-8- General Instructions for Form 990 and Form 990-EZ

|

|

|

- Rudolph Bailey

- 6 years ago

- Views:

Transcription

1

2 b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $250 or value of similar or comparable goods or more. services. Goods or services may be similar or 1. E offers a basic membership benefits Contemporaneous. A written package for $75. The package gives members acknowledgment is contemporaneous if the unique qualities of the goods or services that the right to buy tickets in advance, free parking, donor obtains it on or before the earlier of: are being valued. and a gift shop discount of 10%. E s $150 The date the donor files the original return Goods or services. Goods or services preferred membership benefits package also for the tax year in which the contribution was mean: includes a $20 poster. Both the basic and made; or Cash, preferred membership packages are for a The due date (including extensions) for filing Property, 12-month period and include about 50 the donor s original return for that year. Services, productions. E offers F, a patron of the arts, the Benefits, and preferred membership benefits in return for a Substantiation of payroll contributions. Privileges. payment of $150 or more. F accepts the An organization may substantiate a payroll preferred membership benefits package for contribution by: In consideration for. A donee $300. E s written acknowledgment satisfies the A pay stub, Form W-2, or other document organization provides goods or services in substantiation requirement if it describes the showing a contribution to a donee organization; consideration for a taxpayer s payment if, at poster, gives a good faith estimate of its fair and the time the taxpayer makes the payment to market value ($20), and disregards the A pledge card or other document from the the donee organization, the taxpayer receives, remaining membership benefits. donee organization stating that organization or expects to receive, goods or services in 2. If F received only the basic membership provides no goods or services for any payroll exchange for that payment. package for its $300 payment, E s contributions. Goods or services a donee organization acknowledgment need state only that no goods The amount withheld from each payment of provides in consideration for a payment by a or services were provided. wages to a taxpayer is treated as a separate taxpayer include goods or services provided in 3. G Theater Group performs four plays. contribution. a year other than the year in which the donor Each play is performed twice. Nonmembers Substantiation of payments to a college makes the payment to the donee organization. can purchase a ticket for $15. For a $60 or university for the right to purchase membership fee, however, members are Intangible religious benefits. Intangible tickets to athletic events. The right to offered free admission to any of the religious benefits must be provided by purchase tickets for an athletic event is valued performances. H makes a payment of $350 organizations organized exclusively for at 20% of the payment. and accepts this membership benefit. Because religious purposes. of the limited number of performances, the Example. When a taxpayer pays $ membership privilege cannot be exercised for the right to purchase tickets for an athletic Examples include: frequently. Therefore, G s acknowledgment event, the right is valued at $ The Admission to a religious ceremony, and must describe the free admission benefit and remaining $250 is a charitable contribution that De minimis tangible benefits, such as wine, estimate its value in good faith. the taxpayer must substantiate. provided in connection with a religious Substantiation of matched payments. If ceremony. Certain goods or services provided to a taxpayer s payment to a donee organization Distributing organization as donee. An donor s employees or partners. Certain is matched by another payor, and the taxpayer organization described in section 170(c), or an goods or services provided to employees or receives goods or services in consideration for organization described as a Principal partners of donors may be disregarded for its payment and some or all of the matching Combined Fund Organization for purposes of substantiation and disclosure purposes. payment, those goods or services will be the Combined Federal Campaign, that receives Describe such goods or services. A good faith treated as provided in consideration for the a payment made as a contribution is treated as estimate is not needed. taxpayer s payment and not in consideration a donee organization even if the organization Example. Museum J offers a basic for the matching payment. distributes the amount received to one or more membership benefits package for $40. It Disclosure statement. An organization organizations described in section 170(c). includes free admission and a 10% gift shop must provide a written disclosure statement to Penalties. A charity that knowingly discount. Corporation K makes a $50,000 donors who make a payment, described as a provides a false substantiation payment to J and in return, J offers K s quid pro quo contribution, in excess of $75 acknowledgment to a donor may be subject to employees free admission, a tee shirt with J s (section 6115). This requirement is separate the penalties under section 6701 for aiding and logo that costs J $4.50, and a 25% gift shop from the written substantiation abetting an understatement of tax liability. discount. Because the free admission is acknowledgment a donor needs for offered in both benefit packages and the value deductibility purposes. While, in certain Charities that fail to provide the required of the tee shirts is insubstantial, K s written circumstances, an organization may be able to disclosure statement for a quid pro quo acknowledgment need not value the free meet both requirements with the same written contribution of more than $75 will incur a admission benefit or the tee shirts. However, document, an organization must be careful to penalty of $10 per contribution, not to exceed because the 25% gift shop discount to K s satisfy the section 6115 written disclosure $5,000 per fundraising event or mailing. The employees differs from the 10% discount statement requirement in a timely manner charity may avoid the penalty if it can show that offered in the basic membership benefits because of the penalties involved. the failure was due to reasonable cause package, K s written acknowledgment must (section 6714). describe the 25% discount, but need not Quid pro quo contribution. A quid pro estimate its value. quo contribution is a payment that is given both as a contribution and as a payment for Definitions. M. Public Inspection of goods or services provided by the donee Substantiation. It is the responsibility of organization. Returns, etc. the donor: Example. A donor gives a charity $100 in To value a donation, and Through the IRS consideration for a concert ticket valued at $40 To obtain an organization s written Use Form 4506-A to request: (a quid pro quo contribution). In this example, acknowledgment substantiating the donation. $60 would be deductible. Because the donor s A copy of an exempt or political There is no prescribed format for the payment exceeds $75, the organization must organization s return, report, notice, or organization s written acknowledgment of a furnish a disclosure statement even though the exemption application; donation. Letters, postcards, or taxpayer s deductible amount does not exceed An inspection of a return, report, notice, or computer-generated forms may be acceptable. $75. Separate payments of $75 or less made exemption application at an IRS office. The acknowledgment must, however, provide at different times of the year for separate The IRS can provide copies of exempt sufficient information to substantiate the fundraising events will not be aggregated for organization returns on a compact disk amount of the deductible contribution. purposes of the $75 threshold. (CD-ROM). Requesters can order the complete The organization may either provide: Good faith estimate. An organization set (all Forms 990 and 990-EZ or all Forms Separate statements for each contribution of may use any reasonable method in making a 990-PF filed for a year) or a partial set by state $250 or more, or good faith estimate of the value of goods or or by month. For more information on the cost Furnish periodic statements substantiating services provided by an organization in and how to order CD-ROMs, call the TEGE contributions of $250 or more. consideration for a taxpayer s payment to that Customer Account Services toll-free number comparable even though they do not have the Separate contributions of less than $250 organization. A good faith estimate of the value ( ) or write to the IRS in are not subject to the requirements of section of goods or services that are not generally Cincinnati, OH at the address in General 170(f)(8), regardless of whether the sum of the available in a commercial transaction may be Instruction A. -8- General Instructions for Form 990 and Form 990-EZ

3 The IRS may not disclose portions of an Any letter or other document issued by the request for inspection (normally not more than exemption application relating to any trade IRS concerning the application. 2 weeks) and at a reasonable time of day. secrets, etc. See the instructions for Schedule Application for tax exemption does not May mail, within 2 weeks of receiving the B (Form 990, 990-EZ, or 990-PF) that discuss include: request, a copy of its application for tax the disclosure of that schedule. Any application for tax exemption filed exemption and annual information returns to You can only request Forms 990 or 990-EZ before July 15, 1987, unless the organization the requester instead of allowing an inspection. for section 527 organizations for tax years filing the application had a copy of the May charge the requester for copying and beginning after June 30, application on July 15, 1987; actual postage costs only if the requester In the case of a tax-exempt organization consents to the charge. You may inspect a return, report, notice, or exemption application at an IRS office free of other than a private foundation, the name and An organization that has a permanent charge. You may also obtain a copy of these address of any contributor to the organization; office, but has no office hours, or very limited items through the organization as discussed in or hours during certain times of the year, must the following section. Any material that is not available for public make its documents available during those inspection under section periods when office hours are limited, or not Through the organization Annual information return includes: available, as though it were an organization Public inspection and distribution of An exact copy of the Form 990, or Form without a permanent office. returns and reports for a political 990-EZ filed by a tax-exempt organization as organization. Section 527 political required by section Special rules relating to copies. organizations required to file Form 990, or Any amended return the organization files Form 990-EZ, must, in general, make their with the IRS after the date the original return is Time and place for providing copies in Form 8871, 8872, 990, or 990-EZ available for filed. response to requests made in-person. A public inspection in the same manner as The copy must include all information tax-exempt organization must: annual information returns of section 501(c) furnished to the IRS on Form 990, or Form Provide copies of required documents under organizations and 4947(a) nonexempt 990-EZ, as well as all schedules, attachments section 6104(d) in response to a request made charitable trusts are made available. See the and supporting documents, except for the in person at its principal, regional and district public inspection rules for tax-exempt name and address of any contributor to the offices during regular business hours. organizations below. Generally, Form 8871 organization. See the instructions for Schedule Provide such copies to a requester on the and Form 8872 are available for inspection and B (Form 990, 990-EZ, or 990-PF). day the request is made, except for unusual printing from the Internet. The website address circumstances (see below). Annual returns more than 3 years old. for both of these forms is An annual information return does not include Unusual circumstances. In the case of Note that a section 527 political any return after the expiration of 3 years from an in-person request, where unusual organization (and an organization filing Form the date the return is required to be filed circumstances exist so that fulfilling the request 990-PF) must disclose their Schedule B (Form (including any extension of time that has been on the same business day causes an 990, 990-EZ, or 990-PF), Schedule of granted for filing such return) or is actually unreasonable burden to the tax-exempt Contributors. See the instructions for filed, whichever is later. organization, the organization must provide the Schedule B. copies no later than the next business day If an organization files an amended return, The penalties discussed in General following the day that the unusual however, the amended return must be made Instruction K also apply to section 527 political circumstances cease to exist, or the 5th available for a period of 3 years beginning on organizations (Rev. Rul , business day after the date of the request, the date it is filed with the IRS. I.R.B. 430). whichever occurs first. Local or subordinate organizations. For Public inspection and distribution of rules relating to annual information returns of Unusual circumstances include: applications for tax exemption and annual local or subordinate organizations, see Requests received that exceed the information returns of tax-exempt Regulations section (d)-1(f). organization s daily capacity to make copies; organizations. Under Regulations sections Requests received shortly before the end of Regional or district offices. A regional or (d)-1 through (d)-3, a regular business hours that require an district office is any office of a tax-exempt tax-exempt organization must: extensive amount of copying; or organization, other than its principal office, that Make its application for recognition of Requests received on a day when the has paid employees, whether part-time or exemption and its annual information returns organization s managerial staff capable of full-time, whose aggregate number of paid available for public inspection without charge at fulfilling the request is conducting special hours a week are normally at least 120. its principal, regional and district offices during duties, such as student registration or regular business hours. A site is not considered a regional or district attending an off-site meeting or convention, Make each annual information return office, however, if rather than its regular administrative duties. available for a period of 3 years beginning on The only services provided at the site Agents for providing copies. For rules the date the return is required to be filed further exempt purposes (such as day care, relating to use of agents to provide copies, see (determined with regard to any extension of health care or scientific or medical research); Regulations sections (d)-1(d) time for filing) or is actually filed, whichever is and and. later. The site does not serve as an office for Provide a copy without charge, other than a management staff, other than managers who Request for copies in writing. A reasonable fee for reproduction and actual are involved solely in managing the exempt tax-exempt organization must honor a written postage costs, of all or any part of any function activities at the site. request for a copy of documents (or the application or return required to be made requested part) required under section 6104(d) available for public inspection to any individual if the request: Special rules relating to public inspection. who makes a request for such copy in person 1. Is addressed to, and delivered by mail, Permissible conditions on public or in writing (except as provided in Regulations electronic mail, facsimile, or a private delivery inspection. A tax-exempt organization sections (d)-2 and -3). service, as defined in section 7502(f), to a May have an employee present in the room Definitions principal, regional, or district office of the during an inspection. organization; and Tax-exempt organization is any Must allow the individual conducting the 2. Sets forth the address to which the copy organization that is described in section 501(c) inspection to take notes freely during the of the documents should be sent. or (d) and is exempt from taxation under inspection. section 501(a). The term tax-exempt Must allow the individual to photocopy the Time and manner of fulfilling written organization also includes any section document at no charge, if the individual requests. 4947(a) nonexempt charitable trust or provides photocopying equipment at the place nonexempt private foundation that is subject to of inspection. IF the organization THEN the organization the reporting requirements of section Organizations that do not maintain Application for tax exemption includes permanent offices. A tax-exempt Receives a written Must mail the copy of (except as described later): organization with no permanent office request for a copy, the requested Any prescribed application form (such as Must make its application for tax exemption documents (or the Form 1023 or Form 1024), and its annual information returns available for requested parts) within All documents and statements the IRS inspection at a reasonable location of its 30 days from the date it requires an applicant to file with the form, choice. receives the request. Any statement or other supporting document Must permit public inspection within a submitted in support of the application, and reasonable amount of time after receiving a General Instructions for Form 990 and Form 990-EZ -9-

4 prepayment and a requester does not enclose If the local or subordinate organization Mails the copy of the Is deemed to have payment with a request, an organization must receives a written request for a copy of its requested document, provided the copy on the receive consent from a requester before annual information return, it must fulfill the postmark date or private providing copies for which the fee charged for request by providing a copy of the group return delivery mark (if sent by copying and postage exceeds $20. in the time and manner specified in the certified or registered Documents to be provided by regional paragraph above, Request for copies in writing. mail, the date of registration or the date and district offices. Except as otherwise The requester has the option of requesting of the postmark on the provided, a regional or district office of a from the central or parent organization, at its sender s receipt). tax-exempt organization must satisfy the same principal office, inspection or copies of group rules as the principal office with respect to returns filed by the central or parent allowing public inspection and providing copies Requires payment in Is required to provide organization. The central or parent of its application for tax exemption and annual advance, the copies within 30 organization must fulfill such requests in the information returns. days from the date it time and manner specified in the paragraphs, receives payment. A regional or district office is not required, Special rules relating to public inspection and however, to make its annual information return Special rules relating to copies above. Receives a request or Is deemed to have available for inspection or to provide copies Failure to comply. If an organization fails payment by mail, received it 7 days after until 30 days after the date the return is to comply with the requirements specified in the date of the required to be filed (including any extension of this paragraph, the penalty provisions of postmark, absent time that is granted for filing such return) or is sections 6652(c)(C), 6652(c)(D), and evidence to the contrary. actually filed, whichever is later apply. Documents to be provided by local and Making applications and returns widely Receives a request Is deemed to have subordinate organizations. available. A tax-exempt organization is not transmitted by electronic received it the day the Applications for tax exemption. Except as required to comply with a request for a copy of mail or facsimile, request is transmitted otherwise provided, a tax-exempt organization its application for tax exemption or an annual successfully. that did not file its own application for tax information return if the organization has made exemption (because it is a local or subordinate the requested document widely available (see organization covered by a group exemption Receives a written Must notify the below). letter) must, upon request, make available for request without payment requester of the An organization that makes its application public inspection, or provide copies of, the or with an insufficient prepayment policy and for tax exemption and/or annual information application submitted to the IRS by the central payment, when payment the amount due within 7 return widely available must nevertheless or parent organization to obtain the group in advance is required, days from the date of make the document available for public exemption letter and those documents which the request s receipt. inspection as required under Regulations were submitted by the central or parent section (d)-1(a). organization to include the local or subordinate Receives consent from May provide a copy of organization in the group exemption letter. A tax-exempt organization makes its an individual making a the requested document However, if the central or parent application for tax exemption and/or an annual request, exclusively by electronic organization submits to the IRS a list or information return widely available if the mail (the material is directory of local or subordinate organizations organization complies with the Internet posting provided on the date the covered by the group exemption letter, the requirements and the notice requirements organization local or subordinate organization is required to given below. successfully transmits provide only the application for the group Internet posting. A tax-exempt the electronic mail). exemption ruling and the pages of the list or organization can make its application for tax directory that specifically refer to it. The local or exemption and/or an annual information return Request for a copy of parts of a subordinate organization must permit public widely available by posting the document on a document. A tax-exempt organization must inspection, or comply with a request for copies World Wide Web page that the tax-exempt fulfill a request for a copy of the organization s made in person, within a reasonable amount of organization establishes and maintains or by entire application for tax exemption or annual time (normally not more than 2 weeks) after having the document posted, as part of a information return or any specific part or receiving a request made in person for public database of similar documents of other schedule of its application or return. A request inspection or copies and at a reasonable time tax-exempt organizations, on a World Wide for a copy of less than the entire application or of day. See Regulations section Web page established and maintained by less than the entire return must specifically (d)-1(f) for further information. another entity. The document will be identify the requested part or schedule. Annual information returns. A local or considered widely available only if Fees for copies. A tax-exempt subordinate organization that does not file its (A) The World Wide Web page through organization may charge a reasonable fee for own annual information return (because it is which it is available clearly informs readers that providing copies. affiliated with a central or parent organization the document is available and provides that files a group return) must, upon request, instructions for downloading it; Before the organization provides the make available for public inspection, or provide documents, it may require that the individual (B) The document is posted in a format copies of, the group returns filed by the central requesting copies of the documents pay the that, when accessed, downloaded, viewed and or parent organization. fee. If the organization has provided an printed in hard copy, exactly reproduces the individual making a request with notice of the However, if the group return includes image of the application for tax exemption or fee, and the individual does not pay the fee separate schedules with respect to each local annual information return as it was originally within 30 days, or if the individual pays the fee or subordinate organization included in the filed with the IRS, except for any information by check and the check does not clear upon group return, the local or subordinate permitted by statute to be withheld from public deposit, the organization may disregard the organization receiving the request may omit disclosure; and request. any schedules relating only to other (C) Any individual with access to the organizations included in the group return. Internet can access, download, view and print Form of payment (A) Request made in The local or subordinate organization must the document without special computer person. If a tax-exempt organization charges a permit public inspection, or comply with a hardware or software required for that format fee for copying, it must accept payment by request for copies made in person, within a (other than software that is readily available to cash and money order for requests made in reasonable amount of time (normally not more members of the public without payment of any person. The organization may accept other than 2 weeks) after receiving a request made fee) and without payment of a fee to the forms of payment, such as credit cards and in person for public inspection or copies and at tax-exempt organization or to another entity personal checks. a reasonable time of day. maintaining the World Wide Web page. (B) Request made in writing. If a In a case where the requester seeks Reliability and accuracy. In order for the tax-exempt organization charges a fee for inspection, the local or subordinate document to be widely available through an copying and postage, it must accept payment organization may mail a copy of the applicable Internet posting, the entity maintaining the by certified check, money order, and either documents to the requester within the same World Wide Web page must have procedures personal check or credit card for requests time period instead of allowing an inspection. for ensuring the reliability and accuracy of the made in writing. The organization may accept In such a case, the organization may charge document that it posts on the page and must other forms of payment. the requester for copying and actual postage take reasonable precautions to prevent Avoidance of unexpected fees. Where a costs only if the requester consents to the alteration, destruction or accidental loss of the tax-exempt organization does not require charge. document when posted on its page. In the -10- General Instructions for Form 990 and Form 990-EZ

5 event that a posted document is altered, requirement will be subject to a penalty for Disqualified Person destroyed or lost, the entity must correct or each day on which the offers or solicitations The vast majority of section 501(c) or replace the document. are made. The penalty imposed for a particular 501(c) organization employees and Notice requirement. If a tax-exempt day is the greater of $1,000 or 50% of the total contractors will not be affected by these rules. organization has made its application for tax cost of the offers and solicitations made on that Only the few influential persons within these exemption and/or an annual information return day that lacked the required disclosure (section organizations are covered by these rules when widely available, it must notify any individual 6711). they receive benefits, such as compensation, requesting a copy where the documents are fringe benefits, or contract payments. The IRS available (including the address on the World calls this class of covered individuals Wide Web, if applicable). If the request is made O. Disclosures Regarding Certain disqualified persons. A disqualified person, in person, the organization must provide such Transactions and Relationships regarding any transaction, is any person who notice to the individual immediately. If the In their annual returns on Schedule A (Form was in a position to exercise substantial request is made in writing, the notice must be 990 or 990-EZ), section 501(c) influence over the affairs of the applicable provided within 7 days of receiving the request. organizations must disclose information tax-exempt organization at any time during a Tax-exempt organization subject to regarding their direct or indirect transfers to, 5-year period ending on the date of the harassment campaign. If the Director EO and other direct or indirect relationships with, transaction. Persons who hold certain powers, Examination (or designee) determines that the other section 501(c) organizations (except responsibilities, or interests are among those organization is being harassed, a tax-exempt other section 501(c) organizations) or who are in a position to exercise substantial organization is not required to comply with any section 527 political organizations (section influence over the affairs of the organization. request for copies that it reasonably believes is 6033(b)(9)). This provision helps prevent the This would include, for example, voting part of a harassment campaign. diversion or expenditure of a section 501(c) members of the governing body, and persons organization s funds for purposes not intended holding the power of: Whether a group of requests constitutes a by section 501(c). All section 501(c) Presidents, chief executive officers, or chief harassment campaign depends on the relevant organizations must maintain records regarding operating officers. facts and circumstances such as: all such transfers, transactions, and Treasurers and chief financial officers. A sudden increase in requests; an relationships. See also General Instruction K extraordinary number of requests by form A disqualified person also includes certain regarding penalties. letters or similarly worded correspondence; family members of a disqualified person, and hostile requests; evidence showing bad faith or 35% controlled entities of a disqualified person. deterrence of the organization s exempt P. Intermediate Sanction Who is not a disqualified person? The rules purpose; prior provision of the requested Regulations Excess Benefit also clarify which persons are not considered documents to the purported harassing group; to be in a position to exercise substantial and a demonstration that the organization Transactions influence over the affairs of an organization. routinely provides copies of its documents Final Regulations that interpret the benefit They include: upon request. limitation provisions of section 4958 were An employee who receives benefits that total A tax-exempt organization may disregard issued in January of These rules are less than the highly compensated amount any request for copies of all or part of any important to the exempt organization ($90,000 in 2004) and who does not hold the document beyond the first two received within community as a whole, and for ensuring executive or voting powers just mentioned; is any 30-day period or the first four received compliance in this area. The new rules provide not a family member of a disqualified person; within any 1-year period from the same a roadmap by which an organization may steer and is not a substantial contributor; individual or the same address, regardless of clear of situations that may give rise to Tax-exempt organizations described in whether the Director EO Examination (or inurement. section 501(c); and designee) has determined that the organization Section 501(c) organizations with respect Under section 4958, any disqualified person is subject to a harassment campaign. to transactions engaged in with other section who benefits from an excess benefit 501(c) organizations. A tax-exempt organization may apply for a transaction with an applicable tax-exempt determination that it is the subject of a organization is liable for a 25% tax on the Who else may be considered a disqualified harassment campaign and that compliance excess benefit. The disqualified person is also person? Other persons not described above with requests that are part of the campaign liable for a 200% tax on the excess benefit if can also be considered disqualified persons, would not be in the public interest by the excess benefit is not corrected by a certain depending on all the relevant facts and submitting a signed application to the Director date. Also, organization managers who circumstances. EO Examination (or designee) for the area participate in an excess benefit transaction knowingly, willfully, and without reasonable Facts and circumstances tending to where the organization s principal office is cause are liable for a 10% tax on the excess show substantial influence: located. benefit, not to exceed $10,000 for all The person founded the organization. In addition, the organization may suspend participating managers on each transaction. The person is a substantial contributor to the compliance with any request it reasonably organization under the section 507(d)(A) believes to be part of the harassment Applicable Tax-Exempt Organization definition, only taking into account contributions campaign until it receives a response to its These rules only apply to certain applicable to the organization for the past 5 years. application for a harassment campaign section 501(c) and 501(c) organizations. The person s compensation is primarily determination. However, if the Director EO An applicable tax-exempt organization is a based on revenues derived from activities of Examination (or designee) determines that the section 501(c) or a section 501(c) the organization that the person controls. organization did not have a reasonable basis organization that is tax-exempt under section The person has or shares authority to control for requesting a determination that it was 501(a), or was such an organization at any or determine a substantial portion of the subject to a harassment campaign or time during a 5-year period ending on the day organization s capital expenditures, operating reasonable belief that a request was part of the of the excess benefit transaction. budget, or compensation for employees. campaign, the officer, director, trustee, The person manages a discrete segment or employee, or other responsible individual of the An applicable tax-exempt organization does activity of the organization that represents a organization remains liable for any penalties for not include: substantial portion of the activities, assets, not providing the copies in a timely fashion. A private foundation as defined in section income, or expenses of the organization, as See Regulations section (d) (a). compared to the organization as a whole. A governmental entity that is exempt from The person owns a controlling interest (or not subject to) taxation without regard to (measured by either vote or value) in a N. Disclosures Regarding Certain section 501(a) or relieved from filing an annual corporation, partnership, or trust that is a Information and Services return under Regulations section disqualified person. Furnished (g)(6). The person is a nonstock organization Certain foreign organizations. controlled directly or indirectly by one or more A section 501(c) organization that offers to sell disqualified persons. or solicits money for specific information or a An organization is not treated as a section routine service for any individual that could be 501(c) or 501(c) organization for any Facts and circumstances tending to obtained by such individual from a federal period covered by a final determination that the show no substantial influence: government agency free or for a nominal organization was not tax-exempt under section The person is an independent contractor charge must disclose that fact conspicuously 501(a), but only if the determination was not whose sole relationship to the organization is when making such offer or solicitation. Any based on private inurement or one or more providing professional advice (without having organization that intentionally disregards this excess benefit transactions. decision-making authority) with respect to General Instructions for Form 990 and Form 990-EZ -11-

