HIMANSHU KISHNADWALA 8 AUGUST 2012

|

|

|

- Sabrina Morton

- 5 years ago

- Views:

Transcription

1 HIMANSHU KISHNADWALA 8 AUGUST 2012 CNK 1

2 1. Format / disclosures Revised Schedule VI 2. Disclosures as per notified Accounting Standards (i.e. Companies AS Rules, 2006) 3. Disclosures as per Companies Act, 1956 Buyback of shares (as per sec 77) 4. Disclosures as per other Statutes E.g. MSME Act, RBI notifications for NBFCs 5. Disclosures as per ICAI pronouncements ICAI announcement for derivatives 6. Disclosures as per Clause 32 of listing agreement Loans/advances to subsidiaries, etc. CNK 2 CNK 2

3 For FY commencing on or after 1 st April 2011 First year of applicability FY Cannot be applied earlier on voluntary basis Corresponding figures for mandatory Applicable to ALL companies (except those engaged in banking, insurance) CNK 3 CNK 3

4 Concept of schedules eliminated All information to be given in notes to accounts. Extensive cross-referencing required Terms used to carry meaning as defined by the notified Accounting Standards. If conflict between requirements of the Act and / or AS, requirements of the Act and / or AS will prevail over RS VI. Only vertical format to be followed Format follows permanency in presentation of assets / liabilities CNK 4 CNK 4

5 PL now to be called Statement of Profit and Loss Formats given for both BS and Stt of PL Option of giving functional classification of expenses in PL not available No Appropriation account in Stt of PL All appropriations to be disclosed in Reserves & Surplus Surplus in Statement of PL Debit balance of Profit/Loss to be deducted from Reserves and Surplus Final figure of Reserves & Surplus can even be negative CNK 5 CNK 5

6 Disclosure of additional line items in BS / PL? Instructions to RS VI mentions that the requirements mentioned therein are minimum requirements. Hence additional line items can be included say, for EBDITA, Net Working Capital, Industry Specific Disclosures? Industry specific disclosures for NBFCs, also required to be given as required by the respective statutes. CNK 6 CNK 6

7 Managerial remuneration and computation thereof; Details of Licensed capacity, Installed capacity Quantitative information about actual production, purchases, sales, consumption, etc.; Investments purchased/sold during the year; Investments, sundry debtors and loans/advances pertaining to companies under the same management; Maximum amounts due on account of loans and advances from directors or officers of the company; Information under Part IV of Schedule VI CNK 7 CNK 7

8 only if opted for Same unit of measurement in entire Financial Stts Existing Schedule VI Turnover < Rs 100 Crores R/off to the nearest hundreds, thousands or decimal thereof. Turnover Rs 100 to Rs 500 Crores R/off to the nearest hundreds, thousands, lakhs or millions or decimal thereof. Turnover > Rs 500 Crores R/off to the nearest hundreds, thousands, lakhs millions or crores or decimal thereof. Revised Schedule VI Turnover < Rs 100 Crores R/off to the nearest hundreds, thousands, lakhs or millions or decimal thereof. Turnover > Rs 100 Crores R/off to the nearest lakhs, millions or crores, or decimal thereof. CNK 8 CNK 8

9 Section 115JB requires PL account to be prepared under part II of pre-revised Schedule VI for MAT purposes ICAI GN on 44AB suggests to use format prescribed under governing law For a company having year end other than Financial Year, which format to be followed for FS? CNK 9 CNK 9

10 CNK 10 CNK 10

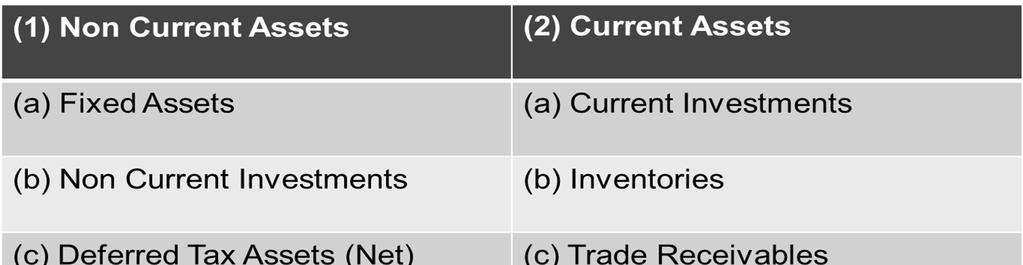

11 Shareholders Funds Share Capital Non Current Liabilities Long term borrowings Reserves and surplus Deferred tax liabilities Money received against share warrants Other Long term liabilities Long-term provisions Current Liabilities Short term borrowings Trade Payables Other current liabilities Short term provisions CNK 11 CNK 11

12 A liability is classified as Current if it satisfies any of the following criteria: a) it is expected to be settled in the company s normal operating cycle; b) it is held primarily for the purpose of being traded; c) it is due to be settled within 12 months after the reporting date; or d) the company does not have an unconditional right to defer settlement of the liability for at least 12 months after the reporting date. CNK 12 CNK 12

13 An asset is classified as Current when it satisfies any of the following criteria: (a) It is expected to be realized in, or is intended for sale or consumption in the company s normal operating cycle; (b) It is held primarily for the purpose of being traded; (c) It is expected to be realized within 12 months after the reporting date; or (d) It is cash or cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least 12 months after reporting period date. CNK 13 CNK 13

14 An Operating Cycle (OC) is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. If an OC cannot be identified, it is assumed to have a duration of 12 months If a company is engaged in multiple businesses, the OC can be different for each line of business CNK 14 CNK 14

15 Different OC for different customers based on different credit terms? say., PSU and non PSU customers Can OC differ from year to year? Whether lead time for procuring raw material should be included in OC? Is credit period allowed by supplier reduced in determination of OC? To determine OC to consider: o Normal business behaviour o Industry practice o Liquidity position?? CNK 15 CNK 15

16 Industry specific OC: Manufacturing Companies: To determine business-wise Real Estate Companies: Can be determined project-wise Finance Companies: Difficult to determine to be assumed at 12 months Service companies: To determine business-wise Relevance of OC for classification of: Trade receivables / payables OC relevant Supplier/Customer advances OC relevant Borrowings OC relevant Loans 12 months period Other assets / liabilities 12 months period CNK 16 CNK 16

17 Manufacturing Companies OC considered as 12 months Bajaj Electricals Ltd, Grasim Industries Ltd Hindustan Unilever Ltd, Excel Industries Ltd Ultratech Cement Ltd Finance Company OC considered as 12 months M & M Financial Services Ltd Multi activity company OC different for specific project / contract / product line / service Larsen & Toubro Ltd CNK 17 CNK 17

18 Real Estate Industry: Disclosures regarding OC Oberoi Realty Limited The Company s normal operating cycle in respect of operations relating to under construction real estate projects may vary from project to project depending upon the size of the project, type of development, project complexities and related approvals. Operating Cycle for all completed projects and hospitality business is based on 12 months period. Assets & Liabilities have been classified into Current and Non Current based on Operating Cycle of respective businesses. CNK 18 CNK 18

19 Real Estate Industry: Disclosures regarding OC Mahindra Lifespace Developers Limited.. Based on the nature of activity carried out by the company and the period between the procurement and realisation in cash and cash equivalents, the Company has ascertained its operating cycle as 5 years for the purpose of Current Non Current classification of assets & liabilities. CNK 19 CNK 19

20 Determining Whether Current or Non-Current? For Assets: To consider expectation of receipt For Liabilities: To consider obligation to pay Whether accounting policy for classification of items into Current / Non Current is to be disclosed? Neither the RS VI nor the GN on RS VI requires such disclosure However, disclosure preferable in case of OC > 12 months In other cases, though not required, maybe given as it lends higher transparency to the FS Classification may have impact on CARO reporting Whether funds raised on short term basis are used for long term purposes? CNK 20 CNK 20

21 Whether Current or Non-Current? Payables or Operating liabilities within operating cycle, but not paid within 12 months. Technical / minor breach on some covenants of Term Loans; Slow-moving Raw Materials Provision for employee benefits like Gratuity and Leave encashment Stock of Finished Goods unsold for 15 months CNK 21 CNK 21

22 Whether Current or Non-Current Loan given to Subsidiary (repayable on demand) Loan from Holding company (repayable on demand) Deposits : Electricity/ Lease deposits Others Advance tax (net of provisions) Provision for tax (net of advance tax) Audit Fees payable? CNK 22 CNK 22

23 Share Capital Shares in the company held by each shareholder holding more than 5% shares specifying the number of shares held. Whether names to be disclosed based on legal ownership or beneficial ownership? Section187CoftheCompaniesAct,1956. Nameofdepositorytobegiven??(ReferTataMotorsLtd) Disclosure for each class of shares as at BS date Comparative information necessary even if in , the amounts are below 5 % Additional disclosures in line with Ind-AS 1 / IAS 1. CNK 23 CNK 23

24 Presentation of Preference Share Capital for a company who has adopted AS 30 Whether to be presented as Share Capital or Liability? RS VI deals only with presentation and disclosure Accounting is governed by applicable AS. If a company early adopts AS 30/31/32 it has to decide classification between the liability/equity of preference shares based on principles of AS 31. ICAI GN mentions that only Accounting Standards notified by Companies (Accounting Standards) Rules, 2006 are to be followed, reclassification of Preference shares not possible under RS VI. CNK 24 CNK 24

25 To be disclosed as a separate line-item on the face of Balance Sheet between Shareholders Funds and Non-current Liabilities. Share application money not exceeding the issued capital and to the extent not refundable is to shown under this line item. Share application money to the extent Refundable shall be shown under Other current liabilities. Inadequacy of Authorised Capital? Transfer to IEPF after 7 years from the date amount becomes due for payment? CNK 25 CNK 25

26 Disclosure requirements: Number of shares proposed to be issued The amount of premium, if any The period before which shares are to be allotted Whether the company has sufficient authorized share capital to cover the share capital amount on allotment Interest accrued on amount due for refund Period for which share application money is pending beyond the period for allotment as mentioned in the share application form along with the reasons thereof for such share application money being pending is to be disclosed. Above disclosures to be made for amounts classified under both Shareholders funds or Current Liabilities CNK 26 CNK 26

27 Disclosure requirements: Nature of Security to be specified in each case (overall disclosure not allowed) Bonds & Debentures (along with rate of interest and particulars redemption or conversion, as the case may be) shall be stated in descending order of maturity or conversion date, as the case may be. Particulars of any redeemable bonds/debentures which the company has the power to reissue shall be disclosed. Terms of Repayment of term loans and other loans Period and amount of continuing default as on BS date in repayment of loans and interest, shall be specified separately in each case. CNK 27 CNK 27

28 How to disclose details of borrowings: No Standard format prescribed. Whether to give name / amount of borrowing / installments due, etc. for each bank or institution? Disclosure of Continuing Default Disclosure in RS VI vs. reporting in CARO CNK 28 CNK 28

29 Illustrative disclosures by companies: Grasim Industries Ltd Rupee term loan secured by exclusive charge on certain specific FA of the Co located at.. Quarterly ballooning repayment from October 20XX, over xx years. Foreign Currency Loans secured by first pari-passu charge on fixed assets, both present & future of the Co located at. Repayable after 5 years, bullet repayment in March, 20XX. CNK 29 CNK 29

30 Illustrative disclosures by companies: Reliance Industries Ltd Maturity Profile and Rate of Interest of Bonds Rate of Interest Maturity Profile % 1, % % Maturity Profile of Unsecured Term Loans: Maturity Profile Particulars 1-2 yrs 2-3 yrs 3-4 yrs Beyond 4 yrs Term Loans from Banks 12,920 3,418 5,926 15,005 CNK 30 CNK 30

31 Illustrative disclosures by companies: Prism Cement Ltd Secured Term Loan from Banks and Others Security Amount as at Repayment Terms Secured by charge on movable and immovable properties of the Cement division, both present and future, subject to prior charges on specific assets in favour of Cement Division's bankers towards Working Capital facilities Secured by first charge on vehicles of HRJ Division together with all accessories and addition to or in the vehicles, whether present or future 500 Quarterly in equal installments payable over a period of 4 years EMI over a period of 5 years. CNK 31 CNK 31

32 Illustrative disclosures by companies: Ramco Industries Term Loan from Banks (Secured) Repayment Schedule given separately in the NTA along with other disclosures Same not cross referenced Rate of Interest Outstanding as on Repayment Schedule % % CNK 32 CNK 32

33 Illustrative disclosures by companies: Petronet LNG Secured by first ranking mortgage and first charge on pari passu basis on all movable and immovable properties, both present & future including Current Assets except on trade receivables on which second charge is created on pari passu basis. Loan From ROI (as on ) No of Installments Year of Maturity Amount Outstanding as on Amount Outstanding as on Indian Banks 11% , ,500 IFC (Washington) 11.37% ,000 23,000 Total XXXXX XXXXX Less: Shown in Current Maturities of Long term Debt (XXXX) (XXXX) Balance shown as above XXXX XXXX CNK 33 CNK 33

34 Illustrative disclosures by companies: UltraTech Cement Ltd Term Loans from Banks in Foreign Currency Secured by way of first charge, having pari passu rights, on the Company s movable and immovable assets (save and except stocks and book debts), both present and future, situated at certain locations, in favour of Co s lenders/trustees. Particulars Hongkong & Shanghai Banking Corporation Ltd, Singapore (Japanese Yen Crores) DBS Bank Ltd, Singapore (Japanese Yen Crores) Less: Current Portion of Foreign Currency Loans shown under Other Current Liabilities Repayment Schedule In 3 equal annual installments beginning September 2012 As at March 31,2012 As at March 31, January (XXX) (XXX) Total XXX XXX CNK 34 CNK 34

35 Disclosure for Defaults Under RS VI Continuing Default for LT Borrowings Default for ST Borrowings Applies to all items of borrowings like bonds / debentures, deferred payment liabilities, finance lease obligations, etc. No disclosure if default made good on BS date Under CARO Defaults in repayment of any dues Applies only to dues of financial institutions, banks and debentures Reporting even if default made good on BS date CNK 35 CNK 35

36 Trade Payable: A payable is classified as trade payable if it is in respect of amount due on account of goods purchased or services received in the normal course of business. Under earlier Sch VI, Sundry Creditors (for goods, services, etc.) included above amounts plus amounts due on account of contractual obligations. Under RS VI, amounts due under contractual obligations cannot be included within trade payables e.g. Contribution to PF, accrued interest, payables for fixed asset purchases, etc. Such amounts are to be disclosed under Other current liabilities with a suitable description. CNK 36 CNK 36

37 CNK 37 CNK 37

38 Fixed Assets Fixed Assets: Tangible (a) Land (b) Buildings (c) Plant and Equipment (d) Furniture and Fixtures (e) Vehicles (f) Office Equipment (g) Others (Specify nature) Assets under lease to be separately specified under each class of asset. CNK 38 CNK 38

39 Fixed Assets: Intangible (a) Goodwill (b) Brands/trademarks (c) Computer software (d) Mastheads and publishing titles (e) Mining rights (f) Copyrights and patents and other intellectual property rights, services and operating rights. (g) Recipes, formulae, models, designs and prototypes (h) Licenses and franchise (i) Others (specify nature) CNK 39 CNK 39

40 Capital Work in Progress Capital advances not to be included Capital Advances should be included under Long Term Loans & Advances Intangible Assets under Development This is a new head under Revised Schedule VI CNK 40 CNK 40

41 Other disclosures regarding Tangible and Intangible Assets are: A Reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period showing: Additions Disposals Acquisitions through business combinations other adjustments and the related depreciation and impairment losses / reversals to be disclosed separately. CNK 41 CNK 41

42 Fixed Assets Particulars Opening Additions Disposals Through Business Combinations Other Adjustments *** Gross *** to include capitalisation of exchange differences (as per AS 11), borrowing costs for each class of assets Opening Depreciation On Business Combinations For the year Total Closing Closing (LY) CNK 42 CNK 42

43 RS VI requires foll. disclosure of Related Parties (RP): Long Term / Short Term borrowings from RP Long Term / Short Term Loans and Advances to RP RS VI requirement is to also give details thereof AS 18 requires detailed disclosures of RP and transactions GN on RS VI states details of RP should be as per AS 18 Illustrative disclosures: Tata Motors Ltd: details of RP given below respective line item Sundaram Fasteners Ltd: cross reference given to AS 18 disclosures L & T Ltd: broad details given and cross referencing also done Cross referencing to disclosures under Clause 32 done in many cases CNK 43 CNK 43

44 Non Current Investments shall be classified as trade Investment or Other Investments. The term trade investments is defined neither in Revised Schedule VI nor Accounting Standards. The term trade investment is normally understood as an investment made by a company in shares or debentures of another company, to promote the trade or business of the first company. Whether investment in subsidiary is to be classified as trade investment or other investment? CNK 44 CNK 44

45 Following Companies have classified Investment in Subsidiaries as Trade Investments : TATA Steel TATA Power UltraTech Cement Ltd Following Companies have NOT classified Investment in Subsidiaries as Trade Investments : Asian Paints JSW Steel Reliance Industries Ltd Infosys CNK 45 CNK 45

46 As per Revised Schedule VI: Current investments to be classified if expected to be realisedwithin12monthsofbsdate As per AS 13 Investment that by its nature is readily realisable and intended to be held for not more than 1 year from the date of investment. Investment made in December 2011 and expected to be realised in February 2013 (i.e. after 14 months) whether current or non-current as on 31 st March 2012? Since RS VI deals with only presentation, investment will be presented as current, with additional disclosure that the same is Long Term as per AS 13. CNK 46 CNK 46

47 Disclosure in Tata Power Ltd Reconciliation for Disclosure as per AS 13 Long Term Investments Non-current Investments Current portion of Long Term Investments (included in current investments) xxx xxx Current Investments Other current Investments xxx CNK 47 CNK 47

48 Investment in preference shares, convertible into equity shares within 1 year from the BS date, whether to be classified as Current or Non Current asset? An investment expected to be realized within 12 months from the reporting date is classified as Current Asset. Such realization should be in the form cash or cash equivalents rather than through conversion of one asset into another non current asset. Above investment is to be classified as Non Current Asset since on conversion it is not cash or cash equivalent. CNK 48 CNK 48

49 Whether classification of Investments in FS has any tax implications? Disclosure in Directors Report by Tata Invt Corpn Ltd The directors confirm that all the investments classified as noncurrent investments / trade investments as per the revised Schedule VI of the Companies Act, 1956 have been made with the intent to hold for long term appreciation, to enhance the income from dividends and are not held for trade. Investments in the category of Current Investments intended to be held for less than one year, which for accounting and other purposes are so classified at the time of making the investment, are indicated separately in the Balance Sheet. CNK 49 CNK 49

50 To be classified as both Current and Non Current o Capital account balance: Non current o Current account balance: Current If the FS of the partnership firm not made up to same date: o Gap cannot exceed 6 months o To consider un-audited amounts till BS date; o The above facts need to be specifically disclosed CNK 50 CNK 50

51 Names of the firms (with the names of all their partners, total capital and shares of each partner) Additional disclosures in Notes for: Change in constitution of Firm. If firm s accounts are not made up to the same date as the date of the company s Balance Sheet Specific disclosure required regarding: Share of partner s in profits of the firm; The total capital of the partnership firm in which the company is a partner; Separate disclosure is required by reference to each partnership firm in which the company is a partner. CNK 51 CNK 51

52 LLP is a Body Corporate and not a partnership firm as envisaged under the Partnership Act, Hence disclosures pertaining to Investments in Partnership firms, not required for Investment in LLP. Share of Profit/loss in LLP: Does not automatically accrue to the partners (like a firm) LLP can carry forward profits (without transfer to partners) No entry can be passed in books of company till profits are transferred to the partners of the LLP CNK 52 CNK 52

53 Trade Receivable: A receivable is classified as trade receivable if it is in respect of amount due on account of goods sold or services rendered in the normal course of business. To be classified as Current and Non Current. Aggregate amount of Trade Receivables outstanding for a period exceeding 6 months from the date they are due for payment (and not billing date) should be separately stated. To also classify the above as Secured, Unsecured, good/doubtful of recovery. Provision for bad and doubtful debts required to be divided into Current / Non Current. Is recovery towards OPE to be included as Trade Receivables? CNK 53 CNK 53

54 CCE as per RS VI includes: Balances with Banks held as margin money or security against borrowings, guarantees, etc. and Bank deposits with more than 12 months maturity As per AS-3 Cash is defined to include cash on hand and demand deposits with banks. Cash equivalents are defined as short term, highly liquid investments (i.e. less than 3 months maturity) that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value. CNK 54 CNK 54

55 Apparent Conflict between the requirements of the Revised Schedule VI and the Accounting Standards. The conflict should be resolved by changing the caption Cash and Cash equivalents to Cash and bank balances, which may have two sub-headings, viz. Cash and cash equivalents and Other bank balances. The former should include only the items that constitute CCE as per AS 3 (and not RS VI), The remaining line-items may be included under the latter heading. As per FAQs to RS VI, Fixed Deposits with more than 12 months are to be classified as Non Current Assets. CNK 55 CNK 55

56 Impact of RS VI on presentation of cash flow statement. Items appearing in the Cash Flow Statement should be aligned with the nomenclature of the items used in BS. E.g. a company cannot present trade receivables in the BS and show movement in Sundry Debtors in Cash Flow Statement. However it is not mandatory for a company to present inflow / outflow from current and non-current components of various line items separately. E.g. for borrowings it can be overall CNK 56 CNK 56

57 Under RS VI, there is no line item like Miscellaneous Expenditure RS VI also does not contain any specific disclosure requirement for the unamortized portion of expense items. Since AS 26 does not apply to share issue expenses and incidental costs of borrowings, how can the unamortized portion of the above be disclosed? These need to be classified as other current / noncurrent assets, depending on whether the amount will be amortized in the next 12 months or thereafter. CNK 57 CNK 57

58 RS VI requires separate disclosure of amount of dividends proposed for the period (in Notes) Existing Schedule VI specifically required proposed dividend to be disclosed under the head Provisions. As per AS-4, dividends stated to be in respect of the period covered by the financial statements, which are proposed or declared by the enterprise after the Balance Sheet date but before approval of the financial statements, should be adjusted. Since AS 4 will override, RS VI, treatment as under: Provision to be made in FS for proposed dividend Separate disclosure of the same in Notes CNK 58 CNK 58

59 CNK 59 CNK 59

60 CNK 60 CNK 60

61 A Company other than a finance company shall disclose separately in the notes revenue from: Sale of Products Sale of services Other operating revenues Less: Excise duty CNK 61 CNK 61

62 Whether Revenue should be Gross or Net? As per GN on terms used in FS, Sales Turnover is defined as: aggregate amount for which sales are effected or services rendered by an enterprise Guide to Company Audit mentions Total turnover is the aggregate amount for which sales are effected, giving the amountofsalesinrespectofeachclassofgoodsdealtwith by the company and indicating quantities separately Statement of CARO and Part II of existing Schedule VI defines turnover as aggregate amount for which sales are effected by the company. Sales effected would include sale ofgoodsaswellasservicesrenderedbythecompany. CNK 62 CNK 62

63 Whether Revenue should be Gross or Net? As per GN on Tax Audit, turnover maybe interpreted to mean the aggregate amount for which sales are effected or services rendered by an enterprise Para 10 of AS 9 requires disclosure of Gross Turnover with separate deduction for Excise Duty. GN on VAT states VAT is collected from customers on behalfofvatauthoritiesand shouldnotberecordedas revenue of the enterprise CNK 63 CNK 63

64 Whether Revenue should be Gross or Net? Service Tax For Service Tax, sec 83 of the Finance Act, 1994, provides that the provisions of certain sections (like sec 9C, 12A, etc.) of the Central Excise Act, 1944 shall apply, so far as may be, in relation to service tax as they may apply to a duty of excise. Section 12 A of the Central Excise Act, 1944, which provides that the amount of excise duty shall form part of the price of the goods sold. On a similar analogy, service tax would form part of the price of the services provided. CNK 64 CNK 64

65 Statement of Profit and Loss Whether Revenue should be Gross or Net? Excise Duty Since format of RS VI clearly mentions Excise Duty as a deduction from Sales, the same would be necessary. Service Tax / VAT As per GN On RS VI Such taxes are generally collected from the customer on behalf of government. Depending on whether company is acting as agent or principal, such taxes should be included in Sales (i.e. Gross or excluded (i.e. Net). CNK 65 CNK 65

66 The term Other Operating Revenue is not defined by RS VI. It would include Revenue arising from a company s operating activities, i.e., either its principal or ancillary revenue-generating activities, but which is not revenue arising from the sale of products or rendering of services. Whether a particular income constitutes other operating revenue or other income is to be decided based on the facts of each case and detailed understanding of the company s activities. CNK 66 CNK 66

67 Revenue from Operations in case of finance company A Finance company shall include revenue from a) Interest and b) Other Financial services The term finance company is not defined under the Companies Act, 1956, or Revised Schedule VI. Hence, the same should be taken to include all companies carrying on activities which are in the nature of business of non-banking financial institution as defined under section 45(1) (f) of the Reserve Bank of India Act, CNK 67 CNK 67

68 Other Income Other Income shall be classified as: a) Interest Income (incaseofacompanyotherthanafinance company); b) Dividend Income; c) Net gain / loss on sale of investments; d) Other non-operating income (net of expenses directly attributable to such income). Since (b) and (c) are always considered Other Income, finance companies can have negligible Revenue from Operations This can have implications in taxation and also affect valuation. CNK 68 CNK 68

69 Whether the following is Other Operating Revenue or Other Income? A Company engaged in manufacture and sale of industrial and consumer products also has one real estate arm. A consumer products company owns a 10 storied building. The company currently does not need one floor for its own use and has given the same temporarily on rent. Sale of Fixed Assets Sale of Scrap Interest from customers on delayed payments Foreign Exchange Gains CNK 69 CNK 69

70 Following treated as Other Operating Revenue : Sale of Carbon credits Dividend from Joint Venture/Subsidiary Since division operates part of its business through Subsidiaries/JVs, dividend income is taken as Operating Income Prism Cements Ltd Insurance Claims and Indirect taxes claimed received Kansai Nerolac Paints Ltd CNK 70 CNK 70

71 Tata Investments Corporation Ltd has classified the following as Revenue from Operations: Income from Investments Dividend Interest on Investments Fees from Shares lent Interest on Deposits and Advances CNK 71 CNK 71

72 RS VI requires separate disclosure for dividends from Subsidiary Companies. Old schedule VI specifically required parent companies to recognise dividend declared by subsidiary companies even if declared after the BS date if they are related to the same period covered by financial statements. RS VI does not prescribe any such accounting/disclosure requirement. Thus Dividend will now be recognised as per AS 9 i.e. only when they have a right to receive the same on or before the balance sheet date. CNK 72 CNK 72

73 Actual Consumption vs. Derived Consumption In case of a manufacturing or manufacturing and trading company care should be taken to ensure that raw material consumed should relate to actual consumption rather than derived consumption. Disclosure by Mahindra & Mahindra Ltd: The consumption in value has been ascertained on the basis of opening stock plus purchases less closing stock and includes adjustment for excesses and shortages as ascertained on physical count and write-off of obsolete and unserviceable raw materials and components. CNK 73 CNK 73

74 Other Commitments Additional requirement in RS VI Scope of terminology very wide AS per GN, it would include all expenditure related to contractual commitments apart from capital commitments such as commitments arising from long term contracts for purchase of RM, employee contracts, lease commitments, sales, investments, etc. Disclosure in L & T Ltd: Other commitments related to sales / procurements made in normal course of business are not disclosed to avoid excessive details CNK 74 CNK 74

75 Illustrative disclosure of Other Commitments Under lease obligations Under derivative contracts Going concern support to group company PE arrangement between Holding co, subsidiary, associate Buy back arrangements Commitment to fund research projects, etc. CNK 75 CNK 75

76 As per AS 21, CFS are presented, to the extent possible, in the same format as that adopted by the parent for its separate financial statements. Thus disclosures of RS VI will be applicable to CFS Bifurcation between current / non current Trade receivables over 6 months from due date of payment, etc. Disclosure of Minority Interest Separate line item on the face of the BS after Shareholders Funds. Mahindra Lifespace developers Ltd Minority Interest classified as Non Current Liabilities. CNK 76 CNK 76

77 Information pertaining to Subsidiaries required for preparation of CFS: Break up of assets / liabilities in current and non current (to also cover related parties); Security details, Terms of repayment of Long term Borrowings; Trade Receivables - ageing analysis from the due date of payment; Break up of cash and cash equivalents any restriction / pledge of fixed deposits, Tenure of deposits; Details of Capital Advances, etc.; Details of any Other Commitments having financial obligations; Details of expenditure in excess of 1% of revenue from operation; etc. CNK 77 CNK 77

78 Balance Sheet Statement of Profit and Loss Cash Flow Statement Company Background (preferable) Significant Accounting Policies Notes pertaining to items appearing in the BS, PL Other disclosures required as per RS VI Disclosures required as per notified AS Disclosures required under other statutes, ICAI, etc. Note that RS VI applied from and that previous year figures are regrouped / reclassified as per requirements of RS VI. CNK 78 CNK 78

79 Additional procedures for verification/documentation Audit Documentation (SA 230) o Documents to be taken and arranged in the Audit file as per classification of items given in RS VI. Representation to be taken from Management (SA 580) o Representation Letter to be taken from the management will undergo a change this year since the company will be preparing its FS in the format of RS VI for the first time, hence the classification of items into Current and Non Current by management. CNK 79 CNK 79

80 CNK 80 CNK 80

26 th Regional Conference of WIRC. Revised Schedule VI. CA N. Venkatram 16th December, 2011

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

REVISED SCHEDULE VI Detailed Analysis with Practical Approach

REVISED SCHEDULE VI Detailed Analysis with Practical Approach By: 28.04.2012 1 SESSION I: o EXISTING PROVISIONS o REVISED SCHEDULE VI o AN OVERVIEW o OVERALL APPROACH o KEY CHANGES B/S o KEY CHANGES P&L

REVISED SCHEDULE VI Detailed Analysis with Practical Approach By: 28.04.2012 1 SESSION I: o EXISTING PROVISIONS o REVISED SCHEDULE VI o AN OVERVIEW o OVERALL APPROACH o KEY CHANGES B/S o KEY CHANGES P&L

Welcome to Presentation on preparation of financial statements under revised schedule VI. K.Chandra Sekhar Company Secretary Ace Designers Limited

Welcome to Presentation on preparation of financial statements under revised schedule VI K.Chandra Sekhar Company Secretary Ace Designers Limited 1 Relevant provisions Indian Companies Act, 1956 Rules

Welcome to Presentation on preparation of financial statements under revised schedule VI K.Chandra Sekhar Company Secretary Ace Designers Limited 1 Relevant provisions Indian Companies Act, 1956 Rules

Reporting Under Revised Schedule VI of. A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA

CA AKSHAY K GUPTA") Reporting Under Revised Schedule VI of Companies Act 1956 A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA 1 The Ministry of Corporate Affairs (MCA) on Tuesday, the 1st day of March notified

Reporting Under Revised Schedule VI of Companies Act 1956 A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA 1 The Ministry of Corporate Affairs (MCA) on Tuesday, the 1st day of March notified

Revised Schedule VI. By: Purushottam Nyati Mukul Rathi. July 27, Page 1

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

REVISED OUTLINE GUIDANCE NOTES

REVISED OUTLINE GUIDANCE NOTES regarding adoption of Schedule VI to the Companies Act 1956 in the subject of ACCOUNTANCY Class XII For the Board Examination, March 2014 1 CONTENT Chapter 1: GENERAL INTRODUCTION

REVISED OUTLINE GUIDANCE NOTES regarding adoption of Schedule VI to the Companies Act 1956 in the subject of ACCOUNTANCY Class XII For the Board Examination, March 2014 1 CONTENT Chapter 1: GENERAL INTRODUCTION

Structure of Revised Schedule VI Key Changes Key Points

Revised Scheduled VI Structure of Presentation Setting the Context Structure of Revised Schedule VI Key Changes Key Points Setting the Context Setting the Context Towards International Format: Harmonize

Revised Scheduled VI Structure of Presentation Setting the Context Structure of Revised Schedule VI Key Changes Key Points Setting the Context Setting the Context Towards International Format: Harmonize

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

Outline Guidance Notes regarding adoption of CLASS XII Revised Schedule VI to the Companies Act 1956 in the subject of Accountancy (Effective for Board Examination 2013) Shiksha Kendra, 2, Community Centre,

Outline Guidance Notes regarding adoption of CLASS XII Revised Schedule VI to the Companies Act 1956 in the subject of Accountancy (Effective for Board Examination 2013) Shiksha Kendra, 2, Community Centre,

REVISED SCHEDULE VI. By : CA Kusai Goawala

REVISED SCHEDULE VI By : CA Kusai Goawala Old Schedule VI was operative from 1956. Outdated format for Balance Sheet replaced Revised Schedule VI is a step towards convergence with IFRS Based on IAS1 or

REVISED SCHEDULE VI By : CA Kusai Goawala Old Schedule VI was operative from 1956. Outdated format for Balance Sheet replaced Revised Schedule VI is a step towards convergence with IFRS Based on IAS1 or

Index. 97 b) Comparison of Old and Revised Schedule VI 98. Illustrative list of disclosures required under Companies Act, 1956

Comparison of Old and Revised Schedule VI 98. Illustrative list of disclosures required under Companies Act, 1956") Index S.No. Contents Page No. 1. Introduction 3 2. Objective and Scope 3 3. Applicability 4 4. Summary of the Revised Schedule VI 4 5. Structure of the Revised Schedule VI 10 6. General Instructions to

Index S.No. Contents Page No. 1. Introduction 3 2. Objective and Scope 3 3. Applicability 4 4. Summary of the Revised Schedule VI 4 5. Structure of the Revised Schedule VI 10 6. General Instructions to

Intermediate (IPC) Course Paper 1: Accounting Chapter 2: Financial Statements of Companies CA. Pankajj Goel

Course Paper 1: Accounting Chapter 2: Financial Statements of Companies CA. Pankajj Goel") Intermediate (IPC) Course Paper 1: Accounting Chapter 2: Financial Statements of Companies CA. Pankajj Goel The Institute of Chartered Accountants of India Recorded on: 24-October-2014 1 This lecture has

Intermediate (IPC) Course Paper 1: Accounting Chapter 2: Financial Statements of Companies CA. Pankajj Goel The Institute of Chartered Accountants of India Recorded on: 24-October-2014 1 This lecture has

NOTES FORMING PART OF THE FINANCIAL STATEMENTS 1. CORPORATE INFORMATION. 2. BASIS OF PREPARATION AND PRESENTATION 2.1 Statement of compliance

103 1. CORPORATE INFORMATION company domiciled and incorporated under the provisions of the Companies Act, 1956. The Company is engaged in the manufacturing and selling of motorised 2. BASIS OF PREPARATION

103 1. CORPORATE INFORMATION company domiciled and incorporated under the provisions of the Companies Act, 1956. The Company is engaged in the manufacturing and selling of motorised 2. BASIS OF PREPARATION

GOVERNMENT OF INDIA Ministry of Corporate Affairs

GOVERNMENT OF INDIA Ministry of Corporate Affairs NOTICE INVITING COMMENTS ON THE REVISED SCHEDULE III TO THE COMPANIES ACT, 2013 FOR A COMPANY WHOSE FINANCIAL STATEMENTS ARE DRAWN UP IN COMPLIANCE OF

GOVERNMENT OF INDIA Ministry of Corporate Affairs NOTICE INVITING COMMENTS ON THE REVISED SCHEDULE III TO THE COMPANIES ACT, 2013 FOR A COMPANY WHOSE FINANCIAL STATEMENTS ARE DRAWN UP IN COMPLIANCE OF

KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory. Revised Schedule VI. By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA]

![KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory. Revised Schedule VI. By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA]](/thumbs/78/78547575.jpg "KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory. Revised Schedule VI. By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA]") KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory Revised Schedule VI By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA] Introduction Old Schedule VI had outlived its utility; Revised Schedule VI

KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory Revised Schedule VI By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA] Introduction Old Schedule VI had outlived its utility; Revised Schedule VI

Jubilant First Trust Healthcare Limited Balance Sheet as at 31 March 2016

Balance Sheet as at 31 March 2016 (Rs. '000) Note As at 31 March 2016 As at 31 March 2015 EQUITY AND LIABILITIES Shareholder's funds Share capital 2 20,500 156,132 Reserves and surplus 3 46,622 581,899

Balance Sheet as at 31 March 2016 (Rs. '000) Note As at 31 March 2016 As at 31 March 2015 EQUITY AND LIABILITIES Shareholder's funds Share capital 2 20,500 156,132 Reserves and surplus 3 46,622 581,899

SCHEDULE-III CHECKLIST SCHEDULE - III CHECKLIST

SCHEDULE- CHECKLST SCHEDULE - CHECKLST 1 SCHEDULE- CHECKLST S.No YES NO N.A (A) Share Capital Whether each class of share capital are shown as - Equity Share Capital and Preference Share Capital (different

SCHEDULE- CHECKLST SCHEDULE - CHECKLST 1 SCHEDULE- CHECKLST S.No YES NO N.A (A) Share Capital Whether each class of share capital are shown as - Equity Share Capital and Preference Share Capital (different

Ind-AS Implementation Issues. Himanshu Kishnadwala

Ind-AS Implementation Issues Himanshu Kishnadwala What is I-GAAP? Accounting Standards in India Till 2006, Standards issued by ASB of ICAI were to be followed Companies (Accounting Standards) Rules, notified

Ind-AS Implementation Issues Himanshu Kishnadwala What is I-GAAP? Accounting Standards in India Till 2006, Standards issued by ASB of ICAI were to be followed Companies (Accounting Standards) Rules, notified

Overview with Schedule III

Overview with Schedule III LUNAWAT & CO. Chartered Accountants 11 th December 2014 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE STRUCTURE 1956 2013 13 Parts 29 Chapters 658 Sections 470 Sections

Overview with Schedule III LUNAWAT & CO. Chartered Accountants 11 th December 2014 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE STRUCTURE 1956 2013 13 Parts 29 Chapters 658 Sections 470 Sections

JR TOLL ROAD PRIVATE LIMITED FINANCIAL STATEMENT FOR

JR TOLL ROAD PRIVATE LIMITED FINANCIAL STATEMENT FOR YEAR ENDED 31ST MARCH 2015 Balance Sheet as at 31st March 2015 Particulars Note As at March 31, 2015 As at March 31, 2014 I. EQUITY AND LIABILITIES

JR TOLL ROAD PRIVATE LIMITED FINANCIAL STATEMENT FOR YEAR ENDED 31ST MARCH 2015 Balance Sheet as at 31st March 2015 Particulars Note As at March 31, 2015 As at March 31, 2014 I. EQUITY AND LIABILITIES

1 Good Company FTA (India) Limited

Limited") 1 Good Company FTA (India) Limited 2 Good Company FTA (India) Limited & Young LLP Contents Introduction... 6 Objective... 6 Consolidated Balance Sheet... 10 Consolidated Statement of Profit & Loss... 13

1 Good Company FTA (India) Limited 2 Good Company FTA (India) Limited & Young LLP Contents Introduction... 6 Objective... 6 Consolidated Balance Sheet... 10 Consolidated Statement of Profit & Loss... 13

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

FANTAIN SPORTS PRIVATE LIMITED 1. Fantain Sports Private Limited

FANTAIN SPORTS PRIVATE LIMITED 1 Fantain Sports Private Limited 2 FANTAIN SPORTS PRIVATE LIMITED Independent Auditor s Report To the Members of Fantain Sports Private Limited Report on the Standalone Financial

FANTAIN SPORTS PRIVATE LIMITED 1 Fantain Sports Private Limited 2 FANTAIN SPORTS PRIVATE LIMITED Independent Auditor s Report To the Members of Fantain Sports Private Limited Report on the Standalone Financial

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES AS 1 Disclosure of Accounting Policies Still few enterprises mention in their accounting policy, accounts are prepared on going concern and accounts

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES AS 1 Disclosure of Accounting Policies Still few enterprises mention in their accounting policy, accounts are prepared on going concern and accounts

PARTICULARS SCHEDULE As at

CONSOLIDATED BALANCE SHEET As at 30.9.2015 I. EQUITY AND LIABILITIES PARTICULARS SCHEDULE As at (1) SHAREHOLDERS' FUNDS : (A) SHARE CAPITAL 1 500.00 (B) RESERVES AND SURPLUS 2 (4801,09,249.02) (C) MONEY

CONSOLIDATED BALANCE SHEET As at 30.9.2015 I. EQUITY AND LIABILITIES PARTICULARS SCHEDULE As at (1) SHAREHOLDERS' FUNDS : (A) SHARE CAPITAL 1 500.00 (B) RESERVES AND SURPLUS 2 (4801,09,249.02) (C) MONEY

CAPITAL FIRST SECURITIES LIMITED BALANCE SHEET AS AT MARCH 31, 2017

BALANCE SHEET AS AT MARCH 31, 2017 Note As at Amount in Rupees As at EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 673,556,000 673,556,000 Reserves and Surplus 4 (195,051,527) (338,181,529)

BALANCE SHEET AS AT MARCH 31, 2017 Note As at Amount in Rupees As at EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 673,556,000 673,556,000 Reserves and Surplus 4 (195,051,527) (338,181,529)

M S GODBOLE & CO Chartered Accountants

Existing Accounting Standards (AS) as issued by ICAI Converged Accounting Standards (IND AS) as prepared by National Advisory Committee on Accounting Standards (NACAS) and MCA will notify the date of application

Existing Accounting Standards (AS) as issued by ICAI Converged Accounting Standards (IND AS) as prepared by National Advisory Committee on Accounting Standards (NACAS) and MCA will notify the date of application

UNIT 1: INTRODUCTION TO COMPANY ACCOUNTS. Understand the reason for the existence and survival of a company.

CHAPTER 10 COMPANY ACCOUNTS UNIT 1: INTRODUCTION TO COMPANY ACCOUNTS LEARNING OUTCOMES After studying this unit, you will be able to: Understand the reason for the existence and survival of a company.

CHAPTER 10 COMPANY ACCOUNTS UNIT 1: INTRODUCTION TO COMPANY ACCOUNTS LEARNING OUTCOMES After studying this unit, you will be able to: Understand the reason for the existence and survival of a company.

As at March 31, 2017 Balance Sheet as at March 31, 2018 Note No. Rs. Lakhs Rs. Lakhs Rs. Lakhs

As at March 31, 2018 As at March 31, 2017 Balance Sheet as at March 31, 2018 Note No. Rs. Lakhs Rs. Lakhs Rs. Lakhs Particulars ASSETS Non-current assets Property, plant and equipment 1.1 162.81 42.76

As at March 31, 2018 As at March 31, 2017 Balance Sheet as at March 31, 2018 Note No. Rs. Lakhs Rs. Lakhs Rs. Lakhs Particulars ASSETS Non-current assets Property, plant and equipment 1.1 162.81 42.76

Suggested Answer_Syl12_June2016_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

Balance Sheet as at March 31, 2018 Amount in Rs. Amount in Rs. Particulars

Balance Sheet as at March 31, 2018 Note Equity and liabilities Shareholders' funds Share capital 3 25,00,00,000 25,00,00,000 Reserves and surplus 4 6,37,76,463 2,22,19,723 Non-Current Liabilities Long-term

Balance Sheet as at March 31, 2018 Note Equity and liabilities Shareholders' funds Share capital 3 25,00,00,000 25,00,00,000 Reserves and surplus 4 6,37,76,463 2,22,19,723 Non-Current Liabilities Long-term

Reliance Gas Pipelines Limited RELIANCE GAS PIPELINES LIMITED 1

Reliance Gas Pipelines Limited RELIANCE GAS PIPELINES LIMITED 1 2 RELIANCE GAS PIPELINES LIMITED Independent Auditor s Report To the Members of Reliance Gas Pipelines Limited Report on the Financial Statements

Reliance Gas Pipelines Limited RELIANCE GAS PIPELINES LIMITED 1 2 RELIANCE GAS PIPELINES LIMITED Independent Auditor s Report To the Members of Reliance Gas Pipelines Limited Report on the Financial Statements

(Amount in Rs.) Particulars Note No. As at As at As at March 31, 2017 March 31, 2016 January 1, 2015

Particulars Note No. As at As at As at March 31, 2017 March 31, 2016 January 1, 2015") BALANCE SHEET AS AT MARCH 31, 2017 0 (0) (0) Note No. March 31, 2016 January 1, 2015 1) ASSETS Non-current assets (a) Property, plant and equipment 5 2,576,098,946 2,635,566,136 35,362,666 (b) Capital

BALANCE SHEET AS AT MARCH 31, 2017 0 (0) (0) Note No. March 31, 2016 January 1, 2015 1) ASSETS Non-current assets (a) Property, plant and equipment 5 2,576,098,946 2,635,566,136 35,362,666 (b) Capital

ED/GN-Div-II/ /24 EXPOSURE DRAFT OF REVISED GUIDANCE NOTE ON DIVISION II - IND AS SCHEDULE III TO THE COMPANIES ACT, 2013 (Last

ED/GN-Div-II/2019-2020/24 EXPOSURE DRAFT OF REVISED GUIDANCE NOTE ON DIVISION II - IND AS SCHEDULE III TO THE COMPANIES ACT, 2013 (Last date for Comments: April 20, 2019) Issued by Corporate Laws & Corporate

ED/GN-Div-II/2019-2020/24 EXPOSURE DRAFT OF REVISED GUIDANCE NOTE ON DIVISION II - IND AS SCHEDULE III TO THE COMPANIES ACT, 2013 (Last date for Comments: April 20, 2019) Issued by Corporate Laws & Corporate

PAPER 5 : ADVANCED ACCOUNTING

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

31,114 29,213 ASSETS Non-current assets Fixed Assets Tangible assets Intangible assets 6-92 Long-term loans and advances ,095

Vanthys Pharmaceutical Development Private Limited Balance Sheet as at Note (Rs '000) EQUITY AND LIABILITIES Shareholders' funds Share capital 2 225,000 225,000 Reserves and surplus 3 (194,437) (196,211)

Vanthys Pharmaceutical Development Private Limited Balance Sheet as at Note (Rs '000) EQUITY AND LIABILITIES Shareholders' funds Share capital 2 225,000 225,000 Reserves and surplus 3 (194,437) (196,211)

RELIANCE COMTRADE PRIVATE LIMITED FINANCIAL STATEMENTS

RELIANCE COMTRADE PRIVATE LIMITED 1 RELIANCE COMTRADE PRIVATE LIMITED FINANCIAL STATEMENTS 2016-17 2 RELIANCE COMTRADE PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE COMTRADE PRIVATE

RELIANCE COMTRADE PRIVATE LIMITED 1 RELIANCE COMTRADE PRIVATE LIMITED FINANCIAL STATEMENTS 2016-17 2 RELIANCE COMTRADE PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE COMTRADE PRIVATE

Copyright -The Institute of Chartered Accountants of India. The forward contract is sold before its due date, hence considered as speculative.

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

MOSER BAER INDIA LIMITED BALANCE SHEET AS AT MARCH 31, 2011

SOURCES OF FUNDS: MOSER BAER INDIA LIMITED BALANCE SHEET AS AT MARCH 31, 2011 Schedule As at As at 31.03.2011 31.03.2010 SHAREHOLDERS' FUNDS: Capital 1 1,683,061,040 1,683,061,040 Reserves and Surplus

SOURCES OF FUNDS: MOSER BAER INDIA LIMITED BALANCE SHEET AS AT MARCH 31, 2011 Schedule As at As at 31.03.2011 31.03.2010 SHAREHOLDERS' FUNDS: Capital 1 1,683,061,040 1,683,061,040 Reserves and Surplus

UNIBEV LIMITED (Formerly known as M/s Uber Blenders & Distillers Limited)

") BALANCE SHEET AS AT 31 st, MARCH,2017 Notes March 31, 2017 March 31, 2016 (Rs.) (Rs.) I EQUITY AND LIABILITIES (1) Shareholders' funds Share Capital 2 12,786,950 500,000 Reserve and Surplus 3 (10,784,813)

BALANCE SHEET AS AT 31 st, MARCH,2017 Notes March 31, 2017 March 31, 2016 (Rs.) (Rs.) I EQUITY AND LIABILITIES (1) Shareholders' funds Share Capital 2 12,786,950 500,000 Reserve and Surplus 3 (10,784,813)

6.2 Need for Changes in Financial Position. 6.3 Statement of Changes in Financial Position--- Meaning

Analysis Overview of Financial Statements UNIT 6 STATEMENT OF CHANGES IN FINANCIAL POSITION Structure 6.0 Objectives 6.1 Introduction 6.2 Need for Changes in Financial Position 6.3 Statement of Changes

Analysis Overview of Financial Statements UNIT 6 STATEMENT OF CHANGES IN FINANCIAL POSITION Structure 6.0 Objectives 6.1 Introduction 6.2 Need for Changes in Financial Position 6.3 Statement of Changes

2 3 4 5 MISSION 47% 6 7 8 9 MISSION 10 11 12 13 14 15 TOTAL INCOME (` IN CRORES) 3,083 2,056 623 934 1,103 1,323 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 NET PROFIT (` IN CRORES) 343 450 194 241

2 3 4 5 MISSION 47% 6 7 8 9 MISSION 10 11 12 13 14 15 TOTAL INCOME (` IN CRORES) 3,083 2,056 623 934 1,103 1,323 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 NET PROFIT (` IN CRORES) 343 450 194 241

RELIANCE RETAIL FINANCE LIMITED 1. Reliance Retail Finance Limited

RELIANCE RETAIL FINANCE LIMITED 1 Reliance Retail Finance Limited 2 RELIANCE RETAIL FINANCE LIMITED Independent Auditor s Report To the Members of Reliance Retail Finance Limited Report on the Financial

RELIANCE RETAIL FINANCE LIMITED 1 Reliance Retail Finance Limited 2 RELIANCE RETAIL FINANCE LIMITED Independent Auditor s Report To the Members of Reliance Retail Finance Limited Report on the Financial

TK TOLL ROAD PRIVATE LIMITED

TK TOLL ROAD PRIVATE LIMITED Financial Statements For The MARCH 2015 Balance Sheet as at 31st March,2015 Particulars I. EQUITY AND LIABILITIES Note No. As at March 31st, 2015 As at 2014 Rupees Rupees

TK TOLL ROAD PRIVATE LIMITED Financial Statements For The MARCH 2015 Balance Sheet as at 31st March,2015 Particulars I. EQUITY AND LIABILITIES Note No. As at March 31st, 2015 As at 2014 Rupees Rupees

Capsule on Accounting Standards

Capsule on Accounting Standards Conducted by Young Members Empowerment Committee jointly with Accounting Standards Board Presented by CA Manish C. Iyer, Deputy Director, Technical Directorate, ICAI 1 Standards

Capsule on Accounting Standards Conducted by Young Members Empowerment Committee jointly with Accounting Standards Board Presented by CA Manish C. Iyer, Deputy Director, Technical Directorate, ICAI 1 Standards

Test Series: March, 2018

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

Jubilant Draximage Limited Balance Sheet as at 31 March 2017 (INR in thousands) As at 31 March 2017

As at 31 March 2017") Balance Sheet as at Notes 1 April 2015 ASSETS Non-current assets Property, plant and equipment 3 498 626 159 Other intangible assets 4 - - 2 Financial assets i. Loans 5(b) 82 37 22 ii. Other financial

Balance Sheet as at Notes 1 April 2015 ASSETS Non-current assets Property, plant and equipment 3 498 626 159 Other intangible assets 4 - - 2 Financial assets i. Loans 5(b) 82 37 22 ii. Other financial

CAPITAL FIRST SECURITIES LIMITED BALANCE SHEET AS AT MARCH 31, 2018

BALANCE SHEET AS AT MARCH 31, 2018 Note EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 673,556,000 673,556,000 Reserves and Surplus 4 (18,500,638) (195,051,527) 655,055,362 478,504,473 Non

BALANCE SHEET AS AT MARCH 31, 2018 Note EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 673,556,000 673,556,000 Reserves and Surplus 4 (18,500,638) (195,051,527) 655,055,362 478,504,473 Non

CRUSTUM PRODUCTS PRIVATE LIMITED

CRUSTUM PRODUCTS P R I V A T E L I M I T E D Financial Statements 2016-17 1 INDEPENDENT AUDITOR S REPORT To the Members CRUSTUM PRODUCTS PRIVATE LIMITED Report on the Financial Statements We have audited

CRUSTUM PRODUCTS P R I V A T E L I M I T E D Financial Statements 2016-17 1 INDEPENDENT AUDITOR S REPORT To the Members CRUSTUM PRODUCTS PRIVATE LIMITED Report on the Financial Statements We have audited

Balance Sheet as at 31st March 2015 Particulars Note March 31, 2015 March 31, 2014 I. EQUITY AND LIABILITIES Shareholders' Funds Share capital 2.1 44,770,000 44,770,000 Reserves and surplus 2.2 202,297,322

Balance Sheet as at 31st March 2015 Particulars Note March 31, 2015 March 31, 2014 I. EQUITY AND LIABILITIES Shareholders' Funds Share capital 2.1 44,770,000 44,770,000 Reserves and surplus 2.2 202,297,322

SEGMENT- I: INFORMATION AND PARTICULARS IN RESPECT OF BALANCE SHEET. From (DD/MM/YYYY) To (DD/MM/YYYY)

To (DD/MM/YYYY)") FORM NO. AOC-4 [Pursuant to section 137 of the Companies Act, 2013 and sub-rule (1) of Rule 12 of Companies (Accounts) Rules, 2014] Form for filing financial statement and other documents with the Registrar

FORM NO. AOC-4 [Pursuant to section 137 of the Companies Act, 2013 and sub-rule (1) of Rule 12 of Companies (Accounts) Rules, 2014] Form for filing financial statement and other documents with the Registrar

11 th April 2018 IIBF CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA

, FCA, FCS, FCMA, LL.B, MIMA, DISA") 11 th April 2018 IIBF CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA BANKERS PERSPECTIVE Corporate Balance sheet Annual Report Directors Report Auditors Report Aspects of Accounting

11 th April 2018 IIBF CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA BANKERS PERSPECTIVE Corporate Balance sheet Annual Report Directors Report Auditors Report Aspects of Accounting

Analysis of Financial Statements

Analysis of Financial Statements DTRTI Chennai 19 th September, 2016 1 G R HARI, Chennai Manohar Chowdhry & Associates Objective of this session Voluminous & Unwanted data. Too many transactions with RP

Analysis of Financial Statements DTRTI Chennai 19 th September, 2016 1 G R HARI, Chennai Manohar Chowdhry & Associates Objective of this session Voluminous & Unwanted data. Too many transactions with RP

NOTES FORMING PART OF FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2016

NOCIL LIMITED NOTES FORMING PART OF FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2016 CORPORATE INFORMATION NOCIL Limited (the Company) was incorporated on 11 May 1961, and is engaged in manufacture

NOCIL LIMITED NOTES FORMING PART OF FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2016 CORPORATE INFORMATION NOCIL Limited (the Company) was incorporated on 11 May 1961, and is engaged in manufacture

Changes in Financial Statements and Auditor s Report. Presentation By CA Anil Sharma

Changes in Financial Statements and Auditor s Report Presentation By CA Anil Sharma Sec 129- Financial Statement The financial statement shall : be in the form in Schedule III and comply with the accounting

Changes in Financial Statements and Auditor s Report Presentation By CA Anil Sharma Sec 129- Financial Statement The financial statement shall : be in the form in Schedule III and comply with the accounting

Financial Statements of Companies

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

Part A (DD/MM/YYYY) (a)* Date of Board of Directors' meeting in which consolidated financial statements were approved

(a)* Date of Board of Directors' meeting in which consolidated financial statements were approved") FORM NO. AOC-4 CFS [Pursuant to section 137 of the Companies Act, 2013 and Rule 12 of Companies (Accounts) Rules, 2014] Form for filing consolidated financial statements and other documents with the Registrar

FORM NO. AOC-4 CFS [Pursuant to section 137 of the Companies Act, 2013 and Rule 12 of Companies (Accounts) Rules, 2014] Form for filing consolidated financial statements and other documents with the Registrar

Ujjivan Financial Services Limited (Formerly Ujjivan Financial Services Private Limited)

") Ujjivan Financial Services Limited (Formerly Ujjivan Financial Services Private Limited) Notes to Financial Statements for the year ended 1 CORPORATE INFORMATION Ujjivan Financial Services Limited is a

Ujjivan Financial Services Limited (Formerly Ujjivan Financial Services Private Limited) Notes to Financial Statements for the year ended 1 CORPORATE INFORMATION Ujjivan Financial Services Limited is a

CYBER MEDIA (INDIA) LIMITED NOTES ON FINANCIAL STATEMENTS FOR THE YEAR ENDED 31ST MARCH, 2016

LIMITED NOTES ON FINANCIAL STATEMENTS FOR THE YEAR ENDED 31ST MARCH, 2016") 1. Significant Accounting Policies The significant accounting policies adopted by the Company in respect of these financial statement, are set out below: 1.1 Basis of Preparation of financial statements

1. Significant Accounting Policies The significant accounting policies adopted by the Company in respect of these financial statement, are set out below: 1.1 Basis of Preparation of financial statements

Net Current Assets (62,748,149) (2,858,178,175) (90,126,095) (4,225,111,319)

(2,858,178,175) (90,126,095) (4,225,111,319)") Balance Sheet as at December 31, 2010 SOURCES OF FUNDS Schedule 2010 2010 2009 2009 (Amount in USD) (Amount in INR) (Amount in USD) (Amount in INR) Shareholders' Funds Share capital A 28 1,275 28 1,313

Balance Sheet as at December 31, 2010 SOURCES OF FUNDS Schedule 2010 2010 2009 2009 (Amount in USD) (Amount in INR) (Amount in USD) (Amount in INR) Shareholders' Funds Share capital A 28 1,275 28 1,313

Valuation. The Institute of Chartered Accountants of India

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1. Reliance Clothing India Private Limited

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1 Reliance Clothing India Private Limited 2 RELIANCE CLOTHING INDIA PRIVATE LIMITED INDEPENDENT AUDITOR S REPORT To the Members of Reliance Clothing India Private

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1 Reliance Clothing India Private Limited 2 RELIANCE CLOTHING INDIA PRIVATE LIMITED INDEPENDENT AUDITOR S REPORT To the Members of Reliance Clothing India Private

Jubilant Infrastructure Limited Ind AS financial statements March 2017

Ind AS financial statements March 2017 Balance Sheet as at Notes 1 April 2015 ASSETS Non-current assets Property, plant and equipment 3 1,459,327 1,354,722 1,227,256 Capital work-in-progress 3 11,073 24,708

Ind AS financial statements March 2017 Balance Sheet as at Notes 1 April 2015 ASSETS Non-current assets Property, plant and equipment 3 1,459,327 1,354,722 1,227,256 Capital work-in-progress 3 11,073 24,708

Quarterly technical updates. April 2017

Agenda 1 Opening Remarks 2 Regulatory updates 3 Ind AS 4 Q & A 2 1. Opening Remarks 3 2. Regulatory updates 4 Integrated reporting in India SEBI reporting requirement for top 500 companies (by market cap.)

Agenda 1 Opening Remarks 2 Regulatory updates 3 Ind AS 4 Q & A 2 1. Opening Remarks 3 2. Regulatory updates 4 Integrated reporting in India SEBI reporting requirement for top 500 companies (by market cap.)

2. Management s Responsibility for the Ind AS Financial Statements

Independent Auditor s Report To the Members of 1. Report on the Ind AS Financial Statements We have audited the accompanying Ind AS financial statements of ( the Company ), which comprise the Balance Sheet

Independent Auditor s Report To the Members of 1. Report on the Ind AS Financial Statements We have audited the accompanying Ind AS financial statements of ( the Company ), which comprise the Balance Sheet

Statement of cash flows PURPOSE & SCOPE

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

(a) in the case of the Balance Sheet, of the state of affairs of the Company as at March 31, 2014;

in the case of the Balance Sheet, of the state of affairs of the Company as at March 31, 2014;") Independent Auditor s Report To the Members of Capital First Commodities Limited Report on the Financial Statements We have audited the accompanying financial statements of Capital First Commodities Limited

Independent Auditor s Report To the Members of Capital First Commodities Limited Report on the Financial Statements We have audited the accompanying financial statements of Capital First Commodities Limited

BALANCE SHEET AS AT 31ST MARCH 2017

TAURUS VALUE STEEL & PIPES PRIVATE LTD., SY No : 487, BACHUPALLY VILLAGE, KUTBULLAPUR MANDAL, TELANGANA - 501 401 CIN : U28112TG2009PTC064592 PHONE : 080 4011 7777 E MAIL ID : chinnappa@shankarabuildpro.com

TAURUS VALUE STEEL & PIPES PRIVATE LTD., SY No : 487, BACHUPALLY VILLAGE, KUTBULLAPUR MANDAL, TELANGANA - 501 401 CIN : U28112TG2009PTC064592 PHONE : 080 4011 7777 E MAIL ID : chinnappa@shankarabuildpro.com

Book-III:- Analysis of Financial Statement of a company. Financial Statements of a Company

SUPPORT MATERIAL ACCOUNTANCY CLASS-XII Book-III:- Analysis of Financial Statement of a company Financial Statements of a Company Financial Statements: Financial statements are the end products of accounting

SUPPORT MATERIAL ACCOUNTANCY CLASS-XII Book-III:- Analysis of Financial Statement of a company Financial Statements of a Company Financial Statements: Financial statements are the end products of accounting

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES NORWAY AS BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated)

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES NORWAY AS BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated)

RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED FINANCIAL STATEMENTS

RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED 1231 RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED FINANCIAL STATEMENTS 2017-18 1232 RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED

RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED 1231 RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED FINANCIAL STATEMENTS 2017-18 1232 RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED

PRIME FOCUS TECHNOLOGIES INC. Notes to Standalone financial statements

Notes to Standalone financial statements 1. Corporate Information Prime Focus Technologies Inc. ("the Holding Company") was incorporated on 21st February, 2013 in USA. Prime Focus Technologies Private

Notes to Standalone financial statements 1. Corporate Information Prime Focus Technologies Inc. ("the Holding Company") was incorporated on 21st February, 2013 in USA. Prime Focus Technologies Private

Oracle Financial Services Software Inc.

To the Members, Oracle Financial Services Software Inc. Directors Report Your Directors are pleased to present the Annual Report on the business and operations of your company, together with the accounts

To the Members, Oracle Financial Services Software Inc. Directors Report Your Directors are pleased to present the Annual Report on the business and operations of your company, together with the accounts

Example Accounts Only

CaseWare Australia & New Zealand Large General Purpose RDR Company Financial Statements Disclaimer: These financials include illustrative disclosures for a large proprietary company who is preparing general

CaseWare Australia & New Zealand Large General Purpose RDR Company Financial Statements Disclaimer: These financials include illustrative disclosures for a large proprietary company who is preparing general

2.1 Summary of significant accounting policies

Annual Report 2015-16 142 Standalone Financials Notes to financial statements for the year ended 31 March 2016 NOTE 1. CORPORATE INFORMATION Sterlite Technologies Limited (the Company) is a public company

Annual Report 2015-16 142 Standalone Financials Notes to financial statements for the year ended 31 March 2016 NOTE 1. CORPORATE INFORMATION Sterlite Technologies Limited (the Company) is a public company

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

29,213 28,197 ASSETS Non-current assets Fixed Assets Tangible assets Intangible assets Long-term loans and advances

Vanthys Pharmaceutical Development Private limited Balance Sheet as at 31 March 2014 (Rs '000) As at As at Notes No EQUITY AND LIABILITIES Shareholders' funds Share capital Reserves and surplus 2 225,000

Vanthys Pharmaceutical Development Private limited Balance Sheet as at 31 March 2014 (Rs '000) As at As at Notes No EQUITY AND LIABILITIES Shareholders' funds Share capital Reserves and surplus 2 225,000

DR. WU SKINCARE CO., LTD. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND REVIEW REPORT OF INDEPENDENT ACCOUNTANTS DECEMBER 31, 2017 AND 2016

DR. WU SKINCARE CO., LTD. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND REVIEW REPORT OF INDEPENDENT ACCOUNTANTS DECEMBER 31, 2017 AND 2016 For the convenience of readers and for information purpose

DR. WU SKINCARE CO., LTD. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND REVIEW REPORT OF INDEPENDENT ACCOUNTANTS DECEMBER 31, 2017 AND 2016 For the convenience of readers and for information purpose

Ind AS presentation and disclosure checklist 2018

Ind AS presentation and disclosure checklist 2018 Introduction This publication presents a checklist of presentation and disclosure requirements applicable to entities preparing financial statements in

Ind AS presentation and disclosure checklist 2018 Introduction This publication presents a checklist of presentation and disclosure requirements applicable to entities preparing financial statements in

DA TOLL ROAD PRIVATE LIMITED. Financial Statements for

DA TOLL ROAD PRIVATE LIMITED Financial Statements for YEAR ENDED MARCH 2015 Balance Sheet as at 31st March 2015 Particulars Note As at March 31, 2015 As at March 31, 2014 I. EQUITY AND LIABILITIES

DA TOLL ROAD PRIVATE LIMITED Financial Statements for YEAR ENDED MARCH 2015 Balance Sheet as at 31st March 2015 Particulars Note As at March 31, 2015 As at March 31, 2014 I. EQUITY AND LIABILITIES

¹Hkkx IIµ[k.M 3(i)º Hkkjr dk jkti=k % vlk/kj.k 19

º Hkkjr dk jkti=k % vlk/kj.k 19") ¹Hkkx IIµ[kM 3º Hkkjr dk jkti=k % vlk/kjk 19 वद श 1 2 3 क ल 3 सभ सह यक, एस शएट और स य उ म (च ह व भ रत य य वद श ह ) क सम कत व य ववरण म श मल कय ज एग 4 नक य, सभ सह यक, य एस शएट य स य उ म जसक सम कत व य ववरण

¹Hkkx IIµ[kM 3º Hkkjr dk jkti=k % vlk/kjk 19 वद श 1 2 3 क ल 3 सभ सह यक, एस शएट और स य उ म (च ह व भ रत य य वद श ह ) क सम कत व य ववरण म श मल कय ज एग 4 नक य, सभ सह यक, य एस शएट य स य उ म जसक सम कत व य ववरण

ACERINOX, S.A. AND SUBSIDIARIES. 31 December 2015

ACERINOX, S.A. AND SUBSIDIARIES Annual Accounts of the Consolidated Group 31 December 2015 (Free translation from the original in Spanish. In the event of discrepancy, the Spanishlanguage version prevails.)

ACERINOX, S.A. AND SUBSIDIARIES Annual Accounts of the Consolidated Group 31 December 2015 (Free translation from the original in Spanish. In the event of discrepancy, the Spanishlanguage version prevails.)

NOTES. To Financial Statements for the year ended 31st March, Financial Statements

NOTES 241 Back ground and operations Marico Limited ( Marico or the Company ), headquartered in Mumbai, Maharashtra, India, carries on business in branded consumer products. Marico manufactures and markets

NOTES 241 Back ground and operations Marico Limited ( Marico or the Company ), headquartered in Mumbai, Maharashtra, India, carries on business in branded consumer products. Marico manufactures and markets

QURIES ON AS-26. (1) Accounting for the profit arising from a sale and lease-back transaction.

Accounting for the profit arising from a sale and lease-back transaction.") QURIES ON AS-26 (1) Accounting for the profit arising from a sale and lease-back transaction. 1. A company registered under the Companies Act, 1913, is carrying on the business of banking. Its operations

QURIES ON AS-26 (1) Accounting for the profit arising from a sale and lease-back transaction. 1. A company registered under the Companies Act, 1913, is carrying on the business of banking. Its operations

2 Non-current liabilities (a) Long-term borrowings 5 73,000,000 73,000,000 (b) Long-term provisions 6 107, ,285 73,107,068 73,148,285

Long-term borrowings 5 73,000,000 73,000,000 (b) Long-term provisions 6 107, ,285 73,107,068 73,148,285") Balance Sheet as at 31 March 2016 I Note EQUITY AND LIABILITIES 1 Shareholders' funds (a) Share capital 3 370,547,180 370,547,180 (b) Money received against share warrants 4 615,000,000 615,000,000 985,547,180

Balance Sheet as at 31 March 2016 I Note EQUITY AND LIABILITIES 1 Shareholders' funds (a) Share capital 3 370,547,180 370,547,180 (b) Money received against share warrants 4 615,000,000 615,000,000 985,547,180

A Practitioner's Guide

Revised Schedule VI : A Practitioner's Guide Committee for Capacity Building of CA Firms and Small & Medium Practitioners (CCBCAF & SMP) The Institute of Chartered Accountants of India (Set up by an Act

Revised Schedule VI : A Practitioner's Guide Committee for Capacity Building of CA Firms and Small & Medium Practitioners (CCBCAF & SMP) The Institute of Chartered Accountants of India (Set up by an Act

(All amount are stated in Indian Rupees, unless stated otherwise) Particulars I. EQUITY AND LIABILITIES

Particulars I. EQUITY AND LIABILITIES") Balance Sheet as at 31st March 2017 I. EQUITY AND LIABILITIES Note No. 31 March 2017 31 March 2016 1 Shareholders funds (a) Share Capital 3 1,99,92,000 1,99,92,000 (b) Reserves and Surplus 4 10,07,74,946

Balance Sheet as at 31st March 2017 I. EQUITY AND LIABILITIES Note No. 31 March 2017 31 March 2016 1 Shareholders funds (a) Share Capital 3 1,99,92,000 1,99,92,000 (b) Reserves and Surplus 4 10,07,74,946

RELIANCE TEXTILES LIMITED FINANCIAL STATEMENTS FY

RELIANCE TEXTILES LIMITED 1 RELIANCE TEXTILES LIMITED FINANCIAL STATEMENTS FY 2016-17 2 RELIANCE TEXTILES LIMITED Independent Auditor s Report To The Members of Reliance Textiles Limited Report on the

RELIANCE TEXTILES LIMITED 1 RELIANCE TEXTILES LIMITED FINANCIAL STATEMENTS FY 2016-17 2 RELIANCE TEXTILES LIMITED Independent Auditor s Report To The Members of Reliance Textiles Limited Report on the

SUGGESTED SOLUTION FINAL MAY 2019 EXAM. Test Code FNJ 7098