Participant Fee Disclosures for ERISA Plans

|

|

|

- Sharleen Tucker

- 5 years ago

- Views:

Transcription

1 Participant Fee Disclosures for ERISA Plans

2 About MetLife MetLife, Inc. (NYSE: MET), through its subsidiaries and affiliates ( MetLife ), is one of the largest life insurance companies in the world. Founded in 1868, MetLife is a global provider of life insurance, annuities, employee benefits and asset management. Serving approximately 100 million customers, MetLife has operations in nearly 50 countries and holds leading market positions in Japan, Latin America, Asia, Europe and the Middle East. For more information, visit Why MetLife Prepared This Paper At MetLife, we re committed to provide you with ongoing communications to help you make informed decisions regarding your defined contribution plans. We build on this tradition by delivering leading insights through nationally acclaimed research, subject matter experts and educational resources. We serve as a leading voice on employee benefits by actively influencing public policy, educating the media and developing intelligent product solutions. We hope you find this material helpful as you look to meet your fiduciary responsibilities. In addition to this paper, we have prepared other in-depth discussions covering topics ranging from Universal Availability Requirements to IRS Audit Results, with an emphasis on the potential impact on your retirement plan. You can view these and other resources at our 403(b) Resource Center at

3 Retirement benefits have changed dramatically over the past thirty years. There has been a gradual shift away from employer-provided defined benefit retirement plans. Many employees now rely more on their employers defined contribution plans to help build financial security for their lives as retirees. As a result, greater responsibility is being placed on plan participants to ensure their retirement security. Recognizing these trends, the U.S. Department of Labor (DOL or the Department) published a regulation on October 20, 2010, charging ERISA plan administrators with responsibilities regarding participant fee disclosures. The goal of the regulation is to ensure that all participants and beneficiaries in ERISA participantdirected individual account plans have the information needed to make informed decisions about their retirement plan investment choices. While an ERISA plan administrator is the party responsible for complying with this regulation, plan recordkeepers and providers associated with the plan s investment options may be able to provide assistance. Portions of the regulation contain disclosures similar to those which some plan administrators have historically provided to participants through a combination of quarterly participant statements, enrollment guides, summary plan descriptions and prospectuses. One significant difference between what may have been furnished to participants in the past versus the regulation is that the regulation requires the disclosure of investment-related performance and fee information in a comparative format on a prescribed, more frequent basis. Effective July 1, 2012, the 408(b)(2) regulation requires certain categories of service providers to ERISA employee pension benefit plans to make disclosures about the direct and indirect compensation they receive for their services. The regulation sets fee disclosure standards for plan service providers, resulting in a more clear and consistent communication of fees across the service provider community. While an ERISA plan administrator is the party responsible for complying with this regulation, plan recordkeepers and providers associated with the plan s investment options may be able to provide assistance. The purpose of this paper is to help plan administrators understand and prepare for their responsibilities associated with the participant fee disclosure regulation. The first disclosure was to be furnished to participants no later than August 30, The purpose of this paper is to help you understand the DOL 408(b)(2) regulation and how it affects your role as a plan fiduciary. 1

4 Background In recent years, the DOL has issued fee disclosure rules and regulations in three separate phases covering both plan sponsor and participant disclosures. These regulations have effectively increased the types and detail of required disclosures. Phase One: In 2009, the DOL amended the ERISA 5500 (annual return/report) Schedule C rules by requiring plan sponsors to report additional details on compensation received by pension and welfare plan service providers. If plan administrators act in good faith based on a reasonable interpretation of the regulations, enforcement by the DOL will generally not be necessary. Phase Two: On October 20, 2010, the DOL expanded the scope of its efforts for greater fee transparency to include participants and charged ERISA plan administrators with the responsibility to comply. These participant fee disclosure rules are intended to: 1) give participants an overview of a plan s investment options, inform them of the mechanics of investing in the options and identify designated investment managers for those options; 2) provide an explanation of general plan fees, as well as those charges that may be made against a participant s individual plan account; and 3) allow participants to compare current investment performance against benchmarks and help them manage their investment selections. Phase Three: On February 3, 2012, the DOL issued the 408(b)(2) Final Regulation defining what information plan service providers must furnish to plan fiduciaries regarding their fees and services. This regulation supplements the changes in Phase One to achieve greater fee transparency and ensure plan fiduciaries have the information they need to monitor their service providers. Participant Fee Disclosure Requirements Definition of Participant Under the regulation, plan administrators will need to deliver the required disclosures and investment information to: Current plan participants Employees who are eligible to participate but are not contributing Beneficiaries who can direct the investments in their accounts (by reason of the death of the participant) Individuals who obtain rights to a participant s plan account under a Qualified Domestic Relations Order (QDRO) 2

5 Types of Disclosures The regulation defines the specific details that must be disclosed to plan participants. Applicable to all participant-directed plans regardless of size, the regulation calls for two broad categories of information that must be disclosed to participants by plan administrators: Plan-Related Investment-Related Plan-Related Information The regulation calls for plan administrators to affirmatively disclose three categories of plan-related information to participants: 1. General Plan Info rmation: A description of the structure and mechanics of the plan including: - a current list of the plan s investment options; - an explanation of how participants may direct their investment choices; - any limitations on transfers to or from an investment option; - the exercise of (and any restrictions on) voting, tender and similar rights; - the identity of any designated investment managers; and - a description of any brokerage windows, self-directed brokerage accounts or similar plan arrangements that enable participants to select investments beyond those designated by the plan. 2. Administrative Expenses: An explanation of any general fees and expenses that may be charged to, or deducted from, all individual participant accounts. The general expenses may include fees for legal, accounting and recordkeeping services, and are not reflected in the total annual operating expenses of any designated investment alternative. The basis on which charges will be assessed against each account (e.g., pro rata, per capita) must be disclosed. 3. Individual Expenses: A description of any fees that may be charged to, or deducted from, the individual participant s account based on the actions taken by that participant so long as the fees are not reflected in the total annual operating expenses of the respective designated investment alternative. These expenses may include charges for plan loans, processing QDROs, fees for investment advice, brokerage windows, redemption fees and similar expenses. 3

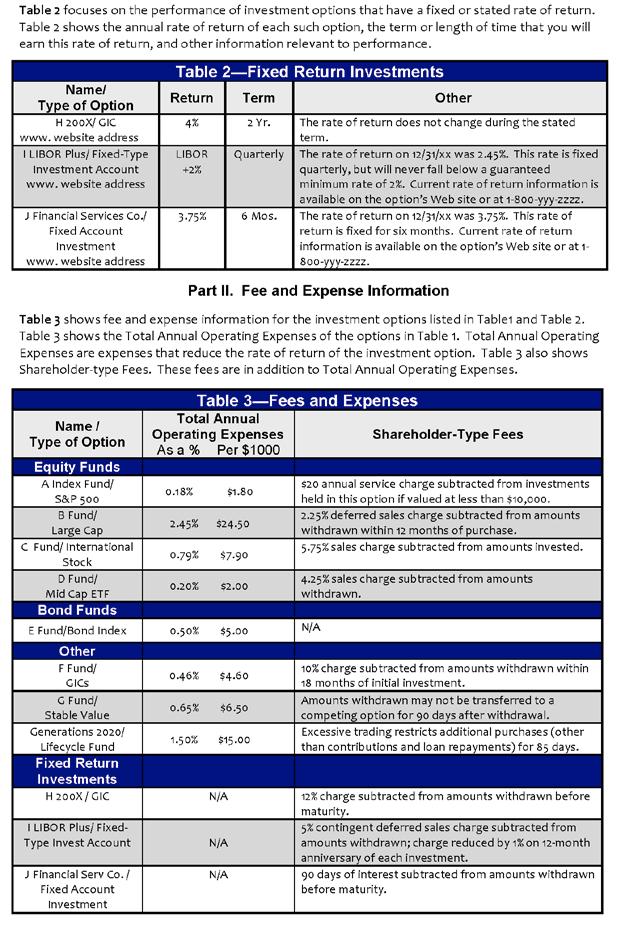

6 Investment-Related Information It is critical for participants to be able to make a comparison of investmentrelated information, including performance, fees and expenses. To facilitate this, the regulation requires that information regarding each investment option available under the plan be furnished in a similar format. The regulation also specifies that the disclosed information must be written in a manner that will be understood by the average person. In effect, this will enable participants to make a better apples-to-apples comparison of the plan s investment choices. A plan administrator must furnish these disclosures even with respect to investment options that are closed to new money, but only to those participants who remain invested in that option. The investment-related information can be found in the service provider fee disclosure document that service providers must have furnished (if within the control of, or reasonably available to the service provider) to the plan administrator, according to the DOL s 408(b)(2) Final Regulation. The disclosed information must be written in a manner that will be understood by the average person. Model Comparative Chart To assist plan administrators with meeting the requirements for disclosing investment-related information, the DOL developed a Model Comparative Chart, which can be viewed at the end of this white paper and at gov/ebsa/participantfeerulemodelchart.doc. According to the DOL, when correctly completed, this chart may be used by plan administrators to satisfy the requirement that a plan s investment options be provided in a comparative format. Regardless of whether the Model Comparative Chart is used in its exact form or another form of disclosure is developed, plan administrators should work closely with legal counsel to ensure that regulatory requirements regarding the disclosure are being met. Plan administrators may furnish multiple comparative charts or documents that are supplied by the plan s various service providers or investment issuers, provided all of the comparative charts or documents are furnished to participants at the same time in a single mailing or transmission and the comparative charts or documents are designed to facilitate a comparison among the investment options available under the plan. information that plan administrators must disclose to participants and beneficiaries: Performance Information, Fee and Expense Information, and Special Disclosure Requirements. Introduction The Model Comparative Chart begins with an introductory paragraph that directs participants to the website address(es) for each investment option and the plan administrator s name, address and telephone number. It informs participants that a hard copy of the investment option information on the website(s) can be obtained and states who the participant can contact to receive this disclosure. Part I Performance Information 4 The first part of the Model Comparative Chart allows the plan administrator to disclose investment performance information on variable return and fixed return investments and must include: Identifying Information: The name of each investment option under the plan and the type or asset class for each investment (e.g., money market fund, balanced fund, large cap stock fund).

7 Performance Data: Information about historical performance for variable return investments over 1, 5, and 10-year periods (or for the life of the investment, if shorter) with a statement that past performance is not necessarily an indication of how the investment will perform in the future. For fixed return investments, the fixed or stated annual rate of return, and the term must be disclosed, and information regarding the issuer s right to adjust the fixed or stated rate of return prospectively, if applicable. Benchmarks: Plan administrators are required to benchmark each investment option in the plan. The provided information should show participants and beneficiaries how the plan options have performed over time and allow the participant to compare the investment options with appropriate benchmarks for the same time period. For variable return investments, a broad-based index (e.g., S&P 500) with 1, 5, and 10-year returns (or the life of the investment, if shorter) must be provided as a benchmark for comparison purposes. The benchmark cannot be administered by an affiliate of the investment provider, its adviser, or a principal underwriter, unless the index is widely recognized and used. A blend of various benchmarks may be used to reflect the composition of blended investments such as balanced and target date funds. Investments with a fixed rate of return are not required to provide this information. Example of Performance-Related Information With No Fixed Rate of Return Part II Fee and Expense Information The second part of the Model Comparative Chart details the total annual operating expenses and shareholder type fees (such as sales loads or redemption fees) for the identified investment options. The total annual operating expenses of the investment must be shown as a percentage (i.e.,expense ratio) and as a dollar amount per $1,000 invested. Restrictions or limitations regarding the purchase, transfer or withdrawal of the investment, in whole or in part, must also be disclosed. Further, there must be a statement indicating that fees and expenses are only one of several factors that participants and beneficiaries should consider when making investment decisions, and a statement that the cumulative effect of fees and expenses can substantially reduce the growth of a participant s retirement account. Also, a statement is required advising that the participant can visit the DOL Employee Benefits Security Administration website for an example demonstrating the long-term effect of fees and expenses. For fixed return investments, the regulation requires a statement of the amount and a description of any shareholder-type fees, restriction or limitation regarding the purchase, transfer or withdrawal of the investment, in whole or in part. Example of Fees and Expense Information 5

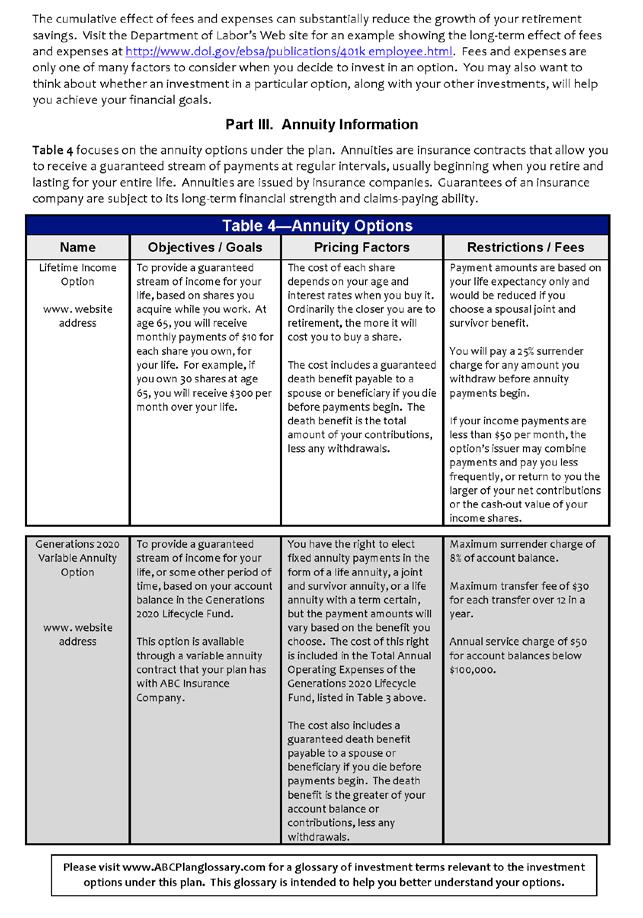

8 Part III Special Disclosure Requirements The third part of the Model Comparative Chart focuses on information relating to any annuity options under the plan. Annuities: If participants can allocate contributions toward the future purchase of a stream of income payments guaranteed by an insurance company, special annuity-related disclosures must be delivered to plan participants and beneficiaries, including: - the name of the annuity contract, fund or product; - the annuity s investment objective (e.g., fixed income payments for life); - the benefits and factors that will determine the price of the guaranteed income payments; - any limitations on the ability of the participant or beneficiary to withdraw or transfer funds from the annuity, as well as any fees for withdrawals or transfers; - any fees, such as administrative fees, sales charges or surrender charges that will reduce the value of amounts contributed to the annuity by participants and beneficiaries; - a statement about the insurance company s guarantees being subject to its long-term financial strength and claims-paying ability; and - a website with additional information about the annuity. Employer Securities: If company stock funds are included as a participant-directed plan investment option, special disclosure requirements apply. They are, however, generally exempt from disclosing fees and expenses, the portfolio turnover rate, and the total operating expenses expressed as a percentage, unless the employer securities option is a fund where participants or beneficiaries acquire units of participation rather than actual shares of employer stock. Timing and Frequency of Communications The information in the following table summarizes the plan administrator s timing requirements for delivering the investment option information disclosures: 6 Communication New Participant Disclosure Annual Disclosure Update of Plan Information Quarterly Statements Participant Request Frequency Plan and investment information must be furnished to participants on or before the date they first direct their contributions to a particular investment. Plan and investment information must be furnished to participants at least annually, or once in any 12-month period thereafter. This will include any eligible employees who are not contributing to the plan. In FAB , the DOL stated that under extraordinary circumstances, the ERISA fiduciary duty of prudence and loyalty may require the plan administrator to inform participants of important changes to investment-related information before the next comparative chart is required. Any changes to plan information in the New Participant or Annual Disclosure must be given at least 30 days, but not more than 90 days prior to any changes. Quarterly statements must be sent to each participant (except as noted below) describing the actual dollar amount of the administrative and individual investment expenses charged to the participant s account during the preceding quarter. Accordingly, eligible, but non-contributing participants will not receive a quarterly statement because no contributions were made to the plan on their behalf. If a participant requests, the plan administrator must provide supplemental information relating to the plan s investment options. Examples include: prospectuses, financial statements and unit/share values.

9 Effective Date The initial disclosures (i.e., all disclosures other than disclosures required at least quarterly) were to be provided to participants in the prescribed format no later than August 30, The first required disclosure date for quarterly statements reflecting fees and expenses actually deducted was no later than November 14, Other Requirements Internet Website The regulation requires plan administrators to furnish participants with access to an Internet website, which provides specific investment option information. The website must be specific enough to provide participants with access to the information in a manner consistent with certain SEC forms 2 and lead the participant, without difficulty, to the following supplemental, investment-related information: - the name of the issuer of each investment option; - the goals and objectives of the investment option; - the investment option s principal strategies (including a general description of the types of assets held by the investment option) and principal risks; - the investment option s turnover rate; - performance data updated on a quarterly basis, or more frequently if required by other applicable law; and Initial disclosures were provided to participants in the new prescribed format by August 30, related fees and expenses for investment options. While the regulation does not require plan administrators to furnish more than one comparative chart annually to participants, fee and expense information made available on the website must be accurate and updated as reasonably possible following a change. In addition, procedures for updating the information must be in place and the website(s) information must also be available in a paper format. Glossary The disclosure must either include a general glossary of terms to help participants understand the plan s investment options or a website(s) address(es) that will provide on-line access to a glossary of terms. Mandated Disclosure Requirement In the past, plan administrators often made information on plan fees and investments generally available to plan participants by providing this information on the employer s Intranet website or the website of a third party administrator. However, under this new regulation, merely posting this information on the employer s, a third party administrator s or other plan service provider s website is not sufficient. The plan administrator must proactively and regularly furnish these disclosures. 7

10 Electronic Delivery DOL issued a technical release which provides guidance on using electronic delivery to satisfy the disclosure requirements of this regulation. Generally, electronic delivery of the participant fee disclosures is permitted as long as the participant consents to electronic delivery or uses a computer regularly at work to perform their job duties. Paper copies will be required for everyone else. Fiduciary Breaches The new regulation requires plan administrators to provide an annual disclosure notice to all eligible participants. Violations of this regulation will result in an ERISA fiduciary breach. While plan administrators have a fiduciary responsibility to comply with the required disclosures, they will not be held liable for any deficiencies in the information furnished to participants if they reasonably relied on the data received from the plan s service providers. It is important to emphasize that this regulation does not relieve fiduciaries of their responsibility to prudently select and monitor providers of services to the plan or the investment options offered under the plan. 8

11 Participant Fee Disclosure Checklist 3 3 Consult with your legal counsel to discuss the regulation and your specific obligations and responsibilities under it. Become familiar with the DOL Model Comparative Chart so that you understand the different components of information that must be disclosed Meet with your service provider(s) and begin discussions on the availability and retrieval of the investment-related and expense information. Research your data sources to make sure you can identify all participants, eligible employees and beneficiaries that need to receive the disclosures. Consider the additional costs that may need to be incurred to fulfill the annual notice requirement. Develop a communication program and secure resources to help you execute the program. Summary As an industry leader, MetLife agrees that participants need the information contained in the disclosures to make informed decisions and become more engaged in planning for their retirement. To help you communicate this information to participants, we have developed tools and resources that you can view by visting the Fee Disclosure section of the Resource Center on the Plan Service Center (mlr.metlife.com). Participants need the information contained in the disclosures to make informed decisions and become more engaged in planning for their retirement. 9

12 Appendix: DOL Model Comparative Chart

13

14

15 1 This is 60 (sixty) days after the July 1, 2012 effective date of the service provider fee disclosure final rule. 2 Securities and Exchange Commission Forms N-1A or N-3, as appropriate. Neither MetLife, its affiliates, nor its representatives or agents are permitted to give legal, ERISA or tax advice. Any discussion of taxes included in or related to this material is for general informational purposes only, and is based on our understanding of the ERISA, tax and other applicable law as of this printing. Such discussion does not purport to be complete or to cover every situation. Tax, ERISA and other applicable laws are subject to change and to different interpretation. Customers and other interested parties should consult with their own tax, ERISA and other legal advisers to determine how these laws impact them. MetLife Resources is a division of Metropolitan Life Insurance Company ( MetLife ), 200 Park Avenue, New York, NY Metropolitan Life Insurance Company New York, NY metlife.com MLR L [0319] 2017 METLIFE, INC

Final Regulation on Participant-Level Fee Disclosures. By: Andrew Varady, Esq. Associate General Counsel, MetLife

Final Regulation on Participant-Level Fee Disclosures By: Andrew Varady, Esq. Associate General Counsel, MetLife Contents 1 Introduction 2 Background 2 New Participant-Level Fee Disclosure Requirements

Final Regulation on Participant-Level Fee Disclosures By: Andrew Varady, Esq. Associate General Counsel, MetLife Contents 1 Introduction 2 Background 2 New Participant-Level Fee Disclosure Requirements

GINGER B. LACHAPELLE, ESQ. BLITMAN & KING LLP

GINGER B. LACHAPELLE, ESQ. BLITMAN & KING LLP FINAL RULE On October 14, 2010, the DOL released final regulations under Section 404(a) of ERISA relating to the disclosure of fee and other information to

GINGER B. LACHAPELLE, ESQ. BLITMAN & KING LLP FINAL RULE On October 14, 2010, the DOL released final regulations under Section 404(a) of ERISA relating to the disclosure of fee and other information to

Date: October 25, 2010 TCRS : Department Of Labor Final Regulations Relating To Participant Fee Disclosure

**** UPDATE: As of February 3, 2012, the DOL has extended the 408(b)(2) effective date to July 1, 2012 and the 404(a) effective date to generally be August 30, 2012. See TCRS 2012-01 memo for details.

**** UPDATE: As of February 3, 2012, the DOL has extended the 408(b)(2) effective date to July 1, 2012 and the 404(a) effective date to generally be August 30, 2012. See TCRS 2012-01 memo for details.

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals.

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. TOPIC: Final Retirement Plan Participant Level Fee Disclosure

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. TOPIC: Final Retirement Plan Participant Level Fee Disclosure

SUMMARY OF FINAL RULE ON FIDUCIARY REQUIREMENTS FOR DISCLOSURE IN PARTICIPANT-DIRECTED INDIVIDUAL ACCOUNT PLANS. February 6, 2012

THE PLAN SPONSOR COUNCIL OF AMERICA Serving Retirement Plan Sponsors for More than 60 Years 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863.7272 ferrigno@401k.org Edward Ferrigno Vice President,

THE PLAN SPONSOR COUNCIL OF AMERICA Serving Retirement Plan Sponsors for More than 60 Years 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863.7272 ferrigno@401k.org Edward Ferrigno Vice President,

Benefits. DOL Fee Disclosure Regulations: What Plan Sponsors Need to Know

Benefits cus Employer Update DOL Fee Disclosure Regulations: What Plan Sponsors Need to Know October 2011 Retirement plan fees and their impact on the retirement savings of plan participants is a topic

Benefits cus Employer Update DOL Fee Disclosure Regulations: What Plan Sponsors Need to Know October 2011 Retirement plan fees and their impact on the retirement savings of plan participants is a topic

Final Regulation on Service Provider Fee Disclosures for ERISA Retirement Plans

Final Regulation on Service Provider Fee Disclosures for ERISA Retirement Plans About MetLife For over 140 years, MetLife has been one of the country s most trusted financial institutions. The MetLife

Final Regulation on Service Provider Fee Disclosures for ERISA Retirement Plans About MetLife For over 140 years, MetLife has been one of the country s most trusted financial institutions. The MetLife

Regulation on service provider fee disclosures for ERISA retirement plans

Regulation on service provider fee disclosures for ERISA retirement plans 2 About MetLife Resources MetLife Resources is the Division of Metropolitan Life Insurance Company that specializes in providing

Regulation on service provider fee disclosures for ERISA retirement plans 2 About MetLife Resources MetLife Resources is the Division of Metropolitan Life Insurance Company that specializes in providing

Attachment to Special Bulletin a 5 Fiduciary requirements for disclosure in participant-directed individual account plans.

2550.404a 5 Fiduciary requirements for disclosure in participant-directed individual account plans. TABLE OF CONTENTS 2550.404A 5 FIDUCIARY REQUIREMENTS FOR DISCLOSURE IN PARTICIPANT- DIRECTED INDIVIDUAL

2550.404a 5 Fiduciary requirements for disclosure in participant-directed individual account plans. TABLE OF CONTENTS 2550.404A 5 FIDUCIARY REQUIREMENTS FOR DISCLOSURE IN PARTICIPANT- DIRECTED INDIVIDUAL

Fiduciary Guide. Helping to protect your plan. MetLife Resources

Fiduciary Guide Helping to protect your plan. MetLife Resources Table of Contents Introduction.... 1 MetLife s Commitment.... 2 Know Your Fiduciary Responsibilities... 3 ERISA Plan Fiduciary Checklist...

Fiduciary Guide Helping to protect your plan. MetLife Resources Table of Contents Introduction.... 1 MetLife s Commitment.... 2 Know Your Fiduciary Responsibilities... 3 ERISA Plan Fiduciary Checklist...

404(c) and OTHER ISSUES

and OTHER ISSUES") 401(k) INVESTMENT ISSUES 404(c) and OTHER ISSUES SUSAN P. SEROTA All rights reserved Pillsbury Winthrop Shaw Pittman LLP New York, New York August, 2008 Fiduciary Responsibilities Who is a Fiduciary? A

401(k) INVESTMENT ISSUES 404(c) and OTHER ISSUES SUSAN P. SEROTA All rights reserved Pillsbury Winthrop Shaw Pittman LLP New York, New York August, 2008 Fiduciary Responsibilities Who is a Fiduciary? A

404(c) and 404a-5 Checklist

and 404a-5 Checklist") 404(c) and 404a-5 Checklist Plan Sponsor: Plan Name(s): Record Keeper: Advisor: Overview The new participant disclosure regulation under ERISA 404a-5 requires the plan fiduciary 1 to furnish much of the

404(c) and 404a-5 Checklist Plan Sponsor: Plan Name(s): Record Keeper: Advisor: Overview The new participant disclosure regulation under ERISA 404a-5 requires the plan fiduciary 1 to furnish much of the

ARE YOU READY FOR NEW DOL FEE DISCLOSURE RULES?

ARE YOU READY FOR NEW DOL FEE DISCLOSURE RULES? (updated June 2, 2011) ANTHONY J. KOLENIC, JR. JUSTIN W. STEMPLE GEORGE L. WHITFIELD 2011 Warner Norcross & Judd LLP. All rights reserved. Agenda General

ARE YOU READY FOR NEW DOL FEE DISCLOSURE RULES? (updated June 2, 2011) ANTHONY J. KOLENIC, JR. JUSTIN W. STEMPLE GEORGE L. WHITFIELD 2011 Warner Norcross & Judd LLP. All rights reserved. Agenda General

Fee Disclosure Q&A for Employers September 2014

Fee Disclosure Q&A for Employers September 2014 The Department of Labor (DOL) has issued two sets of final regulations requiring the disclosure of fees and expenses under plans governed by the Employee

Fee Disclosure Q&A for Employers September 2014 The Department of Labor (DOL) has issued two sets of final regulations requiring the disclosure of fees and expenses under plans governed by the Employee

408(b)(2) Checklist. IS YOUR PLAN COVERED? Plans not Covered. Covered Plans

(2) Checklist. IS YOUR PLAN COVERED? Plans not Covered. Covered Plans") 408(b)(2) Checklist Responsible Plan Fiduciary Duties Under Section 408(b)(2) of the Employee Retirement Income Security Act of 1974 (ERISA): 1. Determine if your plan is covered under the regulation 2.

408(b)(2) Checklist Responsible Plan Fiduciary Duties Under Section 408(b)(2) of the Employee Retirement Income Security Act of 1974 (ERISA): 1. Determine if your plan is covered under the regulation 2.

U.S. Department of Labor FIELD ASSISTANCE BULLETIN NO DATE: MAY 7, 2012 MEMORANDUM FOR: SUBJECT: BACKGROUND

U.S. Department of Labor Employee Benefits Security Administration Washington, DC 20210 FIELD ASSISTANCE BULLETIN NO. 2012-02 DATE: MAY 7, 2012 MEMORANDUM FOR: MABEL CAPOLONGO, DIRECTOR OF ENFORCEMENT

U.S. Department of Labor Employee Benefits Security Administration Washington, DC 20210 FIELD ASSISTANCE BULLETIN NO. 2012-02 DATE: MAY 7, 2012 MEMORANDUM FOR: MABEL CAPOLONGO, DIRECTOR OF ENFORCEMENT

New FAQs Provide Participant Fee Disclosure Guidance. Next Steps for Plan Sponsors September 2012

New FAQs Provide Participant Fee Disclosure Guidance Next Steps for Plan Sponsors September 2012 Table of Contents New FAQs Provide Participant Fee Disclosure Guidance Next Steps for Plan Sponsors 2 Good

New FAQs Provide Participant Fee Disclosure Guidance Next Steps for Plan Sponsors September 2012 Table of Contents New FAQs Provide Participant Fee Disclosure Guidance Next Steps for Plan Sponsors 2 Good

CHAPTER 2 DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2)

(2) DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2)") CHAPTER 2 DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) Following the release of the Interim Final we now have the Final, Final Section 408(b)(2) Regulations.

CHAPTER 2 DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) DOL FINAL REGULATIONS ON ERISA SECTION 408(b)(2) Following the release of the Interim Final we now have the Final, Final Section 408(b)(2) Regulations.

plan sponsor checklist for ERISA 403(b) plans

plans") plan sponsor checklist for ERISA 403(b) plans Keeping Your ERISA 403(b) Plan and Its Operation Compliant This correspondence contains: ERISA 403(b) Plans Annual Requirements At-a-Glance Plan Sponsor Checklist

plan sponsor checklist for ERISA 403(b) plans Keeping Your ERISA 403(b) Plan and Its Operation Compliant This correspondence contains: ERISA 403(b) Plans Annual Requirements At-a-Glance Plan Sponsor Checklist

404(a) annual participant fee disclosure Frequently asked questions

annual participant fee disclosure Frequently asked questions") 404(a) annual participant fee disclosure Frequently asked questions Assisting plan sponsors Q1. What must the plan sponsor of an ERISAgoverned plan do to comply with the 404(a) participant fee disclosure

404(a) annual participant fee disclosure Frequently asked questions Assisting plan sponsors Q1. What must the plan sponsor of an ERISAgoverned plan do to comply with the 404(a) participant fee disclosure

Participant Disclosures: A Guide for Plan Administrators

Participant Disclosures: A Guide for Plan Administrators Table of Contents: Understanding the Impact of the Participant Disclosure Regulations... 2 Summary of the New Requirements... 3 Plan Administrator

Participant Disclosures: A Guide for Plan Administrators Table of Contents: Understanding the Impact of the Participant Disclosure Regulations... 2 Summary of the New Requirements... 3 Plan Administrator

Establishing a Due Diligence File

resource edge TM Establishing a Due Diligence File investment insights practice building solutions retirement resources RESOURCE EDGE TM Table of Contents 3 Introduction 4 401(k) fiduciary documentation

resource edge TM Establishing a Due Diligence File investment insights practice building solutions retirement resources RESOURCE EDGE TM Table of Contents 3 Introduction 4 401(k) fiduciary documentation

Perspectives AN EXECUTIVE COMPENSATION, BENEFITS & HUMAN RESOURCES LAW UPDATE

Volume 3, Edition 1 AN EXECUTIVE COMPENSATION, BENEFITS & HUMAN RESOURCES LAW UPDATE IN THIS EDITION... Compliance Deadlines This issue of provides a comprehensive discussion of the final Department of

Volume 3, Edition 1 AN EXECUTIVE COMPENSATION, BENEFITS & HUMAN RESOURCES LAW UPDATE IN THIS EDITION... Compliance Deadlines This issue of provides a comprehensive discussion of the final Department of

Understanding Fiduciary Responsibilities

making it personal Understanding Fiduciary Responsibilities for plan sponsors every step of the way GET TO KNOW OUR FIDUCIARY RESPONSIBILITIES Products and financial services provided by American United

making it personal Understanding Fiduciary Responsibilities for plan sponsors every step of the way GET TO KNOW OUR FIDUCIARY RESPONSIBILITIES Products and financial services provided by American United

Roadmap to Understanding Retirement Plan Fees. The only guide you need

Roadmap to Understanding Retirement Plan Fees The only guide you need Executive Summary Retirement plan fees under the spotlight You know there are costs associated with offering a retirement plan, but

Roadmap to Understanding Retirement Plan Fees The only guide you need Executive Summary Retirement plan fees under the spotlight You know there are costs associated with offering a retirement plan, but

By Lisa Taggart and Joni Andrioff. Participant disclosure rules are effective. Service provider disclosure rules are effective

A Timely Analysis of Legal Developments A S A P June 6, 2012 DOL s Recent Guidance on New Participant Fee Disclosure Regulations Is a Must Read for Retirement Plan Fiduciaries Preparing for the August

A Timely Analysis of Legal Developments A S A P June 6, 2012 DOL s Recent Guidance on New Participant Fee Disclosure Regulations Is a Must Read for Retirement Plan Fiduciaries Preparing for the August

Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013

and 403(b) Plan Sponsors in 2013") Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013 Presented by: Rose Panico-Marino, AIF, ERPA, QPA Senior Vice President January 30, 2013 Learning Objectives Review specific

Managing Employer Fiduciary Issues for 401(k) and 403(b) Plan Sponsors in 2013 Presented by: Rose Panico-Marino, AIF, ERPA, QPA Senior Vice President January 30, 2013 Learning Objectives Review specific

AUTOMATIC ENROLLMENT 401(k) PLANS. for Small Businesses

PLANS. for Small Businesses") AUTOMATIC ENROLLMENT 401(k) PLANS for Small Businesses Automatic Enrollment 401(k) Plans for Small Businesses is a joint project of the U.S. Department of Labor s Employee Benefits Security Administration

AUTOMATIC ENROLLMENT 401(k) PLANS for Small Businesses Automatic Enrollment 401(k) Plans for Small Businesses is a joint project of the U.S. Department of Labor s Employee Benefits Security Administration

PARTICIPANT FEE DISCLOSURE UNDERSTANDING YOUR RESPONSIBILITIES AS A PLAN SPONSOR

PARTICIPANT FEE DISCLOSURE UNDERSTANDING YOUR RESPONSIBILITIES AS A PLAN SPONSOR In October of 2010, in an effort to help participants make more informed decisions, the Department of Labor ( DOL ) finalized

PARTICIPANT FEE DISCLOSURE UNDERSTANDING YOUR RESPONSIBILITIES AS A PLAN SPONSOR In October of 2010, in an effort to help participants make more informed decisions, the Department of Labor ( DOL ) finalized

SUMMARY OF THE 401(k) FAIR DISCLOSURE FOR RETIREMENT SECURITY ACT OF

FAIR DISCLOSURE FOR RETIREMENT SECURITY ACT OF") SUMMARY OF THE 401(k) FAIR DISCLOSURE FOR RETIREMENT SECURITY ACT OF 2007 1 PREPARED BY THE BENEFITS GROUP OF DAVIS AND HARMAN, LLP OVERVIEW IN GENERAL The Employee Retirement Income Security Act of 1974

SUMMARY OF THE 401(k) FAIR DISCLOSURE FOR RETIREMENT SECURITY ACT OF 2007 1 PREPARED BY THE BENEFITS GROUP OF DAVIS AND HARMAN, LLP OVERVIEW IN GENERAL The Employee Retirement Income Security Act of 1974

Dear Participant: Please refer to Part IV of the attached document for information on who to call with questions.

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

MINIMIZING RISK AND MAXIMIZING OUTCOMES

MINIMIZING RISK AND MAXIMIZING OUTCOMES BASIC REQUIREMENTS AND BEST PRACTICES FOR TODAY S PLAN SPONSORS APRIL 2010 The emerging retirement agenda in Washington seeks to expand retirement plan participation,

MINIMIZING RISK AND MAXIMIZING OUTCOMES BASIC REQUIREMENTS AND BEST PRACTICES FOR TODAY S PLAN SPONSORS APRIL 2010 The emerging retirement agenda in Washington seeks to expand retirement plan participation,

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

This Employer Webinar Series program is presented by Spencer Fane Britt & Browne LLP in conjunction with United Benefit Advisors This Employer Webinar Series program is presented by Spencer Fane Britt

Plan Fee Disclosure for the Retirement Plan Fiduciary Rule 408b-2

Plan Fee Disclosure for the Retirement Plan Fiduciary Rule 408b-2 From The Union Central Life Insurance Company July 15, 2013 OZARK MOTOR LINES INC 401K PLAN ATTN: MIKE HOPPER PO BOX 181077 MEMPHIS, TN

Plan Fee Disclosure for the Retirement Plan Fiduciary Rule 408b-2 From The Union Central Life Insurance Company July 15, 2013 OZARK MOTOR LINES INC 401K PLAN ATTN: MIKE HOPPER PO BOX 181077 MEMPHIS, TN

The Fiduciary Duty of Participant Disclosures

The Fiduciary Duty of Participant Disclosures Kevin A. Wiggins, Esq. Thorp Reed & Armstrong, LLP One Oxford Centre 301 Grant Street, 14 th Floor Pittsburgh, PA 15219 412-394-2401 kwiggins@thorpreed.com

The Fiduciary Duty of Participant Disclosures Kevin A. Wiggins, Esq. Thorp Reed & Armstrong, LLP One Oxford Centre 301 Grant Street, 14 th Floor Pittsburgh, PA 15219 412-394-2401 kwiggins@thorpreed.com

Soltis Investment Advisors Fiduciary Education

Soltis Investment Advisors Fiduciary Education November 2017 Kim D. Anderson, AIF Managing Partner, Retirement Plan Services Soltis Investment Advisors is proud to be among the first investment advisors

Soltis Investment Advisors Fiduciary Education November 2017 Kim D. Anderson, AIF Managing Partner, Retirement Plan Services Soltis Investment Advisors is proud to be among the first investment advisors

How-To Guide for the. Plan and Investment Disclosure

How-To Guide for the Plan and Investment Disclosure Reviewing Your Disclosure T. Rowe Price has created this guide to assist you with reviewing the 2017 Plan and Investment Disclosure for your Plan(s).

How-To Guide for the Plan and Investment Disclosure Reviewing Your Disclosure T. Rowe Price has created this guide to assist you with reviewing the 2017 Plan and Investment Disclosure for your Plan(s).

PHILLIPS 66 SAVINGS PLAN Plan Number Plan Information as of 08/11/2012

PHILLIPS 66 SAVINGS PLAN Plan Number 099066 Plan Information as of 08/11/2012 This notice includes important information to help you compare the investment options under your retirement plan. If you want

PHILLIPS 66 SAVINGS PLAN Plan Number 099066 Plan Information as of 08/11/2012 This notice includes important information to help you compare the investment options under your retirement plan. If you want

Service Provider Compensation Disclosure under Section 408(b)(2) of ERISA

(2) of ERISA") EXECUTIVE COMPENSATION & EMPLOYEE BENEFITS CLIENT PUBLICATION August 17, 2010... Service Provider Compensation Disclosure under Section 408(b)(2) of ERISA... On July 16, 2010, the U.S. Department of Labor

EXECUTIVE COMPENSATION & EMPLOYEE BENEFITS CLIENT PUBLICATION August 17, 2010... Service Provider Compensation Disclosure under Section 408(b)(2) of ERISA... On July 16, 2010, the U.S. Department of Labor

Morgan Stanley Smith Barney Fiduciary Audit File

Morgan Stanley Smith Barney Fiduciary Audit File Helping plan sponsors manage their responsibility smithbarney.com IN THIS GUIDE Introduction Documents Government Reporting Service-Provider Agreements

Morgan Stanley Smith Barney Fiduciary Audit File Helping plan sponsors manage their responsibility smithbarney.com IN THIS GUIDE Introduction Documents Government Reporting Service-Provider Agreements

The Definition of a Fiduciary - The Times They are a Changin

The Definition of a Fiduciary - The Times They are a Changin Bob Kaplan, CFP, CPC QPA, APA VP, National Training Consultant www.ing.com Important Information CIRCULAR 230 DISCLOSURE: Any tax discussion

The Definition of a Fiduciary - The Times They are a Changin Bob Kaplan, CFP, CPC QPA, APA VP, National Training Consultant www.ing.com Important Information CIRCULAR 230 DISCLOSURE: Any tax discussion

EMPLOYEE BENEFITS AND EXECUTIVE COMPENSATION

EMPLOYEE BENEFITS AND EXECUTIVE COMPENSATION ATTORNEY ADVERTISING DOL DELAYS APPLICATION OF SERVICE PROVIDER FEE DISCLOSURE RULES UNTIL JANUARY 1, 2012 By: Mark A. Holdsworth, Esq. April 6, 2011 Introduction

EMPLOYEE BENEFITS AND EXECUTIVE COMPENSATION ATTORNEY ADVERTISING DOL DELAYS APPLICATION OF SERVICE PROVIDER FEE DISCLOSURE RULES UNTIL JANUARY 1, 2012 By: Mark A. Holdsworth, Esq. April 6, 2011 Introduction

FIDUCIARY DEVELOPMENTS, PLAN FEES AND VENDOR SEARCHES. General Fiduciary Guidelines Regarding Fees. Controlling Law

FIDUCIARY DEVELOPMENTS, PLAN FEES AND VENDOR SEARCHES May 21, 2014 General Fiduciary Guidelines Regarding Fees Controlling Law ERISA imposes procedural and substantive duties on fiduciaries of employee

FIDUCIARY DEVELOPMENTS, PLAN FEES AND VENDOR SEARCHES May 21, 2014 General Fiduciary Guidelines Regarding Fees Controlling Law ERISA imposes procedural and substantive duties on fiduciaries of employee

MetLife Resources Participant Online Registration

MetLife Resources Participant Online Registration How to enroll online in your Employer-Sponsored Retirement Savings Plan In just a few short steps, you will be on your way to saving for your future. 1

MetLife Resources Participant Online Registration How to enroll online in your Employer-Sponsored Retirement Savings Plan In just a few short steps, you will be on your way to saving for your future. 1

Participant Disclosure of Plan and Investment Related Information

Participant Disclosure of Plan and Investment Related Information The XXXX Co. 401(k) Retirement Savings Account Plan Participating in The XXXX Co. 401(k) Retirement Savings Account Plan can be one of

Participant Disclosure of Plan and Investment Related Information The XXXX Co. 401(k) Retirement Savings Account Plan Participating in The XXXX Co. 401(k) Retirement Savings Account Plan can be one of

DOL Releases Final Disclosure Regulations for Participant-Directed Individual Account Plans. October 26, 2010

DOL Releases Final Disclosure Regulations for Participant-Directed Individual Account Plans October 26, 2010 On October 14, the Department of Labor (DOL) released final regulations that will impose new

DOL Releases Final Disclosure Regulations for Participant-Directed Individual Account Plans October 26, 2010 On October 14, the Department of Labor (DOL) released final regulations that will impose new

Fiduciary 3(16) Services: How to Survive in the New Fiduciary World

Services: How to Survive in the New Fiduciary World") Fiduciary 3(16) Services: How to Survive in the New Fiduciary World Jean Ackerman, Department of Labor Heather B. Abrigo, Esq., Drinker Biddle & Reath LLP Russell Hooker, Nova 401(k) Associates Heather

Fiduciary 3(16) Services: How to Survive in the New Fiduciary World Jean Ackerman, Department of Labor Heather B. Abrigo, Esq., Drinker Biddle & Reath LLP Russell Hooker, Nova 401(k) Associates Heather

US Department of Labor Issues Final Rule on Service Provider Fee Disclosure

Legal Update February 21, 2012 US Department of Labor Issues Final Rule on Service Provider Fee Disclosure On February 3, 2012, the US Department of Labor (DOL) issued a final rule (the Final Rule) amending

Legal Update February 21, 2012 US Department of Labor Issues Final Rule on Service Provider Fee Disclosure On February 3, 2012, the US Department of Labor (DOL) issued a final rule (the Final Rule) amending

NOTICE OF AUTOMATIC ENROLLMENT AND INVESTMENT MACY S, INC. 401(k) RETIREMENT INVESTMENT PLAN

RETIREMENT INVESTMENT PLAN") NOTICE OF AUTOMATIC ENROLLMENT AND INVESTMENT MACY S, INC. 401(k) RETIREMENT INVESTMENT PLAN This notice informs you of the automatic enrollment feature of the 401(k) Plan. Because you may have been subject

NOTICE OF AUTOMATIC ENROLLMENT AND INVESTMENT MACY S, INC. 401(k) RETIREMENT INVESTMENT PLAN This notice informs you of the automatic enrollment feature of the 401(k) Plan. Because you may have been subject

SUMMARY OF THE DEPARTMENT OF LABOR FINAL RULE UNDER SECTION 408(b)(2) SERVICE PROVIDER FEE DISCLOSURE. February 6, 2012

(2) SERVICE PROVIDER FEE DISCLOSURE. February 6, 2012") THE PLAN SPONSOR COUNCIL OF AMERICA Serving Retirement Plan Sponsors for More than 60 Years 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863.7272 ferrigno@401k.org Edward Ferrigno Vice President,

THE PLAN SPONSOR COUNCIL OF AMERICA Serving Retirement Plan Sponsors for More than 60 Years 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863.7272 ferrigno@401k.org Edward Ferrigno Vice President,

Fiduciary Investment Guide

Fiduciary Investment Guide Helping to make it easier to understand fiduciary responsibilities. For employer use only. Not to be used with the public. Voya Financial is here to help you understand and navigate

Fiduciary Investment Guide Helping to make it easier to understand fiduciary responsibilities. For employer use only. Not to be used with the public. Voya Financial is here to help you understand and navigate

Fee Disclosure in Defined Contribution Retirement Plans: Background and Legislation

Fee Disclosure in Defined Contribution Retirement Plans: Background and Legislation John J. Topoleski Analyst in Income Security January 29, 2010 Congressional Research Service CRS Report for Congress

Fee Disclosure in Defined Contribution Retirement Plans: Background and Legislation John J. Topoleski Analyst in Income Security January 29, 2010 Congressional Research Service CRS Report for Congress

Investment Recommendations Covered Under the Rule

U.S. Department of Labor Employee Benefits Security Administration January 2017 Set out below are a number of Frequently Asked Questions (FAQs) regarding implementation of the conflict of interest (COI)

U.S. Department of Labor Employee Benefits Security Administration January 2017 Set out below are a number of Frequently Asked Questions (FAQs) regarding implementation of the conflict of interest (COI)

Retirement Plan Update: Court Decisions, SEC and DOL Guidance, and More FRED REISH, ESQ.

Retirement Plan Update: Court Decisions, SEC and DOL Guidance, and More FRED REISH, ESQ. April 7, 2016 1 DOL Regulatory Agenda Pension Benefit Statements As part of this initiative, the Department will

Retirement Plan Update: Court Decisions, SEC and DOL Guidance, and More FRED REISH, ESQ. April 7, 2016 1 DOL Regulatory Agenda Pension Benefit Statements As part of this initiative, the Department will

John Hancock s ERISA 408(b)(2) Disclosure

(2) Disclosure") John Hancock s ERISA 408(b)(2) Disclosure John Hancock Life Insurance Company (U.S.A.) and John Hancock Life Insurance Company or New York are collectively referred to as John Hancock. Page 1 The following

John Hancock s ERISA 408(b)(2) Disclosure John Hancock Life Insurance Company (U.S.A.) and John Hancock Life Insurance Company or New York are collectively referred to as John Hancock. Page 1 The following

Diocese of Palm Beach, Inc. 403(b) Plan IMPORTANT INFORMATION REGARDING YOUR PLAN TA

Plan IMPORTANT INFORMATION REGARDING YOUR PLAN TA") 1 Diocese of Palm Beach, Inc. 403(b) Plan IMPORTANT INFORMATION REGARDING YOUR PLAN TA069778 00001 We want you to enjoy the many features and benefits of your retirement plan. We also want to make sure

1 Diocese of Palm Beach, Inc. 403(b) Plan IMPORTANT INFORMATION REGARDING YOUR PLAN TA069778 00001 We want you to enjoy the many features and benefits of your retirement plan. We also want to make sure

Participant Fee Disclosure

Participant Fee Disclosure From The Union Central Life Insurance Company August 14, 2012 OZARK MOTOR LINES INC 401K PLAN PO BOX 181077 MEMPHIS, TN 38181-1077 776841 08/14/2012 Services and Fees Disclosure

Participant Fee Disclosure From The Union Central Life Insurance Company August 14, 2012 OZARK MOTOR LINES INC 401K PLAN PO BOX 181077 MEMPHIS, TN 38181-1077 776841 08/14/2012 Services and Fees Disclosure

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES 1 Today s Agenda Understand where ERISA applies to retirement

Know and Control Your Risk with Retirement Plans PHILLIP LONG, VP EMPLOYEE BENEFIT LEGAL SERVICES BB&T RETIREMENT AND INSTITUTIONAL SERVICES 1 Today s Agenda Understand where ERISA applies to retirement

The New Fee Disclosure Rules: What You Need to Do About 408(b)(2)

(2)") ederated The New Fee Disclosure Rules: What You Need to Do About 408(b)(2) What You Need to Do About 408(b)(2) Are You Ready? On April 1, 2012, the rules governing every 401(k) and every private pension

ederated The New Fee Disclosure Rules: What You Need to Do About 408(b)(2) What You Need to Do About 408(b)(2) Are You Ready? On April 1, 2012, the rules governing every 401(k) and every private pension

Participant Disclosure of Plan and Investment Related Information

Participant Disclosure of Plan and Investment Related Information MidAmerican Energy Company Retirement Savings Plan Participating in the MidAmerican Energy Company Retirement Savings Plan can be one of

Participant Disclosure of Plan and Investment Related Information MidAmerican Energy Company Retirement Savings Plan Participating in the MidAmerican Energy Company Retirement Savings Plan can be one of

Participant Fee Disclosure

Participant Fee Disclosure From Ameritas Life Insurance Corp. July 15, 2014 OZARK MOTOR LINES INC 401K PLAN PO BOX 181077 MEMPHIS, TN 38181-1077 776841 07/15/2014 Services and Fees Disclosure Background

Participant Fee Disclosure From Ameritas Life Insurance Corp. July 15, 2014 OZARK MOTOR LINES INC 401K PLAN PO BOX 181077 MEMPHIS, TN 38181-1077 776841 07/15/2014 Services and Fees Disclosure Background

Managing fiduciary responsibility for plan sponsors

Managing fiduciary responsibility for plan sponsors Invesco PlanForward Foundations SM Putting fiduciary responsibility in action Contents 1 Defining fiduciary responsibility 4 Maximizing fiduciary protection

Managing fiduciary responsibility for plan sponsors Invesco PlanForward Foundations SM Putting fiduciary responsibility in action Contents 1 Defining fiduciary responsibility 4 Maximizing fiduciary protection

Overview of Defined Contribution Plan Design

Overview of Defined Contribution Plan Design September 6, 2016 Mutual of America Your Retirement Company Chris Conway Sr. Regional Vice President & Abbas Moloo Vice President MUTUAL OF AMERICA California

Overview of Defined Contribution Plan Design September 6, 2016 Mutual of America Your Retirement Company Chris Conway Sr. Regional Vice President & Abbas Moloo Vice President MUTUAL OF AMERICA California

Retirement Plan Update

Retirement Plan Update What is a Legitimate Expense for a Plan to Pay? The Department of Labor (DOL) has rules as to what types of expenses a plan sponsor can pay from a retirement plan. This Retirement

Retirement Plan Update What is a Legitimate Expense for a Plan to Pay? The Department of Labor (DOL) has rules as to what types of expenses a plan sponsor can pay from a retirement plan. This Retirement

SAMPLE OF INVESTMENT POLICY STATEMENT

TIAA-CREF Investment Services OF INVESTMENT POLICY STATEMENT FOR THE (PLAN NAME) This document is for sample purposes only. Please review with your legal counsel or Advisor. TABLE OF CONTENTS SECTIONS

TIAA-CREF Investment Services OF INVESTMENT POLICY STATEMENT FOR THE (PLAN NAME) This document is for sample purposes only. Please review with your legal counsel or Advisor. TABLE OF CONTENTS SECTIONS

Service Provider Fee Disclosure

Service Provider Fee Disclosure ERISA 408(b)(2) Regulations AU MEDICAL CENTER, INC. AU MEDICAL CENTER, INC. 403B RETIREMENT SAVINGS PLAN VALIC Mutual Fund Platform The Employee Retirement Income Security

Service Provider Fee Disclosure ERISA 408(b)(2) Regulations AU MEDICAL CENTER, INC. AU MEDICAL CENTER, INC. 403B RETIREMENT SAVINGS PLAN VALIC Mutual Fund Platform The Employee Retirement Income Security

How-To Guide for the. Plan and Investment Disclosure

How-To Guide for the Plan and Investment Disclosure T. Rowe Price has created this guide to assist you with reviewing and approving the annual participant disclosures. Using this guide will assist you

How-To Guide for the Plan and Investment Disclosure T. Rowe Price has created this guide to assist you with reviewing and approving the annual participant disclosures. Using this guide will assist you

University of Southern California Hospital 401(k) Retirement Plan

Retirement Plan") Required Disclosure Information University of Southern California Hospital 401(k) Retirement Plan Participant Disclosure Notice IMPORTANT PLAN AND INVESTMENT- RELATED INFORMATION Produced on July 10, 2017.

Required Disclosure Information University of Southern California Hospital 401(k) Retirement Plan Participant Disclosure Notice IMPORTANT PLAN AND INVESTMENT- RELATED INFORMATION Produced on July 10, 2017.

DOL ISSUES FINAL QDIA GUIDANCE October 26, 2007

THE PROFIT SHARING AND 401(k) ADVOCATE SHARING THE COMMITMENT SINCE 1947 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863 7272 ferrigno@401k.org Edward Ferrigno Vice President, Washington

THE PROFIT SHARING AND 401(k) ADVOCATE SHARING THE COMMITMENT SINCE 1947 500 Eighth Street, NW, Suite 210, Washington, DC 20004 202.863 7272 ferrigno@401k.org Edward Ferrigno Vice President, Washington

Fiduciary Fundamentals

Fiduciary Fundamentals Basics and Best Practices RETIREMENT & BENEFIT PLAN SERVICES At Bank of America Merrill Lynch, we understand the important role that you, the plan fiduciary, serve in maintaining

Fiduciary Fundamentals Basics and Best Practices RETIREMENT & BENEFIT PLAN SERVICES At Bank of America Merrill Lynch, we understand the important role that you, the plan fiduciary, serve in maintaining

THE SAVINGS PLAN OF SAUDI ARABIAN OIL COMPANY Plan Number Plan Information as of 05/24/2017

THE SAVINGS PLAN OF SAUDI ARABIAN OIL COMPANY Plan Number 091353 Plan Information as of 05/24/2017 This legally required notice includes important information about the investment options under your retirement

THE SAVINGS PLAN OF SAUDI ARABIAN OIL COMPANY Plan Number 091353 Plan Information as of 05/24/2017 This legally required notice includes important information about the investment options under your retirement

Proof of Fee Disclosure -An Example

Proof of Fee Disclosure -An Example Plan sponsor review of service provider arrangements required by ERISA 408(b)(2) June 2011 Federal Reserve Plaza 600 Atlantic Ave, FL 30 Boston, MA 02210 617.723.6400

Proof of Fee Disclosure -An Example Plan sponsor review of service provider arrangements required by ERISA 408(b)(2) June 2011 Federal Reserve Plaza 600 Atlantic Ave, FL 30 Boston, MA 02210 617.723.6400

Short Term Protection

Life Term Short Term Protection Smart solutions for real life situations Life insurance is designed to protect you and your loved ones over time whether it s long term or short term. There are situations

Life Term Short Term Protection Smart solutions for real life situations Life insurance is designed to protect you and your loved ones over time whether it s long term or short term. There are situations

WHAT IS REASONABLE? Prepared by The Wagner Law Group. Practical tips for evaluating fees and expenses of plan investments

Prepared by The Wagner Law Group WHAT IS REASONABLE? Practical tips for evaluating fees and expenses of plan investments All investments involve risk, including possible loss of principal. Important note:

Prepared by The Wagner Law Group WHAT IS REASONABLE? Practical tips for evaluating fees and expenses of plan investments All investments involve risk, including possible loss of principal. Important note:

Dear Participant: Please refer to Part IV of the attached document for information on who to call with questions.

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

DUKE UNIVERSITY FACULTY AND STAFF RETIREMENT PLAN Plan Number Plan Information as of 03/26/2015

DUKE UNIVERSITY FACULTY AND STAFF RETIREMENT PLAN Plan Number 091156 Plan Information as of 03/26/2015 This legally required notice includes important information to help you compare the investment options

DUKE UNIVERSITY FACULTY AND STAFF RETIREMENT PLAN Plan Number 091156 Plan Information as of 03/26/2015 This legally required notice includes important information to help you compare the investment options

Advisors Access Bulletin. A plan fiduciary s guide to understanding participant-level fee disclosure under 404(a)5

5") A plan fiduciary s guide to understanding participant-level fee disclosure under 404(a)5 Overview FOR MILLIONS OF AMERICAN WORKERS who participate in their company s retirement plan, this year s third-quarter

A plan fiduciary s guide to understanding participant-level fee disclosure under 404(a)5 Overview FOR MILLIONS OF AMERICAN WORKERS who participate in their company s retirement plan, this year s third-quarter

Nationwide Peak Fixed Indexed Annuity

404(a) (5) Fee Disclosure Statement Nationwide Peak Fixed Indexed Annuity Your retirement plan has selected Nationwide Life and Annuity Insurance Company (Nationwide ) as an investment product provider.

404(a) (5) Fee Disclosure Statement Nationwide Peak Fixed Indexed Annuity Your retirement plan has selected Nationwide Life and Annuity Insurance Company (Nationwide ) as an investment product provider.

Putting 408(b)(2) disclosure rules into practice: A guide for plan sponsors

(2) disclosure rules into practice: A guide for plan sponsors") Putting 408(b)(2) disclosure rules into practice: A guide for plan sponsors Prepared by The Wagner Law Group What s inside 2 Introduction 3 Plan sponsor s 408(b)(2)-related fiduciary duties 4 Contacting

Putting 408(b)(2) disclosure rules into practice: A guide for plan sponsors Prepared by The Wagner Law Group What s inside 2 Introduction 3 Plan sponsor s 408(b)(2)-related fiduciary duties 4 Contacting

CONOCOPHILLIPS SAVINGS PLAN Plan Number Plan Information as of 05/30/2018

CONOCOPHILLIPS SAVINGS PLAN Plan Number 092538 Plan Information as of 05/30/2018 This legally required notice includes important information about the investment options under your retirement plan. You

CONOCOPHILLIPS SAVINGS PLAN Plan Number 092538 Plan Information as of 05/30/2018 This legally required notice includes important information about the investment options under your retirement plan. You

Baird Equity Asset Management Chautauqua Capital Management

Baird Equity Asset Management Chautauqua Capital Management Brochure March 30, 2017 Baird Equity Asset Management Chautauqua Capital Management 777 East Wisconsin Avenue 921 Walnut Street, Suite 250 Milwaukee,

Baird Equity Asset Management Chautauqua Capital Management Brochure March 30, 2017 Baird Equity Asset Management Chautauqua Capital Management 777 East Wisconsin Avenue 921 Walnut Street, Suite 250 Milwaukee,

QDIA PRACTICES CHECKLIST

QDIA PRACTICES CHECKLIST PLAN SPONSOR: PLAN NAME(S): RECORDKEEPER: ADVISOR: ADVISOR GUIDELINES FOR RECOMMENDING QDIAS OVERVIEW: A common question asked by plan sponsors is: How do I select a qualified

QDIA PRACTICES CHECKLIST PLAN SPONSOR: PLAN NAME(S): RECORDKEEPER: ADVISOR: ADVISOR GUIDELINES FOR RECOMMENDING QDIAS OVERVIEW: A common question asked by plan sponsors is: How do I select a qualified

ERISA FIDUCIARY BASICS AND BEST PRACTICES

Presents ERISA FIDUCIARY BASICS AND BEST PRACTICES November 5, 2015 Misty A. Leon mleon@wifilawgroup.com COMPLIANCE 101 General Roles and Responsibilities Who's Involved? Plan Administrator Responsibilities

Presents ERISA FIDUCIARY BASICS AND BEST PRACTICES November 5, 2015 Misty A. Leon mleon@wifilawgroup.com COMPLIANCE 101 General Roles and Responsibilities Who's Involved? Plan Administrator Responsibilities

The Department of Labor Fee Transparency Initiatives: Part 2 - Mandatory Service Provider Fee Disclosures - Updated

Volume 2012 May 1 The Department of Labor Fee Transparency Initiatives: Part 2 - Mandatory Service Provider Fee Disclosures - Updated For a number of years, the Department of Labor has been concerned about

Volume 2012 May 1 The Department of Labor Fee Transparency Initiatives: Part 2 - Mandatory Service Provider Fee Disclosures - Updated For a number of years, the Department of Labor has been concerned about

Sample of Investment Policy Statement

of Investment Policy Statement For the (Plan Name) FOR INSTITUTIONAL INVESTOR USE ONLY. Not for use with or distribution to the general public. Table of Contents Section Page 1 Plan information 3 2 Purpose

of Investment Policy Statement For the (Plan Name) FOR INSTITUTIONAL INVESTOR USE ONLY. Not for use with or distribution to the general public. Table of Contents Section Page 1 Plan information 3 2 Purpose

Got Mail? Participant Notices in Retirement Plans

Got Mail? Participant Notices in Retirement Plans Virginia K. Sutton, QKA, Consultant/Account Executive, VKS Consulting, Johnson & Dugan Insurance Services Corp. Virginia Krieger Sutton is a registered

Got Mail? Participant Notices in Retirement Plans Virginia K. Sutton, QKA, Consultant/Account Executive, VKS Consulting, Johnson & Dugan Insurance Services Corp. Virginia Krieger Sutton is a registered

CYSTIC FIBROSIS FOUNDATION 401(K) PLAN SUMMARY PLAN DESCRIPTION

PLAN SUMMARY PLAN DESCRIPTION") CYSTIC FIBROSIS FOUNDATION 401(K) PLAN SUMMARY PLAN DESCRIPTION January 2017 TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?... 1 What information does this Summary provide?... 1

CYSTIC FIBROSIS FOUNDATION 401(K) PLAN SUMMARY PLAN DESCRIPTION January 2017 TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?... 1 What information does this Summary provide?... 1

10/4/2011. COMPARISON OF DISCLOSURE RULES UNDER FORM 5500 SCHEDULE C AND UNDER 408(b)(2)

(2)") COMPARISON OF DISCLOSURE RULES UNDER FORM 5500 SCHEDULE C AND UNDER Employee Benefits Committee Joint Fall CLE Meeting October 21, 2011 Denver, CO Robert A. Miller Calfee, Halter & Griswold LLP Cleveland,

COMPARISON OF DISCLOSURE RULES UNDER FORM 5500 SCHEDULE C AND UNDER Employee Benefits Committee Joint Fall CLE Meeting October 21, 2011 Denver, CO Robert A. Miller Calfee, Halter & Griswold LLP Cleveland,

Dear Participant: Please refer to Part IV of the attached document for information on who to call with questions.

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

Slicing and dicing retirement plan fees: Allocation consideration for plan sponsors

Slicing and dicing retirement plan fees: Allocation consideration for plan sponsors Vanguard commentary December 2018 Executive summary As a result of fee disclosure requirements and fee litigation trends,

Slicing and dicing retirement plan fees: Allocation consideration for plan sponsors Vanguard commentary December 2018 Executive summary As a result of fee disclosure requirements and fee litigation trends,

White Paper. The truth about institutional income annuities

White Paper The truth about institutional income annuities More often than not, the word annuity raises concerns because of conventional wisdom that all annuities are costly, complicated, offer limited

White Paper The truth about institutional income annuities More often than not, the word annuity raises concerns because of conventional wisdom that all annuities are costly, complicated, offer limited

Dear Participant: Please refer to Part IV of the attached document for information on who to call with questions.

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

An easy way to diversify

American Funds Asset Allocation Portfolios Annuities Variable An easy way to diversify Target allocations as of May 1, 2018* * Allocations subject to change at any time. Available asset allocation options

American Funds Asset Allocation Portfolios Annuities Variable An easy way to diversify Target allocations as of May 1, 2018* * Allocations subject to change at any time. Available asset allocation options

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

You recognize that your retirement plan is a critical benefit that can help your company attract and retain quality employees.

ederated You recognize that your retirement plan is a critical benefit that can help your company attract and retain quality employees. Beyond Gravity Federated s Beyond Gravity toolkit helps financial

ederated You recognize that your retirement plan is a critical benefit that can help your company attract and retain quality employees. Beyond Gravity Federated s Beyond Gravity toolkit helps financial

DOL 408(b)(2) Plan Sponsor Fee Disclosure Summary Document for Retirement Plan Services provided by John Hancock Retirement Plan Services, LLC

(2) Plan Sponsor Fee Disclosure Summary Document for Retirement Plan Services provided by John Hancock Retirement Plan Services, LLC") John Hancock Retirement Plan Services, LLC ( JHRPS ) has always believed in clearly explaining the fees, expenses, and costs associated with our administration of your retirement plan. We have employed

John Hancock Retirement Plan Services, LLC ( JHRPS ) has always believed in clearly explaining the fees, expenses, and costs associated with our administration of your retirement plan. We have employed

two thousand eight ISSUE BROCHURE 403(b) Plans Frequently Asked Questions

Plans Frequently Asked Questions") Brochure 2-403bFAQs 11x17 - FINAL:Fact Sheet 2008.qxd 10/29/2008 11:04 AM Page 1 National Association of Government Defined Contribution Administrators, Inc. two thousand eight ISSUE BROCHURE 403(b) Plans

Brochure 2-403bFAQs 11x17 - FINAL:Fact Sheet 2008.qxd 10/29/2008 11:04 AM Page 1 National Association of Government Defined Contribution Administrators, Inc. two thousand eight ISSUE BROCHURE 403(b) Plans

Employee Relations. Revenue Sharing: Risks, Rewards, and Reality for Plan Fiduciaries. Mark E. Bokert and Alan Hahn

Employee Relations L A W J O U R N A L Employee Benefits Electronically reprinted from Vol. 42, No. 4 Spring 2017 Revenue Sharing: Risks, Rewards, and Reality for Plan Fiduciaries Mark E. Bokert and Alan

Employee Relations L A W J O U R N A L Employee Benefits Electronically reprinted from Vol. 42, No. 4 Spring 2017 Revenue Sharing: Risks, Rewards, and Reality for Plan Fiduciaries Mark E. Bokert and Alan

MetLife Financial Freedom Select

Portfolio Summary Annuities Variable MetLife Financial Freedom Select Read below and learn more about the underlying funding choices available in the MetLife Financial Freedom Select variable annuity.

Portfolio Summary Annuities Variable MetLife Financial Freedom Select Read below and learn more about the underlying funding choices available in the MetLife Financial Freedom Select variable annuity.

Overcome the Increased Scrutiny of Your Organization s Retirement Plan

Overcome the Increased Scrutiny of Your Organization s Retirement Plan Finance, HR & Business Operations Conference Washington, DC April 30 - May 1, 2013 4/30/2013 Goals for Today s Presentation Understand

Overcome the Increased Scrutiny of Your Organization s Retirement Plan Finance, HR & Business Operations Conference Washington, DC April 30 - May 1, 2013 4/30/2013 Goals for Today s Presentation Understand