $220,000 in the last quarter of (Page 2) Servicing issues between mortgage lenders and borrowers continue to cause unnecessary foreclosures. Federal changes have attempted to resolve dual tracking issues in the HAMP program. The majority of loan modifications in Virginia occur outside of the HAMP program, leaving numerous Virginians unprotected from dual tracking and other bad servicing policies. (Page 3) Regional analysis including foreclosures, vacancies, and unemployment are located on pages

.")

4 Virginia Foreclosures 2011 was the first year to see a significant decline in overall foreclosure activity since the housing market collapse in Statewide, from 2010 to 2011, the number of foreclosures decreased 32% from 64,975 to 43, Regardless of this contraction, foreclosures remain 1,000% higher than they were in 2006 (Chart 1). 2 Foreclosures continue to be an obstacle to housing market recovery in Virginia, as the weak housing market is a drag on economic growth. Chart 1: Foreclosure Foreclosure Filings Filings by Total by Total Volume, Volume, ,000 60,000 50,000 40,000 30,000 20,000 10, Source: RealtyTrac.com Foreclosures have effected Virginia s housing market in two specific ways. First, foreclosures led to vacancies. In turn, vacancies are known to lead to increased vandalism, crime, and the continued downward spiral of home prices. 3 In 2010, the number of vacant homes accounted for 10% of all homes in the state a 30% increase from It is estimated that in the last two years alone, Virginia In the last two years alone, Virginia homeowners who lived in close proximity to a vacant property lost $26 billion in home equity. REO NTS homeowners who lived in close proximity to a vacant property lost $26 billion in home equity. 5 Second, the surplus of vacant homes resulting from foreclosure have exerted tremendous downward pressure on home prices throughout the Commonwealth. From 2007 to the end of 2011 the median home sale price has declined by 21%, from $280,000 to $200,000 (Chart 2). Chart Median 2: Median Home Home Sale Sale Price Price, Jan 2007 Jan to 2007 Sept $300,000 $250,000 $200,000 $150,000 $100,000 $50,000 $ 2007, 2007, 2008, 2008, 2009, 2009, 2010, 2010, 2011, 2011, Source: Virginia Association of Realtors. Median Home Sales Price This two pronged attack on property values has placed numerous homeowners throughout the Commonwealth underwater, or owing more on their mortgages than their home is currently worth. A report issued last year placed Virginia 8 th highest in the nation in terms of the number of homeowners underwater. 6 It is estimated that 32 percent of Virginians with a mortgage are underwater. 7 When faced with an economic crisis such as losing a job or a catastrophic illness, underwater homeowners are unable to utilize normal market clearing actions such as selling their home or refinancing their mortgage. Increasingly, those families who have lost their homes to foreclosure find it difficult to obtain affordable rental housing. Many rental markets throughout the Commonwealth have tightened considerably over the past several years driving up rental 2

5 costs. Moreover, in response, the industry has significantly restricted lending, making it more difficult for the average borrower to get a loan. The restrictions on lending, coupled with the surplus of vacant housing has caused numerous issues for local governments, such as decreased tax revenue and increased costs associated with maintaining abandoned and vacant properties. The effects of the foreclosure crisis have been perpetuated by several factors, including loan servicing issues such as improper documentation, forged signatures, and dual tracking. Dual tracking, is a common practice used by mortgage lenders who begin foreclosure proceedings while simultaneously negotiating a loan modification with a homeowner. This practice proved to be a significant issue in a survey of Virginia Association of Housing Counselors conducted by HOME in the fall of This survey found that 87% of housing counselors had clients who were foreclosed upon before their loan modification process was complete. 8 Federal regulations have worked to address these issues with mixed results. For example, dual tracking is not allowed under the Home Affordable Modification Program (HAMP). However, the vast majority of loan modifications are occurring outside the regulatory authority of HAMP. During the third quarter of 2011 only 37.4% of loan modifications occurred through HAMP. 9 This leaves numerous Virginians unprotected from bad servicing policies such as dual tracking. Mortgage Loan Performance and Economic Indicators The effects of subprime lending continues to contribute to the foreclosure crisis. Subprime loans are those loans extended to borrowers that do not qualify for prime loans based on their credit worthiness. Many of these loans have introductory teaser interest rates for 2 or 3 years before they reset at significantly higher interest rates. Interest only loans guarantee low monthly payments by postponing repayment on the principal. Fortunately, the frequency with which these loans are being originated has diminished significantly over time. Examining Home Mortgage Disclosure Act Data (HMDA) from 2004 to 2010 reveals that subprime lending in Virginia peaked in 2006; 17.2% of loans made that year were subprime. 10 Since that time, subprime lending has decreased dramatically; subprime loans accounted for less than 2% of loans originated in Unfortunately, the deleterious effects of subprime mortgages are still hurting Virginia s economy. As these teaser rates expire, homeowners are unable to make payments at the higher interest and are going into default and eventually foreclosure. Subprime loans account for the majority of % 90+ days past due Chart 3: Percent of Loans 90 Days or More Past Due 2nd Qrt rd Qrt th Qrt st Qrt nd Qrt rd Qrt th Qrt st Qrt nd Qrt rd Qrt th Qrt st Qrt nd Qrt rd Qrt Prime Sub Prime Interest Only Source: Federal Reserve Bank of Richmond. Loan Processing Services Inc. Applied Analytics Mortgage Data 3

