Points Of Discussion

|

|

|

- Thomasina Miles

- 5 years ago

- Views:

Transcription

1 Provisional Tax

2 Provisional Tax

3 Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional Taxpayers other than company Company Provisional Taxpayers Medical Scheme Fees Special Trust Taxable Income up to R1 Million Taxable Income above R1 Million Methods of Payment

4 Overview Provisional tax is not a separate tax. It is a method of paying tax due, to ensure the taxpayer does not pay large amounts on assessment, as the tax liability is spread over the relevant year of assessment. It requires the taxpayers to pay at least two amounts in advance, during the year of assessment, which are based on estimated taxable income. A third payment is optional after the end of the tax year, but before the issuing of the assessment Final liability, however, is worked out upon assessment and the payments will be off-set against the liability for normal tax for the applicable year of assessment.

5 Who is liable for Provisional Tax Any person (other than a company) who derives taxable income, other than remuneration, an allowance or advance Any company Any person who is notified by the Commissioner that he is a provisional taxpayer

6 Who is not liable for Provisional Tax PBOs approved by SARS Recreational clubs approved by SARS Any Body-Corporate, share block company or association of persons Any natural person who does not derive income from the carrying on of any business, if in that relevant year of assessment - taxable income does not exceed the tax threshold; or - the taxable income from interest, dividends, foreign dividends and rental from letting fixed property does not exceed R Non-resident owners or charterers of ships and aircraft who are required to make payments under s 33 Any small business funding entity Deceased estates

7 Exemption: Interest Income Local Dividends Investments in South African (local) companies Interest from investments Under 65 yrs R Over 65 yrs R34 500

8 Form Used To Capture Provisional Tax Calculations An IRP6 return must be completed for provisional tax purposes. The IRP6 return can be completed for all types of taxpayers: Individuals Trusts Companies

9 Estimates Of Taxable Income Provisional taxpayers must submit an estimate of the total taxable income which will be derived by the taxpayer in respect of the year of assessment for which the provisional tax is payable. Retirement fund lump sum benefits, Retirement fund lump sum withdrawal benefit or any severance benefit received by or accrued to the taxpayer are excluded

10 Estimates of taxable income and basic amount calculations Example 1: The notice of assessment for 2015 tax year of assessment was issued on 15 August 2015 The IRP6 for the 2016 tax year 1st period is 31 August 2015 The notice of assessment for the 2014 tax year of assessment was issued on 1 February 2015.

11 Estimates of taxable income and basic amount calculations Solution: The 2015 year of assessment was issued 15 days prior to submission of provisional tax estimate was submitted. Due to the 14 day criteria being met, the latest preceding year is the 2015 tax year. The estimate is not made more than 18 months after the end of the latest preceding year (2014). The estimate is not in respect of the period that ends more than 1 year after the end of the latest preceding year of assessment (2015). Therefore, the basic amount will not be increased by 8%.. The basic amount will be the amount of taxable income as assessed in 2015.

12 Estimates of taxable income and basic amount calculations Example 2 The notice of assessment was issued for the 2012 tax year was issued on 30 June 2012 The taxable income as assessed in 2012 was R and included a taxable gain of R and severance benefit of R The IRP6 for the 2016 tax year is 1st period is 28 February 2016 The 2013, 2014 and 2015 tax returns have not been submitted.

13 Estimates of taxable income and basic amount calculations Solution: The 2012 assessment was issued 14 days more than the date on which the provisional tax estimate was submitted on 28 February 2016, as 2013,2014 and 2015 tax returns not Submitted The estimate is more than 18 months after the end of the last preceding year (2012) The estimate is in respect of the period that ends more than 1 year after the end of the latest preceding year of assessment (2015) The basic amount is calculated as follows: Taxable income assessed in 2012 R Less: Taxable capital gain R Less: Severance benefit R R

14 First period When Must Provisional Tax Be Paid Second period Third period The following example refers to a 28 February 2017 year-end (2017 tax year): First provisional tax payment due on 31 Aug 2016 Second provisional tax payment due on 28 Feb 2017 Third or voluntary payment due on 30 Sept 2017 The following example refers to a 31 May 2016 year-end (2016 tax year): First provisional tax payment due on 30 Nov 2016 Second provisional tax payment due on 31 May 2017 Third or voluntary payment due on 30 Nov 2017

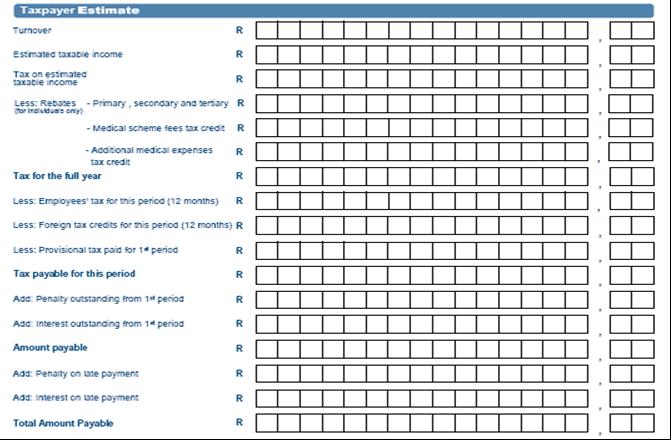

15 Provisional Taxpayers Other Than Companies The first period provisional tax payment is calculated as follows: Estimated taxable income for the year of assessment XXXX Normal tax on estimated taxable income XXXX Less: Primary, secondary and tertiary rebates under section 6 (XXXX) Less: Tax credit for medical scheme fees under section 6A (XXXX) Less: Additional medical expenses tax credit under section 6B (XXXX) Total Tax Payable (A) XXXX Half of the normal tax payable on estimated table income (A/2) XX Less: Employees tax deducted from the provisional taxpayer s remuneration during the first period (X) Less: Foreign tax credits under section 6quat proved to be payable by the end of the first period. (X) FIRST PROVISIONAL TAX PAYMENT xxxx

Less: Tax credit for medical scheme fees under section 6A (XXXX) Less: Additional medical expenses tax credit under")

16 First period for Persons Under 65 years The second period provisional tax payment is calculated as follows: Estimated taxable income for the year of assessment XXXX Normal tax on estimated taxable income XXXX Less: Primary, secondary and tertiary rebates under section 6 (XXXX) Less: Tax credit for medical scheme fees under section 6A (XXXX) Less: Additional medical expenses tax credit under section 6B (XXXX) Total Tax Payable XXXXX Less: Employees tax deducted from the provisional taxpayer s remuneration during the year (XXXX) Less: First provisional tax payment (if actually paid) (X) Less: Foreign tax credits (section 6quat and section 6quin*) for the year (X) SECOND PROVISIONAL TAX PAYMENT XXXX

17 PROVISIONAL TAXPAYERS OTHER THAN COMPANIES The second period provisional tax payment is calculated as follows: Estimated taxable income for the year of assessment XXXX Normal tax on estimated taxable income XXXX Less: Primary, secondary and tertiary rebates under section 6 (XXXX) Less: Tax credit for medical scheme fees under section 6A (XXXX) Less: Additional medical expenses tax credit under section 6B (XXXX) Total Tax Payable XXXXX Less: Employees tax deducted from the provisional taxpayer s remuneration during the year (XXXX) Less: First provisional tax payment (if actually paid) (X) Less: Foreign tax credits (section 6quat and section 6quin*) for the year (X) SECOND PROVISIONAL TAX PAYMENT XXXX

18 Second period for Persons Under 65 years

19 Company Provisional taxpayers Company taxpayers may submit a return of an estimate of the total taxable income which will be derived by the company in respect of the year of assessment. The basic amount is the taxpayer s taxable income assessed for the latest preceding year of assessment LESS the amount of any taxable capital gain. The Commissioner may agree to an estimate lower than the basic amount should the circumstances warrant it The basic amount The basic amount for all taxpayers must be increased by 8% of the basic amount per year if an estimate: Is made for a period that ends more than one year after the end of the latest preceding year of assessment, and The estimate is made more than 18 months after the end of that year of assessment.

20 PROVISIONAL TAXPAYERS OTHER THAN COMPANIES

21 MEDICAL SCHEME FEES TAX CREDIT The tax credit is applicable in respect of fees paid by the taxpayer to a registered medical scheme. The number of persons (dependants) for whom the contributions to a medical scheme determines the value of credit The medical scheme contribution tax credit is as follows: R303 in respect of the person who has paid the contribution R303 in respect of the person s first dependant R204 in respect of the benefits to each additional dependant

22 ADDITIONAL MEDICAL EXPENSES TAX CREDIT A person who is 65 years or older his or her spouse, or his or her child is a person with a disability is eligible for 33.3% of the aggregate of the full medical scheme contributions in excess of three (3) times the credit plus 33.3% of all other qualifying out of pocket medical expenses paid by that person (excluding medical scheme contributions). Persons below 65 years are entitled to 25% of the aggregate of the full medical scheme contributions in excess of four (4) times the plus all other qualifying out of pocket medical expenses (excluding medical scheme contributions), Only to the extent that the amount exceeds 7,5% of the taxable income excluding retirement fund lump sums and severance benefits.

23 MEDICAL EXPENSES TAX CREDIT Example Person under 65 years Ms PAS is 45 years old and she has made R2 000 contributions to the medical scheme of per month on behalf of herself and her two children By 28 February 2017 she incurred R in qualifying medical expenses Her taxable income for the 2017 tax year is R

24 Solution Type of deduction Standard monthly medical scheme fees tax credits MEDICAL EXPENSES TAX CREDIT Expenses Calculation Value of Credit R2 000 p.m. x 12 = R p.a. (R303 + R303 + R204) = R810 p.m. x 12 = R9 720 R9 720 p.a. Additional medical expenses tax credit R (4 x R9 720) = R R38 880= - R14 880* *Therefore, no excess carried forward (R0 + R20 000) = R =R x 7,5% = R R R = R5 000 x 25% = R1 250 p.a. R nil R1 250 p.a.

25 ADDITIONAL MEDICAL EXPENSES TAX CREDIT Example Person 65 years and older Mr ABE is 65 years old and he has made R3000 contribution per month to a medical scheme for himself and his wife from 1 March 2016 His qualifying medical expenses by 28 February 2017 is R

26 ADDITIONAL MEDICAL EXPENSES TAX CREDIT Type of deduction Expenses Calculation Standard monthly medical scheme fees tax credits R3000 p.m. x 12 = R36000 p.a. (R303 + R303) = R606 p.m. x 12 = R7 272 Additional medical expenses tax credit R (3 x 7 272) = R R = R (R R30 000) x 33,3% = R14 713

27 Special trust Trusts are taxed at a flat rate of 45% Except for Special trusts and Testamentary trusts established for the benefit of minor children These trusts are taxed according to the tax rates applicable to individuals Example: First Period: Trusts and Example Second Period Trusts: Income of trust R Less: Allowable expenses R Less: Distribution to beneficiaries R R Retained Income (taxable income) R

28 Special trust

29 Deferral Of Payment Instalment Payment Agreement The agreement remains in effect for the term of the agreement except if: A senior SARS official may modify or terminate an instalment payment agreement if satisfied that either: The collection of tax is in jeopardy The taxpayer has furnished materially incorrect information in applying for the agreement The financial condition of the taxpayer has materially changed.

30 Deferral Of Payment - Criteria For Instalment Payment Agreement A senior SARS official may enter into an instalment payment agreement only if any of the following applies: The taxpayer suffers from a deficiency of assets or liquidity which is reasonably certain to be remedied in the future The taxpayer anticipates income or other receipts which can be used to satisfy the tax debt Prospects of immediate collection activity are poor or uneconomical but are likely to improve in the future Collection activity would be harsh in the particular case and the deferral or instalment agreement is unlikely to prejudice tax collection The taxpayer provides the security as may be required by the official.

31 Provisional taxpayers with a taxable income of up to R1 million An estimated taxable income for the second period must be equal to the lesser of the basic amount or 90% of the actual taxable income for the year. Where the estimate is less than 90% of the actual taxable income and also less than the basic amount, a penalty is levied equal to 20% of the difference between the amount of normal tax calculated in respect of such taxable estimate after taking into account a deductible rebate, and the lesser of: The amount of normal tax calculated in respect of a taxable income equal to 90% of such actual taxable income; and The amount of normal tax calculated in respect of a taxable income equal to such basic amount, at the applicable rate.

32 Example - Provisional taxpayer with a taxable income of up to R1 million Mr XY is a provisional taxpayer and he is required to submit his provisional tax returns for the 2015 year of assessment. Mr XY s basic amount of R is based on the notice of assessment for the 2014 year of assessment. His expected taxable income will be lesser than the basic amount as a result of poor trading conditions. He submitted his first and second period s estimates of a taxable income of R for the year. On assessment Mr XY s taxable income was finally determined as R for the year. His provisional tax payment for the year amounted to R , and employees tax was not paid.

33 Example - Provisional taxpayer with a taxable income of up to R1 million Solution: Mr XY s estimate of R was less than 90% of taxable income as finally determined as follows: R x 90% = R Mr XY s estimate was less than the basic amount of R He is therefore liable for a penalty a the rate of 20% on the difference between the lesser of normal tax; and it is calculated as follows: 90% of taxable income (tax on R = R51 408); the basic amount (tax on R = R65471); and the total provisional and employees tax paid during the 2015 year of assessment is R the penalty payable for the underestimate of provisional tax is therefore: R R = R x 20% = R2 600

34 Provisional taxpayers with a taxable income above R1 million An estimated taxable income for the second period must be equal to 80% of the actual taxable income for the year. A penalty will be equal to 20% of the difference between the amount of normal tax as determined in respect of such estimate, and the amount of normal tax calculated after taking into account a deductible rebate, at the rates applicable in respect of such year of assessment, in respect of a taxable income equal to 80% of such actual taxable income

35 Methods to effect payments Bank Via efiling Via Electronic Funds Transfer (EFT All that will be required is: The client s 19-digit payment reference number The beneficiary ID/account number which is linked to a specific type of tax to make payments. These details are reflected on the payment advice of the IRP6 return. Payments that do not comply with both the above-mentioned payment reference number and the beneficiary ID will not be accepted

36 How To Submit Provisional Tax On E-filling

37 How To Submit Your Return on Efilling Registration Registered E-filler Request For Return Completion Of The Return Submit the Return

38 Registration How to Register on E-filling To register, go to Click on Register

39 Registration Click on the arrow to select the appropriate user type. The options are Individuals Tax Practitioners Organisations.

40 Registration Once you have read through and accepted the e-filing Terms and Conditions, check the I Accept box and then click on Continue to proceed with your registration.

41 Registration If you are registering as: An Individual, you will need to enter all your personal particulars in order to register as an efiler. You will need your: ID/Passport number Tax reference number Contact information Bank account details. A Tax Practitioner, you will need your Tax Practitioner Number (PR) number Complete your registration by choosing your Login Name and Password and entering the special security PIN as displayed on the screen. You can click on the i information button for further information about your login and the password rules

42 Registration

43 Registered E-filer Simply click on the Login button on the e-filing homepage and use your existing login Name and Password to login.

44 Registered E-filer Ensure that the tax type for Provisional Tax (IRP6) is activated Organisations and Tax Practitioners must click on: Organisations Organisation Tax Types

45 Registered E-filer Individuals must click on: Home Tax Types

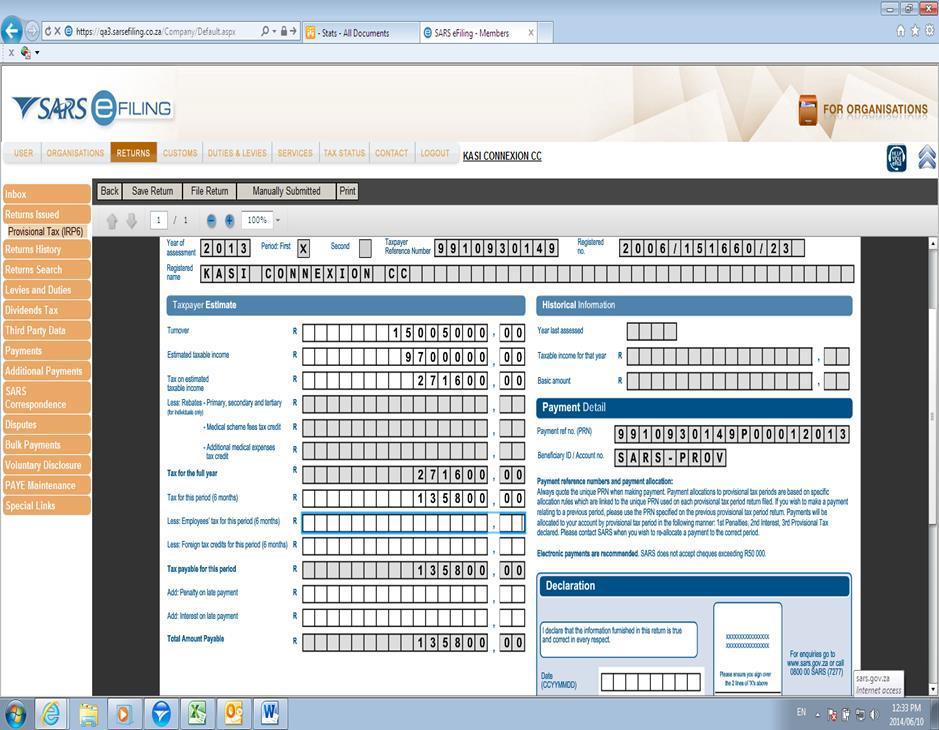

Enter the tax reference number Click on the Register")

46 Registered E-filer Select the tick box for the tax type Provisional Tax (IRP6) Enter the tax reference number Click on the Register button

47 Registered E-filer Click on Returns, and then on Returns Issued. Click on Provisional Tax (IRP6)

48 Request For Return Provisional Tax Returns can only be requested for periods that fall within: The current period The current periods minus two periods Example: if the current period is and , IRP6 forms can be requested for the periods and The current periods plus one period Example: if the current period is and , IRP6 forms can be requested for the periods and Select the provisional tax period from the drop-down menu on the top right hand corner and then click on Request Return.

49 Request For Return

50 Completion Of Return

51 Completion Of Return PERSONAL PARTICULARS The first section of your IRP6 will be pre-populated with the following: Taxpayer s particulars (as per the taxpayer particulars registered on the e-filing website) The tax period. If the taxpayer type is a trust or company/cc, the following information will be pre-populated on the return: Year of assessment Period: First (e.g. first period) Taxpayer reference number Registered name Registered no.

52 Completion Of Return If the taxpayer type is an individual, the following information will be pre-populated on the return: Year of assessment Taxpayer reference number Surname and initials Date of birth.

53 Completion Of Return The historical information will automatically be displayed if the taxpayer has been assessed within five years from the year of assessment reflected on the provisional tax return. The historical information will be blank if: The last year that the taxpayer was assessed is five years or more prior to the year of assessment reflected on the IRP6 return The taxpayer is a new taxpayer.

54 Completion Of Return First Period IRP6 You are required to complete the following fields (the mandatory fields are highlighted in red): Turnover Estimated taxable income Medical scheme fees tax credit Additional medical expenses tax credit Employees tax for this period (six months) This is a mandatory field. If employee s tax is not applicable to the taxpayer, capture the amount 0.00 in this field. Foreign tax credits for this period (six months) Penalty on late payment (if applicable) Interest on late payment (if applicable).

55 Completion Of Return The system will automatically calculate the following for individual taxpayers: Tax on estimated taxable income Rebates The rebate is only applicable to an individual taxpayer and will be determined according to the taxpayer s age as at the end of the year of assessment Refer to the tax tables on the SARS website for more information on the rebate amounts applicable to individuals for each tax year. Tax for the full year Tax for this period (six months) Tax payable for the period Total amount payable As the tax rates applicable to companies and trusts vary, the system will not automatically calculate the Tax on estimated taxable income. The user completing the IRP6 return must therefore calculate this amount manually

56 Completion Of Return Second period IRP6 You are required to complete the following fields (the mandatory fields are highlighted in red): Turnover Estimated taxable income Medical scheme fees tax credit Additional medical expenses tax credit Employees tax for this period (twelve months) This is a mandatory field. If employee s tax is not applicable to the taxpayer, capture 0.00 for the amount in this field. Foreign tax credits for this period (twelve months) Penalty on late payment Interest on late payment.

57 Completion Of Return The system will automatically calculate or pre-populate the following for individual taxpayers: Tax on estimated taxable income Rebates The rebate is only applicable to an individual taxpayer and will be determined according to the taxpayer s age as at the end of the year of assessment Refer to the tax tables on the SARS website for more information on the rebate amounts applicable to individuals for each tax year. Tax for the full year Provisional tax paid for the first period (if paid by the taxpayer) Tax Payable For this period Tax payable for this period Interest Outstanding for First Period Amount Payable

58 Completion Of Return

59 Submit The Return Declaration-enter todays date in a date fields At any stage, you can save your return before filing by clicking on Save Return. Once you have completed your Provisional Tax Return (IRP6), and you are ready to submit it to SARS, simply click on File Return When you click on File Return, e-filing will check the correctness of specific information. Where information is incorrect or incomplete, e-filing will prompt you to correct the captured information.

60 Submit The Return

61 Submit The Return You will receive a confirmation when your Provisional Tax Return has been filed. Click on Continue to return to the Provisional Tax Work Page.

Open: Monday,")

62 Thank you SARS Contact Centre SARS (7277) Visit your nearest SARS branch (to locate a branch visit Open: Monday, Tuesday, Thursday & Friday 08:00 to 16:00; Wednesday 09:00 to 16:00

EXTERNAL GUIDE. How to efile your Provisional Tax Return

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

1. Register For efiling You will need to register as an efiling user before you can file your provisional tax return electronically. To register, go to www.sarsefiling.co.za 1.1. Click on Register 1.2.

Points of Discussion

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

Disclaimer. Copyright notice

Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material) are based on the views and/or opinions of

Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material) are based on the views and/or opinions of

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

EXTERNAL GUIDE HOW TO SUBMIT AN OBJECTION OR APPEAL VIA EFILING

TABLE OF CONTENTS 1 PURPOSE 3 2 INTRODUCTION 3 3 LOGON TO THE EFILING WEBSITE 4 3.1 ACCESS THE REQUEST FOR OBJECTION OR APPEAL FORM AND ADMINISTRATIVE PENALTY ASSESSMENT NOTICE 4 3.2 DETAILED PROCEDURES

TABLE OF CONTENTS 1 PURPOSE 3 2 INTRODUCTION 3 3 LOGON TO THE EFILING WEBSITE 4 3.1 ACCESS THE REQUEST FOR OBJECTION OR APPEAL FORM AND ADMINISTRATIVE PENALTY ASSESSMENT NOTICE 4 3.2 DETAILED PROCEDURES

External Guide on how to submit a Request for Remission

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

External Guide on how to submit a Request for Remission External Guide on how to submit a Request for Remission A CONTENTS 1. INTRODUCTION 2 2. DETAILED PROCEDURES (SUBMIT RFR1 VIA efiling) 4 2.1. LOGON

Individual Income Tax

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

TCS (Tax Clearance Status) November 2018

November 2018") TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

EXTERNAL GUIDE HOW TO COMPLETE THE REGISTRATION, AMENDMENTS AND VERIFICATION FORM (RAV01)

") REGISTRATION, AMENDMENTS TABLE OF CONTENTS 1 2 3 INTRODUCTION 3 INDIVIDUAL 4 REGISTERED REPRESENTATIVE 4 4 TAX PRACTITIONER 4 5 SARS REGISTERED DETAILS 5 6 ACTIVATE REGISTERED USER Tax Practitioner and

REGISTRATION, AMENDMENTS TABLE OF CONTENTS 1 2 3 INTRODUCTION 3 INDIVIDUAL 4 REGISTERED REPRESENTATIVE 4 4 TAX PRACTITIONER 4 5 SARS REGISTERED DETAILS 5 6 ACTIVATE REGISTERED USER Tax Practitioner and

Budget Highlights 2018

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlight 2017

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

WHAT TO DO WITH YOUR IRP YEAR OF ASSESSMENT

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

Change, the new certainty

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

2013 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling 1 EXPLANATION ON THE DISCONTINUATION OF DEBIT PULL TRANSACTIONS ON efiling DISCLAIMER The information contained in this guide

EXTERNAL GUIDE COMPREHENSIVE GUIDE TO THE ITR12T RETURN FOR TRUSTS

THE ITR12T RETURN FOR TABLE OF CONTENTS 1 INTRODUCTION... 6 2 GENERAL INFORMATION... 6 2.1 WHO MUST COMPLETE AND SUBMIT THE IT12T... 6 2.2 HOW TO OBTAIN A RETURN... 7 2.3 HOW TO SUBMIT A RETURN... 8 2.4

THE ITR12T RETURN FOR TABLE OF CONTENTS 1 INTRODUCTION... 6 2 GENERAL INFORMATION... 6 2.1 WHO MUST COMPLETE AND SUBMIT THE IT12T... 6 2.2 HOW TO OBTAIN A RETURN... 7 2.3 HOW TO SUBMIT A RETURN... 8 2.4

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS. Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

Introduction. Lerato Mokoena (SARS Support Consultant-eFiling and specialist) Gauteng and Northwest Province

Gauteng and Northwest Province") Introduction Lerato Mokoena (SARS Support Consultant-eFiling and E@syfile specialist) Gauteng and Northwest Province lmokoena2@sars.gov.za Topics to be discussed Tax Compliance status Functionality on

Introduction Lerato Mokoena (SARS Support Consultant-eFiling and E@syfile specialist) Gauteng and Northwest Province lmokoena2@sars.gov.za Topics to be discussed Tax Compliance status Functionality on

GREATSOFT CRM CLIENT RELEASE NOTES

GREATSOFT CRM 2016.1.0 CLIENT RELEASE NOTES CONTENTS INTRODUCTION...1 Prerequisites...1 CRM...2 Tasks...2 Billings...2 Disbursements...2 TAX...2 ITR12 Changes for 2016...2 Other ITR12 Changes... 15 ITR14

GREATSOFT CRM 2016.1.0 CLIENT RELEASE NOTES CONTENTS INTRODUCTION...1 Prerequisites...1 CRM...2 Tasks...2 Billings...2 Disbursements...2 TAX...2 ITR12 Changes for 2016...2 Other ITR12 Changes... 15 ITR14

A person that elected to be registered as above must be registered by the Commissioner with effect from the beginning of that year of assessment.

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

6.1 WHO QUALIFIES TO REGISTER FOR TURNOVER TAX? A person that qualifies as a micro business may register for TT, if it is a: Natural person (or the deceased or insolvent estate of a natural person is registered

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

FREQUENTLY ASKED QUESTIONS MANUAL COMPLETION AND SUBMISSION OF EMP201 Revision: 1 Page 1 of 6 1 PURPOSE The purpose of these FAQs is to assist employers in understanding the monthly completion and submission

Source Codes. New Source Codes and Validations

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

Source Codes New Source Codes and Validations Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make

DECEASED ESTATES REGISTRATION & ASSESSMENT

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

Dashboard. Dashboard Page

Website User Guide This guide is intended to assist you with the basic functionality of the Journey Retirement Plan Services website. If you require additional assistance, please contact our office at

Website User Guide This guide is intended to assist you with the basic functionality of the Journey Retirement Plan Services website. If you require additional assistance, please contact our office at

How to enroll in your Tulsa Fire Health and Welfare benefits!

How to enroll in your Tulsa Fire Health and Welfare benefits! Step 1: go to https://www.employeenavigator.com Click Login in the upper right hand corner Step 2: Click Register as a new user Step 3: Fill

How to enroll in your Tulsa Fire Health and Welfare benefits! Step 1: go to https://www.employeenavigator.com Click Login in the upper right hand corner Step 2: Click Register as a new user Step 3: Fill

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON ACCOMMODATION

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

Quick Tax Guide 2013/14 Simplicity from complexity

Quick Tax Guide 2013/14 Simplicity from complexity Income Tax for Individuals Tax rates and rebates Individuals, Estates & Special Trusts 1 (Year ending 28 February 2014) Taxable income as exceeds But

Quick Tax Guide 2013/14 Simplicity from complexity Income Tax for Individuals Tax rates and rebates Individuals, Estates & Special Trusts 1 (Year ending 28 February 2014) Taxable income as exceeds But

EXTERNAL GUIDE HOW TO COMPLETE AND SUBMIT YOUR COUNTRY BY COUNTRY INFORMATION

TABLE OF CONTENTS TABLE OF CONTENTS 2 1 PURPOSE 3 2 INTRODUCTION 3 3 THE CBC SUBMISSION 4 3.1 PERSON REQUIRED TO SUBMIT THE CBC 4 3.2 COMPLETE THE CBC REPORT, THE MASTER AND LOCAL FILE 4 3.3 SUBMIT CBC01

TABLE OF CONTENTS TABLE OF CONTENTS 2 1 PURPOSE 3 2 INTRODUCTION 3 3 THE CBC SUBMISSION 4 3.1 PERSON REQUIRED TO SUBMIT THE CBC 4 3.2 COMPLETE THE CBC REPORT, THE MASTER AND LOCAL FILE 4 3.3 SUBMIT CBC01

BUDGET 2019 TAX GUIDE

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

Tax guide 2018/2019 TAX FACTS

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

SARS Tax Guide 2014 / 2015

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

1. Objective of this manual What is efiling and how does it work in TaxWare? Why use TaxWare?... 3

efiling in TaxWare Index 1. Objective of this manual... 3 2. What is efiling and how does it work in TaxWare?... 3 2.1. Why use TaxWare?... 3 3. Activation of efiling on TaxWare... 3 3.1. Steps to activate

efiling in TaxWare Index 1. Objective of this manual... 3 2. What is efiling and how does it work in TaxWare?... 3 2.1. Why use TaxWare?... 3 3. Activation of efiling on TaxWare... 3 3.1. Steps to activate

TRAVEL PORTAL INSTRUCTIONS

TRAVEL PORTAL INSTRUCTIONS Date: June 22, 2018 Version: Version 3.1 Prepared By: Berkley Canada Table of Contents 1 ACCESSING THE PORTAL... 3 1.1 LOGIN & LOGOUT... 3 1.2 RESET YOUR PASSWORD... 3 2 THE

TRAVEL PORTAL INSTRUCTIONS Date: June 22, 2018 Version: Version 3.1 Prepared By: Berkley Canada Table of Contents 1 ACCESSING THE PORTAL... 3 1.1 LOGIN & LOGOUT... 3 1.2 RESET YOUR PASSWORD... 3 2 THE

Guide for tax rates/duties/levies (Issue 11)

") Guide for tax rates/duties/levies (Issue 11) Guide for tax rates/duties/levies Preface This is a guide provides a current and historical view of the rates for various taxes, duties and levies collected

Guide for tax rates/duties/levies (Issue 11) Guide for tax rates/duties/levies Preface This is a guide provides a current and historical view of the rates for various taxes, duties and levies collected

EXTERNAL REFERENCE GUIDE SECURITIES TRANSFER TAX. EXTERNAL GUIDE - SECURITIES TRANSFER TAX GEN-PAYM-11-G01 Revision: 3 EFFECTIVE DATE:

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

2013 EXTERNAL REFERENCE GUIDE SECURITIES EXTERNAL GUIDE - SECURITIES Revision: 3 EFFECTIVE DATE: 2013.11.30 DISCLAIMER The information contained in this guide is intended as guidance only and is not considered

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Welcome to the SARS Tax Workshop The purpose of this presentation is to provide information in an easy-to-understand format and is intended to make the provisions of the legislation more accessible to

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Income Tax. Tax Guide for Small Businesses 2015/16

Income Tax Tax Guide for Small Businesses 2015/16 Preface Tax Guide for Small Businesses 2015/2016 This guide is a general guide dealing with the taxation of small businesses. This guide is not an official

Income Tax Tax Guide for Small Businesses 2015/16 Preface Tax Guide for Small Businesses 2015/2016 This guide is a general guide dealing with the taxation of small businesses. This guide is not an official

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

Integrated Payments: Online Payment Control & Online Payment History Quick Reference Guide

Integrated Payments: Online Payment Control & Online Payment History Quick Reference Guide Table of Contents File Summary (Online Payment Control Only)... 2 Payment Statuses... 4 Payments Search... 5 Pending

Integrated Payments: Online Payment Control & Online Payment History Quick Reference Guide Table of Contents File Summary (Online Payment Control Only)... 2 Payment Statuses... 4 Payments Search... 5 Pending

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16.

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

A guide to understanding the medical scheme fees tax credit

A guide to understanding the medical scheme fees tax credit A guide to understanding the medical scheme fees tax credit 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. WHAT ARE THE CHANGES?... 3 3. THE CHANGES

A guide to understanding the medical scheme fees tax credit A guide to understanding the medical scheme fees tax credit 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. WHAT ARE THE CHANGES?... 3 3. THE CHANGES

HOW TO COMPLETE THE IT14 RETURN

HOW TO COMPLETE THE IT14 RETURN INTRODUCTION This guide is designed to help to accurately complete income tax returns for companies and close corporations (CC). For assistance visit your local SARS branch

HOW TO COMPLETE THE IT14 RETURN INTRODUCTION This guide is designed to help to accurately complete income tax returns for companies and close corporations (CC). For assistance visit your local SARS branch

Apply Online For Social Security Benefits

Apply Online For Social Security Benefits Apply Online For Social Security Benefits Why should I apply for benefits online? Applying for benefits online offers several advantages, among them: You apply

Apply Online For Social Security Benefits Apply Online For Social Security Benefits Why should I apply for benefits online? Applying for benefits online offers several advantages, among them: You apply

EXTERNAL GUIDE GUIDE TO THE ITR12 RETURN FOR DECEASED ESTATES. (For persons who die on or after 1 March 2016)

") EXTERNAL GUIDE GUIDE TO THE ITR12 RETURN FOR DECEASED ESTATES (For persons who die on or after 1 March 2016) TABLE OF CONTENTS 1 PURPOSE... 4 2 GENERAL INFORMATION... 4 2.1... 4 2.2 HOW TO SUBMIT A RETURN

EXTERNAL GUIDE GUIDE TO THE ITR12 RETURN FOR DECEASED ESTATES (For persons who die on or after 1 March 2016) TABLE OF CONTENTS 1 PURPOSE... 4 2 GENERAL INFORMATION... 4 2.1... 4 2.2 HOW TO SUBMIT A RETURN

Tax year end processing

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

Sage One Payroll Tax Year End Guide 1 Tax year end processing This guide will assist you with the running of your tax year end in Sage One Payroll. It is quite a simple process to run the year end by following

INCOME TAX: INDIVIDUALS AND TRUSTS

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

FREQUENTLY ASKED QUESTIONS COMPLETION AND SUBMISSION OF CSV. TM EMPLOYER AND ZIPCENTRALFILE RECONCILIATION DOCUMENTS

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

FREQUENTLY ASKED QUESTIONS Revision: 1 Page 1 of 8 1 PURPOSE The purpose of this document is to provide answers to frequently asked questions by employers in respect of creating CSV data files and submitting

Using the City of Lancaster s Municipal Tax Preparation Tool

Using the City of Lancaster s Municipal Tax Preparation Tool The Municipal Tax Preparation Tool is designed to assist individual taxpayers in completing their Lancaster Income Tax return. The product is

Using the City of Lancaster s Municipal Tax Preparation Tool The Municipal Tax Preparation Tool is designed to assist individual taxpayers in completing their Lancaster Income Tax return. The product is

South African Income Tax Guide for 2013/2014

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

South African Revenue Service How to complete the IT14 return

South African Revenue Service How to complete the IT14 return NEED MORE HELP? Call 0800 00 SARS (7277) Visit www.sars.gov.za or visit any SARS branch INTRODUCTION This guide is designed to help to accurately

South African Revenue Service How to complete the IT14 return NEED MORE HELP? Call 0800 00 SARS (7277) Visit www.sars.gov.za or visit any SARS branch INTRODUCTION This guide is designed to help to accurately

An overview of the financial profile fact finder

An overview of the financial profile fact finder Functions addressed in this document: A step-by-step walk through of the financial profile fact finder. How data entry is presented to the client within

An overview of the financial profile fact finder Functions addressed in this document: A step-by-step walk through of the financial profile fact finder. How data entry is presented to the client within

EXTERNAL FREQUENTLY ASKED QUESTIONS TAXPAYER CENTRICITY (CLIENT APPROACH. FUNCTIONALITY ON efiling)

") EXTERNAL FREQUENTLY ASKED S TAXPAYER CENTRICITY (CLIENT APPROACH FUNCTIONALITY ON Revision: 0 Page 1 of 6 1 PURPOSE These FAQs provide general information regarding taxpayer centricity, which is a new

EXTERNAL FREQUENTLY ASKED S TAXPAYER CENTRICITY (CLIENT APPROACH FUNCTIONALITY ON Revision: 0 Page 1 of 6 1 PURPOSE These FAQs provide general information regarding taxpayer centricity, which is a new

Form 941/C1-ME. Questions regarding: Important

State of Maine Maine Revenue Services and Department of Labor 2001 Combined Filing for Income Tax Withholding and Unemployment Contributions Form 941/C1-ME Questions regarding: Income Tax Withholding 207-626-8475

State of Maine Maine Revenue Services and Department of Labor 2001 Combined Filing for Income Tax Withholding and Unemployment Contributions Form 941/C1-ME Questions regarding: Income Tax Withholding 207-626-8475

Group Pensions Online. User Manual for Employees & Members

Group Pensions Online User Manual for Employees & Members Contents Introduction 1 Glossary 2 How to access your pension information online 3 Accessing your details 4 Member Details page 5 Viewing Fund

Group Pensions Online User Manual for Employees & Members Contents Introduction 1 Glossary 2 How to access your pension information online 3 Accessing your details 4 Member Details page 5 Viewing Fund

Tax data card 2018/2019

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

Welcome to the SARS Tax Workshop

Small Business Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Small Business Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

New Tax VDP Applications using efiling. There are two parts to the application process: Tax Practitioner

Application Guide for efiling Tax Voluntary Disclosure Programme 2010 Introduction The South African Revenue Service (SARS) will implement a Voluntary Disclosure Porgramme (VDP) that will be effective

Application Guide for efiling Tax Voluntary Disclosure Programme 2010 Introduction The South African Revenue Service (SARS) will implement a Voluntary Disclosure Porgramme (VDP) that will be effective

UNPACKING PROVISIONAL TAX PROCESSES 2016

UNPACKING PROVISIONAL TAX PROCESSES 2016 Prepared by Mark Silberman B.Acc C.A.(S.A.) Copyright Accfin Software Page 1 Contents 1. LAWS - THE CHANGING PROVISIONAL TAX PROCESSES... 5 A. Introduction... 5

UNPACKING PROVISIONAL TAX PROCESSES 2016 Prepared by Mark Silberman B.Acc C.A.(S.A.) Copyright Accfin Software Page 1 Contents 1. LAWS - THE CHANGING PROVISIONAL TAX PROCESSES... 5 A. Introduction... 5

TAX GUIDE FOR SMALL BUSINESSES 2013/14

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR SMALL BUSINESSES 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Tax Guide for Small Businesses 2013/14 This is a general

TAX GUIDE FOR MICRO BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

Step by step guide to using AXISe Internet Member Self Service

Step by step guide to using AXISe Internet Member Self Service Table of contents 1 Introduction 4 2 Warning Page 5 3 Password request 7 4 Validation entry Error! Bookmark not defined. 5 Security Password

Step by step guide to using AXISe Internet Member Self Service Table of contents 1 Introduction 4 2 Warning Page 5 3 Password request 7 4 Validation entry Error! Bookmark not defined. 5 Security Password

Completing your online Tax Return

Completing your online Tax Return V10 21/06/2018 1 Contents Introduction... 3 Getting started... 4 Completing the online tax return... 6 State Pension... 10 Private Pension... 10 Foreign Income... 11 UK

Completing your online Tax Return V10 21/06/2018 1 Contents Introduction... 3 Getting started... 4 Completing the online tax return... 6 State Pension... 10 Private Pension... 10 Foreign Income... 11 UK

TAXATION IN SOUTH AFRICA 2013/14

SOUTH AFRICAN REVENUE SERVICE TAXATION IN SOUTH AFRICA 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Taxation in South Africa 2013/14 This is a general guide

SOUTH AFRICAN REVENUE SERVICE TAXATION IN SOUTH AFRICA 2013/14 Another helpful guide brought to you by the South African Revenue Service Preface Taxation in South Africa 2013/14 This is a general guide

TAXATION IN SOUTH AFRICA 2016/7

Retirement Fund March 2016 TAXATION IN SOUTH AFRICA 2016/7 Your Retirement - Our Passion Sentinel Retirement Fund Reg No 12/8/1215 Sentinel House 1 Sunnyside Drive Sunnyside Park PARKTOWN 2193 P O Box

Retirement Fund March 2016 TAXATION IN SOUTH AFRICA 2016/7 Your Retirement - Our Passion Sentinel Retirement Fund Reg No 12/8/1215 Sentinel House 1 Sunnyside Drive Sunnyside Park PARKTOWN 2193 P O Box

VALUE ADDED TAX (VAT) RETURNS USER GUIDE

RETURNS USER GUIDE") VALUE ADDED TAX (VAT) RETURNS USER GUIDE February 2018 1 Contents 1. Brief overview of this user guide... 3 2. Important notes about the VAT Return... 3 3. Completing and Submitting the VAT Return Form...

VALUE ADDED TAX (VAT) RETURNS USER GUIDE February 2018 1 Contents 1. Brief overview of this user guide... 3 2. Important notes about the VAT Return... 3 3. Completing and Submitting the VAT Return Form...

Individual Taxpayer Electronic Filing Instructions

Individual Taxpayer Electronic Filing Instructions Table of Contents INDIVIDUAL TAXPAYER ELECTRONIC FILING OVERVIEW... 3 SUPPORTED BROWSERS... 3 PAGE AND NAVIGATION OVERVIEW... 4 BUTTONS AND ICONS... 5

Individual Taxpayer Electronic Filing Instructions Table of Contents INDIVIDUAL TAXPAYER ELECTRONIC FILING OVERVIEW... 3 SUPPORTED BROWSERS... 3 PAGE AND NAVIGATION OVERVIEW... 4 BUTTONS AND ICONS... 5

ACE Centralised Payment Guidance. Training Providers. August 2013

ACE Centralised Payment Guidance Training Providers August 2013 We recommend installing the latest Adobe Acrobat Reader for the best viewing experience: http://get.adobe.com/reader/ Contents 2 Contents

ACE Centralised Payment Guidance Training Providers August 2013 We recommend installing the latest Adobe Acrobat Reader for the best viewing experience: http://get.adobe.com/reader/ Contents 2 Contents

Paper F6 (ZAF) Taxation (South Africa) Tuesday 4 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (South Africa) Tuesday 4 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (South Africa) Tuesday 4 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Fundamentals Level Skills Module Taxation (South Africa) Tuesday 4 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Employee Enrollment User Guide

Employee Enrollment User Guide Welcome to Online Enrollment! In this guide, you will find information and step-by-step instructions on how to enroll in your benefits. Table of Contents Before you get started:

Employee Enrollment User Guide Welcome to Online Enrollment! In this guide, you will find information and step-by-step instructions on how to enroll in your benefits. Table of Contents Before you get started:

MyBenefits Open Enrollment User Guide

MyBenefits Open Enrollment User Guide This guide will help you navigate MyBenefits, the University s online benefits enrollment application. All benefit-eligible faculty and staff must actively enroll

MyBenefits Open Enrollment User Guide This guide will help you navigate MyBenefits, the University s online benefits enrollment application. All benefit-eligible faculty and staff must actively enroll

Paper P6 (ZAF) Advanced Taxation (South Africa) Friday 5 June Professional Level Options Module

Advanced Taxation (South Africa) Friday 5 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Friday 5 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (South Africa) Friday 5 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

(Contact us if you need help: Call between 07:30-17:30 (Mon - Fri) or

or") RETIREMENT ANNUITY FUND WITHDRAWAL INSTRUCTION Make an informed decision: BEFORE YOU WITHDRAW ADDITIONAL INFORMATION STEP 1 COMPLETE THE FORM & AGREE TO CONDITIONS OF MEMBERSHIP Please consider the tax

RETIREMENT ANNUITY FUND WITHDRAWAL INSTRUCTION Make an informed decision: BEFORE YOU WITHDRAW ADDITIONAL INFORMATION STEP 1 COMPLETE THE FORM & AGREE TO CONDITIONS OF MEMBERSHIP Please consider the tax

Honeywell Savings and Ownership Plan. Distribution Options Guide

Honeywell Savings and Ownership Plan Distribution Options Guide June 2016 For more information on the Plan, visit the HR Direct Website through the Honeywell Intranet or www.honeywell.com, click on 'Employee

Honeywell Savings and Ownership Plan Distribution Options Guide June 2016 For more information on the Plan, visit the HR Direct Website through the Honeywell Intranet or www.honeywell.com, click on 'Employee

STEPS FOR GENERATING ITREG-FILE FOR AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for

sedert 1982 STEPS FOR GENERATING ITREG-FILE FOR e@syfile, AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for e@syfile. 1. Start your reconciliation process by generating the ITREG-file for e@syfile.

sedert 1982 STEPS FOR GENERATING ITREG-FILE FOR e@syfile, AS WELL AS CREATING SARS TAX CERTIFICATES & THE CSV-file for e@syfile. 1. Start your reconciliation process by generating the ITREG-file for e@syfile.

Quick Start Guide to Payroll Tax Year-End

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

Introduction. Ayanda Takela (SARS efiling and specialist)

") Introduction Ayanda Takela (SARS efiling and e@syfile specialist) Agenda efiling Profile types Post-Death Registration Scenarios Process to a successful Registration Acquiring a new number Additional Estate

Introduction Ayanda Takela (SARS efiling and e@syfile specialist) Agenda efiling Profile types Post-Death Registration Scenarios Process to a successful Registration Acquiring a new number Additional Estate

Get Ready for Payroll Year End. April Your guide containing hints and tips for a successful year end.

Get Ready for Payroll Year End April 2011 Your guide containing hints and tips for a successful year end. 2 Contents Tips for a successful year end... 3 Checklist: things to remember... 3 Where do I find

Get Ready for Payroll Year End April 2011 Your guide containing hints and tips for a successful year end. 2 Contents Tips for a successful year end... 3 Checklist: things to remember... 3 Where do I find

IRAdirect User Guide Fully-Administered Program

IRAdirect User Guide Fully-Administered Program It is understood that the publisher is not engaged in rendering legal or accounting services. Every effort has been made to ensure the accuracy of the material

IRAdirect User Guide Fully-Administered Program It is understood that the publisher is not engaged in rendering legal or accounting services. Every effort has been made to ensure the accuracy of the material

VAT REFUND USER GUIDE

VAT REFUND USER GUIDE February 2018 Contents 1. Brief overview of this user guide... 2 2. Purpose of the Claim... 2 3. Timeframes for repayment... 2 4. Submitting the Claim... 3 4.1. Login to FTA e-services

VAT REFUND USER GUIDE February 2018 Contents 1. Brief overview of this user guide... 2 2. Purpose of the Claim... 2 3. Timeframes for repayment... 2 4. Submitting the Claim... 3 4.1. Login to FTA e-services

WELCOME TO INTERNET BANKING. Provided by Scottish Widows Bank

WELCOME TO INTERNET BANKING Provided by Scottish Widows Bank INTRODUCTION INTERNET BANKING PUTS YOU IN CONTROL OF YOUR BANKING BY GIVING YOU THE FLEXIBILITY TO ACCESS YOUR SCOTTISH WIDOWS BANK SAVINGS

WELCOME TO INTERNET BANKING Provided by Scottish Widows Bank INTRODUCTION INTERNET BANKING PUTS YOU IN CONTROL OF YOUR BANKING BY GIVING YOU THE FLEXIBILITY TO ACCESS YOUR SCOTTISH WIDOWS BANK SAVINGS

2017 Tax Return Overview for International Students

2017 Tax Return Overview for International Students This quick guide is provided for international students to become familiar with U.S. Tax return filings. Tax returns are due April 17, 2018 for students

2017 Tax Return Overview for International Students This quick guide is provided for international students to become familiar with U.S. Tax return filings. Tax returns are due April 17, 2018 for students

(Contact us if you need help:

PENSION OR PROVIDENT PRESERVATION FUND WITHDRAWAL INSTRUCTION BEFORE YOU WITHDRAW ADDITIONAL INFORMATION STEP 1 COMPLETE THE FORM & AGREE TO CONDITIONS OF MEMBERSHIP Make an informed decision: Please consider

PENSION OR PROVIDENT PRESERVATION FUND WITHDRAWAL INSTRUCTION BEFORE YOU WITHDRAW ADDITIONAL INFORMATION STEP 1 COMPLETE THE FORM & AGREE TO CONDITIONS OF MEMBERSHIP Make an informed decision: Please consider

Clubs or societies return guide 2012

IR 9GU March 2012 Clubs or societies return guide 2012 Read this guide to help you fill in your IR 9 return. Complete and send us your IR 9 return by 7 July 2012, unless you have an extension of time to

IR 9GU March 2012 Clubs or societies return guide 2012 Read this guide to help you fill in your IR 9 return. Complete and send us your IR 9 return by 7 July 2012, unless you have an extension of time to

Benefits (ESS): Make Benefit Elections

: Make Benefit Elections") Using BearTrax All Employees Introduction Purpose: The purpose of this task is for you to manage, change and/or submit your benefit elections using BearTrax. To request a password, you ll email beartrax@shawnee.edu.

Using BearTrax All Employees Introduction Purpose: The purpose of this task is for you to manage, change and/or submit your benefit elections using BearTrax. To request a password, you ll email beartrax@shawnee.edu.

Employee Online Enrollment User Guide

Employee Online Enrollment User Guide Welcome to Online Enrollment! In this guide, you will find information and step-by-step instructions on how to enroll in your benefits. Table of Contents Before you

Employee Online Enrollment User Guide Welcome to Online Enrollment! In this guide, you will find information and step-by-step instructions on how to enroll in your benefits. Table of Contents Before you

FAST Budget Budget Transfers

FAST Budget Budget Transfers User Guide Millennium FAST The user guide was created using FAST Version 4.2.18 CSU FAST 4.2.18 BUDGET TRANSFER User Guide v0.4.docx (FOAP = FUND ORGANISATION ACCOUNT PROGRAM)

FAST Budget Budget Transfers User Guide Millennium FAST The user guide was created using FAST Version 4.2.18 CSU FAST 4.2.18 BUDGET TRANSFER User Guide v0.4.docx (FOAP = FUND ORGANISATION ACCOUNT PROGRAM)

Next >> Quick Tax Guide 2019/20 South Africa. Making an impact that matters

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters Contents... 1...1...1...2...3...4 Severance and Retirement Fund Lump Sum...4... 5...5...6...7...7...7...7... 8...8...8...9...9...9...9...10...10...10...10...10...11...

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters Contents... 1...1...1...2...3...4 Severance and Retirement Fund Lump Sum...4... 5...5...6...7...7...7...7... 8...8...8...9...9...9...9...10...10...10...10...10...11...

VAT USER GUIDE (REGISTRATION, AMENDMENT, DE-REGISTRATION) December 2017

December 2017") VAT USER GUIDE (REGISTRATION, AMENDMENT, DE-REGISTRATION) December 2017 Contents 1. Brief overview of this user guide... 3 2. Creating and using your e-services account... 4 2.1 Create an e-services account

VAT USER GUIDE (REGISTRATION, AMENDMENT, DE-REGISTRATION) December 2017 Contents 1. Brief overview of this user guide... 3 2. Creating and using your e-services account... 4 2.1 Create an e-services account

CST KARA SAMADHANA SCHEME, 2018 USER MANUAL FOR DEALARS

CST KARA SAMADHANA SCHEME, 2018 USER MANUAL FOR DEALARS VER. 1.0 07-08-2018 Government of Karnataka Commercial Taxes Department National Informatics Centre CTD Karasamadhana Scheme NIC CONTENTS User Manual

CST KARA SAMADHANA SCHEME, 2018 USER MANUAL FOR DEALARS VER. 1.0 07-08-2018 Government of Karnataka Commercial Taxes Department National Informatics Centre CTD Karasamadhana Scheme NIC CONTENTS User Manual

OID Detail 2018 Tax Year End

OID Detail 2018 Tax Year End Occupational Injuries and Diseases (OID) Extracts from the Occupational Injuries and Diseases Act 1.1 Definitions "employee" means a person who has entered into or works under

OID Detail 2018 Tax Year End Occupational Injuries and Diseases (OID) Extracts from the Occupational Injuries and Diseases Act 1.1 Definitions "employee" means a person who has entered into or works under

2018 Online Benefits Enrollment Guide ENROLLMENT GUIDE. Information you need before beginning enrolling 2. Important Definitions and Age Limitations 3

ENROLLMENT GUIDE Information you need before beginning enrolling 2 Important Definitions and Age Limitations 3 Navigating to and Logging-on to PeopleSoft HRMS 4-5 Navigating to Self Service Online Benefits

ENROLLMENT GUIDE Information you need before beginning enrolling 2 Important Definitions and Age Limitations 3 Navigating to and Logging-on to PeopleSoft HRMS 4-5 Navigating to Self Service Online Benefits

Guidance notes for keying Residential Buy-to-Let property under limited company structure. Enquiry

Guidance notes for keying Residential Buy-to-Let property under limited company structure Enquiry A step-by-step guide We know that submitting cases can sometimes seem complicated and time-consuming (especially

Guidance notes for keying Residential Buy-to-Let property under limited company structure Enquiry A step-by-step guide We know that submitting cases can sometimes seem complicated and time-consuming (especially

Tier I Tier II. Retire. Getting Ready to. KP&F Pre-Retirement Planning Guide KPERS

Tier I Tier II Retire Getting Ready to KP&F Pre-Retirement Planning Guide KPERS Countdown to Retirement Checklist Attend a pre-retirement seminar. Our pre-retirement seminars are designed to help you navigate

Tier I Tier II Retire Getting Ready to KP&F Pre-Retirement Planning Guide KPERS Countdown to Retirement Checklist Attend a pre-retirement seminar. Our pre-retirement seminars are designed to help you navigate

A STEP-BY-STEP GUIDE TO THE EMPLOYER RECONCILIATION PROCESS

EF NO. Trading or Other Name: Transaction Year: Time Stamp: 21159840 A STEP-BY-STEP GUIDE TO THE EMPLOYE ECONCILIATION POCESS Transaction Year (CCYY) Period of econciliation (CCYYMM) Business Information

EF NO. Trading or Other Name: Transaction Year: Time Stamp: 21159840 A STEP-BY-STEP GUIDE TO THE EMPLOYE ECONCILIATION POCESS Transaction Year (CCYY) Period of econciliation (CCYYMM) Business Information

Get Ready for Payroll Year End April 2008

Get Ready for Payroll Year End April 2008 Tips for a successful year end Remember: All users who file online must be registered with HMRC via their Online services Web site. After you register with HMRC

Get Ready for Payroll Year End April 2008 Tips for a successful year end Remember: All users who file online must be registered with HMRC via their Online services Web site. After you register with HMRC

Optional Network Election for Single Point Online Transactions Eff. 10/1/13. Follow us!

Optional Network Election for Single Point Online Transactions Eff. 10/1/13 www.myalabamataxes.gov Follow us! @ONESPOTAlabama One Spot Alabama Local governments (cities and counties) have the authority

Optional Network Election for Single Point Online Transactions Eff. 10/1/13 www.myalabamataxes.gov Follow us! @ONESPOTAlabama One Spot Alabama Local governments (cities and counties) have the authority

The Institute of Chartered Accountants of India Western India Regional Council

The Institute of Chartered Accountants of India Western India Regional Council Seminar on E-filing of Returns and Forms under Various Acts Mumbai 11 th June 2011 E-filing of Returns and Forms under MVAT

The Institute of Chartered Accountants of India Western India Regional Council Seminar on E-filing of Returns and Forms under Various Acts Mumbai 11 th June 2011 E-filing of Returns and Forms under MVAT

Accessing Lawson Self-Services

Accessing Lawson Self-Services Contents Lawson Self-Service Access 3 Signing into Lawson 4 Switching between modules 4 Accessing your pay remittances 4 Updating your direct deposit 5 Updating your tax

Accessing Lawson Self-Services Contents Lawson Self-Service Access 3 Signing into Lawson 4 Switching between modules 4 Accessing your pay remittances 4 Updating your direct deposit 5 Updating your tax

New York Guide to List Billing WELCOME TO DEARBORN NATIONAL. Life Insurance Company of New York

www.dearbornnational.com WELCOME TO DEARBORN NATIONAL UNDERWRITTEN BY DEARBORN NATIONAL LIFE INSURANCE COMPANY OF NEW YORK New York Guide to List Billing Life Insurance Company of New York Products and

www.dearbornnational.com WELCOME TO DEARBORN NATIONAL UNDERWRITTEN BY DEARBORN NATIONAL LIFE INSURANCE COMPANY OF NEW YORK New York Guide to List Billing Life Insurance Company of New York Products and