Other Analysis Techniques. Future Worth Analysis (FWA) Benefit-Cost Ratio Analysis (BCRA) Payback Period

|

|

|

- Justin Ross

- 6 years ago

- Views:

Transcription

1 Other Analysis Techniques Future Worth Analysis (FWA) Benefit-Cost Ratio Analysis (BCRA) Payback Period 1

2 Techniques for Cash Flow Analysis Present Worth Analysis Annual Cash Flow Analysis Rate of Return Analysis Incremental Analysis Other Techniques: Future Worth Analysis Benefit-Cost Ration Analysis Payback Period Analysis Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 2

3 Future worth analysis Future worth analysis is equivalent to present worth analysis; the best alternative one way is also best the other way. There are many situations where we want to know what a future situation will be, if we take some particular course of action now. This is called future worth analysis. 3

4 Example 9-1 Ron Jamison, a 20-year-old college student, consumes about a carton of cigarettes a week. He wonders how much money he could accumulate by age 65 if he quit smoking now and put his cigarette money into a savings account. Cigarettes cost $35 per carton. Ron expects: that a savings account would earn 5% interest, compounded semiannually. Compute Ron's future worth at age 65. Semiannual saving $35/carton x 26 weeks = $910 Future worth (FW)= A(F/A,,21/2%, 90) = 910(329.2) = $299,572 4

5 Example 9-2 An east coast firm has decided to establish a second plant in Kansas City. There is a factory for sale for $850,000 that, with extensive remodeling, could be used. As an alternative, the company could buy vacant land for $85,000 and have a new plant constructed there. Either way, it will be 3 years before the company will be able to get a plant into production. The timing and cost of the various components for the factory are given in the following cash flow table. Year Construct New Plant 0 Buy land $ Design and $ initial cost 2 Balance of construction costs 1,200,000 3 Setup of production equipment 200,000 5

6 Remodel Available Factory 0 Purchase factory $850,000 1 Design and remodeling 250,000 2 Additional remodeling 250,000 3 Setup of production equipment 250,000 If interest is 8%, which alternative results in the lower equivalent cost when the firm begins production at the end of the third year? New Plant Future worth of cost (FW)= 85,000(F/ P,8%, 3) + 200,000(F/A, 8%,3) + 1,000,000 (F/P, 8%,1)= $1,836,000 Remodel Available Factory Future worth of cost (FW) = 850,ooo(F/ P, 8%, 3) + 250,000(F/A, 8%, 3) = $

7 Benefit-cost ratio analysis Since we can write PW of cost PW of benefit or EUAC EUAB we can equivalently write (PW of benefit)/pw of cost 1, or EUAB/EUAC 1. Economic analysis based on these ratios is called benefitcost ratio analysis. 7

8 Fixed input Benefit-cost ratio comparison criteria Situation Amount of money or other input resources are fixed Criterion Maximize B/C Fixed output Fixed benefit Maximize B/C Neither input nor output fixed Neither amount of money or other inputs not amount of benefits or other outputs are fixed Compute incremental benefitcost ratio ( B/ C) on the increment of investment between the alternatives. If B/ C 1, choose the highercost alternative; otherwise, choose the lower-cost alternative. 8

9 Example 9-3 Using an interest rate of 7%, choose the best alternative using the benefit-cost ratio analysis Year Device A Device B 0 $1000 $ We have solved this problem using the present worth analysis, the annual cash flow analysis, and the rate of return analysis. Now, we will use the Benefit-Cost Ratio analysis. Since this is a fixed cost case, the criterion is to maximize the B/C ratio. 9

10 Device A PW of cost = $1000 PW of benefits =300(P/A, 7%,5) =300(4.100) =$1230 B/C = PW of benefit/ PW of costs= 1230/ 1000 = 1.23 Device B PW of cost = $1000 PW of benefit = 400(P/ A, 7%, 5) - 50(P/G-, 7%, 5) =400(4.100)- 50(7.647) = = 1258 BPW of benefit 1258 B/C = BPW of benefit /PW of cost = 1258/1000= 1.26 Chose B 10

11 Example 9-4 Using an interest rate of 10%, choose the best machine using the benefit-cost ratio analysis Machine X Machine Y Initial cos $200 $700 Uniform annual benefit End of Useful live salvage value Useful life (years) 6 12 Machine X EUAC = 200(A/ P, 10%,6) - 50(A/ F, 10%,6) = 200(0.2296) - 50(0.1296) = 46-6 = $40 EUAB = $95 11

12 Machine Y EUAC = 700(A/ P, 10%, 12) - 150(A/ F, 10%, 12) = 700(0.1468) - 150(0.0468)= = $96 EUAB =$120 Machine Y - Machine X B / C= (120-95)/(96-40 )= 0.45 Since the incremental benefit-cost ratio is less than 1, it represents an undesirable increment of investment We therefore choose the lower-cost alternative-machine X 12

13 Example 9-5 Each of the five mutually exclusive alternatives presented below will last for 20 years and has no salvage value. MARR = 6%. A B C D E F Cost $4000 $2000 $6000 $1000 $9000 $10000 PWB $7330 $4700 $8730 $1340 $9000 $9500 B/C NPV (to check) The steps are the same as in incremental ROR, except that the criterion is now B/ C, and the cutoff is 1 instead of the MARR: 1) Be sure you identify all alternatives. 2) (Optional) Compute the B/C ratio for each alternative. Discard any with a B/C < 1. (We can discard F). 3) Arrange the remaining alternatives in ascending order of investment. 13

14 Example 9-5 D B A C E F Cost $1000 $2000 $4000 $6000 $9000 $10000 PWB $1340 $4700 $7330 $8730 $9000 $9500 B/C NPV ) Comparing B/ C with 1 for consecutive alternatives select the best alternative. B-D A-B C - A E-A Incremental Cost $1000 $2000 $2000 $5000 Incremental Benefit $3360 $2630 $1400 $1670 B/ C Comparison result B preferred A preferred A preferred A preferred Increment B-D is attractive; therefore B is preferred to D. Increment A-B is attractive; therefore B is preferred to A. Increment C-A is not attractive, as B/ C = 0.76 < 1 ; therefore A is preferred to C. Increment E-A is not attractive, as B/ C = 0.33 < 1 ; therefore A is preferred to E. Finally A is the best project. 14

15 Benefit/Cost Ratio Analysis Graphical representation A, B, C, and D are above the 45-degree line; their B/C ratio is > 1. F is below the line: B/C ratio is < 1. We can discard F if we wish. Examine each separable increment of investment. B/ C < 1 increment is not attractive B/ C 1 increment is desirable. PWB B A C E F PWB/PWC = 1 Compare D to B: Slope or B/ C > 1. B preferred Compare B to A: Slope or B/ C > 1. A preferred Compare A to C: Slope or B/ C < 1; discard C. Compare A to E: Slope or B/ C < 1; discard E. F was discarded earlier since its B/C is less than 1 Therefore A is the best alternative. Note: Despite the fact that Alt. B has the highest B/C ratio, we should not make the mistake of choosing B since the economic criterion here should be based on B/ C (since neither input nor output is fixed) D PWC B-D A-B C - A E-A Incremental Cost $1000 $2000 $2000 $5000 Incremental Benefit $3360 $2630 $1400 $1670 Incr.B/Incr. C

16 Payback Period Payback period is an approximate analysis method. For example, if a $1000 investment today generates $500 of benefits per year, we say its payback period is 1000/500 = 2 years. Four important points about the payback period 1. Payback period is an approximate, rather than an exact, analysis calculation. 2. All costs and all profits, or savings of the investment prior to payback, are included without considering differences in their timing. 3. All the economic consequences beyond the payback period are completely ignored. 4. Payback period may or may not select the same alternative as an exact economic analysis method. Payback period is used because 1. the concept can be readily understood, 2. the calculations can be readily made and understood by people unfamiliar with the use of the time value of money. The rate of return only measures the speed of return of the investment. The other analysis techniques we studied before measure the economic efficiency or the overall profitability of the investment. 16

17 Example 9-6 The cash flows for two alternatives are as follows: Year A B 0 -$1000 -$ You may assume the benefits occur throughout the year rather than just at the end of the year. Based on payback period which alternative should be selected? 17

18 Alternative A Payback period is the period of time required for the profit or other benefits of an investment to equal the cost of the investment. In the first 2 years, only $400 of the $1000 cost is recovered. The remaining $600 cost is recovered in the first half of Year3. Thus the payback period for Alt. A is 2.5 years. Alternative B Since the annual benefits are uniform, the payback period is simply $2783/$1200 per year = 2.3 years To minimize the payback period, choose Alt. B. 18

19 Example 9-7 A firm is trying to decide which of two weighing scales it should install to check a package-filling operation in the plant. If both scales have a 6-year life, which one should be selected? Assume an 8% interest rate. Alternative cost Uniform Annual Benefit End-of-Useful-Life Salvage Atlas $2000 $450 $100 Tom Thumb $ Atlas Scale Payback period = Cost /Uniform annual benefit 2000/450 = 4.4 years Tom Thumb Scale Payback period = Cost /Uniform annual benefit = 3000/600= 5 years 19

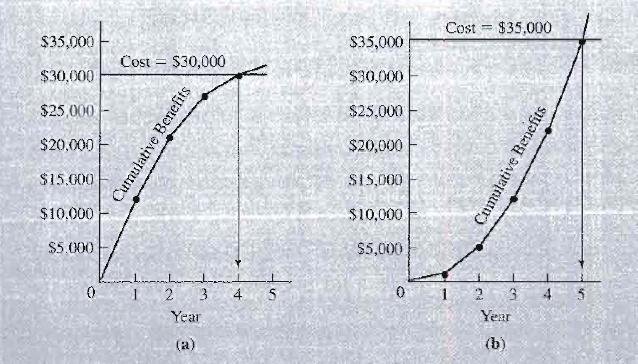

20 Example 9-8 A :firm is purchasing production equipment for a new plant. Two alternative machines are being considered for a particular operation. Tempo Machine Dura Machine Installed cost $30,000 $35000 Net annual benefit after $12,000 the first year, $1000 the first year, all annual expenses declining $3000 increasing $3000 per year thereafter per year thereafter have been deducted Useful life, in years 4 8 Neither machine has any salvage value. Compute the payback period for each of the alternatives 20

21 21

22 Now, as a check on the payback period analysis, compute the rate of return for each alternative. Assume the minimum attractive rate of return is 10%. The cash flows for the two alternatives are as follows: 22

23 Year Tempo Machine Dura Machine sum

24 Tempo Machine Since the sum of the cash flows for the Tempo machine is zero, we see immediately that the $30,000 investment just equals the subsequent benefits. The resulting rate of return is 0%. 24

25 Dura Machine 35,000 = 1000(P/A, i, 8) +3000(P/G, i, 8) Try i = 20%: 35,000 =~ 1000(3.837)+ 3000(9.883) =~ ,649 = 33,486 The 20% interest rate is too high. Try i = 15%: 35,000 =~ 1000(4.487)+ 3000(12.481) =~ ,443 = 41,930 This time, the interest rate is too low. Linear interpolation would show that the rate of return is approximately 19%. Using an exact calculation-rate of return. It is clear that the Tempo is not very attractive economicly 25

26 Yet it was this alternative,and not "the Dura Machine, that was preferred based On the payback period calculations. On the other hand, the shorter payback period for the Tempo does give a measure of the speed of the return of the investment not found in the Dura. The conclusion to be drawn is that liquidity and profitability may be two quite different criteria. 26

27 From the discussion and the examples, we see that payback period can be helpful in providing a measure of the speed of the return of the investment. This might be quite important, for example, for a company that is short of working capital or for a firm in an industry experiencing rapid changes in technology. Calculation of payback period alone, however, must not be confused with a careful economic analysis. We have shown that a short payback period does not always mean that the associated investment is desirable. Thus, payback period should not be considered a suitable replacement for accurate economic analysis calculations. 27

28 SENSITIVITY AND BREAKEVEN ANALYSIS The variation to a particular estimate that would be necessary to change a particular decision."this is called sensitivity analysis. An analysis of the sensitivity of a problem's decision to its various parameters highlights the important and significant aspects of that problem. Breakeven analysis is a form of sensitivity analysis. To illustrate the sensitivity of a decision between alternatives to particular estimates, breakeven analysis is often presented as a breakeven chart. 28

29 Example 9-9 Consider a project that may be constructed to full capacity now or may be constructed in two stages. Construction Costs Two-stage construction Construct first stage now $ Construct second stage $ n years from now Full-capacity construction Construct full capacity now $

30 Other Factors 1. All facilities will last for 40 years regardless of when they are installed; after 40 years, they will have zero salvage value. 2. The annual cost of operation and maintenance is the same for both two-stage construction and full-capacity construction. 3. Assume an 8% interest rate. Plot "age when second stage is constructed" versus "costs for both alternatives." Mark the breakeven point on your graph. What is the sensitivity of the decision to secondstage construction 16 or more years in the future? 30

31 Since we are dealing with a common analysis period, the calculations may be either annual cost or present worth. Present worth calculations appear simpler and are used here. Construct Full Capacity Now PW of cost = $140,000 31

32 Two-Stage Construction First stage constructed now and the second stage to be constructed n years hence...compute the PW of cost for several values of n (years). PW of cost = 100, ,000(P/F, 8%, n) n=5 PW= 100, ,000(0.6806)=$181,700 n = 10 PW = 100, ,000(0.4632)=155,600 n =20 PW= 100, ,000(0.2145)=125,700 n=30 PW= 100, ,000(0.0994)=111,900 These data are plotted in the form of a breakevell chart in Figure

33 The breakeven point on the graph is the point at which both alternatives have equivalent costs. 33

34 Example 9-10 Example 8-3 posed the following situation. Three mutually exclusive alternatives are given, each with a 20-year life and no salvage value. The minimum attractive rate of return is 6%. A B C Initial Cost $2000 $4000 $5000 Uniform Annual Benefit In Example 8-3 we found that Alt. B was the preferred alternative. Here we would like to know how sensitive the decision is to our estimate of the initial cost of B. If B is preferred at an initial cost of $4000, it will continue to be preferred at any smaller initial cost. But how much higher than $4000 can the initial cost be and still have B the preferred alternative? The computations may be done several different ways. With neither input nor output fixed, maximizing net present worth is a suitable criterion. 34

35 Alternative A NPW = PW of benefit - PW of cost Alternative B =41O(P / A, 6%, 20) = 410(11.470) = $2703 Let x = initial cost of B. NPW = 639(P/ A, 6%, 20) - x = 639(11.470)- x = x Alternative C NPW = 700(P/A, 6%,20) = 700(11.470) = $3029 For the three alternatives, we see that B will only maximize NPW as long as its NPW is greater than = x x = = $4300 Therefore, B is the preferred alternative if its initial cost does not exceed $

36 Initial cost above $4300, C is preferred. We have a breakeven point at $4300. When B has an initial cost of $4300, B and C are equally desirable. 36

37 HW Chapter Chapter

38 Lesson from Example 9-8: liquidity and profitability can be very different criteria. We discussed the definitions of liquidity and profitability in class. 38

39 Summary Future Worth. A future worth calculation occurs when the point in time at which the comparison between alternatives will be made is in the future. The best alternative according to future worth should also be best according to present worth. Benefit-Cost Ratio Analysis. We compute a ratio of benefits to costs, using either PW or ACF calculations. Graphically, the method is similar to PW analysis. When neither input nor output is fixed, we use incremental benefit-cost analysis ( B/ C). Payback Period. The payback period is the period of time needed for the profit or other benefits of an investment to equal its cost. This method is simple to use and understand, but is a poor analysis technique for ranking alternatives. It provides a measure of the speed of return of the investment, but is not an accurate measure of its profitability. 39

Chapter 7 Rate of Return Analysis

Chapter 7 Rate of Return Analysis 1 Recall the $5,000 debt example in chapter 3. Each of the four plans were used to repay the amount of $5000. At the end of 5 years, the principal and interest payments

Chapter 7 Rate of Return Analysis 1 Recall the $5,000 debt example in chapter 3. Each of the four plans were used to repay the amount of $5000. At the end of 5 years, the principal and interest payments

An Interesting News Item

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 26: Other Analysis Techniques If you work just for money, you'll never make it, but if you love what you're doing and you always

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 26: Other Analysis Techniques If you work just for money, you'll never make it, but if you love what you're doing and you always

Carefully read all directions given in a problem. Please show all work for all problems, and clearly label all formulas.

Carefully read all directions given in a problem. Please show all work for all problems, and clearly label all formulas. 1. You have been asked to make a decision regarding two alternatives. To make your

Carefully read all directions given in a problem. Please show all work for all problems, and clearly label all formulas. 1. You have been asked to make a decision regarding two alternatives. To make your

Chapter 15 Inflation

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

Comparing Mutually Exclusive Alternatives

Comparing Mutually Exclusive Alternatives Comparing Mutually Exclusive Projects Mutually Exclusive Projects Alternative vs. Project Do-Nothing Alternative 2 Some Definitions Revenue Projects Projects whose

Comparing Mutually Exclusive Alternatives Comparing Mutually Exclusive Projects Mutually Exclusive Projects Alternative vs. Project Do-Nothing Alternative 2 Some Definitions Revenue Projects Projects whose

Multiple Choice: 5 points each

Carefully read each problem before answering. Please write clearly, and show and label all factors used in any problem requiring mathematical calculations. SHOW ALL WORK. Multiple Choice: 5 points each

Carefully read each problem before answering. Please write clearly, and show and label all factors used in any problem requiring mathematical calculations. SHOW ALL WORK. Multiple Choice: 5 points each

Economic Decision Making Using Fuzzy Numbers Shih-Ming Lee, Kuo-Lung Lin, Sushil Gupta. Florida International University Miami, Florida

Economic Decision Making Using Fuzzy Numbers Shih-Ming Lee, Kuo-Lung Lin, Sushil Gupta Florida International University Miami, Florida Abstract In engineering economic studies, single values are traditionally

Economic Decision Making Using Fuzzy Numbers Shih-Ming Lee, Kuo-Lung Lin, Sushil Gupta Florida International University Miami, Florida Abstract In engineering economic studies, single values are traditionally

Department of Humanities. Sub: Engineering Economics and Costing (BHU1302) (4-0-0) Syllabus

(4-0-0) Syllabus") Department of Humanities Sub: Engineering Economics and Costing (BHU1302) (4-0-0) Syllabus Module I (10 Hours) Time value of money : Simple and compound interest, Time value equivalence, Compound interest

Department of Humanities Sub: Engineering Economics and Costing (BHU1302) (4-0-0) Syllabus Module I (10 Hours) Time value of money : Simple and compound interest, Time value equivalence, Compound interest

FE Review Economics and Cash Flow

4/4/16 Compound Interest Variables FE Review Economics and Cash Flow Andrew Pederson P = present single sum of money (single cash flow). F = future single sum of money (single cash flow). A = uniform series

4/4/16 Compound Interest Variables FE Review Economics and Cash Flow Andrew Pederson P = present single sum of money (single cash flow). F = future single sum of money (single cash flow). A = uniform series

CHAPTER 7: ENGINEERING ECONOMICS

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

Leland Blank, P. E. Texas A & M University American University of Sharjah, United Arab Emirates

Eighth Edition ENGINEERING ECONOMY Leland Blank, P. E. Texas A & M University American University of Sharjah, United Arab Emirates Anthony Tarquin, P. E. University of Texas at El Paso Mc Graw Hill Education

Eighth Edition ENGINEERING ECONOMY Leland Blank, P. E. Texas A & M University American University of Sharjah, United Arab Emirates Anthony Tarquin, P. E. University of Texas at El Paso Mc Graw Hill Education

IE463 Chapter 3. Objective: INVESTMENT APPRAISAL (Applications of Money-Time Relationships)

") IE463 Chapter 3 IVESTMET APPRAISAL (Applications of Money-Time Relationships) Objective: To evaluate the economic profitability and liquidity of a single proposed investment project. CHAPTER 4 2 1 Equivalent

IE463 Chapter 3 IVESTMET APPRAISAL (Applications of Money-Time Relationships) Objective: To evaluate the economic profitability and liquidity of a single proposed investment project. CHAPTER 4 2 1 Equivalent

School of Engineering University of Guelph. ENGG*3240 Engineering Economics Course Description & Outline - Fall 2008

School of Engineering University of Guelph ENGG*3240 Engineering Economics Course Description & Outline - Fall 2008 CALENDAR DESCRIPTION Principle of project evaluation, analysis of capital and operating

School of Engineering University of Guelph ENGG*3240 Engineering Economics Course Description & Outline - Fall 2008 CALENDAR DESCRIPTION Principle of project evaluation, analysis of capital and operating

Techniques for Cash Flow Analysis

Techniques for Cash Flow Analysis Present Worth Analysis Chapter 5 Annual Cash Flow Analysis Chapter 6 Rate of Return Analysis Chapter 7 Incremental Analysis Other Techniques: Future Worth Analysis Benefit-Cost

Techniques for Cash Flow Analysis Present Worth Analysis Chapter 5 Annual Cash Flow Analysis Chapter 6 Rate of Return Analysis Chapter 7 Incremental Analysis Other Techniques: Future Worth Analysis Benefit-Cost

SOLUTIONS TO SELECTED PROBLEMS. Student: You should work the problem completely before referring to the solution. CHAPTER 1

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 1 Solutions included for problems 1, 4, 7, 10, 13, 16, 19, 22, 25, 28, 31, 34, 37,

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 1 Solutions included for problems 1, 4, 7, 10, 13, 16, 19, 22, 25, 28, 31, 34, 37,

Chapter 8. Rate of Return Analysis. Principles of Engineering Economic Analysis, 5th edition

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

Chapter 13 Breakeven and Payback Analysis

Chapter 13 Breakeven and Payback Analysis by Ir Mohd Shihabudin Ismail 13-1 LEARNING OUTCOMES 1. Breakeven point one parameter 2. Breakeven point two alternatives 3. Payback period analysis 13-2 Introduction

Chapter 13 Breakeven and Payback Analysis by Ir Mohd Shihabudin Ismail 13-1 LEARNING OUTCOMES 1. Breakeven point one parameter 2. Breakeven point two alternatives 3. Payback period analysis 13-2 Introduction

Comparing Mutually Exclusive Alternatives

Comparing Mutually Exclusive Alternatives Lecture No. 18 Chapter 5 Contemporary Engineering Economics Copyright 2016 Comparing Mutually Exclusive Projects: Basic Terminologies Mutually Exclusive Projects

Comparing Mutually Exclusive Alternatives Lecture No. 18 Chapter 5 Contemporary Engineering Economics Copyright 2016 Comparing Mutually Exclusive Projects: Basic Terminologies Mutually Exclusive Projects

Chapter One. Definition and Basic terms and terminology of engineering economy

Chapter One Definition and Basic terms and terminology of engineering economy 1. Introduction: The need for engineering economy is primarily motivated by the work that engineers do in performing analysis,

Chapter One Definition and Basic terms and terminology of engineering economy 1. Introduction: The need for engineering economy is primarily motivated by the work that engineers do in performing analysis,

Transportation Economics and Decision Making. L e c t u r e - 3

Transportation Economics and Decision Making L e c t u r e - 3 Arithmetic Gradient Series Amount increases by G each period A+2G A+(n-1)G A+3G A A+G This is equivalent to Arithmetic Gradient Series A A

Transportation Economics and Decision Making L e c t u r e - 3 Arithmetic Gradient Series Amount increases by G each period A+2G A+(n-1)G A+3G A A+G This is equivalent to Arithmetic Gradient Series A A

IE463 Chapter 4. Objective: COMPARING INVESTMENT AND COST ALTERNATIVES

IE463 Chapter 4 COMPARING INVESTMENT AND COST ALTERNATIVES Objective: To learn how to properly apply the profitability measures described in Chapter 3 to select the best alternative out of a set of mutually

IE463 Chapter 4 COMPARING INVESTMENT AND COST ALTERNATIVES Objective: To learn how to properly apply the profitability measures described in Chapter 3 to select the best alternative out of a set of mutually

Inflation Homework. 1. Life = 4 years

Inflation Homework 1. Life = 4 years 700 9001100 500 0 1 2 3 4-1500 You are to analyze the cash flow on the left with several assumptions regarding inflation. In all cases the general inflation rate is

Inflation Homework 1. Life = 4 years 700 9001100 500 0 1 2 3 4-1500 You are to analyze the cash flow on the left with several assumptions regarding inflation. In all cases the general inflation rate is

Selection from Independent Projects Under Budget Limitation

Basics In previous weeks, the alternatives have been mutually exclusive; only one could be selected. If the projects are not mutually exclusive; they are called independent projects. We learned the criteria

Basics In previous weeks, the alternatives have been mutually exclusive; only one could be selected. If the projects are not mutually exclusive; they are called independent projects. We learned the criteria

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1 LEARNING OBJECTIVES Work with mutually exclusive alternatives based upon ROR analysis 1. Why Incremental Analysis? 2. Incremental Cash Flows

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1 LEARNING OBJECTIVES Work with mutually exclusive alternatives based upon ROR analysis 1. Why Incremental Analysis? 2. Incremental Cash Flows

Lecture 5 Present-Worth Analysis

Seg2510 Management Principles for Engineering Managers Lecture 5 Present-Worth Analysis Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review

Seg2510 Management Principles for Engineering Managers Lecture 5 Present-Worth Analysis Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review

# 6. Comparing Alternatives

IE 5441 1 # 6. Comparing Alternatives One of the main purposes of this course is to discuss how to make decisions in engineering economy. Let us first consider a single period case. Suppose that there

IE 5441 1 # 6. Comparing Alternatives One of the main purposes of this course is to discuss how to make decisions in engineering economy. Let us first consider a single period case. Suppose that there

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR. ENG2000: R.I. Hornsey CM_2: 1

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR ENG2000: R.I. Hornsey CM_2: 1 Introduction This chapter introduces a second method for comparing between projects While the result of the process

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR ENG2000: R.I. Hornsey CM_2: 1 Introduction This chapter introduces a second method for comparing between projects While the result of the process

The future and present cash flow series are shown for a project. How long is the simple payback period?

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 27: Effects of Inflation on Present Worth; Introduction to Sensitivity Analysis Analysis A weak currency is the sign of a weak economy,

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 27: Effects of Inflation on Present Worth; Introduction to Sensitivity Analysis Analysis A weak currency is the sign of a weak economy,

INVESTMENT APPRAISAL TECHNIQUES FOR SMALL AND MEDIUM SCALE ENTERPRISES

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

Discounted Cash Flow Analysis

Discounted Cash Flow Analysis Lecture No.16 Chapter 5 Contemporary Engineering Economics Copyright 2016 Net Present Worth Measure Principle: Compute the equivalent net surplus at n = 0 for a given interest

Discounted Cash Flow Analysis Lecture No.16 Chapter 5 Contemporary Engineering Economics Copyright 2016 Net Present Worth Measure Principle: Compute the equivalent net surplus at n = 0 for a given interest

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I ECONOMIC ANALYSIS AND LIFE CYCLE COSTING Engineering Economy and Economics 1. Several questions on basic economics. 2. Several problems on simple engineering

ECONOMIC ANALYSIS AND LIFE CYCLE COSTING SECTION I ECONOMIC ANALYSIS AND LIFE CYCLE COSTING Engineering Economy and Economics 1. Several questions on basic economics. 2. Several problems on simple engineering

ch11 Student: 3. An analysis of what happens to the estimate of net present value when only one variable is changed is called analysis.

ch11 Student: Multiple Choice Questions 1. Forecasting risk is defined as the: A. possibility that some proposed projects will be rejected. B. process of estimating future cash flows relative to a project.

ch11 Student: Multiple Choice Questions 1. Forecasting risk is defined as the: A. possibility that some proposed projects will be rejected. B. process of estimating future cash flows relative to a project.

IE 343 Section 1 Engineering Economy Exam 2 Review Problems Solutions Instructor: Tian Ni March 30, 2012

IE 343 Section 1 Engineering Economy Exam 2 Review Problems Solutions Instructor: Tian Ni March 30, 2012 1. A firm is considering investing in a machine that has an initial cost of $36,000. For a period

IE 343 Section 1 Engineering Economy Exam 2 Review Problems Solutions Instructor: Tian Ni March 30, 2012 1. A firm is considering investing in a machine that has an initial cost of $36,000. For a period

INTERNAL RATE OF RETURN

INTERNAL RATE OF RETURN Introduction You put money in a bank account and expect to get a return 1 percent You can think of investment/business/project in the same way Every investment/business/project

INTERNAL RATE OF RETURN Introduction You put money in a bank account and expect to get a return 1 percent You can think of investment/business/project in the same way Every investment/business/project

i* = IRR i*? IRR more sign changes Passes: unique i* = IRR

Decision Rules Single Alternative Based on Sign Changes of Cash Flow: Simple Investment i* = IRR Accept if i* > MARR Single Project start with zero, one sign change Non-Simple Investment i*? IRR Net Investment

Decision Rules Single Alternative Based on Sign Changes of Cash Flow: Simple Investment i* = IRR Accept if i* > MARR Single Project start with zero, one sign change Non-Simple Investment i*? IRR Net Investment

Tax Homework. A B C Installed cost $10,000 $15,000 $20,000 Net Uniform annual before 3,000 6,000 10,000

Tax Homework 1. A firm is considering three mutually exclusive alternatives as part of a production improvement program. Management requires that you must select one. The alternatives are: A B C Installed

Tax Homework 1. A firm is considering three mutually exclusive alternatives as part of a production improvement program. Management requires that you must select one. The alternatives are: A B C Installed

SOLUTIONS TO SELECTED PROBLEMS. Student: You should work the problem completely before referring to the solution. CHAPTER 17

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 17 Solutions included for all or part of problems: 4, 6, 9, 12, 15, 18, 21, 24,

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 17 Solutions included for all or part of problems: 4, 6, 9, 12, 15, 18, 21, 24,

Outline of Review Topics

Outline of Review Topics Cash flow and equivalence Depreciation Special topics Comparison of alternatives Ethics Method of review Brief review of topic Problems 1 Cash Flow and Equivalence Cash flow Diagrams

Outline of Review Topics Cash flow and equivalence Depreciation Special topics Comparison of alternatives Ethics Method of review Brief review of topic Problems 1 Cash Flow and Equivalence Cash flow Diagrams

Present Worth Analysis

Present Worth Analysis Net Present Worth of initial and future cash flows can be used to select among alternative projects It is important to understand what Net Present Worth means, especially when the

Present Worth Analysis Net Present Worth of initial and future cash flows can be used to select among alternative projects It is important to understand what Net Present Worth means, especially when the

Overall ROR: 30,000(0.20) + 70,000(0.14) = 100,000(x) x = 15.8% Prepare a tabulation of cash flow for the alternatives shown below.

+ 70,000(0.14) = 100,000(x) x = 15.8% Prepare a tabulation of cash flow for the alternatives shown below.") Chapter 8, Problem 2. What is the overall rate of return on a $100,000 investment that returns 20% on the first $30,000 and 14% on the remaining $70,000? Chapter 8, Solution 2. Overall ROR: 30,000(0.20)

Chapter 8, Problem 2. What is the overall rate of return on a $100,000 investment that returns 20% on the first $30,000 and 14% on the remaining $70,000? Chapter 8, Solution 2. Overall ROR: 30,000(0.20)

Chapter 7 Rate of Return Analysis

Chapter 7 Rate of Return Analysis Rate of Return Methods for Finding ROR Internal Rate of Return (IRR) Criterion Incremental Analysis Mutually Exclusive Alternatives Why ROR measure is so popular? This

Chapter 7 Rate of Return Analysis Rate of Return Methods for Finding ROR Internal Rate of Return (IRR) Criterion Incremental Analysis Mutually Exclusive Alternatives Why ROR measure is so popular? This

Engineering Economics

Engineering Economics Lecture 7 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1 Chapter

Engineering Economics Lecture 7 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1 Chapter

Mutually Exclusive Choose at most one From the Set

1 Mutually Exclusive Choose at most one From the Set This lecture addresses an issue that is confusing to many users of the rate of return method. When choosing among mutually exclusive alternatives, never

1 Mutually Exclusive Choose at most one From the Set This lecture addresses an issue that is confusing to many users of the rate of return method. When choosing among mutually exclusive alternatives, never

Homework 4. Public Projects. (a) Using the benefit cost ratio, which system should be selected?

Using the benefit cost ratio, which system should be selected?") Homework 4. Public Projects 1. A city government is considering two types of town-dump sanitary systems, Design A requires an initial outlay of $400,000, with annual operating and maintenance costs of

Homework 4. Public Projects 1. A city government is considering two types of town-dump sanitary systems, Design A requires an initial outlay of $400,000, with annual operating and maintenance costs of

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

FACTFILE: GCSE BUSINESS STUDIES. UNIT 2: Break-even. Break-even (BE) Learning Outcomes

Learning Outcomes") FACTFILE: GCSE BUSINESS STUDIES UNIT 2: Break-even Break-even (BE) Learning Outcomes Students should be able to: calculate break-even both graphically and by formula; explain the significance of the break-even

FACTFILE: GCSE BUSINESS STUDIES UNIT 2: Break-even Break-even (BE) Learning Outcomes Students should be able to: calculate break-even both graphically and by formula; explain the significance of the break-even

ME 353 ENGINEERING ECONOMICS

ME 353 ENGINEERING ECONOMICS Final Exam Sample Scoring gives priority to the correct formulas. Numerical answers without the correct formulas for justification receive no credit. Decisions without numerical

ME 353 ENGINEERING ECONOMICS Final Exam Sample Scoring gives priority to the correct formulas. Numerical answers without the correct formulas for justification receive no credit. Decisions without numerical

What Is a Project? How Do We Justify a Project? 1.011Project Evaluation: Comparing Costs & Benefits Carl D. Martland

MIT Civil Engineering 1.11 -- Project Evaluation Spring Term 23 1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs

MIT Civil Engineering 1.11 -- Project Evaluation Spring Term 23 1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs

Six Ways to Perform Economic Evaluations of Projects

Six Ways to Perform Economic Evaluations of Projects Course No: B03-003 Credit: 3 PDH A. Bhatia Continuing Education and Development, Inc. 9 Greyridge Farm Court Stony Point, NY 10980 P: (877) 322-5800

Six Ways to Perform Economic Evaluations of Projects Course No: B03-003 Credit: 3 PDH A. Bhatia Continuing Education and Development, Inc. 9 Greyridge Farm Court Stony Point, NY 10980 P: (877) 322-5800

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules -1 Chapter 7: Investment Decision Rules Note: Read the chapter then look at the following. Fundamental question: What criteria should firms use when deciding which

Chapter 7: Investment Decision Rules -1 Chapter 7: Investment Decision Rules Note: Read the chapter then look at the following. Fundamental question: What criteria should firms use when deciding which

Engineering Economy Chapter 4 More Interest Formulas

Engineering Economy Chapter 4 More Interest Formulas 1. Uniform Series Factors Used to Move Money Find F, Given A (i.e., F/A) Find A, Given F (i.e., A/F) Find P, Given A (i.e., P/A) Find A, Given P (i.e.,

Engineering Economy Chapter 4 More Interest Formulas 1. Uniform Series Factors Used to Move Money Find F, Given A (i.e., F/A) Find A, Given F (i.e., A/F) Find P, Given A (i.e., P/A) Find A, Given P (i.e.,

ENGINEERING ECONOMIC ANALYSIS

ENGINEERING ECONOMIC ANALYSIS r T ~' ELEVENTH EDITION Donald G. Newnan San Jose State University Ted G. Eschenbach University of Alaska Anchorage Jerome P. Lavelle North Carolina State t University New

ENGINEERING ECONOMIC ANALYSIS r T ~' ELEVENTH EDITION Donald G. Newnan San Jose State University Ted G. Eschenbach University of Alaska Anchorage Jerome P. Lavelle North Carolina State t University New

Engineering Economy. Lecture 8 Evaluating a Single Project IRR continued Payback Period. NE 364 Engineering Economy

Engineering Economy Lecture 8 Evaluating a Single Project IRR continued Payback Period Internal Rate of Return (IRR) The internal rate of return (IRR) method is the most widely used rate of return method

Engineering Economy Lecture 8 Evaluating a Single Project IRR continued Payback Period Internal Rate of Return (IRR) The internal rate of return (IRR) method is the most widely used rate of return method

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh Quiz 1, 2, 7, 15,19, 20, 22, 26, 36, 40. The objective of chapter 6 is to evaluate correctly capital investment alternatives when

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh Quiz 1, 2, 7, 15,19, 20, 22, 26, 36, 40. The objective of chapter 6 is to evaluate correctly capital investment alternatives when

2. Basic Concepts In Project Appraisal [DoF Ch. 4; FP Ch. 3, 4, 5]

![2. Basic Concepts In Project Appraisal [DoF Ch. 4; FP Ch. 3, 4, 5]](/thumbs/82/85732785.jpg "2. Basic Concepts In Project Appraisal [DoF Ch. 4; FP Ch. 3, 4, 5]") R.E.Marks 2003 Lecture 3-1 2. Basic Concepts In Project Appraisal [DoF Ch. 4; FP Ch. 3, 4, 5] 1. Which Investment Criterion? 2. Investment Decision Criteria 3. Net Present Value Annual User Charge / Value

R.E.Marks 2003 Lecture 3-1 2. Basic Concepts In Project Appraisal [DoF Ch. 4; FP Ch. 3, 4, 5] 1. Which Investment Criterion? 2. Investment Decision Criteria 3. Net Present Value Annual User Charge / Value

CAPITAL BUDGETING AND THE INVESTMENT DECISION

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

29/09/2010. Outline Module 4. Selection of Alternatives. Proposals for Investment Alternatives. Module 4: Present Worth Analysis

Outline Module 4 Proposals for nvestment Alternatives Selection of Alternatives Future Worth Analysis Capitalized-cost calculation Module 4: Present Worth Analysis S-4251 konomi Teknik 4-2 S-4251 konomi

Outline Module 4 Proposals for nvestment Alternatives Selection of Alternatives Future Worth Analysis Capitalized-cost calculation Module 4: Present Worth Analysis S-4251 konomi Teknik 4-2 S-4251 konomi

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam Scoring gives priority to the correct formulation. Numerical answers without the correct formulas for justification receive no credit. Decisions

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam Scoring gives priority to the correct formulation. Numerical answers without the correct formulas for justification receive no credit. Decisions

FNCE 370v8: Assignment 3

FNCE 370v8: Assignment 3 Assignment 3 is worth 5% of your final mark. Complete and submit Assignment 3 after you complete Lesson 9. There are 12 questions in this assignment. The break-down of marks for

FNCE 370v8: Assignment 3 Assignment 3 is worth 5% of your final mark. Complete and submit Assignment 3 after you complete Lesson 9. There are 12 questions in this assignment. The break-down of marks for

COMPARING ALTERNATIVES

CHAPTER 6 COMPARING FEASIBLE DESIGN Alternatives may be mutually exclusive (i.e., choice if one excludes the choice of any other alternative) because : The alternatives being considered may require different

CHAPTER 6 COMPARING FEASIBLE DESIGN Alternatives may be mutually exclusive (i.e., choice if one excludes the choice of any other alternative) because : The alternatives being considered may require different

Sixth Edition. Global Edition CONTEMPORARY ENGINEERING ECONOMICS. Chan S. Park Department of Industrial and Systems Engineering Auburn University

Sixth Edition Global Edition CONTEMPORARY ENGINEERING ECONOMICS Chan S. Park Department of Industrial and Systems Engineering Auburn University PEARSON Boston Columbus Indianapolis New York San Francisco

Sixth Edition Global Edition CONTEMPORARY ENGINEERING ECONOMICS Chan S. Park Department of Industrial and Systems Engineering Auburn University PEARSON Boston Columbus Indianapolis New York San Francisco

International Project Management. prof.dr MILOŠ D. MILOVANČEVIĆ

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

1. depreciation is the newest and most widely used depreciation method. It was introduced by the Tax Reform Act of 1986.

Carefully read each problem before answering. Please write clearly, and show and label all factors/numbers used in any problem requiring mathematical calculations. Show all work. Multiple Choice: 4 points

Carefully read each problem before answering. Please write clearly, and show and label all factors/numbers used in any problem requiring mathematical calculations. Show all work. Multiple Choice: 4 points

1.011Project Evaluation: Comparing Costs & Benefits

1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs of the project? Present, Future, and Annual Worth Internal

1.11Project Evaluation: Comparing Costs & Benefits Carl D. Martland Basic Question: Are the future benefits large enough to justify the costs of the project? Present, Future, and Annual Worth Internal

IE 343 Midterm Exam. March 7 th Closed book, closed notes.

IE 343 Midterm Exam March 7 th 2013 Closed book, closed notes. Write your name in the spaces provided above. Write your name on each page as well, so that in the event the pages are separated, we can still

IE 343 Midterm Exam March 7 th 2013 Closed book, closed notes. Write your name in the spaces provided above. Write your name on each page as well, so that in the event the pages are separated, we can still

LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS. Overview of Interest Formulas and Their Applications. Symbols Used in Engineering Economy

Lesson Two: Interest Formulas and Their Applications from Understanding Engineering Economy: A Practical Approach LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS Overview of Interest Formulas and Their

Lesson Two: Interest Formulas and Their Applications from Understanding Engineering Economy: A Practical Approach LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS Overview of Interest Formulas and Their

IE 343 Midterm Exam 2

IE 343 Midterm Exam 2 Nov 16, 2011 Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Exam 2 has three

IE 343 Midterm Exam 2 Nov 16, 2011 Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Exam 2 has three

Economic Evaluation. Objectives of Economic Evaluation Analysis

Economic Evaluation Objective of Analysis Criteria Nature Peculiarities Comparison of Criteria Recommended Approach Massachusetts Institute of Technology Economic Evaluation Slide 1 of 17 Objectives of

Economic Evaluation Objective of Analysis Criteria Nature Peculiarities Comparison of Criteria Recommended Approach Massachusetts Institute of Technology Economic Evaluation Slide 1 of 17 Objectives of

KING FAHAD UNIVERSITY OF PETROLEUM & MINERALS COLLEGE OF ENVIROMENTAL DESGIN CONSTRUCTION ENGINEERING & MANAGEMENT DEPARTMENT

KING FAHAD UNIVERSITY OF PETROLEUM & MINERALS COLLEGE OF ENVIROMENTAL DESGIN CONSTRUCTION ENGINEERING & MANAGEMENT DEPARTMENT Report on: Associated Problems with Life Cycle Costing As partial fulfillment

KING FAHAD UNIVERSITY OF PETROLEUM & MINERALS COLLEGE OF ENVIROMENTAL DESGIN CONSTRUCTION ENGINEERING & MANAGEMENT DEPARTMENT Report on: Associated Problems with Life Cycle Costing As partial fulfillment

Profitability Estimates

CH2404 Process Economics Unit III Profitability Estimates Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110,

CH2404 Process Economics Unit III Profitability Estimates Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110,

Cash Flow and the Time Value of Money

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Sensitivity Analysis

CH2404 Process Economics Unit III Sensitivity Analysis Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

CH2404 Process Economics Unit III Sensitivity Analysis Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

Engineering Economics

Engineering Economics Lecture 6 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1 Chapter

Engineering Economics Lecture 6 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1 Chapter

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

7 - Engineering Economic Analysis

Construction Project Management (CE 110401346) 7 - Engineering Economic Analysis Dr. Khaled Hyari Department of Civil Engineering Hashemite University Introduction Is any individual project worthwhile?

Construction Project Management (CE 110401346) 7 - Engineering Economic Analysis Dr. Khaled Hyari Department of Civil Engineering Hashemite University Introduction Is any individual project worthwhile?

which considers any inflationary effects in the cash flows.

Note 1: Unless otherwise stated, all cash flows given in the problems represent aftertax cash flows in actual dollars. The MARR also represents a market interest rate, which considers any inflationary

Note 1: Unless otherwise stated, all cash flows given in the problems represent aftertax cash flows in actual dollars. The MARR also represents a market interest rate, which considers any inflationary

Capital Budgeting Decisions

Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012

Capital Budgeting Decisions Chapter 13 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright 2012

Year 10 General Maths Unit 2

Year 10 General Mathematics Unit 2 - Financial Arithmetic II Topic 2 Linear Growth and Decay In this area of study students cover mental, by- hand and technology assisted computation with rational numbers,

Year 10 General Mathematics Unit 2 - Financial Arithmetic II Topic 2 Linear Growth and Decay In this area of study students cover mental, by- hand and technology assisted computation with rational numbers,

The formula for the net present value is: 1. NPV. 2. NPV = CF 0 + CF 1 (1+ r) n + CF 2 (1+ r) n

n + CF 2 (1+ r) n") Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

Chapter 5 Present Worth Analysis

Chapter 5 Present Worth Analysis 1. Net Present Worth (NPW) Analysis NPW is a comparison of alternatives by determining at year 0 (i.e., the present time). At least one of the following three situations

Chapter 5 Present Worth Analysis 1. Net Present Worth (NPW) Analysis NPW is a comparison of alternatives by determining at year 0 (i.e., the present time). At least one of the following three situations

Lecture - 25 Depreciation Accounting

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology Kharagpur Lecture - 25 Depreciation Accounting Good

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology Kharagpur Lecture - 25 Depreciation Accounting Good

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009 MG Lipsett 2008 last updated December 8, 2008 Introduction This document provides concise explanations

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009 MG Lipsett 2008 last updated December 8, 2008 Introduction This document provides concise explanations

$82, $71, $768, $668,609.67

Question # 1 of 15 ( Start time: 07:14:23 PM ) Total Marks: 1 If you deposit $12,000 per year for 16 years (each deposit is made at the beginning of each year) in an account that pays an annual interest

Question # 1 of 15 ( Start time: 07:14:23 PM ) Total Marks: 1 If you deposit $12,000 per year for 16 years (each deposit is made at the beginning of each year) in an account that pays an annual interest

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 13 Multiple Cash Flow-1 and 2 Welcome to the lecture

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 13 Multiple Cash Flow-1 and 2 Welcome to the lecture

There are significant differences in the characteristics of private and public sector alternatives.

Public Sector Projects Projects in private sector are owned by corporations, partnerships, and individuals and used by customers. Projects in public sector are owned, used and financed by citizens. Public

Public Sector Projects Projects in private sector are owned by corporations, partnerships, and individuals and used by customers. Projects in public sector are owned, used and financed by citizens. Public

Appendix A. Engineering Economics ENGINEERING ECONOMICS. Compound Interest

Appendix A Engineering Economics Greater knowledge of engineering economics and cost analysis is expected of industrial engineers than of other engineers. On the 110-question FE Exam, expect 10 15 questions

Appendix A Engineering Economics Greater knowledge of engineering economics and cost analysis is expected of industrial engineers than of other engineers. On the 110-question FE Exam, expect 10 15 questions

UNIT 16 BREAK EVEN ANALYSIS

UNIT 16 BREAK EVEN ANALYSIS Structure 16.0 Objectives 16.1 Introduction 16.2 Break Even Analysis 16.3 Break Even Point 16.4 Impact of Changes in Sales Price, Volume, Variable Costs and on Profits 16.5

UNIT 16 BREAK EVEN ANALYSIS Structure 16.0 Objectives 16.1 Introduction 16.2 Break Even Analysis 16.3 Break Even Point 16.4 Impact of Changes in Sales Price, Volume, Variable Costs and on Profits 16.5

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Topic 1 (Week 1): Capital Budgeting

: Capital Budgeting") 4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

4.2. The Three Rules of Time Travel Rule 1: Comparing and combining values Topic 1 (Week 1): Capital Budgeting It is only possible to compare or combine values at the same point in time. A dollar today

Capital investment decisions: 1

Capital investment decisions: 1 Solutions to Chapter 13 questions Question 13.24 (i) Net present values: Year 0% 10% 20% NPV Discount NPV Discount NPV ( ) Factor ( ) Factor ( ) 0 (142 700) 1 000 (142 700)

Capital investment decisions: 1 Solutions to Chapter 13 questions Question 13.24 (i) Net present values: Year 0% 10% 20% NPV Discount NPV Discount NPV ( ) Factor ( ) Factor ( ) 0 (142 700) 1 000 (142 700)

Cost Benefit Analysis (CBA) Economic Analysis (EA)

Economic Analysis (EA)") Cost Benefit Analysis (CBA) Economic Analysis (EA) This is an overview of the preliminary work that should be completed before launching into a full CBA to determine the net economic worth of a proposal

Cost Benefit Analysis (CBA) Economic Analysis (EA) This is an overview of the preliminary work that should be completed before launching into a full CBA to determine the net economic worth of a proposal

INVESTMENT CRITERIA. Net Present Value (NPV)

") 227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

227 INVESTMENT CRITERIA Net Present Value (NPV) 228 What: NPV is a measure of how much value is created or added today by undertaking an investment (the difference between the investment s market value

The Mathematics of Interest An Example Assume a bank pays 8% interest on a $100 deposit made today. How much

The Mathematics of Interest An Example CAPITAL BUDGETING Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? F n = P(1 + r) n 1 3 Typical Capital Budgeting

The Mathematics of Interest An Example CAPITAL BUDGETING Assume a bank pays 8% interest on a $100 deposit made today. How much will the $100 be worth in one year? F n = P(1 + r) n 1 3 Typical Capital Budgeting

CE 561 Lecture Notes. Engineering Economic Analysis. Set 2. Time value of money. Cash Flow Diagram. Interest. Inflation Opportunity cost

CE 56 Lecture otes Set 2 Engineering Economic Analysis Time value of money Inflation Opportunity cost Cash Flow Diagram P A A PInvestment AYearly Return 0 o. of Years Interest Profit Motive MARR Public

CE 56 Lecture otes Set 2 Engineering Economic Analysis Time value of money Inflation Opportunity cost Cash Flow Diagram P A A PInvestment AYearly Return 0 o. of Years Interest Profit Motive MARR Public

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

GROUP VERSUS STAGGERED REPLACEMENT POLICY- STRATEGIC REPLACEMENT DECISIONS

GROUP VERSUS STAGGERED REPLACEMENT POLICY- STRATEGIC REPLACEMENT DECISIONS Except where reference is made to the work of others, the work described in this thesis is my own or was done in collaboration

GROUP VERSUS STAGGERED REPLACEMENT POLICY- STRATEGIC REPLACEMENT DECISIONS Except where reference is made to the work of others, the work described in this thesis is my own or was done in collaboration

Dr. Maddah ENMG 400 Engineering Economy 07/06/09. Chapter 5 Present Worth (Value) Analysis

Analysis") Dr. Maddah ENMG 400 Engineering Economy 07/06/09 Chapter 5 Present Worth (Value) Analysis Introduction Given a set of feasible alternatives, engineering economy attempts to identify the best (most viable)

Dr. Maddah ENMG 400 Engineering Economy 07/06/09 Chapter 5 Present Worth (Value) Analysis Introduction Given a set of feasible alternatives, engineering economy attempts to identify the best (most viable)

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Chapter 7. Net Present Value and Other Investment Rules

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be