Ø Sales Tax alone accounts for 34% of state revenue. Average of the 50 State Revenue Sources. Ø Online commerce continues to grow.

|

|

|

- Winifred Dickerson

- 5 years ago

- Views:

Transcription

1

2 Ø Sales Tax alone accounts for 34% of state revenue. Average of the 50 State Revenue Sources Ø Online commerce continues to grow. Ø This past Black Friday, for the second consecutive year, more people shopped online than did in stores. Ø For the last five years, e-commerce grew annually by 15% and now accounts for 10% of all retail sales.

3 113 th Congress Ø Marketplace Fairness Act (S. 743) (Passed Senate on May 6, 2013) 114 th Congress Ø Marketplace Fairness Act (S. 698) (24 sponsors but never received a hearing) Ø Remote Transactions Parity Act (H.R. 2775) (69 sponsors but never received a hearing) 115 th Congress Ø Marketplace Fairness Act (S. 976) (24 sponsors) Ø Remote Transactions Parity Act (H.R. 2193) (11 sponsors) Ø No Regulation Without Representation Act Ø Online Sales Simplification Act (Never Introduced)

4 ØDestination Sourcing ØA single state-level entity to administer all sales and use tax laws ØA single audit for all state and local taxing jurisdictions within the state ØA single sales and use tax return for remote sellers to file with the state-level entity ØA uniform sales and use tax base among the state and its local taxing jurisdictions ØInformation regarding the taxability of products and services, along with any product and service exemptions ØA rates and boundary database ØA 90-day notice of rate changes, along with liability relief to both remote sellers and Certified Service Providers (CSPs)

5 Only one thing you need to know about this proposal Just say No Hybrid Origin Sales Tax

6

7 In 1999, the NCSL Executive Committee established the Task Force on State and Local Taxation to review the issue of collection of sales and use taxes from out-of-state transactions and then recommend legislative solutions to Congress. That was 18 years ago.

8

9

10

11 Typically require non-collecting businesses who have a defined amount of in state sales to: Ø Inform customers that they may be subject to use tax; Ø Send an annual purchase summary to customers who purchase a defined amount of taxable goods in one year, along with a reminder of their use tax obligation; and/or Ø Provide the Department of Revenue with annual customer information (names, addresses, and amount of purchases).

12 Ø Colorado (2010) Ø Louisiana (2016) For sellers with +$50,000 in sales. Effective July 1, 2017 Ø Oklahoma (2016) Report only to Customers Ø Vermont (2016) Colorado-style. Effective July 1, 2017

13 On February 22, 2016, the United States Court of Appeals for the Tenth Circuit upheld the constitutionality of the Colorado law. The court held that the notification and reporting requirements do not violate the Commerce Clause because they do not discriminate against or unduly burden interstate commerce. On December 12, 2016, the United States Supreme Court denied DMA s petition to hear the case, thus allowing the Colorado to begin enforcing its law. On February 22, 2017 the state s Department of Revenue and DMA reached a settlement agreement where the DOR agreed to waive penalties for noncompliant retailers until July.

14 legislation introduced in 2017 taxpayer and the Department taxpayer only notification only WA OR ID MT WY ND SD MN WI MI NY VT NH MA CT ME RI CA NV UT CO NE KS IA MO IL IN KY OH WV PA VA NJ DE MD DC AZ NM OK AR TN NC SC AK MS AL GA TX LA HI FL 14

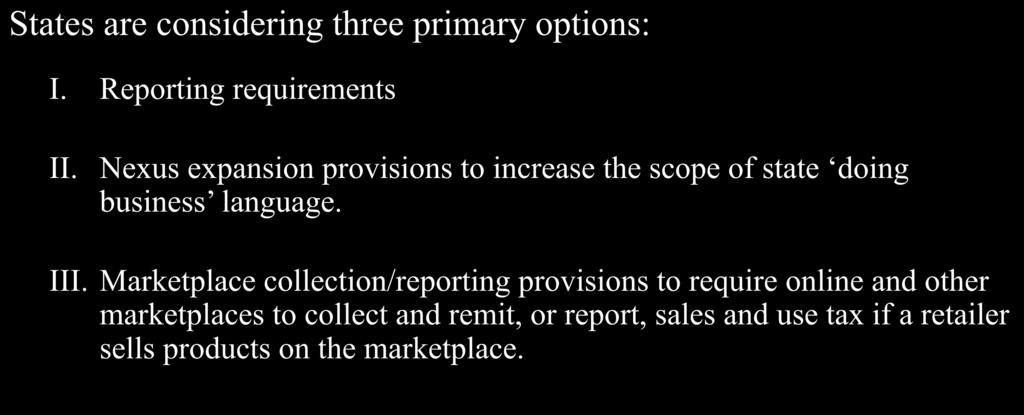

15 ØAmend definitions, such as vendor or doing business in the state ØEconomic Nexus ØExpands to include storage of inventory

16 Click-Through Nexus in 2017 Sales Tax legislation introduced in 2017 enacted by legislation enacted by regulation WA OR ID MT WY ND SD MN WI MI NY ME VT NH MA CT RI CA NV UT CO NE KS IA MO IL IN OH KY WV PA VA NJ DE MD DC AZ NM OK AR TN NC SC AK MS AL GA TX LA HI FL 16

17 Sales Factor/Transactional Nexus Sales/Use Taxes legislation introduced in 2017 enacted by legislation enacted by regulation WA 2016 CA OR NV ID UT MT WY CO ND SD NE KS MN IA MO WI IL MI OH IN KY WV PA VA NY ME VT NH MA CT RI NJ DE MD DC 1989 law, notice 92(19) repealed Dec AZ NM OK AR TN NC SC AK MS AL GA Delayed TX LA HI 2016 FL 17

18

19 legislation introduced in 2017 enacted by legislation/regulation WA OR ID MT WY ND SD MN WI MI NY ME VT NH MA CT RI Delayed? CA NV UT CO NE KS IA MO IL IN OH KY WV PA VA NJ DE MD DC AZ NM OK AR TN NC SC AK MS AL GA TX LA HI Bill vetoed FL 19

20 22 states introduced legislation to collect sales taxes from remote purchases. Notable Enacted Legislation Louisiana (Expanded Nexus & Reporting) Oklahoma (Reporting) South Dakota (Economic Nexus) Vermont (Colorado-style Reporting) Administrative Rules Alabama ($250,000 Economic Nexus) Tennessee ($500,000 Economic Nexus)

21 Legislation has been introduced in at least 30 states to address the remote sales tax collection problem Notable legislation enacted so far this year in: Alabama (Reporting requirement) Indiana (South Dakota Model of Economic Nexus) Minnesota (Marketplace Provider, Effective July 1, 2019) North Dakota (Contingent upon federal collection authority) Virginia (Adds "storage of inventory" to definition of nexus) Wyoming (South Dakota Model of Economic Nexus) Notable Regulations: Massachusetts Mississippi

22

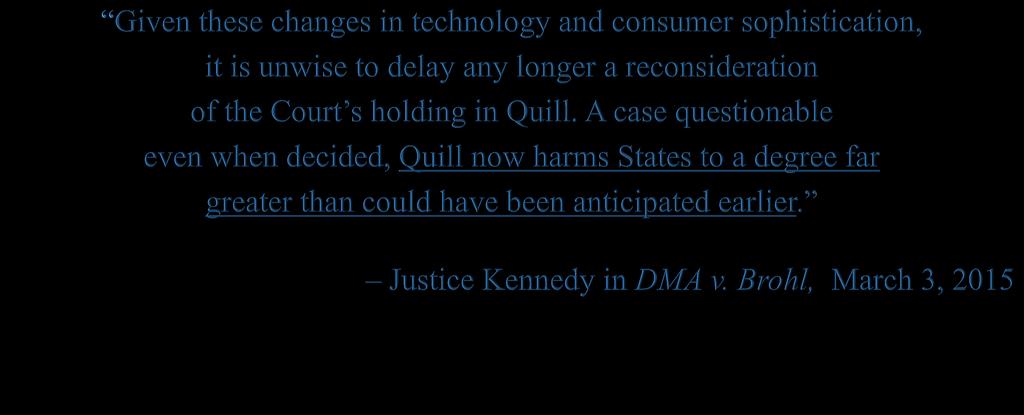

23 Whether characterized as affirmative or dormant, the fundamental negative purpose of the Commerce Clause was and is to assure that state governments do not unreasonably burden commerce among the states through unfair trade barriers that disfavor out-of-state commerce. The Commerce Clause cannot possibly mean that the Constitution gives out-of-state competitors the advantage of an un-level playing field by evading equal responsibility for taxation and tax collection.

24 [I]t is highly unlikely that the language of Quill that a state s ability to compel a vendor to collect a sales and use tax may turn on the presence in the taxing State of a small sales force, plant or office was intended as a definitive description of other contacts that might demonstrate the existence of a substantial nexus. (Scholastic Book Clubs, Inc., Connecticut Supreme Court, 2012)

25 CGS (a)(15)(A) engaged in business in the state incudes: Selling or any activity in this state in connection with selling tangible personal property. Retail sales made outside the state to an in-state destination even without a place of business in the state. Regular or systematic solicitation by electronic means for the purpose of effecting sales. Agency, control, assignment, independent contracting. Including hosted click-through sales. CGS (4) enforcement: Examine the books, papers, records and may investigate in order to verify the accuracy of any return or, if no return, determine the amount to be paid.

26 Senate Bill 106 Background Inability to collect sales tax from remote sellers threatens South Dakota s efforts to sustain a broad tax system, which allows South Dakota to keep taxes low. Because South Dakota doesn t have a state income tax, sales and use tax revenue are essential in funding state and local services. The growth of online retail ensures further erosion to our sales tax base.

27 Senate Bill 106 Background Remote Sellers must remit South Dakota sales tax if they meet one of two criteria The seller s gross revenue exceeds $100,000. The sellers made 200 or more separate transactions into South Dakota. Any sales tax obligation required by this act cannot be applied to past sales.

28 Legal Action On April 28, 2016, the State of South Dakota filed a declaratory judgment action in the Sixth Judicial Circuit Court, Hughes County, against four remote sellers: Newegg, Overstock, Systemax, Wayfair. On May 25, 2016, Defendants file notice of intent to move from State court to US District Federal Court.

29 Legal Action On January 17, 2017, Opinion entered to grant State s motion to remand back to state court. On March 6, 2017, South Dakota Sixth Circuit Court Judge Mark Barnett enters order granting Defendant s Motion for Summary Judgement. On March 8, 2017, South Dakota files Notice to Appeal Circuit Court s ruling to the Supreme Court of South Dakota.

30

31

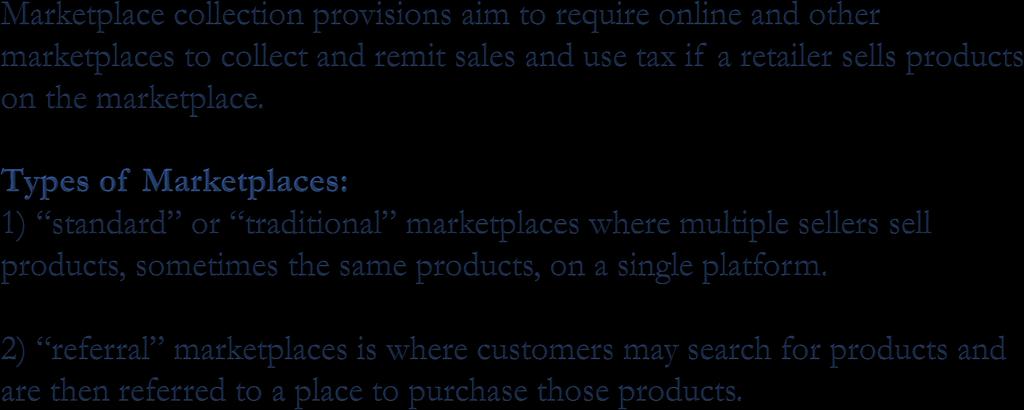

32 FY Marketplace Provider Budget Proposal Legislative proposal to expand sales tax collection responsibilities to online marketplace providers Purpose: Online marketplaces such as Amazon Marketplace, ebay, Etsy, Walmart.com and various app stores represent a large and growing share of online retail sales. Under the typical online marketplace business model, the marketplace provider: 1) provides a forum in which third-party sellers are able to display their products and transact sales; and 2) facilitates the collection and processing of payments for these third-party sellers. As a general rule, online marketplaces do not collect sales tax as part of their service.

33 The Tax Department has documented sales tax compliance problems with online marketplaces. Desk audits 21 selected, only one collecting Field Audits 2 not registered, 12 under reporting Information from marketplace marketplace collects 20% not registered or under reporting taxable sales NEW YORKERS PAID 3 rd PARTY DID NOT REMIT! Current- inefficient and costly compliance Marketplace third party sellers not collecting must register and file returns Numbers are high could double the 600K registered Marketplace efficiencies one registration, one filing Note many voluntarily collect and remit (Sears.com, Apple s App store)

34 Proposal: Tax would be collected and remitted by the marketplace provider on sales to New Yorkers by all third-party sellers, including those that do not have a presence (nexus) in the State. Approximately additional $275 million 1 st year (State and local) growth of 15% to 20% annually is expected for the foreseeable future. The tax collection requirement only to sales of tangible personal property. Part X also applied to sales of services, hotel occupancy, and admission tickets. Small start-up online marketplaces would be excluded from the collection requirement with the inclusion of a sales threshold (i.e., $100 million in annual sales).

35 The recent focus has been on South Dakota s and Alabama s litigation of their law/regulation directly challenging Quill However, Irwin Naturals, a company based in California that sells nutritional products, will likely request the U.S. Supreme Court review a Washington Court of Appeals decision, see Docket 16A1078; cert. petition due 7/14/2017, that addresses Quill s separation of the states authority to tax under the Due Process Clause and Commerce Clause Irwin Naturals, citing Norton v. IL Dep t of Rev., 340 U.S. 354 (1951), is arguing its retail sales shipped to customers in WA should be dissociated with its wholesale sales made to retailers and distributors in WA While Norton addressed a gross receipts tax, Irwin Natural asserts that should also apply to sales/use taxes and that the Court s holding in Nat l Geographic Soc. V. Cal. Bd. of Equal., 430 U.S. 551 (1977), which held a taxpayer s presence in the state did not have to be directly related to its sales activity for California to impose a sales/use tax collection and remittance obligation on a business Irwin Naturals argues that in the Court s 1992 Quill decision, where the Court distinguishing Due Process Clause minimum contacts from the Commerce Clause s substantial nexus, the Court made Nat l Geographic no longer relevant because the Court s analysis in that case was based on the Due Process Clause and not the Commerce Clause Could this case be a vehicle for the Court to address Quill? 35

