Innocent Spouse. Introduction. What s New? 7/14/2016

|

|

|

- Kelley Cobb

- 5 years ago

- Views:

Transcription

1 Innocent Spouse Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 14, 2016 Introduction Many married taxpayers choose to file a joint tax return because of certain benefits this filing status allows Both taxpayers are jointly and individually responsible for the tax and any interest or penalty due on the joint return even if they later divorce This is true even if a divorce decree states that a former spouse will be responsible for any amounts due on previously filed joint returns One spouse may be held responsible for all the tax due even if all the income was earned by the other spouse In some cases, a spouse will be relieved of the tax, interest, and penalties on a joint tax return What s New? The Internal Revenue Service issued Revenue Procedure This revenue procedure expands how the IRS will take into account abuse and financial control by the non requesting spouse in determining whether equitable relief is warranted It also broadens the availability of refunds in cases involving deficiencies 1

2 Rev. Proc Factors Marital Status Economic Hardship Knowledge Abuse Legal Obligation Significant benefit Compliance with Income Tax Laws Mental or Physical Health Determinations In the taxpayers favor Neutral Not in the taxpayers favor Form

3 Should the Taxpayer File Form 8857? Three Types of Relief is Available Innocent spouse relief Separation of liability Equitable relief The taxpayer is not required to figure the tax, interest, and penalties that qualify for relief The IRS will figure these amounts after the taxpayer files Form 8857, Request for Innocent Spouse Relief Married persons who file separate returns in community property states may also qualify for relief businesses selfemployed/three types of relief at a glance Three Types of Relief 3

4 Three Types of Relief Three Types of Relief Three Types of Relief 4

5 How Does a Taxpayer Request Relief? File Form 8857, Request for Innocent Spouse Relief Multiple forms are not required One form can cover multiple years The taxpayer can include a letter and any other information they would like IRS to consider when they file When Should Form 8857 be Filed? The taxpayer should file Form 8857 as soon as you become aware of a tax liability for which they believe only the spouse or former spouse should be held responsible The following are some of the ways you may become aware of such a liability The IRS is examines the tax return and proposes an increase in the tax liability The IRS sends a notice Timing of the Filing The taxpayer generally must file Form 8857 no later than 2 years after the first IRS attempt to collect the tax after July 22, 1998 There are exceptions Do not delay filing because the taxpayer does not have the required documentation 5

6 Exception for Equitable Relief On July 25, 2011, the IRS issued Notice expanding the amount of time to request equitable relief The amount of time to request equitable relief depends on whether you are seeking relief from A balance due Seeking a credit or refund, or Both Balance Due Generally, you must file your request within the time period the IRS has to collect the tax Generally, the IRS has 10 years from the date the tax liability was assessed to collect the tax In certain cases, the 10 year period is suspended Offer in Compromise Bankruptcy Judgment litigation Suit to reduce assessment judgment Collection due process hearing Relief From Joint And Several Liability On Joint Returns/Innocent Spouse Taxpayer Living Outside the U.S. Policies For Adjusting the CSED When Internal Revenue Code (IRC) 6503(c) Applies Suspension for Partnerships with Addresses Outside the U.S. Combat Zone or Contingency Operation Military Deferment Wrongful Levy (Seizure) Estate Tax Lien Taxpayer Assistance Order (TAO) Substitute for Return Credit or Refund Generally, the taxpayer must file the request within 3 years after the date the original return was filed or within 2 years after the date the tax was paid, whichever is later But they may have more time to file if they live in a federally declared disaster area or they are physically or mentally unable to manage their financial affairs 6

7 Both a Balance Due and a Credit or Refund If the taxpayer is seeking a refund of amounts paid and relief from a balance due over and above what they have paid, the time period for credit or refund will apply to any payments they have made, and the time period for collection of a balance due amount will apply to any unpaid liability Exception for Relief Based on Community Property Laws If the taxpayer is requesting relief based on community property laws, they must file Form 8857 no later than 6 months before the expiration of the period of limitations on assessment (including extensions) against the spouse or former spouse for the tax year for which they are requesting relief If the IRS begins an examination of the return during the 6 month period the latest time for requesting relief is 30 days after the date of the IRS initial contact letter The period of limitations on assessment is the amount of time, generally 3 years, that the IRS has from the date the taxpayer filed the return to assess taxes that are owed If the taxpayer does not qualify for the relief described above and are now liable for an unpaid or understated tax they believe should be paid only by the spouse or former spouse, they may request equitable relief 6015 Relief from Joint and Several Liability on Joint Return In general Notwithstanding 6013(d)(3) An individual who has made a joint return may elect to seek relief Such individual may, if eligible elect to limit such individual s liability for any deficiency with respect to such joint return Any determination under this section shall be made without regard to community property laws 7

8 Innocent Spouse Relief 6015(b) Procedures for relief from liability applicable to all joint filers A joint return has been made for a taxable year that has an understatement of tax attributable to erroneous items of one of the spouses The other individual filing the joint return establishes that in signing the return he or she did not know, and had no reason to know, that there was such understatement Taking into account all the facts and circumstances, it is inequitable to hold the other individual liable for the deficiency in tax for such taxable year attributable to such understatement; and The other individual elects the benefits of this subsection not later than the date which is 2 years after the date the Secretary has begun collection activities with respect to the individual making the election Then the other individual shall be relieved of liability for tax (including interest, penalties, and other amounts) for such taxable year to the extent such liability is attributable to such understatement Erroneous Items Unreported income This is any gross income item received by the spouse (or former spouse) that is not reported Incorrect deduction, credit, or basis This is any improper deduction, credit, or property basis claimed by the spouse (or former spouse) The following are examples of erroneous items The expense for which the deduction is taken was never paid or incurred For example, the spouse, a cash basis taxpayer, deducted $10,000 of advertising expenses on Schedule C of the joint Form 1040, but never paid for any advertising The expense does not qualify as a deductible expense For example, the spouse claimed a business fee deduction of $10,000 that was for the payment of state fines Fines are not deductible No factual argument can be made to support the deductibility of the expense The spouse claimed $4,000 for security costs related to a home office, which were actually veterinary and food costs for your family's two dogs Actual Knowledge or Reason To Know The taxpayer knew or had reason to know of an understatement if: They actually knew of the understatement, or A reasonable person in similar circumstances would have known of the understatement 8

9 Partial Relief When Portion of Erroneous Item is Unknown The taxpayer may qualify for partial relief if, at the time they filed the return, they had no knowledge or reason to know of only a portion of an erroneous item They will be relieved of the understatement due to that portion of the item if all other requirements are met for that portion Example If at the time the taxpayer signed the joint return, they knew that the spouse did not report $5,000 of gambling winnings The IRS examined the tax return several months after they filed it and determined that the spouse's unreported gambling winnings were actually $25,000 The taxpayer established that they did not know about, and had no reason to know about, the additional $20,000 because of the way the spouse handled gambling winnings The understatement of tax due to the $20,000 will qualify for innocent spouse relief if they meet the other requirements The understatement of tax due to the $5,000 of gambling winnings will not qualify for relief Indications of Unfairness for Innocent Spouse Relief The IRS will consider all of the facts and circumstances of the case in order to determine whether it is unfair to hold the taxpayer responsible for the understatement The following are examples of factors the IRS will consider Whether the taxpayer received a significant benefit, either directly or indirectly, from the understatement Whether the spouse (or former spouse) deserted the taxpayer Whether the taxpayer and your spouse had been divorced or separated Whether the taxpayer received a benefit on the return from the understatement Significant Benefit A significant benefit is any benefit in excess of normal support Normal support depends on the particular circumstances Evidence of a direct or indirect benefit may consist of transfers of property or rights to property, including transfers that may be received several years after the year of the understatement Example The taxpayer receives money from the spouse that is beyond normal support The money can be traced to the spouse's lottery winnings that were not reported on a joint return The taxpayer will be considered to have received a significant benefit from that income This is true even if your spouse gives you the money several years after he or she received it 9

10 Allocation of Liability 6015(c) If an individual who has made a joint return for any taxable year elects the application of this subsection, the individual s liability for any deficiency shall not exceed the portion of such deficiency properly allocable to the individual Burden of proof Each individual who elects the application shall have the burden of proof with respect to establishing the portion of any deficiency allocable to such individual What are the Rules for Separation of Liability? Under this type of relief, the taxpayer divides (separate) the understatement of tax (plus interest and penalties) on the joint return between the taxpayer and the spouse The understatement of tax allocated to the taxpayer is generally the amount of income and deductions attributable to their earnings and assets To qualify for separate liability, the taxpayer must have filed a joint return and meet either of the following requirements at the time they file Form 8857: They are no longer married to, or are legally separated from, the spouse with whom they filed the joint return for which they are requesting relief. (Under this rule, they are no longer married if they are widowed.) The taxpayer was not a member of the same household as the spouse with whom they filed the joint return at any time during the 12 month period ending on the date they file Form 8857 Members of the Same Household The taxpayer and spouse are not members of the same household if you are living apart and are estranged However, the taxpayer and spouse are considered members of the same household if any of the following conditions are met: The taxpayer and spouse reside in the same dwelling The taxpayer and spouse reside in separate dwellings but are not estranged, and one of them is temporarily absent from the other's household Either spouse is temporarily absent from the household and it is reasonable to assume that the absent spouse will return to the household The household or a substantially equivalent household is maintained in anticipation of the absent spouse's return Examples of temporary absences include absence due to imprisonment, illness, business, vacation, military service, or education. 10

11 Burden of Proof The taxpayer must be able to prove that they meet all of the requirements for separation of liability (except actual knowledge) and that they did not transfer property to avoid tax They must also establish the basis for allocating the erroneous items Actual Knowledge The taxpayer has actual knowledge of an erroneous item if: They knew that an item of unreported income was received They knew of the facts that made an incorrect deduction or credit unallowable For a false or inflated deduction, they knew that the expense was not incurred, or not incurred to the extent shown on the tax return Factors Supporting Actual Knowledge Whether the taxpayer made a deliberate effort to avoid learning about the item in order to be shielded from liability Whether the taxpayer and your spouse (or former spouse) jointly owned the property that resulted in the erroneous item 11

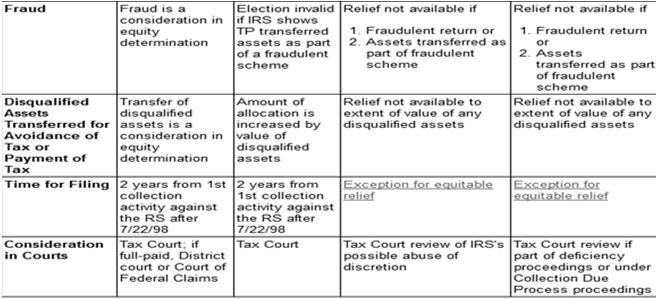

12 Domestic Abuse Exception Even if the taxpayer had actual knowledge, they may still qualify for relief if they establish that: They were the victim of domestic abuse before signing the return, and Because of that abuse, they did not challenge the treatment of any items on the return because they were afraid the spouse (or former spouse) would retaliate against them If the taxpayer establishes that they signed the joint return under duress, then it is not a joint return, and they are not liable for any tax shown on that return or any tax deficiency for that return However, the taxpayer may be required to file a separate return for that tax year Transfers of Property to Avoid Tax If the spouse transfers property (or the right to property) to the taxpayer for the main purpose of avoiding tax or payment of tax, the tax liability allocated to the taxpayer will be increased by the fair market value of the property on the date of the transfer The increase may not be more than the entire amount of the liability Transfers of Property to Avoid Tax A transfer will be presumed to have as its main purpose the avoidance of tax or payment of tax if the transfer is made after the date that is one year before the date on which the IRS sent its first letter of proposed deficiency This presumption will not apply if the transfer was made under a divorce decree, separate maintenance agreement, or a written instrument incident to such an agreement The presumption will also not apply if the taxpayer establishes that the transfer did not have as its main purpose the avoidance of tax or payment of tax 12

13 Transfers of Property to Avoid Tax If the presumption does not apply, but the IRS can establish that the purpose of the transfer was the avoidance of tax or payment of tax, the tax liability allocated to the taxpayer will be increased Why Would a Request for Separate Liability be Denied? Even if the taxpayer meets the requirements, a request for separate liability will not be granted in the following situations: The IRS proves that the taxpayer and the spouse transferred assets for the main purpose of avoiding payment of tax The IRS proves that at the time the taxpayer signed the joint return, they had actual knowledge that any items giving rise to the deficiency and allocable to the spouse were incorrect If a Husband and Wife are still Married but Separated for 12 Months, Prior to Filing a Claim for Relief due to an Involuntary Reason such as Incarceration or Military Duty, can Separation of Liability Relief be Granted? Separation of liability applies to taxpayers who are : No longer married Legally separated Living apart for the 12 months prior to the filing of a claim Under this rule, the taxpayer is no longer married if they are widowed Living apart does not include a spouse who is temporarily absent from the household A temporary absence exists if it is reasonable to assume that the absent spouse will return to the household, or A substantially equivalent household is maintained in anticipation of such a return A temporary absence may include absence due to incarceration, illness, business, vacation, military service, or education A claim can be filed if any of the three statutory requirements are met 13

14 What are the Rules for Equitable Relief? Equitable relief is only available if the taxpayer meets all of the following conditions: The taxpayer does not qualify for innocent spouse relief or the separation of liability election The requesting spouse filed a joint return for the taxpayer year for which he or she seeks relief The claim must be filed timely No assets were transferred between spouses as part of a fraudulent scheme The no requesting spouse did not transfer disqualified assets to the requesting spouse The ex spouse did not knowingly participate in the filing of a fraudulent joint return The IRS determines that it is unfair to hold the taxpayer liable for the understatement of tax taking into account all the facts and circumstances The income tax liability from which the requesting spouse seeks relief is attributable (either in full or in part) to an item of the non requesting spouse or an underpayment resulting from the non requesting spouse s income Note: Unlike innocent spouse relief or separation of liability, if the taxpayer qualifies for equitable relief, they can get relief from an understatement of tax or an underpayment of tax Equitable Relief 6015(f) Taking into account all the facts and circumstances, it is inequitable to hold the individual liable for any unpaid tax or any deficiency (or any portion of either) and Relief is not available to such individual, as provided in other subsections, the Secretary may relieve such individual of such liability Equitable Relief The taxpayer may be allowed equitable relief if both of the following conditions are met: They have an understated tax or unpaid tax, and Equitable relief is the only type of relief available for an unpaid tax 14

15 What Factors are Considered in Determining Whether or not to Grant Equitable Relief? The following factors may be considered, but the list is not all inclusive: Current marital status Reasonable belief of the requesting spouse, at the time he or she signed the return, that the tax was going to be paid; or in the case of an understatement, whether the requesting spouse had knowledge or reason to know of the understatement Current financial hardship/inability to pay basic living expenses Spouses' legal obligation to pay the tax liability pursuant to a divorce decree or agreement to pay the liability To whom the liability is attributable Significant benefit received by the requesting spouse Mental or physical health of the requesting spouse on the date the requesting spouse signed the return or at the time the requesting spouse requested the relief Compliance with income tax laws following the taxable year or years to which the request for relief relates Abuse experienced during the marriage Unpaid Tax An unpaid tax is tax that is properly shown on the return but has not been paid Understated Tax The taxpayer has an understated tax if the IRS determined that the total tax should be more than the amount actually shown on the return 15

16 6015(d) Allocation of Deficiency The portion of any deficiency on a joint return allocated to an individual shall be the amount which bears the same ratio to such deficiency as the net amount of items taken into account in computing the deficiency and allocable to the individual Certain Items are Treated Separately The disallowance of a credit Any tax required to be included with the joint return Items allocated to one individual as required by the code Child s Liability If the liability of a child of a taxpayer is included on a joint return, such liability shall be disregarded in computing the separate liability of either spouse and such liability shall be allocated appropriately between the spouses 16

