Agricultural Credit: Institutions and Issues

|

|

|

- Lindsey Aleesha Martin

- 5 years ago

- Views:

Transcription

1 Jim Monke Specialist in Agricultural Policy June 18, 2014 Congressional Research Service RS21977

2 Summary The federal government provides credit assistance to farmers to help assure adequate and reliable lending in rural areas, particularly for farmers who cannot obtain loans elsewhere. Federal farm loan programs also target credit to beginning farmers and socially-disadvantaged groups. The primary federal lender to farmers, though with a small share of the market, is the Farm Service Agency (FSA) in the U.S. Department of Agriculture (USDA). Congress funds FSA loans with annual discretionary appropriations about $90 million of budget authority and $300 million for salaries to support $5.5 billion of new direct loans and guarantees. FSA issues direct loans to farmers who cannot qualify for regular credit and guarantees the repayment of loans made by other lenders. FSA thus is called a lender of last resort. Of about $309 billion in total farm debt, FSA provides about 2% through direct loans and guarantees about another 4%-5% of loans. Another federally related lender is the Farm Credit System (FCS) cooperatively owned and funded by the sale of bonds in the financial markets. Congress sets the statutes that govern the banks and lending associations, mandating that they serve agriculture-related borrowers. FCS makes loans to creditworthy farmers and is not a lender of last resort. FCS accounts for nearly 41% of farm debt and is the largest lender for farm real estate. Commercial banks are the other primary agricultural lender, holding slightly less than FCS with about 40% of total farm debt. Commercial banks are the largest lender for farm production loans. Generally speaking, the farm sector s balance sheet has remained strong in recent years. While delinquency rates on farm loans increased from 2008 into 2010, farmers and agricultural lenders did not face credit problems as severe as those of other economic sectors. Since 2010, loan repayment rates have improved. But appropriations for the FSA loan program and the ability of FSA to meet demand for its loans and guarantees have been constrained during an era of tight federal budgets. Congressional Research Service

3 Contents Current Situation... 1 Major Players and Market Shares... 1 The Farm Balance Sheet... 3 Delinquency Rates on Farm Loans... 5 Description of Government-Related Farm Lenders... 7 USDA s Farm Service Agency (FSA)... 7 Farm Credit System (FCS)... 7 Farmer Mac... 8 Recent Congressional Issues... 8 Credit Title in the 2014 Farm Bill... 8 Term Limits on USDA Farm Loans... 8 Figures Figure 1. Market Shares by Lender of Total Farm Debt, Figure 2. Market Shares of Real Estate Farm Debt, Figure 3. Market Shares of Non-Real Estate Farm Debt, Figure 4. Farm Assets, Figure 5. Farm Debt, Figure 6. Debt-to-Asset Ratio, Figure 7. Net Farm Income, Figure 8. Net Farm Income and Government Payments, Figure 9. Debt-to-Net Farm Income Ratio, Figure 10. Delinquency Rates on Loans at Commercial Banks, Figure 11. Nonperforming Farm Loans, Tables Table 1. Term Limits on Farm Service Agency Loans... 9 Contacts Author Contact Information... 9 Congressional Research Service

4 Current Situation Major Players and Market Shares The federal government has a long history of assisting farmers with obtaining loans for farming. This intervention has been justified at one time or another by many factors, including the presence of asymmetric information among lenders, asymmetric information between lenders and farmers, lack of competition in some rural lending markets, insufficient lending resources in rural areas compared to more populated areas, and the desire for targeted lending to disadvantaged groups (such as small farms or socially disadvantaged farmers). 1 Several types of lenders make loans to farmers. Some are government entities or have a statutory mandate to serve agriculture. The one most controlled by the federal government is the Farm Service Agency (FSA) in the U.S. Department of Agriculture (USDA). It receives federal appropriations to make direct loans to farmers and to issue guarantees on loans made by commercial lenders to farmers who do not qualify for regular credit. FSA is a lender of last resort, but also of first opportunity because it targets loans or reserves funds for disadvantaged groups. The lender with the next-largest amount of government intervention is the Farm Credit System (FCS). It is a cooperatively owned and funded but federally chartered private lender with a statutory mandate to serve agriculture-related borrowers only. FCS makes loans to creditworthy farmers, and is not a lender of last resort, but is a government-sponsored enterprise (GSE). Third is Farmer Mac, another GSE that is privately held, and provides a secondary market for agricultural loans. FSA, FCS, and Farmer Mac are described in more detail later in this report. Other lenders do not have direct government involvement in their funding or existence. These include commercial banks, life insurance companies, and individuals, merchants, and dealers. Figure 1 shows that the FCS and commercial banks provide most of the farm credit (40.7% and 39.6%, respectively), followed by individuals and others (11.5%), and life insurance companies (4.3%). FSA provides about 2.4% of the debt through direct loans. FSA also guarantees about another 4%-5% of the market through loans that are made by commercial banks and the FCS. The total amount of farm debt ($309 billion in 2013) is concentrated relatively more in real estate debt (59%) than in non-real estate debt (41%). FCS is the largest lender for real estate, although both commercial banks and FCS s shares have grown as others shares have decreased (Figure 2). Commercial banks are the largest lender for non-real estate loans, although FCS has gained share in recent years as the share by FSA and individuals and others has decreased (Figure 3). As the figures show, market shares among these lenders have changed over time. Commercial banks held relatively little farm real estate debt through 1985, but now hold a sizeable amount (Figure 2). The share of loans from individuals and others has steadily decreased over time, with fewer private contracts for farm real estate and relatively less dealer financing in operating credits. FSA held a much larger share of farm debt during the farm financial crisis of the 1980s, but that ratio declined as the farm economy improved through the 1990s (Figure 3). 1 USDA-FSA, Evaluating the Relative Cost Effectiveness of the Farm Service Agency s Farm Loan Programs, report to Congress, August 2006, pp , at Congressional Research Service 1

5 Figure 1. Market Shares by Lender of Total Farm Debt, Source: CRS, using USDA-ERS data at Notes: Shares in the graph are for direct loans; guarantees issued on other lenders loans are not shown. USDA-FSA issued guarantees on about 4%-5% of farm loans that are not shown separately but are included in the shares of commercial banks and the Farm Credit System. ERS began publishing data on Farmer Mac in Figure 2. Market Shares of Real Estate Farm Debt, (58% of total farm debt in 2012) Figure 3. Market Shares of Non-Real Estate Farm Debt, (42% of total farm debt in 2012) Source: CRS, using USDA-ERS data. Source: CRS, using USDA-ERS data. Congressional Research Service 2

