4. Expected Total Loss on Contract (Contract Price? 2400 Less Total Expected Cost ` 3250) ` 850 Crores

|

|

|

- Prudence Fisher

- 5 years ago

- Views:

Transcription

1 INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUTING Branch: Multiple Date: Note: All questions are compulsory. Question 1 A) 1. Basic Computations (2 marks) 1. Cost Incurred Till Date (Cost of Work Certified ` Cost of Work Not Certified ` 250) ` 1,500 Crores 2. Total Expected Cost on Contract (Cost till date ` Estimated Further Cost ` 1750) ` 3,250 Crores 3. Precentage of Completion = = ` ` 46.15% 4. Expected Total Loss on Contract (Contract Price? 2400 Less Total Expected Cost ` 3250) ` 850 Crores 2. Disclosure / Recognition under AS 7 (3 marks) 1. Contract Revenue Recognized (Contract Price ` 2,400 Crores x 46.15%) ` 1, Crores 2. Contract Costs Recognized ` 1, Crores 3. Loss Recognized for the Year ` Crores 4. Further Loss to be Provided for (Total Loss ` 850 Cr Less Current Year Loss ` Cr.) ` Crores 5. Progress Payments Received ` 1, Crores 6. Gross Amount Due To Customers (Note) ` 750 Crores Note: Contract Costs ` 1500 Crores less Recognized Losses ` 850 Crores less Progress Payments Received ` 1100 Crores less Progress Payments to be received ` 300 Crores = (` 750 Crores), i.e. Amount Due To Customers. B) 1. Holding: As per the holding structure given above, P Ltd has an economic interest of 26% in R Ltd. (Total Holding = Direct Holding of 14% + Indirect Holding through Q Ltd, i.e. 60% of 20% = 12%). (1 mark) 2. Substantial Interest and Significant Influence: (a) An Enterprise / Individual is considered to have a substantial interest in another enterprise, if that Enterprise / Individual owns, directly or indirectly, 20% or more interest in the voting power of the other enterprise. (b) When an investing party holds, directly or indirectly through intermediaries, 20% or more of the voting power, it is presumed that there is a significant influence, unless otherwise proved.(1.5 marks) 3. Analysis: (a) P Ltd is a majority Shareholder (60%) in Q Ltd. Thus, P Ltd has control over Q Ltd. (b) Q Ltd holds 20% Shares in R Ltd. So, Q Ltd has significant influence over R Ltd. [As per Point 2(a) 8i (b) (c) above]. P Ltd and Q Ltd, together hold 14% + 20% = 34% of the Shares in R Ltd. So, P Ltd has significant influence over R Ltd. [As per Point 2(a) and (b) above]. (1.5 marks) 4. Conclusion: P Ltd, Q Ltd and R Ltd are Related Parties. Hence, the disclosure requirements of AS - 18 are applicable in the above case. (1 marks) C) Historical Cost of Software is determined as under (5 marks) Particulars Purchase Price ($1,00,000 x ` 52) [Spot Rate under AS 11] 52,00,000 Less: Trade Discounts at 5% on above ss(2,60,000) Net Invoice Value Add : Import Duty (20% on Net Invoice Value) Add: Purchase Tax (assumed no credit available) 10% on (Net Invoice Value + Import Duty) Add: Installation Expenses Add: Professional Fees for clearance from Customs ` 49,40,000 9,88,000 5,92,800 25,000 20,000 Total 65,65,800 Page 1

2 Note: Entry Tax is not added to the Cost of the Software since it is recoverable from the Tax Department. D) 1. Expenditure charged to P&L for : ` 16 Lakhs will be recognized as an Expense because the recognition criteria were not met until 1st December This expenditure will not form part of the cost of the Production Process recognized in the Balance Sheet. (1.5 mark) 2. Carrying Amount of Intangible Asset as on : Production Process will be recognized (i.e. Carrying Amount) as an Intangible Asset at a cost of ` 24 Lakhs (i.e. expenditure incurred till the date in which recognition criteria were met, i.e. Total during FY ? 40 Lakhs less Expenses upto 1st Dec 2016 ` 16 Lakhs). (1 mark) 3. Expenditure charged to P&L A/c for : (1.5 marks) Particulars ` Lakhs Book Value on = Carrying Amt on Expenditure in = Less: Recoverable Amount 62 Impairment Loss to be charged to P&L A/c Carrying Amount of Intangible Asset as on : The Production Process will be shown at Book Value ` 94 Lakhs, or Recoverable Amount ` 62 Lakhs, whichever is less, hence at ` 62 Lakhs as above. (1 mark) Question 2 1. Loss to be borne by Equity and Preference Shareholders and Sharing of Loss (8 marks) Particulars ` Profit and Loss Account (Debit Balance) 7,00,000 Preliminary Expenses Goodwill Plant and Machinery (` 18,00,000 - ` 15,00,000) 1,00,000 2,00,000 3,00,000 Debtors (` 7,50,000 - ` 4,00,000) 3,50,000 Amount to be Written otf 16,50,000 Less: 50% of Sundry Creditors = Claim foregone 3,50,000 Total Loss to be Borne by the Equity and Preference Shareholders 13,00,000 Total Loss of ` 13,00,000 being more than 50% of Equity Share Capital, i.e. ` 10,00,000 (a) Pref. Shareholders' Share of Loss (20% of 10,00,000), contributed by Pcef. Capital Reduction 2,00,000 (b) Balance being Equity Shareholders' Share of Loss (` 13,00,000 - ` 2,00,000), contributed by Equity Capital Reduction 11,00,000 Note: Two years' Preference Dividend (Arrears) has been ignored in the computation of Loss to be borne by Equity and Preference Shareholders. 2. New Structure of Share Capital after Reorganisation (1.5 marks) Particulars ` Equity Shares: 20,000 Equity Shares of ` 45 each fully paid up (` 20,00,000 - ` 11,00,000) Preference Shares: 10,000, 9% Preference Shares of ` 80 each fully paid up (`10,00,000 - ` 2,00,000) Less: 9,00,000 8,00,000 Total 17,00, Working Capital of the Reorganized Company: (1.5 marks) Particulars ` ` Current Assets: Stock 3,00,000 Debtors 4,00,000 Cash 1,50,000 8,50,000 Current Liabilities: Creditors 3,50,000 Bank Overdraft (See Note) 75,000 4,25,000 Working capital 4,25,000 Creditors = ` 3,50,000. Hence, balance Bank Overdraft = ` 4,25,000 - ` 3,50,000 = ` 75,000 Page 2

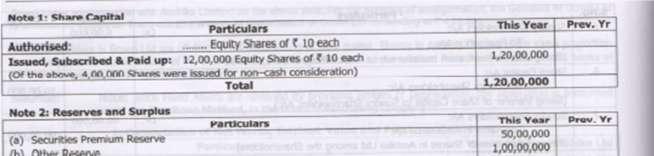

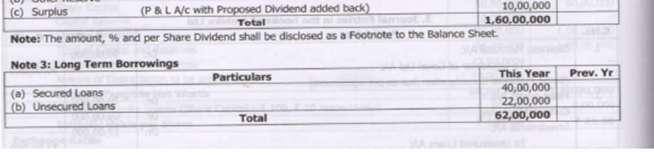

3 4. Balance Sheet of Shiva Ltd as on 31st March (after Reconstruction)(4 marks) Particulars as at 31 st March Note This Year Prev. Yr IEQUITY AND LIABILITIES: (1) Shareholders' Funds: Share Capital 1 17,00,000 (2) Non-Current Liabilities: Long Term Borrowings - Term Loan with Bank (Secured) 2,25,000 (3) Current Liabilities: (a) Short Term Borrowings - Bank Overdraft 75,000 (b) Trade Payables - Sundry Creditors 3,50,000 Total 23,50,000 IIASSETS (1) Non-Current Assets - Fixed Assets: Tangible Assets - Plant & Machinery (Cost 18,00,000 - Deer, under Reconstruction 3,00,000) 15,00,000 (2) Current Assets: (a) Inventories - Stock-in-Trade 3,00,000 (b) Trade Receivables - Sundry Debtors 4,00,000 (c) Cash and Cash Equivalents - Cash on Hand 1,50,000 Total 23,50,000 Note 1: Share Capital (1 mark) Particulars This Year Prev. Yr Authorised: 20,000 Equity Shares of ` 45 each 9,00,000 10,000 9% Preference Shares of `80 each 8,00,000 Issued, Subscribed & Paid up: 20,000 Equity Shares of ` 45 each 10,000 9% Preference Shares of ` 80 each 9,00,000 8,00,000 Total 17,00,000 Question 3 A) 1. Basic Information Company Status Dates Holding Status Holding Co. Subsidiary = Arjuna = Kanteeba Acquisition: SKanteeba's Incorporation Consolidation: 31 st March Holding Company Minority Interest = 80% = 20% 2. Analysis of General Reserves of Kanteeba Ltd Since Arjuna holds shares in Kanteeba since its incorporation, the entire Reserve balance ` 50,000 will be Revenue. 3. Consolidation of Balances (2 marks) Holding - 80%, Minority - 20% Total Minority Interest Pre-Acqn. Post Acqn. General Reserve Equity Capital 2,00,000 40,000 1,60,000 - General Reserves 50,000 10,000-40,000 Total [Cr] 1,60,000 40,000 Cost of Investment [Dr.] (1,60,000) Parent's Balances - 50,000 For Consolidated Balance Sheet NIL 90,000' 4. Consolidated Balance Sheet of Arjuna Ltd and its Subsidiary Kanteeba Ltd as on 31 st March (6 marks) Particulars as at 31 st March Note This Year Prev. Yr I EQUITY AND LIABILITIES (1) Shareholders' Funds: (a) Share Capital 1 3,00,000 Page 3

4 (b) Reserves & Surplus - General Reserve 90,000 (2) Minority Interest 50,000 (3) Non-Current Liabilities Long Term Borrowings - 8% Debentures (1,00, ,000) 1,50,000 (4) Current Liabilities: Trade Payables, i.e. Creditors (50, ,000) 1,00,000 Total 6,90,000 II ASSETS (1) Non-Current Assets Fixed Assets: -Tangible Assets (2,00, ,50,000) 3,50,000 (2) Current Assets (a) Inventories = 80, ,00,000 1,80,000 (b) Trade Receivables -Debtors (40, ,000) 1,10,000 (c) Cash & Cash Equivalents = 20, ,000 50,000 Total 6,90,000 Notes to the Balance Sheet: Authorised:.. Equity Shares of ` 10 each Note 1: Share Capital Particulars This Year Prev. Year Issued, Subscribed & Paid up: 30,000 Equity Shares of ` 10 each 3,00,000 B) Part (i): Bills for Collection - Asset and Liability A/c 1. Bills for Collection (Asset) A/c (1.5 marks) Particulars ` Particulars ` To Balance b/d (as on ) To Bills for Collection (Liability) A/c 28,00,000 By Bills for Collection (Liability) A/c 2,58,00,000 By Bills for Collection (Liability) A/c By balance c/d (as on ) (bal. fig.) 1,88,00,000 22,00,000 76,00,000 Total 2,86,00,000 Total 2,86,00, Bills for Collection (Liability) A/c (1.5 marks) Particulars ` Particulars ` To Bills for Collection (Asset)A/c To Bills for Collection (Asset)A/c To balance c/d (as on ) (bal. fig.) 1,88,00,000 22,00,000 76,00,000 By balance b/d (as on ) By Bills for Collection (Asset) A/c 28,00,000 2,58,00,000 Total 2,86,00,000 Total 2,86,00,000 Part (ii): Acceptances, Endorsements, etc. Acceptances, Endorsements and Other Obligations Account (in General Ledger) (` in Lakhs) (3 marks) Date Particulars Amt Date Particulars Amt To Constituents' Liabilities for Acceptances / By balance b/d 58 Guarantees etc. (Paid off by Clients) To Constituents Liabilities for Acceptances / By Constituent's Liabilities for 176 Guarantees etc. (Honoured by Bank) acceptance / guarantees, etc To Constituents Liabilities for Acceptances / Guarantees etc. (Honored by Bank on Party's failure to pay) To balance c/d - Acceptance not yet satisfied 90 [shown as Contingent Liability] Total 234 Total 234 Part (iii): Valuation of Security and Classification of Asset 1. For Classification of Assets as Secured, the Realizable Value of the Security should be taken on realistic basis. 2. The Stock Prices on 30th Sep and 31 Mar, i.e. half-year end, and B/s date are comparatively higher. It is also given that the fall in price in Jan is due to fluctuations. 3. Value of the Security for the Loan as on = 40,000 fully paid shares x? 96 =? 38,40,000, which is more than the Loan amount of? 24,00, Hence, the Loan may be classified as Secured Loan by the Banking Company. Part (iv): Rebate on Bills Discounted Page 4

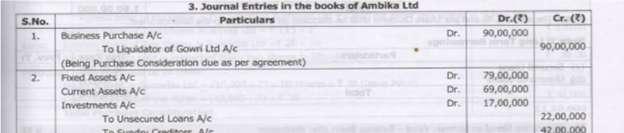

5 1. Rebate on Bills Discounted Account (1 mark) Date Particulars ` Date Particulars ` To Interest and Discount A/c 80, By balance b/d 80, To balance c/d 56, By Interest and Discount A/c (Rebate Required at year-end) 56,000 Total 1,36,000 Total 1,36, Interest and Discount Account (1 mark) Date Particulars ` Date Particulars ` To Rebate on Bills 56, By Rebate on Bills Discounted 80, To Profit8iLoss A/c(bal. fig.) 3,92,24,000 (Opening Balance) (Income for the year) By Cash and Sundries 3,92,00,000 Total 3,92,80,000 Total 3,92,80,000 Question 4 A) (2 marks for each) Asset Funded Period Overdue Provisioning Norms Provision LCD Television 4 months Upto 12 Months - Nil Nil Washing Machines For 16 Months 12 months to 24 months - 10% of Net Book Value 2,410 x 10% = Refrigerator For 36 Months 24 months to 36 months - 40% of Net Book Value 1,280 x 40% = Air Conditioners For 48 Months 36 months to 48 months - 70% of Net Book Value 647 x 70% = Total Provision 1, B) ( Particulars Year 1 Year 2 Year 3 1. Assets: Net Fixed Assets (Book Value assumed as Fair Value) 1,104 1,212 1,311 Trade Investment (Book Value taken as Market Value) Current Assets (Book Value taken as realisable) 715 1,015 1,112 Total Operating Assets ,354 2, Liabilities: 10% Debentures % Term Loan Bank Overdraft Sundry Creditors Provision for Taxation Total External Liabilities 1,015 1,365 1, Capital Employed (1-2)(6 marks) Average Capital Employed (Year 2) =, (Year 3) = (2 marks) Note: Capital Employed can also be calculated through the Liabilities Route, i.e. Share Capital + Reserves and Surplus Less Non-Trade Investments Less Discount on Issue of Shares. Question 5 Note: Since Fixed Assets are revalued by providing Arrears of Depreciation, the absorption is accounted under the Purchase Method, in the books of Purchasing Company. 1. Computation of Net Worth, Intrinsic Value and Purchase Consideration (2.5 marks) Particulars Gowri Ltd Ambika Ltd Share Capital 50,00,000 80,00,000 Capital Reserve 10,00,000 - General Reserve 36,00,000 1,00,00,000 Total of Capital and Reserves 96,00,000 1,80,00,000 Less: Goodwill considered valueless (2,00,000) - Arrears of Depreciation to be provided for (4,00,000) - Page 5

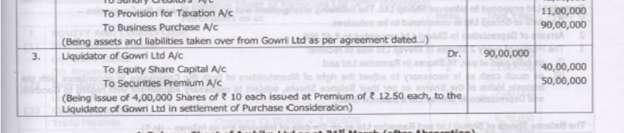

6 Balance Tangible Net Worth 90,00,000 1,80,00,000 Number of Equity Shares (Share Capital ` 100, ` 10 respectively) 50,000 8,00,000 Intrinsic Value per Share ` ` Exchange Ratio: (a) Number of Shares to be issued by Ambika Ltd to Gowri Ltd = (b) (c) `, `. = 4,00,000 shares. Manner of Issue = 4,00,000 Shares of ` 10 FV, issued at ` Premium. Exchange Ratio = 4,00,000 Shares of Ambika Ltd for 50,000 Shares of Gowri Ltd, i.e. 8 Shares of Ambika Ltd for every Share of Gowri Ltd. Note: Tangible Net Worth can also be computed as Net Tangible Assets Less External Liabilities, i.e. Net Assets Taken Over. However, in this Illustration, the "Liability Route" for computing the Intrinsic Value is considered. 2. Journal Entries in the books of Gowri Ltd (3.5 marks) S.No. Particulars Dr.(?) Cr. (?) 1. Realisation A/c Dr. 1,71,00,000 To Fixed Assets A/c To Current Assets A/c To Investment A/c To Goodwill A/c 83,00,000 69,00,000 17,00,000 2,00,000 (Being transfer of Sundry assets to Realisation A/c on sale of business) 2. Unsecured Loans A/c Dr. Sundry Creditors A/c Dr. Provision for Taxation A/c Dr. To Realisation A/c (Being transfer of Sundry Liabilities to Realisation A/c, on sale of business) 3. Ambika Ltd A/c Dr. To Realisation A/c (Being Purchase Consideration due under the agreement) 4. Shares in Ambika Ltd A/c Dr. To Ambika Ltd A/c (Being Shares received against Purchase Consideration due) 5. General Reserve A/c Dr. Capital Reserve A/c Dr. To Sundry Shareholders A/c (Being transfer of General Reserve and Capital Reserve to Sundry Shareholders) 6. Sundry Shareholders A/c Dr. To Realisation A/c (Being Loss on Realisation transferred, i.e. Net Effect of JE 1, 2 & 3) 6. Share Capital A/c Dr. To Sundry Shareholders A/c (Being transfer of Share Capital to Sundry Shareholders' A/c) 7. Sundry Shareholders A/c Dr. To Shares in Ambika Ld A/c (Being distribution of Shares in Ambika Ltd among the Shareholders) (3 3 marks, 4-4 marks, 5 3 marks) 22,00,000 42,00,000 11,00,000 90,00,000 90,00,000 36,00,000 10,00,000 6,00,000 50,00,000 90,00,000 75,00,000 90,00,000 90,00,000 46,00,000 6,00,000 50,00,000 90,00,000 Page 6

7 Page 7

(5")

8 Question 6 A) (5 marks for journal entries) Page 8

9 (2 2 marks, notes 1 mark) B) (students are required to assume either) (1 4 marks, 2 4 marks) Page 9

10 Page 10

11 Page 11

Particulars ` Particulars ` To Net")

Amount available for Distribution 12,90,000 Policyholders'")

12 Question 7 A) 1. Valuation Balance Sheet as on 31st December (1 mark) Particulars ` Particulars ` To Net Liability as per Actuarial Valuation To Profit / Surplus on Valuation (balancing figure) 74,25,000 12,23,000 By Life Fund 86,48,000 Total 86,48,000 Total 86,48, Distribution Statement (3 marks) Particulars ` Profit as per Valuation Balance Sheet 12,23,000 Add: Interim Bonus Paid 1,48,000 Profit made during the Year 13,71,000 Add: Balance brought forward from previous year 8,50,000 Total Profit 22,21,000 Less: Surplus to be carried forward (9,31,000) Amount available for Distribution 12,90,000 Policyholders' Share (12,90,000 x 95%) 12,55,500 Less: Interim Bonus Paid (1,48,000) Balance due to Policyholders 10,77,500 Page 12

Particulars Result (a) Fair Value of Option per Share = MPS on Grant Date ` 120 less Exercise Price ` 50 ` 70 (b)")

Particulars Dr.( `) Cr.")

To Securities Premium A/c [16,000 Shares x ` (120-10)] (Being")

13 B) 1. Computation of Expense to be recognized (1.5 marks) Particulars Result (a) Fair Value of Option per Share = MPS on Grant Date ` 120 less Exercise Price ` 50 ` 70 (b) No. of Shares vesting under the Scheme 16,000 Shares (c) Total Fair Value of Options = 16,000 options x` 70, to be recognised as Expense ` 11,20, Journal Entry for ESOP (2.5 marks) Particulars Dr.( `) Cr. (`) Bank A/c (16,000 Shares x ` 50) Dr. 8,00,000 Employees' Compensation Expense A/c (16,000 Shares x ` 70) Dr. 11,20,000 To Equity Share Capital A/c (16,000 Shares x ` 10) To Securities Premium A/c [16,000 Shares x ` (120-10)] (Being 16,000 Shares allotted to Employees under ESOP at a Premium of? 110 per Share) 1,60,000 17,60,000 C) (1-6 marks, 2 2 marks) Page 13

Note: Question 1 is compulsory. Attempt any five from the rest.

INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUTING Branch: Multiple Date: Question 1 (5 marks each) Note: Question 1 is compulsory. Attempt any five from the rest. A) Trilochan Ltd are Heavy Engineering Contractors

INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUTING Branch: Multiple Date: Question 1 (5 marks each) Note: Question 1 is compulsory. Attempt any five from the rest. A) Trilochan Ltd are Heavy Engineering Contractors

2. Value of Machine to be recognized in the Books of Lessee(1 ½ marks) OR Whichever is lower. = ` 1, 50,000

OR Whichever is lower. = ` 1, 50,000") INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUNTS Branch: Multiple Date: Q 1 (A) 1. Provisions of AS 9: (2 marks) (a) When the Claim made is in the course of ordinary activities of the Company, it can be recognized

INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUNTS Branch: Multiple Date: Q 1 (A) 1. Provisions of AS 9: (2 marks) (a) When the Claim made is in the course of ordinary activities of the Company, it can be recognized

FINAL CA May 2018 Financial Reporting

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

Gurukripa s Guideline Answers to May 2015 Exam Questions CA Final Financial Reporting

Gurukripa s Guideline Answers to May 2015 Exam Questions CA Final Financial Reporting Question No.1 is compulsory (4 5 = 20 Marks). Answer any five questions from the remaining six questions (16 5 = 80

Gurukripa s Guideline Answers to May 2015 Exam Questions CA Final Financial Reporting Question No.1 is compulsory (4 5 = 20 Marks). Answer any five questions from the remaining six questions (16 5 = 80

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING Question 1 is compulsory (4 5 = 20 Marks) Answer any five questions from the remaining six questions (16 5 = 80 Marks).

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING Question 1 is compulsory (4 5 = 20 Marks) Answer any five questions from the remaining six questions (16 5 = 80 Marks).

Guideline Answers for Accounting Group I

Guideline Answers for Accounting Group I Question 1(a): 5 Marks Heramba Ltd gives you the following information for the year ended 31 st March 20X2: ` Sales for the year ` 48,00,000 (The Company sold goods

Guideline Answers for Accounting Group I Question 1(a): 5 Marks Heramba Ltd gives you the following information for the year ended 31 st March 20X2: ` Sales for the year ` 48,00,000 (The Company sold goods

Suggested Answer_Syl12_Dec2015_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper- 18 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper- 18 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

(50 Marks) Department Trading Account For the year ending on In the books of Head Office (2 marks)

Department Trading Account For the year ending on In the books of Head Office (2 marks)") INTER CA MAY 218 Sub Accountancy & Advanced Accountancy Topic Redemption of Debentures, Investments Accounts, Departmental Accounts, Amalgamation & absorption & Internal reconstruction. Test Code M22 Branch:

INTER CA MAY 218 Sub Accountancy & Advanced Accountancy Topic Redemption of Debentures, Investments Accounts, Departmental Accounts, Amalgamation & absorption & Internal reconstruction. Test Code M22 Branch:

Copyright -The Institute of Chartered Accountants of India. The forward contract is sold before its due date, hence considered as speculative.

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

SUGGESTED SOLUTION. Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

, Mumbai 69. Tel : (022)") SUGGESTED SOLUTION Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Ans. 1 (a) Computation of Weighted Average Number of Shares Outstanding

SUGGESTED SOLUTION Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Ans. 1 (a) Computation of Weighted Average Number of Shares Outstanding

Gurukripa s Guideline Answers for May 2015 IPCC Exam Questions ADVANCED ACCOUNTING Group II

Gurukripa s Guideline Answers for May 2015 IPCC Exam Questions ADVANCED ACCOUNTING Group II Question No.1 is Compulsory. Answer any 5 Questions from the remaining 6 Questions. Wherever appropriate, suitable

Gurukripa s Guideline Answers for May 2015 IPCC Exam Questions ADVANCED ACCOUNTING Group II Question No.1 is Compulsory. Answer any 5 Questions from the remaining 6 Questions. Wherever appropriate, suitable

Revisionary Test Paper_Final_Syllabus 2008_Dec2013

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING

: GROUP I PAPER 1: ACCOUNTING") MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING 1 Test Series: March, 2018 SUGGESTED ANSWERS/HINTS 1. (a) Constructing or acquiring a new asset may result in incremental costs that would

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING 1 Test Series: March, 2018 SUGGESTED ANSWERS/HINTS 1. (a) Constructing or acquiring a new asset may result in incremental costs that would

PAPER 5 : ADVANCED ACCOUNTING

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

Suggested Answer_Syl12_Dec2017_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Answer to PTP_Final_Syllabus 2012_Jun2015_Set 2 Paper 18: Corporate Financial Reporting

Paper 18: Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C The following table lists the learning

Paper 18: Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C The following table lists the learning

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM FINANCIAL REPORTING Test Code - F M J 4 0 1 5 BRANCH - (MULTIPLE) (Date : ) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM FINANCIAL REPORTING Test Code - F M J 4 0 1 5 BRANCH - (MULTIPLE) (Date : ) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel

UNIT 4 : AMALGAMATION AND RECONSTRUCTION

Company Accounts 3.1 UNIT 4 : AMALGAMATION AND RECONSTRUCTION (A) Write short notes on : Question 1 Amalgamation and Absorption of companies a comparison.(3 marks)(intermediate Nov. 1994) Answer In accounting

Company Accounts 3.1 UNIT 4 : AMALGAMATION AND RECONSTRUCTION (A) Write short notes on : Question 1 Amalgamation and Absorption of companies a comparison.(3 marks)(intermediate Nov. 1994) Answer In accounting

Financial Statements of Companies

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

Internal Reconstruction

5 Internal Reconstruction BASIC CONCEPTS Reconstruction is a process by which affairs of a company are reorganized by revaluation of assets, reassessment of liabilities and by writing off the losses already

5 Internal Reconstruction BASIC CONCEPTS Reconstruction is a process by which affairs of a company are reorganized by revaluation of assets, reassessment of liabilities and by writing off the losses already

Paper-18 : CORPORATE FINANCIAL REPORTING

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS Test Series: October, 2017 1. (a) Statement Showing Impairment Loss ( in crores) Carrying amount of the machine as

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS Test Series: October, 2017 1. (a) Statement Showing Impairment Loss ( in crores) Carrying amount of the machine as

Gurukripa s Guideline Answers to Nov 2015 Exam Questions CA Inter (IPC) Group I Accounting

Group I Accounting") Gurukripa s Guideline Answers to Nov 2015 Exam Questions CA Inter (IPC) Group I Accounting Question No.1 is compulsory (4 X 5 = 20 Marks). Answer any five questions from the remaining six questions (16

Gurukripa s Guideline Answers to Nov 2015 Exam Questions CA Inter (IPC) Group I Accounting Question No.1 is compulsory (4 X 5 = 20 Marks). Answer any five questions from the remaining six questions (16

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting Question No. 1 is Compulsory. Answer any FIVE questions from the remaining SIX questions. Question 1(a)

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting Question No. 1 is Compulsory. Answer any FIVE questions from the remaining SIX questions. Question 1(a)

Gurukripa s Guideline Answers for Nov 2016 IPCC Exam Questions ADVANCED ACCOUNTING Group II Question No.1 is Compulsory. Answer any 5 Questions from the remaining 6 Questions. [Any 4 out of 5 in Q.7] Wherever

Gurukripa s Guideline Answers for Nov 2016 IPCC Exam Questions ADVANCED ACCOUNTING Group II Question No.1 is Compulsory. Answer any 5 Questions from the remaining 6 Questions. [Any 4 out of 5 in Q.7] Wherever

6 Amalgamation of Companies

6 Amalgamation of Companies Learning Objectives After studying this chapter, you will be able to: Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept

6 Amalgamation of Companies Learning Objectives After studying this chapter, you will be able to: Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept

MODEL TEST PAPER 12 (Solution)

") MODEL TEST PAPER 12 (Solution) SECTION A PART I 1. (i) (a) Share of Existing Goodwill written off. (b) Share of Loss up to the date of retirement. (c) Share of Accumulated Losses up to the date of retirement.

MODEL TEST PAPER 12 (Solution) SECTION A PART I 1. (i) (a) Share of Existing Goodwill written off. (b) Share of Loss up to the date of retirement. (c) Share of Accumulated Losses up to the date of retirement.

Test Series: March, 2017

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary suitable

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary suitable

IPCC Accounts PAPER 1 NOV

IPCC Accounts PAPER 1 NOV. 2011 1 Qn1. In Case of loss or inadequate profits, Managerial remuneration is payable as per rates specified in schedule XIII depending upon the effective capital of the company.

IPCC Accounts PAPER 1 NOV. 2011 1 Qn1. In Case of loss or inadequate profits, Managerial remuneration is payable as per rates specified in schedule XIII depending upon the effective capital of the company.

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016)

") Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) Objectives 1. Multiple Choice Questions: (i) Dido Ltd. deals in three products, and, which are neither similar nor interchangeable.

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) Objectives 1. Multiple Choice Questions: (i) Dido Ltd. deals in three products, and, which are neither similar nor interchangeable.

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

Suggested Answer_Syl12_Dec2016_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

Sree Lalitha Academy s Key for CA IPC Accounting - Nov 2013

Question No.1 is compulsory Answer any 5 questions from the remaining 6 questions 1. (a) Solution : Cost of Fixed Asset is calculated as follows: - Purchase Price 5,278,000 Add: Sales Tax - 4% on 52,78,000

Question No.1 is compulsory Answer any 5 questions from the remaining 6 questions 1. (a) Solution : Cost of Fixed Asset is calculated as follows: - Purchase Price 5,278,000 Add: Sales Tax - 4% on 52,78,000

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

Model Test Paper - 1 IPCC Gr. I Paper - 1 Accounting Question No. 1 is Compulsory. Attempt any five question from the remaining six question. 1.

Model Test Paper - 1 IPCC Gr. I Paper - 1 Accounting Question No. 1 is Compulsory. Attempt any five question from the remaining six question. 1. (a) M/s Progressive Company Limited has not charged depreciation

Model Test Paper - 1 IPCC Gr. I Paper - 1 Accounting Question No. 1 is Compulsory. Attempt any five question from the remaining six question. 1. (a) M/s Progressive Company Limited has not charged depreciation

Suggested Answer_Syl12_June2016_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 6 Total number of printed pages : 12

Roll No.... : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 12 NOTE : 1. Answer ALL Questions. 2. All working notes shall be shown distinctly.

Roll No.... : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 12 NOTE : 1. Answer ALL Questions. 2. All working notes shall be shown distinctly.

Internal Reconstruction

1 Internal Reconstruction IPCC Paper 1 : Accounting Chapter V CA. S.S. Prathap, FCA 2 Learning Objectives To understand the concept of Internal reconstruction Learn to pass Reconstruction / Capital Reduction

1 Internal Reconstruction IPCC Paper 1 : Accounting Chapter V CA. S.S. Prathap, FCA 2 Learning Objectives To understand the concept of Internal reconstruction Learn to pass Reconstruction / Capital Reduction

Test Series: March, 2017

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP II PAPER 5: ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP II PAPER 5: ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary

Suggested Answer_Syl12_Dec13_Paper 18 FINAL EXAMINATION GROUP - IV

FINAL EXAMINATION GROUP - IV SYLLABUS - 2012 SUGGESTED ANSWERS TO QUESTION DECEMBER 2013 Paper 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION GROUP - IV SYLLABUS - 2012 SUGGESTED ANSWERS TO QUESTION DECEMBER 2013 Paper 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

Liabilities Rs. Assets Rs.

MARKING SCHEME SAMPLE QUESTION PAPER -I ACCOUNTANCY Class - XII Set - I Part A Accounting for Not for Profit Organizations, Partnership Firms and Companies 1. Such organisations are formed for providing

MARKING SCHEME SAMPLE QUESTION PAPER -I ACCOUNTANCY Class - XII Set - I Part A Accounting for Not for Profit Organizations, Partnership Firms and Companies 1. Such organisations are formed for providing

PAPER 18 - CORPORATE FINANCIAL REPORTING

PAPER 18 - CORPORATE FINANCIAL REPORTING Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C The following table lists the learning

PAPER 18 - CORPORATE FINANCIAL REPORTING Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C The following table lists the learning

INTERMEDIATE EXAMINATION

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2013 Paper-5 : FINANCIAL ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right side

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2013 Paper-5 : FINANCIAL ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right side

Working notes should form part of the answers.

PAPER 1 : FINANCIAL REPORTING Question No.1 is compulsory. Candidates are required to answer any five questions from the remaining six questions. Wherever necessary, suitable assumptions may be made and

PAPER 1 : FINANCIAL REPORTING Question No.1 is compulsory. Candidates are required to answer any five questions from the remaining six questions. Wherever necessary, suitable assumptions may be made and

PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR MAY, 2018 EXAMINATION

PAPER 5: ADVANCED ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR MAY, 2018 EXAMINATION A. Applicable for May, 2018 Examination I. Applicability of the Companies Act, 2013

PAPER 5: ADVANCED ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR MAY, 2018 EXAMINATION A. Applicable for May, 2018 Examination I. Applicability of the Companies Act, 2013

Answer to MTP_Final _Syllabus 2016_Jun2017_Set 1 Paper 17- Corporate Financial Reporting

Paper 17- Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full

Paper 17- Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION A. Applicable for November, 2015 examination (i) Companies Act, 2013 (ii) The relevant

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION A. Applicable for November, 2015 examination (i) Companies Act, 2013 (ii) The relevant

Accounting for Corporate Restructuring

CHAPTER 4 Accounting for Corporate Restructuring BASIC CONCEPTS Corporate restructuring (CR) is a broad term to denote significant reorientation or realignment of the investment (assets) and/or financing

CHAPTER 4 Accounting for Corporate Restructuring BASIC CONCEPTS Corporate restructuring (CR) is a broad term to denote significant reorientation or realignment of the investment (assets) and/or financing

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May Answer : Provisions: According to AS 10, Property, Plant and Equipment: 1.

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May - 2017 1. (a) M/s Progressive Company Limited has not charged depreciation for the year ended on 31 st March, 2012, in respect of a spare bus

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May - 2017 1. (a) M/s Progressive Company Limited has not charged depreciation for the year ended on 31 st March, 2012, in respect of a spare bus

Answer to MTP_Final _Syllabus 2016_Jun 2018_Set 1 Paper 17- Corporate Financial Reporting

Paper 17- Corporate Financial Reporting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full Marks : 100 Time

Paper 17- Corporate Financial Reporting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full Marks : 100 Time

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM. Test Code CIN 5010

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- ADVANCED ACCOUNTS Test Code CIN 5010 Date: 25.08.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- ADVANCED ACCOUNTS Test Code CIN 5010 Date: 25.08.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

Test Series: March, 2018

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

(50 Marks) Date Particulars Nominal Interest Amount Date Particulars Nominal Interest Amount

Date Particulars Nominal Interest Amount Date Particulars Nominal Interest Amount") Note: All questions are compulsory. INTER CA MAY 2018 Sub: Advanced Accounts & Accounts Topics: Average Due Date, Self-Balancing Ledger, Investment Accounts, Underwriters Liability, Insurance Company Final

Note: All questions are compulsory. INTER CA MAY 2018 Sub: Advanced Accounts & Accounts Topics: Average Due Date, Self-Balancing Ledger, Investment Accounts, Underwriters Liability, Insurance Company Final

Internal Reconstruction

5 Internal Reconstruction Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

5 Internal Reconstruction Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

SUGGESTED ANSWERS TO MAY 2015 IPCC EXAMS ADVANCED ACCOUNTS

No.1 for CA/CWA & MEC/CEC MASTER MINDS SUGGESTED ANSWERS TO MAY 2015 IPCC EXAMS ADVANCED ACCOUNTS Dear students, These suggested answers are meant for easy and quick assessment of possible outcome of IPCC

No.1 for CA/CWA & MEC/CEC MASTER MINDS SUGGESTED ANSWERS TO MAY 2015 IPCC EXAMS ADVANCED ACCOUNTS Dear students, These suggested answers are meant for easy and quick assessment of possible outcome of IPCC

Solved Answer Acc._Paper_5 CA Ipcc May

Solved Answer Acc._Paper_5 CA Ipcc May. 2010 1 Qn. 1. Answer the following questions : [ 10 x 2 = 20 marks ] (i) A Company had issued 20,000, 13% Convertible debentures of Rs.100 each on 1st April, 2007.

Solved Answer Acc._Paper_5 CA Ipcc May. 2010 1 Qn. 1. Answer the following questions : [ 10 x 2 = 20 marks ] (i) A Company had issued 20,000, 13% Convertible debentures of Rs.100 each on 1st April, 2007.

All BATCHES DATE: MAXIMUM MARKS: 100 TIMING: 3¼Hours

All BATCHES DATE: 09.07.2018 MAXIMUM MARKS: 100 TIMING: 3¼Hours PAPER 1: ACCOUNTS Q. No. 1 is compulsory. Candidates are required to answer any four questions from the remaining five questions. Wherever

All BATCHES DATE: 09.07.2018 MAXIMUM MARKS: 100 TIMING: 3¼Hours PAPER 1: ACCOUNTS Q. No. 1 is compulsory. Candidates are required to answer any four questions from the remaining five questions. Wherever

Suggested Answer_Syl12_Dec2014_Paper_18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

Revisionary Test Paper_Dec 2018

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

SAMVIT ACADEMY IPCC MOCK EXAM

1. (a) SUGGESTED ANSWERS - Group 1 Accounting (Code HAL) Disclaimer (Read carefully) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working

1. (a) SUGGESTED ANSWERS - Group 1 Accounting (Code HAL) Disclaimer (Read carefully) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working

P18_Practice Test Paper_Syl12_Dec13_Set 3

Full Marks: 100 Paper 18 : Corporate Financial Reporting Time : 3 hours 1. Answer any two Questions from Question No.1 [2 5] (a) Write a note on IFRS. (b) As on 1st April, 2011 the Fair Value of Plan Assets

Full Marks: 100 Paper 18 : Corporate Financial Reporting Time : 3 hours 1. Answer any two Questions from Question No.1 [2 5] (a) Write a note on IFRS. (b) As on 1st April, 2011 the Fair Value of Plan Assets

*

Solved Ans. Accounts_5 CA IPCC Nov. 2010 1 Attention C.A. Pcc & Ipcc Students Solved Ans. Accounts_5 Ipcc_Nov.10 Keep Watching our website* for further solution. *www.jainclassesonline.com (No.1 Institute

Solved Ans. Accounts_5 CA IPCC Nov. 2010 1 Attention C.A. Pcc & Ipcc Students Solved Ans. Accounts_5 Ipcc_Nov.10 Keep Watching our website* for further solution. *www.jainclassesonline.com (No.1 Institute

INTERNAL RECONSTRUCTION

5 INTERNAL RECONSTRUCTION Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

5 INTERNAL RECONSTRUCTION Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

Paper-5: FINANCIAL ACCOUNTING

Paper-5: FINANCIAL ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 Whenever necessary, suitable assumptions should be made and indicate in answer by the candidates. Working Notes should be form part

Paper-5: FINANCIAL ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 Whenever necessary, suitable assumptions should be made and indicate in answer by the candidates. Working Notes should be form part

SOLVED ANSWER ACCOUNTS PAPER-5 CA IPCC Nov. 09 (Collected by Manish Sharma, Kolkata) 1

1") SOLVED ANSWER ACCOUNTS PAPER-5 CA IPCC Nov. 09 (Collected by Manish Sharma, Kolkata) 1 Qn. 1. Answer the following questions : 10 x 2 = 20 (i) Goods worth 5,00,000 were destroyed due to flood in September,

SOLVED ANSWER ACCOUNTS PAPER-5 CA IPCC Nov. 09 (Collected by Manish Sharma, Kolkata) 1 Qn. 1. Answer the following questions : 10 x 2 = 20 (i) Goods worth 5,00,000 were destroyed due to flood in September,

Cash-Flow Statement. According to. Revised Schedule VI Part I of Companies Act, Cash-Flow Statement

Cash-Flow Statement According to Revised Schedule VI Part I of Companies Act, 1956 Cash-Flow Statement QUESTION Prepare a Cash Flow Statement from the following Balance Sheets of Gokaldas Exports Ltd.

Cash-Flow Statement According to Revised Schedule VI Part I of Companies Act, 1956 Cash-Flow Statement QUESTION Prepare a Cash Flow Statement from the following Balance Sheets of Gokaldas Exports Ltd.

PAPER 1 : ACCOUNTING PART I : ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2012 EXAMINATION

PAPER 1 : ACCOUNTING PART I : ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2012 EXAMINATION A. Applicable for November, 2012 examination Schedule VI revised by the Ministry of

PAPER 1 : ACCOUNTING PART I : ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2012 EXAMINATION A. Applicable for November, 2012 examination Schedule VI revised by the Ministry of

PROFITS OR LOSS PRIOR TO INCORPORATION

CHAPTER 3 PROFITS OR LOSS PRIOR TO INCORPORATION Learning Objectives After studying this chapter, you will be able to: Account for pre-incorporation profit. Learn various methods for computing profit or

CHAPTER 3 PROFITS OR LOSS PRIOR TO INCORPORATION Learning Objectives After studying this chapter, you will be able to: Account for pre-incorporation profit. Learn various methods for computing profit or

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2014 EXAMINATION

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2014 EXAMINATION A. Applicable for November, 2014 examination Revision in the Criteria for classifying

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2014 EXAMINATION A. Applicable for November, 2014 examination Revision in the Criteria for classifying

AMALGAMATION, ABSORPTION AND RECONSTRUCTION

CHAPTER-5 AMALGAMATION, ABSORPTION AND RECONSTRUCTION Q. 1. The following is the summarized Balance Sheet of A Ltd. as on 31.3.2012 Liabilities Assets 14,000 Equity shares of Sundry assets 18,00,000 100

CHAPTER-5 AMALGAMATION, ABSORPTION AND RECONSTRUCTION Q. 1. The following is the summarized Balance Sheet of A Ltd. as on 31.3.2012 Liabilities Assets 14,000 Equity shares of Sundry assets 18,00,000 100

Answer to MTP_Final_Syllabus 2008_Jun2015_Set 1

Paper-16: Advanced Financial Accounting & Reporting Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Working Notes should form part of the answer.

Paper-16: Advanced Financial Accounting & Reporting Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Working Notes should form part of the answer.

FINAL EXAMINATION GROUP - IV (SYLLABUS 2012)

") FINAL EXAMINATION GROUP - IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE - 2017 Paper-18 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP - IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE - 2017 Paper-18 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

The Institute of Chartered Accountants of India

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

Shree Guru Kripa s Institute of Management

Reg. No.. ADVANCED ACCOUNTING GROUP II Total Number of Questions: 6 Date: 01/04/2016 Time 3 H Maximum Marks: 100 1. (a) Given below is the Capital Structure of Kiran Ltd as on 31 st March (5 Marks) Equity

Reg. No.. ADVANCED ACCOUNTING GROUP II Total Number of Questions: 6 Date: 01/04/2016 Time 3 H Maximum Marks: 100 1. (a) Given below is the Capital Structure of Kiran Ltd as on 31 st March (5 Marks) Equity

RTP_FAC_Inter_Syl08_Dec13. Group I Paper 5 Financial Accounting

Group I Paper 5 Financial Accounting 1. Answer the following questions (give workings): (i) Mukta Ltd. purchased a machine for 40 lakhs including excise duty of 8 lakhs. The excise duty is Cenvatable under

Group I Paper 5 Financial Accounting 1. Answer the following questions (give workings): (i) Mukta Ltd. purchased a machine for 40 lakhs including excise duty of 8 lakhs. The excise duty is Cenvatable under

FINAL CA May 2018 Financial Reporting

FINAL CA May 2018 Financial Reporting Test Code F9 Branch : Borivali Date: 17.12.2017 (50 Marks) compulsory. Note: All questions are Question 1 (9 marks) Following information is provided in respect of

FINAL CA May 2018 Financial Reporting Test Code F9 Branch : Borivali Date: 17.12.2017 (50 Marks) compulsory. Note: All questions are Question 1 (9 marks) Following information is provided in respect of

Chapter 3 Accounting for debentures. The general ledger arising from these entries would appear as follows:

Chapter 3 Accounting for debentures 41 The general ledger arising from these entries would appear as follows: General ledger of Grampians Ltd Date Particulars Debit Credit Balance Debenture interest expense

Chapter 3 Accounting for debentures 41 The general ledger arising from these entries would appear as follows: General ledger of Grampians Ltd Date Particulars Debit Credit Balance Debenture interest expense

BANKING COMPANY FINAL ACCOUNTS

BANKING COMPANY FINAL ACCOUNTS Q.1. From the following information, prepare the profit and loss account of Trinity Bank Ltd, for the year ended 31 st March 03 Particulars Rs. Particulars Rs. Interest on

BANKING COMPANY FINAL ACCOUNTS Q.1. From the following information, prepare the profit and loss account of Trinity Bank Ltd, for the year ended 31 st March 03 Particulars Rs. Particulars Rs. Interest on

Sreeram Coaching Point PCC - Advanced Accounting Nov. 2008

1 Solution to Question No. 1 Reconstruction A/c To Investment in Q Ltd 11500 By 8% cumulative Preference share 160000 capital (Rs 10) (64000x2.50) To Provision For Baddebts 6400 By Equity Share capital

1 Solution to Question No. 1 Reconstruction A/c To Investment in Q Ltd 11500 By 8% cumulative Preference share 160000 capital (Rs 10) (64000x2.50) To Provision For Baddebts 6400 By Equity Share capital

FINAL EXAMINATION GROUP - IV (SYLLABUS 2016)

") FINAL EXAMINATION GROUP - IV (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS JUNE - 2017 Paper-17 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the right side indicate

FINAL EXAMINATION GROUP - IV (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS JUNE - 2017 Paper-17 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the right side indicate

T.Y.BAF Financial Accounting Paper V Marks: 75 Sem V Pre Final Exam 2 (2017) Time:2 ½ hrs.

Time:2 ½ hrs.") Bandra West Vile Parle West H. O. : Shop No. 5, Hill Crest Society, 16 th Road, Bandra (W), Mum: 50. Ph: 26051635 Branch : Avon Arcade, Shop No. A/121, 1 st Fl.,Vile Parle (W), Mumbai: 56. Ph: 26189748

Bandra West Vile Parle West H. O. : Shop No. 5, Hill Crest Society, 16 th Road, Bandra (W), Mum: 50. Ph: 26051635 Branch : Avon Arcade, Shop No. A/121, 1 st Fl.,Vile Parle (W), Mumbai: 56. Ph: 26189748

16. COMPANY FINAL ACCOUNTS

16. COMPANY FINAL ACCOUNTS SOLUTIONS TO ASSIGNMENT PROBLEMS PROBLEM NO.1 Journal Entries in the Books of CODIG Ltd. Date Debit Credit 31.03.03 Profit and Loss A/c Dr. To Provision for Income Tax A/c (Being

16. COMPANY FINAL ACCOUNTS SOLUTIONS TO ASSIGNMENT PROBLEMS PROBLEM NO.1 Journal Entries in the Books of CODIG Ltd. Date Debit Credit 31.03.03 Profit and Loss A/c Dr. To Provision for Income Tax A/c (Being

MTP_Intermediate_Syllabus 2012_Dec2013_Set 1. Paper 12 - Company Accounts & Audit. Section A

Paper 12 - Company Accounts & Audit Section A (1) Answer the following (compulsory) [2x2=4] Full Marks: 100 (i) Distinguish between Monetary items and Non Monetary Items. (ii) Write short notes on accounting

Paper 12 - Company Accounts & Audit Section A (1) Answer the following (compulsory) [2x2=4] Full Marks: 100 (i) Distinguish between Monetary items and Non Monetary Items. (ii) Write short notes on accounting

DEAR PRIME ACADEMY STUDENT, 1. FOR FINANCIAL INSTRUMENTS (PRACTICAL QUESTIONS), REFER TO ICAI BOOKLET ON THE SAME ONLY

, REFER TO ICAI BOOKLET ON THE SAME ONLY") DEAR PRIME ACADEMY STUDENT, 1. FOR FINANCIAL INSTRUMENTS (PRACTICAL QUESTIONS), REFER TO ICAI BOOKLET ON THE SAME ONLY 2. REFER LATEST RTP AND TO THAT EXTENT QUESTIONS THAT WERE COMMON IN THIS PRACTICE

DEAR PRIME ACADEMY STUDENT, 1. FOR FINANCIAL INSTRUMENTS (PRACTICAL QUESTIONS), REFER TO ICAI BOOKLET ON THE SAME ONLY 2. REFER LATEST RTP AND TO THAT EXTENT QUESTIONS THAT WERE COMMON IN THIS PRACTICE

Suggested Answer_Syl12_Dec13_Paper 5 INTERMEDIATE EXAMINATION

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2013 Paper-5: FINANCIAL ACCOUNTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2013 Paper-5: FINANCIAL ACCOUNTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

Accountancy. Class XII: Sample Paper. Source: mycbseguide.com

Accountancy Class XII: Sample Paper Source: mycbseguide.com SAMPLE PAPER- 1 (solved) ACCOUNTANCY Class XII Time allowed: 3 hours Maximum Marks: 80 General Instructions: 1. This question paper contains

Accountancy Class XII: Sample Paper Source: mycbseguide.com SAMPLE PAPER- 1 (solved) ACCOUNTANCY Class XII Time allowed: 3 hours Maximum Marks: 80 General Instructions: 1. This question paper contains

DISCLAIMER. Question No. 1

No.1 for CA/CWA & MEC/CEC MASTER MINDS Dear students, These suggested answers are meant for easy and quick assessment of possible outcome of IPCC aspirants for their inadvance preparation and future course

No.1 for CA/CWA & MEC/CEC MASTER MINDS Dear students, These suggested answers are meant for easy and quick assessment of possible outcome of IPCC aspirants for their inadvance preparation and future course

MTP_Final_Syllabus 2012_Jun 2017_Set 2 Paper 18: Corporate Financial Reporting

Paper 18: Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 18 - Corporate Financial Reporting Full

Paper 18: Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 18 - Corporate Financial Reporting Full

Paper-5: FINANCIAL ACCOUNTING

Paper5: FINANCIAL ACCOUNTING Time Allowed: 3 Hours Full Marks : 100 Whenever necessary, suitable assumptions should be made and indicate in answer by the candidates. Working Notes should be form part of

Paper5: FINANCIAL ACCOUNTING Time Allowed: 3 Hours Full Marks : 100 Whenever necessary, suitable assumptions should be made and indicate in answer by the candidates. Working Notes should be form part of

Gurukripa s Guideline Answers for May 2016 IPCC Exam Questions ADVANCED ACCOUNTING Group II

Gurukripa s Guideline Answers for May 2016 IPCC Exam Questions ADVANCED ACCOUNTING Group II Question No.1 is Compulsory. Answer any 5 Questions from the remaining 6 Questions. [Any 4 out of 5 in Q.7] Wherever

Gurukripa s Guideline Answers for May 2016 IPCC Exam Questions ADVANCED ACCOUNTING Group II Question No.1 is Compulsory. Answer any 5 Questions from the remaining 6 Questions. [Any 4 out of 5 in Q.7] Wherever

Answer to PTP_Intermediate_Syllabus 2012_Dec 2015_Set 1 Paper 12: Company Accounts and Audit

Paper 12: Company Accounts and Audit Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Pg 1 LEVEL B Answer to PTP_Intermediate_Syllabus 2012_Dec

Paper 12: Company Accounts and Audit Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Pg 1 LEVEL B Answer to PTP_Intermediate_Syllabus 2012_Dec

PAPER 18 - CORPORATE FINANCIAL REPORTING

PAPER 18 - CORPORATE FINANCIAL REPORTING Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C Answer to MTP_Final_Syllabus 2012_Dec2015_Set

PAPER 18 - CORPORATE FINANCIAL REPORTING Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C Answer to MTP_Final_Syllabus 2012_Dec2015_Set

Free of Cost ISBN : IPCC Gr. II. (Solution of May & Questions of Nov ) Paper - 5 : Advanced Accounting

Paper - 5 : Advanced Accounting") Free of Cost ISBN : 978-93-5034-725-6 IPCC Gr. II Appendix (Solution of May - 2013 & Questions of Nov - 2013) Paper - 5 : Advanced Accounting Chapter - 1 : Preparation and Presentation of Financial Statements

Free of Cost ISBN : 978-93-5034-725-6 IPCC Gr. II Appendix (Solution of May - 2013 & Questions of Nov - 2013) Paper - 5 : Advanced Accounting Chapter - 1 : Preparation and Presentation of Financial Statements

Required: Calculate the current tax payable (for SFP) and relevant current tax expense (for SPL) for the year 2011.

and relevant current tax expense (for SPL) for the year 2011.") IAS 12 Income Taxes CURRENT TAX DEFINITIONS Accounting profit Taxable profit (tax loss) Tax expense (tax income) Current tax is profit or loss for a period before deducting tax expense. is the profit (loss)

IAS 12 Income Taxes CURRENT TAX DEFINITIONS Accounting profit Taxable profit (tax loss) Tax expense (tax income) Current tax is profit or loss for a period before deducting tax expense. is the profit (loss)

Answer to MTP_Final _Syllabus 2016_Dec2017_Set 2 Paper 17- Corporate Financial Reporting

Paper 17- Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full

Paper 17- Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full

Free of Cost ISBN : Solved. Scanner. Appendix. IPCC Gr. II. (Solution of Nov & Questions of May )

") Free of Cost ISBN : 978-93-5034-547-4 Solved Scanner Appendix IPCC Gr. II (Solution of Nov - 2012 & Questions of May - 2013) Paper - 5 : Advanced Accounting Solution of Nov - 2012 Chapter - 2 : Accounting

Free of Cost ISBN : 978-93-5034-547-4 Solved Scanner Appendix IPCC Gr. II (Solution of Nov - 2012 & Questions of May - 2013) Paper - 5 : Advanced Accounting Solution of Nov - 2012 Chapter - 2 : Accounting

,

Ques 1 MAGNI PROFS CMA COACHING INSTITUTE (A) i. A ii. B iii. B iv. B v. D vi. A vii. D viii. C ix. C x. A (B) i. C ii. E iii. F iv. A v. B (C) i. T ii. F iii. T iv. F v. F (D) (a) Trade (b) DOM 12.04.2014

Ques 1 MAGNI PROFS CMA COACHING INSTITUTE (A) i. A ii. B iii. B iv. B v. D vi. A vii. D viii. C ix. C x. A (B) i. C ii. E iii. F iv. A v. B (C) i. T ii. F iii. T iv. F v. F (D) (a) Trade (b) DOM 12.04.2014