6 loans 90 or more days delinquent (Chart 3), and they are more likely to result in foreclosure. It is of grave concern that while the overall number of foreclosures has declined over the past year, the percentage of subprime mortgages going into foreclosure continues to increase (Chart 4). Subprime and interest only loans are typically reserved for individuals with less than favorable credit and characterized by higher interests rates and other terms to compensate for increased risk to the lender. Research has shown that these loans were often made in a discriminatory and predatory manner to predominantly lower income, minority borrowers with little regard for the long term sustainability of such practices. 12 Recently, the U.S % in Foreclosure Chart 4: Percent of Loans in Foreclosure 2nd Qrt rd Qrt th Qrt st Qrt nd Qrt rd Qrt th Qrt st Qrt nd Qrt rd Qrt th Qrt st Qrt nd Qrt rd Qrt Prime Sub Prime Interest Only Source: Federal Reserve Bank of Richmond. Loan Processing Services Inc. Applied Analytics Mortgage Data Department of Justice reached a $335 million settlement over lending discrimination by Countrywide Financial for placing African American and Hispanic borrowers into subprime loans and charging them higher fees. 13 Research has shown that these loans were often made in a discriminatory and predatory manner to predominantly lower income, minority borrowers with little regard for the long term sustainability of such practices. Because of such practices, minority neighborhoods throughout the Commonwealth have experienced up to five times as many foreclosures as non minority neighborhoods. 14 Over the next year, more of Virginias homeowners with subprime mortgages may lose their homes to foreclosure. These foreclosures will continue to impede robust economic recovery. Loss mitigation efforts have done much to keep paying borrowers in their homes. The lower than expected total number of loan modifications through the HAMP program is offset by the fact that HAMP modifications have outperformed other modifications 70.5% to 55.7% respectively. 15 Thus, the chance of a HAMP modified loan going into foreclosure is significantly less than for other types of loan modifications. This is due in large part to the significant reduction in monthly payments offered by the HAMP program. 16 To date the HAMP program has helped keep over 34,000 Virginians in their homes. 17 It is expected that the number of loan modifications will continue to decrease as the pool of qualified applicants applying for loan modifications will continue to decline. 4,500 4,000 3,500 3,000 2,500 2,000 1,500 1, Loan Modifications Chart 5: Loan Modifications by Type 2nd Q rd Q th Q st Q nd Q 2011 Source: OCC Mortgage Metrics Report Hamp Other 4

7 Looking Forward Some relief may be on the horizon as the percentage of loans that are 90 days or more past due appears to be stabilizing, if not declining. More importantly, the percentage of subprime loans that are 90 or more days past due has declined significantly from its peak in late 2009 to early 2010, from 22% to 13%. As the economy continues its protracted recovery and unemployment continues to decrease, the percentage of homeowners who are unable to make their monthly mortgage payments due to unemployment or underemployment will continue to decline Unemployment Rate Jan to Oct Chart 6: Unemployment Rate Jan Oct January 2007 April 2007 July 2007 October 2008 January 2008 April 2008 July 2008 October 2009 January 2009 April 2009 July 2009 October 2010 January 2010 April 2010 July 2010 October 2011 January 2011 April 2011 July 2011 October Source: Virginia Employment Commission (Chart 6). It is too early to predict with any accuracy the state of the foreclosures in the coming months and years. Though foreclosures decreased dramatically over the past year, thanks in large part to the stabilization of the unemployment rate and a marginally growing economy, Virginia s housing market remains stagnant. Even accounting for seasonal variations, the general trend in homes sales has been downward (Chart 7, see the blue trend line). This may signify a housing market that has reached the bottom and will begin to gradually recover in the coming years. It could also signify a market Chart 7: Quarterly Quarterly Residential Residential Sales, Qtr.1, 2007 Qtr. Sales 3, ,000 30,000 25,000 20,000 15,000 10,000 5, , 2007, 2008, 2008, 2009, Source: Virginia Association of Realtors 2009, 2010, 2010, 2011, 2011, that is still adjusting and will not begin to recover for some time. Given the decline in median sale prices and the vast inventory of vacant real estate, it is doubtful that the housing market will grow dramatically in the coming year unless there is strong employment growth. Now that many facets of the foreclosure crisis have begun to stabilize, it is important to continue mitigating unnecessary foreclosures. With unemployment slowly decreasing, loss mitigation activities by mortgage servicers and lenders should see more success. Loan modifications should be more successful and will allow Virginia s homeowners to retain the equity in their homes. More households in Virginia are in a better financial position than they were during the worst of the Great Recession. Policies that address servicing issues such as dual tracking and promote loss mitigation will help stabilize Virginia s housing market and promote economic growth. 5

8 Recommendations on Foreclosures and Mortgage Lending Expand funding for foreclosure prevention counseling. The more Virginia homeowners who are able to pursue loss mitigation instead of foreclosure, the better the outlook for economic growth. Many Virginians going through foreclosure are still unprotected from dual tracking. Ending dual tracking in Virginia will ensure that unnecessary foreclosures do not further weaken the housing market. Stabilizing employment means that loss mitigation activities should be more successful for financial institutions. Mortgage servicers should expand efforts to grant loan modifications to Virginians who are working their way through the process. Increase investments in housing counseling for first time homebuyers and downpayment assistance to help low and moderate income Virginians qualify for prime mortgages. Neither the financial institutions, nor the borrowers were well served by subprime mortgages. Mortgage lenders and originators should remain wary of subprime loans. Ensuring that Virginias homeowners qualify for prime mortgages promotes sustainable homeownership and economic growth. The nationwide robo signing scandal has shown that Virginia s property owners are at risk of losing their homes to fake signatures and fraudulent paperwork. Ensuring that foreclosure fraud victims can recoup damages from those responsible will strengthen property rights for Virginia s families. The large numbers of vacant properties across the Commonwealth presents a challenge and an opportunity. Steps should be taken to rehabilitate these vacant homes to meet the new demand for rental units and affordable, workforce housing. More Virginians should have the opportunity to live in communities of their choice and the rehabilitation of vacant properties will assist with this. 6

