Structure of Revised Schedule VI Key Changes Key Points

|

|

|

- Amberlynn Patterson

- 5 years ago

- Views:

Transcription

1 Revised Scheduled VI

2 Structure of Presentation Setting the Context Structure of Revised Schedule VI Key Changes Key Points

3 Setting the Context

4 Setting the Context Towards International Format: Harmonize and synchronize the disclosure requirements with Internatinal formats & in the direction of Ind AS (IFRS converged AS) For e. g. Certain concepts like current/ non current classification ofassets and liabilities, Elimination of concept of schedule and such information will now be provided in the notes to accounts Applicability Applicable to all Companies (except Banking and Insurance Companies) Applicability date: Financial years commencing on or after 1 April 2011 Can a company apply Revised Schedule VI early from 1 January 2011?

5 Setting the Context Format No option to use horizontal format for presentation of BS No option to use functional classification of expenses Each item of the face of the BS and P&L shall be cross referenced to any related information in notes to accounts Revised Schedule VI has flexibility Addition, deletion, amendment, substitution, tion modification of line/sub line items AS/ Act override Revised Schedule VI Balance between providing excessive detail or excessive aggregation

6 Concept of Materiality Revised schedule VI specifically recognizes concept of materiality Existing schedule VI materiality threshold Expenses exceeding 1% of the total revenue or Rs. 5,000, whichever is higher, shall be shown as a separate and distinct item Revised schedule VI materiality threshold Items of income or expense which exceeds 1% of the revenue from operations or Rs 100,000 whichever is higher

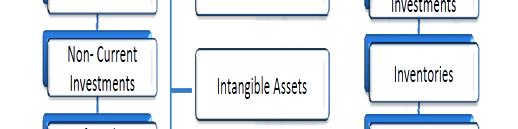

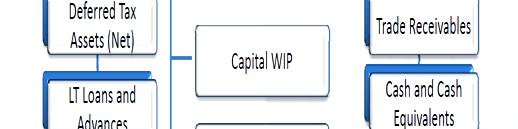

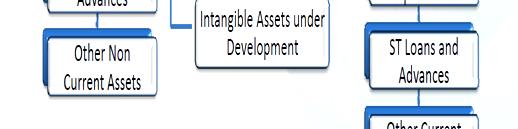

7 Structure of Revised Schedule VI

")

8 Balance Sheet Revised Format (Rupees in )

")

9 Balance Sheet Revised Format (Rupees in )

10 P&L Revised Format (Rupees in )

11 P&L Revised Format (Rupees in )

12 Equity and Liability Classification

13 Assets Classification

14 Key Changes

15 New Disclosures Current/ non current classification If an asset or a liability has both the portions, company will need to break the same into current and non current portions e.g., Current maturities of a long term borrowing will have to be separated and classified under the head other current liabilities Will Impact Working Capital, Current Ratio & Debt Equity Ratios Loans and Advances from Related Parties Revised schedule VI requires separate disclosure for loans and advance received from and given to related parties

16 New Disclosures Commitments Requires disclosure of all commitments (including commitments other than capital commitments) Loan Defaults Requires disclosure of all defaults df in repayment of loans and interest Currently CARO requires only defaults in repayment of dues to financial institutions, banks and debenture holders to be specified Terms of repayment of term loans & other loans to be disclosed (earlier only debentures) Shares of each class held by: Holding Company Ultimate Holding Company Subsidiaries or Associates of Above 2

17 New Disclosures Shareholder s Funds Additional Disclosures Reconciliation of no. of shares outstanding at beginning and end of reporting period Rights, preferences and restrictions of each class of shares including restrictions on distribution of dividends and repayment py of capital Details of shareholders holding more than 5% shares Details of shares issuable under options and contracts/ commitments Unpaid calls by directors and officers shall be shown separately For 5 years immediately preceding the date of BS disclose aggregate number & class of shares : pursuant to contract(s) without payment being received in cash (presently to be given throughout the life of the Company) bonus shares (presently to be given throughout the life of the Company) bought back (presently not required)

18 New Disclosures Share Application money pending allotment Not exceeding issued capital and not refundable disclosure after shareholders h fund and before liability If refundable other current liability Additional Disclosures of Share Application Money Terms & Conditions Number of shares to be issued Amount of premium period before which shareswill be allotted Whether company has sufficient authorized capital to allot the shares out of application money Period for which it is pending beyond the date of allotment mentioned in offer document with reasons Investments With respect to Investments, separate disclosure required for investment in controlled special purpose entities What is meant by controlled special purpose entities

19 Disclosures No Longer Required Profit and Loss Account Commission, brokerage and non trade discounts Balance Sheet Investments purchased and sold during the year Investments, sundry debtors andloans & advances pertaining to companies under the same management Break up of Bank Balances between Scheduled & Other Banks, Break up between current account, call account & deposit accounts, Details of names, amount, maximum amounts with non scheduled hdldbanks Notes Managerial remuneration and computation of net profits for calculation of commission Licensed capacity, installed capacity and actual production Balance sheet Abstract & Company s General Profile under Part IV

20 Accounting No Longer Required Dividend Existing Schedule VI required the parent company to recognize dividend declared by subsidiary companies even after the date of the balance sheet if they were pertaining to the period ending on or before the balance sheet date. Such requirement no longer exists in Revised Schedule VI Whether the dividend recognized in the previous year needs to be derecognized and the previous year financial statement to be restated? By virtue of AS 4, Subsidiary Co will provide for proposed p dividend and if holding Co., would not recognise same, how to deal with it in Consolidated Accounts?

21 Disclosures Modified Debtors Currently, dbt debtors Outstanding t for a period exceeding 6 months based on billing date Revised schedule VI requires debtors outstanding for a period exceeding 6 months from the date they became due for payment Capital advances Currently, capital advances can be presented as part of Capital Work in Progress / Fixed Assets Revised Schedule VI requires the same to be presented separately under the head Loans & Advances Profit & Loss Account Appropriation / Reserves & Surplus Appropriation of Profit & Loss to be presented under Reserves & Surplus Debit Balance of Profit & Loss to be shown as a negative figure under Surplus Reserves & Surplus balance will be shown after adjusting negative balance of P&L, even if negative

22 Key Points

23 Important Definitions Current/ Non Current asset An asset is classified as current when it satisfies any of the following criteria: It is expected to be realized in, or is intended for sale or consumption in, the company s normal operating cycle; It is held primarily for the purpose of being traded; It is expected to be realized within ihi twelve months after the reporting date; or It is cash or cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting date. Current/ Non Current liability A liability shall be classified as current when it satisfies any of the following criteria: It is expected to be settled in the company s normal operating cycle; It is held primarily for the purpose p of being traded; It is due to be settled within twelve months after the reporting date; or The company does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting date.

24 Important Definitions Operating Cycle It is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. Where the normal operating cycle cannot be identified, it is assumed to have a duration of 12 month Trade Receivable A receivable shall be classified as a Trade Receivable if it is in respect of the amount due on account of goods sold or services rendered in the normalcourse ofbusiness Trade Payable A payable shall be classified as a Trade Payable if it is in respect of the amount due on account of goods purchased or services received in the normal course of business

25 Key Points Commitments Earlier Schedule VI only capital commitments. Revised Schedule VI requires the disclosure of all commitments, i.e., including other commitments. What is the nature of commitments that will get covered under this disclosure requirement? Trade Receivable/ Payable classification Liability for purchase of fixed assets/ receivable for sale of Fixed Assets not to be classified as Trade Payable/ Trade Receivable Investment Investments Basis ofvaluation (Revised) Vs ModeofValuation of (earlier) Long Term investments carried at other than cost Current Investment (individual investments)

26 Key Points Current and Non Current Classification Deferred Tax should always be classified as Non Current Capital advances to be classified as non current assets Unconditional right to defer settlement of liability Non compliance of debt covenants e.g. quarterly information, non payment of monthly interest. Most loan agreements have a clause that in case of non compliance of anyclause theloanwill bepayable ondemand. Classification of Long term investment expected to be realized within 12 months from the BS date as current investment Employee Benefits like Bonus/ Incentives, Post employment obligations e.g. Gratuity and Pension, Other long term benefits e.g. Accumulated compensated absence

27 Key issues related to Balance Sheet Current and non current classification some questions Company A has taken a loan which is repayable py on demand. However, based on the past experience, it is not expected that the lender will demand the repayment within next 12 months. Company B has taken a 5 year loan. The loan contains certain debt covenants, e.g., filing of quarterly information. The company defaulted in filing of such information in the previous quarter, with the effect that loan has become repayable on demand. However, based on the past experience, the management believes that df default lis minor and the bank will not demand dthe repayment of loan. It has also started the process of getting waiver for this default. After the reporting period and before the approval of the financial statements for issue, the bank agreed to waive the default and not to demand payment as a consequence of the default. A company has taken a 5 year term loan. Out of abundant caution, the bank includes a covenant that it has a right to recall the loan on demand even where the company hasnot violated anyof the debt covenants.