36 Ø Will the Highest Court of a State Overrule Quill? Ø If not, would the Court still take up the case? Ø What would be the nexus standard if Quill is reversed? Ø Is Retroactivity still a concern? Ø Will Congress act? Ø Does it depend of whether the U.S. Supreme Court takes up a Case? Ø Will membership in the SSUTA be needed? 36

Age of Insured Discount

A discount may apply based on the age of the insured. The age of each insured shall be calculated as the policyholder s age as of the last day of the calendar year. The age of the named insured in the

A discount may apply based on the age of the insured. The age of each insured shall be calculated as the policyholder s age as of the last day of the calendar year. The age of the named insured in the

Agenda. Overview. Digital Age SALT Issues Applying Old Rules to New Technology

COST NORTHWEST REGIONAL TAX SEMINAR Digital Age SALT Issues Applying Old Rules to New Technology June 17, 2010 Presented By: Carolynn S. Iafrate Stephen P. Kranz 1 Agenda Overview Sourcing of Digital Products

COST NORTHWEST REGIONAL TAX SEMINAR Digital Age SALT Issues Applying Old Rules to New Technology June 17, 2010 Presented By: Carolynn S. Iafrate Stephen P. Kranz 1 Agenda Overview Sourcing of Digital Products

Comparative Revenues and Revenue Forecasts Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

KPMG Share Forum. The Wayfair decision: navigating a world without Quill. Los Angeles, CA

KPMG Share Forum The Wayfair decision: navigating a world without Quill Los Angeles, CA [August 23, 2018 Notices The following information is not intended to be written advice concerning one or more Federal

KPMG Share Forum The Wayfair decision: navigating a world without Quill Los Angeles, CA [August 23, 2018 Notices The following information is not intended to be written advice concerning one or more Federal

Bad Debts: How Contractual Terms and Sales Tax Intersect IPT Annual Conference Charlotte, North Carolina

Bad Debts: How Contractual Terms and Sales Tax Intersect Thomas Zessman Senior Tax Manager U.S. Bank Minneapolis, Minnesota thomas.zessman@usbank.com Kyle Brehm State and Local Tax Director PricewaterhouseCoopers

Bad Debts: How Contractual Terms and Sales Tax Intersect Thomas Zessman Senior Tax Manager U.S. Bank Minneapolis, Minnesota thomas.zessman@usbank.com Kyle Brehm State and Local Tax Director PricewaterhouseCoopers

The Acquisition of Regions Insurance Group. April 6, 2018

The Acquisition of Regions Insurance Group April 6, 2018 Forward-Looking Statements This presentation contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform

The Acquisition of Regions Insurance Group April 6, 2018 Forward-Looking Statements This presentation contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform

STATE TAX WITHHOLDING GUIDELINES

STATE TAX WITHHOLDING GUIDELINES ( Guardian Insurance & Annuity Company, Inc. and Guardian Life Insurance Company of America (hereafter collectively referred to as Company )) (Last Updated 11/2/215) state

STATE TAX WITHHOLDING GUIDELINES ( Guardian Insurance & Annuity Company, Inc. and Guardian Life Insurance Company of America (hereafter collectively referred to as Company )) (Last Updated 11/2/215) state

Property Tax Relief in New England

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

Installment Loans CHARTS. No cap other than unconscionability:

NCLC NATIONAL CONSUMER LAW CENTER Installment Loans WILL STATES PROTECT BORROWERS FROM A NEW WAVE OF PREDATORY LENDING? Copyright 2015, National Consumer Law Center, Inc. CHARTS CHART 1 Full APRs Allowed

NCLC NATIONAL CONSUMER LAW CENTER Installment Loans WILL STATES PROTECT BORROWERS FROM A NEW WAVE OF PREDATORY LENDING? Copyright 2015, National Consumer Law Center, Inc. CHARTS CHART 1 Full APRs Allowed

Michael Bannasch

1 2 Michael Bannasch michael.bannasch@rehmann.com 734.302.4137 3 Physical presence nexus requirement Sales tax definitely Other taxes? Not so sure National Bellas Hess Due Process Clause = Commerce Clause

1 2 Michael Bannasch michael.bannasch@rehmann.com 734.302.4137 3 Physical presence nexus requirement Sales tax definitely Other taxes? Not so sure National Bellas Hess Due Process Clause = Commerce Clause

SALES TAX AND WAYFAIR -

SALES TAX AND WAYFAIR - WHAT DOES IT MEAN FOR YOUR BUSINESS? by Karen Poist, CPA On June 21, 2018, the Supreme Court issued its decision on the South Dakota v. Wayfair, Inc. case (Wayfair). This is the

SALES TAX AND WAYFAIR - WHAT DOES IT MEAN FOR YOUR BUSINESS? by Karen Poist, CPA On June 21, 2018, the Supreme Court issued its decision on the South Dakota v. Wayfair, Inc. case (Wayfair). This is the

NCSL Midwest States Fiscal Leaders Forum. March 10, 2017

NCSL Midwest States Fiscal Leaders Forum March 10, 2017 Public Pensions: 50-State Overview David Draine, Senior Officer Public Sector Retirement Systems Project The Pew Charitable Trusts More than 40 active,

NCSL Midwest States Fiscal Leaders Forum March 10, 2017 Public Pensions: 50-State Overview David Draine, Senior Officer Public Sector Retirement Systems Project The Pew Charitable Trusts More than 40 active,

COMPARISON OF ABA MODEL RULE FOR REGISTRATION OF IN-HOUSE COUNSEL WITH STATE VERSIONS

As of September 7, 2016 2016 American Bar Association COMPARISON OF ABA MODEL RULE FOR REGISTRATION OF IN-HOUSE COUNSEL WITH STATE VERSIONS AMERICAN BAR ASSOCIATION CENTER FOR PROFESSIONAL RESPONSIBILITY

As of September 7, 2016 2016 American Bar Association COMPARISON OF ABA MODEL RULE FOR REGISTRATION OF IN-HOUSE COUNSEL WITH STATE VERSIONS AMERICAN BAR ASSOCIATION CENTER FOR PROFESSIONAL RESPONSIBILITY

ACORD Forms Updated in AMS R1

ACORD Forms Updated in AMS360 2017 R1 The following forms will use the ACORD form viewer, also new in this release. Forms with an indicate they were added because of requests in the Product Enhancement

ACORD Forms Updated in AMS360 2017 R1 The following forms will use the ACORD form viewer, also new in this release. Forms with an indicate they were added because of requests in the Product Enhancement

Streamlined Sales Tax Governing Board and Business Advisory Council Update

Streamlined Sales Tax Governing Board and Business Advisory Council Update Charles Collins, ADP Fred Nicely, Council On State Taxation Craig Johnson, Streamlined Sales Tax Governing Board NCSL SALT Taskforce

Streamlined Sales Tax Governing Board and Business Advisory Council Update Charles Collins, ADP Fred Nicely, Council On State Taxation Craig Johnson, Streamlined Sales Tax Governing Board NCSL SALT Taskforce

Multistate indirect tax trends and policies

Multistate indirect tax trends and policies Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

Multistate indirect tax trends and policies Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

Tax Freedom Day 2018 is April 19th

Apr. 2018 Tax Freedom Day 2018 is April 19th Erica York Analyst Key Findings Tax Freedom Day is a significant date for taxpayers and lawmakers because it represents how long Americans as a whole have to

Apr. 2018 Tax Freedom Day 2018 is April 19th Erica York Analyst Key Findings Tax Freedom Day is a significant date for taxpayers and lawmakers because it represents how long Americans as a whole have to

medicaid a n d t h e How will the Medicaid Expansion for Adults Impact Eligibility and Coverage? Key Findings in Brief

on medicaid a n d t h e uninsured July 2012 How will the Medicaid Expansion for Adults Impact Eligibility and Coverage? Key Findings in Brief Effective January 2014, the ACA establishes a new minimum Medicaid

on medicaid a n d t h e uninsured July 2012 How will the Medicaid Expansion for Adults Impact Eligibility and Coverage? Key Findings in Brief Effective January 2014, the ACA establishes a new minimum Medicaid

Whirlwind Review of New State Tax Laws

Todd Lard, Partner Sutherland Asbill & Brennan LLP Carley Roberts, Partner Sutherland Asbill & Brennan LLP FTA Annual Conference June 10, 2014 Whirlwind Review of New State Tax Laws Agenda Factor Weighting

Todd Lard, Partner Sutherland Asbill & Brennan LLP Carley Roberts, Partner Sutherland Asbill & Brennan LLP FTA Annual Conference June 10, 2014 Whirlwind Review of New State Tax Laws Agenda Factor Weighting

Older consumers and student loan debt by state

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

36 Million Without Health Insurance in 2014; Decreases in Uninsurance Between 2013 and 2014 Varied by State

36 Million Without Health Insurance in 2014; Decreases in Uninsurance Between 2013 and 2014 Varied by State An estimated 36 million people in the United States had no health insurance in 2014, approximately

36 Million Without Health Insurance in 2014; Decreases in Uninsurance Between 2013 and 2014 Varied by State An estimated 36 million people in the United States had no health insurance in 2014, approximately

TCJA and the States Responding to SALT Limits

TCJA and the States Responding to SALT Limits Kim S. Rueben Tuesday, January 29, 2019 1 What does this mean for Individuals under TCJA About two-thirds of taxpayers will receive a tax cut with the largest

TCJA and the States Responding to SALT Limits Kim S. Rueben Tuesday, January 29, 2019 1 What does this mean for Individuals under TCJA About two-thirds of taxpayers will receive a tax cut with the largest

State Tax Chart Results

State Tax Chart Results Tax Type: Sales/Use Legend: N/A - Not Applicable Software as a Service (SaaS) This chart shows whether or not the state imposes a tax on the sales of Software as a Service (SaaS).

State Tax Chart Results Tax Type: Sales/Use Legend: N/A - Not Applicable Software as a Service (SaaS) This chart shows whether or not the state imposes a tax on the sales of Software as a Service (SaaS).

2016 Workers compensation premium index rates

2016 Workers compensation premium index rates NH WA OR NV CA AK ID AZ UT MT WY CO NM MI VT ND MN SD WI NY NE IA PA IL IN OH WV VA KS MO KY NC TN OK AR SC MS AL GA TX LA FL ME MA RI CT NJ DE MD DC = Under

2016 Workers compensation premium index rates NH WA OR NV CA AK ID AZ UT MT WY CO NM MI VT ND MN SD WI NY NE IA PA IL IN OH WV VA KS MO KY NC TN OK AR SC MS AL GA TX LA FL ME MA RI CT NJ DE MD DC = Under

SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008

U.S. DEPARTMENT OF LABOR EMPLOYMENT AND TRAINING ADMINISTRATION Office Workforce Security SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008 AL AK AZ AR CA CO CT DE DC FL GA HI /

U.S. DEPARTMENT OF LABOR EMPLOYMENT AND TRAINING ADMINISTRATION Office Workforce Security SIGNIFICANT PROVISIONS OF STATE UNEMPLOYMENT INSURANCE LAWS JANUARY 2008 AL AK AZ AR CA CO CT DE DC FL GA HI /

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004 by Dr. Donald Bruce, Research Assistant Professor dbruce@utk.edu and Dr. William F. Fox, Professor and Director billfox@utk.edu

State and Local Sales Tax Revenue Losses from E-Commerce: Estimates as of July 2004 by Dr. Donald Bruce, Research Assistant Professor dbruce@utk.edu and Dr. William F. Fox, Professor and Director billfox@utk.edu

State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

IMPORTANT TAX INFORMATION

IMPORTANT TAX INFORMATION To set up and maintain your account with WestconGroup, we require you to provide us valid Resale Certificates for all states that you are located in, as well as for any other

IMPORTANT TAX INFORMATION To set up and maintain your account with WestconGroup, we require you to provide us valid Resale Certificates for all states that you are located in, as well as for any other

Remote Seller Collection Authority Issues. August 22, 2016

Midwestern States Association of Tax Administrators 2016 Annual Meeting Des Moines, IA Remote Seller Collection Authority Issues August 22, 2016 Andy Gerlach Secretary, South Dakota DOR Craig Johnson SSTBG

Midwestern States Association of Tax Administrators 2016 Annual Meeting Des Moines, IA Remote Seller Collection Authority Issues August 22, 2016 Andy Gerlach Secretary, South Dakota DOR Craig Johnson SSTBG

Federal Tax Reform Impact on 2019 Legislative Sessions: GILTI

Federal Tax Reform Impact on 2019 Legislative Sessions: GILTI Executive Committee Task Force on State and Local Taxation Scottsdale, Arizona November 17, 2018 Karl Frieden, COST Deborah Bierbaum, AT&T

Federal Tax Reform Impact on 2019 Legislative Sessions: GILTI Executive Committee Task Force on State and Local Taxation Scottsdale, Arizona November 17, 2018 Karl Frieden, COST Deborah Bierbaum, AT&T

The Lincoln National Life Insurance Company Term Portfolio

The Lincoln National Life Insurance Company Term Portfolio State Availability as of 7/16/2018 PRODUCTS AL AK AZ AR CA CO CT DE DC FL GA GU HI ID IL IN IA KS KY LA ME MP MD MA MI MN MS MO MT NE NV NH NJ

The Lincoln National Life Insurance Company Term Portfolio State Availability as of 7/16/2018 PRODUCTS AL AK AZ AR CA CO CT DE DC FL GA GU HI ID IL IN IA KS KY LA ME MP MD MA MI MN MS MO MT NE NV NH NJ

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015 Norton Francis State and Local Finance Initiative Urban-Brookings

Taxing Investment Income in the States New Hampshire Fiscal Policy Institute 2 nd Annual Budget and Policy Conference Concord, NH January 23, 2015 Norton Francis State and Local Finance Initiative Urban-Brookings

ehealth, Inc Fall Cost Report for Individual and Family Policyholders

ehealth, Inc. 2010 Fall Cost Report for and Family Policyholders Table of Contents Page Methodology.................................................................. 2 ehealth, Inc. 2010 Fall Cost Report

ehealth, Inc. 2010 Fall Cost Report for and Family Policyholders Table of Contents Page Methodology.................................................................. 2 ehealth, Inc. 2010 Fall Cost Report

American Memorial Contract

American Memorial Contract Please complete all pages of the contract and send it back to Stephens- Matthews with a copy of each state license you choose to appoint in. You are required to submit with the

American Memorial Contract Please complete all pages of the contract and send it back to Stephens- Matthews with a copy of each state license you choose to appoint in. You are required to submit with the

Non-Financial Change Form

Non-Financial Change Form Please Print All Information Below Section 1. Contract Owner s Information Administrative Offices: PO BOX 19097 Greenville, SC 29602-9097 Phone number (800) 449-0523 Overnight

Non-Financial Change Form Please Print All Information Below Section 1. Contract Owner s Information Administrative Offices: PO BOX 19097 Greenville, SC 29602-9097 Phone number (800) 449-0523 Overnight

Local Anesthesia Administration by Dental Hygienists State Chart

Education or AK 1981 General Both Specific Yes WREB 16 hrs didactic; 6 hrs ; 8 hrs lab AZ 1976 General Both Accredited Yes WREB 36 hrs; 9 types of AR 1995 Direct Both Accredited/ Board Approved No 16 hrs

Education or AK 1981 General Both Specific Yes WREB 16 hrs didactic; 6 hrs ; 8 hrs lab AZ 1976 General Both Accredited Yes WREB 36 hrs; 9 types of AR 1995 Direct Both Accredited/ Board Approved No 16 hrs

Uniform Consent to Service of Process

Applicant Company Name: NAIC No. FEIN: Uniform Consent to Service of Process Original Designation Amended Designation (must be submitted directly to states) Applicant Company Name: Previous Name (if applicable):

Applicant Company Name: NAIC No. FEIN: Uniform Consent to Service of Process Original Designation Amended Designation (must be submitted directly to states) Applicant Company Name: Previous Name (if applicable):

Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average

Issue Brief March 6, 2012 Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average The money we pay in fees and taxes helps create jobs, build a strong economy, and preserve Oregon

Issue Brief March 6, 2012 Oregon: Where Taxes Are Low, Fees Are High and Revenue Is Slightly Below Average The money we pay in fees and taxes helps create jobs, build a strong economy, and preserve Oregon

STATE MOTOR FUEL TAX INCREASES:

STATE MOTOR FUEL TAX INCREASES: 2013-2018 Since 2013, 27 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-four of those states increased their

STATE MOTOR FUEL TAX INCREASES: 2013-2018 Since 2013, 27 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-four of those states increased their

States and Medicaid Provider Taxes or Fees

March 2016 Fact Sheet States and Medicaid Provider Taxes or Fees Medicaid is jointly financed by states and the federal government. Provider taxes are an integral source of Medicaid financing governed

March 2016 Fact Sheet States and Medicaid Provider Taxes or Fees Medicaid is jointly financed by states and the federal government. Provider taxes are an integral source of Medicaid financing governed

State Trust Fund Solvency

Unemployment Insurance State Trust Fund Solvency National Employment Law Project Conference - Washington DC December 7, 2009 Robert Pavosevich pavosevich.robert@dol.gov Unemployment Insurance Program

Unemployment Insurance State Trust Fund Solvency National Employment Law Project Conference - Washington DC December 7, 2009 Robert Pavosevich pavosevich.robert@dol.gov Unemployment Insurance Program

Sales Factors Based on the Benefit Received

Sales Factors Based on the Benefit Received ABA Tax Section Meeting San Diego, CA February 17, 2012 Giles Sutton, Partner Grant Thornton Robert Mahon, Partner Perkins Coie LLP 704.632.6885 206.359.6260

Sales Factors Based on the Benefit Received ABA Tax Section Meeting San Diego, CA February 17, 2012 Giles Sutton, Partner Grant Thornton Robert Mahon, Partner Perkins Coie LLP 704.632.6885 206.359.6260

Tax Breaks for Elderly Taxpayers in the States in 2016

AL Payments from defined benefit private plans are exempt; most public systems are exempt; military and US Civil service are exempt Special Homestead ion for 65+ +25.2% +2.4% AK No PIT Homestead ion for

AL Payments from defined benefit private plans are exempt; most public systems are exempt; military and US Civil service are exempt Special Homestead ion for 65+ +25.2% +2.4% AK No PIT Homestead ion for

Who s Above the Social Security Payroll Tax Cap? BY NICOLE WOO, JANELLE JONES, AND JOHN SCHMITT*

Issue Brief September 2011 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Who s Above the Social Security

Issue Brief September 2011 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Who s Above the Social Security

Household Income for States: 2010 and 2011

Household Income for States: 2010 and 2011 American Community Survey Briefs By Amanda Noss Issued September 2012 ACSBR/11-02 INTRODUCTION Estimates from the 2010 American Community Survey (ACS) and the

Household Income for States: 2010 and 2011 American Community Survey Briefs By Amanda Noss Issued September 2012 ACSBR/11-02 INTRODUCTION Estimates from the 2010 American Community Survey (ACS) and the

Massachusetts Budget and Policy Center

Progressive Massachusetts 2013 Policy Conference March 24, 2013 Lasell College Newton, MA Presentation by Massachusetts Budget and Policy Center Our State Budget: Building a Better Future Together Massachusetts

Progressive Massachusetts 2013 Policy Conference March 24, 2013 Lasell College Newton, MA Presentation by Massachusetts Budget and Policy Center Our State Budget: Building a Better Future Together Massachusetts

Please print using blue or black ink. Please keep a copy for your records and send completed form to the following address.

20 Disbursement for Beneficiary/QDRO Account IBEW Local Union No. 716 Retirement Plan Instructions About You Please print using blue or black ink. Please keep a copy for your records and send completed

20 Disbursement for Beneficiary/QDRO Account IBEW Local Union No. 716 Retirement Plan Instructions About You Please print using blue or black ink. Please keep a copy for your records and send completed

Comments and Thoughts on Senate Tax Legislation Senate Hearing March 4, 2015

Comments and Thoughts on Senate Tax Legislation Senate Hearing March 4, 2015 Dale Craymer Texas Taxpayers and Research Association 400 West 15 th Street Austin, Texas 78701 www.ttara.org Page 2 TTARA For:

Comments and Thoughts on Senate Tax Legislation Senate Hearing March 4, 2015 Dale Craymer Texas Taxpayers and Research Association 400 West 15 th Street Austin, Texas 78701 www.ttara.org Page 2 TTARA For:

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Charts with Analysis: Tax Tax Type: Sales and Use Tax Topic: Cash for Clunkers Payments

Effective July 1, 2009, until November 1, 2009, the federal government has enacted the Consumer Assistance to Recycle and Save (CARS) Program, Title XIII of PL 111-32 (2009), 123 Stat. 1859. The program,

Effective July 1, 2009, until November 1, 2009, the federal government has enacted the Consumer Assistance to Recycle and Save (CARS) Program, Title XIII of PL 111-32 (2009), 123 Stat. 1859. The program,

Long-Term Care Education Requirements Prior to Selling

for AK All Health 8 hrs 4 hrs 24 months AL All Accident & Health 8 hrs 4 hrs Renewal deadline is the date the license expires. s are renewed biennially based on agent's birth month and year. AR All Accident,

for AK All Health 8 hrs 4 hrs 24 months AL All Accident & Health 8 hrs 4 hrs Renewal deadline is the date the license expires. s are renewed biennially based on agent's birth month and year. AR All Accident,

Tax Freedom Day 2019 is April 16th

Apr. 2019 Tax Freedom Day 2019 is April 16th Erica York Economist Madison Mauro Research Assistant Emma Wei Research Assistant Key Findings This year, Tax Freedom Day falls on April 16, or 105 days into

Apr. 2019 Tax Freedom Day 2019 is April 16th Erica York Economist Madison Mauro Research Assistant Emma Wei Research Assistant Key Findings This year, Tax Freedom Day falls on April 16, or 105 days into

Florida 1/1/2016 Workers Compensation Rate Filing

Florida 1/1/2016 Workers Compensation Rate Filing Kirt Dooley, FCAS, MAAA October 21, 2015 1 $ Billions 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Florida s Workers Compensation Premium Volume 2.368 0.765 0.034

Florida 1/1/2016 Workers Compensation Rate Filing Kirt Dooley, FCAS, MAAA October 21, 2015 1 $ Billions 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 Florida s Workers Compensation Premium Volume 2.368 0.765 0.034

The State of State Taxes: Impact of Federal Tax Reform, and Modernizing State Sales Tax Systems after Wayfair

The State of State Taxes: Impact of Federal Tax Reform, and Modernizing State Sales Tax Systems after Wayfair Arizona Tax Research Association Annual Meeting November 15, 2018 Speakers: Douglas L. Lindholm

The State of State Taxes: Impact of Federal Tax Reform, and Modernizing State Sales Tax Systems after Wayfair Arizona Tax Research Association Annual Meeting November 15, 2018 Speakers: Douglas L. Lindholm

State Tax Policy Update

State Tax Policy Update Broadband Tax Institute October 17, 2017 Moderator Jamie Fenwick Charter Communications Speakers Ellen Berenholz Comcast Corp. Deborah Bierbaum AT&T Annabelle Canning Capitol Tax

State Tax Policy Update Broadband Tax Institute October 17, 2017 Moderator Jamie Fenwick Charter Communications Speakers Ellen Berenholz Comcast Corp. Deborah Bierbaum AT&T Annabelle Canning Capitol Tax

Long-Term Care Partnership Overview & Training Requirements Guide

Long-Term Care Partnership Overview & Training Requirements Guide Version Sept. 12, 2012 M28108 Contents LONG-TERM CARE PARTNERSHIP OVERVIEW & TRAINING REQUIREMENTS GUIDE Long-Term Care Partnership Overview...4

Long-Term Care Partnership Overview & Training Requirements Guide Version Sept. 12, 2012 M28108 Contents LONG-TERM CARE PARTNERSHIP OVERVIEW & TRAINING REQUIREMENTS GUIDE Long-Term Care Partnership Overview...4

Required Minimum Distribution Election Form for IRA s, 403(b)/TSA and other Qualified Plans

/TSA and other Qualified Plans") Required Minimum Distribution Election Form for IRA s, 403(b)/TSA and other Qualified Plans For Policyholders who have not annuitized their deferred annuity contracts Zurich American Life Insurance Company

Required Minimum Distribution Election Form for IRA s, 403(b)/TSA and other Qualified Plans For Policyholders who have not annuitized their deferred annuity contracts Zurich American Life Insurance Company

Corporate Income Tax and Policy Considerations

Corporate Income Tax and Policy Considerations Presentation by Richard Anklam, Executive Director, New Mexico Tax Research Institute To The Interim Revenue Stabilization and Tax Policy Committee September

Corporate Income Tax and Policy Considerations Presentation by Richard Anklam, Executive Director, New Mexico Tax Research Institute To The Interim Revenue Stabilization and Tax Policy Committee September

STATE MOTOR FUEL TAX INCREASES:

Since 2013, 26 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-three of those states increased their state gas tax, while three states Kentucky,

Since 2013, 26 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-three of those states increased their state gas tax, while three states Kentucky,

Charles Gullickson (Penn Treaty/ANIC Task Force Chair), Richard Klipstein (NOLHGA)

, Richard Klipstein (NOLHGA)") MEMO DATE: TO: Charles Gullickson (Penn Treaty/ANIC Task Force Chair), Richard Klipstein (NOLHGA) FROM: Vincent L. Bodnar, ASA, MAAA RE: Penn Treaty Network American Insurance Company and American Network

MEMO DATE: TO: Charles Gullickson (Penn Treaty/ANIC Task Force Chair), Richard Klipstein (NOLHGA) FROM: Vincent L. Bodnar, ASA, MAAA RE: Penn Treaty Network American Insurance Company and American Network

Long-Term Care Education Requirements Prior to Selling

for Training AK All Health 8 hrs 4 hrs 24 months AL All Accident & Health 8 hrs 4 hrs Renewal deadline is the date the license expires. s are renewed biennially based on agent's birth month and year. AR

for Training AK All Health 8 hrs 4 hrs 24 months AL All Accident & Health 8 hrs 4 hrs Renewal deadline is the date the license expires. s are renewed biennially based on agent's birth month and year. AR

Long-Term Care Partnership Overview & Training Requirements Guide

Long-Term Care Insurance Mutual of Omaha Insurance Company SM Long-Term Care Partnership Overview & Training Requirements Guide 75014 Version November 16, 2015 For producer use only. Not for use with the

Long-Term Care Insurance Mutual of Omaha Insurance Company SM Long-Term Care Partnership Overview & Training Requirements Guide 75014 Version November 16, 2015 For producer use only. Not for use with the

UNIFORM SALES & USE TAX CERTIFICATE

UNIFORM SALES & USE TAX CERTIFICATE The issuer and the recipient have the responsibility of determining the proper use of this certificate under applicable laws in each state, as these may change from

UNIFORM SALES & USE TAX CERTIFICATE The issuer and the recipient have the responsibility of determining the proper use of this certificate under applicable laws in each state, as these may change from

FISCAL YEAR 2016 AT A GLANCE Number of Authorized Firms

FISCAL YEAR 2016 AT A GLANCE Number of Authorized Firms 300,000 275,000 250,000 225,000 200,000 175,000 150,000 125,000 100,000 246,565 252,962 261,150 258,632 260,115 FY 2012 FY 2013 FY 2014 FY 2015 FY

FISCAL YEAR 2016 AT A GLANCE Number of Authorized Firms 300,000 275,000 250,000 225,000 200,000 175,000 150,000 125,000 100,000 246,565 252,962 261,150 258,632 260,115 FY 2012 FY 2013 FY 2014 FY 2015 FY

2018 NAFC ANNUAL CONFERENCE. THE CHANGING FINANCIAL LANDSCAPE IN TRUCKING: addressing opportunities and challenges

2018 NAFC ANNUAL CONFERENCE THE CHANGING FINANCIAL LANDSCAPE IN TRUCKING: addressing opportunities and challenges State Income Tax Update Agenda State Impacts of Federal Reform State Nexus Apportionment

2018 NAFC ANNUAL CONFERENCE THE CHANGING FINANCIAL LANDSCAPE IN TRUCKING: addressing opportunities and challenges State Income Tax Update Agenda State Impacts of Federal Reform State Nexus Apportionment

Health Insurance Price Index for October-December February 2014

Health Insurance Price Index for October-December 2013 February 2014 ehealth 2.2014 Table of Contents Introduction... 3 Executive Summary and Highlights... 4 Nationwide Health Insurance Costs National

Health Insurance Price Index for October-December 2013 February 2014 ehealth 2.2014 Table of Contents Introduction... 3 Executive Summary and Highlights... 4 Nationwide Health Insurance Costs National

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA Phone: Fax:

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA 30329 Phone: 404-315-9515 Fax: 404-315-6558 AGENCY/BROKER PROFILE Please type your answers. Use a separate

RLI TRANSPORTATION A Division of RLI Insurance Company 2970 Clairmont Road, Suite 1000 Atlanta, GA 30329 Phone: 404-315-9515 Fax: 404-315-6558 AGENCY/BROKER PROFILE Please type your answers. Use a separate

ACORD Forms in ebixasp (03/2004)

") ACORD Forms in ebixasp (03/2004) Form number Form Name Edition Date 1 Property Loss Notice 2002/1 2 Automobile Loss Notice 2002/1 3 General Liability Notice of Occurrence/Claim 2002/1 4 Workers Compensation

ACORD Forms in ebixasp (03/2004) Form number Form Name Edition Date 1 Property Loss Notice 2002/1 2 Automobile Loss Notice 2002/1 3 General Liability Notice of Occurrence/Claim 2002/1 4 Workers Compensation

Data Note: What if Per Enrollee Medicaid Spending Growth Had Been Limited to CPI-M from ?

Data Note: What if Per Enrollee Medicaid Spending Growth Had Been Limited to CPI-M from 2001-2011? Rachel Garfield, Robin Rudowitz, and Katherine Young Congress is currently debating the American Health

Data Note: What if Per Enrollee Medicaid Spending Growth Had Been Limited to CPI-M from 2001-2011? Rachel Garfield, Robin Rudowitz, and Katherine Young Congress is currently debating the American Health

NASRA Issue Brief: Employee Contributions to Public Pension Plans

NASRA Issue Brief: Employee Contributions to Public Pension Plans September 2017 Unlike in the private sector, nearly all employees of state and local government are required to share in the cost of their

NASRA Issue Brief: Employee Contributions to Public Pension Plans September 2017 Unlike in the private sector, nearly all employees of state and local government are required to share in the cost of their

The State Tax Implications of Federal Tax Reform Legislation

The State Tax Implications of Federal Tax Reform Legislation Executive Committee Task Force on State and Local Taxation Phoenix, Arizona January 14, 2017 Joe Crosby, Multistate Associates Karl Frieden,

The State Tax Implications of Federal Tax Reform Legislation Executive Committee Task Force on State and Local Taxation Phoenix, Arizona January 14, 2017 Joe Crosby, Multistate Associates Karl Frieden,

Report to Congressional Defense Committees

Report to Congressional Defense Committees The Department of Defense Comprehensive Autism Care Demonstration December 2016 Quarterly Report to Congress In Response to: Senate Report 114-255, page 205,

Report to Congressional Defense Committees The Department of Defense Comprehensive Autism Care Demonstration December 2016 Quarterly Report to Congress In Response to: Senate Report 114-255, page 205,

Unemployment Insurance Benefit Adequacy: How many? How much? How Long?

Unemployment Insurance Benefit Adequacy: How many? How much? How Long? Joel Sacks, Deputy Commissioner Washington State Employment Security Department March 1, 2012 1 Outline How many get unemployment

Unemployment Insurance Benefit Adequacy: How many? How much? How Long? Joel Sacks, Deputy Commissioner Washington State Employment Security Department March 1, 2012 1 Outline How many get unemployment

Impact of Federal Reform on State Corporate Income Tax Base & the Best and Worst of Sales Tax Administration Focus on New Mexico

Council On State Taxation 1 2018 15 th Annual NMTRI Tax Policy Conference Impact of Federal Reform on State Corporate Income Tax Base & the Best and Worst of Sales Tax Administration Focus on New Mexico

Council On State Taxation 1 2018 15 th Annual NMTRI Tax Policy Conference Impact of Federal Reform on State Corporate Income Tax Base & the Best and Worst of Sales Tax Administration Focus on New Mexico

Systematic Distribution Form

Systematic Distribution Form (To be used for all Qualified Plans, IRA s and Non-Qualified Plans) (This form is not applicable to a Required Minimum Distribution ( RMD ). If you are older than 70 ½, refer

Systematic Distribution Form (To be used for all Qualified Plans, IRA s and Non-Qualified Plans) (This form is not applicable to a Required Minimum Distribution ( RMD ). If you are older than 70 ½, refer

State Sales Tax on Drop Shipments: Navigating Various States' Rules on Registrations and Exemptions

Navigating Various States' Rules on Registrations and Exemptions THURSDAY, JUNE 25, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you

Navigating Various States' Rules on Registrations and Exemptions THURSDAY, JUNE 25, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you

The Economics of Homelessness

15 The Economics of Homelessness Despite frequent characterization as a psychosocial problem, the problem of homelessness is largely economic. People who become homeless have insufficient financial resources

15 The Economics of Homelessness Despite frequent characterization as a psychosocial problem, the problem of homelessness is largely economic. People who become homeless have insufficient financial resources

Request for Disbursement Vermont State Teachers Retirement System 403(b) Plan

Plan") Instructions Request for Disbursement Vermont State Teachers Retirement System 403(b) Plan Please print using blue or black ink. This request must be authorized by your employer. Please forward this form

Instructions Request for Disbursement Vermont State Teachers Retirement System 403(b) Plan Please print using blue or black ink. This request must be authorized by your employer. Please forward this form

Percent of Employees Waiving Coverage 27.0% 30.6% 29.1% 23.4% 24.9%

Number of Health Plans Reported 18,186 3,561 681 2,803 3,088 Offer HRA or HSA 34.0% 42.7% 47.0% 39.7% 35.0% Annual Employer Contribution $1,353 $1,415 $1,037 $1,272 $1,403 Percent of Employees Waiving

Number of Health Plans Reported 18,186 3,561 681 2,803 3,088 Offer HRA or HSA 34.0% 42.7% 47.0% 39.7% 35.0% Annual Employer Contribution $1,353 $1,415 $1,037 $1,272 $1,403 Percent of Employees Waiving

Final Paycheck Laws by State

ALABAMA AL No Provision No Provision ALASKA AK 23.05.140(b) ARIZONA AZ Ariz. Rev. Stat. 23-350, 23-353 ARKANSAS AR Ark. Code Ann. 11-4-405 CALIFORNIA CA Cal. Lab. Code 201 to 202, 227.3 COLORADO CO Colo.

ALABAMA AL No Provision No Provision ALASKA AK 23.05.140(b) ARIZONA AZ Ariz. Rev. Stat. 23-350, 23-353 ARKANSAS AR Ark. Code Ann. 11-4-405 CALIFORNIA CA Cal. Lab. Code 201 to 202, 227.3 COLORADO CO Colo.

Application Trade Credit Insurance Multi Buyer

Chubb Global Markets Political Risk & Credit 1133 Avenue of the Americas New York, NY 10036 (212) 835-3138 (NY) (312) 612-8827 (Chicago) (213) 612-5512 (Los Angeles) Application Trade Credit Insurance

Chubb Global Markets Political Risk & Credit 1133 Avenue of the Americas New York, NY 10036 (212) 835-3138 (NY) (312) 612-8827 (Chicago) (213) 612-5512 (Los Angeles) Application Trade Credit Insurance

Domestic violence funding reduced from $1,253,000 to $1,000,000. $53,000 to fund elder law hotline eliminated.

Court Fees and Fines and State Appropriations by State* 2009-10 Amounts, Major Changes from 2009 Legislative Sessions Noted Revised 3/8/10 (**See note below related to court fees and fines) State Court

Court Fees and Fines and State Appropriations by State* 2009-10 Amounts, Major Changes from 2009 Legislative Sessions Noted Revised 3/8/10 (**See note below related to court fees and fines) State Court

The State of Children s Health

Figure 0 The State of Children s Health Robin Rudowitz Principal Policy Analyst Kaiser Commission on NCSL Annual Meeting Boston, MA August 8, 2007 Figure 1 SCHIP Builds on Medicaid for Children s Coverage

Figure 0 The State of Children s Health Robin Rudowitz Principal Policy Analyst Kaiser Commission on NCSL Annual Meeting Boston, MA August 8, 2007 Figure 1 SCHIP Builds on Medicaid for Children s Coverage

kaiser medicaid and the uninsured commission on The Cost and Coverage Implications of the ACA Medicaid Expansion: National and State-by-State Analysis

kaiser commission on medicaid and the uninsured The Cost and Coverage Implications of the ACA Expansion: National and State-by-State Analysis Executive Summary John Holahan, Matthew Buettgens, Caitlin

kaiser commission on medicaid and the uninsured The Cost and Coverage Implications of the ACA Expansion: National and State-by-State Analysis Executive Summary John Holahan, Matthew Buettgens, Caitlin

Just The Facts: On The Ground SIF Utilization

Just The Facts: On The Ground SIF Utilization The Access 4 Learning Community (A4L), previously the SIF Association, has changed its brand name due to the fact that the majority of its 3,000 members represent

Just The Facts: On The Ground SIF Utilization The Access 4 Learning Community (A4L), previously the SIF Association, has changed its brand name due to the fact that the majority of its 3,000 members represent

SCHIP: Let the Discussions Begin

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

MEMORANDUM. SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08

MEMORANDUM TO: FROM: HR Investment Center Members Matt Cinque, Managing Director DATE: March 12, 2009 SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08 Please find enclosed the

MEMORANDUM TO: FROM: HR Investment Center Members Matt Cinque, Managing Director DATE: March 12, 2009 SUBJECT: Benchmarks for the Second Half of 2008 & 12 Months Ending 12/31/08 Please find enclosed the

Life After Wayfair - MSATA 2018 Annual Meeting

Life After Wayfair - MSATA 2018 Annual Meeting Panel Doug Schinkel, Director, Business Tax Division South Dakota Department of Revenue Adam Krupp, Commissioner Indiana Department of Revenue Maria Sanders,

Life After Wayfair - MSATA 2018 Annual Meeting Panel Doug Schinkel, Director, Business Tax Division South Dakota Department of Revenue Adam Krupp, Commissioner Indiana Department of Revenue Maria Sanders,

Highlights. Percent of States with a Decrease in MH Expenditures from Prior Year: FY2001 to 2010

FY 2010 State Mental Health Revenues and Expenditures Information from the National Association of State Mental Health Program Directors Research Institute, Inc (NRI) Sept 2012 Highlights SMHA Funding

FY 2010 State Mental Health Revenues and Expenditures Information from the National Association of State Mental Health Program Directors Research Institute, Inc (NRI) Sept 2012 Highlights SMHA Funding

Supplemental Nutrition Assistance Program (SNAP) Preliminary Authorization of Food Purchasing and Delivery Services for the Elderly or Disabled

Preliminary Authorization of Food Purchasing and Delivery Services for the Elderly or Disabled") Food and Nutrition Service (FNS) Supplemental Nutrition Assistance Program (SNAP) Preliminary Authorization of Food Purchasing and Delivery Services for the Elderly or Disabled Request for Volunteers (RFV)

Food and Nutrition Service (FNS) Supplemental Nutrition Assistance Program (SNAP) Preliminary Authorization of Food Purchasing and Delivery Services for the Elderly or Disabled Request for Volunteers (RFV)

Sub Plan number. area code

617 Request for Unforeseeable Emergency Withdrawal MTA 457 Plan Instructions Please print using blue or black ink. Send completed form to the following address or fax it to 1-866-439-8602. If faxing, please

617 Request for Unforeseeable Emergency Withdrawal MTA 457 Plan Instructions Please print using blue or black ink. Send completed form to the following address or fax it to 1-866-439-8602. If faxing, please

The 2018 National Multistate Tax Symposium Take the lead Tax reform and fortifying state positions. February 7-9, 2018

The 2018 National Multistate Tax Symposium Take the lead Tax reform and fortifying state positions February 7-9, 2018 Planning for future-state taxation regimes And the future state Scott Schiefelbein,

The 2018 National Multistate Tax Symposium Take the lead Tax reform and fortifying state positions February 7-9, 2018 Planning for future-state taxation regimes And the future state Scott Schiefelbein,

Medicare Alert: Temporary Member Access

Medicare Alert: Temporary Member Access Plan Sponsor: Coventry/Aetna Medicare Part D Effective Date: Jan. 12, 2015 Geographic Area: National If your pharmacy is a Non Participating provider in the Aetna/Coventry

Medicare Alert: Temporary Member Access Plan Sponsor: Coventry/Aetna Medicare Part D Effective Date: Jan. 12, 2015 Geographic Area: National If your pharmacy is a Non Participating provider in the Aetna/Coventry

Current Trends in the Medicaid RFP Procurement Landscape

Current Trends in the Medicaid RFP Procurement Landscape This is a Presentation Subtitle PRESENTED BY: Michael Lutz Avalere Health October 31, 2017 About Us Michael Lutz Vice President mlutz@avalere.com

Current Trends in the Medicaid RFP Procurement Landscape This is a Presentation Subtitle PRESENTED BY: Michael Lutz Avalere Health October 31, 2017 About Us Michael Lutz Vice President mlutz@avalere.com

BY THE NUMBERS 2016: Another Lackluster Year for State Tax Revenue

BY THE NUMBERS 2016: Another Lackluster Year for State Tax Revenue Jim Malatras May 2017 Lucy Dadayan and Donald J. Boyd 2016: Another Lackluster Year for State Tax Revenue Lucy Dadayan and Donald J. Boyd

BY THE NUMBERS 2016: Another Lackluster Year for State Tax Revenue Jim Malatras May 2017 Lucy Dadayan and Donald J. Boyd 2016: Another Lackluster Year for State Tax Revenue Lucy Dadayan and Donald J. Boyd

State, Local and Net Tuition Revenue Supporting General Operating Expenses of Higher Education, U.S., Fiscal Year 2010, Current (unadjusted) Dollars

Dollars") State, Local and Net Tuition Revenue Supporting General Operating Expenses of Higher Education, U.S., Fiscal Year 2010, Current (unadjusted) Dollars Net Tuition $51.3 Billion 37% All State Support $73.7

State, Local and Net Tuition Revenue Supporting General Operating Expenses of Higher Education, U.S., Fiscal Year 2010, Current (unadjusted) Dollars Net Tuition $51.3 Billion 37% All State Support $73.7

Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston

The Growing Instability of Revenues over the Business Cycle: Putting the New England States in Perspective Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston Lincoln Institute

The Growing Instability of Revenues over the Business Cycle: Putting the New England States in Perspective Yolanda K. Kodrzycki New England Public Policy Center Federal Reserve Bank of Boston Lincoln Institute

2018 ADDENDUM INSTRUCTIONS

2018 ADDENDUM INSTRUCTIONS FEBRUARY 22, 2019 UPDATE: 2018 MUNICIPAL REFERENCE BOOK 1. DELAWARE funds are listed on page 15. You may note on page 15 to see the addendum for additional Delaware funds. The

2018 ADDENDUM INSTRUCTIONS FEBRUARY 22, 2019 UPDATE: 2018 MUNICIPAL REFERENCE BOOK 1. DELAWARE funds are listed on page 15. You may note on page 15 to see the addendum for additional Delaware funds. The

Introduction to Washington Business Taxes

Introduction to Washington Business Taxes Washington State Department of Revenue Maureen O Connell, September 30, 2017 Objectives Provide information on major taxes in Washington Provide helpful contacts

Introduction to Washington Business Taxes Washington State Department of Revenue Maureen O Connell, September 30, 2017 Objectives Provide information on major taxes in Washington Provide helpful contacts