This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors

|

|

|

- Willis Todd

- 6 years ago

- Views:

Transcription

1 This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors Kansas City Omaha Overland Park Denver St. Louis Jefferson City

2 Retirement Plan Fee Disclosure Rules: Now What? Greg Ash, Esq. and Chadron Patton, Esq.

3 Presenters Greg Ash Partner Chadron Patton Associate

4 Program Highlights Background Focus on Fee Transparency Fee Disclosure Rules Service provider fee disclosures (disclosure to plan fiduciaries) Participant fee disclosures (disclosure by plan fiduciaries) Fiduciary Compliance Strategies Evaluating service provider disclosures Addressing participant fee disclosure inquiries 4

account balance of $25,000.")

5 Focus on Fee Transparency Fees charged to/paid by DC plan participants can dramatically affect retirement income: Let s take a quick look at how fees can affect you: Assume that you are an employee with 35 years until retirement and a current 401(k) account balance of $25,000. If returns on investments in your account over the next 35 years average 7 percent and fees and expenses reduce your average return by 0.5 percent, your account balance will grow to $227,000 at retirement, even if there are no further contributions to your account. If fees and expenses are 1.5 percent, however, your account balance will grow to only $163,000. The 1 percent difference in fees and expenses would reduce your account balance at retirement by 28 percent. FAQs on Disclosures to Help Employees Understand Their Retirement Plan Fees, U.S. Dept. of Labor, Employee Benefits Security Administration 5

6 Participants in the Dark Although 401(k) and 403(b) plan fees can be significant, participants and employers often don t know who pays them Participants pay 91% of fees (up from 78% in 2009) Median all-in fee for typical plan was 0.78% in a 2011 ICI survey, or about $248/participant But in a 2011 AARP study: 71% of U.S. employees believed they paid no 401(k) fees 6% were not sure 6

7 Call to Action DOL and media outlets are encouraging 401(k) plan activism You could encourage your employer to shop around for other providers willing to offer the same services, but at a much lower cost. And, just so you know, the law is on your side: plan fiduciaries have an obligation to consider the fees and expenses paid by your plan and to operate the plan in your interest. DOL Fee Disclosure FAQs A July 2012 Consumer Reports article encouraged readers to arm yourself with comparisons and join other plan participants to agitate for change. Fees Skim Big Bucks from 401(k)s, Consumer Reports, July 2012, p. 7 7

8 Fee Litigation 30+ cases pending, challenging DC plan fee practices, beginning in 2006 Legal theory: Excessive and undisclosed fees diminish returns and are unreasonable Plans overpay when fiduciaries don t understand fee structures Service providers are conflicted by revenue sharing 8

9 DOL Fee Initiatives 9

10 401(k) and 403(b) Fees Three general categories: Plan Administration Fees Individual Service Fees Investment Fees 10

11 Plan Administration Fees Recordkeeping Accounting Actuarial Appraisal Consulting Legal Third party administrator Trustee services 11

12 Individual Service Fees Loans Hardship withdrawals QDROs Distributions 12

13 Investment Fees Mutual funds Management fees Sales charges Rule 12b-1 fees Variable annuities Management fees Mortality expense charges Surrender and transfer charges 13

14 Mutual Fund Prospectus Annual fund operating expenses (deducted from fund assets) Class R-1 Class R-2 Class R-3 Class R-4 Class R-5 Management fees 0.27% 0.27% 0.27% 0.27% 0.27% Distribution and/or service (12b-1) fees none Other expenses Total annual fund operating expenses

15 Service Provider Fee Disclosure February 2, 2012 DOL published final regulations under 408(b)(2) of ERISA requiring disclosure of fees by covered service providers July 1, 2012 deadline for covered service providers to provide written disclosures to the responsible plan fiduciary (e.g., plan sponsor) 15

16 408(b)(2) Background Payments to parties-in-interest (from plan assets) are generally prohibited transactions (under 406) Constitutes breach of fiduciary duty 15% excise tax Parties-in-interest include service providers ERISA 408(b)(2) is exception to rule 16

17 ERISA Section 408(b)(2) Statutory exemption from P/T rules for payments (from plan) to service providers, so long as: Services are necessary for establishment or operation of plan The contract/arrangement is reasonable No more than reasonable compensation is paid to service provider 17

18 Reasonable Contract Under the final regulations, a contract is not reasonable unless service provider discloses (in writing, in advance) the services it will provide and the direct and indirect compensation it will receive Failure to disclose = unreasonable contract = prohibited transaction = breach of fiduciary duty 18

19 408(b)(2) Consequences If service provider fails to disclose fees (or if plan pays unreasonable fees): Parties have committed a prohibited transaction under ERISA 406 Plan fiduciary has breached its fiduciary duty may be personally liable for loss Service provider is subject to a 15% excise tax (100% if P/T not corrected) 19

20 Innocent Fiduciary Rule Class exemption covers fiduciary who: Innocently enters into unreasonable arrangement (due to lack of disclosure) Makes formal demand for fee disclosure Notifies DOL if provider does not comply 20

plans Covered plans do not")

plans Section 457(b) plans IRAs, SEPs, or SIMPLE")

21 Covered Plans ERISA-covered qualified plans both DB and DC plans ERISA-covered 403(b) plans Covered plans do not include: Non-ERISA (govt. or church) plans Section 457(b) plans IRAs, SEPs, or SIMPLE plans Health/welfare plans (at least for now) 21

22 Covered Service Providers Disclosure requirements apply to those who provide covered services to a plan, which include: Services provided as a fiduciary or RIA Recordkeeping and brokerage services Other services if the provider received indirect compensation (i.e., compensation from sources other than the plan or employer) 22

23 Covered Service Providers Investment advisors for plan Recordkeepers Brokers Asset allocation model managers Managed account provider Custom target date/life cycle fund managers Commingled funds/collective trusts NOT most mutual funds 23

at least $1,000 in direct or indirect compensation from the covered")

24 Covered Arrangements Contract/agreement to perform services for a covered plan Reasonably expects to receive (together with subcontractors and affiliates) at least $1,000 in direct or indirect compensation from the covered plan 24

25 Required Disclosures Description of services to be provided Statement regarding status of covered service providers Description of all direct, indirect, relatedparty, and termination compensation service provider is expected to receive Manner of receipt of compensation (e.g., billed separately or paid directly from plan assets) 25

26 Definition of Services Fiduciary services Any recordkeeping services All services that will be provided in connection with the arrangement (including services provided by an affiliate or subcontractor) 26

27 Direct Compensation Direct Compensation is compensation received directly from the plan Example: TPA charges each participant account $50/year (or 5 basis points) May be expressed as a dollar amount, percentage, formula, per-participant charge, or any other reasonable method 27

28 Indirect Compensation Indirect Compensation is compensation received from any source other than the plan or plan sponsor Example: TPA receives 20 bps revenue sharing from mutual fund company whose fund(s) are investment options under the plan 28

29 What is Revenue Sharing? #1 Direct Fee Payments 29

30 What is Revenue Sharing? #2 Indirect Fee Payments 30

31 Related Party Compensation Must describe compensation paid among related parties (including affiliates and subcontractors) to the covered service provider, if it is either: Set on a transaction basis (e.g., finder s fee or commission); or Charged directly against the covered plan s investments (e.g., Rule 12b-1 fees) 31

32 Termination Compensation Disclosure must describe any compensation that the covered service provider, an affiliate, or a subcontractor reasonably expects to receive in connection with the termination of its contract or arrangement with the covered plan 32

33 Recordkeepers and Brokers Must provide fee information for each designated investment alternative (other than brokerage window) that is made available to plan, including: Expense ratios Transaction fees Any other ongoing charges May use investment provider materials 33

34 Recordkeeping Services Paid Through Revenue Sharing If providing recordkeeping services without explicit compensation, recordkeeper must provide reasonable, good-faith estimate of cost of services including: Explanation of the methodology and assumptions used to prepare the estimate; and Detailed explanation of the recordkeeping services that will be provided to the covered plan 34

35 Format Disclosures must be written, but do not have to be part of services contract Service providers permitted to provide the required disclosures electronically, including by making information available on a secure website, if: Disclosure information on the website is readily accessible to responsible plan fiduciaries; and Responsible plan fiduciaries have clear notification on how to access this information 35

36 Timing Initial disclosure deadline was July 1, 2012 Changes to the following types of information must be disclosed as soon as practicable, but in no case later than 60 days after the covered service provider knows of the change: Services to be provided Status of the covered service provider, an affiliate, or a subcontractor as an ERISA fiduciary or registered investment advisor Compensation to be received Cost of recordkeeping services 36

37 Participant Fee Disclosures General: Plan administrator must disclose plan- and investment-related information to participants Disclosures required On participant s initial eligibility Annual notice of general plan information Quarterly notice of actual fees/expenses 37

38 Covered Plans Applies to all participant-directed individual account plans subject to ERISA (e.g., 401(k), 403(b)) Excludes old money 403(b) contracts (pre-2009) Does not apply to IRAs, IRA annuities, SEPs, or SIMPLEs 38

protection Disclosures not optional, but are")

39")

39 Key Issues for Employers Plan administrator is responsible for compliance Compliance required to obtain 404(c) protection Disclosures not optional, but are required as part of fiduciary duty under ERISA Violations risk fiduciary liability and litigation, not just sanctions and penalties (e.g., investment losses and excessive fees) 39

40 Who is Responsible? ERISA 3(16) plan administrator Often, plan administrator is the employer Plans may contractually delegate this responsibility (e.g., to service provider) Relief for reasonable and good faith reliance on third parties Plan administrator not liable for completeness and accuracy of disclosures made by third parties But no relief from obligation to provide the notice 40

41 Content of Annual Notice Plan-Related Information General operational and identification How to give investment instructions Exercise of voting, tender, similar rights Designated investment alternatives Brokerage windows and self-directed accounts Associated fees and expenses Administrative expenses General explanation of fees for plan-level and individual administrative fees that may be charged (e.g., accounting, legal, QDROs, loans) 41

42 Content of Annual Notice Investment-Related Information Identifying information for investment funds (name, category, internet address for supplemental information) Performance data (1-, 5-, and 10-year returns) Special rules for fixed return funds (e.g., GICs) and employer stock Special rules for target-date funds TBA 42

43 Content of Annual Notice Investment-Related Information Benchmark information Fee and expense information Amount and description Description of limits on purchase, transfer, or withdrawal Total annual operating expenses as a percentage and per $1,000 invested Website information for investment funds Glossary of terms (sample at 43

44 Format of Annual Notice Investment-related information must be presented in chart (or similar) format that facilitates comparison Chart must include: Date compiled Name and address of plan administrator How to obtain additional information DOL has published a model chart 44

45 Model Chart Returns Table 1 Variable Return Investments Name/ Type of Option Equity Funds A Index Fund/ S&P 500 www. website address B Fund/ Large Cap www. website address C Fund/ Int l Stock www. website address Bond Funds D Fund/ Bond Index www. website address Other E Fund/ GICs www. website address F Fund/ Stable Value www. website address Average Annual Total Return as of 12/31/XX 1yr. 5yr. 10yr. Since Inception 1yr. 5yr. 10yr. Since Inception 26.5%.34% -1.03% 9.25% 26.46%.42% -.95% 9.30% Benchmark S&P %.99% N/A 2.26% 27.80% 1.02% N/A 2.77% US Prime Market 750 Index 36.73% 5.26% 2.29% 9.37% 40.40% 5.40% 2.40% 12.09% MSCI EAFE 6.45% 4.43% 6.08% 7.08% 5.93% 4.97% 6.33% 7.01% Barclays Cap. Aggr. Bd..72% 3.36% 3.11% 5.56% 1.8% 3.1% 3.3% 5.75% 3-month US T-Bill Index 4.36% 4.64% 5.07% 3.75% 1.8% 3.1% 3.3% 4.99% 3-month US T-Bill Index 45

46 Model Chart Fees Name / Type of Option Equity Funds A Index Fund/ S&P 500 B Fund/ Large Cap C Fund/ International Stock Bond Funds E Fund/ Bond Index Other F Fund/ GICs G Fund/ Stable Value Generations 2020/ Lifecycle Fund Fixed Return Investments Total Annual Operating Expenses As a % Per $ % $ % $ % $ % $ % $ % $ % $15.00 Table 3 Fees and Expenses Shareholder-Type Fees $20 annual service charge subtracted from investments held in this option if valued at less than $10, % deferred sales charge subtracted from amounts withdrawn within 12 months of purchase. 5.75% sales charge subtracted from amounts invested. N/A 10% charge subtracted from amounts withdrawn within 18 months of initial investment. Amounts withdrawn may not be transferred to a competing option for 90 days after withdrawal. Excessive trading restricts additional purchases (other than contributions and loan repayments) for 85 days. H 200X / GIC N/A 12% charge subtracted from amounts withdrawn before maturity. I LIBOR Plus/ Fixed- Type Invest Account N/A 5% contingent deferred sales charge subtracted from amounts withdrawn; charge reduced by 1% on 12-month anniversary of each investment. 46

47 Content of Quarterly Notice Amount actually charged to participant accounts during prior quarter Plan-level charges Description of services to which charges relate No requirement to unbundle and report amounts included in investment fund operating expenses But, if applicable, explanation that some plan administrative expenses were paid from annual operating expenses of one or more investment funds (i.e., revenue sharing) Individual charges (e.g., for loans, QDROs, distributions, investment advice services) 47

48 To Whom? Annual and Quarterly Notice Any individual who is eligible to participate in plan Participants currently contributing Participants eligible but not contributing Term-vested with accounts Beneficiaries Alternate payees under QDROs 48

49 When? Annual Notice Initial Annual Notice later of: 8/31/2012, or 60 days after 1 st day of 1 st plan year beginning on/after 11/1/2011 Subsequent Annual Notices at least once in any 12-month period New employees on or before first day eligible to participate in plan Updates days before effective date of change 49

50 When? Quarterly Notice Initial Quarterly Notice 45 days after end of calendar quarter in which Initial Annual Notice required For calendar year plans, 11/14/2012 Subsequent Quarterly Notices at least once in any 3-month period 50

51 How? Service providers will take the laboring oar DOL reserved rules on method of distribution Generally: Stand-alone paper forms Quarterly statements SPD (if meet the frequency requirements) Electronic 51

52 Muted Reaction To Disclosures So Far 408(b)(2) Service Provider Disclosures Confusion from employers Fees still unclear What should we do with this information? But, DOL expanding examination and enforcement activities 404a-5 Participant Disclosures Largely a non-event But, first quarterly statements still not out 52

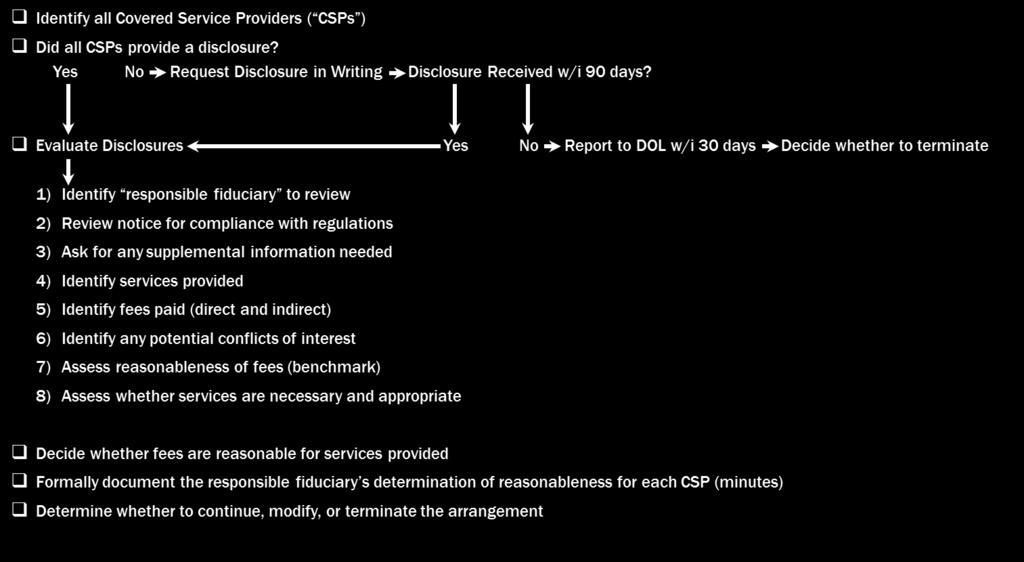

53 Fiduciary Compliance Plan 408(b)(2) Service Provider Disclosures Don t just file them away! Make sure you have written agreements with all service providers Fiduciary duty to assess reasonableness of arrangement, and thus entitlement to prohibited transaction exemption Minutes of fiduciary committee meeting should reflect compliance process 53

54 408(b)(2) Disclosure Checklist 54

55 Fiduciary Compliance Plan 404a-5 Participant Disclosures Make sure service providers will distribute the notices (Annual and Quarterly) Insist on contractual delegation of responsibility to service provider Review and understand the fee chart Prepare for questions from participants Decide who will answer questions (e.g., employer, service provider) Consider creating a Q&A template to keep answers consistent Create a complaint log and have fiduciaries review it 55

56 Fiduciary Compliance Plan 404a-5 Participant Disclosures Be prepared for tough questions: Why didn t you tell me about these fees before? What do these fees pay for? My neighbor pays less than $5 for every $1,000 invested. Why are we paying twice that? If I use a fund with a higher price, will I get more value? Did you stop deducting fees when my investments lost value? 56

57 404a-5 Compliance Plan If service provider prepares Annual Notice, review plan-related disclosures for accuracy Consider supplementing disclosures that have already been distributed Benchmark fees Evaluate how fees are allocated Asset-based? Break point? Pro rata? Per capita? Compare fund benchmarks in disclosure with those in IPS Communicate value of plan before disclosures are made 57

58 Q & A 58

59 Thank You! Greg Ash Partner Chadron Patton Associate

60 This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors Kansas City Omaha Overland Park Denver St. Louis Jefferson City

ARE YOU READY FOR NEW DOL FEE DISCLOSURE RULES?

ARE YOU READY FOR NEW DOL FEE DISCLOSURE RULES? (updated June 2, 2011) ANTHONY J. KOLENIC, JR. JUSTIN W. STEMPLE GEORGE L. WHITFIELD 2011 Warner Norcross & Judd LLP. All rights reserved. Agenda General

ARE YOU READY FOR NEW DOL FEE DISCLOSURE RULES? (updated June 2, 2011) ANTHONY J. KOLENIC, JR. JUSTIN W. STEMPLE GEORGE L. WHITFIELD 2011 Warner Norcross & Judd LLP. All rights reserved. Agenda General

GINGER B. LACHAPELLE, ESQ. BLITMAN & KING LLP

GINGER B. LACHAPELLE, ESQ. BLITMAN & KING LLP FINAL RULE On October 14, 2010, the DOL released final regulations under Section 404(a) of ERISA relating to the disclosure of fee and other information to

GINGER B. LACHAPELLE, ESQ. BLITMAN & KING LLP FINAL RULE On October 14, 2010, the DOL released final regulations under Section 404(a) of ERISA relating to the disclosure of fee and other information to

Benefits. DOL Fee Disclosure Regulations: What Plan Sponsors Need to Know

Benefits cus Employer Update DOL Fee Disclosure Regulations: What Plan Sponsors Need to Know October 2011 Retirement plan fees and their impact on the retirement savings of plan participants is a topic

Benefits cus Employer Update DOL Fee Disclosure Regulations: What Plan Sponsors Need to Know October 2011 Retirement plan fees and their impact on the retirement savings of plan participants is a topic

408(b)(2) Checklist. IS YOUR PLAN COVERED? Plans not Covered. Covered Plans

(2) Checklist. IS YOUR PLAN COVERED? Plans not Covered. Covered Plans") 408(b)(2) Checklist Responsible Plan Fiduciary Duties Under Section 408(b)(2) of the Employee Retirement Income Security Act of 1974 (ERISA): 1. Determine if your plan is covered under the regulation 2.

408(b)(2) Checklist Responsible Plan Fiduciary Duties Under Section 408(b)(2) of the Employee Retirement Income Security Act of 1974 (ERISA): 1. Determine if your plan is covered under the regulation 2.

SUMMARY OF THE DEPARTMENT OF LABOR FINAL RULE UNDER SECTION 408(b)(2) SERVICE PROVIDER FEE DISCLOSURE. February 6, 2012

(2) SERVICE PROVIDER FEE DISCLOSURE. February 6, 2012") THE PLAN SPONSOR COUNCIL OF AMERICA Serving Retirement Plan Sponsors for More than 60 Years 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863.7272 ferrigno@401k.org Edward Ferrigno Vice President,

THE PLAN SPONSOR COUNCIL OF AMERICA Serving Retirement Plan Sponsors for More than 60 Years 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863.7272 ferrigno@401k.org Edward Ferrigno Vice President,

Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013

and 403(b) Plan Sponsors in 2013") Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013 Presented by: Rose Panico-Marino, AIF, ERPA, QPA Senior Vice President January 30, 2013 Learning Objectives Review specific

Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013 Presented by: Rose Panico-Marino, AIF, ERPA, QPA Senior Vice President January 30, 2013 Learning Objectives Review specific

Date: October 25, 2010 TCRS : Department Of Labor Final Regulations Relating To Participant Fee Disclosure

**** UPDATE: As of February 3, 2012, the DOL has extended the 408(b)(2) effective date to July 1, 2012 and the 404(a) effective date to generally be August 30, 2012. See TCRS 2012-01 memo for details.

**** UPDATE: As of February 3, 2012, the DOL has extended the 408(b)(2) effective date to July 1, 2012 and the 404(a) effective date to generally be August 30, 2012. See TCRS 2012-01 memo for details.

The Department of Labor Fee Transparency Initiatives: Part 2 - Mandatory Service Provider Fee Disclosures - Updated

Volume 2012 May 1 The Department of Labor Fee Transparency Initiatives: Part 2 - Mandatory Service Provider Fee Disclosures - Updated For a number of years, the Department of Labor has been concerned about

Volume 2012 May 1 The Department of Labor Fee Transparency Initiatives: Part 2 - Mandatory Service Provider Fee Disclosures - Updated For a number of years, the Department of Labor has been concerned about

401(k) Fee Disclosure Form

Fee Disclosure Form") 401(k) Fee Disclosure Form The 401(k) Fee Disclosure Form is designed as a tool for plan sponsors to identify the fees and potential conflicts of interest of service providers. The Form may be used to

401(k) Fee Disclosure Form The 401(k) Fee Disclosure Form is designed as a tool for plan sponsors to identify the fees and potential conflicts of interest of service providers. The Form may be used to

Plan Sponsor Fee Disclosure

Plan Sponsor Fee Disclosure Standard Retirement Services, Inc. Overview Full, clear disclosure of all fees associated with qualified retirement plans has long been a goal of the Department of Labor (DOL).

Plan Sponsor Fee Disclosure Standard Retirement Services, Inc. Overview Full, clear disclosure of all fees associated with qualified retirement plans has long been a goal of the Department of Labor (DOL).

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals.

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. TOPIC: Final Retirement Plan Participant Level Fee Disclosure

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. TOPIC: Final Retirement Plan Participant Level Fee Disclosure

By Lisa Taggart and Joni Andrioff. Participant disclosure rules are effective. Service provider disclosure rules are effective

A Timely Analysis of Legal Developments A S A P June 6, 2012 DOL s Recent Guidance on New Participant Fee Disclosure Regulations Is a Must Read for Retirement Plan Fiduciaries Preparing for the August

A Timely Analysis of Legal Developments A S A P June 6, 2012 DOL s Recent Guidance on New Participant Fee Disclosure Regulations Is a Must Read for Retirement Plan Fiduciaries Preparing for the August

SUMMARY OF FINAL RULE ON FIDUCIARY REQUIREMENTS FOR DISCLOSURE IN PARTICIPANT-DIRECTED INDIVIDUAL ACCOUNT PLANS. February 6, 2012

THE PLAN SPONSOR COUNCIL OF AMERICA Serving Retirement Plan Sponsors for More than 60 Years 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863.7272 ferrigno@401k.org Edward Ferrigno Vice President,

THE PLAN SPONSOR COUNCIL OF AMERICA Serving Retirement Plan Sponsors for More than 60 Years 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863.7272 ferrigno@401k.org Edward Ferrigno Vice President,

Final Regulation on Participant-Level Fee Disclosures. By: Andrew Varady, Esq. Associate General Counsel, MetLife

Final Regulation on Participant-Level Fee Disclosures By: Andrew Varady, Esq. Associate General Counsel, MetLife Contents 1 Introduction 2 Background 2 New Participant-Level Fee Disclosure Requirements

Final Regulation on Participant-Level Fee Disclosures By: Andrew Varady, Esq. Associate General Counsel, MetLife Contents 1 Introduction 2 Background 2 New Participant-Level Fee Disclosure Requirements

Soltis Investment Advisors Fiduciary Education

Soltis Investment Advisors Fiduciary Education November 2017 Kim D. Anderson, AIF Managing Partner, Retirement Plan Services Soltis Investment Advisors is proud to be among the first investment advisors

Soltis Investment Advisors Fiduciary Education November 2017 Kim D. Anderson, AIF Managing Partner, Retirement Plan Services Soltis Investment Advisors is proud to be among the first investment advisors

EMPLOYEE BENEFITS AND EXECUTIVE COMPENSATION

EMPLOYEE BENEFITS AND EXECUTIVE COMPENSATION ATTORNEY ADVERTISING DOL DELAYS APPLICATION OF SERVICE PROVIDER FEE DISCLOSURE RULES UNTIL JANUARY 1, 2012 By: Mark A. Holdsworth, Esq. April 6, 2011 Introduction

EMPLOYEE BENEFITS AND EXECUTIVE COMPENSATION ATTORNEY ADVERTISING DOL DELAYS APPLICATION OF SERVICE PROVIDER FEE DISCLOSURE RULES UNTIL JANUARY 1, 2012 By: Mark A. Holdsworth, Esq. April 6, 2011 Introduction

Participant Fee Disclosures for ERISA Plans

Participant Fee Disclosures for ERISA Plans About MetLife MetLife, Inc. (NYSE: MET), through its subsidiaries and affiliates ( MetLife ), is one of the largest life insurance companies in the world. Founded

Participant Fee Disclosures for ERISA Plans About MetLife MetLife, Inc. (NYSE: MET), through its subsidiaries and affiliates ( MetLife ), is one of the largest life insurance companies in the world. Founded

Fee Disclosure. Get the 411 on 408(b)(2) Presented by: Ben Healy, AVP, Operations Eric Grzejka, Manager, Retirement Plan Consulting

(2) Presented by: Ben Healy, AVP, Operations Eric Grzejka, Manager, Retirement Plan Consulting") Fee Disclosure Get the 411 on 408(b)(2) Presented by: Ben Healy, AVP, Operations Eric Grzejka, Manager, Retirement Plan Consulting Save the Date UPCOMING EVENTS May 28 2015 For Companies (New York, NY)

Fee Disclosure Get the 411 on 408(b)(2) Presented by: Ben Healy, AVP, Operations Eric Grzejka, Manager, Retirement Plan Consulting Save the Date UPCOMING EVENTS May 28 2015 For Companies (New York, NY)

How-To Guide for the. Plan and Investment Disclosure

How-To Guide for the Plan and Investment Disclosure T. Rowe Price has created this guide to assist you with reviewing and approving the annual participant disclosures. Using this guide will assist you

How-To Guide for the Plan and Investment Disclosure T. Rowe Price has created this guide to assist you with reviewing and approving the annual participant disclosures. Using this guide will assist you

Perspectives AN EXECUTIVE COMPENSATION, BENEFITS & HUMAN RESOURCES LAW UPDATE

Volume 3, Edition 1 AN EXECUTIVE COMPENSATION, BENEFITS & HUMAN RESOURCES LAW UPDATE IN THIS EDITION... Compliance Deadlines This issue of provides a comprehensive discussion of the final Department of

Volume 3, Edition 1 AN EXECUTIVE COMPENSATION, BENEFITS & HUMAN RESOURCES LAW UPDATE IN THIS EDITION... Compliance Deadlines This issue of provides a comprehensive discussion of the final Department of

CHAPTER 2 DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2)

(2) DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2)") CHAPTER 2 DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) Following the release of the Interim Final we now have the Final, Final Section 408(b)(2) Regulations.

CHAPTER 2 DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) Following the release of the Interim Final we now have the Final, Final Section 408(b)(2) Regulations.

Regulation on service provider fee disclosures for ERISA retirement plans

Regulation on service provider fee disclosures for ERISA retirement plans 2 About MetLife Resources MetLife Resources is the Division of Metropolitan Life Insurance Company that specializes in providing

Regulation on service provider fee disclosures for ERISA retirement plans 2 About MetLife Resources MetLife Resources is the Division of Metropolitan Life Insurance Company that specializes in providing

New ERISA 408(b)(2) Regulations Mastering Detailed Requirements for Service Provider Fee Disclosures

(2) Regulations Mastering Detailed Requirements for Service Provider Fee Disclosures") Presenting a live 110 minute webinar with interactive Q&A New ERISA 408(b)(2) Regulations Mastering Detailed Requirements for Service Provider Fee Disclosures WEDNESDAY, JANUARY 26, 2011 1pm Eastern 12pm

Presenting a live 110 minute webinar with interactive Q&A New ERISA 408(b)(2) Regulations Mastering Detailed Requirements for Service Provider Fee Disclosures WEDNESDAY, JANUARY 26, 2011 1pm Eastern 12pm

Fee Disclosure Q&A for Employers September 2014

Fee Disclosure Q&A for Employers September 2014 The Department of Labor (DOL) has issued two sets of final regulations requiring the disclosure of fees and expenses under plans governed by the Employee

Fee Disclosure Q&A for Employers September 2014 The Department of Labor (DOL) has issued two sets of final regulations requiring the disclosure of fees and expenses under plans governed by the Employee

Roadmap to Understanding Retirement Plan Fees. The only guide you need

Roadmap to Understanding Retirement Plan Fees The only guide you need Executive Summary Retirement plan fees under the spotlight You know there are costs associated with offering a retirement plan, but

Roadmap to Understanding Retirement Plan Fees The only guide you need Executive Summary Retirement plan fees under the spotlight You know there are costs associated with offering a retirement plan, but

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

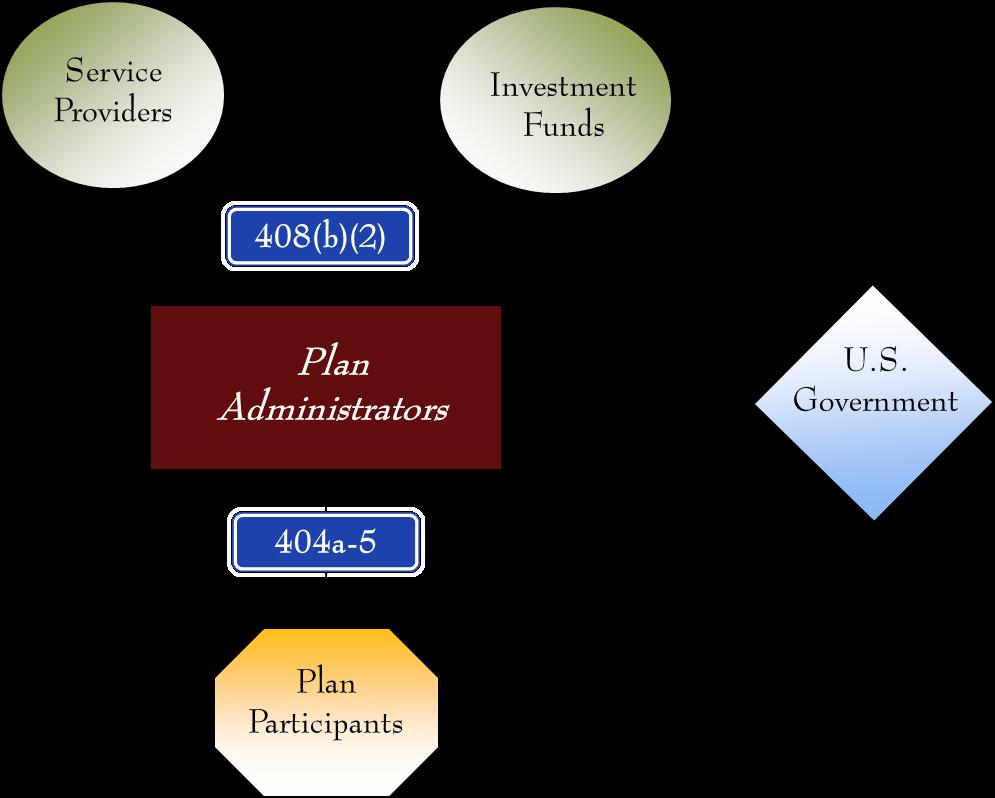

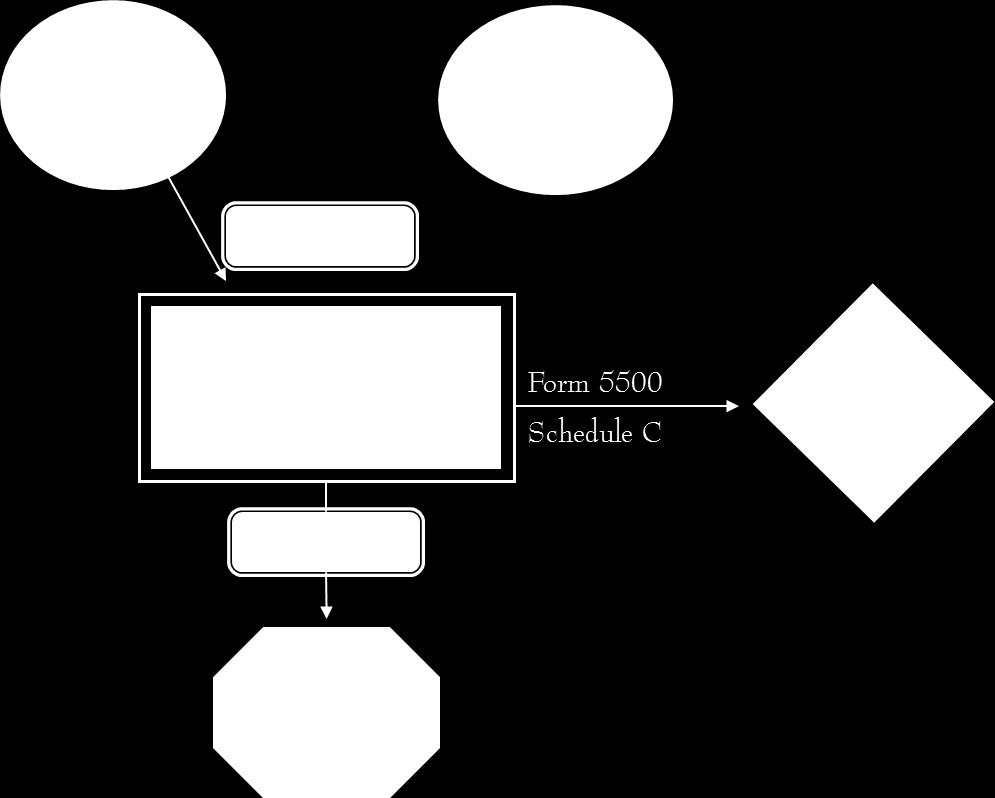

10/4/2011. COMPARISON OF DISCLOSURE RULES UNDER FORM 5500 SCHEDULE C AND UNDER 408(b)(2)

(2)") COMPARISON OF DISCLOSURE RULES UNDER FORM 5500 SCHEDULE C AND UNDER Employee Benefits Committee Joint Fall CLE Meeting October 21, 2011 Denver, CO Robert A. Miller Calfee, Halter & Griswold LLP Cleveland,

COMPARISON OF DISCLOSURE RULES UNDER FORM 5500 SCHEDULE C AND UNDER Employee Benefits Committee Joint Fall CLE Meeting October 21, 2011 Denver, CO Robert A. Miller Calfee, Halter & Griswold LLP Cleveland,

How-To Guide for the. Plan and Investment Disclosure

How-To Guide for the Plan and Investment Disclosure Reviewing Your Disclosure T. Rowe Price has created this guide to assist you with reviewing the 2017 Plan and Investment Disclosure for your Plan(s).

How-To Guide for the Plan and Investment Disclosure Reviewing Your Disclosure T. Rowe Price has created this guide to assist you with reviewing the 2017 Plan and Investment Disclosure for your Plan(s).

404(c) and OTHER ISSUES

and OTHER ISSUES") 401(k) INVESTMENT ISSUES 404(c) and OTHER ISSUES SUSAN P. SEROTA All rights reserved Pillsbury Winthrop Shaw Pittman LLP New York, New York August, 2008 Fiduciary Responsibilities Who is a Fiduciary? A

401(k) INVESTMENT ISSUES 404(c) and OTHER ISSUES SUSAN P. SEROTA All rights reserved Pillsbury Winthrop Shaw Pittman LLP New York, New York August, 2008 Fiduciary Responsibilities Who is a Fiduciary? A

The New Fee Disclosure Rules: What You Need to Do About 408(b)(2)

(2)") ederated The New Fee Disclosure Rules: What You Need to Do About 408(b)(2) What You Need to Do About 408(b)(2) Are You Ready? On April 1, 2012, the rules governing every 401(k) and every private pension

ederated The New Fee Disclosure Rules: What You Need to Do About 408(b)(2) What You Need to Do About 408(b)(2) Are You Ready? On April 1, 2012, the rules governing every 401(k) and every private pension

U.S. Department of Labor FIELD ASSISTANCE BULLETIN NO DATE: MAY 7, 2012 MEMORANDUM FOR: SUBJECT: BACKGROUND

U.S. Department of Labor Employee Benefits Security Administration Washington, DC 20210 FIELD ASSISTANCE BULLETIN NO. 2012-02 DATE: MAY 7, 2012 MEMORANDUM FOR: MABEL CAPOLONGO, DIRECTOR OF ENFORCEMENT

U.S. Department of Labor Employee Benefits Security Administration Washington, DC 20210 FIELD ASSISTANCE BULLETIN NO. 2012-02 DATE: MAY 7, 2012 MEMORANDUM FOR: MABEL CAPOLONGO, DIRECTOR OF ENFORCEMENT

WORKSHOP 9: What s the Hype on 3(16) and 3(38) Fiduciaries?

and 3(38) Fiduciaries?") WORKSHOP 9: What s the Hype on 3(16) and 3(38) Fiduciaries? FRED REISH, ESQ. January 22, 2014 Fiduciary Mumbo Jumbo The 401(k) industry has an unlimited number of labels for ERISA fiduciaries--some accurate

WORKSHOP 9: What s the Hype on 3(16) and 3(38) Fiduciaries? FRED REISH, ESQ. January 22, 2014 Fiduciary Mumbo Jumbo The 401(k) industry has an unlimited number of labels for ERISA fiduciaries--some accurate

Final Regulation on Service Provider Fee Disclosures for ERISA Retirement Plans

Final Regulation on Service Provider Fee Disclosures for ERISA Retirement Plans About MetLife For over 140 years, MetLife has been one of the country s most trusted financial institutions. The MetLife

Final Regulation on Service Provider Fee Disclosures for ERISA Retirement Plans About MetLife For over 140 years, MetLife has been one of the country s most trusted financial institutions. The MetLife

1. About Fees and Expenses

Important Information About Your Investment Options, Fees, and Other Expenses for the DXC Technology Matched Asset Plan Annual Information Statement on Investment Options and Fees and Expenses as of January

Important Information About Your Investment Options, Fees, and Other Expenses for the DXC Technology Matched Asset Plan Annual Information Statement on Investment Options and Fees and Expenses as of January

Retirement Plan Fundamentals Zero to Sixty. Todd Kading, CFP, ChFC, RF LeafHouse Financial Advisors

Retirement Plan Fundamentals Zero to Sixty Todd Kading, CFP, ChFC, RF LeafHouse Financial Advisors Meet Our Speaker Todd Kading Managing Director LeafHouse Financial Advisors Top 10 Most Dependable Wealth

Retirement Plan Fundamentals Zero to Sixty Todd Kading, CFP, ChFC, RF LeafHouse Financial Advisors Meet Our Speaker Todd Kading Managing Director LeafHouse Financial Advisors Top 10 Most Dependable Wealth

404(c) and 404a-5 Checklist

and 404a-5 Checklist") 404(c) and 404a-5 Checklist Plan Sponsor: Plan Name(s): Record Keeper: Advisor: Overview The new participant disclosure regulation under ERISA 404a-5 requires the plan fiduciary 1 to furnish much of the

404(c) and 404a-5 Checklist Plan Sponsor: Plan Name(s): Record Keeper: Advisor: Overview The new participant disclosure regulation under ERISA 404a-5 requires the plan fiduciary 1 to furnish much of the

Managing fiduciary responsibility for plan sponsors

Managing fiduciary responsibility for plan sponsors Invesco PlanForward Foundations SM Putting fiduciary responsibility in action Contents 1 Defining fiduciary responsibility 4 Maximizing fiduciary protection

Managing fiduciary responsibility for plan sponsors Invesco PlanForward Foundations SM Putting fiduciary responsibility in action Contents 1 Defining fiduciary responsibility 4 Maximizing fiduciary protection

The Definition of a Fiduciary - The Times They are a Changin

The Definition of a Fiduciary - The Times They are a Changin Bob Kaplan, CFP, CPC QPA, APA VP, National Training Consultant www.ing.com Important Information CIRCULAR 230 DISCLOSURE: Any tax discussion

The Definition of a Fiduciary - The Times They are a Changin Bob Kaplan, CFP, CPC QPA, APA VP, National Training Consultant www.ing.com Important Information CIRCULAR 230 DISCLOSURE: Any tax discussion

404(a) annual participant fee disclosure Frequently asked questions

annual participant fee disclosure Frequently asked questions") 404(a) annual participant fee disclosure Frequently asked questions Assisting plan sponsors Q1. What must the plan sponsor of an ERISAgoverned plan do to comply with the 404(a) participant fee disclosure

404(a) annual participant fee disclosure Frequently asked questions Assisting plan sponsors Q1. What must the plan sponsor of an ERISAgoverned plan do to comply with the 404(a) participant fee disclosure

US Department of Labor Issues Final Rule on Service Provider Fee Disclosure

Legal Update February 21, 2012 US Department of Labor Issues Final Rule on Service Provider Fee Disclosure On February 3, 2012, the US Department of Labor (DOL) issued a final rule (the Final Rule) amending

Legal Update February 21, 2012 US Department of Labor Issues Final Rule on Service Provider Fee Disclosure On February 3, 2012, the US Department of Labor (DOL) issued a final rule (the Final Rule) amending

Regulatory Compliance: Targeting Solutions for Your Client s Greatest Challenges

fi 360 Annual Conference April 2013 Regulatory Compliance: Targeting Solutions for Your Client s Greatest Challenges Jason C. Roberts, Esq., AIFA Chief Executive Officer Pension Resource Institute, LLC

fi 360 Annual Conference April 2013 Regulatory Compliance: Targeting Solutions for Your Client s Greatest Challenges Jason C. Roberts, Esq., AIFA Chief Executive Officer Pension Resource Institute, LLC

PHCM 401(k) Savings Plan Disclosure & Comparative Chart for Retirement Plan Participants

Savings Plan Disclosure & Comparative Chart for Retirement Plan Participants") PHCM 401(k) Savings Plan Disclosure & Comparative Chart for Retirement Plan Participants All individuals who have the right to direct investments in an employer-sponsored retirement plan are being provided

PHCM 401(k) Savings Plan Disclosure & Comparative Chart for Retirement Plan Participants All individuals who have the right to direct investments in an employer-sponsored retirement plan are being provided

Fiduciary Update and Best Practices for Retirement Plan Committee Members April 7, 2017

Fiduciary Update and Best Practices for Retirement Plan Committee Members April 7, 2017 Presented by: Nicole Berlowski ProHealth Care, Inc. 725 American Drive 191 N. Wacker Drive POB Suite 305 Suite 3700

Fiduciary Update and Best Practices for Retirement Plan Committee Members April 7, 2017 Presented by: Nicole Berlowski ProHealth Care, Inc. 725 American Drive 191 N. Wacker Drive POB Suite 305 Suite 3700

July 28, days after plan year-end: Deadline for distributing the Summary of Material Modification (SMM) if the plan was amended in 2015.

if the plan was amended in 2015.") Important Approaching Deadlines April 30, 2016 Same date for all plan years: Deadline to execute (i.e., sign and date) all documents that have been restated for the Pension Protection Act. June 30, 2016

Important Approaching Deadlines April 30, 2016 Same date for all plan years: Deadline to execute (i.e., sign and date) all documents that have been restated for the Pension Protection Act. June 30, 2016

ABC 401(k) Plan. Benchmark Fee Report. May 19, Report created by: James Jones Advisors Inc. (410)

Plan. Benchmark Fee Report. May 19, Report created by: James Jones Advisors Inc. (410)") May 19, 2017 Report created by: James Jones Advisors Inc. (410) 296-1000 Are Your Plan s Fees Reasonable? Introduction Fees and expenses associated with the management of a qualified retirement plan have

May 19, 2017 Report created by: James Jones Advisors Inc. (410) 296-1000 Are Your Plan s Fees Reasonable? Introduction Fees and expenses associated with the management of a qualified retirement plan have

SUMMARY PLAN DESCRIPTION FOR. Richmond Public Schools 403(b) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION FOR Richmond Public Schools 403(b) Retirement Plan 3-1-2014 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description

SUMMARY PLAN DESCRIPTION FOR Richmond Public Schools 403(b) Retirement Plan 3-1-2014 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description

NOTICE OF AUTOMATIC ENROLLMENT AND INVESTMENT MACY S, INC. 401(k) RETIREMENT INVESTMENT PLAN

RETIREMENT INVESTMENT PLAN") NOTICE OF AUTOMATIC ENROLLMENT AND INVESTMENT MACY S, INC. 401(k) RETIREMENT INVESTMENT PLAN This notice informs you of the automatic enrollment feature of the 401(k) Plan. Because you may have been subject

NOTICE OF AUTOMATIC ENROLLMENT AND INVESTMENT MACY S, INC. 401(k) RETIREMENT INVESTMENT PLAN This notice informs you of the automatic enrollment feature of the 401(k) Plan. Because you may have been subject

Retirement Plans 101: An Introduction to Section 403(b)

") Retirement Plans 101: An Introduction to Section 403(b) 2008 Giller & Calhoun LLC I. Overview Educational institutions have been offering annuity contracts to their faculty since the early 1900s. The practice

Retirement Plans 101: An Introduction to Section 403(b) 2008 Giller & Calhoun LLC I. Overview Educational institutions have been offering annuity contracts to their faculty since the early 1900s. The practice

and Fees and Expenses as of December 31, About Fees and Expenses What s Inside Expenses

Important Information About Your Investment Options, Fees, and Other Expenses for the DXC Matched Asset Plan Annual Information Statement on Investment Options What s Inside and Fees and Expenses as of

Important Information About Your Investment Options, Fees, and Other Expenses for the DXC Matched Asset Plan Annual Information Statement on Investment Options What s Inside and Fees and Expenses as of

The Cost of Doing Nothing: Examples of 401(k) Fee Disclosure in Action (Inaction)

Fee Disclosure in Action (Inaction)") The Cost of Doing Nothing: Examples of 401(k) Fee Disclosure in Action (Inaction) Michael Kiley and Emily Hooyman February 21, 2013 CompuPay is registered with the National Association of State Boards

The Cost of Doing Nothing: Examples of 401(k) Fee Disclosure in Action (Inaction) Michael Kiley and Emily Hooyman February 21, 2013 CompuPay is registered with the National Association of State Boards

First Data Corporation Incentive Savings Plan Summary Plan Description

First Data Corporation Incentive Savings Plan Summary Plan Description January 2017 This document is being provided exclusively by your employer, which retains responsibility for the content. 300465376

First Data Corporation Incentive Savings Plan Summary Plan Description January 2017 This document is being provided exclusively by your employer, which retains responsibility for the content. 300465376

SUMMARY PLAN DESCRIPTION FOR. Harford County Public Schools 403(b) Plan

Plan") SUMMARY PLAN DESCRIPTION FOR 1-1-2015 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description of Plan Article 4... Plan Contributions

SUMMARY PLAN DESCRIPTION FOR 1-1-2015 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description of Plan Article 4... Plan Contributions

Employee Benefits and Qualified Plan Update

Employee Benefits and Qualified Plan Update Sonya D. Wright, CFP, CEBS, QKA First, a Quiz... There will be prizes! Getting to Know You! Percentage of your business in qualified retirement plans? Securities

Employee Benefits and Qualified Plan Update Sonya D. Wright, CFP, CEBS, QKA First, a Quiz... There will be prizes! Getting to Know You! Percentage of your business in qualified retirement plans? Securities

Participant Disclosures: A Guide for Plan Administrators

Participant Disclosures: A Guide for Plan Administrators Table of Contents: Understanding the Impact of the Participant Disclosure Regulations... 2 Summary of the New Requirements... 3 Plan Administrator

Participant Disclosures: A Guide for Plan Administrators Table of Contents: Understanding the Impact of the Participant Disclosure Regulations... 2 Summary of the New Requirements... 3 Plan Administrator

1. Plan Documents 2. ERISA Fidelity Bond 3. Government/Regulatory Requirements and Communications 4. Journals and Ledgers

This Fiduciary Audit File Checklist is intended to be a general guide for assisting 401(k) plan fiduciaries in developing a plan documentation file. We believe that a fiduciary s primary responsibility

This Fiduciary Audit File Checklist is intended to be a general guide for assisting 401(k) plan fiduciaries in developing a plan documentation file. We believe that a fiduciary s primary responsibility

Getting Ready for the 2009 Form 5500

Getting Ready for the 2009 Form 5500 Part Three of a Three-Part Series: Understanding the Report of Indirect Compensation We have prepared this list of frequently asked questions ( FAQs ) for the benefit

Getting Ready for the 2009 Form 5500 Part Three of a Three-Part Series: Understanding the Report of Indirect Compensation We have prepared this list of frequently asked questions ( FAQs ) for the benefit

plan sponsor checklist for ERISA 403(b) plans

plans") plan sponsor checklist for ERISA 403(b) plans Keeping Your ERISA 403(b) Plan and Its Operation Compliant This correspondence contains: ERISA 403(b) Plans Annual Requirements At-a-Glance Plan Sponsor Checklist

plan sponsor checklist for ERISA 403(b) plans Keeping Your ERISA 403(b) Plan and Its Operation Compliant This correspondence contains: ERISA 403(b) Plans Annual Requirements At-a-Glance Plan Sponsor Checklist

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

October 16, 2003 CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing Required or Repeal of multiple-use test

October 16, 2003 CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing Required or Repeal of multiple-use test

Qualified Retirement Plan. Summary Plan Description Individual Standardized 401(k) Plan

Plan") Qualified Retirement Plan Summary Plan Description Individual Standardized 401(k) Plan Individual Standardized 401(k) Plan Summary Plan Description Plan Name: Your Employer has adopted the qualified retirement

Qualified Retirement Plan Summary Plan Description Individual Standardized 401(k) Plan Individual Standardized 401(k) Plan Summary Plan Description Plan Name: Your Employer has adopted the qualified retirement

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

DOL Conflict of Interest Proposal: What to Expect?

DOL Conflict of Interest Proposal: What to Expect? Brought to you by the Advanced Consulting Group of Nationwide Nationwide, the Nationwide N and Eagle and Nationwide is on your side are service marks

DOL Conflict of Interest Proposal: What to Expect? Brought to you by the Advanced Consulting Group of Nationwide Nationwide, the Nationwide N and Eagle and Nationwide is on your side are service marks

404a-5 Plan & Investment Notice

404a-5 Plan & Investment Notice Saving for retirement is an important part of your financial planning. And your company-sponsored retirement plan with John Hancock is a convenient way to help you save

404a-5 Plan & Investment Notice Saving for retirement is an important part of your financial planning. And your company-sponsored retirement plan with John Hancock is a convenient way to help you save

Retirement Plan Update

Retirement Plan Update What is a Legitimate Expense for a Plan to Pay? The Department of Labor (DOL) has rules as to what types of expenses a plan sponsor can pay from a retirement plan. This Retirement

Retirement Plan Update What is a Legitimate Expense for a Plan to Pay? The Department of Labor (DOL) has rules as to what types of expenses a plan sponsor can pay from a retirement plan. This Retirement

401(k) Advantage, LLC 401(k) Plan Disclosure & Comparative Chart for Retirement Plan Participants

Advantage, LLC 401(k) Plan Disclosure & Comparative Chart for Retirement Plan Participants") 401(k) Advantage, LLC 401(k) Plan Disclosure & Comparative Chart for Retirement Plan Participants All individuals who have the right to direct investments in an employer-sponsored retirement plan are being

401(k) Advantage, LLC 401(k) Plan Disclosure & Comparative Chart for Retirement Plan Participants All individuals who have the right to direct investments in an employer-sponsored retirement plan are being

ERISA FIDUCIARY BASICS AND BEST PRACTICES

Presents ERISA FIDUCIARY BASICS AND BEST PRACTICES November 5, 2015 Misty A. Leon mleon@wifilawgroup.com COMPLIANCE 101 General Roles and Responsibilities Who's Involved? Plan Administrator Responsibilities

Presents ERISA FIDUCIARY BASICS AND BEST PRACTICES November 5, 2015 Misty A. Leon mleon@wifilawgroup.com COMPLIANCE 101 General Roles and Responsibilities Who's Involved? Plan Administrator Responsibilities

IMPORTANT INFORMATION Regarding Your BB&T Corporation 401(k) Savings Plan

Savings Plan") BB&T Corporation 200 West Second Street 10th Floor Winston Salem, NC 27101 IMPORTANT INFORMATION Regarding Your BB&T Corporation 401(k) Savings Plan CONTENTS A message about this packet page 1 Qualified

BB&T Corporation 200 West Second Street 10th Floor Winston Salem, NC 27101 IMPORTANT INFORMATION Regarding Your BB&T Corporation 401(k) Savings Plan CONTENTS A message about this packet page 1 Qualified

EMPLOYEE BENEFITS & EXECUTIVE COMPENSATION

EMPLOYEE BENEFITS & EXECUTIVE COMPENSATION February 2011 Disclosure of Fees Received by Retirement Plan Service Providers. PRACTICE LEADER Paul W. Holloway pholloway@hselaw.com PARTNERS Thomas J. Hurley

EMPLOYEE BENEFITS & EXECUTIVE COMPENSATION February 2011 Disclosure of Fees Received by Retirement Plan Service Providers. PRACTICE LEADER Paul W. Holloway pholloway@hselaw.com PARTNERS Thomas J. Hurley

Hartford Retirement Services, LLC. Recordkeeper Plus. Form 5500 Schedule C. Reporting Package

Hartford Retirement Services, LLC Recordkeeper Plus Form 5500 Schedule C Reporting Package Table of Contents 2009 Schedule C Reporting: Introduction...3 COMPENSATION THAT MAY BE REPORTABLE ON THE SCHEDULE

Hartford Retirement Services, LLC Recordkeeper Plus Form 5500 Schedule C Reporting Package Table of Contents 2009 Schedule C Reporting: Introduction...3 COMPENSATION THAT MAY BE REPORTABLE ON THE SCHEDULE

Summary Plan Description of the The MidwestHR, LLC 401(k) and Profit Sharing Plan For Employees of Bird in the Hand Staffing, LLC ( Plan )

and Profit Sharing Plan For Employees of Bird in the Hand Staffing, LLC ( Plan )") Summary Plan Description of the The MidwestHR, LLC 401(k) and Profit Sharing Plan For Employees of Bird in the Hand Staffing, LLC ( Plan ) NOTICE: The provisions described in this Summary Plan Description

Summary Plan Description of the The MidwestHR, LLC 401(k) and Profit Sharing Plan For Employees of Bird in the Hand Staffing, LLC ( Plan ) NOTICE: The provisions described in this Summary Plan Description

employee savings investment plan (ESIP) summary plan description effective january 1, 2017 human energy. yours. TM

summary plan description effective january 1, 2017 human energy. yours. TM") employee savings investment plan (ESIP) summary plan description effective january 1, 2017 human energy. yours. TM This summary plan description (SPD) describes the Chevron ( the plan or the ESIP ). It

employee savings investment plan (ESIP) summary plan description effective january 1, 2017 human energy. yours. TM This summary plan description (SPD) describes the Chevron ( the plan or the ESIP ). It

Overview of Defined Contribution Plan Design

Overview of Defined Contribution Plan Design September 6, 2016 Mutual of America Your Retirement Company Chris Conway Sr. Regional Vice President & Abbas Moloo Vice President MUTUAL OF AMERICA California

Overview of Defined Contribution Plan Design September 6, 2016 Mutual of America Your Retirement Company Chris Conway Sr. Regional Vice President & Abbas Moloo Vice President MUTUAL OF AMERICA California

The Best Asset Allocation Solution for Retirement Plan Participants: Model Portfolios, Managed Accounts or CIFs?

The Best Asset Allocation Solution for Retirement Plan Participants: Model Portfolios, Managed Accounts or CIFs? A White Paper Prepared by The Wagner Law Group On Behalf of Hand Benefits & Trust Company

The Best Asset Allocation Solution for Retirement Plan Participants: Model Portfolios, Managed Accounts or CIFs? A White Paper Prepared by The Wagner Law Group On Behalf of Hand Benefits & Trust Company

Synergy Services 401(k) Plan 2012 Disclosure & Comparative Chart for Retirement Plan Participants

Plan 2012 Disclosure & Comparative Chart for Retirement Plan Participants") Synergy Services 401(k) Plan 2012 Disclosure & Comparative Chart for Retirement Plan Participants All individuals who have the right to direct investments in an employer-sponsored retirement plan are being

Synergy Services 401(k) Plan 2012 Disclosure & Comparative Chart for Retirement Plan Participants All individuals who have the right to direct investments in an employer-sponsored retirement plan are being

A Look At 401(k) Plan Fees

Plan Fees") 1 of 6 7/30/2009 6:49 AM July 30, 2009 DOL > EBSA > Publications > A Look At 401(k) Plan Fees A Look At 401(k) Plan Fees Printer Friendly Version PDF Version Introduction Employee Benefits Security Administration

1 of 6 7/30/2009 6:49 AM July 30, 2009 DOL > EBSA > Publications > A Look At 401(k) Plan Fees A Look At 401(k) Plan Fees Printer Friendly Version PDF Version Introduction Employee Benefits Security Administration

2018 Retirement Plans

2018 Retirement Plans Harvard Medical Faculty Physicians at BIDMC, Inc. 401(k) Savings and Investment Plan Harvard Medical Faculty Physicians at BIDMC, Inc. Retirement Plan Table of Contents Section A:

2018 Retirement Plans Harvard Medical Faculty Physicians at BIDMC, Inc. 401(k) Savings and Investment Plan Harvard Medical Faculty Physicians at BIDMC, Inc. Retirement Plan Table of Contents Section A:

SUMMARY PLAN DESCRIPTION FOR. Florida Tech Retirement Plan

SUMMARY PLAN DESCRIPTION FOR 1-1-2018 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description of Plan Article 4... Plan Contributions

SUMMARY PLAN DESCRIPTION FOR 1-1-2018 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description of Plan Article 4... Plan Contributions

INTEGRATING ERISA INTO YOUR COMPLIANCE SYSTEMS. May 7, Marcia S. Wagner, Esq.

INTEGRATING ERISA INTO YOUR COMPLIANCE SYSTEMS May 7, 2012 Marcia S. Wagner, Esq. The Wagner Law Group A Professional Corporation 99 Summer Street, 13 th Floor Boston, MA 02110 Tel: (617) 357-5200 Fax:

INTEGRATING ERISA INTO YOUR COMPLIANCE SYSTEMS May 7, 2012 Marcia S. Wagner, Esq. The Wagner Law Group A Professional Corporation 99 Summer Street, 13 th Floor Boston, MA 02110 Tel: (617) 357-5200 Fax:

Vendor to Plan Sponsor Fee Disclosure

Vendor to Plan Sponsor Fee Disclosure New vendor to plan sponsor fee disclosure rules are scheduled to go into effect on April 1, 2012. 1 The new rules apply to most employee benefit plans and will require

Vendor to Plan Sponsor Fee Disclosure New vendor to plan sponsor fee disclosure rules are scheduled to go into effect on April 1, 2012. 1 The new rules apply to most employee benefit plans and will require

Managing Fiduciary Risk Under ERISA: A Primer for Employers, HR Directors, and Plan Administrators. Copyright

Managing Fiduciary Risk Under ERISA: A Primer for Employers, HR Directors, and Plan Administrators Copyright 2011 1 Presenters Gregory L. Ash, JD Partner gash@spencerfane.com 913.327.5115 Julia M. Vander

Managing Fiduciary Risk Under ERISA: A Primer for Employers, HR Directors, and Plan Administrators Copyright 2011 1 Presenters Gregory L. Ash, JD Partner gash@spencerfane.com 913.327.5115 Julia M. Vander

Qualified Retirement Plan. Adoption Agreement Individual Standardized 401(k) Plan

Plan") Qualified Retirement Plan Adoption Agreement Individual Standardized 401(k) Plan A Guide to Establishing a Qualified Retirement Plan Getting Started Once you ve decided to establish a qualified retirement

Qualified Retirement Plan Adoption Agreement Individual Standardized 401(k) Plan A Guide to Establishing a Qualified Retirement Plan Getting Started Once you ve decided to establish a qualified retirement

Proof of Fee Disclosure -An Example

Proof of Fee Disclosure -An Example Plan sponsor review of service provider arrangements required by ERISA 408(b)(2) June 2011 Federal Reserve Plaza 600 Atlantic Ave, FL 30 Boston, MA 02210 617.723.6400

Proof of Fee Disclosure -An Example Plan sponsor review of service provider arrangements required by ERISA 408(b)(2) June 2011 Federal Reserve Plaza 600 Atlantic Ave, FL 30 Boston, MA 02210 617.723.6400

Retirement Plan Update: Court Decisions, SEC and DOL Guidance, and More FRED REISH, ESQ.

Retirement Plan Update: Court Decisions, SEC and DOL Guidance, and More FRED REISH, ESQ. April 7, 2016 1 DOL Regulatory Agenda Pension Benefit Statements As part of this initiative, the Department will

Retirement Plan Update: Court Decisions, SEC and DOL Guidance, and More FRED REISH, ESQ. April 7, 2016 1 DOL Regulatory Agenda Pension Benefit Statements As part of this initiative, the Department will

A guide to the fiduciary role in a retirement plan

Retirement Plan Solutions Content provided by: Compliments of TD Ameritrade Institutional A guide to the fiduciary role in a retirement plan Understanding your status, supporting plan sponsors as fiduciaries,

Retirement Plan Solutions Content provided by: Compliments of TD Ameritrade Institutional A guide to the fiduciary role in a retirement plan Understanding your status, supporting plan sponsors as fiduciaries,

Qualified Retirement Plan

Qualified Retirement Plan Standardized Adoption Agreement PO Box 2760 Omaha, NE 68103-2760 Fax: 866-468-6268 SIMPLIFIED PROFIT SHARING PLAN KEY INFORMATION WHEN ESTABLISHING A QUALIFIED RETIREMENT PLAN

Qualified Retirement Plan Standardized Adoption Agreement PO Box 2760 Omaha, NE 68103-2760 Fax: 866-468-6268 SIMPLIFIED PROFIT SHARING PLAN KEY INFORMATION WHEN ESTABLISHING A QUALIFIED RETIREMENT PLAN

Liberty Mutual 401(k) Plan Annual Fee Disclosure Statement

Plan Annual Fee Disclosure Statement") Liberty Mutual 401(k) Plan Annual Fee Disclosure Statement Important information about Your Options, Fees and Other Expenses The Liberty Mutual 401(k) Plan (the Plan ) is a great way to build savings for

Liberty Mutual 401(k) Plan Annual Fee Disclosure Statement Important information about Your Options, Fees and Other Expenses The Liberty Mutual 401(k) Plan (the Plan ) is a great way to build savings for

John Hancock s ERISA 408(b)(2) Disclosure

(2) Disclosure") John Hancock s ERISA 408(b)(2) Disclosure John Hancock Life Insurance Company (U.S.A.) and John Hancock Life Insurance Company or New York are collectively referred to as John Hancock. Page 1 The following

John Hancock s ERISA 408(b)(2) Disclosure John Hancock Life Insurance Company (U.S.A.) and John Hancock Life Insurance Company or New York are collectively referred to as John Hancock. Page 1 The following

Unblurring the Lines: Understanding the Roles of Investment Providers

Unblurring the Lines: Understanding the Roles of Investment Providers Workshop 32 Monday, October 19, 2015 2:15 p.m. 3:30 p.m. Speaker: Virginia Sutton, QKA 1 Investment Provider Roles This session will

Unblurring the Lines: Understanding the Roles of Investment Providers Workshop 32 Monday, October 19, 2015 2:15 p.m. 3:30 p.m. Speaker: Virginia Sutton, QKA 1 Investment Provider Roles This session will

DOL Survival Guide and Top Ten 401(k) Pitfalls

Pitfalls") DOL Survival Guide and Top Ten 401(k) Pitfalls Presented by CohnReznick s Government Contracting Industry Practice Sandy Wendler, Manager and Travis Dutton, Principal, Lockton Retirement Services PLEASE

DOL Survival Guide and Top Ten 401(k) Pitfalls Presented by CohnReznick s Government Contracting Industry Practice Sandy Wendler, Manager and Travis Dutton, Principal, Lockton Retirement Services PLEASE

403(b) Glossary 401(k) Plan: 403(b) Plan: 457(b) Plan (Governmental):

Glossary 401(k) Plan: 403(b) Plan: 457(b) Plan (Governmental):") 403(b) Glossary 1. 401(k) Plan: A retirement savings plan which permits employees to make voluntarily contributions of amounts that have not already been paid or made available to them. It is named for

403(b) Glossary 1. 401(k) Plan: A retirement savings plan which permits employees to make voluntarily contributions of amounts that have not already been paid or made available to them. It is named for

Summary Plan Description

The American Red Cross Savings Plan Summary Plan Description Take Charge of Your Savings Contents Contents A Quick Look at the Savings Plan 3 Participating In the Savings Plan 4 Eligibility 4 Enrollment

The American Red Cross Savings Plan Summary Plan Description Take Charge of Your Savings Contents Contents A Quick Look at the Savings Plan 3 Participating In the Savings Plan 4 Eligibility 4 Enrollment

Fiduciary Guide. How to Help Meet Your Retirement Plan Fiduciary Responsibilities. ADP Retirement Services

ADP Retirement Services Fiduciary Guide How to Help Meet Your Retirement Plan Fiduciary Responsibilities FOR PLAN SPONSOR/FINANCIAL ADVISOR USE ONLY NOT FOR DISTRIBUTION TO THE PUBLIC. Who Are Plan Fiduciaries?

ADP Retirement Services Fiduciary Guide How to Help Meet Your Retirement Plan Fiduciary Responsibilities FOR PLAN SPONSOR/FINANCIAL ADVISOR USE ONLY NOT FOR DISTRIBUTION TO THE PUBLIC. Who Are Plan Fiduciaries?

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

Workshop 47: Revenue Streams from the Non-Profit Space. Susan D. Diehl, QKA, CPC, ERPA President, PenServ Plan Services, Inc.

Workshop 47: Revenue Streams from the Non-Profit Space Susan D. Diehl, QKA, CPC, ERPA President, PenServ Plan Services, Inc. Agenda for Today Market Opportunities in the Nonprofit Space Discovering New

Workshop 47: Revenue Streams from the Non-Profit Space Susan D. Diehl, QKA, CPC, ERPA President, PenServ Plan Services, Inc. Agenda for Today Market Opportunities in the Nonprofit Space Discovering New

SUMMARY PLAN DESCRIPTION. Of the. Arthritis Foundation Defined Contribution Retirement Plan Revised January 1, 2013

SUMMARY PLAN DESCRIPTION Of the Arthritis Foundation Defined Contribution Retirement Plan Revised January 1, 2013 TABLE OF CONTENTS INTRODUCTION...1 PART I- Information about the Plan...2 1. Information

SUMMARY PLAN DESCRIPTION Of the Arthritis Foundation Defined Contribution Retirement Plan Revised January 1, 2013 TABLE OF CONTENTS INTRODUCTION...1 PART I- Information about the Plan...2 1. Information

SUMMARY PLAN DESCRIPTION FOR. Independent Support Services, Inc. 403(b) Plan

Plan") SUMMARY PLAN DESCRIPTION FOR Independent Support Services, Inc. 403(b) Plan 1-1-2018 Table of Contents Article 1...Introduction Article 2...General Plan Information and Key Definitions Article 3...Description

SUMMARY PLAN DESCRIPTION FOR Independent Support Services, Inc. 403(b) Plan 1-1-2018 Table of Contents Article 1...Introduction Article 2...General Plan Information and Key Definitions Article 3...Description

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors

Thank You For Your Participation This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors www.spencerfane.com www.ubabenefits.com

Thank You For Your Participation This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors www.spencerfane.com www.ubabenefits.com

Managed Accounts in 401(k) Plans: Solution or Fad. Linda Ruiz-Zaiko Bridgebay Financial, Inc.

Plans: Solution or Fad. Linda Ruiz-Zaiko Bridgebay Financial, Inc.") Managed Accounts in 401(k) Plans: Solution or Fad Linda Ruiz-Zaiko Bridgebay Financial, Inc. www.bridgebay.com US Retirement Assets 36% of US Household Financial Assets IRAs $7.2 Trillion FERS $0.4 Trillion

Managed Accounts in 401(k) Plans: Solution or Fad Linda Ruiz-Zaiko Bridgebay Financial, Inc. www.bridgebay.com US Retirement Assets 36% of US Household Financial Assets IRAs $7.2 Trillion FERS $0.4 Trillion

CREATING A CULTURE OF FIDUCIARY RESPONSIBILITY

CREATING A CULTURE OF FIDUCIARY RESPONSIBILITY Presented by: Mark Hogan Regional Director Pentegra Retirement Services July 2016 Our Difference. Your Advantage. IN THE NEWS How Lawsuits Are Reshaping 401(k)

CREATING A CULTURE OF FIDUCIARY RESPONSIBILITY Presented by: Mark Hogan Regional Director Pentegra Retirement Services July 2016 Our Difference. Your Advantage. IN THE NEWS How Lawsuits Are Reshaping 401(k)

General Information for 401k Plan Participant

General Information for 401k Plan Participant Welcome to our 401(k) Guide for the Plan Participant! The information contained on this site was designed and developed by various governmental agencies, and

General Information for 401k Plan Participant Welcome to our 401(k) Guide for the Plan Participant! The information contained on this site was designed and developed by various governmental agencies, and

Source 4 Solutions, LLC 401(k) Plan Disclosure & Comparative Chart for Retirement Plan Participants

Plan Disclosure & Comparative Chart for Retirement Plan Participants") Source 4 Solutions, LLC 401(k) Plan Disclosure & Comparative Chart for Retirement Plan Participants All individuals who have the right to direct investments in an employer-sponsored retirement plan are

Source 4 Solutions, LLC 401(k) Plan Disclosure & Comparative Chart for Retirement Plan Participants All individuals who have the right to direct investments in an employer-sponsored retirement plan are