9 1 RealtyTrac.com monthly foreclosure reports. 2 This number represents the total number of properties in the foreclosure pipeline. REO or Real Estate Owned, are those properties which have been purchased by the lender at the foreclosure auction. NTS or Notice of Trustee Sale, is the noticed received by the borrower that their property is going to be auctioned. 3 US Department of Justice. Office of Justice Programs. Geography and Public Safety. Volume 1 Issue 3, October Available at 4 United State Census Bureau. Decennial Census, 2000 and Center for Responsible Lending. The Cost of Bad Lending in Virginia. Available at lending/tools resources/factsheets/virginia.html 6 Mamta Badkar. The 14 States Where Homeowners are Drowning in Negative Equity. Business Insider. September 13, Ibid. 8 Will Sanford and Ali Faruk. Virginia Foreclosure Trends Jan 24, Available at pdf. 9 US Department of Treasury, Comptroller of the Currency. OCC Mortgage Metrics Report: Disclosure of National Bank and Federal Savings Association Mortgage Loan Data. Washington DC, December This encompasses only first lien, owner occupied, 1 4 family home purchases. 11 Since 2004, HMDA requires lenders to report loan price information in the form of a rate spread which is the difference between the annual percentage rate (APR) on a loan and the rate on a Treasury security of comparable maturity. The threshold set by the Board in Regulation C for first lien loans is three percentage points above the Treasury security of comparable maturity. The Board chose this threshold in the belief that they would exclude the vast majority of prime rate loans and include the vast majority of subprime loans. 12 Jakabovics, Andrew and Chapman, Jeff. Unequal Opportunity Lenders? Analyzing Racial Disparities in Big Banks Higher Priced Lending. American Progress, September Available at U.S. Department of Justice. Justice Department Reaches $335 Million Settlement to Resolve Allegations of Lending Discrimination by Countrywide Financial Corporation. 21 Dec ag 1694.html 14 HOME analysis of over 500 Deeds of Trusts for properties in the Greater Richmond Region. 15 US Department of Treasury, Comptroller of the Currency. OCC Mortgage Metrics Report: Disclosure of National Bank and Federal Savings Association Mortgage Loan Data. Washington DC, December Ibid. 17 HOME Analysis of HAMP Data. 7