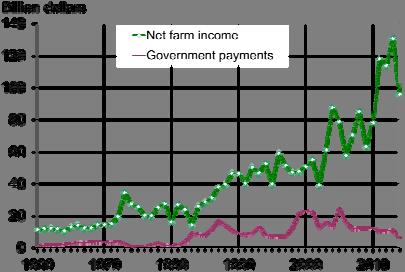

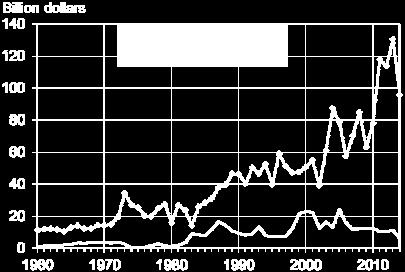

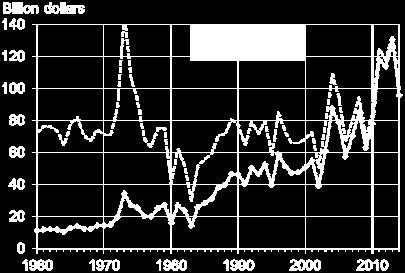

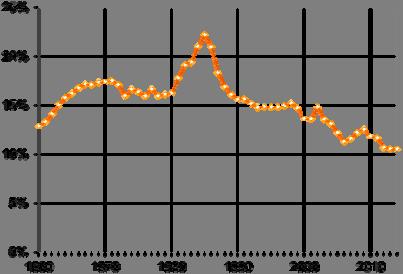

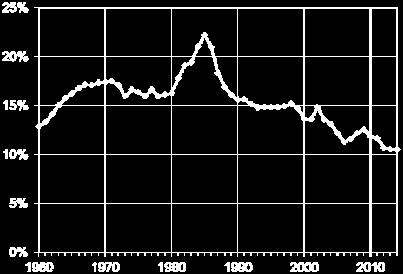

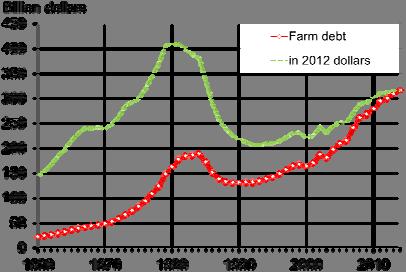

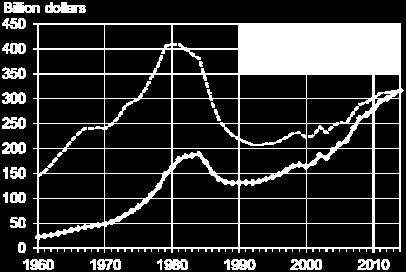

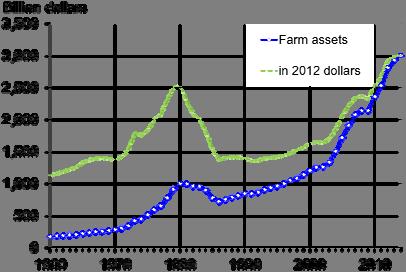

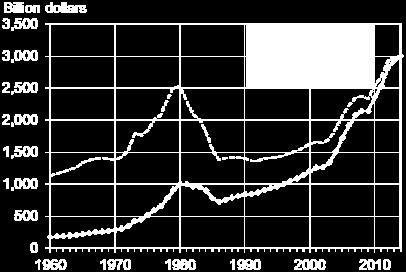

6 The Farm Balance Sheet As a whole, farm sector assets have remained strong despite pressure on other real estate sectors. The value of farm assets has grown steadily since the end of the 1980s, and particularly since At the end of 2013, farm assets reached nearly $3 trillion (Figure 4). These highs in total farm assets now exceed the previous peak from 1980 in inflation-adjusted terms. 2 Real estate is about 82% of the total amount of farm assets; machinery and vehicles are the next-largest category at about 9% of the total. 3 Farm debt reached a historic high of $309 billion at the end of 2013 (Figure 5). Debt is forecasted to rise 2.3% in In inflation-adjusted terms, however, this level of debt is still well below the peak debt levels of the 1980s. Debts and assets can be compared in a single measure by dividing debts by assets the debt-toasset ratio. A lower debt-to-asset ratio generally implies less financial risk to the sector than a higher ratio. Farm debt-to-asset ratio levels have declined fairly steadily since the late 1980s after the farm financial crisis, and reached a historic low of 10.5% in When farm asset growth paused in , the debt-to-asset ratio rose to 12.5% (Figure 6). However, by 2012, the debt-to-asset ratio had reached historically low levels. As a whole, farms are not as highly leveraged as they were in the farm financial crisis of the 1980s. Net farm income has become more variable, especially since After reaching historic highs in 2004, net farm income fell by a third into 2006 (Figure 7). After peaking again in 2008 at $85 billion, net farm income fell by one-quarter in one year to $63 billion in New highs were set in 2011 and 2013, but are expected to decline by 26% in 2014 albeit to a level only exceeded in Despite the severe declines in farm income in 2006, 2009, and 2014, the relative recent lows in net farm income are still higher than the inflation-adjusted lows from the farm financial crisis of the 1980s. 4 Government payments to farmers also have risen from decades ago, but do not always offset the variability in net farm income. Fixed direct payments that were not tied to prices or revenue were the primary form of government payments in recent years; these payments support farm income but do not necessarily help farmers manage risks. Figure 8 shows that more of net farm income is coming from the market rather than the government, compared to the 1980s. Another indicator of farmers leverage compares debt to net farm income. A lower debt-to-income ratio (with the ratio expressing the number of years of current income that debt represents) implies less financial leverage and risk. The farm-debt-to-net-farm-income ratio is more variable than the debt-to-asset ratio because of the variability of net farm income. It reached a 35-year low of 2.3 in 2004 and rose to 4.3 in 2009 before falling again to 2.4 in The expected decline in net income in 2014 would cause this measure to rise (Figure 9). These levels, while more variable than in the 1990s, are roughly within 50-year historical levels between 2 and 4, and are certainly less than from 1976 to 1986 (a period surrounding the 1980s financial crisis). 2 Comparisons are made to conditions in the 1980s because that was the last major financial crisis in agriculture. 3 USDA, Economic Research Service. Farm Sector Income Forecast. 4 For more information on farm income expectations, see CRS Report R40152, U.S. Farm Income, by Randy Schnepf. Congressional Research Service 3

7 Figure 4. Farm Assets, Figure 5. Farm Debt, Source: CRS, using USDA-ERS data at ers.usda.gov/data-products/farm-income-and-wealthstatistics.aspx forecast. Figure 6. Debt-to-Asset Ratio, Source: CRS, using USDA-ERS data at ers.usda.gov/data-products/farm-income-and-wealthstatistics.aspx forecast. Figure 7. Net Farm Income, Source: CRS, using USDA-ERS data at ers.usda.gov/data-products/farm-income-and-wealthstatistics.aspx forecast. Figure 8. Net Farm Income and Government Payments, Source: CRS, using USDA-ERS data at ers.usda.gov/data-products/farm-income-and-wealthstatistics.aspx forecast. Figure 9. Debt-to-Net Farm Income Ratio, Source: CRS, using USDA-ERS data at ers.usda.gov/data-products/farm-income-and-wealthstatistics.aspx forecast. Source: CRS, using USDA-ERS data at ers.usda.gov/data-products/farm-income-and-wealthstatistics.aspx forecast. Congressional Research Service 4

8 Delinquency Rates on Farm Loans While the global financial crisis was slower to affect the balance sheets of farmers and agricultural lenders than the housing market, its presence was observed in agricultural lending. Credit standards were tightened (more documentation and oversight of loans was required) and lenders sometimes made less credit available to producers. As the lender of last resort, the USDA Farm Service Agency experienced significantly higher demand for its direct loans and guarantees. In 2007, 2008, and 2010, farm commodity prices were particularly high, supporting farm income at above-average levels. But in 2006 and 2009, net farm income fell by about one-third (Figure 7), reducing some farmers ability to repay loans, particularly in some farm sectors such as dairy, hogs, and poultry. Recent strong farm income has improved most farmers ability to repay loans. Delinquency rates on residential mortgages began to rise in 2005, and for all loans particularly in Delinquencies include loans that are 30 days or more past due and still accruing interest, as well as those in nonaccrual status. The delinquency rates on residential mortgages and all loans appear to have reached a peak in mid-2010 (11.3% for residential mortgages and 7.4% for all commercial bank loans, Figure 10). The delinquency rates for agricultural loans did not begin to rise until mid-2008, after continuing to fall to historic lows while delinquencies were rising in residential mortgages and other loans. Moreover, the rate of increase in delinquencies on farm production loans at commercial banks has not been as sharp as in the non-farm sectors, and appears to have peaked in June 2010 at 3.3%. Delinquency rates on farm production loans at commercial banks have since returned to near-historic lows below 2%. 5 A more severe measure of loan performance is nonperforming loans. Nonperforming loans include nonaccrual loans and accruing loans 90 days or more past due. These loans are more in jeopardy than delinquent loans, and represent a smaller subset of loans. Within the agricultural loan portfolio, FCS nonperforming loans rose from 0.5% at the beginning of 2008 to a near-term peak of 2.8% on September 30, 2009, before decreasing again to about 1.1% as of March 31, 2014 (Figure 11). 6 The FCS nonperforming loan rate has returned to levels of the period after the system had finally recovered from the farm financial crisis of the 1980s. Nonperforming farm loans at commercial banks also rose but have declined to more normal levels. Nonperforming farm real estate loans at commercial banks rose from a low of 0.7% in December 2006 to 2.9% in March 2011, before declining to 1.5% as of December 31, Nonperforming farm production loans rose from a low of 0.6% in December 2006 to 2.4% in March 2010, before declining to 0.7% as of December 31, 2013 (Figure 11). 7 5 Federal Reserve Bank, Delinquency Rates on Loans at Commercial Banks (seasonally adjusted), at federalreserve.gov/releases/chargeoff. 6 Federal Farm Credit Banks Funding Corporation, First Quarter 2010 Quarterly Information Statement of the Farm Credit System, p. 9, May 10, 2010, at assetid= Federal Reserve Bank, Agricultural Finance Data Book, Tables B.2 and B.4, at research/indicatorsdata/agfinance/index.cfm. Congressional Research Service 5

9 Figure 10. Delinquency Rates on Loans at Commercial Banks, Source: Compiled by CRS. Data through March 31, 2014, using Federal Reserve Bank, Delinquency Rates on Loans at Commercial Banks (seasonally adjusted), at Notes: Delinquencies include loans that are 30 days or more past due and still accruing interest, as well as those in nonaccrual status. The amounts are percentages of end-of-period loans. Figure 11. Nonperforming Farm Loans, Source: Compiled by CRS. Federal Farm Credit Banks Funding Corp. data through March 31, 2014, at Federal Reserve Bank, Agricultural Finance Data Book, Tables B.2 and B.4, through December 31, 2013, at Notes: Nonperforming loans include nonaccrual loans and accruing loans 90 days or more past due. The amounts are percentages of total loans. Congressional Research Service 6

10 Description of Government-Related Farm Lenders USDA s Farm Service Agency (FSA) USDA s Farm Service Agency is a lender of last resort because it makes direct farm ownership and operating loans to family-sized farms that are unable to obtain credit elsewhere. 8 FSA also guarantees timely payment of principal and interest on qualified loans made by commercial lenders such as commercial banks and FCS. Permanent authority exists in the Consolidated Farm and Rural Development Act (CONACT, 7 U.S.C et seq.). Prior to the banking crisis in 2008, FSA usually made and guaranteed about $3.5 billion of farm loans annually. Supplemental appropriations during the financial crisis raised FSA loan activity to about $6.0 billion in FY2010. In FY2014, an appropriation of $90 million in budget authority (and $300 million for salaries) supports the issuance of $5.5 billion of new direct loans and guarantees. 9 Direct loans are limited to $300,000 per borrower ($35,000 for microloans), and guaranteed loans to $1,355,000 per borrower (adjusted annually for inflation). Direct emergency loans are available for disasters. Part of the FSA loan program is reserved for beginning farmers and ranchers (7 U.S.C (b)(2)). For direct loans, 75% of the funding for farm ownership loans and 50% of operating loans are reserved for the first 11 months of the fiscal year. For guaranteed loans, 40% is reserved for ownership loans and farm operating loans for the first half of the fiscal year. Funds are also targeted to socially disadvantaged farmers by race, gender, and ethnicity (7 U.S.C. 2003). Because of these provisions, FSA also is known as lender of first opportunity for borrowers who are not yet creditworthy for regular commercial business loans. Farm Credit System (FCS) Congress established the Farm Credit System in 1916 to provide a dependable and affordable source of credit to rural areas at a time when commercial lenders avoided farm loans. FCS is neither a government agency nor guaranteed by the U.S. government, but is a network of borrower-owned lending institutions operating as a government-sponsored enterprise (GSE). It is not a lender of last resort; it is a for-profit lender with a statutory mandate to serve agriculture. Funds are raised through the sale of bonds on Wall Street. 10 Four large banks allocate these funds to 82 credit associations 11 that, in turn, make loans to eligible creditworthy borrowers. FCS is unique among the GSEs because it is a retail lender making loans directly to farmers, and thus is in direct competition with commercial banks. Statutes and oversight by the House and Senate Agriculture Committees determine the scope of FCS activity. Benefits such as tax exemptions also are provided. Eligibility is limited to farmers, 8 U.S. Department of Agriculture, Farm Service Agency, Farm Loan Program, at 9 CRS Report R43110, Agriculture and Related Agencies: FY2014 and FY2013 (Post-Sequestration) Appropriations. 10 Federal Farm Credit Banks Funding Corporation, Overview, overview.html. 11 Farm Credit Administration, Number of FCS Banks and Associations, at number_of_fcs_institutions.html. Congressional Research Service 7

11 farm input suppliers, rural homeowners in towns under 2,500 population, and cooperatives. The federal regulator is the Farm Credit Administration (FCA). Farmer Mac Farmer Mac is a separate GSE that is a secondary market for agricultural loans. 12 It is related to the FCS in that FCA is its regulator and it was created by the same legislation, but it is a financially separate entity. Farmer Mac purchases mortgages from lenders and guarantees mortgage-backed securities that are bought by investors. Permanent authority rests in the Farm Credit Act of 1971 (12 U.S.C et seq.). Recent Congressional Issues Credit Title in the 2014 Farm Bill 13 The enacted 2014 farm bill (P.L ) makes relatively small policy changes to USDA s credit programs. It gives USDA discretion to recognize alternative legal entities to qualify for farm loans and allow alternatives to meet a three-year farming experience requirement. It increases the maximum size of down-payment loans and eliminates term limits on guaranteed operating loans (by removing a maximum number of years that an individual can remain eligible). It increases the percentage of a conservation loan that can be guaranteed, adds another lending priority for beginning farmers, and facilitates loans for the purchase of highly fractionated land in Indian reservations, among other changes. Term Limits on USDA Farm Loans Congress added term limits to the USDA farm loan program in 1992 and 1996 to restrict eligibility for government farm loans and encourage farmers to graduate to commercial loans. The term limits place a maximum number of years that farmers are eligible for certain types of FSA loans or guarantees. However, until the end of 2010, Congress had suspended application of one of the term limits to prevent some farmers from being denied credit. The 2014 farm bill eliminated term limits on guaranteed operating loans (Table 1). 12 Federal Farm Credit Banks Funding Corporation, FarmerMac, at fcsystem/overview_farmer_mac.jsp. 13 CRS Report R43076, The 2014 Farm Bill (P.L ): Summary and Side-by-Side. Congressional Research Service 8

12 Farm Operating Loans Direct operating loans are limited to a six-year period. In certain cases, borrowers may qualify for a one-time, two-year extension (7 U.S.C. 1941(c)(1)(C) and (c)(4)). 14 Guaranteed operating loans have no term limit (a change in the 2014 farm bill). 15 Farm Ownership Loans A borrower is eligible for direct farm ownership (real estate) loans for a maximum of 10 years after the first loan is made (7 U.S.C. 1922(b)(1)(C)). There is no time limit on eligibility for guaranteed farm ownership loans. 16 Table 1. Term Limits on Farm Service Agency Loans Maximum number of years that farmers are eligible for loans Type of FSA Loan Direct loans term limits Guaranteed loans term limits Farm Operating Loans (OL) 6 years, plus possible 2-yr. extension No term limit a Farm Ownership Loans (FO) 10 years No term limit Source: CRS, based on statute and unpublished USDA data. Note: Term limits are separate from the maximum maturity or duration of an individual loan, which may be as long as 40 years for a farm ownership loan or as short as 1 year for a farm operating loan. a. Prior to the 2014 farm bill, guaranteed operating loans were limited to a 15-year period. Enforcement of that term limit, however, had been suspended by statute until December 31, Author Contact Information Jim Monke Specialist in Agricultural Policy jmonke@crs.loc.gov, In June 2009, USDA said that about 4,800 FSA borrowers were limited to one more year of direct operating loans, and another 7,800 borrowers were limited to two more years. USDA did not expect many of these borrowers to graduate to commercial credit (Doug Caruso, FSA Administrator, in testimony before the House Agriculture Subcommittee on Conservation, Credit, Energy and Research, June 11, 2009, at 111/h061109sc/Caruso.doc). 15 Prior to the 2014 farm bill, guaranteed operating loans were limited to a 15-year period (former 7 U.S.C. 1949(b)(1)). However, enforcement of that term limit was suspended by statute until December 31, Upon expiration of the suspension, the 15-year term limit applied from USDA had said that about 1,600 borrowers had reached the guaranteed term limit and would not qualify for additional operating loan guarantees (personal communication with House Agriculture Committee and USDA farm loan staff, December 2010). 16 USDA-FSA, Evaluating the Relative Cost Effectiveness of the Farm Service Agency s Farm Loan Programs, Report to Congress, August 2006, p. 76, at Congressional Research Service 9

Agricultural Credit: Institutions and Issues

Jim Monke Specialist in Agricultural Policy November 5, 2015 Congressional Research Service 7-5700 www.crs.gov RS21977 Summary The federal government provides credit assistance to farmers to help assure

Jim Monke Specialist in Agricultural Policy November 5, 2015 Congressional Research Service 7-5700 www.crs.gov RS21977 Summary The federal government provides credit assistance to farmers to help assure

Agricultural Credit: Institutions and Issues

Jim Monke Specialist in Agricultural Policy March 26, 2018 Congressional Research Service 7-5700 www.crs.gov RS21977 Summary The federal government provides credit assistance to farmers to help assure

Jim Monke Specialist in Agricultural Policy March 26, 2018 Congressional Research Service 7-5700 www.crs.gov RS21977 Summary The federal government provides credit assistance to farmers to help assure

Farm Credit System. Jim Monke Specialist in Agricultural Policy. May 17, Congressional Research Service

Jim Monke Specialist in Agricultural Policy May 17, 2016 Congressional Research Service 7-5700 www.crs.gov RS21278 Summary The Farm Credit System (FCS) is a nationwide financial cooperative lending to

Jim Monke Specialist in Agricultural Policy May 17, 2016 Congressional Research Service 7-5700 www.crs.gov RS21278 Summary The Farm Credit System (FCS) is a nationwide financial cooperative lending to

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21278 Farm Credit System Jim Monke, Resources, Science and Industry Division June 12, 2007 Abstract. The Farm Credit

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21278 Farm Credit System Jim Monke, Resources, Science and Industry Division June 12, 2007 Abstract. The Farm Credit

Summary As households and taxpayers, Americans have a large stake in the future of Fannie Mae and Freddie Mac. Homeowners and potential homeowners ind

Proposals to Reform Fannie Mae and Freddie Mac in the 112 th Congress N. Eric Weiss Specialist in Financial Economics May 18, 2011 Congressional Research Service CRS Report for Congress Prepared for Members

Proposals to Reform Fannie Mae and Freddie Mac in the 112 th Congress N. Eric Weiss Specialist in Financial Economics May 18, 2011 Congressional Research Service CRS Report for Congress Prepared for Members

Expiring Farm Bill Programs Without a Budget Baseline

Expiring Farm Bill Programs Without a Budget Baseline Jim Monke Specialist in Agricultural Policy March 30, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

Expiring Farm Bill Programs Without a Budget Baseline Jim Monke Specialist in Agricultural Policy March 30, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

Agricultural Credit Policy

Agricultural Credit Policy Steven R. Koenig, Economic Research Service, USDA Damona G. Doye, Oklahoma State University Background Modern agricultural production systems are capital intensive, but relatively

Agricultural Credit Policy Steven R. Koenig, Economic Research Service, USDA Damona G. Doye, Oklahoma State University Background Modern agricultural production systems are capital intensive, but relatively

Testimony of. Matthew H. Williams AMERICAN BANKERS ASSOCIATION. Subcommittee on Department Operations, Oversight, and Credit.

Testimony of Matthew H. Williams On Behalf of the AMERICAN BANKERS ASSOCIATION Before the Subcommittee on Department Operations, Oversight, and Credit of the House Committee on Agriculture United States

Testimony of Matthew H. Williams On Behalf of the AMERICAN BANKERS ASSOCIATION Before the Subcommittee on Department Operations, Oversight, and Credit of the House Committee on Agriculture United States

By providing access to credit, FSA s Farm Loan Programs offer opportunities to:

By providing access to credit, FSA s Farm Loan Programs offer opportunities to: Start, improve, expand, transition, market, and strengthen family farming and ranching operations. Provide viable farming

By providing access to credit, FSA s Farm Loan Programs offer opportunities to: Start, improve, expand, transition, market, and strengthen family farming and ranching operations. Provide viable farming

Farm Bill Programs Without a Budget Baseline Beyond FY2018

Farm Bill Programs Without a Budget Baseline Beyond FY2018 Jim Monke Specialist in Agricultural Policy July 21, 2017 Congressional Research Service 7-5700 www.crs.gov R44758 Summary The 2014 farm bill

Farm Bill Programs Without a Budget Baseline Beyond FY2018 Jim Monke Specialist in Agricultural Policy July 21, 2017 Congressional Research Service 7-5700 www.crs.gov R44758 Summary The 2014 farm bill

Agricultural Income and Finance Annual Lender Issue

United States Department of Agriculture AIS-78 Feb. 26, 2002 Electronic Outlook Report from the Economic Research Service www.ers.usda.gov Agricultural Income and Finance Annual Lender Issue Jerome Stam,

United States Department of Agriculture AIS-78 Feb. 26, 2002 Electronic Outlook Report from the Economic Research Service www.ers.usda.gov Agricultural Income and Finance Annual Lender Issue Jerome Stam,

Agricultural Disaster Assistance

Order Code RS21212 Updated July 3, 2008 Summary Agricultural Disaster Assistance Ralph M. Chite Specialist in Agricultural Policy Resources, Science, and Industry Division The U.S. Department of Agriculture

Order Code RS21212 Updated July 3, 2008 Summary Agricultural Disaster Assistance Ralph M. Chite Specialist in Agricultural Policy Resources, Science, and Industry Division The U.S. Department of Agriculture

U.S. agriculture depends on capital for its

Capital for Agriculture and Rural America: Redefining the Federal Role By Mark Drabenstott U.S. agriculture depends on capital for its success. Nearly a trillion dollars of capital is at work in production

Capital for Agriculture and Rural America: Redefining the Federal Role By Mark Drabenstott U.S. agriculture depends on capital for its success. Nearly a trillion dollars of capital is at work in production

FSA Direct Loans Loan Making

FSA Direct Loans Loan Making CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can

FSA Direct Loans Loan Making CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can

CRS Report for Congress

Order Code RS21278 Updated November 23, 2005 CRS Report for Congress Received through the CRS Web Summary Farm Credit System Jim Monke Analyst in Agricultural Policy Resources, Science, and Industry Division

Order Code RS21278 Updated November 23, 2005 CRS Report for Congress Received through the CRS Web Summary Farm Credit System Jim Monke Analyst in Agricultural Policy Resources, Science, and Industry Division

Department of Economics. Financial Intermediation in Agriculture Chapter 15, 16 & 17

Financial Intermediation in Agriculture Chapter 15, 16 & 17 Who has worked for a financial institution? What did you do? For whom? Functions of a financial intermediaries 1. Origination Create the financial

Financial Intermediation in Agriculture Chapter 15, 16 & 17 Who has worked for a financial institution? What did you do? For whom? Functions of a financial intermediaries 1. Origination Create the financial

and Finance Situation and Outlook Report Total farm business debt held by commercial banks, the Farm Credit System, and the Farm Service Agency

United States Department of Agriculture ERS Agricultural Income Economic Research Service AIS-76 February 2001 and Finance Situation and Outlook Report Total farm business debt held by commercial banks,

United States Department of Agriculture ERS Agricultural Income Economic Research Service AIS-76 February 2001 and Finance Situation and Outlook Report Total farm business debt held by commercial banks,

Statement for the Record AMERICAN BANKERS ASSOCIATION. House Agriculture Committee. United States House of Representatives

March 29, 2017 Statement for the Record On behalf of the AMERICAN BANKERS ASSOCIATION before the House Agriculture Committee of the United States House of Representatives Statement for the Record On behalf

March 29, 2017 Statement for the Record On behalf of the AMERICAN BANKERS ASSOCIATION before the House Agriculture Committee of the United States House of Representatives Statement for the Record On behalf

Payment Limits for Farm Commodity Programs: Issues and Proposals

Order Code RS21493 Updated March 12, 2007 Summary Payment Limits for Farm Commodity Programs: Issues and Proposals Jim Monke Analyst in Agricultural Economics Resources, Science, and Industry Division

Order Code RS21493 Updated March 12, 2007 Summary Payment Limits for Farm Commodity Programs: Issues and Proposals Jim Monke Analyst in Agricultural Economics Resources, Science, and Industry Division

GOVERNMENT-SPONSORED ENTERPRISES

GOVERNMENT-SPONSORED ENTERPRISES This chapter contains descriptions of and data on the Government-sponsored enterprises listed below. These enterprises were established and chartered by the Federal Government.

GOVERNMENT-SPONSORED ENTERPRISES This chapter contains descriptions of and data on the Government-sponsored enterprises listed below. These enterprises were established and chartered by the Federal Government.

Budget Issues Shaping a 2012 Farm Bill

Jim Monke Specialist in Agricultural Policy June 1, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov R42484 Summary Budget

Jim Monke Specialist in Agricultural Policy June 1, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov R42484 Summary Budget

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS22336 GSE Reform: A New Affordable Housing Fund N. Eric Weiss, Government and Finance Division January 5, 2007 Abstract.

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS22336 GSE Reform: A New Affordable Housing Fund N. Eric Weiss, Government and Finance Division January 5, 2007 Abstract.

Agricultural Income and Finance

USDA United States Department of Agriculture ERS Economic Research Service AIS-74 February 2000 Agricultural Income and Finance Situation and Outlook Report Direct government payments are important to

USDA United States Department of Agriculture ERS Economic Research Service AIS-74 February 2000 Agricultural Income and Finance Situation and Outlook Report Direct government payments are important to

Statement for the Record. American Bankers Association

Statement for the Record On behalf of the American Bankers Association Senate Agriculture, Rural Development, Food and Drug Administration, and Related Agencies Appropriations Subcommittee of the United

Statement for the Record On behalf of the American Bankers Association Senate Agriculture, Rural Development, Food and Drug Administration, and Related Agencies Appropriations Subcommittee of the United

CRS Report for Congress

Order Code RS21604 Updated December 15, 2004 CRS Report for Congress Received through the CRS Web Marketing Loans, Loan Deficiency Payments, and Commodity Certificates Summary Jim Monke Analyst in Agricultural

Order Code RS21604 Updated December 15, 2004 CRS Report for Congress Received through the CRS Web Marketing Loans, Loan Deficiency Payments, and Commodity Certificates Summary Jim Monke Analyst in Agricultural

Commodities, Credit, & Crop Insurance:

Commodities, Credit, & Crop Insurance: Perspectives on Risk Management Tools and Trends for the 2018 Farm Bill Brenda Kluesner Independent Community Bankers of America U.S. Senate Committee on Agriculture,

Commodities, Credit, & Crop Insurance: Perspectives on Risk Management Tools and Trends for the 2018 Farm Bill Brenda Kluesner Independent Community Bankers of America U.S. Senate Committee on Agriculture,

CRS Report for Congress

Order Code RS22336 November 28, 2005 CRS Report for Congress Received through the CRS Web GSE Reform: A New Affordable Housing Fund Summary Eric Weiss Analyst in Financial Institutions Government and Finance

Order Code RS22336 November 28, 2005 CRS Report for Congress Received through the CRS Web GSE Reform: A New Affordable Housing Fund Summary Eric Weiss Analyst in Financial Institutions Government and Finance

Testimony of. Leonard Wolfe AMERICAN BANKERS ASSOCIATION. Subcommittee on Livestock, Rural Development, and Credit. of the

Testimony of Leonard Wolfe On Behalf of the AMERICAN BANKERS ASSOCIATION before the Subcommittee on Livestock, Rural Development, and Credit of the House Committee on Agriculture United States House of

Testimony of Leonard Wolfe On Behalf of the AMERICAN BANKERS ASSOCIATION before the Subcommittee on Livestock, Rural Development, and Credit of the House Committee on Agriculture United States House of

2017 Farm Bank Performance Report

2017 Farm Bank Performance Report 2017 Farm Bank Performance Report Key Findings The banking industry is the nation s most important supplier of credit to agriculture providing nearly 50 percent of all

2017 Farm Bank Performance Report 2017 Farm Bank Performance Report Key Findings The banking industry is the nation s most important supplier of credit to agriculture providing nearly 50 percent of all

Leverage of U.S. Farmers: A Deeper Perspective

1 st Quarter 2016 Leverage of U.S. Farmers: A Deeper Perspective Paul Ellinger, Allen Featherstone, and Michael Boehlje JEL Classifications: G21, Q10, Q14, Q18 Keywords: Farm Finance, Financial Stress,

1 st Quarter 2016 Leverage of U.S. Farmers: A Deeper Perspective Paul Ellinger, Allen Featherstone, and Michael Boehlje JEL Classifications: G21, Q10, Q14, Q18 Keywords: Farm Finance, Financial Stress,

FEDERAL AGRICULTURAL MORTGAGE CORPORATION Universal Debt Facility Discount Notes and Medium-Term Notes

OFFERING CIRCULAR FEDERAL AGRICULTURAL MORTGAGE CORPORATION Universal Debt Facility Discount Notes and Medium-Term Notes Offered Securities... Discount Notes and Medium-Term Notes (collectively, the Notes

OFFERING CIRCULAR FEDERAL AGRICULTURAL MORTGAGE CORPORATION Universal Debt Facility Discount Notes and Medium-Term Notes Offered Securities... Discount Notes and Medium-Term Notes (collectively, the Notes

Farmers have significantly increased their debt levels

2010 Debt, Income and Farm Financial Stress By Brian C. Briggeman, Economist, Federal Reserve Bank of Kansas City Farmers have significantly increased their debt levels in recent years. Since 2004, real

2010 Debt, Income and Farm Financial Stress By Brian C. Briggeman, Economist, Federal Reserve Bank of Kansas City Farmers have significantly increased their debt levels in recent years. Since 2004, real

Fannie Mae and Freddie Mac in Conservatorship

Order Code RS22950 September 15, 2008 Fannie Mae and Freddie Mac in Conservatorship Mark Jickling Specialist in Financial Economics Government and Finance Division Summary On September 7, 2008, the Federal

Order Code RS22950 September 15, 2008 Fannie Mae and Freddie Mac in Conservatorship Mark Jickling Specialist in Financial Economics Government and Finance Division Summary On September 7, 2008, the Federal

Testimony of. Shan Hanes AMERICAN BANKERS ASSOCIATION. Agriculture, Nutrition and Forestry Committee. United States Senate

Testimony of Shan Hanes On Behalf of the AMERICAN BANKERS ASSOCIATION before the Agriculture, Nutrition and Forestry Committee United States Senate Testimony of Shan Hanes On behalf of the American Bankers

Testimony of Shan Hanes On Behalf of the AMERICAN BANKERS ASSOCIATION before the Agriculture, Nutrition and Forestry Committee United States Senate Testimony of Shan Hanes On behalf of the American Bankers

Chapter 4. Agricultural Finance Calum G. Turvey, W.I. Myers Professor of Agricultural Finance

Chapter 4. Calum G. Turvey, W.I. Myers Professor of General Outlook The financial condition of New York s agricultural economy in 2014 is holding steady if not improving over 2013. Although there is some

Chapter 4. Calum G. Turvey, W.I. Myers Professor of General Outlook The financial condition of New York s agricultural economy in 2014 is holding steady if not improving over 2013. Although there is some

Statement for the Record. American Bankers Association. Agriculture Committee. United States House of Representatives

Statement for the Record On Behalf of the American Bankers Association before the Agriculture Committee of the United States House of Representatives Statement for the Record On behalf of the American

Statement for the Record On Behalf of the American Bankers Association before the Agriculture Committee of the United States House of Representatives Statement for the Record On behalf of the American

Testimony of. Leonard Wolfe AMERICAN BANKERS ASSOCIATION. Agriculture, Nutrition and Forestry Committee. United States Senate

Testimony of Leonard Wolfe On Behalf of the AMERICAN BANKERS ASSOCIATION before the Agriculture, Nutrition and Forestry Committee United States Senate Testimony of Leonard Wolfe On behalf of the American

Testimony of Leonard Wolfe On Behalf of the AMERICAN BANKERS ASSOCIATION before the Agriculture, Nutrition and Forestry Committee United States Senate Testimony of Leonard Wolfe On behalf of the American

United States General Accounting Office. Before the Subcommittee on Conservation, Credit, and Rural Development, House Committee on Agriculture

GAO United States General Accounting Office Testimony Before the Subcommittee on Conservation, Credit, and Rural Development, House Committee on Agriculture For Release on Delivery Expected at 10:00 a.m.,

GAO United States General Accounting Office Testimony Before the Subcommittee on Conservation, Credit, and Rural Development, House Committee on Agriculture For Release on Delivery Expected at 10:00 a.m.,

THE ROLE OF DEBT IN FARMLAND OWNERSHIP

2nd Quarter 2011 26(2) THE ROLE OF DEBT IN FARMLAND OWNERSHIP Brian C. Briggeman JEL Classifications: Q14, Q15 Keywords: Agricultural Finance, Debt, Farmland Farm real estate debt often plays a key role

2nd Quarter 2011 26(2) THE ROLE OF DEBT IN FARMLAND OWNERSHIP Brian C. Briggeman JEL Classifications: Q14, Q15 Keywords: Agricultural Finance, Debt, Farmland Farm real estate debt often plays a key role

2018 SECOND QUARTER REPORT

2018 SECOND QUARTER REPORT SECOND QUARTER 2018 Table of Contents Report on Internal Control Over Financial Reporting... 2 Management s Discussion and Analysis of Financial Condition and Results of Operations...

2018 SECOND QUARTER REPORT SECOND QUARTER 2018 Table of Contents Report on Internal Control Over Financial Reporting... 2 Management s Discussion and Analysis of Financial Condition and Results of Operations...

Agricultural Disaster Assistance

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Congressional Research Service Reports Congressional Research Service 2010 Agricultural Disaster Assistance Dennis A. Shields

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Congressional Research Service Reports Congressional Research Service 2010 Agricultural Disaster Assistance Dennis A. Shields

FSA Guaranteed Loans

FSA Guaranteed Loans CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can change

FSA Guaranteed Loans CAUTION: This is an outline for educational purposes only. To learn the details about any certain point, read the current statutes, regulations, and policy notices, which can change

Agricultural Income and Finance Annual Lender Issue

United States Department of Agriculture AIS-80 March 11, 2003 Electronic Outlook Report from the Economic Research Service www.ers.usda.gov Agricultural Income and Finance Annual Lender Issue Jerome Stam,

United States Department of Agriculture AIS-80 March 11, 2003 Electronic Outlook Report from the Economic Research Service www.ers.usda.gov Agricultural Income and Finance Annual Lender Issue Jerome Stam,

Farm Bill Programs Without a Budget Baseline Beyond FY2018

Farm Bill Programs Without a Budget Baseline Beyond FY2018 name redacted Specialist in Agricultural Policy February 7, 2017 Congressional Research Service 7-... www.crs.gov R44758 Summary The 2014 farm

Farm Bill Programs Without a Budget Baseline Beyond FY2018 name redacted Specialist in Agricultural Policy February 7, 2017 Congressional Research Service 7-... www.crs.gov R44758 Summary The 2014 farm

FALL 2018 AGRICULTURAL LENDER SURVEY RESULTS

FALL 2018 AGRICULTURAL LENDER SURVEY RESULTS A Contents Key Takeaways... 2 Introduction... 3 Agricultural Economy... 4 Farm Profitability and Economic Conditions... 4 Land Values and Cash Rent Levels...

FALL 2018 AGRICULTURAL LENDER SURVEY RESULTS A Contents Key Takeaways... 2 Introduction... 3 Agricultural Economy... 4 Farm Profitability and Economic Conditions... 4 Land Values and Cash Rent Levels...

FHA-Insured Home Loans: An Overview

Katie Jones Analyst in Housing Policy March 28, 2018 Congressional Research Service 7-5700 www.crs.gov RS20530 Summary The Federal Housing Administration (FHA), an agency of the Department of Housing and

Katie Jones Analyst in Housing Policy March 28, 2018 Congressional Research Service 7-5700 www.crs.gov RS20530 Summary The Federal Housing Administration (FHA), an agency of the Department of Housing and

NORTH CAROLINA AGRICULTURAL FINANCE AUTHORITY

NORTH CAROLINA AGRICULTURAL FINANCE AUTHORITY Mission Statement The North Carolina Agricultural Finance Authority (NCAFA) was established by the North Carolina General Assembly to provide credit to agriculture

NORTH CAROLINA AGRICULTURAL FINANCE AUTHORITY Mission Statement The North Carolina Agricultural Finance Authority (NCAFA) was established by the North Carolina General Assembly to provide credit to agriculture

2017 Quarterly Report SEPTEMBER 30, 2017

2017 Quarterly Report SEPTEMBER 30, 2017 Dear CoBank Customer-Owner: We re pleased to report that CoBank recorded solid financial performance in the third quarter of 2017. Though quarterly net income declined

2017 Quarterly Report SEPTEMBER 30, 2017 Dear CoBank Customer-Owner: We re pleased to report that CoBank recorded solid financial performance in the third quarter of 2017. Though quarterly net income declined

The ABA Advantage: Agricultural Banking Update & Resources BANKERS aba.com

The ABA Advantage: Agricultural Banking Update & Resources aba.com Meet today s speakers Ed Elfmann Vice President ABA Center for Agriculture and Rural Banking Sarah Grano Vice President Public Relations

The ABA Advantage: Agricultural Banking Update & Resources aba.com Meet today s speakers Ed Elfmann Vice President ABA Center for Agriculture and Rural Banking Sarah Grano Vice President Public Relations

Improper Payments in High-Priority Programs: In Brief

Improper Payments in High-Priority Programs: In Brief Garrett Hatch Specialist in American National Government July 16, 8 Congressional Research Service 7-5700 www.crs.gov R45257 Improper Payments in High-Priority

Improper Payments in High-Priority Programs: In Brief Garrett Hatch Specialist in American National Government July 16, 8 Congressional Research Service 7-5700 www.crs.gov R45257 Improper Payments in High-Priority

Florida: An Economic Overview

Florida: An Economic Overview August 21, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview August 21, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

The Loan Limits for Government-Backed Mortgages

The Loan Limits for Government-Backed Mortgages N. Eric Weiss Specialist in Financial Economics Katie Jones Analyst in Housing Policy Libby Perl Specialist in Housing Policy Tadlock Cowan Analyst in Natural

The Loan Limits for Government-Backed Mortgages N. Eric Weiss Specialist in Financial Economics Katie Jones Analyst in Housing Policy Libby Perl Specialist in Housing Policy Tadlock Cowan Analyst in Natural

Report on Staff Visit to Washington, D.C. October 9 13, 2017

Report on Staff Visit to Washington, D.C. October 9 13, 2017 During the week of October 9, 2017, CBAI s Vice President of Federal Governmental Relations, David Schroeder, visited the offices of every member

Report on Staff Visit to Washington, D.C. October 9 13, 2017 During the week of October 9, 2017, CBAI s Vice President of Federal Governmental Relations, David Schroeder, visited the offices of every member

Early Withdrawals and Required Minimum Distributions in Retirement Accounts: Issues for Congress

Early Withdrawals and Required Minimum Distributions in Retirement Accounts: Issues for Congress John J. Topoleski Analyst in Income Security January 7, 2011 Congressional Research Service CRS Report for

Early Withdrawals and Required Minimum Distributions in Retirement Accounts: Issues for Congress John J. Topoleski Analyst in Income Security January 7, 2011 Congressional Research Service CRS Report for

2018 THIRD QUARTER REPORT

2018 THIRD QUARTER REPORT THIRD QUARTER 2018 Table of Contents Report on Internal Control Over Financial Reporting... 2 Management s Discussion and Analysis of Financial Condition and Results of Operations...

2018 THIRD QUARTER REPORT THIRD QUARTER 2018 Table of Contents Report on Internal Control Over Financial Reporting... 2 Management s Discussion and Analysis of Financial Condition and Results of Operations...

Fannie Mae and Freddie Mac. Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons

Fannie Mae and Freddie Mac Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons Origins of Fannie Mae Great Depression New Deal Personal income, tax revenue, profits, and prices all drop

Fannie Mae and Freddie Mac Joseph Dashevsky, Nicole Davessar, Sarah Nicholson, and Scott Symons Origins of Fannie Mae Great Depression New Deal Personal income, tax revenue, profits, and prices all drop

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE CBO. The Budget and Economic Outlook: Fiscal Years 2013 to 2023

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: Fiscal Years 2013 to 2023 Percentage of GDP 120 100 Actual Projected 80 60 40 20 0 1940 1945 1950 1955 1960 1965

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: Fiscal Years 2013 to 2023 Percentage of GDP 120 100 Actual Projected 80 60 40 20 0 1940 1945 1950 1955 1960 1965

November 14, The Honorable Melvin L. Watt Director Federal Housing Finance Agency th St SW Washington, DC 20219

November 14, 2018 The Honorable Melvin L. Watt Director Federal Housing Finance Agency 400 7 th St SW Washington, DC 20219 Re: Enterprise Capital Rules; RIN 2590-AA95 Dear Director Watt: The Independent

November 14, 2018 The Honorable Melvin L. Watt Director Federal Housing Finance Agency 400 7 th St SW Washington, DC 20219 Re: Enterprise Capital Rules; RIN 2590-AA95 Dear Director Watt: The Independent

The Budget Control Act of 2011: Effects on Spending Levels and the Budget Deficit

The Budget Control Act of 2011: Effects on Spending Levels and the Budget Deficit Marc Labonte Specialist in Macroeconomic Policy Mindy R. Levit Analyst in Public Finance November 29, 2011 CRS Report for

The Budget Control Act of 2011: Effects on Spending Levels and the Budget Deficit Marc Labonte Specialist in Macroeconomic Policy Mindy R. Levit Analyst in Public Finance November 29, 2011 CRS Report for

Farm Finance Update. Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City. March 17, 2017

Farm Finance Update March 17, 2017 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect the

Farm Finance Update March 17, 2017 Nate Kauffman Omaha Branch Executive and Economist Federal Reserve Bank of Kansas City The views expressed are those of the author and do not necessarily reflect the

Analysis of Borrower and Lender Use of Interest Assistance on FSA Guaranteed Farm Loans

Analysis of Borrower and Lender Use of Interest Assistance on FSA Guaranteed Farm Loans By Bruce L. Ahrendsen, Steve R. Koenig, Bruce L. Dixon, Charles B. Dodson and Latisha A. Settlage Agricultural Finance

Analysis of Borrower and Lender Use of Interest Assistance on FSA Guaranteed Farm Loans By Bruce L. Ahrendsen, Steve R. Koenig, Bruce L. Dixon, Charles B. Dodson and Latisha A. Settlage Agricultural Finance

The Community Development Financial

Community Development Financial Institutions Fund By Shannon Ross, Director, Government Relations, Housing Partnership Network Administering agency: U.S. Department of the Treasury (Treasury) Year program

Community Development Financial Institutions Fund By Shannon Ross, Director, Government Relations, Housing Partnership Network Administering agency: U.S. Department of the Treasury (Treasury) Year program

2015 Mortgage Lending Trends in New England

Federal Reserve Bank of Boston Community Development Issue Brief No. 2017-3 May 2017 2015 Mortgage Lending Trends in New England Amy Higgins Abstract In 2014 the mortgage and housing market underwent important

Federal Reserve Bank of Boston Community Development Issue Brief No. 2017-3 May 2017 2015 Mortgage Lending Trends in New England Amy Higgins Abstract In 2014 the mortgage and housing market underwent important

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS22212 Credit Union Regulatory Improvements Act of 2005 (CURIA) Pauline Smale, Government and Finance Division March 9,

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS22212 Credit Union Regulatory Improvements Act of 2005 (CURIA) Pauline Smale, Government and Finance Division March 9,

Selected Legislative Proposals to Reform the Housing Finance System

Selected Legislative Proposals to Reform the Housing Finance System Sean M. Hoskins Analyst in Financial Economics N. Eric Weiss Specialist in Financial Economics Katie Jones Analyst in Housing Policy

Selected Legislative Proposals to Reform the Housing Finance System Sean M. Hoskins Analyst in Financial Economics N. Eric Weiss Specialist in Financial Economics Katie Jones Analyst in Housing Policy

Rethinking Federal Credit: Managing Loan and Loan Guarantee Programs in a Changing Environment. Thursday, May 17, 2018

Rethinking Federal Credit: Managing Loan and Loan Guarantee Programs in a Changing Environment Thursday, May 17, 2018 Changing Economic and Policy Environments for the World s Largest Financial Institution

Rethinking Federal Credit: Managing Loan and Loan Guarantee Programs in a Changing Environment Thursday, May 17, 2018 Changing Economic and Policy Environments for the World s Largest Financial Institution

Federal National Mortgage Association

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

Cost-of-Living Adjustments for Federal Civil Service Annuities

Cost-of-Living Adjustments for Federal Civil Service Annuities Katelin P. Isaacs Analyst in Income Security Updated October 11, 2018 Congressional Research Service 7-5700 www.crs.gov 94-834 Summary Cost-of-living

Cost-of-Living Adjustments for Federal Civil Service Annuities Katelin P. Isaacs Analyst in Income Security Updated October 11, 2018 Congressional Research Service 7-5700 www.crs.gov 94-834 Summary Cost-of-living

Notes Except where noted otherwise, dollar amounts are expressed in 214 dollars. Nominal (current-dollar) spending was adjusted to remove the effects

spending was adjusted to remove the effects") CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Public Spending on Transportation and Water Infrastructure, 1956 to 214 MARCH 215 Notes Except where noted otherwise, dollar amounts are expressed

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Public Spending on Transportation and Water Infrastructure, 1956 to 214 MARCH 215 Notes Except where noted otherwise, dollar amounts are expressed

Farm Loan Volume Prospects for the New Farmer Mac. by Steven R. Koenig and James T. Ryan 1. Introduction

Farm Loan Volume Prospects for the New Farmer Mac by Steven R. Koenig and James T. Ryan 1 Introduction The Federal Agricultural Mortgage Corporation (Farmer Mac) is a government sponsored enterprise (GSE)

Farm Loan Volume Prospects for the New Farmer Mac by Steven R. Koenig and James T. Ryan 1 Introduction The Federal Agricultural Mortgage Corporation (Farmer Mac) is a government sponsored enterprise (GSE)

Federal National Mortgage Association

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December

Progressive Farm Credit Services, ACA

Quarterly Report June 30, 2017 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Quarterly Report June 30, 2017 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Farm Credit. Partners. Opportunity. Setting the standard. Annual Report for rural community support. Western Oklahoma.

Farm Credit Western Oklahoma Setting the standard for rural community support Annual Report - 2017 www.farmcreditloans.com Partners Opportunity Five-Year Summary of Selected Consolidated Financial Data

Farm Credit Western Oklahoma Setting the standard for rural community support Annual Report - 2017 www.farmcreditloans.com Partners Opportunity Five-Year Summary of Selected Consolidated Financial Data

WikiLeaks Document Release

WikiLeaks Document Release February 2, 29 Congressional Research Service Report 97-417 Tobacco-Related Programs and Activities of the U.S. Department of Agriculture: Operation and Cost Jasper Womach, Environment

WikiLeaks Document Release February 2, 29 Congressional Research Service Report 97-417 Tobacco-Related Programs and Activities of the U.S. Department of Agriculture: Operation and Cost Jasper Womach, Environment

ARKANSAS BANKERS ASSOCIATION. Ed Elfmann, Vice President for Congressional Relations American Bankers Association

ARKANSAS BANKERS ASSOCIATION Ed Elfmann, Vice President for Congressional Relations American Bankers Association American Bankers Association Founded in 1875 First convention was held in September, 1875

ARKANSAS BANKERS ASSOCIATION Ed Elfmann, Vice President for Congressional Relations American Bankers Association American Bankers Association Founded in 1875 First convention was held in September, 1875

Farmer Mac Relationship Managers How Community Banks are Using Farmer Mac to Grow Their Ag Portfolios

Farmer Mac Relationship Managers How Community Banks are Using Farmer Mac to Grow Their Ag Portfolios Refresh Webinar - April 2015 1 Guest Panelist Perry Forst, President & CEO Citizens State Bank Norwood

Farmer Mac Relationship Managers How Community Banks are Using Farmer Mac to Grow Their Ag Portfolios Refresh Webinar - April 2015 1 Guest Panelist Perry Forst, President & CEO Citizens State Bank Norwood

The Financial Crisis and the Future of the J-REIT Market

The Financial Crisis and the Future of the J-REIT Market Yuta Seki Senior Analyst, Chief Representative, New York Representative Office of Nomura Institute of Capita Markets Research I. Refinancing risk

The Financial Crisis and the Future of the J-REIT Market Yuta Seki Senior Analyst, Chief Representative, New York Representative Office of Nomura Institute of Capita Markets Research I. Refinancing risk

Nurturing Agricultural Businesses ESLC Conference, November 2014 Stephen McHenry, Executive Director

Nurturing Agricultural Businesses ESLC Conference, November 2014 Stephen McHenry, Executive Director www.marbidco.org Is an Ag Development Financial Intermediary Organization Serving All of Maryland With

Nurturing Agricultural Businesses ESLC Conference, November 2014 Stephen McHenry, Executive Director www.marbidco.org Is an Ag Development Financial Intermediary Organization Serving All of Maryland With

First Quarter. Equity Investor Presentation

First Quarter Equity Investor Presentation 2018 Forward-Looking Statements In addition to historical information, this presentation includes forwardlooking statements that reflect management s current

First Quarter Equity Investor Presentation 2018 Forward-Looking Statements In addition to historical information, this presentation includes forwardlooking statements that reflect management s current

Request for Input Enterprise Guarantee Fees

August 14, 2014 BY ELECTRONIC SUBMISSION Federal Housing Finance Agency Office of Policy Analysis and Research Constitution Center 400 7th Street, SW, Ninth Floor Washington, D.C. 20024 Re: Request for

August 14, 2014 BY ELECTRONIC SUBMISSION Federal Housing Finance Agency Office of Policy Analysis and Research Constitution Center 400 7th Street, SW, Ninth Floor Washington, D.C. 20024 Re: Request for

There are multiple avenues of credit available to agricultural producers. Let s begin by identifying who can provide financing for your agricultural

1 There are multiple avenues of credit available to agricultural producers. Let s begin by identifying who can provide financing for your agricultural venture. Local commercial banks and credit unions

1 There are multiple avenues of credit available to agricultural producers. Let s begin by identifying who can provide financing for your agricultural venture. Local commercial banks and credit unions

Credit for Military Service Under Civilian Federal Employee Retirement Systems

Credit for Military Service Under Civilian Federal Employee Retirement Systems Katelin P. Isaacs Analyst in Income Security December 20, 2012 CRS Report for Congress Prepared for Members and Committees

Credit for Military Service Under Civilian Federal Employee Retirement Systems Katelin P. Isaacs Analyst in Income Security December 20, 2012 CRS Report for Congress Prepared for Members and Committees

CRS Report for Congress

Order Code RS21949 Updated November 15, 2005 CRS Report for Congress Received through the CRS Web Summary Accounting Problems at Fannie Mae Mark Jickling Specialist in Public Finance Government and Finance

Order Code RS21949 Updated November 15, 2005 CRS Report for Congress Received through the CRS Web Summary Accounting Problems at Fannie Mae Mark Jickling Specialist in Public Finance Government and Finance

Multiemployer Defined Benefit (DB) Pension Plans: A Primer

Pension Plans: A Primer") Multiemployer Defined Benefit (DB) Pension Plans: A Primer John J. Topoleski Analyst in Income Security Updated September 24, 2018 Congressional Research Service 7-5700 www.crs.gov R43305 Summary Multiemployer

Multiemployer Defined Benefit (DB) Pension Plans: A Primer John J. Topoleski Analyst in Income Security Updated September 24, 2018 Congressional Research Service 7-5700 www.crs.gov R43305 Summary Multiemployer

FOCUS ON FUNDAMENTALS. Strength and Stability for Farm Credit Associations

FOCUS ON FUNDAMENTALS Strength and Stability for Farm Credit Associations AGRIBANK DISTRICT 2018 QUARTERLY REPORT JUNE 30, 2018 AGRIBANK, FCB AND DISTRICT ASSOCIATIONS FA R M C R E D I T B A N K Copies

FOCUS ON FUNDAMENTALS Strength and Stability for Farm Credit Associations AGRIBANK DISTRICT 2018 QUARTERLY REPORT JUNE 30, 2018 AGRIBANK, FCB AND DISTRICT ASSOCIATIONS FA R M C R E D I T B A N K Copies

CRS Report for Congress

Order Code RS21212 Updated August 29, 2005 CRS Report for Congress Received through the CRS Web Summary Agricultural Disaster Assistance Ralph M. Chite Specialist in Agricultural Policy Resources, Science,

Order Code RS21212 Updated August 29, 2005 CRS Report for Congress Received through the CRS Web Summary Agricultural Disaster Assistance Ralph M. Chite Specialist in Agricultural Policy Resources, Science,

AGRICULTURAL LENDER SURVEY RESULTS

Summer 2017 AGRICULTURAL LENDER SURVEY RESULTS Summer 2017 / Agricultural Lender Survey Results / 1 Contents Key Takeaways... 3 Introduction... 4 Agricultural Economy... 5 Farm Profitability and Economic

Summer 2017 AGRICULTURAL LENDER SURVEY RESULTS Summer 2017 / Agricultural Lender Survey Results / 1 Contents Key Takeaways... 3 Introduction... 4 Agricultural Economy... 5 Farm Profitability and Economic

The Budget Control Act of 2011: Legislative Changes to the Law and Their Budgetary Effects

The Budget Control Act of 2011: Legislative Changes to the Law and Their Budgetary Effects Mindy R. Levit Specialist in Public Finance March 6, 2014 Congressional Research Service 7-5700 www.crs.gov R43411

The Budget Control Act of 2011: Legislative Changes to the Law and Their Budgetary Effects Mindy R. Levit Specialist in Public Finance March 6, 2014 Congressional Research Service 7-5700 www.crs.gov R43411

National Housing Market Summary

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

Report for Congress Received through the CRS Web

Order Code RL30048 Report for Congress Received through the CRS Web Federal Student Loans: Program Data and Default Statistics Updated September 23, 2002 Adam Stoll Specialist in Social Legislation Domestic

Order Code RL30048 Report for Congress Received through the CRS Web Federal Student Loans: Program Data and Default Statistics Updated September 23, 2002 Adam Stoll Specialist in Social Legislation Domestic

Another Approach to GSE Reform

Another Approach to GSE Reform Jim Sivon September, 2015 It has been over seven years since Fannie Mae and Freddie Mac failed and were placed into conservatorship. During that time, both the Administration

Another Approach to GSE Reform Jim Sivon September, 2015 It has been over seven years since Fannie Mae and Freddie Mac failed and were placed into conservatorship. During that time, both the Administration

AGFIRST FARM CREDIT BANK & DISTRICT ASSOCIATIONS

AGFIRST FARM CREDIT BANK & DISTRICT ASSOCIATIONS 2018 FINANCIAL INFORMATION 2018 Financial Information INTRODUCTION AND DISTRICT OVERVIEW The following commentary reviews the Combined Financial Statements

AGFIRST FARM CREDIT BANK & DISTRICT ASSOCIATIONS 2018 FINANCIAL INFORMATION 2018 Financial Information INTRODUCTION AND DISTRICT OVERVIEW The following commentary reviews the Combined Financial Statements

Quarterly Report March 31, 2018

Quarterly Report March 31, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Quarterly Report March 31, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Re: Amendments to the 2013 Escrows Final Rule under the Truth in Lending Act. Regulation Z [Docket No. CFPB ]

![Re: Amendments to the 2013 Escrows Final Rule under the Truth in Lending Act. Regulation Z [Docket No. CFPB ]](/thumbs/90/101433273.jpg "Re: Amendments to the 2013 Escrows Final Rule under the Truth in Lending Act. Regulation Z [Docket No. CFPB ]") May 3, 2013 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Amendments to the 2013 Escrows Final Rule under the Truth in

May 3, 2013 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Amendments to the 2013 Escrows Final Rule under the Truth in

CRS Report for Congress

Order Code RL33421 CRS Report for Congress Received through the CRS Web USDA Rural Housing Programs: An Overview May 11, 2006 Bruce E. Foote Analyst in Housing Domestic Social Policy Division Congressional

Order Code RL33421 CRS Report for Congress Received through the CRS Web USDA Rural Housing Programs: An Overview May 11, 2006 Bruce E. Foote Analyst in Housing Domestic Social Policy Division Congressional

Agricultural Outlook Forum 1999 Presented: Monday, February 22, 1999

Agricultural Outlook Forum 1999 Presented: Monday, February 22, 1999 Farm Credit Conditions During the Agricultural Contraction of the 198's and Now Robert N. Collender Senior Financial Economist, Economic

Agricultural Outlook Forum 1999 Presented: Monday, February 22, 1999 Farm Credit Conditions During the Agricultural Contraction of the 198's and Now Robert N. Collender Senior Financial Economist, Economic

Fourth Quarter Highlights

Fourth Quarter Highlights Year over year, profitability (ROA) continued to improve at both large and community banking organizations. Year over year, loan growth was basically flat at community banks nationally,

Fourth Quarter Highlights Year over year, profitability (ROA) continued to improve at both large and community banking organizations. Year over year, loan growth was basically flat at community banks nationally,

Notes Numbers in the text and tables may not add up to totals because of rounding. Unless otherwise indicated, years referred to in describing the bud

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 4 to 4 Percentage of GDP 4 Surpluses Actual Projected - -4-6 Average Deficit, 974 to Deficits -8-974 979 984 989

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 4 to 4 Percentage of GDP 4 Surpluses Actual Projected - -4-6 Average Deficit, 974 to Deficits -8-974 979 984 989

May 1965 CONSTRUCTION AND MORTGAGE MARKETS. Digitized for FRASER Federal Reserve Bank of St. Louis

May 1965 CONSTRUCTION AND MORTGAGE MARKETS May 1965 outlays for new construction in April continued at the high established in the first quarter. Total outlays for the first 4 months of the year were moderately

May 1965 CONSTRUCTION AND MORTGAGE MARKETS May 1965 outlays for new construction in April continued at the high established in the first quarter. Total outlays for the first 4 months of the year were moderately

To understand where the U.S. Economy is going, we need to understand where we have been

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical