Collection Manual Guidelines for Attachment

|

|

|

- Godfrey Morgan

- 6 years ago

- Views:

Transcription

1 Collection Manual Guidelines for Attachment January

2 Table of Contents 1. Summary Introduction Purpose Scope Terms of Reference - Definitions: S.1002 (1) (a) TCA, Conditions & Instructions for Attachment Legal Issues / Precedents Attachment Obligations When is Attachment Used Enforcement Summary Attachment Case-Working Procedures Final Demand The Notice of Attachment Notice of Revocation Follow Up on Notice of Attachment ICM Attachment Process Manual Attachment Contact Details S of Taxes Consolidation Act, On-Line Payment of Attachment Amounts...16 Appendix 1 - Attachment Proposal Checklist and FAQ s...17 Appendix 2 - Final Demands...17 Appendix 3 Institute Specific Instructions...17 Appendix 4 - Penalty proceedings...17 Appendix 5 - Attachment Letters (Non Wages / Salary)...17 Appendix 6 Links to Attachment Letters (Wages / Salary)...17 Appendix 7 Attachment Update Reasons...18 Appendix 8 On-Line Payments

3 1. Summary The following is a summary of the main points covered in these guidelines to assist staff in the use of attachment and in identifying cases suitable for this form of enforcement: Attachment is an exemplary enforcement option and should be used by caseworkers where conventional enforcement, i.e. Sheriff/Solicitor, has failed. Attachment should not be deployed where the taxpayer is proactively engaging with the caseworker to agree a mutually acceptable phased payment arrangement. Attachment can be used only in this jurisdiction, i.e. within 26 counties. Notices of Attachment can only be issued against debtors to or employer(s) of the taxpayer (attachee). A Final Demand must have issued to the taxpayer prior to issuing a Notice of Attachment. There is a specific Final Demand where attachment of wages or salary is contemplated and this demand must be accompanied by a blank Financial Statement. A debt made up of tax, interest and/or penalties due to Revenue may be the subject of a Notice of Attachment. The minimum debt for the use of a general attachment is 1,000 in the cases of an attachment of wages and salary it is 10,000. Attachment of wages or salary should only be considered where: Total tax, interest & penalties due exceed 10,000 and The amount due is in default for a period of at least 6 months and The defaulting taxpayer is currently earning in excess of 50,000 gross annually. There is no other attachment option available, e.g. attachment of bank accounts. Notices of Attachment can not issue until the time specified in the Final Demand has elapsed minimum of 14 days in cases of attachment of wages or salary and minimum of 7 days for all other cases. Caseworkers should always verify the names and addresses and other relevant details of taxpayers and attachees before issuing Notices of Attachment. Notices of Attachment require approval by an Authorised Officer, i.e. a Principal Officer or a nominated Assistant Principal Officer. The Attachment Proposal checklist at Appendix 2 must be completed by the caseworker. The original Notice of Attachment issues to the Attachee (debtor or employer) by registered post or is hand delivered. A copy is then sent to the taxpayer. See 3

4 Page 39 in relation to retention of all original Notice of Attachment documentation. An Attachment Order remains in place until it is satisfied (paid in full) or revoked by the caseworker, usually on one of the following grounds: Satisfied in part when part of the amount specified in the Notice of Attachment has been paid and there is little or no likelihood of further payment, or Revoked when the attachee does not owe money to the taxpayer, or the attachee ceases to be legally liable to pay salary/wages under a contract of service, or Engagement - the taxpayer is negotiating a phased payment arrangement with the caseworker and there are grounds to believe that an acceptable arrangement can be concluded. The ICM Attachment Process contains all the instructions required for issuing Notices of Attachment. 2. Introduction Revenue s power of attachment originated in the Finance Act, 1988 and is now covered by S of the Taxes Consolidation Act, (TCA) This legislation authorises Revenue to attach a third party, or an employer, where there is a debt due to the taxpayer from the attachee, for tax outstanding to Revenue. Attachment is a very effective enforcement method of collecting unpaid tax debts where conventional enforcement, i.e. Sheriff/Solicitor has failed. The main advantages of attachment are: Speed: The attachee must submit a statutory return/payment within 10 days. The outcome is known in days. No judgment or legal proceedings required, i.e. no court delays. Several Notices of Attachment can be issued to different attachees simultaneously to cover different portions of the liability. Cost: Attachment is very cost effective. Revenue or the taxpayer. There are no legal fees incurred by Results: Attachment remains active until the debt on the Notice of Attachment is either paid or the Notice of Attachment is revoked by Revenue In cases where the taxpayer, who is currently an employee, refuses to address a tax debt it can ensure that the outstanding debt is recovered, in whole or in part. Attachment can be helpful in getting a taxpayer to engage meaningfully with Revenue because of the implications that ongoing attachment can have for a taxpayer s standing with clients and financial institutions. 4

5 3. Purpose The purpose of these guidelines is to assist caseworkers in understanding attachment as a method of enforcement and to highlight the benefits of using attachment to enforce payment of outstanding debt owed to Revenue. 4. Scope These guidelines are for all Revenue staff engaged in debt collection caseworking and may be supplemented by local instructions in the Collector-General s Division or in a Region, as necessary, to reflect particular concerns in individual areas. 5. Terms of Reference - Definitions: S.1002 (1) (a) TCA, Debt A debt may be described as the aggregate amount of money due by the debtor (attachee), to the taxpayer from the time of receipt of the Notice of Attachment until the debt is fully paid or the Notice of Attachment is revoked. S.74 Finance Act, 2011, amended Section 1002(1)(c), removing the exclusion in the original legislation in relation to the attachment of any amount due by a third party to the taxpayer as emoluments, under a contract of service i.e. wage/salary payments assessable to Income Tax under Schedule E. The amended S.1002 (1) (c) provides for Revenue to issue Notices of Attachment to employers in respect of wages/salaries where the employee has a tax debt. Relevant Person/Attachee A relevant person (attachee) for the purposes of attachment is a person that Revenue has reason to believe owes a debt to the taxpayer. Suitable attachees include: Financial Institutions (Banks, Building Societies, Insurance Companies, Credit Unions, Merchant Acquirers) and State Agencies (Government Departments, Health Boards, An Post, the Legal Aid Board, OPW). Other Debtors e.g. Regular customers Employers Other entities from which the taxpayer is due to receive once-off payments, e.g. Court settlements, Compulsory Purchases Orders. Please note that in this guideline the Relevant Person is mostly commonly called the Attachee. The definition above applies to both. 5

6 Specified Amount The specified amount is the amount, or portion of the amount of the outstanding tax, interest and penalties included in the Notice of Attachment. It covers all taxes, duties, levies or charges placed under the care and management of the Revenue Commissioners. This includes debts in respect of the following taxes, duties and levies: Income tax (including employer s PAYE), Corporation Tax Capital Gains Tax / Capital Acquisitions Tax Stamp Duties / Customs Duties / Excise Duties Value Added Tax PRSI Self-employed PRSI Contributions Universal Social Charge Environmental Levy Local Property Tax Relevant Period The relevant period is the period starting at the time of receipt by the relevant person (e.g. the bank) of the Notice of Attachment and ending on the earliest of: Payment of the specified amount to Revenue by the relevant person, or Receipt of a Notice of Revocation by the relevant person, or The relevant person or the taxpayer (an individual), being declared bankrupt, or, if the relevant person or taxpayer is a company, being wound up. 6. Conditions & Instructions for Attachment The following conditions apply to the use of Attachment: A final demand must have issued. There is a specific Final Demand Notice that outlines our intention to attach wages/salary and includes a Financial Statement. This gives the taxpayer the opportunity to bring particular financial pressures to our attention. These financial pressures will be taken into account when deciding on the period over which collection through the Notice of Attachment may be spread. In the case of a general attachment the following criteria apply The total debt [tax, interest and penalties] must be a minimum of 1,000 The debt must be in default for at least one month The final demand period of 7 days has elapsed. 6

7 In cases of attachment of wages/salary the following criteria apply The total debt [tax, interest and penalties] must be a minimum of 10,000 and The taxpayer must be in default for a period of at least 6 months, and The final demand period of 14 days has elapsed. Gross earnings must be in excess of 50,000 per annum (this can encompass multiple employments) and be based on the most recent year for which P35 or P60 data is available this data should be less than 2 years old. Examples of suitability for attachment of wages and salaries The debt may be spread over a number of attachments. But each portion of the debt must be included in only one Notice of Attachment. If good attachment information is obtained while other forms of enforcement are ongoing the caseworker may decide, in consultation with the solicitor/sheriff, to withdraw proceedings or recovery action and issue a Notice of Attachment. If a VAT repayment claim has been made by a taxpayer and it is the subject of an open work item - then BEFORE enforcing any outstanding tax the caseworker should contact the relevant district to confirm whether the claim is available for offset - If the claim is available for offset and will be set against the outstanding tax then only the remaining debt should be enforced. If the claim is not available for offset then the caseworker should contact the taxpayer stating that the claim is not available to offset against outstanding taxes prior to sending the tax to enforcement. In some cases the VAT repayment claim is being held pending receipt of additional information. The caseworker should make it clear to the taxpayer that if the information requested is not provided within a defined deadline (1-2 weeks) then the outstanding tax will be enforced. Notices of Attachment / Revocation Orders are signed at PO level or upwards in their absence a nominated AP may sign. Notices of Attachment must be sent by registered post or hand-delivered. The following may not be attached as they are not regarded as debt due to the taxpayer: Deposits (e.g. down-payments on property) held by Solicitors in Client Accounts. Any amount owed to the taxpayer that is in dispute or subject to litigation. A grant to which the taxpayer has no legal entitlement, i.e. it is payable at the discretion of the awarding body. The amount remaining in an overdraft facility. Amounts that are subject to a court order e.g. court mandated maintenance payments may be made from an account that is attached 7

8 Suitability for Attachment (Wages/Salary) Where the taxpayer cannot pay the debt included in the final demand in full or make solid and acceptable arrangements to pay the debt due to Revenue, they should complete and return the Financial Statement. Once the Financial Statement has been received the caseworker will then examine the Financial Statement and if necessary consult with their manager to determine: If the taxpayer has the capacity to pay some or all of the debt. By taking into account the information provided in the Financial Statement a decision can be made as to whether it is appropriate to proceed with the attachment of wages/salary. The Financial Statement will allow for avoidance of a situation whereby the Notice of Attachment would result in the defaulting taxpayer (employee) requiring financial assistance for basic living expenses from another Government department or agency. If the taxpayer does not submit a completed Financial Statement and the caseworker is proceeding with a notice of Attachment to an employer then the thresholds set out in the Department of Social Protection s Family Income Supplement (FIS) scheme should form the basis for the living expenses allowed. The caseworker should therefore be familiar with criteria and thresholds for Family Income Supplement (FIS) as set out in Dept Social Protection website (access Family Income Supplement through the Search facility) If appropriate, the caseworker can insert an instruction on the Notice of Attachment to the employer specifying the amount and duration of payments to be paid to Revenue. The caseworker should ensure that any instructions sent to an employer are of a reasonable duration. 8

9 The following examples will assist caseworkers in using the information on the Financial Statement to determine suitability for Notice of Attachment (Wages / Salary): Case 1 (i) T/P owes Revenue 15,000 (ii) T/P is married with two dependant children (iii) Prior to the issue of the final demand, there isn t up to date information on t/p s annual income (iv) T/P income for month per the financial statement is 2,200 (less than 50k pa) As income for the year is less than 50k, Notice of Attachment (Wages/Salary) is not appropriate. Case 2 (i) T/P owes Revenue 15,000 (ii) T/P is married with two dependant children (iii) Prior to the issue of the final demand, P35 data indicated that t/p s annual income for the previous year was 60,000 (iv) Total T/P income for month per the Financial Statement is 6,000 (greater than 50k per annum) (v) Monthly outlay per Financial Statement is 2,500 (vi) Balance suitable for attachment = 1,092 (i.e. 6,000-2,500-2,408 FIS threshold) (vii) (viii) 15,000 divided by 1,092 = months. The Notice of Attachment will specify that the employer will pay Revenue 1,092 for 13 months followed by a final payment of 804 to cover the full specified amount of 15,000. Collection of Liabilities relating to Business Partnerships (Wages/Salary) To assist the employer in identifying the relevant employee, the Notice of Attachment documentation issued in relation to attachment of wages/salary will contain the current tax reference number for the employee. To ensure the correct allocation of payments received under Notices of Attachment (Wages / Salary) where the employee s earnings are attached to cover liabilities relating to a Partnership, caseworkers must insert the letter P after Our Ref., e.g. G P on the Return under Notice of Attachment and Further Return under Notice of Attachment (wages/salary) documents in advance of issuing them to the attachee (employer). 9

10 7. Legal Issues / Precedents The following circumstances in relation to attachment have previously arisen and were researched. Additional scenarios can be found in the Attachment FAQ s. (i) (ii) (iii) (iv) Joint Bank A/Cs Joint accounts with financial institutions may be attached. Unless evidence to the contrary is produced within 10 days of the Notice of Attachment, a joint account will be deemed to be held equally for the benefit of each party to the account. Where contrary evidence is produced within the time limit, the amount shown to be held by the taxpayer is regarded as a debt due to him/her and is covered by the attachment provisions once the Notice of Attachment has issued. Credit Unions Where a Credit Union standard loan agreement required the taxpayer to genuinely pledge his existing account balance as security, the attachment provisions do not cover such account balance. Any doubts may be resolved by requesting a copy of the loan agreement. Proceeds of Property Sales These are not suitable for attachment. Due to the nature of conveyancing transactions, a debt normally only arises on the closing date of a sale. This debt is normally paid on that same day. After the closing date, there is no debt, as the sum has been discharged. Revenue cannot attach a solicitor holding undistributed funds from an estate either. Banks Off-Setting Accounts Banks may exercise a right of off-set if there is an immediately recoverable debt due to the bank by the customer. The contract between the bank and the customer will determine if a debt is immediately recoverable. Example 1 A taxpayer operates two current accounts: Account No. 1 is 10,000 overdrawn; Account No. 2 is 4,000 in credit. The Bank can off-set in this case and is not obliged to pay over the 4,000 from the No. 2 Account under a Notice of Attachment. The taxpayer cannot sue the Bank for any debt due, as s/he is still indebted to the Bank for the sum of 6,000, ( 10,000 minus 4,000). Example 2 A taxpayer operates two accounts with the financial institution: Account No. 1 is a Loan account for 3,000; Account No. 2 is 1,000 in credit. The bank cannot use off-set in this case. An off-set must be in respect of an active, immediately recoverable debt due to the bank, whereas loan repayments are governed by a contract. 10

11 (v) Post-Dated Arrangements Amounts covered by post-dated arrangements are not subject to attachment. A debt does not exist between the parties unless the Bank fails to honour a post-dated arrangement. Example: A Ltd owes 10,000 to B Ltd and begins a post-dated arrangement with B Ltd for 10,000. B Ltd owes Revenue 10,000. If a Notice of Attachment is issued to A Ltd, they do not have to pay Revenue, as the debt was paid when the post-dated arrangement for 10,000 was agreed. If the arrangement is not honoured when presented to the bank then the original debt becomes due. (vi) Attachment of pension funds and/or payments Pension funds may be the subject of an attachment as a debt due to the taxpayer. In order for a debt to be due the funds have to be paying out to the taxpayer. A fund due to pay a taxpayer at a future date is not suitable for attachment. Any attachment placed on a pension should be revoked if the caseworker becomes aware that the pension is not due to pay out until a future date. (vii) Attachment of Individual Partner s Account for Debt of Partnership Individuals within an ordinary partnership are jointly and severally liable for the debts of the partnership. Ordinary partnership is defined as the relationship which subsists between persons carrying on a business in common with a view of profit (Section 1(1) of the Partnership Act, 1890). The provisions of the Partnership Act govern an ordinary partnership where no partnership agreement is in place. Individual partners can be pursued for the full debts of the partnership provided the debt arose during a period when they were members of a partnership. Where individual partners bank accounts are held in personal names as opposed to under the name of the partnership, the contents of same can be attached. A Final Demand must issue to the partnership and each individual partner. Where Revenue issues a Notice of Attachment to a financial institution for the debts of a partnership Revenue can also request that it is applied to each individual partner s bank account. Caseworkers can issue the Notice of Attachment under the Partnership details i.e. registration number, name/address of partnership and also list the names and addresses of the partners. DO NOT INCLUDE THE PPSN OF THE PARTNERS IN THE NOTICE OF ATTACHMENT. 11

12 8. Attachment Obligations The obligations on the Relevant Person, Taxpayer and Revenue are: Relevant Person (Attachee): Within 10 days of receiving the Notice of Attachment from Revenue, the attachee must deliver to Revenue, a return in writing, indicating whether or not any debt is due to the taxpayer specified in the notice. If a return is not received within 10 working days then under S1002 (7) of TCA, 97 a liability to a penalty arises under Section 1052(1) on the attachee and if the attachee is a company then also under Section 1054 on the company secretary. Wages/Salary Where the attachee employs the taxpayer under a contract of service, s/he is required to provide details of all wages/salary payable to the taxpayer. The attachee (employer) must pay Revenue the specified amount over the specified period of time in the Notice of Attachment out of the wages/salary payable to the taxpayer. Non -Wages/Salary Where a debt is due to the taxpayer, the debt due must be paid to Revenue up to the value of the specified amount. Where the specified amount on the Notice of Attachment has not been fully satisfied and a further debt becomes due to the taxpayer during the relevant period, the attachee must make another return and payment to Revenue within 10 days of the date the debt is due to be paid. This process continues until the amount specified has been paid. If there is no debt outstanding by the attachee to the taxpayer, a Nil return must be submitted to Revenue by the attachee. The attachee in non-wages/salary cases may not make any disbursement out of the debt/additional debt due to the taxpayer during the relevant period except to the extent that: (i) it will not reduce the debt below the amount of debt shown in the Notice of Attachment, or (ii) the disbursement is made pursuant to a Court Order The attachee must advise the taxpayer that payment has been made to Revenue under a Notice of Attachment. The attachee is liable for prosecution under Section 1002(5) TCA, 1997, for the provision of an incorrect return. Section 904K, TCA, 1997 as introduced under S.74 of the FA 2011 allows an authorised Revenue Officer to enter a premises or place of business of a relevant person at all reasonable times for the purposes of auditing a return made under a Notice of Attachment. 12

13 The Taxpayer: The taxpayer may pay Revenue on foot of the final demand or at any time before the attachee pays Revenue. If the taxpayer pays Revenue in full, the Notice of Attachment is satisfied and should be revoked promptly. Where the attachee pays money to Revenue, the taxpayer must treat the payment as if s/he received it directly. Revenue: Copies of Notices of Attachment and Notices of Revocation should be given promptly by Revenue to the taxpayer. Revenue will issue receipts to both taxpayer and the attachee for all payments received on foot of a Notice of Attachment. 9. When is Attachment Used In most cases, the first enforcement option selected will be Sheriff or Solicitor. However, attachment may be considered as a first option if the overall debt to Revenue is already at a substantial level or is escalating rapidly. Caseworkers should discuss the possibility of using attachment as a first enforcement option with their manager in advance of proceeding. The Principal Officer signing the notification must be made aware of the reasons for using attachment as a first option. Attachment may be used to secure payment of all or part of the debt in a case. Multiple Notices of Attachment may be issued to one attachee by Revenue in respect of different taxpayers. Multiple Notices of Attachment may be issued to multiple debtors of one taxpayer at the same time provided the debt is divided among the debtors. Where only part of the debt is paid on foot of the Notice of Attachment, i.e. when the debt owed to the taxpayer by the attachee is less than that owed to Revenue the Notice of Attachment must be revoked in advance of pursuing alternative enforcement methods to address the balance of the debt. Example: 13

14 Mr. Bronach supplies Circles to the Square Diamond Co. Mr. Bronach owes 20k in VAT for the taxable period July/Aug, due on 19th Sept. Mr Bronach has been referred twice to sheriff in the last six months and while the tax has been paid his compliance has not improved. Revenue has reason to believe that the Square Diamond Co. owes a substantial debt to Mr. Bronach. 10th Oct: A Final Demand for the 20k tax is issued. 24 th Oct: There has been no response from Mr. Bronach and the VAT remains outstanding. As it is a Friday, the attachment doesn t issue until Monday the 27 th October after checking to ensure the VAT remains unpaid. 27 th Oct: The pre-conditions for issuing a Notice of Attachment have been satisfied, i.e. 30 days have passed since the date of default and 7 days have passed since a Final Demand notice has been served on the taxpayer. A Notice of Attachment issues to the Square Diamond Co., for the 20, tax and interest due to Revenue by Mr. Bronach. A copy of the Notice of Attachment is sent to Mr. Bronach. 29 th Oct: A very irate Mr. Bronach phones and accuses Revenue of breaching his right to confidentiality for disclosing his tax affairs to the Square Diamond Co. and insists that the Notice of Attachment is revoked immediately. Mr. Bronach is advised that under Sec 1002 (15) TCA 1997, the secrecy obligations imposed on Revenue do not apply in relation to information contained in a Notice of Attachment. He apologises and offers to pay the tax immediately. Later that afternoon, Mr. Bronach hand delivers a bank draft for 20, He requests that the Notice of Attachment be revoked immediately. On the same afternoon, the debtor is notified that Revenue is revoking the attachment and a Notice of Revocation is issued to the Square Diamond Co., which they receive on 31 st Oct. For the purposes of Attachment in the above example: Relevant Person/Attachee: Square Diamond Co Specified Amount: Debt: Relevant Period: 20, VAT plus interest owed by Mr. Bronach to Revenue 30,000 owed by the Square Diamond Co to Mr Bronach The period starting on the date the Square Diamond Co. receives the Notice of Attachment (26 th Oct.) and ending on the date on which they receive the Notice of Revocation (31 st Oct.) 14

15 10. Enforcement Summary 11. Attachment Case-Working Procedures Final Demand 12. The Notice of Attachment 13. Notice of Revocation 14. Follow Up on Notice of Attachment 15. ICM Attachment Process 15

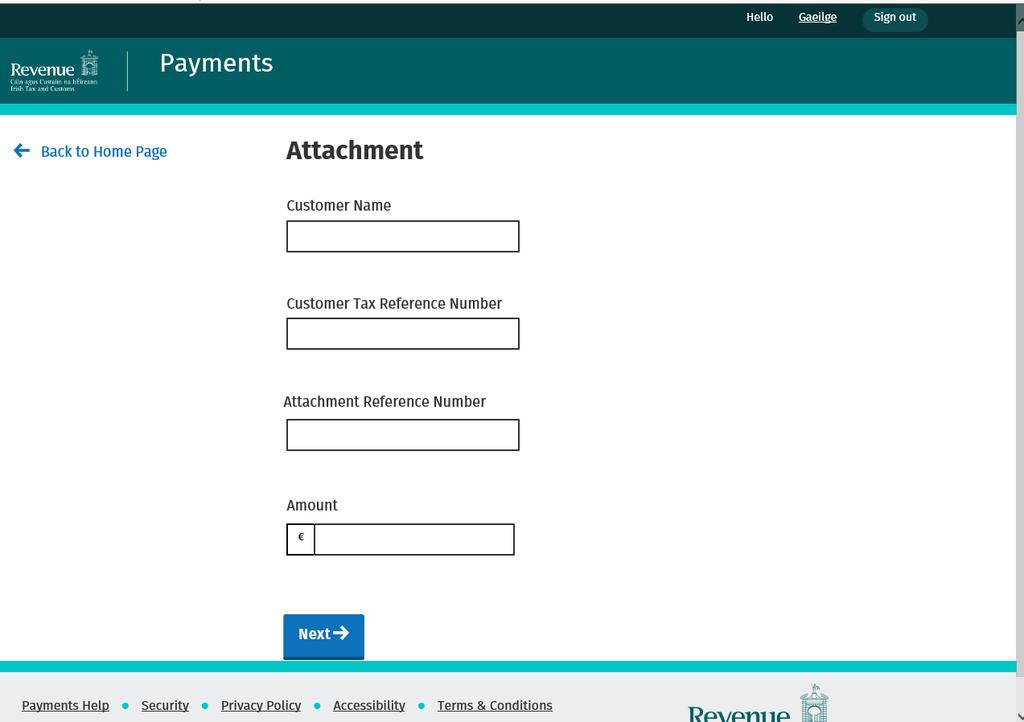

16 16 Manual Attachment 17 Contact Details 18 S of Taxes Consolidation Act, 1997 This Legislation is available on Revenue s website. 19 On-Line Payment of Attachment Amounts Revenue On-Line Service (ROS) ROS customers can make attachment payments online through ROS. To access ROS or to register for ROS, click on the ROS link on the Revenue home page at myaccount myaccount customers can make attachment payments online by clicking on the myaccount link on the Revenue home page. You can register for myaccount on the Register for myaccount link on On the payment screen on ROS or myaccount click Attachment. You will be asked to provide the following details in order to make a payment: Customer name ; insert the business or entity named on the attachment order Customer tax reference: insert the business or entity named on the attachment order Attachment reference number: this is provided on the notice of attachment Amount: Insert the amount that you are paying on foot of the attachment Payment can be made online using: 16

17 debit card or credit card once off debit a Single Debit Instruction using a bank account capable of accepting a direct debit. For further details please see Appendix 8 Appendix 1 - Attachment Proposal Checklist and FAQ s Appendix 2 - Final Demands Appendix 3 Institute Specific Instructions Appendix 4 - Penalty proceedings Appendix 5 - Attachment Letters (Non Wages / Salary) Appendix 6 Links to Attachment Letters (Wages / Salary) 17

18 Appendix 7 Attachment Update Reasons Appendix 8 On-Line Payments ROS 18

19 19

20 20

21 MYACCOUNT Paying an Attachment via myaccount - 5 Easy Steps Step 1 Access the myaccount online payment facility on the Revenue website by clicking on the myaccount link on the homepage. You will see a Payments section on the home page. Step 2 Click on Pay now on the Payments Section on the myaccount home page. You will be asked What type of payments are you making the drop down menu defaults to tax. Click Attachment and you will be presented with the attachment payments screen. Step 3 Click Add payment. Enter the details requested on the payment screen and click Add payment Step 4 You will now be asked How do you wish to pay. Select your preferred payment method and enter the relevant details. Remember to insert an address. When complete click Add payment to proceed. Step 5 You will now be presented with a Sign and Submit screen with your PPSN prepopulated. You must enter your myaccount password to complete the payments process. Click Sign and submit and you will then be presented with a screen that confirms payment. This completes the payment process. 21

Requirement for Security Bonds. Section 960S TCA Revised: September 2017

Section 960S TCA 1997 Revised: September 2017 0 Contents 1. Introduction...2 2. Purpose...3 3. Types of Bonds acceptable to Revenue...3 4. Criteria for Determining Case Suitability for Bond Application...3

Section 960S TCA 1997 Revised: September 2017 0 Contents 1. Introduction...2 2. Purpose...3 3. Types of Bonds acceptable to Revenue...3 4. Criteria for Determining Case Suitability for Bond Application...3

Guidelines for issuing manual PAYE/PRSI/USC/LPT Annual P35 Estimates and Amended Estimates. Document last updated December 2018

Guidelines for issuing manual PAYE/PRSI/USC/LPT Annual P35 Estimates and Amended Estimates Document last updated December 2018 This applies to all periods prior to 1/1/2019 1 PART 1 GUIDELINES FOR ISSUE

Guidelines for issuing manual PAYE/PRSI/USC/LPT Annual P35 Estimates and Amended Estimates Document last updated December 2018 This applies to all periods prior to 1/1/2019 1 PART 1 GUIDELINES FOR ISSUE

Capital Acquisitions Tax. Collector-General / District Guidelines

Capital Acquisitions Tax Collector-General / District Guidelines This document was last updated April 2017 Table of Contents: 1. Introduction...3 6. Due Dates 3 7. Interest on Late Payments...4 14. Postponement

Capital Acquisitions Tax Collector-General / District Guidelines This document was last updated April 2017 Table of Contents: 1. Introduction...3 6. Due Dates 3 7. Interest on Late Payments...4 14. Postponement

Part 41A Assessing rules including rules for self assessment

Part 41A Assessing rules including rules for self assessment CHAPTER 1 Interpretation (Part 41A) 959A Interpretation 959B Supplemental interpretation provisions CHAPTER 2 Assessments: General Rules 959C

Part 41A Assessing rules including rules for self assessment CHAPTER 1 Interpretation (Part 41A) 959A Interpretation 959B Supplemental interpretation provisions CHAPTER 2 Assessments: General Rules 959C

Tax & Duty Manual. Procedures for Personal Insolvency Caseworking. Collector-General s Office

Tax & Duty Manual Procedures for Personal Insolvency Caseworking Collector-General s Office Updated September 2017 1 Table of Contents 1. Background Legislation...4 2. Procedures for Dealing with Personal

Tax & Duty Manual Procedures for Personal Insolvency Caseworking Collector-General s Office Updated September 2017 1 Table of Contents 1. Background Legislation...4 2. Procedures for Dealing with Personal

Frequently Asked Questions about Qualifying Disclosures relating to Offshore Matters

Frequently Asked Questions about Qualifying Disclosures relating to Offshore Matters 1 . FOREIGN INCOME AND ASSETS DISCLOSURE... 5 1.1. What proposed changes were announced in the recent Budget?... 5 1.2

Frequently Asked Questions about Qualifying Disclosures relating to Offshore Matters 1 . FOREIGN INCOME AND ASSETS DISCLOSURE... 5 1.1. What proposed changes were announced in the recent Budget?... 5 1.2

Νοtes for Guidance Taxes Consolidation Act 1997 Finance Act 2017 Edition - Part 42

Part 42 Collection and Recovery CHAPTER 1 Income Tax 960 Date for payment of income tax other than under self assessment 961 Issue of demand notes and receipts 962 Recovery by sheriff or county registrar

Part 42 Collection and Recovery CHAPTER 1 Income Tax 960 Date for payment of income tax other than under self assessment 961 Issue of demand notes and receipts 962 Recovery by sheriff or county registrar

Collection Manual Liquidation of Companies and other Company Law issues

Collection Manual Liquidation of Companies and other Company Law issues Updated November 2015 CONTENTS 1 Introduction...3 2 What is Liquidation?...3 3 When is it appropriate to seek liquidation of a company?...3

Collection Manual Liquidation of Companies and other Company Law issues Updated November 2015 CONTENTS 1 Introduction...3 2 What is Liquidation?...3 3 When is it appropriate to seek liquidation of a company?...3

Summary of Pay & File system for Income Tax and CGT

Part 41A-01-03 Summary of Pay & File system for Income Tax and CGT under Part 41A of the TCA 1997 Part 41A-01-03 This document was last updated September 2017 1 Table of Contents 1 Obligation to file a

Part 41A-01-03 Summary of Pay & File system for Income Tax and CGT under Part 41A of the TCA 1997 Part 41A-01-03 This document was last updated September 2017 1 Table of Contents 1 Obligation to file a

Important information regarding Term Deposits and Farm Management Deposits

Important information regarding Term Deposits and Farm Management Deposits 31 day notice period for early terminations New rules apply from 1 January 2015. You will need to give St.George 31 days notice

Important information regarding Term Deposits and Farm Management Deposits 31 day notice period for early terminations New rules apply from 1 January 2015. You will need to give St.George 31 days notice

Facility Agreement Continuing Credit Facility - Line of Credit Terms & Conditions

Facility Agreement Continuing Credit Facility - Line of Credit Terms & Conditions Version 2, March 2013 Contents Section 1 Section 2 LINE OF CREDIT....1 DRAWDOWNS... 1 Section 3 REPAYMENTS........1 Section

Facility Agreement Continuing Credit Facility - Line of Credit Terms & Conditions Version 2, March 2013 Contents Section 1 Section 2 LINE OF CREDIT....1 DRAWDOWNS... 1 Section 3 REPAYMENTS........1 Section

PROCLAMATION NO. /2016 TAX ADMINISTRATION PROCLAMATION

PROCLAMATION NO. /2016 TAX ADMINISTRATION PROCLAMATION WHERAS, it is necessary to enact a separate tax administration proclamation governing the administration of domestic taxes with a view to render the

PROCLAMATION NO. /2016 TAX ADMINISTRATION PROCLAMATION WHERAS, it is necessary to enact a separate tax administration proclamation governing the administration of domestic taxes with a view to render the

Guidelines for Charging Interest on Late Payment Through PAILP, ICM Activities and Direct Debit. This document was last updated in November 2017

Tax and Duty Manual Guidelines for charging Interest on Late Payment Guidelines for Charging Interest on Late Payment Through PAILP, ICM Activities and Direct Debit This document was last updated in November

Tax and Duty Manual Guidelines for charging Interest on Late Payment Guidelines for Charging Interest on Late Payment Through PAILP, ICM Activities and Direct Debit This document was last updated in November

Term Deposits. Terms and Conditions and General Information.

Term Deposits. Terms and Conditions and General Information. Effective Date: 12 November 2016 This booklet sets out the terms and conditions for BankSA Term Deposit Accounts, along with general information

Term Deposits. Terms and Conditions and General Information. Effective Date: 12 November 2016 This booklet sets out the terms and conditions for BankSA Term Deposit Accounts, along with general information

APPOINTMENT AS TAX CONSULTANTS TO:

APPOINTMENT AS TAX CONSULTANTS TO: Name: Identity Number: Tax Number: SIR / MADAM We hereby wish to confirm our appointment by you, as tax consultants and financial advisors. The terms and conditions of

APPOINTMENT AS TAX CONSULTANTS TO: Name: Identity Number: Tax Number: SIR / MADAM We hereby wish to confirm our appointment by you, as tax consultants and financial advisors. The terms and conditions of

DEBT RECOVERY SEPTEMBER 2006 BRIAN O BRIEN SOLICITORS

DEBT RECOVERY 129 Capel Building Mary s Abbey Dublin 7 Tel: 01 8788 649 Fax: 01 8788 650 E-mail: boblaw@brianobrien.ie DEBT RECOVERY The legal system for recovery of debts is poorly used. Often companies

DEBT RECOVERY 129 Capel Building Mary s Abbey Dublin 7 Tel: 01 8788 649 Fax: 01 8788 650 E-mail: boblaw@brianobrien.ie DEBT RECOVERY The legal system for recovery of debts is poorly used. Often companies

Non-Filing of Returns - Prosecution and Penalty Programmes. Collection Manual. Collector-General s Division

Collection Manual Collector-General s Division This document was last updated July 2017 1 CONTENTS Introduction...3 Part 1 Collector-General s Prosecution Programme...4 1. VAT - Criminal Prosecution Programme...4

Collection Manual Collector-General s Division This document was last updated July 2017 1 CONTENTS Introduction...3 Part 1 Collector-General s Prosecution Programme...4 1. VAT - Criminal Prosecution Programme...4

Universal Social Charge. Frequently Asked Questions

Universal Social Charge Frequently Asked Questions 15 March 2011 These FAQs have been updated on 15 March 2011. The changes from the previous version (published on 7 February 2011) are listed hereunder:

Universal Social Charge Frequently Asked Questions 15 March 2011 These FAQs have been updated on 15 March 2011. The changes from the previous version (published on 7 February 2011) are listed hereunder:

Special Terms and Conditions for Business Customer Agreement & Special Terms and Conditions for Business Current Account

February 2014 Page 1 of 6 Special Terms and Conditions for Business Customer Agreement & Special Terms and Conditions for Business Current Account (Please note that these Special Terms and Conditions apply

February 2014 Page 1 of 6 Special Terms and Conditions for Business Customer Agreement & Special Terms and Conditions for Business Current Account (Please note that these Special Terms and Conditions apply

BARD.ANZGBC ANZ GENERAL BANKING CONDITIONS

BARD.ANZGBC.00113 ANZ GENERAL BANKING CONDITIONS INTRODUCTION These ANZ General Banking Conditions set out the terms on which the Bank provides its Customer with one or more Accounts and Services and must

BARD.ANZGBC.00113 ANZ GENERAL BANKING CONDITIONS INTRODUCTION These ANZ General Banking Conditions set out the terms on which the Bank provides its Customer with one or more Accounts and Services and must

DEPOSIT PROTECTION CORPORATION ACT

CHAPTER 24:29 DEPOSIT PROTECTION CORPORATION ACT ARRANGEMENT OF SECTIONS Acts 7/2011, 9/2011 PART I PRELIMINARY Section 1. Short title. 2. Interpretation. 3. When contributory institution becomes financially

CHAPTER 24:29 DEPOSIT PROTECTION CORPORATION ACT ARRANGEMENT OF SECTIONS Acts 7/2011, 9/2011 PART I PRELIMINARY Section 1. Short title. 2. Interpretation. 3. When contributory institution becomes financially

Invoice Finance. General Conditions

Invoice Finance General Conditions 1 Contents CONDITIONS APPLICABLE TO ALL FACILITIES... 4 1. Period of the Agreement... 4 2. Sale and purchase of Debts... 4 3. Trusts... 4 4. Schedules... 4 5. Approval

Invoice Finance General Conditions 1 Contents CONDITIONS APPLICABLE TO ALL FACILITIES... 4 1. Period of the Agreement... 4 2. Sale and purchase of Debts... 4 3. Trusts... 4 4. Schedules... 4 5. Approval

Private Client Conditions of Use

Private Client Conditions of Use Contents General Conditions 2 Section A: Conditions of General Application and current accounts (a payment account) 2 Your information 2 Opening an account 4 Giving us

Private Client Conditions of Use Contents General Conditions 2 Section A: Conditions of General Application and current accounts (a payment account) 2 Your information 2 Opening an account 4 Giving us

Hackett & Dabbs LLP OUR STANDARD TERMS AND CONDITIONS

Hackett & Dabbs LLP OUR STANDARD TERMS AND CONDITIONS 1 Interpretation 1.1 These are the Terms and Conditions which apply to legal professional services supplied by Hackett & Dabbs LLP of 7 Stratfield

Hackett & Dabbs LLP OUR STANDARD TERMS AND CONDITIONS 1 Interpretation 1.1 These are the Terms and Conditions which apply to legal professional services supplied by Hackett & Dabbs LLP of 7 Stratfield

Circular 13/2009: Special Incentive Career Break Scheme 2009

Mr Tom Boland Secretary/Chief Executive Higher Education Authority Brooklawn House Crampton Avenue Shelbourne Road Dublin 4 26 June 2009 Circular 13/2009: Special Incentive Career Break Scheme 2009 1.

Mr Tom Boland Secretary/Chief Executive Higher Education Authority Brooklawn House Crampton Avenue Shelbourne Road Dublin 4 26 June 2009 Circular 13/2009: Special Incentive Career Break Scheme 2009 1.

U M B B A N K, N. A. H E A L T H S A V I N G S A C C O U N T C U S T O D I A L A G R E E M E N T ( R E T A I N F O R Y O U R R E C O R D S

UMB BANK, N.A. HEALTH SAVINGS ACCOUNT CUSTODIAL AGREEMENT (RETAIN FOR YOUR RECORDS) This agreement is made between UMB Bank, n.a. (referred to herein as we, us or the Custodian ) and the individual person

UMB BANK, N.A. HEALTH SAVINGS ACCOUNT CUSTODIAL AGREEMENT (RETAIN FOR YOUR RECORDS) This agreement is made between UMB Bank, n.a. (referred to herein as we, us or the Custodian ) and the individual person

Limerick City & County Council. House Purchase Loan. Application Form

Limerick City & County Council House Purchase Loan Application Form Limerick City & County Council Community Support Services City Hall Merchant s Quay Limerick. Tel 061 557203 2 GUIDANCE DOCUMENT PLEASE

Limerick City & County Council House Purchase Loan Application Form Limerick City & County Council Community Support Services City Hall Merchant s Quay Limerick. Tel 061 557203 2 GUIDANCE DOCUMENT PLEASE

Failure to cooperate fully with a Revenue Compliance Intervention. Document last updated January 2019

Failure to cooperate fully with a Revenue Compliance Intervention Document last updated January 2019 1 Table of Contents 1. Self-Assessment...3 2. Failure to cooperate fully with a Revenue compliance intervention...3

Failure to cooperate fully with a Revenue Compliance Intervention Document last updated January 2019 1 Table of Contents 1. Self-Assessment...3 2. Failure to cooperate fully with a Revenue compliance intervention...3

Country-By-Country Reporting. Some Frequently Asked Questions (FAQs)

") Country-By-Country Reporting Some Frequently Asked Questions (FAQs) These Frequently Asked Questions (FAQs) are designed to provide information in relation to the introduction of Country-by-Country Reporting

Country-By-Country Reporting Some Frequently Asked Questions (FAQs) These Frequently Asked Questions (FAQs) are designed to provide information in relation to the introduction of Country-by-Country Reporting

Home Loan Facility Agreement.

Home Loan Facility Agreement. Terms and Conditions Issued by Citigroup Pty Limited ABN 88 004 325 080 AFSL No. 238098 Australian credit licence 238098 Important notice This document contains important

Home Loan Facility Agreement. Terms and Conditions Issued by Citigroup Pty Limited ABN 88 004 325 080 AFSL No. 238098 Australian credit licence 238098 Important notice This document contains important

MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS (AMENDMENT) ACT 2017 ARRANGEMENT OF SECTIONS

ACT 2017 ARRANGEMENT OF SECTIONS") BELIZE: MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS (AMENDMENT) ACT 2017 ARRANGEMENT OF SECTIONS 1. Short title. 2. Insertion of new heading. 3. Amendment of section 2. 4. Insertion of new section

BELIZE: MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS (AMENDMENT) ACT 2017 ARRANGEMENT OF SECTIONS 1. Short title. 2. Insertion of new heading. 3. Amendment of section 2. 4. Insertion of new section

Fees and charges summary 4. Before you start 8. Early collection 9. Prospects of Recovery Check 10. Your right to interest explained 10

2 Roythornes Debt Recovery Service Contents Fees and charges summary 4 Before you start 8 Early collection 9 Prospects of Recovery Check 10 Your right to interest explained 10 Pre-Action Stage 11 Legal

2 Roythornes Debt Recovery Service Contents Fees and charges summary 4 Before you start 8 Early collection 9 Prospects of Recovery Check 10 Your right to interest explained 10 Pre-Action Stage 11 Legal

REPUBLIC OF SOUTH AFRICA

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

[1997.] Taxes Consolidation Act, [No. 39.]

![[1997.] Taxes Consolidation Act, [No. 39.]](/thumbs/76/73340162.jpg "[1997.] Taxes Consolidation Act, [No. 39.]") [1997.] Taxes Consolidation Act, 1997. [No. 39.] until the contrary is proved to have been signed by such inspector. CHAPTER 3 Capital gains tax penalties 1077. (1) Without prejudice to the generality

[1997.] Taxes Consolidation Act, 1997. [No. 39.] until the contrary is proved to have been signed by such inspector. CHAPTER 3 Capital gains tax penalties 1077. (1) Without prejudice to the generality

ANZ ASSURED & PERSONAL OVERDRAFT

ANZ ASSURED & PERSONAL OVERDRAFT TERMS AND CONDITIONS 12.2017 Introduction If you are thinking about obtaining a personal credit facility from ANZ or have any questions about your existing facility, simply

ANZ ASSURED & PERSONAL OVERDRAFT TERMS AND CONDITIONS 12.2017 Introduction If you are thinking about obtaining a personal credit facility from ANZ or have any questions about your existing facility, simply

JUNE 2013 DSA. Debt Solutions DSA Scenario. Preferential and Excludable Debts

JUNE 2013 DSA Debt Solutions DSA Scenario Preferential and Excludable Debts TO HELP EXPLAIN SOME OF THE CONCEPTS CONTAINED IN THE PERSONAL INSOLVENCY LEGISLATION, THE INSOLVENCY SERVICE OF IRELAND HAS

JUNE 2013 DSA Debt Solutions DSA Scenario Preferential and Excludable Debts TO HELP EXPLAIN SOME OF THE CONCEPTS CONTAINED IN THE PERSONAL INSOLVENCY LEGISLATION, THE INSOLVENCY SERVICE OF IRELAND HAS

Introduction to Payroll

Introduction to Payroll The following is a brief introduction to payroll including how to register the business and employees, how best to operate a payroll system and details of what Revenue returns are

Introduction to Payroll The following is a brief introduction to payroll including how to register the business and employees, how best to operate a payroll system and details of what Revenue returns are

Points Of Discussion

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Business Charge Card Terms and Conditions

Business Charge Card Terms and Conditions November 2017 CONTENTS 1. Use of Your Business Charge Card 3 2. Making and Stopping Payments 4 3. Payments and Statements 4 4. Refunds 6 5. Charges 6 6. Lost and

Business Charge Card Terms and Conditions November 2017 CONTENTS 1. Use of Your Business Charge Card 3 2. Making and Stopping Payments 4 3. Payments and Statements 4 4. Refunds 6 5. Charges 6 6. Lost and

COMMUNITY FINANCIAL CREDIT UNION MasterCard CARD HOLDER AGREEMENT

COMMUNITY FINANCIAL CREDIT UNION MasterCard CARD HOLDER AGREEMENT THIS IS YOUR AGREEMENT WITH COMMUNITY FINANCIAL CREDIT UNION (COMMUNITY FINANCIAL) REGARDING RIGHTS AND RESPONSIBILITIES ASSOCIATED WITH

COMMUNITY FINANCIAL CREDIT UNION MasterCard CARD HOLDER AGREEMENT THIS IS YOUR AGREEMENT WITH COMMUNITY FINANCIAL CREDIT UNION (COMMUNITY FINANCIAL) REGARDING RIGHTS AND RESPONSIBILITIES ASSOCIATED WITH

Offset Savings Account.

Offset Savings Account. Terms and Conditions Issued by Citigroup Pty Limited ABN 88 004 325 080 AFSL No. 238098 Australian credit licence 238098 This document: Does not form part of your Citibank Home

Offset Savings Account. Terms and Conditions Issued by Citigroup Pty Limited ABN 88 004 325 080 AFSL No. 238098 Australian credit licence 238098 This document: Does not form part of your Citibank Home

Academic Year 2009/ Taxation. Republic of Ireland

Academic Year 2009/2010 www.accountingtechniciansireland.ie Taxation Republic of Ireland PART A CHAPTER 1: THE TAXATION SYSTEM Taxation is a major economic tool and the operation of an efficient tax system

Academic Year 2009/2010 www.accountingtechniciansireland.ie Taxation Republic of Ireland PART A CHAPTER 1: THE TAXATION SYSTEM Taxation is a major economic tool and the operation of an efficient tax system

VAT and Employers PAYE DIRECT DEBIT GUIDELINES

VAT and Employers PAYE DIRECT DEBIT GUIDELINES Created June 2017 1 CONTENTS 1. Scope...3 2. Purpose...3 3. Introduction...3 4. SEPA Monthly Direct Debit Scheme...4 5. Summary...4 6. Process Using Direct

VAT and Employers PAYE DIRECT DEBIT GUIDELINES Created June 2017 1 CONTENTS 1. Scope...3 2. Purpose...3 3. Introduction...3 4. SEPA Monthly Direct Debit Scheme...4 5. Summary...4 6. Process Using Direct

Please read the Pre-Agreement Statement below. You ll need to refer to it if your loan is approved.

Pre-Agreement Statement Please read the Pre-Agreement Statement below. You ll need to refer to it if your loan is approved. Babereki Personal Loan Pre Agreement Statement in terms of Section 92 of the

Pre-Agreement Statement Please read the Pre-Agreement Statement below. You ll need to refer to it if your loan is approved. Babereki Personal Loan Pre Agreement Statement in terms of Section 92 of the

Term Deposit. Terms and Conditions, Fees and Charges and General Information. Effective Date: 12 November

Term Deposit Terms and Conditions, Fees and Charges and General Information Effective Date: 12 November 2016 1 Terms and Conditions This booklet sets out the terms and conditions for Bank of Melbourne

Term Deposit Terms and Conditions, Fees and Charges and General Information Effective Date: 12 November 2016 1 Terms and Conditions This booklet sets out the terms and conditions for Bank of Melbourne

Health Savings Account (HSA) Enrollment Form

Enrollment Form") Health Savings Account (HSA) Enrollment Form A. Individual Health Savings Account (HSA) Owner Information. Note: We comply with Section 326 of the USA Patriot Act, which requires us to collect and verify

Health Savings Account (HSA) Enrollment Form A. Individual Health Savings Account (HSA) Owner Information. Note: We comply with Section 326 of the USA Patriot Act, which requires us to collect and verify

Cape Town Johannesburg Durban

APPOINTMENT AS ACCOUNTANTS TO: SIR / MADAM We hereby wish to confirm our appointment as accountants and financial advisors to the above business and its owners / members / directors. The terms and conditions

APPOINTMENT AS ACCOUNTANTS TO: SIR / MADAM We hereby wish to confirm our appointment as accountants and financial advisors to the above business and its owners / members / directors. The terms and conditions

Debt Recovery. A Guide to the Debt Recovery Process

Debt Recovery A Guide to the Debt Recovery Process How does Debt Recovery work? STAGE 1 Letter before action No response from Debtor/Discontinuance STAGE 2 Issue Claim Form No response from Debtor Request

Debt Recovery A Guide to the Debt Recovery Process How does Debt Recovery work? STAGE 1 Letter before action No response from Debtor/Discontinuance STAGE 2 Issue Claim Form No response from Debtor Request

Important Account Information for Our Members

TERMS AND CONDITIONS OF YOUR ACCOUNT Dear Credit Union Member: Important Account Information for Our Members This document contains the rules which govern your account(s) with us. Please read this document

TERMS AND CONDITIONS OF YOUR ACCOUNT Dear Credit Union Member: Important Account Information for Our Members This document contains the rules which govern your account(s) with us. Please read this document

Corporate & Commercial Banking Overdraft Facility Terms and Conditions

60 20 291 v4 08.2010 Corporate & Commercial Banking Overdraft Facility Terms and Conditions August 2010 Edition 60 20 291 v4 08.2010 Page 1 of 6 60 20 291 v4 08.2010 Page 2 of 6 1 Tax gross up and indemnities

60 20 291 v4 08.2010 Corporate & Commercial Banking Overdraft Facility Terms and Conditions August 2010 Edition 60 20 291 v4 08.2010 Page 1 of 6 60 20 291 v4 08.2010 Page 2 of 6 1 Tax gross up and indemnities

SOCIAL WELFARE CONSOLIDATION ACT 2005

SOCIAL WELFARE CONSOLIDATION ACT 2005 EXPLANATORY GUIDE Our mission is to promote a caring society through ensuring access to income support and other services, enabling active participation, promoting

SOCIAL WELFARE CONSOLIDATION ACT 2005 EXPLANATORY GUIDE Our mission is to promote a caring society through ensuring access to income support and other services, enabling active participation, promoting

UMB BANK, N.A. HEALTH SAVINGS ACCOUNT CUSTODIAL AGREEMENT (RETAIN FOR YOUR RECORDS)

") Page 1 of 9 UMB BANK, N.A. HEALTH SAVINGS ACCOUNT CUSTODIAL AGREEMENT (RETAIN FOR YOUR RECORDS) This agreement is made between UMB Bank, n.a. (referred to herein as we, us or the Custodian ) and the individual

Page 1 of 9 UMB BANK, N.A. HEALTH SAVINGS ACCOUNT CUSTODIAL AGREEMENT (RETAIN FOR YOUR RECORDS) This agreement is made between UMB Bank, n.a. (referred to herein as we, us or the Custodian ) and the individual

Procedural Guidelines for Alcohol Product Seizure

Procedural Guidelines for Alcohol Product Seizure This document should be read in conjunction with section 125A of the Finance Act 2001 and section 1094 of the Taxes Consolidation Act 1997 Document reviewed

Procedural Guidelines for Alcohol Product Seizure This document should be read in conjunction with section 125A of the Finance Act 2001 and section 1094 of the Taxes Consolidation Act 1997 Document reviewed

RESIDENTIAL TENANCY (DEPOSIT SCHEME) (JERSEY) REGULATIONS 2014

(JERSEY) REGULATIONS 2014") RESIDENTIAL TENANCY (DEPOSIT SCHEME) (JERSEY) REGULATIONS 2014 Revised Edition Showing the law as at 1 January 2016 This is a revised edition of the law Residential Tenancy (Deposit Scheme) (Jersey) Arrangement

RESIDENTIAL TENANCY (DEPOSIT SCHEME) (JERSEY) REGULATIONS 2014 Revised Edition Showing the law as at 1 January 2016 This is a revised edition of the law Residential Tenancy (Deposit Scheme) (Jersey) Arrangement

Airbnb. General guidance on the taxation of rental income, including Frequently Asked Questions

Airbnb General guidance on the taxation of rental income, including Frequently Asked Questions These guidance notes are provided by EY solely for the use of Airbnb and may not be relied upon or used by

Airbnb General guidance on the taxation of rental income, including Frequently Asked Questions These guidance notes are provided by EY solely for the use of Airbnb and may not be relied upon or used by

ARTICLE I ARTICLE II ARTICLE III ARTICLE IV

SIMPLE Individual Retirement Custodial Account (Under section 408A of the Internal Revenue Code) Form 5305-SA (Rev. March 2002) Department of the Treasury, Internal Revenue Service. Do not file with the

SIMPLE Individual Retirement Custodial Account (Under section 408A of the Internal Revenue Code) Form 5305-SA (Rev. March 2002) Department of the Treasury, Internal Revenue Service. Do not file with the

Macquarie Vision Macquarie Super and Pension Further Information Guide

Macquarie Vision Macquarie Super and Pension Further Information Guide Document number MAQVSP01.0 The information contained in this Further Information Guide (FIG) is incorporated by reference into the

Macquarie Vision Macquarie Super and Pension Further Information Guide Document number MAQVSP01.0 The information contained in this Further Information Guide (FIG) is incorporated by reference into the

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

The above addresses are the addresses to which Notices, Letters of Advice and disclosure documents will be sent.

Southland Building Society 51 Don Street Invercargill SBS ADVANCE LOAN AGREEMENT (and including key information that is required to be set out in an Initial Disclosure document under Section 17 of the

Southland Building Society 51 Don Street Invercargill SBS ADVANCE LOAN AGREEMENT (and including key information that is required to be set out in an Initial Disclosure document under Section 17 of the

PRELIMINARY INCOME TAX DIRECT DEBIT GUIDELINES

PRELIMINARY INCOME TAX DIRECT DEBIT GUIDELINES This document was last updated June 2017 Contents 1. Scope...3 2. Purpose...3 3. Introduction...3 4. SEPA Monthly Direct Debit Scheme...4 5. Summary...5 6.

PRELIMINARY INCOME TAX DIRECT DEBIT GUIDELINES This document was last updated June 2017 Contents 1. Scope...3 2. Purpose...3 3. Introduction...3 4. SEPA Monthly Direct Debit Scheme...4 5. Summary...5 6.

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

Asian Infrastructure Investment Bank. General Conditions for Sovereign-backed Loans

Asian Infrastructure Investment Bank General Conditions for Sovereign-backed Loans May 1, 2016 Table of Contents ARTICLE I Introductory Provisions Section 1.01. Application of General Conditions Section

Asian Infrastructure Investment Bank General Conditions for Sovereign-backed Loans May 1, 2016 Table of Contents ARTICLE I Introductory Provisions Section 1.01. Application of General Conditions Section

Revenue Information Powers Introduction

Revenue Information Powers Introduction Guidance Notes and Instructions on the use of the information powers contained in 900-902A, s 906A to 908 and 909 Taxes Consolidation Act 1997. This document should

Revenue Information Powers Introduction Guidance Notes and Instructions on the use of the information powers contained in 900-902A, s 906A to 908 and 909 Taxes Consolidation Act 1997. This document should

SAMPLE. 1.1 Drawing your Loan Unless otherwise agreed by Westpac NZ you can draw your Loan in one lump sum or in instalments.

Choices Everyday Home Loan Terms And Conditions, having its principal place of business at 16 Takutai Square, Auckland (Westpac NZ) may offer to provide Choices Everyday Home Loans (each a Loan) to you

Choices Everyday Home Loan Terms And Conditions, having its principal place of business at 16 Takutai Square, Auckland (Westpac NZ) may offer to provide Choices Everyday Home Loans (each a Loan) to you

Potential Construction Defect Claim Site: 100 Eton Road, Lindfield "Dunstan Grove"

3 April 2017 Partner: David Andrews Direct Line: 9233 9023 Direct Facsimile: 9233 9123 Email: dandrews@makdap.com.au Our Ref: DA: BEL: 170658 BY EMAIL: raymond.reg@stratplus.com.au The Secretary The Owners

3 April 2017 Partner: David Andrews Direct Line: 9233 9023 Direct Facsimile: 9233 9123 Email: dandrews@makdap.com.au Our Ref: DA: BEL: 170658 BY EMAIL: raymond.reg@stratplus.com.au The Secretary The Owners

Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay.

Fixed Fee Account Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay. Choose the account plan that best suits your

Fixed Fee Account Paying for your business banking needn t be complicated. That s why our Fixed Fee Account gives you greater control over the charges you pay. Choose the account plan that best suits your

HSA TOOLS ENROLLMENT FORM for your Health Savings Account with UMB Bank, n.a.

HSA TOOLS ENROLLMENT FORM for your Health Savings Account with UMB Bank, n.a. Instructions: Please complete this page and submit along with the insurance application to the Underwriting Department. If

HSA TOOLS ENROLLMENT FORM for your Health Savings Account with UMB Bank, n.a. Instructions: Please complete this page and submit along with the insurance application to the Underwriting Department. If

Starting in Business MCHUGH & CO. ACCOUNTANTS & TAX ADVISORS JOANNE MCHUGH BBS ACA AITI. Ardnageehy East, Watergrasshill, Co. Cork

Starting in Business MCHUGH & CO. ACCOUNTANTS & TAX ADVISORS JOANNE MCHUGH BBS ACA AITI Ardnageehy East, Watergrasshill, Co. Cork Tel: 021-4513663 Mobile: 087-8571500 Email: joanne@mchughacc.ie Web: www.mchughacc.ie

Starting in Business MCHUGH & CO. ACCOUNTANTS & TAX ADVISORS JOANNE MCHUGH BBS ACA AITI Ardnageehy East, Watergrasshill, Co. Cork Tel: 021-4513663 Mobile: 087-8571500 Email: joanne@mchughacc.ie Web: www.mchughacc.ie

ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE

ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE This Electronic Funds Transfer Agreement is the contract which covers your and our rights and responsibilities concerning the electronic funds transfer

ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE This Electronic Funds Transfer Agreement is the contract which covers your and our rights and responsibilities concerning the electronic funds transfer

CORNERSTONE COMMUNITY FINANCIAL CREDIT UNION MEMBERSHIP AND ACCOUNT AGREEMENT

CORNERSTONE COMMUNITY FINANCIAL CREDIT UNION MEMBERSHIP AND ACCOUNT AGREEMENT This is the Agreement ( Agreement ) between you (the member) and CORNERSTONE COMMUNITY FINANCIAL CREDIT UNION ( Credit Union

CORNERSTONE COMMUNITY FINANCIAL CREDIT UNION MEMBERSHIP AND ACCOUNT AGREEMENT This is the Agreement ( Agreement ) between you (the member) and CORNERSTONE COMMUNITY FINANCIAL CREDIT UNION ( Credit Union

STANDARD CONDITIONS FOR COMPANY VOLUNTARY ARRANGEMENTS

STANDARD CONDITIONS FOR COMPANY VOLUNTARY ARRANGEMENTS Version 3 January 2013 TABLE OF CONTENTS 1 COMPANY VOLUNTARY ARRANGEMENTS 1 PART I: INTERPRETATION 5 1 Miscellaneous definitions 5 2 The Conditions

STANDARD CONDITIONS FOR COMPANY VOLUNTARY ARRANGEMENTS Version 3 January 2013 TABLE OF CONTENTS 1 COMPANY VOLUNTARY ARRANGEMENTS 1 PART I: INTERPRETATION 5 1 Miscellaneous definitions 5 2 The Conditions

Mandate for Banking Services. with permanent tsb. Unincorporated Club, Society or Charity. (the 'Association')

") Mandate for Banking Services with permanent tsb Unincorporated Club, Society or Charity (the 'Association') Introduction This Mandate authorises permanent tsb to open accounts and provide services to the

Mandate for Banking Services with permanent tsb Unincorporated Club, Society or Charity (the 'Association') Introduction This Mandate authorises permanent tsb to open accounts and provide services to the

Finance Terms and Conditions

Finance Terms and Conditions Welcome to Oxford Finance We know you re unique. That s why we have real people assessing real finance needs. Contact Us For any enquiries on your loan, or to update your details,

Finance Terms and Conditions Welcome to Oxford Finance We know you re unique. That s why we have real people assessing real finance needs. Contact Us For any enquiries on your loan, or to update your details,

BUSINESS REWARDS CREDIT CARD AGREEMENT (TO BE USED FOR CORPORATIONS, PARTNERSHIPS, LLCs, SERVICE ORGANIZATIONS OR OTHER BUSINESSES)

") BUSINESS REWARDS CREDIT CARD AGREEMENT (TO BE USED FOR CORPORATIONS, PARTNERSHIPS, LLCs, SERVICE ORGANIZATIONS OR OTHER BUSINESSES) This AGREEMENT made and entered into this day of, 20, by and between

BUSINESS REWARDS CREDIT CARD AGREEMENT (TO BE USED FOR CORPORATIONS, PARTNERSHIPS, LLCs, SERVICE ORGANIZATIONS OR OTHER BUSINESSES) This AGREEMENT made and entered into this day of, 20, by and between

STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS. Produced by the IVA FORUM

Protocol Annex 4 STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the IVA FORUM Revised January 25 th 2008 TABLE OF CONTENTS FOR STANDARD CONDITIONS PART I: INTERPRETATION Page 1 Definitions

Protocol Annex 4 STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the IVA FORUM Revised January 25 th 2008 TABLE OF CONTENTS FOR STANDARD CONDITIONS PART I: INTERPRETATION Page 1 Definitions

BP p.l.c. Individual Savings Account (ISA) 1 July 2018

1 July 2018") BP p.l.c. Individual Savings Account (ISA) 1 July 2018 2 Contents page About this brochure 2 How to contact us 2 ISAs explained 3 Taxation 3 Risks associated with this investment 4 Eligibility for new

BP p.l.c. Individual Savings Account (ISA) 1 July 2018 2 Contents page About this brochure 2 How to contact us 2 ISAs explained 3 Taxation 3 Risks associated with this investment 4 Eligibility for new

BP p.l.c. Individual Savings Account (ISA)

") BP p.l.c. Individual Savings Account (ISA) January 2018 2 Contents page How to contact us About this brochure 2 How to contact us 2 ISAs explained 3 Taxation 3 Risks associated with this investment 4 Eligibility

BP p.l.c. Individual Savings Account (ISA) January 2018 2 Contents page How to contact us About this brochure 2 How to contact us 2 ISAs explained 3 Taxation 3 Risks associated with this investment 4 Eligibility

BP p.l.c. Individual Savings Account (ISA) 1 July 2018

1 July 2018") BP p.l.c. Individual Savings Account (ISA) 1 July 2018 2 Contents page About this brochure 2 How to contact us 2 ISAs explained 3 Taxation 3 Risks associated with this investment 4 Eligibility for new

BP p.l.c. Individual Savings Account (ISA) 1 July 2018 2 Contents page About this brochure 2 How to contact us 2 ISAs explained 3 Taxation 3 Risks associated with this investment 4 Eligibility for new

G A U D A L R IN A E G NTE O E E F S H ACI E L R ITE

CASH COVER INDEMNITY HEADLINE GUARANTEE GOES FACILITY HERE ADDITIONAL DESCRIPTION DATE TERMS AND CONDITIONS 09.2017 CONTENTS 1. Indemnity Guarantee Facility 2 1.1 Application of these Terms and Conditions.

CASH COVER INDEMNITY HEADLINE GUARANTEE GOES FACILITY HERE ADDITIONAL DESCRIPTION DATE TERMS AND CONDITIONS 09.2017 CONTENTS 1. Indemnity Guarantee Facility 2 1.1 Application of these Terms and Conditions.

ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE

ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE This Electronic Funds Transfer Agreement is the contract which covers your and our rights and responsibilities concerning the electronic funds transfer

ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE This Electronic Funds Transfer Agreement is the contract which covers your and our rights and responsibilities concerning the electronic funds transfer

BLUESTONE GENERAL TERMS AND CONDITIONS

BLUESTONE GENERAL TERMS AND CONDITIONS NEW ZEALAND VERSION 9 [OCTOBER 2017] Bluestone Servicing NZ Limited trading as Bluestone Mortgages is the manager of loans incorporating these terms and conditions.

BLUESTONE GENERAL TERMS AND CONDITIONS NEW ZEALAND VERSION 9 [OCTOBER 2017] Bluestone Servicing NZ Limited trading as Bluestone Mortgages is the manager of loans incorporating these terms and conditions.

APPLICATION FOR COMMERCIAL CREDIT

APPLICATION FOR COMMERCIAL CREDIT Lofts Quarries Pty Ltd Please return your completed Credit Application to: (ABN 19 005 671 465) Suite 7, 20 Cato Street, Hawthorn East Vic 3123 Date of application: APPLICANT

APPLICATION FOR COMMERCIAL CREDIT Lofts Quarries Pty Ltd Please return your completed Credit Application to: (ABN 19 005 671 465) Suite 7, 20 Cato Street, Hawthorn East Vic 3123 Date of application: APPLICANT

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

Jersey Disclosure Facility: Frequently Asked Questions (FAQs)

") Jersey Disclosure Facility: Frequently Asked Questions (FAQs) FAQs The following is intended to provide answers to commonly asked questions about the Jersey Disclosure Facility (JDF). The answers given

Jersey Disclosure Facility: Frequently Asked Questions (FAQs) FAQs The following is intended to provide answers to commonly asked questions about the Jersey Disclosure Facility (JDF). The answers given

PO Box 179 Greenbelt, MD esfcu.org

PO Box 179 Greenbelt, MD 20768-0179 301.779.8500 esfcu.org Electronic Fund Transfers Agreement and Disclosure This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and

PO Box 179 Greenbelt, MD 20768-0179 301.779.8500 esfcu.org Electronic Fund Transfers Agreement and Disclosure This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ACCOUNT AGREEMENT & DISCLOSURES. Effective September 30, 2017

ACCOUNT AGREEMENT & DISCLOSURES Effective September 30, 2017 TABLE OF CONTENTS Introduction...1 General Information About All Of Our Accounts...1 Money Market Account...2 Additional Share ( savings ) Accounts...3

ACCOUNT AGREEMENT & DISCLOSURES Effective September 30, 2017 TABLE OF CONTENTS Introduction...1 General Information About All Of Our Accounts...1 Money Market Account...2 Additional Share ( savings ) Accounts...3

BP p.l.c. Individual Savings Account

BP p.l.c. Individual Savings Account April 2016 2 Contents page How to contact us About this brochure 2 How to contact us 2 ISAs explained 3 Taxation 3 Risks associated with this investment 4 Eligibility

BP p.l.c. Individual Savings Account April 2016 2 Contents page How to contact us About this brochure 2 How to contact us 2 ISAs explained 3 Taxation 3 Risks associated with this investment 4 Eligibility

Help to Buy Buyers Guide

Help to Buy Buyers Guide Homes England http://www.homesengland.gov.uk/helptobuy Page 1 of 29 Contents Key information... 3 What is Help to Buy?... 4 Help to Buy overview... 5 How does it work?... 6 Who

Help to Buy Buyers Guide Homes England http://www.homesengland.gov.uk/helptobuy Page 1 of 29 Contents Key information... 3 What is Help to Buy?... 4 Help to Buy overview... 5 How does it work?... 6 Who

Liquidation of Companies and other Company Law Issues. Collection Manual. This document was last reviewed December 2017

Collection Manual Liquidation of Companies and other Company Law issues This document was last reviewed December 2017 1 Table of Contents 1. Introduction...3 2. What is Liquidation?...3 4. Procedure for

Collection Manual Liquidation of Companies and other Company Law issues This document was last reviewed December 2017 1 Table of Contents 1. Introduction...3 2. What is Liquidation?...3 4. Procedure for

GENERAL TERMS AND CONDITIONS FOR CONSUMER LENDING TO PRIVATE CLIENTS OF PROCREDIT BANK (BULGARIA) EAD

EAD") GENERAL TERMS AND CONDITIONS FOR CONSUMER LENDING TO PRIVATE CLIENTS OF PROCREDIT BANK (BULGARIA) EAD I. GRANTING THE LOAN: CHANGES IN THE CONTRACTUAL RELATIONSHIP 1. The loan shall be granted after the

GENERAL TERMS AND CONDITIONS FOR CONSUMER LENDING TO PRIVATE CLIENTS OF PROCREDIT BANK (BULGARIA) EAD I. GRANTING THE LOAN: CHANGES IN THE CONTRACTUAL RELATIONSHIP 1. The loan shall be granted after the

SCOTLAND INSOLVENCY PRACTITIONERS ASSOCIATION CERTIFICATE OF PROFICIENCY IN INSOLVENCY. Examination Friday 4 June 2004 pm

SCOTLAND INSOLVENCY PRACTITIONERS ASSOCIATION CERTIFICATE OF PROFICIENCY IN INSOLVENCY Examination Friday 4 June 2004 pm INSOLVENCY (3 HOURS) Part A: Part B: Part C: All questions to be answered All questions

SCOTLAND INSOLVENCY PRACTITIONERS ASSOCIATION CERTIFICATE OF PROFICIENCY IN INSOLVENCY Examination Friday 4 June 2004 pm INSOLVENCY (3 HOURS) Part A: Part B: Part C: All questions to be answered All questions

User Manual. Jobs and Pensions Service

User Manual Jobs and Pensions Service December 2016 1 Table of Contents 1. Background...4 2. Accessing Jobs and Pensions service...4 2.1 Agents...4 3. Who is the Jobs and Pensions service for?...4 4. Information

User Manual Jobs and Pensions Service December 2016 1 Table of Contents 1. Background...4 2. Accessing Jobs and Pensions service...4 2.1 Agents...4 3. Who is the Jobs and Pensions service for?...4 4. Information

Form 1(Firms) Partnership Tax Return 2016

Partnership Tax Return 2016") 2016155 Form 1(Firms) Partnership Tax Return 2016 TAIN GCD Tax Reference Number Remember to quote this number in all correspondence or when calling at your Revenue office This Tax Return is for use by

2016155 Form 1(Firms) Partnership Tax Return 2016 TAIN GCD Tax Reference Number Remember to quote this number in all correspondence or when calling at your Revenue office This Tax Return is for use by

HSA CUSTODIAL AGREEMENT AND DISCLOSURES. Health Savings Custodial Agreement

HSA CUSTODIAL AGREEMENT AND DISCLOSURES Health Savings Custodial Agreement Health Savings Account Terms and Conditions Health Savings Account Disclosure Statement Health Savings Custodial Agreement Form

HSA CUSTODIAL AGREEMENT AND DISCLOSURES Health Savings Custodial Agreement Health Savings Account Terms and Conditions Health Savings Account Disclosure Statement Health Savings Custodial Agreement Form

Income Tax (Budget Amendment) Act 2004

Act 2004") Income Tax (Budget Amendment) Act 2004 FIJI ISLANDS INCOME TAX (BUDGET AMENDMENT) ACT 2004 ARRANGEMENT OF SECTIONS 1. Short title and commencement 2. Interpretation 3. Normal Tax 4. Non-resident miscellaneous

Income Tax (Budget Amendment) Act 2004 FIJI ISLANDS INCOME TAX (BUDGET AMENDMENT) ACT 2004 ARRANGEMENT OF SECTIONS 1. Short title and commencement 2. Interpretation 3. Normal Tax 4. Non-resident miscellaneous

INVESTOR PORTFOLIO SERVICE (IPS) THE INVESTOR PORTFOLIO SERVICE NON-ADVISED TERMS AND CONDITIONS.

THE INVESTOR PORTFOLIO SERVICE NON-ADVISED TERMS AND CONDITIONS.") INVESTOR PORTFOLIO SERVICE (IPS) THE INVESTOR PORTFOLIO SERVICE NON-ADVISED TERMS AND CONDITIONS. 2 THE INVESTOR PORTFOLIO SERVICE NON-ADVISED TERMS AND CONDITIONS THE INVESTOR PORTFOLIO SERVICE NON-ADVISED

INVESTOR PORTFOLIO SERVICE (IPS) THE INVESTOR PORTFOLIO SERVICE NON-ADVISED TERMS AND CONDITIONS. 2 THE INVESTOR PORTFOLIO SERVICE NON-ADVISED TERMS AND CONDITIONS THE INVESTOR PORTFOLIO SERVICE NON-ADVISED

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

ANZ COMMERCIAL CARD TERMS AND CONDITIONS

ANZ COMMERCIAL CARD TERMS AND CONDITIONS 20.07.2016 ANZ CORPORATE CARD ANZ VISA PURCHASING CARD ANZ BUSINESS ONE Containing Terms and Conditions for: Facility Terms and Conditions Electronic Banking Conditions

ANZ COMMERCIAL CARD TERMS AND CONDITIONS 20.07.2016 ANZ CORPORATE CARD ANZ VISA PURCHASING CARD ANZ BUSINESS ONE Containing Terms and Conditions for: Facility Terms and Conditions Electronic Banking Conditions

NAB EQUITY LENDING. Facility Terms

NAB EQUITY LENDING Facility Terms This document contains important information regarding the terms and conditions which will apply to your NAB Equity Lending Facility. You should read this document carefully

NAB EQUITY LENDING Facility Terms This document contains important information regarding the terms and conditions which will apply to your NAB Equity Lending Facility. You should read this document carefully