28 Key Points Share Capital Shareholder holding more than 5% shares Classification of preference shares Different classes of Preference Shares to be treated separately. Does it mean that a company should compulsorily classify preference shares based on their substance, i.e., ie redeemable preference shares should always be classified as liability? Disclosure of Preference Shares for companies following AS 30 to 32 on Financial Instruments.

29 Key Points Disclosure Level of disclosure pertaining to default/continuing default in repayment of loans & interest in each case i.e. category wise or loan wise within the category? Details of continuing default (in case of long term borrowing) and default (in case of short term borrowing) as on the balance sheet date in repayment of loans and interest shall be specified separately in each case". The wordings give rise to following issues: Default pertaining to borrowing apart from banks and FI s are also required for items such as bonds/ debentures, deposits, finance lease obligations Defaults other than repayment of loan and interest, e.g., compliance with debt covenants not required to be disclosed

30 Key Points Disclosure Loans and Advances to related parties Details of Loans and Advances given to related parties to be disclosed What details need to be disclosed are not specified? Whether disclosures required to be made in addition to AS 18 (& ASI 13) Disclosure for information about items that do not qualify for recognition in financial statements Postponement of Revenue Recognition Disputed Cases Remote Liability Not Contingent

31 Key Issues Profit and Loss Account Quantitative Information Nature of Company Manufacturing companies Trading companies Companies rendering or supplying li services Company that falls in more than one category Disclosures Required Raw materials under broad heads Goods purchased under broad heads Purchases of goods traded under broad heads Gross income derived from services rendered dunder broad dheads It will be sufficient compliance with the requirements, if purchases, sales and consumption of raw materialand and the gross income from services rendered are shown under broad heads

32 Key Issues Profit and Loss Account Quantitative Information Is a Company required to disclose quantitative details or not? Will a manufacturing company disclose purchase, sale or consumption of raw material? What is meant by good purchased in case of manufacturing companies? Does a manufacturing or a trading company required to disclose sales? How should broad heads for Work in Progress be disclosed? Whether broad heads of Opening and Closing Inventory should also be disclosed?

33 Key Issues Profit and Loss Account Excise Duty, Sales Tax and VAT Revised Schedule VI requires excise duty to be presented as deduction from revenue of a non finance company in the notes No specific requirement for presentation of VAT and Sales Tax Issues AS 9 Revenue Recognition requires excise duty to be shown as deduction from sales on the face of P&L Account (and not in notes) No notified AS deals with accounting for VAT. However, the ICAI GN requires that revenue recognized should be net of VAT Service Tax??

34 Key Issues Profit and Loss Account Accounting and disclosure of share of profit/ loss in Partnership Firms Whether disclosures for Names of all Partners, Total Capital and Share (Profit/ Loss Sharing Ratio) of Each Partner should be disclosed for LLP also? Proposed dividend accounting and disclosure Whether dividend income for finance companies should be taken to main revenue or Other Income?

35 Key Issues Disclosure Meaning of other operating revenues for non finance companies Where should Profit on Sale of Fixed Assets be classified Other Operating Revenue/ Other Income? Should the net gains arising on foreign exchange fluctuations be included under the head Other Operating Revenues or Other Income? Disclosure of value of imports and expenditure in foreign currency whether accrual or cash? Does Small and Medium Company as defined under Companies (Accounting Standards) Rules, 2006 need to disclose Diluted EPS?

36 Key Issues Takeaways Comparative Numbers To commence exercise of validating previous year numbers in Revised Schedule VI Format Changes to be made MIS/ IT systems to collate information of current/ non current portions of each asset and liabilities Break up of Employee Benefit Liabilities in Current and Non Current to be obtained from Independent Actuary. Review Loan Agreements to avoid becoming current liability in case of non compliance of minor clauses Additional time and efforts for the Companies and Auditors to understand and implement changes Use of judgment to maintain balance between excessive information and over aggregation

37 Differential Comparison SN Particular Existing Revised 1 Net Working Capital Current assets and Liabilities are shown together under application of funds. Net Working Capital appears on balance sheet Assets & Liabilities are to be bifurcated into current & Non current and shown separately. Hence, Net Working Capital will not be appearing in Balance sheet 2 Fixed Assets No bifurcation required into Tangible & Intangible assets 3 Borrowings Short term & long term borrowings are grouped together under the head Loan funds sub head Secured/ Unsecured Fixed assets to be shown under non current assets and it has to be bifurcated in to Tangible & Intangible assets Long term borrowings to be shown under non current liabilities and short term borrowings to be shown under current liabilities with separate disclosure of secured/ unsecured loans. Period and amount of continuing default as on the balance sheet date in repayment py of loans and interest to be separately specified

38 Differential Comparison SN Particular Existing Revised 4 Finance lease obligation Finance lease obligations are included in current liabilities Finance lease obligations are to be grouped under the head non current Liabilities 5 Deposits Lease deposits are part of loans & Lease deposits to be disclosed as long advances term loans & advances under the head non current assets 6 Investments Both current & non current investments to be disclosed under the head investments Current and non current investments are to be disclosed separately under current assets & non current assets respectively 7 Loans & Advances Loans & Advances are disclosed along with current assets Loans & Advance to subsidiaries & others to be disclosed separately Loans & Advances to be broken up in long term & short term and to be disclosed under non current & current assets respectively. Loans & Advance from related parties & others to be disclosed separately.

39 Differential Comparison SN Particular Existing Revised 8 DTA/ DTL Deferred Tax assets/ liabilities to be disclosed separately DTA/ DTL to be disclosed under non current assets/ liabilities as applicable 9 Cash & Bank Balances 10 Profit & Loss (Dr Balance) Bank balance to be bifurcated in scheduled banks & others P&L debit balance to be shown under the head Miscellaneous expenditure & losses Bank balances in relation to earmarked balances, held as margin money, deposits with more than 12 months maturity, each to be shown Separately. Debit balance of Profit and Loss Account to be shown as negative figure under the head Surplus. Therefore, reserve & surplus balance can be negative 11 Format A company has an option to use horizontal format for presentation of financial statements. A company will not have option to use horizontal format for presentation of financial statements.

