2011 Federal & California Tax Update for Individuals

|

|

|

- Preston Haynes

- 5 years ago

- Views:

Transcription

1 CALIFORNIA CPA EDUCATION FOUNDATION 2011 Federal & California Tax Update for Individuals Gary R. McBride & Thomas C. Daley January 2012 Supplement

2 2012 Busy Season Look-Out List Foreign Asset Reporting: New Form 8938 required for individuals with specified foreign financial asset holdings over threshold amounts. Cost Basis Reporting: New Form 8949 requires segregation and identification of capital gain transactions. (Sch. D Instructions) Cost Basis Elections: New cost basis rules require election of default methods for determining basis of stock and mutual funds. Capitalization Regs: Regulations effective 1/1/2012 provide new rules and safe harbors for distinguishing capital expenditures from repairs. (Reg 1.263(a)-2T & 3T) Revised Schedule E: Disclosure of property type required. Form 1099-MISC Questions: Business tax returns and 1040 Schedules C, E, and F require inquiry regarding client filing of Form 1009s. Passive Activity Grouping Disclosure: New passive activity grouping disclosure rules kick in for activities acquired in (Rev. Proc ) Late Aggregation Elections for Real Professionals: Retroactive rental property aggregation election allowed for real estate professionals under the new relief provision. (Rev. Proc ). Mortgage Assistance Payments: Safe harbor method for reporting mortgage interest and property tax payments for recipients of federal mortgage assistance payments. (Notice ) Adult Child Insurance Coverage: California retroactive conformity to 2010 federal law change creates potential refund opportunity for clients who reported a 2010 fed- Cal difference for health insurance on an adult child. (AB 36) Self-Employed Health Insurance: Health insurance premiums no longer deductible in computing SE Tax; however, IRS now allows Medicare premiums to count as SE health insurance. Earned Income Tax Credit Due Diligence Requirements: Submission of Form 8867 required to avoid $500 preparer penalty. Energy Credits: New dollar limits and eligibility requirements apply in 2011 for residential energy credits and green vehicle credits. (Secs. 25C,, 30, 30B, 30C) California Use Tax Table: New standard use tax table for safe-harbor reporting of small internet purchases. (SB 86)

3 New Hire Credit: Federal credit of $1,000 for qualified employees hired in 2010 and retained for 52 weeks. (Form 5884-B) Credit for Hiring Veterans. Expanded work opportunity tax credit for hiring qualified veterans after 11/21/2011. California Multi-State Apportionment Changes: Single sales factor apportionment option (with market-based sourcing for services and intangibles) may be elected in Finnigan Rule applies for determining throwback sales of combined groups. Bonus Depreciation Component Election: Written election required to claim 100% bonus depreciation on components of building placed in service in 2011, where construction began prior to 9/9/2010. (Rev. Proc ) Accounting Method Changes: New Rev. Proc replaced Rev. Proc as operative guidance for automatic accounting method changes. Includes a new automatic change for accrual of California franchise tax deduction. IRS Voluntary Classification Settlement Program: Low-cost settlement program offered by IRS to employers who have misclassified employees as independent contractors. New California Penalties for Misclassifying Employees: SB 459 gives the California Department of Industrial Relations authority to impose penalties on employers who misclassify employees as independent contractors. The penalty can also be imposed on CPAs who give incorrect advice on employee classification. Innocent Spouse Relief: IRS drops 2-year limit on filing claims for equitable relief under the innocent spouse rules. (Notice ) Estate Tax $5 Million Exclusion Portability: For deaths of a first spouse in 2011, consideration must be given to filing a Form 706 in order to elect to carry over the unused exclusion amount to the estate of the surviving spouse. Estate Tax Deductions for Unpaid Claims: The IRS has established new procedures for filing protective claims for refund of estate tax based upon deductions for claims of against the estate that remain unpaid as of the filing date of the Form 706. (Rev. Proc ) Modified Carryover Basis Calculations: IRS has established safe harbor rules for calculating the basis of assets inherited from the estate of a 2010 decedent that elects out of federal estate tax. (Rev. Proc ) Reinstatement of Exempt Status: IRS establishes procedures for charities to reinstate exempt status lost due to failure to file 990s. (Notices & 44)