17 Allocation of Items Giving Rise to the Deficiency Any item giving rise to a deficiency on a joint return shall be allocated to individuals filing the return in the same manner as it would have been allocated if the individuals had filed separate returns for the taxable year Exception where other spouse benefits An item otherwise allocable to an individual shall be allocated to the other individual filing the joint return to the extent the item gave rise to a tax benefit on the joint return to the other individual Exception for fraud The Secretary may provide for an allocation of any item if the Secretary establishes that such allocation is appropriate due to fraud of one or both individuals Limitations on separate returns disregarded If an item of deduction or credit is disallowed in its entirety solely because a separate return is filed, such disallowance shall be disregarded and the item shall be computed as if a joint return had been filed and then allocated between the spouses appropriately Example You and your former spouse filed a joint return showing $5,000 of tax, which was fully paid The IRS later examines the return and finds $10,000 of income that the former spouse earned but did not report With the additional income, the total tax becomes $6,500 The understated tax is $1,500, for which you and the former spouse are both liable Erroneous Items Any income, deduction, credit, or basis is an erroneous item if it is omitted from or incorrectly reported on the joint return Partial innocent spouse relief If the taxpayer knew about any of the erroneous items, but not the full extent of the item(s), the taxpayer may be allowed relief for the part of the understatement they did not know about 17

18 Separation of Liability Relief The taxpayer may be allowed separation of liability relief for any understated tax shown on the joint return(s) if the person with whom they filed the joint return is deceased or the taxpayer and that person: Are now divorced Are now legally separated, or Have lived apart at all times during the 12 month period prior to the date the Form 8857 is filed The IRS Must Contact Your Spouse or Former Spouse By law, the IRS must contact the spouse or former spouse There are no exceptions, even for victims of spousal abuse or domestic violence The IRS will inform the spouse or former spouse that a Form 8857 has been filed and will allow him or her to participate in the process If the taxpayer is requesting relief from joint and several liability on a joint return, the IRS must also inform him or her of its preliminary and final determinations regarding the requested relief Privacy To protect the taxpayer s privacy, the IRS will not disclose personal information such as: The current name Address Phone number(s) Information about the current employer Income Assets Any other information the taxpayer provides that the IRS uses to make a determination about the request for relief from liability could be disclosed to the person listed on line 5 If the taxpayer has other concerns about privacy or the privacy of others, they should redact or black out personal information in the material submitted 18

19 Line 5 Enter the current name and SSN (if known) of the person to whom the taxpayer was married at the end of the year(s) listed on line 3 P.O. box. Enter the box number only if: The taxpayer does not know the street address, or The post office does not deliver mail to the street address Domestic Abuse Line 8 Victim of Abuse If you wish to have the note removed from the account, call IRS at or write at either of the addresses or the fax number Please include the social security number on the written request 19

20 Part V Part V Part III Signing the Return 20

21 Part III Signing the Return By law, if a person's name is signed to a return, it is presumed to be signed by that person, unless that person proves otherwise If the taxpayer believes the signature was forged or they signed under duress, an explanation is needed If the taxpayer signed a joint return under duress or the signature was forged, the election to file jointly is not valid and the taxpayer has no valid return The taxpayer would not be jointly and severally liable for any income tax liabilities arising from that return In that case, innocent spouse relief does not apply and is not necessary for obtaining relief Part III Signing the Return If the taxpayer files Form 8857, but also maintain that there is no valid joint return due to duress or forgery, the IRS will first make a determination as to the validity of the joint return and may accordingly deny the request for innocent spouse relief based on the fact that no joint return was filed If it is ultimately determined that a valid joint return was filed, the IRS will then consider whether the taxpayer would be entitled to innocent spouse relief on the merits Forged Signature The signature on the joint return is considered to be forged if it was not signed by the taxpayer and they did not authorize (give tacit consent) the signing of the name to the return 21

22 Tacit Consent Tacit consent means that, based on the taxpayer s actions at the time the joint return was filed, they agreed to the filing of the joint return even if they now claim the signature on the return is not theirs Whether the taxpayer has tacitly consented to the filing of the joint return is based on an examination of all the facts of the case Factors that may support a finding that the taxpayer consented to the filing of the joint return include the following. They gave tax information (such as Forms W 2 and 1099) to the spouse They did not object to the filing There was an apparent advantage to the taxpayer in filing a joint return The taxpayer filed joint returns with your spouse or former spouse in prior years The taxpayer failed to file a married filing separate return and they had a filing requirement Signed Under Duress The taxpayer is considered to have signed under duress (threat of harm or other form of coercion) if they were unable to resist demands to sign the return and they would not have signed the return except for the constraint applied by the spouse or former spouse The duress must be directly connected with the signing of the joint return Transfer of Assets or Money The taxpayer may not be entitled to relief if either of the following applies. The spouse (or former spouse) transferred property (or the right to property) to the filer of Form 8857 for the main purpose of avoiding tax or payment of tax A transfer will be presumed to meet this condition if the transfer is made after the date that is 1 year before the date on which the IRS sent its first letter of proposed deficiency The IRS proves that the taxpayer and the spouse (or former spouse) transferred property to one another as part of a fraudulent scheme A fraudulent scheme includes a scheme to defraud the IRS or another third party such as a creditor, former spouse, or business partner 22

23 Fair Market Value Fair market value (FMV) is the price at which property would change hands between a willing buyer and a willing seller when both have reasonable knowledge of the relevant facts and neither has to buy or sell FMV is not necessarily the cost of replacing the item Is there a toll free number to call if I have questions regarding an Innocent Spouse Claim or how to complete the Form 8857 Request for Innocent Spouse Relief? Documents to Submit with the Claim The taxpayer should carefully review the Form 8857, Request for Innocent Spouse Relief, and it will guide them on what documents to submit 23

24 How Long will the Process Take? When a Form 8857, Request for Innocent Spouse Relief, is filed with the IRS, it may take up to 6 months before a determination is made During the processing time, the Service is requesting tax information and contacting the non requesting spouse Should the Taxpayer Wait to File the Current year Tax Return Pending the Outcome of the Claim? No The taxpayer should file the current return and IRS will not hold any refund due The Innocent Spouse Claim was Previously Denied and the Taxpayer has New Additional Information, Can they File the Claim Again? Yes They can file a second claim, provide the new additional information and it will be reconsidered However, the taxpayer will not have tax court rights on the reconsideration 24

25 Does the Non Requesting Spouse Have any Appeal Rights? Per Rev. Proc , the non requesting spouse has the right to appeal the preliminary determination to grant partial or full relief to the requesting spouse when the preliminary determination letter is issued April 1, 2003 or later However, the non requesting spouse may not petition the Tax Court from the final determination letter If relief is denied in part or in full, and the requesting spouse petitions the U.S. Tax Court, the non requesting spouse, by law, will be given the opportunity to become a party in that proceeding For claims where a preliminary determination was issued prior to April 1, 2003, the non requesting spouse had no appeal rights when the preliminary determination letter granted relief in part or in full to the requesting spouse If relief was denied and the requesting spouse petitioned the U.S. Tax Court, the non requesting spouse, by law, was given the opportunity to be a party in that proceeding Will the Taxpayer Qualify for Innocent Spouse Relief in any Situation Where there is an Understatement of Tax? Not always There are many situations in which the taxpayer may owe tax that is related to the spouse, but not be eligible for innocent spouse relief For example, the taxpayer and spouse file a joint return that reports $10,000 of income and deductions, but the taxpayer knew or had reason to know that the spouse was not reporting $5,000 of dividends The taxpayer would not be eligible for innocent spouse relief when they have knowledge or reason to know of the understatement How do State Community Property Laws Affect a taxpayer s Ability to Qualify for Relief? Community property states are Arizona California Idaho Louisiana Nevada New Mexico Texas Washington, and Wisconsin Generally, community property laws require a taxpayer to allocate community income and expenses equally between both spouses However, community property laws are not taken into account in determining whether an item belongs to the taxpayer or their spouse (or former spouse) for purposes of requesting any relief from liability 25

26 If the Taxpayer is Denied Innocent Spouse Relief, Do They Have to Re Apply to Qualify Under One of the other Two Provisions? No The IRS will automatically consider whether any of the other provisions would apply If you requested innocent spouse relief or separation of liability, IRS will automatically consider equitable relief The only time a taxpayer can reapply for relief is if they were denied relief because IRS considered them still married at the time the request for relief was filed and they can now satisfy the marital status requirements to elect to separate the liability Will the IRS Deny Relief if the Taxpayer Does Not Provide the information IRS Requests? IRS will base the decision upon all the information available to them If enough information is not available, it could adversely affect a request for relief The Taxpayer Filed an Offer in Compromise that IRS Accepted, Can the Taxpayer Still Apply for Innocent Spouse Relief? No IRS cannot consider the claim for any year in which an Offer in Compromise was accepted Acceptance of an Offer in Compromise conclusively closes the tax year(s) compromised from any re determination of the tax liability 26

27 The Taxpayer Signed a Closing Agreement, Can They Still Apply for Innocent Spouse Relief? It depends on the type of closing agreement signed If the taxpayer signed Form 866, Agreement as to Final Determination of the Tax Liability, the tax year is closed with finality and you cannot apply for innocent spouse relief If the taxpayer signed Form 906, Closing Agreement on Final Determination Covering Specific Matters, only those matters covered in the closing agreement are conclusively closed Innocent spouse relief may be requested for matters not covered in the closing agreement The Taxpayer is Currently Under Examination, How Do They Request Innocent Spouse Relief? Prepare Form 8857, Request for Innocent Spouse Relief, and mail it to: Internal Revenue Service P.O. Box Covington, KY OR If using a private delivery service, please mail the Form 8857, Request for Innocent Spouse Relief, to: Internal Revenue Service 201 W. Rivercenter Blvd. Stop 840F Covington, KY What if the IRS has Levied the Taxpayer s Account for the Tax Liability and They Decide to Request Relief? Upon receipt of the request for relief all collection activity against the taxpayer will be suspended unless the liability is in jeopardy or the statute of limitation on collection will expire shortly 27

28 What Constitutes a Collection Activity for Purposes of Starting the Two Year Statute of Limitations that Cover the Filing of Form 8857? When the IRS (1) sends a notice under 6330 of the Service s intent to levy and of the taxpayer s right to a collection due process (CDP) hearing (2) offsets a refund from another tax year and you received a notice advising you of your rights under 6015 or (3) files a judicial suit or claim that puts the requesting spouse on notice the IRS intends to collect the joint tax liability from specific property belonging to that spouse The Taxpayer Filed a Valid Joint Return with the Spouse and Has an Installment Agreement to Pay the Taxes Can the Taxpayer still Apply for Relief? The innocent spouse rules may apply in your situation However, regarding the installment agreement, there are some important considerations: If you do not continue to make payments while the IRS considers the request for relief, the installment agreement will default and full payment will be due immediately if the request for relief is denied What is the Meaning of Economic Hardship for Purposes of Equitable Relief of an Underpayment of Tax Liability Shown on a Tax Return? "Economic hardship" means that you are unable to pay your basic living expenses, e.g. food, clothing, housing, utilities, medical expenses (including health insurance), transportation, child care, child support, etc 28

29 Will the Taxpayer Receive a Refund of all Amounts Paid if Relief is Granted? It depends upon the provision under which relief is granted If innocent spouse relief is granted under 6015(b), refunds are allowable for amounts paid on or after July 22, 1998 If separation of liability is granted under 6015(c), no refunds are allowable If equitable relief is granted under 6015(f), refunds are allowed for payments made after unless the payments were made jointly with the non requesting spouse, payments were made with the return or payments were made by the non requesting spouse Note: All refunds are subject to Internal Revenue Code section 6511 This code section only allows refunds for payments made within 2 years after the tax was paid or 3 years after the return was filed whichever is later Will the Taxpayer be Granted Innocent Spouse Relief with Respect to Unreported Income if They feel it Was the Accountant s Fault that the Income was not Reported on the Return? Innocent spouse relief is in no way meant to transfer the liability to an accountant If the income was the taxpayer s (rather than the spouse's), or was the spouse's but the taxpayer knew about it, they will probably not be relieved of liability Understatement If an understatement is the result of signing an examination report that lists omissions of income, does this indicate there was knowledge of items giving rise to the deficiency? No The innocent spouse provisions clearly state the knowledge has to do with what was known at the time the return was signed 29

30 Where Should the Innocent Spouse Claim be Filed? If using the U.S. Postal Service, please mail the Form 8857, Request for Innocent Spouse Relief, to: Internal Revenue Service P.O. Box Covington, KY OR If using a private delivery service, please mail the Form 8857, Request for Innocent Spouse Relief, to: Internal Revenue Service 201 W. Rivercenter Blvd. Stop 840F Covington, KY OR You may fax the Form 8857 and attachments to the IRS at Please write your name and social security number on any attachments Note: Please do not file the Form 8857 with your tax return or Tax Court CALT Website Tour of the CALT Website 30

31 Changes to the Iowa Farm and Urban Tax Schools It has been a season of change this is good Our Fall and Winter Tax Schools are changing this is good September 9, 2016 Farm Tax Seminar All Farm issues All day For the winter tax schools, farm issues may come up but we will center on other issues important to your practice, including ethics for early bird attendees at some sessions Please Welcome Phil Harris Professor, Agricultural and Applied Economics University of Wisconsin Madison J.D., University of Chicago, 1977 M.A., Economics, University of Chicago, 1975 B.S., Economics, Iowa State University, 1973 His research program focuses on business and tax planning for agricultural producers The program includes information on the choice of entity for organizing a farm business and for transferring a farm business to the next generation Income, estate and gift tax consequences as well as non tax issues Phil Harris Phil Harris CALT Speaker September 9, 2016 Farm Tax Seminar The session will also be available via webinar Instructor Farm and Urban Tax School November Waterloo December Ames 31

32 Fall Tax Schools Though they are named the Farm and Urban Tax Schools the schools cover more than farm issues Common return issues for all kinds of returns are covered All kinds of business entities Problematic issues Sometimes we even get into to issues that you many encounter only once or twice a year or tax season The Tax Schools are a blend of diverse topics of interest to all tax professionals This year: New instructors with diverse backgrounds Your adventure awaits at Iowa State s Center for Agricultural Law and Taxation Farm and Urban Tax Schools 2016 November 2, 2016 to December 13, Locations in Iowa and Online Webinar Save the Date for the 2016 Annual Farm and Urban Income Tax Schools The program is intended for tax professionals and is designed to provide up to date training on current tax law and regulations November 2 3: Maquoketa November 7 8: Red Oak November 9 10: Sheldon November 14 15: Mason City November 17 18: Ottumwa November 21 22: Waterloo December 5 6: Denison December 12 13: Ames and Live Webinar September Farm Tax School Navigating Changing Times September 8, 2016 to September 9, 2016, Ames, Iowa and Online Attend any one day or both days, either in person or online! Company discount for 3 or more individuals from the same employer! Ag Law Seminar, September 8 Our Thursday seminar will offer practical, interesting information you can immediately apply in your practice or ag related business. You ll leave with forms and other tools to help you more efficiently serve your ag clients. Farm Tax Workshop, September 9 Our Friday seminar will be a comprehensive one day farm tax workshop designed to equip tax practitioners with the tools they need to prepare farm income tax returns, from the simple to the complex. Online Registration: 32

33 Registration Fees Early Rate Registered on/by August 31 Attend in person or watch from your computer Any one day: $200 Both days: $350 Company Discount: $10 discount per individual if 3 or more are registered from the same employer this is available for either on site or online attendance Late Rate Registered after August 31 Attend in person or watch from your computer Any one day: $220 Both days: $370 Company Discount: $10 discount per individual if 3 or more are registered from the same employer this is available for either on site or online attendance Continuing Education Ag Law Seminar (September 8) Continuing Legal Education (CLEs) 7 hours (including one hour of ethics) Others Professional Education (CPEs) 7 8 hours (including one hour of ethics) Farm Tax Workshop (September 9) Continuing Legal Education (CLEs) 7 hours (including one hour of ethics) Others Professional Education (CPEs) 7 8 hours (including one hour of ethics) Speakers Ag Law Seminar Shannon Ferrell, Associate Professor, Agricultural Economics, Oklahoma State University Eldon McAfee, Shareholder, Brick Gentry P.C. Erin Herbold Swalwell, Shareholder, Brick Gentry P.C. Julia Vyskocil, Shareholder, Brick Gentry P.C. Pat Dillon, Dillon Law P.C. Professor Neil Hamilton, Director of Drake Law School Agricultural Law Center John Baker, Iowa State s Beginning Farmer Center Administrator Jennifer Zwagerman, Associate Director of Drake Law School Agricultural Law Center Kristine Tidgren, Assistant Director for the Center for Agricultural Law & Taxation Farm Tax Workshop Philip E. Harris, JD, University of Wisconsin professor Kristy Maitre, Tax Specialist with the Center for Agricultural Law & Taxation 33

34 Farm Tax Seminar Topics Legislative Update: The Protecting Americans from Tax Hikes Act of 2015 (PATH Act) and the Consolidated Appropriations Act, 2016 (CAA of 2016) Income Issues Constructive Receipt Installment Sales of Livestock Hedging and Other Marketing Transactions Farm Income Averaging Farm vs. Nonfarm Income Easements Sale vs. Lease of Equipment by a Retiring Farmer Conservation Reserve Program Payments Income in Respect of a Decedent Reporting Property as Self rental on Schedule E (Form 1040) Deduction Issues Tangible Property Regulations Lease vs. Purchase of Farm Equipment Segregating Fertilizer Costs Domestic Production Activity Deduction Start Up Expenses Farm Tax Seminar Topics Entity Issues Partnership Formation and Contributed Assets with Debt in Excess of Tax Basis Guaranteed Payments Qualified Joint Ventures Issues for Farmers with Multiple Entities Miscellaneous Farm Issues Material Participation Capitalization of Preproduction Expenses Farm Inventory Hobby Losses Gift of Commodities Valuation of growing crops Cases and Rulings: A summary of rulings and cases from the past year that affect farmers Accommodations Quality Inn & Suites Starlite Village Conference Center 2601 East 13th Street, Ames, Iowa Discounted overnight rooms are available for $89.00 per night (for the dates of September 7, 8 and 9) Call the hotel at and mention you are attending the Iowa State University September Seminars 34

35 Summer Webinars Above the Line Deductions Roth IRA s Injured Spouse Preparing for an IRS Audit Net Operating Losses The Portability Election IRS Return Preparer Penalties Overview Miscellaneous Income New Developments Summer Webinars Tax Research with Limited Resources IRS Representation Inventory Issues Appeals How to Write Your Appeals Request Start Up Costs Hobby Losses Beginning Tax Preparers Class CALT is working on offering a basic class for NEW tax preparers this fall in October The week long webinar will cover the basics an individual needs to know such as: Requirement to file Dependents Filing Status Itemized deductions Education Credits Other issues a first or second year preparer needs to know as well as a refresher for others who need to brush up on issues The class will be a week long or more and will be offered at a special rate 35

36 The Scoop Throughout the filing season two Scoops will be held on Scoop Dates 8:00 8:30 am Central time 12:00 12:30 Central time This assists with accommodating our west coast practitioners The same information will be shared at both sessions You have the option of registering for whatever session suits your schedule node fieldseminar date/month Future Scoop Dates July 20, 2016 August 24, 2016 September 7, 2016 October 5, 2016 October 19, 2016 November 16, 2016 December 14, nodefield seminar date/month The CALT Staff John D. Lawrence Interim Director Associate Dean, College of Agriculture & Life Sciences Extension Programs and Outreach Director, Agriculture & Natural Resources Extension 132 Curtiss Hall Iowa State University Ames, Iowa Kristine A. Tidgren Assistant Director E mail: ktidgren@iastate.edu Phone: (515) Fax: (515)

37 The CALT Staff Kristy S. Maitre Tax Specialist E mail: ksmaitre@iastate.edu Phone: (515) Fax: (515) Tiffany L. Kayser Program Administrator E mail: tlkayser@iastate.edu Phone: (515) Fax: (515)

The Scoop. Agenda. Get A Transcript 7/5/2016. Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 6, 2016

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 6, 2016 Agenda Get A Transcript ACA Return stats for 2014 House Committee Testimony on Agents Training IP Pin Breach

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 6, 2016 Agenda Get A Transcript ACA Return stats for 2014 House Committee Testimony on Agents Training IP Pin Breach

Injured Spouse. How the System Works. What Is the Treasury Offset Program? 7/26/2016

Injured Spouse Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 20, 2016 How the System Works What Is the Treasury Offset Program? The Treasury Offset Program (TOP) is a centralized

Injured Spouse Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 20, 2016 How the System Works What Is the Treasury Offset Program? The Treasury Offset Program (TOP) is a centralized

The Scoop. Agenda. Walk In (TAC Offices) 7/19/2016. TAC Offices are beginning to change policies on appointment only services without notice

7/19/2016. TAC Offices are beginning to change policies on appointment only services without notice") The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 20, 2016 Agenda IRS Walk In Office Changes Tax Preparer Safeguard of cyber data Electronic Tax Administration proposes

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 20, 2016 Agenda IRS Walk In Office Changes Tax Preparer Safeguard of cyber data Electronic Tax Administration proposes

Request for Innocent Spouse Relief

Form 8857 (Rev. September 2010) Department of the Treasury Internal Revenue Service (99) Request for Innocent Spouse Relief See separate instructions. OMB 1545-1596 Important things you should know Do

Form 8857 (Rev. September 2010) Department of the Treasury Internal Revenue Service (99) Request for Innocent Spouse Relief See separate instructions. OMB 1545-1596 Important things you should know Do

The Scoop. Agenda. When Age Matters 2/8/2016. Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation February 10, 2015

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation February 10, 2015 Agenda Age matters Good reminders Ordering Publication 17 Estate Closing letters Refunds ACS support sites

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation February 10, 2015 Agenda Age matters Good reminders Ordering Publication 17 Estate Closing letters Refunds ACS support sites

Comprehensive Seminars, Practical Resources

stay INFORMED Social Media If you want to keep up with the latest tax and agricultural law happenings, make sure to follow us on Twitter, @CALT_IowaState, and find us on Facebook. The CALT Brief Every

stay INFORMED Social Media If you want to keep up with the latest tax and agricultural law happenings, make sure to follow us on Twitter, @CALT_IowaState, and find us on Facebook. The CALT Brief Every

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies Presented to CPA Academy Lawrence A. Sannicandro, Esq. 1 Overview I. Introduction II. Conflicts of Interest III. Overview of Innocent

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies Presented to CPA Academy Lawrence A. Sannicandro, Esq. 1 Overview I. Introduction II. Conflicts of Interest III. Overview of Innocent

COPYRIGHTED MATERIAL. Filing Status. Chapter 1

Chapter 1 Filing Status The filing status you use when you file your return determines the tax rates that will apply to your taxable income; see 1.2. Filing status also determines the standard deduction

Chapter 1 Filing Status The filing status you use when you file your return determines the tax rates that will apply to your taxable income; see 1.2. Filing status also determines the standard deduction

Child and Dependent Care Credit. Basics. Form /13/2016. Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 12, 2016

Child and Dependent Care Credit Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 12, 2016 Basics The client may be able to claim the child and dependent care credit if they

Child and Dependent Care Credit Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 12, 2016 Basics The client may be able to claim the child and dependent care credit if they

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Divorce and Tax Issues: Evaluating Key Opportunities and Risks Navigating Tax Consequences for Support, Assets and Liabilities Division, Deductions,

Presenting a live 90-minute webinar with interactive Q&A Divorce and Tax Issues: Evaluating Key Opportunities and Risks Navigating Tax Consequences for Support, Assets and Liabilities Division, Deductions,

Section 66. Treatment of Community Income

Section 66. Treatment of Community Income 26 CFR 1.66 4(b): Equitable relief from the federal income tax liability resulting from the operation of community property law. This revenue procedure provides

Section 66. Treatment of Community Income 26 CFR 1.66 4(b): Equitable relief from the federal income tax liability resulting from the operation of community property law. This revenue procedure provides

The Scoop. Agenda. E Services Changes Ahead 10/7/2016. Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 6, 2016

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 6, 2016 Agenda E Services Changes Fake CP 2000 New Procedure for Rollover Requirement Waivers Rev. Proc. 2016 47 Premium

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 6, 2016 Agenda E Services Changes Fake CP 2000 New Procedure for Rollover Requirement Waivers Rev. Proc. 2016 47 Premium

The Scoop. Liens. New Scam 6/22/2016. Don t Forget to Report Certain Foreign Accounts to Treasury by the June 30 Deadline

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation June 22, 2016 Don t Forget to Report Certain Foreign Accounts to Treasury by the June 30 Deadline Taxpayers who have one

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation June 22, 2016 Don t Forget to Report Certain Foreign Accounts to Treasury by the June 30 Deadline Taxpayers who have one

INNOCENT SPOUSE DEFENSE

INNOCENT SPOUSE DEFENSE First Run Broadcast: August 21, 2012 Live Replay: August 16, 2013 1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes) When a married couple files its tax

INNOCENT SPOUSE DEFENSE First Run Broadcast: August 21, 2012 Live Replay: August 16, 2013 1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes) When a married couple files its tax

3/22/2017. The Iowa 2016 Uncoupling. How We Got Here?

The Iowa 2016 Uncoupling March 22, 2017 How We Got Here? Governor s 2015 limited uncoupling proposal Legislature coupled for one year only - 2015 Governor proposes limited uncoupling for 2016 Legislature

The Iowa 2016 Uncoupling March 22, 2017 How We Got Here? Governor s 2015 limited uncoupling proposal Legislature coupled for one year only - 2015 Governor proposes limited uncoupling for 2016 Legislature

Correspondence Examination

Correspondence Examinations Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 14, 2015 Correspondence Reporting Compliance Programs Two major compliance programs within the Campus

Correspondence Examinations Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 14, 2015 Correspondence Reporting Compliance Programs Two major compliance programs within the Campus

First We Calculate the NOL 7/7/2017. NOL Part 2 Examples. NOL Importance

NOL Part 2 Examples June 21, 2017 NOL Importance Allows taxpayers to maximize the use of deductions and losses not limiting them to a single year A bit of history 2 First We Calculate the NOL 3 1 Example

NOL Part 2 Examples June 21, 2017 NOL Importance Allows taxpayers to maximize the use of deductions and losses not limiting them to a single year A bit of history 2 First We Calculate the NOL 3 1 Example

FOR DOMESTIC VIOLENCE SURVIVORS. Morgan Young Immigration and Poverty Attorney End Domestic Abuse WI

TAX PROTECTIONS FOR DOMESTIC VIOLENCE SURVIVORS Morgan Young Immigration and Poverty Attorney End Domestic Abuse WI Some materials adapted from the National Women s Law Center STARTING THE TAX RETURN 1

TAX PROTECTIONS FOR DOMESTIC VIOLENCE SURVIVORS Morgan Young Immigration and Poverty Attorney End Domestic Abuse WI Some materials adapted from the National Women s Law Center STARTING THE TAX RETURN 1

The Scoop. Agenda. Proposed Legislation 2 3/21/2017. March 22, Deadlines American Health Care Act

The Scoop March 22, 2017 Deadlines Agenda Offer in Compromise Changes Secretary of the Treasury Announces Senior Staff S Corporation Issues IRS Online Accounts SBSE-04-0217-0014 - Pilot Program Auditing

The Scoop March 22, 2017 Deadlines Agenda Offer in Compromise Changes Secretary of the Treasury Announces Senior Staff S Corporation Issues IRS Online Accounts SBSE-04-0217-0014 - Pilot Program Auditing

Innocent Spouse Relief Under IRC Section 6015 Navigating New Tax Rules to Avoid Liability for Divorced, Widowed or Married Clients

Presenting a live 110-minute teleconference with interactive Q&A Innocent Spouse Relief Under IRC Section 6015 Navigating New Tax Rules to Avoid Liability for Divorced, Widowed or Married Clients TUESDAY,

Presenting a live 110-minute teleconference with interactive Q&A Innocent Spouse Relief Under IRC Section 6015 Navigating New Tax Rules to Avoid Liability for Divorced, Widowed or Married Clients TUESDAY,

Ch. 119 LIABILITIES AND ASSESSMENT CHAPTER 119. LIABILITIES AND ASSESSMENT PROCEDURE AND ADMINISTRATION

Ch. 119 LIABILITIES AND ASSESSMENT 61 119.1 CHAPTER 119. LIABILITIES AND ASSESSMENT PROCEDURE AND ADMINISTRATION Sec. 119.1. Payment on notice and demand. 119.2. Assessment. 119.3. Bankruptcy or receivership.

Ch. 119 LIABILITIES AND ASSESSMENT 61 119.1 CHAPTER 119. LIABILITIES AND ASSESSMENT PROCEDURE AND ADMINISTRATION Sec. 119.1. Payment on notice and demand. 119.2. Assessment. 119.3. Bankruptcy or receivership.

7/4/2017. The Scoop. Agenda. Data Breach

The Scoop July 5, 2017 Agenda Data Breach contacts Form 2290 changes Electronic Tax Administration Advisory Committee June 2017 ANNUAL REPORT TO CONGRESS The National Taxpayer Advocate Report to Congress

The Scoop July 5, 2017 Agenda Data Breach contacts Form 2290 changes Electronic Tax Administration Advisory Committee June 2017 ANNUAL REPORT TO CONGRESS The National Taxpayer Advocate Report to Congress

The Scoop. Tax Freedom Day 2016

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation April 20, 2016 Tax Freedom Day 2016 April 24 114 days into the year Tax Freedom Day is the day when the nation as a whole

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation April 20, 2016 Tax Freedom Day 2016 April 24 114 days into the year Tax Freedom Day is the day when the nation as a whole

ALI-ABA Course of Study Tax Controversy Practice: From Administrative Audit Through Litigation

171 ALI-ABA Course of Study Tax Controversy Practice: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 12-13, 2008 Chicago, Illinois Relief

171 ALI-ABA Course of Study Tax Controversy Practice: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 12-13, 2008 Chicago, Illinois Relief

The New Partnership Audit Regime

The New Partnership Audit Regime October 19, 2017 Small Partnerships Current Rules Partnership audits with 10 or fewer qualified partners (e.g., no flow through entities, like LLCs, as partners) are conducted

The New Partnership Audit Regime October 19, 2017 Small Partnerships Current Rules Partnership audits with 10 or fewer qualified partners (e.g., no flow through entities, like LLCs, as partners) are conducted

Form 1040X. Preparing Form 1040X Kristy S. Maitre, Tax Specialist Center for Agricultural Law and Taxation

Preparing Form 1040X Kristy S. Maitre, Tax Specialist Center for Agricultural Law and Taxation What is New with the Form1040X? December 2014 Line 6 has been to allow a list of multiple methods to figure

Preparing Form 1040X Kristy S. Maitre, Tax Specialist Center for Agricultural Law and Taxation What is New with the Form1040X? December 2014 Line 6 has been to allow a list of multiple methods to figure

Injured Spouse / Innocent Spouse

Injured Spouse / Innocent Spouse OVERVIEW: There are similarities and also distinct differences in the law between an injured spouse and an innocent spouse, although in each case a spouse is harmed from

Injured Spouse / Innocent Spouse OVERVIEW: There are similarities and also distinct differences in the law between an injured spouse and an innocent spouse, although in each case a spouse is harmed from

Exemptions and the Share Responsibility Payment. Exemption from What? What Exemptions Are Available? 10/19/2015

Exemptions and the Share Responsibility Payment Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 20, 2015 Exemption from What? Having to have insurance coverage Having to pay

Exemptions and the Share Responsibility Payment Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 20, 2015 Exemption from What? Having to have insurance coverage Having to pay

INNOCENT SPOUSE RELIEF

INNOCENT SPOUSE RELIEF by Carey J. Messina Kean Miller Hawthorne D Armond McCowan & Jarman, L.L.P. P.O. Box 3513 Baton Rouge, LA 70821-3513 (225) 387-0999 www.keanmiller.com The IRS has issued interim

INNOCENT SPOUSE RELIEF by Carey J. Messina Kean Miller Hawthorne D Armond McCowan & Jarman, L.L.P. P.O. Box 3513 Baton Rouge, LA 70821-3513 (225) 387-0999 www.keanmiller.com The IRS has issued interim

Offer-in-Compromise Why or Why Not

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

STATUTE OF LIMITATIONS Analyze This. By LG Brooks Enrolled Agent

The capital of Texas enrolled agents Austin, Texas November 2008 STATUTE OF LIMITATIONS Analyze This By LG Brooks Enrolled Agent I. BIOGRAPHY LG Brooks, BA, EA LG Brooks is an Enrolled Agent and is the

The capital of Texas enrolled agents Austin, Texas November 2008 STATUTE OF LIMITATIONS Analyze This By LG Brooks Enrolled Agent I. BIOGRAPHY LG Brooks, BA, EA LG Brooks is an Enrolled Agent and is the

7/18/2017. The Scoop. Agenda. EA Special Enrollment Exam Fee Increase

The Scoop July 5, 2017 Agenda EIN application restrictions online Notice 2017 38 burdensome regulations PTIN update IRS Funding H.R. 1843, the Restraining Excessive Seizure of Property State News Ohio,

The Scoop July 5, 2017 Agenda EIN application restrictions online Notice 2017 38 burdensome regulations PTIN update IRS Funding H.R. 1843, the Restraining Excessive Seizure of Property State News Ohio,

OUR INSTRUCTOR FOR THE TWO DAY SEMINAR MICHAEL MIRANDA

EXPLORING THE TAX AND PLANNING ASPECTS OF OUR PRIVATE AND PUBLIC RETIREMENT PLAN SYSTEMS WEBINAR PRESENTED BY KRISTY MAITRE AND MICHAEL MIRANDA OCTOBER 10 TH AND 11 TH 2017 1 OUR INSTRUCTOR FOR THE TWO

EXPLORING THE TAX AND PLANNING ASPECTS OF OUR PRIVATE AND PUBLIC RETIREMENT PLAN SYSTEMS WEBINAR PRESENTED BY KRISTY MAITRE AND MICHAEL MIRANDA OCTOBER 10 TH AND 11 TH 2017 1 OUR INSTRUCTOR FOR THE TWO

Innocent Spouse Relief from Interest & Penalty Granted to Sole Earner Despite Contrary Rev Proc

Innocent Spouse Relief from Interest & Penalty Granted to Sole Earner Despite Contrary Rev Proc Joseph Patrick Boyle, TC Memo 2016-87 The Tax Court, rejecting IRS's contention that Code Sec. 6015 innocent

Innocent Spouse Relief from Interest & Penalty Granted to Sole Earner Despite Contrary Rev Proc Joseph Patrick Boyle, TC Memo 2016-87 The Tax Court, rejecting IRS's contention that Code Sec. 6015 innocent

5/16/2017. It s More Than a Number. The Most Common Question At CALT Surrounds the EIN# What is an EIN

It s More Than a Number May 16, 2017 The Federal Identification Number/Employer Identification Number The Most Common Question At CALT Surrounds the EIN# Do You Need an EIN? Do You Need a New EIN? How

It s More Than a Number May 16, 2017 The Federal Identification Number/Employer Identification Number The Most Common Question At CALT Surrounds the EIN# Do You Need an EIN? Do You Need a New EIN? How

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES 1. What is a chapter 7 bankruptcy case and how does it work? A chapter 7 bankruptcy case is a proceeding under federal law

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES 1. What is a chapter 7 bankruptcy case and how does it work? A chapter 7 bankruptcy case is a proceeding under federal law

6/20/2017. The Scoop. Agenda PTIN

The Scoop June 21, 2017 Agenda PTIN Iowa's First Time Homebuyer Reporting Requirements Announced Tax Reform and Debt Limit E-Services Platform Change Delayed Treasury Department's Tax Division, Highlighted

The Scoop June 21, 2017 Agenda PTIN Iowa's First Time Homebuyer Reporting Requirements Announced Tax Reform and Debt Limit E-Services Platform Change Delayed Treasury Department's Tax Division, Highlighted

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE. The IRS Restructuring and Reform Act of 1998.

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

Ridesharing Taxes for Uber and Lyft Drivers

Ridesharing Taxes for Uber and Lyft Drivers August 22, 2017 Agenda Independent Contractor = Business Entity Self Employment Tax Expenses and Recordkeeping Estimated Tax Payments Sales Tax Form 1099 K 2

Ridesharing Taxes for Uber and Lyft Drivers August 22, 2017 Agenda Independent Contractor = Business Entity Self Employment Tax Expenses and Recordkeeping Estimated Tax Payments Sales Tax Form 1099 K 2

3/6/2017. The Scoop. Agenda. Agenda

The Scoop March 8, 2017 Agenda Farm Audits Alimony Audits ID Theft Lock Security Criminal Investigations 2016 Annual Report Trumps Address to Congress Confusion Still Reigns with IRS Decision on ACA Filing

The Scoop March 8, 2017 Agenda Farm Audits Alimony Audits ID Theft Lock Security Criminal Investigations 2016 Annual Report Trumps Address to Congress Confusion Still Reigns with IRS Decision on ACA Filing

Tax Practice National Income Tax Workbook

Tax Practice Chapter 6 pp.157-203 2018 National Income Tax Workbook Tax Practice p. 157 When the IRS Pays a Taxpayer Interest Requesting Technical Advice from IRS Responding to IRS Liens and Levies Installment

Tax Practice Chapter 6 pp.157-203 2018 National Income Tax Workbook Tax Practice p. 157 When the IRS Pays a Taxpayer Interest Requesting Technical Advice from IRS Responding to IRS Liens and Levies Installment

DEALING WITH THE IRS

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency.

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency.

Highlights from the 199A Proposed Regulations

Highlights from the 199A Proposed Regulations August 13, 2018 Kristine A. Tidgren Treasury and the IRS released IRC 199A proposed regulations, REG-107892-18, on August 8, 2018. The regulations will not

Highlights from the 199A Proposed Regulations August 13, 2018 Kristine A. Tidgren Treasury and the IRS released IRC 199A proposed regulations, REG-107892-18, on August 8, 2018. The regulations will not

TAX CONTROVERSY TOOLKIT

TAX CONTROVERSY TOOLKIT Toolkit for Handling a Pro Bono Tax Controversy Texas Young Lawyers Association 2014 Edition Disclaimer: This publication is intended to provide lawyers with current and accurate

TAX CONTROVERSY TOOLKIT Toolkit for Handling a Pro Bono Tax Controversy Texas Young Lawyers Association 2014 Edition Disclaimer: This publication is intended to provide lawyers with current and accurate

The Scoop. Agenda 7/31/2017

The Scoop August 2, 2017 Agenda Tsehay v. Commissioner TC Memo 2016 200 PTIN update Virtual Appeal Conference T.D. 9821, REG 128483 15, Due Dates Prisoner Fraudulent Tax Returns Tax reform Update myra

The Scoop August 2, 2017 Agenda Tsehay v. Commissioner TC Memo 2016 200 PTIN update Virtual Appeal Conference T.D. 9821, REG 128483 15, Due Dates Prisoner Fraudulent Tax Returns Tax reform Update myra

Gleim EA Review Updates to Part Edition, 1st Printing April 2016

Page 1 of 6 Gleim EA Review Updates to Part 3 2016 Edition, 1st Printing April 2016 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. This

Page 1 of 6 Gleim EA Review Updates to Part 3 2016 Edition, 1st Printing April 2016 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. This

Federal Tax Issues. TASFAA Conference October 7, Jim Briggs The Tax Detective

Federal Tax Issues TASFAA Conference October 7, 2015 Jim Briggs The Tax Detective Session Outline 2014 Tax Filing Income Thresholds ITINs/SSN s/w-2 s Tax Filing Status Rules Single Married Joint/Separate

Federal Tax Issues TASFAA Conference October 7, 2015 Jim Briggs The Tax Detective Session Outline 2014 Tax Filing Income Thresholds ITINs/SSN s/w-2 s Tax Filing Status Rules Single Married Joint/Separate

Bankruptcy Questions Answered!

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Taxation of Corporations and their Shareholders. Chapter 17. Tax Penalties. UNC Charlotte Master of Accountancy Program

Taxation of Corporations and their Shareholders Chapter 17 Tax Penalties UNC Charlotte Master of Accountancy Program April 27, 2015 UNC Charlotte MACC Program Chapter 17. Some Important Tax Penalties Page

Taxation of Corporations and their Shareholders Chapter 17 Tax Penalties UNC Charlotte Master of Accountancy Program April 27, 2015 UNC Charlotte MACC Program Chapter 17. Some Important Tax Penalties Page

Trust Fund Recovery. A Tax Resolution Institute Publication 2016

A Tax Resolution Institute Publication 2016 Trust Fund Recovery Facing possible retributions such as civil liability for unpaid employment taxes, including penalties and interest, and possible criminal

A Tax Resolution Institute Publication 2016 Trust Fund Recovery Facing possible retributions such as civil liability for unpaid employment taxes, including penalties and interest, and possible criminal

Pension/Profit Sharing/401(k) Annuity Surrender Request for Qualified Plans With MetLife Tax Reporting Fax:

Annuity Surrender Request for Qualified Plans With MetLife Tax Reporting Fax:") Return this form to: MetLife PO Box 9146 Des Moines, IA 50306-9146 POLICY SERVICE OFFICE MetLife Insurance Company of Connecticut Pension/Profit Sharing/401(k) Annuity Surrender Request for Qualified Plans

Return this form to: MetLife PO Box 9146 Des Moines, IA 50306-9146 POLICY SERVICE OFFICE MetLife Insurance Company of Connecticut Pension/Profit Sharing/401(k) Annuity Surrender Request for Qualified Plans

Centralized Partnership Audit Regime: Rules for Election Under Sections 6226 and

This document is scheduled to be published in the Federal Register on 12/19/2017 and available online at https://federalregister.gov/d/2017-27071, and on FDsys.gov [4830-01-p] DEPARTMENT OF THE TREASURY

This document is scheduled to be published in the Federal Register on 12/19/2017 and available online at https://federalregister.gov/d/2017-27071, and on FDsys.gov [4830-01-p] DEPARTMENT OF THE TREASURY

Ch. 35 TAX EXAMINATIONS AND ASSESSMENTS CHAPTER 35. TAX EXAMINATIONS AND ASSESSMENTS

Ch. 35 TAX EXAMINATIONS AND ASSESSMENTS 61 35.1 CHAPTER 35. TAX EXAMINATIONS AND ASSESSMENTS Sec. 35.1. Tax examinations and assessments. 35.2. Interest, additions, penalties, crimes, and offenses. 35.3.

Ch. 35 TAX EXAMINATIONS AND ASSESSMENTS 61 35.1 CHAPTER 35. TAX EXAMINATIONS AND ASSESSMENTS Sec. 35.1. Tax examinations and assessments. 35.2. Interest, additions, penalties, crimes, and offenses. 35.3.

1/23/2018. The Scoop. Agenda. Agenda

The Scoop January 24, 2018 Agenda The EIC Election to Use PYEI Due to Disaster Declaration Denial of Passport in Case of Certain Tax Delinquencies U.S. Supreme Court Agrees to Hear South Dakota v. Wayfair

The Scoop January 24, 2018 Agenda The EIC Election to Use PYEI Due to Disaster Declaration Denial of Passport in Case of Certain Tax Delinquencies U.S. Supreme Court Agrees to Hear South Dakota v. Wayfair

Earned Income Credit i

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Instructions for Form 990-BL

Instructions for Form 990-BL (Rev. December 2008) Information and Initial Excise Tax Return for Black Lung Benefit Trusts and Certain Related Persons Department of the Treasury Internal Revenue Service

Instructions for Form 990-BL (Rev. December 2008) Information and Initial Excise Tax Return for Black Lung Benefit Trusts and Certain Related Persons Department of the Treasury Internal Revenue Service

5/30/2017. The Scoop. Agenda. New Medicare Cards Are on the Way

The Scoop May 31, 2017 Agenda New Medicare Cards Are on the Way Fraudsters Exploited Lax Security at Equifax s TALX Payroll Division Opportunity Coming to Participate in New Correspondence Examination

The Scoop May 31, 2017 Agenda New Medicare Cards Are on the Way Fraudsters Exploited Lax Security at Equifax s TALX Payroll Division Opportunity Coming to Participate in New Correspondence Examination

Topical Index to Chapter 3 Statute of Limitations

Topical Index to Chapter 3 Statute of Limitations 3.01 Limitation Code Sections 6501 Assessment 3 years 6502 Collection 10years 6511 Refund filing 2-3 years 6672/ 6501 Trust funds 3 years 1311 Mitigation

Topical Index to Chapter 3 Statute of Limitations 3.01 Limitation Code Sections 6501 Assessment 3 years 6502 Collection 10years 6511 Refund filing 2-3 years 6672/ 6501 Trust funds 3 years 1311 Mitigation

BOARD OF EQUALIZATION STATE OF CALIFORNIA ) ) ) ) ) ) ) )

) ) ) ) ) ) )") STATE BOARD OF EQUALIZATION In the Matter of the Appeal of: PEDRO V. DATING AND SIMONA V. DATING Representing the Parties: For Appellants: For Franchise Tax Board: Counsel for the Board of Equalization:

STATE BOARD OF EQUALIZATION In the Matter of the Appeal of: PEDRO V. DATING AND SIMONA V. DATING Representing the Parties: For Appellants: For Franchise Tax Board: Counsel for the Board of Equalization:

REPRESENTING NON-FILERS. Journal of the National Association of Enrolled Agents

REPRESENTING NON-FILERS Journal of the National Association of Enrolled Agents Published September/October 2007 By Howard S. Levy Non-filers are often overwhelmed by their predicament. Many times they

REPRESENTING NON-FILERS Journal of the National Association of Enrolled Agents Published September/October 2007 By Howard S. Levy Non-filers are often overwhelmed by their predicament. Many times they

Conflicts of Interest Concerns for Tax Professionals. Kyle Coleman

Conflicts of Interest Concerns for Tax Professionals Presented By: Kyle Coleman Coleman, Anastopulos & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX 75248 Phone: (972) 810 4380 Fax: (972)

Conflicts of Interest Concerns for Tax Professionals Presented By: Kyle Coleman Coleman, Anastopulos & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX 75248 Phone: (972) 810 4380 Fax: (972)

Table of Contents. About This Book How To Use This Book Foreword Acknowledgments Preface

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Tax Issues in Foreclosure Cases

Tax Issues in Foreclosure Cases September 19, 2017 Christopher Fasano Staff Attorney Mobilization for Justice, Inc. cfasano@mfjlegal.org Contents of Presentation I. Income from the discharge of indebtedness

Tax Issues in Foreclosure Cases September 19, 2017 Christopher Fasano Staff Attorney Mobilization for Justice, Inc. cfasano@mfjlegal.org Contents of Presentation I. Income from the discharge of indebtedness

2011 INSTRUCTIONS FOR FILING RI-1040NR

2011 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2011 Rhode Island Nonresident

2011 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2011 Rhode Island Nonresident

STATEMENT OF FINANCIAL INTERESTS

FORM 1 2017 STATEMENT OF FINANCIAL INTERESTS Please print or type your name, mailing address, agency name, and position below: FOR OFFICE USE ONLY: LAST NAME -- FIRST NAME -- MIDDLE NAME : MAILING ADDRESS

FORM 1 2017 STATEMENT OF FINANCIAL INTERESTS Please print or type your name, mailing address, agency name, and position below: FOR OFFICE USE ONLY: LAST NAME -- FIRST NAME -- MIDDLE NAME : MAILING ADDRESS

ADOPTED REGULATION OF THE DEPARTMENT OF TAXATION. LCB File No. R Effective April 30, 2004

ADOPTED REGULATION OF THE DEPARTMENT OF TAXATION LCB File No. R224-03 Effective April 30, 2004 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted. AUTHORITY:

ADOPTED REGULATION OF THE DEPARTMENT OF TAXATION LCB File No. R224-03 Effective April 30, 2004 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted. AUTHORITY:

Payment. Billing Summary $9,999.99

Department of the Treasury Internal Revenue Service P.O. Box 480 Holtsville, NY 11742-0480 s018999546711s JOHN AND MARY SMITH 123 N HARRIS ST HARVARD, TX 12345 To contact us Phone 1-800-829-0922 Your caller

Department of the Treasury Internal Revenue Service P.O. Box 480 Holtsville, NY 11742-0480 s018999546711s JOHN AND MARY SMITH 123 N HARRIS ST HARVARD, TX 12345 To contact us Phone 1-800-829-0922 Your caller

Partnership Audits. Crowell & Moring, LLP. Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration)

") Partnership Audits Crowell & Moring, LLP Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration) Jennifer Ray, Partner, Crowell & Moring, LLP September 29, 2016

Partnership Audits Crowell & Moring, LLP Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration) Jennifer Ray, Partner, Crowell & Moring, LLP September 29, 2016

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-third Edition (June 2015)

") Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

HOUSE BILL No As Amended by House Committee

Session of 0 As Amended by House Committee HOUSE BILL No. 0 By Committee on Taxation - 0 0 0 AN ACT concerning taxation; relating to the use of a debt collection agency to collect delinquent taxes; time

Session of 0 As Amended by House Committee HOUSE BILL No. 0 By Committee on Taxation - 0 0 0 AN ACT concerning taxation; relating to the use of a debt collection agency to collect delinquent taxes; time