DESIGNING AND IMPLEMENTING LAST- MILE SERVICE DELIVERY SOLUTIONS AND INNOVATIONS: FINANCIAL INCLUSION OF POOR THROUGH COMMUNITY INSTITUTIONS IN INDIA

|

|

|

- Nicholas Anderson

- 5 years ago

- Views:

Transcription

1 DESIGNING AND IMPLEMENTING LAST- MILE SERVICE DELIVERY SOLUTIONS AND INNOVATIONS: FINANCIAL INCLUSION OF POOR THROUGH COMMUNITY INSTITUTIONS IN INDIA

2 Livelihoods Story Incomes Expenses Wage Income 53% Food Expenses 58% Farm 18% Healthcare 12% Livestock 15% Personal 15% Non Farm 14 % Interest Burden15% Bleeding Livelihoods Sheikwara, Gaya District (Birthplace of Bhoodan in Bihar) - Farm wages are paid in form of grain. NO WORK NO FOOD. - All Bhoodan lands mortgaged due FOOD and HEALTH SHOCKS. - Lease-in land (up to 10 decimals) to GROW FOOD for own consumption. - FOOD LOANS repaid in kind or tied labour and/or produce. - MIGRATION offers plausible solution, but with heavy upfront costs. Poor need financial products matching cash, income, expenditure and risk cycles in their life.

3 Livelihood projects made with Lego* Social mobilization of poor Building institutional platforms for the poor Developing pro-poor financial sector Access to entitlements Linking with markets & services Gender empowerment * Lego

4 Investing on demand side: Building access to markets agenda Entitlements and Social Security Food Security PDS, Food Security Enterprise Health Security Nutrition, CMHS Income Security NREGA, Pensions Risk Management Insurance (Life, health, assets) Access to Markets and Services Productive assets and skills Productivity Enhancement - SRI, SWI, CMSA, Dairy Collective Marketing - Agri Commodities, NTFP, Dairy Market linked Jobs

5 But Financial Inclusion has always been a story of the Fox and the Crane Both friends had an equal opportunity for nourishment, but each time one of them could not take advantage of the opportunity.

6 Financial Inclusion Strategies Building an inclusive financial sector Making poor preferred clients for banking system Monetize livelihoods economy of the poor Reduction in high cost indebtedness for the poor Financial education for planned investments Leveraging investments from mainstream banks Pro-active and systematic initiatives working on both supply and demand side of financial inclusion agenda

7 Lessons from banking with the poor Initial engagement in AP, Tamil Nadu and Orissa Saturation approach to SHG formation Saturated training and sensitization effort Coordination mechanisms: Govt, NABARD & banks Sharing of MIS with banks and tracking credit linkage Result: Initial inertia overcome, momentum picked up Accelerated change in AP, Bihar and Odisha Micro Credit Plan based lending Community involvement for bank linkage & recovery Livelihood innovations triggered financial innovations

8 Transformation in Delivery of Financial Services to the Poor Product innovations by the communities by bundling micro-credit with livelihood services Food Credit and Nutrition Credit Co-production model for rural financial services Relationship managers for the poor (Bima Mitras) Agency arrangements for financial services delivery New technologies and business models transform last mile service delivery IT enabled with Micro-insurance Companies Smart Card based Payment Systems

9 Co producing Financial Services: Innovations Strategic Partnerships with Commercial Banks AP: New product development Bihar & MP: Business process re-engineering Bihar: Dedicated spear head teams Product Innovations AP & Bihar: Bundling microcredit with Food & Nutrition AP & Bihar: Health savings Bihar: Swapping high cost debts land and milk Bihar: Loans for land and animal leasing AP & Bihar: Loans against anticipated NREGA payments AP: AP: Bank product for assistance food security line AP: Bank assistance for Total Financial Inclusion (TFI)

10 Co producing Financial Services: Innovations Service Innovations AP & Bihar: Help-desks at Bank Branches (Bank Mitras) AP: Branchless Banking for Social Security Payments AP & Bihar: SHG Federations as Banking Touch Points/CSC AP: SHG Federations as micro insurance franchisees enabling universal access to insurance by setting high standard of service delivery Consumer Innovations AP: Savings from social security payments Bihar: Poor use savings accounts of SHGs on CBS platform to make and receive remittances at ZERO COST Bihar: Micro Credit Planning as tool for financial and business education

11 Co producing Financial Services: Innovations Service Innovations Bihar & Odisha: Financial literacy and credit counseling Vitta Mitra AP, Bihar & Odisha: Help desks - Bank Mitra Alternative Banking Channels Odisha: Mobile Van (UCO Bank) Bihar: Kiosk Banking (SBI) AP & Bihar: Dairy Banking (HDFC Bank)

12 Financial Inclusion Building Informed, Empowered and Responsible Clients Micro Planning Financial Literacy and Counselling Vitta Mitras Community Managed audit and recovery Mechanism Enabling access to Insurance Product Innovations using CIF as catalytic fund Debt Swapping, Food Security Fund, Health Risk Fund etc. Making Formal Financial Sector Deliver Partnerships ( formal MoUs) with commercial banks & sensitization of local bankers Placement of customer relations managers (Bank Mitra) to smoothen the transactions at the branch level Alternate Banking Models for Total Financial Inclusion Enabling access to a suite of financial services at the doorstep SHG women as CSPs at the last mile

13 Vitth Mitra Financial Counseling

14 Bank Mitra Help Desk Outreach 4500 Bank Mitras across the Country Impact Transaction time down from 2.5 hours to just 15 minutes 95 + percent SHGs in these branches are credit linked NPA is less by at least 30%

15 Alternate Banking Pilots

16 Livelihoods Banking Pilot Center Operator as Business Correspondent for Cash Deposit/Disbursal Cash management thru Nearest Branch HDFC Bank Branch Customer Touch Points HDFC Bank s Maestro debit Card with the Customers EDC Terminal POS terminal at BC Centre to capture customer transactions Introduction of Hub ATMs HDFC DC Connectivity to HDFC Bank s Data Centre thru Landline/CDMA/GSM phone phone

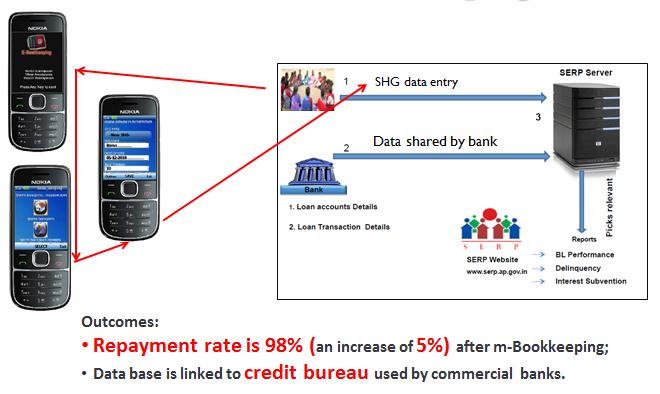

17 Mobile-bookkeeping

18 Community led Micro Insurance Model Insurance Claim Settlement Process Claim village Phone Call Centre located in District Federation Payment of Solatium/Relief US$ 125 Alert ATM Commercial Bank Area Committee Members Area Committee completes documentation and sends e-claim to Insurance Company via District Federation

19 Favorable Investment Climate for Rural Poor Saving 5.5 billion

20 Learnings Invest with a long term perspective Investing in institutions requires experimentation, failure and learning. We need to put risk capital in and learn from failures Invest in political economy from the beginning. Governments need to see a political value preposition Need to invest in aggregate forms of social capital and institutions to create a favorable investment climate

Impacts of the Andhra Pradesh Rural Poverty Reduction Program

Society for Elimination of Rural Poverty National Rural Livelihood Mission Impacts of the Andhra Pradesh Rural Poverty Reduction Program Summary of key outcomes of Rural livelihoods programs in Andhra

Society for Elimination of Rural Poverty National Rural Livelihood Mission Impacts of the Andhra Pradesh Rural Poverty Reduction Program Summary of key outcomes of Rural livelihoods programs in Andhra

Micro Finance in the World and in India: Status, Problems and Prospects

Micro Finance in the World and in India: Status, Problems and Prospects By Vijay Mahajan Chair, CGAP ExCom Founder and CEO, BASIX Social Enterprise Group, India President, MFIN (MFI Network of India) March

Micro Finance in the World and in India: Status, Problems and Prospects By Vijay Mahajan Chair, CGAP ExCom Founder and CEO, BASIX Social Enterprise Group, India President, MFIN (MFI Network of India) March

Can RLP (Rural Livelihood Project) and WSP (Water & Sanitation Project) collaborate? Shouvik Mitra Consultant SASDL - WB

and WSP (Water & Sanitation Project) collaborate? Shouvik Mitra Consultant SASDL - WB") Can RLP (Rural Livelihood Project) and WSP (Water & Sanitation Project) collaborate? Shouvik Mitra Consultant SASDL - WB Understanding RLP Broad objectives Targeting the poor, poorest and most vulnerable

Can RLP (Rural Livelihood Project) and WSP (Water & Sanitation Project) collaborate? Shouvik Mitra Consultant SASDL - WB Understanding RLP Broad objectives Targeting the poor, poorest and most vulnerable

SHPI-Bank Consultation Meet Taking SHG Bank Linkage to the Next Level 3 rd May, 2013, Patna. Organized by: ACCESS ASSIST.

SHPI-Bank Consultation Meet Taking SHG Bank Linkage to the Next Level 3 rd May, 2013, Patna Organized by: ACCESS ASSIST Summary Paper SAMRIDHI (Poorest State Inclusive Growth Programme)is being implemented

SHPI-Bank Consultation Meet Taking SHG Bank Linkage to the Next Level 3 rd May, 2013, Patna Organized by: ACCESS ASSIST Summary Paper SAMRIDHI (Poorest State Inclusive Growth Programme)is being implemented

PRESS RELEASE. Performance driven Progress

CORPORATE OFFICE: GANDHINAGAR BANGALORE PRESS RELEASE 30.07.2012 SyndicateBank Announces its Financial Results for the quarter ended 30 th June 2012 Performance driven Progress (Q 1 of 2012 vis a vis Q

CORPORATE OFFICE: GANDHINAGAR BANGALORE PRESS RELEASE 30.07.2012 SyndicateBank Announces its Financial Results for the quarter ended 30 th June 2012 Performance driven Progress (Q 1 of 2012 vis a vis Q

Outline. Why a national financial inclusion strategy? Why digital? Where we want to go targets. Where we are now context.

National Financial Inclusion Strategy: Strategic Considerations Outline Why a national financial inclusion strategy? Why digital? Where we want to go targets Where we are now context Key thrusts Exploring

National Financial Inclusion Strategy: Strategic Considerations Outline Why a national financial inclusion strategy? Why digital? Where we want to go targets Where we are now context Key thrusts Exploring

JEEViKA Bihar Rural Livelihoods Promotion Society State Rural Livelihoods Mission (SRLM), Govt. of Bihar

, Govt. of Bihar") CONVERGENCE ----- MGNREGS (20 th Dec,12) JEEViKA Bihar Rural Livelihoods Promotion Society State Rural Livelihoods Mission (SRLM), Govt. of Bihar JEEViKA : at a Glance BRLPS registered in 2006 & JEEViKA

CONVERGENCE ----- MGNREGS (20 th Dec,12) JEEViKA Bihar Rural Livelihoods Promotion Society State Rural Livelihoods Mission (SRLM), Govt. of Bihar JEEViKA : at a Glance BRLPS registered in 2006 & JEEViKA

India & ICICI Group. Trends & Outlook. November 2015

India & ICICI Group Trends & Outlook November 2015 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

India & ICICI Group Trends & Outlook November 2015 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

ICICI Group. Performance and Strategy. February 2016

ICICI Group Performance and Strategy February 2016 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

ICICI Group Performance and Strategy February 2016 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

Using Innovative Mechanisms & Technology to enable flow of funds to Small holder farms. by Michael Andrade Business Head Agriculture HDFC BANK, India

Using Innovative Mechanisms & Technology to enable flow of funds to Small holder farms by Michael Andrade Business Head Agriculture HDFC BANK, India Lending to Small holder Farmers Traditional Approach

Using Innovative Mechanisms & Technology to enable flow of funds to Small holder farms by Michael Andrade Business Head Agriculture HDFC BANK, India Lending to Small holder Farmers Traditional Approach

Dairying as Livelihood Activity among SHGs - An overview. Dr. K. Natchimuthu RAGACOVAS, Puducherry.

Dairying as Livelihood Activity among SHGs - An overview Dr. K. Natchimuthu RAGACOVAS, Puducherry. Introduction Organised but unregistered groups involved primarily in savings and credit. Neighbourhood

Dairying as Livelihood Activity among SHGs - An overview Dr. K. Natchimuthu RAGACOVAS, Puducherry. Introduction Organised but unregistered groups involved primarily in savings and credit. Neighbourhood

A Case Study: Micro Financial Institutions (MFI) - Loan Maintenance

- Loan Maintenance") A Case Study: Micro Financial Institutions (MFI) - Loan Maintenance Introduction Small time farmers find it very challenging to access loans for their farming activities. Though many financial institutions

A Case Study: Micro Financial Institutions (MFI) - Loan Maintenance Introduction Small time farmers find it very challenging to access loans for their farming activities. Though many financial institutions

Financial Inclusion and Fintech

Financial Inclusion and Fintech The views expressed in this presentation are those of the author and do not necessarily represent the views of the NBC. 2 Agenda Financial Inclusion Landscape Regulatory

Financial Inclusion and Fintech The views expressed in this presentation are those of the author and do not necessarily represent the views of the NBC. 2 Agenda Financial Inclusion Landscape Regulatory

Regional Rural Banks- Sustainability through Outreach. Amarendra Sahoo Chief General Manager RBI, Mumbai

Regional Rural Banks- Sustainability through Outreach Amarendra Sahoo Chief General Manager RBI, Mumbai Scheme of Presentation I. RRBs mandate and to what extent fulfilled II. Perceived tension between

Regional Rural Banks- Sustainability through Outreach Amarendra Sahoo Chief General Manager RBI, Mumbai Scheme of Presentation I. RRBs mandate and to what extent fulfilled II. Perceived tension between

Financial Results Q3/FY February 2019

Financial Results Q3/FY18-19 08 February 2019 HIGHLIGHTS - DEC 2018 Total Business Total Deposit Gross Advance Operating Profit (Q-3) Rs. 291519 Crore Rs. 177906 Crore Rs.113610 Crore Rs. 381 Crore Basel

Financial Results Q3/FY18-19 08 February 2019 HIGHLIGHTS - DEC 2018 Total Business Total Deposit Gross Advance Operating Profit (Q-3) Rs. 291519 Crore Rs. 177906 Crore Rs.113610 Crore Rs. 381 Crore Basel

PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Report No.: AB4152 Second Madhya Pradesh District Poverty Initiatives Project Project Name

APPRAISAL STAGE Report No.: AB4152 Second Madhya Pradesh District Poverty Initiatives Project Project Name") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Report No.: AB4152 Second Madhya Pradesh

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROJECT INFORMATION DOCUMENT (PID) APPRAISAL STAGE Report No.: AB4152 Second Madhya Pradesh

DateDdddd. UNITED BANK OF INDIA (The Bank that begins with U) Financial Results for Q-3 (FY ) PRESS RELEASE

Financial Results for Q-3 (FY ) PRESS RELEASE") DateDdddd Date: 20 th January, 2011 UNITED BANK OF INDIA (The Bank that begins with U) Financial Results for Q-3 (FY 2010-11) PRESS RELEASE 1. Table of Contents Highlights for Q3 ended, December, 2010

DateDdddd Date: 20 th January, 2011 UNITED BANK OF INDIA (The Bank that begins with U) Financial Results for Q-3 (FY 2010-11) PRESS RELEASE 1. Table of Contents Highlights for Q3 ended, December, 2010

: Rs % Performance Highlights for the Q3 FY 12 and 9M FY 12 ended December 2011

Press Release TOTAL BUSINESS CROSSES Rs 6,00,000 CRORE. CASA DEPOSITS CROSS Rs 1,25,000 CRORE TOTAL ASSETS CROSS Rs. 4,21,000 CRORE. NET INTEREST MARGIN REMAINS HIGH AT 3.85% BOOK VALUE PER SHARE ABOVE

Press Release TOTAL BUSINESS CROSSES Rs 6,00,000 CRORE. CASA DEPOSITS CROSS Rs 1,25,000 CRORE TOTAL ASSETS CROSS Rs. 4,21,000 CRORE. NET INTEREST MARGIN REMAINS HIGH AT 3.85% BOOK VALUE PER SHARE ABOVE

Performance of Self-help Groups in Micro Finance

Economic Affairs, Vol. 6, No. 4, pp. 609-6, December 06 DOI: 0.5958/0976-4666.06.00075.9 06 New Delhi Publishers. All rights reserved Performance of Self-help Groups in Micro Finance Vanita Khobarkar,

Economic Affairs, Vol. 6, No. 4, pp. 609-6, December 06 DOI: 0.5958/0976-4666.06.00075.9 06 New Delhi Publishers. All rights reserved Performance of Self-help Groups in Micro Finance Vanita Khobarkar,

Postal Financial Services. India Post

Postal Financial Services India Post India Post : a socially committed, technology driven, professionally managed & forward looking Organization Serving the nation for more than 150 years, and enjoying

Postal Financial Services India Post India Post : a socially committed, technology driven, professionally managed & forward looking Organization Serving the nation for more than 150 years, and enjoying

Overview. Financial Systems approach to microfinance Basic roles and functions of government and donors at various points within the financial sector

Overview Financial Systems approach to microfinance Basic roles and functions of government and donors at various points within the financial sector The Borders of Microfinance are Blurring Khan bank serving

Overview Financial Systems approach to microfinance Basic roles and functions of government and donors at various points within the financial sector The Borders of Microfinance are Blurring Khan bank serving

Half Yearly Results (FY ) PRESS RELEASE

PRESS RELEASE") Date-31 st October, 2011 UNITED BANK OF INDIA (The Bank that begins with U) Half Yearly Results (FY 2011-12) PRESS RELEASE L to R: Shri S.L.Bansal-ED, Shri Bhaskar Sen-CMD & Shri D.Basu-GM(Accounts) Table

Date-31 st October, 2011 UNITED BANK OF INDIA (The Bank that begins with U) Half Yearly Results (FY 2011-12) PRESS RELEASE L to R: Shri S.L.Bansal-ED, Shri Bhaskar Sen-CMD & Shri D.Basu-GM(Accounts) Table

FINANCIAL LITERACY: AN INDIAN SCENARIO

ABSTRACT FINANCIAL LITERACY: AN INDIAN SCENARIO DEAN ROY NASH* *Research Associate in Commerce, Saint Albert s College, Ernakulam, Kerala, India. Financial literacy is nothing but knowledge about finance.

ABSTRACT FINANCIAL LITERACY: AN INDIAN SCENARIO DEAN ROY NASH* *Research Associate in Commerce, Saint Albert s College, Ernakulam, Kerala, India. Financial literacy is nothing but knowledge about finance.

Country Practice Area(Lead) Additional Financing India Agriculture P130546

Additional Financing India Agriculture P130546") Public Disclosure Authorized Independent Evaluation Group (IEG) 1. Project Data Report Number : ICRR0020734 Public Disclosure Authorized Public Disclosure Authorized Project ID P090764 Project Name IN:

Public Disclosure Authorized Independent Evaluation Group (IEG) 1. Project Data Report Number : ICRR0020734 Public Disclosure Authorized Public Disclosure Authorized Project ID P090764 Project Name IN:

IJEMR - May Vol.2 Issue 5 - Online - ISSN Print - ISSN

Role of Public Sector Banks in Microfinance - A Study of Public Sector Banks in the Southern Region of India * Dr. Sujatha Susanna Kumari. D Asst. Professor, Dept. of Commerce, School of Business Studies,

Role of Public Sector Banks in Microfinance - A Study of Public Sector Banks in the Southern Region of India * Dr. Sujatha Susanna Kumari. D Asst. Professor, Dept. of Commerce, School of Business Studies,

Challenges to Financial Inclusion in India: The Case of Andhra Pradesh

Challenges to Financial Inclusion in India: The Case of Andhra Pradesh S. Ananth and T. Sabri Öncü Estimated Scale of Financial Exclusion The scale of financial exclusion is phenomenally large in India.

Challenges to Financial Inclusion in India: The Case of Andhra Pradesh S. Ananth and T. Sabri Öncü Estimated Scale of Financial Exclusion The scale of financial exclusion is phenomenally large in India.

State Bank of India Q2FY09 RESULTS ANALYSTS MEET

State Bank of India Q2FY09 RESULTS ANALYSTS MEET 27.10.2008 Operating and Net Profit 4193 Q2FY08 Q2FY09 Rs. In Crs 2714 28.43% 54.52% 1611 36.04% 2260 40.23% Operating Profit Net Profit 1 34454 Deposit

State Bank of India Q2FY09 RESULTS ANALYSTS MEET 27.10.2008 Operating and Net Profit 4193 Q2FY08 Q2FY09 Rs. In Crs 2714 28.43% 54.52% 1611 36.04% 2260 40.23% Operating Profit Net Profit 1 34454 Deposit

SUMMARY OF PROCEEDINGS

Third Meeting of State Financial Inclusion Forum (SFIF), Bihar 3 rd July, 2014 Hotel Chanakya, Patna Background-Bihar, which is in the bottom five of CRISIL Financial Inclusion Index, requires cooperation

Third Meeting of State Financial Inclusion Forum (SFIF), Bihar 3 rd July, 2014 Hotel Chanakya, Patna Background-Bihar, which is in the bottom five of CRISIL Financial Inclusion Index, requires cooperation

ANSWER KEY C F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C Indian Financial System

(CHOICE BASE) SEMESTER - I / C Indian Financial System") ANSWER KEY-00135 C0921 - F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C0584 - Indian Financial System Q1) a) Answer whether the below statements are True or False: (Attempt any 8) (8

ANSWER KEY-00135 C0921 - F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C0584 - Indian Financial System Q1) a) Answer whether the below statements are True or False: (Attempt any 8) (8

Agenda/ Background Papers

Background: Agenda/ Background Papers NABARD, R.O. Jammu, vide communication bearing Ref. No. NB (J&K)/ mcid /2015-16 dated 28 May, 2015 intimated that SHG-Bank Linkage programme has grown exponentially

Background: Agenda/ Background Papers NABARD, R.O. Jammu, vide communication bearing Ref. No. NB (J&K)/ mcid /2015-16 dated 28 May, 2015 intimated that SHG-Bank Linkage programme has grown exponentially

Analysis on Determinants of Micro-Credit Borrowings Rural SHG Women in North Coastal Andhra Pradesh

Analysis on Determinants of Micro-Credit Borrowings Rural SHG Women in North Coastal Andhra Pradesh M. Madhuri Dept. of Commerce and Management Studies, Andhra University, Visakhapatnam, Andhra Pradesh

Analysis on Determinants of Micro-Credit Borrowings Rural SHG Women in North Coastal Andhra Pradesh M. Madhuri Dept. of Commerce and Management Studies, Andhra University, Visakhapatnam, Andhra Pradesh

A Peer Reviewed International Journal of Asian Research Consortium AJRBF:

ABSTRACT A Peer Reviewed International Journal of Asian Research Consortium : ASIAN JOURNAL OF RESEARCH IN BANKING AND FINANCE FINANCIAL INCLUSION AND ROLE OF MICROFINANCE DR. MUKUND CHANDRA MEHTA* *Assistant

ABSTRACT A Peer Reviewed International Journal of Asian Research Consortium : ASIAN JOURNAL OF RESEARCH IN BANKING AND FINANCE FINANCIAL INCLUSION AND ROLE OF MICROFINANCE DR. MUKUND CHANDRA MEHTA* *Assistant

CHAPTER 3. Financial Inclusion in India

CHAPTER 3 Financial Inclusion in India 3.1 Introduction: Bank nationalization in India marked a paradigm shift in the focus of banking. The importance of financial inclusion, based on the principle of

CHAPTER 3 Financial Inclusion in India 3.1 Introduction: Bank nationalization in India marked a paradigm shift in the focus of banking. The importance of financial inclusion, based on the principle of

Banking Awareness of The Residents in The Present Financial Inclusion ERA in Nagapattinam District, Tamil Nadu

Banking Awareness of The Residents in The Present Financial Inclusion ERA in Nagapattinam District, Tamil Nadu Dr. S. Rajaswaminathan Guest Faculty, Department of Commerce School of Management, Pondicherry

Banking Awareness of The Residents in The Present Financial Inclusion ERA in Nagapattinam District, Tamil Nadu Dr. S. Rajaswaminathan Guest Faculty, Department of Commerce School of Management, Pondicherry

E- ISSN X ISSN MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA

MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA Dr.K.Jayalakshmi PDF(ICSSR),Dept. of Commerce,S.K.University, Anantapur. Andhra Pradesh. Abstract Financial inclusion is a flagship programme

MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA Dr.K.Jayalakshmi PDF(ICSSR),Dept. of Commerce,S.K.University, Anantapur. Andhra Pradesh. Abstract Financial inclusion is a flagship programme

Why Financial Inclusion

Yogesh Suri, Chief Economist (AGM), SBBJ, Jaipur December 16, 2008 1 Indian Economy During the last 58 years, India s GDP at current prices has grown 450 times from Rs.9,547 crore in 1950-51 to Rs.43,03,654

Yogesh Suri, Chief Economist (AGM), SBBJ, Jaipur December 16, 2008 1 Indian Economy During the last 58 years, India s GDP at current prices has grown 450 times from Rs.9,547 crore in 1950-51 to Rs.43,03,654

Commissioner General Of Samurdhi Ministry of Economic Development Si Sri Lanka

Chandra Wickramasinghe Commissioner General Of Samurdhi Ministry of Economic Development Si Sri Lanka Country Profile The Democratic Socialist Republic of Sri Lanka A Picturesque Tropical Island in South

Chandra Wickramasinghe Commissioner General Of Samurdhi Ministry of Economic Development Si Sri Lanka Country Profile The Democratic Socialist Republic of Sri Lanka A Picturesque Tropical Island in South

Investor Presentation

Investor Presentation Contents Well positioned across India s GDP spectrum Meeting Diverse Customers Needs Unique Franchise in the Indian Banking Sector Key Business Initiatives Financial Highlights Value

Investor Presentation Contents Well positioned across India s GDP spectrum Meeting Diverse Customers Needs Unique Franchise in the Indian Banking Sector Key Business Initiatives Financial Highlights Value

UNITED BANK OF INDIA FINANCIAL RESULTS FY

29 th April, 2011 UNITED BANK OF INDIA FINANCIAL RESULTS FY 2010-11 PRESS RELEASE 1. Table of Contents Highlights for Q4 ended March 31, 2011 (Q4 FY11) Highlights for FY ended March 31, 2011 (FY11) Other

29 th April, 2011 UNITED BANK OF INDIA FINANCIAL RESULTS FY 2010-11 PRESS RELEASE 1. Table of Contents Highlights for Q4 ended March 31, 2011 (Q4 FY11) Highlights for FY ended March 31, 2011 (FY11) Other

SAMRUDHI Micro Fin Society (SMS) Brief Profile

Brief Profile") SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

UN-OHRLLS COUNTRY-LEVEL PREPARATIONS

UN-OHRLLS COMPREHENSIVE HIGH-LEVEL MIDTERM REVIEW OF THE IMPLEMENTATION OF THE ISTANBUL PROGRAMME OF ACTION FOR THE LDCS FOR THE DECADE 2011-2020 COUNTRY-LEVEL PREPARATIONS ANNOTATED OUTLINE FOR THE NATIONAL

UN-OHRLLS COMPREHENSIVE HIGH-LEVEL MIDTERM REVIEW OF THE IMPLEMENTATION OF THE ISTANBUL PROGRAMME OF ACTION FOR THE LDCS FOR THE DECADE 2011-2020 COUNTRY-LEVEL PREPARATIONS ANNOTATED OUTLINE FOR THE NATIONAL

Access to Financial Services to the Rural Household Enterprises A Study of Srikakulam District, Andhra Pradesh

Access to Financial Services to the Rural Household Enterprises A Study of Srikakulam District, Andhra Pradesh Ch. Ganga Bhavani *, Prof.P. Veni** * Research Scholar, Department of Commerce and Management

Access to Financial Services to the Rural Household Enterprises A Study of Srikakulam District, Andhra Pradesh Ch. Ganga Bhavani *, Prof.P. Veni** * Research Scholar, Department of Commerce and Management

Financial Inclusion and India-Challenges, Opportunities

Financial Inclusion and India-Challenges, Opportunities New Horizon College, 3 RD A Cross, 2 nd A main, Kasturinagar, Bangalore-560003. Abstract In recent times Financial Inclusion and Inclusive Growth

Financial Inclusion and India-Challenges, Opportunities New Horizon College, 3 RD A Cross, 2 nd A main, Kasturinagar, Bangalore-560003. Abstract In recent times Financial Inclusion and Inclusive Growth

INVESTOR PRESENTATION

INVESTOR PRESENTATION 1 Contents Well positioned across India s GDP spectrum Meeting Diverse Customers Needs Unique Franchise in the Indian Banking Sector Key Business Initiatives Financial Highlights

INVESTOR PRESENTATION 1 Contents Well positioned across India s GDP spectrum Meeting Diverse Customers Needs Unique Franchise in the Indian Banking Sector Key Business Initiatives Financial Highlights

Community Managed Revolving Fund (Sustainable mechanism of microfinance practices to disadvantaged community)

") Community Managed Revolving Fund (Sustainable mechanism of microfinance practices to disadvantaged community) A paper presented in Micro Finance Summit 2008 New departure in expanding the outreach of Micro-finance

Community Managed Revolving Fund (Sustainable mechanism of microfinance practices to disadvantaged community) A paper presented in Micro Finance Summit 2008 New departure in expanding the outreach of Micro-finance

Learning Journey. IFFCO-TOKIO General Insurance Co. Ltd.

Learning Journey IFFCO-TOKIO General Insurance Co. Ltd. Loss Mitigation in Cattle Insurance through RFID Contents Project Basics... 1 About the project... 1 Project Updates... 3 Key Indicators... 3 What

Learning Journey IFFCO-TOKIO General Insurance Co. Ltd. Loss Mitigation in Cattle Insurance through RFID Contents Project Basics... 1 About the project... 1 Project Updates... 3 Key Indicators... 3 What

IMPLEMENTATION COMPLETION AND RESULTS REPORT (Cr IN) ON A CREDIT IN THE AMOUNT OF XDR MILLION (US$ MILLION EQUIVALENT) TO THE

ON A CREDIT IN THE AMOUNT OF XDR MILLION (US$ MILLION EQUIVALENT) TO THE") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Document of The World Bank IMPLEMENTATION COMPLETION AND RESULTS REPORT (Cr. 3732-IN)

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Document of The World Bank IMPLEMENTATION COMPLETION AND RESULTS REPORT (Cr. 3732-IN)

A study on the performance of SHG-Bank Linkage Programme towards Savings and Loan disbursements to beneficiaries in India

A study on the performance of SHG-Bank Linkage Programme towards Savings and to beneficiaries in India Prof. Noorbasha Abdul, Ph.D. Professor of Commerce & Management, Acharya Nagarjuna University, Nagarjuna

A study on the performance of SHG-Bank Linkage Programme towards Savings and to beneficiaries in India Prof. Noorbasha Abdul, Ph.D. Professor of Commerce & Management, Acharya Nagarjuna University, Nagarjuna

Regional trends on gender data collection and analysis

Sex-disaggregated data for the SDG indicators in Asia and the Pacific: What and how? Regional trends on gender data collection and analysis Rajesh Sharma UNDP Bangkok Regional Hub ISSUES (1) In the past,

Sex-disaggregated data for the SDG indicators in Asia and the Pacific: What and how? Regional trends on gender data collection and analysis Rajesh Sharma UNDP Bangkok Regional Hub ISSUES (1) In the past,

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka. Florence Kariuki August 2013

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka Florence Kariuki August 2013 Introduction Equity Bank was founded as Equity Building Society (EBS) in October 1984 and

Financing Agriculture Forum 2013: Profitable Agricultural Banking Colombo, Sri Lanka Florence Kariuki August 2013 Introduction Equity Bank was founded as Equity Building Society (EBS) in October 1984 and

Impact Assessment of Microfinance For SIDBI Foundation for Micro Credit (SFMC)

") Impact Assessment of Microfinance For SIDBI Foundation for Micro Credit (SFMC) Phase 1 Report July 2001 March 2002 By Putting people first EDA Rural Systems Pvt Ltd 107 Qutab Plaza, DLF Qutab Enclave-1,

Impact Assessment of Microfinance For SIDBI Foundation for Micro Credit (SFMC) Phase 1 Report July 2001 March 2002 By Putting people first EDA Rural Systems Pvt Ltd 107 Qutab Plaza, DLF Qutab Enclave-1,

Delivering Financial Inclusion Services to Rural Citizens through the Common Service Centers. An Evaluation of State Implementation Models

Delivering Financial Inclusion Services to Rural Citizens through the Common Service Centers An Evaluation of State Implementation Models March 2011 Table of Contents I. Introduction... 3 II. Financial

Delivering Financial Inclusion Services to Rural Citizens through the Common Service Centers An Evaluation of State Implementation Models March 2011 Table of Contents I. Introduction... 3 II. Financial

RBI/ /40 RPCD. MFFI. BC.No.09 / / July 1, Master Circular on Micro Credit

RBI/ 2009-10/40 RPCD. MFFI. BC.No.09 / 12.01.001/ 2009-10 July 1, 2009 The Chairman/ Managing Director/ Chief Executive Officer All Scheduled Commercial Banks Dear Sir, Master Circular on Micro Credit

RBI/ 2009-10/40 RPCD. MFFI. BC.No.09 / 12.01.001/ 2009-10 July 1, 2009 The Chairman/ Managing Director/ Chief Executive Officer All Scheduled Commercial Banks Dear Sir, Master Circular on Micro Credit

A Premier Public Sector Bank

Sector Bank A Premier Public Sector Bank Performance highlights for the Quarter/ Year ended 31 st March, 2016. 1. Performance highlights of the Bank for the 12 months ended 31.03.2016: [Rs. in Crore] Parameter

Sector Bank A Premier Public Sector Bank Performance highlights for the Quarter/ Year ended 31 st March, 2016. 1. Performance highlights of the Bank for the 12 months ended 31.03.2016: [Rs. in Crore] Parameter

Draft ToR for Thematic study on Financial inclusion Interventions, Challenges and Lessons under NERLP

Draft ToR for Thematic study on Financial inclusion Interventions, Challenges and Lessons under NERLP 1. Background NERLP is a World Bank funded rural poverty reduction project of the Ministry of Development

Draft ToR for Thematic study on Financial inclusion Interventions, Challenges and Lessons under NERLP 1. Background NERLP is a World Bank funded rural poverty reduction project of the Ministry of Development

Bihar: What is holding back growth in Bihar? Bihar Development Strategy Workshop, Patna. June 18

Bihar: What is holding back growth in Bihar? Bihar Development Strategy Workshop, Patna. June 18 Ejaz Ghani World Bank. Structure of Presentation How does Bihar compare with other states? What is constraining

Bihar: What is holding back growth in Bihar? Bihar Development Strategy Workshop, Patna. June 18 Ejaz Ghani World Bank. Structure of Presentation How does Bihar compare with other states? What is constraining

KCB GROUP PLC INVESTOR PRESENTATION. H FINANCIAL RESULTS

KCB GROUP PLC INVESTOR PRESENTATION. H1 2018 FINANCIAL RESULTS MACRO-ECONOMIC HIGHLIGHTS Macro-Economic Highlights Kenya GDP Growth Rate (%) 5.7% 5.3% 4.7% 4.7% 6.2% Kenya 5.2% 1.0% Q2 2017 Q3 2017 Q4

KCB GROUP PLC INVESTOR PRESENTATION. H1 2018 FINANCIAL RESULTS MACRO-ECONOMIC HIGHLIGHTS Macro-Economic Highlights Kenya GDP Growth Rate (%) 5.7% 5.3% 4.7% 4.7% 6.2% Kenya 5.2% 1.0% Q2 2017 Q3 2017 Q4

NABARD & microfinance

NABARD & microfinance 2001-2002 Ten years of SHG-Bank Linkage (1992-2002) Self Help Groups An SHG is a group of about 20 people from a homogeneous class, who come together for addressing their common problems.

NABARD & microfinance 2001-2002 Ten years of SHG-Bank Linkage (1992-2002) Self Help Groups An SHG is a group of about 20 people from a homogeneous class, who come together for addressing their common problems.

ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE :: KADAPA. Circular No BC - CD Date:

ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE :: KADAPA Circular No. 317 2011 - BC - CD Date: 31.12.2011 SHG - BANK LINKAGE PROGRAMME SANCTION OF CASH CREDIT LIMIT REVISED GUIDELINES Ref. Cir. No. 1) 145-2006-BC-CST,

ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE :: KADAPA Circular No. 317 2011 - BC - CD Date: 31.12.2011 SHG - BANK LINKAGE PROGRAMME SANCTION OF CASH CREDIT LIMIT REVISED GUIDELINES Ref. Cir. No. 1) 145-2006-BC-CST,

Indian Overseas Bank इण ड यन ओवरस ज ब क PERFORMANCE ANALYSIS Q2/H

Indian Overseas Bank इण ड यन ओवरस ज ब क PERFORMANCE ANALYSIS Q2/H1 2018-19 OUR HERITAGE Indian Overseas Bank (IOB) was founded on 10th February 1937 by Shri.M.Ct.M. Chidambaram Chettyar. Objective was

Indian Overseas Bank इण ड यन ओवरस ज ब क PERFORMANCE ANALYSIS Q2/H1 2018-19 OUR HERITAGE Indian Overseas Bank (IOB) was founded on 10th February 1937 by Shri.M.Ct.M. Chidambaram Chettyar. Objective was

FINANCIAL INCLUSION - INDIAN EXPERIENCE

FINANCIAL INCLUSION - INDIAN EXPERIENCE Financial Inclusion (FI) Simplicity and reliability in financial inclusion in India, though not a cure all, can be a way of liberating the poor from dependence on

FINANCIAL INCLUSION - INDIAN EXPERIENCE Financial Inclusion (FI) Simplicity and reliability in financial inclusion in India, though not a cure all, can be a way of liberating the poor from dependence on

Self-Help Groups Catalyst to Financial Inclusion of Rural Women A Case Study of Dakshina Kannada District, Karnataka.

Self-Help Groups Catalyst to Financial Inclusion of Rural Women A Case Study of Dakshina Kannada District, Karnataka. Mr. Ramakrishna B *Research Scholar, GITAM Institute of Management, GITAM University,

Self-Help Groups Catalyst to Financial Inclusion of Rural Women A Case Study of Dakshina Kannada District, Karnataka. Mr. Ramakrishna B *Research Scholar, GITAM Institute of Management, GITAM University,

Financial Inclusion & Postal Banking The India Story

Financial Inclusion & Postal Banking The India Story A Presentation by Sandip Ghose Reserve Bank of India at the UPU-AFI Workshop, Berne, Switzerland 9 th & 10 th November, 2009 Financial Inclusion : Definition

Financial Inclusion & Postal Banking The India Story A Presentation by Sandip Ghose Reserve Bank of India at the UPU-AFI Workshop, Berne, Switzerland 9 th & 10 th November, 2009 Financial Inclusion : Definition

PUDHU VAAZHVU The World Bank funded Project

TAMIL NADU EMPOWERMENT AND POVERTY REDUCTION PROJECT PUDHU VAAZHVU The World Bank funded Project About the Project A key Project of World Bank in Tamil Nadu to address inequity and to promote inclusive

TAMIL NADU EMPOWERMENT AND POVERTY REDUCTION PROJECT PUDHU VAAZHVU The World Bank funded Project About the Project A key Project of World Bank in Tamil Nadu to address inequity and to promote inclusive

Airo International Research Journal June, 2017 Volume XI, ISSN:

1 FINANCIAL INCLUSION THROUGH BUSINESS CORRESPONDENT MODEL IN HARYANA: A CRITICAL ANALYSIS Manoj Siwach 1 and Kavita Gahlot 2 Declaration of Author: I hereby declare that the content of this research paper

1 FINANCIAL INCLUSION THROUGH BUSINESS CORRESPONDENT MODEL IN HARYANA: A CRITICAL ANALYSIS Manoj Siwach 1 and Kavita Gahlot 2 Declaration of Author: I hereby declare that the content of this research paper

A STUDY ON COMMUNITY INVESTMENT FUND IN ANDHRA PRADERSH

A STUDY ON COMMUNITY INVESTMENT FUND IN ANDHRA PRADERSH APMAS Presentation by Dr. K. Raja Reddy, krajareddy@apmas.org 1 OBJECTIVIES OF THE STUDY To understand the socio-economic profile of the CIF beneficiaries

A STUDY ON COMMUNITY INVESTMENT FUND IN ANDHRA PRADERSH APMAS Presentation by Dr. K. Raja Reddy, krajareddy@apmas.org 1 OBJECTIVIES OF THE STUDY To understand the socio-economic profile of the CIF beneficiaries

Evaluation of SHG-Bank Linkage: A Case Study of Rural Andhra Pradesh Women

EUROPEAN ACADEMIC RESEARCH Vol. II, Issue 8/ November 2014 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.1 (UIF) DRJI Value: 5.9 (B+) Evaluation of SHG-Bank Linkage: A Case Study of Rural Andhra Pradesh

EUROPEAN ACADEMIC RESEARCH Vol. II, Issue 8/ November 2014 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.1 (UIF) DRJI Value: 5.9 (B+) Evaluation of SHG-Bank Linkage: A Case Study of Rural Andhra Pradesh

Sustainable Development Goals Fund (SDG Fund) Framework and Guidance for Partnerships with the Private Sector

Framework and Guidance for Partnerships with the Private Sector") Sustainable Development Goals Fund (SDG Fund) Framework and Guidance for Partnerships with the Private Sector Why partner with the SDG Fund The private sector has played an active role in the work of the

Sustainable Development Goals Fund (SDG Fund) Framework and Guidance for Partnerships with the Private Sector Why partner with the SDG Fund The private sector has played an active role in the work of the

Performance Appraisal of Andhra Bank and its role in Financial Inclusion

WWW..COM ISSN: 2278-3970 Performance Appraisal of Andhra Bank and its role in Financial Inclusion Dr. K.V.S.Prasad 1, Prof. G. Sudarsana Rao 2 1 Assistant Professor, Department of Basic Science and Humanities,

WWW..COM ISSN: 2278-3970 Performance Appraisal of Andhra Bank and its role in Financial Inclusion Dr. K.V.S.Prasad 1, Prof. G. Sudarsana Rao 2 1 Assistant Professor, Department of Basic Science and Humanities,

The Role Of Micro Finance In Women s Empowerment (An Empirical Study In Chittoor Rural Shg s) In A.P.

In A.P.") The Role Of Micro Finance In Women s Empowerment (An Empirical Study In Chittoor Rural Shg s) In A.P. Dr. S. Sugunamma Lecturer in Economics, P.V.K.N. Govt College, Chittoor Abstract: The SHG method is

The Role Of Micro Finance In Women s Empowerment (An Empirical Study In Chittoor Rural Shg s) In A.P. Dr. S. Sugunamma Lecturer in Economics, P.V.K.N. Govt College, Chittoor Abstract: The SHG method is

Microfinance for Agriculture: Perspectives from India

Microfinance for Agriculture: Perspectives from India SATISH PILLARISETTI National Bank for Agriculture and Rural Development (NABARD) INDIA 11 December 2007 1 PROLOGUE State interventions in rural finance

Microfinance for Agriculture: Perspectives from India SATISH PILLARISETTI National Bank for Agriculture and Rural Development (NABARD) INDIA 11 December 2007 1 PROLOGUE State interventions in rural finance

Peter Graves Senior Vice President, Technical Services World Council of Credit Unions

Expanding Access to Finance to the Bottom Billion Critical Factors Presentation to UN Preparatory Process/3 rd International Conference on Financing for Development 14 November 2014 Peter Graves Senior

Expanding Access to Finance to the Bottom Billion Critical Factors Presentation to UN Preparatory Process/3 rd International Conference on Financing for Development 14 November 2014 Peter Graves Senior

An Overview of Microfinance in AP

National Seminar on Women Empowerment through Microfinance and Small Enterprises (11 th &12 th November 2010) organized by Dept. of Commerce, Govt. College for Women, Begumpet, Hyderabad Presentation on

National Seminar on Women Empowerment through Microfinance and Small Enterprises (11 th &12 th November 2010) organized by Dept. of Commerce, Govt. College for Women, Begumpet, Hyderabad Presentation on

FINANCIAL INCLUSION AND ECONOMIC GROWTH

FINANCIAL INCLUSION AND ECONOMIC GROWTH Associate Professor & HOD, Banking & Finance Poona College of Arts, Science & Commerce, Camp, Pune-1 Savitribai Phule Pune University. (MS) INDIA Economic growth

FINANCIAL INCLUSION AND ECONOMIC GROWTH Associate Professor & HOD, Banking & Finance Poona College of Arts, Science & Commerce, Camp, Pune-1 Savitribai Phule Pune University. (MS) INDIA Economic growth

State Bank of India

State Bank of India 24.01.2009 Disclaimer This presentation is made purely for information. We have tried to give relevant information which we believe will help in knowing the Bank. The viewers may use

State Bank of India 24.01.2009 Disclaimer This presentation is made purely for information. We have tried to give relevant information which we believe will help in knowing the Bank. The viewers may use

CO:RURAL BANKING DEPARTMENT. Revised Kisan Credit Card (KCC) Scheme

Scheme") a MAIN : ADV - 29/2012-13 DT. 14-05-2012 SUB : Rural Lending - 04 CO:RURAL BANKING DEPARTMENT FILE M-2 S-201 Revised Kisan Credit Card (KCC) Scheme Our Bank issued Master circular on Indian Bank Kisan

a MAIN : ADV - 29/2012-13 DT. 14-05-2012 SUB : Rural Lending - 04 CO:RURAL BANKING DEPARTMENT FILE M-2 S-201 Revised Kisan Credit Card (KCC) Scheme Our Bank issued Master circular on Indian Bank Kisan

FY First Quarter Results. Investor Presentation

FY 2009-10 First Quarter Results Investor Presentation 1 Performance Highlights Q1FY10 Net Profit Net Interest Income Fee Income Operating Revenue Operating Profit 70% YOY 29% YOY 17% YOY 40% YOY 47% YOY

FY 2009-10 First Quarter Results Investor Presentation 1 Performance Highlights Q1FY10 Net Profit Net Interest Income Fee Income Operating Revenue Operating Profit 70% YOY 29% YOY 17% YOY 40% YOY 47% YOY

Financial Inclusion and Millennium Development Goals

Financial Inclusion and Millennium Development Goals At the outset, I take this opportunity to thank the Planning Commission, the United Nations Development Programme (UNDP) and the College of Agricultural

Financial Inclusion and Millennium Development Goals At the outset, I take this opportunity to thank the Planning Commission, the United Nations Development Programme (UNDP) and the College of Agricultural

Financial Inclusion in India: The Role of Microfinance as a Tool

Financial Inclusion in India: The Role of Microfinance as a Tool Jagadeesh B* Assistant Professor Department of Commerce Field Marshal K.M Cariappa College, Madikeri, Kodagu Abstract Microfinance has assumed

Financial Inclusion in India: The Role of Microfinance as a Tool Jagadeesh B* Assistant Professor Department of Commerce Field Marshal K.M Cariappa College, Madikeri, Kodagu Abstract Microfinance has assumed

PRADHAN MANTRI JAN DHAN YOJNA AN APPROACH TO TAKE IT AHEAD

PRADHAN MANTRI JAN DHAN YOJNA AN APPROACH TO TAKE IT AHEAD Contents PMJDY - Pradhan Mantri Jan Dhan Yojna... Achievements of PJMJDY... Issues faced by PJMJDY... Threats... Way ahead... The Current and

PRADHAN MANTRI JAN DHAN YOJNA AN APPROACH TO TAKE IT AHEAD Contents PMJDY - Pradhan Mantri Jan Dhan Yojna... Achievements of PJMJDY... Issues faced by PJMJDY... Threats... Way ahead... The Current and

BSE: NSE: SATIN CSE: Corporate Identity No. L65991DL1990PLC Familiarization Programme for Independent Directors

BSE: 539404 NSE: SATIN CSE: 30024 Corporate Identity No. L65991DL1990PLC041796 Familiarization Programme for Independent Directors Microfinance Through Window of Relevance Micro-finance is defined as financial

BSE: 539404 NSE: SATIN CSE: 30024 Corporate Identity No. L65991DL1990PLC041796 Familiarization Programme for Independent Directors Microfinance Through Window of Relevance Micro-finance is defined as financial

Anil Swarup Additional Secretary & Director General Ministry of Labour and Employment Government of India

Health Insurance for the poor India s Rashtriya Swathya Bima Yojana Anil Swarup Additional Secretary & Director General Ministry of Labour and Employment Government of India STRUCTURE OF THE PRESENTATION

Health Insurance for the poor India s Rashtriya Swathya Bima Yojana Anil Swarup Additional Secretary & Director General Ministry of Labour and Employment Government of India STRUCTURE OF THE PRESENTATION

EMPOWERING FINANCIAL INCLUSION THROUGH FINANCIAL LITERACY

Abstract EMPOWERING FINANCIAL INCLUSION THROUGH FINANCIAL LITERACY The term financial inclusion means availability of banking services at an affordable cost to disadvantaged and low-income groups. The

Abstract EMPOWERING FINANCIAL INCLUSION THROUGH FINANCIAL LITERACY The term financial inclusion means availability of banking services at an affordable cost to disadvantaged and low-income groups. The

Smart Power for Rural Development

Smart Power for Rural Development The Challenge India s electrification challenge Largest un-electrified population in the world: 300+ mn people Even villages classified as electrified may have as few

Smart Power for Rural Development The Challenge India s electrification challenge Largest un-electrified population in the world: 300+ mn people Even villages classified as electrified may have as few

WOMEN ENTREPRENEURSHIP IN UNORGANISED SECTOR

Continuous issue-24 April May 2016 WOMEN ENTREPRENEURSHIP IN UNORGANISED SECTOR ABSTRACT The socioeconomic transformation of Indian society in the present century and especially in the postindependence

Continuous issue-24 April May 2016 WOMEN ENTREPRENEURSHIP IN UNORGANISED SECTOR ABSTRACT The socioeconomic transformation of Indian society in the present century and especially in the postindependence

Y V Reddy: Micro-finance - Reserve Bank s approach

Y V Reddy: Micro-finance - Reserve Bank s approach Address by Dr Y V Reddy, Governor of the Reserve Bank of India, at the Micro-Finance Conference organised by the Indian School of Business, Hyderabad,

Y V Reddy: Micro-finance - Reserve Bank s approach Address by Dr Y V Reddy, Governor of the Reserve Bank of India, at the Micro-Finance Conference organised by the Indian School of Business, Hyderabad,

Catalyzing Financial Inclusion

Catalyzing Financial Inclusion Through the CSCs An Implementation Handbook Contents Introduction 2 Salient Features of India s Financial Inclusion Strategy 3 Understanding the Business Correspondent Model

Catalyzing Financial Inclusion Through the CSCs An Implementation Handbook Contents Introduction 2 Salient Features of India s Financial Inclusion Strategy 3 Understanding the Business Correspondent Model

Financial Inclusion Glossary

Financial Inclusion Glossary In order to achieve full financial inclusion we must agree on what it means. Defining financial inclusion requires building out a shared language and describing how various

Financial Inclusion Glossary In order to achieve full financial inclusion we must agree on what it means. Defining financial inclusion requires building out a shared language and describing how various

MICRO FINANCE: A TOOL FOR SELF EMPLOYMENT WITH SPECIAL REFERENCE TO RURAL POOR

MICRO FINANCE: A TOOL FOR SELF EMPLOYMENT WITH SPECIAL REFERENCE Dr. Babaraju K. Bhatt* Ronak A. Mehta** TO RURAL POOR Abstract: Indian population comprises roughly one sixth of the world s population.

MICRO FINANCE: A TOOL FOR SELF EMPLOYMENT WITH SPECIAL REFERENCE Dr. Babaraju K. Bhatt* Ronak A. Mehta** TO RURAL POOR Abstract: Indian population comprises roughly one sixth of the world s population.

India s model of inclusive growth: Measures taken, experience gained and lessons learnt

India s model of inclusive growth: Measures taken, experience gained and lessons learnt Dr. Pronab Sen Principal Adviser Planning Commission Government of India Macro Economic Context High Growth trajectory-

India s model of inclusive growth: Measures taken, experience gained and lessons learnt Dr. Pronab Sen Principal Adviser Planning Commission Government of India Macro Economic Context High Growth trajectory-

Aarhat Multidisciplinary International Education Research Journal (AMIERJ) ISSN

ISSN") Page18 MICRO-FINANCE IN INDIA PROGRESS OF SHG-BANK LINKAGE PROGRAMME RAVINDER KUMAR Deptt. Of Commerce Kurukshetra University Kurukshetra RITIKA Deptt. Of Commerce Kurukshetra University Kurukshetra Abstract

Page18 MICRO-FINANCE IN INDIA PROGRESS OF SHG-BANK LINKAGE PROGRAMME RAVINDER KUMAR Deptt. Of Commerce Kurukshetra University Kurukshetra RITIKA Deptt. Of Commerce Kurukshetra University Kurukshetra Abstract

APMAS. Reaching the vulnerable with micro financial services. Presentation by CS Reddy

APMAS Self-help groups in India: Reaching the vulnerable with micro financial services Presentation by CS Reddy creddy@apmas.org European Microfinance Week Luxembourg, 13 th November 2008 About APMAS Vision:

APMAS Self-help groups in India: Reaching the vulnerable with micro financial services Presentation by CS Reddy creddy@apmas.org European Microfinance Week Luxembourg, 13 th November 2008 About APMAS Vision:

FINANCIAL INCLUSION AND SOCIAL CHANGES

FINANCIAL INCLUSION AND SOCIAL CHANGES Asst. Professor Poona College, Pune (MS) INDIA The concept of Inclusive growth was first envisaged in the Eleventh five year plan document which intended to achieve

FINANCIAL INCLUSION AND SOCIAL CHANGES Asst. Professor Poona College, Pune (MS) INDIA The concept of Inclusive growth was first envisaged in the Eleventh five year plan document which intended to achieve

MICROFINANCE IN INDIA: ITS ISSUES AND CHALLENGES

MICROFINANCE IN INDIA: ITS ISSUES AND CHALLENGES *Dr. Ambrish Assistant Professor, Department of Microfinance, Amity University, Lucknow,U.P ABSTRACT: Microfinance refers to small savings, credit and insurance

MICROFINANCE IN INDIA: ITS ISSUES AND CHALLENGES *Dr. Ambrish Assistant Professor, Department of Microfinance, Amity University, Lucknow,U.P ABSTRACT: Microfinance refers to small savings, credit and insurance

India & ICICI Group. Trends & Outlook. September 2015

India & ICICI Group Trends & Outlook September 2015 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

India & ICICI Group Trends & Outlook September 2015 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

The Global Findex Database. Adults with an account at a formal financial institution (%) OTHER BRICS ECONOMIES REST OF DEVELOPING WORLD

OTHER BRICS ECONOMIES REST OF DEVELOPING WORLD") 08 NOTE NUMBER FINDEX NOTES Asli Demirguc-Kunt Leora Klapper Douglas Randall WWW.WORLDBANK.ORG/GLOBALFINDEX FEBRUARY 2013 The Global Findex Database Financial Inclusion in India In India 35 percent of

08 NOTE NUMBER FINDEX NOTES Asli Demirguc-Kunt Leora Klapper Douglas Randall WWW.WORLDBANK.ORG/GLOBALFINDEX FEBRUARY 2013 The Global Findex Database Financial Inclusion in India In India 35 percent of

Learning Journey. FINO Fintech Foundation

Learning Journey FINO Fintech Foundation Leveraging technology-enabled banking agent distribution networks Contents Project Basics... 1 About the project... 1 Project Updates... 3 Key Indicators... 3 What

Learning Journey FINO Fintech Foundation Leveraging technology-enabled banking agent distribution networks Contents Project Basics... 1 About the project... 1 Project Updates... 3 Key Indicators... 3 What

African Journal of Hospitality, Tourism and Leisure Vol. 1 (3) - (2011) ISSN: Abstract

- (2011) ISSN: Abstract") African Journal of Hospitality, Tourism and Leisure Vol. 1 (3) - (2011) ISSN: 1819-2025 Micro-Women Entrepreneurship and its potential for hospitality and tourism related enterprises amongst others: a

African Journal of Hospitality, Tourism and Leisure Vol. 1 (3) - (2011) ISSN: 1819-2025 Micro-Women Entrepreneurship and its potential for hospitality and tourism related enterprises amongst others: a

Hawala cash transfers for food assistance and livelihood protection

Afghanistan Hawala cash transfers for food assistance and livelihood protection EUROPEAN COMMISSION Humanitarian Aid and Civil Protection In response to repeated flooding, ACF implemented a cash-based

Afghanistan Hawala cash transfers for food assistance and livelihood protection EUROPEAN COMMISSION Humanitarian Aid and Civil Protection In response to repeated flooding, ACF implemented a cash-based

Micro Finance in India A Key Driver for Inclusive and Sustainable Growth

Micro Finance in India A Key Driver for Inclusive and Sustainable Growth Vimal Nishant.R Associate Professor Excel Business School, Komarapalayam, TN - India Senthil Kumar.C Assistant Professor, K.S.Rangasamy

Micro Finance in India A Key Driver for Inclusive and Sustainable Growth Vimal Nishant.R Associate Professor Excel Business School, Komarapalayam, TN - India Senthil Kumar.C Assistant Professor, K.S.Rangasamy