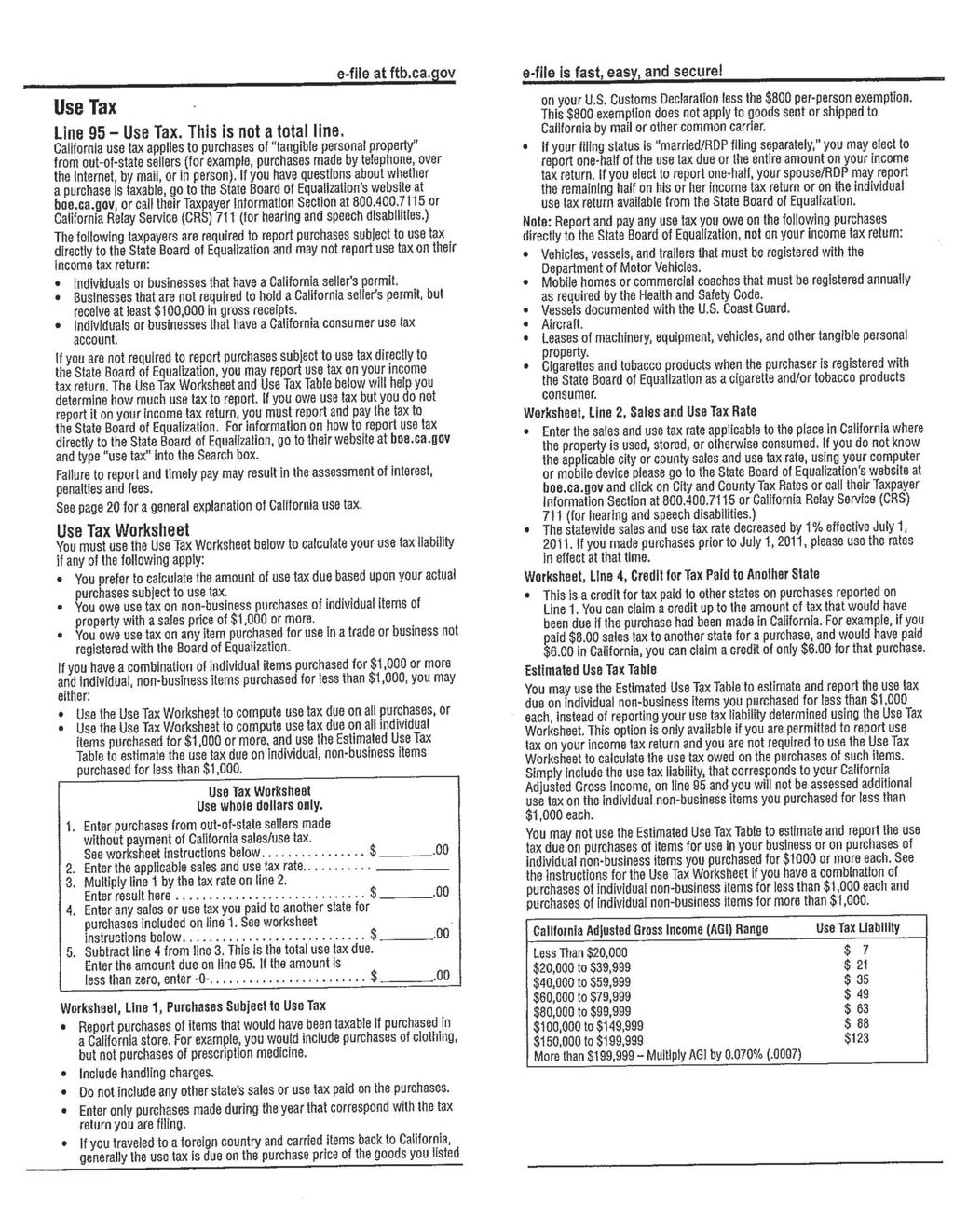

4 January 2012 Supplement Chapter 1: Page 1-1: Deficit Reduction Committee Fails to Produce Recommendations As everyone knows, the 12-member Super-Committee failed to agree upon a package for reducing the federal deficit over the next 10 years. Therefore, no new tax legislation emerged from their deliberations. Absent further action, the automatic sequestration process goes into effect to automatically cut federal program budgets at the end of this year. Page 1-2: No Sunset for SB 401 Because there have been no lawsuits filed challenging the constitutionality of SB 401, the conformity changes made by that legislation will remain in effect for 2011 tax returns. Page 1-6: 2% Payroll Tax Cut Extended for 2 Months On 12/23/2011, President Obama signed into law P.L , extending the 2% cut in the employee FICA and self-employment tax rates through the end of February If the cut is not further extended for the remainder of 2012, there is a recapture mechanism which imposes additional income tax equal to the amount of the 2% payroll tax savings on earnings in the first two months of 2012 in excess of $18,350 i.e., 2/12 of the social security wage base for Page 1-9: Correction The second to last paragraph should read For 2011 we are back to... Page 1-10: Correction of 2012 Sec. 179 Expense Amounts For tax years beginning in 2012, the correct sec. 179 expense limit is $139,000, with the phaseout of the limit for sec. 179 asset acquisitions in excess of $560,000. Page 1-13: FTB Publishes Standard Use Tax Table California individuals who report use tax on out-of-state purchases can elect to pay the tax by reporting it on their Form 540. This year, the form includes a table with standard use tax amounts that be reported (based upon AGI) for non-business purchases of items costing under $1,000 individually. The table and instructions are shown on the following two pages.

5

6 Chapter 2: Page 2-9: Form 8938 Finalized and Required for 2011 Tax Returns The IRS has issued the final version of form 8938 and instructions, in conjunction with the publication of temporary regulations under sec. 6038D outlining the new reporting requirements. These new reporting rules are covered in the second day of this course. Chapter 3: Page 3-3: Form 1098-MA Issued for Reporting Mortgage Assistance Payments The IRS has issued a new form to be used by state housing authorities to report mortgage assistance payments made to lenders on behalf of homeowners participating in HFA Hardest Hit Fund and Emergency Homeowners Loan Program. The Form 1098-MA informs the homeowner how much the agency paid to the mortgage lender, split between the amount paid by agency and the amount paid by the homeowner. Chapter 4: Page 4-2: Correction The first line of page 4-2 should read The IRS has changed both the 1099-B and the Form 1040 Schedule D... Page 4-6: IRS Issues final Schedule D Instructions with Form 8949 Adjustment Codes The IRS issued the final version of the instructions for completing the Form 8949, including a table with 10 Column b codes, as shown on the following page. This represents a significant change from the initial version of the instructions, which had 21 different codes to be used in reporting a wide variety of different gains and losses. Our initial speculation was that these codes were sought for IRS data mining purposes, in seeking to gather additional information on asset sales. For whatever reason, the Service backed off on this in the final version of the form. Page 4-14: Form 8937 Issued for Reporting Organizational Actions Affecting Stock Basis The IRS has issued Form 8937, the form to be used by corporations to report organizational actions (such as mergers) that affect the basis of their securities held by investors. It is unlikely that many corporations will ever use this form, given the alternative they have of simply reporting the organizational action on their website.

