OTP BANKA SRBIJA A.D., NOVI SAD. Consolidated Financial Statements Year Ended December 31, 2014 and Independent Auditors Report

|

|

|

- Edward Matthew Clark

- 5 years ago

- Views:

Transcription

1 Consolidated Financial Statements Year Ended 2014 and Independent Auditors Report

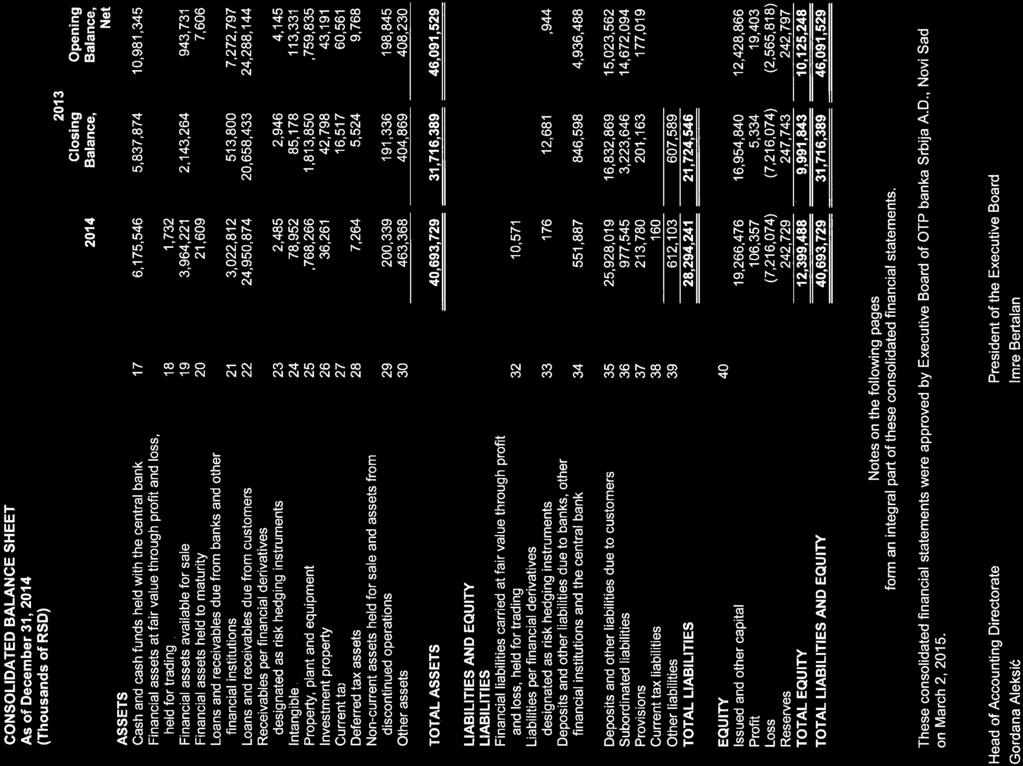

2 CONTENTS Page Independent Auditors' Report 1 Consolidated Financial Statements: Consolidated Income Statement 2 Consolidated Statement of Other Comprehensive Income 3 Consolidated Balance Sheet 4 Consolidated Statement of Cash Flows 5 Consolidated Statement of Changes in Equity 6 Notes to the Consolidated Financial Statements 7-72 Appendix: Annual Business Report

3

4

5

6

7

8

9 BANK S ESTABLISHMENT AND ACTIVITY These consolidated financial statements include the stand-alone financial statements of OTP Banka Srbija a.d. Novi Sad and those of its subsidiary OTP Investments d.o.o. Novi Sad. OTP Banka Srbija a.d. Novi Sad, as a parent entity to the subsidiary OTP Investments d.o.o. Novi Sad, prepares consolidated financial statements. OTP Banka Srbija a.d., Novi Sad (hereinafter: the Bank ) is a direct legal successor of Kulska banka a.d., Novi Sad. Kulska banka a.d., Novi Sad was registered as a shareholding company with the Commercial Court of Sombor, in accordance with May 17, 1995 Decision No. Fi 488/95. Pursuant to the Serbian Business Registers Agency Decision number BD 32735/2007 as of May 18, 2007, the name Kulska banka a.d., Novi Sad was changed into OTP banka Srbija a.d., Novi Sad. Simultaneously, the status change of merger and acquisition was registered, whereby Zepter banka a.d. Beograd and Niška banka a.d. Niš were merged with and acquired by Kulska banka a.d. Novi Sad as the Acquirer; through the aforesaid status change Zepter banka a.d. Beograd and Niška banka a.d. Niš ceased to exist and were deleted from the Business Register. The Bank is registered in the Republic of Serbia to provide banking services of payment transfers, lending and depositary activities in accordance with the Law on Banks, and it is obligated to operate based upon principles of liquidity, safety and profitability. As at 2014, the Bank consisted of the Head Office in Novi Sad, at No. 80 Bulevar Oslobođenja Street, 6 regional affiliates and 48 branches. As at 2014, the Bank had 670 employees ( 2013: 691 employees). The Bank s tax identification number is OTP Investments d.o.o., Novi Sad is a legal successor of the company KB-NS Investments d.o.o. KB- NS Investments d.o.o. was established pursuant to the Decision of Foundation dated January 19, 2006 as a limited liability company. The Company was registered with the Serbian Business Registers Agency in Novi Sad no. BD /2006. The Company s core business activities are factoring and consulting. The Bank is the sole owner of the Company. As of 2014, the Company had 1 employee (2013: 1 employee). The tax identification number of the company OTP Investments d.o.o. is BASIS OF PREPARATION AND PRESENTATION OF THE CONSOLIDATED FINANCIAL STATEMENTS 2.1. Basis of Preparation and Presentation of the Consolidated Financial Statements Legal entities and entrepreneurs incorporated in Serbia are required to maintain their books of account, to recognize and value assets and liabilities, income and expenses, and to present, submit and disclose financial statements in conformity the Law on Accounting (hereinafter referred as: the Law, Official Gazette of the Republic of Serbia no. 63/2013). As a large legal entity, the Bank is required to apply International Financial Reporting Standards ( IFRS ), which as per the aforementioned law comprise the following: the Framework for the Preparation and Presentation of Financial Statements (the Framework ), International Accounting Standards ( IAS ), International Financial Reporting Standards ( IFRS ), as well as the related interpretations issued by the International Financial Reporting Interpretations Committee ( IFRIC ) and additional related interpretations issued by International Accounting Standards Board ( IASB ), the translations of which to the Serbian language were approved and issued by the competent Ministry of Finance and which were in effect as at

10 BASIS OF PREPARATION AND PRESENTATION OF THE CONSOLIDATED FINANCIAL STATEMENTS (Continued) 2.1. Basis of Preparation and Presentation of the Consolidated Financial Statements (Continued) The amendments to IAS, as well as the newly issued IFRS and the related interpretations issued by the IASB and the IFRIC, in the period between 2002 and January 1, 2009, were officially adopted pursuant to a Decision enacted by the Ministry of Finance of the Republic of Serbia (the Ministry ) on October 5, 2010 and published the Official Gazette of the Republic of Serbia no. 77/2010. The Ministry s Decision dated March 13, 2014 adopted the translation of the Conceptual Framework for Financial Reporting and (the Conceptual Framework, adopted by the IASB in September 2010, which supplants the Framework for Preparation and Presentation of the Financial Statements) and basic texts of IAS and IFRS ( Decision on Adoption of the Translations of the Conceptual Framework for Financial Reporting and Basic Texts of International Accounting Standards and International Financial Reporting Standards, published the Official Gazette of the Republic of Serbia no. 35 on March 27, 2014 ( Decision on Adoption of the Translations ), encompassing amendments to IAS and new IFRS and related interpretations. Based on this Decision on Adoption of the Translations, the Conceptual Framework, IAS, IFRS, IFRIC and related interpretations that have been translated shall be applied to the financial statements prepared as of Standards and interpretations issued that came into effect in the current period pursuant to the Decision on Adoption of the Translations are disclosed in Note 2.2, while standards and interpretations in issue but not yet in effect are disclosed in Note 2.3. The accompanying consolidated financial statements are presented in the format prescribed under the Decision on the Forms and Contents of the Items in the Forms of the Financial Statements of Banks (Official Gazette of RS nos. 71/2014 and 135/2014). These consolidated financial statements were prepared at historical cost principle unless otherwise stipulated in the accounting policies presented hereunder. In the preparation of the accompanying consolidated financial statements, the Bank adhered to the accounting policies described in Note 3. The Bank s consolidated financial statements are stated in thousands of dinars (RSD). Dinar is the official reporting currency in the Republic of Serbia Standards and Interpretations Issued that Came into Effect in the Current Period Pursuant to the Decision on Adoption of the Translations of the Ministry Amendments to IFRS 7 Financial Instruments: Disclosures Amendments improving fair value and liquidity risk disclosures (revised in March 2009, effective for annual periods beginning on or after January 1, 2009); Amendments to IFRS 1 First-Time Adoption of IFRS Additional Exemptions for First-Time Adopters. The amendments relate to assets in oil and gas industry and determining whether an arrangement contains a lease (revised in July 2009, effective for annual periods beginning on or after January 1, 2010); Amendments to various standards and interpretations resulting from the Annual Quality Improvement Project of IFRS published on April 16, 2009 (IFRS 5, IFRS 8, IAS 1, IAS 7, IAS 17, IAS 36, IAS 39, IFRIC 16) primarily with a view to removing inconsistencies and clarifying wording, (amendments are to be applied for annual periods beginning on or after 1 January 2010, while the amendment to IFRIC is to become effective as of July 1, 2009); Amendments to IAS 38 Intangible Assets (revised in July 2009, effective for annual periods beginning on or after July 1, 2009); 8

11 BASIS OF PREPARATION AND PRESENTATION OF THE CONSOLIDATED FINANCIAL STATEMENTS (Continued) 2.2. Standards and Interpretations Issued that Came into Effect in the Current Period Pursuant to the Decision on Adoption of the Translations of the Ministry (Continued) Amendments to IFRS 2 Share-Based Payment : Amendments resulting from the Annual Quality Improvement Project of IFRS (revised in April 2009, effective for annual periods beginning on or after July 1, 2009) and amendments relating to group cash-settled share-based payment transactions (revised in June 2009, effective for annual periods beginning on or after January 1, 2010); Amendments IFRIC 9 Reassessment of Embedded Derivatives effective for annual periods beginning on or after July 1, 2009 and IAS 39 Financial Instruments: Recognition and Measurement Embedded Derivatives (effective for annual periods beginning on or after June 30, 2009); IFRIC 18 Transfers of Assets from Customers (effective for annual periods beginning on or after July 1, 2009); Conceptual Framework for Financial Reporting 2010 being amendments to Framework for the Preparation and Presentation of Financial Statements (effective for transfer of assets from customers received on or after September 2010); Amendments to IFRS 1 First-time Adoption of International Financial Reporting Standards Limited Exemption from Comparative IFRS 7 Disclosures for First-time Adopters (effective for annual periods beginning on or after July 1, 2010); Amendments to IAS 24 Related Party Disclosures Simplifying the disclosure requirements for government-related entities and clarifying the definition of a related party (effective for annual periods beginning on or after January 1, 2011); Amendments to IAS 32 Financial Instruments: Presentation Accounting for Rights Issues (effective for annual periods beginning on or after February 1, 2010); Amendments to various standards and interpretations Improvements to IFRSs (2010) resulting from the Annual quality improvement project of IFRS published on May 6, 2010 (IFRS 1, IFRS 3, IFRS 7, IAS 1, IAS 27, IAS 34, IFRIC 13) primarily with a view to removing inconsistencies and clarifying wording, (most amendments are to be applied for annual periods beginning on or after January 1, 2011); Amendments to IFRIC 14 IAS 19 The Limit on a Defined Benefit Asset, Minimum Funding Requirements and Their Interaction Prepayments of a Minimum Funding Requirement (effective for annual periods beginning on or after January 1, 2011); IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments (effective for annual periods beginning on or after July 1, 2010). Amendments to IFRS 1 First-Time Adoption of IFRS Severe Hyperinflation and Removal of Fixed Dates for First-time Adopters (effective for annual periods beginning on or after July 1, 2011); Amendments to IFRS 7 Financial Instruments: Disclosures Transfers of Financial Assets (effective for annual periods beginning on or after January 1, 2011); Amendments to IAS 12 Income Taxes Deferred Tax: Recovery of Underlying Assets (effective for annual periods beginning on or after January 1, 2012); IFRS 10 Consolidated Financial Statements (effective for annual periods beginning on or after January 1, 2013); 9

12 BASIS OF PREPARATION AND PRESENTATION OF THE CONSOLIDATED FINANCIAL STATEMENTS (Continued) 2.2. Standards and Interpretations Issued that Came into Effect in the Current Period Pursuant to the Decision on Adoption of the Translations of the Ministry (Continued) IFRS 11 Joint Arrangements (effective for annual periods beginning on or after January 1, 2013); IFRS 12 Disclosures of Involvement with Other Entities (effective for annual periods beginning on or after January 1, 2013); Amendments to IFRS 10, IFRS 11 and IFRS 12 Consolidated Financial Statements, Joint Arrangements and Disclosures of Involvement with Other Entities: Transition Guidance (effective for annual periods beginning on or after January 1, 2013); IAS 27 (revised in 2011) Separate Financial Statements (effective for annual periods beginning on or after January 1, 2013); IAS 28 (revised in 2011) Investments in Associates and Joint Ventures (effective for annual periods beginning on or after January 1, 2013); IFRS 13 Fair Value Measurement (effective for annual periods beginning on or after January 1, 2013); Amendments to IFRS 1 First-time Adoption of International Financial Reporting Standards Government Loans with a Below-Market Rate of Interest (effective for annual periods beginning on or after January 1, 2013); Amendments to IFRS 7 Financial Instruments: Disclosures Offsetting Financial Assets and Financial Liabilities (effective for annual periods beginning on or after January 1, 2013); Amendments to IAS 1 Presentation of Financial Statements Presentation of Items of Other Comprehensive Income (effective for annual periods beginning on or after July 1, 2012); Amendments to IAS 19 Employee Benefits Improvements to the Accounting for Post- Employment Benefits (effective for annual periods beginning on or after January 1, 2013); Amendments to various standards Improvements to IFRSs ( Cycle) issued in May 2012, resulting from the annual improvement project of IFRS (IFRS 1, IAS 1, IAS 16, IAS 32, IAS 34) primarily with a view to removing inconsistencies and clarifying wording (amendments are to be applied for annual periods beginning on or after January 1, 2013); IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine (effective for annual periods beginning on or after January 1, 2013); and Amendments to IAS 32 Financial Instruments: Presentation Offsetting Financial Assets and Financial Liabilities (effective for annual periods beginning on or after January 1, 2014) Standards and Interpretations in Issue not yet in Effect At the date of issuance of these consolidated financial statements the following standards, revisions and interpretations were in issue but not yet effective: IFRS 9 Financial Instruments and subsequent amendments, supplanting the requirements of IAS 39 Financial Instruments: Recognition and Measurement, with regard to classification and measurement of financial assets. This standard eliminates the categories existing under IAS 39 assets held to maturity, assets available for sale and loans and receivables. IFRS 9 shall be effective for annual periods beginning on or after January 1, 2018, with early adoption permitted. 10

13 BASIS OF PREPARATION AND PRESENTATION OF THE CONSOLIDATED FINANCIAL STATEMENTS (Continued) 2.3. Standards and Interpretations in Issue not yet in Effect (Continued) In accordance with IFRS 9, financial assets shall be classified in one of the following two categories upon initial recognition: financial assets at amortized cost or financial assets at fair value. A financial asset shall be measured at amortized cost if the following two criteria are met: financial assets relate to the business model whose objective is to collect the contractual cash flows and the contractual terms provide the basis for collection at certain future dates of cash flows that are solely payments of principal and interest on the principal outstanding. All other financial assets shall be measured at fair value. Gains and losses on the fair value measurement of financial assets shall be recognized in the profit and loss statement, except for investments in equity instruments which are not traded, where IFRS 9 allows at initial recognition a subsequently irreversible choice to recognize changes in fair value within other gains and losses in the statement of comprehensive income. An amount recognized in such a manner within the statement of comprehensive income cannot subsequently be recognized in profit and loss. Given the nature of the Bank s operations, the adoption of the standard is expected to have a significant impact on the Bank s consolidated financial statements. Amendments to IFRS 11 Joint Arrangements Accounting for Acquisition of an Interest in a Joint Operation (effective for annual periods beginning on or after January 1, 2016); IFRS 14 Regulatory Deferral Accounts (effective for annual periods beginning on or after January 1, 2016); IFRS 15 Revenue from Contracts with Customers, defining the framework for revenue recognition. IFRS 15 supplants IAS 18 Revenue, IAS 11 Construction Contracts, IFRIC 13 Customer Loyalty Programs, IFRIC 15 Agreements for the Construction of Real Estate and IFRIC 18 Transfers of Assets from Customers. IFRS 15 shall be effective for annual periods beginning on or after January 1, 2017, with early adoption permitted. Amendments to IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assets Clarification of Acceptable Methods of Depreciation and Amortization (effective for annual periods beginning on or after January 1, 2016 ); Amendments to IAS 16 Property, Plant and Equipment and IAS 41 Agriculture Agriculture: Bearer Plants (effective for annual periods beginning on or after January 1, 2016); IAS 27 Separate Financial Statements Equity Method in Separate Financial Statements (effective for annual periods beginning on or after January 1, 2016); Amendments to IFRS 10 Consolidated Financial Statements and IAS 28 Investments in Associates and Joint Ventures Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (effective for annual periods beginning on or after January 1, 2016 ); Amendments to IAS 19 Employee Benefits Defined Benefit Plans: Employee Contributions (effective for annual periods beginning on or after January 1, 2014); Amendments resulting from Annual Improvements Cycle issued in December 2013 (IFRS 2, IFRS 3, IFRS 8, IFRS 13, IAS 16, IAS 24 and IAS 38) with a view to removing inconsistencies and clarifying wording (effective for annual periods beginning on or after July 1, 2014); and Amendments resulting from Annual Improvements Cycle issued in December 2013 (IFRS 1, IFRS 3, IFRS 13 and IAS 40) with a view to removing inconsistencies and clarifying wording (effective for annual periods beginning on or after July 1, 2014). 11

