Intermediate (IPC) Course Paper 1: Accounting Chapter 2: Financial Statements of Companies CA. Pankajj Goel

|

|

|

- Suzanna Green

- 5 years ago

- Views:

Transcription

1 Intermediate (IPC) Course Paper 1: Accounting Chapter 2: Financial Statements of Companies CA. Pankajj Goel The Institute of Chartered Accountants of India Recorded on: 24-October-2014

2 1 This lecture has been delivered by faculty members to supplement the Study Material, Practice Manual and other content 2 3 The views expressed in this lecture are of the Faculty Member. The content of this video lecture has not been specifically discussed by the Council of the Institute or any of its Committees and the views expressed herein may not be taken to necessarily represent the views of the Council or any of its committees 2

3 Students are advised to refer to e-lectures available on the Students LMS for this and other topics Free Access Register with your Student Registration Number and Start learning immediately 3

4 This e-lecture was Recorded on: October 24, 2014 The e-lectures, PPT, Podcasts and Video lectures on ICAI Cloud Campus aim to supplement the Study Material, Practice Manual and Supplementary Study Material The lecture recordings are made according to the syllabus and laws existing/ applicable as on the date of recording. Due to changes in law, there is likely to be some time gap between these changes and the recording of updated lectures. Hence, students are advised to refer to the Study Material including Supplementary Study Material, if any, and other relevant legislation for latest provisions/ amendments required for forthcoming examination. 4

5 Shares can be issued at discount with some conditions (sec 79) No Preference shares can be issued if redemption period is more than 20 years Specific percentage of profit to transfer to reserve. No shares can be issued at discount except sweat equity shares (sec 53) Preference shares can be issued if redemption period is more than 20 years.( infrastructure case) No specific percentage required to transfer to general reserve. 5

6 Concept1:Adjustments for Dividend Concept2:Managerial Remuneration Concept3:Adjustments for Taxation Concept4:Preparation of Final Accounts as per Schedule III(Earlier revised Schedule VI) 6

7 An Intro. 7

8 Section 51:Payment of dividend in proportion to amount paid-up.a company may, if so authorised by its articles, pay dividends in proportion to the amount paid-up on each share Section 123:company may, before the declaration of any dividend in any financial year, transfer such percentage of its profits for that financial year as it may consider appropriate to the reserves of the company: The Board of Directors of a company may declare interim dividend during any financial year out of the surplus in the profit and loss account and out of profits of the financial year in which such interim dividend is sought to be declared The Board of Directors of a company may declare interim dividend during any financial year out of the surplus in the profit and loss account and out of profits of the financial year in which such interim dividend is sought to be declared 8

9 Dividend can be declared only on the recommendation of the Board of Directors of the Company. The shareholders do not have any power to declare any dividend. The Board of Directors after considering and approval of the financial statements of the Company, determines the rate of dividend to be declared and then recommends the same to the shareholders. For this purpose, a Board Meeting shall be convened to pass the resolution for Rate of dividend and the amount of dividend to be paid. Book closure date for dividend purposes Date of annual general meeting Bank with which the account shall be opened for the purpose of remittance of dividend. 9

10 Profit & Loss Appropriation A/c/Surplus A/c Dr. To Proposed Dividend-Preference To Proposed Dividend-Equity To Corporate Dividend Tax-Equity & Preference 10

11 Proposed Dividend A/c Dr To Dividend Payable A/c 11

12 The dividend recommended by the Board of Directors is declared by a resolution passed at the Annual General Meeting by the shareholders. The declaration of dividend should form part of an ordinary business item to be transacted in the notice of the Annual General Meeting. While approving the rate of dividend at the Annual General Meeting, the shareholders have power to declare a lower rate of dividend than what is recommended by the Board but they have no power to increase the amount or the rate of dividend so recommended by the Board of Directors. Dividend when declared becomes debt against the company 12

13 Step 3- Open New Bank Account So That Money Is Not Used For Any Other Purpose. This Is Like Transferring From SBI TO PNB DIVIDEND BANK A/C DR TO BANKA/C DIVIDEND 13

14 The Company should deposit the dividend amount ( including interim dividend) within 5 days of its declaration in the separate bank account opened for this purpose. It means that the interim dividend will have to be deposited in a bank account within 5 days of the Board Meeting whereas final dividend will have to be deposited within 5 days from the date of Annual General Meeting in which it was approved by the shareholders. Also Section 205 (1B) stipulates that the amount so deposited shall be used only for the purpose of payment of dividend ( whether interim or final). 14

15 Rate of dividend is calculated on paid up capital but transfer to reserve is calculated on PAT. Subject to Rules to be prescribed, dividend can be paid out of accumulated reserves without restrictions as to rate of dividend As per The companies Act 2013, companies are free to transfer any or no amount to it s reserves.mandatory transfer of profits to reserves before declaration of dividend done away with. Companies may voluntarily transfer a portion of its profits to reserves Dividend to be paid out of profits of the company for the year after providing for depreciation; or profits of the previous years arrived at after providing for depreciation and remaining undistributed; or both of the above 15

16 Dividend to be distributed within 30 days of its declaration in cash only. Dividend cannot be distributed in kind. Where unpaid / unclaimed dividend has been transferred to IEPF, the corresponding shares on which such dividend was unpaid / unclaimed shall also be transferred by the company to IEPF 16

17 STEP 4- ISSUE CHEQUE FOR PAYMENT OF DIVIDEND DIVIDEND PAYABLE a/c DR TO DIVIDEND BANK A/C DIVIDEND 17

18 Concept 2:MANAGERIAL REMUNERATION 18

19 Remuneration in case of nil or inadequate profits.(section II) Remuneration in case of adequate or sufficient profits. (section I)

20 Remuneration may be paid by way of salary, dearness allowance, perquisites or any other allowances not exceeding the ceiling limit of : Rs 24,00,000 per annum or 2,00,000 per month. Rs48,00,000 per annum or 4,00,000 per month.

21 Effective capital i. Less than Rs.1 crore ii. Rs. 1 crore or more but less than 5 crores iii. Rs. 5 crores or more but less than 25 crores iv. Rs 25 crores or more but less than 50 crores Maximum remuneration payable per month 75,000 1,00,000 1,25,000 1,50,000

22 iv. Rs.50 crores or more but less than 100 crores 1,75,000 v. Rs100 crores or more 2,00,000

23 Effective capital i. Less than Rs. 1 crore. ii. Rs 1 crore or more but less than 5 crores iii. Rs 5 crores or more but less than 25 crores iv. Rs 25 crores or more but less than 50 crores Maximum remuneration payable per month 1,50,000 2,00,000 2,50,000 3,00,000

24 v. Rs. 50 crores or more but less than 100 crores. vi. Rs. 100 crores or more 3,50,000 4,00,000

25 Maximum Limit Section 198 of the companies act, 1956 puts a maximum limit of 11% of the net profits in any financial year on the managerial remuneration payable by a public company or a private company which is a subsidiary of a public company to it s directors including any managing or whole time director or manager Minimum Limit if in any financial year a company has no profits or its profits are inadequate, the company shall not pay to its directors including any managing or whole time director or manager, by way of remuneration any sum except with the previous approval of the central government. 25

26 Total of : Paid -up share capital(excluding share application money or advances) Share premium account balance Reserves and surplus (excluding revaluation reserve) Long-term loans and deposits repayable after 1 year(excluding working capital loans, overdrafts, interest due on loans unless funded, bank guarantee etc. and other short -term advances)

27 Less: Investment(except investment by an investment company) Accumulated losses Preliminary expenses (not written off).

28 But except with the previous approval of the central government the remuneration shall not exceed: Ø If one whole time director : 5% Ø If More than one whole time director : 10% Ø If only part time directors : 3% Ø If part time directors as well as whole time directors and managers 11% 28

29 Public company-limit if Adequate Profit Overall managerial remuneration not to exceed 11% of the Net Profit of the F.Y. MD/WTD: 5% of NP if one. 10% of NP if more than one. Manager: 5% of NP Other directors 1% of NP if company has MD/WTD/Manager 3% of NP if company has no MD/WTD/Manager In all the above cases the approval of central government is required if the company wants to exceed the above limit. 29

30 Net profit for the purpose of calculation of Managerial Remuneration Net profit as per P & L account xxxx Add: ALL Provisions including reserves made in books xxxx Add: Managerial remuneration (if debited to P & L account) xxxx Add: Depreciation charged in books xxxx Less: Depreciation as per schedule iv xxxx Less: Actual expenditures (not debited to P&L account) xxxx Book profit xxxx 30

31 The Manager of LIBERTY LTD. is entitled to get a salary of Rs per month plus 1% commission on the net profits of the company after such salary and commission. The following is the profit and loss account of the company for the year ended 31st March,2014:

32 To salaries and wages 1,92,500 By gross profit b/d 11,70,000 To general expenses 74,000 By subsidy from govt. 60,000 To depreciation 82,000 By profit on sale of assets(cost price Rs.2,50,000 and WDV Rs. 1,80,000) To expenditure on scientific research 14,000 To manager s salary 3,00,000 To commission to manager(on account) 6,000 To reserve for bad debts 17,500 To provision for tax 2,40,000 To proposed dividend 1,00,000 To balance c/d 3,04,000 1,00,000 13,30,000 13,30,000

33 Calculation of net profit for the purpose of calculation of managerial remuneration: Net profit as per Statement of Profit and Loss Add: Items to be added back- proposed dividend 1,00,000 provision for taxation 2,40,000 reserve for bad debts 17,500 commission to manager (on account) 6,000 expenditure on scientific research 14,000 depreciation (as per schedule IV) 1,000

34 Less : Items to be deducted Profit on sale of fixed asset 30,000 Net profit for the purpose of managerial calculation 6,52,500 Manager s commission 6,460 Less: advance paid on account of commission 6000 Amount still payable to manager 460

35 Profit on sale: 1 Book value=original cost-accumulated depreciation 1,80,000=2,50,000-accumulated depreciation Accumulated depreciation=70,000 2 Selling price-book value=+profit/-loss Selling price-1,80,000=1,00,000 Selling price=2,80,000

36 Manager s commission=(net profit x rate)/100+rate Manager s commission =( x 1)/101 Manager s commission =6460

37 Provision of tax for the year P&L Account Dr To Provision for Taxation Payment of Advance tax during the year Advance tax account Dr To Bank account 37

38 The trial balance of Mona Creations Ltd. as at 31 March 2014 shows the following terms : Debit Credit Rs. Rs. Provision for taxation 5,40,000 Advance Payment of Tax 10,50,000 38

39 You are also given the following information : (i) Advance payment of tax includes Rs. 6,20,000 for (ii) Assessment for is completed in and the actual tax liability amounts to Rs. 6,45,000 and no payment has been made so far for the same (iii) For the financial year , provision for income tax required is Rs. 7,50,000. Make journal entries and prepare the various ledger accounts affected. 39

40 1. Profit and Loss Account Dr. 1,05,000 To Provision for Taxation Account 1,05,000 (Being the additional amount for tax appropriated on completion of the assessment for ) 2. Provision for Taxation Account Dr. 6,45,000 To Advance Tax Account 6,20,000 To Liability for Taxation Account 25,000 (Provision for taxation adjusted against advance tax and balance transferred to liability for taxation account) 3. Profit and Loss Account Dr. 7,50,000 To Provision for Taxation Account 7,50,000 (Estimated tax liability for provided) 40

41 Ledger Accounts Provision for taxation Account Rs Liability for taxation account Balance c/d 7,50,000 Rs. 5,40,000 Balance b/d 5,40, Profit and loss account(estimate liability for 13-14) 7,50,000 12,90,000 12,90,000 41

42 Advance tax Account Rs Balance b/d 6,20,000 Liability for taxation Account Rs. 6,20,000 To Bank 4,30,000 Balance c/d 4,30,000 10,50,000 10,50,000 Liability for taxation Account Advance tax Account 6,20,000 By P&L(Bal) Balance c/d 25,000 Provision for taxation 5,40,000 42

43 43

44 Every balance sheet shall be in the form set out in Part I of Schedule III Every profit and loss account shall comply with the requirements of Part II of Schedule III These sub-sections are not applicable to banking co., insurance co. and companies engaged in generation and supply of electricity.

45 General Instructions Part 1 Form of Balance Sheet General Instructions for preparation of Balance Sheet Part 2 Form of Statement of Profit and loss General Instructions for preparation of Statement of Profit and Loss

46 For Balance sheet only vertical format is available. Format of Profit and Loss Account is also available now. Part III Interpretation- containing explanation of provisions, reserve etc. is not given now. Part IV- Balance sheet Abstract and Co s General Business Profile is not required to be given.

47 Rounding off conditions-turnover -Rounding off < Rs. 100 crores-to the nearest hundreds, thousands, lakhs or millions, or decimals thereof. > = Rs. 100 crores-to the nearest, lakhs, millions or crores, or decimals thereof.

48 Particulars Note No. Figures as at the end of the current reporting period Figures as at the end of the previous reporting period I. EQUITY AND LIABILITIES (1) Shareholders Funds (2) Share application money pending allotment (3) Non-current liabilities (4) Current Liabilities II. ASSETS TOTAL (1) Non-current assets (2) Current assets TOTAL

49 Particulars Note No. Figures as at the end of the current reporting period Figures as at the end of the previous reporting period I. EQUITY AND LIABILITIES (1) Shareholders Funds 1 (a) share capital 2 (b) Reserve and Surplus (c) Money received against share warrants (2) Share application money pending allotment 3 (3) Non-current liabilities (a) Long term borrowings (b) Deferred tax liabilities (net) (c) Other long term liabilities (d) Long term provisions (4) Current Liabilities (a) Short term borrowings (b) Trade payables (c) Other current liabilities (d) Short term provisions TOTAL

50 Criteria to be met to classify as current liability: Expected to be settled in the co s normal operating cycle, Due to be settled within twelve months after the reporting date, Held primarily for the purpose of being traded or There is no unconditional right to defer settlement for at least 12 months after the reporting date. Operating cycle time between the acquisition of assets for processing and their realisation in cash or cash equivalents. If can not be identified- duration of twelve months. All other liabilities are classified as non-current liabilities.

51 Particulars Note No. Figures as at the end of the current reporting period Figures as at the end of the previous reporting period II. ASSETS (1) Non-current assets (a) fixed assets (i) Tangible assets (ii) Intangible assets (iii) Capital work-in-progress (iv) Intangible assets under development (b) Non- current investments 13 (c) Deferred tax assets (Net) (d) Long term loans and advances (e) Other non-current assets (2) Current assets (a) Current investments (b) Inventories (c) Trade receivables (d) Cash and cash equivalents (e) Short term loans and advances (f) Other current assets TOTAL

52 Criteria to be met to classify as current asset: Expected to be realise in or intended for sale or consumption in normal operating cycle of the co., Held primarily for the purpose of trading, Expected to be realised within 12 months from the closing date or It is cash or cash equivalent. Operating cycle time between the acquisition of assets for processing and their realisation in cash or cash equivalents. If can not be identified- duration of twelve months. All other assets shall be classified as non-current.

53 Particulars Note For the For the No. Current year Last year I. Revenue from operations XXX XXX II. Other income XXX III. Total Revenue (I + II) XXX IV. Expenses: Cost of materials consumed XXX XXX Purchases of Stock-in-Trade XXX XXX Changes in inventories of finished goods, WIP and Stock-in-Trade XXX XXX Employee benefits expense XXX XXX Finance costs XXX XXX Depreciation and amortization expense XXX XXX Other expenses XXX XXX Total expenses XXX XXX V. Profit before exceptional and extraordinary items and tax (III-IV) XXX XXX VI. Exceptional items XXX XXX VII. Profit before extraordinary items and tax (V - VI) XXX XXX VIII. Extraordinary Items XXX XXX IX. Profit before tax (VII- VIII) XXX XXX X. Tax expense: (1) Current tax XXX XXX (2) Deferred tax XXX XXX XI. Profit (Loss) for the period from continuing operations (VII-VIII) XXX XXX XII Profit/(loss) from discontinuing operations XXX XXX XIII. Tax expense of discontinuing operations XXX XXX XIV. Profit/(loss) from Discontinuing operations (after tax) (XII-XIII) XXX XXX XV. Profit (Loss) for the period (XI + XIV) XXX XXX

54 (i) Cost of material consumed (ii) Purchase of stock-in-trade (iii) Changes in inventories of finished goods,work-in-progress and stock in trade (iv) Employee benefit expenses (v) Finance cost (vi) Depreciation and amortisation expenses (vii)other expenses.

55 In respect of contingent liabilities Claims against the co not acknowledged as debts Guarantees Other moneys for which co is contingently liable In respect of commitments Estimated amount of contracts remaining to be executed on capital account and not provided for Uncalled liability on shares and other investments partly paid Other commitments

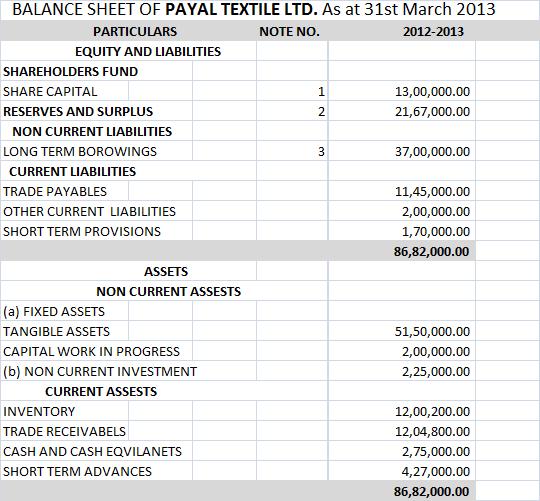

56 1. Prepare the Balance Sheet of Payal Textiles Ltd. as required under Schedule III of the Companies Act, 2013, as on 31 March Following balances are given : NTM Accounts Dr. Cr. Secured Term Loans 10,00,000 Creditors 11,45,000 6% Debentures Account 27,00,000 Provision for Tax 1,70,000 Share Premium Account 4,75,000 General Reserves 20,50,000 Loans from Debtors 2,00,000 Provision for (Doubtful) Debts 20,200 Provision for Depreciation 5,00,000 Equity Share Capital (30,000 10) 3,00,000 8% Preference Share Capital (10, ) 10,00,000 Advances given 3,72,000 Advances to staff 55,000 Cash and Bank 2,75,000 Loose Tools 50,000 Investments 2,25,000 Profit and Loss Account (Losses) 3,00,000 Debtors 12,25,000 Miscellaneous Expenditure 58,000 Stores Items 4,00,000 Fixed Assets 56,50,000 Capital Work-in-Progress 2,00,000 Finished Goods Stock 7,50,200 Rs. Rs. 95,60,200 95,60,200 56

57 57

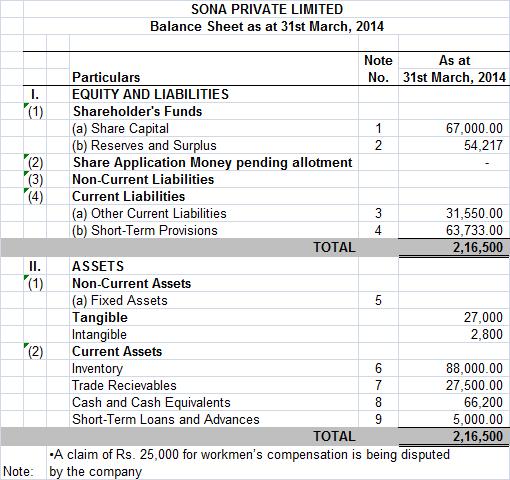

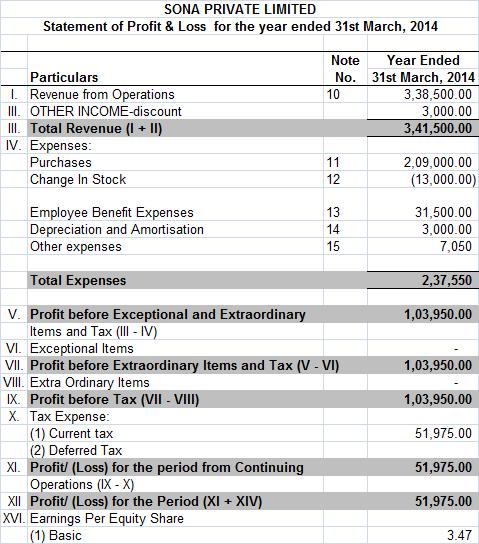

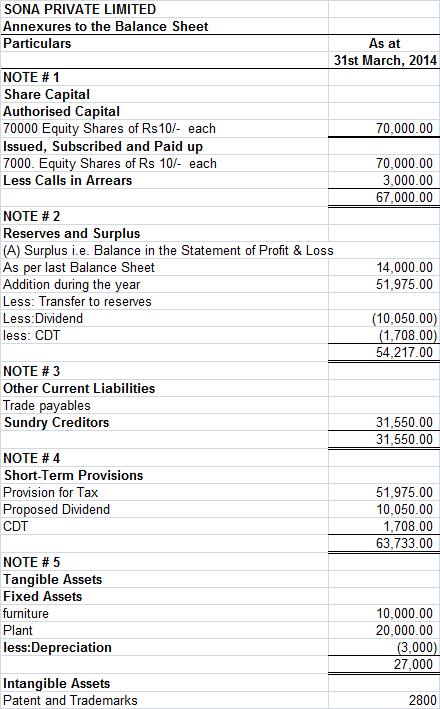

58 The following is the trial balance of SONA Ltd. as at 31 March, 2014: Rs. Rs. Stock, 1 April, ,000 Purchases returns 10,000 Purchases and sales 2,19,000 3,40,000 Sales Returns 1500 Wages Discount 3,000 Furniture and fittings 10,000 Salaries 4,500 Advance Tax 5000 Bad Debts 4,050 Preliminary Expenses 3000 Profit and loss appropriation account, 31 March ,000 Share capital 70,000 Calls In arrears 3000 Debtors and creditors 27, Plant and machinery 20,000 Cash at bank 66,200 Patents and trade marks 2,

59 Prepare Statement of Profit and Loss and profit and loss appropriation account for the year ended 31 March, 2014 and a balance sheet at that date. Take into consideration the following adjustments: a) Stock on 31 March, 2014 was valued at Rs. 88,000. b) Make a provision for income 50%. c) Depreciate plant and 15%, d) The Directors propose a 15% per annum for the year ended 31 March, 2009 e) A claim of Rs. 25,000 for workmen s compensation is being disputed by the company 59

60 60

61 61

62 , Nov-14 62

63 63

64 64

65

26 th Regional Conference of WIRC. Revised Schedule VI. CA N. Venkatram 16th December, 2011

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

situations Remuneration in case of adequate or sufficient profits. (section I) Remuneration in case of nil or inadequate profits.

Remuneration in case of nil or inadequate profits.") INTRODUCTION Section I/II of part II of schedule XIII of the companies act deals. According to section 198 of the Companies Act 1956 total remuneration to be paid to directors, manager and managing director

INTRODUCTION Section I/II of part II of schedule XIII of the companies act deals. According to section 198 of the Companies Act 1956 total remuneration to be paid to directors, manager and managing director

Revised Schedule VI. By: Purushottam Nyati Mukul Rathi. July 27, Page 1

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

Financial Statements of Companies

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

REVISED OUTLINE GUIDANCE NOTES

REVISED OUTLINE GUIDANCE NOTES regarding adoption of Schedule VI to the Companies Act 1956 in the subject of ACCOUNTANCY Class XII For the Board Examination, March 2014 1 CONTENT Chapter 1: GENERAL INTRODUCTION

REVISED OUTLINE GUIDANCE NOTES regarding adoption of Schedule VI to the Companies Act 1956 in the subject of ACCOUNTANCY Class XII For the Board Examination, March 2014 1 CONTENT Chapter 1: GENERAL INTRODUCTION

Welcome to Presentation on preparation of financial statements under revised schedule VI. K.Chandra Sekhar Company Secretary Ace Designers Limited

Welcome to Presentation on preparation of financial statements under revised schedule VI K.Chandra Sekhar Company Secretary Ace Designers Limited 1 Relevant provisions Indian Companies Act, 1956 Rules

Welcome to Presentation on preparation of financial statements under revised schedule VI K.Chandra Sekhar Company Secretary Ace Designers Limited 1 Relevant provisions Indian Companies Act, 1956 Rules

Outline Guidance Notes regarding adoption of CLASS XII Revised Schedule VI to the Companies Act 1956 in the subject of Accountancy (Effective for Board Examination 2013) Shiksha Kendra, 2, Community Centre,

Outline Guidance Notes regarding adoption of CLASS XII Revised Schedule VI to the Companies Act 1956 in the subject of Accountancy (Effective for Board Examination 2013) Shiksha Kendra, 2, Community Centre,

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

PAPER 5 : ADVANCED ACCOUNTING

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

Reporting Under Revised Schedule VI of. A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA

CA AKSHAY K GUPTA") Reporting Under Revised Schedule VI of Companies Act 1956 A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA 1 The Ministry of Corporate Affairs (MCA) on Tuesday, the 1st day of March notified

Reporting Under Revised Schedule VI of Companies Act 1956 A Comparative Study- Old v/s Revised(2011) CA AKSHAY K GUPTA 1 The Ministry of Corporate Affairs (MCA) on Tuesday, the 1st day of March notified

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION A. Applicable for November, 2015 examination (i) Companies Act, 2013 (ii) The relevant

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION A. Applicable for November, 2015 examination (i) Companies Act, 2013 (ii) The relevant

Hire Purchase and Instalment Sale Transactions Part 2

Recording Date: September 16, 2015 CA Intermediate (IPC) Course Paper 1 Accounting Chapter 11 Hire Purchase and Instalment Sale Transactions Part 2 CA. Mayur Toshniwal The Institute of Chartered Accountants

Recording Date: September 16, 2015 CA Intermediate (IPC) Course Paper 1 Accounting Chapter 11 Hire Purchase and Instalment Sale Transactions Part 2 CA. Mayur Toshniwal The Institute of Chartered Accountants

Company Accounts. iii. Need to reduce risks for non-corporate forms of organisations (sole proprietor, partnership or HUF),

,") Company Accounts With i. Increasing scale of operations ii. Increasing capital requirements iii. Need to reduce risks for non-corporate forms of organisations (sole proprietor, partnership or HUF), A relatively

Company Accounts With i. Increasing scale of operations ii. Increasing capital requirements iii. Need to reduce risks for non-corporate forms of organisations (sole proprietor, partnership or HUF), A relatively

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING

: GROUP I PAPER 1: ACCOUNTING") MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING 1 Test Series: March, 2018 SUGGESTED ANSWERS/HINTS 1. (a) Constructing or acquiring a new asset may result in incremental costs that would

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING 1 Test Series: March, 2018 SUGGESTED ANSWERS/HINTS 1. (a) Constructing or acquiring a new asset may result in incremental costs that would

Part A (DD/MM/YYYY) (a)* Date of Board of Directors' meeting in which consolidated financial statements were approved

(a)* Date of Board of Directors' meeting in which consolidated financial statements were approved") FORM NO. AOC-4 CFS [Pursuant to section 137 of the Companies Act, 2013 and Rule 12 of Companies (Accounts) Rules, 2014] Form for filing consolidated financial statements and other documents with the Registrar

FORM NO. AOC-4 CFS [Pursuant to section 137 of the Companies Act, 2013 and Rule 12 of Companies (Accounts) Rules, 2014] Form for filing consolidated financial statements and other documents with the Registrar

MODEL TEST PAPER 12 (Solution)

") MODEL TEST PAPER 12 (Solution) SECTION A PART I 1. (i) (a) Share of Existing Goodwill written off. (b) Share of Loss up to the date of retirement. (c) Share of Accumulated Losses up to the date of retirement.

MODEL TEST PAPER 12 (Solution) SECTION A PART I 1. (i) (a) Share of Existing Goodwill written off. (b) Share of Loss up to the date of retirement. (c) Share of Accumulated Losses up to the date of retirement.

FINAL CA May 2018 Financial Reporting

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

UNIT 4 : AMALGAMATION AND RECONSTRUCTION

Company Accounts 3.1 UNIT 4 : AMALGAMATION AND RECONSTRUCTION (A) Write short notes on : Question 1 Amalgamation and Absorption of companies a comparison.(3 marks)(intermediate Nov. 1994) Answer In accounting

Company Accounts 3.1 UNIT 4 : AMALGAMATION AND RECONSTRUCTION (A) Write short notes on : Question 1 Amalgamation and Absorption of companies a comparison.(3 marks)(intermediate Nov. 1994) Answer In accounting

16. COMPANY FINAL ACCOUNTS

16. COMPANY FINAL ACCOUNTS SOLUTIONS TO ASSIGNMENT PROBLEMS PROBLEM NO.1 Journal Entries in the Books of CODIG Ltd. Date Debit Credit 31.03.03 Profit and Loss A/c Dr. To Provision for Income Tax A/c (Being

16. COMPANY FINAL ACCOUNTS SOLUTIONS TO ASSIGNMENT PROBLEMS PROBLEM NO.1 Journal Entries in the Books of CODIG Ltd. Date Debit Credit 31.03.03 Profit and Loss A/c Dr. To Provision for Income Tax A/c (Being

Paper-5: FINANCIAL ACCOUNTING

Paper5: FINANCIAL ACCOUNTING Time Allowed: 3 Hours Full Marks : 100 Whenever necessary, suitable assumptions should be made and indicate in answer by the candidates. Working Notes should be form part of

Paper5: FINANCIAL ACCOUNTING Time Allowed: 3 Hours Full Marks : 100 Whenever necessary, suitable assumptions should be made and indicate in answer by the candidates. Working Notes should be form part of

Analysis of Financial Statement & Cash Flow Statements

Analysis of Financial Statement & Cash Flow Statements Q.1 ow are the various activities classified according to AS-3 (Revised) while preparing the Cash Flow Statement? While preparing the cash flow statement

Analysis of Financial Statement & Cash Flow Statements Q.1 ow are the various activities classified according to AS-3 (Revised) while preparing the Cash Flow Statement? While preparing the cash flow statement

REVISED SCHEDULE VI Detailed Analysis with Practical Approach

REVISED SCHEDULE VI Detailed Analysis with Practical Approach By: 28.04.2012 1 SESSION I: o EXISTING PROVISIONS o REVISED SCHEDULE VI o AN OVERVIEW o OVERALL APPROACH o KEY CHANGES B/S o KEY CHANGES P&L

REVISED SCHEDULE VI Detailed Analysis with Practical Approach By: 28.04.2012 1 SESSION I: o EXISTING PROVISIONS o REVISED SCHEDULE VI o AN OVERVIEW o OVERALL APPROACH o KEY CHANGES B/S o KEY CHANGES P&L

SEGMENT- I: INFORMATION AND PARTICULARS IN RESPECT OF BALANCE SHEET. From (DD/MM/YYYY) To (DD/MM/YYYY)

To (DD/MM/YYYY)") FORM NO. AOC-4 [Pursuant to section 137 of the Companies Act, 2013 and sub-rule (1) of Rule 12 of Companies (Accounts) Rules, 2014] Form for filing financial statement and other documents with the Registrar

FORM NO. AOC-4 [Pursuant to section 137 of the Companies Act, 2013 and sub-rule (1) of Rule 12 of Companies (Accounts) Rules, 2014] Form for filing financial statement and other documents with the Registrar

Elgi Compressors Italy S.r.l. Balance Sheet As At 31st March 2017

Balance Sheet As At 31st March 2017 Particulars Note March 31, 2017 March 31, 2016 Non Current Assets Property, Plant and Equipment 3 127,486,695 145,048,621 Capital work-in-progress 3 - Investment Property

Balance Sheet As At 31st March 2017 Particulars Note March 31, 2017 March 31, 2016 Non Current Assets Property, Plant and Equipment 3 127,486,695 145,048,621 Capital work-in-progress 3 - Investment Property

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

SPC Co. Ltd Sudan BALANCE SHEET AS AT Mar 31, 2016

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 b) Reserves and Surplus 2 (936) (936) (936) (936) 2. Minority Interest 3. Share application

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 b) Reserves and Surplus 2 (936) (936) (936) (936) 2. Minority Interest 3. Share application

CRUSTUM PRODUCTS PRIVATE LIMITED

CRUSTUM PRODUCTS P R I V A T E L I M I T E D Financial Statements 2016-17 1 INDEPENDENT AUDITOR S REPORT To the Members CRUSTUM PRODUCTS PRIVATE LIMITED Report on the Financial Statements We have audited

CRUSTUM PRODUCTS P R I V A T E L I M I T E D Financial Statements 2016-17 1 INDEPENDENT AUDITOR S REPORT To the Members CRUSTUM PRODUCTS PRIVATE LIMITED Report on the Financial Statements We have audited

INTERNAL RECONSTRUCTION

CHAPTER-4 Q. 1. Green Limited had decided to reconstruct the Balance Sheet since it has accumulated huge losses. The following is the summarized Balance Sheet of the Company on 31.3.2012 before reconstruction

CHAPTER-4 Q. 1. Green Limited had decided to reconstruct the Balance Sheet since it has accumulated huge losses. The following is the summarized Balance Sheet of the Company on 31.3.2012 before reconstruction

Model Test Paper - 1 IPCC Gr. I Paper - 1 Accounting Question No. 1 is Compulsory. Attempt any five question from the remaining six question. 1.

Model Test Paper - 1 IPCC Gr. I Paper - 1 Accounting Question No. 1 is Compulsory. Attempt any five question from the remaining six question. 1. (a) M/s Progressive Company Limited has not charged depreciation

Model Test Paper - 1 IPCC Gr. I Paper - 1 Accounting Question No. 1 is Compulsory. Attempt any five question from the remaining six question. 1. (a) M/s Progressive Company Limited has not charged depreciation

RTP_FAC_Inter_Syl08_Dec13. Group I Paper 5 Financial Accounting

Group I Paper 5 Financial Accounting 1. Answer the following questions (give workings): (i) Mukta Ltd. purchased a machine for 40 lakhs including excise duty of 8 lakhs. The excise duty is Cenvatable under

Group I Paper 5 Financial Accounting 1. Answer the following questions (give workings): (i) Mukta Ltd. purchased a machine for 40 lakhs including excise duty of 8 lakhs. The excise duty is Cenvatable under

Revisionary Test Paper_Final_Syllabus 2008_Dec2013

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

*

Solved Ans. Accounts_5 CA IPCC Nov. 2010 1 Attention C.A. Pcc & Ipcc Students Solved Ans. Accounts_5 Ipcc_Nov.10 Keep Watching our website* for further solution. *www.jainclassesonline.com (No.1 Institute

Solved Ans. Accounts_5 CA IPCC Nov. 2010 1 Attention C.A. Pcc & Ipcc Students Solved Ans. Accounts_5 Ipcc_Nov.10 Keep Watching our website* for further solution. *www.jainclassesonline.com (No.1 Institute

Guideline Answers for Accounting Group I

Guideline Answers for Accounting Group I Question 1(a): 5 Marks Heramba Ltd gives you the following information for the year ended 31 st March 20X2: ` Sales for the year ` 48,00,000 (The Company sold goods

Guideline Answers for Accounting Group I Question 1(a): 5 Marks Heramba Ltd gives you the following information for the year ended 31 st March 20X2: ` Sales for the year ` 48,00,000 (The Company sold goods

Answer to MTP_ Intermediate_Syllabus2016_June2018_Set1 Paper 12- Company Accounts & Audit

Paper 12- Company Accounts & Audit DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 12- Company Accounts & Audit Full Marks: 100 Time allowed: 3

Paper 12- Company Accounts & Audit DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 12- Company Accounts & Audit Full Marks: 100 Time allowed: 3

Strides Pharma Namibia BALANCE SHEET AS AT Mar 31, 2016

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 1,777,104 1,777,104 b) Reserves and Surplus 2 (485,737) 1,490,552 1,291,367 3,267,656 2. Share

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 1,777,104 1,777,104 b) Reserves and Surplus 2 (485,737) 1,490,552 1,291,367 3,267,656 2. Share

Strides Pharma Cameroon BALANCE SHEET AS AT Mar 31, 2016

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 10,000,000 10,000,000 b) Reserves and Surplus 2 10,000,000 10,000,000 2. Share application

BALANCE SHEET AS AT Mar 31, 2016 Schedule A. EQUITY AND LIABILITIES 1. Shareholders' funds a) Share capital 1 10,000,000 10,000,000 b) Reserves and Surplus 2 10,000,000 10,000,000 2. Share application

UNIT 1: INTRODUCTION TO COMPANY ACCOUNTS. Understand the reason for the existence and survival of a company.

CHAPTER 10 COMPANY ACCOUNTS UNIT 1: INTRODUCTION TO COMPANY ACCOUNTS LEARNING OUTCOMES After studying this unit, you will be able to: Understand the reason for the existence and survival of a company.

CHAPTER 10 COMPANY ACCOUNTS UNIT 1: INTRODUCTION TO COMPANY ACCOUNTS LEARNING OUTCOMES After studying this unit, you will be able to: Understand the reason for the existence and survival of a company.

Copyright -The Institute of Chartered Accountants of India. The forward contract is sold before its due date, hence considered as speculative.

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

PARTICULARS SCHEDULE As at

CONSOLIDATED BALANCE SHEET As at 30.9.2015 I. EQUITY AND LIABILITIES PARTICULARS SCHEDULE As at (1) SHAREHOLDERS' FUNDS : (A) SHARE CAPITAL 1 500.00 (B) RESERVES AND SURPLUS 2 (4801,09,249.02) (C) MONEY

CONSOLIDATED BALANCE SHEET As at 30.9.2015 I. EQUITY AND LIABILITIES PARTICULARS SCHEDULE As at (1) SHAREHOLDERS' FUNDS : (A) SHARE CAPITAL 1 500.00 (B) RESERVES AND SURPLUS 2 (4801,09,249.02) (C) MONEY

Company Accounts, Cost & Management Accounting 262 PART A

Company Accounts, Cost & Management Accounting 262 : 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 11 NOTE : All working notes should

Company Accounts, Cost & Management Accounting 262 : 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 11 NOTE : All working notes should

ADISONS PRECISION INSTRUMENTS MANUFACTURING COMPANY LIMITED BALANCE SHEET AS AT 31ST MARCH, 2016 ( `.in INR)

") ADISONS PRECISION INSTRUMENTS MANUFACTURING COMPANY LIMITED BALANCE SHEET AS AT 31ST MARCH, 2016 I. EQUITY AND LIABILITIES Particulars Note No 31-03-2016 31-03-2015 (1) SHAREHOLDERS' FUNDS (a) Share Capital

ADISONS PRECISION INSTRUMENTS MANUFACTURING COMPANY LIMITED BALANCE SHEET AS AT 31ST MARCH, 2016 I. EQUITY AND LIABILITIES Particulars Note No 31-03-2016 31-03-2015 (1) SHAREHOLDERS' FUNDS (a) Share Capital

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM. Test Code CIN 5010

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- ADVANCED ACCOUNTS Test Code CIN 5010 Date: 25.08.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- ADVANCED ACCOUNTS Test Code CIN 5010 Date: 25.08.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

PAPER 1 : ACCOUNTING QUESTIONS

PAPER 1 : ACCOUNTING QUESTIONS Profit or Loss Prior to Incorporation 1. A firm which was carrying on business from 1 st January, 2009 gets itself incorporated as a company on 1st May, 2009. The first accounts

PAPER 1 : ACCOUNTING QUESTIONS Profit or Loss Prior to Incorporation 1. A firm which was carrying on business from 1 st January, 2009 gets itself incorporated as a company on 1st May, 2009. The first accounts

ACCOUNTS (858) CLASS XI

CLASS XI") ACCOUNTS (858) Aims: 1. To provide an understanding of the principles of accounts and practice in recording transactions and interpreting individual as well as company accounts. 2. To develop an understanding

ACCOUNTS (858) Aims: 1. To provide an understanding of the principles of accounts and practice in recording transactions and interpreting individual as well as company accounts. 2. To develop an understanding

I. EQUITY AND LIABILITIES EQUITY Equity Share Capital , ,000 Other Equity 19 1,492,255 26,719

ERGO DESIGN PRIVATE LIMITED Balance Sheet as at 31.03.2018 Non Current Assets Property, Plant and Equipment 3 639,731 58,912 Capital work-in-progress 3 Investment Property 4 Goodwill 5 Other Intangible

ERGO DESIGN PRIVATE LIMITED Balance Sheet as at 31.03.2018 Non Current Assets Property, Plant and Equipment 3 639,731 58,912 Capital work-in-progress 3 Investment Property 4 Goodwill 5 Other Intangible

Book-III:- Analysis of Financial Statement of a company. Financial Statements of a Company

SUPPORT MATERIAL ACCOUNTANCY CLASS-XII Book-III:- Analysis of Financial Statement of a company Financial Statements of a Company Financial Statements: Financial statements are the end products of accounting

SUPPORT MATERIAL ACCOUNTANCY CLASS-XII Book-III:- Analysis of Financial Statement of a company Financial Statements of a Company Financial Statements: Financial statements are the end products of accounting

Notes Forming Part of the Profit & Loss Accounts as at 31st March, 2012 Note : 13 Revenue from Operations ` ` Sr. No Particulars 2012 2011 1 Sale of shares & Securities 828496 1,281,469 2 Profit on sale

Notes Forming Part of the Profit & Loss Accounts as at 31st March, 2012 Note : 13 Revenue from Operations ` ` Sr. No Particulars 2012 2011 1 Sale of shares & Securities 828496 1,281,469 2 Profit on sale

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

GOVERNMENT OF INDIA Ministry of Corporate Affairs

GOVERNMENT OF INDIA Ministry of Corporate Affairs NOTICE INVITING COMMENTS ON THE REVISED SCHEDULE III TO THE COMPANIES ACT, 2013 FOR A COMPANY WHOSE FINANCIAL STATEMENTS ARE DRAWN UP IN COMPLIANCE OF

GOVERNMENT OF INDIA Ministry of Corporate Affairs NOTICE INVITING COMMENTS ON THE REVISED SCHEDULE III TO THE COMPANIES ACT, 2013 FOR A COMPANY WHOSE FINANCIAL STATEMENTS ARE DRAWN UP IN COMPLIANCE OF

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

4. Expected Total Loss on Contract (Contract Price? 2400 Less Total Expected Cost ` 3250) ` 850 Crores

` 850 Crores") INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUTING Branch: Multiple Date: Note: All questions are compulsory. Question 1 A) 1. Basic Computations (2 marks) 1. Cost Incurred Till Date (Cost of Work Certified

INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUTING Branch: Multiple Date: Note: All questions are compulsory. Question 1 A) 1. Basic Computations (2 marks) 1. Cost Incurred Till Date (Cost of Work Certified

ERGO DESIGN PRIVATE LIMITED BALANCE SHEET AS AT 31ST MARCH, 2016

I. EQUITY AND LIABILITIES ERGO DESIGN PRIVATE LIMITED BALANCE SHEET AS AT 31ST MARCH, 2016 Particulars Note No 31-03-2016 31-03-2015 (1) SHAREHOLDERS' FUNDS (a) Share Capital 2 10000 (b) Reserves and Surplus

I. EQUITY AND LIABILITIES ERGO DESIGN PRIVATE LIMITED BALANCE SHEET AS AT 31ST MARCH, 2016 Particulars Note No 31-03-2016 31-03-2015 (1) SHAREHOLDERS' FUNDS (a) Share Capital 2 10000 (b) Reserves and Surplus

ABHISHEK FINLEASE LTD BALANCE SHEET AS AT 31ST MARCH, 2013 Particulars te. 2013 2012 (1) Shareholder's Funds (a) Share Capital 1 42,637,500 42,637,500 (b) Reserves and Surplus 2-5,889,860-6,060,583 (c)

ABHISHEK FINLEASE LTD BALANCE SHEET AS AT 31ST MARCH, 2013 Particulars te. 2013 2012 (1) Shareholder's Funds (a) Share Capital 1 42,637,500 42,637,500 (b) Reserves and Surplus 2-5,889,860-6,060,583 (c)

Revisionary Test Paper for June 2012 Examination

Question 1 Paper 16 Advanced Financial Accounting & Reporting How would you deal with the following in the annual accounts of a company for the year ended 31st March, 2012? (a) (b) Answer (a) The company

Question 1 Paper 16 Advanced Financial Accounting & Reporting How would you deal with the following in the annual accounts of a company for the year ended 31st March, 2012? (a) (b) Answer (a) The company

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS Test Series: October, 2017 1. (a) Statement Showing Impairment Loss ( in crores) Carrying amount of the machine as

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS Test Series: October, 2017 1. (a) Statement Showing Impairment Loss ( in crores) Carrying amount of the machine as

Redemption of Preference Shares. Fundamentals Of Accounting

Redemption of Fundamentals Of Accounting Learning Objectives After studying this unit, you will be able to: Understand the meaning of redemption and the purpose of issuing redeemable preference shares,

Redemption of Fundamentals Of Accounting Learning Objectives After studying this unit, you will be able to: Understand the meaning of redemption and the purpose of issuing redeemable preference shares,

The Institute of Chartered Accountants of India

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

SOLVED ANSWER ACCOUNTS PAPER-5 CA IPCC Nov. 09 (Collected by Manish Sharma, Kolkata) 1

1") SOLVED ANSWER ACCOUNTS PAPER-5 CA IPCC Nov. 09 (Collected by Manish Sharma, Kolkata) 1 Qn. 1. Answer the following questions : 10 x 2 = 20 (i) Goods worth 5,00,000 were destroyed due to flood in September,

SOLVED ANSWER ACCOUNTS PAPER-5 CA IPCC Nov. 09 (Collected by Manish Sharma, Kolkata) 1 Qn. 1. Answer the following questions : 10 x 2 = 20 (i) Goods worth 5,00,000 were destroyed due to flood in September,

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May Answer : Provisions: According to AS 10, Property, Plant and Equipment: 1.

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May - 2017 1. (a) M/s Progressive Company Limited has not charged depreciation for the year ended on 31 st March, 2012, in respect of a spare bus

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May - 2017 1. (a) M/s Progressive Company Limited has not charged depreciation for the year ended on 31 st March, 2012, in respect of a spare bus

Free of Cost ISBN : Solved. Scanner. Appendix. IPCC Gr. II. (Solution of Nov & Questions of May )

") Free of Cost ISBN : 978-93-5034-547-4 Solved Scanner Appendix IPCC Gr. II (Solution of Nov - 2012 & Questions of May - 2013) Paper - 5 : Advanced Accounting Solution of Nov - 2012 Chapter - 2 : Accounting

Free of Cost ISBN : 978-93-5034-547-4 Solved Scanner Appendix IPCC Gr. II (Solution of Nov - 2012 & Questions of May - 2013) Paper - 5 : Advanced Accounting Solution of Nov - 2012 Chapter - 2 : Accounting

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

Elgi Compressors Europe S.r.l. Balance Sheet As At 31st March, 2018 Particulars Note March 31, 2018 March 31, 2017

Balance Sheet As At 31st March, 2018 Particulars Note March 31, 2018 March 31, 2017 Non Current Assets Property, Plant and Equipment 3 144,494,837 127,486,695 Capital workinprogress 3 Investment Property

Balance Sheet As At 31st March, 2018 Particulars Note March 31, 2018 March 31, 2017 Non Current Assets Property, Plant and Equipment 3 144,494,837 127,486,695 Capital workinprogress 3 Investment Property

¹Hkkx IIµ[k.M 3(i)º Hkkjr dk jkti=k % vlk/kj.k 19

º Hkkjr dk jkti=k % vlk/kj.k 19") ¹Hkkx IIµ[kM 3º Hkkjr dk jkti=k % vlk/kjk 19 वद श 1 2 3 क ल 3 सभ सह यक, एस शएट और स य उ म (च ह व भ रत य य वद श ह ) क सम कत व य ववरण म श मल कय ज एग 4 नक य, सभ सह यक, य एस शएट य स य उ म जसक सम कत व य ववरण

¹Hkkx IIµ[kM 3º Hkkjr dk jkti=k % vlk/kjk 19 वद श 1 2 3 क ल 3 सभ सह यक, एस शएट और स य उ म (च ह व भ रत य य वद श ह ) क सम कत व य ववरण म श मल कय ज एग 4 नक य, सभ सह यक, य एस शएट य स य उ म जसक सम कत व य ववरण

CHAPTER 10 Financial Statement of Companies

CHAPTER 10 Financial Statement of Companies Basic Financial Statement also called Final Accounts 1. Income Statement : It show the net result of business operation i.e. Net/profit/Net loss during an accounting

CHAPTER 10 Financial Statement of Companies Basic Financial Statement also called Final Accounts 1. Income Statement : It show the net result of business operation i.e. Net/profit/Net loss during an accounting

Having understood how a company raises its

Financial Statements of a Company 3 LEARNING OBJECTIVES After studying this chapter, you will be able to : Explain the nature and objectives of financial statements of a company; Describe the form and

Financial Statements of a Company 3 LEARNING OBJECTIVES After studying this chapter, you will be able to : Explain the nature and objectives of financial statements of a company; Describe the form and

Test Series: March, 2017

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP II PAPER 5: ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP II PAPER 5: ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary

BANKING COMPANY FINAL ACCOUNTS

BANKING COMPANY FINAL ACCOUNTS Q.1. From the following information, prepare the profit and loss account of Trinity Bank Ltd, for the year ended 31 st March 03 Particulars Rs. Particulars Rs. Interest on

BANKING COMPANY FINAL ACCOUNTS Q.1. From the following information, prepare the profit and loss account of Trinity Bank Ltd, for the year ended 31 st March 03 Particulars Rs. Particulars Rs. Interest on

Sree Lalitha Academy s Key for CA IPC Accounting - Nov 2013

Question No.1 is compulsory Answer any 5 questions from the remaining 6 questions 1. (a) Solution : Cost of Fixed Asset is calculated as follows: - Purchase Price 5,278,000 Add: Sales Tax - 4% on 52,78,000

Question No.1 is compulsory Answer any 5 questions from the remaining 6 questions 1. (a) Solution : Cost of Fixed Asset is calculated as follows: - Purchase Price 5,278,000 Add: Sales Tax - 4% on 52,78,000

ELGI GULF FZE BALANCE SHEET AS AT 31ST MARCH, 2016

I. EQUITY AND LIABILITIES ELGI GULF FZE BALANCE SHEET AS AT 31ST MARCH, 2016 Particulars Note No 31-03-2016 31-03-2015 (1) SHAREHOLDERS' FUNDS (a) Share Capital 2 1777500 1777500 (b) Reserves and Surplus

I. EQUITY AND LIABILITIES ELGI GULF FZE BALANCE SHEET AS AT 31ST MARCH, 2016 Particulars Note No 31-03-2016 31-03-2015 (1) SHAREHOLDERS' FUNDS (a) Share Capital 2 1777500 1777500 (b) Reserves and Surplus

Solved Answer Acc._Paper_5 CA Ipcc May

Solved Answer Acc._Paper_5 CA Ipcc May. 2010 1 Qn. 1. Answer the following questions : [ 10 x 2 = 20 marks ] (i) A Company had issued 20,000, 13% Convertible debentures of Rs.100 each on 1st April, 2007.

Solved Answer Acc._Paper_5 CA Ipcc May. 2010 1 Qn. 1. Answer the following questions : [ 10 x 2 = 20 marks ] (i) A Company had issued 20,000, 13% Convertible debentures of Rs.100 each on 1st April, 2007.

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

Corporate Accounting I B.Com Code :CM305P Mr. D.Prabakaran, Mr.P.Vaihiyanathan, Mrs.Margret Usha, Dr.P.Arul Prasad. SECTION A 2 Marks Questions

Corporate Accounting I B.Com Code :CM305P Mr. D.Prabakaran, Mr.P.Vaihiyanathan, Mrs.Margret Usha, Dr.P.Arul Prasad SECTION A 2 Marks Questions Unit -I 1. Define company 2. What is share? 3. What is meant

Corporate Accounting I B.Com Code :CM305P Mr. D.Prabakaran, Mr.P.Vaihiyanathan, Mrs.Margret Usha, Dr.P.Arul Prasad SECTION A 2 Marks Questions Unit -I 1. Define company 2. What is share? 3. What is meant

Suggested Answer_Syl12_Dec2017_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

Valuation. The Institute of Chartered Accountants of India

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

Total Non Current Assets 13,64, ,33,862.00

ERGO DESIGN PRIVATE LIMITED, INDIA HOUSE, TRICHY ROAD BALANCE SHEET AS AT 31.03.2017 II. ASSETS Non Current Assets Property, Plant and Equipment 3 58,912.00 1,13,014.00 Capital work-in-progress 3 Investment

ERGO DESIGN PRIVATE LIMITED, INDIA HOUSE, TRICHY ROAD BALANCE SHEET AS AT 31.03.2017 II. ASSETS Non Current Assets Property, Plant and Equipment 3 58,912.00 1,13,014.00 Capital work-in-progress 3 Investment

Test Series: March, 2018

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

Indian Steel Corporation Limited IndependentAuditors'Report

IndependentAuditors'Report To, The Members of Indian Steel SEZ Limited Report on the Standalone Financial Statements We have audited the accompanying standalone financial statements of Indian Steel SEZ

IndependentAuditors'Report To, The Members of Indian Steel SEZ Limited Report on the Standalone Financial Statements We have audited the accompanying standalone financial statements of Indian Steel SEZ

Paper-18 : CORPORATE FINANCIAL REPORTING

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016)

") Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) Objectives 1. Multiple Choice Questions: (i) Dido Ltd. deals in three products, and, which are neither similar nor interchangeable.

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) Objectives 1. Multiple Choice Questions: (i) Dido Ltd. deals in three products, and, which are neither similar nor interchangeable.

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1. Reliance Clothing India Private Limited

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1 Reliance Clothing India Private Limited 2 RELIANCE CLOTHING INDIA PRIVATE LIMITED INDEPENDENT AUDITOR S REPORT To the Members of Reliance Clothing India Private

RELIANCE CLOTHING INDIA PRIVATE LIMITED 1 Reliance Clothing India Private Limited 2 RELIANCE CLOTHING INDIA PRIVATE LIMITED INDEPENDENT AUDITOR S REPORT To the Members of Reliance Clothing India Private

UNDERSTANDING FINANCIAL STATEMENTS

UNIT 4 UNDERSTANDING FINANCIAL STATEMENTS Understanding Financial Statements Structure 4.0 Objectives 4.1 Introduction 4.2 Vertical Format of Corporate Financial Statements 4.2.1 Vertical Format of Balance

UNIT 4 UNDERSTANDING FINANCIAL STATEMENTS Understanding Financial Statements Structure 4.0 Objectives 4.1 Introduction 4.2 Vertical Format of Corporate Financial Statements 4.2.1 Vertical Format of Balance

22 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)]

![22 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)]](/thumbs/86/93323018.jpg "22 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)]") 22 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)] MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 27 th July,2016 G.S.R. 742(E). In exercise of the powers conferred by sub-sections

22 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)] MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the 27 th July,2016 G.S.R. 742(E). In exercise of the powers conferred by sub-sections

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM FINANCIAL REPORTING Test Code - F M J 4 0 1 5 BRANCH - (MULTIPLE) (Date : ) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM FINANCIAL REPORTING Test Code - F M J 4 0 1 5 BRANCH - (MULTIPLE) (Date : ) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel

Accounting Leaving Certificate Higher Level. Past Exam Questions on: Published Accounts

Accounting Leaving Certificate Higher Level Past Exam Questions on: Published Accounts Page 1 of 12 OVER Q6 2013 Q9 2011 Q6 2009 Q4 Published Accounts Lemont PLC has an Authorised share capital of 700,000

Accounting Leaving Certificate Higher Level Past Exam Questions on: Published Accounts Page 1 of 12 OVER Q6 2013 Q9 2011 Q6 2009 Q4 Published Accounts Lemont PLC has an Authorised share capital of 700,000

Analysis of Financial Statement Chapter VI. Answers to the very short answers questions.

Analysis of Financial Statement Chapter VI Answers to the very short answers questions. Ans.1 Ans.2 Analysis of Financial statement is the systematic process of identifying the financial strength and weaknesses

Analysis of Financial Statement Chapter VI Answers to the very short answers questions. Ans.1 Ans.2 Analysis of Financial statement is the systematic process of identifying the financial strength and weaknesses

1,200 9,700 20,000 35,000 50,000 1,15,900

50 QUESTIONS OF ACCOUNTANCY CLASS 12 Ques 1 A and B are partners in a firm sharing profits and losses in the ratio of 2 : 1. They decide to take C into partnership for 1/5 th share on 1 st April 2011.

50 QUESTIONS OF ACCOUNTANCY CLASS 12 Ques 1 A and B are partners in a firm sharing profits and losses in the ratio of 2 : 1. They decide to take C into partnership for 1/5 th share on 1 st April 2011.

Total Non Current Assets 1,210,797 4,134,177

PART I - Form of Balance Sheet Balance Sheet as at 31.03.2017 II. ASSETS Non Current Assets Note No Value in INR 31.03.2017 31 03 2016 Property, Plant and Equipment 3 1,030,404 2,427,862 Capital work-in-progress

PART I - Form of Balance Sheet Balance Sheet as at 31.03.2017 II. ASSETS Non Current Assets Note No Value in INR 31.03.2017 31 03 2016 Property, Plant and Equipment 3 1,030,404 2,427,862 Capital work-in-progress

I. EQUITY AND LIABILITIES EQUITY Equity Share Capital ,061, ,061,139 Other Equity 19 (223,428,513) (199,234,465)

(199,234,465)") ELGI COMPRESSORES DO BRASIL IMPORTADORA E EXPORTADORA LTDA. Balance Sheet as at 31.03.2018 Non Current Assets Property, Plant and Equipment 3 3,985,033 4,560,869 Capital work-in-progress 3 Investment Property

ELGI COMPRESSORES DO BRASIL IMPORTADORA E EXPORTADORA LTDA. Balance Sheet as at 31.03.2018 Non Current Assets Property, Plant and Equipment 3 3,985,033 4,560,869 Capital work-in-progress 3 Investment Property

QUESTIONS. Inventory ,65,000 Bank Current Account 20,000 Discounts & Rebates allowed

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR MAY, 2018 EXAMINATION A. Applicable for May, 2018 examination I. Companies Act, 2013 II. Relevant Sections of the

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR MAY, 2018 EXAMINATION A. Applicable for May, 2018 examination I. Companies Act, 2013 II. Relevant Sections of the

CASH FLOW STATEMENT.. No.

CHAPTER 12 CASH FLOW STATEMENT Question 12.1 Prepare cash flow statement for the year ended 31 st March 2016 from the following balance sheets of KYC Ltd. Particulars I. EQUITY AND LIABILITIES Share holders

CHAPTER 12 CASH FLOW STATEMENT Question 12.1 Prepare cash flow statement for the year ended 31 st March 2016 from the following balance sheets of KYC Ltd. Particulars I. EQUITY AND LIABILITIES Share holders

Test Series: March, 2017

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary suitable

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary suitable

Financial Statements of Companies

2 Financial Statements of Companies Learning Objectives Unit 1: Preparation of Financial Statements After studying this unit, you will be able to: Know how to maintain books of account of a company. Learn

2 Financial Statements of Companies Learning Objectives Unit 1: Preparation of Financial Statements After studying this unit, you will be able to: Know how to maintain books of account of a company. Learn

Valuation. The Institute of Chartered Accountants of India

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

chapter - 9 Unit 1 Introduction to Company Accounts The Institute of Chartered Accountants of India

chapter - 9 COMPANY ACCOUNTS Unit 1 Introduction to Company Accounts Introduction to Company accounts Learning Objectives After studying this unit you will be able to Understand the reason for the existence

chapter - 9 COMPANY ACCOUNTS Unit 1 Introduction to Company Accounts Introduction to Company accounts Learning Objectives After studying this unit you will be able to Understand the reason for the existence

ACCOUNTING AND FINANCE

EXAMINATION FOR ENTRANCE SCHOLARSHIPS AND EXHIBITIONS FEBRUARY 2014 ACCOUNTING AND FINANCE Time Allowed 2 hours YOU SHOULD ANSWER ONLY TWO QUESTIONS from the four questions, all of which carry equal marks.

EXAMINATION FOR ENTRANCE SCHOLARSHIPS AND EXHIBITIONS FEBRUARY 2014 ACCOUNTING AND FINANCE Time Allowed 2 hours YOU SHOULD ANSWER ONLY TWO QUESTIONS from the four questions, all of which carry equal marks.

Test Series: September, 2014

MOCK TEST PAPER 1 INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: September, 2014 Wherever necessary

MOCK TEST PAPER 1 INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: September, 2014 Wherever necessary

Free of Cost ISBN : IPCC Gr. II. (Solution of May & Questions of Nov ) Paper - 5 : Advanced Accounting

Paper - 5 : Advanced Accounting") Free of Cost ISBN : 978-93-5034-725-6 IPCC Gr. II Appendix (Solution of May - 2013 & Questions of Nov - 2013) Paper - 5 : Advanced Accounting Chapter - 1 : Preparation and Presentation of Financial Statements

Free of Cost ISBN : 978-93-5034-725-6 IPCC Gr. II Appendix (Solution of May - 2013 & Questions of Nov - 2013) Paper - 5 : Advanced Accounting Chapter - 1 : Preparation and Presentation of Financial Statements

Savant Infocomm Limited

25 April 2017 Department of Corporate Services Bombay Stock Exchange Limited PJ Towers, First Floor Dalal Street Mumbai 400 001 Sir Scrip Code 517320 Regulation 33(3)(d) compliance Please refer to our

25 April 2017 Department of Corporate Services Bombay Stock Exchange Limited PJ Towers, First Floor Dalal Street Mumbai 400 001 Sir Scrip Code 517320 Regulation 33(3)(d) compliance Please refer to our

FANLING LUTHERAN SECONDARY SCHOOL

FANLING LUTHERAN SECONDARY SCHOOL 2012 2013 2 nd Term Examination S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 20th June, 2013 Time allowed: 8:30 am - 11:00 am (2 hour 30 minutes)

FANLING LUTHERAN SECONDARY SCHOOL 2012 2013 2 nd Term Examination S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 20th June, 2013 Time allowed: 8:30 am - 11:00 am (2 hour 30 minutes)