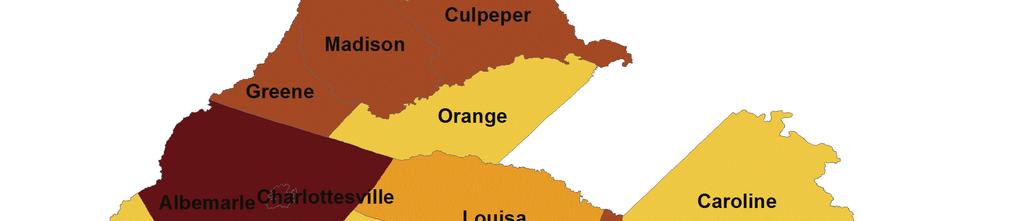

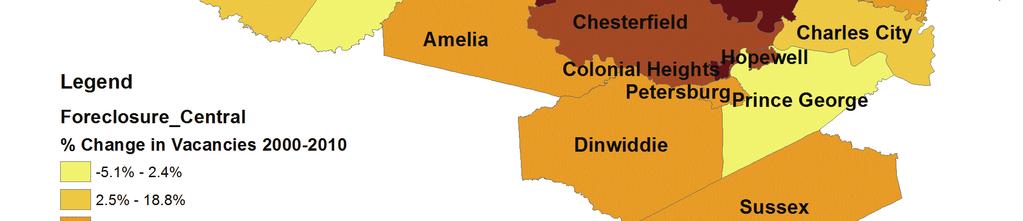

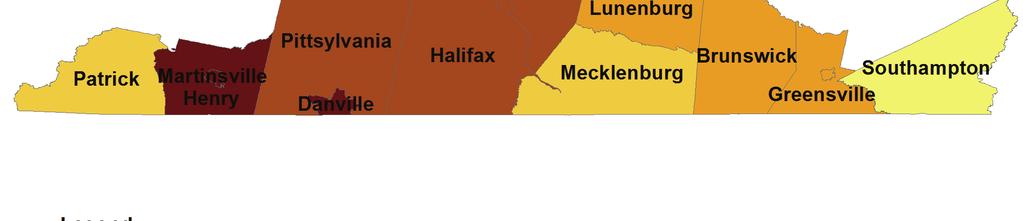

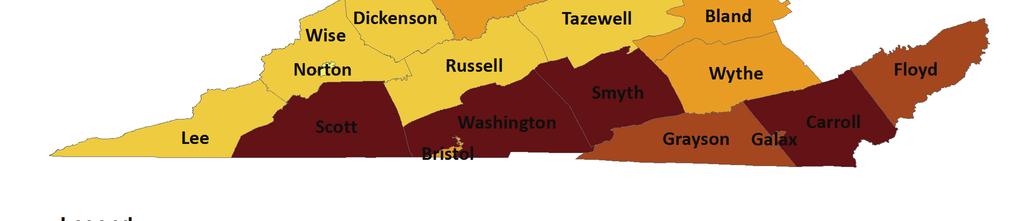

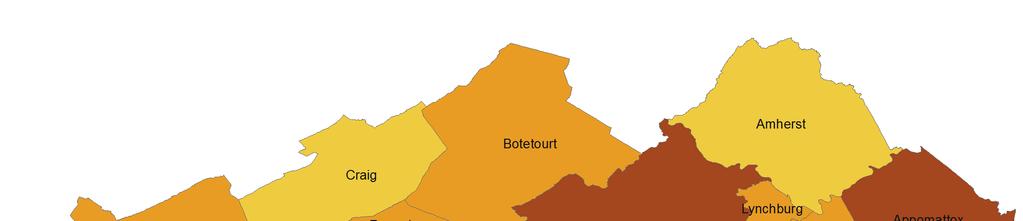

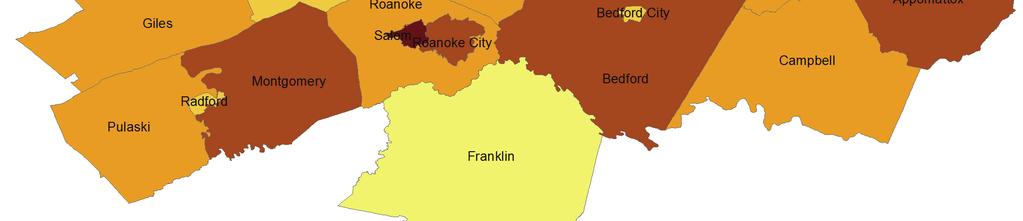

10 Central Region 8

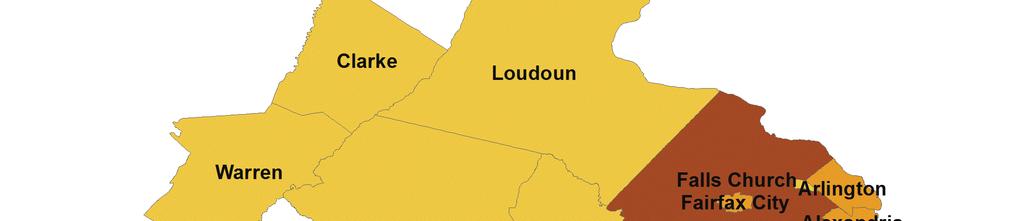

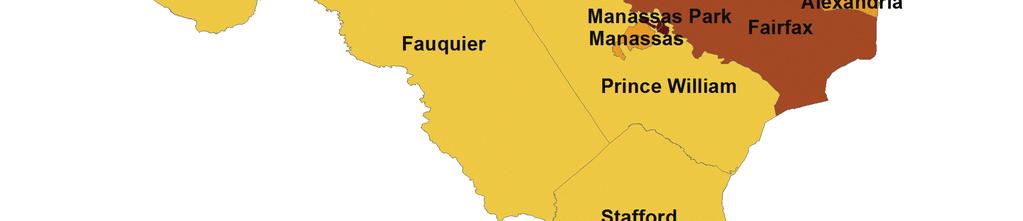

11 Eastern Region 9

12 10

13 11

14 12

15 13

16 14

17 15

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

Homeownership Preservation in Maryland

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

U.S. Housing Markets: Looking Back, Looking Forward

U.S. Housing Markets: Looking Back, Looking Forward Dr. Raphael Bostic Assistant Secretary, Office of Policy Development and Research U.S. Department of Housing and Urban Development Special Thanks Ed

U.S. Housing Markets: Looking Back, Looking Forward Dr. Raphael Bostic Assistant Secretary, Office of Policy Development and Research U.S. Department of Housing and Urban Development Special Thanks Ed

Review of Northern Virginia Market Conditions and Trends

Review of Northern Virginia Market Conditions and Trends Prepared for Northern Virginia Area Association of Realtors November 12, 2011 Virginia Housing Development Authority Northern Virginia s existing

Review of Northern Virginia Market Conditions and Trends Prepared for Northern Virginia Area Association of Realtors November 12, 2011 Virginia Housing Development Authority Northern Virginia s existing

Subprime Lending in Washington State

sound research. Bold Solutions.. Policy BrieF. March 9, 2009 The High Cost of Subprime Lending in Washington State By Jeff Chapman Executive Summary In Washington State in 2006, African- American and Hispanic

sound research. Bold Solutions.. Policy BrieF. March 9, 2009 The High Cost of Subprime Lending in Washington State By Jeff Chapman Executive Summary In Washington State in 2006, African- American and Hispanic

Testimony of Dean Baker. Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee

Testimony of Dean Baker Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee Hearing on the Recently Announced Revisions to the Home Affordable Modification

Testimony of Dean Baker Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee Hearing on the Recently Announced Revisions to the Home Affordable Modification

U.S. HOUSING RECOVERY WILL NOT DROWN IN A SEA OF DISTRESSED SALES

OBSERVATION TD Economics February 3, 1 U.S. HOUSING RECOVERY WILL NOT DROWN IN A SEA OF DISTRESSED SALES Highlights The housing market is showing signs of life. Home sales and housing starts are rising

OBSERVATION TD Economics February 3, 1 U.S. HOUSING RECOVERY WILL NOT DROWN IN A SEA OF DISTRESSED SALES Highlights The housing market is showing signs of life. Home sales and housing starts are rising

Mortgage Delinquencies and Foreclosures: Hawaii

Mortgage Delinquencies and Foreclosures: Hawaii Craig Nolte Community Development Department Federal Reserve Bank of San Francisco October 16, 2008 Do not cite or reproduce without permission. Overview

Mortgage Delinquencies and Foreclosures: Hawaii Craig Nolte Community Development Department Federal Reserve Bank of San Francisco October 16, 2008 Do not cite or reproduce without permission. Overview

A Nation of Renters? Promoting Homeownership Post-Crisis. Roberto G. Quercia Kevin A. Park

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

Review of Regional Market Conditions in the Greater Piedmont Area

Review of Regional Market Conditions in the Greater Piedmont Area Greater Piedmont Area Association of Realtors June 7, 2010 Virginia Housing Development Authority Overview of Current Market Conditions

Review of Regional Market Conditions in the Greater Piedmont Area Greater Piedmont Area Association of Realtors June 7, 2010 Virginia Housing Development Authority Overview of Current Market Conditions

Who is Lending and Who is Getting Loans?

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

The Office of Economic Policy HOUSING DASHBOARD. March 16, 2016

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

The Office of Economic Policy HOUSING DASHBOARD March 16, 216 Recent housing market indicators suggest that housing activity continues to strengthen. Solid residential investment in 215Q4 contributed.3

PREPARED REMARKS FOR DAVID H. STEVENS ASSISTANT SECRETARY FOR HOUSING FHA COMMISSIONER U.S

PREPARED REMARKS FOR DAVID H. STEVENS ASSISTANT SECRETARY FOR HOUSING FHA COMMISSIONER U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT AT THE THE WORLD BANK 4 TH GLOBAL CONFERENCE ON HOUSING FINANCE IN

PREPARED REMARKS FOR DAVID H. STEVENS ASSISTANT SECRETARY FOR HOUSING FHA COMMISSIONER U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT AT THE THE WORLD BANK 4 TH GLOBAL CONFERENCE ON HOUSING FINANCE IN

Florida: An Economic Overview

Florida: An Economic Overview May 1, 2012 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Mixed Economy Turned

Florida: An Economic Overview May 1, 2012 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Mixed Economy Turned

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

Why is Non-Bank Lending Highest in Communities of Color?

Why is Non-Bank Lending Highest in Communities of Color? An ANHD White Paper October 2017 New York is a city of renters, but nearly a third of New Yorkers own their own homes. The stock of 2-4 family homes

Why is Non-Bank Lending Highest in Communities of Color? An ANHD White Paper October 2017 New York is a city of renters, but nearly a third of New Yorkers own their own homes. The stock of 2-4 family homes

LISC Building Sustainable Communities Initiative Neighborhood Quality Monitoring Report

LISC Building Sustainable Communities Initiative Neighborhood Quality Monitoring Report Neighborhood:, Kansas City, MO The LISC Building Sustainable Communities (BSC) Initiative supports community efforts

LISC Building Sustainable Communities Initiative Neighborhood Quality Monitoring Report Neighborhood:, Kansas City, MO The LISC Building Sustainable Communities (BSC) Initiative supports community efforts

Credit Access and Consumer Protection: Searching for the Right Balance

Credit Access and Consumer Protection: Searching for the Right Balance North Carolina Banking Institute March 26, 2013 Charlotte, NC Michael D. Calhoun Impact On Consumer Finances Already New Rapidly Appreciating

Credit Access and Consumer Protection: Searching for the Right Balance North Carolina Banking Institute March 26, 2013 Charlotte, NC Michael D. Calhoun Impact On Consumer Finances Already New Rapidly Appreciating

The State of the Nation s Housing Report 2017

The State of the Nation s Housing Report 217 Tennessee Governor s Housing Conference Nashville, Tennessee September 2, 217 The Report s Major Themes National home prices have regained their previous peak,

The State of the Nation s Housing Report 217 Tennessee Governor s Housing Conference Nashville, Tennessee September 2, 217 The Report s Major Themes National home prices have regained their previous peak,

U.S. Foreclosure Outlook. To: Company Name Here Date: Goes Here

U.S. Foreclosure Outlook To: Company Name Here Date: Goes Here A brief note on methodology RealtyTrac collects foreclosure documents, postings and published notices from about 2,200 counties nationwide.

U.S. Foreclosure Outlook To: Company Name Here Date: Goes Here A brief note on methodology RealtyTrac collects foreclosure documents, postings and published notices from about 2,200 counties nationwide.

Prince William County ECONOMIC INDICATORS NEWSLETTER Volume 7, Issue 4 October - December 2007

Prince William County ECONOMIC INDICATORS NEWSLETTER Volume 7, Issue 4 October - December 2007 Highlights Fourth quarter GDP: 0.6% compared to 4.9% in previous quarter. National unemployment rate: 5.0%

Prince William County ECONOMIC INDICATORS NEWSLETTER Volume 7, Issue 4 October - December 2007 Highlights Fourth quarter GDP: 0.6% compared to 4.9% in previous quarter. National unemployment rate: 5.0%

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN NORTHERN CALIFORNIA August 2009 Lena Robinson, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends

TRENDS IN DELINQUENCIES AND FORECLOSURES IN NORTHERN CALIFORNIA August 2009 Lena Robinson, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends

Weakness in the U.S. Housing Market Likely to Persist in 2008

Weakness in the U.S. Housing Market Likely to Persist in 2008 Commentary by Sondra Albert, Chief Economist AFL-CIO Housing Investment Trust January 29, 2008 The national housing market entered 2008 mired

Weakness in the U.S. Housing Market Likely to Persist in 2008 Commentary by Sondra Albert, Chief Economist AFL-CIO Housing Investment Trust January 29, 2008 The national housing market entered 2008 mired

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland The Reinvestment Fund builds wealth and opportunity for low-wealth people and places through the promotion of socially and environmentally

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland The Reinvestment Fund builds wealth and opportunity for low-wealth people and places through the promotion of socially and environmentally

FORECLOSURE PREVENTION PRINCIPAL REDUCTION AND. Preliminary Report, Findings and Recommendations from the IDT. Seattle City Council March 26, 2014

1 PRINCIPAL REDUCTION AND FORECLOSURE PREVENTION Preliminary Report, Findings and Recommendations from the IDT Seattle City Council March 26, 2014 2 IDT Scope of Work Resolution 31495 directed IDT to explore

1 PRINCIPAL REDUCTION AND FORECLOSURE PREVENTION Preliminary Report, Findings and Recommendations from the IDT Seattle City Council March 26, 2014 2 IDT Scope of Work Resolution 31495 directed IDT to explore

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties.

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo,

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo,

Despite Growing Market, African Americans and Latinos Remain Underserved

Despite Growing Market, African Americans and Latinos Remain Underserved Issue Brief September 2017 Introduction Enacted by Congress in 1975, the Home Mortgage Disclosure Act (HMDA) requires an annual

Despite Growing Market, African Americans and Latinos Remain Underserved Issue Brief September 2017 Introduction Enacted by Congress in 1975, the Home Mortgage Disclosure Act (HMDA) requires an annual

The High Cost of Segregation: Exploring the Relationship Between Racial Segregation and Subprime Lending

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

National Housing Market Summary

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

FY 2015 SECOND QUARTER REVENUE UPDATE, CURRENT ECONOMIC OUTLOOK & FY GENERAL REVENUE FORECAST

FY 2015 SECOND QUARTER REVENUE UPDATE, CURRENT ECONOMIC OUTLOOK & FY 2016-2020 GENERAL REVENUE FORECAST Michelle L. Attreed Director of Finance February 17, 2015 Proposed FY2016-2020 General Revenue Forecast-

FY 2015 SECOND QUARTER REVENUE UPDATE, CURRENT ECONOMIC OUTLOOK & FY 2016-2020 GENERAL REVENUE FORECAST Michelle L. Attreed Director of Finance February 17, 2015 Proposed FY2016-2020 General Revenue Forecast-

Housing and Credit Markets Outlook

Housing and Credit Markets Outlook FTA Revenue Estimating Conference Springfield, IL Amy Crews Cutts, SVP Chief Economist October 7, Equifax Inc. Government Shutdown and Debt Ceiling! As of October 1 st

Housing and Credit Markets Outlook FTA Revenue Estimating Conference Springfield, IL Amy Crews Cutts, SVP Chief Economist October 7, Equifax Inc. Government Shutdown and Debt Ceiling! As of October 1 st

Homeowner Affordability and Stability Plan Fact Sheet

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Compliance Challenges in a Changing Economic Environment

Compliance Challenges in a Changing Economic Environment Call the Fed Audio Conference December 10, 2008 The following presentation contains the views and opinions of the speakers and his or her interpretation

Compliance Challenges in a Changing Economic Environment Call the Fed Audio Conference December 10, 2008 The following presentation contains the views and opinions of the speakers and his or her interpretation

Hearing on The Housing Decline: The Extent of the Problem and Potential Remedies December 13, 2007

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Statement of Michael Decker Senior Managing Director, Research and Public Policy Before the Committee on Finance United States Senate Hearing on The Housing Decline: The Extent of the Problem and Potential

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE. SUBJECT: Home Loan Program 2012 Mid-Year Report CONSENT: X ATTACHMENT(S): 1

: 1") TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE SUBJECT: Home Loan Program 2012 Mid-Year Report ITEM NUMBER: 4c CONSENT: X ATTACHMENT(S): 1 ACTION: DATE OF MEETING: September 7, 2012 INFORMATION: X PRESENTER(S):

TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE SUBJECT: Home Loan Program 2012 Mid-Year Report ITEM NUMBER: 4c CONSENT: X ATTACHMENT(S): 1 ACTION: DATE OF MEETING: September 7, 2012 INFORMATION: X PRESENTER(S):

The state of the nation s Housing 2013

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA April 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA April 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

Targeting Neighborhood Stabilization Funds to Community Need: An Assessment of Georgia s Proposed Funding Allocations

Targeting Neighborhood Stabilization Funds to Community Need: An Assessment of Georgia s Proposed Funding Allocations Presented to the Georgia Department of Community Affairs November 28, 2008 Dr. Michael

Targeting Neighborhood Stabilization Funds to Community Need: An Assessment of Georgia s Proposed Funding Allocations Presented to the Georgia Department of Community Affairs November 28, 2008 Dr. Michael

Florida: An Economic Overview

Florida: An Economic Overview August 21, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview August 21, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

In the first three months of 2007, there

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties by Jeff Crump In the first three months of 2007, there were 678 foreclosure sales in the city of Minneapolis, an increase of more than 100%

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties by Jeff Crump In the first three months of 2007, there were 678 foreclosure sales in the city of Minneapolis, an increase of more than 100%

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA April 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA April 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO February 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO February 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

The Current Foreclosure Crisis Trends and Roadblocks to Recovery

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

HUD-9902 Desk Guide. Don't Forget! HUD-9902 Category. How to Complete

Don't Forget! Data is CUMULATIVE! For example, your Q3 report should include all households served from Q1 - Q3. If your agency received HUD approval mid-way through the fiscal year, you should still report

Don't Forget! Data is CUMULATIVE! For example, your Q3 report should include all households served from Q1 - Q3. If your agency received HUD approval mid-way through the fiscal year, you should still report

June 29, 2011 Acting Director Edward DeMarco Federal Housing Finance Agency 1700 G Street, NW, 4th Floor Washington, DC 20552

June 29, 2011 Acting Director Edward DeMarco Federal Housing Finance Agency 1700 G Street, NW, 4th Floor Washington, DC 20552 Dear Acting Director DeMarco, On April 28, 2011, the Federal Housing Finance

June 29, 2011 Acting Director Edward DeMarco Federal Housing Finance Agency 1700 G Street, NW, 4th Floor Washington, DC 20552 Dear Acting Director DeMarco, On April 28, 2011, the Federal Housing Finance

The Five-Point Plan. Creating a Sustainable Path to Minority Homeownership

The Five-Point Plan Creating a Sustainable Path to Minority Homeownership The National Association of Hispanic Real Estate Professionals, The Asian Real Estate Association of America and the National Association

The Five-Point Plan Creating a Sustainable Path to Minority Homeownership The National Association of Hispanic Real Estate Professionals, The Asian Real Estate Association of America and the National Association

Missouri Home Ownership Preservation Summit

Missouri Home Ownership Preservation Summit January 14, 2010 Foreclosure, Fraud and Consumer Protection: Current trends and the role of mortgage fraud, appraisal fraud, mortgage rescue scams in the mortgage

Missouri Home Ownership Preservation Summit January 14, 2010 Foreclosure, Fraud and Consumer Protection: Current trends and the role of mortgage fraud, appraisal fraud, mortgage rescue scams in the mortgage

Housing and Economic Outlook

Housing and Economic Outlook JANUARY 22, 2013 // 2:30 4:00PM Presenters: David Crowe // NAHB, Washington DC Frank Nothaft // Freddie Mac, McLean, VA David Berson // Nationwide Insurance, Columbus, OH Housing

Housing and Economic Outlook JANUARY 22, 2013 // 2:30 4:00PM Presenters: David Crowe // NAHB, Washington DC Frank Nothaft // Freddie Mac, McLean, VA David Berson // Nationwide Insurance, Columbus, OH Housing

TRENDS IN DELINQUENCIES AND FORECLOSURES IN NEVADA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN NEVADA January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession

TRENDS IN DELINQUENCIES AND FORECLOSURES IN NEVADA January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession

THE NSP SUBSTANTIAL AMENDMENT

THE NSP SUBSTANTIAL AMENDMENT Jurisdiction(s): _Pasco County (identify lead entity in case of joint agreements) Jurisdiction Web Address: www.pascocountyfl.net (URL where NSP Substantial Amendment materials

THE NSP SUBSTANTIAL AMENDMENT Jurisdiction(s): _Pasco County (identify lead entity in case of joint agreements) Jurisdiction Web Address: www.pascocountyfl.net (URL where NSP Substantial Amendment materials

Making Home Affordable

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

The National Mortgage Settlement: July 31, :00 4:00pm

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Webinar Objectives Today Provide an overview of the National Mortgage

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Webinar Objectives Today Provide an overview of the National Mortgage

The US Housing Market Crisis and Its Aftermath

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

The US Housing Market Crisis and Its Aftermath Asian Development Bank November 16, 2009 Table of Contents Section I II III IV V US Economy and the Housing Market Freddie Mac Overview Business Activities

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA August 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA August 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO August 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Recession and

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO August 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Recession and

Race and Housing in Pennsylvania

w w w. t r f u n d. c o m About this Paper TRF created a data warehouse and mapping tool for the Pennsylvania Housing Finance Agency (PHFA). In follow-up to this work, PHFA commissioned TRF to analyze

w w w. t r f u n d. c o m About this Paper TRF created a data warehouse and mapping tool for the Pennsylvania Housing Finance Agency (PHFA). In follow-up to this work, PHFA commissioned TRF to analyze

Florida: An Economic Overview

Florida: An Economic Overview June 19, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview June 19, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012

Contact: Pete Bakel Resource Center: 1-800-732-6643 202-752-2034 Date: August 8, 2012 Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012 Net Income of $7.8 Billion for First Half 2012

Contact: Pete Bakel Resource Center: 1-800-732-6643 202-752-2034 Date: August 8, 2012 Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012 Net Income of $7.8 Billion for First Half 2012

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO April 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO April 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN OREGON

TRENDS IN DELINQUENCIES AND FORECLOSURES IN OREGON January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession

TRENDS IN DELINQUENCIES AND FORECLOSURES IN OREGON January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA August 2009 Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Recession and turmoil

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA August 2009 Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Recession and turmoil

Mortgage Performance Summary

Mortgage Performance Summary QUARTERLY UPDATE Housing Market and Mortgage Performance in the 1st Quarter, 2017 Joseph Mengedoth Michael Stanley 475 450 425 400 375 350 325 300 275 250 225 200 175 150 125

Mortgage Performance Summary QUARTERLY UPDATE Housing Market and Mortgage Performance in the 1st Quarter, 2017 Joseph Mengedoth Michael Stanley 475 450 425 400 375 350 325 300 275 250 225 200 175 150 125

HOUSING & MORTGAGE COUNSELOR

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

Federal Housing Legislation and Dallas Foreclosure Update. A Briefing To The Housing Committee September 2, 2008

Federal Housing Legislation and Dallas Foreclosure Update A Briefing To The Housing Committee September 2, 2008 Purpose To provide: An update on the status of foreclosures in the City of Dallas and the

Federal Housing Legislation and Dallas Foreclosure Update A Briefing To The Housing Committee September 2, 2008 Purpose To provide: An update on the status of foreclosures in the City of Dallas and the

TRENDS IN DELINQUENCIES

TRENDS IN DELINQUENCIES AND FORECLOSURES IN UTAH January 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN UTAH January 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

35% 26% 57% 51% PROFILE. CIty of durham: Assets & opportunity ProfILe. key highlights. ABoUt the ProfILe ASSETS & OPPORTUNITY

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

Housing Market and Mortgage Performance in the Fifth District

QUARTERLY UPDATE Housing Market and Mortgage Performance in the Fifth District 3 rd Quarter, 2013 Jamie Feik Lisa Hearl Joseph Mengedoth An Update on Housing Market and Mortgage Performance in the Fifth

QUARTERLY UPDATE Housing Market and Mortgage Performance in the Fifth District 3 rd Quarter, 2013 Jamie Feik Lisa Hearl Joseph Mengedoth An Update on Housing Market and Mortgage Performance in the Fifth

State of the Housing Market

State of the Housing Market 2 Freddie Mac s Mission Freddie Mac makes homeownership and rental housing more accessible and affordable by providing liquidity, stability, and affordability to the U.S. housing

State of the Housing Market 2 Freddie Mac s Mission Freddie Mac makes homeownership and rental housing more accessible and affordable by providing liquidity, stability, and affordability to the U.S. housing

Bank of america reo for sale REO Bank for REO for

Bank of america reo for sale The sudden and rapid collapse in home values has astronomically increased the number of home owners and investors defaulting on their loans. California, Nevada and Florida

Bank of america reo for sale The sudden and rapid collapse in home values has astronomically increased the number of home owners and investors defaulting on their loans. California, Nevada and Florida

HOUSING & MORTGAGE COUNSELOR

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

Protecting Communities on the Road to Recovery. Why Strong Standards are Critical for the Distressed Asset Stabilization Program

Protecting Communities on the Road to Recovery Why Strong Standards are Critical for the Distressed Asset Stabilization Program By Sarah Edelman, Michela Zonta, and Shiv Rawal June 2016 W W W.AMERICANPROGRESS.ORG

Protecting Communities on the Road to Recovery Why Strong Standards are Critical for the Distressed Asset Stabilization Program By Sarah Edelman, Michela Zonta, and Shiv Rawal June 2016 W W W.AMERICANPROGRESS.ORG

NATIONAL ASSOCIATION OF REALTORS

NATIONAL ASSOCIATION OF REALTORS The Voice for Real Estate 430 North Michigan Avenue Chicago, Illinois 60611-4087 312.329.8411 Fax 312.329.5962 Visit us at www.realtor.org. Coldwell Banker AJS Schmidt

NATIONAL ASSOCIATION OF REALTORS The Voice for Real Estate 430 North Michigan Avenue Chicago, Illinois 60611-4087 312.329.8411 Fax 312.329.5962 Visit us at www.realtor.org. Coldwell Banker AJS Schmidt

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession s

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO January 2011 Community Development Research Federal Reserve Bank of San Francisco National Trends Even though NBER officially announced the recession s

Credit Research Center Seminar

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

Credit Research Center Seminar Ensuring Fair Lending: What Do We Know about Pricing in Mortgage Markets and What Will the New HMDA Data Fields Tell US? www.msb.edu/prog/crc March 14, 2005 Introduction

June 14, Dear Regulations Division:

June 14, 2017 Regulations Division Office of General Counsel Department of Housing and Urban Development 451 7th Street S.W., Room 10276 Washington, DC 20410-0500 RE: Comments to Office of Secretary, HUD

June 14, 2017 Regulations Division Office of General Counsel Department of Housing and Urban Development 451 7th Street S.W., Room 10276 Washington, DC 20410-0500 RE: Comments to Office of Secretary, HUD

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities J. Michael Collins Assistant Professor, School of Human Ecology Director, Center for Financial Security

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities J. Michael Collins Assistant Professor, School of Human Ecology Director, Center for Financial Security

A Look Behind the Numbers: FHA Lending in Ohio

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

Page1 Recent news articles have carried the worrisome suggestion that Federal Housing Administration (FHA)-insured loans may be the next subprime. Given the high correlation between subprime lending and

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

This Month in Real Estate

Keller Williams Research This Month in Real Estate Released: December 4, 2009 Commentary. 2 The Numbers That Drive Real Estate 3 Recent Government Action. 9 Topics for Buyers and Sellers. 15 1 Steps to

Keller Williams Research This Month in Real Estate Released: December 4, 2009 Commentary. 2 The Numbers That Drive Real Estate 3 Recent Government Action. 9 Topics for Buyers and Sellers. 15 1 Steps to

VIRGINIA HOUSING DEVELOPMENT AUTHORITY (A Component Unit of the Commonwealth of Virginia)

") Management s Discussion and Analysis, Basic Financial Statements, and Supplementary Information (With Independent Auditor s Reports Thereon) Table of Contents Management s Discussion and Analysis 1 Independent

Management s Discussion and Analysis, Basic Financial Statements, and Supplementary Information (With Independent Auditor s Reports Thereon) Table of Contents Management s Discussion and Analysis 1 Independent

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS CRA IMPLEMENTATION WORKSHOP January 23, 2015 2 South Florida Context Areas of Opportunity Overview of HMDA Data

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS CRA IMPLEMENTATION WORKSHOP January 23, 2015 2 South Florida Context Areas of Opportunity Overview of HMDA Data

MORTGAGE COUNSELOR. Ver Mortgage Counselor Page: 1

MORTGAGE COUNSELOR COMPENSATION: $60,000 to $100,000+ (based on substantial production incentives) LOCATION: NACA Offices Nationwide CONTACT: HR Department: jobs@naca.com BENEFITS: Excellent single/family

MORTGAGE COUNSELOR COMPENSATION: $60,000 to $100,000+ (based on substantial production incentives) LOCATION: NACA Offices Nationwide CONTACT: HR Department: jobs@naca.com BENEFITS: Excellent single/family

The National Mortgage Settlement: Loan Modifications and Servicing Standards

The National Mortgage Settlement: Loan Modifications and Servicing Standards MHA Trusted Advisor Webinar July 24, 2013 Sarah Bolling Mancini Home Defense Program of the Atlanta Legal Aid Society, Inc.

The National Mortgage Settlement: Loan Modifications and Servicing Standards MHA Trusted Advisor Webinar July 24, 2013 Sarah Bolling Mancini Home Defense Program of the Atlanta Legal Aid Society, Inc.

Analyzing Trends in Subprime Originations and Foreclosures: A Case Study of the Boston Metro Area

Analyzing Trends in Originations and : A Case Study of the Boston Metro Area Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo, Egypt Johannesburg, South Africa September

Analyzing Trends in Originations and : A Case Study of the Boston Metro Area Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo, Egypt Johannesburg, South Africa September

Home Mortgage Disclosure Act Report ( ) Submitted by Jonathan M. Cabral, AICP

Submitted by Jonathan M. Cabral, AICP") Home Mortgage Disclosure Act Report (2008-2015) Submitted by Jonathan M. Cabral, AICP Introduction This report provides a review of the single family (1-to-4 units) mortgage lending activity in Connecticut

Home Mortgage Disclosure Act Report (2008-2015) Submitted by Jonathan M. Cabral, AICP Introduction This report provides a review of the single family (1-to-4 units) mortgage lending activity in Connecticut

in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008

Rising Foreclosures in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008 Mark E. Pearce, Deputy Commissioner NC Office of the Commissioner of Banks NCCOB s regulation of

Rising Foreclosures in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008 Mark E. Pearce, Deputy Commissioner NC Office of the Commissioner of Banks NCCOB s regulation of

The U.S. Housing Market

U.S. economic expansions, contractions, and subsequent recoveries are inextricably linked to the housing market. Housing has always played a major role in economic cycles, but for a number of reasons its

U.S. economic expansions, contractions, and subsequent recoveries are inextricably linked to the housing market. Housing has always played a major role in economic cycles, but for a number of reasons its

Special Report. March 10, ,600 1,400 1,200

March 1, 1 HIGHLIGHTS After nearly three years of decline, the U.S housing market showed considerable signs of improvement in 9. In particular, a rise in home sales helped to pull down housing inventories

March 1, 1 HIGHLIGHTS After nearly three years of decline, the U.S housing market showed considerable signs of improvement in 9. In particular, a rise in home sales helped to pull down housing inventories

B-09-DN-DE April 1, 2018 thru June 30, 2018 Performance Report. Community Development Systems Disaster Recovery Grant Reporting System (DRGR)

") Grantee: Grant: Delaware B-09-DN-DE-0012 April 1, 2018 thru June 30, 2018 Performance Report 1 Grant Number: B-09-DN-DE-0012 Grantee Name: Delaware Grant Award Amount: $10,007,109.00 LOCCS Authorized Amount:

Grantee: Grant: Delaware B-09-DN-DE-0012 April 1, 2018 thru June 30, 2018 Performance Report 1 Grant Number: B-09-DN-DE-0012 Grantee Name: Delaware Grant Award Amount: $10,007,109.00 LOCCS Authorized Amount:

Florida: An Economic Overview

Florida: An Economic Overview May 14, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview May 14, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Washington, D.C., Metropolitan Area Foreclosure Monitor Technical Appendix NeighborhoodInfo DC April 2010

Washington, D.C., Metropolitan Area Foreclosure Monitor Technical Appendix NeighborhoodInfo DC April 2010 The primary data on the performance of residential mortgages presented in the Foreclosure Monitor

Washington, D.C., Metropolitan Area Foreclosure Monitor Technical Appendix NeighborhoodInfo DC April 2010 The primary data on the performance of residential mortgages presented in the Foreclosure Monitor

Florida: An Economic Overview

Florida: An Economic Overview March 31, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview March 31, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

New policies to help underwater borrowers

Testimony of Andrew Jakabovics, Associate Director for Housing and Economics, Center for American Progress Action Fund Before the House Financial Services Committee Subcommittee on Housing and Community

Testimony of Andrew Jakabovics, Associate Director for Housing and Economics, Center for American Progress Action Fund Before the House Financial Services Committee Subcommittee on Housing and Community

THDA Homebuyer Education Initiative Customer Intake Form

Sample 3 Date Case# (Trainer completes) Trainer Organization County (Trainer completes) THDA Homebuyer Education Initiative Customer Intake Form Please provide information about yourself for customer tracking

Sample 3 Date Case# (Trainer completes) Trainer Organization County (Trainer completes) THDA Homebuyer Education Initiative Customer Intake Form Please provide information about yourself for customer tracking

Community Development Block Grant Program

U.S. DEPARTMENT OF HOUSING ANn URBAN DEVELOPMENT FOR: FROM: SUBJECT: Housing under Development Block Grant (CDBG) and Neighborhood Stabilization Programs (NSP) This memorandum provides information on how

U.S. DEPARTMENT OF HOUSING ANn URBAN DEVELOPMENT FOR: FROM: SUBJECT: Housing under Development Block Grant (CDBG) and Neighborhood Stabilization Programs (NSP) This memorandum provides information on how