7 How To Complete Form 8949, Columns (b) and (g) For most transactions, you do not need to complete columns (b) and (g) and can leave them blank. You may need to complete columns (b) and (g) if you got a Form 1099-B or 1099-S that is incorrect, if you are excluding or postponing a capital gain, if you have a disallowed loss, or in certain other situations. Details are in the table below. THEN enter this code IF... AND... in column (b)... You received a Form 1099-B (or substitute statement) and the basis shown in box 3 is incorrect.... Enter the basis shown on Form 1099-B (or substitute statement) in column (f). B If the correct basis is higher than the basis shown on Form 1099-B (or substitute statement), enter the difference between the two amounts as a negative number (in parentheses) in column (g). If the correct basis is lower than the basis shown on Form 1099-B (or substitute statement), enter the difference between the two amounts as a positive number in column (g). You received a Form 1099-B (or substitute statement) Enter -0- in column (g) unless an adjustment is required because of and the type of gain or loss (short term or long term) T another code. Report the gain or loss in the correct Part of Form shown in box 8 is incorrect You received a Form 1099-B or 1099-S as a nominee Report the transaction on Form 8949 as you would if you were the for the actual owner of the property.... N actual owner, but enter any resulting gain as a negative adjustment (in parentheses) in column (g) or any resulting loss as a positive adjustment in column (g). However, if you received capital gain distributions as a nominee, report them instead as described under Capital Gain Distributions, earlier. You sold or exchanged your main home at a gain, Report the sale or exchange on Form 8949 as you would if you were must report the sale or exchange on Form 8949, and not taking the exclusion. Then enter the amount of excluded H can exclude some or all of the gain.... (nontaxable) gain as a negative number (in parentheses) in column (g). See the example in the instructions for Form 8949, column (g). You sold or exchanged qualified small business stock Report the sale or exchange on Form 8949 as you would if you were and can exclude part of the gain.... S not taking the exclusion. Then enter the amount of the exclusion as a negative number (in parentheses) in column (g). You can exclude all or part of your gain under the Report the sale or exchange on Form 8949 as you would if you were rules explained earlier in these instructions for DC X not taking the exclusion. Then enter the amount of the exclusion as a Zone assets or qualified community assets.... negative number (in parentheses) in column (g). You are electing to postpone all or part of your gain Report the sale or exchange on Form 8949 as you would if you were under the rules explained earlier in these instructions not making the election. Then enter the amount of postponed gain as for rollover of gain from QSB stock, empowerment R a negative number (in parentheses) in column (g). zone assets, publicly traded securities, or stock sold to ESOPs or certain cooperatives.... You have a nondeductible loss from a wash sale.... Enter the amount of the nondeductible loss as a positive number in W column (g). See Wash Sales, earlier, for details. You have a nondeductible loss other than a loss Enter the amount of the nondeductible loss as a positive number in L indicated by code W.... column (g). See the example under Nondeductible Losses, earlier. You include any expense of sale or certain option Enter your expenses of sale or the appropriate adjustment amount in premiums in column (g) or you have an adjustment column (g). Enter any expenses of sale as a negative number (in not explained above in this column.... parentheses). See the instructions for Form 8949, column (g). If you O sold a call option and it was exercised, see Gain or Loss From Options, earlier, for information about reporting certain option premiums. None of the other statements in this column apply... Leave columns (b) and (g) blank. Schedule D next dollar. For example, $1.39 becomes sales price (column (e)). Then take into ac- $1 and $2.50 becomes $3. count any adjustments in column (g). Enter Complete all necessary pages of Form 8949 the gain or loss in column (h). Enter negabefore you complete line 1, 2, 3, 8, 9, or 10 If you have to add two or more amounts tive amounts in parentheses. of Schedule D. to figure the amount to enter on a line, include cents when adding the amounts and Rounding Off to Whole Dollars Example 1. Column (e) is $6,000 and round off only the total. column (f) is ($2,000). Enter $4,000 in col- You can round off cents to whole dollars on Lines 1, 2, 3, 8, 9, and 10, column umn (h). your Schedule D. If you do round to whole dollars, you must round all amounts. To (h) Gain or Loss Example 2. Column (e) is $6,000 and round, drop amounts under 50 cents and Figure gain or loss on each line. First, sub- column (f) is ($8,000). Enter ($2,000) in increase amounts from 50 to 99 cents to the tract cost or other basis (column (f)) from column (h). D-10

8 Chapter 5: Page 5-13: Case Name Correction The name of the case at the top of the page should be Viralam v. Comm r. (Gundanna is the taxpayer s middle name.) Chapter 6: Page 6-7: IRS Extends Special Madoff Loss Safe Harbor to Dead Ponzis As noted on page 6-7, Rev. Proc provides an optional safe harbor allowing certain investors to claim a theft loss deduction e for qualified losses from certain fraudulent investment schemes.use of this safe requires that authorities have charged the lead figure by indictment, information, or criminal complaint with a crime that meets the definition of theft for purposes of sec What happens if the swindler dies before the required criminal charges can be filed? Rev. Proc addresses this, by expanding the safe harbor to cover a situation where: A lead figure, or an associated entity involved in the specified fraudulent arrangement, was the subject of one or more civil complaints or similar documents that a state or federal governmental entity filed with a court or in an administrative agency enforcement proceeding, and: (a) The civil complaint or similar documents together allege facts that comprise substantially all of the elements of a specified fraudulent arrangement, conducted by the lead figure; (b) The death of the lead figure precludes a charge by indictment, information, or criminal complaint against that lead figure; and (c) A receiver or trustee was appointed with respect to the arrangement or assets of the arrangement were frozen. Page 6-16: IRS Acquiesces in Mayo Decision In AOD , the IRS announced its acquiescence in the Tax Court s decision in Mayo v. Comm r., ruling that a professional gambler s expenses (as distinguished from wagering losses) are not limited to gambling winnings (thereby allowing a professional gambler to generate a Schedule C loss). Chapter 7: Page 7-14: Final Regs Issued on EITC Due Diligence Requirement for Tax Preparers The proposed regulations discussed on page 7-14 have been finalized. As a result, paid preparers who prepare a 2011 tax return claiming the earned income tax credit will have to submit Form 8867, the Earned Income Credit Checklist, with the return I order to satisfy the new due diligence requirements for the credit. Failure to do so will subject the preparer (and potentially also the preparer s firm) to a $500 penalty.

9 Chapter 9: Page 9-2: Correction Note 4 in the middle of the page should read as follows: Note 4: If the deficiency is attributable to unreported community property income on a joint return, or improper community property deductions, reg. sec (f) provides that community property laws are disregarded in allocating income and deductions between spouses. If married couples in a community property state file separate returns, an innocent spouse can avoid liability of tax on unreported community property income of the guilty spouse under sec. IRC 66(c), which applies the same principles that apply for traditional relief under sec. 6015(b). Chapter 10: Page 10-15: Correction to Case Header The header to this case should read: Reliance on CPA Does Not Excuse Omission of $3.4 Million from Tax Return

1099 LETTER REPEAL OF NEW INFORMATION REPORTING REQUIREMENTS INSIDE THIS ISSUE:

DECEMBER 2011 INSIDE THIS ISSUE: Repeal of New Information Reporting Requirements IRS Voluntary Classification Settlement Program California s New Penalties for Misclassifying Employees as Independent

DECEMBER 2011 INSIDE THIS ISSUE: Repeal of New Information Reporting Requirements IRS Voluntary Classification Settlement Program California s New Penalties for Misclassifying Employees as Independent

Instructions for Form 8949

2012 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted.

2012 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted.

Tax Topics /24/14. Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist

Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist Tax Topics 2014-11 11/24/14 IRS releases 2015 inflation-adjusted numbers Last month, the IRS released its 2015 inflation-adjusted

Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist Tax Topics 2014-11 11/24/14 IRS releases 2015 inflation-adjusted numbers Last month, the IRS released its 2015 inflation-adjusted

Instructions for Form 8949

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2015 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2015 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the

Article 1 Section moves to amend H.F. No as follows: 1.2 Delete everything after the enacting clause and insert: 1.

1.1... moves to amend H.F. No. 4385 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes 2017 Supplement,

1.1... moves to amend H.F. No. 4385 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes 2017 Supplement,

President Obama's 2016 Federal Budget Proposal

President Obama's 2016 Federal Budget Proposal March 10, 2015 by Tim Steffen On the heels of his first State of the Union address to the nation after the mid-term elections, President Obama released his

President Obama's 2016 Federal Budget Proposal March 10, 2015 by Tim Steffen On the heels of his first State of the Union address to the nation after the mid-term elections, President Obama released his

AARP FOUNDATION TAX-AIDE SCOPE MANUAL WHAT S IN WHAT S OUT

AARP Foundation Tax-Aide helps low and moderate income taxpayers, with special attention to those 60 and older. Volunteers are trained to assist in filing Form 1040 and certain other schedules and forms.

AARP Foundation Tax-Aide helps low and moderate income taxpayers, with special attention to those 60 and older. Volunteers are trained to assist in filing Form 1040 and certain other schedules and forms.

COUNSEL ESS/NP/JW/JP/RER/GC SCS3982A-3

1.1 Senator... moves to amend S.F. No. 3982 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes 2017 Supplement,

1.1 Senator... moves to amend S.F. No. 3982 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes 2017 Supplement,

Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 2016 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2016 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2013 NEW DEVELOPMENTS LETTER

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

Advance Draft. as of Member s Share of Income, Deductions, Credits, etc.

TAXABLE YEAR 2011 Member s Share of Income, Deductions, Credits, etc. CALIFORNIA SCHEDULE K-1 (568) For calendar year 2011 or fiscal year beginning month day year, and ending month day year. Member s identifying

TAXABLE YEAR 2011 Member s Share of Income, Deductions, Credits, etc. CALIFORNIA SCHEDULE K-1 (568) For calendar year 2011 or fiscal year beginning month day year, and ending month day year. Member s identifying

President Obama Releases 2014 Federal Budget Proposal

Private Wealth Management Products & Services April 2013 President Obama Releases 2014 Federal Budget Proposal 2014 proposal consistent with prior budgets, but enactment is uncertain After more than two

Private Wealth Management Products & Services April 2013 President Obama Releases 2014 Federal Budget Proposal 2014 proposal consistent with prior budgets, but enactment is uncertain After more than two

Tax Law Snapshot for Individuals 2014 Filing Season

Tax Law Snapshot for Individuals 2014 Filing Season (480) 776-3358 1237 S. Val Vista Dr. Suite 206 Mesa, AZ 85204-6401 (480) 323-2474 fax kboudreau@bcsbs.net Taxes Contract Financial Management Financial

Tax Law Snapshot for Individuals 2014 Filing Season (480) 776-3358 1237 S. Val Vista Dr. Suite 206 Mesa, AZ 85204-6401 (480) 323-2474 fax kboudreau@bcsbs.net Taxes Contract Financial Management Financial

97 Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 97 Department Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Credits, Deductions, etc. (For Shareholder's Use Only) Section references are to the Internal Revenue

97 Department Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Credits, Deductions, etc. (For Shareholder's Use Only) Section references are to the Internal Revenue

Shareholder s Share of Income, Deductions, Credits, etc.

Schedule K-1 (Form 1120S) Department of the Treasury Internal Revenue Service 2010 For calendar year 2010, or tax year beginning, 2010 ending, 20 Shareholder s Share of Income, Deductions, Credits, etc.

Schedule K-1 (Form 1120S) Department of the Treasury Internal Revenue Service 2010 For calendar year 2010, or tax year beginning, 2010 ending, 20 Shareholder s Share of Income, Deductions, Credits, etc.

Bankruptcy Questions Answered!

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

2001 Instructions for Schedule D, Capital Gains and Losses

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

THE NONQUALIFIED DEFERRED COMPENSATION ADVISOR 2007 SUPPLEMENT

THE NONQUALIFIED DEFERRED COMPENSATION ADVISOR 2007 SUPPLEMENT PPA Restricts Trusts for Top Executives The Pension Protection Act added new restrictions to IRC Section 409A to prohibit top executives from

THE NONQUALIFIED DEFERRED COMPENSATION ADVISOR 2007 SUPPLEMENT PPA Restricts Trusts for Top Executives The Pension Protection Act added new restrictions to IRC Section 409A to prohibit top executives from

WSRP, LLC Salt Lake City UT, Lehi UT & Las Vegas NV

Background on WSRP The firm began in 1985 with 6 people. Now the firm has over 100 + professionals and one of the largest CPA firms in Utah. Offices in SLC, Lehi, Las Vegas, and Ogden shortly. We primarily

Background on WSRP The firm began in 1985 with 6 people. Now the firm has over 100 + professionals and one of the largest CPA firms in Utah. Offices in SLC, Lehi, Las Vegas, and Ogden shortly. We primarily

American Taxpayer Relief Act of 2012 Changes Effective in New Law Before Law Change Date Page 1 Alternative Minimum Tax (AMT) Individuals AMT

Individuals AMT") American Taxpayer Relief Act of 202 Changes Effective in 202 Effective QF New Law Before Law Change Date Page Alternative Minimum Tax (AMT) Individuals AMT 2-3 For 202, the AMT exemption amounts are: $50,600

American Taxpayer Relief Act of 202 Changes Effective in 202 Effective QF New Law Before Law Change Date Page Alternative Minimum Tax (AMT) Individuals AMT 2-3 For 202, the AMT exemption amounts are: $50,600

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now Rich Shavell, CPA, CVA, CCIFP Shavell & Company, P.A. info@shavell.net www.shavell.net 1 THE DISCLAIMER Information provided herein

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now Rich Shavell, CPA, CVA, CCIFP Shavell & Company, P.A. info@shavell.net www.shavell.net 1 THE DISCLAIMER Information provided herein

Year-End Tax Planning Letter

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Defined Contribution Listing of Required Modifications and Information Package (LRM)

") Defined Contribution Listing of Required Modifications and Information Package (LRM) To Providers of Pre-approved Plans: This information package contains samples of plan provisions that have been found

Defined Contribution Listing of Required Modifications and Information Package (LRM) To Providers of Pre-approved Plans: This information package contains samples of plan provisions that have been found

2010 Update. The Rebirth of. Roth. A CPA s Ultimate Guide for Client Care. By: Robert S. Keebler, CPA, MST, AEP (Distinguished)

") 2010 Update The Rebirth of Roth A CPA s Ultimate Guide for Client Care By: Robert S. Keebler, CPA, MST, AEP (Distinguished) The Rebirth of Roth The Small Business Jobs Act of 2010 (SBJA) (P.L. 111-240)

2010 Update The Rebirth of Roth A CPA s Ultimate Guide for Client Care By: Robert S. Keebler, CPA, MST, AEP (Distinguished) The Rebirth of Roth The Small Business Jobs Act of 2010 (SBJA) (P.L. 111-240)

97 Partner's Instructions for Schedule K-1 (Form 1065)

") 97 Department Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Credits, Deductions, etc. (For Partner's Use Only) Section references are to the Internal Revenue Code unless

97 Department Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Credits, Deductions, etc. (For Partner's Use Only) Section references are to the Internal Revenue Code unless

PROSHARES SAMPLE TAX PACKAGE 7501 WISCONSIN AVE SUITE 1000 BETHESDA, MD PROSHARES. K-1 Account Number:

PROSHARES 750 WISCONSIN AVE SUITE 000 BETHESDA, MD 2084 PROSHARES K- Account Number: 207 SCHEDULE K- SUPPLEMENTAL INFORMATION % of the amount of interest income included on your Schedule K- is from US

PROSHARES 750 WISCONSIN AVE SUITE 000 BETHESDA, MD 2084 PROSHARES K- Account Number: 207 SCHEDULE K- SUPPLEMENTAL INFORMATION % of the amount of interest income included on your Schedule K- is from US

The Administration's Tax Reform Targets -- Selected Issues

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2015 The Administration's Tax Reform Targets

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2015 The Administration's Tax Reform Targets

(married filing jointly) indexed for inflation in future years.

indexed for inflation in future years.") 2 AMERICAN TAXPAYER RELIEF ACT OF 2012 excess of the applicable threshold. These thresholds will be indexed for inflation in future years. Because the tax rates are permanent, for 2013 you can employ the

2 AMERICAN TAXPAYER RELIEF ACT OF 2012 excess of the applicable threshold. These thresholds will be indexed for inflation in future years. Because the tax rates are permanent, for 2013 you can employ the

Federal Tax Update 63rd Annual Institute on Taxation Tuesday, November 15, :30am - 9:45am

Federal Tax Update 63rd Annual Institute on Taxation Tuesday, November 15, 2016 8:30am - 9:45am By: Peter X. Bellanti, CPA Amato, Fox & Company PC 36 Niagara Street Tonawanda, NY 14150 (716) 694-0336 Email

Federal Tax Update 63rd Annual Institute on Taxation Tuesday, November 15, 2016 8:30am - 9:45am By: Peter X. Bellanti, CPA Amato, Fox & Company PC 36 Niagara Street Tonawanda, NY 14150 (716) 694-0336 Email

REVISOR EAP/IL A

1.1... moves to amend H.F. No. 4385, the third engrossment, as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes

1.1... moves to amend H.F. No. 4385, the third engrossment, as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes

2002 Instructions for Schedule D, Capital Gains and Losses

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

State of Rhode Island and Providence Plantations 2017 Form RI-1040NR Nonresident Individual Income Tax Return

State of Rhode Island and Providence Plantations 2017 Form RI-1040NR Nonresident Individual Income Tax Return 17100499990101 Your social security number Spouse s social security number Your first name

State of Rhode Island and Providence Plantations 2017 Form RI-1040NR Nonresident Individual Income Tax Return 17100499990101 Your social security number Spouse s social security number Your first name

Current topics and trends in real estate tax MARK LEE LEVINE

Current topics and trends in real estate tax BY MARK LEE LEVINE Current Topics and Trends in Real Estate Tax Objectives: 1. Provide an Update on Tax Issues Impacting Commercial Real Estate and Personal

Current topics and trends in real estate tax BY MARK LEE LEVINE Current Topics and Trends in Real Estate Tax Objectives: 1. Provide an Update on Tax Issues Impacting Commercial Real Estate and Personal

Welcome to Tax Update Your hosts: For Businesses & Estates Gary McBride and Annette Nellen Federal and California Tax Update for Businesses & Estates Dec 2015/Jan2016 http://mntaxclass.com Slides Supplements

Welcome to Tax Update Your hosts: For Businesses & Estates Gary McBride and Annette Nellen Federal and California Tax Update for Businesses & Estates Dec 2015/Jan2016 http://mntaxclass.com Slides Supplements

Your Comprehensive Guide to 2013 Year-End Tax Planning

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Internal Revenue Service. Enrolled Agent Exam Part ONE. Exam Year May 1, 2017 February 28, Table of Contents

Internal Revenue Service Enrolled Agent Exam Part ONE Exam Year May 1, 2017 February 28, 2018 Table of Contents Lesson 1. Taxpayer Identification and Data Gathering Expansion of the Tax Code Internal Taxes

Internal Revenue Service Enrolled Agent Exam Part ONE Exam Year May 1, 2017 February 28, 2018 Table of Contents Lesson 1. Taxpayer Identification and Data Gathering Expansion of the Tax Code Internal Taxes

FTB Publication California Tax Forms and Related Federal Forms

FTB Publication 1006 2017 California Tax Forms and Related Federal Forms THIS PAGE INTENTIONALLY LEFT BLANK Visit our website: ftb.ca.gov Page 2 FTB Pub. 1006 2017 FRANCHISE TAX BOARD (FTB) FORMS CALIFORNIA

FTB Publication 1006 2017 California Tax Forms and Related Federal Forms THIS PAGE INTENTIONALLY LEFT BLANK Visit our website: ftb.ca.gov Page 2 FTB Pub. 1006 2017 FRANCHISE TAX BOARD (FTB) FORMS CALIFORNIA

2017 Tax Considerations

2017 Tax Considerations Tax Laws Enacted During 2017 Individual Income Tax Provisions Education Trust, Estate & Descendent Income Tax Estate, Gift & Generation-Skipping Transfer Taxes Pension & IRA Provisions

2017 Tax Considerations Tax Laws Enacted During 2017 Individual Income Tax Provisions Education Trust, Estate & Descendent Income Tax Estate, Gift & Generation-Skipping Transfer Taxes Pension & IRA Provisions

Bollenbacher and Associates Certified Public Accountants Taxpayer Relief Act

Bollenbacher and Associates Certified Public Accountants 2012 Taxpayer Relief Act Highlights of the 2012 Taxpayer Relief Act (1) the elimination of EGTRRA sunsetting (Bush Tax Cuts), (2) tax rate increases

Bollenbacher and Associates Certified Public Accountants 2012 Taxpayer Relief Act Highlights of the 2012 Taxpayer Relief Act (1) the elimination of EGTRRA sunsetting (Bush Tax Cuts), (2) tax rate increases

Carol's Tax Return-2016 Tax Year. Part 2. Compute income tax

Turner School of Accountancy Chapter 1 and Chapter 2 Materials Page 1 Part 1. Complete Columns F,G,H. Part 2. Compute amount of tax due or refund Complete Form 1040, page 1 & 2, and Form 1040 Schedules

Turner School of Accountancy Chapter 1 and Chapter 2 Materials Page 1 Part 1. Complete Columns F,G,H. Part 2. Compute amount of tax due or refund Complete Form 1040, page 1 & 2, and Form 1040 Schedules

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2016 www.cordascocpa.com INTRODUCTION 2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS It s that time of year again.

2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2016 www.cordascocpa.com INTRODUCTION 2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS It s that time of year again.

AN EXAMINATION OF FEDERAL TAX RULES IMPACTING MARRIED SAME-SEX COUPLES FROM THE U.S. SUPREME COURT RULING IN U.S. v WINDSOR

AN EXAMINATION OF FEDERAL TAX RULES IMPACTING MARRIED SAME-SEX COUPLES FROM THE U.S. SUPREME COURT RULING IN U.S. v WINDSOR Ahroni, Scott Queens College of the City University of New York Silliman, Benjamin

AN EXAMINATION OF FEDERAL TAX RULES IMPACTING MARRIED SAME-SEX COUPLES FROM THE U.S. SUPREME COURT RULING IN U.S. v WINDSOR Ahroni, Scott Queens College of the City University of New York Silliman, Benjamin

Tax Cuts and Jobs Act of 2017 (TCJA) Key Individual Tax Provisions

Key Individual Tax Provisions") Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

TABLE OF CONTENTS. General Rules

T41 1/18 10-1 10 Interest and Taxes TABLE OF CONTENTS KEY ISSUE DESCRIPTION PAGE Introduction... 10-1 10A Investment Interest Expense... 10-2 General Rules... 10-2 Reporting Deductible Investment Interest...

T41 1/18 10-1 10 Interest and Taxes TABLE OF CONTENTS KEY ISSUE DESCRIPTION PAGE Introduction... 10-1 10A Investment Interest Expense... 10-2 General Rules... 10-2 Reporting Deductible Investment Interest...

Midyear Tax Planning Letter

Midyear Tax Planning Letter 2015 Introduction Tax planning for 2015 is a venture in uncertainty. Last December, Congress passed legislation extending a number of expired tax provisions. Unfortunately,

Midyear Tax Planning Letter 2015 Introduction Tax planning for 2015 is a venture in uncertainty. Last December, Congress passed legislation extending a number of expired tax provisions. Unfortunately,

Chapter 5: Personal Tax Credits. 05: Personal Tax Credits

Page 55-68 Chapter 5: Personal Tax Credits 1 Learning Objectives Page 55-68 Upon completion of this seminar, participants should be able to Identify personal tax credits for which our clients may qualify

Page 55-68 Chapter 5: Personal Tax Credits 1 Learning Objectives Page 55-68 Upon completion of this seminar, participants should be able to Identify personal tax credits for which our clients may qualify

Capital Asset Taxation Introduction

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Product Profile ToolBox CS CS Professional Suite. Quick Access to Key Utilities. Meet Client Needs with a Wealth of Tools. Financial Calculators

Product Profile ToolBox CS CS Professional Suite Quick Access to Key Utilities ToolBox CS puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout the

Product Profile ToolBox CS CS Professional Suite Quick Access to Key Utilities ToolBox CS puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout the

2017 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR)

") 2017 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2017 Rhode Island Nonresident

2017 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2017 Rhode Island Nonresident

2018 TAX AND FINANCIAL PLANNING TABLES

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

Rental Real Estate Deductions

Rental Real Estate Deductions 15 th Edition Stephen Fishman, J.D. Chapter 1 Tax Deduction Basics for Landlords... 1 Learning Objectives... 1 Introduction... 1 How Landlords Are Taxed... 1 Income Taxes

Rental Real Estate Deductions 15 th Edition Stephen Fishman, J.D. Chapter 1 Tax Deduction Basics for Landlords... 1 Learning Objectives... 1 Introduction... 1 How Landlords Are Taxed... 1 Income Taxes

Quick Facts. Comprehensive Calculations. Prior Year Comparisons Software Updates Delivered Online Alerts Ability to Returns to Support

Quick Facts Access State Data Entry from Federal Data Entry Federal Information Flows to State Returns Auto-fill Available for Amended Returns Group Sales of Depreciable Assets Many Credit Forms Available

Quick Facts Access State Data Entry from Federal Data Entry Federal Information Flows to State Returns Auto-fill Available for Amended Returns Group Sales of Depreciable Assets Many Credit Forms Available

Expiring Tax Provisions

Expiring Tax Provisions The term Bush-era tax cuts or Bush tax cuts is often used to describe the tax related reductions that were contained in legislation enacted by Congress in 2001 and 2003, the Economic

Expiring Tax Provisions The term Bush-era tax cuts or Bush tax cuts is often used to describe the tax related reductions that were contained in legislation enacted by Congress in 2001 and 2003, the Economic

OUT OF SCOPE - VITA 2017 TAX YEAR The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only.

The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only. Legislative Extenders Residential energy-efficient property credit (Form 5695, Part I)

The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only. Legislative Extenders Residential energy-efficient property credit (Form 5695, Part I)

Tax Cuts and Jobs Act of 2017

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

2017 Annual Federal Tax Refresher

2017 Annual Federal Tax Refresher i Copyright 2016 by Paul J. Winn CLU ChFC ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE

2017 Annual Federal Tax Refresher i Copyright 2016 by Paul J. Winn CLU ChFC ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE

Capital Gain or Loss. Introduction. Capital Asset Taxation. Introduction. Capital Asset Taxation. What is a Capital Asset

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

IRS RETURN PREPARER TEST SPECIFICATIONS

IRS RETURN PREPARER TEST SPECIFICATIONS GLEIM Comment: Please do not spend time reading, studying, etc. these specifications. We have analyzed them line by line to assure a complete and all-inclusive study

IRS RETURN PREPARER TEST SPECIFICATIONS GLEIM Comment: Please do not spend time reading, studying, etc. these specifications. We have analyzed them line by line to assure a complete and all-inclusive study

Eligible individuals. All individual taxpayers are eligible for the credit, except for: a nonresident alien,

Taxpayers May Request Waiver of Underpayment of Estimated Tax Penalty from MWPC The IRS recently announced that taxpayers may request waiver of the penalty for underpayment of estimated tax resulting from

Taxpayers May Request Waiver of Underpayment of Estimated Tax Penalty from MWPC The IRS recently announced that taxpayers may request waiver of the penalty for underpayment of estimated tax resulting from

Individual Taxation and Planning

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

NAVIGATING THE 2012 TO 2013 TAX LANDSCAPE

NAVIGATING THE 2012 TO 2013 TAX LANDSCAPE An Advisory Services Publication If man will begin with certainties, he shall end in doubts; but if he will be content to begin with doubts, he will end in certainties.

NAVIGATING THE 2012 TO 2013 TAX LANDSCAPE An Advisory Services Publication If man will begin with certainties, he shall end in doubts; but if he will be content to begin with doubts, he will end in certainties.

Instructions for Form 4797

2017 Instructions for Form 4797 Sales of Business Property (Also Involuntary Conversions and Recapture Amounts Under Sections 179 and 280F(b)(2)) Department of the Treasury Internal Revenue Service Section

2017 Instructions for Form 4797 Sales of Business Property (Also Involuntary Conversions and Recapture Amounts Under Sections 179 and 280F(b)(2)) Department of the Treasury Internal Revenue Service Section

e-pocket TAX TABLES 2014 and 2015 Quick Links:

e-pocket TAX TABLES 2014 and 2015 Quick Links: 2014 Income and Payroll Tax Rates 2015 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

e-pocket TAX TABLES 2014 and 2015 Quick Links: 2014 Income and Payroll Tax Rates 2015 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

Article 1 Section moves to amend H.F. No as follows: 1.2 Delete everything after the enacting clause and insert: 1.

1.1... moves to amend H.F. No. 2125 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL CONFORMITY 1.5 Section 1. Minnesota Statutes 2018, section 270A.03,

1.1... moves to amend H.F. No. 2125 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL CONFORMITY 1.5 Section 1. Minnesota Statutes 2018, section 270A.03,

PUBLIC DISCLOSURE COPY

Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) For calendar year 2014 or other tax year beginning, 2014, and ending, 20. Department of

Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) For calendar year 2014 or other tax year beginning, 2014, and ending, 20. Department of

business owner issues and depreciation deductions

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

2016 Year-End Tax-Planning Letter

Dear Clients and Friends: With a new administration taking shape in our nation s capital after the elections, you can expect that significant tax reforms will be debated, and perhaps enacted, in the near

Dear Clients and Friends: With a new administration taking shape in our nation s capital after the elections, you can expect that significant tax reforms will be debated, and perhaps enacted, in the near

*Brackets adjusted for inflation in future years Long Term Capital Gains & Dividends Taxable income up to $413,200/$457,600 0% - 15%*

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s 1040 Deskbook. Thirtieth Edition (October 2017)

") Route To: j Partners j Managers j Staff j File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1040 Deskbook Thirtieth Edition (October 2017) Highlights of this Edition The following are some of the important

Route To: j Partners j Managers j Staff j File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1040 Deskbook Thirtieth Edition (October 2017) Highlights of this Edition The following are some of the important

Year-end Tax Planning Letter

Year-end Tax Planning Letter 2015 Introduction At this point in 2015, with the end of the year and the income tax filing deadline on the horizon, tax planning presents more of a challenge than usual. So

Year-end Tax Planning Letter 2015 Introduction At this point in 2015, with the end of the year and the income tax filing deadline on the horizon, tax planning presents more of a challenge than usual. So

COPYRIGHTED MATERIAL. Filing Status. Chapter 1

Chapter 1 Filing Status The filing status you use when you file your return determines the tax rates that will apply to your taxable income; see 1.2. Filing status also determines the standard deduction

Chapter 1 Filing Status The filing status you use when you file your return determines the tax rates that will apply to your taxable income; see 1.2. Filing status also determines the standard deduction

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

1998 Instructions for Schedule D, Capital Gains and Losses

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

Individual Items to Note (1040)

") Items to Note Individual Items to Note (1040) This list provides details about how ProSeries converts the following 1040 calculated carryovers. Number of Assets - The conversion program converts a maximum

Items to Note Individual Items to Note (1040) This list provides details about how ProSeries converts the following 1040 calculated carryovers. Number of Assets - The conversion program converts a maximum

SHORT VERSION S CORPORATION INCOME TAX RETURN CHECKLIST 2008 FORM 1120S

Client Name and Number: Prepared by: Date: Reviewed by: Date: 100) GENERAL INFORMATION 101) Consider obtaining signed:.1) Engagement letter..2) Engagement letter for tax advice under the CPA-client privilege

Client Name and Number: Prepared by: Date: Reviewed by: Date: 100) GENERAL INFORMATION 101) Consider obtaining signed:.1) Engagement letter..2) Engagement letter for tax advice under the CPA-client privilege

Earned Income Credit i

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Weighted average. Owned 0 on January 1, bought 50% from James on May Norma Shipper Owned all year 100

Case Study Corntax Inc Using 2017 Forms adapted for 2017 tax laws.., had three shareholders in 2018 Weighted average James Robertson Owned 50% on January 1, sold to John on May 26 40 John Bouchet Owned

Case Study Corntax Inc Using 2017 Forms adapted for 2017 tax laws.., had three shareholders in 2018 Weighted average James Robertson Owned 50% on January 1, sold to John on May 26 40 John Bouchet Owned

Individual Items to Note (1040)

") Items to Note Individual Items to Note (1040) During the conversion process, the following Form 1040 carryover information will NOT be converted to your 2016 ProSeries data files. To ensure your calculated

Items to Note Individual Items to Note (1040) During the conversion process, the following Form 1040 carryover information will NOT be converted to your 2016 ProSeries data files. To ensure your calculated

2010 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS

2010 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION As we approach the close of 2010, there is still time to take steps that can reduce your 2010 tax bill. Year-end tax planning is more complicated

2010 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION As we approach the close of 2010, there is still time to take steps that can reduce your 2010 tax bill. Year-end tax planning is more complicated

2011 INSTRUCTIONS FOR FILING RI-1040NR

2011 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2011 Rhode Island Nonresident

2011 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2011 Rhode Island Nonresident

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS Following are income tax items that could affect your return for 2014. Please review and make sure you have alerted your tax consultant for all of

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS Following are income tax items that could affect your return for 2014. Please review and make sure you have alerted your tax consultant for all of

THE AGENDA YEAR END TAX PLANNING

YEAR END TAX PLANNING TUESDAY, DECEMBER 8, 2015 PRESENTED BY: JOE CAWLEY, CPA, PRINCIPAL-JOECAWLEY@BSSF.COM JOHN WEIDMAN, CPA, PRINCIPAL-JOHNWEIDMAN@BSSF.COM PHONE NUMBER-(717)761-7171 1 THE AGENDA Part

YEAR END TAX PLANNING TUESDAY, DECEMBER 8, 2015 PRESENTED BY: JOE CAWLEY, CPA, PRINCIPAL-JOECAWLEY@BSSF.COM JOHN WEIDMAN, CPA, PRINCIPAL-JOHNWEIDMAN@BSSF.COM PHONE NUMBER-(717)761-7171 1 THE AGENDA Part

Why Keep Records? Kinds of Records To Keep

Why Keep Records? There are many reasons to keep records. In addition to tax purposes, you may need to keep records for insurance purposes or for getting a loan. Good records will help you: Identify sources

Why Keep Records? There are many reasons to keep records. In addition to tax purposes, you may need to keep records for insurance purposes or for getting a loan. Good records will help you: Identify sources

2010 Internal Revenue Service

Sign Here Paid Preparer Use Only U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is OMB No. 545-3 Form 2S attaching Form 2553 to elect to be an S corporation.

Sign Here Paid Preparer Use Only U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is OMB No. 545-3 Form 2S attaching Form 2553 to elect to be an S corporation.

G. Modify Rules Governing Tax-Exempt Bonds for Section 501(c)(3) Organizations as Applied to Organizations Engaged in Timber Conservation Activities

(3) Organizations as Applied to Organizations Engaged in Timber Conservation Activities") CONTENTS I. MARGINAL TAX RATE REDUCTION... 1 A. Individual Income Tax Rate Structure (secs. 2 and 3 of the House bill, sec. 101 of the Senate amendment and sec. 1 of the Code)... 1 B. Increase Starting

CONTENTS I. MARGINAL TAX RATE REDUCTION... 1 A. Individual Income Tax Rate Structure (secs. 2 and 3 of the House bill, sec. 101 of the Senate amendment and sec. 1 of the Code)... 1 B. Increase Starting

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

October 16, 2003 CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing Required or Repeal of multiple-use test

October 16, 2003 CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing Required or Repeal of multiple-use test

2018 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR)

") 2018 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) The RI-1040NR Nonresident booklet contains returns and instructions for filing the 2018

2018 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) The RI-1040NR Nonresident booklet contains returns and instructions for filing the 2018

Public Law H.R Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221

9/5/2008 Housing Assistance Tax Act of 2008 Public Law 110-289 H.R. 3221 Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221 H.R. 3221, the Housing and Economic Recovery Act of

9/5/2008 Housing Assistance Tax Act of 2008 Public Law 110-289 H.R. 3221 Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221 H.R. 3221, the Housing and Economic Recovery Act of

2017 Year-End Income Tax Planning for Individuals December 2017

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

Year-End Tax Planning Letter

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

TOOLBOX CS PRODUCT PROFILE QUICK ACCESS TO KEY UTILITIES MEET CLIENT NEEDS WITH A WEALTH OF TOOLS FINANCIAL CALCULATORS CS PROFESSIONAL SUITE

PRODUCT PROFILE TOOLBOX CS CS PROFESSIONAL SUITE QUICK ACCESS TO KEY UTILITIES ToolBox CS, puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout

PRODUCT PROFILE TOOLBOX CS CS PROFESSIONAL SUITE QUICK ACCESS TO KEY UTILITIES ToolBox CS, puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout

Exempt Organization Business Income Tax Return

990-T Exempt Organization Business Income Tax Return Form OMB No. 1545-0687 (and proxy tax under section 6033(e)) For calendar year 2016 or other tax year beginning JUL 1, 2016, and ending JUN 30, 2017.

990-T Exempt Organization Business Income Tax Return Form OMB No. 1545-0687 (and proxy tax under section 6033(e)) For calendar year 2016 or other tax year beginning JUL 1, 2016, and ending JUN 30, 2017.

Recent Developments in the Estate and Gift Tax Area. Annual Business Plan and the Proposed Regulations under Section 2642

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

TAX UPDATE TAX CUTS & JOBS ACT (2018) Add l Elderly & Blind Joint & Surviving Spouse: $1,300

Add l Elderly & Blind Joint & Surviving Spouse: $1,300") TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

Congress Passes Fiscal Cliff Act

Congress Passes Fiscal Cliff Act Pulling back from the fiscal cliff at the 13th hour, Congress preserved most of the George W. Bush-era tax cuts and extended many other lapsed tax provisions. The Senate

Congress Passes Fiscal Cliff Act Pulling back from the fiscal cliff at the 13th hour, Congress preserved most of the George W. Bush-era tax cuts and extended many other lapsed tax provisions. The Senate

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE November 20, 2015 Presented by Wallingford Law, PSC J. Whitney Wallingford, Esq. e-mail: whitney@wallingfordlaw.com Brian A. Ritchie, Esq. e-mail: brian@wallingfordlaw.com

BEST PRACTICES FOR EMPLOYEE BENEFIT PLAN COMPLIANCE November 20, 2015 Presented by Wallingford Law, PSC J. Whitney Wallingford, Esq. e-mail: whitney@wallingfordlaw.com Brian A. Ritchie, Esq. e-mail: brian@wallingfordlaw.com