The National Mortgage Settlement: Loan Modifications and Servicing Standards

|

|

|

- Michael York

- 5 years ago

- Views:

Transcription

1 The National Mortgage Settlement: Loan Modifications and Servicing Standards MHA Trusted Advisor Webinar July 24, 2013 Sarah Bolling Mancini Home Defense Program of the Atlanta Legal Aid Society, Inc.

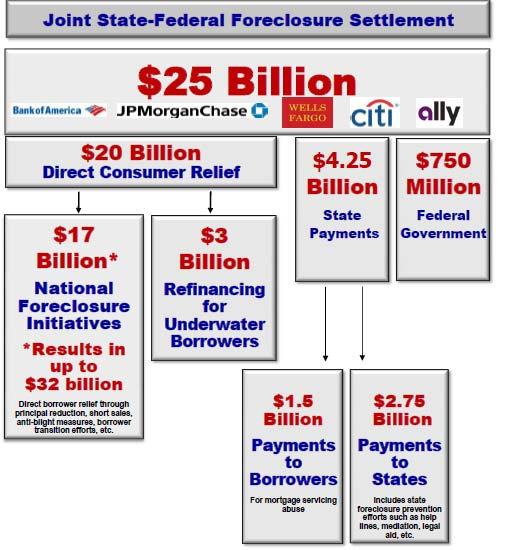

2 Plaintiffs Department of Justice (for HUD, Treasury, US Bankruptcy Trustee), Federal Trade Commission, 49 state AGs and state banking regulators (all but Oklahoma) 2

3 Defendants Bank of America CitiGroup JPMorgan Chase Ally Financial/GMAC Wells Fargo 3

4 Details of the Settlement Filed in US District Court for District of Columbia on April 4, 2012 Monitor: Joseph A. Smith, Jr., former Commissioner of Banks for NC will monitor compliance Monitoring committee (DOJ, HUD, and some state AGs) will oversee and enforce terms 4

5 Conduct at Issue Robo-signing of foreclosure affidavits and mortgage assignments Improper foreclosures Abusive conduct in bankruptcy cases, including filing padded claims and frivolous motions for relief from the bankruptcy stay 5

6 Overview of Relief Money payments/consumer relief (not for GSE loans) Injunctive provisions setting servicing standards Enforcement provisions Exceptions to release of liability Consent judgments remain in effect 3½ years (until October 2015) 6

7 7

8 Redress for 3 main groups of borrowers 1. Borrowers who have lost their homes to foreclosure get cash payments; 2. Borrowers who are current but are underwater may be eligible for a refinance; 3. Borrowers who are still in their homes but behind on mortgage payments and underwater are eligible for principal reductions on 1 st or 2 nd mortgages and other Consumer Relief. These three kinds of relief cannot be applied to Fannie Mae or Freddie Mac owned loans. 8

9 1. Money for borrowers who lost their homes Home sold in foreclosure Payment of up to $2,000 per borrower No requirement of release of private claims, but payment shall be offset against any other relief This payment is separate from OCC Settlement Information set out in Appendix C of Settlements APPLICATION DEADLINE HAS PASSED! Can t apply now. 9

10 2. Refinance provisions Borrowers who are current but are underwater may be eligible for a refinance: Applies only to servicer-owned 1 st mortgages Does not cover FHA or VA loans Must be current no delinquency in past 12 months No loan modifications, bankruptcy, or foreclosure activity in past 24 months LTV must be > 100% Loan must have been originated before Jan. 1, 2009 Current Interest rate must be at least 5.25% (or PMMS bp, whichever is greater) Credit to the Servicer is based on interest rate reduction x UPB x a multiplier 10

11 3. Other Consumer Relief Banks get credit for providing an array of Consumer Relief: 1st and 2 nd mortgage principal reduction Borrower transitional funds Short sales/extinguishment of 2 nd liens Deficiency waivers Forbearance for unemployed homeowners Anti-blight provisions Details set out in Exhibit D to Settlements 11

12 3. Consumer Relief: Principal Reduction Loan Modifications 1 st mortgage modifications: Borrower must be 30 days delinquent or at imminent risk of default; Pre-modification LTV must be greater than 100%; Modification must reduce P&I payment by 10% Post-modification: LTV no more than 120%; DTI no more than 31% 12

13 3. Principal Reduction Loan Modifications DTI requirements may be waived for first lien mortgages that are 180 days or more delinquent, as long as payment is reduced by at least 20% and LTV is reduced to at least 120%; Servicer shall also be entitled to credit for any amounts of principal reduction which lower LTV below 120%; May get credit for HAMP principal reductions. 13

14 Example 1 PI: PITI: $1,000 $1200 PITI: Income: $1,200 $2400 Income: $3,100 Value of home $100,000 Amount owed on first mortgage $150,000

15 Example 1 PI: $736 PITI: $936 Income: $3,100 DTI = 30.2% Value of home $100,000 $30,000 Principal Reduction Modified P Balance $120,000

16 Example 2 PI: PITI: $1,000 $1200 PITI: Income: $1,200 $2400 Income: $3,219 Value of home $100,000 Amount owed on first mortgage $150,000

17 Example 2 PI: $798 PITI: $998 Income: $3,219 DTI = 31% Value of home $100,000 $20,000 Principal Reduction $130,000 = LTV 130%!

18 Example 2 PI: $736 PITI: $936 Income: $3,219 DTI = 29% Value of home $100,000 $30,000 Principal Reduction Modified P Balance $120,000 = LTV 120%

19 Example 3 PI: PITI: $1,000 $1200 PITI: Income: $1,200 $2400 Income: $2,400 Value of home $100,000 Amount owed on first mortgage $150,000

20 Example 3 PI: $736 PITI: $936 Income: $2,400 DTI = 39% Value of home $100,000 $30,000 Principal Reduction Modified P Balance $120,000 = LTV 120%

21 3. Principal Reduction Loan Modifications 2 nd mortgages: If principal is reduced on 1 st and 2 nd is owned by the servicer, servicer must modify the 2 nd ; If participating servicer holds the 2 nd and another participating servicer holds the 1 st, servicer holding the 2 nd must reduce 2 nd ; Extinguishment of 2d mortgage if greater than 180 days delinquent; Modification according to 2MP terms. 21