6 Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( ) ( ) 408(e) 408A 220(e) 530(a) Print or Type Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2010 or other tax year beginning, 2010, and ending, 20. See separate instructions. Name of organization ( Check box if name changed and see instructions.) Number, street, and room or suite no. If a P.O. box, see instructions. City or town, state, and ZIP code OMB No Open to Public Inspection for 501(c) Organizations Only D Employer identification number (Employees trust, see instructions.) E Unrelated business activity codes (See instructions.) 529(a) C Book value of all assets F Group exemption number (See instructions.) at end of year G Check organization type 501(c) corporation 501(c) trust 401(a) trust Other trust H Describe the organization s primary unrelated business activity. I During the tax year, was the corporation a subsidiary in an affiliated group or a parent-subsidiary controlled group?.. Yes No If Yes, enter the name and identifying number of the parent corporation. J The books are in care of Telephone number Part I Unrelated Trade or Business Income (A) Income (B) Expenses (C) Net 1a Gross receipts or sales b Less returns and allowances c Balance 1c 2 Cost of goods sold (Schedule A, line 7) Gross profit. Subtract line 2 from line 1c a Capital gain net income (attach Schedule D) a b Net gain (loss) (Form 4797, Part II, line 17) (attach Form 4797) 4b c Capital loss deduction for trusts c 5 Income (loss) from partnerships and S corporations (attach statement) 5 6 Rent income (Schedule C) Unrelated debt-financed income (Schedule E) Interest, annuities, royalties, and rents from controlled organizations (Schedule F) Investment income of a section 501(c)(7), (9), or (17) organization (Schedule G) Exploited exempt activity income (Schedule I) Advertising income (Schedule J) Other income (See instructions; attach schedule.) Total. Combine lines 3 through Part II Deductions Not Taken Elsewhere (See instructions for limitations on deductions.) (Except for contributions, deductions must be directly connected with the unrelated business income.) 14 Compensation of officers, directors, and trustees (Schedule K) Salaries and wages Repairs and maintenance Bad debts Interest (attach schedule) Taxes and licenses Charitable contributions (See instructions for limitation rules.) Depreciation (attach Form 4562) Less depreciation claimed on Schedule A and elsewhere on return.. 22a 22b 23 Depletion Contributions to deferred compensation plans Employee benefit programs Excess exempt expenses (Schedule I) Excess readership costs (Schedule J) Other deductions (attach schedule) Total deductions. Add lines 14 through Unrelated business taxable income before net operating loss deduction. Subtract line 29 from line Net operating loss deduction (limited to the amount on line 30) Unrelated business taxable income before specific deduction. Subtract line 31 from line Specific deduction (Generally $1,000, but see line 33 instructions for exceptions.) Unrelated business taxable income. Subtract line 33 from line 32. If line 33 is greater than line 32, enter the smaller of zero or line For Paperwork Reduction Act Notice, see instructions. Cat. No J Form 990-T (2010)

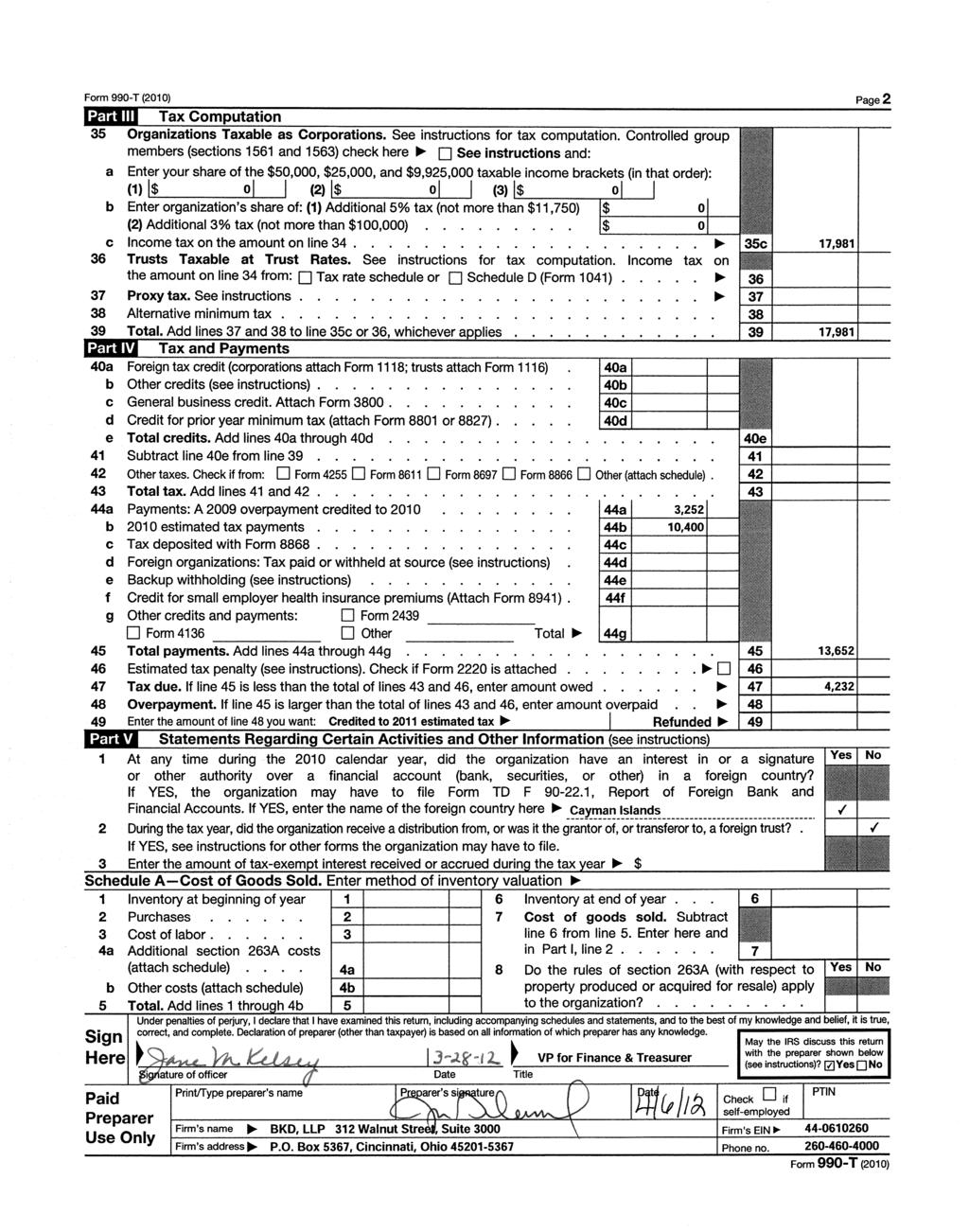

7 Form 990-T (2010) Page 2 Part III Tax Computation 35 Organizations Taxable as Corporations. See instructions for tax computation. Controlled group members (sections 1561 and 1563) check here See instructions and: a Enter your share of the $50,000, $25,000, and $9,925,000 taxable income brackets (in that order): $ $ $ b Enter organization s share of: Additional 5% tax (not more than $11,750) $ Additional 3% tax (not more than $100,000) $ c Income tax on the amount on line c 36 Trusts Taxable at Trust Rates. See instructions for tax computation. Income tax on the amount on line 34 from: Tax rate schedule or Schedule D (Form 1041) Proxy tax. See instructions Alternative minimum tax Total. Add lines 37 and 38 to line 35c or 36, whichever applies Part IV Tax and Payments 40a Foreign tax credit (corporations attach Form 1118; trusts attach Form 1116). 40a b Other credits (see instructions) b c General business credit. Attach Form c d Credit for prior year minimum tax (attach Form 8801 or 8827) d e Total credits. Add lines 40a through 40d e 41 Subtract line 40e from line Other taxes. Check if from: Form 4255 Form 8611 Form 8697 Form 8866 Other (attach schedule) Total tax. Add lines 41 and a Payments: A 2009 overpayment credited to a b 2010 estimated tax payments b c Tax deposited with Form c d Foreign organizations: Tax paid or withheld at source (see instructions). 44d e Backup withholding (see instructions) e f Credit for small employer health insurance premiums (Attach Form 8941). 44f g Other credits and payments: Form 2439 Form 4136 Other Total 44g 45 Total payments. Add lines 44a through 44g Estimated tax penalty (see instructions). Check if Form 2220 is attached Tax due. If line 45 is less than the total of lines 43 and 46, enter amount owed Overpayment. If line 45 is larger than the total of lines 43 and 46, enter amount overpaid Enter the amount of line 48 you want: Credited to 2011 estimated tax Refunded 49 Part V Statements Regarding Certain Activities and Other Information (see instructions) 1 At any time during the 2010 calendar year, did the organization have an interest in or a signature or other authority over a financial account (bank, securities, or other) in a foreign country? If YES, the organization may have to file Form TD F , Report of Foreign Bank and Financial Accounts. If YES, enter the name of the foreign country here 2 During the tax year, did the organization receive a distribution from, or was it the grantor of, or transferor to, a foreign trust?. If YES, see instructions for other forms the organization may have to file. 3 Enter the amount of tax-exempt interest received or accrued during the tax year $ Schedule A Cost of Goods Sold. Enter method of inventory valuation 1 Inventory at beginning of year 1 2 Purchases Cost of labor a Additional section 263A costs (attach schedule).... 4a b Other costs (attach schedule) 4b 5 Total. Add lines 1 through 4b 5 Sign Here 6 Inventory at end of year Cost of goods sold. Subtract line 6 from line 5. Enter here and in Part I, line Do the rules of section 263A (with respect to property produced or acquired for resale) apply to the organization? Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. May the IRS discuss this return with the preparer shown below Signature of officer Date Title (see instructions)? Yes No Print/Type preparer s name Preparer s signature Date Check if PTIN self-employed Firm s name Firm's EIN Firm s address Phone no. Form 990-T (2010) Paid Preparer Use Only Yes Yes No No

8

9 Form 990-T (2010) Page 3 Schedule C Rent Income (From Real Property and Personal Property Leased With Real Property) (see instructions) 1. Description of property (a) From personal property (if the percentage of rent for personal property is more than 10% but not more than 50%) Total 2. Rent received or accrued (b) From real and personal property (if the percentage of rent for personal property exceeds 50% or if the rent is based on profit or income) Total (c) Total income. Add totals of columns 2(a) and 2(b). Enter here and on page 1, Part I, line 6, column (A)... Schedule E Unrelated Debt-Financed Income (see instructions) 1. Description of debt-financed property 4. Amount of average acquisition debt on or allocable to debt-financed property (attach schedule) 5. Average adjusted basis of or allocable to debt-financed property (attach schedule) 2. Gross income from or allocable to debt-financed property 6. Column 4 divided by column 5 % % % % 3(a) Deductions directly connected with the income in columns 2(a) and 2(b) (attach schedule) (b) Total deductions. Enter here and on page 1, Part I, line 6, column (B) 3. Deductions directly connected with or allocable to debt-financed property (a) Straight line depreciation (attach schedule) 7. Gross income reportable (column 2 column 6) Enter here and on page 1, Part I, line 7, column (A). Totals Total dividends-received deductions included in column Schedule F Interest, Annuities, Royalties, and Rents From Controlled Organizations (see instructions) Exempt Controlled Organizations 1. Name of controlled organization Nonexempt Controlled Organizations 2. Employer identification number 3. Net unrelated income (loss) (see instructions) 4. Total of specified payments made 5. Part of column 4 that is included in the controlling organization s gross income (b) Other deductions (attach schedule) 8. Allocable deductions (column 6 total of columns 3(a) and 3(b)) Enter here and on page 1, Part I, line 7, column (B). 6. Deductions directly connected with income in column 5 7. Taxable Income 8. Net unrelated income (loss) (see instructions) 9. Total of specified payments made 10. Part of column 9 that is included in the controlling organization s gross income 11. Deductions directly connected with income in column 10 Totals Add columns 5 and 10. Enter here and on page 1, Part I, line 8, column (A). Add columns 6 and 11. Enter here and on page 1, Part I, line 8, column (B). Form 990-T (2010)

10 Form 990-T (2010) Page 4 Schedule G Investment Income of a Section 501(c)(7), (9), or (17) Organization (see instructions) 1. Description of income 2. Amount of income Enter here and on page 1, Part I, line 9, column (A). 3. Deductions directly connected (attach schedule) 4. Set-asides (attach schedule) Totals Schedule I Exploited Exempt Activity Income, Other Than Advertising Income (see instructions) 1. Description of exploited activity 2. Gross unrelated business income from trade or business 3. Expenses directly connected with production of unrelated business income 4. Net income (loss) from unrelated trade or business (column 2 minus column 3). If a gain, compute cols. 5 through Gross income from activity that is not unrelated business income 6. Expenses attributable to column 5 5. Total deductions and set-asides (col. 3 plus col. 4) Enter here and on page 1, Part I, line 9, column (B). 7. Excess exempt expenses (column 6 minus column 5, but not more than column 4). Enter here and on page 1, Part I, line 10, col. (A). Enter here and on page 1, Part I, line 10, col. (B). Totals Schedule J Advertising Income (see instructions) Part I Income From Periodicals Reported on a Consolidated Basis 1. Name of periodical 2. Gross advertising income 3. Direct advertising costs 4. Advertising gain or (loss) (col. 2 minus col. 3). If a gain, compute cols. 5 through Circulation income 6. Readership costs Enter here and on page 1, Part II, line Excess readership costs (column 6 minus column 5, but not more than column 4). Totals (carry to Part II, line (5)).. Part II Income From Periodicals Reported on a Separate Basis (For each periodical listed in Part II, fill in columns 2 through 7 on a line-by-line basis.) 1. Name of periodical 2. Gross advertising income 3. Direct advertising costs 4. Advertising gain or (loss) (col. 2 minus col. 3). If a gain, compute cols. 5 through Circulation income 6. Readership costs 7. Excess readership costs (column 6 minus column 5, but not more than column 4). Totals from Part I Enter here and on page 1, Part I, line 11, col. (A). Enter here and on page 1, Part I, line 11, col. (B). Totals, Part II (lines 1-5).... Schedule K Compensation of Officers, Directors, and Trustees (see instructions) 3. Percent of 1. Name 2. Title time devoted to business % % % % Total. Enter here and on page 1, Part II, line Enter here and on page 1, Part II, line Compensation attributable to unrelated business Form 990-T (2010)

-8- General Instructions for Form 990 and Form 990-EZ

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $250 or value of similar

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $250 or value of similar

organization provides in consideration Use Form 4506-A to request:

Goods or services a donee Through the IRS Note that a section 527 political organization provides in consideration Use Form 4506-A to request: TIP organization (and an for a payment by a taxpayer include

Goods or services a donee Through the IRS Note that a section 527 political organization provides in consideration Use Form 4506-A to request: TIP organization (and an for a payment by a taxpayer include

-8- General Instructions for Form 990 and Form 990-EZ

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $25 or value of similar

b. Within the low-cost article limitation. contributions made by a taxpayer to a donee determined by reference to the fair market Examples. organization during a tax year equals $25 or value of similar

Brett R. Harris, Esq.

Sobel & Co. s Nonprofit and Social Services Group Webinar IRS Disclosure Requirements: What Do Organizations Need to Provide to Donors? February 15, 2012 Brett R. Harris, Esq. Wilentz, Goldman & Spitzer,

Sobel & Co. s Nonprofit and Social Services Group Webinar IRS Disclosure Requirements: What Do Organizations Need to Provide to Donors? February 15, 2012 Brett R. Harris, Esq. Wilentz, Goldman & Spitzer,

Exempt Organization Business Income Tax Return

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2017

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2017

Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e))

)") Form 99-T PUBLIC DISCLOSURE COPY Exempt Organization Business Income Tax Return (and proxy tax under section 633(e)) OMB No. 1545-687 215 For calendar year 215 or other tax year beginning 7/1, 215, and

Form 99-T PUBLIC DISCLOSURE COPY Exempt Organization Business Income Tax Return (and proxy tax under section 633(e)) OMB No. 1545-687 215 For calendar year 215 or other tax year beginning 7/1, 215, and

Print or Type. For Paperwork Reduction Act Notice, see instructions. Cat. No J Form 990-T (2010)

") Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( ) ( ) 408(e) 408A 220(e) 530(a) Print or Type Exempt Organization Business Income

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( ) ( ) 408(e) 408A 220(e) 530(a) Print or Type Exempt Organization Business Income

*** PUBLIC DISCLOSURE COPY*** Exempt Organization Business Income Tax Return. (and proxy tax under section 6033(e)) OCT 1, 2016 SEP 30, 2017

) OCT 1, 2016 SEP 30, 2017") Form Department of the Treasury Internal Revenue Service A 62701 01-18-17 For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at

Form Department of the Treasury Internal Revenue Service A 62701 01-18-17 For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at

Exempt Organization Business Income Tax Return

Form 990-T Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) OMB No. 1545-0687 For calendar year 2010 or other tax year beginning, 2010, and 2010 Department of the Treasury

Form 990-T Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) OMB No. 1545-0687 For calendar year 2010 or other tax year beginning, 2010, and 2010 Department of the Treasury

Exempt Organization Business Income Tax Return

Form A B C H I J Part I Part II 990-T Department of the Treasury Internal Revenue Service Check box if address changed Exempt under section X C 3 Exempt Organization Business Income Tax Return Unrelated

Form A B C H I J Part I Part II 990-T Department of the Treasury Internal Revenue Service Check box if address changed Exempt under section X C 3 Exempt Organization Business Income Tax Return Unrelated

EXTENSION GRANTED TO 05/15/13 OMB No Form. (and proxy tax under section 6033(e)) 2011

) 2011") EXTENSION GRANTED TO 05/15/1 OMB No. 1545-0687 Form 0-T Exempt Organization Business Income Tax Return Department of the Treasury (and proxy tax under section 60(e)) 011 Open to Public Inspection for Internal

EXTENSION GRANTED TO 05/15/1 OMB No. 1545-0687 Form 0-T Exempt Organization Business Income Tax Return Department of the Treasury (and proxy tax under section 60(e)) 011 Open to Public Inspection for Internal

990-T PUBLIC DISCLOSURE

015 0-T PUBLIC DISCLOSURE Form OMB No. 1545-0687 (and proxy tax under section 60(e)) For calendar year 015 or other tax year beginning JUL 1, 015, and ending JUN 0, 016. 015 Information about Form 0-T

015 0-T PUBLIC DISCLOSURE Form OMB No. 1545-0687 (and proxy tax under section 60(e)) For calendar year 015 or other tax year beginning JUL 1, 015, and ending JUN 0, 016. 015 Information about Form 0-T

Exempt Organization Business Income Tax Return

PUBLIC DISCLOSURE EXTENDED TO NOVEMBER 15, 2018 Form Exempt Organization Business Income Tax Return 0-T For calendar year 2017 or other tax year beginning Check box if address changed B Exempt under section

PUBLIC DISCLOSURE EXTENDED TO NOVEMBER 15, 2018 Form Exempt Organization Business Income Tax Return 0-T For calendar year 2017 or other tax year beginning Check box if address changed B Exempt under section

Exempt Organization Business Income Tax Return

Exempt Organization Business Income Tax Return Form OMB No. 1545-0687 0-T (and proxy tax under section 6033(e)) For calendar year 2016 or other tax year beginning APR 1, 2016, and ending MAR 31, 2017.

Exempt Organization Business Income Tax Return Form OMB No. 1545-0687 0-T (and proxy tax under section 6033(e)) For calendar year 2016 or other tax year beginning APR 1, 2016, and ending MAR 31, 2017.

Extended to November 15, 2017 Exempt Organization Business Income Tax Return. (and proxy tax under section 6033(e))

)") Form Department of the Treasury Internal Revenue Service A For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at www.irs.gov/form0t.

Form Department of the Treasury Internal Revenue Service A For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at www.irs.gov/form0t.

OMB No Form. (and proxy tax under section 6033(e)) Name of organization ( Check box if name changed and see instructions.

) Name of organization ( Check box if name changed and see instructions.") OMB No. 1545-0687 Form 0-T Exempt Organization Business Income Tax Return Department of the Treasury (and proxy tax under section 60(e)) 00 Open to Public Inspection for Internal Revenue Service (77) For

OMB No. 1545-0687 Form 0-T Exempt Organization Business Income Tax Return Department of the Treasury (and proxy tax under section 60(e)) 00 Open to Public Inspection for Internal Revenue Service (77) For

990-T PUBLIC DISCLOSURE

015 0-T PUBLIC DISCLOSURE Form OMB No. 1545-0687 (and proxy tax under section 60(e)) For calendar year 015 or other tax year beginning JUL 1, 015, and ending JUN 0, 016. 015 Information about Form 0-T

015 0-T PUBLIC DISCLOSURE Form OMB No. 1545-0687 (and proxy tax under section 60(e)) For calendar year 015 or other tax year beginning JUL 1, 015, and ending JUN 0, 016. 015 Information about Form 0-T

Exempt Organization Business Income Tax Return

0-T Exempt Organization Business Income Tax Return Form OMB No. 1545-0687 (and proxy tax under section 6033(e)) For calendar year 2015 or other tax year beginning, and ending. 2015 Information about Form

0-T Exempt Organization Business Income Tax Return Form OMB No. 1545-0687 (and proxy tax under section 6033(e)) For calendar year 2015 or other tax year beginning, and ending. 2015 Information about Form

Copy for Public Inspection

Copy for Public Inspection Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) Department of the Treasury Internal Revenue Service Open A Check

Copy for Public Inspection Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) Department of the Treasury Internal Revenue Service Open A Check

Exempt Organization Business Income Tax Return OMB No

Form 990-T Exempt Organization Business Income Tax Return OMB No. 1545-0687 For calendar year 2016 or other tax year beginning (and proxy tax under section 6033(e)), 2016, and ending, 2016 G Information

Form 990-T Exempt Organization Business Income Tax Return OMB No. 1545-0687 For calendar year 2016 or other tax year beginning (and proxy tax under section 6033(e)), 2016, and ending, 2016 G Information

Exempt Organization Business Income Tax Return

Form Department of the Treasury Internal Revenue Service A For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at www.irs.gov/form0t.

Form Department of the Treasury Internal Revenue Service A For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at www.irs.gov/form0t.

Go to for instructions and the latest information.

Form 990-T Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2017 or other tax year beginning, and ending. Department of the Treasury Go to www.irs.gov/form990t

Form 990-T Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2017 or other tax year beginning, and ending. Department of the Treasury Go to www.irs.gov/form990t

Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e))

)") 5/14/218 2:18:46 PM 1 216 Return Temple University - Of the Commonwealth Form 99-T PUBLIC DISCLOSURE COPY Exempt Organization Business Income Tax Return (and proxy tax under section 633(e)) OMB No. 1545-687

5/14/218 2:18:46 PM 1 216 Return Temple University - Of the Commonwealth Form 99-T PUBLIC DISCLOSURE COPY Exempt Organization Business Income Tax Return (and proxy tax under section 633(e)) OMB No. 1545-687

Instructions for Form 990-PF

2001 Instructions for Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Section references are to the Internal Revenue Code unless

2001 Instructions for Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Section references are to the Internal Revenue Code unless

Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e))

)") 5/11/218 11:23: AM 1 217 Return YOUNG MEN'S CHRISTIAN ASSOCIATION Form 99-T PUBLIC DISCLOSURE COPY Exempt Organization Business Income Tax Return (and proxy tax under section 633(e)) OMB No. 1545-687 217

5/11/218 11:23: AM 1 217 Return YOUNG MEN'S CHRISTIAN ASSOCIATION Form 99-T PUBLIC DISCLOSURE COPY Exempt Organization Business Income Tax Return (and proxy tax under section 633(e)) OMB No. 1545-687 217

Exempt Organization Business Income Tax Return (and

Form 990-T Exempt Organization Business Income Tax Return (and OMB No. 1545-0687 proxy tax under section 6033(e)) For calendar year 2012 or other tax year beginning 7/01, 2012, 2012 and ending 6/30, 2013

Form 990-T Exempt Organization Business Income Tax Return (and OMB No. 1545-0687 proxy tax under section 6033(e)) For calendar year 2012 or other tax year beginning 7/01, 2012, 2012 and ending 6/30, 2013

Exempt Organization Business Income Tax Return

OMB No. 1545-06 Form Exempt Organization Business Income Tax Return Department of the Treasury (and proxy tax under section 6033(e)) Open to Public Inspection for Internal Revenue Service For calendar

OMB No. 1545-06 Form Exempt Organization Business Income Tax Return Department of the Treasury (and proxy tax under section 6033(e)) Open to Public Inspection for Internal Revenue Service For calendar

A For the 2011 calendar year, or tax year beginning, 2011, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black

Exempt Organization Business Income Tax Return

Form Department of the Treasury Internal Revenue Service For calendar year 2017 or other tax year beginning, and ending. Go to www.irs.gov/form0t for instructions and the latest information. Do not enter

Form Department of the Treasury Internal Revenue Service For calendar year 2017 or other tax year beginning, and ending. Go to www.irs.gov/form0t for instructions and the latest information. Do not enter

Charitable Contributions

Charitable Contributions Substantiation and Disclosure Requirements INTERNAL REVENUE SERVICE Tax Exempt and Government Entities Exempt Organizations Are you an organization that receives contributions

Charitable Contributions Substantiation and Disclosure Requirements INTERNAL REVENUE SERVICE Tax Exempt and Government Entities Exempt Organizations Are you an organization that receives contributions

Exempt Organization Business Income Tax Return

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2016

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2016

Charitable Contributions. Substantiation and Disclosure Requirements

Charitable Contributions Substantiation and Disclosure Requirements 1 Are you an organization that receives contributions of $250 or more? or Are you an organization that provides goods or services to

Charitable Contributions Substantiation and Disclosure Requirements 1 Are you an organization that receives contributions of $250 or more? or Are you an organization that provides goods or services to

Exempt Organization Business Income Tax Return

Form Department of the Treasury Internal Revenue Service A For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at www.irs.gov/form0t.

Form Department of the Treasury Internal Revenue Service A For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at www.irs.gov/form0t.

Exempt Organization Business Income Tax Return. (and proxy tax under section 6033(e))

)") Form A B 990-T Department of the Treasury Internal Revenue Service Check box if address changed Exempt under section Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e))

Form A B 990-T Department of the Treasury Internal Revenue Service Check box if address changed Exempt under section Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e))

EXTENDED TO NOVEMBER 15, 2018 Exempt Organization Business Income Tax Return. (and proxy tax under section 6033(e)) YORBA LINDA, CA

) YORBA LINDA, CA") Form 0-T Department of the Treasury Internal Revenue Service EXTENDED TO NOVEMBER 15, 2018 Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2017 or

Form 0-T Department of the Treasury Internal Revenue Service EXTENDED TO NOVEMBER 15, 2018 Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2017 or

EXTENDED TO MAY 15, 2019 Exempt Organization Business Income Tax Return. (and proxy tax under section 6033(e)) JUL 1, 2017 JUN 30, 2018

) JUL 1, 2017 JUN 30, 2018") Form Department of the Treasury Internal Revenue Service For calendar year 2017 or other tax year beginning, and ending. Go to www.irs.gov/form0t for instructions and the latest information. Do not enter

Form Department of the Treasury Internal Revenue Service For calendar year 2017 or other tax year beginning, and ending. Go to www.irs.gov/form0t for instructions and the latest information. Do not enter

Exempt Organization Business Income Tax Return

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( c ) ( 3 ) 408(e) 408A 220(e) 530(a) Print or Type Exempt Organization Business

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( c ) ( 3 ) 408(e) 408A 220(e) 530(a) Print or Type Exempt Organization Business

**PUBLIC DISCLOSURE COPY** Exempt Organization Business Income Tax Return. (and proxy tax under section 6033(e))

)") Form Department of the Treasury Internal Revenue Service 72371 1-22-18 For calendar year 217 or other tax year beginning, and ending. Go to www.irs.gov/formt for instructions and the latest information.

Form Department of the Treasury Internal Revenue Service 72371 1-22-18 For calendar year 217 or other tax year beginning, and ending. Go to www.irs.gov/formt for instructions and the latest information.

Exempt Organization Business Income Tax Return

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( ) ( ) c 408(e) 408A 220(e) 530(a) Exempt Organization Business Income Tax Return

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( ) ( ) c 408(e) 408A 220(e) 530(a) Exempt Organization Business Income Tax Return

A For the 2010 calendar year, or tax year beginning, 2010, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Exempt Organization Business Income Tax Return

Form 623701 01-18-17 OMB No. 1545-0687 For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at www.irs.gov/form0t. Department of

Form 623701 01-18-17 OMB No. 1545-0687 For calendar year 2016 or other tax year beginning, and ending. Information about Form 0-T and its instructions is available at www.irs.gov/form0t. Department of

Number and street (or P.O. box, if mail is not delivered to street address) Room/suite

Room/suite") Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring organizations

Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring organizations

Exempt Organization Business Income Tax Return

Form Department of the Treasury Internal Revenue Service A For calendar year 2016 or other tax year beginning, and ending. OMB No. 1545-0687 Information about Form 0-T and its instructions is available

Form Department of the Treasury Internal Revenue Service A For calendar year 2016 or other tax year beginning, and ending. OMB No. 1545-0687 Information about Form 0-T and its instructions is available

TAX RETURN FILING INSTRUCTIONS

TAX RETURN FILING INSTRUCTIONS PUBLIC DISCLOSURE COPY FEDERAL FORM 990-T FOR THE YEAR ENDING DECEMBER 31, 2016 ~~~~~~~~~~~~~~~~~ Prepared for AMERICAN PSYCHOLOGICAL ASSOCIATION, INC. 750 FIRST STREET,

TAX RETURN FILING INSTRUCTIONS PUBLIC DISCLOSURE COPY FEDERAL FORM 990-T FOR THE YEAR ENDING DECEMBER 31, 2016 ~~~~~~~~~~~~~~~~~ Prepared for AMERICAN PSYCHOLOGICAL ASSOCIATION, INC. 750 FIRST STREET,

Open to Public Internal Revenue Service The organization may have to use a copy of this return to satisfy state reporting requirements.

Form990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) 2002

Form990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) 2002

Return of Organization Exempt From Income Tax

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust

EXTENDED TO APRIL 18, 2017 Exempt Organization Business Income Tax Return. (and proxy tax under section 6033(e)) JUN 1, 2015 MAY 31, 2016

) JUN 1, 2015 MAY 31, 2016") Form Department of the Treasury Internal Revenue Service A B For calendar year 2015 or other tax year beginning, and ending. OMB No. 1545-0687 Information about Form 0-T and its instructions is available

Form Department of the Treasury Internal Revenue Service A B For calendar year 2015 or other tax year beginning, and ending. OMB No. 1545-0687 Information about Form 0-T and its instructions is available

Exempt Organization Business Income Tax Return

OMB No. 1545-0687 Form Exempt Organization Business Income Tax Return Department of the Treasury (and proxy tax under section 60(e)) Open to Public Inspection for Internal Revenue Service For calendar

OMB No. 1545-0687 Form Exempt Organization Business Income Tax Return Department of the Treasury (and proxy tax under section 60(e)) Open to Public Inspection for Internal Revenue Service For calendar

Number and street (or P.O. box, if mail is not delivered to street address) Room/suite

Room/suite") Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

PUBLIC INSPECTION COPY

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e))

)") Form 990-T Department of the Treasury Internal Revenue Service - Check box if A address changed B Exempt under section 3--(1 501( C )( 3 I 408(e) 408A 529(a) C Book value of all assets at end of year 220(e)

Form 990-T Department of the Treasury Internal Revenue Service - Check box if A address changed B Exempt under section 3--(1 501( C )( 3 I 408(e) 408A 529(a) C Book value of all assets at end of year 220(e)

F Group Exemption Number G Accounting Method: Cash Accrual Other (specify) H Check if the organization is not I Website:

H Check if the organization is not I Website:") Form 99-EZ Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

Form 99-EZ Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

A For the 2011 calendar year, or tax year beginning 07/01 B Check if applicable:

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

SEATTLE ART MUSEUM FORM 990 T

SEATTLE ART MUSEUM PUBLIC DISCLOSURE INSTRUCTIONS FOR EXEMPT ORGANIZATION BUSINESS INCOME TAX RETURN FORM 0 T 1. THE PUBLIC DISCLOSURE COPY MUST BE SIGNED AND DATED BY AN OFFICER OF THE ORGANIZATION, INDICATING

SEATTLE ART MUSEUM PUBLIC DISCLOSURE INSTRUCTIONS FOR EXEMPT ORGANIZATION BUSINESS INCOME TAX RETURN FORM 0 T 1. THE PUBLIC DISCLOSURE COPY MUST BE SIGNED AND DATED BY AN OFFICER OF THE ORGANIZATION, INDICATING

Short Form 990-EZ Return of Organization Exempt From Income Tax

Form B G I J Short Form 990-EZ Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Do not enter Social

Form B G I J Short Form 990-EZ Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Do not enter Social

A For the 2010 calendar year, or tax year beginning, 2010, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Open to Public Inspection for 501(c)(3) Organizations Only A Check box if. D Employer identification number address changed

(3) Organizations Only A Check box if. D Employer identification number address changed") Form 990-T Exempt Organization Business Income Tax Return OMB No. 1545-0687 (and proxy tax under section 6033(e)) For calendar year 2016 or other tax year beginning 10/01, 2016, and ending 9/30, 2017 2016

Form 990-T Exempt Organization Business Income Tax Return OMB No. 1545-0687 (and proxy tax under section 6033(e)) For calendar year 2016 or other tax year beginning 10/01, 2016, and ending 9/30, 2017 2016

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Exempt Organization Business Income Tax Return OMB No

Form 990-T Exempt Organization Business Income Tax Return OMB No. 1545-0687 For calendar year 2016 or other tax year beginning (and proxy tax under section 6033(e)), 2016, and ending, 2016 G Information

Form 990-T Exempt Organization Business Income Tax Return OMB No. 1545-0687 For calendar year 2016 or other tax year beginning (and proxy tax under section 6033(e)), 2016, and ending, 2016 G Information

HOW TO COMPLY WITH THE PRIVATE FOUNDATION DISCLOSURE REQUIREMENTS

HOW TO COMPLY WITH THE PRIVATE FOUNDATION DISCLOSURE REQUIREMENTS SIMPSON THACHER & BARTLETT LLP FEBRUARY 17, 2000 The Treasury Department recently published final regulations which require broader public

HOW TO COMPLY WITH THE PRIVATE FOUNDATION DISCLOSURE REQUIREMENTS SIMPSON THACHER & BARTLETT LLP FEBRUARY 17, 2000 The Treasury Department recently published final regulations which require broader public

A For the 2011 calendar year, or tax year beginning, 2011, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black