40 Differential Comparison SN Particular Existing Revised 13 Other current No separate disclosure of Current Current maturities of long term debt to liabilities maturities of long term debt. No separate disclosure of Current maturities of finance lease Obligation be disclosed under other current Liabilities. Current maturities of finance lease obligation to be disclosed 14 Purchases Purchases, Opening & closing stock, Goods traded din by the company to be giving break up in respect of each class of goods traded in indicating the quantities thereof disclosed in broad heads notes. Disclosure of quantitative details of goods is much diluted. 15 Expense Function wise & Nature wise Classification based on nature of Classification in P & L expenses A/c. 16 Finance Cost To be classified in fixed loans & other loans To be classified as interest expense, other borrowing costs & Gain/ Loss on forex transactions/ translations. 17 Foreign exchange gain/ loss Gain/ Loss on foreign currency transaction to be shown under finance cost Gain/ Loss on foreign currency transaction to be separated into finance costs and other expenses

41 THANKS

Welcome to Presentation on preparation of financial statements under revised schedule VI. K.Chandra Sekhar Company Secretary Ace Designers Limited

Welcome to Presentation on preparation of financial statements under revised schedule VI K.Chandra Sekhar Company Secretary Ace Designers Limited 1 Relevant provisions Indian Companies Act, 1956 Rules

Welcome to Presentation on preparation of financial statements under revised schedule VI K.Chandra Sekhar Company Secretary Ace Designers Limited 1 Relevant provisions Indian Companies Act, 1956 Rules

26 th Regional Conference of WIRC. Revised Schedule VI. CA N. Venkatram 16th December, 2011

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory. Revised Schedule VI. By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA]

![KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory. Revised Schedule VI. By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA]](/thumbs/78/78547575.jpg "KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory. Revised Schedule VI. By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA]") KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory Revised Schedule VI By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA] Introduction Old Schedule VI had outlived its utility; Revised Schedule VI

KGMA IFRS Audit & Assurance FEMA Valuation Corporate Advisory Revised Schedule VI By: CA Kamal Garg [FCA, DISA(ICAI), LLB, MBA] Introduction Old Schedule VI had outlived its utility; Revised Schedule VI

Revised Schedule VI. By: Purushottam Nyati Mukul Rathi. July 27, Page 1

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

Index. 97 b) Comparison of Old and Revised Schedule VI 98. Illustrative list of disclosures required under Companies Act, 1956

Comparison of Old and Revised Schedule VI 98. Illustrative list of disclosures required under Companies Act, 1956") Index S.No. Contents Page No. 1. Introduction 3 2. Objective and Scope 3 3. Applicability 4 4. Summary of the Revised Schedule VI 4 5. Structure of the Revised Schedule VI 10 6. General Instructions to

Index S.No. Contents Page No. 1. Introduction 3 2. Objective and Scope 3 3. Applicability 4 4. Summary of the Revised Schedule VI 4 5. Structure of the Revised Schedule VI 10 6. General Instructions to

REVISED SCHEDULE VI Detailed Analysis with Practical Approach

REVISED SCHEDULE VI Detailed Analysis with Practical Approach By: 28.04.2012 1 SESSION I: o EXISTING PROVISIONS o REVISED SCHEDULE VI o AN OVERVIEW o OVERALL APPROACH o KEY CHANGES B/S o KEY CHANGES P&L

REVISED SCHEDULE VI Detailed Analysis with Practical Approach By: 28.04.2012 1 SESSION I: o EXISTING PROVISIONS o REVISED SCHEDULE VI o AN OVERVIEW o OVERALL APPROACH o KEY CHANGES B/S o KEY CHANGES P&L

Reporting Under Revised Schedule VI of. A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA

CA AKSHAY K GUPTA") Reporting Under Revised Schedule VI of Companies Act 1956 A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA 1 The Ministry of Corporate Affairs (MCA) on Tuesday, the 1st day of March notified

Reporting Under Revised Schedule VI of Companies Act 1956 A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA 1 The Ministry of Corporate Affairs (MCA) on Tuesday, the 1st day of March notified

REVISED SCHEDULE VI. By : CA Kusai Goawala

REVISED SCHEDULE VI By : CA Kusai Goawala Old Schedule VI was operative from 1956. Outdated format for Balance Sheet replaced Revised Schedule VI is a step towards convergence with IFRS Based on IAS1 or

REVISED SCHEDULE VI By : CA Kusai Goawala Old Schedule VI was operative from 1956. Outdated format for Balance Sheet replaced Revised Schedule VI is a step towards convergence with IFRS Based on IAS1 or

CAPITAL FIRST SECURITIES LIMITED BALANCE SHEET AS AT MARCH 31, 2017

BALANCE SHEET AS AT MARCH 31, 2017 Note As at Amount in Rupees As at EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 673,556,000 673,556,000 Reserves and Surplus 4 (195,051,527) (338,181,529)

BALANCE SHEET AS AT MARCH 31, 2017 Note As at Amount in Rupees As at EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 673,556,000 673,556,000 Reserves and Surplus 4 (195,051,527) (338,181,529)

CAPITAL FIRST SECURITIES LIMITED BALANCE SHEET AS AT MARCH 31, 2018

BALANCE SHEET AS AT MARCH 31, 2018 Note EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 673,556,000 673,556,000 Reserves and Surplus 4 (18,500,638) (195,051,527) 655,055,362 478,504,473 Non

BALANCE SHEET AS AT MARCH 31, 2018 Note EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 673,556,000 673,556,000 Reserves and Surplus 4 (18,500,638) (195,051,527) 655,055,362 478,504,473 Non

HIMANSHU KISHNADWALA 8 AUGUST 2012

HIMANSHU KISHNADWALA 8 AUGUST 2012 CNK 1 1. Format / disclosures Revised Schedule VI 2. Disclosures as per notified Accounting Standards (i.e. Companies AS Rules, 2006) 3. Disclosures as per Companies

HIMANSHU KISHNADWALA 8 AUGUST 2012 CNK 1 1. Format / disclosures Revised Schedule VI 2. Disclosures as per notified Accounting Standards (i.e. Companies AS Rules, 2006) 3. Disclosures as per Companies

RELIANCE SIBUR ELASTOMERS PRIVATE LIMITED 1. Reliance Sibur Elastomers Private Limited

RELIANCE SIBUR ELASTOMERS PRIVATE LIMITED 1 Reliance Sibur Elastomers Private Limited 2 RELIANCE SIBUR ELASTOMERS PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE SIBUR ELASTOMERS

RELIANCE SIBUR ELASTOMERS PRIVATE LIMITED 1 Reliance Sibur Elastomers Private Limited 2 RELIANCE SIBUR ELASTOMERS PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE SIBUR ELASTOMERS

RELIANCE JIO ASIAINFO INNOVATION CENTRE LIMITED 1. Reliance Jio Asia Info Innovation Centre Limited

RELIANCE JIO ASIAINFO INNOVATION CENTRE LIMITED 1 Reliance Jio Asia Info Innovation Centre Limited 2 RELIANCE JIO ASIAINFO INNOVATION CENTRE LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE

RELIANCE JIO ASIAINFO INNOVATION CENTRE LIMITED 1 Reliance Jio Asia Info Innovation Centre Limited 2 RELIANCE JIO ASIAINFO INNOVATION CENTRE LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE

SPC Co. Ltd Sudan BALANCE SHEET AS AT Mar 31, 2016

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 b) Reserves and Surplus 2 (936) (936) (936) (936) 2. Minority Interest 3. Share application

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 b) Reserves and Surplus 2 (936) (936) (936) (936) 2. Minority Interest 3. Share application

Company ), explanatory. information. under. our audit. the Act.

, explanatory. information. under. our audit. the Act.") Independent Auditor s Report To the Members of M/ /s. Future Trendz Limited Report on the Standalone Ind AS Financial Statements We have audited the standalone Ind AS Financial Statements of Future Trendz

Independent Auditor s Report To the Members of M/ /s. Future Trendz Limited Report on the Standalone Ind AS Financial Statements We have audited the standalone Ind AS Financial Statements of Future Trendz

Outline Guidance Notes regarding adoption of CLASS XII Revised Schedule VI to the Companies Act 1956 in the subject of Accountancy (Effective for Board Examination 2013) Shiksha Kendra, 2, Community Centre,

Outline Guidance Notes regarding adoption of CLASS XII Revised Schedule VI to the Companies Act 1956 in the subject of Accountancy (Effective for Board Examination 2013) Shiksha Kendra, 2, Community Centre,

RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

RRB MEDIASOFT PRIVATE LIMITED 1 RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 RRB MEDIASOFT PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RRB MEDIASOFT PRIVATE LIMITED

RRB MEDIASOFT PRIVATE LIMITED 1 RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 RRB MEDIASOFT PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RRB MEDIASOFT PRIVATE LIMITED

WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

WATERMARK INFRATECH PRIVATE LIMITED 1 WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 WATERMARK INFRATECH PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF WATERMARK INFRATECH