22 BOA/Countrywide Loans Exhibit I to the BOA Settlement Special Loan Modification Option, only available if: Loan is in a Countrywide Securitization or in portfolio of BOA or Affiliate DTI is currently over 25% First lien mortgage > 60 days delinquent 22

23 Servicing Standards Protections for Service Members Requirements prior to imposing forceplaced insurance Proprietary loan mods Short sales Development of Loan Portals 23

24 Servicing Standards Accuracy and transparency in foreclosure and bankruptcy proceedings Enhanced loss mitigation protection for borrowers Restrictions on servicing fees Measures to deter community blight Standards apply to all loans serviced by the 5 banks, including Fannie/Freddie loans Details set out in Exhibit A to Settlements 24

25 Single Point of Contact Servicer shall establish an easily accessible and reliable single point of contact ( SPOC ) for each potentially-eligible 1 st mortgage: Communicate options to borrower; Coordinate receipt of documents; Be knowledgeable about borrower s situation and current status; Have access to individuals with ability to stop foreclosure. (P. A-20 through 23) 25

26 Communication Servicers shall solicit borrowers for loss mit in accordance with HAMP timelines; Servicer shall communicate, at the written request of borrower, with the borrower s authorized representative, including housing counselors; Servicer shall cease collection activity while borrower is in a trial mod or has submitted documents for loan mod application. (A-23) 26

27 Servicing Standards: Loss Mitigation Requirements Servicer shall notify potentially eligible borrowers of available loss mitigation options prior to foreclosure referral But no obligation to solicit borrowers in active bankruptcy Servicer shall offer and facilitate NPV positive loan modifications Servicer shall convert successful trial mods to permanent mods (Exhibit A, Section IV, beginning at p. A-16) 27

28 Loss Mitigation Requirements Servicer shall not make inaccurate delinquency reports to credit reporting agencies when borrower is making timely reduced payments pursuant to a trial modification; Servicer shall provide a copy of fully executed loan mod within 45 days; Servicer shall not instruct, advise, or recommend that a borrower go into default in order to qualify for loss mitigation relief. 28

29 Loan Modification Timelines Provide written acknowledgment of receipt of documentation within 3 business days; Notify borrower of any known deficiency in document submission within 5 business days; Decision within 30 days. 29

30 Required Notices: prior to foreclosure referral At least 14 days prior to foreclosure referral, Servicer shall send borrower a letter including: Facts supporting the right to foreclose; Account information (total amount needed to reinstate, date of last payment, etc); Statement outlining loss mitigation efforts made, why borrower ineligible (Ex. A, Sec. I.A.18, at p. A-4) 30

31 Required Notices: Post Referral to Foreclosure Letter Within 5 business days after referral to foreclosure, Servicer shall send a letter to borrower explaining: That borrower can still be evaluated for alternatives to foreclosure even if (s)he has not previously applied; That borrower should contact Servicer to obtain a loss mitigation application; That borrower must submit an application to be considered for loss mit, and giving contact info; Borrower may reapply in lieu of appealing denial 31

32 Right to Appeal a Denial Provided that complete loan mod application package is submitted > 37 days prior to scheduled foreclosure sale, Servicer shall secure an independent evaluation (by an independent entity or separate employee) prior to issuing a denial letter. (Ex. A, Sec. IV.G, beginning at p. A-26) 32

33 Right to Appeal a Denial Provided that complete loan mod application is submitted >37 days prior to sale, borrowers shall have 30 days to appeal a denial, unless the denial reason was: Ineligible mortgage Ineligible property Offer not accepted or request withdrawn Loan was previously modified 33

34 Right to Appeal a Denial Denial notice shall inform the borrower: That (s)he has 30 days from denial letter to provide evidence that the determination was in error If denied because of investor restrictions, the name of the investor and a summary of reason for investor denial If denied because of negative NPV result, the monthly gross income and property value used in NPV test 34

35 Dual Tracking Restrictions 35

36 Dual Tracking Restrictions 36

37 Dual Tracking: First 120 Days If borrower submits a complete loss mitigation package with 120 days of default (or substantially complete and remaining docs by 130 days postdefault), no referral to foreclosure until: Servicer determines that borrower is not eligible; or Borrower declines loan mod offer or fails to accept within 14 days; or Borrower fails to send first trial payment or breaches the trial mod 37

38 Dual Tracking: First 120 Days If Servicer issues a denial giving rise to an appeal right, Servicer shall not proceed to a foreclosure sale until: Expiration of the 30-day appeal window; If borrower appeals, 15 days after servicer sends a letter denying the appeal; or If servicer grants the appeal and loan mod, until borrower fails to accept or breaches trial mod. 38

39 Within 30 days of Post Referral to Foreclosure Letter If borrower submits a complete loss mitigation package within 30 days after Post Referral to Foreclosure Letter, Servicer shall not proceed to sale until: Servicer determines that borrower is not eligible; or Borrower declines loan mod offer or fails to accept within 14 days; or Borrower fails to send first trial payment or breaches the trial mod 39

40 Within 30 days of Post Referral to Foreclose Letter If Servicer issues a denial giving rise to an appeal right, Servicer shall not proceed to a foreclosure sale until: Expiration of the 30-day appeal window; If borrower appeals, 15 days after servicer sends a letter denying the appeal; or If servicer grants the appeal and loan mod, until borrower fails to accept or breaches trial mod. 40

41 More than 37 days prior to foreclosure sale If borrower submits a complete loan mod application more than 30 days after the Post Referral to Foreclosure Letter but more than 37 days prior to sale: Servicer shall not proceed to sale pending review; And if more than >90 days remain until foreclosure date, servicer shall not proceed to sale during appeal window 41

42 15-37 days before sale If borrower submits a complete loan mod application more than 30 days after the Post Referral to Foreclosure Letter, but between 37 and 15 days prior to sale: Servicer shall conduct an expedited review, and if borrower is approved for a loan mod, shall not foreclose until borrower declines or breaches trial mod 42

43 Less than 15 days before sale If borrower submits a complete loan mod application more than 30 days after the Post Referral to Foreclosure Letter and less than 15 days before a scheduled foreclosure sale: Servicer must notify the borrower before the sale date as to Servicer s determination or inability to complete its review 43

44 Compare HAMP Dual Tracking Limitations If borrower submits a complete application no later than midnight on the seventh business day prior to foreclosure, servicer must suspend foreclosure sale as necessary to complete HAMP evaluation. (MHA Handbook 4.2 at Section 3.3.) 44

45 Dual Tracking Restricted Servicer shall not move for judgment or order of sale or proceed with a sale if: Borrower is in compliance with the terms of a trial mod, forbearance, or repayment plan; A short sale or deed in lieu has been approved by all parties. 45

46 Example: Georgia 9/1/2012 Default 2/1/2013 Servicer refers to foreclosure law firm 2/3/2013 Post Referral to Foreclosure Letter sent 2/22/2013 Foreclosure Notice Letter: scheduled for sale on April 2, /28/13 Borrower submits a complete package 46

47 Example: Georgia 47

48 Example: Nevada 9/1/2012 Default 2/1/2013 Servicer refers to foreclosure law firm 2/3/2013 Post Referral to Foreclosure Letter sent 2/15/2013 Notice of Default: scheduled for sale on June 25, 2013 (3 months) 3/8/13 Borrower submits a complete package 48

49 Example: Nevada 49

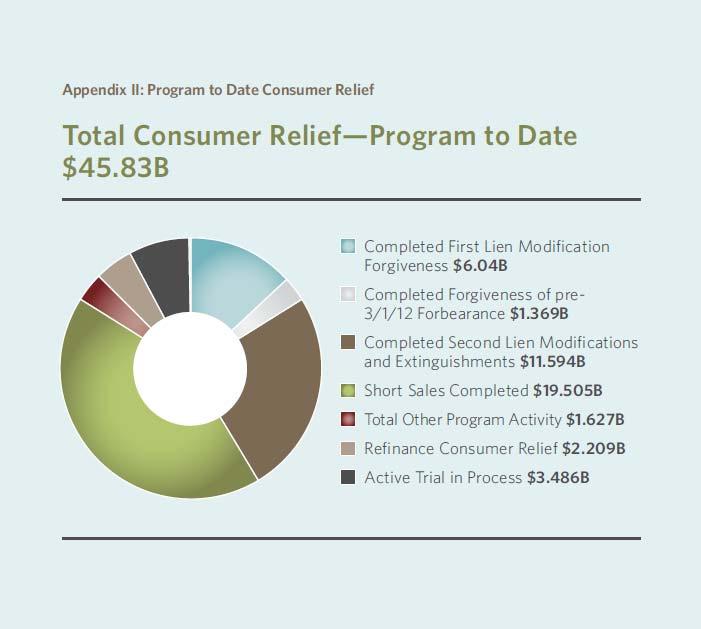

50 NMS How much has come out of the settlement so far? Per latest progress report from monitor (Note: these numbers are not the actual credits, which would be less than these totals per credit calculations): Consumer relief in US = $45.83 billion Of which $ billion was used for short sales 554,389 borrowers got some form of relief 50

51 51

52 Consumer Complaints 52

53 Professional Complaints 53

54 Consumer Complaints 54

55 Professional Complaints 55

56 Report Servicer Noncompliance! Office of Mortgage Settlement Oversight: Report Client/Constituent Issues (by housing counselor) Reporting by homeowner: mortgage/ask 56

National Mortgage Settlement & California Commitment

National Mortgage Settlement & California Commitment Help for Homeowners Community Pre Event Webinar Noah Zinner, Visiting Clinical Professor, UC Irvine Law School California Monitor, A Program of the

National Mortgage Settlement & California Commitment Help for Homeowners Community Pre Event Webinar Noah Zinner, Visiting Clinical Professor, UC Irvine Law School California Monitor, A Program of the

REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement

Office of WV Attorney General Darrell McGraw MORTGAGE FORECLOSURE SETTLEMENT REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement As negotiated nationally I. RETURN

Office of WV Attorney General Darrell McGraw MORTGAGE FORECLOSURE SETTLEMENT REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement As negotiated nationally I. RETURN

Government and Private Initiatives to Address the Foreclosure Crisis

Government and Private Initiatives to Address the Foreclosure Crisis David Moskowitz Deputy General Counsel Berkeley Business Law Journal Berkeley Center for Law, Business and the Economy 2012 Symposium

Government and Private Initiatives to Address the Foreclosure Crisis David Moskowitz Deputy General Counsel Berkeley Business Law Journal Berkeley Center for Law, Business and the Economy 2012 Symposium

HAMP Trusted Advisor 1

Home Affordable Modification Program ( ) Training for Trusted Advisors Making Home Affordable February February 2016 2016 Objectives 1 MHA Program Highlights 2 Overview 3 Eligibility Criteria 4 Protections

Home Affordable Modification Program ( ) Training for Trusted Advisors Making Home Affordable February February 2016 2016 Objectives 1 MHA Program Highlights 2 Overview 3 Eligibility Criteria 4 Protections

HAMP Home Affordable Modification Program UPDATE

HAMP Home Affordable Modification Program UPDATE The whole purpose of HAMP is to try and prevent foreclosures. Homeowners have to prove a hardship and go through a protocol that proves this is a good use

HAMP Home Affordable Modification Program UPDATE The whole purpose of HAMP is to try and prevent foreclosures. Homeowners have to prove a hardship and go through a protocol that proves this is a good use

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Trusted Advisors Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview Eligibility Criteria Protections

Home Affordable Modification Program (HAMP ) Training for Trusted Advisors Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview Eligibility Criteria Protections

Servicing and Loss Mitigation. Jennifer Schultz, Esq. Community Legal Services, Inc W. Erie Ave. Philadelphia, PA

Servicing and Loss Mitigation Jennifer Schultz, Esq. Community Legal Services, Inc. 1410 W. Erie Ave. Philadelphia, PA 19140 jschultz@clsphila.org What kind of loan do you have? FHA GSE Origination-based

Servicing and Loss Mitigation Jennifer Schultz, Esq. Community Legal Services, Inc. 1410 W. Erie Ave. Philadelphia, PA 19140 jschultz@clsphila.org What kind of loan do you have? FHA GSE Origination-based

Understanding the National Mortgage Settlement A Guide for Housing Counselors

Understanding the National Mortgage Settlement A Guide for Housing Counselors June 2013 Copyright 2013, National Consumer Law Center, Inc. All rights reserved. This work is copyrighted by the National

Understanding the National Mortgage Settlement A Guide for Housing Counselors June 2013 Copyright 2013, National Consumer Law Center, Inc. All rights reserved. This work is copyrighted by the National

TOPIC CFPB HBOR NMS. January 10, January 1, April 4, Servicers and sub-servicers; not trustees acting under a DOT (a).

.") TOPIC CFPB HBOR NMS Effective date January 10, 2014. January 1, 2013. April 4, 2012. Entities regulated Property protected All servicers of federally related mortgage loans (nearly all servicers). 1024.2.*

TOPIC CFPB HBOR NMS Effective date January 10, 2014. January 1, 2013. April 4, 2012. Entities regulated Property protected All servicers of federally related mortgage loans (nearly all servicers). 1024.2.*

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017 1 Diane Cipollone, Esq. Consultant to National Fair Housing Alliance Former Director

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017 1 Diane Cipollone, Esq. Consultant to National Fair Housing Alliance Former Director

The National Mortgage Settlement: July 31, :00 4:00pm

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Webinar Objectives Today Provide an overview of the National Mortgage

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Webinar Objectives Today Provide an overview of the National Mortgage

Streamline HAMP Modification Process. Training for Servicers

Streamline HAMP Modification Process Training for Servicers Agenda 1 2 3 64 5 Overview Eligibility Criteria Streamline HAMP Policy and Streamline HAMP NPV Tool Streamline HAMP Process Resources 2 MHA Offers

Streamline HAMP Modification Process Training for Servicers Agenda 1 2 3 64 5 Overview Eligibility Criteria Streamline HAMP Policy and Streamline HAMP NPV Tool Streamline HAMP Process Resources 2 MHA Offers

HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012

LOAN MODIFICATION UPDATE July 17, 2012") HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012 Diane Thompson, NCLC, Moderator Jeff Gentes, Connecticut Fair Housing Center Lisa Sitkin, Housing and Economic Rights Advocates 0 The World of

HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012 Diane Thompson, NCLC, Moderator Jeff Gentes, Connecticut Fair Housing Center Lisa Sitkin, Housing and Economic Rights Advocates 0 The World of

HAMP Resolution Matrix

Homeowner HAMP Eligibility Issues HAMP Resolution Matrix 1 (1) Verify whether the property is owner occupied (for HAMP Tier 2 rental properties, must have missed 2 or more payments). Homeowner is (2) Verify

Homeowner HAMP Eligibility Issues HAMP Resolution Matrix 1 (1) Verify whether the property is owner occupied (for HAMP Tier 2 rental properties, must have missed 2 or more payments). Homeowner is (2) Verify

First Lien Modification Program Home Affordable Modification Program. Phase 1 Engagement

First Lien Modification Program Home Affordable Modification Program Objective The objective of this three part training series is to assist servicers in the execution of the Home Affordable Modification

First Lien Modification Program Home Affordable Modification Program Objective The objective of this three part training series is to assist servicers in the execution of the Home Affordable Modification

Supplemental Directive November 3, Home Affordable Modification Program Borrower Notices

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Making Home Affordable. The Second Lien Modification Program (2MP) for Servicers

for Servicers") Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MP

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MP

Servicing Standards Quarterly Compliance Metrics Executive Summary

EXHIBIT E-1 Servicing Standards Quarterly Compliance Metrics Executive Summary Sampling: (a) A random selection of the greater of 100 loans and a statistically significant sample. (b) Sample will be selected

EXHIBIT E-1 Servicing Standards Quarterly Compliance Metrics Executive Summary Sampling: (a) A random selection of the greater of 100 loans and a statistically significant sample. (b) Sample will be selected

2MP Servicer Training 1

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MPTrial

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MPTrial

Supplemental Directive May 11, Home Affordable Unemployment Program. Help for Unemployed Borrowers. Background

Supplemental Directive 10-04 May 11, 2010 Home Affordable Unemployment Program Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility, underwriting and

Supplemental Directive 10-04 May 11, 2010 Home Affordable Unemployment Program Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility, underwriting and

Making Home Affordable

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

Loan Modifications 101 Tara Twomey National Consumer Law Center

Loan ifications 101 Tara Twomey National Consumer Law Center By the time the foreclosure crisis reached its peak in 2008, the climate for loan modifications had changed dramatically from earlier options

Loan ifications 101 Tara Twomey National Consumer Law Center By the time the foreclosure crisis reached its peak in 2008, the climate for loan modifications had changed dramatically from earlier options

Supplemental Directive November 30, 2012

Supplemental Directive 12-09 November 30, 2012 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 12-09 November 30, 2012 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Home Affordable Unemployment Program (UP)

") Home Affordable Unemployment Program (UP) Training for Servicers 1 Agenda 1 2 Phase 1 Phase 2 Phase 3 3 4 Overview UP Process Evaluation Phase Forbearance Period Transition Phase Reporting Requirements

Home Affordable Unemployment Program (UP) Training for Servicers 1 Agenda 1 2 Phase 1 Phase 2 Phase 3 3 4 Overview UP Process Evaluation Phase Forbearance Period Transition Phase Reporting Requirements

Effective Foreclosure Timeline Management Reference Guide

Effective Foreclosure Timeline Management Reference Guide A foreclosure timeline is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the foreclosure

Effective Foreclosure Timeline Management Reference Guide A foreclosure timeline is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the foreclosure

Workout Hierarchy for Fannie Mae Conventional Loans NOTE: Refer to the Fannie Mae Servicing Guide

Workout Hierarchy for Fannie Mae Conventional Loans The following table is a summary of Fannie Mae workout options available to assist borrowers experiencing financial hardship. The servicer must first

Workout Hierarchy for Fannie Mae Conventional Loans The following table is a summary of Fannie Mae workout options available to assist borrowers experiencing financial hardship. The servicer must first

Making Home Affordable Program Performance Report Third Quarter 2015

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE THIRD QUARTER OF 2015 MHA AT-A-GLANCE Approximately 2.5 Million Homeowner Assistance Actions have taken place under Making Home Affordable

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE THIRD QUARTER OF 2015 MHA AT-A-GLANCE Approximately 2.5 Million Homeowner Assistance Actions have taken place under Making Home Affordable

New CFPB Mortgage Servicing Rules (Part 2): Loss Mitigation Procedures. John Rao Lisa Sitkin Josh Zinner

: Loss Mitigation Procedures. John Rao Lisa Sitkin Josh Zinner") D4 D4 New CFPB Mortgage Servicing Rules (Part 2): Loss Mitigation Procedures John Rao Lisa Sitkin Josh Zinner RESPA Servicing Rules Rules effective Jan. 10, 2014 dealing with foreclosure avoidance: New

D4 D4 New CFPB Mortgage Servicing Rules (Part 2): Loss Mitigation Procedures John Rao Lisa Sitkin Josh Zinner RESPA Servicing Rules Rules effective Jan. 10, 2014 dealing with foreclosure avoidance: New

Supplemental Directive December 21, 2017

Supplemental Directive 17-02 December 21, 2017 Making Home Affordable Program Handbook for Servicers Version 5.2 and Administrative Clarifications In February 2009, the Federal Government introduced the

Supplemental Directive 17-02 December 21, 2017 Making Home Affordable Program Handbook for Servicers Version 5.2 and Administrative Clarifications In February 2009, the Federal Government introduced the

Navigating the Loan Modification Process Part III. Presented by: Empire Justice Center Kevin Purcell, Esq.

Navigating the Loan Modification Process Part III Presented by: Empire Justice Center Kevin Purcell, Esq. 1 Other MHA Programs HAMP Tier Two Principal Reduction Alternative Home Affordable Unemployment

Navigating the Loan Modification Process Part III Presented by: Empire Justice Center Kevin Purcell, Esq. 1 Other MHA Programs HAMP Tier Two Principal Reduction Alternative Home Affordable Unemployment

MHA Reason Codes and Descriptions

s and s MHA Reason Code 1 Ineligible Mortgage Loan is not eligible for modification under the MHA program because it does not meet one or more of the following basic program eligibility criteria: Mortgage

s and s MHA Reason Code 1 Ineligible Mortgage Loan is not eligible for modification under the MHA program because it does not meet one or more of the following basic program eligibility criteria: Mortgage

The National Mortgage Settlement: July 31, :00 4:00pm

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Presenters Moderator: National Development Council (NDC) Jennie Vertrees

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Presenters Moderator: National Development Council (NDC) Jennie Vertrees

Supplemental Directive December 10, Making Home Affordable Program Program End Date and Administrative Clarifications

Supplemental Directive 18-01 December 10, 2018 Making Home Affordable Program Program End Date and Administrative Clarifications In February 2009, the Making Home Affordable (MHA) Program was introduced

Supplemental Directive 18-01 December 10, 2018 Making Home Affordable Program Program End Date and Administrative Clarifications In February 2009, the Making Home Affordable (MHA) Program was introduced

Making Home Affordable

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Loan Workout Hierarchy for Fannie Mae Conventional Loans

Loan Workout Hierarchy for Fannie Mae Conventional Loans The following table identifies the Fannie Mae loss mitigation options that are available to assist borrowers experiencing financial hardship. Generally,

Loan Workout Hierarchy for Fannie Mae Conventional Loans The following table identifies the Fannie Mae loss mitigation options that are available to assist borrowers experiencing financial hardship. Generally,

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness Edward DeMarco, Acting Director Federal Housing Finance Agency The Brookings Institution April 10, 2012 My goal today is to answer

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness Edward DeMarco, Acting Director Federal Housing Finance Agency The Brookings Institution April 10, 2012 My goal today is to answer

The National Mortgage Settlement Monitor s Final Crediting Report March 18, 2014

Final Crediting Report The National Mortgage Settlement Monitor s Final Crediting Report March 18, 2014 On March 18, 2014, I filed reports with the United States District Court for the District of Columbia

Final Crediting Report The National Mortgage Settlement Monitor s Final Crediting Report March 18, 2014 On March 18, 2014, I filed reports with the United States District Court for the District of Columbia

Case 1:12-cv RMC Document 14 Filed 04/04/12 Page 1 of 92

Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 1 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 2 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 3 of 92 Case 1:12-cv-00361-RMC

Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 1 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 2 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 3 of 92 Case 1:12-cv-00361-RMC

Case 1:12-cv RMC Document 11 Filed 04/04/12 Page 1 of 86

Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 1 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 2 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 3 of 86 Case 1:12-cv-00361-RMC

Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 1 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 2 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 3 of 86 Case 1:12-cv-00361-RMC

Delinquency Management for Mortgages Secured by Primary Residences

Delinquency Management for Mortgages Secured by Primary Residences This reference guide highlights Freddie Mac s requirements for managing delinquent mortgages secured by a borrower s primary residence.

Delinquency Management for Mortgages Secured by Primary Residences This reference guide highlights Freddie Mac s requirements for managing delinquent mortgages secured by a borrower s primary residence.

Supplemental Directive October 18, 2013

Supplemental Directive 13-09 October 18, 2013 Making Home Affordable Program CFPB Mortgage Servicing Regulations In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-09 October 18, 2013 Making Home Affordable Program CFPB Mortgage Servicing Regulations In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation FIS Regulatory Advisory Services Regulatory.Services@fisglobal.com New Servicing Rules Under RESPA Early Intervention,

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation FIS Regulatory Advisory Services Regulatory.Services@fisglobal.com New Servicing Rules Under RESPA Early Intervention,

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017 1 Diane Cipollone, Esq. Consultant to National Fair

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017 1 Diane Cipollone, Esq. Consultant to National Fair

Home Affordable Modification Program Policies and Procedures Manual

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

Supplemental Directive June 3, Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative

Supplemental Directive 10-05 June 3, 2010 Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative Background In Supplemental Directive 09-01, the Treasury Department

Supplemental Directive 10-05 June 3, 2010 Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative Background In Supplemental Directive 09-01, the Treasury Department

Supplemental Directive December 10, 2013

Supplemental Directive 13-12 December 10, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-12 December 10, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive August 9, Home Affordable Foreclosure Alternatives Program Policy Update

Supplemental Directive 11-08 August 9, 2011 Home Affordable Foreclosure Alternatives Program Policy Update In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 11-08 August 9, 2011 Home Affordable Foreclosure Alternatives Program Policy Update In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Making Home Affordable

Making Home Affordable Today s Topics: MHA Resources MHA Refinance (HARP) MHA Loan Modifications (HAMP) Other Programs for Borrowers 2 What is Making Home Affordable? Part of President Obama s Homeowner

Making Home Affordable Today s Topics: MHA Resources MHA Refinance (HARP) MHA Loan Modifications (HAMP) Other Programs for Borrowers 2 What is Making Home Affordable? Part of President Obama s Homeowner

Servicemember Financial Protection

Servicemember Financial Protection Outlook Live Webinar September 10, 2012 An Interagency Discussion of Recent Servicemember Financial Protection Guidance and Compliance with the Servicemembers Civil Relief

Servicemember Financial Protection Outlook Live Webinar September 10, 2012 An Interagency Discussion of Recent Servicemember Financial Protection Guidance and Compliance with the Servicemembers Civil Relief

Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers

Model (v5.02) Training Module for Servicers") Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers # Agenda 1 2 3 4 5 6 7 8 9 HAMP Eligibility Criteria Base NPV Model Overview Standard and Alternative Modification

Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers # Agenda 1 2 3 4 5 6 7 8 9 HAMP Eligibility Criteria Base NPV Model Overview Standard and Alternative Modification

Audit Survival. Jon Paukovich Vice President, Mortgage Lending Ent Federal Credit Union. Casey Perkins Director, Collections Ent Federal Credit Union

Audit Survival Jon Paukovich Vice President, Mortgage Lending Ent Federal Credit Union Casey Perkins Director, Collections Ent Federal Credit Union What to Expect Thorough review of quality control plan

Audit Survival Jon Paukovich Vice President, Mortgage Lending Ent Federal Credit Union Casey Perkins Director, Collections Ent Federal Credit Union What to Expect Thorough review of quality control plan

Making Home Affordable Program Principal Reduction Alternative Update

Supplemental Directive 10-14 October 15, 2010 Making Home Affordable Program Principal Reduction Alternative Update In February 2009, the Obama Administration introduced the Making Home Affordable Program

Supplemental Directive 10-14 October 15, 2010 Making Home Affordable Program Principal Reduction Alternative Update In February 2009, the Obama Administration introduced the Making Home Affordable Program

HFA Mortgage Assistance Programs Servicer Q&A

HFA Mortgage Assistance Programs Servicer Q&A Freddie Mac is reinforcing its on-going commitment to help financially distressed homeowners with Freddie Mac-owned or guaranteed mortgages avoid foreclosure

HFA Mortgage Assistance Programs Servicer Q&A Freddie Mac is reinforcing its on-going commitment to help financially distressed homeowners with Freddie Mac-owned or guaranteed mortgages avoid foreclosure

Freddie Mac Standard Modification Overview for Housing Counselors. Counselor Connection Baltimore, Maryland May 8, 2012

Freddie Mac Standard Modification Overview for Housing Counselors Counselor Connection Baltimore, Maryland May 8, 2012 Objectives Understand how Servicers will apply Freddie Mac requirements for the Standard

Freddie Mac Standard Modification Overview for Housing Counselors Counselor Connection Baltimore, Maryland May 8, 2012 Objectives Understand how Servicers will apply Freddie Mac requirements for the Standard

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

Foreclosure Diversion Program Information Session. Understanding and Preparing for Mediation

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Foreclosure Process in Minnesota

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

HAMP Servicer Training 1

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Lisa Sitkin National Housing Law Project May 23, 2017

Helping Your Clients Avoid Foreclosure after HAMP: A Refresher and Update on the California Homeowner Bill of Rights and Related Regulations and Programs 1 Lisa Sitkin National Housing Law Project May

Helping Your Clients Avoid Foreclosure after HAMP: A Refresher and Update on the California Homeowner Bill of Rights and Related Regulations and Programs 1 Lisa Sitkin National Housing Law Project May

Analysis of Ongoing Implementation, the Report of the Monitor of the National Mortgage Settlement

Analysis of Ongoing Implementation, the Report of the Monitor of the National Mortgage Settlement March 19, 2013 CRL Policy Brief On February 21, 2013, Joseph A. Smith, Jr., Monitor of the National Mortgage

Analysis of Ongoing Implementation, the Report of the Monitor of the National Mortgage Settlement March 19, 2013 CRL Policy Brief On February 21, 2013, Joseph A. Smith, Jr., Monitor of the National Mortgage

SPECIAL RULES FOR FORECLOSURES ON HOMES. Joseph M. Licare, Esq. Bryan Cave LLP New York, New York

SPECIAL RULES FOR FORECLOSURES ON HOMES by Joseph M. Licare, Esq. Bryan Cave LLP New York, New York 81 82 Special Rules For Foreclosures On Homes A. 90-day Pre-Foreclosure Notice and Related Requirements

SPECIAL RULES FOR FORECLOSURES ON HOMES by Joseph M. Licare, Esq. Bryan Cave LLP New York, New York 81 82 Special Rules For Foreclosures On Homes A. 90-day Pre-Foreclosure Notice and Related Requirements

Lender Letter LL

Lender Letter LL-2017-09 November 2, 2017 To: All Fannie Mae Single-Family Servicers Fannie Mae Extend Modification for Disaster Relief and Other Clarifications for Mortgage Loans Impacted by Disaster

Lender Letter LL-2017-09 November 2, 2017 To: All Fannie Mae Single-Family Servicers Fannie Mae Extend Modification for Disaster Relief and Other Clarifications for Mortgage Loans Impacted by Disaster

HAMP. The Hamp Program. Avoid Foreclosure. More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages

The Program Works to Help Homeowners Avoid Foreclosure Avoid Foreclosure HAMP More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages What is HAMP? Home Affordable Modification

The Program Works to Help Homeowners Avoid Foreclosure Avoid Foreclosure HAMP More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages What is HAMP? Home Affordable Modification

Supplemental Directive January 28, Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications

Supplemental Directive 10-01 January 28, 2010 Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications Background In Supplemental Directive 09-01, the Treasury Department

Supplemental Directive 10-01 January 28, 2010 Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications Background In Supplemental Directive 09-01, the Treasury Department

Announcement SVC September 21, 2010

Announcement SVC-2010-15 September 21, 2010 Updates to Fannie Mae's Forbearance, Income Eligibility, and Home Affordable Modification Program Requirements. Introduction In this Announcement, Fannie Mae

Announcement SVC-2010-15 September 21, 2010 Updates to Fannie Mae's Forbearance, Income Eligibility, and Home Affordable Modification Program Requirements. Introduction In this Announcement, Fannie Mae

Servicing Alignment Initiative Overview for Freddie Mac Servicers

Servicing Alignment Initiative Overview for Freddie Mac Servicers Consistent requirements and processes for servicing delinquent mortgages Working at the direction of, and in concert with, the Federal

Servicing Alignment Initiative Overview for Freddie Mac Servicers Consistent requirements and processes for servicing delinquent mortgages Working at the direction of, and in concert with, the Federal

Announcement November 2, Updates and Clarifications to the Home Affordable Modification Program

Announcement 09-31 November 2, 2009 Amends these Guides: Servicing Updates and Clarifications to the Home Affordable Modification Program Introduction Announcement 09-05R, Reissuance of the Introduction

Announcement 09-31 November 2, 2009 Amends these Guides: Servicing Updates and Clarifications to the Home Affordable Modification Program Introduction Announcement 09-05R, Reissuance of the Introduction

What is the Servicing Alignment Initiative? Overview:

Servicing Alignment Initiative: Freddie Mac Requirements Overview for Housing Counselors Orlando, September 27, 2011 What is the Servicing Alignment Initiative? Overview: Freddie Mac launched a comprehensive

Servicing Alignment Initiative: Freddie Mac Requirements Overview for Housing Counselors Orlando, September 27, 2011 What is the Servicing Alignment Initiative? Overview: Freddie Mac launched a comprehensive

Making Home Affordable Case Escalation Process Training Presentation for Servicers

Making Home Affordable Case Escalation Process Training Presentation for s August July 2014 2014 Making Home Home Affordable Home Affordable July 2016 Objectives Defining Escalated Cases Commonly Escalated

Making Home Affordable Case Escalation Process Training Presentation for s August July 2014 2014 Making Home Home Affordable Home Affordable July 2016 Objectives Defining Escalated Cases Commonly Escalated

STANDARD MODIFICATION

Bulletin NUMBER: 2011-16 TO: Freddie Mac Servicers September 12, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are announcing complete requirements related to the Freddie

Bulletin NUMBER: 2011-16 TO: Freddie Mac Servicers September 12, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are announcing complete requirements related to the Freddie

Making Home Affordable Program Performance Report Second Quarter 2014

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE SECOND QUARTER OF 2014 MHA AT-A-GLANCE More than 2.1 Million Homeowner Assistance Actions have taken place under Making Home Affordable (MHA)

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE SECOND QUARTER OF 2014 MHA AT-A-GLANCE More than 2.1 Million Homeowner Assistance Actions have taken place under Making Home Affordable (MHA)

Version 3.4 As of December 15, 2011

Version 3.4 As of December 15, 2011 Table of Contents MHA Handbook v3.4 1 FOREWORD... 12 OVERVIEW... 13 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 18 1 SERVICER PARTICIPATION IN MHA... 19 1.1 SERVICER

Version 3.4 As of December 15, 2011 Table of Contents MHA Handbook v3.4 1 FOREWORD... 12 OVERVIEW... 13 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 18 1 SERVICER PARTICIPATION IN MHA... 19 1.1 SERVICER

Summary of Compliance. A Report from the Monitor of the National Mortgage Settlement

Summary of Compliance A Report from the Monitor of the National Mortgage Settlement June 19, 013 The following report summarizes my first compliance reports as Monitor under the National Mortgage Settlement,

Summary of Compliance A Report from the Monitor of the National Mortgage Settlement June 19, 013 The following report summarizes my first compliance reports as Monitor under the National Mortgage Settlement,

Supplemental Directive August 30, 2013

Supplemental Directive 13-06 August 30, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-06 August 30, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive September 30, 2014

Supplemental Directive 14-03 September 30, 2014 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 14-03 September 30, 2014 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Standard and Alternative Waterfalls 1

Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda 1 2 3 4 5 6 7 8 Overview of Eligibility Tier 1 Standard Modification Waterfall Tier 1 Alternative Modification

Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda 1 2 3 4 5 6 7 8 Overview of Eligibility Tier 1 Standard Modification Waterfall Tier 1 Alternative Modification

MHA Case Escalation Process. Training Presentation for Trusted Advisors

MHA Case Escalation Process Training Presentation for Trusted Advisors 1 MHA Case Escalations Process Objectives Type of Mortgage Loan - Determines Escalation Path Escalation Contacts Definition of an

MHA Case Escalation Process Training Presentation for Trusted Advisors 1 MHA Case Escalations Process Objectives Type of Mortgage Loan - Determines Escalation Path Escalation Contacts Definition of an

Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing

October 27, 2010 Media Contact: Brad Dwin (202) 589-1938 brad@hopenow.com Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing (WASHINGTON, DC) Faith Schwartz, senior adviser, and former

October 27, 2010 Media Contact: Brad Dwin (202) 589-1938 brad@hopenow.com Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing (WASHINGTON, DC) Faith Schwartz, senior adviser, and former

Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015

Compensation Last Updated: April 30, 2015") Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015 Program Name Frequency and Timing Payee/Beneficiary Amount Accrual and Notes Servicer Incentive One time Servicer/Servicer Non-GSE

Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015 Program Name Frequency and Timing Payee/Beneficiary Amount Accrual and Notes Servicer Incentive One time Servicer/Servicer Non-GSE

Version 2.0 As of September 22, 2010

Version 2.0 As of September 22, 2010 MHA Handbook v2.0 1 FOREWORD... 6 OVERVIEW... 7 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 11 1 SERVICER PARTICIPATION IN MHA... 12 1.1 SERVICER PARTICIPATION

Version 2.0 As of September 22, 2010 MHA Handbook v2.0 1 FOREWORD... 6 OVERVIEW... 7 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 11 1 SERVICER PARTICIPATION IN MHA... 12 1.1 SERVICER PARTICIPATION

Example H.O.M.E. Report- Beta1 of 42.

