Re: Amendments to the 2013 Escrows Final Rule under the Truth in Lending Act. Regulation Z [Docket No. CFPB ]

|

|

|

- Edwin Peters

- 5 years ago

- Views:

Transcription

.")

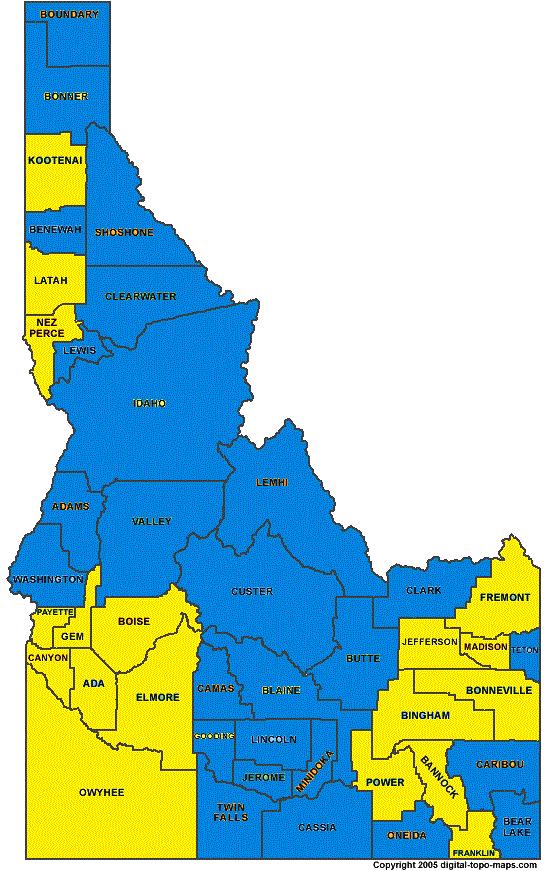

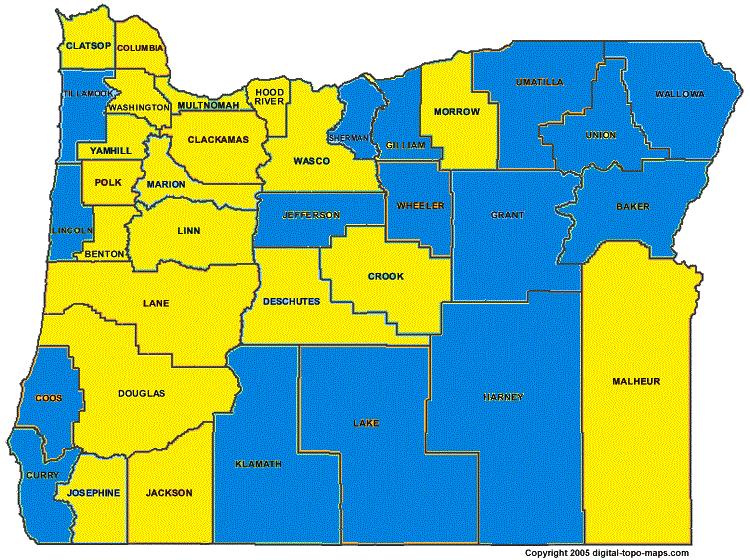

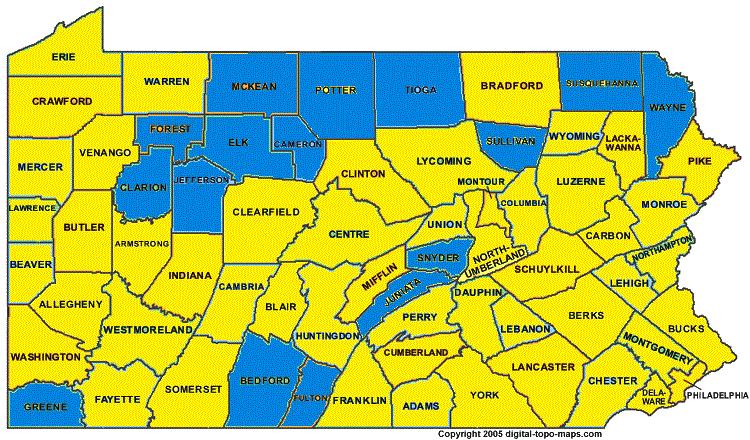

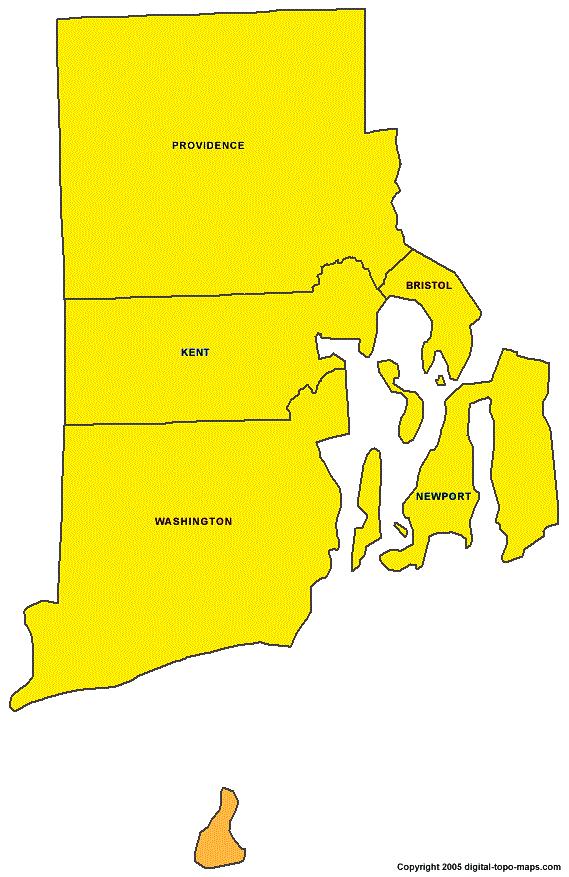

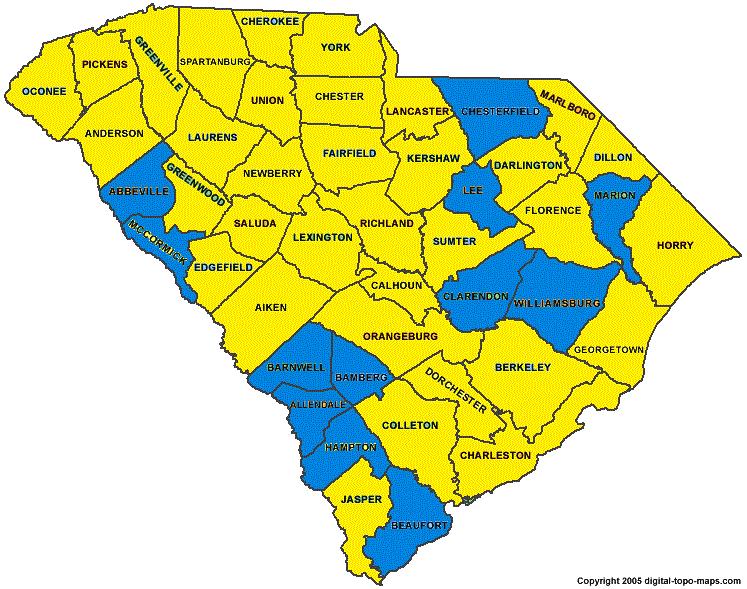

1 May 3, 2013 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC Re: Amendments to the 2013 Escrows Final Rule under the Truth in Lending Act. Regulation Z [Docket No. CFPB ] Dear Ms. Jackson: The Independent Community Bankers of America (ICBA) 1 appreciates this opportunity to comment on the proposed amendment to the Escrows Final Rule, originally issued January 10, 2013 by the Consumer Financial Protection Bureau (the Bureau). This rule, among other things, imposes new requirements on financial institutions regarding the mandatory use of escrow accounts for Higher Priced Mortgage Loans (HPMLs). This rule also established an exemption from the mandatory escrow requirements for certain creditors that operate predominantly in rural or underserved areas. The amendment as proposed by the Bureau seeks to provide certain clarifications regarding the definition of rural as well as to provide for continuity of certain consumer protections under the current HPML rules regarding a creditor s current responsibilities 1 The Independent Community Bankers of America, the nation s voice for more than 7,000 community banks of all sizes and charter types, is dedicated exclusively to representing the interests of the community banking industry and its membership through effective advocacy, best in class education and high quality products and services. With nearly 5,000 members, representing more than 24,000 locations nationwide and employing more than 300,000 Americans, ICBA members hold more than $1.2 trillion in assets, $1 trillion in deposits, and $750 billion in loans to consumers, small businesses and the agricultural community. For more information, visit ICBA s website at

2 under the ability to repay rules. These ability to repay rules for HPMLs will be replaced by the new ability to repay rules as issued by the Bureau January 10, 2013 and will take effect on January 10, While ICBA generally supports the proposed amendment as written, we urge the Bureau to broaden the definition of rural to include more communities and consumers. ICBA strongly urges the Bureau to amend its current definition of rural to include all non-metropolitan counties and any town or community with a population of 50,000 or less as rural. The current definition of rural as defined by the Bureau is too narrow and excludes many counties and communities that are very rural in nature. This will prevent the community banks which serve those markets from benefiting from the exemptions in the escrow rule, as well as from receiving QM safe harbor legal protections on balloon payment mortgages they make and retain in portfolio. ICBA appreciates the challenging task that the Bureau has undertaken to define what is rural and what is not. There are a variety of definitions used by various financial services regulators, government agencies, GSEs and the states and counties themselves. The Bureau has chosen to use Urban Influence Codes (UICs) as produced by the United States Department of Agriculture-Economic Research Service (USDA-ERS). USDA- ERS has assigned a code ranging from 1-12 to each of the 3141 counties in the United States. Codes 1 and 2 are for metropolitan counties, and codes 3-12 for non metropolitan counties. 2 The current designations are based on the 2000 census, and will be updated later this year with the results of the 2010 national census. The Bureau s current definition of rural is any county that is not part of a Metropolitan Statistical Area (MSA) or a Micropolitan Area adjacent to an MSA. As such, counties with UICs of 1,2,3,5 are not considered rural, and based on the 2000 census data account for 251,394,317 citizens or 89.7% of the U.S. population. When looking at the census data, the Census Bureau indicates that 82% of the U.S. population lives in urban and suburban areas, which would suggest that they believe 18% of the U.S. population lives in rural areas, a full seven percentage points or almost 20 million residents more than the Bureau s definition would support. The problem with the Bureau s definition is that it assumes the entire county is either rural or non rural. The reality, however, is that many counties, including some in MSAs are a mix of rural and non rural, and by excluding the entire county the Bureau is excluding many rural communities where community banks provide much of the mortgage financing through loans they originate and retain in portfolio. Many of these loans are balloon payment loans, and many community banks do not escrow for taxes and insurance. The Bureau s definition of rural will cause many of these community banks to significantly curtail portfolio lending or exit the business all together. For many borrowers in rural communities, community banks are their only source of mortgage credit, due to unique or rural property types or due to the borrower s special 2 Urban Influence Codes

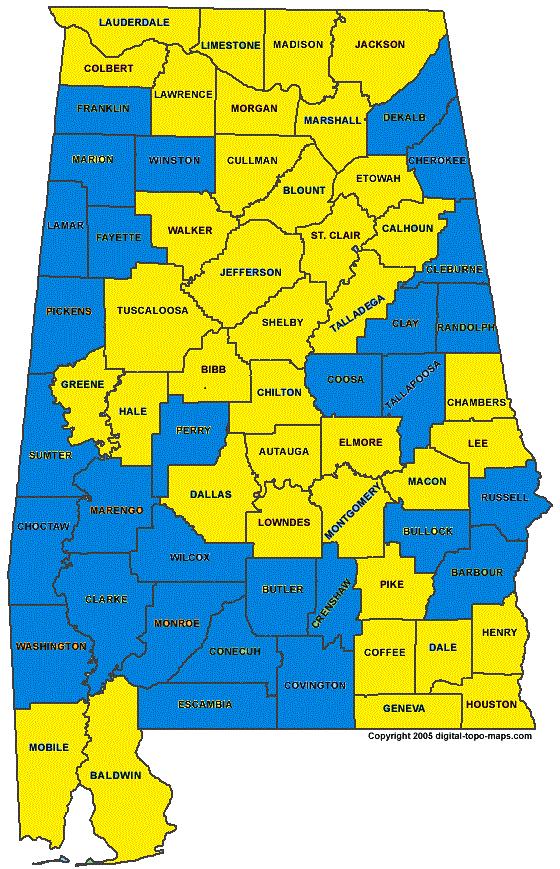

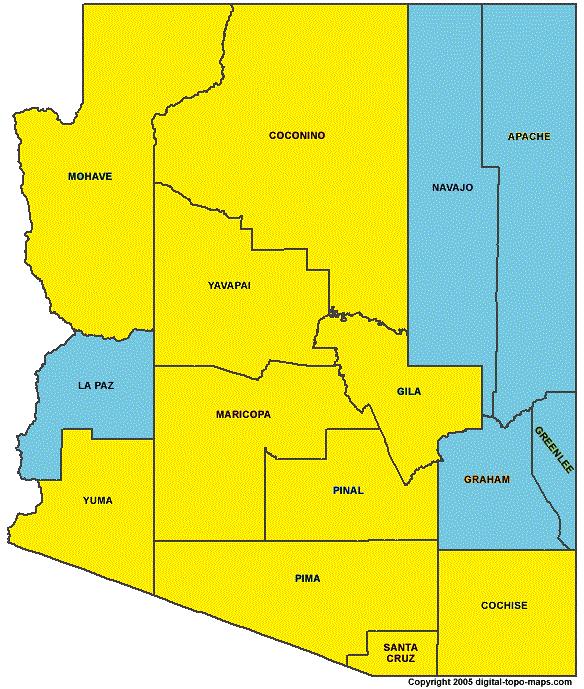

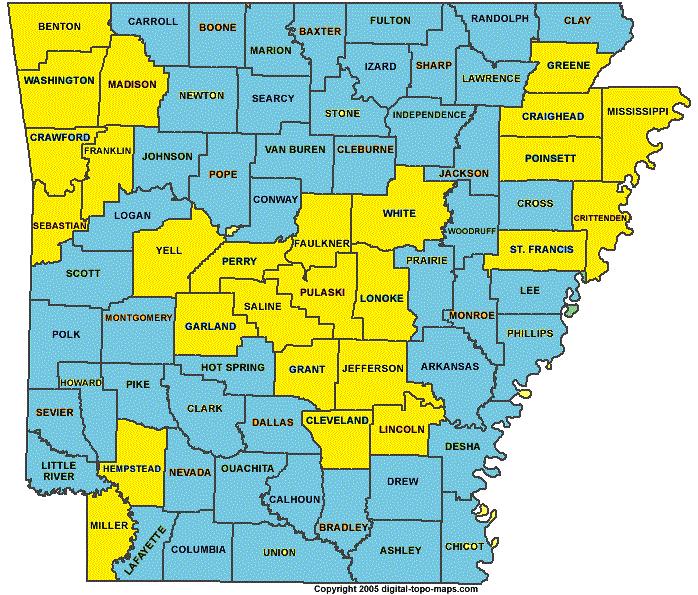

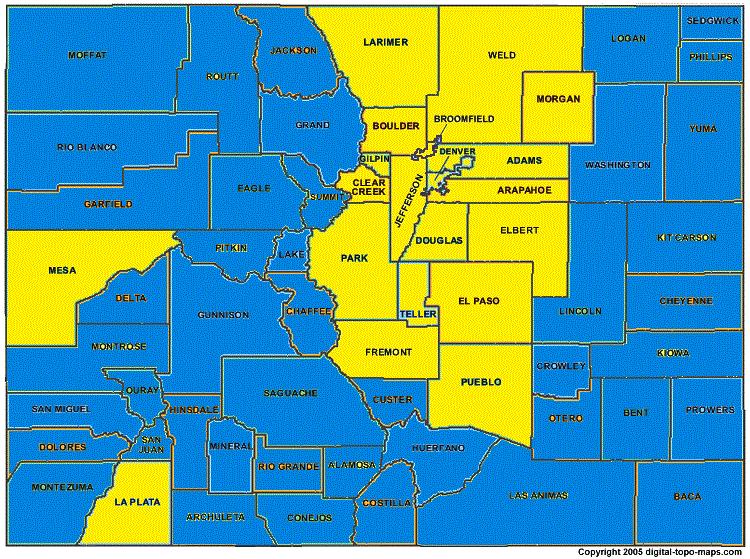

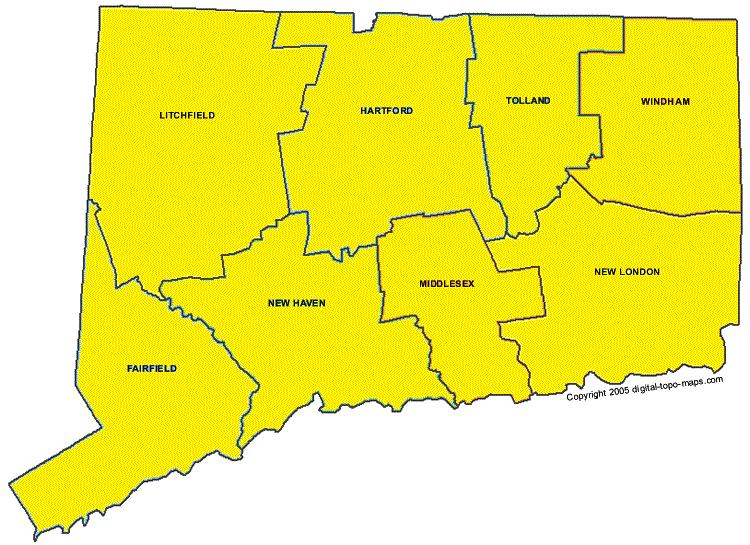

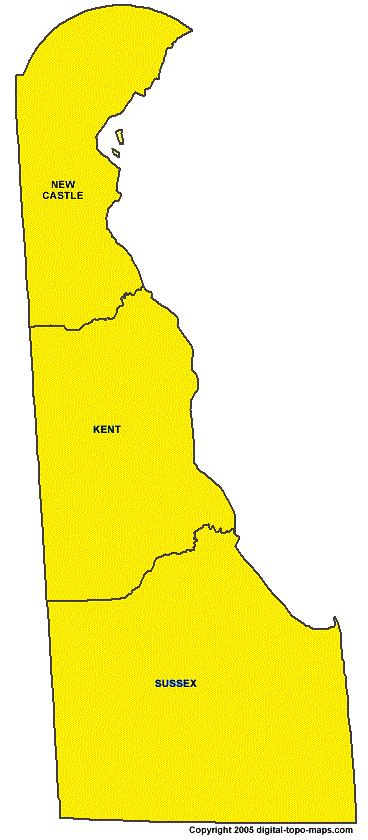

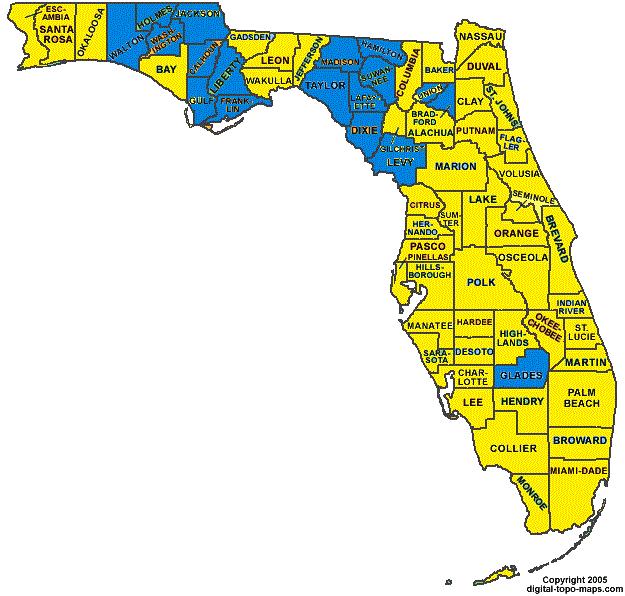

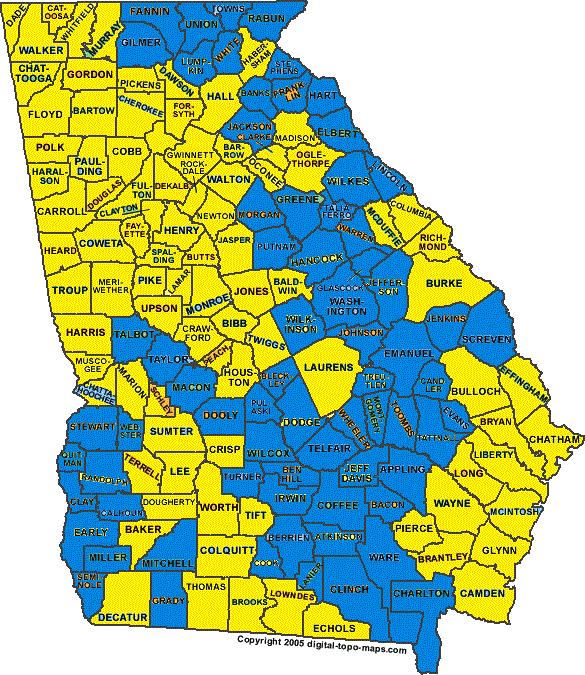

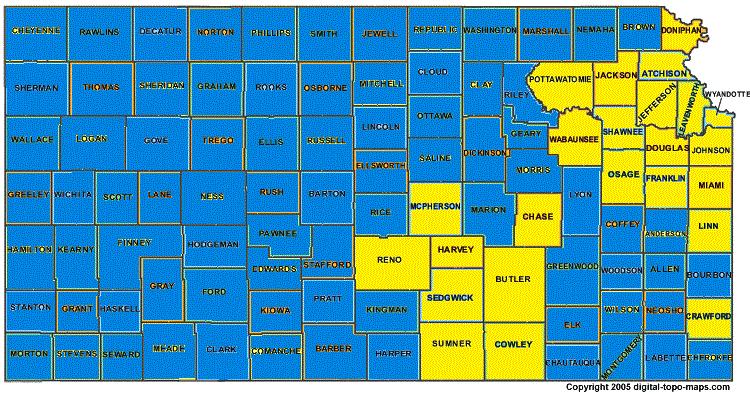

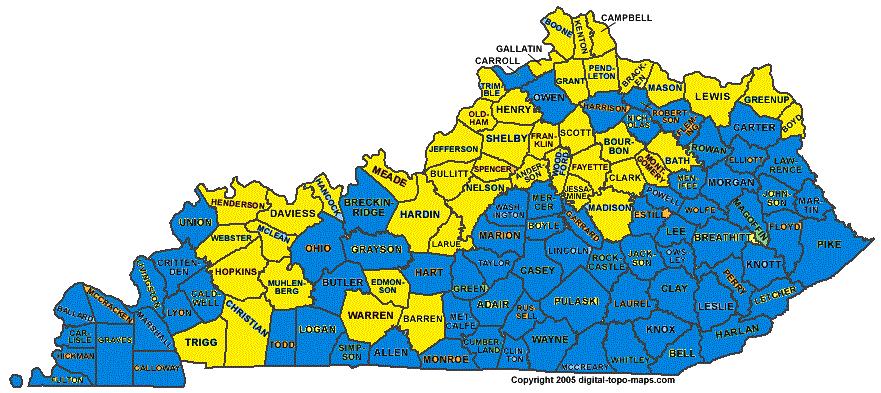

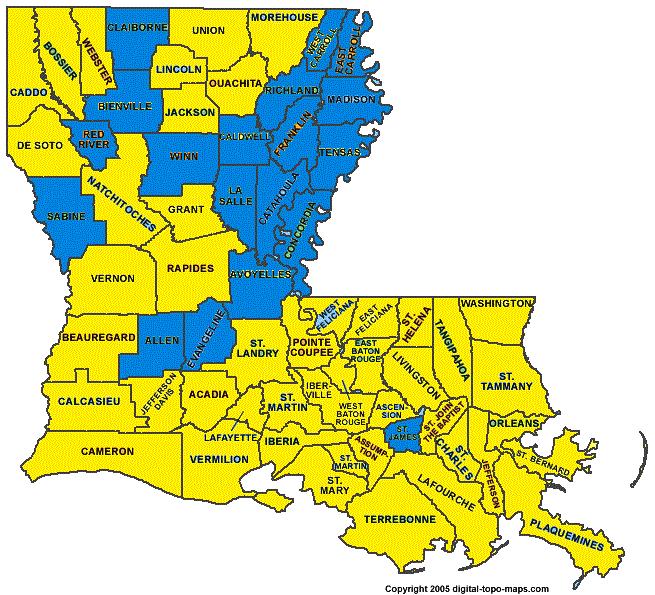

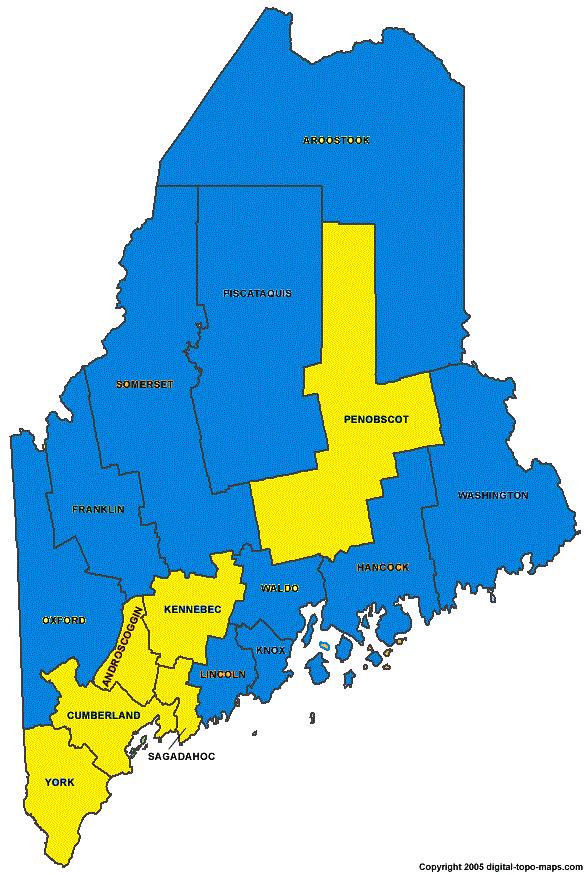

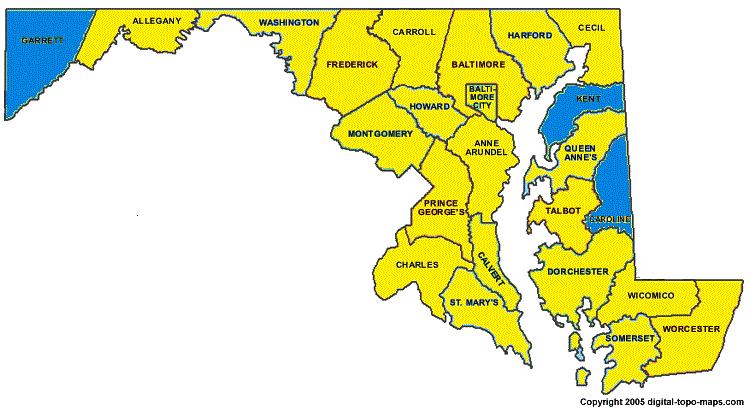

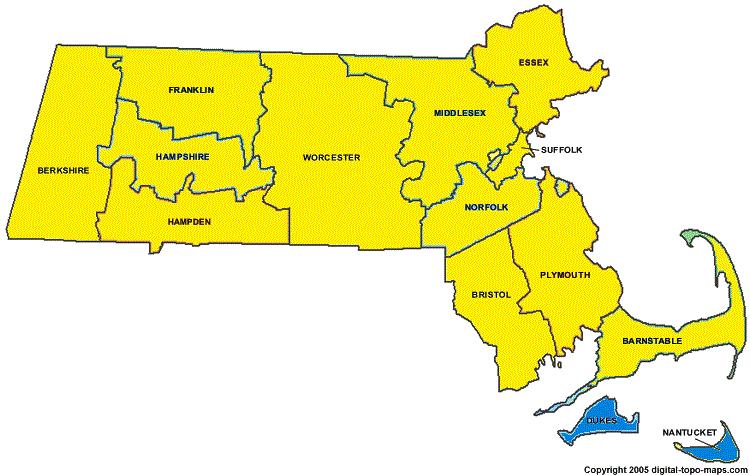

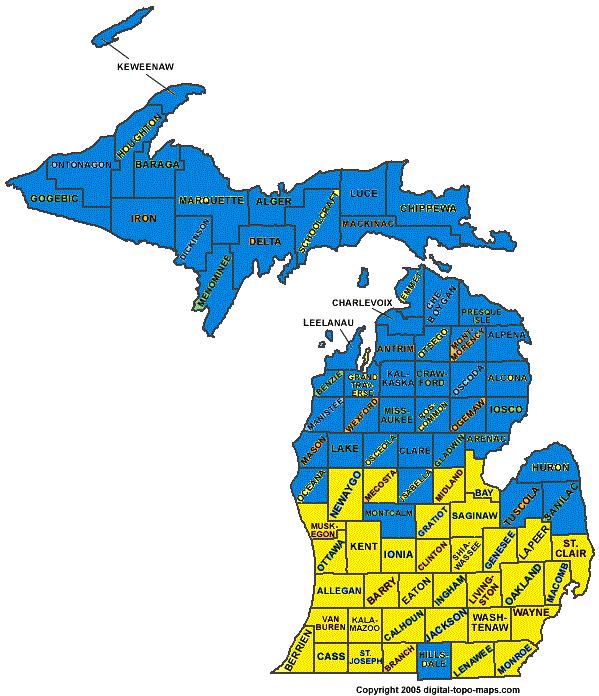

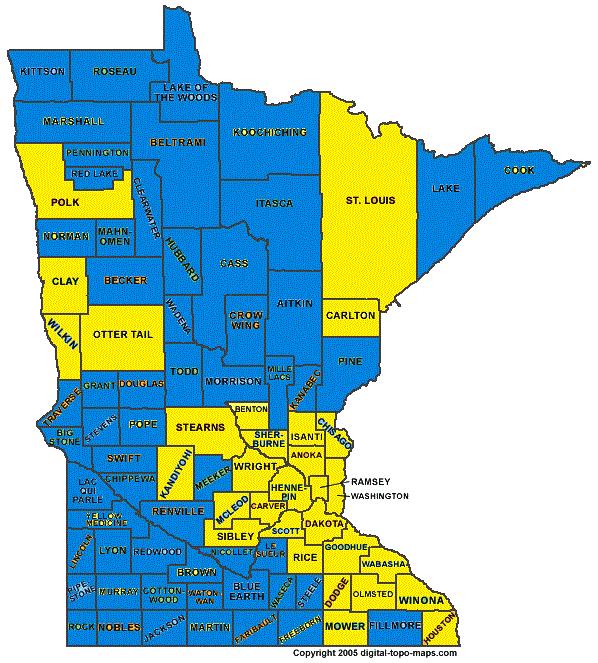

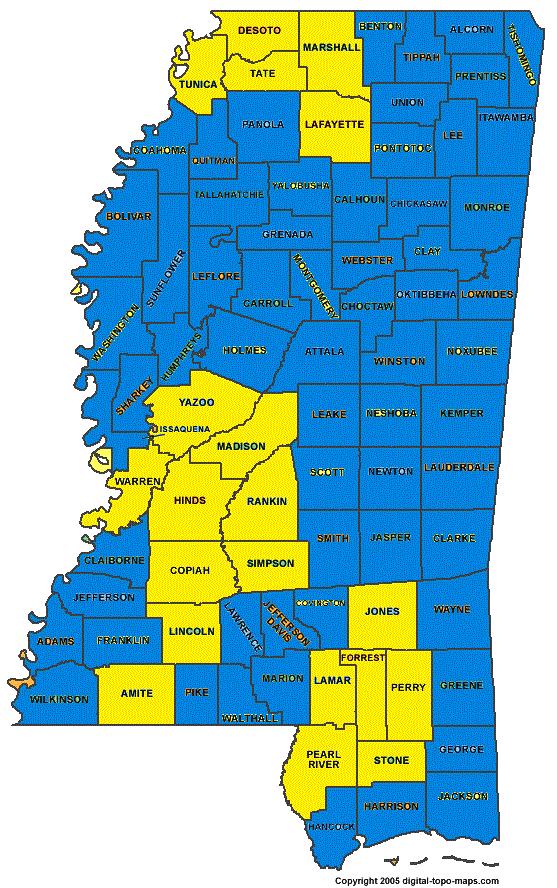

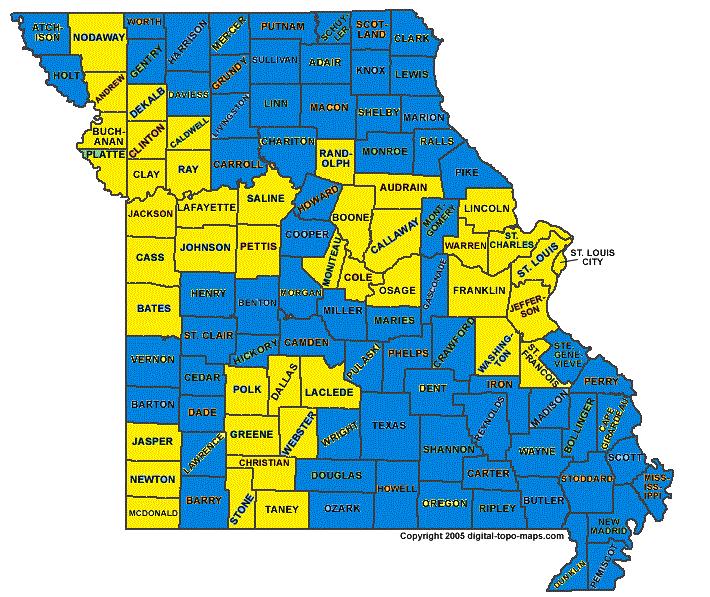

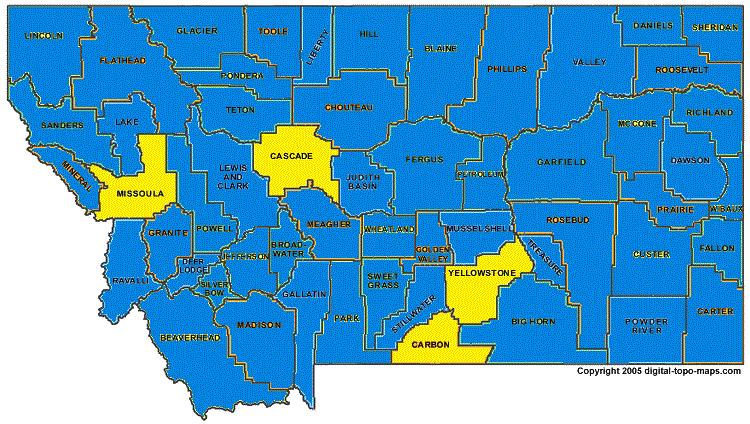

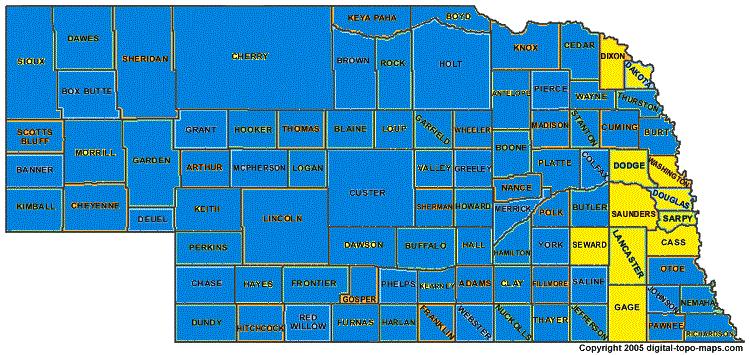

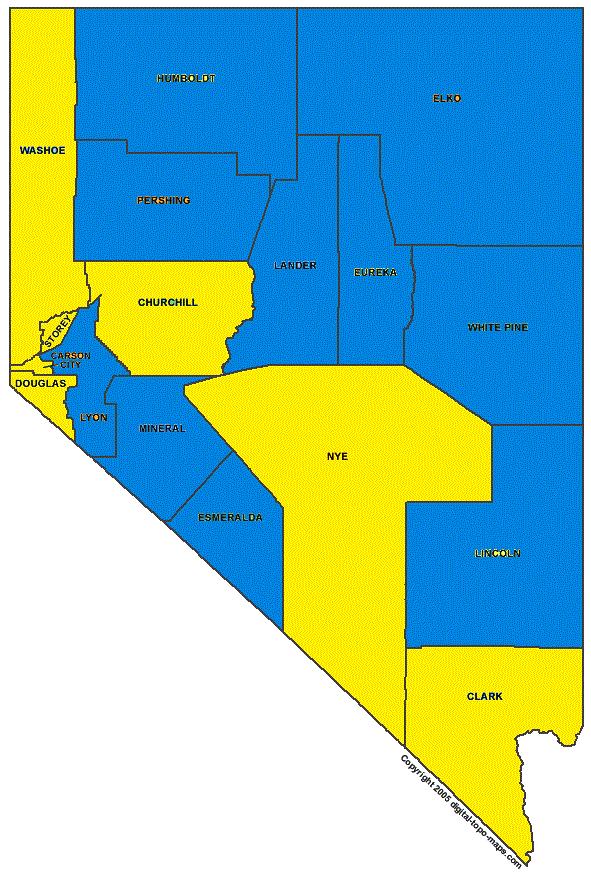

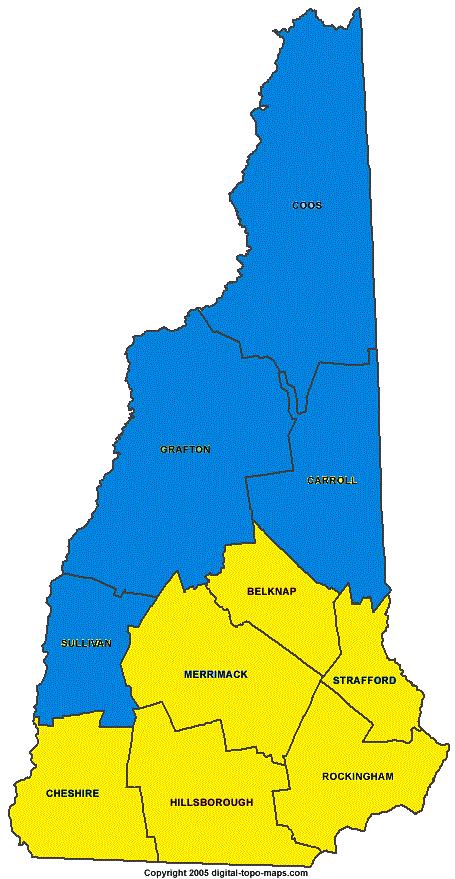

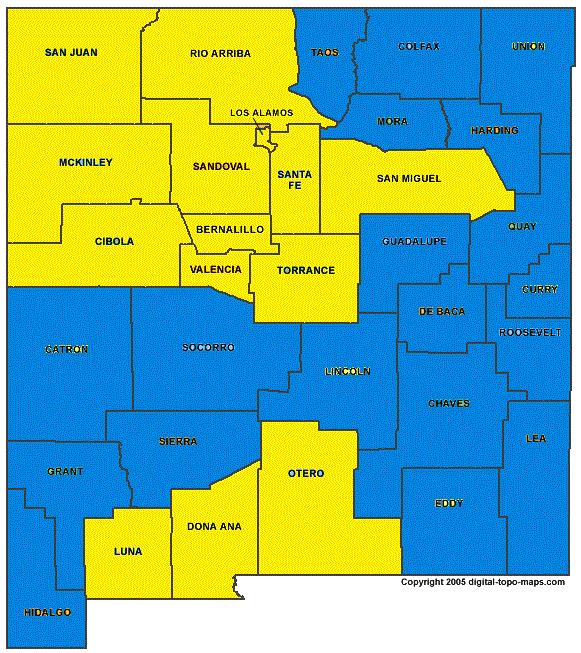

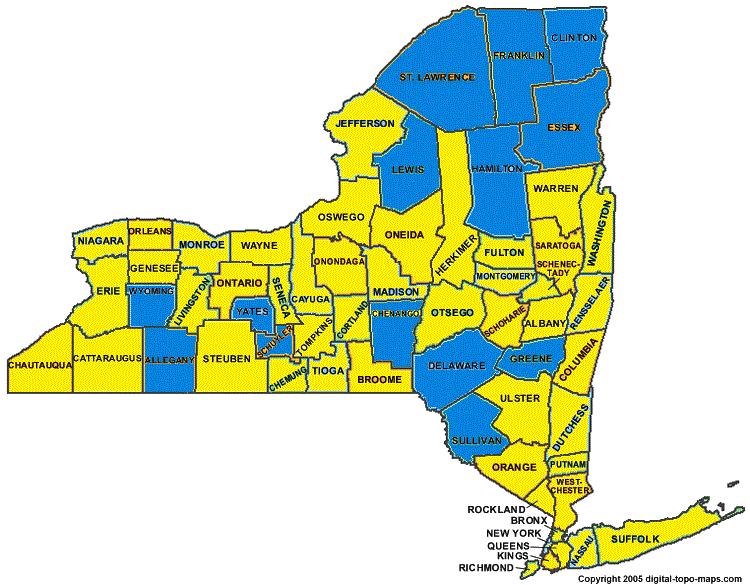

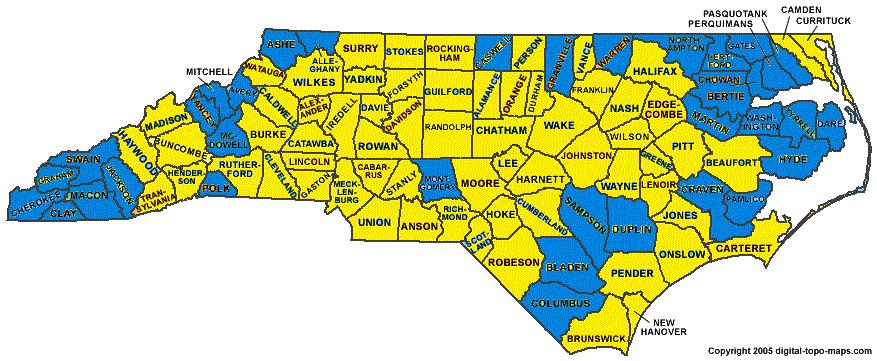

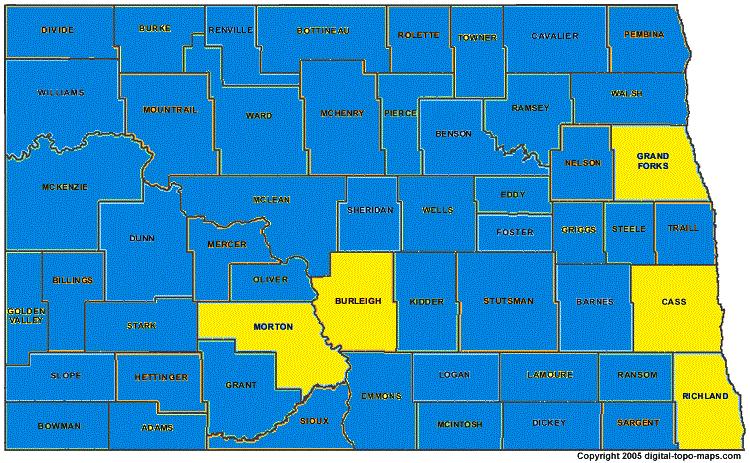

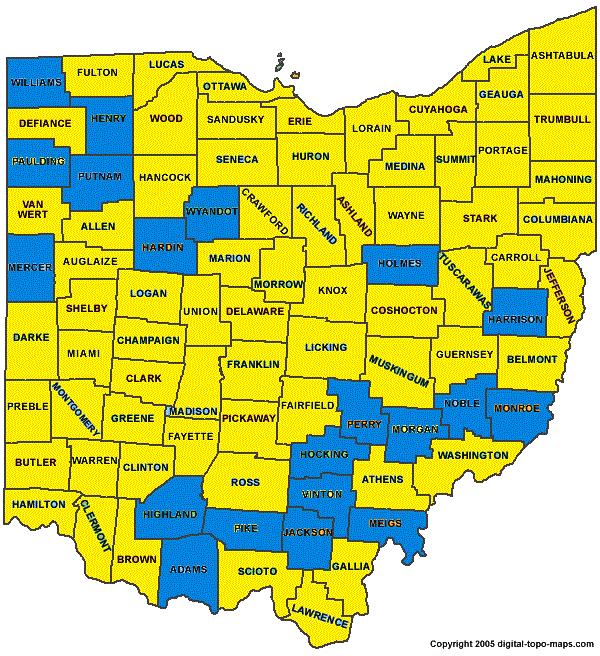

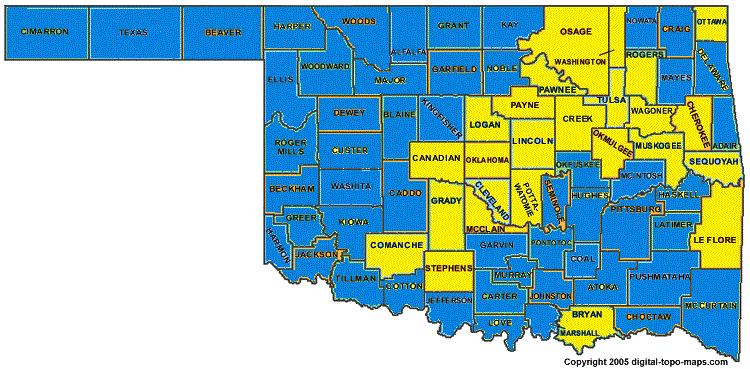

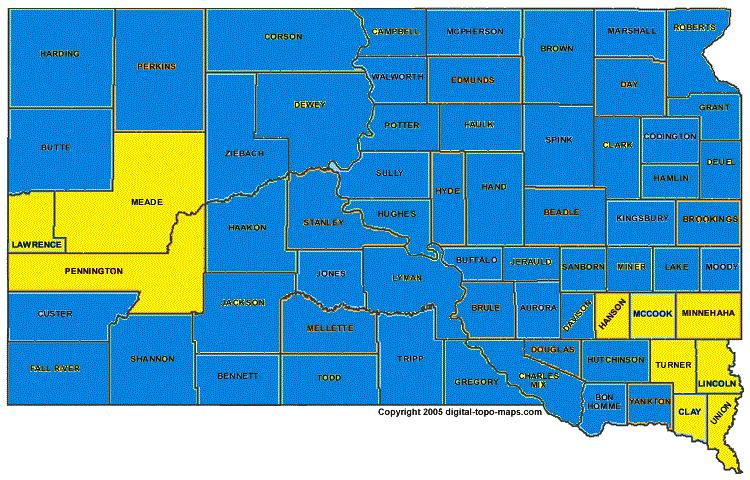

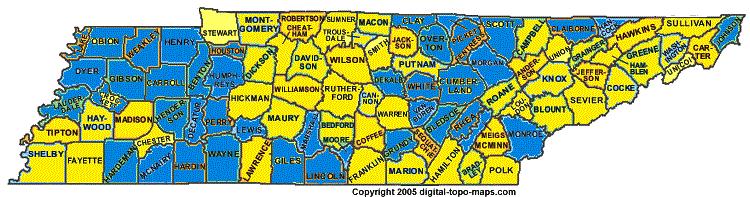

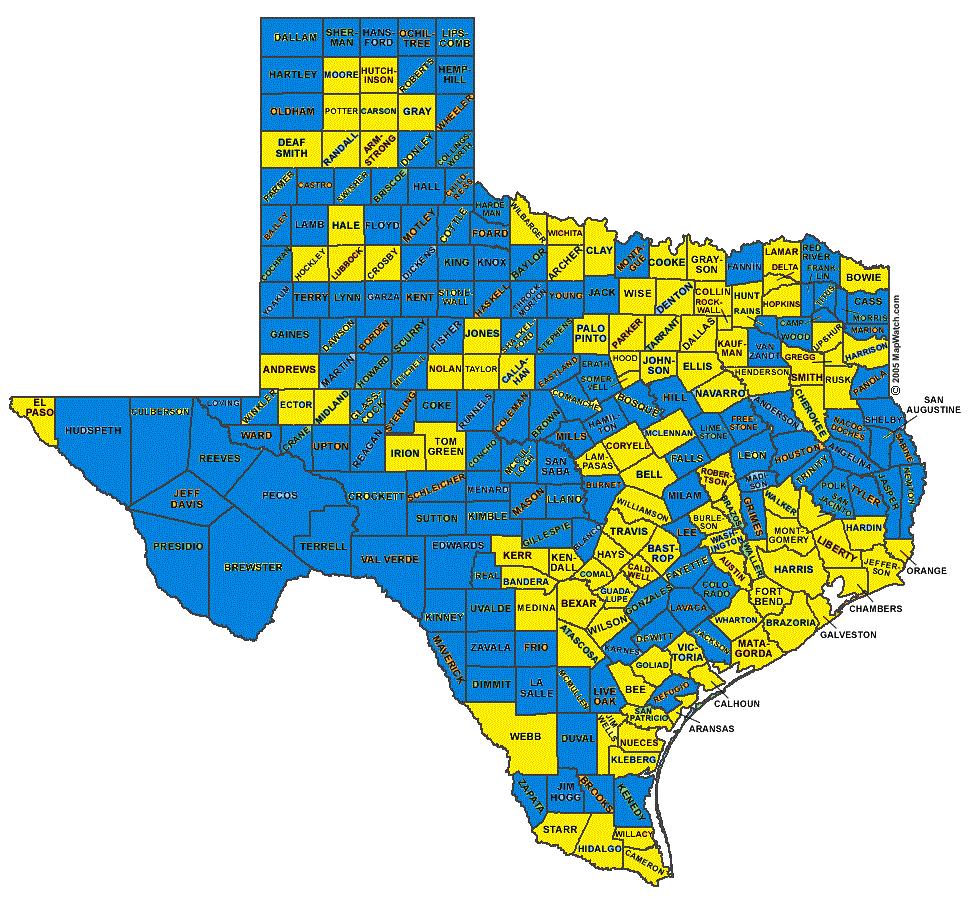

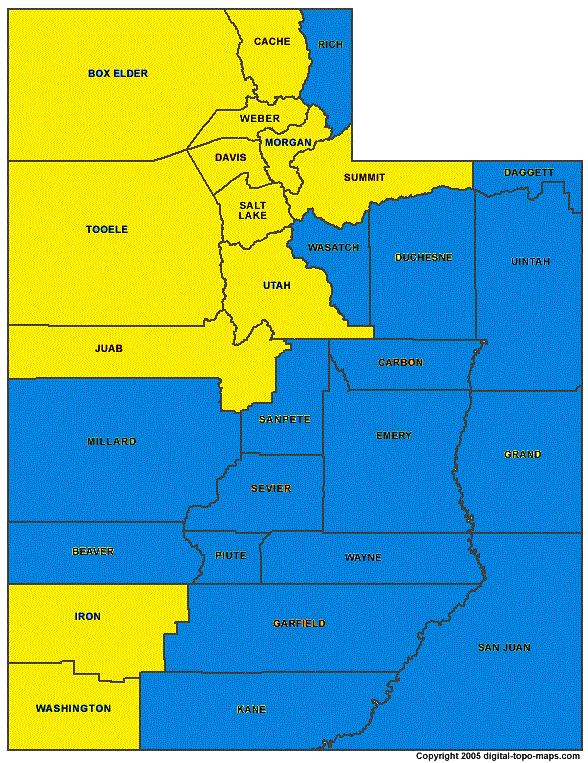

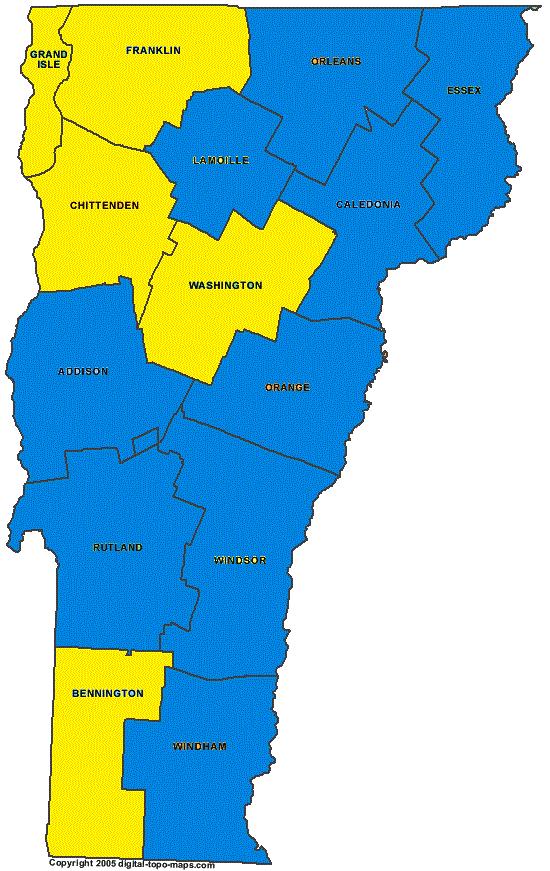

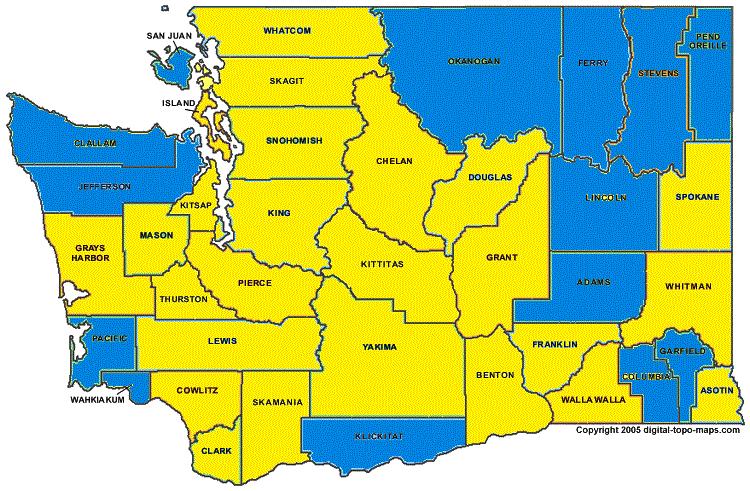

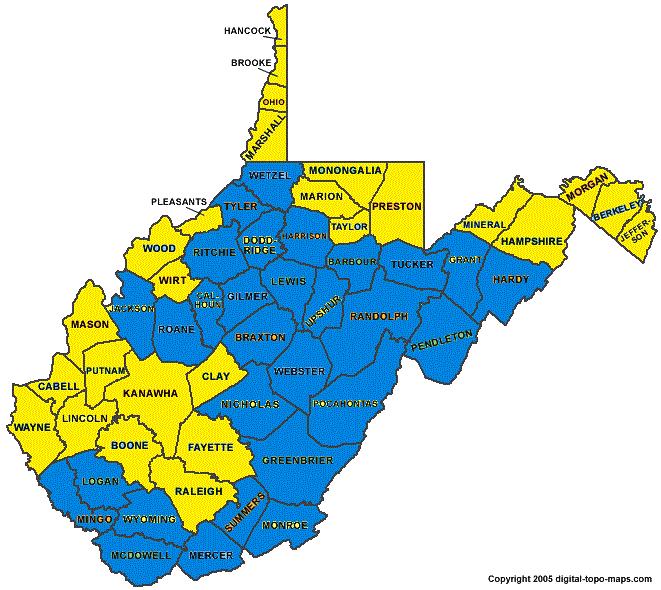

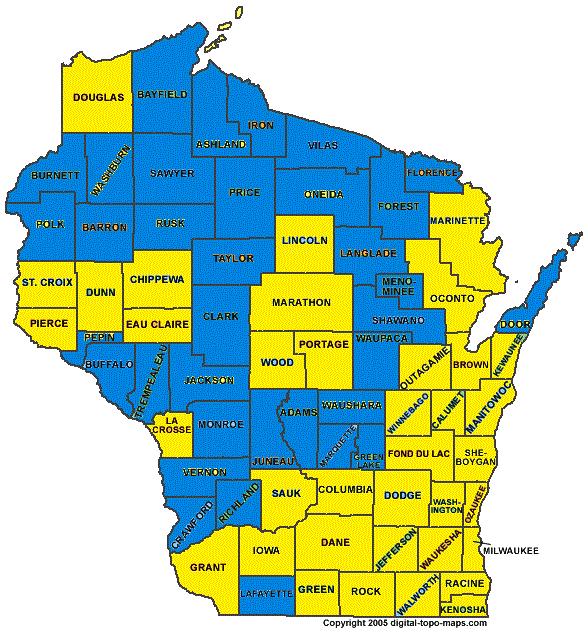

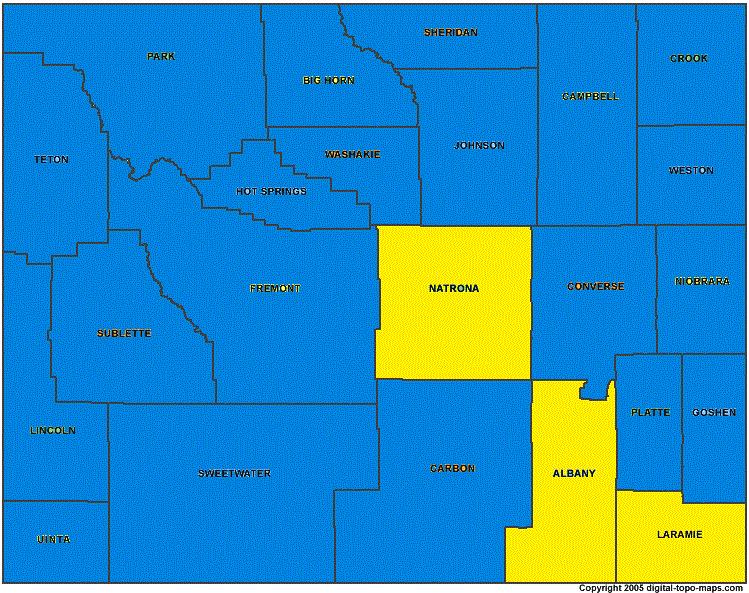

3 financial situation, such as seasonal employment, which makes it impossible to qualify for a secondary market loan. Community bankers have made these types of loans, frequently balloon loans for decades, safely and soundly. But unless the Bureau amends the definition of rural to include more counties and towns, many of these community banks will exit the mortgage business. The attached maps illustrate this impact and were created based on the UICs for rural and non rural under the Bureau s current definition of rural. Counties in yellow are non-rural counties and counties in blue are rural counties. In a recent survey of approximately 400 ICBA members, 75% of those community banks indicated they currently make balloon payment mortgages, and that only 46% of the banks would be able to use the balloon mortgage exemption to the ability to repay rule. Additionally, of the banks that responded to the survey that considered themselves to be rural or in a rural community, 44% did not meet the Bureau s definition of rural. The following are some of the comments we received from the banks who responded to the survey: While we are in a MSA we are a rural bank, in a rural area, in a village of 4,000 people. We are $60 million [in assets]. About half of the mortgage loans we make are to customers that do not fit into the secondary market parameters because of the type of property, their income or job history, or their credit score. They are still considered part of our good customer base that we maintain as a community bank. Many of these people have banked with us for many years, their families have banked here, and they might even hold a few shares of stock in our bank. These new rules will severely limit our ability to provide a mortgage to a good share of our customer base. We don't want to go to an adjustable rate mortgage. It's simply too much work, too much compliance. I have been making balloon loans to my mortgage customers for 38 years, without a problem. We hold the balloon loans in our portfolio and service them without an issue. Again, some fly by night lenders made some bad balloons loans and created a problem for us all. The definition of rural and underserved is way too narrow and will severely restrict the availability of mortgage loans for many people in the country. We are a small community bank located in Houston County, Minnesota with the City of LaCrosse, WI located across the river (the real MSA). We are totally NOT a metropolitan area. We have an agricultural concentration with approximately 80% of our loan portfolio in agricultural related loans. We do in-house balloon loans for borrowers who do not qualify for a secondary market loan due to a ding in their underwriting (approximately 10%of our portfolio). None of the balloon loans are over 30 days delinquent. We will discontinue offering in-house loans if we cannot offer balloon loans. We are considering discontinuing loans not qualifying for the secondary market already, due to required escrow accounts, which we do not offer. Rates on this type loan do not reflect risk, due to limiting the interest rate by not offering escrow accounts.

4 Our bank has 2 offices located on one side of a county but the other side of the county is part of a MSA. So, even though we are certainly in a "rural" farming area, and the population of our 2 communities is less than 1,400 people, we are explicitly excluded from the "rural" exemption due to a large city located in our county, approximately 20 miles away. Our bank has 10 employees covering 2 offices. We have 3 loan officers, one of which is our only mortgage loan officer - in other words, we have a mortgage department of "1". Due to the staggering regulatory burden placed on community banks during the recent mortgage reform, our bank has had to stop offering consumer owner-occupied loans. Recent mortgage revisions and prohibitions have made mortgage lending not only impractical, but impossible for a small community bank such as ours. As indicated above, the Bureau s definition of rural will have far reaching unintended impacts on the availability of credit in many communities. These are the same communities in which community banks have served consumers safely for decades by making mortgage loans only to consumers who could afford to repay them, along with paying their taxes and insurance, as well as all of their other household expenses. Community bankers did not exploit consumers as some other lenders did, yet they and their customers will suffer for deeds done by others which now drive these rules. The Bureau created this definition of rural, and the Bureau has the authority to change it so community banks can continue to serve their customers. ICBA strongly urges the Bureau to amend its definition of rural for purposes of the escrow rule, and the recently issued balloon mortgage exception to the ability to repay rule, by including all non metropolitan counties (UICs 3-12) and any town or community with a population less than 50,000. ICBA looks forward to working with Bureau staff on this and future rulemakings. We appreciate the Bureau s ongoing outreach to ICBA and community bankers. If you have any questions regarding this letter, please contact the undersigned at ron.haynie@icba.org. Sincerely, Ron Haynie Senior Vice President- Mortgage Finance Policy Independent Community Bankers of America

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

Re: CFPB Request for Information regarding the Ability-to-Repay/Qualified Mortgage Rule Assessment

July 31, 2017 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1275 First Street, NE Washington, DC 20002 Re: CFPB-2017-0014 Request for Information regarding the Ability-to-Repay/Qualified

July 31, 2017 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1275 First Street, NE Washington, DC 20002 Re: CFPB-2017-0014 Request for Information regarding the Ability-to-Repay/Qualified

Joe Gendron, Director of Government Relations 5555 Bankers Avenue, Baton Rouge, LA (225) ,

,") Joe Gendron, Director of Government Relations 5555 Bankers Avenue, Baton Rouge, LA 70808 (225) 214-4837, gendron@lba.org February 15, 2013 Comment Letter Ability-to-Repay Standards under TILA Docket No.

Joe Gendron, Director of Government Relations 5555 Bankers Avenue, Baton Rouge, LA 70808 (225) 214-4837, gendron@lba.org February 15, 2013 Comment Letter Ability-to-Repay Standards under TILA Docket No.

CBAI will be submitting two comment letters; this letter regarding the definition of

Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Amendments Relating to Small Creditors and Rural and Underserved Areas

Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Amendments Relating to Small Creditors and Rural and Underserved Areas

Submitted Electronically. August 14, 2017

