Refund to Savings: Evidence of Tax- Time Saving in a National Randomized Control Trial

|

|

|

- Colin Watkins

- 5 years ago

- Views:

Transcription

1 Refund to Savings: Evidence of Tax- Time Saving in a National Randomized Control Trial Dana C. Perantie Michal Grinstein-Weiss May 16, 2014 Note: Statistical compilations disclosed in this document relate directly to the bona fide research of and public policy discussions concerning the use of the IRS split refund capability and promotion of increased savings in connection with the tax compliance process. All compilations are anonymous and do not disclose cells containing data from fewer than ten tax returns. IRS Reg

2 About the Refund to Savings Initiative Largest saving experiment ever conducted in the United States in terms of sample size Developing and testing model for a universal, scalable savings policy Tax time is a major financial event for households 146M individual returns filed $323 billion refunded

3 2013 Refund to Savings Initiative Randomized controlled trial in TurboTax 684,000 participants Household Financial Survey 6 months 20,000 survey takers 8,300 survey takers

4

5 In-Product Intervention

6 Motivational Prompts Family Future Emergency

7 Anchors

8 R2S Participant Characteristics Household Income: $13,294 Federal Tax Refund: $921 Claiming EITC: 39%; Median: $1,985 Age: 28 68% Single; 21% Head; 11% Married

9 Key Questions 1. Can behavioral economics techniques increase deposits to savings at tax time? 2. Does R2S increase savings 6 months later? 3. What factors are associated with saving?

10 Key Questions 1. Can behavioral economics techniques increase deposits to savings at tax time? 2. Does R2S increase savings 6 months later? 3. What factors are associated with saving?

11 Overall Tax Time Impact Increased number of people who deposited to savings 4,800 additional savers Increased amount deposited to savings $5.9 million dollars more deposited into savings

12 Percentage Who Split Refunds into Savings % of Participants Who Split Refund n = 228,828

n = 228,828")

13 Amount Deposited into Savings Amount Deposited to Savings ($) n = 228,828

14 Splitters: Amounts Deposited into Savings Amount Deposited to Savings ($) n = 10,365

15 Key Questions 1. Can behavioral economics techniques increase deposits to savings at tax time? 2. Does R2S increase savings 6 months later? 3. What factors are associated with saving?

16 Probability of Saving Refund 6 Months % of Participants Who Saved Refund * * n = 4,833

17 Percentage of Refund Saved 6 Months Control Group Mean = 19.2% % of Refund Saved 0.7% 2.6% 5.0% -1.2% Anchor 25% Anchor 50%* Anchor 75%** Anchor $100 or $250 n = 4,833

18 Probability of Access to $2K in an Emergency 6 Months after Tax Time 60% 56% 50% 44% 48% 50% 51% % of Respondents 40% 30% 20% 10% 0% * * * Control Anchor 25% Anchor 50% Anchor 75% Anchor $100 or $250

19 Key Questions 1. Can behavioral economics techniques increase deposits to savings at tax time? 2. Does R2S increase savings 6 months later? 3. What factors are associated with saving?

20 Factors Associated with Saving Financial shocks Debt Use of alternative financial services Asset limits

21 Financial Shocks 66% experienced at least one of the following: Trip to hospital Major vehicle repair Period of unemployment Legal fees/expenses n = 5,552

22 Saving 6 Months by Financial Shock % of Participants Who Saved Refund n = 5,556

23 Saving 6 Months by Type of Debt % of Participants Who Saved Refund n = 8,126

24 Saving 6 Months by Alternative Financial Services Use % of Participants Who Saved Refund Check casher Non-bank money order Non-bank wire transfer Payday loan Rent-to-own Payroll card Auto title loan n = 5,825

25 Asset Limits Percentage of Refund Saved 6 Months % of Refund Saved If I saved more, I would lose government benefits. n = 8,300

26 Summary R2S increased both the number and amount of deposits to savings Impact observed 6 months after tax filing Anchors more effective than prompts Financial shocks, debt, use of AFS, and asset limits associated with less saving

27 Thank You Intuit Inc. Ford Foundation Annie E. Casey Foundation University of North Carolina Anonymous funder

28 Why Tax Time Saving? Universal, Permanent, and Recurring Major Financial Event for Households o Approximately 146M individual returns filed every year 1 o $323 billion refunded each year 2 o 27M low-income households received nearly $63 billion in EITC for TY Golden opportunity Evidence from asset-building research $**2, IRS Data Book Publication 55B IRS Data Book IRS Statistics for Tax Returns with Earned Income Tax Credit

29 HFS - Insights 22% homeowners $2,500 in credit card debt 38% used alternative financial services in previous year 57% skipped paying a bill in previous year

30 Products Used by Savers Type of Account % of Respondents Savings Acct 66% Checking Acct 33% Prepaid Card 1% IRA 5% Education Acct 1% Savings Bonds 2% Other 6% N = 2,224

31 Anchoring Subject spins a wheel to generate random number Asked, What % of countries in Africa belong to the UN? Guess is influenced by anchor : o Wheel says 65, avg. guess = 45% o Wheel says 10, avg. guess = 25% Tversky & Kahneman, 1974

32 DEMOGRAPHICS

33 Gender and family status 61% are women 59% are single, never married 20% are unmarried, divorced 62% have no kids under 18 in the household 77% have 2 or fewer adults in the household

34 Race Hispanic Asian 8% 2% Race Other 4% Black 11% White 75% N=19,269

35 Education 43% 38% 27% college degree or more some college currently enrolled

36 FINANCIAL POSITION

37 Income Median household: $17,600 National Median Household Income: $50, households (2%) report $0 or negative income 25 th percentile: $8, th percentile: $26,593

38 Employment Employment Out of labor force 20% Unemployed 11% Full-time/self 48% Part-time 21%

39 Highest interest rate 42% don t know the rate on their debt with the highest interest rate Among those who do know: Type of Debt N Mean rate by % Credit cards Student loans Personal loans Bank loans Payday loans Medical bills Past due rent/bills Negative balances

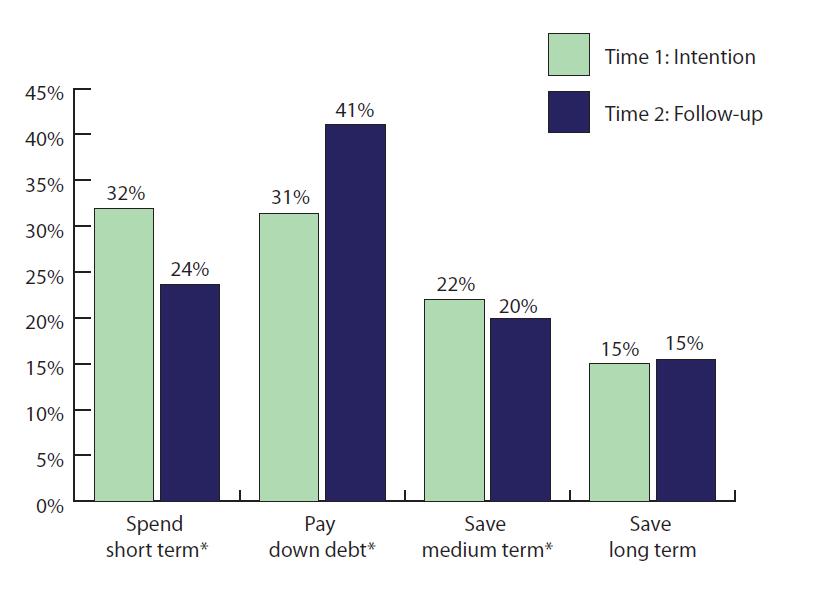

40 Among those who bank (94% of sample) at a 2-12% rate for a $1-10 fee for a $10-25 fee with an average Annual Percentage Rate of 400% with an Annual Percentage Rate up to 240% that cost 10% of the refund at prices well above market price with an Annual Percentage Rate up to 250%

41 Assets % of responders that own median liquid assets

42 Current money management strategy pen and paper software bank website internet service smartphone app accountant don t use anything (people could circle as many as they use)

43 Average refund saved is more than average monthly income $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100 $0 Source: 2012 R2S Experiment $839 Median Monthly Income $951 Median Refund Saved Among Low Income Refund Savers

44 Debt Credit Card Medical Education Past-due rent/bills Median debt = $1,500 Median debt = $1,522 Median debt = $20,000 Median debt = $500

45 Bank Access Access Unbanked 6% Banked 57% Underbanked 37%

46 Plan for the tax refund 62% plan to save part of their refund for at least a few months How does the average person plan to allocate their refund? ~ 1/3 to spending within one month ~ 1/3 to debt clearing ~ 1/3 to savings

47 Overall Impact 6 Months Later Anchors affected the number of people with any portion of the refund 6 months later Anchors also influenced the percentage of refund saved Higher anchors tended to be more effective (50% and 75%)

48 Tax Time Intention for Refund

49 Actual Allocation

50 Tax Time Intention vs. Actual Allocation

51 % of Refund Saved for Six Months Variable Coefficient Robust P-Value Standard Error Treatment: Anchor 25% Anchor 50% Anchor 75% Anchor $100 or $

52 Does tax time deposit predict 6 months saving? 50% Saved any amount 30% Proportion Saved % who saved 6 months 45% 40% 35% 30% 25% 20% 15% 10% 5% Proportion of refund saved 6 months 25% 20% 15% 10% 5% 0% No Deposit Deposit 0% No Deposit Deposit

53 Access to $2,000 in an Emergency N=7,645

54 Financial Hardships n =7,624

70%")

55 Financial Insecurity (% who skipped ) 70% skipped at least one of the following Rent Bills Medical Care Medications N=20,558

56 Highest interest rate Out of the kinds of debt you indicated having, which has the highest interest rate? don t know credit or charge cards student loans pay day loans medical bills

57 Are you familiar with U.S. savings bonds? YES SORT OF NO

58 Saving by Hardship Experience % of Participants who Saved Refund

59 Difficulty in Covering Expenses % of Participants who Saved Refund n = 8,267

60 Types of Debt % of Participants with Debt n = 18,956

61 Interest in Alternative Refund Methods n = 17,901

62 Interest in Alternative Refund Methods by Banked Status n = 961

63 Conclusions R2S interventions increased: Number of savers Amount of savings Number of splitters Proportion of split to savings Follow-up survey revealed: Tax time deposits saved 6 months Many barriers to saving for low-income people Interest in tax time product innovation

Refund to Savings (R2S): Overcoming Barriers to Economic Security

: Overcoming Barriers to Economic Security") Refund to Savings (R2S): Overcoming Barriers to Economic Security Krista Comer, Michal Grinstein-Weiss, Dan Ariely, and Clint Key Southern Regional Asset Building Coalition October 17, 2013 American families

Refund to Savings (R2S): Overcoming Barriers to Economic Security Krista Comer, Michal Grinstein-Weiss, Dan Ariely, and Clint Key Southern Regional Asset Building Coalition October 17, 2013 American families

Refund to Savings (R2S):

:") 2012 Refund to Savings (R2S): Insight from the Field Refund to Savings (R2S): Insight from the Field, 2012 Krista Holub Center for Social Development Washington University in St. Louis Michal Grinstein-Weiss

2012 Refund to Savings (R2S): Insight from the Field Refund to Savings (R2S): Insight from the Field, 2012 Krista Holub Center for Social Development Washington University in St. Louis Michal Grinstein-Weiss

Behavioral Economics at Tax Time

Behavioral Economics at Tax Time Joe Valenti, Director of Asset Building at the Center for American Progress Dr. Michal Grinstein-Weiss, Associate Director of the Center for Social Development at Washington

Behavioral Economics at Tax Time Joe Valenti, Director of Asset Building at the Center for American Progress Dr. Michal Grinstein-Weiss, Associate Director of the Center for Social Development at Washington

June 2014 CSD POLICY BRIEF 14-13

June 2014 CSD POLICY BRIEF 14-13 Lack of Emergency Savings Puts American Households at Risk: Evidence from the Refund to Savings Initiative By Michal Grinstein-Weiss, Blair Russell, Brad Tucker, and Krista

June 2014 CSD POLICY BRIEF 14-13 Lack of Emergency Savings Puts American Households at Risk: Evidence from the Refund to Savings Initiative By Michal Grinstein-Weiss, Blair Russell, Brad Tucker, and Krista

The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet

The CFSI Underbanked Consumer Study - Fact Sheet June 8, 28 The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet Released: June 8, 28 Introduction The purpose

The CFSI Underbanked Consumer Study - Fact Sheet June 8, 28 The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet Released: June 8, 28 Introduction The purpose

In Baltimore City today, 20% of households live in poverty, but more than half of the

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

*Remember to attach a copy of your state issued ID and credit report*

INDIVIDUAL DEVELOPMENT ACCOUNT (IDA) APPLICATION CONTACT INFORMATION Date of Application Regional Communty Action Agency Last Name First Name M.I. SS # DOB Home and Cell Phone # (include area code) Street

INDIVIDUAL DEVELOPMENT ACCOUNT (IDA) APPLICATION CONTACT INFORMATION Date of Application Regional Communty Action Agency Last Name First Name M.I. SS # DOB Home and Cell Phone # (include area code) Street

United Way Worldwide: MyFreeTaxes Survey November 18-23, Report Date: January 28, 2016

United Way Worldwide: MyFreeTaxes Survey November 18-23, 2015 Report Date: January 28, 2016 Methodology Survey Type: The national public opinion survey was conducted using Lightspeed GMI online survey.

United Way Worldwide: MyFreeTaxes Survey November 18-23, 2015 Report Date: January 28, 2016 Methodology Survey Type: The national public opinion survey was conducted using Lightspeed GMI online survey.

S E P T E M B E R MassMutual African American Middle America Financial Security Study

S E P T E M B E R 2 0 1 7 MassMutual African American Middle America Financial Security Study Background and Methodology Study Objectives To raise awareness of the threats and obstacles to African American

S E P T E M B E R 2 0 1 7 MassMutual African American Middle America Financial Security Study Background and Methodology Study Objectives To raise awareness of the threats and obstacles to African American

INDIVIDUAL DEVELOPMENT ACCOUNT (IDA) APPLICATION. AGENCY INFORMATION Regional Communty Action Agency

APPLICATION. AGENCY INFORMATION Regional Communty Action Agency") Date of Application How did you hear about the IDA program? INDIVIDUAL DEVELOPMENT ACCOUNT (IDA) APPLICATION AGENCY INFORMATION Regional Communty Action Agency What will you save for? Education First Home

Date of Application How did you hear about the IDA program? INDIVIDUAL DEVELOPMENT ACCOUNT (IDA) APPLICATION AGENCY INFORMATION Regional Communty Action Agency What will you save for? Education First Home

OECD-Brazilian International Conference on Financial Education

OECD-Brazilian International Conference on Financial Education Debt Literacy, Financial Experiences and Overindebtedness December 15-16, 2009 Annamaria Lusardi Dartmouth College & NBER (Joint work with

OECD-Brazilian International Conference on Financial Education Debt Literacy, Financial Experiences and Overindebtedness December 15-16, 2009 Annamaria Lusardi Dartmouth College & NBER (Joint work with

FAMILY ASSETS FOR INDEPENDENCE IN MINNESOTA (FAIM) FAIM New Participant Application Form AGENCY USE ONLY : Agency Name:

FAIM New Participant Application Form AGENCY USE ONLY : Agency Name:") FAMILY ASSETS FOR INDEPENDENCE IN MINNESOTA (FAIM) AGENCY USE ONLY : FAIM New Participant Application Form Revised 05/23/14 Agency Name: Bank Account Number of 1 st Deposit Asset Grant First Name MI Last

FAMILY ASSETS FOR INDEPENDENCE IN MINNESOTA (FAIM) AGENCY USE ONLY : FAIM New Participant Application Form Revised 05/23/14 Agency Name: Bank Account Number of 1 st Deposit Asset Grant First Name MI Last

Homeownership, the Great Recession, and Wealth: Evidence from the Survey of Consumer Finance Michal Grinstein-Weiss Clinton Key

Homeownership, the Great Recession, and Wealth: Evidence from the Survey of Consumer Finance Michal Grinstein-Weiss Clinton Key Presented at The Federal Reserve Bank of St. Louis 6 February 2013 The American

Homeownership, the Great Recession, and Wealth: Evidence from the Survey of Consumer Finance Michal Grinstein-Weiss Clinton Key Presented at The Federal Reserve Bank of St. Louis 6 February 2013 The American

STATE OUTCOME & POLICY REPORT OUTCOME RANK POLICIES ADOPTED

STATE OUTCOME & POLICY REPORT OUTCOME RANK POLICIES ADOPTED 31 12 out of 50 OUTCOME HIGHLIGHTS POLICY HIGHLIGHTS 59.6% of Indiana households kept emergency savings in the past year Has state eliminated

STATE OUTCOME & POLICY REPORT OUTCOME RANK POLICIES ADOPTED 31 12 out of 50 OUTCOME HIGHLIGHTS POLICY HIGHLIGHTS 59.6% of Indiana households kept emergency savings in the past year Has state eliminated

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics Annamaria Lusardi, GFLEC Carlo de Bassa Scheresberg, GFLEC Paul Yakoboski, TIAA-CREF Institute National

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics Annamaria Lusardi, GFLEC Carlo de Bassa Scheresberg, GFLEC Paul Yakoboski, TIAA-CREF Institute National

AMERICA AT HOME SURVEY American Attitudes on Homeownership, the Home-Buying Process, and the Impact of Student Loan Debt

AMERICA AT HOME SURVEY 2017 American Attitudes on Homeownership, the Home-Buying Process, and the Impact of Student Loan Debt 1 Objective and Methodology Objective The purpose of the survey was to understand

AMERICA AT HOME SURVEY 2017 American Attitudes on Homeownership, the Home-Buying Process, and the Impact of Student Loan Debt 1 Objective and Methodology Objective The purpose of the survey was to understand

Saving at Work for a Rainy Day Results from a National Survey of Employees

Saving at Work for a Rainy Day Results from a National Survey of Employees Catherine Harvey and David John AARP Public Policy Institute S. Kathi Brown AARP Research September 2018 AARP PUBLIC POLICY INSTITUTE

Saving at Work for a Rainy Day Results from a National Survey of Employees Catherine Harvey and David John AARP Public Policy Institute S. Kathi Brown AARP Research September 2018 AARP PUBLIC POLICY INSTITUTE

TIAA-CREF Investing in You Survey Executive Summary. August 12, 2014

{ TIAA-CREF Investing in You Survey Executive Summary August 12, 2014 TIAA-CREF Survey Finds One-Third of Americans Have Never Increased Their Retirement Plan Contribution Rate Millennials are most likely

{ TIAA-CREF Investing in You Survey Executive Summary August 12, 2014 TIAA-CREF Survey Finds One-Third of Americans Have Never Increased Their Retirement Plan Contribution Rate Millennials are most likely

What does your Community look like and how is it changing?

What does your Community look like and how is it changing? Trends in the State population related to health and health determinants and where you can find this data to support your local work Who is Likely

What does your Community look like and how is it changing? Trends in the State population related to health and health determinants and where you can find this data to support your local work Who is Likely

STATE OUTCOME & POLICY REPORT OUTCOME RANK POLICIES ADOPTED

STATE OUTCOME & POLICY REPORT OUTCOME RANK POLICIES ADOPTED 20 28 out of 53 OUTCOME HIGHLIGHTS POLICY HIGHLIGHTS 30.8% of Connecticut households live in liquid asset poverty Has state enacted a refundable

STATE OUTCOME & POLICY REPORT OUTCOME RANK POLICIES ADOPTED 20 28 out of 53 OUTCOME HIGHLIGHTS POLICY HIGHLIGHTS 30.8% of Connecticut households live in liquid asset poverty Has state enacted a refundable

Underbanked 101. Joshua Sledge, Analyst, Innovation and Research, CFSI CFSI Underbanked Financial Services Forum June 13, 2012

2012 2012 Center Center for for Financial Financial Services Services Innovation Innovation Underbanked 101 Joshua Sledge, Analyst, Innovation and Research, CFSI CFSI Underbanked Financial Services Forum

2012 2012 Center Center for for Financial Financial Services Services Innovation Innovation Underbanked 101 Joshua Sledge, Analyst, Innovation and Research, CFSI CFSI Underbanked Financial Services Forum

A PARTNERSHIP OF THE KAISER FAMILY FOUNDATION AND THE NEWSHOUR WITH JIM LEHRER. The NewsHour with Jim Lehrer/Kaiser Family Foundation.

HEALTH DESK A PARTNERSHIP OF THE KAISER FAMILY FOUNDATION AND THE NEWSHOUR WITH JIM LEHRER Highlights and Chartpack The NewsHour with Jim Lehrer/Kaiser Family Foundation National Survey on the Uninsured

HEALTH DESK A PARTNERSHIP OF THE KAISER FAMILY FOUNDATION AND THE NEWSHOUR WITH JIM LEHRER Highlights and Chartpack The NewsHour with Jim Lehrer/Kaiser Family Foundation National Survey on the Uninsured

Online Appendix for: Minimum Wages and Consumer Credit: Lisa J. Dettling and Joanne W. Hsu

Online Appendix for: Minimum Wages and Consumer Credit: Impacts on Access to Credit and Traditional and High-Cost Borrowing Lisa J. Dettling and Joanne W. Hsu A1 Appendix Figure 1: Regional Representation

Online Appendix for: Minimum Wages and Consumer Credit: Impacts on Access to Credit and Traditional and High-Cost Borrowing Lisa J. Dettling and Joanne W. Hsu A1 Appendix Figure 1: Regional Representation

STATE OF WORKING ARIZONA

Fall, 2008 STATE OF WORKING ARIZONA Public Policy Helps Arizona Families Move Ahead with Education, Child Care and Health Care In 2008, the mortgage crisis toppled Arizona s housing market, dramatically

Fall, 2008 STATE OF WORKING ARIZONA Public Policy Helps Arizona Families Move Ahead with Education, Child Care and Health Care In 2008, the mortgage crisis toppled Arizona s housing market, dramatically

Segmentation Survey. Results of Quantitative Research

Segmentation Survey Results of Quantitative Research August 2016 1 Methodology KRC Research conducted a 20-minute online survey of 1,000 adults age 25 and over who are not unemployed or retired. The survey

Segmentation Survey Results of Quantitative Research August 2016 1 Methodology KRC Research conducted a 20-minute online survey of 1,000 adults age 25 and over who are not unemployed or retired. The survey

Lending Strategies 2.0. Carolinas Credit Union League 2015 Leadership Conference October 22, 2015

Lending Strategies 2.0 Carolinas Credit Union League 2015 Leadership Conference October 22, 2015 WHAT DOES THE FUTURE HOLD? CUES - Scenarios for Credit Unions through 2020 Two Uncertainties/Four Scenarios

Lending Strategies 2.0 Carolinas Credit Union League 2015 Leadership Conference October 22, 2015 WHAT DOES THE FUTURE HOLD? CUES - Scenarios for Credit Unions through 2020 Two Uncertainties/Four Scenarios

Women Voters Ages 50+ and the 2016 Election. Annotated Questionnaire for Women Ages 50+ in Florida* TOTAL Unweighted N=

Women Voters Ages 50+ and the 2016 Election Annotated Questionnaire for Women Ages 50+ in Florida* Please note that all results shown are percentages. TOTAL 50-69 70+ Unweighted N= 717 475 242 Northeast...

Women Voters Ages 50+ and the 2016 Election Annotated Questionnaire for Women Ages 50+ in Florida* Please note that all results shown are percentages. TOTAL 50-69 70+ Unweighted N= 717 475 242 Northeast...

A report from Sept 2017

A report from Sept 2017 Survey Highlights Worker Perspectives on Barriers to Retirement Saving Insights from those at small to midsize businesses could inform efforts to encourage more saving Blank page

A report from Sept 2017 Survey Highlights Worker Perspectives on Barriers to Retirement Saving Insights from those at small to midsize businesses could inform efforts to encourage more saving Blank page

Debt Literacy, Financial Experiences and Overindebtedness

Presentation to the World Bank Conference on Measurement, Promotion and Impact of Access to Financial Services Debt Literacy, Financial Experiences and Overindebtedness March 12, 2009 Annamaria Lusardi

Presentation to the World Bank Conference on Measurement, Promotion and Impact of Access to Financial Services Debt Literacy, Financial Experiences and Overindebtedness March 12, 2009 Annamaria Lusardi

17 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness

1 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness December 2016 TCRS 1335-1216 Transamerica Institute, 2016 Welcome to the 1 th Annual Transamerica Retirement Survey

1 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness December 2016 TCRS 1335-1216 Transamerica Institute, 2016 Welcome to the 1 th Annual Transamerica Retirement Survey

Resource Evaluation Question Guide

QUESTION Resource Evaluation Question Guide Non-Custodial Parent Form INSTRUCTIONS PARENT INFORMATION SECTION What is your relationship to the student? Report the parent s relationship to the student Biological

QUESTION Resource Evaluation Question Guide Non-Custodial Parent Form INSTRUCTIONS PARENT INFORMATION SECTION What is your relationship to the student? Report the parent s relationship to the student Biological

17 th Annual Transamerica Retirement Survey Influences of Ethnicity on Retirement Readiness

1 th Annual Transamerica Retirement Survey Influences of Ethnicity on Retirement Readiness December 01 TCRS 1-11 Transamerica Institute, 01 Welcome to the 1 th Annual Transamerica Retirement Survey Welcome

1 th Annual Transamerica Retirement Survey Influences of Ethnicity on Retirement Readiness December 01 TCRS 1-11 Transamerica Institute, 01 Welcome to the 1 th Annual Transamerica Retirement Survey Welcome

Copyright 2005 Freddie Mac. All Rights Reserved. Foreclosure Avoidance Research

Copyright 2005 Freddie Mac. All Rights Reserved. Foreclosure Avoidance Research Purpose & Methodology Over half of the borrowers in foreclosure proceedings have had no contact with their lender. Freddie

Copyright 2005 Freddie Mac. All Rights Reserved. Foreclosure Avoidance Research Purpose & Methodology Over half of the borrowers in foreclosure proceedings have had no contact with their lender. Freddie

REQUIRED DOCUMENTS FOR RENTAL COUNSELING APPOINTMENT

REQUIRED DOCUMENTS FOR RENTAL COUNSELING APPOINTMENT Appointment Time: Please Note: You MUST bring the following documents your counseling session in order receive counseling. You are REQUIRED take everything

REQUIRED DOCUMENTS FOR RENTAL COUNSELING APPOINTMENT Appointment Time: Please Note: You MUST bring the following documents your counseling session in order receive counseling. You are REQUIRED take everything

Renters Report Future Home Buying Optimism, While Family Financial Assistance Is Most Available to Populations with Higher Homeownership Rates

Renters Report Future Home Buying Optimism, While Family Financial Assistance Is Most Available to Populations with Higher Homeownership Rates National Housing Survey Topic Analysis Q3 2016 Published on

Renters Report Future Home Buying Optimism, While Family Financial Assistance Is Most Available to Populations with Higher Homeownership Rates National Housing Survey Topic Analysis Q3 2016 Published on

July 2016 Financial Capability in the United States 2016

July 2016 Financial Capability in the United States 2016 Financial Capability in the United States 2016 1 Contents Introduction 2 1. Making Ends Meet 4 Spending vs. Saving 6 Indicators of Financial Stress

July 2016 Financial Capability in the United States 2016 Financial Capability in the United States 2016 1 Contents Introduction 2 1. Making Ends Meet 4 Spending vs. Saving 6 Indicators of Financial Stress

California Dreaming or California Struggling?

California Dreaming or California Struggling? 2017 Findings from the AARP study of California Adults Ages 36-70 in the Workforce #CADreamingOrStruggling https://doi.org/10.26419/res.00163.001 SURVEY METHODOLOGY

California Dreaming or California Struggling? 2017 Findings from the AARP study of California Adults Ages 36-70 in the Workforce #CADreamingOrStruggling https://doi.org/10.26419/res.00163.001 SURVEY METHODOLOGY

Lower savings rates now may have long-term implications for mothers, who are also less engaged in calculating and planning for their retirement.

Mom s retirement A Voya Retirement Research Institute study that looks at financial habits and retirement planning for women who are currently also focused on raising children. The joys and challenges

Mom s retirement A Voya Retirement Research Institute study that looks at financial habits and retirement planning for women who are currently also focused on raising children. The joys and challenges

WHO WE ARE (DATA AS OF )

") WHO WE ARE (DATA AS OF 4.17.18) 515 volunteers give 22,609 hours 10,345 received $21 million in refunds $1.9 million saved by 1,290 people 150+ receive financial coaching every 6- months Advocate for tax

WHO WE ARE (DATA AS OF 4.17.18) 515 volunteers give 22,609 hours 10,345 received $21 million in refunds $1.9 million saved by 1,290 people 150+ receive financial coaching every 6- months Advocate for tax

18 th Annual Transamerica Retirement Survey Influences of Household Income on Retirement Readiness. June 2018 TCRS

1 th Annual Transamerica Retirement Survey Influences of Household Income on Retirement Readiness June 01 TCRS -01 Transamerica Institute, 01 Welcome to the 1 th Annual Transamerica Retirement Survey Welcome

1 th Annual Transamerica Retirement Survey Influences of Household Income on Retirement Readiness June 01 TCRS -01 Transamerica Institute, 01 Welcome to the 1 th Annual Transamerica Retirement Survey Welcome

Exhibit 1. One-Quarter of All U.S. Working-Age Adults Have Visited the Health Insurance Marketplaces

Exhibit 1. One-Quarter of All U.S. Working-Age Adults Have Visited the Health Insurance Marketplaces Have you gone to this new marketplace to shop for health insurance? This could be by mail, in person,

Exhibit 1. One-Quarter of All U.S. Working-Age Adults Have Visited the Health Insurance Marketplaces Have you gone to this new marketplace to shop for health insurance? This could be by mail, in person,

Credit Cards and Financial Health Member-Exclusive Report from CFSI s Consumer Financial Health Study

Credit Cards and Financial Health Member-Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products, calibrate existing ones,

Credit Cards and Financial Health Member-Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products, calibrate existing ones,

2016 AARP SURVEY: GUBERNATORIAL ISSUES FACING NORTH CAROLINA VOTERS AGES 45+

2016 AARP SURVEY: GUBERNATORIAL ISSUES FACING NORTH CAROLINA VOTERS AGES 45+ This AARP survey of 1,000 registered voters ages 45 and older found nearly all plan on voting in November. Among the number

2016 AARP SURVEY: GUBERNATORIAL ISSUES FACING NORTH CAROLINA VOTERS AGES 45+ This AARP survey of 1,000 registered voters ages 45 and older found nearly all plan on voting in November. Among the number

Student Lending Reform

Student Lending Reform Findings from a Survey of 400 Maine adults with education debt November 2018 Lake Research Partners Washington, DC Berkeley, CA New York, NY LakeResearch.com 202.776.9066 Jonathan

Student Lending Reform Findings from a Survey of 400 Maine adults with education debt November 2018 Lake Research Partners Washington, DC Berkeley, CA New York, NY LakeResearch.com 202.776.9066 Jonathan

Banking the Poor Financial Services, Asset-building & Economic Development: New Public Policy Perspectives for Puerto Rico

Banking the Poor Financial Services, Asset-building & Economic Development: New Public Policy Perspectives for Puerto Rico October 8, 2004 Michael S. Barr University of Michigan Law School Msbarr@umich.edu

Banking the Poor Financial Services, Asset-building & Economic Development: New Public Policy Perspectives for Puerto Rico October 8, 2004 Michael S. Barr University of Michigan Law School Msbarr@umich.edu

18 th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness. June 2018 TCRS

th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness June 0 TCRS -06 Transamerica Institute, 0 Welcome to the th Annual Transamerica Retirement Survey Welcome to this

th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness June 0 TCRS -06 Transamerica Institute, 0 Welcome to the th Annual Transamerica Retirement Survey Welcome to this

Women Voters Ages 50+ and the 2016 Election

Women Voters Ages 50+ and the 2016 Election Annotated Questionnaire for Latina Women Ages 50+ Across 15 Battleground States* (AZ, CO, FL, GA, IA, MI, MN, NC, NH, NM, NV, OH, PA, VA, and WI) Please note

Women Voters Ages 50+ and the 2016 Election Annotated Questionnaire for Latina Women Ages 50+ Across 15 Battleground States* (AZ, CO, FL, GA, IA, MI, MN, NC, NH, NM, NV, OH, PA, VA, and WI) Please note

Women Voters Ages 50+ and the 2016 Election

Women Voters Ages 50+ and the 2016 Election Annotated Questionnaire for African American/Black Women Ages 50+ Across 15 Battleground States* (AZ, CO, FL, GA, IA, MI, MN, NC, NH, NM, NV, OH, PA, VA, and

Women Voters Ages 50+ and the 2016 Election Annotated Questionnaire for African American/Black Women Ages 50+ Across 15 Battleground States* (AZ, CO, FL, GA, IA, MI, MN, NC, NH, NM, NV, OH, PA, VA, and

City of Modesto Homeowner Rehabilitation Program

City of Modesto Homeowner Rehabilitation Program Overview The City of Modesto s (City) Homeowner Rehabilitation Program is designed to repair or eliminate health and safety hazards in residential properties,

City of Modesto Homeowner Rehabilitation Program Overview The City of Modesto s (City) Homeowner Rehabilitation Program is designed to repair or eliminate health and safety hazards in residential properties,

Women in the Labor Force: A Databook

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 2-2013 Women in the Labor Force: A Databook Bureau of Labor Statistics Follow this and additional works at:

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 2-2013 Women in the Labor Force: A Databook Bureau of Labor Statistics Follow this and additional works at:

index The financial stress, challenges and fragility of Canadians from low-income households Financial Health

May 2018 The financial stress, challenges and fragility of Canadians from low-income households Insights from the 2017 Financial Health Index Study May 2018 Financial Health index Definitions Financial

May 2018 The financial stress, challenges and fragility of Canadians from low-income households Insights from the 2017 Financial Health Index Study May 2018 Financial Health index Definitions Financial

FINANCIAL CAPABILITY AMONG MILITARY PERSONNEL

FINANCIAL CAPABILITY AMONG MILITARY PERSONNEL INITIAL REPORT OF RESEARCH FINDINGS FROM THE 2009 MILITARY SURVEY A COMPONENT OF THE NATIONAL FINANCIAL CAPABILITY STUDY Prepared for the FINRA INVESTOR EDUCATION

FINANCIAL CAPABILITY AMONG MILITARY PERSONNEL INITIAL REPORT OF RESEARCH FINDINGS FROM THE 2009 MILITARY SURVEY A COMPONENT OF THE NATIONAL FINANCIAL CAPABILITY STUDY Prepared for the FINRA INVESTOR EDUCATION

ASSOCIATED PRESS-LIFEGOESSTRONG.COM BOOMERS SURVEY OCTOBER 2011 CONDUCTED BY KNOWLEDGE NETWORKS October 14, 2011

2100 Geng Road Suite 100 Palo Alto, CA 94303 www.knowledgenetworks.com Interview dates: October 5 October 12, 2011 Interviews: 1,410 adults; 1,095 boomers Sampling margin of error for a 50% statistic with

2100 Geng Road Suite 100 Palo Alto, CA 94303 www.knowledgenetworks.com Interview dates: October 5 October 12, 2011 Interviews: 1,410 adults; 1,095 boomers Sampling margin of error for a 50% statistic with

Massachusetts Household Survey on Health Insurance Status, 2007

Massachusetts Household Survey on Health Insurance Status, 2007 Division of Health Care Finance and Policy Executive Office of Health and Human Services Massachusetts Household Survey Methodology Administered

Massachusetts Household Survey on Health Insurance Status, 2007 Division of Health Care Finance and Policy Executive Office of Health and Human Services Massachusetts Household Survey Methodology Administered

Aging in America: Income and Assets of People on Medicare

Aging in America: Income and Assets of People on Medicare November 6, 2015 National Health Policy Forum Gretchen Jacobson, Ph.D. Associate Director, Program on Medicare Policy Kaiser Family Foundation

Aging in America: Income and Assets of People on Medicare November 6, 2015 National Health Policy Forum Gretchen Jacobson, Ph.D. Associate Director, Program on Medicare Policy Kaiser Family Foundation

17 th Annual Transamerica Retirement Survey Influences of Educational Attainment on Retirement Readiness

th Annual Transamerica Retirement Survey Influences of Educational Attainment on Retirement Readiness December 0 TCRS - Transamerica Institute, 0 Welcome to the th Annual Transamerica Retirement Survey

th Annual Transamerica Retirement Survey Influences of Educational Attainment on Retirement Readiness December 0 TCRS - Transamerica Institute, 0 Welcome to the th Annual Transamerica Retirement Survey

Snapshots of Financial Coaching. Bank of America & Annie E. Casey Foundation Meeting April 26, 2010

Snapshots of Financial Coaching Bank of America & Annie E. Casey Foundation Meeting April 26, 2010 Context for Coaching Financial Capacity Building Information Models Advice Models Mechanism Models Disclosures

Snapshots of Financial Coaching Bank of America & Annie E. Casey Foundation Meeting April 26, 2010 Context for Coaching Financial Capacity Building Information Models Advice Models Mechanism Models Disclosures

17 th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness

1 th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness December 016 TCRS 1-6 Transamerica Institute, 016 Table of Contents Welcome to the 1 th Annual Transamerica Retirement

1 th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness December 016 TCRS 1-6 Transamerica Institute, 016 Table of Contents Welcome to the 1 th Annual Transamerica Retirement

MUST BE 35 TO 64 TO QUALIFY. ALL OTHERS TERMINATE. COUNTER QUOTA FOR AGE GROUPS.

2016 Puerto Rico Survey Retirement Security & Financial Resilience Labor Force Participants (working or looking for work) age 35 to 64 and current Retirees Total sample n=800, max Retirees (may be current

2016 Puerto Rico Survey Retirement Security & Financial Resilience Labor Force Participants (working or looking for work) age 35 to 64 and current Retirees Total sample n=800, max Retirees (may be current

HOME SWEET HOME COMMUNITY REDEVELOPMENT CORPORATION Rebuilding our community one day at a time Customer Intake Form

Customer Intake Form CUSTOMER Please print Name: City: State: Zip Code: Date of Birth: / / Social Security: - - Gender: Male Female Handicapped? Yes or No Home: ( ) - Work: ( ) - Cell: ( ) - E-mail: Race

Customer Intake Form CUSTOMER Please print Name: City: State: Zip Code: Date of Birth: / / Social Security: - - Gender: Male Female Handicapped? Yes or No Home: ( ) - Work: ( ) - Cell: ( ) - E-mail: Race

CHASE RUN APARTMENTS RENTAL APPLICATION PACKET

CHASE RUN APARTMENTS RENTAL APPLICATION PACKET Thank you for your interest in Chase Run Apartments. Please feel free to contact our office at 989-772 772-7029 7029 if you have any questions while completing

CHASE RUN APARTMENTS RENTAL APPLICATION PACKET Thank you for your interest in Chase Run Apartments. Please feel free to contact our office at 989-772 772-7029 7029 if you have any questions while completing

Distribution of Family Wealth,

Distribution of Family Wealth, 1963 2016 1963 1983 2016 $12 million 99th percentile $10,400,000 $9 $6 $3 0 10th 50th 90th 10th 50th 90th $-19 $41,028 $238,860 $724 $82,746 $520,133 0 0 Source: Urban Institute

Distribution of Family Wealth, 1963 2016 1963 1983 2016 $12 million 99th percentile $10,400,000 $9 $6 $3 0 10th 50th 90th 10th 50th 90th $-19 $41,028 $238,860 $724 $82,746 $520,133 0 0 Source: Urban Institute

Harris Interactive. ACEP Emergency Care Poll

ACEP Emergency Care Poll Table of Contents Background and Objectives 3 Methodology 4 Report Notes 5 Executive Summary 6 Detailed Findings 10 Demographics 24 Background and Objectives To assess the general

ACEP Emergency Care Poll Table of Contents Background and Objectives 3 Methodology 4 Report Notes 5 Executive Summary 6 Detailed Findings 10 Demographics 24 Background and Objectives To assess the general

Women in the Labor Force: A Databook

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 9-2007 Women in the Labor Force: A Databook Bureau of Labor Statistics Follow this and additional works at:

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 9-2007 Women in the Labor Force: A Databook Bureau of Labor Statistics Follow this and additional works at:

2005 Health Confidence Survey Wave VIII

2005 Health Confidence Survey Wave VIII June 30 August 6, 2005 Hello, my name is [FIRST AND LAST NAME]. I am calling from National Research, a research firm in Washington, D.C. May I speak to the youngest

2005 Health Confidence Survey Wave VIII June 30 August 6, 2005 Hello, my name is [FIRST AND LAST NAME]. I am calling from National Research, a research firm in Washington, D.C. May I speak to the youngest

BUSINESS LOAN APPLICATION. Note: We encourage you to speak with a loan officer before submitting a loan application.

Mailing address: PO Box 342, Barre, VT 05641 Physical address: 105 N. Main St. Barre, VT 05641 Tel: 802-479-0167 Fax: 802-476-1926 Building Communities, One Vermont Business At A Time www.communitycapitalvt.org

Mailing address: PO Box 342, Barre, VT 05641 Physical address: 105 N. Main St. Barre, VT 05641 Tel: 802-479-0167 Fax: 802-476-1926 Building Communities, One Vermont Business At A Time www.communitycapitalvt.org

Demographic and Other Statistics for Women and Men Aged 50 and Older,

Demographic and Other Statistics for Women and Men Aged 50 and Older, 1999-2001 Population in 2001 Proportion of Population Over Age 50 30.0 % 28.6 % 28.6 % 25.2 % Age Distribution: 50-61 41.9 49.6 45.5

Demographic and Other Statistics for Women and Men Aged 50 and Older, 1999-2001 Population in 2001 Proportion of Population Over Age 50 30.0 % 28.6 % 28.6 % 25.2 % Age Distribution: 50-61 41.9 49.6 45.5

Women Voters Ages 50+ and the 2016 Election: Thoughts on Social Security and the Presidential Candidates

Women Voters Ages 50+ and the 2016 Election: Thoughts on Social Security and the Presidential Candidates Annotated Questionnaire for Full Sample of 1500 Women Ages 50+ Across 15 Battleground States* (AZ,

Women Voters Ages 50+ and the 2016 Election: Thoughts on Social Security and the Presidential Candidates Annotated Questionnaire for Full Sample of 1500 Women Ages 50+ Across 15 Battleground States* (AZ,

Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters

A brief from Feb 2015 Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters Overview According to an analysis of banks account data published by the Consumer

A brief from Feb 2015 Overdraft Frequency and Payday Borrowing An analysis of characteristics associated with overdrafters Overview According to an analysis of banks account data published by the Consumer

LONG ISLAND INDEX SURVEY CLIMATE CHANGE AND ENERGY ISSUES Spring 2008

LONG ISLAND INDEX SURVEY CLIMATE CHANGE AND ENERGY ISSUES Spring 2008 Pervasive Belief in Climate Change but Fewer See Direct Personal Consequences There is broad agreement among Long Islanders that global

LONG ISLAND INDEX SURVEY CLIMATE CHANGE AND ENERGY ISSUES Spring 2008 Pervasive Belief in Climate Change but Fewer See Direct Personal Consequences There is broad agreement among Long Islanders that global

Women in the Labor Force: A Databook

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 12-2011 Women in the Labor Force: A Databook Bureau of Labor Statistics Follow this and additional works at:

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 12-2011 Women in the Labor Force: A Databook Bureau of Labor Statistics Follow this and additional works at:

Freedom Financial (Example Only) Market Insights Report. Prepared by Kasasa s Executive Strategy Department

Market Insights Report. Prepared by Kasasa s Executive Strategy Department") Freedom Financial (Example Only) Market Insights Report Prepared by Kasasa s Executive Strategy Department Demographic Analysis Executive Summary POPULATION City, ST Sample County Example DMA Total Population

Freedom Financial (Example Only) Market Insights Report Prepared by Kasasa s Executive Strategy Department Demographic Analysis Executive Summary POPULATION City, ST Sample County Example DMA Total Population

What Do Consumers Know About The Mortgage Qualification Criteria?

Fannie Mae 2015 Mortgage Qualification Research What Do Consumers Know About The Mortgage Qualification Criteria? Economic & Strategic Research Group December 2015 Disclaimer The analyses, opinions, estimates,

Fannie Mae 2015 Mortgage Qualification Research What Do Consumers Know About The Mortgage Qualification Criteria? Economic & Strategic Research Group December 2015 Disclaimer The analyses, opinions, estimates,

HOMEOWNERSHIP APPLICATION (Rev. 3/16/17) = Submit a copy of each requested item to the application

= Submit a copy of each requested item to the application") PART 1: Applicant(s) Information HOMEOWNERSHIP APPLICATION (Rev. 3/16/17) = Submit a copy of each requested item to the application Application deadline: no exceptions APPLICANT (Head of Household owner

PART 1: Applicant(s) Information HOMEOWNERSHIP APPLICATION (Rev. 3/16/17) = Submit a copy of each requested item to the application Application deadline: no exceptions APPLICANT (Head of Household owner

MassMutual LGBTQ Retirement Savings Risk Study

J U N E 2018 MassMutual Retirement Savings Risk Study RS-45520-00 Background & Methodology Background To better understand the investment preferences and philosophies of Americans approaching retirement

J U N E 2018 MassMutual Retirement Savings Risk Study RS-45520-00 Background & Methodology Background To better understand the investment preferences and philosophies of Americans approaching retirement

Women in the Labor Force: A Databook

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 12-2010 Women in the Labor Force: A Databook Bureau of Labor Statistics Follow this and additional works at:

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 12-2010 Women in the Labor Force: A Databook Bureau of Labor Statistics Follow this and additional works at:

Homebuyer Education Demographic Tracking Information

Homebuyer Education Demographic Tracking Information Applicant Information Name: Email: Address: Pending Address: Phone Number: Co-Applicant Information Name: Email: Address: Pending Address: Phone Number:

Homebuyer Education Demographic Tracking Information Applicant Information Name: Email: Address: Pending Address: Phone Number: Co-Applicant Information Name: Email: Address: Pending Address: Phone Number:

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui.

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui. Annamaria Lusardi Brussels Month Year November 7, 2018 Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui. Annamaria Lusardi Brussels Month Year November 7, 2018 Lorem ipsum dolor sit

Volunteer Income Tax Assistance

Volunteer Income Tax Assistance The VITA Program provides free tax preparation services to low income residents of Winnebago County Tax Services Provided in Calendar Year 2016 1 Site Coordinators Sue Panek

Volunteer Income Tax Assistance The VITA Program provides free tax preparation services to low income residents of Winnebago County Tax Services Provided in Calendar Year 2016 1 Site Coordinators Sue Panek

Health Insurance Coverage in the District of Columbia

Health Insurance Coverage in the District of Columbia Estimates from the 2009 DC Health Insurance Survey The Urban Institute April 2010 Julie Hudman, PhD Director Department of Health Care Finance Linda

Health Insurance Coverage in the District of Columbia Estimates from the 2009 DC Health Insurance Survey The Urban Institute April 2010 Julie Hudman, PhD Director Department of Health Care Finance Linda

Random digital dial Results are weighted to be representative of registered voters Sampling Error: +/-4% at the 95% confidence level

South Carolina Created for: American Petroleum Institute Presented by: Harris Poll Interviewing: November 18 22, 2015 Respondents: 607 Registered Voters in South Carolina Method: Telephone Sample: Random

South Carolina Created for: American Petroleum Institute Presented by: Harris Poll Interviewing: November 18 22, 2015 Respondents: 607 Registered Voters in South Carolina Method: Telephone Sample: Random

The 2007 Retiree Survey

The Ariel-Schwab Black Investor Survey: The 00 Retiree Survey October 11, 00 BACKGROUND, OBJECTIVES, AND METHODOLOGY Ariel Mutual Funds and The Charles Schwab Corporation commissioned Argosy Research to

The Ariel-Schwab Black Investor Survey: The 00 Retiree Survey October 11, 00 BACKGROUND, OBJECTIVES, AND METHODOLOGY Ariel Mutual Funds and The Charles Schwab Corporation commissioned Argosy Research to

Financial Literacy and Banking Affiliation: Results for the Unbanked, Underbanked, and Fully Banked 1

Perspectives on Economic Education Research 9(1) 20-35 Journal homepage: www.isu.edu/peer/ Financial Literacy and Banking Affiliation: Results for the Unbanked, Underbanked, and Fully Banked 1 Elizabeth

Perspectives on Economic Education Research 9(1) 20-35 Journal homepage: www.isu.edu/peer/ Financial Literacy and Banking Affiliation: Results for the Unbanked, Underbanked, and Fully Banked 1 Elizabeth

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

ASSOCIATED PRESS-LIFEGOESSTRONG.COM BOOMERS SURVEY CONDUCTED BY KNOWLEDGE NETWORKS March 16, 2011

1350 Willow Rd, Suite 102 Menlo Park, CA 94025 www.knowledgenetworks.com Interview dates: March 04 March 13, 2011 Interviews: 1,490 adults, including 1,160 baby boomers Sampling margin of error for a 50%

1350 Willow Rd, Suite 102 Menlo Park, CA 94025 www.knowledgenetworks.com Interview dates: March 04 March 13, 2011 Interviews: 1,490 adults, including 1,160 baby boomers Sampling margin of error for a 50%

2018 AARP SURVEY: EXPERIENCE AND KNOWLEDGE OF MEDICARE CARD SCAMS https: ://doi.org/ /res

2018 AARP SURVEY: EXPERIENCE AND KNOWLEDGE OF MEDICARE CARD SCAMS https: ://doi.org/10.26419/res.00222.001 This month, Medicare unveils its new beneficiary cards. The new card will be much the same as

2018 AARP SURVEY: EXPERIENCE AND KNOWLEDGE OF MEDICARE CARD SCAMS https: ://doi.org/10.26419/res.00222.001 This month, Medicare unveils its new beneficiary cards. The new card will be much the same as

the unemployed in 2012 had been without work for 27 weeks or more compared to only 17.6 percent prior to the recession. 3

Policy Brief #37, August 2013 The National Poverty Center s Policy Brief series summarizes key academic research findings, highlighting implications for policy. The NPC encourages the dissemination of

Policy Brief #37, August 2013 The National Poverty Center s Policy Brief series summarizes key academic research findings, highlighting implications for policy. The NPC encourages the dissemination of

Type of Service Seeking: Home Purchase Education Rehab Assistance APPLICANT INFORMATION. 3. Current Mailing Address: City: Zip:

1 St. Tammany Homeownership Center A Service of Habitat for Humanity St. Tammany West Personal Profile Form Type of Service Seeking: Home Purchase Education Rehab Assistance APPLICANT INFORMATION 1. Applicant

1 St. Tammany Homeownership Center A Service of Habitat for Humanity St. Tammany West Personal Profile Form Type of Service Seeking: Home Purchase Education Rehab Assistance APPLICANT INFORMATION 1. Applicant

SURVEY OF CONSUMER EXPECTATIONS. Housing Survey 2016

SURVEY OF CONSUMER EXPECTATIONS Housing Survey 2016 Federal Reserve Bank of New York Andreas Fuster and Basit Zafar with Kevin Morris une 2, 2016 SCE ederal Housing Reserve Survey 2016 Bank of New York

SURVEY OF CONSUMER EXPECTATIONS Housing Survey 2016 Federal Reserve Bank of New York Andreas Fuster and Basit Zafar with Kevin Morris une 2, 2016 SCE ederal Housing Reserve Survey 2016 Bank of New York

Expanding the CalEITC: A Smart Investment to Broaden Economic Security in California

calbudgetcenter.org Expanding the CalEITC: A Smart Investment to Broaden Economic Security in California @alissa_brie @skimberca @CalBudgetCenter ALISSA ANDERSON, SENIOR POLICY ANALYST SARA KIMBERLIN,

calbudgetcenter.org Expanding the CalEITC: A Smart Investment to Broaden Economic Security in California @alissa_brie @skimberca @CalBudgetCenter ALISSA ANDERSON, SENIOR POLICY ANALYST SARA KIMBERLIN,

PROPOSED SHOPPING CENTER

PROPOSED SHOPPING CENTER Southeast Corner I-95 & Highway 192 Melbourne, Florida In a 5 Mile Radius 80,862 Population 32,408 Households $61K Avg HH Income SOONER INVESTMENT Commercial & Investment Real

PROPOSED SHOPPING CENTER Southeast Corner I-95 & Highway 192 Melbourne, Florida In a 5 Mile Radius 80,862 Population 32,408 Households $61K Avg HH Income SOONER INVESTMENT Commercial & Investment Real

Survey of Household Economics and Decisionmaking

SHED Survey of Household Economics and Decisionmaking Jeff Larrimore Consumer & Community Development Research Division of Consumer & Community Affairs The analysis and conclusions set forth in this presentation

SHED Survey of Household Economics and Decisionmaking Jeff Larrimore Consumer & Community Development Research Division of Consumer & Community Affairs The analysis and conclusions set forth in this presentation

July Sub-group Audiences Report

July 2013 Sub-group Audiences Report SURVEY OVERVIEW Methodology Penn Schoen Berland completed 4,000 telephone interviews among the following groups between April 4, 2013 and May 3, 2013: Audience General

July 2013 Sub-group Audiences Report SURVEY OVERVIEW Methodology Penn Schoen Berland completed 4,000 telephone interviews among the following groups between April 4, 2013 and May 3, 2013: Audience General

Financial Shocks Put Retirement Security at Risk Smart policies can help meet immediate needs without depleting long-term savings

A brief from Oct 2017 Financial Shocks Put Retirement Security at Risk Smart policies can help meet immediate needs without depleting long-term savings Overview Because most households have relatively

A brief from Oct 2017 Financial Shocks Put Retirement Security at Risk Smart policies can help meet immediate needs without depleting long-term savings Overview Because most households have relatively

31% 41% 11% 50% 18% PROFILE ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO KEY HIGHLIGHTS ABOUT THE PROFILE ASSETS & OPPORTUNITY

ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 31% of San Francisco residents live in asset poverty Cities have long been thought of as places of opportunity for

ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 31% of San Francisco residents live in asset poverty Cities have long been thought of as places of opportunity for

IWPR R345 February The Female Face of Poverty and Economic Insecurity: The Impact of the Recession on Women in Pennsylvania and Pittsburgh MSA

INSTITUTE FOR WOMEN S POLICY RESEARCH Briefing Paper IWPR R345 February 2010 : The Impact of the Recession on Women in and Ariane Hegewisch and Claudia Williams Since the beginning of the recession at

INSTITUTE FOR WOMEN S POLICY RESEARCH Briefing Paper IWPR R345 February 2010 : The Impact of the Recession on Women in and Ariane Hegewisch and Claudia Williams Since the beginning of the recession at

Class Notes. Intermediate Macroeconomics. Li Gan. Lecture 5: Unemployment Rate. Basic facts about unemployment:

Class Notes Intermediate Macroeconomics Li Gan Lecture 5: Unemployment Rate Basic facts about unemployment: (1) Unemployment varies a lot over time. (2) More recently, (2) Current status: 1 08/09 06/10

Class Notes Intermediate Macroeconomics Li Gan Lecture 5: Unemployment Rate Basic facts about unemployment: (1) Unemployment varies a lot over time. (2) More recently, (2) Current status: 1 08/09 06/10

HOME SWEET HOME COMMUNITY REDEVELOPMENT CORPORATION

Customer Intake Form CUSTOMER 1 P age HOME SWEET HOME COMMUNITY REDEVELOPMENT CORPORATION Please print Name: Address: City: State: Zip Code: Date of Birth: / / Social Security: - - Gender: Male Female

Customer Intake Form CUSTOMER 1 P age HOME SWEET HOME COMMUNITY REDEVELOPMENT CORPORATION Please print Name: Address: City: State: Zip Code: Date of Birth: / / Social Security: - - Gender: Male Female

February 24, 2014 Media Contact: Joanna Norris, Associate Director Department of Public Relations (904)

") February 24, 2014 Media Contact: Joanna Norris, Associate Director Department of Public Relations (904) 620-2102 University of North Florida Poll Reveals that a Vast Majority of Duval County Residents

February 24, 2014 Media Contact: Joanna Norris, Associate Director Department of Public Relations (904) 620-2102 University of North Florida Poll Reveals that a Vast Majority of Duval County Residents

2008 Financial Literacy Survey

Summary Report and Topline 2008 Financial Literacy Survey Prepared by Princeton Survey Research Associates International for the National Foundation for Credit Counseling and MSN Money 04.29.08 Many economists

Summary Report and Topline 2008 Financial Literacy Survey Prepared by Princeton Survey Research Associates International for the National Foundation for Credit Counseling and MSN Money 04.29.08 Many economists