Example H.O.M.E. Report- Beta1 of 42. PREPARED BY: BORROWER(s): PROPERTY ADDRESS: DIY Internal Demo Company, 123 swe 12 ave, miami, FL 33167, (786) 787-8878 (Phone), (987) 897-8978 (fascimile) HAMP Example

Example H.O.M.E. Report- Beta1 of 42. PREPARED BY: BORROWER(s): PROPERTY ADDRESS: DIY Internal Demo Company, 123 swe 12 ave, miami, FL 33167, (786) 787-8878 (Phone), (987) 897-8978 (fascimile) HAMP Example

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Making Home Affordable Working Together to Help Homeowners

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Legal Basics: Foreclosure Prevention. March 21, 2017 Odette Williamson National Consumer Law Center

Legal Basics: Foreclosure Prevention March 21, 2017 Odette Williamson National Consumer Law Center National Consumer Law Center 2013 National Consumer Law Center Advocate on behalf of low-income consumers

Legal Basics: Foreclosure Prevention March 21, 2017 Odette Williamson National Consumer Law Center National Consumer Law Center 2013 National Consumer Law Center Advocate on behalf of low-income consumers

Servicing Guide Announcement SVC

Servicing Guide Announcement SVC-2012-18 Updates to Delinquency Management and Default Prevention Requirements August 22, 2012 This Announcement describes policy changes to several delinquency management

Servicing Guide Announcement SVC-2012-18 Updates to Delinquency Management and Default Prevention Requirements August 22, 2012 This Announcement describes policy changes to several delinquency management

Housing Risk. Policy Issues & Responses

Housing Risk Policy Issues & Responses Fifth Annual Risk Management Conference Federal Reserve Bank of Chicago April 11, 2012 Bill Longbrake Executive in Residence Robert H. Smith School of Business, University

Housing Risk Policy Issues & Responses Fifth Annual Risk Management Conference Federal Reserve Bank of Chicago April 11, 2012 Bill Longbrake Executive in Residence Robert H. Smith School of Business, University

The deadline for implementation by servicers was April 5, Mortgage delinquent or default is reasonably foreseeable.

1. What is HAFA? The Home Affordable Foreclosure Alternatives Program, known as HAFA, is designed to help owners (referred to below as borrowers) who are unable to retain their home under the Home Affordable

1. What is HAFA? The Home Affordable Foreclosure Alternatives Program, known as HAFA, is designed to help owners (referred to below as borrowers) who are unable to retain their home under the Home Affordable

Deanne R. Stodden. Member, Rogers & Stodden, LLC Of Counsel, Carpenter & Klatskin, PC

Deanne R. Stodden Member, Rogers & Stodden, LLC Of Counsel, Carpenter & Klatskin, PC Loss Mitigation is generally defined as the process a lender goes through to work with a borrower (home owner or business

Deanne R. Stodden Member, Rogers & Stodden, LLC Of Counsel, Carpenter & Klatskin, PC Loss Mitigation is generally defined as the process a lender goes through to work with a borrower (home owner or business

A Report from the Monitor of the National Mortgage Settlement May 14, 2014

Compliance in Progress A Report from the Monitor of the National Mortgage Settlement May 14, 2014 The following summary is an overview of my third set of compliance reports, which I have filed with the

Compliance in Progress A Report from the Monitor of the National Mortgage Settlement May 14, 2014 The following summary is an overview of my third set of compliance reports, which I have filed with the

A Report from the Monitor of the National Mortgage Settlement June 30, 2015

Compliance Update A Report from the Monitor of the National Mortgage Settlement June 30, 2015 The following is a summary of the fifth set of compliance reports I have filed with the United States District

Compliance Update A Report from the Monitor of the National Mortgage Settlement June 30, 2015 The following is a summary of the fifth set of compliance reports I have filed with the United States District

Senate Bill No. 818 CHAPTER 404

Senate Bill No. 818 CHAPTER 404 An act to amend Section 2924 of, to amend and repeal Sections 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.15, and 2924.17 of, to add Sections 2923.55, 2924.9, 2924.10,

Senate Bill No. 818 CHAPTER 404 An act to amend Section 2924 of, to amend and repeal Sections 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.15, and 2924.17 of, to add Sections 2923.55, 2924.9, 2924.10,

Freddie Mac Standard and Streamlined Modification. Reference Guide. September 2017

Freddie Mac Standard and Streamlined Modification Reference Guide September 2017 This Page Intentionally Left Blank Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard

Freddie Mac Standard and Streamlined Modification Reference Guide September 2017 This Page Intentionally Left Blank Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

CFPB s PROPOSED RULE ON SERVICING STANDARDS

CFPB s PROPOSED RULE ON SERVICING STANDARDS September 25, 2012 Larry E. Platt 202.778.9034 Larry.platt@klgates.com Nanci L. Weissgold 202.778.9314 Nanci.weissgold@klgates.com Kerri M. Smith 202.778.9445

CFPB s PROPOSED RULE ON SERVICING STANDARDS September 25, 2012 Larry E. Platt 202.778.9034 Larry.platt@klgates.com Nanci L. Weissgold 202.778.9314 Nanci.weissgold@klgates.com Kerri M. Smith 202.778.9445

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu *

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu * Description & Purpose Contents As a condition to receiving the incentive payments offered through the Home Affordable

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu * Description & Purpose Contents As a condition to receiving the incentive payments offered through the Home Affordable

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies Effective September 1, 2011 There are approximately 3.3 million Americans who are in or close to foreclosure. Fannie Mae and Freddie

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies Effective September 1, 2011 There are approximately 3.3 million Americans who are in or close to foreclosure. Fannie Mae and Freddie

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications United Guaranty Residential Insurance Company P. O. Box 21367 Greensboro, NC 27420-1367 Phone: 888.822.5584 (select

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications United Guaranty Residential Insurance Company P. O. Box 21367 Greensboro, NC 27420-1367 Phone: 888.822.5584 (select

Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet

Eligibility Worksheet") Loan Look Up Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet HAFA: A Making Home Affordable (MHA) Initiative Determine the type of first lien (Fannie Mae, Freddie Mac or Treasury)

Loan Look Up Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet HAFA: A Making Home Affordable (MHA) Initiative Determine the type of first lien (Fannie Mae, Freddie Mac or Treasury)

Freddie Mac Standard and Streamlined Modification Reference Guide. April 2015

Freddie Mac Standard and Streamlined Modification Reference Guide April 2015 Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard Modifications... 2 Ineligible Criteria

Freddie Mac Standard and Streamlined Modification Reference Guide April 2015 Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard Modifications... 2 Ineligible Criteria

Communicating with Borrowers: Collections and Loss Mitigation Reference Guide

Communicating with Borrowers: Collections and Loss Mitigation Reference Guide It is important to establish trust and confidence in the early stages of communications with borrowers. The more knowledge

Communicating with Borrowers: Collections and Loss Mitigation Reference Guide It is important to establish trust and confidence in the early stages of communications with borrowers. The more knowledge