organization provides in consideration Use Form 4506-A to request:

|

|

|

- Kelley Hood

- 5 years ago

- Views:

Transcription

1

2 Goods or services a donee Through the IRS Note that a section 527 political organization provides in consideration Use Form 4506-A to request: TIP organization (and an for a payment by a taxpayer include organization filing Form 990-PF) goods or services provided in a year A copy of an exempt or political must disclose their Schedule B (Form other than the year in which the donor organization s return, report, notice, or 990, 990-EZ, or 990-PF). See the makes the payment to the donee exemption application; Instructions for Schedule B. organization. An inspection of a return, report, The penalties discussed in General Intangible religious benefits. notice, or exemption application at an Instruction K also apply to section 527 Intangible religious benefits must be IRS office. political organizations (Rev. Rul. provided by organizations organized The IRS can provide copies of , I.R.B. 903). exclusively for religious purposes. exempt organization returns on a Public inspection and distribution of Examples include: compact disc (CD). Requesters can applications for tax exemption and Admission to a religious ceremony, order the complete set (all Forms 990 annual information returns of and and 990-EZ or all Forms 990-PF filed tax-exempt organizations. Under De minimis tangible benefits, such as for a year) or a partial set by state or by Regulations sections (d)-1 wine, provided in connection with a month. For more information on the through (d)-3, a tax-exempt religious ceremony. cost and how to order CDs, call the organization must: Distributing organization as TEGE Customer Account Services Make its application for recognition of donee. An organization described in toll-free number ( ) or exemption and its annual information section 170(c), or an organization write to the IRS in Cincinnati, OH, at returns available for public inspection described as a Principal Combined the address in General Instruction A. without charge at its principal, regional, Fund Organization for purposes of the and district offices during regular Combined Federal Campaign, that The IRS may not disclose portions of business hours. receives a payment made as a an exemption application relating to any Make each annual information return contribution is treated as a donee trade secrets, etc. Additionally, the IRS available for a period of 3 years organization even if the organization may not disclose the names and beginning on the date the return is distributes the amount received to one addresses of contributors. See the required to be filed (determined with or more organizations described in Instructions for Schedule B (Form 990, regard to any extension of time for section 170(c). 990-EZ, or 990-PF) for more filing) or is actually filed, whichever is Penalties. A charity that knowingly information about the disclosure of that later. provides a false substantiation schedule. Provide a copy without charge, (for acknowledgment to a donor may be Forms 990 or 990-EZ can only be Form 990-T, this requirement only subject to the penalties under section requested for section 527 organizations applies to Form 990-T s filed after 6701 for aiding and abetting an for tax years beginning after June 30, August 17, 2006) other than a understatement of tax liability reasonable fee for reproduction and Charities that fail to provide the actual postage costs, of all or any part A return, report, notice, or exemption required disclosure statement for a quid of any application or return required to application may be inspected at an IRS pro quo contribution of more than $75 be made available for public inspection office free of charge. Copies of these will incur a penalty of $10 per to any individual who makes a request items may also be obtained through the contribution, not to exceed $5,000 per for such copy in person or in writing organization as discussed in the fundraising event or mailing. The (except as provided in Regulations following section. charity may avoid the penalty if it can sections (d)-2 and -3). show that the failure was due to Through the Organization Definitions. reasonable cause (section 6714). Public inspection and distribution of Tax-exempt organization is any certain returns of unrelated business organization that is described in section M. Public Inspection of income. Section 501(c)(3) 501(c) or (d) and is exempt from organizations that are required to file taxation under section 501(a). The term Returns, etc. Form 990-T after August 17, 2006, tax-exempt organization also includes Some members of the public rely on must make Form 990-T available for any section 4947(a)(1) nonexempt Form 990, or Form 990-EZ, as the public inspection under section charitable trust or nonexempt private primary or sole source of information 6104(d)(1)(A)(ii). foundation that is subject to the about a particular organization. How the reporting requirements of section public perceives an organization in Public inspection and distribution of such cases may be determined by the Application for tax exemption returns and reports for a political information presented on its returns. includes: organization. Section 527 political Any prescribed application form An organization s completed Form organizations required to file Form 990, (such as Form 1023 or Form 1024), 990, or Form 990-EZ, is available for or Form 990-EZ, must, in general, All documents and statements the public inspection as required by section make their Form 8871, 8872, 990, or IRS requires an applicant to file with the Schedule B (Form 990, 990-EZ, 990-EZ available for public inspection in form, or 990-PF) is open for public inspection the same manner as annual information Any statement or other supporting for section 527 organizations filing returns of section 501(c) organizations document submitted in support of the Form 990 or Form 990-EZ. For other and 4947(a)(1) nonexempt charitable application, and organizations that file Form 990 or trusts are made available. See the Any letter or other document issued Form 990-EZ, parts of Schedule B may public inspection rules for Tax-exempt by the IRS concerning the application. be open to public inspection. Form organization, later. Generally, Form 990-T filed after August 17, 2006, by a 8871 and Form 8872 are available for Application for tax exemption 501(c)(3) organization to report any inspection and printing from the does not include: unrelated business income, is also Internet. The website address for both Any application for tax exemption available for public inspection and of these forms is / filed before July 15, 1987, unless the disclosure. political/article/0,,id=109332,00.html. organization filing the application had a -12- General Instructions for Form 990 and Form 990-EZ

3 copy of the application on July 15, managing the exempt function activities day following the day that the unusual 1987; at the site. circumstances cease to exist, or the 5th In the case of a tax-exempt business day after the date of the organization other than a private Special rules relating to public request, whichever occurs first. foundation, the name and address of inspection. any contributor to the organization; or Unusual circumstances include: Any material that is not available for Permissible conditions on public Requests received that exceed the public inspection under section inspection. A tax-exempt organization s daily capacity to make organization: copies; If there is no prescribed May have an employee present in application form, see Requests received shortly before the! the room during an inspection. CAUTION Regulations section end of regular business hours that Must allow the individual conducting (d)-1(b)(4)(i). require an extensive amount of the inspection to take notes freely copying; or Annual information return during the inspection. Must allow the individual to Requests received on a day when includes: An exact copy of the Form 990, or photocopy the document at no charge, the organization s managerial staff Form 990-EZ, filed by a tax-exempt if the individual provides photocopying capable of fulfilling the request is organization as required by section equipment at the place of inspection. conducting special duties, such as student registration or attending an Organizations that do not Any amended return the organization off-site meeting or convention, rather maintain permanent offices. A files with the IRS after the date the than its regular administrative duties. tax-exempt organization with no original return is filed. permanent office: Agents for providing copies. For An exact copy of Form 990-T if one is Must make its application for tax filed by a 501(c)(3) organization. rules relating to use of agents to exemption and its annual information provide copies, see Regulations The copy must include all returns available for inspection at a sections (d)-1(d)(1) and (2). information furnished to the IRS on reasonable location of its choice. Form 990, Form 990-EZ, or Form 990-T Must permit public inspection within a Request for copies in writing. A as well as all schedules, attachments, reasonable amount of time after tax-exempt organization must honor a and supporting documents, except for receiving a request for inspection written request for a copy of documents the name and address of any (normally not more than 2 weeks) and (or the requested part) required under contributor to the organization. See the at a reasonable time of day. section 6104(d) if the request: Instructions for Schedule B (Form 990, May mail, within 2 weeks of receiving 1. Is addressed to, and delivered by 990-EZ, or 990-PF). the request, a copy of its application for mail, electronic mail, facsimile, or a Annual returns more than 3 years tax exemption and annual information private delivery service, as defined in old. An annual information return does returns to the requester instead of section 7502(f), to a principal, regional, not include any return after the allowing an inspection. or district office of the organization; and expiration of 3 years from the date the May charge the requester for copying and actual postage costs only if the 2. Sets forth the address to which return is required to be filed (including requester consents to the charge. the copy of the documents should be any extension of time that has been sent. granted for filing such return) or is An organization that has a actually filed, whichever is later. permanent office, but has no office hours, or very limited hours during Time and manner of fulfilling written If an organization files an amended certain times of the year, must make its requests. return, however, the amended return must be made available for a period of documents available during those IF the organization.. THEN the organization 3 years beginning on the date it is filed periods when office hours are limited, with the IRS. or not available, as though it were an Receives a written Must mail the copy of organization without a permanent request for a copy, the requested Local or subordinate office. documents (or the organizations. For rules relating to requested parts) within annual information returns of local or Special rules relating to copies. 30 days from the date it subordinate organizations, see receives the request. Time and place for providing Regulations section copies in response to requests made (d)-1(f)(2). Mails the copy of the Is deemed to have in-person. A tax-exempt organization requested document, provided the copy on the Regional or district offices. A must: postmark date or private regional or district office is any office of Provide copies of required delivery mark (if sent by a tax-exempt organization, other than documents under section 6104(d) in certified or registered its principal office, that has paid response to a request made in person mail, the date of registration or the date employees, whether part-time or at its principal, regional, and district of the postmark on the full-time, whose aggregate number of offices during regular business hours. sender s receipt). paid hours a week are normally at least Provide such copies to a requester 120. on the day the request is made, except Requires payment in Is required to provide for unusual circumstances (see below). advance, the copies within 30 A site is not considered a regional or days from the date it district office, however, if: Unusual circumstances. In the receives payment. The only services provided at the site case of an in-person request, where further exempt purposes (such as day unusual circumstances exist so that Receives a request or Is deemed to have care, health care, scientific research, or fulfilling the request on the same payment by mail, received it 7 days after medical research); and business day causes an unreasonable the date of the The site does not serve as an office burden to the tax-exempt organization, postmark, absent evidence to the contrary. for management staff, other than the organization must provide the managers who are involved solely in copies no later than the next business General Instructions for Form 990 and Form 990-EZ -13-

4 Receives a request Is deemed to have Documents to be provided by each local or subordinate organization transmitted by electronic received it the day the regional and district offices. Except included in the group return, the local or mail or facsimile, request is transmitted as otherwise provided, a regional or subordinate organization receiving the successfully. district office of a tax-exempt request may omit any schedules organization must satisfy the same relating only to other organizations Receives a written Must notify the rules as the principal office with respect included in the group return. request without payment requester of the to allowing public inspection and or with an insufficient prepayment policy and The local or subordinate payment, when payment the amount due within 7 providing copies of its application for organization must permit public in advance is required, days from the date of tax exemption and annual information inspection, or comply with a request for the request s receipt. returns. copies made in person, within a A regional or district office is not reasonable amount of time (normally Receives consent from May provide a copy of required, however, to make its annual an individual making a the requested document not more than 2 weeks) after receiving request, exclusively by electronic information return available for a request made in person for public mail (the material is inspection or to provide copies until 30 inspection or copies and at a provided on the date the days after the date the return is reasonable time of day. organization required to be filed (including any successfully transmits In a case where the requester seeks extension of time that is granted for the electronic mail). inspection, the local or subordinate filing such return) or is actually filed, organization may mail a copy of the whichever is later. applicable documents to the requester Request for a copy of parts of a Documents to be provided by within the same time period instead of document. A tax-exempt organization local and subordinate organizations. allowing an inspection. In such a case, must fulfill a request for a copy of the the organization may charge the organization s entire application for tax Applications for tax exemption. requester for copying and actual exemption or annual information return Except as otherwise provided, a postage costs only if the requester or any specific part or schedule of its tax-exempt organization that did not file consents to the charge. application or return. A request for a its own application for tax exemption copy of less than the entire application If the local or subordinate (because it is a local or subordinate or less than the entire return must organization receives a written request organization covered by a group specifically identify the requested part for a copy of its annual information exemption letter) must, upon request, or schedule. return, it must fulfill the request by make available for public inspection, or providing a copy of the group return in Fees for copies. A tax-exempt provide copies of, the application the time and manner specified in the organization may charge a reasonable submitted to the IRS by the central or paragraph earlier, Request for copies in fee for providing copies. parent organization to obtain the group writing. exemption letter and those documents Before the organization provides the which were submitted by the central or The requester has the option of documents, it may require that the parent organization to include the local requesting from the central or parent individual requesting copies of the or subordinate organization in the group organization, at its principal office, documents pay the fee. If the exemption letter. inspection or copies of group returns organization has provided an individual filed by the central or parent making a request with notice of the fee, However, if the central or parent organization. The central or parent and the individual does not pay the fee organization submits to the IRS a list or organization must fulfill such requests within 30 days, or if the individual pays directory of local or subordinate in the time and manner specified in the the fee by check and the check does organizations covered by the group paragraphs, Special rules relating to not clear upon deposit, the organization exemption letter, the local or public inspection and Special rules may disregard the request. subordinate organization is required to relating to copies earlier. provide only the application for the Form of payment (A) Request group exemption ruling and the pages Failure to comply. If an made in person. If a tax-exempt of the list or directory that specifically organization fails to comply with the organization charges a fee for copying, refer to it. The local or subordinate requirements specified in this it must accept payment by cash and organization must permit public paragraph, the penalty provisions of money order for requests made in inspection, or comply with a request for sections 6652(c)(1)(C), 6652(c)(1)(D), person. The organization may accept copies made in person, within a and 6685 apply. other forms of payment, such as credit reasonable amount of time (normally Making applications and returns cards and personal checks. not more than 2 weeks) after receiving widely available. A tax-exempt (B) Request made in writing. If a a request made in person for public organization is not required to comply tax-exempt organization charges a fee inspection or copies and at a with a request for a copy of its for copying and postage, it must accept reasonable time of day. See application for tax exemption or an payment by certified check, money Regulations section (d)-1(f) for annual information return if the order, and either personal check or further information. organization has made the requested credit card for requests made in writing. Annual information returns. A document widely available (see below). The organization may accept other local or subordinate organization that An organization that makes its forms of payment. does not file its own annual information application for tax exemption and/or Avoidance of unexpected fees. return (because it is affiliated with a annual information return widely Where a tax-exempt organization does central or parent organization that files available must nevertheless make the not require prepayment and a requester a group return) must, upon request, document available for public does not enclose payment with a make available for public inspection, or inspection as required under request, an organization must receive provide copies of, the group returns Regulations section (d)-1(a). consent from a requester before filed by the central or parent A tax-exempt organization makes its providing copies for which the fee organization. application for tax exemption and/or an charged for copying and postage However, if the group return includes annual information return widely exceeds $20. separate schedules with respect to available if the organization complies -14- General Instructions for Form 990 and Form 990-EZ

5 with the Internet posting requirements and the notice requirements given Tax-exempt organization subject to harassment campaign. If the Director N. Disclosures Regarding below. EO Examination (or designee) Certain Information and Internet posting. A tax-exempt determines that the organization is Services Furnished organization can make its application being harassed, a tax-exempt organization is not required to comply A section 501(c) organization that offers for tax exemption and/or an annual with any request for copies that it to sell or solicits money for specific information return widely available by reasonably believes is part of a information or for a routine service for posting the document on a World Wide harassment campaign. any individual that could be obtained by Web page that the tax-exempt such individual from a federal organization establishes and maintains government agency free or for a or by having the document posted, as Whether a group of requests nominal charge, must disclose that fact part of a database of similar documents constitutes a harassment campaign conspicuously when making such offer of other tax-exempt organizations, on a depends on the relevant facts and or solicitation. Any organization that World Wide Web page established and circumstances such as: intentionally disregards this requirement maintained by another entity. The will be subject to a penalty for each day document will be considered widely A sudden increase in requests; an on which the offers or solicitations are available only if: extraordinary number of requests by made. The penalty imposed for a The World Wide Web page through form letters or similarly worded particular day is the greater of $1,000 which it is available clearly informs correspondence; hostile requests; or 50% of the total cost of the offers readers that the document is available evidence showing bad faith or and solicitations made on that day that and provides instructions for deterrence of the organization s exempt lacked the required disclosure (section downloading it; purpose; prior provision of the 6711). The document is posted in a format requested documents to the purported that, when accessed, downloaded, harassing group; and a demonstration viewed, and printed in hard copy, that the organization routinely provides O. Disclosures Regarding exactly reproduces the image of the copies of its documents upon request. Certain Transactions and application for tax exemption or annual information return as it was originally Relationships filed with the IRS, except for any A tax-exempt organization may In their annual returns on Schedule A information permitted by statute to be disregard any request for copies of all (Form 990 or 990-EZ), section withheld from public disclosure; and or part of any document beyond the 501(c)(3) organizations must disclose Any individual with access to the first two received within any 30-day information regarding their direct or Internet can access, download, view, period or the first four received within indirect transfers to, and other direct or and print the document without special any 1-year period from the same indirect relationships with, other section computer hardware or software individual or the same address, 501(c) organizations (except other required for that format (other than regardless of whether the Director EO section 501(c)(3) organizations) or software that is readily available to Examination (or designee) has section 527 political organizations members of the public without payment determined that the organization is (section 6033(b)(9)). This provision of any fee) and without payment of a subject to a harassment campaign. helps prevent the diversion or fee to the tax-exempt organization or to expenditure of a section 501(c)(3) another entity maintaining the World A tax-exempt organization may organization s funds for purposes not Wide Web page. apply for a determination that it is the intended by section 501(c)(3). All subject of a harassment campaign and section 501(c)(3) organizations must Reliability and accuracy. In order that compliance with requests that are maintain records regarding all such for the document to be widely available part of the campaign would not be in transfers, transactions, and through an Internet posting, the entity the public interest by submitting a relationships. See also General maintaining the World Wide Web page signed application to the Director EO Instruction K regarding penalties. must have procedures for ensuring the reliability and accuracy of the document Examination (or designee) for the area that it posts on the page and must take where the organization s principal office P. Intermediate Sanction reasonable precautions to prevent is located. Regulations Excess alteration, destruction, or accidental loss of the document when posted on In addition, the organization may Benefit Transactions its page. In the event that a posted suspend compliance with any request it The intermediate sanction regulations document is altered, destroyed, or lost, reasonably believes to be part of the are important to the exempt the entity must correct or replace the harassment campaign until it receives a organization community as a whole, document. response to its application for a and for ensuring compliance in this Notice requirement. If a harassment campaign determination. area. The rules provide a roadmap by tax-exempt organization has made its However, if the Director EO which an organization may steer clear application for tax exemption and/or an Examination (or designee) determines of situations that may give rise to annual information return widely that the organization did not have a inurement. available, it must notify any individual reasonable basis for requesting a Under section 4958, any disqualified requesting a copy where the determination that it was subject to a person who benefits from an excess documents are available (including the harassment campaign or reasonable benefit transaction with an applicable address on the World Wide Web, if belief that a request was part of the tax-exempt organization is liable for a applicable). If the request is made in campaign, the officer, director, trustee, 25% tax on the excess benefit. The person, the organization must provide employee, or other responsible disqualified person is also liable for a such notice to the individual individual of the organization remains 200% tax on the excess benefit if the immediately. If the request is made in liable for any penalties for not providing excess benefit is not corrected by a writing, the notice must be provided the copies in a timely fashion. See certain date. Also, organization within 7 days of receiving the request. Regulations section (d)-3. managers who participate in an excess General Instructions for Form 990 and Form 990-EZ -15-

6

7

8

9

10

11

12

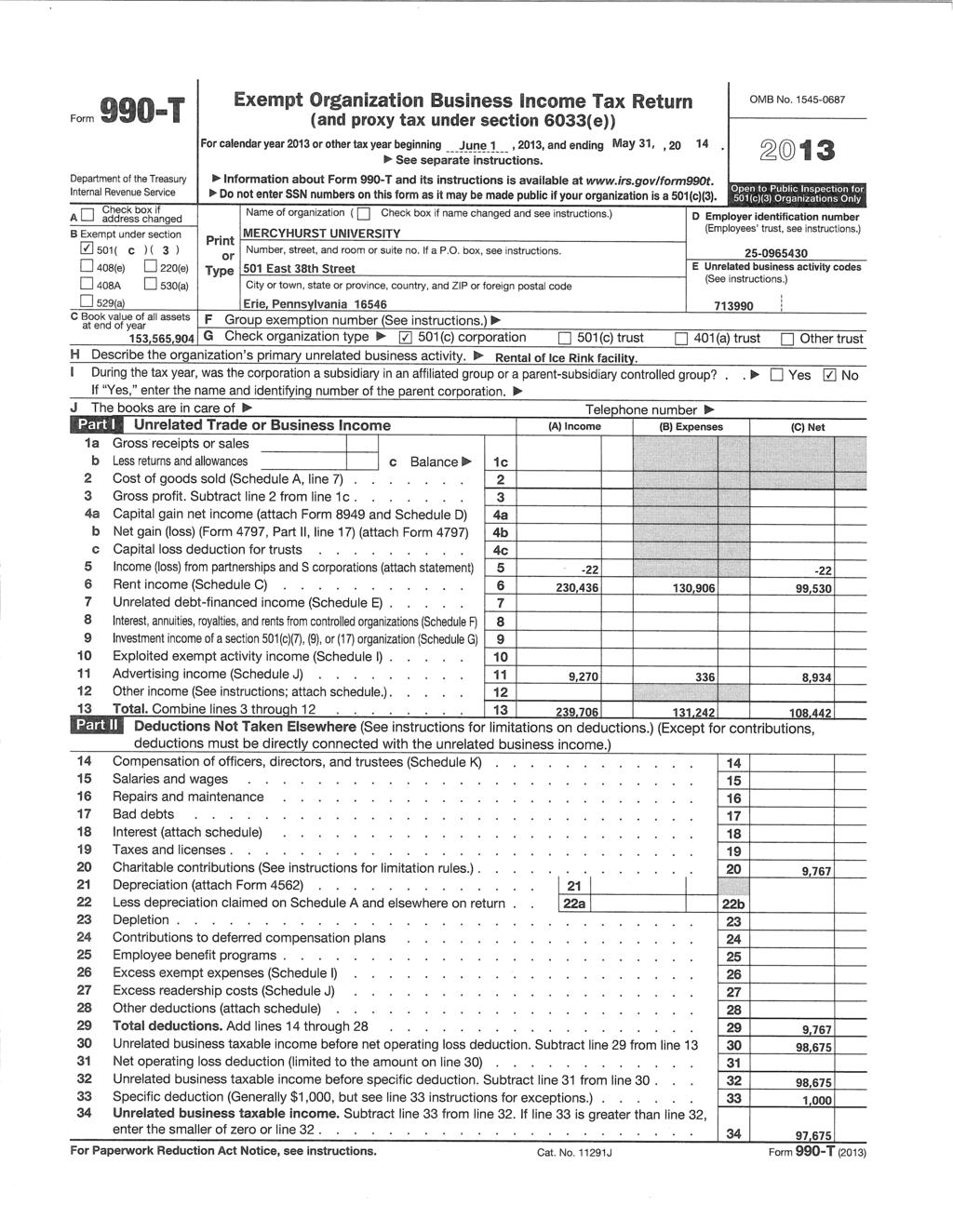

13 MERCYHURST UNIVERSITY FORM 990T - SCHEDULE INCOME (LOSS) FROM PARTNERSHIPS AND S-CORPORATIONS - PART I - LINE COMMON SENSE INVESTORS II, L.P. $ (22.00) CHARITABLE CONTRIBUTIONS - PART II - LINE TOTAL CHARITABLE CONTRIBUTIONS MADE BY THE UNIVERSITY $ 73, UNRELATED BUSINESS TAXABLE INCOME - FORM 990T - PART 1 - LINE 34 97,675 10% LIMITATION 9,767 GREATER OF TOTAL OR 10% LIMITATION (REPORTED ON PART II - LINE 20) CAPITAL LOSS CARRYOVER - SCHEDULE D - PART 1 - LINE UNUSED LOSS FROM THE PRIOR YEAR - ESTIMATED K-1 (REPORTED ON 2012 RETURN) $ (15,744.00) ADDITIONAL UNUSED LOSS FROM THE PRIOR YEAR - FROM FINAL K-1 - CURRENT YEAR CAPITAL GAIN 1, AMOUNT CARRIED FORWARD SUBSEQUENT YEAR $ (14,727.00)

14 MERCYHURST UNIVERSITY FORM 990T - SCHEDULE ICE CENTER EXPENSES EXP TYPE FYE EXPENSES % ALLOCATION TO UNRELATED INCOME UBTI EXPENSES SALARIES FT : ICE CENTER : ER : CUF V 99, % 39,866 SALARIES PT : ICE CENTER : ER : CUF V 28, % 11,226 ALLOCATED FRINGE BENEFITS : ICE CENTER : E V 34, % 13,900 BOOKS : ICE CENTER : ER : CUF V % - CONTRACT SERV. : ICE CENTER : ER : CUF V % 375 COPYING : ICE CENTER : ER : CUF F % 16 POSTAGE : ICE CENTER : ER : CUF F % - RENT/LEASE EQUIPMENT : ICE CENTER : ER : CUF F 1, % 283 REPAIR & MAINT : ICE CENTER : ER : CUF F 40, % 6,715 SUPPLIES : ICE CENTER : ER : CUF F 9, % 1,522 TELEPHONE : ICE CENTER : ER : CUF F % - TRAVEL & LIVING : ICE CENTER : ER : CUF V % 91 NON CAP EQUIP <$1,000 : ICE CENTER : ER : V 15, % 6,342 UTIL/ELECTRIC : ICE CENTER : ER : CUF F 76, % 12,657 UTIL/NATL GAS : ICE CENTER : ER : CUF F 27, % 4, , ADD: INTEREST F 22, % 3,671 ADD: INSURANCE F 3, % 495 ADD: GENERAL OVERHEAD ALLOCATION (20%) F 89, % 14,790 ADD: DEPRECIATION (FORM 4562) F 87, % 14,415 $ 537, $ 130,906 The formula for overhead is 20% of the total, before overhead is added in. 447,815.30

15 MERCYHURST UNIVERSITY FORM 990T - SCHEDULE ICE CENTER INTEREST EXPENSE EXP TYPE FYE EXPENSES PRIMARY FINANCING: 1991 BOND ISSUE 1,250, REFINANCING: 1993 BOND ISSUE: OUTSTANDING ON 1991 BOND ISSUE 1,250, FACE AMOUNT OF 1993 ISSUE 23,715, PORTION OF PRIMARY FINANCING WITHIN 1993 BOND ISSUE 5.27% 2004 BOND ISSUE: OUTSTANDING ON 1993 BOND ISSUE WHEN REFINANCED 17,880, FACE AMOUNT OF 2004 ISSUE 18,365, PORTION OF 1993 WITHIN 2004 BOND ISSUE 97.36% PORTION OF PRIMARY FINANCING WITHIN 2004 BOND ISSUE 5.13% % ALLOCATION TO UNRELATED INCOME UBTI EXPENSES INTEREST EXPENSE FOR ON 2004 BOND ISSUE 384, SHARE ATTRIBUTABLE TO ICE CENTER (2004 ISSUE) 5.13% INTEREST ATTRIBUTABLE TO ICE CENTER F $ 19, % $ 19, FINANCING of ICE CENTER ADDITIONS : 2001 BOND ISSUE 300, FACE AMOUNT OF 2001 ISSUE 5,500, PORTION OF PRIMARY FINANCING WITHIN 2001 BOND ISSUE 5.45% INTEREST EXPENSE FOR ON 2011 BOND ISSUE 114, SHARE ATTRIBUTABLE TO ICE CENTER (2011 ISSUE) 2.16% INTEREST ATTRIBUTABLE TO ICE CENTER F $ 2, % $ 2, TOTAL INTEREST EXPENSE $ 22,232.32

16 MERCYHURST UNIVERSITY FORM 990T - SCHEDULE ICE CENTER DEPRECIATION BUILDINGS CARRYING 2014 BOOK 52-xx ADJ 52-xx BOOK VALUE ADDITIONS VALUE ACCM DEPR FOR ASSET DEPR EXP ACCM DEPR VALUE DESCRIPTION METH LIFE 6/1/13 (DISPOSITIONS) 5/31/14 6/1/13 DISPOSAL 5/31/14 5/31/14 5/31/ MERCYHURST ICE CENTER SL 39 1,509, ,509, , , , , MERCYHURST ICE CENTER SL 39 35, , , , , MERCYHURST ICE CENTER SL , , , , , , MIC - BLOCK STORAGE BUILDING SL 39 16, , , , , ICE CENTER ADDITION SL , , , , , , ICE CENTER ADDITION SL 39 71, , , , , , ICE CENTER - LOCKERS SL , , , , , , ICE CENTER - ROOF SL 39 8, , , , , ICE CENTER - GENERAL SL 39 7, , , ICE CENTER - GENERAL SL 39 82, , , , , , ICE CENTER - WEIGHT ROOM SL , , , , , , ICE CENTER - ROOF INSULATION SL 39 12, , , ,098, ,098, ,193, , ,272, ,825, EQUIPMENT 9/1/04 ICE MACHINE MACRS 7 4, , , , /27/98 ZAMBONI MACRS 7 53, , , , /31/07 BOARDS & GLASS MACRS 7 68, , , , , /31/07 BOARDS & GLASS SEC , , , , , , , , , ,331, ,331, ,419, , ,506, ,825,423.14

17 MERCYHURST UNIVERSITY FORM 990T - SCHEDULE ICE CENTER USAGE SPACE DIRECT SHARED TOTAL USAGE Men's Hockey 3, % 14.08% 21.73% Women's Hockey 3, % 14.34% 22.40% Club Hockey % 4.90% 6.35% Men's Golf % 0.00% 0.08% Women's Golf % 0.00% 0.08% Men's Soccer % 0.00% 0.30% Women's Soccer % 0.00% 0.78% Baseball % 0.00% 0.58% Football % 0.00% 0.14% Men's Lacrosse % 0.00% 0.20% Mercyhurst Student Skating % 2.38% 2.38% Concessions % 0.00% 0.54% Shared Use Area 31, % % 0.00% RELATED USE 39, % % 55.56% Unrelated Use 1, % 40.01% 44.44% 41, % 0.00% % SHARED USE ALLOCATION (ICE TIME) Ice Hours % of Ice Time % of Total Shared Use Men's Hockey % 12.65% Women's Hockey % 13.10% Club Hockey % 4.90% Mercyhurst Student Skating % 2.38% Varsity Hockey Camps % 2.67% Fundraising Events % 0.00% Unrelated 1, % 40.01% 2, % 75.72% Related Use Hours Unrelated Use Hours Total Hours 7, , , USEAGE ALLOCATION - FIXED EXPENSES 83.49% 16.51% %

-8- General Instructions for Form 990 and Form 990-EZ

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $250 or value of similar

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $250 or value of similar

-8- General Instructions for Form 990 and Form 990-EZ

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $250 or value of similar

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $250 or value of similar

-8- General Instructions for Form 990 and Form 990-EZ

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $25 or value of similar

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $25 or value of similar

Brett R. Harris, Esq.

Sobel & Co. s Nonprofit and Social Services Group Webinar IRS Disclosure Requirements: What Do Organizations Need to Provide to Donors? February 15, 2012 Brett R. Harris, Esq. Wilentz, Goldman & Spitzer,

Sobel & Co. s Nonprofit and Social Services Group Webinar IRS Disclosure Requirements: What Do Organizations Need to Provide to Donors? February 15, 2012 Brett R. Harris, Esq. Wilentz, Goldman & Spitzer,

HOW TO COMPLY WITH THE PRIVATE FOUNDATION DISCLOSURE REQUIREMENTS

HOW TO COMPLY WITH THE PRIVATE FOUNDATION DISCLOSURE REQUIREMENTS SIMPSON THACHER & BARTLETT LLP FEBRUARY 17, 2000 The Treasury Department recently published final regulations which require broader public

HOW TO COMPLY WITH THE PRIVATE FOUNDATION DISCLOSURE REQUIREMENTS SIMPSON THACHER & BARTLETT LLP FEBRUARY 17, 2000 The Treasury Department recently published final regulations which require broader public

Instructions for Form 990-PF

2001 Instructions for Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Section references are to the Internal Revenue Code unless

2001 Instructions for Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Section references are to the Internal Revenue Code unless

organization provides in consideration Use Form 4506-A to request:

Goods or services a donee Through the IRS te that a section 527 political organization provides in consideration Use Form 456-A to request: TIP organization (and an for a payment y a taxpayer include organization

Goods or services a donee Through the IRS te that a section 527 political organization provides in consideration Use Form 456-A to request: TIP organization (and an for a payment y a taxpayer include organization

Charitable Contributions. Substantiation and Disclosure Requirements

Charitable Contributions Substantiation and Disclosure Requirements 1 Are you an organization that receives contributions of $250 or more? or Are you an organization that provides goods or services to

Charitable Contributions Substantiation and Disclosure Requirements 1 Are you an organization that receives contributions of $250 or more? or Are you an organization that provides goods or services to

Attention: The IRS is Revising Publication 4302, A Charity s Guide to Car Donations

Attention: The IRS is Revising Publication 4302, A Charity s Guide to Car Donations The IRS is in the process of revising Publication 4302 dated August 2004. This version does not include the tax law changes

Attention: The IRS is Revising Publication 4302, A Charity s Guide to Car Donations The IRS is in the process of revising Publication 4302 dated August 2004. This version does not include the tax law changes

JUL Dear Applicant: Letter 1045 {DO/CG)

") INTERNAL REVENUE SERVICE P. O. BOX 2508 CINCINNATI, OH 45201 Date: JUL 19 2004 FRIENDS OF THE STEFAN BATORY FOUNDATION INC C/O IRENE GRUDZINSKA-GROSS 96 BAYSTATE RD BOSTON, MA 02215 DEPARTMENT OF THE TREASURY

INTERNAL REVENUE SERVICE P. O. BOX 2508 CINCINNATI, OH 45201 Date: JUL 19 2004 FRIENDS OF THE STEFAN BATORY FOUNDATION INC C/O IRENE GRUDZINSKA-GROSS 96 BAYSTATE RD BOSTON, MA 02215 DEPARTMENT OF THE TREASURY

A Charity s Guide to. Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible contributions.

Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations A Charity s Guide to Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible

Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations A Charity s Guide to Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible

Charitable Contributions

Charitable Contributions Substantiation and Disclosure Requirements INTERNAL REVENUE SERVICE Tax Exempt and Government Entities Exempt Organizations Are you an organization that receives contributions

Charitable Contributions Substantiation and Disclosure Requirements INTERNAL REVENUE SERVICE Tax Exempt and Government Entities Exempt Organizations Are you an organization that receives contributions

2006 Instructions for Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation

(1) Nonexempt Charitable Trust Treated as a Private Foundation") 2006 Instructions for Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Department of the Treasury Internal Revenue Service Section

2006 Instructions for Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Department of the Treasury Internal Revenue Service Section

2008 Instructions for Form 990 Return of Organization Exempt From Income Tax Contents A B C D E F J A B C D E F G

2008 Instructions for Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation)

2008 Instructions for Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation)

What Must a Tax-Exempt Organization Do To Acknowledge Donations?

What Must a Tax-Exempt Organization Do To Acknowledge Donations? An important feature of being a tax-exempt organization under Section 501(c)(3) of the Internal Revenue Code is the ability to accept tax-deductible

What Must a Tax-Exempt Organization Do To Acknowledge Donations? An important feature of being a tax-exempt organization under Section 501(c)(3) of the Internal Revenue Code is the ability to accept tax-deductible

Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support

Public Charity Status and Public Support") 2008 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal If the accounting

2008 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal If the accounting

[26 CFR ]: Returns by exempt organizations and returns by certain nonexempt

![[26 CFR ]: Returns by exempt organizations and returns by certain nonexempt](/thumbs/82/85277399.jpg "[26 CFR ]: Returns by exempt organizations and returns by certain nonexempt") Part III Administrative, Procedural, and Miscellaneous [26 CFR 1.6033-2]: Returns by exempt organizations and returns by certain nonexempt organizations (Also: 6001, 6033, and 1.6001-1) Rev. Proc. 2018-38

Part III Administrative, Procedural, and Miscellaneous [26 CFR 1.6033-2]: Returns by exempt organizations and returns by certain nonexempt organizations (Also: 6001, 6033, and 1.6001-1) Rev. Proc. 2018-38

Number and street (or P.O. box, if mail is not delivered to street address) Room/suite

Room/suite") Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring organizations

Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring organizations

Part I Overview of New Form 990

E1C01_1 11/12/2008 1 C H A P T E R O N E Part I Overview of New Form 990 The annual information return filed by most tax-exempt organizations with the Internal Revenue Service (IRS) is the Form 990. This

E1C01_1 11/12/2008 1 C H A P T E R O N E Part I Overview of New Form 990 The annual information return filed by most tax-exempt organizations with the Internal Revenue Service (IRS) is the Form 990. This

INTERNAL REVENUE SERVICE P. 0. BOX 2508 CINCINNATI, OH DEPARTMENT OF THE TREASURY

INTERNAL REVENUE SERVICE P. 0. BOX 2508 CINCINNATI, OH 45201 MARTIN COUNTY FLORIDA ARES/FLACES INC PO BOX 2769 STUART, FL 34995 DEPARTMENT OF THE TREASURY Employer Identification Number: 65-0861168 DLN

INTERNAL REVENUE SERVICE P. 0. BOX 2508 CINCINNATI, OH 45201 MARTIN COUNTY FLORIDA ARES/FLACES INC PO BOX 2769 STUART, FL 34995 DEPARTMENT OF THE TREASURY Employer Identification Number: 65-0861168 DLN

File a separate application for each return. Information about Form 8868 and its instructions is at

Form 8868 Application for Automatic Extension of Time To File an Exempt Organization Return (Rev. January 2017) OMB No. 1545-1709 Department of the Treasury Internal Revenue Service File a separate application

Form 8868 Application for Automatic Extension of Time To File an Exempt Organization Return (Rev. January 2017) OMB No. 1545-1709 Department of the Treasury Internal Revenue Service File a separate application

Instructions for Form 990-EZ

2011 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2011 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

Attention: The IRS is Revising Publication 4303, A Donor s Guide to Car Donations

Attention: The IRS is Revising Publication 4303, A Donor s Guide to Car Donations The IRS is in the process of revising Publication 4303 dated August 2004. This version does not include the tax law changes

Attention: The IRS is Revising Publication 4303, A Donor s Guide to Car Donations The IRS is in the process of revising Publication 4303 dated August 2004. This version does not include the tax law changes

Short Form 990-EZ Return of Organization Exempt From Income Tax

Form B G I J Short Form 990-EZ Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Do not enter Social

Form B G I J Short Form 990-EZ Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Do not enter Social

Section references are to the Internal Revenue Code unless otherwise noted.

2008 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2008 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

EF Transmission Status

990EF EF Transmission Status (Keep for your records) Name(s) as shown on return EIN number The following will be transmitted to the IRS. 990 8868 Amended The following state returns will be transmitted:

990EF EF Transmission Status (Keep for your records) Name(s) as shown on return EIN number The following will be transmitted to the IRS. 990 8868 Amended The following state returns will be transmitted:

(c)(3) Applying for 501(c)(3) Tax-Exempt Status,

(3) Applying for 501(c)(3) Tax-Exempt Status,") Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

V e h i c l e Donation,

This publication is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. Tax Exempt and Government Entities EXEMPT ORGANIZATIONS A Donor s Guide to V e h i c l e Donation,

This publication is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. Tax Exempt and Government Entities EXEMPT ORGANIZATIONS A Donor s Guide to V e h i c l e Donation,

Short Form OMB No Return of Organization Exempt From Income Tax

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

INTERNAL REVENUE SERVICE P. O. BOX 2508 CINCINNATI, OH DEPARTMENT OF THE TREASURY

INTERNAL REVENUE SERVICE P. O. BOX 2508 CINCINNATI, OH 45201 Date: CONSERVANCY INC C/O JAMES A ALOIS I JR GOULSTON & STORRS PC 400 ATLANTIC AVE BOSTON, MA 02110-0000 DEPARTMENT OF THE TREASURY Employer

INTERNAL REVENUE SERVICE P. O. BOX 2508 CINCINNATI, OH 45201 Date: CONSERVANCY INC C/O JAMES A ALOIS I JR GOULSTON & STORRS PC 400 ATLANTIC AVE BOSTON, MA 02110-0000 DEPARTMENT OF THE TREASURY Employer

Instructions for Form 990-EZ

2009 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2009 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

PRIVATE FOUNDATION CAUTION: The purposes of this memorandum are to assist you, the directors of your private foundation, and your accountant in:

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

A For the 2011 calendar year, or tax year beginning, 2011, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black

IMPORTANT TAX AND FIDELITY BOND INFORMATION

AMERICAN LEGION AUXILIARY NATIONAL HEADQUARTERS IMPORTANT TAX AND FIDELITY BOND INFORMATION This information is intended to assist Units, Departments, Districts/Counties/Councils in understanding their

AMERICAN LEGION AUXILIARY NATIONAL HEADQUARTERS IMPORTANT TAX AND FIDELITY BOND INFORMATION This information is intended to assist Units, Departments, Districts/Counties/Councils in understanding their

A For the 2010 calendar year, or tax year beginning, 2010, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Instructions for Form 1128

Instructions for Form 1128 (Rev. January 2008) Application To Adopt, Change, or Retain a Tax Year Department of the Treasury Internal Revenue Service Section references are to the Internal Regulations

Instructions for Form 1128 (Rev. January 2008) Application To Adopt, Change, or Retain a Tax Year Department of the Treasury Internal Revenue Service Section references are to the Internal Regulations

A For the 2009 calendar year, or tax year beginning, 2009, and ending, D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Revenue Expenses Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Department of the Treasury Internal Revenue Service Revenue Expenses Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Open to Public Internal Revenue Service The organization may have to use a copy of this return to satisfy state reporting requirements.

Form990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) 2002

Form990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) 2002

2016 Do not enter social security numbers on this form as it may be made public. Open to Public

Short Form OMB. 545-50 Return of Organization Exempt From Income Tax Form 990-EZ Under section 50(c), 57, or 4947(a)() of the Internal Revenue Code (except private foundations) 06 Do not enter social security

Short Form OMB. 545-50 Return of Organization Exempt From Income Tax Form 990-EZ Under section 50(c), 57, or 4947(a)() of the Internal Revenue Code (except private foundations) 06 Do not enter social security

EASIER COMPLIANCE IS GOAL OF NEW INTERMEDIATE SANCTION REGULATIONS

EASIER COMPLIANCE IS GOAL OF NEW INTERMEDIATE SANCTION REGULATIONS By Steven T. Miller 1 On January 10, 2001, the Treasury Department issued Temporary Regulations interpreting the benefit limitation provisions

EASIER COMPLIANCE IS GOAL OF NEW INTERMEDIATE SANCTION REGULATIONS By Steven T. Miller 1 On January 10, 2001, the Treasury Department issued Temporary Regulations interpreting the benefit limitation provisions

Compliance Guide for Tax-Exempt Organizations

INTERNAL REVENUE SERVICE TAX-EXEMPT AND GOVERNMENT ENTITIES EXEMPT ORGANIZATIONS, Compliance Guide for Tax-Exempt Organizations (Other than 501(c)(3) Public Charities and Private Foundations), Inside:

INTERNAL REVENUE SERVICE TAX-EXEMPT AND GOVERNMENT ENTITIES EXEMPT ORGANIZATIONS, Compliance Guide for Tax-Exempt Organizations (Other than 501(c)(3) Public Charities and Private Foundations), Inside:

DESCRIPTION OF THE "CARE ACT OF 2003"

DESCRIPTION OF THE "CARE ACT OF 2003" Scheduled for a Markup By the SENATE COMMITTEE ON FINANCE on February 5, 2003 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION February 3, 2003 JCX-04-03 CONTENTS

DESCRIPTION OF THE "CARE ACT OF 2003" Scheduled for a Markup By the SENATE COMMITTEE ON FINANCE on February 5, 2003 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION February 3, 2003 JCX-04-03 CONTENTS

Everest REIT Investors

Everest REIT Investors 199 SOUTH LOS ROBLES AVENUE, SUITE 200 PASADENA, CALIFORNIA 91101 TEL (626) 585-5920 FAX (626) 585-5929 To the Shareholders of Resource Real Estate Opportunity REIT, Inc. October

Everest REIT Investors 199 SOUTH LOS ROBLES AVENUE, SUITE 200 PASADENA, CALIFORNIA 91101 TEL (626) 585-5920 FAX (626) 585-5929 To the Shareholders of Resource Real Estate Opportunity REIT, Inc. October

Return of Organization Exempt From Income Tax

990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Form Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung Department of the Treasury benefit trust

990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Form Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung Department of the Treasury benefit trust

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

A For the 2010 calendar year, or tax year beginning, 2010, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Number and street (or P.O. box, if mail is not delivered to street address) Room/suite

Room/suite") Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

Short Form OMB No Return of Organization Exempt From Income Tax

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Section 2 Federal and State Tax Matters

Section 2 Federal and State Tax Matters Chapter 8: Tax-Exempt Status INTRODUCTION... 100 Political Campaign Prohibition... 101 Congregations... 105 Lutheran Schools... 110 Early Childhood Centers... 115

Section 2 Federal and State Tax Matters Chapter 8: Tax-Exempt Status INTRODUCTION... 100 Political Campaign Prohibition... 101 Congregations... 105 Lutheran Schools... 110 Early Childhood Centers... 115

Instructions for Form 990-EZ

Contents Page General Instructions 1 6 A Who Must File 1 B Exempt Organization Reference Chart 2 C Organizations Not Required To File 2 D Forms and Publications To File or Use 2 E Use of Form 990-EZ To

Contents Page General Instructions 1 6 A Who Must File 1 B Exempt Organization Reference Chart 2 C Organizations Not Required To File 2 D Forms and Publications To File or Use 2 E Use of Form 990-EZ To

Short Form OMB No Return of Organization Exempt From Income Tax

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e))

)") 4/16/218 11:11:26 AM 1 216 Return University of the Pacific Form 99-T PUBLIC DISCLOSURE COPY Exempt Organization Business Income Tax Return (and proxy tax under section 633(e)) OMB No. 1545-687 216 For

4/16/218 11:11:26 AM 1 216 Return University of the Pacific Form 99-T PUBLIC DISCLOSURE COPY Exempt Organization Business Income Tax Return (and proxy tax under section 633(e)) OMB No. 1545-687 216 For

Federal Tax Return AUM HOME SHALA. ALBERT CORRADA CPA 2655 LEJEUNE ROAD SUITE 902 CORAL GABLES, FL Phone: (305)

") Federal Tax Return AUM HOME SHALA 2016 ALBERT CORRADA CPA 2655 LEJEUNE ROAD SUITE 902 CORAL GABLES, FL 33134 Phone: (305) 804-8569 ACORRADA@CORRADACPA.COM ALBERT CORRADA CPA 2655 LEJEUNE ROAD SUITE 902

Federal Tax Return AUM HOME SHALA 2016 ALBERT CORRADA CPA 2655 LEJEUNE ROAD SUITE 902 CORAL GABLES, FL 33134 Phone: (305) 804-8569 ACORRADA@CORRADACPA.COM ALBERT CORRADA CPA 2655 LEJEUNE ROAD SUITE 902

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Applicable Sections: Revenue Procedure SECTION 1. PURPOSE

Applicable Sections: 26 CFR 1.6033-2. Returns by exempt organizations (taxable years beginning after December 31, 1969) and returns by certain nonexempt organizations (taxable years beginning after December

Applicable Sections: 26 CFR 1.6033-2. Returns by exempt organizations (taxable years beginning after December 31, 1969) and returns by certain nonexempt organizations (taxable years beginning after December

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

COPYRIGHTED MATERIAL. Contents. About the Authors Preface xxi

Hopkins_NF_FM_1 11/13/2008 5 Contents About the Authors Preface xxi xix Chapter One: Part I Overview of New Form 990 1 1.1 Form 990 Basics 2 (a) Various Forms 2 (b) Filing Exceptions 2 (c) Filing Due Dates

Hopkins_NF_FM_1 11/13/2008 5 Contents About the Authors Preface xxi xix Chapter One: Part I Overview of New Form 990 1 1.1 Form 990 Basics 2 (a) Various Forms 2 (b) Filing Exceptions 2 (c) Filing Due Dates

Return of Organization Exempt From Income Tax

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust

Other (specify) H Check if the organization is not I Website: GlobalOutreachTanzania.org

H Check if the organization is not I Website: GlobalOutreachTanzania.org") Form 99-EZ Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

Form 99-EZ Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

GOVERNMENT COPY DES ACTION USA 823 PROMENADE WAY SUITE 208 JUPITER, FL

2013 TA RETURN GOVERNMENT COPY Client: Prepared for: 20121115 DES ACTION USA 823 PROMENADE WAY SUITE 208 JUPITER, FL 33458 561-876-1224 Prepared by: SELLERSCONSULTANT.COM INC. 156 MORNING DEW CIRCLE JUPITER,

2013 TA RETURN GOVERNMENT COPY Client: Prepared for: 20121115 DES ACTION USA 823 PROMENADE WAY SUITE 208 JUPITER, FL 33458 561-876-1224 Prepared by: SELLERSCONSULTANT.COM INC. 156 MORNING DEW CIRCLE JUPITER,

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51, 527, or 4947(a)(1) of the Internal Revenue Code (except private

PUBLIC INSPECTION COPY

Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) Department of the Treasury Internal Revenue Service A Check box if address changed For

Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) Department of the Treasury Internal Revenue Service A Check box if address changed For

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 57, or 4947(a)(1) of the Internal Revenue Code 016 (except private foundations) G Do not enter

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 57, or 4947(a)(1) of the Internal Revenue Code 016 (except private foundations) G Do not enter

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2015 (except private foundations) G Do not enter

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2015 (except private foundations) G Do not enter

Give Me Your 990! Public Disclosure Requirements for Tax-Exempt Organizations 2015 Edition

Give Me Your 990! Public Disclosure Requirements for Tax-Exempt Organizations 2015 Edition Give me your 990! What do you have to do when you hear these words? Unfortunately, not every nonprofit knows how

Give Me Your 990! Public Disclosure Requirements for Tax-Exempt Organizations 2015 Edition Give me your 990! What do you have to do when you hear these words? Unfortunately, not every nonprofit knows how

Public Inspection Copy

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2012

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2012

Activities that may jeopardize exempt status. Federal information returns, tax returns or notices that must be filed. Recordkeeping why, what, when

(a) Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Compliance Guide for Tax-Exempt Organizations (other than 501(c)(3) Public Charities and Private Foundations) Covers:

(a) Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Compliance Guide for Tax-Exempt Organizations (other than 501(c)(3) Public Charities and Private Foundations) Covers:

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 57, or 4947(a)(1) of the Internal Revenue Code 017 (except private foundations) G Do not enter

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 57, or 4947(a)(1) of the Internal Revenue Code 017 (except private foundations) G Do not enter

Private Foundations Deeper Dive

Private Foundations Deeper Dive David Lawson, Davis Wright Tremaine November 2, 2017 Seattle, Washington What is a private foundation? Can be a nonprofit corporation or a charitable trust Nonprofit corporation

Private Foundations Deeper Dive David Lawson, Davis Wright Tremaine November 2, 2017 Seattle, Washington What is a private foundation? Can be a nonprofit corporation or a charitable trust Nonprofit corporation

Instructions for Schedule A (Form 990 or 990-EZ)

") 2018 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2018 Instructions for Schedule A (Form 990 or 990-EZ) Public Charity Status and Public Support Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance March 20, 2009 9:30 am 11:15 am North County Philanthropy Council Lake San Marcos Country Club 1750 San

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance March 20, 2009 9:30 am 11:15 am North County Philanthropy Council Lake San Marcos Country Club 1750 San

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Return of Organization Exempt From Income Tax

990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Form Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung Department of the Treasury benefit trust

990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Form Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung Department of the Treasury benefit trust

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990 Tax Exempt Reporting

Form 990 Tax Exempt Reporting CLAconnect.com Speaker Introductions Amanda Treml, CPA Amanda is a Manager with CliftonLarsonAllen and provides assurance and tax compliance services to non-profit organizations.

Form 990 Tax Exempt Reporting CLAconnect.com Speaker Introductions Amanda Treml, CPA Amanda is a Manager with CliftonLarsonAllen and provides assurance and tax compliance services to non-profit organizations.

Open to Public Inspection. 11/14/2017 TY Form 990EZ. 1/5

11/14/2017 TY Form 990EZ Form990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal

11/14/2017 TY Form 990EZ Form990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal

A For the 2010 calendar year, or tax year beginning 01/01 B Check if applicable:

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

2013 G Do not enter Social Security numbers on this form as it may be made public. Open to Public

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 2013 Do not enter

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 2013 Do not enter

Return of Organization Exempt From Income Tax

Form 990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 2017 Do not enter social security

Form 990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 2017 Do not enter social security

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

PENSION PROTECTION ACT OF 2006 (H.R. 4) SUMMARY OF PROVISIONS RELATING TO CHARITABLE GIVING AND EXEMPT ORGANIZATIONS. by Michele A. W.

SUMMARY OF PROVISIONS RELATING TO CHARITABLE GIVING AND EXEMPT ORGANIZATIONS. by Michele A. W.") PENSION PROTECTION ACT OF 2006 (H.R. 4) SUMMARY OF PROVISIONS RELATING TO CHARITABLE GIVING AND EXEMPT ORGANIZATIONS by Michele A. W. McKinnon I. CHARITABLE GIVING INCENTIVES. A. IRA Charitable Rollover.

PENSION PROTECTION ACT OF 2006 (H.R. 4) SUMMARY OF PROVISIONS RELATING TO CHARITABLE GIVING AND EXEMPT ORGANIZATIONS by Michele A. W. McKinnon I. CHARITABLE GIVING INCENTIVES. A. IRA Charitable Rollover.

Instructions for Form 990

Instructions for Form 990 Return of Organization Exempt From Income Tax Under section 501(c) of the Internal Revenue Code (except black lung benefit trust or private foundation) or section 4947(a)(1) nonexempt

Instructions for Form 990 Return of Organization Exempt From Income Tax Under section 501(c) of the Internal Revenue Code (except black lung benefit trust or private foundation) or section 4947(a)(1) nonexempt

Do not enter social security numbers on this form as it may be made public.

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

23 rd Annual Health Sciences Tax Conference

23 rd Annual Health Sciences Tax Conference and public charity status December 9, 2013 Disclaimer Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the

23 rd Annual Health Sciences Tax Conference and public charity status December 9, 2013 Disclaimer Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

Short Form. Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Copy for Public Inspection

Copy for Public Inspection Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) Department of the Treasury Internal Revenue Service Open A Check

Copy for Public Inspection Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) Department of the Treasury Internal Revenue Service Open A Check

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2014 (except private foundations) G Do not enter

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2014 (except private foundations) G Do not enter

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private