WATERMARK INFRATECH PRIVATE LIMITED 1 WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 WATERMARK INFRATECH PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF WATERMARK INFRATECH

REVISED OUTLINE GUIDANCE NOTES

REVISED OUTLINE GUIDANCE NOTES regarding adoption of Schedule VI to the Companies Act 1956 in the subject of ACCOUNTANCY Class XII For the Board Examination, March 2014 1 CONTENT Chapter 1: GENERAL INTRODUCTION

REVISED OUTLINE GUIDANCE NOTES regarding adoption of Schedule VI to the Companies Act 1956 in the subject of ACCOUNTANCY Class XII For the Board Examination, March 2014 1 CONTENT Chapter 1: GENERAL INTRODUCTION

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

BALANCE SHEET AS AT MARCH 31, 2018 Amount in Rupees. Note

BALANCE SHEET AS AT MARCH 31, 2018 Note EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 283,250,000 283,250,000 Reserves and Surplus 4 85,569,492 64,402,076 368,819,492 347,652,076 Current Liabilities

BALANCE SHEET AS AT MARCH 31, 2018 Note EQUITY AND LIABILITIES Shareholders' Funds Share Capital 3 283,250,000 283,250,000 Reserves and Surplus 4 85,569,492 64,402,076 368,819,492 347,652,076 Current Liabilities

ADVENTURE MARKETING PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

1 ANNUAL ACCOUNTS - FY : 2016-17 2 Independent Auditor s Report TO THE MEMBERS OF Report on the Financial Statements We have audited the accompanying financial statements of Adventure Marketing Private

1 ANNUAL ACCOUNTS - FY : 2016-17 2 Independent Auditor s Report TO THE MEMBERS OF Report on the Financial Statements We have audited the accompanying financial statements of Adventure Marketing Private

Strides Pharma Namibia BALANCE SHEET AS AT Mar 31, 2016

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 1,777,104 1,777,104 b) Reserves and Surplus 2 (485,737) 1,490,552 1,291,367 3,267,656 2. Share

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 1,777,104 1,777,104 b) Reserves and Surplus 2 (485,737) 1,490,552 1,291,367 3,267,656 2. Share

Strides Pharma Cameroon BALANCE SHEET AS AT Mar 31, 2016

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 10,000,000 10,000,000 b) Reserves and Surplus 2 10,000,000 10,000,000 2. Share application

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 10,000,000 10,000,000 b) Reserves and Surplus 2 10,000,000 10,000,000 2. Share application

Capsule on Accounting Standards

Capsule on Accounting Standards Conducted by Young Members Empowerment Committee jointly with Accounting Standards Board Presented by CA Manish C. Iyer, Deputy Director, Technical Directorate, ICAI 1 Standards

Capsule on Accounting Standards Conducted by Young Members Empowerment Committee jointly with Accounting Standards Board Presented by CA Manish C. Iyer, Deputy Director, Technical Directorate, ICAI 1 Standards

2. Management s Responsibility for the Ind AS Financial Statements

Independent Auditor s Report To the Members of 1. Report on the Ind AS Financial Statements We have audited the accompanying Ind AS financial statements of ( the Company ), which comprise the Balance Sheet

Independent Auditor s Report To the Members of 1. Report on the Ind AS Financial Statements We have audited the accompanying Ind AS financial statements of ( the Company ), which comprise the Balance Sheet

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 1 WIPRO TECHNOLOGIES SPAIN BALANCE SHEET AS AT MARCH 31, (Amount in INR, except share and per share data,

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 1 WIPRO TECHNOLOGIES SPAIN BALANCE SHEET AS AT MARCH 31, (Amount in INR, except share and per share data,

RELIANCE JIO MESSAGING SERVICES PRIVATE LIMITED 1. Reliance Jio Messaging Services Private Limited

RELIANCE JIO MESSAGING SERVICES PRIVATE LIMITED 1 Reliance Jio Messaging Services Private Limited 2 RELIANCE JIO MESSAGING SERVICES PRIVATE LIMITED Independent Auditor s Report To The Members Of Reliance

RELIANCE JIO MESSAGING SERVICES PRIVATE LIMITED 1 Reliance Jio Messaging Services Private Limited 2 RELIANCE JIO MESSAGING SERVICES PRIVATE LIMITED Independent Auditor s Report To The Members Of Reliance

(All amount are stated in Indian Rupees, unless stated otherwise) Particulars I. EQUITY AND LIABILITIES

Particulars I. EQUITY AND LIABILITIES") Balance Sheet as at 31st March 2017 I. EQUITY AND LIABILITIES Note No. 31 March 2017 31 March 2016 1 Shareholders funds (a) Share Capital 3 1,99,92,000 1,99,92,000 (b) Reserves and Surplus 4 10,07,74,946

Balance Sheet as at 31st March 2017 I. EQUITY AND LIABILITIES Note No. 31 March 2017 31 March 2016 1 Shareholders funds (a) Share Capital 3 1,99,92,000 1,99,92,000 (b) Reserves and Surplus 4 10,07,74,946

SAIBA Industries Private Limited Financials FY

SAIBA Industries Private Limited Financials FY -2016-17 Independent Auditor s Report To the Members of Saiba Industries Private Limited Report on the Standalone Ind AS Financial Statements We have audited

SAIBA Industries Private Limited Financials FY -2016-17 Independent Auditor s Report To the Members of Saiba Industries Private Limited Report on the Standalone Ind AS Financial Statements We have audited

GREYCELLS18 MEDIA LIMITED ANNUAL ACCOUNTS - FY :

GREYCELLS18 MEDIA LIMITED 1 GREYCELLS18 MEDIA LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 GREYCELLS18 MEDIA LIMITED Independent Auditor s Report TO THE MEMBERS OF GREYCELLS18 MEDIA LIMITED Report on the Financial

GREYCELLS18 MEDIA LIMITED 1 GREYCELLS18 MEDIA LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 GREYCELLS18 MEDIA LIMITED Independent Auditor s Report TO THE MEMBERS OF GREYCELLS18 MEDIA LIMITED Report on the Financial

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1. Reliance Clothing India Private Limited

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1 Reliance Clothing India Private Limited 2 RELIANCE CLOTHING INDIA PRIVATE LIMITED INDEPENDENT AUDITOR S REPORT To the Members of Reliance Clothing India Private

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1 Reliance Clothing India Private Limited 2 RELIANCE CLOTHING INDIA PRIVATE LIMITED INDEPENDENT AUDITOR S REPORT To the Members of Reliance Clothing India Private

BSE INSTITUTE LIMITED

Public BSE INSTITUTE LIMITED ANNUAL ACCOUNTS FY 2017-18 BSE INSTITUTE LIMITED INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF BSE INSTITUTE LIMITED Report on the Standalone Financial Statements We have

Public BSE INSTITUTE LIMITED ANNUAL ACCOUNTS FY 2017-18 BSE INSTITUTE LIMITED INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF BSE INSTITUTE LIMITED Report on the Standalone Financial Statements We have

Independent Auditor s Report. To the Members of Jubilant Innovation India Limited. 1. Report on the Ind AS Financial Statements

Independent Auditor s Report To the Members of Jubilant Innovation India Limited 1. Report on the Ind AS Financial Statements We have audited the accompanying Ind AS financial statements of Jubilant Innovation

Independent Auditor s Report To the Members of Jubilant Innovation India Limited 1. Report on the Ind AS Financial Statements We have audited the accompanying Ind AS financial statements of Jubilant Innovation

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

INDEPENDENT AUDITOR'S REPORT

To the Members of MONETA FINANCE PRIVATE LIMITED INDEPENDENT AUDITOR'S REPORT 1. Report on the Ind AS Financial Statements We have audited the accompanying Indian Accounting Standards (Ind AS) financial

To the Members of MONETA FINANCE PRIVATE LIMITED INDEPENDENT AUDITOR'S REPORT 1. Report on the Ind AS Financial Statements We have audited the accompanying Indian Accounting Standards (Ind AS) financial

(a) in the case of the Balance Sheet, of the state of affairs of the Company as at March 31, 2014;

in the case of the Balance Sheet, of the state of affairs of the Company as at March 31, 2014;") Independent Auditor s Report To the Members of Capital First Commodities Limited Report on the Financial Statements We have audited the accompanying financial statements of Capital First Commodities Limited

Independent Auditor s Report To the Members of Capital First Commodities Limited Report on the Financial Statements We have audited the accompanying financial statements of Capital First Commodities Limited

Companies (Auditor s Report) Order, 2016 Key changes. CA T.V.Ganesh

Order, 2016 Key changes. CA T.V.Ganesh") Companies (Auditor s Report) Order, 2016 CA T.V.Ganesh 1 CARO 2016 notified Applicable for all financial years beginning on or after April 1, Does not apply to consolidated financial statements Changes

Companies (Auditor s Report) Order, 2016 CA T.V.Ganesh 1 CARO 2016 notified Applicable for all financial years beginning on or after April 1, Does not apply to consolidated financial statements Changes

RELIANCE UNIVERSAL COMMERCIAL LIMITED 1. Reliance Universal Commercial Limited

RELIANCE UNIVERSAL COMMERCIAL LIMITED 1 Reliance Universal Commercial Limited 2 RELIANCE UNIVERSAL COMMERCIAL LIMITED Independent Auditor s Report To the Members of Reliance Universal Commercial Limited

RELIANCE UNIVERSAL COMMERCIAL LIMITED 1 Reliance Universal Commercial Limited 2 RELIANCE UNIVERSAL COMMERCIAL LIMITED Independent Auditor s Report To the Members of Reliance Universal Commercial Limited

WIPRO PROMAX ANALYTICS SOLUTIONS LLC FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO PROMAX ANALYTICS SOLUTIONS LLC FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO PROMAX ANALYTICS SOLUTIONS LLC BALANCE SHEET (Amount in ` except share and per share data,

WIPRO PROMAX ANALYTICS SOLUTIONS LLC FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO PROMAX ANALYTICS SOLUTIONS LLC BALANCE SHEET (Amount in ` except share and per share data,

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

YES SECURITIES (INDIA) LIMITED. Audited Financial Statements for the year ended March 31, 2015

LIMITED. Audited Financial Statements for the year ended March 31, 2015") YES SECURITIES (INDIA) LIMITED Audited Financial Statements for the year ended March 31, 2015 Independent Auditors Report To the Members of YES Securities (India) Limited Report on the financial statements

YES SECURITIES (INDIA) LIMITED Audited Financial Statements for the year ended March 31, 2015 Independent Auditors Report To the Members of YES Securities (India) Limited Report on the financial statements

Jubilant Draximage Limited Balance Sheet as at 31 March 2017 (INR in thousands) As at 31 March 2017

As at 31 March 2017") Balance Sheet as at Notes 1 April 2015 ASSETS Non-current assets Property, plant and equipment 3 498 626 159 Other intangible assets 4 - - 2 Financial assets i. Loans 5(b) 82 37 22 ii. Other financial

Balance Sheet as at Notes 1 April 2015 ASSETS Non-current assets Property, plant and equipment 3 498 626 159 Other intangible assets 4 - - 2 Financial assets i. Loans 5(b) 82 37 22 ii. Other financial

BSE SAMMAAN CSR LIMITED

Public BSE SAMMAAN CSR LIMITED ANNUAL ACCOUNTS FY 2017-18 BSE SAMMAAN CSR LIMITED INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF BSE SAMMAAN CSR LIMITED Report on the Financial Statements We have audited

Public BSE SAMMAAN CSR LIMITED ANNUAL ACCOUNTS FY 2017-18 BSE SAMMAAN CSR LIMITED INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF BSE SAMMAAN CSR LIMITED Report on the Financial Statements We have audited

GOVERNMENT OF INDIA Ministry of Corporate Affairs

GOVERNMENT OF INDIA Ministry of Corporate Affairs NOTICE INVITING COMMENTS ON THE REVISED SCHEDULE III TO THE COMPANIES ACT, 2013 FOR A COMPANY WHOSE FINANCIAL STATEMENTS ARE DRAWN UP IN COMPLIANCE OF

GOVERNMENT OF INDIA Ministry of Corporate Affairs NOTICE INVITING COMMENTS ON THE REVISED SCHEDULE III TO THE COMPANIES ACT, 2013 FOR A COMPANY WHOSE FINANCIAL STATEMENTS ARE DRAWN UP IN COMPLIANCE OF

RELIANCE-GRANDOPTICAL PRIVATE LIMITED 1. Reliance-GrandOptical Private Limited

RELIANCE-GRANDOPTICAL PRIVATE LIMITED 1 Reliance-GrandOptical Private Limited 2 RELIANCE-GRANDOPTICAL PRIVATE LIMITED INDEPENDENT AUDITOR S REPORT To the Members of Reliance-Grand Optical Private Limited

RELIANCE-GRANDOPTICAL PRIVATE LIMITED 1 Reliance-GrandOptical Private Limited 2 RELIANCE-GRANDOPTICAL PRIVATE LIMITED INDEPENDENT AUDITOR S REPORT To the Members of Reliance-Grand Optical Private Limited

DEEPAK PHENOLICS LIMITED (Formerly known as Deepak Clean Tech Limited ) Balance Sheet as at March 31, 2016 As at March 31, 2016

Balance Sheet as at March 31, 2016 As at March 31, 2016") DEEPAK PHENOLICS LIMITED (Formerly known as Deepak Clean Tech Limited ) Balance Sheet as at Note No. I. EQUITY AND LIABILITIES Shareholders Funds Share Capital 2 6,184.41 1,405.00 Reserves and Surplus

DEEPAK PHENOLICS LIMITED (Formerly known as Deepak Clean Tech Limited ) Balance Sheet as at Note No. I. EQUITY AND LIABILITIES Shareholders Funds Share Capital 2 6,184.41 1,405.00 Reserves and Surplus

RELIANCE RETAIL FINANCE LIMITED 1. Reliance Retail Finance Limited

RELIANCE RETAIL FINANCE LIMITED 1 Reliance Retail Finance Limited 2 RELIANCE RETAIL FINANCE LIMITED Independent Auditor s Report To the Members of Reliance Retail Finance Limited Report on the Financial

RELIANCE RETAIL FINANCE LIMITED 1 Reliance Retail Finance Limited 2 RELIANCE RETAIL FINANCE LIMITED Independent Auditor s Report To the Members of Reliance Retail Finance Limited Report on the Financial

CAPITAL18 FINCAP PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

89 CAPITAL18 FINCAP PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2017-18 90 CAPITAL18 FINCAP PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF CAPITAL18 FINCAP PRIVATE LIMITED Report on the Standalone

89 CAPITAL18 FINCAP PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2017-18 90 CAPITAL18 FINCAP PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF CAPITAL18 FINCAP PRIVATE LIMITED Report on the Standalone

IRDA Public Disclosures

IRDA Public Disclosures QUARTER ENDED 31ST MARCH 2015 Aviva Life Insurance Company India Limited S. No. Form No. Description Page No. 1 L-1 REVENUE ACCOUNT 1-2 2 L-2 PROFIT & LOSS ACCOUNT 3 3 L-3 BALANCE

IRDA Public Disclosures QUARTER ENDED 31ST MARCH 2015 Aviva Life Insurance Company India Limited S. No. Form No. Description Page No. 1 L-1 REVENUE ACCOUNT 1-2 2 L-2 PROFIT & LOSS ACCOUNT 3 3 L-3 BALANCE

552 INFOMEDIA PRESS LIMITED INFOMEDIA PRESS LIMITED ANNUAL ACCOUNTS - FY :

552 ANNUAL ACCOUNTS - FY : 2017-18 553 Independent Auditor s Report To the Members of Infomedia Press Limited Report on the Ind AS Financial Statements We have audited the accompanying Ind AS financial

552 ANNUAL ACCOUNTS - FY : 2017-18 553 Independent Auditor s Report To the Members of Infomedia Press Limited Report on the Ind AS Financial Statements We have audited the accompanying Ind AS financial

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES NORWAY AS BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated)

WIPRO TECHNOLOGIES NORWAY AS FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES NORWAY AS BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated)

Total Non-Current Assets 11,052,694 7,819,990

Balance Sheet as at Notes As at As at ASSETS Non-current Assets Property Plant and Equipment ('PPE') 3 6,074,314 2,513,990 Financial Assets (i) Other Financial Assets 4 4,978,380 4,386,000 Other Non-current

Balance Sheet as at Notes As at As at ASSETS Non-current Assets Property Plant and Equipment ('PPE') 3 6,074,314 2,513,990 Financial Assets (i) Other Financial Assets 4 4,978,380 4,386,000 Other Non-current

RELIANCE TEXTILES LIMITED FINANCIAL STATEMENTS FY

RELIANCE TEXTILES LIMITED 1 RELIANCE TEXTILES LIMITED FINANCIAL STATEMENTS FY 2016-17 2 RELIANCE TEXTILES LIMITED Independent Auditor s Report To The Members of Reliance Textiles Limited Report on the

RELIANCE TEXTILES LIMITED 1 RELIANCE TEXTILES LIMITED FINANCIAL STATEMENTS FY 2016-17 2 RELIANCE TEXTILES LIMITED Independent Auditor s Report To The Members of Reliance Textiles Limited Report on the

Balance Sheet as at March 31, 2015 (All amounts in Indian Rupees Million)

") Balance Sheet as at (All amounts in Indian Rupees Million) Notes EQUITY AND LIABILITIES Shareholders funds Share capital 3 1,991 261 Reserves and surplus 4 6,458 6,332 8,449 6,593 Non - current liabilities

Balance Sheet as at (All amounts in Indian Rupees Million) Notes EQUITY AND LIABILITIES Shareholders funds Share capital 3 1,991 261 Reserves and surplus 4 6,458 6,332 8,449 6,593 Non - current liabilities

Jubilant Infrastructure Limited Ind AS financial statements March 2017

Ind AS financial statements March 2017 Balance Sheet as at Notes 1 April 2015 ASSETS Non-current assets Property, plant and equipment 3 1,459,327 1,354,722 1,227,256 Capital work-in-progress 3 11,073 24,708

Ind AS financial statements March 2017 Balance Sheet as at Notes 1 April 2015 ASSETS Non-current assets Property, plant and equipment 3 1,459,327 1,354,722 1,227,256 Capital work-in-progress 3 11,073 24,708

Note No. TOTAL 23,615,211,006 7,073,089,104. ASSETS Non - Current Assets Fixed assets - Tangible assets 13 1,947,384-1,947,384 -

BALANCE SHEET AS AT MARCH 31, 2018 Note No. EQUITY AND LIABILITIES Shareholders' Funds Share capital 3 1,377,330,790 663,045,150 Reserves and surplus 4 642,359,050 251,549,782 2,019,689,840 914,594,932

BALANCE SHEET AS AT MARCH 31, 2018 Note No. EQUITY AND LIABILITIES Shareholders' Funds Share capital 3 1,377,330,790 663,045,150 Reserves and surplus 4 642,359,050 251,549,782 2,019,689,840 914,594,932

WEB18 SOFTWARE SERVICES LIMITED 1. Web18 Software Services Limited

WEB18 SOFTWARE SERVICES LIMITED 1 Web18 Software Services Limited 2 WEB18 SOFTWARE SERVICES LIMITED Independent Auditor s Report To the Members of Web18 Software Services Limited Report on the Financial

WEB18 SOFTWARE SERVICES LIMITED 1 Web18 Software Services Limited 2 WEB18 SOFTWARE SERVICES LIMITED Independent Auditor s Report To the Members of Web18 Software Services Limited Report on the Financial

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016)

") Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) Objectives 1. Multiple Choice Questions: (i) Dido Ltd. deals in three products, and, which are neither similar nor interchangeable.

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) Objectives 1. Multiple Choice Questions: (i) Dido Ltd. deals in three products, and, which are neither similar nor interchangeable.

3. Our responsibility is to express an opinion on these financial statements based on our audit.

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF Report on the Financial Statements 1. We have audited the accompanying financial statements of ( the Company ), which comprise the Balance Sheet as at March

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF Report on the Financial Statements 1. We have audited the accompanying financial statements of ( the Company ), which comprise the Balance Sheet as at March

P r a t i m a B h i n g e & A s s o c i a t e C h a r t e r e d A c c o u n t a n t s

P r a t i m a B h i n g e & A s s o c i a t e C h a r t e r e d A c c o u n t a n t s Head Office: 606, 7 th Floor, Stellar Spaces, Opposite Zensar Technologies Ltd., Kharadi, Pune 14 INDEPENDENT AUDITOR

P r a t i m a B h i n g e & A s s o c i a t e C h a r t e r e d A c c o u n t a n t s Head Office: 606, 7 th Floor, Stellar Spaces, Opposite Zensar Technologies Ltd., Kharadi, Pune 14 INDEPENDENT AUDITOR

EQUITY AND LIABILITIES Equity Equity share capital Other equity (525) (1,844) Total Equity 963 (237) (1,556)

(1,844) Total Equity 963 (237) (1,556)") Balance sheet as at March 31, 2017 Notes As at As at As at March 31, 2017 March 31, 2016 April 1, 2015 ASSETS Non-current assets Property, plant and equipment 3 4,329 4,179 4,274 Capital work-in-progress

Balance sheet as at March 31, 2017 Notes As at As at As at March 31, 2017 March 31, 2016 April 1, 2015 ASSETS Non-current assets Property, plant and equipment 3 4,329 4,179 4,274 Capital work-in-progress

Jubilant First Trust Healthcare Limited Balance Sheet as at 31 March 2016

Balance Sheet as at 31 March 2016 (Rs. '000) Note As at 31 March 2016 As at 31 March 2015 EQUITY AND LIABILITIES Shareholder's funds Share capital 2 20,500 156,132 Reserves and surplus 3 46,622 581,899

Balance Sheet as at 31 March 2016 (Rs. '000) Note As at 31 March 2016 As at 31 March 2015 EQUITY AND LIABILITIES Shareholder's funds Share capital 2 20,500 156,132 Reserves and surplus 3 46,622 581,899

Overview of Transition to IND-AS. CA Sanjeev Maheshwari

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

MONEYCONTROL DOT COM INDIA LIMITED 1. MoneyControl Dot Com India Limited

MONEYCONTROL DOT COM INDIA LIMITED 1 MoneyControl Dot Com India Limited 2 MONEYCONTROL DOT COM INDIA LIMITED Independent Auditor s Report To the Members of Moneycontrol Dot Com India Limited Report on

MONEYCONTROL DOT COM INDIA LIMITED 1 MoneyControl Dot Com India Limited 2 MONEYCONTROL DOT COM INDIA LIMITED Independent Auditor s Report To the Members of Moneycontrol Dot Com India Limited Report on

Siemens Rail Automation Private Limited. Audited Financial Statements for the financial year ended 30 th September, 2017

Audited Financial Statements for the financial year ended 30 th September, 2017 CIN: U31200MH2003PTC259831 Registered Office: Plot No. 2, Sector No. 2, Kharghar Node, Navi Mumbai 410210 Telephone +91 22

Audited Financial Statements for the financial year ended 30 th September, 2017 CIN: U31200MH2003PTC259831 Registered Office: Plot No. 2, Sector No. 2, Kharghar Node, Navi Mumbai 410210 Telephone +91 22

Notes. Shareholders funds Share capital 1 8,600,000 8,600,000 Reserves and surplus 2 1,357,851,494 1,313,331,058 1,366,451,494 1,321,931,058

Balance Sheet as at March 31st, 2015 Notes I. EQUITY AND LIABILITIES Shareholders funds Share capital 1 8,600,000 8,600,000 Reserves and surplus 2 1,357,851,494 1,313,331,058 1,366,451,494 1,321,931,058

Balance Sheet as at March 31st, 2015 Notes I. EQUITY AND LIABILITIES Shareholders funds Share capital 1 8,600,000 8,600,000 Reserves and surplus 2 1,357,851,494 1,313,331,058 1,366,451,494 1,321,931,058

SPACEBOUND WEB LABS PRIVATE LIMITED 1. SpaceBound Web Labs Private Limited

SPACEBOUND WEB LABS PRIVATE LIMITED 1 SpaceBound Web Labs Private Limited 2 SPACEBOUND WEB LABS PRIVATE LIMITED INDEPENDENT AUDITORS REPORT To The Members Of Spacebound Web labs Private limited., Report

SPACEBOUND WEB LABS PRIVATE LIMITED 1 SpaceBound Web Labs Private Limited 2 SPACEBOUND WEB LABS PRIVATE LIMITED INDEPENDENT AUDITORS REPORT To The Members Of Spacebound Web labs Private limited., Report

RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED FINANCIAL STATEMENTS

RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED 1231 RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED FINANCIAL STATEMENTS 2017-18 1232 RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED

RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED 1231 RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED FINANCIAL STATEMENTS 2017-18 1232 RELIANCE EMINENT TRADING & COMMERCIAL PRIVATE LIMITED

2636 SURELA INVESTMENT & TRADING PRIVATE LIMITED SURELA INVESTMENT & TRADING PRIVATE LIMITED FINANCIAL STATEMENTS

2636 SURELA INVESTMENT & TRADING PRIVATE LIMITED SURELA INVESTMENT & TRADING PRIVATE LIMITED FINANCIAL STATEMENTS 2017-18 SURELA INVESTMENT & TRADING PRIVATE LIMITED 2637 INDEPENDENT AUDITOR S REPORT TO

2636 SURELA INVESTMENT & TRADING PRIVATE LIMITED SURELA INVESTMENT & TRADING PRIVATE LIMITED FINANCIAL STATEMENTS 2017-18 SURELA INVESTMENT & TRADING PRIVATE LIMITED 2637 INDEPENDENT AUDITOR S REPORT TO

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES AS 1 Disclosure of Accounting Policies Still few enterprises mention in their accounting policy, accounts are prepared on going concern and accounts

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES AS 1 Disclosure of Accounting Policies Still few enterprises mention in their accounting policy, accounts are prepared on going concern and accounts

A Practitioner's Guide

Revised Schedule VI : A Practitioner's Guide Committee for Capacity Building of CA Firms and Small & Medium Practitioners (CCBCAF & SMP) The Institute of Chartered Accountants of India (Set up by an Act

Revised Schedule VI : A Practitioner's Guide Committee for Capacity Building of CA Firms and Small & Medium Practitioners (CCBCAF & SMP) The Institute of Chartered Accountants of India (Set up by an Act

NOTES TO FINANCIAL STATEMENTS for the year ended March 31, 2016

Financial Statements Standalone 92 for the year ended March 31, 2016 NOTE 1. CORPORATE INFORMATION Bharat Forge Limited ( the Company ) is a public company domiciled in India. Its shares and debentures

Financial Statements Standalone 92 for the year ended March 31, 2016 NOTE 1. CORPORATE INFORMATION Bharat Forge Limited ( the Company ) is a public company domiciled in India. Its shares and debentures

ISSUES ON ACCOUNTING STANDARDS (AS 15, 22 & 29) H I M A N S H U K I S H N A D W A L A 1 4 D E C E M B E R

H I M A N S H U K I S H N A D W A L A 1 4 D E C E M B E R") ISSUES ON ACCOUNTING STANDARDS (AS 15, 22 & 29) H I M A N S H U K I S H N A D W A L A 1 4 D E C E M B E R 2 0 1 3 1 AS 15 EMPLOYEE BENEFITS Types of Employee Benefits Payable during Service Payable Post

ISSUES ON ACCOUNTING STANDARDS (AS 15, 22 & 29) H I M A N S H U K I S H N A D W A L A 1 4 D E C E M B E R 2 0 1 3 1 AS 15 EMPLOYEE BENEFITS Types of Employee Benefits Payable during Service Payable Post

Aepona Limited CONDENSED BALANCE SHEET AS AT MARCH 31, 2016

CONDENSED BALANCE SHEET AS AT MARCH 31, 2016 Notes EQUITY AND LIABILITIES Shareholders funds Share capital 1 1,230,620,264 Reserves and surplus 2 (1,137,001,443) (A) 93,618,821 Non- current liabilities

CONDENSED BALANCE SHEET AS AT MARCH 31, 2016 Notes EQUITY AND LIABILITIES Shareholders funds Share capital 1 1,230,620,264 Reserves and surplus 2 (1,137,001,443) (A) 93,618,821 Non- current liabilities

Auditor's Responsibility Our responsibility is to express an opinion on these standalone financial statements based on our audit.

INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF BSE SKILLS LIMITED Report on the Standalone Financial Statements We have audited the accompanying standalone financial statements of BSE Skills Limited ("the

INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF BSE SKILLS LIMITED Report on the Standalone Financial Statements We have audited the accompanying standalone financial statements of BSE Skills Limited ("the

Brinda Exports Ltd F.Y

Independent Auditors Report To the Members of, Brinda Exports Ltd. 1. Report on the IND-AS Financial Statements We have audited the accompanying IND-AS financial statements of Brinda Exports Ltd which

Independent Auditors Report To the Members of, Brinda Exports Ltd. 1. Report on the IND-AS Financial Statements We have audited the accompanying IND-AS financial statements of Brinda Exports Ltd which

Annual Report for the year ended June 30, 2014 FINANCIAL STATEMENTS

Annual Report FINANCIAL STATEMENTS 33 34 Mughal Iron & Steel Industries Limited Annual Report 35 AUDITORS REPORT TO THE MEMBERS We have audited the annexed balance sheet of MUGHAL IRON & STEEL INDUSTRIES

Annual Report FINANCIAL STATEMENTS 33 34 Mughal Iron & Steel Industries Limited Annual Report 35 AUDITORS REPORT TO THE MEMBERS We have audited the annexed balance sheet of MUGHAL IRON & STEEL INDUSTRIES

PAPER 5 : ADVANCED ACCOUNTING

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

Independent Auditor s Report

Independent Auditor s Report To the members of Kotak Forex Brokerage Limited Report on the Financial Statements We have audited the accompanying financial statements of Kotak Forex Brokerage Limited (the

Independent Auditor s Report To the members of Kotak Forex Brokerage Limited Report on the Financial Statements We have audited the accompanying financial statements of Kotak Forex Brokerage Limited (the

EQUITY AND LIABILITIES Equity Equity share capital 14 3,414 3,414 3,414 Other equity 15 9,839 8,533 7,453 Total Equity 13,253 11,947 10,867

Balance sheet as at March 31, 2017 Notes As at As at As at March 31, 2017 March 31, 2016 April 1, 2015 ASSETS Non-current assets Property, plant and equipment 3 3,550 4,391 5,049 Capital work-in-progress

Balance sheet as at March 31, 2017 Notes As at As at As at March 31, 2017 March 31, 2016 April 1, 2015 ASSETS Non-current assets Property, plant and equipment 3 3,550 4,391 5,049 Capital work-in-progress

RELIANCE LNG LIMITED ANNUAL REPORT FY:

RELIANCE LNG LIMITED 1 RELIANCE LNG LIMITED ANNUAL REPORT FY: 2016-17 2 RELIANCE LNG LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE LNG LIMITED Report on the Financial Statements We have

RELIANCE LNG LIMITED 1 RELIANCE LNG LIMITED ANNUAL REPORT FY: 2016-17 2 RELIANCE LNG LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE LNG LIMITED Report on the Financial Statements We have

Arrow Pharma Pte Limited BALANCE SHEET AS AT Mar 31, 2016

BALANCE SHEET AS AT Mar 31, 2016 Schedule Mar16 A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 72,625 b) Reserves and Surplus 2 (360,205) (287,580) 2. Share application money pending

BALANCE SHEET AS AT Mar 31, 2016 Schedule Mar16 A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 72,625 b) Reserves and Surplus 2 (360,205) (287,580) 2. Share application money pending

RELIANCE SUPPLY SOLUTIONS PRIVATE LIMITED

664 1 RELIANCE SUPPLY SOLUTIONS PRIVATE LIMITED 2 Independent Auditor s Report To the Members of Reliance Supply Solutions Private Limited (formerly Office Depot Reliance Supply Solutions Private Limited)

664 1 RELIANCE SUPPLY SOLUTIONS PRIVATE LIMITED 2 Independent Auditor s Report To the Members of Reliance Supply Solutions Private Limited (formerly Office Depot Reliance Supply Solutions Private Limited)

Our responsibility is to express an opinion on these standalone financial statements based on our audit.

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF AIRJET GROUND SERVICES LIMITED Report on the Standalone Financial Statements We have audited the accompanying standalone financial statements of Airjet Ground

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF AIRJET GROUND SERVICES LIMITED Report on the Standalone Financial Statements We have audited the accompanying standalone financial statements of Airjet Ground

RELIANCE CAPITAL ASSET MANAGEMENT LIMITED ANNUAL REPORT

RELIANCE CAPITAL ASSET MANAGEMENT LIMITED ANNUAL REPORT 2010-11 Auditors Report To the Members of Reliance Capital Asset Management Limited We have audited the attached balance sheet of Reliance

RELIANCE CAPITAL ASSET MANAGEMENT LIMITED ANNUAL REPORT 2010-11 Auditors Report To the Members of Reliance Capital Asset Management Limited We have audited the attached balance sheet of Reliance

Persistent Systems France SAS

BALANCE SHEET AS AT MARCH 31, 2015 Note EQUITY AND LIABILITIES Shareholders funds Share capital 1 97,467,000 97,467,000 Reserves and surplus 2 26,912,584 (10,908,264) (A) 124,379,584 86,558,736 Current

BALANCE SHEET AS AT MARCH 31, 2015 Note EQUITY AND LIABILITIES Shareholders funds Share capital 1 97,467,000 97,467,000 Reserves and surplus 2 26,912,584 (10,908,264) (A) 124,379,584 86,558,736 Current

Annual Report. Principal Pnb Asset Management Company Private Limited

Annual Report Principal Pnb Asset Management Company Private Limited 2010-2011 Balance Sheet as at March 31, 2011 March 31, 2011 March 31, 2011 March 31, 2010 Schedule Rs. Rs. Rs. Sources of Funds

Annual Report Principal Pnb Asset Management Company Private Limited 2010-2011 Balance Sheet as at March 31, 2011 March 31, 2011 March 31, 2011 March 31, 2010 Schedule Rs. Rs. Rs. Sources of Funds

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF IL&FS TRANSPORTATION NETWORKS LIMITED. Report on the Financial Statements

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF IL&FS TRANSPORTATION NETWORKS LIMITED Report on the Financial Statements We have audited the accompanying financial statements of IL&FS TRANSPORTATION NETWORKS

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF IL&FS TRANSPORTATION NETWORKS LIMITED Report on the Financial Statements We have audited the accompanying financial statements of IL&FS TRANSPORTATION NETWORKS

RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED 1. Reliance Energy and Project Development Limited

RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED 1 Reliance Energy and Project Development Limited 2 RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED Independent Auditor s Report To the Members of Reliance

RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED 1 Reliance Energy and Project Development Limited 2 RELIANCE ENERGY AND PROJECT DEVELOPMENT LIMITED Independent Auditor s Report To the Members of Reliance

FANTAIN SPORTS PRIVATE LIMITED 1. Fantain Sports Private Limited

FANTAIN SPORTS PRIVATE LIMITED 1 Fantain Sports Private Limited 2 FANTAIN SPORTS PRIVATE LIMITED Independent Auditor s Report To the Members of Fantain Sports Private Limited Report on the Standalone Financial

FANTAIN SPORTS PRIVATE LIMITED 1 Fantain Sports Private Limited 2 FANTAIN SPORTS PRIVATE LIMITED Independent Auditor s Report To the Members of Fantain Sports Private Limited Report on the Standalone Financial

29,213 28,197 ASSETS Non-current assets Fixed Assets Tangible assets Intangible assets Long-term loans and advances

Vanthys Pharmaceutical Development Private limited Balance Sheet as at 31 March 2014 (Rs '000) As at As at Notes No EQUITY AND LIABILITIES Shareholders' funds Share capital Reserves and surplus 2 225,000

Vanthys Pharmaceutical Development Private limited Balance Sheet as at 31 March 2014 (Rs '000) As at As at Notes No EQUITY AND LIABILITIES Shareholders' funds Share capital Reserves and surplus 2 225,000

INFOMEDIA PRESS LIMITED ANNUAL ACCOUNTS - FY :

1 ANNUAL ACCOUNTS - FY : 2016-17 2 Independent Auditor s Report To the Members of Infomedia Press Limited Report on the Financial Statements 1. We have audited the accompanying financial statements of

1 ANNUAL ACCOUNTS - FY : 2016-17 2 Independent Auditor s Report To the Members of Infomedia Press Limited Report on the Financial Statements 1. We have audited the accompanying financial statements of

Audited Financial Statements. Philips Home Care Services India Private Limited. Financial Year ended March 31, 2017

Audited Financial Statements Philips Home Care Services India Private Limited Financial Year ended March 31, 2017 INDEPENDENT AUDITOR S REPORT To the Members of Philips Home Care Services India Private

Audited Financial Statements Philips Home Care Services India Private Limited Financial Year ended March 31, 2017 INDEPENDENT AUDITOR S REPORT To the Members of Philips Home Care Services India Private

Independent Auditor s Report To the Members of Biocon Research Limited Report on the Financial Statements We have audited the accompanying financial

Independent Auditor s Report To the Members of Biocon Research Limited Report on the Financial Statements We have audited the accompanying financial statements of Biocon Research Limited ( the Company

Independent Auditor s Report To the Members of Biocon Research Limited Report on the Financial Statements We have audited the accompanying financial statements of Biocon Research Limited ( the Company

Copyright -The Institute of Chartered Accountants of India. The forward contract is sold before its due date, hence considered as speculative.

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Eagle Group 24 th September 2017 WHAT TO DO CA. Pramod Jain Get the FS prepared complying

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Eagle Group 24 th September 2017 WHAT TO DO CA. Pramod Jain Get the FS prepared complying

RELIANCE RETAIL INSURANCE BROKING LIMITED. Reliance Retail Insurance Broking Limited

RELIANCE RETAIL INSURANCE BROKING LIMITED 1 Reliance Retail Insurance Broking Limited 2 RELIANCE RETAIL INSURANCE BROKING LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE RETAIL INSURANCE

RELIANCE RETAIL INSURANCE BROKING LIMITED 1 Reliance Retail Insurance Broking Limited 2 RELIANCE RETAIL INSURANCE BROKING LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE RETAIL INSURANCE

RELIANCE COMTRADE PRIVATE LIMITED 1. Reliance Comtrade Private Limited

RELIANCE COMTRADE PRIVATE LIMITED 1 Reliance Comtrade Private Limited 2 RELIANCE COMTRADE PRIVATE LIMITED Independent Auditor s Report To the Members of Reliance Comtrade Private Limited Report on the

RELIANCE COMTRADE PRIVATE LIMITED 1 Reliance Comtrade Private Limited 2 RELIANCE COMTRADE PRIVATE LIMITED Independent Auditor s Report To the Members of Reliance Comtrade Private Limited Report on the

SUGGESTED SOLUTION FINAL MAY 2019 EXAM. Test Code FNJ 7098

SUGGESTED SOLUTION FINAL MAY 2019 EXAM SUBJECT- FR Test Code FNJ 7098 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 Answer 1:

SUGGESTED SOLUTION FINAL MAY 2019 EXAM SUBJECT- FR Test Code FNJ 7098 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 Answer 1: