Preview. Chapter 13. Depreciation and Appreciation. Definitions of Exchange Rates. Exchange Rates and the Foreign Exchange Market: An Asset Approach

|

|

|

- Walter Robinson

- 6 years ago

- Views:

Transcription

1 Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Preview The basics of exchange rates Exchange rates and the prices of goods The foreign exchange markets The demand for currency and other assets A model of foreign exchange markets role of interest rates on currency deposits role of expectations about the exchange rates Slides prepared by Thomas Bishop Copyright 2006 Pearson Addison-Wesley. All rights reserved Definitions of Exchange Rates Depreciation and Appreciation Exchange rates are quoted as foreign currency per unit of domestic currency or domestic currency per unit of foreign currency. How much can be exchanged for one dollar? 102/$1 How much can be exchanged for one yen? $0.0098/ 1 Exchange rate allow us to denominate the cost or price of a good or service in a common currency. How much does a Honda cost? 3,000,000 Or, 3,000,000 x $0.0098/ 1 = $29,400 Depreciation is a decrease in the value of a currency relative to another currency. A depreciated currency is less valuable (less expensive) and therefore can be exchanged for (can buy) a smaller amount of foreign currency. $1/ 1! $1.20/ 1 means that the dollar has depreciated relative to the euro. It now takes $1.20 to buy one euro, so that the dollar is less valuable. The euro has appreciated relative to the dollar: it is now more valuable. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

2 Depreciation and Appreciation (cont.) Depreciation and Appreciation (cont.) Appreciation is an increase in the value of a currency relative to another currency. An appreciated currency is more valuable (more expensive) and therefore can be exchanged for (can buy) a larger amount of foreign currency. $1/ 1! $0.90/ 1 means that the dollar has appreciated relative to the euro. It now takes only $0.90 to buy one euro, so that the dollar is more valuable. The euro has depreciated relative to the dollar: it is now less valuable. A depreciated currency is less valuable, and therefore it can buy fewer foreign produced goods that are denominated in foreign currency. How much does a Honda cost? 3,000,000 3,000,000 x $0.0098/ 1 = $29,400 3,000,000 x $0.0100/ 1 = $30,000 A depreciated currency means that imports are more expensive and domestically produced goods and exports are less expensive. A depreciated currency lowers the price of exports relative to the price of imports. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved Depreciation and Appreciation (cont.) The Foreign Exchange Market An appreciated currency is more valuable, and therefore it can buy more foreign produced goods that are denominated in foreign currency. How much does a Honda cost? 3,000,000 3,000,000 x $0.0098/ 1 = $29,400 3,000,000 x $0.0090/ 1 = $27,000 An appreciated currency means that imports are less expensive and domestically produced goods and exports are more expensive. An appreciated currency raises the price of exports relative to the price of imports. The participants: 1. Commercial banks and other depository institutions: transactions involve buying/selling of bank deposits in different currencies for investment. 2. Non bank financial institutions (pension funds, insurance funds) may buy/sell foreign assets. 3. Private firms: conduct foreign currency transactions to buy/sell goods, assets or services. 4. Central banks: conduct official international reserves transactions. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

3 The Foreign Exchange Market (cont.) The Foreign Exchange Market (cont.) Buying and selling in the foreign exchange market are dominated by commercial banks. Inter-bank transactions of deposits in foreign currencies occur in amounts $1 million or more per transaction. Central banks sometimes intervene, but the direct effects of their transactions are usually small and transitory. Characteristics of the market: Trading occurs mostly in major financial cities: London, New York, Tokyo, Frankfurt, Singapore. The volume of foreign exchange has grown: in 1989 the daily volume of trading was $600 billion, in 2001 the daily volume of trading was $1.2 trillion. About 90% of transactions in 2001 involved US dollars. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved The Foreign Exchange Market (cont.) Spot Rates and Forward Rates Computers transmit information rapidly and have integrated markets. The integration of markets implies that there is no significant arbitrage between markets. if dollars are cheaper in New York than in London, people will buy them in New York and stop buying them in London. The price of dollars in New York rises and the price of dollars in London falls, until the prices in the two markets are equal. Copyright 2006 Pearson Addison-Wesley. All rights reserved Spot rates are exchange rates for currency exchanges on the spot, or when trading is executed in the present. Forward rates are exchange rates for currency exchanges that will occur at a future ( forward ) date. forward dates are typically 30, 90, 180 or 360 days in the future. rates are negotiated between individual institutions in the present, but the exchange occurs in the future. Copyright 2006 Pearson Addison-Wesley. All rights reserved

4 Spot and Forward Rates Other methods of currency exchange Foreign exchange swaps: a combination of a spot sale with a forward repurchase, both negotiated between individual institutions. swaps often result in lower fees or transactions costs because they combine two transactions. Futures contracts: a contract designed by a third party for a standard amount of foreign currency delivered/received on a standard date. contracts can be bought and sold in markets, and only the current owner is obliged to fulfill the contract. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved Other Methods of Currency Exchange The Demand for Currency Deposits Options contracts: a contract designed by a third party for a standard amount of foreign currency delivered/received on or before a standard date. contracts can be bought and sold in markets. a contract gives the owner the option, but not obligation, of buying or selling currency if the need arises. What influences the demand for (willingness to buy) deposits denominated in domestic or foreign currency? Factors that influence the return on assets determine the demand for those assets. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

5 The Demand for Currency Deposits (cont.) The Demand for Currency Deposits (cont.) Rate of return: the percentage change in value that an asset offers during a time period. The annual return for $100 savings account with an interest rate of 2% is $100 x 1.02 = $102, so that the rate of return = ($102 - $100)/$100 = 2% Real rate of return: inflation-adjusted rate of return. stated in terms of real purchasing power: the amount of real goods & services that can be purchased with the asset. the real rate of return for the above savings account when inflation is 1.5%: 2% 1.5% = 0.5%. The asset can purchase 0.5% more goods and services after 1 year. If prices are given at some level, inflation is 0% and (nominal) rates of return = real rates of return. For bank deposits in different currencies, we often assume that prices are given at some level. (A good short run assumption.) Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved The Demand for Currency Deposits (cont.) The Demand for Currency Deposits (cont.) Risk of holding assets also influences decisions about whether to buy them. Liquidity of an asset, or ease of using the asset to buy goods and services, also influences the willingness to buy assets. But we assume that risk and liquidity of bank deposits in the foreign exchange market are the same, regardless of their currency denomination. risk and liquidity are only of secondary importance when deciding to buy or sell currency. importers and exporters may be concerned about risk and liquidity, but they make up a small fraction of the market. We assume that investors are primarily concerned about the rates of return on bank deposits. Rates of return are determined by interest rates that the assets earn expectations about appreciation or depreciation Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

6 The Demand for Currency Deposits (cont.) The Demand for Currency Deposits (cont.) A currency s interest rate is the amount of a currency an individual can earn by lending a unit of the currency for a year. The rate of return for a deposit in domestic currency is the interest rate that the bank deposit earns. To compare the rate of return on a deposit in domestic currency with one in foreign currency, consider the interest rate for the foreign currency deposit the expected rate of appreciation or depreciation of the foreign currency relative to the domestic currency. Suppose the interest rate on a dollar deposit is 2%. Suppose the interest rate on a euro deposit is 4%. Does a euro deposit yield a higher expected rate of return? Suppose today the exchange rate is $1/ 1, and the expected rate 1 year in the future is $0.97/ 1. $100 can be exchanged today for 100. These 100 will yield 104 after 1 year. These 104 are expected to be worth $0.97/ 1 x 104 = $ Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved The Demand for Currency Deposits (cont.) The Demand for Currency Deposits (cont.) The rate of return in terms of dollars from investing in euro deposits is ($ $100)/$100 = 0.88%. Let s compare this rate of return with the rate of return from a dollar deposit. rate of return is simply the interest rate After 1 year the $100 is expected to yield $102: ($102-$100)/$100 = 2% The euro deposit has a lower expected rate of return: all investors will prefer dollar deposits and none are willing to hold euro deposits. Note that the expected rate of appreciation of the euro is ($0.97- $1)/$1 = = -3%. We simplify the analysis by saying that the dollar rate of return on euro deposits approximately equals the interest rate on euro deposits plus the expected rate of appreciation on euro deposits 4% + -3% = 1% 0.88% R + (E e $/ -E $/ )/E $/ Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

The Demand for Currency Assets The difference in the rate of return on dollar deposits and euro deposits is R $ -(R + (E e $/ -E $/ )/E $/ ) = R $ - R -(E e $/ -E $/ )/E $/ expected rate of return")

7 The Demand for Currency Deposits (cont.) The Demand for Currency Assets The difference in the rate of return on dollar deposits and euro deposits is R $ -(R + (E e $/ -E $/ )/E $/ ) = R $ - R -(E e $/ -E $/ )/E $/ expected rate of return = interest rate on dollar deposits interest rate on euro deposits expected exchange rate current exchange rate expected rate of appreciation of the euro expected rate of return on euro deposits Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved The Market for Foreign Exchange The Market for Foreign Exchange (cont.) We use the demand for (rate of return on) dollar denominated deposits and the demand for (rate of return on) foreign currency denominated deposits to construct a model of the foreign exchange market. The foreign exchange market is in equilibrium when deposits of all currencies offer the same expected rate of return: interest parity. interest parity implies that deposits in all currencies are deemed equally desirable assets. Interest parity says: R $ = R + (E e $/ -E $/ )/E $/ Why should this condition hold? Suppose it didn t. Suppose R $ > R + (E e $/ -E $/ )/E $/. Then no investor would want to hold euro deposits, driving down the demand and price of euros. Then all investors would want to hold dollar deposits, driving up the demand and price of dollars. The dollar would appreciate and the euro would depreciate, increasing the right side until equality was achieved. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

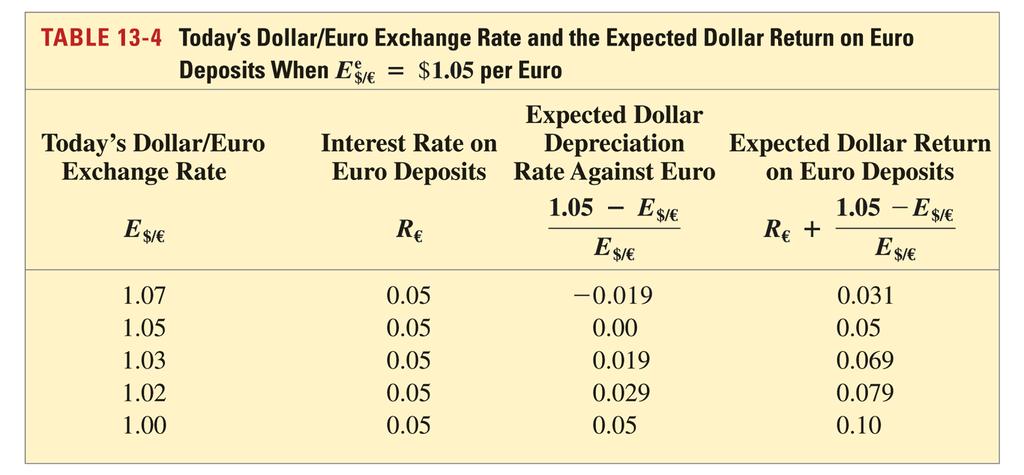

8 The Market for Foreign Exchange (cont.) The Market for Foreign Exchange (cont.) How do changes in the current exchange rate affect expected returns in foreign currency? Depreciation of the domestic currency today lowers the expected return on deposits in foreign currency. A current depreciation of domestic currency will raise the initial cost of investing in foreign currency, thereby lowering the expected return in foreign currency. Appreciation of the domestic currency today raises the expected return of deposits in foreign currency. A current appreciation of the domestic currency will lower the initial cost of investing in foreign currency, thereby raising the expected return in foreign currency. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved Expected Returns on Euro Deposits when E e $/ = $1.05 Per Euro Current exchange rate E $/ Interest rate on euro deposits R Expected rate of dollar depreciation ( E $/ )/E $/ Expected dollar return on euro deposits R + ( E $/ )/E $/ The Current Exchange Rate and the Expected Return on Dollar Deposits Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

9 The Current Exchange Rate and the Expected Return on Dollar Deposits Determination of the Equilibrium Exchange Rate Current exchange rate, E $/ No one is willing to hold euro deposits No one is willing to hold dollar deposits R Expected dollar return $ on dollar deposits, R $ Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved The Market for Foreign Exchange The effects of changing interest rates: an increase in the interest rate paid on deposits denominated in a particular currency will increase the rate of return on those deposits. This leads to an appreciation of the currency. A rise in dollar interest rates causes the dollar to appreciate. A rise in euro interest rates causes the dollar to depreciate. The Effect of a Rise in the Dollar Interest Rate A depreciation of the euro is an appreciation of the dollar. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

10 The Effect of a Rise in the Euro Interest Rate The Effect of an Expected Appreciation of the Euro People now expect the euro to appreciate Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved The Effect of an Expected Appreciation of the Euro (cont.) If people expect the euro to appreciate in the future, then investment will pay off in a valuable ( strong ) euro, so that these future euros will be able to buy many dollars and many dollar denominated goods. the expected return on euros therefore increases. an expected appreciation of a currency leads to an actual appreciation (a self-fulfilling prophecy) an expected depreciation of a currency leads to an actual depreciation (a self-fulfilling prophecy) Covered Interest Parity Covered interest parity relates interest rates across countries and the rate of change between forward exchange rates and the spot exchange rate: R $ = R + (F $/ -E $/ )/E $/ where F $/ is the forward exchange rate. It says that rates of return on dollar deposits and covered foreign currency deposits are the same. How could you make easy, risk-free money in the foreign exchange markets if covered interest parity did not hold? Covered positions using the forward rate involve little risk. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

11 Summary Summary (cont.) 1. Exchange rates are prices of foreign currencies in terms of domestic currencies, or vice versa. 2. Depreciation of a country s currency means that it is less expensive (valuable) and goods denominated in it are less expensive: exports are cheaper and imports more expensive. A depreciation will hurt consumers of imports but help producers of exports. 3. Appreciation of a country s currency means that it is more expensive (valuable) and goods denominated in it are more expensive: exports are more expensive and imports cheaper. An appreciation will help consumers of imports but hurt producers of exports. 4. Commercial banks that invest in deposits of different currencies dominate the foreign exchange market. Expected rates of return are most important in determining the willingness to hold these deposits. Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved Summary (cont.) 5. Returns on bank deposits in the foreign exchange market are influenced by interest rates and expected exchange rates. 6. Equilibrium in the foreign exchange market occurs when returns on deposits in domestic currency and in foreign currency are equal: interest rate parity. 7. An increase in the interest rate on a currency s deposit leads to an increase in the rate of return and to an appreciation of the currency. Copyright 2006 Pearson Addison-Wesley. All rights reserved Summary (cont.) 8. An expected appreciation of a currency leads to an increase in the expected rate of return for that currency, and leads to an actual appreciation. 9. Covered interest parity says that rates of return on domestic currency deposits and covered foreign currency deposits using the forward exchange rate are the same. Copyright 2006 Pearson Addison-Wesley. All rights reserved

12 Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved Copyright 2006 Pearson Addison-Wesley. All rights reserved

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run.

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Introduction to Foreign Exchange Slides for International Finance (KOMIF Chapter 3)

") Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Lecture 14 Internatinaa Ecinimics. Exchange Rates and the Fireign Exchange Market: An Asset Appriach

Lecture 14 Internatinaa Ecinimics Exchange Rates and the Fireign Exchange Market: An Asset Appriach Preview The basics of exchange rates: defnitons and computaton Exchange rates and the relatve prices

Lecture 14 Internatinaa Ecinimics Exchange Rates and the Fireign Exchange Market: An Asset Appriach Preview The basics of exchange rates: defnitons and computaton Exchange rates and the relatve prices

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice

Chapter 8. Preview. Instruments of trade policy. The Instruments of Trade Policy

Chapter 8 The Instruments of Trade Policy Slides prepared by Thomas Bishop Preview Partial equilibrium analysis of tariffs: supply, demand and trade in a single industry Costs and benefits of tariffs Export

Chapter 8 The Instruments of Trade Policy Slides prepared by Thomas Bishop Preview Partial equilibrium analysis of tariffs: supply, demand and trade in a single industry Costs and benefits of tariffs Export

Chapter 4. Understanding Interest Rates

Chapter 4 Understanding Interest Rates Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright 2007 Pearson Addison-Wesley. All rights reserved.

Chapter 4 Understanding Interest Rates Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright 2007 Pearson Addison-Wesley. All rights reserved.

Chapter 17: Output and the Exchange Rate in the Short Run

Chapter 17: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 420-459 1 Preview Determinants of

Chapter 17: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 420-459 1 Preview Determinants of

Chapter 17 (6) Output and the Exchange Rate in the Short Run

Output and the Exchange Rate in the Short Run") Chapter 17 (6) Output and the Exchange Rate in the Short Run Preview Determinants of aggregate demand in the short run A short-run model of output markets A short-run model of asset markets A short-run

Chapter 17 (6) Output and the Exchange Rate in the Short Run Preview Determinants of aggregate demand in the short run A short-run model of output markets A short-run model of asset markets A short-run

Chapter 5. The Standard Trade Model. Slides prepared by Thomas Bishop

Chapter 5 The Standard Trade Model Slides prepared by Thomas Bishop Preview Measuring the values of production and consumption Welfare and terms of trade Effects of economic growth Effects of international

Chapter 5 The Standard Trade Model Slides prepared by Thomas Bishop Preview Measuring the values of production and consumption Welfare and terms of trade Effects of economic growth Effects of international

The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination Prof. George Alogoskoufis

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination Prof. George Alogoskoufis

International Finance

International Finance Chapter 21 CHAPTER CHECKLIST 1. Describe a country s balance of payments accounts and explain what determines the amount of international borrowing and lending. 2. Explain how the

International Finance Chapter 21 CHAPTER CHECKLIST 1. Describe a country s balance of payments accounts and explain what determines the amount of international borrowing and lending. 2. Explain how the

Determining the Quantity Demanded of an Asset

Determining the Quantity Demanded of an Asset Wealth the total resources owned by the individual, including all assets Expected Return the return expected over the next period on one asset relative to

Determining the Quantity Demanded of an Asset Wealth the total resources owned by the individual, including all assets Expected Return the return expected over the next period on one asset relative to

Chapter 12. Preview. National Income Accounts. National Income Accounting and the Balance of Payments. National income accounts

Chapter 12 National Income Accounting and the Balance of Payments Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview National income accounts measures

Chapter 12 National Income Accounting and the Balance of Payments Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview National income accounts measures

Chapter 2 International Financial Markets, Interest Rates and Exchange Rates

George Alogoskoufis, International Macroeconomics and Finance Chapter 2 International Financial Markets, Interest Rates and Exchange Rates This chapter examines the role and structure of international

George Alogoskoufis, International Macroeconomics and Finance Chapter 2 International Financial Markets, Interest Rates and Exchange Rates This chapter examines the role and structure of international

Chapter 15. The Foreign Exchange Market. Chapter Preview

Chapter 15 The Foreign Exchange Market Chapter Preview In the mid-1980s, American businesses became less competitive relative to their foreign counterparts. By the 2000s, though, competitiveness increased.

Chapter 15 The Foreign Exchange Market Chapter Preview In the mid-1980s, American businesses became less competitive relative to their foreign counterparts. By the 2000s, though, competitiveness increased.

Chapter 15. Multiple Deposit Creation and the Money Supply Process

Chapter 15 Multiple Deposit Creation and the Money Supply Process Players in the Money Supply Process Central bank - the government agency that oversees the banking system and is responsible for the conduct

Chapter 15 Multiple Deposit Creation and the Money Supply Process Players in the Money Supply Process Central bank - the government agency that oversees the banking system and is responsible for the conduct

4. Understanding.. Interest Rates. Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention

Fixed Exchange Rates and Foreign Exchange Intervention") Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention

Fixed Exchange Rates and Foreign Exchange Intervention") Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L8: The Foreign Exchange Market www. notes638.wordpress.com Copyright 2015 Pearson Education, Ltd. All rights reserved. 8-1 Chapter

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L8: The Foreign Exchange Market www. notes638.wordpress.com Copyright 2015 Pearson Education, Ltd. All rights reserved. 8-1 Chapter

Lower prices. Lower costs, esp. wages. Higher productivity. Higher quality/more desirable exports. Greater natural resources. Higher interest rates

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

Preview. Chapter 9. The Instruments of Trade Policy

Chapter 9 The Instruments of Trade Policy Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Partial equilibrium analysis of tariffs in a single industry: supply, demand, and trade Costs

Chapter 9 The Instruments of Trade Policy Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Partial equilibrium analysis of tariffs in a single industry: supply, demand, and trade Costs

Chapter 17 Appendix A

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Chapter 10. Preview. Introduction. Trade Policy in Developing Countries

Chapter 10 Trade Policy in Developing Countries Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Import substituting industrialization Trade liberalization

Chapter 10 Trade Policy in Developing Countries Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Import substituting industrialization Trade liberalization

Chapter 18: Output and the Exchange Rate in the Short Run

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

Determining Exchange Rates. Determining Exchange Rates

Determining Exchange Rates Determining Exchange Rates Chapter Objectives To explain how exchange rate movements are measured; To explain how the equilibrium exchange rate is determined; and To examine

Determining Exchange Rates Determining Exchange Rates Chapter Objectives To explain how exchange rate movements are measured; To explain how the equilibrium exchange rate is determined; and To examine

UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm

The International Monetary Environment and Financial Management in the Global Firm") UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm Objectives Exchange rates and currencies How exchange rates are determined The monetary and financial systems

UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm Objectives Exchange rates and currencies How exchange rates are determined The monetary and financial systems

Preview. Chapter 10. Introduction. Introduction

Chapter 10 Trade Policy in Developing Countries Preview Import substituting industrialization Trade liberalization since 1985 Export oriented industrialization Slides prepared by Thomas Bishop Copyright

Chapter 10 Trade Policy in Developing Countries Preview Import substituting industrialization Trade liberalization since 1985 Export oriented industrialization Slides prepared by Thomas Bishop Copyright

Chapter 10. The Foreign Exchange Market

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Nominal exchange rate

Nominal exchange rate The nominal exchange rate between two currencies is the price of one currency in terms of the other. The nominal exchange rate (or, for short, exchange rate) will be denoted by the

Nominal exchange rate The nominal exchange rate between two currencies is the price of one currency in terms of the other. The nominal exchange rate (or, for short, exchange rate) will be denoted by the

The answer lies in the role of the exchange rate, which is determined in the foreign exchange market.

In yesterday s lesson we saw that the market for loanable funds shows us how financial capital flows into or out of a nation s financial account. Goods and services also flow, but this flow is tracked

In yesterday s lesson we saw that the market for loanable funds shows us how financial capital flows into or out of a nation s financial account. Goods and services also flow, but this flow is tracked

Quoting an exchange rate. The exchange rate. Examples of appreciation. Currency appreciation. Currency depreciation. Examples of depreciation

The exchange rate The nominal exchange rate (or, for short, exchange rate) between two currencies is the price of one currency in terms of the other. It allows domestic purchasing power to be spent abroad.

The exchange rate The nominal exchange rate (or, for short, exchange rate) between two currencies is the price of one currency in terms of the other. It allows domestic purchasing power to be spent abroad.

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

05/12/2011. Preview. Chapter 9. The Instruments of Trade Policy

Chapter 9 The Instruments of Trade Policy Preview Partial equilibrium analysis of tariffs in a single industry: supply, demand, and trade Costs and benefits of tariffs Export subsidies Import quotas Voluntary

Chapter 9 The Instruments of Trade Policy Preview Partial equilibrium analysis of tariffs in a single industry: supply, demand, and trade Costs and benefits of tariffs Export subsidies Import quotas Voluntary

Problems involving Foreign Exchange Solutions

Problems involving Foreign Exchange Solutions 1. A bank quotes the following rates: CHF/USD 1.0898-1.0910 and JPY/USD 119 121. What is the minimum JPY/CHF bid and the maximum ask rate that the bank would

Problems involving Foreign Exchange Solutions 1. A bank quotes the following rates: CHF/USD 1.0898-1.0910 and JPY/USD 119 121. What is the minimum JPY/CHF bid and the maximum ask rate that the bank would

1 The Structure of the Market

The Foreign Exchange Market 1 The Structure of the Market The foreign exchange market is an example of a speculative auction market that trades the money of various countries continuously around the world.

The Foreign Exchange Market 1 The Structure of the Market The foreign exchange market is an example of a speculative auction market that trades the money of various countries continuously around the world.

Chapter 13 (2) National Income Accounting and the Balance of Payments

National Income Accounting and the Balance of Payments") Chapter 13 (2) National Income Accounting and the Balance of Payments Preview National income accounts measures of national income measures of value of production measures of value of expenditure National

Chapter 13 (2) National Income Accounting and the Balance of Payments Preview National income accounts measures of national income measures of value of production measures of value of expenditure National

Financial Management

Financial Management International Finance 1 RISK AND HEDGING In this lecture we will cover: Justification for hedging Different Types of Hedging Instruments. How to Determine Risk Exposure. Good references

Financial Management International Finance 1 RISK AND HEDGING In this lecture we will cover: Justification for hedging Different Types of Hedging Instruments. How to Determine Risk Exposure. Good references

Chapter 13: National Income Accounting and the Balance of Payments

Chapter 13: National Income Accounting and the Balance of Payments Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 288-316 1 Preview National

Chapter 13: National Income Accounting and the Balance of Payments Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 288-316 1 Preview National

Chapter 20 (9) Financial Globalization: Opportunity and Crisis

Financial Globalization: Opportunity and Crisis") Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

FOREIGN EXCHANGE MARKET. Luigi Vena 05/08/2015 Liuc Carlo Cattaneo

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

Week-7. Dr. Ahmed. Domestic Firms International Firms Multinational Firms Global Firms

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

Chapter 16. Price Levels and the Exchange Rate in the Long Run

Chapter 16 Price Levels and the Exchange Rate in the Long Run Preview Law of one price Purchasing power parity Long-run model of exchange rates: monetary approach (based on absolute version of PPP) Relationship

Chapter 16 Price Levels and the Exchange Rate in the Long Run Preview Law of one price Purchasing power parity Long-run model of exchange rates: monetary approach (based on absolute version of PPP) Relationship

Chapter 2. Overview of the Financial System. Chapter Preview

Chapter 2 Overview of the Financial System Chapter Preview Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds. At the same time, Walter has money he wishes

Chapter 2 Overview of the Financial System Chapter Preview Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds. At the same time, Walter has money he wishes

Preview PP542. International Capital Markets. Gains from Trade. International Capital Markets. The Three Types of International Transaction Trade

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

6 The Open Economy. This chapter:

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

Chapter 17. Exchange Rates and International Economic Policy

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Lecture 6: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

In this Session, you will explore international financial markets. You will also: Learn about the international bond, international equity, and

1 In this Session, you will explore international financial markets. You will also: Learn about the international bond, international equity, and Eurocurrency markets. Understand the primary functions

1 In this Session, you will explore international financial markets. You will also: Learn about the international bond, international equity, and Eurocurrency markets. Understand the primary functions

Chapter 9. Banking and the Management of Financial Institutions

Chapter 9 Banking and the Management of Financial Institutions Copyright 2007 Pearson Addison-Wesley. All rights reserved. 9-2 Basic Banking Cash Deposit First National Bank First National Bank Assets

Chapter 9 Banking and the Management of Financial Institutions Copyright 2007 Pearson Addison-Wesley. All rights reserved. 9-2 Basic Banking Cash Deposit First National Bank First National Bank Assets

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 1. Name:

Rutgers University Spring 2013 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 1 Name: 1. When the exchange value of the euro rises in terms of the U.S. dollar, U.S. residents

Rutgers University Spring 2013 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 1 Name: 1. When the exchange value of the euro rises in terms of the U.S. dollar, U.S. residents

dr Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Determinants of the demand for foreign currencies To understand what factors determine the exchange

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Determinants of the demand for foreign currencies To understand what factors determine the exchange

Slides for International Finance Financial Globalization (KOM 21)

") Financial Globalization (KOM 21) American University 2011-10-05 Preview International Capital Markets Gains from Trade International Capital Markets Policy constraints and international financial markets

Financial Globalization (KOM 21) American University 2011-10-05 Preview International Capital Markets Gains from Trade International Capital Markets Policy constraints and international financial markets

Chapter 7. Leverage and Capital Structure

Chapter 7 Leverage and Capital Structure INTRODUCTION Leverage, as a business term, refers to debt or to the borrowing of funds to finance the purchase of a company's assets. Business owners can use either

Chapter 7 Leverage and Capital Structure INTRODUCTION Leverage, as a business term, refers to debt or to the borrowing of funds to finance the purchase of a company's assets. Business owners can use either

The Money Supply Model

The Money Supply Model Define money as currency plus checkable deposits: M1 The Fed can control the monetary base better than it can control reserves Link the money supply (M) to the monetary base (MB)

The Money Supply Model Define money as currency plus checkable deposits: M1 The Fed can control the monetary base better than it can control reserves Link the money supply (M) to the monetary base (MB)

ECON MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 14 - FED and Monetary Policy Towson University 1 / 32 Disclaimer These lecture notes are customized for

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 14 - FED and Monetary Policy Towson University 1 / 32 Disclaimer These lecture notes are customized for

Interna2onal Capital and Financial Markets, and the Determina2on of Exchange Rates. Prof. George Alogoskoufis Fletcher School, TuEs University

Interna2onal Capital and Financial Markets, and the Determina2on of Exchange Rates Prof. George Alogoskoufis Fletcher School, TuEs University Methods of Financing Deficits in the Current Account 1. Foreign

Interna2onal Capital and Financial Markets, and the Determina2on of Exchange Rates Prof. George Alogoskoufis Fletcher School, TuEs University Methods of Financing Deficits in the Current Account 1. Foreign

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic exposure?

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic exposure?

INTERNATIONAL FINANCE TOPIC

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

FIN 4140 Financial Markets & Institutions

FIN 4140 Financial Markets & Institutions Lecture 9-10 Money Market Money Market Securities Securities with maturities within one year are referred to as money market securities. They are issued by corporations

FIN 4140 Financial Markets & Institutions Lecture 9-10 Money Market Money Market Securities Securities with maturities within one year are referred to as money market securities. They are issued by corporations

Exchange rate and interest rates. Rodolfo Helg, February 2018 (adapted from Feenstra Taylor)

") Exchange rate and interest rates Rodolfo Helg, February 2018 (adapted from Feenstra Taylor) Defining the Exchange Rate Exchange rate (E domestic/foreign ) The price of a unit of foreign currency in terms

Exchange rate and interest rates Rodolfo Helg, February 2018 (adapted from Feenstra Taylor) Defining the Exchange Rate Exchange rate (E domestic/foreign ) The price of a unit of foreign currency in terms

Chapter 6. The Standard Trade Model

Chapter 6 The Standard Trade Model Preview Relative supply and relative demand The terms of trade and welfare Effects of economic growth, import tariffs, and export subsidies International borrowing and

Chapter 6 The Standard Trade Model Preview Relative supply and relative demand The terms of trade and welfare Effects of economic growth, import tariffs, and export subsidies International borrowing and

Stochastic Models. Introduction to Derivatives. Walt Pohl. April 10, Department of Business Administration

Stochastic Models Introduction to Derivatives Walt Pohl Universität Zürich Department of Business Administration April 10, 2013 Decision Making, The Easy Case There is one case where deciding between two

Stochastic Models Introduction to Derivatives Walt Pohl Universität Zürich Department of Business Administration April 10, 2013 Decision Making, The Easy Case There is one case where deciding between two

Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences.

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

Opening the Economy. Topic 9

Opening the Economy Topic 9 Goals of Topic 9 What is the exchange rate? NX is back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

Opening the Economy Topic 9 Goals of Topic 9 What is the exchange rate? NX is back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

International Economics: the Exchange Rate

Paolo Sospiro Dipartimento degli Studi sullo Sviluppo Economico Facoltà di Scienze Politiche Università di Macerata paolo.sospiro@unimc.it International Economics: the Exchange Rate Macerata 16 November

Paolo Sospiro Dipartimento degli Studi sullo Sviluppo Economico Facoltà di Scienze Politiche Università di Macerata paolo.sospiro@unimc.it International Economics: the Exchange Rate Macerata 16 November

ECO 328 SUMMER Sample Questions Topics I.1-3. I.1 National Income Accounting and the Balance of Payments

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

Chapter 18. The International Financial System

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Operating Exposure. Operating & Financing Cash Flows. Expected Versus Unexpected Changes in Cash Flows. Operating & Financing Cash Flows

Chapter 9 Prepared by Shafiq Jadallah To Accompany Fundamentals of Multinational Finance Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman Copyright 2003 Pearson Education, Inc. Slide 9-1 Chapter

Chapter 9 Prepared by Shafiq Jadallah To Accompany Fundamentals of Multinational Finance Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman Copyright 2003 Pearson Education, Inc. Slide 9-1 Chapter

INTERNATIONAL FINANCIAL MARKETS

INTERNATIONAL FINANCIAL MARKETS The Market for Currencies The Forex trading market is the market for currencies. It is a large network of central banks and individual investors all engaged in the process

INTERNATIONAL FINANCIAL MARKETS The Market for Currencies The Forex trading market is the market for currencies. It is a large network of central banks and individual investors all engaged in the process

Chapter 11: Financial Markets Section 2

Chapter 11: Financial Markets Section 2 Objectives 1. Describe the characteristics of bonds as financial assets. 2. Identify different types of bonds. 3. Describe the characteristics of other types of

Chapter 11: Financial Markets Section 2 Objectives 1. Describe the characteristics of bonds as financial assets. 2. Identify different types of bonds. 3. Describe the characteristics of other types of

Chapter 5. The Foreign Exchange Market. Foreign Exchange Markets: Learning Objectives. Foreign Exchange Markets. Foreign Exchange Markets

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Chapter 19 International Monetary Systems: An Historical Overview

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

Capital & Money Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

Chapter 19 (8) International Monetary Systems: An Historical Overview

International Monetary Systems: An Historical Overview") Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 2. The Foreign Exchange Market Cambridge University Press 2-1

Chapter 2 The Foreign Exchange Market 2018 Cambridge University Press 2-1 Exhibit 2.1 The Structure of the Foreign Exchange Market Most important cities: London, New York, Tokyo ForEx (or FX) operates

Chapter 2 The Foreign Exchange Market 2018 Cambridge University Press 2-1 Exhibit 2.1 The Structure of the Foreign Exchange Market Most important cities: London, New York, Tokyo ForEx (or FX) operates

Foreign Exchange Markets: Key Institutional Features (cont)

") Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

International Finance

International Finance Review of previous lecture January 16, 2018 Review of previous lecture () Econ 457 Spring 2018 January 16, 2018 1 / 9 Exchange rate Bilateral; e.g., dollar per euro or euro per dollar

International Finance Review of previous lecture January 16, 2018 Review of previous lecture () Econ 457 Spring 2018 January 16, 2018 1 / 9 Exchange rate Bilateral; e.g., dollar per euro or euro per dollar

Bond and Common Share Valuation

Bond and Common Share Valuation Lakehead University Fall 2004 Outline of the Lecture Bonds and Bond Valuation The Determinants of Interest Rates Common Share Valuation 2 Bonds and Bond Valuation A corporation

Bond and Common Share Valuation Lakehead University Fall 2004 Outline of the Lecture Bonds and Bond Valuation The Determinants of Interest Rates Common Share Valuation 2 Bonds and Bond Valuation A corporation

1. Exchange Rates Definition: An exchange rate is a price: The relative price of two currencies.

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management International Finance Many of the concepts and techniques are the same as the one used in other Finance classes.

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management International Finance Many of the concepts and techniques are the same as the one used in other Finance classes.

Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy

Bank of Japan Review 27-E-2 Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy Teppei Nagano, Eiko Ooka, and Naohiko Baba Money Markets

Bank of Japan Review 27-E-2 Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy Teppei Nagano, Eiko Ooka, and Naohiko Baba Money Markets

International Finance multiple-choice questions

International Finance multiple-choice questions 1. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the

International Finance multiple-choice questions 1. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the

Chapter 4. Why Do Interest Rates Change? Chapter Preview

Chapter 4 Why Do Interest Rates Change? Chapter Preview In the early 1950s, short-term Treasury bills were yielding about 1%. By 1981, the yields rose to 15% and higher. But then dropped back to 1% by

Chapter 4 Why Do Interest Rates Change? Chapter Preview In the early 1950s, short-term Treasury bills were yielding about 1%. By 1981, the yields rose to 15% and higher. But then dropped back to 1% by

Stock Market. Copyright 2007 Pearson Addison-Wesley. All rights reserved. 12-1

Stock Market Copyright 2007 Pearson Addison-Wesley. All rights reserved. 12-1 What is a Stock Stock implies ownership of the company, with each share of stock representing a tiny piece of ownership of

Stock Market Copyright 2007 Pearson Addison-Wesley. All rights reserved. 12-1 What is a Stock Stock implies ownership of the company, with each share of stock representing a tiny piece of ownership of

Exam 2 Sample Questions FINAN430 International Finance McBrayer Spring 2018

Sample Multiple Choice Questions 1. Suppose you observe a spot exchange rate of $1.0500/. If interest rates are 5% APR in the U.S. and 3% APR in the euro zone, what is the no-arbitrage 1-year forward rate?

Sample Multiple Choice Questions 1. Suppose you observe a spot exchange rate of $1.0500/. If interest rates are 5% APR in the U.S. and 3% APR in the euro zone, what is the no-arbitrage 1-year forward rate?

Chapter 6. Government Influence on Exchange Rates. Lecture Outline

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

LECTURE XIII. 30 July Monday, July 30, 12

LECTURE XIII 30 July 2012 TOPIC 15 Exchange Rates BIG PICTURE How do we evaluate currency across countries? How is the exchange rate determined? What is the relationship of the foreign exchange market

LECTURE XIII 30 July 2012 TOPIC 15 Exchange Rates BIG PICTURE How do we evaluate currency across countries? How is the exchange rate determined? What is the relationship of the foreign exchange market

Currency Swap or FX Swapd Difinition and Pricing Guide

or FX Swapd Difinition and Pricing Guide Michael Taylor FinPricing An FX swap or currency swap agreement is a contract in which both parties agree to exchange one currency for another currency at a spot

or FX Swapd Difinition and Pricing Guide Michael Taylor FinPricing An FX swap or currency swap agreement is a contract in which both parties agree to exchange one currency for another currency at a spot

3. What is Money? Copyright 2007 Pearson Addison-Wesley. All rights reserved. 3-1

3. What is Money? Copyright 2007 Pearson Addison-Wesley. All rights reserved. 3-1 Meaning of Money Money (money supply) anything that is generally accepted in payment for goods or services or in the repayment

3. What is Money? Copyright 2007 Pearson Addison-Wesley. All rights reserved. 3-1 Meaning of Money Money (money supply) anything that is generally accepted in payment for goods or services or in the repayment

2. (Figure: Change in the Demand for U.S. Dollars) Refer to the information

Refer to the information") Name: Date: Use the following to answer questions 1-3: Figure: Change in the Demand for U.S. Dollars 1. (Figure: Change in the Demand for U.S. Dollars) Refer to the information in the figure. The change

Name: Date: Use the following to answer questions 1-3: Figure: Change in the Demand for U.S. Dollars 1. (Figure: Change in the Demand for U.S. Dollars) Refer to the information in the figure. The change

International Parity Conditions

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

TOPIC 9. International Economics

TOPIC 9 International Economics 2 Goals of Topic 9 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

TOPIC 9 International Economics 2 Goals of Topic 9 What is the exchange rate? NX back!! What is the link between the exchange rate and net exports? What is the trade deficit? How do different shocks affect

14.54 International Trade Lecture 5: Exchange Economies (II) Welfare, Inequality, and Trade Imbalances

Welfare, Inequality, and Trade Imbalances") 14.54 International Trade Lecture 5: Exchange Economies (II) Welfare, Inequality, and Trade Imbalances 14.54 Week 3 Fall 2016 14.54 (Week 3) Welfare and Applications Fall 2016 1 / 30 Today s Plan 1 2 3

14.54 International Trade Lecture 5: Exchange Economies (II) Welfare, Inequality, and Trade Imbalances 14.54 Week 3 Fall 2016 14.54 (Week 3) Welfare and Applications Fall 2016 1 / 30 Today s Plan 1 2 3

THE FOREIGN EXCHANGE MARKET

THE FOREIGN EXCHANGE MARKET 1. The Structure of the Market The foreign exchange market is an example of a speculative auction market that has the same "commodity" traded virtually continuously around the

THE FOREIGN EXCHANGE MARKET 1. The Structure of the Market The foreign exchange market is an example of a speculative auction market that has the same "commodity" traded virtually continuously around the

Less Reliable International Parity Conditions

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

China Warms to a More Flexible Yuan

Page 1 of 5 This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com. http://www.wsj.com/articles/china-warms-to-a-more-flexible-yuan-1418811977

Page 1 of 5 This copy is for your personal, non-commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or customers visit http://www.djreprints.com. http://www.wsj.com/articles/china-warms-to-a-more-flexible-yuan-1418811977