14 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES 3.1. Interest Income and Expenses Interest income and expenses are recognized in the income statement for all interest-bearing financial instruments following the effective interest method. Interest income and expenses are recorded in the Bank s income statement in the period to which they belong by applying the matching principle and following the requirements delineated in the agreement signed between a customer and the Bank. Loan origination fees are credited to profit and loss account as interest income, i.e., as the adjustment to the effective return on loans disbursed proportionately to the outstanding loan maturities. Interest accrued is recorded within the income statements when there is no doubt as to its collectability in accordance with IAS 18 and the Guidance for Recognition Interest Income and Manner of Interest Recognition after Unwinding, which is an integral part of the Bank's Accounting Policies. Up to 2014, in accordance with the Rules on the Layout of Chart of Accounts and Content of Accounts in the Chart of Accounts for Banks (Official Gazette of RS, nos. 98/2007, 57/2008 and 3/2009), the Bank suspended interest, i.e., discontinued adding interest to assets with certain degree of recoverability. Interest suspension was performed in the manner and via account prescribed by the aforecited Rules, while the collection of suspended interest was recorded in the income accounts under the aforecited Rules. In 2014 the Bank no longer suspended interest. Interest income from performing and risk-free loans whose collection is certain is fully recognized. Interest income from the borrowers/loans subject to individual impairment assessment is recognized in accordance with IAS 39. When a financial asset or a group of similar financial assets is written off due to impairment loss, the related interest income is recognized from then on using the interest rate applied in discounting the future cash flows for the purpose of measuring the impairment loss. For borrowers/loans subject to group or collective impairment assessment, interest income is recognized in proportion to the net value of the loan. The Bank's management is of the opinion that this change to the accounting policy of interest income has no material effect on the prior years' consolidated financial statements of the Bank Fee and Commission Income and Expenses Fee and commission income and expenses from banking services (payment transactions, issuance of guaranties and other sureties, letters of credit, purchase and sale of foreign currencies and other banking services) when such services are invoiced and rendered. Fees and commission charged for guarantees, sureties and letters of credit issued are deferred and recognized as income proportionately over their maturity periods. The Bank recognizes fee and commission income that is part of the effective interest as interest income Foreign Exchange Translation Assets and liabilities denominated in foreign currencies at the balance sheet date are translated into dinars at official middle exchange rates of the National Bank of Serbia effective as at the reporting date. Gains or losses arising on the translation of receivables and payables are credited or charged to income statement. Transactions denominated in foreign currencies are translated into dinars at official exchange rates effective at the date of each transaction. Net foreign exchange positive or negative effects arising upon the translation of transactions, and the assets and liabilities denominated in foreign currencies are credited or charged to the income statement as foreign exchange gains or losses. Commitment and contingent liabilities in foreign currencies are translated into dinars at official middle exchange rates of the National Bank of Serbia effective as at the reporting date. 12

15 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) 3.3. Foreign Exchange Translation (Continued) The exchange rates for major currencies used in the translation of balance sheet components into dinars were as follows: Currency Official middle exchange rate at 2014 Official middle exchange rate at 2013 USD CHF EUR impairment of Financial Assets and Credit risk-weighted Off-Balance Sheet Items The bank makes impairment allowance for loans and other financial assets as well as credit riskweighted off-balance sheet items when recoverability thereof is no longer certain as well as when there is a probability of incurring losses per credit risk-weighted off-balance sheet items. Impairment allowance is made under the Bank's Accounting Policy adopted in accordance with IAS 39 and defined in the Procedure for Assessing Impairment of Balance Sheet Assets and Probable Losses per Off-Balance Sheet Items in accordance with IFRS/IAS Cash and Cash Funds Held with the Central Bank Cash and cash funds held with the central bank include cash on hand in local and in foreign currencies, balances on the current accounts with the National Bank of Serbia, including the obligatory RSD and foreign currency reserves, gold and other precious metals as well as funds on current accounts held with other domestic and foreign banks in local and in foreign currencies (Note 17). Cash equivalents comprise gold and other precious metals initially measured at cost and subsequently carried at their market value. The market value is determined based on the price of precious metals quoted on the world market. The increase in the market value is recognized as income while the decrease is included in expenses on the income statement Financial Instruments Loans and Receivables Loans and receivables are non-derivative financial assets with fixed or determinable payment that are not quoted on an active market. Loans originated by the Bank are recognized within the balance sheet upon the transfer of loan funds to the borrower. Loans are initially recorded at the price representing the market value of the cash funds disbursed as loans, including all transaction costs; loans are subsequently measured at amortized cost using effective interest method. The Bank makes impairment allowance for those loans that are no longer recoverable in accordance with the Procedure for Assessing Impairment of Balance Sheet Assets and Probable Losses per Off-Balance Sheet Items in accordance with IFRS/IAS. In its loan portfolio the Bank has loans agreed upon with a number of borrowers with contractually defined currency clause as a risk hedge. Income arising from currency clause effects is recorded within the income statement under net foreign gains and positive currency clause effects (Note 9). Currency clause is a derivative which is not recorded separately from its host contract given that the economic benefits and risks of the embedded derivative closely related to the host contract. In its loan portfolio the Bank has loans linked to the consumer price index (officially published), which were contracted and approved in prior periods. Income and expenses arising therefrom are recorded as gains and losses on risk hedges (Note 7). Contractual loan link to the consumer price index represents embedded derivatives which are closely related to the host contracts yet recorded separately from those host contracts. 13

16 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) 3.6. Financial Instruments (Continued) Impairment Allowance of Balance Sheet Assets and Provisions for Losses per Off-Balance Sheet Items Impairment allowance of balance sheet assets and provisions for losses per off-balance sheet items are made based on the estimate of the impairment of balance sheet assets and probable losses per offbalance sheet items in accordance with IFRS/IAS as part of the Bank's accounting policies adopted based on IAS 39. Impairment allowance of balance sheet assets is recorded within assets on the impairment allowance accounts in the income statements while provisions for losses per off-balance sheet items are recorded on the accounts prescribed for this purpose by NBS, within liabilities Securities and Financial Assets Carried at Fair value through Profit and Loss (Trading Assets) Trading securities comprise those securities held by the Bank for the purpose of their sale with the objective of generating a profit from short-term fluctuations in their market prices. The Bank uses the settlement date calculation upon recording transactions of purchasing securities held for trading. Transaction costs are not included in the value thereof but presented within the expenses of the period. Any unrealized gains and losses arising from changes in the market value of such assets are recognized as from the transaction origination date (trade date) in the profit and loss statement. Following the trading date, when the transaction is settled (settlement date), the resulting financial assets shall be recognized within the balance sheet at market value of the consideration paid for acquisition of securities increased by the changes in the market value of the contract arisen since the trading date. Market value is determined based on the valuation techniques, fair value hierarchies and inputs of the certain fair value hierarchy levels in accordance with the provisions of the relevant IFRS/IAS. All realized and unrealized gains and losses arising from changes in the market value of trading securities are recognized in the income statement as gains and losses on the financial assets held for trading (Note 6). As of 2014 the Bank had only derivatives held for trading in its portfolio (Note 18) Securities and Other Financial Assets Held to Maturity Securities and other financial assets held to maturity are financial assets with fixed maturities that the Bank intends to hold up to their maturity dates. Securities held to maturity are stated at their amortized cost using the effective interest method net of accumulated impairment. The amortized cost is calculated taking into account all discounts or premiums earned upon the purchase over the maturity period. Interest accrued as of the balance sheet date is credited to income in the profit and loss account. Changes in the fair value of these securities are also included in the profit and loss under gains or losses on the valuation of securities. This category of securities includes bills of exchange received for discounting and commercial papers (Note 20) Securities and Other Financial Assets Available for Sale Securities and other financial assets available for sale are non-derivative financial assets designated as available for sale (AFS) and are not classified as: loans and receivables, investments held to maturity or financial assets ate fair value through profit and loss. AFS financial assets represent financial instruments intended to be held for and indefinite period, which can nevertheless be sold for liquidity maintenance or due to changes in interest rates, foreign exchange rates or equity prices. 14

17 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) 3.6. Financial Instruments (Continued) Securities and Other Financial Assets Available for Sale (Continued) Securities available for sale are measured at market value. Market value is determined based on the valuation techniques, fair value hierarchies and inputs of the certain fair value hierarchy levels in accordance with the provisions of the relevant IFRS/IAS. Unrealized gains and losses arising from changes in the market value of available-for sale investments are stated as reserves within equity until such a financial asset is sold, collected or otherwise disposed of or until it is determined to have suffered impairment. Upon sales or permanent impairment of these securities adequate amounts of previously formed revaluation reserves are stated in the income statement as net gains or losses on securities Equity Investments Equity investments represent long-term financial investments in other legal entities equity, without any intention of their sale in the near future. All investments are initially recorded at their nominal value. Equity investments are recorded in the Bank s financial statements using the historical cost method Intangible Assets, Property, Plant and Equipment The Bank s property, plant and equipment and intangible assets are recognized at cost (historical cost) less any accumulated depreciation and amortization and impairment. Depreciation and amortization are calculated on a straight-line basis at the following annual rates in order to write off the cost of assets over their estimated useful lives: Buildings 1% 6.59% Computers 20% Calculators, typewriters and money handling machines 15.5% Passenger vehicles 15.5% Communications equipment 10% Heating equipment 16.5% Copying equipment 14.3% Furniture 12,5% IT equipment 10 20% Mobile phones 33.33% Other equipment 11% In accordance with the relevant Leasehold improvements lease agreement terms Property, plant and equipment are periodically reviewed in order to determine indicators of impairment, if any Investment Property The Bank s investment property is property held to earn rental income and/or for capital appreciation. An investment property is measured at fair value which accounts for all movements in the market value and is recorded in the income statement. The Bank's investment property is not depreciated. 15

18 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) 3.9. Non-Current Assets Held for Sale Non-current assets held for sale are the assets classified upon acquisition as non-current, which the Bank decided to dispose of after a certain period of use. Upon the reclassification of a portion of assets into non-current assets held for sale, assets are measured at the lower of their carrying value and fair value less costs to sell. In the first case, the asset is stated at its carrying value whereas in the latter case, revaluation surplus accrued for that particular asset is reversed, and the amount in excess of such surplus is charged to expenses of the given period as impairment of assets. Impairment losses are transferred to losses on the sale in case such asset is reclassified into the category of assets held for sale and sold in the same year. In case of reclassification from investment property carried at fair value the rules of measurement need not be applied. In order to reclassify and asset from investment property to non-current assets held for sale, not only a relevant decision on the sale is to be made but also the capital expenditure of reclassification of such an asset. Depreciation of non-current assets held for sale is not calculated. Sales of such assets are recorded as net sales. The remaining assets classified in this category meet the requirements prescribed by IFRS 5 for continued recognition of non-current assets held for sale and are available for sale (Note 30) Assets Held for Sale Equity Tangible assets received in lieu of debt collection, as well as property from joint ventures are classified as assets held for sale and presented within the line item of inventories. Assets held for sale are measured at the lower of cost and at fair value less costs to sell. These assets are not depreciated as long as they are classified as tangible assets received in lieu of debt collection in the above described manner. The Bank's equity is comprised of: issued capital, share issue premium, reserves and retained earnings/ accumulated losses. Issued Capital The Bank's share capital is formed from the monetary contributions made by the Bank's founders. For funds invested, shareholders receive a proportionate number of shares or receipts as defined in the Law on the Capital Market (Official Gazette of RS no. 31/11). Shareholders cannot withdraw funds invested in the Bank s share capital. The Bank uses capital to perform banking operations and cover operating risks. Revaluation Reserves The surplus determined in the revaluation of property and equipment is credited to revaluation reserves. If a previously revalued asset with positive revaluation effects credited to revaluation reserves is sold or disposed of, the respective revaluation surplus credited to revaluation reserves is transferred to retained earnings (Note 40). Where the fair value of property decreases because the asset s market value is below its carrying value, revaluation surplus arising from that particular asset is reversed accordingly to the extent of the previously formed revaluation reserves. Unrealized gains and losses arising from remeasurement of securities available for sale to their market value are recorded as reserves within equity (Note 40). The structure of and changes in the Bank's equity are disclosed in Note

19 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Borrowings and Due Deposits Liabilities arising from borrowings and due deposits are recognized within the balance sheet when the respective funds are deposited. Upon initial recognition, borrowings and deposits are measured at fair value increased by transaction costs which may be added to the respective deposits or presented as separate financial liabilities. Subsequent to initial recognition, liabilities arising from borrowings and deposits due are measured at amortized cost by applying the effective interest method. Foreign currency deposits are stated in RSD as translated by applying the middle exchange rates effective as of the balance sheet date Managed Funds The Bank manages funds on behalf of and for the account of third parties and charges fees for these services. These items are not included in the Bank s balance sheet and are presented within off-balance sheet items (Note 41) Employee Benefits The Bank does not have defined benefit plans or share-based remuneration options and there were no identified liabilities thereof as of The Bank calculated future retirement benefits in accordance with IAS 19, based on the assumptions made in accordance with the provisions of the aforesaid standard. As of 2014, the Bank increased provisions in comparison to Taxes and Contributions Current Income Tax The Bank does not perform tax consolidation. With regard thereto, disclosures of income taxes are made separately for the Bank and its subsidiary. Current income tax represents an amount that is calculated by applying the prescribed income tax rate of 15% to the taxable base stated in the income tax return, which includes the profit shown in the statutory statement of income, as adjusted for certain permanent and temporary differences that are specifically defined under statutory tax rules of the Republic of Serbia. Current income tax is calculated and paid in accordance with the Corporate Income Tax Law and other relevant fiscal regulations prevailing in the Republic of Serbia. The monthly advance income tax payment is paid on monthly basis while the adjustment of the sum of advance payments is made at the year-end, i.e. upon submission of the tax balance and the annual income tax return to the tax authorities for advance and final determination of the corporate income tax Deferred Income Taxes Deferred income taxes are provided for temporary differences arising between the tax bases of assets and liabilities and their carrying values in the Bank's consolidated financial statements in accordance with IAS 12. Deferred tax liabilities are recognized for all taxable temporary differences as at the balance sheet date between the tax bases of assets and liabilities and their carrying values used for financial reporting purposes, which will result in taxable amounts in the future periods. Deferred tax assets are income tax amounts recoverable in the future periods which pertain to all deductible temporary differences and all unused tax credits and losses available for carryforward. Deferred tax assets and liabilities are determined at the tax rate expected to be applied in the period of the relevant asset realization/liability settlement, based on the currently enacted or tax rates expected to be enacted up to the balance sheet date. As at 2014, deferred tax assets and liabilities were provided at the rate of 15%. 17

20 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Taxes and Contributions (Continued) Deferred Income Taxes (Continued) In 2014 the Bank recognized deferred tax assets based on the temporary differences between the base of calculation tax-purpose and financial reporting depreciation and amortization of fixed assets, provisions for retirement benefits calculated in accordance with IAS 19, impairment of assets and unpaid public duties payable. The Bank did not recognize deferred tax assets based on the stated tax losses and unused tax credit in accordance with IAS 12, paragraph Indirect Taxes and Contributions Indirect taxes and contributions include property taxes, value added tax, payroll taxes and contributions and various other taxes and contributions paid pursuant to effective republic and local tax regulations. These taxes and contributions are included within operating expenses and staff costs. VAT may be presented within certain balance sheet items if related to procurements that do not represent expenses but certain balance sheet items according to IAS Financial Derivatives The Bank recognizes financial derivatives at their contractually defined value (cost) within off-balance sheet items, which represents the fair value of consideration received or receivable where any fair value adjustment as of the balance sheet date is recorded in the balance sheet and in the income statement Fair Value The Bank applies provisions of IFRS 13 to determine the fair values of items that are measured at fair value according to its adopted accounting policy. It is the policy of the Bank to disclose the fair value information on those financial assets and financial liabilities for which published market information is readily and reliably available, and whose fair value is materially different from their recorded amounts. The Bank records loans at their fair values as the terms at which the Bank extends loans are reconciled with the market prices through the variable interest rates. As per the Bank s management, amounts expressed in the consolidated financial statements reflect the fair value which is most reliable and useful for the needs of the financial reporting in accordance with the International Financial Reporting Standards as per the Law on Accounting of the Republic of Serbia and regulations of the National Bank of Serbia governing financial reporting of banks Loan Adjustment to Market Prices The Bank agrees with retail customers on either fixed or variable interest rates. Where a variable interest rate is agreed in a relevant contract clause, it is subject to reconciliation with variable interest rate elements which are officially published (key policy rate, consumer price index, etc.). In case such an element changes, an annex to the agreement regulating the interest rate change is not signed. Instead, before the changed interest rate is applied, the Bank will inform the customer in writing, or using any other permanent data carrier, of the changed interest rate, stipulating the date when the changed interest rate will come in effect along with a new loan repayment schedule. More detailed terms for the change of interest rate are determined in individual loan agreements. This manner of reconciliations is in accordance with the Law on the Protection of Users of Financial Services. The Bank agrees on variable interest rate with corporate customers, which rate is reconciled with the movements in the key policy rate and amendments to the General Business Terms and formal documents of the Bank determining the product and service prices. 18

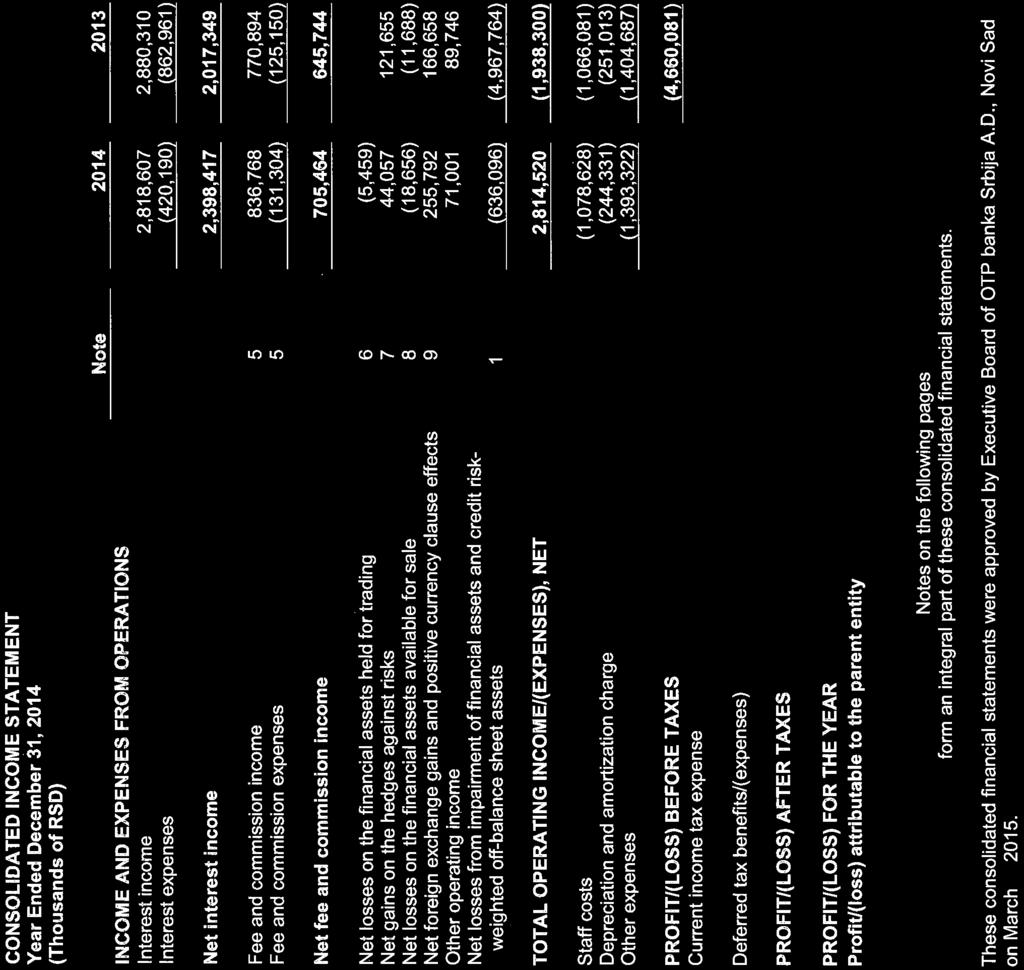

21 INTEREST INCOME AND EXPENSES Year Ended Interest income arising from: Loans 2,512,047 2,487,657 Deposits 65,179 93,258 Securities 234, ,595 Other investments 6,744 63,800 Total interest income 2,818,607 2,880,310 Interest expenses arising from: Loans (52,206) (289,627) Deposits (366,348) (571,698) Other investments (1,636) (1,636) Total interest expenses (420,190) (862,961) Net interest income for the year 2,398,417 2,017,349 Interest expenses from other investments of RSD 1,636 thousand related to dividends per cumulative preference shares calculated for the year FEE AND COMMISSION INCOME AND EXPENSES Year Ended Fee and commission income Loan origination fees 7,015 12,149 Payment card transaction fees 234, ,836 Payment transaction fees 266, ,644 Electronic banking fees 19,256 18,226 Other fees and commissions 309, ,039 Total fee and commission income 836, ,894 Fee and commission expenses Other financial liabilities (1,222) (10,311) Payment card transaction fees (86,385) (71,313) Other fees and commissions (28,791) (29,607) Loan origination fees (14,906) (13,919) Total fee and commission expenses (131,304) (125,150) Net fee and commission income for the year 705, , NET LOSS ON THE FINANCIAL ASSETS HELD FOR TRADING Year Ended 2014 Gains on the fair value changes of derivatives held for trading 57,349 - Losses on the fair value changes of derivatives held for trading (62,808) - Net loss on the financial assets held for trading for the year (5,459) - As from November 1, 2014, the Bank started classifying swap transactions as derivatives held for trading. 19

22 NET GAINS ON THE HEDGES AGAINST RISKS Year Ended Gains on the valuation of loans and receivables changes in retail prices 184 1,048 Gains on the valuation of loans and receivables gains on changes in the value of gold and other precious metals 2,831 - Gains on the valuation of derivatives designated for risk hedging interest rate swap 200, ,970 Losses on the valuation of loans and receivables changes in retail prices (30) (561) Losses on the valuation of loans and receivables gains on changes in the value of gold and other precious metals (7) (6,475) Losses on the valuation of derivatives designated for risk hedging interest rate swap (159,475) (203,327) Net gains on the hedges against risks for the year 44, , NET LOSSES ON THE FINANCIAL ASSETS AVAILABLE FOR SALE Year Ended Gains on the sale of securities and other financial assets available for sale Losses on the sale of securities and other financial assets available for sale (18,656) (12,547) Net losses on the financial assets available for sale for the year (18,656) (11,688) 9. NET FOREIGN EXCHANGE GAINS AND POSITIVE CURRENCY CLAUSE EFFECTS Year Ended Foreign exchange gains Unrealized foreign exchange gains 1,119,178 2,244,021 Realized foreign exchange gains 277, ,373 On valuation of loans, receivables and liabilities 987, ,671 Total foreign exchange gains 2,384,263 3,478,065 Foreign exchange losses Unrealized foreign exchange losses (1,671,821) (2,295,762) Realized foreign exchange losses (136,492) (113,138) On valuation of loans, receivables and liabilities (320,158) (902,507) Total foreign exchange losses (2,128,471) (3,311,407) Net foreign exchange gains and positive currency clause effects for the year 255, ,658 20

23 OTHER OPERATING INCOME Year Ended Gains on the sale of other loans and receivables 2,974 4,264 Other income from operations 11,665 12,448 Reversal of unreleased provisions for liabilities 73 27,584 Gains on the sale of property, plant, equipment and intangible assets 3,483 6,913 Write-off of liabilities 2,356 10,872 Dividend income and income from equity investments Surpluses 2,502 1,458 Payment card operations 19,210 - Other income 27,985 25,638 Total other operating income for the year 71,001 89, NET LOSSES FROM IMPAIRMENT OF FINANCIAL ASSETS AND CREDIT RISK-WEIGHTED OFF-BALANCE SHEET ITEMS Year Ended Impairment losses on loans and receivables included in the balance sheet (1,767,488) (6,456,235) Provisions for off-balance sheet items (58,286) (58,033) Write-off of irrecoverable receivables (6,797) (19,104) (1,832,571) (6,533,372) Reversal of impairment losses on loans and receivables included in the balance sheet 1,154,728 1,538,674 Reversal of provisions for off-balance sheet items 38,837 26,386 Collected receivables previously written off 2, ,196,475 1,565,608 Net losses from impairment of financial assets and credit risk-weighted off-balance sheet items for the year (636,096) (4,967,764) 12. STAFF COSTS Year Ended Net salaries 792, ,696 Net benefits 8,434 3,466 Taxes on salaries and benefits 82,898 89,056 Contributions to salaries and benefits 161, ,112 Temporary and seasonal employees 1,435 3,048 Other staff costs 26,487 13,828 Provisions for retirement and other employee benefits 4,863 2,875 Total staff costs for the year 1,078,628 1,066,081 Other staff costs in 2014 mostly relate to the remunerations paid to the members of the Board of Directors in the amount of RSD 8,518 thousand. Expenses in respect of provisions for retirement benefits amounted to RSD 3,367 thousand. Other provisions for employee benefits relate to short-term provisions for unused annual leave (vacation) benefits. 21

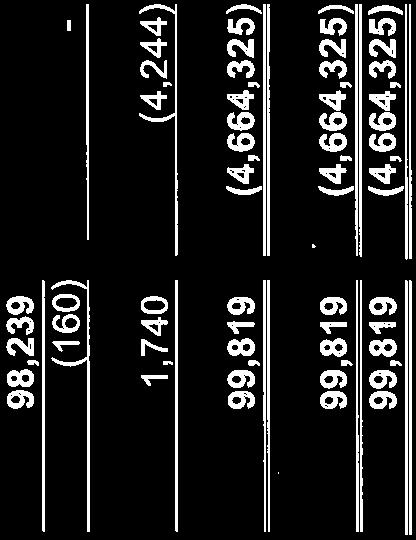

24 DEPRECIATION AND AMORTIZATION CHARGE Year Ended Depreciation charge property owned by the Bank 15,837 15,899 Depreciation charge leasehold improvements 24,046 21,287 Amortization charge intangible assets 60,303 67,552 Depreciation charge computer equipment 44,821 44,919 Depreciation charge office equipment and devices 25,792 22,509 Depreciation charge other equipment 73,532 78,840 Depreciation charge equipment acquired under finance lease - 7 Total depreciation and amortization charge for the year 244, , OTHER EXPENSES Year Ended Losses on the sale of other loans and receivables - 20,676 Cost of materials 98, ,761 Cost of production services 470, ,293 Non-material costs 483, ,385 Taxes payable 56,315 74,127 Contributions payable 167, ,337 Other costs and charges 63,593 30,579 Provisions for liabilities 17,258 26,386 Losses on the sale of property, plant, equipment and intangible assets 1,642 1,955 Losses on the disposal and write-off of property, plant, equipment and intangible assets 3, Shortages and damages 1,096 5,046 Other expenses 28,773 67,734 Total other expenses for the year 1,393,322 1,404, INCOME TAXES 1 CURRENT INCOME TAX Year Ended Current income tax expense Total current income tax expense as at December INCOME TAXES 2 DEFERRED TAX ASSETS/(LIABILITIES) AND TAX BENEFITS/(EXPENSES) a) Movements on Deferred Tax Assets/(Liabilities) at the reporting date the Bank stated deferred tax assets as totaling RSD 7,264 thousand. Movements on deferred tax assets are presented in the table below: Year Ended Balance of deferred tax assets/liabilities as at January 1 5,524 9,768 Effect of the temporary tax differences credited/(charged) to the income statement 1,740 (4,244) Other - - Balance of deferred tax assets as at December 31 7,264 5,524 22

25 INCOME TAXES 2 DEFERRED TAX ASSETS/(LIABILITIES) AND TAX BENEFITS/(EXPENSES) (Continued) a) Movements on Deferred Tax Assets/(Liabilities) (Continued) As of 2014 the Bank recognized deferred tax assets in the amount of RSD 7,264 thousand ( 2013: RSD 5,524 thousand), on various grounds. Namely, deferred tax assets were recognized based on the temporary difference between depreciation and amortization recognized for accounting and for tax purposes of RSD 3,046 thousand, provisions made for employee retirement benefits in accordance with IAS 19 of RSD 1,637 thousand, based on unpaid public duties of RSD 745 thousand, and deductible temporary differences in allowances for impairment losses of RSD 1,836 thousand. b) Numerical Reconciliation between Total Tax Expense Stated in the Income Statement and the Product of the Accounting Results Multiplied by the Applicable Tax Rate Year Ended Bank s profit/(loss) before taxes 105,799 (4,652,365) Income tax at the statutory tax rate of 15% 15,870 (697,855) (Prior years loss as per tax balance up to the amount of taxable profit) / Unrecognized tax losses (17,756) 548,624 Effects of the expenses not recognized within the tax balance 1, ,231 Deferred tax benefit/(expense) 1,740 (4,244) Total tax benefit/(expense) 1,740 (4,244) Effective tax rate 1.64% 0.09% c) Gains/(losses) on the Created Deferred Tax Assets Year Ended Gains on the created deferred tax assets and decrease in deferred tax liabilities 1,740 (4,244) Gains on the created deferred tax assets and decrease in deferred tax liabilities as at December 31 1,740 (4,244) 23

26 INCOME TAXES 2 DEFERRED TAX ASSETS/(LIABILITIES) AND TAX BENEFITS/(EXPENSES) (Continued) d) Income Tax Benefit/(Expense) Year Ended Accounting profit/(loss) before taxes 105,799 (4,652,365) Expenses not recognized for tax purposes permanent differences 12, ,871 Taxable income 118,375 (3,657,494) Capital gains/(losses) 2,046 (20,274) Taxable base - - Tax rate 15% 15% Calculated income tax - - Current income tax expense - - Loss decrease by created deferred tax assets 1,740 (4,244) Total tax benefit/(expense) 1,740 (4,244) Net profit 107,539 (4,656,609) Current income tax expense - - Deferred income tax benefit 1,740 (4,244) 1,740 (4,244) 17. CASH AND CASH FUNDS HELD WITH THE CENTRAL BANK In RSD Cash funds in RSD 2,824,806 2,406,203 Cash on hand in RSD 511, ,661 Total cash funds in RSD 3,336,019 2,964,864 In foreign currencies Cash on hand in foreign currencies 266, ,669 Other monetary items in foreign currencies 20,987 12,948 Obligatory foreign currency reserve held with NBS 2,534,058 2,588,792 Total cash funds in foreign currencies 2,821,103 2,857,409 Gold and other precious metals 18,424 15,601 Total cash and cash funds held with the central bank, balance as at December 31 6,175,546 5,837,874 The Bank s obligatory RSD reserve represents the minimum RSD reserve set aside in accordance with the NBS Decision on Required Reserves of Banks with the National Bank of Serbia (Official Gazette of RS, nos. 3/11, 31/12, 57/12, 78/12, 87/12, 107/12, 62/13, 125/14 and 135/14). Pursuant to the aforesaid Decision, the obligatory reserve is to be calculated at the rate of 5% on the portion of the RSD base comprised of liabilities maturing within 2 years, i.e. within 730 days, and at the rate of 0% on the portion of the dinar base comprised of liabilities with maturities of over 2 years, i.e. over 730 days. The RSD base for the calculation of the obligatory reserve is the amount of average daily balance of RSD liabilities during the preceding calendar month, except RSD liabilities indexed to a currency clause as follows: - non-indexed liabilities arising from RSD deposits, loans, securities and other RSD liabilities to domestic legal entities and retail bank clients; - non-indexed liabilities arising from RSD deposits, loans and other RSD liabilities to foreign creditors. 24

27 CASH AND CASH FUNDS HELD WITH THE CENTRAL BANK (Continued) A portion of the obligatory foreign currency reserve was converted into obligatory RSD reserve at the rates of 36% and 28% for the obligatory reserves of up to and over 2 years, respectively. The obligatory RSD reserve balance that had to be maintained from December 18, 2014 to January 17, 2015 amounted to RSD 1,892,528 thousand, where the calculated RSD portion of the reserve amounted to RSD 471,166 thousand, and the RSD equivalent of the reserve portion calculated in EUR and deposited in RSD amounted to RSD 1,421,362 thousand. The Bank is under obligation to calculate and maintain the average daily balance of the allocated obligatory RSD reserve on its gyro account over the accounting period. The calculated obligatory RSD reserve is deposited in RSD on the Bank's gyro account. As at 2014 the Bank was in full compliance with the regulations of the National Bank of Serbia with regard to the calculation and allocation of the obligatory RSD reserve. The obligatory foreign currency reserve represents the minimum foreign currency reserve set aside in accordance with the NBS Decision on Required Reserves of Banks with the National Bank of Serbia (Official Gazette of RS nos. 3/11, 31/12, 57/12, 78/12, 87/12, 107/12, 62/13, 125/14 and 135/14) which prescribes that banks calculate the obligatory foreign currency reserve at the following rates: - 27% on the portion of the foreign currency reserve comprised of liabilities maturing within 2 years, i.e. up to 730 days, and exceptionally at the rate of 50% on the portion of the foreign currency reserve comprised of RSD liabilities indexed to a currency clause maturing within 2 years, i.e. up to 730 days; - 20% on the portion of the foreign currency reserve comprised of liabilities with maturities of over 2 years, i.e. over 730 days, and exceptionally at the rate of 50% on the portion of the foreign currency reserve comprised of RSD liabilities indexed to a currency clause with maturities of over 2 years, i.e. over 730 days. The foreign currency base for the calculation of required reserve is the amount of average daily balance of foreign currency liabilities during the preceding calendar month and the amount of average daily balance of RSD liabilities from the preceding calendar month indexed to a currency clause as follows: - liabilities arising from deposits, loans, securities and other foreign currency liabilities to foreign creditors; - liabilities arising from deposits, loans, securities and other foreign currency liabilities to domestic legal entities and other liabilities; - foreign currency savings deposits with other banks; - indexed liabilities arising from deposits, loans, securities and other RSD liabilities as well as indexed RSD deposits received through transactions the Bank performs on behalf of and for the account of third parties if they exceed the amounts of loans the Bank disbursed from these deposits. The Bank deposits the obligatory foreign currency reserve onto the foreign currency account with the National Bank of Serbia. As at 2014 the Bank was in full compliance with the regulations of the National Bank of Serbia with regard to the calculation and allocation of the obligatory foreign currency reserve. Based on the Decision on the Conditions and Manner of Implementing Open Market Operations (Official Gazette of RS, nos. 45/2011 and 34/2013), the Bank conducts repurchase transactions with the National Bank of Serbia. The subject of repo transactions are commercial papers issued by the NBS. The NBS has the obligation to repurchase commercial papers before their maturity. As of 2014 the Bank had no contracted repo transactions; however, during 2014 the Bank had a significant turnover per repo transactions totaling RSD 41 billion. Total income from interest accrued per repo transactions in 2014 amounted to RSD 52,825 thousand. In 2014 the Bank had a larger volume of contracted loans based on repurchase transactions in foreign currencies with OTP Bank Ltd. Budapest as compared to the previous year in the amount of RSD 1,291,800 thousand. 25

28 FINANCIAL ASSETS AT FAIR VALUE THROUGH PROFIT AND LOSS HELD FOR TRADING Receivables per derivatives held for trading currency swap 1,732 - Total financial assets at fair value through profit and loss held for trading as at December 31 1,732 - The Bank had no securities held for trading in its portfolio. This line item comprises derivatives held for trading. 19. FINANCIAL ASSETS AVAILABLE FOR SALE Face value 4,531,998 2,736,488 Departures from the face value (78,187) (83,909) Impairment allowance (489,590) (509,315) Total financial assets available for sale, net as at December 31 3,964,221 2,143, Investments in financial assets available for sale Shares of insurance companies - reclassified Shares of other financial institutions 2,243 2,243 Shares of holding companies 121, ,670 Shares of other companies 97, ,471 Shares of other companies - reclassified - 3 Treasury bills and public sector bonds 3,953,859 2,132,769 Shares of other customers 278, ,215 Shares of other customers - reclassified Securities available for sale 4,453,811 2,652,578 Faxe value of securities available for sale 4,531,998 2,736,488 Departures from the face value (78,187) (83,910) Impairment allowance (489,590) (509,314) Securities available for sale, net as at December 31 3,964,221 2,143,264 Increase in securities available for sale was due to the purchases of Treasury bills and bonds of the Republic of Serbia. As at 2014 the Bank had Treasury bills and bonds of the Republic of Serbia totaling RSD 4,012,480 thousand in its portfolio. Treasury bills and bonds of the Republic of Serbia were classified as securities available for sale. The following table shows the breakdown of Treasury bills per maturity: Maturity Book value Interest accrued up to maturity Short-term T-bills 1,502,600 (22,734) Long-term T-bills 2,054,880 (69,298) Long-term bonds 455,000 32,750 Total as at December 31 4,012,480 (59,282) As at 2014 the Bank determined the fair value of Treasury bills in accordance with the provisions of IFRS

29 FINANCIAL ASSETS AVAILABLE FOR SALE (Continued) Investments in financial assets available for sale (Continued) Upon determining the fair value of the Treasury bills the Bank used valuation techniques which it deemed appropriate under the circumstances and for which it had sufficient data available for fair value measurement, with the maximum use of observable inputs and an effort to minimize the use of unobservable input data. Regarding the aforesaid, the Bank decided on the use of combined market and income approaches and estimated the fair value based on hierarchy Level 2 inputs. Fair values were determined based on: prices available at the principal/secondary market in the observation period which is deemed relevant for trading these securities (a period of two weeks); based on prices offered for specific maturities. Based on the fair value estimate, it was determined that the value of Treasury bills as at 2014 was impaired by RSD 661 thousand and that it amounted to RSD 3,953,859 thousand. 20. FINANCIAL ASSETS HELD TO MATURITY Face value 73,173 51,237 Departures from the face value (86) 241 Impairment allowance (51,478) (51,478) Total financial assets held to maturity, net as at December 31 21, LOANS AND RECEIVABLES DUE FROM BANKS AND OTHER FINANCIAL INSTITUTIONS Loans per transaction accounts - 63,614 Overnight loans 1,250,312 - Other RSD loans 123, Other loans Interest and fees per deposits and off-balance sheet items Net Bank s RSD loans and receivables 1,374,884 64,867 Foreign currency accounts 86, ,003 Loans per foreign currency repo transactions 1,493,248 - Other foreign currency loans 345, ,455 Other general foreign currency deposits 53, ,570 Earmarked foreign currency deposits received in accordance with the regulations 4,838 4,586 Other earmarked foreign currency deposits 8,467 - Other foreign currency receivables 1,721 1,666 Interest and fees per deposits and off-balance sheet items Net Bank s FX loans and receivables 1,993, ,420 Impairment allowance (345,169) (288,487) Total Bank s loans and receivables, net as at December 31 3,022, ,800 27

30 LOANS AND RECEIVABLES DUE FROM CUSTOMERS Loans and receivables due from customers breakdown per product Loans per transaction accounts 973,906 1,118,867 Consumer loans 79, ,373 RSD loans for liquidity maintenance and working capital 12,357,790 7,787,837 RSD export loans 51,488 51,488 Investment loans 3,538,180 3,386,331 Housing loans 4,535,222 4,303,909 Cash loans 6,924,341 6,040,263 Other RSD loans 7,660,840 9,186,471 Receivables from factoring with the right to recourse 2,903 14,958 Receivables for acceptances, bills of exchange and payments per guarantees called on 961, ,283 Other loans and receivables 19,095 22,526 Interest and fees per deposits and off-balance sheet items 89,040 56,350 Net Bank s RSD loans and receivables 37,193,260 33,041,656 Foreign currency cheques Foreign currency loans for payment of imported goods and services 227, ,195 Other foreign currency loans 80,902 77,072 Other foreign currency earmarked deposits 109,411 91,441 Other foreign currency loans and receivables 1,578 1,042 Interest and fees per deposits and off-balance sheet items 2,924 3,177 Net Bank s foreign currency loans and receivables 422, ,204 Impairment allowance (12,664,660) (12,859,427) Total Bank s loans and receivables, net as at December 31 24,950,874 20,658, Loans and receivables due from customers breakdown per industry Public companies 3,873,796 1,993,690 Corporate customers 8,430,876 6,771,900 Entrepreneurs 251, ,673 Public sector 40,628 47,916 Retail customers 10,714,678 10,020,402 Non-residents 117,764 99,494 Agricultural producers 339, ,616 Other customers 1,181,874 1,382,742 Total Bank s loans and receivables as at December 31 24,950,874 20,658,433 28

31 RECEIVABLES PER FINANCIAL DERIVATIVES DESIGNATED AS RISK HEDGING INSTRUMENTS With contracted risk hedges consumer price index growth Receivables per financial derivatives designated as risk hedging instruments 2,485 2,497 In foreign currencies Currency swap Total receivables per financial derivatives designated as risk hedging instruments as at December 31 2,485 2, INTANGIBLE ASSETS Licenses 153, ,087 Software 302, ,812 Total intangible assets 455, ,899 Impairment of intangible assets (22,558) (22,558) Accumulated amortization of intangible assets (354,466) (294,163) Intangible assets, net book value as at December 31 78,952 85, PROPERTY, PLANT AND EQUIPMENT Land Buildings 1,346,648 1,346,063 Equipment 1,486,788 1,460,152 Equipment in progress 17,247 45,935 Leasehold improvements 303, ,022 Total property, plant and equipment 3,154,400 3,112,311 Accumulated depreciation of property, plant and equipment (1,386,134) (1,298,461) Property, plant and equipment, net book value as at December 31 1,768,266 1,813,850 29

32 PROPERTY, PLANT AND EQUIPMENT (Continued) Movements on Property, Plant and Equipment, Investment Property and Intangible Assets: Land and Buildings Equipme nt and Other Assets Constructio n in Progress Intangible Assets Total Cost Balance, January 1, ,556,075 1,460,152 96, ,898 3,514,209 Additions 26,877 10, ,124 40, ,371 Transfers from construction in progress 83, ,550 (198,758) 13,449 - Disposals and retirements (17,331) (85,655) (1,218) - (104,204) Balance, ,649,380 1,486,788 18, ,976 3,610,376 Accumulated depreciation and amortization Balance, January 1, , , ,721 1,615,182 Charge for the year 39, ,146-60, ,331 Disposals and retirements (11,275) (85,080) - - (96,355) Balance, ,896 1,019, ,024 1,763,158 Net book value as of ,282, ,550 18,232 78,952 1,847,218 Land and Buildings Equipment and Other Assets Constructio n in Progress Intangible Assets Total Cost Balance, January 1, ,518,399 1,561,030 33, ,551 3,569,723 Additions 6,633 5, ,663 33, ,186 Transfers from construction in progress 40, ,977 (175,322) 6,021 - Disposals and retirements (9,281) (235,368) - (94,051) (338,700) Balance, ,556,075 1,460,152 96, ,898 3,514,209 Accumulated depreciation and amortization Balance, January 1, ,700 1,048, ,220 1,696,556 Charge for the year 37, ,275-67, ,013 Disposals and retirements (3,597) (234,739) - (94,051) (332,387) Balance, , , ,721 1,615,182 Net book value as of ,217, ,980 96,084 85,177 1,899,027 As of 2014 the Bank had no mortgages instituted over its property and equipment to securitize loan repayment. 26. INVESTMENT PROPERTY Investment property 36,261 42,798 Investment property, net book value as at December 31 36,261 42,798 30

33 CURRENT TAX ASSETS Current tax assets - 16,517 Current tax assets as at December 31-16, DEFERRED TAX ASSETS Deferred tax assets 7,264 5,524 Deferred tax assets as at December 31 7,264 5,524 Temporary difference amount Deferred tax amount Deductible temporary differences per depreciable assets deferred tax assets 20,305 3,046 Deductible temporary differences per provisions made for employee retirement benefits in accordance with IAS 19 deferred tax assets 10,912 1,637 Deductible temporary differences per unpaid public duties deferred tax assets 4, Deductible temporary differences per impairment losses deferred tax assets 12,240 1,836 Total as at ,427 7,264 At the year-end total deferred tax assets amounted to RSD 7,264 thousand. 29. NON-CURRENT ASSETS HELD FOR SALE AND ASSETS FROM DISCONTINUED OPERATIONS Non-current assets held for sale 200, ,336 Non-current assets held for sale as at December , ,336 Non-current assets held for sale as of 2014 comprise the following: Building properties Area Amount Apartment for sale, Prote Mateje 66, Beograd 151m² 14,877 Building in Novi Sad, Bulevar oslobođenja m² 18,170 Business premises, Knjaževačka bb., Niš 15.16m² 987 Residential premises Slatinski venac 5a Vrnjačka Banja m² 166, ,339 31

34 OTHER ASSETS In RSD RSD fee and commission receivables per other assets 23,597 23,786 RSD receivables from sales 103,140 55,881 Interest receivables per other assets 20 2 Total receivables for fees, sales, and other assets 126,757 79,669 Impairment allowance (45,741) (35,586) Receivables for fees, sales, and other assets, net 81,016 44,083 Receivables arising from RSD advances for working capital 11,952 15,387 Receivables arising from advances for property, plant and equipment 16,056 17,554 RSD receivables from employees Receivables arising from prepaid taxes and contributions 19,433 16,010 Other RSD receivables from operations 196, ,709 RSD suspense and temporary accounts (1,458) (6,485) RSD receivables in settlement 238, ,099 Total other receivables and advances paid 481, ,422 Impairment allowance (172,111) (165,107) Other receivables and advances paid, net 309, ,315 Inventories Tangible assets received in lieu of debt collection 22,310 13,934 Tools and fixtures in use 2,406 2,956 Total inventories 25,058 17,376 Impairment allowance (2,406) (2,956) Inventories, net 22,652 14,420 In foreign currencies Other receivables from regular operations for determining foreign currency income 5,480 5,187 Total other receivables 5,480 5,187 Impairment allowance (5,472) (5,171) Other receivables, net 8 16 Receivables arising from foreign currency advances for working capital Foreign currency advances paid 5,114 4,452 Foreign currency receivables from employees 2,268 2,436 Other foreign currency receivables from operations 3,077 2,749 Foreign currency suspense and temporary accounts (609) (578) Foreign currency receivables in settlement 15,918 22,205 Total other receivables and advances paid 26,197 31,552 Impairment allowance (4,458) (4,297) Other receivables and advances paid, net 21,739 27,255 Deferred other RSD expenses 22,383 9,608 Other RSD prepayments 2,588 3,762 Deferred foreign currency interest expenses Deferred other foreign currency expenses 3,287 1,628 Other foreign currency prepayments Total deferred receivables 28,647 15,780 Total other assets as at December , ,869 32

35 PROVISIONS FOR IDENTIFIED LOSSES PER BALANCE SHEET ITEMS Provisions for interest, fee and sales receivables and prepayments 232, ,540 Provisions for loans, deposits and other advances 12,828,046 13,059,132 Provisions for securities 541, ,289 Provisions for other receivables 176, ,413 Total provisions for potential losses per balance sheet items as at December 31 13,778,680 13,924,374 Movements on provisions for identified losses per balance sheet items in 2014 were as follows: Opening balance Increase during the year Decrease during the year Prior years decrease FX differences Closing balance Write-off Provisions for interest, fee and sales receivables and prepayments 129,540 (22,614) 167,192 (25,316) (16,848) 1, ,995 Provisions for loans, deposits and other advances 13,059,132 (940,667) 2,324,032 (836,684) (1,042,636) 264,869 12,828,046 Provisions for securities 563,289 (13) - - (22,586) ,069 Provisions for other receivables 172,413 (11,239) 39,603 (9,826) (14,792) ,570 Total provisions for potential losses per balance sheet items 13,924,374 (974,533) 2,530,827 (871,826) (1,096,862) 266,700 13,778,680 Movements on provisions for identified losses per balance sheet items in 2013 were as follows: Opening balance Increase during the year Decrease during the year Prior years decrease FX differences Closing balance Write-off Provisions for interest, fee and sales receivables and prepayments 110,355 (14,109) 98,608 (28,794) (36,811) ,540 Provisions for loans, deposits and other advances 9,604,499 (1,401,898) 7,138,177 (844,232) (1,446,418) 9,004 13,059,132 Provisions for securities 577,212 (11,873) 13,999 (3,791) (12,188) (70) 563,289 Provisions for other receivables 179,041 (29,446) 77,150 (4,472) (49,835) (25) 172,413 Total provisions for potential losses per balance sheet items 10,471,107 (1,457,326) 7,327,934 (881,289) (1,545,252) 9,200 13,924,374 Required Reserve for Estimated Losses Based on the categorization of loans and receivables in accordance with the regulations of the National Bank of Serbia, the Bank calculated the reserve for estimated losses based on the total Bank's exposure to credit risk as of Calculated reserve for estimated losses in accordance with the Decision of the National bank of Serbia per: Balance sheet assets 18,452,693 Off-balance sheet items 171,294 Total 18,623,987 33

36 PROVISIONS FOR IDENTIFIED LOSSES PER BALANCE SHEET ITEMS (Continued) Required Reserve for Estimated Losses (Continued) Impairment allowance and provisions calculated in accordance with the internally adopted methodology (IAS 39): Impairment allowance of balance sheet assets 13,776,693 Provisions for losses per off-balance sheet items 183,736 13,960,429 Pursuant to the NBS Decision on the Classification of Balance Sheet Assets and Off-Balance Sheet Items, the sum of positive differences between the reserve for estimated losses calculated in accordance with the aforecited decision and the amount of impairment allowance of balance sheet assets and provisions for losses per off-balance sheet items in accordance with the internally adopted methodology represents the amount of the required reserve for estimated losses. If the amount of impairment allowance for balance sheet assets and off-balance sheet items exceeds the amount of the reserve for potential losses as calculated for an individual borrower, the Bank is under no obligation to calculate the required special reserve for potential losses per balance sheet assets and off-balance items. Required reserve for estimated losses per balance sheet assets and off-balance sheet items 5,033, FINANCIAL LIABILITIES AT FAIR VALUE THROUGH PROFIT AND LOSS HELD FOR TRADING Currency swap 10,571 - Total financial liabilities at fair value through profit and loss held for trading as at December 31 10, LIABILITIES PER FINANCIAL DERIVATIVES DESIGNATED AS RISK HEDGING INSTRUMENTS With contracted risk hedges consumer price index growth Liabilities per financial derivatives designated as risk hedging instruments In foreign currencies Currency swap - 12,505 Total liabilities per financial derivatives designated as risk hedging instruments as at December ,681 34

37 DEPOSITS AND OTHER LIABILITIES DUE TO BANKS, OTHER FINANCIAL INSTITUTIONS AND THE CENTRAL BANK In RSD Transaction deposits 345,205 23,310 Earmarked deposits 4,392 5,805 Other deposits 2,573 12,223 Overnight deposits and borrowings - 556,089 Other financial liabilities 10,213 6,799 RSD deposits and other liabilities 362, ,226 In foreign currencies Transaction deposits 36,918 54,831 Earmarked deposits Other deposits 152, ,447 Other financial liabilities 1 25 Foreign currency deposits and other liabilities 189, ,372 Total deposits and other liabilities due to banks, other financial institutions and the central bank as at December , , DEPOSITS AND OTHER LIABILITIES DUE TO CUSTOMERS Deposits and other liabilities due to customers breakdown per product In RSD Transaction deposits 6,625,732 3,795,285 Savings deposits 417, ,318 Deposits based on approved loans 30,748 2,148 Earmarked deposits 333, ,554 Other deposits 2,191, ,404 Overnight deposits 1,009, ,881 Borrowings 2,675 2,675 Other financial liabilities 75,176 75,866 RSD deposits and other liabilities 10,685,928 5,654,131 In foreign currencies Transaction deposits 3,388,199 1,831,437 Savings deposits 9,786,531 8,189,671 Deposits based on approved loans 481, ,186 Earmarked deposits 406, ,993 Other deposits 990, ,889 Other financial liabilities 188,968 42,562 Foreign currency deposits and other liabilities 15,242,091 11,178,738 Total deposits and other liabilities due to customers as at December 31 25,928,019 16,832,869 35

38 DEPOSITS AND OTHER LIABILITIES DUE TO CUSTOMERS (Continued) Deposits and other liabilities due to customers breakdown per industry Holding companies - 9 Public companies 2,413, ,635 Corporate customers 6,478,136 3,873,947 Entrepreneurs 586, ,577 Public sector 2,030, ,619 Retail customers 12,693,869 10,426,249 Non-residents 956, ,402 Agricultural producers 260, ,724 Other customers 508, ,707 Total deposits and other liabilities due to customers as at December 31 25,928,019 16,832, SUBORDINATED LIABILITIES Subordinated liabilities in foreign currency 976,100 3,217,972 Deferred interest payable per subordinated liabilities in foreign currency 1,445 5,674 Total subordinated liabilities as at December ,545 3,223,646 Decrease in liabilities for subordinated loans was a result of conversion of subordinated debt into the Bank's equity in 2014 (Note 46). 37. PROVISIONS Provisions for potential litigation losses 19,131 27,597 Provisions for losses per off-balance sheet items 183, ,301 Provisions for retirement benefits 10,912 10,265 Total provisions as at December , ,163 Movements on provisions are presented in the table below: Provisions for potential litigation losses Balance as at January 1 27,597 30,892 Charge for the year 17,257 26,386 Reversal of provisions (25,723) (29,681) Balance as at December 31 19,131 27,597 Provisions for losses per off-balance sheet items Balance as at January 1 163, ,599 Charge for the year 58,286 58,033 Reversal of provisions (38,837) (26,386) Foreign exchange differences Balance as at December , ,301 Provisions for retirement benefits Balance as at January 1 10,265 10,025 Charge for the year 3,639 2,875 Reversal of provisions (2,992) (2,635) Balance as at December 31 10,912 10,265 36

39 CURRENT TAX LIABILITIES Current income tax expense liabilities - subsidiary Total current tax liabilities as at December OTHER LIABILITIES In RSD Fees and commission payable per other liabilities 8,041 6,514 Trade payables 81,039 91,716 Advances received 47,369 48,324 Dividend payment liabilities 198, ,779 Liabilities per managed funds 18 - Other liabilities from operations 28,903 30,964 Liabilities in settlement 32,691 27,187 Total other liabilities 396, ,484 Net salaries 71 - Payroll taxes 10 - Payroll contributions 21 1 Other liabilities to employees 1, Value added tax payable 4,117 3,124 Other taxes and contributions payable 2,625 4,144 Total liabilities for salaries, taxes and contributions 8,660 7,523 Accrued liabilities for other expenses 155, ,995 Deferred interest income 9, Deferred other income 10,062 12,923 Other accruals 462 1,588 Total accruals 175, ,448 In foreign currencies Fees and commission payable per other liabilities 1,604 1,416 Trade payables 1,849 1,603 Advances received 21,443 16,650 Liabilities per managed funds Other liabilities from operations 1 1 Liabilities in settlement Temporary and suspense accounts 6 6 Total other liabilities 25,759 20,111 Accrued liabilities for other expenses 5,568 2,460 Deferred other income 158 1,563 Total accruals 5,726 4,023 Total other liabilities as at December , ,589 37

40 OTHER LIABILITIES (Continued) Taxes Payable Value added tax payable 4,117 3,124 Payroll taxes charged to the Bank Payroll contributions charged to the Bank City development land fees 4 1,584 Other contributions communal tax for business sign display 1,277 1,439 Personal income tax payables 1, Other taxes and contributions payable Total taxes payable as at December 31 6,742 7, Dividend Payment Liabilities Payment of dividend regular shares 19,544 19,544 Payment of dividend preferred shares Payment of dividend regular shares for prior years (prior to 2003) Payment of dividend preferred shares for prior years (prior to 2003) Payment of dividend regular shares for ,157 4,157 Payment of dividend preferred shares for Payment of dividend regular shares for ,337 6,337 Payment of dividend preferred shares for Payment of dividend preferred shares for ,849 8,849 Payment of dividend preferred shares for ,282 47,282 Payment of dividend preferred shares for ,282 47,282 Payment of dividend preferred shares for ,282 47,282 Payment of dividend preferred shares for ,749 7,749 Payment of dividend preferred shares for ,924 4,924 Payment of dividend preferred shares for ,636 1,636 Payment of dividend preferred shares for ,636 1,636 Payment of dividend preferred shares for ,636 - Total dividend payment liabilities as at December , ,779 Dividend payables based on preferred shares for 2014 were recognized in the Bank's income statement for the year 2014 in the amount of RSD 1,636 thousand. The Bank had no liabilities for current income tax in