Submitted Electronically August 14, 2017 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1275 First Street NE Washington, DC 20002 Re: Request for Comment Regarding

Submitted Electronically August 14, 2017 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1275 First Street NE Washington, DC 20002 Re: Request for Comment Regarding

October 30, Legislative and Regulatory Activities Division Office of the Comptroller of the Currency

October 30, 2013 Robert dev. Frierson, Secretary Board of Governors of the Federal Reserve System 20 th Street and Constitution Avenue, NW Washington, DC 20551 Docket No. R-1411 Robert E. Feldman Executive

October 30, 2013 Robert dev. Frierson, Secretary Board of Governors of the Federal Reserve System 20 th Street and Constitution Avenue, NW Washington, DC 20551 Docket No. R-1411 Robert E. Feldman Executive

TIB 2016 Annual Conference Small Creditor and Rural or Underserved Updates By: Venessa Snell

TIB 2016 Annual Conference 2016 Small Creditor and Rural or Underserved Updates By: Venessa Snell Small Creditors I. Who were you then?- 1026.35(b)(2)(iii)(B) and (C)-January 10, 2014-December 31, 2015:

TIB 2016 Annual Conference 2016 Small Creditor and Rural or Underserved Updates By: Venessa Snell Small Creditors I. Who were you then?- 1026.35(b)(2)(iii)(B) and (C)-January 10, 2014-December 31, 2015:

Qualified Mortgage Rule Will Jeopardize Access to Credit

On behalf of the 7,000 community banks represented by the Independent Community Bankers of America (ICBA), thank you for convening today s hearing titled: Examining How the Dodd- Frank Act Hampers Home

On behalf of the 7,000 community banks represented by the Independent Community Bankers of America (ICBA), thank you for convening today s hearing titled: Examining How the Dodd- Frank Act Hampers Home

See 12 U.S. Codes 1021(b)(3), 1022, available at 111publ203/pdf/PLAW-111publ203.pdf. 4

(3), 1022, available at 111publ203/pdf/PLAW-111publ203.pdf. 4") July 31, 2017 Ms. Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection 1700 G Street, NW Washington, DC 20552 Via electronic submission Re: Response of the Consumer

July 31, 2017 Ms. Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection 1700 G Street, NW Washington, DC 20552 Via electronic submission Re: Response of the Consumer

Mortgage Lending Compliance Issues Session 1. Higher Priced and High-Cost Mortgages

Mortgage Lending Compliance Issues Session 1 Higher Priced and High-Cost Mortgages Today s Topics Learn the definitions of Higher Priced and High Cost Mortgages and how to test to determine if you are

Mortgage Lending Compliance Issues Session 1 Higher Priced and High-Cost Mortgages Today s Topics Learn the definitions of Higher Priced and High Cost Mortgages and how to test to determine if you are

Simplifications to the Capital Rule Pursuant to the Economic Growth and Regulatory Paperwork Reduction Act of 1996

December 18, 2017 Legislative and Regulatory Activities Division Office of the Comptroller of the Currency 400 7 th Street SW Suite 3E-218, Mail Stop 9W-11 Washington, DC 20219 Ms. Ann E. Misback Secretary

December 18, 2017 Legislative and Regulatory Activities Division Office of the Comptroller of the Currency 400 7 th Street SW Suite 3E-218, Mail Stop 9W-11 Washington, DC 20219 Ms. Ann E. Misback Secretary

November 6, Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552

November 6, 2012 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 Re: Proposed Rule on High-Cost Mortgage and Homeownership

November 6, 2012 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 Re: Proposed Rule on High-Cost Mortgage and Homeownership

March 21, Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551

March 21, 2016 Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551 Robert E. Feldman, Executive Secretary Federal Deposit Insurance

March 21, 2016 Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551 Robert E. Feldman, Executive Secretary Federal Deposit Insurance

Docket No. CFPB Mortgage Servicing Rules Under the Real Estate Settlement Procedures Act (Regulation X)

") Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 By electronic delivery to: www.regulations.gov Re: Docket No. CFPB-2017-0031

Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 By electronic delivery to: www.regulations.gov Re: Docket No. CFPB-2017-0031

PPDocs System Training CFPB changes effective January 2014

PPDocs System Training CFPB changes effective January 2014 Please direct all questions to: CFPB@ppdocs.com What you should be doing today: What type of QM are you going to be doing? *Are you going to be

PPDocs System Training CFPB changes effective January 2014 Please direct all questions to: CFPB@ppdocs.com What you should be doing today: What type of QM are you going to be doing? *Are you going to be

TESTIMONY OF MR. JERRY REED CHIEF LENDING OFFICER ALASKA USA FEDERAL CREDIT UNION ON BEHALF OF THE CREDIT UNION NATIONAL ASSOCIATION

TESTIMONY OF MR. JERRY REED CHIEF LENDING OFFICER ALASKA USA FEDERAL CREDIT UNION ON BEHALF OF THE CREDIT UNION NATIONAL ASSOCIATION BEFORE THE SUBCOMMITTEE ON FINANCIAL INSTITUTIONS AND CONSUMER CREDIT

TESTIMONY OF MR. JERRY REED CHIEF LENDING OFFICER ALASKA USA FEDERAL CREDIT UNION ON BEHALF OF THE CREDIT UNION NATIONAL ASSOCIATION BEFORE THE SUBCOMMITTEE ON FINANCIAL INSTITUTIONS AND CONSUMER CREDIT

June 3, Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street N.W. Washington, D.C.

Robert R. Davis Executive Vice President Mortgage Markets, Financial Management & Public Policy (202) 663-5588 RDavis@aba.com Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection

Robert R. Davis Executive Vice President Mortgage Markets, Financial Management & Public Policy (202) 663-5588 RDavis@aba.com Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection

November 14, The Honorable Melvin L. Watt Director Federal Housing Finance Agency th St SW Washington, DC 20219

November 14, 2018 The Honorable Melvin L. Watt Director Federal Housing Finance Agency 400 7 th St SW Washington, DC 20219 Re: Enterprise Capital Rules; RIN 2590-AA95 Dear Director Watt: The Independent

November 14, 2018 The Honorable Melvin L. Watt Director Federal Housing Finance Agency 400 7 th St SW Washington, DC 20219 Re: Enterprise Capital Rules; RIN 2590-AA95 Dear Director Watt: The Independent

Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules

April 23, 2012 Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules The Consumer Financial Protection Bureau ( CFPB or Bureau ) recently issued final rules related to mortgage

April 23, 2012 Notice Regarding Updated Regulations and Summary of Recent CFPB Mortgage Rules The Consumer Financial Protection Bureau ( CFPB or Bureau ) recently issued final rules related to mortgage

February 25, Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC

Robert R. Davis Executive Vice President Mortgage Markets, Financial Management & Public Policy (202) 663-5588 RDavis@aba.com Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection

Robert R. Davis Executive Vice President Mortgage Markets, Financial Management & Public Policy (202) 663-5588 RDavis@aba.com Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection

Regulation Z Michelle Nuckols, CRCM. financial services

Regulation Z Michelle Nuckols, CRCM 1 Amendments to Regulation Z The CFPB has changed the definition of small creditors, and rural and underserved areas under Regulation Z - January 1, 2016 Expands the

Regulation Z Michelle Nuckols, CRCM 1 Amendments to Regulation Z The CFPB has changed the definition of small creditors, and rural and underserved areas under Regulation Z - January 1, 2016 Expands the

CONSUMER CREDIT INDUSTRY ASSOCIATION

CONSUMER CREDIT INDUSTRY ASSOCIATION Scott J, Cipinko 6300 Powers Ferry Road, Suite 600-286 Executive Vice President & CEO Atlanta, Georgia 30339 678.858.4001 sjcipinko@cciaonline.com Ms. Monica Jackson

CONSUMER CREDIT INDUSTRY ASSOCIATION Scott J, Cipinko 6300 Powers Ferry Road, Suite 600-286 Executive Vice President & CEO Atlanta, Georgia 30339 678.858.4001 sjcipinko@cciaonline.com Ms. Monica Jackson

Request for Information Regarding the Bureau s Consumer Complaint and Inquiry Handling Processes [Docket No. CFPB ]

![Request for Information Regarding the Bureau s Consumer Complaint and Inquiry Handling Processes [Docket No. CFPB ]](/thumbs/91/106245462.jpg "Request for Information Regarding the Bureau s Consumer Complaint and Inquiry Handling Processes [Docket No. CFPB ]") Via electronic submission July 16, 2018 The Honorable J. Michael Mulvaney Acting Director Bureau of Consumer Financial Protection 1700 G Street, NW Washington, DC 20552 Re: Request for Information Regarding

Via electronic submission July 16, 2018 The Honorable J. Michael Mulvaney Acting Director Bureau of Consumer Financial Protection 1700 G Street, NW Washington, DC 20552 Re: Request for Information Regarding

Summary of CBA s Comments

June 3, 2013 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Docket No. CFPB-2013-0010 Proposed Amendments to the 2013 Mortgage

June 3, 2013 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Docket No. CFPB-2013-0010 Proposed Amendments to the 2013 Mortgage

Testimony of. Kenneth E. Bentsen Jr., Executive Vice President, Public Policy and Advocacy. Securities Industry and Financial Markets Association

Testimony of Kenneth E. Bentsen Jr., Executive Vice President, Public Policy and Advocacy Securities Industry and Financial Markets Association Before the U.S. House Subcommittee on Financial Institutions

Testimony of Kenneth E. Bentsen Jr., Executive Vice President, Public Policy and Advocacy Securities Industry and Financial Markets Association Before the U.S. House Subcommittee on Financial Institutions

Impact: Federal and State Chartered Credit Unions Relevant Department: Lending and Collections / CEO Priority Level: Medium

Comment Call (15-1) CFPB: Amendments to 2013 Mortgage Servicing Rules under Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Impact: Federal and State Chartered

Comment Call (15-1) CFPB: Amendments to 2013 Mortgage Servicing Rules under Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Impact: Federal and State Chartered

October 30, Honorable Martin J. Gruenberg Chairman Federal Deposit Insurance Corporation Washington, DC Re: RIN 3064-AD74

Robert R. Davis Executive Vice President Mortgage Markets, Financial Management & Public Policy (202) 663-5588 RDavis@aba.com October 30, 2013 Honorable Ben S. Bernanke Chairman Board of Governors of the

Robert R. Davis Executive Vice President Mortgage Markets, Financial Management & Public Policy (202) 663-5588 RDavis@aba.com October 30, 2013 Honorable Ben S. Bernanke Chairman Board of Governors of the

December 9, Gerard S. Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, Virginia 22314

December 9, 2016 Gerard S. Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, Virginia 22314 Re: Chartering and Field of Membership Manual: RIN 3133-AD31

December 9, 2016 Gerard S. Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, Virginia 22314 Re: Chartering and Field of Membership Manual: RIN 3133-AD31

Mortgage Reform Under the Dodd-Frank Act

Mortgage Reform Under the Dodd-Frank Act Kenneth Benton Senior Consumer Regulations Specialist September 20, 2013 FEDERAL RESERVE BANK OF PHILADELPHIA DISCLAIMER: The views expressed are the presenters

Mortgage Reform Under the Dodd-Frank Act Kenneth Benton Senior Consumer Regulations Specialist September 20, 2013 FEDERAL RESERVE BANK OF PHILADELPHIA DISCLAIMER: The views expressed are the presenters

August 31, Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551

August 31, 2015 Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551 Robert E. Feldman, Executive Secretary Federal Deposit Insurance

August 31, 2015 Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551 Robert E. Feldman, Executive Secretary Federal Deposit Insurance

Supporting Responsible Innovation in the Federal Banking System: An OCC Perspective

May 31, 2016 The Honorable Thomas J. Curry Comptroller of the Currency Office of the Comptroller of the Currency 400 7 th Street, SW Washington, DC 20219 Re: Supporting Responsible Innovation in the Federal

May 31, 2016 The Honorable Thomas J. Curry Comptroller of the Currency Office of the Comptroller of the Currency 400 7 th Street, SW Washington, DC 20219 Re: Supporting Responsible Innovation in the Federal

USDA RURAL DEVELOPMENT HOUSING PROGRAMS

Housing Assistance Council 1025 Vermont Ave. NW Suite 606 Washington DC 20005 Phone: (202) 842-8600 Fax: (202) 347-3441 E-mail: hac@ruralhome.org USDA RURAL DEVELOPMENT HOUSING PROGRAMS FY 2009 Year-End

Housing Assistance Council 1025 Vermont Ave. NW Suite 606 Washington DC 20005 Phone: (202) 842-8600 Fax: (202) 347-3441 E-mail: hac@ruralhome.org USDA RURAL DEVELOPMENT HOUSING PROGRAMS FY 2009 Year-End

USDA OneRD Regulation, Request for Comment, Docket ID - RHS-18-CF / Federal Register Number:

October 22 nd, 2018 Ms. Michele Brooks, Team Lead, Regulations Management Team Rural Development Innovation Center United States Department of Agriculture 1400 Independence Ave., STOP 1522, Room 5159 Washington,

October 22 nd, 2018 Ms. Michele Brooks, Team Lead, Regulations Management Team Rural Development Innovation Center United States Department of Agriculture 1400 Independence Ave., STOP 1522, Room 5159 Washington,

Dodd-Frank Implementation Checklist

Dodd-Frank Implementation Checklist Project Initiation Determine the nature and scope of the project 1. Determine who will be responsible for implementing Dodd-Frank Act compliance requirements, and how

Dodd-Frank Implementation Checklist Project Initiation Determine the nature and scope of the project 1. Determine who will be responsible for implementing Dodd-Frank Act compliance requirements, and how

R. Scott Heitkamp President and CEO of ValueBank Corpus Christi, TX

Testimony of R. Scott Heitkamp President and CEO of ValueBank Corpus Christi, TX On behalf of the Independent Community Bankers of America Before the United States Senate Committee Banking, Housing, and

Testimony of R. Scott Heitkamp President and CEO of ValueBank Corpus Christi, TX On behalf of the Independent Community Bankers of America Before the United States Senate Committee Banking, Housing, and

Submitted electronically to:

Submitted electronically to: cfpb_overdraft_forms@cfpb.gov November 3, 2017 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552

Submitted electronically to: cfpb_overdraft_forms@cfpb.gov November 3, 2017 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552

Re: Docket No. CFPB Amendments to Federal Mortgage Disclosure Requirements under the Truth in Lending Act (Regulation Z)

") Rod J. Alba Vice President, Mortgage Finance & Senior Regulatory Counsel 202-663-5592 ralba@aba.com October 10, 2017 Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection

Rod J. Alba Vice President, Mortgage Finance & Senior Regulatory Counsel 202-663-5592 ralba@aba.com October 10, 2017 Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection

May 19, 2017 VIA ELECTRONIC SUBMISSION

VIA ELECTRONIC SUBMISSION Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Dear Ms. Jackson: May 19, 2017 The undersigned, a

VIA ELECTRONIC SUBMISSION Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Dear Ms. Jackson: May 19, 2017 The undersigned, a

RE: Request for Information Regarding Bureau Financial Education Programs (Docket No. CFPB )

") Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 RE: Request for Information Regarding Bureau Financial Education Programs

Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 RE: Request for Information Regarding Bureau Financial Education Programs

Consumer Compliance Hot Topics

Consumer Compliance Hot Topics Agenda Regulatory Update: Timeline and Title XIV Summary Frequently Asked Questions Supervisory Expectations Future Rules Areas of Emerging Risk Risk Focused Supervision

Consumer Compliance Hot Topics Agenda Regulatory Update: Timeline and Title XIV Summary Frequently Asked Questions Supervisory Expectations Future Rules Areas of Emerging Risk Risk Focused Supervision

Draft Model Regulatory Framework for Virtual Currency Activities

February 13, 2015 Via Electronic Delivery David Cotney Chairman Emerging Payments Task Force Conference of State Bank Supervisors 1129 20 th Street NW Washington, DC 20036 Re: Draft Model Regulatory Framework

February 13, 2015 Via Electronic Delivery David Cotney Chairman Emerging Payments Task Force Conference of State Bank Supervisors 1129 20 th Street NW Washington, DC 20036 Re: Draft Model Regulatory Framework

With so much change, be sure to stay up to date!

With so much change, be sure to stay up to date! Glory LeDu Glory.LeDu@mcul.org Sarah Stevenson Sarah.Stevenson@mcul.org Barb Boyd Barb.Boyd@cusolutionsgroup.com Your Crazy Compliance Peeps Agenda What

With so much change, be sure to stay up to date! Glory LeDu Glory.LeDu@mcul.org Sarah Stevenson Sarah.Stevenson@mcul.org Barb Boyd Barb.Boyd@cusolutionsgroup.com Your Crazy Compliance Peeps Agenda What

S DODD-FRANK ACT REVISIONS REGULATORY RELIEF

July 27, 2018 Vol. XXXV, No. 16 S. 2155 DODD-FRANK ACT REVISIONS REGULATORY RELIEF I. INTRODUCTION President Trump recently signed Senate Bill 2155, the Economic Growth, Regulatory Relief and Consumer

July 27, 2018 Vol. XXXV, No. 16 S. 2155 DODD-FRANK ACT REVISIONS REGULATORY RELIEF I. INTRODUCTION President Trump recently signed Senate Bill 2155, the Economic Growth, Regulatory Relief and Consumer

Request for Information Regarding the Bureau's Adopted Regulations and New Rulemaking Authorities (Docket No. CFPB )

") Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection 1700 G Street, NW Washington, DC 20552 RE: Request for Information Regarding the Bureau's Adopted Regulations and

Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection 1700 G Street, NW Washington, DC 20552 RE: Request for Information Regarding the Bureau's Adopted Regulations and

NACHA Requests for Comment on ACH Quality and Risk Management Topics and ACH Rules Compliance Audit Requirements

Submitted via email July 20, 2018 Mr. Michael Herd Senior Vice President, ACH Network Administration NACHA The Electronic Payment Association 2550 Wasser Terrace, Suite 400 Herndon, VA 20171 Re: NACHA

Submitted via email July 20, 2018 Mr. Michael Herd Senior Vice President, ACH Network Administration NACHA The Electronic Payment Association 2550 Wasser Terrace, Suite 400 Herndon, VA 20171 Re: NACHA

Re: Docket No. CFPB Proposal to Amend the Ability to Pay Provisions of the Credit Card Accountability Responsibility and Disclosure Act

January 7, 2013 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Docket No. CFPB-2012-0039 Proposal to Amend the Ability

January 7, 2013 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Docket No. CFPB-2012-0039 Proposal to Amend the Ability

May 14, Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551

May 14, 2015 Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551 Robert E. Feldman, Executive Secretary Federal Deposit Insurance

May 14, 2015 Robert dev. Frierson, Secretary Board of Governors Federal Reserve System 20 th Street and Constitution Washington, DC 20551 Robert E. Feldman, Executive Secretary Federal Deposit Insurance

Jefferson County Housing Market Update

Jefferson County Housing Market Update June 26, 2013 Jim Fuchs Assistant Vice President Federal Reserve Bank of St. Louis These comments reflect my own views, not necessarily those of the Federal Reserve

Jefferson County Housing Market Update June 26, 2013 Jim Fuchs Assistant Vice President Federal Reserve Bank of St. Louis These comments reflect my own views, not necessarily those of the Federal Reserve

October 7, Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC

Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552. Cooperative Credit Union Association, Inc. Comments on Proposed Rule Payday,

Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552. Cooperative Credit Union Association, Inc. Comments on Proposed Rule Payday,

What s New in Mortgage Lending Compliance?

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

New Lending Opportunities in the Changed Mortgage Market: Dodd-Frank Act Mortgage Regulations

New Lending Opportunities in the Changed Mortgage Market: Dodd-Frank Act Mortgage Regulations Kenneth Benton Senior Consumer Regulations Specialist May 14, 2014 FEDERAL RESERVE BANK OF PHILADELPHIA Disclaimer:

New Lending Opportunities in the Changed Mortgage Market: Dodd-Frank Act Mortgage Regulations Kenneth Benton Senior Consumer Regulations Specialist May 14, 2014 FEDERAL RESERVE BANK OF PHILADELPHIA Disclaimer:

Testimony of. James Gardill. American Bankers Association. Financial Institutions Subcommittee. Financial Services Committee

Testimony of James Gardill On behalf of the American Bankers Association before the Financial Institutions Subcommittee of the Financial Services Committee United States House of Representatives James

Testimony of James Gardill On behalf of the American Bankers Association before the Financial Institutions Subcommittee of the Financial Services Committee United States House of Representatives James

NATIONAL ASSOCIATION OF REALTORS

NATIONAL ASSOCIATION OF REALTORS The Voice for Real Estate 430 North Michigan Avenue Chicago, Illinois 60611-4087 312.329.8411 Fax 312.329.5962 Visit us at www.realtor.org. Coldwell Banker AJS Schmidt

NATIONAL ASSOCIATION OF REALTORS The Voice for Real Estate 430 North Michigan Avenue Chicago, Illinois 60611-4087 312.329.8411 Fax 312.329.5962 Visit us at www.realtor.org. Coldwell Banker AJS Schmidt

Re: Docket No. CFPB ; RIN 3170-AA51 CFPB proposed rule re: class action waivers and arbitral records

Via E-Mail to: FederalRegisterComments@cfpb.gov U.S. Bureau of Consumer Financial Protection 1700 G Street, NW Washington DC 20552 Attn: Monica Jackson, Office of the Executive Secretary Re: Docket No.

Via E-Mail to: FederalRegisterComments@cfpb.gov U.S. Bureau of Consumer Financial Protection 1700 G Street, NW Washington DC 20552 Attn: Monica Jackson, Office of the Executive Secretary Re: Docket No.

Qualified Mortgages and Qualified Residential Mortgages under the Dodd-Frank Act

Qualified Mortgages and Qualified Residential Mortgages under the Dodd-Frank Act Kenneth Benton Senior Consumer Regulations Specialist Greg Bell Banking Supervisor Consumer Compliance Risk Team FEDERAL

Qualified Mortgages and Qualified Residential Mortgages under the Dodd-Frank Act Kenneth Benton Senior Consumer Regulations Specialist Greg Bell Banking Supervisor Consumer Compliance Risk Team FEDERAL

Dear Majority Leader McConnell, Minority Leader Schumer, Chairman Crapo, and Ranking Member Brown:

March 9, 2018 The Honorable Mitch McConnell Majority Leader S-230, The Capitol The Honorable Mike Crapo Chairman Committee on Banking, Housing and Urban Affairs 239 Dirksen Senate Office Building The Honorable

March 9, 2018 The Honorable Mitch McConnell Majority Leader S-230, The Capitol The Honorable Mike Crapo Chairman Committee on Banking, Housing and Urban Affairs 239 Dirksen Senate Office Building The Honorable

May 9, Alternative Capital. Dear Ladies and Gentlemen:

May 9, 2017 Mr. Gerald Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, VA 22314-3428 Re: Alternative Capital Dear Ladies and Gentlemen: The Independent

May 9, 2017 Mr. Gerald Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, VA 22314-3428 Re: Alternative Capital Dear Ladies and Gentlemen: The Independent

Amendments to Federal Mortgage Disclosure Requirements under the Truth in Lending

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2017-0018] RIN 3170-AA61 Amendments to Federal Mortgage Disclosure Requirements under the Truth in Lending

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2017-0018] RIN 3170-AA61 Amendments to Federal Mortgage Disclosure Requirements under the Truth in Lending

Request for Information Regarding Ability-to-Repay/Qualified Mortgage Rule Assessment

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION [Docket No. CFPB-2017-0014] Request for Information Regarding Ability-to-Repay/Qualified Mortgage Rule Assessment AGENCY: Bureau of Consumer

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION [Docket No. CFPB-2017-0014] Request for Information Regarding Ability-to-Repay/Qualified Mortgage Rule Assessment AGENCY: Bureau of Consumer

September 7, 2012 VIA ELECTRONIC DELIVERY AND HAND DELIVERY

VIA ELECTRONIC DELIVERY AND HAND DELIVERY Monica Jackson Office of the Executive Secretary 1700 G Street, N.W. Washington, D.C. 20552 Re: Docket No. CFPB-2012-0029; RIN3170-AA12; Proposed Rule - High-Cost

VIA ELECTRONIC DELIVERY AND HAND DELIVERY Monica Jackson Office of the Executive Secretary 1700 G Street, N.W. Washington, D.C. 20552 Re: Docket No. CFPB-2012-0029; RIN3170-AA12; Proposed Rule - High-Cost

Subject: Interagency Proposed Rule regarding Credit Risk Retention. 12 CFR Part 43 [Docket NO. OCC ] RIN 1557-AD40

![Subject: Interagency Proposed Rule regarding Credit Risk Retention. 12 CFR Part 43 [Docket NO. OCC ] RIN 1557-AD40](/thumbs/96/127018417.jpg "Subject: Interagency Proposed Rule regarding Credit Risk Retention. 12 CFR Part 43 [Docket NO. OCC ] RIN 1557-AD40") October 30, 2013 Mr. Thomas Curry Comptroller Office of the Comptroller of the Currency Washington, DC 20219 The Honorable Ben S. Bernanke Chairman Board of Governors of the Federal Reserve System Washington,

October 30, 2013 Mr. Thomas Curry Comptroller Office of the Comptroller of the Currency Washington, DC 20219 The Honorable Ben S. Bernanke Chairman Board of Governors of the Federal Reserve System Washington,

The de minimis exception to designation as a Swap Dealer should be available to regional banks and dealers that intermediate regional Swap markets.

November 10, 2010 Mr. David A. Stawick Secretary Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, N.W. Washington DC 20581 Ms. Elizabeth M. Murphy Secretary Securities and

November 10, 2010 Mr. David A. Stawick Secretary Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, N.W. Washington DC 20581 Ms. Elizabeth M. Murphy Secretary Securities and

Testimony of. Michael Middleton. American Bankers Association. United States Senate

Testimony of Michael Middleton On behalf of the American Bankers Association for the hearing Creating a Housing Finance System Built to Last: Ensuring Access for Community Institutions before the Banking,

Testimony of Michael Middleton On behalf of the American Bankers Association for the hearing Creating a Housing Finance System Built to Last: Ensuring Access for Community Institutions before the Banking,

A Nation of Renters? Promoting Homeownership Post-Crisis. Roberto G. Quercia Kevin A. Park

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

Qualified Mortgage Definition for HUD Insured and Guaranteed Single Family Mortgages Docket No. FR 5707-P-01

Robert R. Davis Executive Vice President Mortgage Markets, Financial Management & Public Policy (202) 663-5588 RDavis@aba.com October 25, 2013 Submitted electronically to www.regulations.gov Regulations

Robert R. Davis Executive Vice President Mortgage Markets, Financial Management & Public Policy (202) 663-5588 RDavis@aba.com October 25, 2013 Submitted electronically to www.regulations.gov Regulations

ABILITY-TO-REPAY: REGULATING OR UNDERWRITING? PART I. Author: Jonathan Foxx

Lenders Compliance Group June 20, 2011 ABILITY-TO-REPAY: REGULATING OR UNDERWRITING? PART I Author: Jonathan Foxx MAGAZINE ARTICLE Then, said Poirot, having placed my solution before you, I have the honour

Lenders Compliance Group June 20, 2011 ABILITY-TO-REPAY: REGULATING OR UNDERWRITING? PART I Author: Jonathan Foxx MAGAZINE ARTICLE Then, said Poirot, having placed my solution before you, I have the honour

Re: Regulatory Capital Treatment for High Volatility Commercial Real Estate (HVCRE) Exposures

Exposures") November 27, 2018 Robert E. Feldman Executive Secretary Federal Deposit Insurance Corporation 550 17th Street, N.W. Washington, D.C. 20429 Ann E. Misback Secretary Board of Governors of the Federal Reserve

November 27, 2018 Robert E. Feldman Executive Secretary Federal Deposit Insurance Corporation 550 17th Street, N.W. Washington, D.C. 20429 Ann E. Misback Secretary Board of Governors of the Federal Reserve

February 22, Dear Sir or Madam:

February 22, 2016 Office of the Comptroller of the Currency Legislative and Regulatory Activities Division Attn: 1557-NEW 400 7 th Street SW Suite 3E-218; Mail Stop 9W-11 Washington, DC 20219 PRAInfo@occ.treas.gov

February 22, 2016 Office of the Comptroller of the Currency Legislative and Regulatory Activities Division Attn: 1557-NEW 400 7 th Street SW Suite 3E-218; Mail Stop 9W-11 Washington, DC 20219 PRAInfo@occ.treas.gov

11 th Annual Eastern Secondary Market Conference. February 5-7, 2014 The Hyatt Regency Orlando

11 th Annual Eastern Secondary Market Conference February 5-7, 2014 The Hyatt Regency Orlando Scott D. Samlin Partner Scott Samlin is a New York partner in the firm s Financial Services & Products Group.

11 th Annual Eastern Secondary Market Conference February 5-7, 2014 The Hyatt Regency Orlando Scott D. Samlin Partner Scott Samlin is a New York partner in the firm s Financial Services & Products Group.

In summary, ABA s positions are:

1120 Connecticut Avenue, NW Washington, DC 20036 1-800-BANKERS www.aba.com World-Class Solutions, Leadership & Advocacy Since 1875 July 25, 2002 Jennifer J. Johnson Secretary Board of Governors of the

1120 Connecticut Avenue, NW Washington, DC 20036 1-800-BANKERS www.aba.com World-Class Solutions, Leadership & Advocacy Since 1875 July 25, 2002 Jennifer J. Johnson Secretary Board of Governors of the

10/17/2016. Honorable Kenneth Spearman Board Chair & Chief Executive Officer Farm Credit Administration McLean, Virginia 22102

10/17/2016 Honorable Kenneth Spearman Board Chair & Chief Executive Officer Farm Credit Administration McLean, Virginia 22102 Dear Chair/CEO Spearman: I am writing on behalf of the Independent Community

10/17/2016 Honorable Kenneth Spearman Board Chair & Chief Executive Officer Farm Credit Administration McLean, Virginia 22102 Dear Chair/CEO Spearman: I am writing on behalf of the Independent Community

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C

Revisions to Regulation C") ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C June 2017 INSERT YEAR HERE Contact Information: Rhonda Thomas-Whitley Assistant Vice President & Regulatory Counsel Rhonda.Thomas-Whitley@icba.org

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C June 2017 INSERT YEAR HERE Contact Information: Rhonda Thomas-Whitley Assistant Vice President & Regulatory Counsel Rhonda.Thomas-Whitley@icba.org

NATIONAL ASSOCIATION OF REALTORS

NATIONAL ASSOCIATION OF REALTORS The Voice for Real Estate 430 North Michigan Avenue Chicago, Illinois 60611-4087 312.329.8411 Fax 312.329.5962 Visit us at www.realtor.org. 222 St Joseph Avenue Long Beach,

NATIONAL ASSOCIATION OF REALTORS The Voice for Real Estate 430 North Michigan Avenue Chicago, Illinois 60611-4087 312.329.8411 Fax 312.329.5962 Visit us at www.realtor.org. 222 St Joseph Avenue Long Beach,

CFPB s Final Mortgage Regulations: Ability-to-Repay and Qualified Mortgage Rules March 6, E. Andrew Keeney, Esq. Kaufman & Canoles, P.C.

CFPB s Final Mortgage Regulations: Ability-to-Repay and Qualified Mortgage Rules March 6, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew Keeney,

CFPB s Final Mortgage Regulations: Ability-to-Repay and Qualified Mortgage Rules March 6, 2013 E. Andrew Keeney, Esq. Kaufman & Canoles, P.C. Ability-to-Repay and Qualified Mortgage Rules E. Andrew Keeney,

January 18, Reduced Reporting for Covered Depository Institutions. Dear Ladies and Gentlemen:

January 18, 2019 Legislative and Regulatory Activities Division Office of the Comptroller of the Currency 400 7 th Street SW Suite 3E-218 Washington, DC 20219 Ms. Ann E. Misback Secretary Board of Governors

January 18, 2019 Legislative and Regulatory Activities Division Office of the Comptroller of the Currency 400 7 th Street SW Suite 3E-218 Washington, DC 20219 Ms. Ann E. Misback Secretary Board of Governors

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau. April 4, Dear Mr.

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau April 4, 2014 Dear Mr. Silberman, The Assets & Opportunity Network (the Network) is grateful for

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau April 4, 2014 Dear Mr. Silberman, The Assets & Opportunity Network (the Network) is grateful for

Jack E. Hopkins President and CEO of CorTrust Bank Sioux Falls, SD

Testimony of Jack E. Hopkins President and CEO of CorTrust Bank Sioux Falls, SD On behalf of the Independent Community Bankers of America Before the United States Senate Committee on Banking, Housing and

Testimony of Jack E. Hopkins President and CEO of CorTrust Bank Sioux Falls, SD On behalf of the Independent Community Bankers of America Before the United States Senate Committee on Banking, Housing and

Closing disclosure provided to the consumer three days before closing the loan

November 2, 2012 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Docket No. CFPB-2012-0028 Closing disclosure provided

November 2, 2012 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Docket No. CFPB-2012-0028 Closing disclosure provided

Comptroller of the Currency. Re: Market and Consumer Impact of the Treatment of Mortgage Servicing assets under Basel III

Honorable Janet Yellen Honorable Thomas J. Curry Chair Comptroller of the Currency Board of Governors of the Office of the Comptroller of the Currency Federal Reserve System 400 7 th Street SW, Suite 3E-218

Honorable Janet Yellen Honorable Thomas J. Curry Chair Comptroller of the Currency Board of Governors of the Office of the Comptroller of the Currency Federal Reserve System 400 7 th Street SW, Suite 3E-218

Testimony of. Matthew H. Williams AMERICAN BANKERS ASSOCIATION. Subcommittee on Department Operations, Oversight, and Credit.

Testimony of Matthew H. Williams On Behalf of the AMERICAN BANKERS ASSOCIATION Before the Subcommittee on Department Operations, Oversight, and Credit of the House Committee on Agriculture United States

Testimony of Matthew H. Williams On Behalf of the AMERICAN BANKERS ASSOCIATION Before the Subcommittee on Department Operations, Oversight, and Credit of the House Committee on Agriculture United States

The Independent Community Bankers of America (ICBA) appreciates the opportunity to comment in response to Notice

appreciates the opportunity to comment in response to Notice") August 7, 2016 Internal Revenue Service CC:PA:LPD:PR (Notice 2017-38) Room 5205 Ben Franklin Station, P.O. Box 7604 Washington, D.C. 20224 RE: Comments in Response to Notice 2017-38 To Whom It May Concern:

August 7, 2016 Internal Revenue Service CC:PA:LPD:PR (Notice 2017-38) Room 5205 Ben Franklin Station, P.O. Box 7604 Washington, D.C. 20224 RE: Comments in Response to Notice 2017-38 To Whom It May Concern:

October 18, Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552

October 18, 2016 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 Re: Docket No. CFPB-2016-0038 or RIN 3170-AA61 Dear Ms. Jackson:

October 18, 2016 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 Re: Docket No. CFPB-2016-0038 or RIN 3170-AA61 Dear Ms. Jackson:

RE: Loans and Lines of Credit to Members (RIN 3133-AE88)

") Mr. Gerard Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, VA 22314 RE: Loans and Lines of Credit to Members (RIN 3133-AE88) Dear Mr. Poliquin: On behalf

Mr. Gerard Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, VA 22314 RE: Loans and Lines of Credit to Members (RIN 3133-AE88) Dear Mr. Poliquin: On behalf

RE: Title IV Program Integrity and Improvement Negotiated Rulemaking

April 2, 2014 Ms. Pamela Moran U.S. Department of Education Office of Postsecondary Education 1990 K Street, N.W. Washington, DC 20006 Submitted via email to: pamela.moran@ed.gov RE: Title IV Program Integrity

April 2, 2014 Ms. Pamela Moran U.S. Department of Education Office of Postsecondary Education 1990 K Street, N.W. Washington, DC 20006 Submitted via email to: pamela.moran@ed.gov RE: Title IV Program Integrity

November 5, Dear Sir or Madam:

Regulations Division Office of the General Counsel U.S. Department of Housing and Urban Development 451 7th Street, S.W. Room 10276 Washington, DC 20410-0500 Subject: Request for Comments on Ending Hold

Regulations Division Office of the General Counsel U.S. Department of Housing and Urban Development 451 7th Street, S.W. Room 10276 Washington, DC 20410-0500 Subject: Request for Comments on Ending Hold

How to Start Planning for the CFPB Mortgage Rules. May 2, 2013

How to Start Planning for the CFPB Mortgage Rules May 2, Jon Bundy Regulatory Compliance Manager CUNA Mutual Group 608-665-7101 Jonathan.bundy@cunamutual.com Agenda Short Review of Each Rule We will avoid

How to Start Planning for the CFPB Mortgage Rules May 2, Jon Bundy Regulatory Compliance Manager CUNA Mutual Group 608-665-7101 Jonathan.bundy@cunamutual.com Agenda Short Review of Each Rule We will avoid

Re: Docket No. CFPB , Payday, Vehicle Title, and Certain High-Cost Installment Loans

http://www.regulations.gov. October 7, 2016 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Docket No. CFPB-2016-0025,

http://www.regulations.gov. October 7, 2016 Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Docket No. CFPB-2016-0025,

January 8, Alison Touhey Vice President Office of Regulatory Affairs Phone:

Alison Touhey Vice President Office of Regulatory Affairs Email: atouhey@aba.com Phone: 202-663-5182 January 8, 2018 Submitted Electronically Legislative and Regulatory Activities Division Office of the

Alison Touhey Vice President Office of Regulatory Affairs Email: atouhey@aba.com Phone: 202-663-5182 January 8, 2018 Submitted Electronically Legislative and Regulatory Activities Division Office of the

SUMMARY: The Bureau of Consumer Financial Protection (CFPB or Bureau) is publishing this agenda

is publishing this agenda") This document is scheduled to be published in the Federal Register on 06/09/2016 and available online at http://federalregister.gov/a/2016-12931, and on FDsys.gov BUREAU OF CONSUMER FINANCIAL PROTECTION

This document is scheduled to be published in the Federal Register on 06/09/2016 and available online at http://federalregister.gov/a/2016-12931, and on FDsys.gov BUREAU OF CONSUMER FINANCIAL PROTECTION

Statement for the Record. American Bankers Association. Agriculture Committee. United States House of Representatives

Statement for the Record On Behalf of the American Bankers Association before the Agriculture Committee of the United States House of Representatives Statement for the Record On behalf of the American

Statement for the Record On Behalf of the American Bankers Association before the Agriculture Committee of the United States House of Representatives Statement for the Record On behalf of the American

S Analysis of Regulatory Relief for Credit Union

S. 2155 Analysis of Regulatory Relief for Credit Union June 2018 SECTION Minimum Standards for Residential Mortgage Loans (Section 101) Adds a new safe harbor category of Qualified Mortgages (QMs) to Section

S. 2155 Analysis of Regulatory Relief for Credit Union June 2018 SECTION Minimum Standards for Residential Mortgage Loans (Section 101) Adds a new safe harbor category of Qualified Mortgages (QMs) to Section

HOUSING & MORTGAGE COUNSELOR

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

Loan participations should not be swept up within the swap definition under Dodd- Frank. In relevant part, the new definition of swap includes:

January 25, 2011 Mr. David A. Stawick Secretary Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, N.W. Washington DC 20581 Ms. Elizabeth M. Murphy Secretary Securities and Exchange

January 25, 2011 Mr. David A. Stawick Secretary Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, N.W. Washington DC 20581 Ms. Elizabeth M. Murphy Secretary Securities and Exchange

Usda loan credit score requirements texas

Usda loan credit score requirements texas Learn about the USDA Mortgage program and prequalify for a $0 down USDA Loan with the specialists at USDALoans.com Program Status: Open Program Factsheet: PDF.

Usda loan credit score requirements texas Learn about the USDA Mortgage program and prequalify for a $0 down USDA Loan with the specialists at USDALoans.com Program Status: Open Program Factsheet: PDF.

Jim Nussle President & CEO. Phone:

Jim Nussle President & CEO 99 M Street SE Suite 300 Washington, DC 20003-3799 Phone: 202-508-6745 jnussle@cuna.coop March 11, 2019 The Honorable Mike Crapo Chairman Committee on Banking, Housing and Urban

Jim Nussle President & CEO 99 M Street SE Suite 300 Washington, DC 20003-3799 Phone: 202-508-6745 jnussle@cuna.coop March 11, 2019 The Honorable Mike Crapo Chairman Committee on Banking, Housing and Urban

Covered loans or applications if the property is

Application Date 1003.4(a)(1)(ii) Property Address State County Census Tract Covered loans or applications if the property address of the property securing the covered loan is not known (e.g., the property

Application Date 1003.4(a)(1)(ii) Property Address State County Census Tract Covered loans or applications if the property address of the property securing the covered loan is not known (e.g., the property

TIPS BULLETIN #13-17

TIPS BULLETIN #13-17 To: Subject: All Credit Unions Ability to Repay & Qualified Mortgage Standards under the Truth in Lending Act (Regulation Z) The material in this publication is provided for educational

TIPS BULLETIN #13-17 To: Subject: All Credit Unions Ability to Repay & Qualified Mortgage Standards under the Truth in Lending Act (Regulation Z) The material in this publication is provided for educational

Request for Additional Clarity and Guidance Related to the FHA Single Family Housing Policy Handbook

Brian Montgomery FHA Commissioner and Assistant Secretary for Housing U.S. Department of Housing and Urban Development 451 7 th Street, SW Washington, DC 20410 Request for Additional Clarity and Guidance

Brian Montgomery FHA Commissioner and Assistant Secretary for Housing U.S. Department of Housing and Urban Development 451 7 th Street, SW Washington, DC 20410 Request for Additional Clarity and Guidance

Re: Request for Information Regarding Bureau Enforcement Processes (Docket No. CFPB )

") May 14, 2018 By Electronic Submission Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 www.regulations.gov Jan Stieger, CMP,

May 14, 2018 By Electronic Submission Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 www.regulations.gov Jan Stieger, CMP,

19 FREQUENTLY ASKED QUESTIONS

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

February 14, Dear Ms. Naulty:

February 14, 2014 Ms. Peggy Naulty Division of Consumer and Community Affairs Board of Governors of the Federal Reserve System 20 th Street and Constitution Avenue N.W. Washington, DC 20551 Dear Ms. Naulty:

February 14, 2014 Ms. Peggy Naulty Division of Consumer and Community Affairs Board of Governors of the Federal Reserve System 20 th Street and Constitution Avenue N.W. Washington, DC 20551 Dear Ms. Naulty: