Chapter 4: Job Costing

|

|

|

- Russell Goodman

- 6 years ago

- Views:

Transcription

manner. Cost Pool A grouping of individual cost items.")

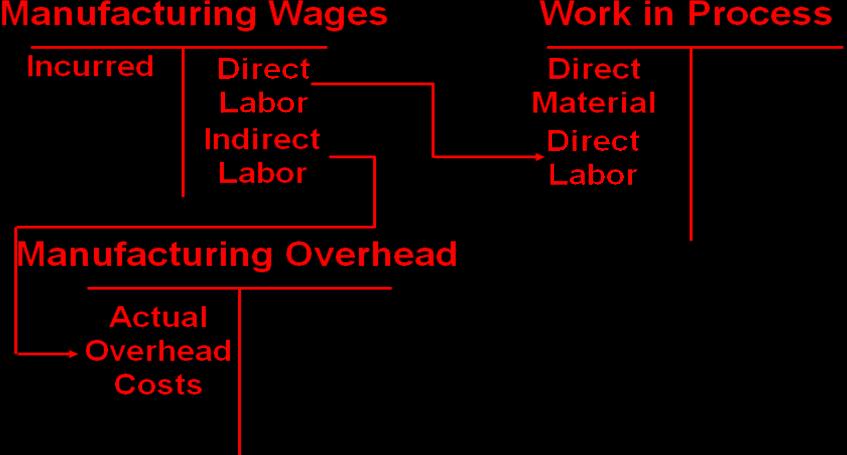

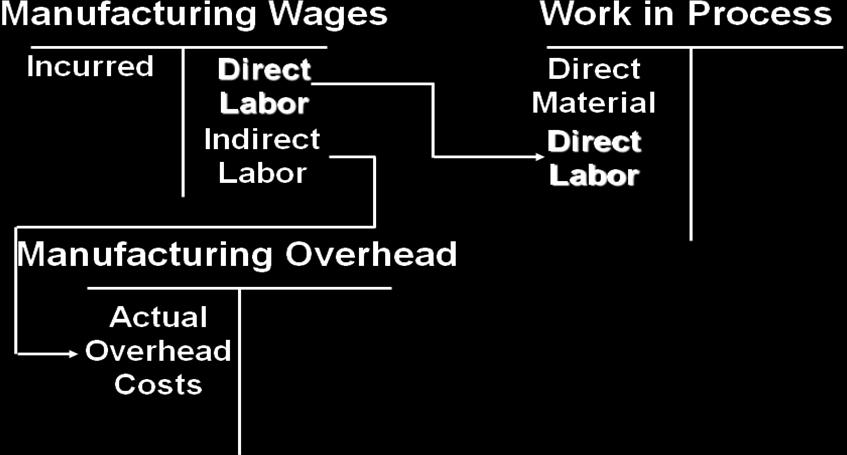

1 Chapter 4: Job Costing Costing System Terminology: Cost Object Anything for which a separate measurement of costs is desired. Direct Cost Costs that are related to a particular cost object in an economically feasible (Costeffective) manner. Cost Pool A grouping of individual cost items. Cost Allocation Base A factor that is the common denominator for systematically linking an indirect cost or group of indirect costs to a cost object. Costing Systems: Job-Costing System Process-Costing System Costs are assigned to a distinct unit or batch. Costs are assigned to a mass of similar units. Resources are expended to bring a distinct product or service to market for a specific customer. Examples: A CPA firm, A textbook publisher, A medical care facility, A landscaping company, An auto repair shop. Resources are used to mass-produce a product or service and not for any specific customer. Examples: Postal delivery, Oil refining, A tire manufacturing, A cola-drink-concentrate producer, A paper mill. Job Costing Approach: 1- Identify the cost object(s). 2- Identify the direct costs for the cost object(s). 3- Select cost-allocation bases to use in allocating the indirect costs to the cost object(s). 4- Identify the indirect costs associated with each cost-allocation base. 5- Compute the rate per unit of each cost-allocation base to allocate indirect costs to the cost object(s). 6- Compute the indirect costs allocated to the cost object(s). 7- Determine the cost of the cost object(s) by adding the direct and indirect costs. Three major source documents used in job-costing systems are: 1- Job cost record or job cost sheet, a document that records and accumulates all costs assigned to a specific job, starting when work begins. 2- Materials requisition record, a document that contains information about the cost of direct materials used on a specific job and in a specific department; and 3- Labor-time record, a document that contains information about the labor time used on a specific job and in a specific department. Job Costing Overview:

2 Time Period for Indirect-Cost Rates: Usually calculate indirect-cost rates once each year. Use a yearly rate because using a shorter period of time (such as monthly or quarterly) would cause the rate to be higher or lower at different times during the year due to: Seasonality of costs (higher heating costs in the winter months). Fluctuating volumes (units produced in low volume months would be charged a greater cost). Actual Costing: Actual costing is a costing system that traces direct costs to a cost object by using the actual direct-cost rates times the actual quantities of the direct-cost inputs. It allocates indirect costs based on the actual indirect-cost rates times the actual quantities of the cost-allocation bases. Normal Costing: Normal costing is a method that traces direct costs to a cost object. In a normal costing system, the Manufacturing Overhead Control account will not, in general, equal the amounts in the Manufacturing Overhead Allocated account. The Manufacturing Overhead Control account aggregates the actual overhead costs incurred while Manufacturing Overhead Allocated allocates overhead costs to jobs on the basis of a budgeted rate times the actual quantity of the cost-allocation base. Budgeted total cost in indirect-cost pool Budgeted indirect-cost rate = Budgeted total quantity of the cost-allocation base Underallocation or overallocation of indirect (overhead) costs can arise because of (a) the Numerator reason the actual overhead costs differ from the budgeted overhead costs, and (b) the Denominator reason the actual quantity used of the allocation base differs from the budgeted quantity. Allocate Manufacturing Overhead Predetermined manufacturing overhead x actual quantity of the allocation base used by each job. Actual costing and normal costing differ in their use of actual or budgeted indirect cost rates: Actual Costing Normal Costing Direct-cost rates Indirect-cost rates Actual rates Actual rates Actual rates Budgeted rates Each costing method uses the actual quantity of the direct-cost input and the actual quantity of the costallocation base. The reasons actual and applied overhead costs are different are frequently separated into two categories. Overhead variances occur when: 1) the actual quantities used and actual prices paid for the various indirect resources are different from the prices and quantities estimated or budgeted for the overhead rate calculation and 2) the actual level of activity is different from the activity level used to calculate the overhead rates. The first category of differences causes variances for both variable and fixed overhead costs. The second category is only related to fixed costs. Steps for Developing a Predetermined Cost Allocation Rate: Estimate Total Indirect Costs (IDC). Identify Cost Allocation Base. Estimate Total Quantity of Allocation Base. Compute Predetermined IDC Allocation Rate. Obtain actual quantity of cost allocation base used by individual jobs. Allocate Indirect Costs to Jobs. Example: A company budgets for manufacturing overhead of $1,280,000 and direct manufacturing labor-hours of 32,000. Budgeted indirect-cost rate = $1,280,000 32,000 = $40 per direct manufacturing labor-hour 2

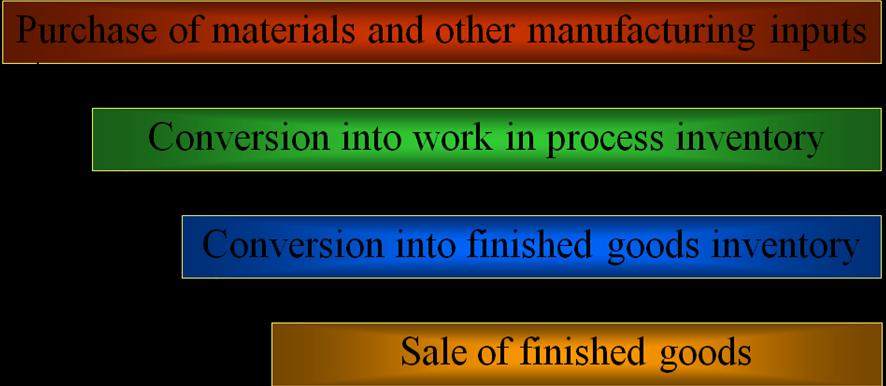

3 Job Costing System in Manufacturing: Account for manufacturing materials and labor: Accounting for Materials: Accounting for Labor: 3

in work in process, finished goods, and cost of goods sold. 3- Year-end write-off to Cost of Goods Sold.")

4 Account for manufacturing overhead: Indirect Costs and End-of-Period Adjustments: At the end of the period, there is usually a difference between indirect costs incurred and indirect costs allocated to work-in-process during the year. Indirect costs Incurred > Indirect costs allocated Under-Allocated indirect costs. Indirect costs Incurred < Indirect costs allocated Over-Allocated indirect costs. Under and Overallocated Indirect Costs: Example, Most companies write-off over or under-allocated overhead to cost of goods sold at the end of the year. Prorating the difference among the ending inventory and cost of goods sold accounts can be done if the amount is material. Alternative ways to make end-of-period adjustments for underallocated or overallocated overhead are as follows: 1- Proration based on the total amount of indirect costs allocated (before proration) in the ending balances of work in process, finished goods, and cost of goods sold. 2- Proration based on total ending balances (before proration) in work in process, finished goods, and cost of goods sold. 3- Year-end write-off to Cost of Goods Sold. 4- Restatement of all overhead entries using actual indirect cost rates rather than budgeted indirect cost rates. Account for completion and sales of finished goods and close manufacturing overhead Accounting for Finished Goods: 4

5 Job Costing in the Service Industry: How does job costing at a service firm work? Very similar to job costing at a manufacturing company. Main difference is that the company is allocating indirect period costs to each client, rather than manufacturing costs. Since there is no inventory, no journal entries are needed. Example 1: Donnelly Corporation used a job-costing system with two direct-cost categories (direct materials and indirect manufacturing labor) and one manufacturing overhead cost pool. Donnelly allocates manufacturing overhead costs using direct manufacturing labor costs. Donnelly provides the following information: Budget for 2009 Actual Results for 2009 Direct material costs $2,150,000 $2,000,000 Direct manufacturing labor costs 1,450,000 1,400,000 Manufacturing overhead costs 2,755,000 2,800,000 Required 1- Compute the actual and budgeted manufacturing overhead rates for During March, the job-cost record for 195 contained the following information: Direct material used $50,000 Direct manufacturing labor costs $40,000 Compute the cost of job 195 using (a) actual costing and (b) normal costing. 3- At the end of 2009, compute the under or overallocated manufacturing overhead under normal costing. Why is there is no under- or overallocated overhead under actual costing? Solution: 1- Budgeted manufacturing overhead rate Actual manufacturing overhead rate = = = = Budgeted manufacturing overhead costs Budgeted direct manufacturing labor costs $2,755,000 = 1.90 or 190% $1,450,000 Actual manufacturing overhead costs Actual direct manufacturing labor costs $2,800, 000 = 2.0 or 200% $1,400,000 5

6 2- Costs of Job 195 under actual and normal costing follow: Actual Costing Normal Costing Direct materials $ 50,000 $ 50,000 Direct manufacturing labor costs 40,000 40,000 Manufacturing overhead costs $40, ; $40, ,000 76,000 Total manufacturing costs of Job 195 $170,000 $166, Total manufacturing overhead allocated under normal costing = Actual manufacturing labor costs Budgeted overhead rate = $1,400, = $2,660,000 Underallocated manufacturing overhead = Actual manufacturing overhead costs Manufacturing overhead allocated = $2,800,000 $2,660,000 = $140,000 There is no under- or overallocated overhead under actual costing because overhead is allocated under actual costing by multiplying actual manufacturing labor costs and the actual manufacturing overhead rate. This, of course equals the actual manufacturing overhead costs. All actual overhead costs are allocated to products. Hence, there is no under- or overallocatead overhead. Example 2: Richmore Company produces gadgets for the coveted small appliance market. The following data reflects activity for the year Costs incurred: Purchases of direct materials (net) on credit $139,000 Direct manufacturing labor cost 95,000 Indirect labor 69,500 Depreciation, factory equipment 45,000 Depreciation, office equipment 22,000 Maintenance, factory equipment 35,000 Miscellaneous factory overhead 24,500 Rent, factory building 85,000 Advertising expense 105,000 Sales commissions 45,000 Inventories: January 1, 2009 December 31, 2009 Direct materials $24,000 $26,000 Work in process 21,000 36,000 Finished goods 84,000 39,000 Richmore Co. uses a normal cost system and allocates overhead to work in process at rate of $5.00 per direct manufacturing labor dollar. Indirect materials are insignificant so there is no inventory account for indirect materials. 6

7 Required 1- Prepare journal entries to record the transactions for 2009 including an entry to close out over- or underallocated overhead to cost of goods sold. For each entry indicate the source document that would be used to authorize each entry. Also, note which subsidiary ledger, if any, should be referenced as backup for the entry. 2- Post the journal entries to T-accounts for all of the inventories, Cost of Goods Sold, the Manufacturing Overhead Control Account, and the Manufacturing Overhead Allocated Account. Solution: Preparing the journal entries: 1- Direct Materials Control 139,000 Accounts Payable Control 139,000 Source Document: Purchase Invoice, Receiving Report Subsidiary Ledger: Direct Materials Record, Accounts Payable 2- Work in Process Control a 137,000 Direct Materials Control 137,000 Source Document: Material Requisition Records, Job Cost Record Subsidiary Ledger: Direct Materials Record, Work-in-Process Inventory, Records by Jobs 3- Work in Process Control 95,000 Manufacturing Overhead Control 69,500 Wages Payable Control 164,500 Source Document: Labor Time Records, Job Cost Records Subsidiary Ledger: Manufacturing Overhead Records, Employee Labor Records, Work-in-Process Inventory Records by Jobs 4- Manufacturing Overhead Control 189,500 Salaries Payable Control 35,000 Accounts Payable Control 24,500 Accumulated Depreciation Control 45,000 Rent Payable Control 85,000 Source Document: Depreciation Schedule, Rent Schedule, Maintenance wages due, Invoices for miscellaneous factory overhead items Subsidiary Ledger: Manufacturing Overhead Records 5- Work in Process Control 475,000 Manufacturing Overhead Allocated 475,000 ($95,000 $5.00) Source Document: Labor Time Records, Job Cost Record Subsidiary Ledger: Work-in-Process Inventory Records by Jobs 6- Finished Goods Control b 692,000 Work in Process Control 692,000 Source Document: Job Cost Record, Completed Job Cost Record Subsidiary Ledger: Work-in-Process Inventory Records by Jobs, Finished Goods Inventory Records by Jobs 7

8 7- Cost of Goods Sold c 737,000 Finished Goods Control 737,000 Source Document: Sales Invoice, Completed Job Cost Record Subsidiary Ledger: Finished Goods Inventory Records by Jobs 8- Manufacturing Overhead Allocated 475,000 Manufacturing Overhead Control 259,000 Cost of Goods Sold 216,000 Source Document: Prior Journal Entries 9- Administrative Expenses 22,000 Marketing Expenses 150,000 Sales Commissions 45,000 Advertising Expense Control 105,000 Accumulated Depreciation, Office Equipment 22,000 Source Document: Depreciation Schedule, Marketing Payroll Request, Invoice for Advertising, Sales Commission Schedule. Subsidiary Ledger: Employee Salary Records, Administration Cost Records, Marketing Cost Records. a Materials used = Beginning direct materials inventory + Purchases - Ending direct materials inventory = $24,000 + $139,000 $26,000 = $137,000 b Cost of goods manufactured = Beginning WIP inventory + Manufacturing cost Ending WIP inventory = $21,000 + ($137,000 + $95,000 + $475,000) $236,000 = 692,000 c Cost of Goods Sold = Beginning fin. goods inventory + Cost of goods manuf. Ending fin. goods inventory = $84,000 + $692,000 $39,000 = $737,000 8

9 T-accounts: Direct Materials Control Bal. 1/1/ ,000 (2) Materials used 137,000 (1) Purchases 139,000 Bal. 12/31/ ,000 Bal. 1/1/2009 (2) Direct materials used (3) Direct manuf. labor (5) Manuf. overhead allocated 475,000 Bal. 12/31/ ,000 Work-in-Process Control 21,000 (6) Cost of goods manufactured 692, ,000 95,000 Finished Goods Control Bal. 1/1/ ,000 (7) Cost of goods sold 737,000 (6) Cost of goods manuf. 692,000 Bal. 12/31/ ,000 Cost of Goods Sold (7) Goods sold 737,000 (8) Adjust for overallocation 216,000 Manufacturing Overhead Control (3)Indirect labor (4) Supplies (4) Miscellaneous 69,500 35,000 24,500 (8) To close 259,000 (4 Depreciation 45,000 (4) Rent 85,000 Bal. 0 Manufacturing Overhead Allocated (8) To close 475,000 (5) Manuf. overhead allocated 475,000 Bal. 0 9 Prepared by Dr. Helal Afify 2013

CHAPTER 4 JOB COSTING

CHAPTER 4 JOB COSTING 4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base. Cost pool a grouping of individual indirect cost items. Cost tracing the assigning of direct costs to

CHAPTER 4 JOB COSTING 4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base. Cost pool a grouping of individual indirect cost items. Cost tracing the assigning of direct costs to

Job Costing Cost Accounting Horngreen, Datar, Foster 1

Job Costing 1 Building Block Concepts of Costing Systems The following five terms constitute the building blocks that will be used in this chapter: 1 A cost object is anything for which a separate measurement

Job Costing 1 Building Block Concepts of Costing Systems The following five terms constitute the building blocks that will be used in this chapter: 1 A cost object is anything for which a separate measurement

CHAPTER 4 JOB COSTING

CHAPTER 4 JOB ING 4-1 Cost pool a grouping of individual cost items. Cost tracing the assigning of direct costs to the chosen cost object. Cost allocation the assigning of indirect costs to the chosen

CHAPTER 4 JOB ING 4-1 Cost pool a grouping of individual cost items. Cost tracing the assigning of direct costs to the chosen cost object. Cost allocation the assigning of indirect costs to the chosen

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing

Chapter 4 Job Costing") Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

No. of Branches (11) Answer (9) questions only

Answer (9) questions only") Answer all Questions First Question: True or False No. of Branches (11) Answer (9) questions only ( /09) (6-9 Minutes) 1- Jacob's Manufacturing sales is equal to production. If Jacob's Manufacturing presented

Answer all Questions First Question: True or False No. of Branches (11) Answer (9) questions only ( /09) (6-9 Minutes) 1- Jacob's Manufacturing sales is equal to production. If Jacob's Manufacturing presented

CHAPTER 8: PERFORMANCE EVALUATION Pearson Education. All rights reserved.

CHAPTER 8: PERFORMANCE EVALUATION Learning Objectives 1. Explain static budgets and static-budget variances 2. Develop flexible budgets and compute flexiblebudget variances and sales-volume variances 3.

CHAPTER 8: PERFORMANCE EVALUATION Learning Objectives 1. Explain static budgets and static-budget variances 2. Develop flexible budgets and compute flexiblebudget variances and sales-volume variances 3.

Spring Manufacturing Company Sales Budget 2007

8-56 Comprehensive Profit Plan (90 minutes) 1. Sales Budget Sales Budget Sales (in units) 12,000 9,000 21,000 x Selling Price Per Unit $150 $220 Total Sales Revenue $1,800,000 $1,980,000 $3,780,000 2.

8-56 Comprehensive Profit Plan (90 minutes) 1. Sales Budget Sales Budget Sales (in units) 12,000 9,000 21,000 x Selling Price Per Unit $150 $220 Total Sales Revenue $1,800,000 $1,980,000 $3,780,000 2.

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities

COSTING SYSTEMS part I.

MANAGERIAL ACCOUNTING Topic5 COSTING SYSTEMS part I. Structureofthelecture5 5.1 Key terms 5.2 Costing systems 5.3 Absorption vs. variable costing 5.4 Actual vs. Normal vs. Extended normal costing 5.5 Job

MANAGERIAL ACCOUNTING Topic5 COSTING SYSTEMS part I. Structureofthelecture5 5.1 Key terms 5.2 Costing systems 5.3 Absorption vs. variable costing 5.4 Actual vs. Normal vs. Extended normal costing 5.5 Job

Product costing (process costing) In Class Exercise

In Class Exercise") Product costing (process costing) In Class Exercise makes stained glass lamps. Production process uses two departments: cutting department and assembly department where they are put together. Record the

Product costing (process costing) In Class Exercise makes stained glass lamps. Production process uses two departments: cutting department and assembly department where they are put together. Record the

ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 )

") ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 ) MIDTERM EXAMINATION MGT402- Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate

ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 ) MIDTERM EXAMINATION MGT402- Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate

Exercise E21-1 page 932. (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000

Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000") Exercise E21-1 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 92,700 Manufacturing Overhead

Exercise E21-1 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 92,700 Manufacturing Overhead

MGT402 - COST & MANAGEMENT ACCOUNTING

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

Principles of Managerial Accounting

GALILEO, University System of Georgia GALILEO Open Learning Materials Business Administration, Management, and Economics Open Textbooks Business Administration, Management, and Economics Spring 2019 Principles

GALILEO, University System of Georgia GALILEO Open Learning Materials Business Administration, Management, and Economics Open Textbooks Business Administration, Management, and Economics Spring 2019 Principles

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 4: Costing Major Topics are: Job Costing Operating Costing Process Costing Standard Costing (Variance Analysis) Gross Domestic Product (GDP) Job Costing

Engineering Economics and Financial Accounting Unit 4: Costing Major Topics are: Job Costing Operating Costing Process Costing Standard Costing (Variance Analysis) Gross Domestic Product (GDP) Job Costing

INTER CA MAY COSTING Topic: Standard Costing, Budgetary Control, Integral and Non Integral, Materials, Marginal Costing.

INTER CA MAY 218 COSTING Topic: Standard Costing, Budgetary Control, Integral and Non Integral, Materials, Marginal Costing. Note: All questions are compulsory. Test Code M33 Branch: MULTIPLE Date: 21.1.218

INTER CA MAY 218 COSTING Topic: Standard Costing, Budgetary Control, Integral and Non Integral, Materials, Marginal Costing. Note: All questions are compulsory. Test Code M33 Branch: MULTIPLE Date: 21.1.218

Summerset Fencing. Introduction

Summerset Fencing An Algorithmic Practice Set Featuring Job-Order Costing and JIT Inventories 1 st Web-Based Edition Introduction Page 1 An Introduction To Summerset Fencing Summerset Fencing operates

Summerset Fencing An Algorithmic Practice Set Featuring Job-Order Costing and JIT Inventories 1 st Web-Based Edition Introduction Page 1 An Introduction To Summerset Fencing Summerset Fencing operates

Ramblewood Manufacturing, Incorporated. 1 st Web-Based Edition. Introduction

Ramblewood Manufacturing, Incorporated 1 st Web-Based Edition Introduction Page 1 An Introduction To Ramblewood Manufacturing, Incorporated Ramblewood Manufacturing, Incorporated operates in a job-order

Ramblewood Manufacturing, Incorporated 1 st Web-Based Edition Introduction Page 1 An Introduction To Ramblewood Manufacturing, Incorporated Ramblewood Manufacturing, Incorporated operates in a job-order

2018 LAST MINUTE CPA EXAM NOTES

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

Accounting 2. For Professor Howard J. Levine

Accounting 2 Chapters 12 to 26 Class Handouts For Professor Howard J. Levine Note: This packet should be brought to class every week. If you forget or misplace it you can reprint the set by going to the

Accounting 2 Chapters 12 to 26 Class Handouts For Professor Howard J. Levine Note: This packet should be brought to class every week. If you forget or misplace it you can reprint the set by going to the

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS COST ACCOUNTING ACC 2360

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS COST ACCOUNTING ACC 2360 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Spring 02 NOTE: This course is NOT designed

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS COST ACCOUNTING ACC 2360 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Spring 02 NOTE: This course is NOT designed

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with

SYMBIOSIS CENTRE FOR DISTANCE LEARNING (SCDL) Subject: Management Accounting

Subject: Management Accounting") Sample Questions: Section I: Subjective Questions 1. How does Subsidiary Book help in accounting process? Which subsidiary books are used very frequently? 2. Differentiate between the liabilities and assets.

Sample Questions: Section I: Subjective Questions 1. How does Subsidiary Book help in accounting process? Which subsidiary books are used very frequently? 2. Differentiate between the liabilities and assets.

Cost Accounting, 14e (Horngren/Datar/Rajan) Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control

Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control") Cost Accounting, 14e (Horngren/Datar/Rajan) Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control Objective 8.1 1) Overhead costs have been increasing due to all of the following

Cost Accounting, 14e (Horngren/Datar/Rajan) Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control Objective 8.1 1) Overhead costs have been increasing due to all of the following

Pricing for Services

Pricing for Services 1. Introduction This aid discusses costing and pricing of services to assure that each job earns a reasonable profit. The figures used in the tables and examples do not reflect what

Pricing for Services 1. Introduction This aid discusses costing and pricing of services to assure that each job earns a reasonable profit. The figures used in the tables and examples do not reflect what

Summative Case Study: SRS Educational Supply Company. Part 1 Job Order Costing / Process Costing

The following case study is adapted from: Samuels, J. A., & Sawers, K. M. (2017). SRS Educational Supply Company: An instructional budget project. Issues in Accounting Education: November 2017, Vol. 32,

The following case study is adapted from: Samuels, J. A., & Sawers, K. M. (2017). SRS Educational Supply Company: An instructional budget project. Issues in Accounting Education: November 2017, Vol. 32,

NETWORK BUSINESS SYSTEMS SOFTWARE SYSTEM DOCUMENTATION GENERAL LEDGER

NETWORK BUSINESS SYSTEMS SOFTWARE SYSTEM DOCUMENTATION GENERAL LEDGER FEATURES Allows 99 divisions within 99 companies Separate General Ledger Data for Multiple Companies with Multiple Division and Multiple

NETWORK BUSINESS SYSTEMS SOFTWARE SYSTEM DOCUMENTATION GENERAL LEDGER FEATURES Allows 99 divisions within 99 companies Separate General Ledger Data for Multiple Companies with Multiple Division and Multiple

MIDTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate the cost of manufacturing

MIDTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate the cost of manufacturing

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 3,000 Ending Raw Materials Inventory 4,500 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 3,000 Ending Raw Materials Inventory 4,500 Purchases of Raw Materials

COMPOSED AND SOLVED BY (SADIA ALI) MBA

MBA") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 3) Time: 60 min Question No: 1 ( Marks: 1 ) - Please choose one Mr. A sold goods to Mr. B for Rs. 3,000 on October 8, 2008 and Mr.

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 3) Time: 60 min Question No: 1 ( Marks: 1 ) - Please choose one Mr. A sold goods to Mr. B for Rs. 3,000 on October 8, 2008 and Mr.

Index COPYRIGHTED MATERIAL

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

CLASSIFICATION OF COST

Cost Accounting Standard 1 CLASSIFICATION OF COST Draft Developed by Technical Support and Practice Development Committee Institute of Cost and Managemet Accountants of Pakistan Implementation Status This

Cost Accounting Standard 1 CLASSIFICATION OF COST Draft Developed by Technical Support and Practice Development Committee Institute of Cost and Managemet Accountants of Pakistan Implementation Status This

Illustrative Example Xander Barkley s XYX Company manufactures a single product. The standard cost card for one unit is as follows:

Appendix 11A General Ledger Entries to Record Variances 11A-1 General Ledger Entries to Record Variances Although standard costs and variances can be computed and used by management without being formally

Appendix 11A General Ledger Entries to Record Variances 11A-1 General Ledger Entries to Record Variances Although standard costs and variances can be computed and used by management without being formally

Graded Project Ice Cream Systems

Graded Project Ice Cream Systems PROJECT GOAL 1 PROJECT INFORMATION 1 PROJECT INSTRUCTIONS 14 SUBMITTING YOUR PROJECT 26 C o n t e n t s iii Ice Cream Systems PROJECT GOAL The goal of this graded project

Graded Project Ice Cream Systems PROJECT GOAL 1 PROJECT INFORMATION 1 PROJECT INSTRUCTIONS 14 SUBMITTING YOUR PROJECT 26 C o n t e n t s iii Ice Cream Systems PROJECT GOAL The goal of this graded project

CAS-3 (Revised 2011) 1. COST ACCOUNTING STANDARD ON OVERHEADS (Revised 2011)

1. COST ACCOUNTING STANDARD ON OVERHEADS (Revised 2011)") CAS-3 (Revised 2011) 1 The Cost Accounting Standards Board (CASB) COST ACCOUNTING STANDARD ON OVERHEADS (Revised 2011) The following is the revised COST ACCOUNTING STANDARD 3 (CAS-3) issued by the Council

CAS-3 (Revised 2011) 1 The Cost Accounting Standards Board (CASB) COST ACCOUNTING STANDARD ON OVERHEADS (Revised 2011) The following is the revised COST ACCOUNTING STANDARD 3 (CAS-3) issued by the Council

Accounting For Decision Making

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

Chapter 10 Process Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Chapter 10 Process Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) The Basic of Process Costing Process costing is a costing method used where it is not

Chapter 10 Process Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) The Basic of Process Costing Process costing is a costing method used where it is not

MANAGERIAL (COST) ACCOUNTING

ACCOUNTING") MANAGERIAL (COST) ACCOUNTING EXERCISE BOOK ERASMUS WINTER SEMESTER 2014 Exercise 2.1 Consider the following company, Chip Making Systems, that manufactures computer chips. It incurs the following costs

MANAGERIAL (COST) ACCOUNTING EXERCISE BOOK ERASMUS WINTER SEMESTER 2014 Exercise 2.1 Consider the following company, Chip Making Systems, that manufactures computer chips. It incurs the following costs

SUGGESTED SOLUTION IPCC MAY 2017EXAM. Test Code - I M J

SUGGESTED SOLUTION IPCC MAY 2017EXAM COSTING Test Code - I M J 7 1 3 5 BRANCH - (MULTIPLE) (Date : 01.01.2017) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

SUGGESTED SOLUTION IPCC MAY 2017EXAM COSTING Test Code - I M J 7 1 3 5 BRANCH - (MULTIPLE) (Date : 01.01.2017) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

ACTIVITY BASE COSTING

ACTIVITY BASE COSTING Key Terms and Concepts to Know Single Plantwide Rate vs. Multiple Department Rates Job order costing relied on a single plantwide overhead rate to apply overhead to work-in-process.

ACTIVITY BASE COSTING Key Terms and Concepts to Know Single Plantwide Rate vs. Multiple Department Rates Job order costing relied on a single plantwide overhead rate to apply overhead to work-in-process.

I B.Com PA [ ] Semester II Core: Management Accounting - 218A Multiple Choice Questions.

![I B.Com PA [ ] Semester II Core: Management Accounting - 218A Multiple Choice Questions.](/thumbs/80/82536614.jpg "I B.Com PA [ ] Semester II Core: Management Accounting - 218A Multiple Choice Questions.") 1 of 23 1/27/2018, 11:53 AM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

1 of 23 1/27/2018, 11:53 AM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

Overhead Cost Controlling

Overhead Cost Controlling Objectives To gain understanding of key business processes of SAP Overhead Cost Management (OCM) Understand the Organizational unit in Controlling Determine the origin of posting

Overhead Cost Controlling Objectives To gain understanding of key business processes of SAP Overhead Cost Management (OCM) Understand the Organizational unit in Controlling Determine the origin of posting

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team.

Solved by Mehreen Humayun vuzs Team.") FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

Examinations for Academic Year Semester I / Academic Year 2015 Semester II. 1. This question paper consists of Section A and Section B.

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1,000 Ending Raw Materials Inventory 2,500 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1,000 Ending Raw Materials Inventory 2,500 Purchases of Raw Materials

Hydro Paddle Boards, Inc.

Hydro Paddle Boards, Inc. CONTENTS General Journal... 1 General Journal (Adjusting Entries)... 6 General Journal (Closing Entries)... 7 General Ledger... 8 Accounts Receivable Ledger... 21 Accounts Payable

Hydro Paddle Boards, Inc. CONTENTS General Journal... 1 General Journal (Adjusting Entries)... 6 General Journal (Closing Entries)... 7 General Ledger... 8 Accounts Receivable Ledger... 21 Accounts Payable

Solution to Cost Paper of CA IPCC COST MAY Solution to Question 1 (a) 10% = Avg. No. of workers on roll = 500

10% = Avg. No. of workers on roll = 500") Solution to Cost Paper of CA IPCC COST MAY 2017 Solution to Question 1 (a) Average no. of workers on roll during the year No.of replacements 1. Labour turnover rate under replacement method = x 100 Average

Solution to Cost Paper of CA IPCC COST MAY 2017 Solution to Question 1 (a) Average no. of workers on roll during the year No.of replacements 1. Labour turnover rate under replacement method = x 100 Average

Chapter 2 Job-Order Costing: Calculating Unit Product Costs

Managerial Accounting 16th Edition Garrison Solutions Manual Full Download: http://testbanklive.com/download/managerial-accounting-16th-edition-garrison-solutions-manual/ Chapter 2 Job-Order Costing: Calculating

Managerial Accounting 16th Edition Garrison Solutions Manual Full Download: http://testbanklive.com/download/managerial-accounting-16th-edition-garrison-solutions-manual/ Chapter 2 Job-Order Costing: Calculating

MTP_Intermediate_Syl2016_June2018_Set 2 Paper 8- Cost Accounting

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

7 Solved Mid Term Papers of MGT402 BY.

7 Solved Mid Term Papers of MGT402 BY http://vustudents.ning.com Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process

7 Solved Mid Term Papers of MGT402 BY http://vustudents.ning.com Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process

MANAGERIAL ACCOUNTING Hilton Chapter 3 Adobe Connect

1 MANAGERIAL ACCOUNTING Hilton Chapter 3 Adobe Connect We change gears dramatically in managerial accounting. Because of the limited time we have, we do not cover many advanced concepts. An overview of

1 MANAGERIAL ACCOUNTING Hilton Chapter 3 Adobe Connect We change gears dramatically in managerial accounting. Because of the limited time we have, we do not cover many advanced concepts. An overview of

INTER CA MAY Test Code M32 Branch: MULTIPLE Date: (50 Marks) Note: All questions are compulsory.

Note: All questions are compulsory.") (5 Marks) Note: All questions are compulsory. INTER CA MAY 218 COSTING Topic: Contract Costing, Budgetary Control, Labour, Joint & By- Product, Absorption Costing, Overheads, Integral & Non Integral, Marginal

(5 Marks) Note: All questions are compulsory. INTER CA MAY 218 COSTING Topic: Contract Costing, Budgetary Control, Labour, Joint & By- Product, Absorption Costing, Overheads, Integral & Non Integral, Marginal

About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11

CONTENTS About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11 1 INTRODUCTION u Cost 1 u Costing 2 u Cost accounting 2 u Cost accountancy 2 u Classification of costs 3 u Distinction between

CONTENTS About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11 1 INTRODUCTION u Cost 1 u Costing 2 u Cost accounting 2 u Cost accountancy 2 u Classification of costs 3 u Distinction between

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13. Chapter 11: Standard Costs and Variance Analysis

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

CAS-3 (Revised 2011) 1. COST ACCOUNTING STANDARD ON OVERHEADS (Revised 2011)

1. COST ACCOUNTING STANDARD ON OVERHEADS (Revised 2011)") CAS-3 (Revised 2011) 1 The Cost Accounting Standards Board (CASB) COST ACCOUNTING STANDARD ON OVERHEADS (Revised 2011) The following is the revised COST ACCOUNTING STANDARD 3 (CAS-3) issued by the Council

CAS-3 (Revised 2011) 1 The Cost Accounting Standards Board (CASB) COST ACCOUNTING STANDARD ON OVERHEADS (Revised 2011) The following is the revised COST ACCOUNTING STANDARD 3 (CAS-3) issued by the Council

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

Cost & management accounting an introduction. Synopsis:

Cost & management accounting an introduction Synopsis: Accounting has always concerned itself with information production, processing and reporting while cost and management accounting has sought to provide

Cost & management accounting an introduction Synopsis: Accounting has always concerned itself with information production, processing and reporting while cost and management accounting has sought to provide

Unit Costing & Reconciliation

Unit Costing & Reconciliation Answer to Q.1: (Nov, 2003) CA Past Years Exam Answer (i) Closing stock of finished goods Sales Gross profit = Cost of goods sold available closing stock of finished goods

Unit Costing & Reconciliation Answer to Q.1: (Nov, 2003) CA Past Years Exam Answer (i) Closing stock of finished goods Sales Gross profit = Cost of goods sold available closing stock of finished goods

Graded Project. Lesson 1: Business Accounting and You OVERVIEW INSTRUCTIONS

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

Plz Remember Me in ur Prayers.

Assalam-0-Alaikum Cost & Management Accounting (MGT402) Final term papers Solved by SilentLips Ghulam Abbas Zahid MC090402571 MBA 3 rd (Management) Cell # +92-300-687 6387 +92-345-873 2201 E-mail silentlips687@hotmail.com

Assalam-0-Alaikum Cost & Management Accounting (MGT402) Final term papers Solved by SilentLips Ghulam Abbas Zahid MC090402571 MBA 3 rd (Management) Cell # +92-300-687 6387 +92-345-873 2201 E-mail silentlips687@hotmail.com

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Test Series: March 2018 Answers are to be given only in English except in the case of the candidates who have

MOCK TEST PAPER INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Test Series: March 2018 Answers are to be given only in English except in the case of the candidates who have

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2014 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice 1 B 16 B 2 B 17 B 3 B 18 D 4 C 19 D 5 C 20 C 6 D 21 C 7 B 22 C 8 B 23

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice 1 B 16 B 2 B 17 B 3 B 18 D 4 C 19 D 5 C 20 C 6 D 21 C 7 B 22 C 8 B 23

ALLAMA IQBAL OPEN UNIVERSITY ISLAMABAD (Department of Business Administration) COST ACCOUNTING (186) CHECKLIST SEMESTER: SPRING 2014

COST ACCOUNTING (186) CHECKLIST SEMESTER: SPRING 2014") Final on 13-3-2014 ALLAMA IQBAL OPEN UNIVERSITY ISLAMABAD (Department of Business Administration) COST ACCOUNTING (186) CHECKLIST SEMESTER: SPRING 2014 This packet comprises the following material: 1.

Final on 13-3-2014 ALLAMA IQBAL OPEN UNIVERSITY ISLAMABAD (Department of Business Administration) COST ACCOUNTING (186) CHECKLIST SEMESTER: SPRING 2014 This packet comprises the following material: 1.

Advantage Multiple Currency Support Current Procedures

Advantage Multiple Currency Support Current Procedures Overview: This document explains how to process multiple currencies in a single database; how to convert to a HOME currency and how to consolidate

Advantage Multiple Currency Support Current Procedures Overview: This document explains how to process multiple currencies in a single database; how to convert to a HOME currency and how to consolidate

REVIEW FOR FINAL EXAM, ACCT-2302 (SAC)

") 1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

Question No: 5 ( Marks: 1 ) - Please choose one Which of the following manufacturers is most likely to use a job order cost accounting system?

- Please choose one Which of the following manufacturers is most likely to use a job order cost accounting system?") MGT402 Latest Solved MCQs From Current Papers 2010 By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one If Selling price per unit Rs. 15.00; Direct Materials cost per unit Rs.

MGT402 Latest Solved MCQs From Current Papers 2010 By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one If Selling price per unit Rs. 15.00; Direct Materials cost per unit Rs.

Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form.

Opening Entries Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form. The journal is the book of original entry. The journal

Opening Entries Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form. The journal is the book of original entry. The journal

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

7110 PRINCIPLES OF ACCOUNTS

CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Ordinary Level MARK SCHEME for the May/June 2014 series 7110 PRINCIPLES OF ACCOUNTS 7110/22 Paper 2 (Structured), maximum raw mark 120 This mark scheme is published

CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Ordinary Level MARK SCHEME for the May/June 2014 series 7110 PRINCIPLES OF ACCOUNTS 7110/22 Paper 2 (Structured), maximum raw mark 120 This mark scheme is published

FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Ref No: Time: 120 min Marks: Total

Ref No: Time: 120 min Marks: Total") Student Info FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Ref No: 1232793 Time: 120 min Marks: 84 ExamDate: 2/22/2010 12:00:00 AM For Teacher's Use Only Q No. 1 2

Student Info FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Ref No: 1232793 Time: 120 min Marks: 84 ExamDate: 2/22/2010 12:00:00 AM For Teacher's Use Only Q No. 1 2

Full file at

1. a. Job order cost system and process cost system. b. The job order cost system provides a separate record of each quantity of product that passes through the factory. c. Process cost systems accumulate

1. a. Job order cost system and process cost system. b. The job order cost system provides a separate record of each quantity of product that passes through the factory. c. Process cost systems accumulate

B.COM II ADVANCED AND COST ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

Manufacturing Accounts

All questions copyright of Cambridge International Examinations 1 Manufacturing Accounts All questions copyright of Cambridge International Examinations 2 2 1 The following balances were extracted from

All questions copyright of Cambridge International Examinations 1 Manufacturing Accounts All questions copyright of Cambridge International Examinations 2 2 1 The following balances were extracted from

CAS 13 COST ACCOUNTING STANDARD ON COST OF SERVICE COST CENTRE

CAS 13 COST ACCOUNTING STANDARD ON COST OF SERVICE COST CENTRE The following is the COST ACCOUNTING STANDARD 13 (CAS - 13) issued by the Council of The Institute of Cost Accountants of India on COST OF

CAS 13 COST ACCOUNTING STANDARD ON COST OF SERVICE COST CENTRE The following is the COST ACCOUNTING STANDARD 13 (CAS - 13) issued by the Council of The Institute of Cost Accountants of India on COST OF

Answer to MTP_Intermediate_Syllabus 2008_Jun2014_Set 1

Paper-8: COST & MANAGEMENT ACCOUNTING SECTION - A Answer Q No. 1 (Compulsory) and any 5 from the rest Question.1 (a) Match the statement in Column 1 with the most appropriate statement in Column 2 : [1

Paper-8: COST & MANAGEMENT ACCOUNTING SECTION - A Answer Q No. 1 (Compulsory) and any 5 from the rest Question.1 (a) Match the statement in Column 1 with the most appropriate statement in Column 2 : [1

2016 Automobile Rules. Computation of Personal Use

2016 Automobile Rules Computation of Personal Use 2016 Automobile Rules: Computation of Personal Use... 2 Exhibit 1A... 8 Exhibit 1B... 9 Exhibit 1C... 10 Exhibit 1D... 11 LEGAL NOTICE: The contents of

2016 Automobile Rules Computation of Personal Use 2016 Automobile Rules: Computation of Personal Use... 2 Exhibit 1A... 8 Exhibit 1B... 9 Exhibit 1C... 10 Exhibit 1D... 11 LEGAL NOTICE: The contents of

6 Non-integrated, Integrated & Reconciliation of Cost and Financial Accounts

5.43 Activity Based Costing 6 Non-integrated, Integrated & Reconciliation of Cost and Financial Accounts Question 1 Write short note on Cost Ledger Control Account (May, 1996, 4 marks) Answer Cost Ledger

5.43 Activity Based Costing 6 Non-integrated, Integrated & Reconciliation of Cost and Financial Accounts Question 1 Write short note on Cost Ledger Control Account (May, 1996, 4 marks) Answer Cost Ledger

ACTIVITY BASE COSTING

ACTIVITY BASE COSTING Key Terms and Concepts to Know Activity-Based Costing (ABC): Activity Based Costing is a two-stage costing method in which overhead costs are assigned to overhead cost pools and the

ACTIVITY BASE COSTING Key Terms and Concepts to Know Activity-Based Costing (ABC): Activity Based Costing is a two-stage costing method in which overhead costs are assigned to overhead cost pools and the

MGT402 Cost & Management Accounting. Composed By Faheem Saqib MIDTERM EXAMINATION. Spring MGT402- Cost & Management Accounting (Session - 1)

") MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

SUGGESTED SOLUTION IPCC May 2017 EXAM. Test Code - I N J

SUGGESTED SOLUTION IPCC May 2017 EXAM COSTING Test Code - I N J 1 0 7 1 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Answer-1 (a) : Computation

SUGGESTED SOLUTION IPCC May 2017 EXAM COSTING Test Code - I N J 1 0 7 1 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Answer-1 (a) : Computation

B.COM II ADVANCED AND COST ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review (Yellow) 1) Beginning Raw Materials Inventory $ 1 Ending Raw Materials Inventory 3 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review (Yellow) 1) Beginning Raw Materials Inventory $ 1 Ending Raw Materials Inventory 3 Purchases of Raw Materials

CHAPTER 13. Performance evaluation for managers CONTENTS

CHAPTER 13 Performance evaluation for managers CONTENTS 13.1 Departmental accounting 13.2 Indirect expense allocation 13.3 Statement of financial performance with departmental contributions 13.4 Flexible

CHAPTER 13 Performance evaluation for managers CONTENTS 13.1 Departmental accounting 13.2 Indirect expense allocation 13.3 Statement of financial performance with departmental contributions 13.4 Flexible

10/21/2010. Presented By Monte Zwang Wellness Capital Management

Presented By Monte Zwang Wellness Capital Management 1 EVALUATE YOUR CURRENT FINANCIAL CONDITION (minus) (equals) (minus) (equals) (minus) (equals) Sales Direct Costs Gross Margin Overhead Expenses Net

Presented By Monte Zwang Wellness Capital Management 1 EVALUATE YOUR CURRENT FINANCIAL CONDITION (minus) (equals) (minus) (equals) (minus) (equals) Sales Direct Costs Gross Margin Overhead Expenses Net

Mark Machlis Monte Zwang

Building a Better Business Plan From the Sparkle in Your Eye through the Terrible Two's Mark Machlis Monte Zwang HONEY, I WANT TO HAVE A BUSINESS. 1 BUSINESS PLANNING MARKET RESEARCH 2 FIRST, SOME BASICS

Building a Better Business Plan From the Sparkle in Your Eye through the Terrible Two's Mark Machlis Monte Zwang HONEY, I WANT TO HAVE A BUSINESS. 1 BUSINESS PLANNING MARKET RESEARCH 2 FIRST, SOME BASICS

IPCC November COSTING & FM Test Code 8051 Branch (MULTIPLE) (Date : ) All questions are compulsory.

(Date : ) All questions are compulsory.") IPCC November 2017 COSTING & FM Test Code 8051 Branch (MULTIPLE) (Date : 09.07.2017) (50 Marks) Note: All questions are compulsory. Question 1 (8 marks) Cash Flow Statement As on 31 st March, 2015 A. Cash

IPCC November 2017 COSTING & FM Test Code 8051 Branch (MULTIPLE) (Date : 09.07.2017) (50 Marks) Note: All questions are compulsory. Question 1 (8 marks) Cash Flow Statement As on 31 st March, 2015 A. Cash

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review (Blue) 1) Beginning Raw Materials Inventory $ 3 Ending Raw Materials Inventory 5 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review (Blue) 1) Beginning Raw Materials Inventory $ 3 Ending Raw Materials Inventory 5 Purchases of Raw Materials

MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING. Suggested Answers/ Hints

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING. Suggested Answers/ Hints") MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Suggested Answers/ Hints 1. (a) (i) Standard input (kg.) of Material SW: Test Series:

MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Suggested Answers/ Hints 1. (a) (i) Standard input (kg.) of Material SW: Test Series:

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2014 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

Interpretation of Financial Statements

Interpretation of Financial Statements Steven M. Bragg Chapter 1 Overview of the Financial Statements... 1 Learning Objectives... 1 Introduction... 1 The General Ledger... 1 The Accrual Basis of Accounting...

Interpretation of Financial Statements Steven M. Bragg Chapter 1 Overview of the Financial Statements... 1 Learning Objectives... 1 Introduction... 1 The General Ledger... 1 The Accrual Basis of Accounting...

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Chapter 3: Cost-Volume-Profit Analysis (CVP)

") Chapter 3: Cost-Volume-Profit Analysis (CVP) Identify how changes in volume affect costs: Cost Behavior How costs change in response to changes in a cost driver. Cost driver: any factor whose change makes

Chapter 3: Cost-Volume-Profit Analysis (CVP) Identify how changes in volume affect costs: Cost Behavior How costs change in response to changes in a cost driver. Cost driver: any factor whose change makes

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1 Ending Raw Materials Inventory 3 Purchases of Raw Materials 6 Direct

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1 Ending Raw Materials Inventory 3 Purchases of Raw Materials 6 Direct

Accounting for Managers

Accounting for Managers 2 nd Edition Steven M. Bragg Chapter 1 The Need for Accounting Information... 1 Learning Objectives... 1 Introduction... 1 The Accountancy Concept... 1 Financial and Managerial

Accounting for Managers 2 nd Edition Steven M. Bragg Chapter 1 The Need for Accounting Information... 1 Learning Objectives... 1 Introduction... 1 The Accountancy Concept... 1 Financial and Managerial

Chapter 23 Flexible Budgets and Standard Cost Systems

Chapter 23 Flexible Budgets and Standard Cost Systems Review Questions 1. What is a variance? A variance is the difference between an actual amount and the budgeted amount. 2. Explain the difference between

Chapter 23 Flexible Budgets and Standard Cost Systems Review Questions 1. What is a variance? A variance is the difference between an actual amount and the budgeted amount. 2. Explain the difference between

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an):

- Please choose one Wages outstanding given in the trial balance will be treated as a (an):") Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose