(married filing jointly) indexed for inflation in future years.

|

|

|

- Damian Fox

- 5 years ago

- Views:

Transcription

1

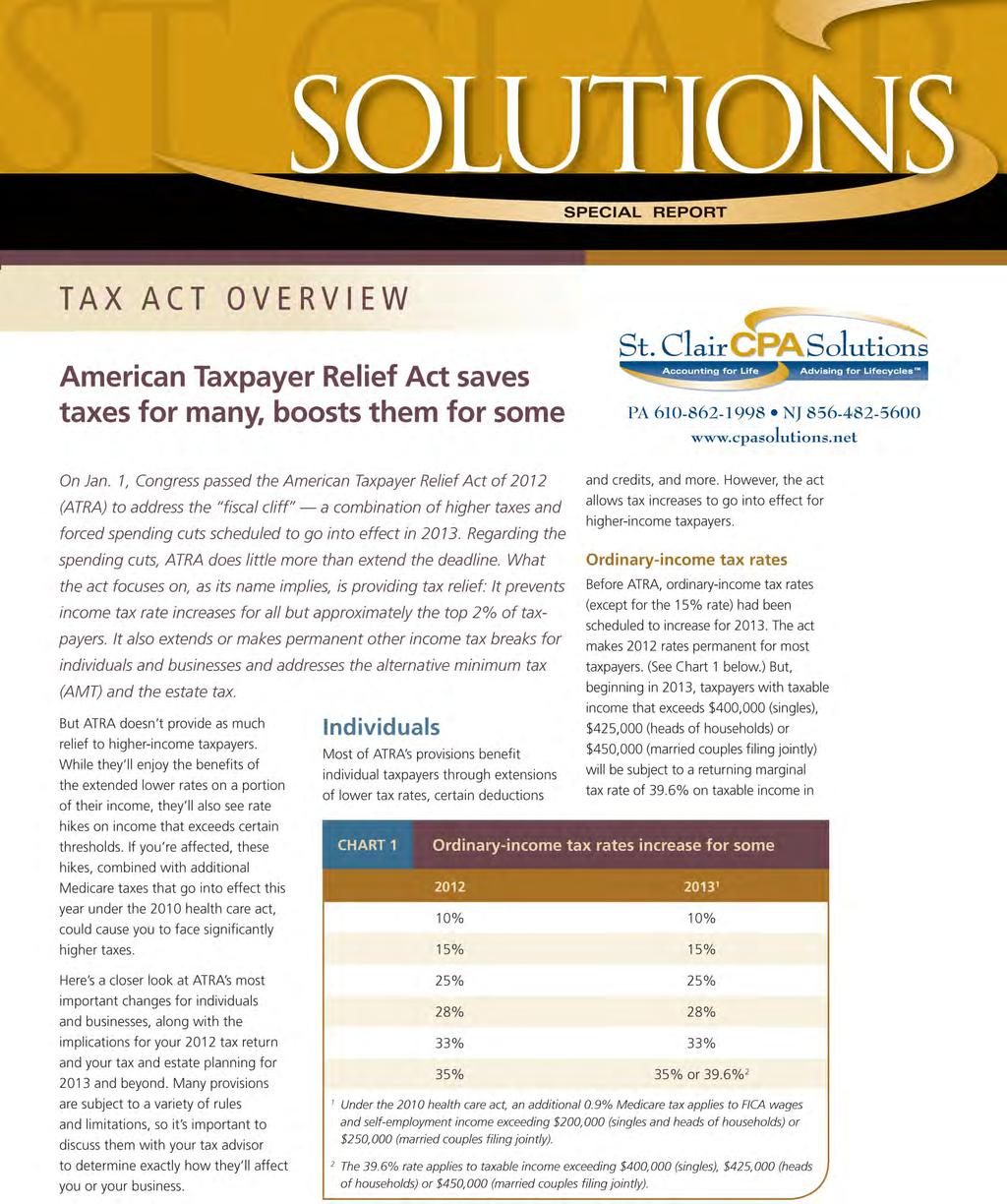

2 2 AMERICAN TAXPAYER RELIEF ACT OF 2012 excess of the applicable threshold. These thresholds will be indexed for inflation in future years. Because the tax rates are permanent, for 2013 you can employ the traditional timing strategies of accelerating deductible expenses into the current year and deferring income to the next year, where possible, to defer tax (assuming you don t expect to be in a higher tax bracket in 2014). If you re facing the 39.6% rate, however, you may want to see if there are additional strategies you can employ to help minimize the impact of the higher rate. Capital gains tax rates The 15% long-term capital gains rate had been scheduled to increase to 20% in ATRA makes the 15% rate permanent. However, it brings back the 20% rate for higherincome taxpayers. As with the 39.6% ordinary-income tax rate, the 20% rate kicks in when taxable income exceeds $400,000 (singles), $425,000 (heads of households) or $450,000 (married filing jointly) indexed for inflation in future years. ATRA also makes permanent the 0% long-term gains rate for taxpayers in the bottom two brackets. If you have children or other loved ones in these brackets, consider transferring appreciated assets to them. They can sell the assets and pay no tax on the capital gain. You may find this strategy particularly powerful if you d pay tax at the 20% rate if you sold the assets. But before gifting any assets, if the recipients are under age 24, make sure they won t be subject to the kiddie tax. And regardless of their age, consider the gift tax consequences. Finally, be aware that different income tax rates apply to capital gains in some situations. (See Chart 2.) And if you re subject to the 39.6% ordinary-income tax rate, you ll pay more tax on shortterm gains. Qualified dividend tax rates ATRA makes permanent the long-term capital gains treatment of qualified dividends. So most taxpayers will continue to enjoy a 15% rate (0% for those in the bottom two brackets). But taxpayers with taxable incomes exceeding the applicable income thresholds will face a rate increase from 15% to 20% on qualified dividends. Nevertheless, without ATRA, they would have paid a much higher rate, because dividends would have gone back to being taxed at ordinary-income rates in 2013, with a top rate of 39.6%. Chart 2 Assets held months or less (short term) 35% 39.6% 2 More than 12 months (long term) 15% 20% 2 Some key exceptions What s the maximum income tax rate on capital gains? Long-term gain on collectibles, such as artwork and antiques Long-term gain attributable to certain recapture of prior depreciation on real property Gain on qualified small business stock held more than 5 years Long-term gain that would be taxed at 15% or less based on the taxpayer s ordinary-income rate 28% 28% 25% 25% 14% 3 14% 3 0% 0% 1 Under the 2010 health care act, a new 3.8% Medicare tax applies to net investment income to the extent that modified adjusted gross income (MAGI) exceeds $200,000 (singles and heads of households) or $250,000 (married couples filing jointly). 2 Rate increase over 2012 applies only to those with taxable income exceeding $400,000 (singles), $425,000 (heads of households) or $450,000 (married couples filing jointly). 3 Effective rate based on 50% exclusion from a 28% rate. If you hold dividend-producing investments and will face the 20% rate, consider whether you should make adjustments to your portfolio in light of their potentially higher tax cost. Keep in mind, however, that the tax treatment of qualified dividends, even if taxed at 20%, will remain more attractive than the treatment of many other income investments. For example, interest from CDs, money market accounts and taxable bonds will continue to be taxed at ordinary-income rates. Exclusion on small business stock gains To make investing in certain small businesses more attractive, previous legislation increased the qualified small business (QSB) stock gain exclusion to 100% for stock acquired after Sept. 27, 2010, and before Jan. 1, 2012, that s held for at least five years. ATRA extends the acquisition deadline for 100% gain exclusion to Dec. 31, 2013.

3 AMERICAN TAXPAYER RELIEF ACT OF QSB stock can help diversify your portfolio while providing additional potential tax benefits. So purchasing it by the end of 2013 may be worth considering. (To be a QSB, the company can t hold gross assets exceeding $50 million at the time the stock is issued and must be engaged in an active trade or business.) AMT The AMT is a separate tax system that limits some deductions and credits, doesn t permit others and treats certain income items differently. If your AMT liability is greater than your regular tax liability, you must pay the AMT. Before ATRA, unlike the regular tax system, the AMT system wasn t regularly adjusted for inflation. Instead, Congress had to legislate any adjustments. Typically, it did so in the form of a patch an increase in the AMT exemption. And the last patch had expired Dec. 31, So millions more taxpayers could have been subject to the AMT for ATRA makes the patch permanent by increasing the exemptions for 2012 and indexing them for inflation for future years. (See Chart 3 at right.) The act also makes permanent the ability to offset your AMT liability with certain nonrefundable personal credits (such as the dependent care credit and certain energy-related credits) you re otherwise eligible for. Chart 3 Exemption patch provides permanent AMT relief You may be able to time income and deductions to avoid the AMT or reduce its impact. Now that AMT relief is permanent, much of the uncertainty involved in AMT planning has been eliminated, making such planning a little easier. Nevertheless, it is still far from simple. Talk to your tax advisor to determine the best strategy for your situation. Deduction for state and local sales taxes For the last several years, taxpayers have been allowed to take an itemized deduction for state and local sales taxes in lieu of state and local income taxes. This break can be valuable to those residing in states with no or low income tax rates or who purchase major items, such as a car or boat. But this break expired Dec. 31, AMT exemption Single or head of household Married filing jointly Without patch $33,750 $45, patch $50,600 $78, patch $51,900 $80,800 Note: Consult your tax advisor for AMT exemptions for children subject to the kiddie tax. Now ATRA extends it for 2012 and If you re contemplating a major purchase, you may want to make it in 2013 to ensure the sales tax deduction is available. Breaks related to children and education Many child- and education-related breaks that had expired (generally Dec. 31, 2012) have been made permanent by ATRA, while others have been temporarily extended: n The $1,000 child credit and other enhancements of the credit have been made permanent. n The higher adoption credit and income exclusion for employerprovided adoption assistance have been made permanent. n The higher dependent care credit has been made permanent.

4 4 AMERICAN TAXPAYER RELIEF ACT OF 2012 Expanded Medicare taxes will hit more taxpayers than ATRA s income tax hikes Under the 2010 health care act, an additional 0.9% Medicare tax on earned income and a new 3.8% Medicare tax on net investment income go into effect in The employee portion of Medicare taxes is normally 1.45%, and, previously, investment income wasn t subject to Medicare tax. The expanded Medicare taxes apply when income exceeds certain levels. Taxpayers hit with higher income tax rates under ATRA will generally also face expanded Medicare taxes. Factoring together both income and Medicare taxes, these taxpayers could see a 5.5 percentage point tax increase on a portion of their earned income and an 8.8 percentage point tax increase on some or all of their long-term capital gains and qualified dividend income (8.4 percentage points on short-term gains, nonqualified dividends and taxable interest). But some taxpayers who escape an income tax hike will still face a Medicare tax increase. This is because the thresholds for expanded Medicare taxes are much lower than those for the 39.6% ordinary-income tax rate and the 20% longterm capital gains rate. (See Ordinary-income tax rates and Capital gains tax rates on pages 1 and 2.) The additional 0.9% Medicare tax applies to FICA wages and self-employment income exceeding $200,000 (singles and heads of households) or $250,000 (married couples filing jointly). The new 3.8% Medicare tax applies to net investment income to the extent that modified adjusted gross income (MAGI) exceeds $200,000 (singles and heads of households) or $250,000 (married couples filing jointly). ATRA did nothing to change these thresholds. Taxpayers who could be affected by the expanded Medicare taxes need to keep them in mind along with the relevant tax law changes under ATRA in their tax planning. n The American Opportunity education credit has been extended through n The above-the-line tuition and fees deduction (expired Dec. 31, 2011) has been extended through n The enhancements to the student loan interest deduction have been made permanent. n The income exclusion for employerprovided education assistance has been made permanent. n The $2,000 Coverdell Education Savings Account (ESA) annual contribution limit, the ability to use tax-free ESA distributions for elementary and secondary school expenses, and other ESA enhancements have been made permanent. Be aware that the benefit of many of these breaks is phased out if a taxpayer s income exceeds certain limits. Your tax advisor can help you determine which breaks you or your children may qualify for. Charitable giving breaks ATRA extends some valuable charitable giving breaks through The breaks had expired Dec. 31, 2011, and the extensions are retroactive to Jan. 1, 2012: 1. Tax-free IRA distributions for charitable purposes. If you re age 70½ or older, you can make a direct contribution from your IRA to a qualified charitable organization without owing any income tax on the distribution. The contribution can be used to satisfy a required minimum distribution. The maximum allowable distribution for charitable contribution purposes is $100,000 per tax year. 2. Contributions of capital gains real property for conservation purposes. You can make such a contribution and take a larger deduction than is allowed for most other capital gains property contributions. Specifically, your deduction for a contribution of capital gains real property for conservation purposes generally

5 AMERICAN TAXPAYER RELIEF ACT OF If you made asset purchases that might qualify for 50% bonus depreciation on your 2012 tax return, be sure to discuss them with your tax advisor. And if you re anticipating major asset purchases in the next year or two, you may want to time them so you can benefit from 50% bonus depreciation. But also consider whether you qualify for Section 179 expensing, which may provide a greater tax benefit. Sec. 179 expensing can be up to 50% of your adjusted gross income (AGI) rather than the 30% of AGI limit that normally applies to contributions of capital gains property. Businesses Because their income flows through to the owners tax returns, entities such as partnerships, limited liability companies (LLCs) and S corporations will in a sense be affected by ATRA s changes to ordinary-income tax rates for individuals. So, if you re the owner of such an entity and will face the 39.6% rate, traditional income and deduction timing strategies may help you minimize the impact, or at least defer taxes. You also may want to consider converting your business to a C corporation, because the top corporate rate remains at 35%. But there are many other tax and nontax consequences of a conversion, so it s important to discuss the impact with your tax advisor as well as your attorney before implementing such a change. On the plus side, ATRA extends and enhances many breaks for businesses. In particular, it provides incentives for businesses to invest in assets, research and people. Section 179 is another tax law provision that encourages investment. It allows smaller businesses to immediately write off the full price of qualifying asset purchases rather than depreciating them over several years. The deduction is reduced by $1 for every $1 of expenses in excess of a phaseout threshold, which is why the break Bonus depreciation primarily benefits smaller businesses. The expensing election can be claimed only ATRA extends 50% bonus depreciation to offset net income, not to reduce net an additional first-year depreciation income below zero. allowance generally through (See Chart 4 for an overview of bonus depreciation s rise and fall.) Before ATRA, the Sec. 179 expensing limit for 2012 was $125,000, with a phaseout threshold of $500,000 and Qualified assets include new tangible these amounts were scheduled to drop to property with a recovery period of 20 $25,000 and $200,000, respectively, for years or less (such as office furniture and The act increases these amounts equipment), off-the-shelf computer software, water utility property and qualified for assets placed in service in both years to $500,000 and $2 million, respectively leasehold improvement property. (the same amounts that applied in 2010 ATRA also extends the provision allowing and 2011). corporations to accelerate certain credits If you re eligible for full Sec. 179 expensing, it may provide a greater benefit in lieu of claiming bonus depreciation for qualified assets placed in service through than bonus depreciation because it can Dec. 31, 2013 (Dec. 31, 2014, for certain allow you to deduct 100% of an asset long-lived and transportation property). Chart 4 Bonus depreciation s rise and fall Qualified assets placed in service Bonus depreciation Jan. 1, 2010, through Sept. 8, % Sept. 9, 2010, through Dec. 31, % Jan. 1, 2012, through Dec. 31, % After Dec. 31, 2013 none Note: Later deadlines apply to certain long-lived and transportation property.

6 6 AMERICAN TAXPAYER RELIEF ACT OF 2012 Many energy-related breaks have been extended ATRA extends certain energy-related incentives. While most are typically applicable to either home builders or manufacturers of energy-efficient appliances, there are some that are more generally applicable. Nonbusiness energy credits that had expired at the end of 2011 have been retroactively extended through The credit can be taken for 10% of the cost of 1) qualified energy efficiency improvements, and 2) residential energy property expenditures, with a lifetime credit limit of $500 ($200 for windows and skylights). So, if, for example, you weren t able to install energy-efficient windows and doors by the Dec. 31, 2011, deadline you may still be able to get a tax credit. acquisition s cost. Plus, only Sec. 179 expensing is available for used property. However, bonus depreciation may benefit more taxpayers than Sec. 179 expensing, because it isn t subject to any asset purchase limit or net income requirement. You ll also want to consider state tax consequences. Leasehold-improvement, restaurant and retailimprovement property For 2009 through 2011, accelerated depreciation was available for qualified leasehold-improvement, restaurant and retail-improvement property. ATRA extends it to 2012 and Specifically, the provision allows a shortened recovery period of 15 years rather than 39 years for such property. If you made asset purchases that might qualify for accelerated depreciation on your 2012 tax return, be sure to discuss them with your tax advisor. And if you re considering making such investments, you may want to do so in 2013 to ensure you can take advantage of this break if it s not extended again. Research credit For many years, the research credit (also commonly referred to as the research and development or research and experimentation credit) has provided an incentive for businesses to increase their investments in research. But the credit expired at the end of ATRA extends the credit to 2012 and The credit is generally equal to a portion of qualified research expenses. It s complicated to calculate, but the tax savings can be substantial. So consult your tax advisor. Work Opportunity credit The Work Opportunity credit, designed to encourage hiring from certain disadvantaged groups, expired Dec. 31, 2011, for most groups. An expanded credit for qualifying veterans expired Dec. 31, ATRA extends the credit for most eligible groups through Examples of disadvantaged groups for purposes of the credit include food stamp recipients, ex-felons and nondisabled veterans who ve been unemployed for four weeks or more, but less than six months. For these groups, the credit generally equals 40% of the first $6,000 of wages paid to qualifying employees, for a maximum credit of $2,400. A larger credit of up to $4,800 is generally available for hiring disabled veterans. And, if you re hiring veterans who ve been unemployed for six months or more in the preceding year, the maximum credits are even greater: n $5,600 for nondisabled veterans, and n $9,600 for disabled veterans. If you re considering making new hires, and workers from one or more of these disadvantaged groups might meet your needs, making the hires before the end of 2013 may be beneficial from a tax perspective. And be sure to check with your tax advisor to see if you qualify for the credit on your 2012 tax return. Transit benefits Some fringe benefits aren t included in an employee s wages for income and payroll tax purposes, yet the employer is still allowed to deduct them. Generally, the maximum transit benefit that could receive such treatment has been higher for parking than for van-pooling and mass transit. Tax legislation in 2009, however, provided for the limits to be equal through Legislation in 2010 extended this parity through ATRA has extended it through For 2012 and 2013, the limits are both now $240 per month, though there s been some discussion about increasing the 2013 amount. (Check with your tax advisor for the latest information.) If you offer transit benefits, keep parity in mind for your 2013 program. Other breaks ATRA also extends many other business breaks that had expired Dec. 31, These breaks are too limited in applicability to cover here, but they can provide significant benefits to the taxpayers that qualify for them. Talk to your tax advisor to learn which breaks may apply to you.

7 AMERICAN TAXPAYER RELIEF ACT OF Estate planning On the estate planning front, ATRA provides substantial relief compared to what would have occurred in 2013 without the act. However, it increases the estate tax rate compared to the 2012 estate tax law regime. Exemptions and rates Without congressional action, gift, estate and generation-skipping transfer tax exemptions would have dropped precipitously (by more than $4 million) and the top rates would have jumped significantly (by 20 percentage points) beginning in ATRA increases transfer taxes for some families, but much less dramatically. The act retains the 2012 exemptions (indexed for inflation) and increases the top rates by five percentage points. (See Chart 5 at right.) The changes are permanent, which, despite the rate increases, will be welcome news to many taxpayers. The Chart 5 Transfer taxes increase for some families Gift tax exemption $5.12 million $5.25 million Estate tax exemption 1 $5.12 million $5.25 million Generation-skipping transfer (GST) tax exemption $5.12 million $5.25 million Highest gift and estate tax rates and GST tax rate 35% 40% 1 Less any gift tax exemption already used during life. exemptions remain at an all-time high level and will keep up with inflation for future years. This means that, even if you used up your exemptions in 2012 to lock them in, you ll still have some more exemption available in future available exemptions and ensure your assets will be distributed according to your wishes. Without a review, it s possible the exemption and rate changes could have unintended consequences on your estate plan. years. In addition, the top rate, though higher than it was in 2012, is still quite low historically. Exemption portability Legislation in 2010 included a provision that temporarily provided significant It s important to review your estate estate planning flexibility to married plan in light of these changes. Doing couples. If one spouse died in 2011 or so will allow you to make the most of 2012 and part (or all) of his or her estate tax exemption was unused at his or her death, the estate could elect to permit the surviving spouse to use the deceased Increased tax law certainty makes estate planning a little easier spouse s remaining estate tax exemption. One of the most beneficial aspects of ATRA s estate tax provisions is their permanence. For more than a decade, much uncertainty due to expiring exemptions and rates had made estate planning a challenge. The fact that rates, exemptions and other estate-tax-related breaks under the act won t expire will make it easier to determine how to make the most of your exemptions and keep taxes to a minimum while achieving your other estate planning goals. Of course, just because the provisions don t expire doesn t mean legislation couldn t be signed into law in the future that would change exemptions, rates or breaks or even repeal the estate tax. There are still many who support an estate tax repeal. But a repeal is probably unlikely for at least the next four years, given the current balance of power in Washington and concerns about deficit reduction. Nevertheless, it s always a good idea to build flexibility into an estate plan that will allow it to adapt to changing circumstances. Also bear in mind that the state estate tax continues to be a consideration. If you live in a state with an estate tax, the exemption amount could be dramatically different from the federal exemption amount. Improper planning could lead to an unpleasant surprise in the form of significant state estate tax liability. Further complicating matters is that, even if your state doesn t have an estate tax, it s possible you may be subject to estate tax in other states in which you own property. This relief was somewhat hollow in most cases, however, because it applied only if the surviving spouse made gifts using the exemption or died by the end of ATRA has made the portability provision permanent. Making asset transfers between spouses during life and/or setting up certain trusts at death can produce similar results to portability. But making the portability election is much simpler and provides flexibility if sufficient planning hasn t been done before the first spouse s death. Still, using lifetime asset transfers and trusts can provide benefits that exemption portability doesn t offer. For example, portability doesn t protect future growth on assets from estate tax as effectively as applying the exemption to a credit shelter trust does.

8 8 AMERICAN TAXPAYER RELIEF ACT OF 2012 Also be aware that the provision doesn t allow the deceased spouse s remaining GST tax exemption to be used by the surviving spouse. In addition, some states don t recognize exemption portability. Other provisions ATRA preserves several other provisions that affect estate planning, including: n The federal estate tax deduction (rather than a credit) for state estate taxes paid, n Deferral and installment payment of estate taxes attributable to qualified closely held business interests, and n GST tax protections, including deemed and retroactive allocation of GST tax exemptions, relief for late allocations, and the ability to sever trusts for GST tax purposes. Certain income tax provisions can also be beneficial for estate planning purposes. For example, ATRA makes it easier to convert an existing traditional 401(k), 403(b) or 457(b) account into a Roth account. Roth accounts can be attractive from an estate planning perspective because they don t require you to take distributions during your life, allowing you to let the entire balance grow tax-free over your lifetime for the benefit of your heirs. Tax planning must be ongoing The changes under ATRA affect many areas of planning and will result in tax increases for higher-income taxpayers. Complicating matters is the fact that higher rates and limits on breaks go into effect at different income levels, depending on the type of tax or break. There also are recently expired breaks that haven t been extended by ATRA see 2 valuable breaks ATRA doesn t extend at right. In addition, tax reform is on the agenda for It may be and divorces can all have an impact. So unlikely that tax reform will change tax can changes in your personal finances law for 2013, but even changes effective in future years can have a significant or your business. So to ensure that you minimize your impact on what the best tax planning tax liability, your tax planning needs to strategies are for the current year. be an ongoing activity, not just a year Changes in your personal situation may end one. Consult your tax advisor about also require a change in tax planning how ATRA and other changes affect strategies. Births, deaths, marriages your planning. w 2 valuable breaks ATRA doesn t extend 1. Payroll tax relief. For 2011 and 2012 the employee portion of the Social Security tax on earned income was temporarily reduced from 6.2% to 4.2% as a stimulus measure. Similarly, the rate for the self-employed was reduced from 12.4% to 10.4%. ATRA doesn t extend this relief, so taxpayers will see a two percentage point Social Security tax increase on earned income up to the Social Security wage base ($113,700 in 2013) in 2013 and beyond. 2. Elimination of the itemized deduction reduction and personal exemption phaseout. Legislation in 2001 reduced the adjusted gross income (AGI)-based reduction on itemized deductions and phaseout of personal exemptions for 2006 through 2009 and eliminated them for Legislation in 2010 extended this elimination through ATRA allows both limits to return in 2013, and sets thresholds for them of $250,000 (singles), $275,000 (heads of households) and $300,000 (married filing jointly). This actually provides some tax savings over what would have occurred without the act, because the 2013 thresholds would have been significantly lower. For future years, the thresholds will be indexed for inflation. The itemized deduction limitation reduces otherwise allowable deductions by 3% of the amount by which a taxpayer s AGI exceeds the applicable threshold (not to exceed 80% of otherwise allowable deductions). It doesn t apply, however, to deductions for medical expenses, investment interest, or casualty, theft or wagering losses. The personal exemption phaseout reduces exemptions by 2% for each $2,500 (or portion thereof) by which a taxpayer s AGI exceeds the applicable threshold (2% of each $1,250 for married taxpayers filing separately). This publication was developed by a third-party publisher and is distributed with the understanding that the publisher and distributor are not rendering legal, accounting or other professional advice or opinions on specific facts or matters and recommend you consult an attorney, accountant, tax professional, financial advisor or other appropriate industry professional. This publication reflects tax law as of Jan. 2, Some material may be affected by subsequent changes in the laws or in the interpretation of such laws. Therefore, the services of a legal or tax advisor should be sought before implementing any ideas contained in this publication. 2013

What the New Tax Laws Mean to You

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

Davis & associates, p.a. Certified Public Accountants and Consultants

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

2017 YEAR-END. tax planning INDIVIDUALS. guide for

2017 YEAR-END tax planning INDIVIDUALS guide for year in review 2017 is unlike any previous tax year. Major congressional tax reform proposals that generally would go into effect in 2018 if signed into

2017 YEAR-END tax planning INDIVIDUALS guide for year in review 2017 is unlike any previous tax year. Major congressional tax reform proposals that generally would go into effect in 2018 if signed into

2015 PATH Act: What all Taxpayers Need to Know

2015 PATH Act: What all Taxpayers Need to Know AUTHORS Loree Dubois, CPA Laura H. Yalanis, CPA,MST Loree is the Chair of the Firm s Corporate Tax Group and Co-Chair of the Firms Healthcare Services Group.

2015 PATH Act: What all Taxpayers Need to Know AUTHORS Loree Dubois, CPA Laura H. Yalanis, CPA,MST Loree is the Chair of the Firm s Corporate Tax Group and Co-Chair of the Firms Healthcare Services Group.

Year End Tax Planning for Individuals

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

2013 Tax Planning Guide Year-round strategies to make the tax laws work for you

2013 Tax Planning Guide Year-round strategies to make the tax laws work for you 2032 Caribou Drive, Suite 200 Fort Collins, CO 80525 970.223.2727 www.soukupbush.com Dear Clients and Friends, We wish we

2013 Tax Planning Guide Year-round strategies to make the tax laws work for you 2032 Caribou Drive, Suite 200 Fort Collins, CO 80525 970.223.2727 www.soukupbush.com Dear Clients and Friends, We wish we

It s a new day for tax planning

It s a new day for tax planning On Dec. 22, 2017, the most sweeping tax legislation since the Tax Reform Act of 1986 was signed into law. The Tax Cuts and Jobs Act (TCJA) makes small reductions to income

It s a new day for tax planning On Dec. 22, 2017, the most sweeping tax legislation since the Tax Reform Act of 1986 was signed into law. The Tax Cuts and Jobs Act (TCJA) makes small reductions to income

Tax Planning Guide. 310 Commercial Drive, Suite 100 Savannah, GA office fax

2018 2019 Tax Planning Guide Year-round strategies to make the tax laws work for you 310 Commercial Drive, Suite 100 Savannah, GA 31406 www.cordascocpa.com 912.353.7800 office 912.353.7801 fax Although

2018 2019 Tax Planning Guide Year-round strategies to make the tax laws work for you 310 Commercial Drive, Suite 100 Savannah, GA 31406 www.cordascocpa.com 912.353.7800 office 912.353.7801 fax Although

Key Provisions of 2017 Tax Reform

Key Provisions of 2017 Tax Reform The final provisions of the 2017 tax reform bill are finally here. The goal of this publication is to briefly highlight some of the key changes and planning issues of

Key Provisions of 2017 Tax Reform The final provisions of the 2017 tax reform bill are finally here. The goal of this publication is to briefly highlight some of the key changes and planning issues of

Time is running out to make important planning moves before the year s end, so don t delay.

2015 Year-end tax planning Time is running out to make important planning moves before the year s end, so don t delay. The changes in various tax provisions brought about with the 2012 Tax Act continue

2015 Year-end tax planning Time is running out to make important planning moves before the year s end, so don t delay. The changes in various tax provisions brought about with the 2012 Tax Act continue

Expiring Tax Provisions

Expiring Tax Provisions The term Bush-era tax cuts or Bush tax cuts is often used to describe the tax related reductions that were contained in legislation enacted by Congress in 2001 and 2003, the Economic

Expiring Tax Provisions The term Bush-era tax cuts or Bush tax cuts is often used to describe the tax related reductions that were contained in legislation enacted by Congress in 2001 and 2003, the Economic

Tax Impact. How to claim research payroll tax credits. Restricted stock: Should you pay tax now or later?

Tax Impact November/December 2017 How to claim research payroll tax credits Restricted stock: Should you pay tax now or later? To file or not to file What you need to know about filing gift and estate

Tax Impact November/December 2017 How to claim research payroll tax credits Restricted stock: Should you pay tax now or later? To file or not to file What you need to know about filing gift and estate

The New Tax Relief Act: How Will You Be Impacted?

STRATEGIC THINKING The New Tax Relief Act: How Will You Be Impacted? The President signed the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 ( the Act ) on December 17th,

STRATEGIC THINKING The New Tax Relief Act: How Will You Be Impacted? The President signed the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 ( the Act ) on December 17th,

DeLeon & Stang, CPAs and Advisors

Dear Clients and Friends: This year-end tax planning letter is intended only to serve as a general guideline. Of course, your personal circumstances may require in-depth examination. We would be glad to

Dear Clients and Friends: This year-end tax planning letter is intended only to serve as a general guideline. Of course, your personal circumstances may require in-depth examination. We would be glad to

Biggest tax bill in 30+ years redefines tax landscape

NBC Tower - Suite 1500 455 North Cityfront Plaza Drive Chicago, IL 60611 312.670.7444 www.orba.com Biggest tax bill in 30+ years redefines tax landscape On December 22, 2017, the most sweeping tax legislation

NBC Tower - Suite 1500 455 North Cityfront Plaza Drive Chicago, IL 60611 312.670.7444 www.orba.com Biggest tax bill in 30+ years redefines tax landscape On December 22, 2017, the most sweeping tax legislation

TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU

2018 2019 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU It s a new day for tax planning On Dec. 22, 2017, the most sweeping tax legislation since the Tax Reform Act of 1986

2018 2019 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU It s a new day for tax planning On Dec. 22, 2017, the most sweeping tax legislation since the Tax Reform Act of 1986

Financial Intelligence

Financial Intelligence Volume 14 Issue 1 Tax Changes and Planning Considerations in 2018 and Beyond by Brent Yanagida, CFP, EA On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs

Financial Intelligence Volume 14 Issue 1 Tax Changes and Planning Considerations in 2018 and Beyond by Brent Yanagida, CFP, EA On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs

Tax Planning Strategies

Tax Planning Strategies 2012-2013 YEAR-TO-DATE REVIEW 2 EXECUTIVE COMPENSATION 6 INVESTING 8 REAL ESTATE 12 BUSINESS OWNERSHIP 14 CHARITABLE GIVING 16 FAMILY & EDUCATION 18 RETIREMENT 20 ESTATE PLANNING

Tax Planning Strategies 2012-2013 YEAR-TO-DATE REVIEW 2 EXECUTIVE COMPENSATION 6 INVESTING 8 REAL ESTATE 12 BUSINESS OWNERSHIP 14 CHARITABLE GIVING 16 FAMILY & EDUCATION 18 RETIREMENT 20 ESTATE PLANNING

Federal Tax Rates BURKHART & COMPANY, P.C. 900 S. GAY ST, STE KNOXVILLE, TN PHONE FAX

208 Federal Tax Rates BURKHART & COMPANY, P.C. Certified Public Accountants 900 S. GAY ST, STE. 900 KNOXVILLE, TN 37902 PHONE 865.523.7400 FAX 865.637.7239 WWW.BURKHARTCPA.COM INDIVIDUAL INCOME TAX RATES

208 Federal Tax Rates BURKHART & COMPANY, P.C. Certified Public Accountants 900 S. GAY ST, STE. 900 KNOXVILLE, TN 37902 PHONE 865.523.7400 FAX 865.637.7239 WWW.BURKHARTCPA.COM INDIVIDUAL INCOME TAX RATES

Tax Reform Legislation: Changes, Impacts, Planning Considerations

The following information and opinions are provided courtesy of Wells Fargo Bank N.A. Wealth Planning Update Tax Reform Legislation:, s, JANUARY 2018 Jay Messing, CFA, CFP Sr. Director of Planning Wells

The following information and opinions are provided courtesy of Wells Fargo Bank N.A. Wealth Planning Update Tax Reform Legislation:, s, JANUARY 2018 Jay Messing, CFA, CFP Sr. Director of Planning Wells

Tax Law Changes Make Planning Both Complicated and Critical. Presented by: Jennifer F. Flinchum, CPA, CFP Partner

2013 Planning Opportunities Tax Law Changes Make Planning Both Complicated and Critical Presented by: Jennifer F. Flinchum, CPA, CFP Partner IRS Circular 230 Disclosure: To ensure compliance with requirements

2013 Planning Opportunities Tax Law Changes Make Planning Both Complicated and Critical Presented by: Jennifer F. Flinchum, CPA, CFP Partner IRS Circular 230 Disclosure: To ensure compliance with requirements

2011 Tax Guide. What You Need to Know About the New Rules

2011 Tax Guide What You Need to Know About the New Rules Tax Guide 2011 This guide is not intended to be tax advice and should not be treated as such. Each individual s tax situation is different. You

2011 Tax Guide What You Need to Know About the New Rules Tax Guide 2011 This guide is not intended to be tax advice and should not be treated as such. Each individual s tax situation is different. You

Your Comprehensive Guide to 2013 Year-End Tax Planning

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU

2014-2015 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU Tax planning challenging but crucial for higher-income taxpayers At the beginning of 2013, many tax rates and breaks

2014-2015 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU Tax planning challenging but crucial for higher-income taxpayers At the beginning of 2013, many tax rates and breaks

Robert A Cowen Certified Public Accountant year end Tax planning for individuals

Robert A Cowen Certified Public Accountant 2017 year end Tax planning for individuals The end of the year is just a month away. It is good time to start to think about year-end planning. If you have been

Robert A Cowen Certified Public Accountant 2017 year end Tax planning for individuals The end of the year is just a month away. It is good time to start to think about year-end planning. If you have been

BURKHART & COMPANY, P.C. 900 S. GAY ST, STE KNOXVILLE, TN PHONE FAX Certified Public Accountants

2017 FEDERAL TAX RATES BURKHART & COMPANY, P.C. Certified Public Accountants 900 S. GAY ST, STE. 1900 KNOXVILLE, TN 37902 PHONE 865.523.7400 FAX 865.637.7239 WWW.BURKHARTCPA.COM INDIVIDUAL INCOME TAX RATES

2017 FEDERAL TAX RATES BURKHART & COMPANY, P.C. Certified Public Accountants 900 S. GAY ST, STE. 1900 KNOXVILLE, TN 37902 PHONE 865.523.7400 FAX 865.637.7239 WWW.BURKHARTCPA.COM INDIVIDUAL INCOME TAX RATES

2013 TAX AND FINANCIAL PLANNING TABLES. An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning.

2013 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning. WHAT YOU WILL SEE IN THIS BROCHURE 2013 Income Tax Changes Tax Rates

2013 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning. WHAT YOU WILL SEE IN THIS BROCHURE 2013 Income Tax Changes Tax Rates

TAX PLANNING GUIDE

2012-2013 TAX PLANNING GUIDE Year-round strategies to make the tax laws work for you Dear Clients and Friends, I wish I could tell you exactly what s going to happen in the coming months with the economy,

2012-2013 TAX PLANNING GUIDE Year-round strategies to make the tax laws work for you Dear Clients and Friends, I wish I could tell you exactly what s going to happen in the coming months with the economy,

Client Tax Letter. Income Tax Rates Hold Steady. What s Inside. Still a Bargain. April/May/June 2011

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Income Tax Rates Hold Steady April/May/June 2011 Tax legislation passed at the end of 2010 the Tax Relief, Unemployment

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Income Tax Rates Hold Steady April/May/June 2011 Tax legislation passed at the end of 2010 the Tax Relief, Unemployment

Tax Changes for 2016: A Checklist

Tax Changes for 2016: A Checklist Welcome, 2016! As the New Year rolls around, it's always a sure bet that there will be changes to current tax law and 2016 is no different. From health savings accounts

Tax Changes for 2016: A Checklist Welcome, 2016! As the New Year rolls around, it's always a sure bet that there will be changes to current tax law and 2016 is no different. From health savings accounts

Tax Planning Guide Year-round strategies to make the tax laws work for you

2015-2016 Tax Planning Guide Year-round strategies to make the tax laws work for you Be ready to revise your individual or business tax plan quickly in 2015 When it comes to tax law, uncertain remains

2015-2016 Tax Planning Guide Year-round strategies to make the tax laws work for you Be ready to revise your individual or business tax plan quickly in 2015 When it comes to tax law, uncertain remains

Tax Impact. Accelerating depreciation deductions A cost segregation study may reduce taxes. How basis planning can result in significant tax savings

Tax Impact September/October 2016 Accelerating depreciation deductions A cost segregation study may reduce taxes How basis planning can result in significant tax savings Watch out for the alternative minimum

Tax Impact September/October 2016 Accelerating depreciation deductions A cost segregation study may reduce taxes How basis planning can result in significant tax savings Watch out for the alternative minimum

IMPACT OF THE ELECTION President-Elect Trump proposes significant changes to the tax law including:

December 2016 To Our Clients and Friends: While many of you are making plans for year-end holidays, what should not be overlooked this time of year is year-end tax planning, especially considering the

December 2016 To Our Clients and Friends: While many of you are making plans for year-end holidays, what should not be overlooked this time of year is year-end tax planning, especially considering the

Year-End Tax Tips for Individuals

Year-End Tax Tips for Individuals New tax legislation has brought greater certainty to year-end planning, but also created new challenges. There is still time to set up an appointment for year-end planning.

Year-End Tax Tips for Individuals New tax legislation has brought greater certainty to year-end planning, but also created new challenges. There is still time to set up an appointment for year-end planning.

Tax Law Snapshot for Individuals 2014 Filing Season

Tax Law Snapshot for Individuals 2014 Filing Season (480) 776-3358 1237 S. Val Vista Dr. Suite 206 Mesa, AZ 85204-6401 (480) 323-2474 fax kboudreau@bcsbs.net Taxes Contract Financial Management Financial

Tax Law Snapshot for Individuals 2014 Filing Season (480) 776-3358 1237 S. Val Vista Dr. Suite 206 Mesa, AZ 85204-6401 (480) 323-2474 fax kboudreau@bcsbs.net Taxes Contract Financial Management Financial

2018 Year-End Tax Planning for Individuals

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

2018 Tax Planning & Reference Guide

2018 Tax Planning & Reference Guide The 2018 Tax Planning & Reference Guide is designed to be a reference only and is not intended to provide tax advice. Please consult your professional tax advisor prior

2018 Tax Planning & Reference Guide The 2018 Tax Planning & Reference Guide is designed to be a reference only and is not intended to provide tax advice. Please consult your professional tax advisor prior

Dear Client: Basic Numbers You Need to Know

Dear Client: As 2013 draws to a close, there is still time to reduce your 2013 tax bill and plan ahead for 2014. This letter highlights several potential tax-saving opportunities for you to consider. I

Dear Client: As 2013 draws to a close, there is still time to reduce your 2013 tax bill and plan ahead for 2014. This letter highlights several potential tax-saving opportunities for you to consider. I

Year-End Tax Planning Letter

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

THE AGENDA YEAR END TAX PLANNING

YEAR END TAX PLANNING TUESDAY, DECEMBER 8, 2015 PRESENTED BY: JOE CAWLEY, CPA, PRINCIPAL-JOECAWLEY@BSSF.COM JOHN WEIDMAN, CPA, PRINCIPAL-JOHNWEIDMAN@BSSF.COM PHONE NUMBER-(717)761-7171 1 THE AGENDA Part

YEAR END TAX PLANNING TUESDAY, DECEMBER 8, 2015 PRESENTED BY: JOE CAWLEY, CPA, PRINCIPAL-JOECAWLEY@BSSF.COM JOHN WEIDMAN, CPA, PRINCIPAL-JOHNWEIDMAN@BSSF.COM PHONE NUMBER-(717)761-7171 1 THE AGENDA Part

Tax Topics /24/14. Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist

Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist Tax Topics 2014-11 11/24/14 IRS releases 2015 inflation-adjusted numbers Last month, the IRS released its 2015 inflation-adjusted

Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist Tax Topics 2014-11 11/24/14 IRS releases 2015 inflation-adjusted numbers Last month, the IRS released its 2015 inflation-adjusted

2017 Tax Planning Tables

2017 Tax Planning Tables 2017 Important Deadlines Last day to January 17 Pay fourth-quarter 2016 federal individual estimated income tax January 25 Buy in to close a short-against-the-box position (regular-way

2017 Tax Planning Tables 2017 Important Deadlines Last day to January 17 Pay fourth-quarter 2016 federal individual estimated income tax January 25 Buy in to close a short-against-the-box position (regular-way

2004 Tax-smart strategies guide. Keep more of what you earn

2004 Tax-smart strategies guide Keep more of what you earn 2004 Tax-smart strategies guide Keep more of what you earn As a taxpayer, you currently have some of the largest tax cuts in history working

2004 Tax-smart strategies guide Keep more of what you earn 2004 Tax-smart strategies guide Keep more of what you earn As a taxpayer, you currently have some of the largest tax cuts in history working

Year End Tax Planning, 2013

Fall, 2013 Year End Tax Planning, 2013 Introduction points that might put you in a higher tax bracket or limit your deductions. Tax planning to reduce income and/or consolidate deductions may avoid various

Fall, 2013 Year End Tax Planning, 2013 Introduction points that might put you in a higher tax bracket or limit your deductions. Tax planning to reduce income and/or consolidate deductions may avoid various

Brackets (seven) - Taxable Income Single Filers. Between $9,525 and $38,700. Between $2,550 and $9,150. Between $157,500 and $200,000

- Taxable Income Single Filers. Between $9,525 and $38,700. Between $2,550 and $9,150. Between $157,500 and $200,000") Individual Taxes (Which Would Expire After 2025) Brackets (seven) - Taxable Income Single Filers Up to $9,525 Between $9,525 and $38,700 Between $38,700 and $82,500 Between $200,000 and $500,000 Above

Individual Taxes (Which Would Expire After 2025) Brackets (seven) - Taxable Income Single Filers Up to $9,525 Between $9,525 and $38,700 Between $38,700 and $82,500 Between $200,000 and $500,000 Above

2018 TAX AND FINANCIAL PLANNING TABLES

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

Year-End Tax Planning Letter

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

2017 Year-End Tax Planning for Individuals

2017 Year-End Tax Planning for Individuals As 2017 draws to a close, there is still time to reduce your 2017 tax bill and plan ahead for 2018. This letter highlights several potential tax-saving opportunities

2017 Year-End Tax Planning for Individuals As 2017 draws to a close, there is still time to reduce your 2017 tax bill and plan ahead for 2018. This letter highlights several potential tax-saving opportunities

Client Newsletter. 551 West 78th Street, Ste. 204, P.O. Box 254 Chanhassen, MN Office: Fax:

Client Newsletter 2015 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: RODENZ ACCOUNTING & TAX SERVICE LLC Accounting Business Consulting Tax Preparation Payroll Services Darrell E. Rodenz Certified Public Accountant

Client Newsletter 2015 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: RODENZ ACCOUNTING & TAX SERVICE LLC Accounting Business Consulting Tax Preparation Payroll Services Darrell E. Rodenz Certified Public Accountant

Re: 2012 American Taxpayer Relief Act (ATRA)

") 50 W Mashta Drive, Suite 6 Key Biscayne, FL 33149 Tel: (305) 361-1014 Fax: (305) 361-7078 www.lancaster-cpas.com JANUARY 2nd, 2013 Re: 2012 American Taxpayer Relief Act (ATRA) Dear Friends, After much

50 W Mashta Drive, Suite 6 Key Biscayne, FL 33149 Tel: (305) 361-1014 Fax: (305) 361-7078 www.lancaster-cpas.com JANUARY 2nd, 2013 Re: 2012 American Taxpayer Relief Act (ATRA) Dear Friends, After much

2016 Tax Planning Tables

2016 Tax Planning Tables 2016 Important Deadlines Last day to January 15 Pay fourth-quarter 2015 federal individual estimated income tax January 26 Buy in to close a short-against-the-box position (regular-way

2016 Tax Planning Tables 2016 Important Deadlines Last day to January 15 Pay fourth-quarter 2015 federal individual estimated income tax January 26 Buy in to close a short-against-the-box position (regular-way

New Law Extends and Enhances Numerous Tax Breaks

220 Market Ave. S., Suite 700 Canton Ohio 44702 330-453-7633 Winter 2016 Vol. 12, Issue 1 New Law Extends and Enhances Numerous Tax Breaks At the end of last year, the Protecting Americans from Tax Hikes

220 Market Ave. S., Suite 700 Canton Ohio 44702 330-453-7633 Winter 2016 Vol. 12, Issue 1 New Law Extends and Enhances Numerous Tax Breaks At the end of last year, the Protecting Americans from Tax Hikes

American Taxpayer Relief Act of 2012 Workshop

American Taxpayer Relief Act of 2012 Workshop John Kilroy, CPA, CFP May 14, 2013 Agenda Estate, Gift and GST provisions Individual Income Tax provisions Trust and Estate Income Tax provisions Business

American Taxpayer Relief Act of 2012 Workshop John Kilroy, CPA, CFP May 14, 2013 Agenda Estate, Gift and GST provisions Individual Income Tax provisions Trust and Estate Income Tax provisions Business

2017 INCOME AND PAYROLL TAX RATES

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

Re: 2012 Year-End Tax Planning for Individuals

Re: 2012 Year-End Tax Planning for Individuals To Our Valued Clients and Friends: Year-end tax planning is always complicated by the uncertainty that the following year may bring and 2012 is no exception.

Re: 2012 Year-End Tax Planning for Individuals To Our Valued Clients and Friends: Year-end tax planning is always complicated by the uncertainty that the following year may bring and 2012 is no exception.

Year-End Tax Moves for 2016

Year-End Tax Moves for 2016 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

Year-End Tax Moves for 2016 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

Tax Planning Guide

2015-2016 Tax Planning Guide Year-round strategies to make the tax laws work for you JAMES D. MILLER & CO. LLP CERTIFIED PUBLIC ACCOUNTANTS 350 FIFTH AVENUE SUITE 4601 NEW YORK, NEW YORK 10118-4601 TELEPHONE:

2015-2016 Tax Planning Guide Year-round strategies to make the tax laws work for you JAMES D. MILLER & CO. LLP CERTIFIED PUBLIC ACCOUNTANTS 350 FIFTH AVENUE SUITE 4601 NEW YORK, NEW YORK 10118-4601 TELEPHONE:

2017 INDIVIDUAL TAX PLANNING

2017 INDIVIDUAL TAX PLANNING We hope that you are looking forward to the Holiday Season. It is hard to believe that it is mid-december and this year is quickly ending. If you ve been following the news

2017 INDIVIDUAL TAX PLANNING We hope that you are looking forward to the Holiday Season. It is hard to believe that it is mid-december and this year is quickly ending. If you ve been following the news

Tax-cutting time is ticking away. Review options for accelerating income. Dear Clients and Friends,

Dear Clients and Friends, Taxes are going to be a major issue for the rest of 2012 and for much of 2013. On January 1, 2013, the country faces what Federal Reserve Chairman Ben Bernanke has called a fiscal

Dear Clients and Friends, Taxes are going to be a major issue for the rest of 2012 and for much of 2013. On January 1, 2013, the country faces what Federal Reserve Chairman Ben Bernanke has called a fiscal

planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value

2019 tax planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value 2019 important deadlines Last day to January 15 Pay fourth-quarter 2018 federal individual

2019 tax planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value 2019 important deadlines Last day to January 15 Pay fourth-quarter 2018 federal individual

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

Spott, Lucey & Wall, Inc.

2017-2018 TAX PLANNING GUIDE Year-round strategies to make the tax laws work for you Spott, Lucey & Wall, Inc. CERTIFIED PUBLIC ACCOUNTANTS 601 Montgomery Street Suite 1400 San Francisco, CA 94111 www.spottluceywall-cpas.com

2017-2018 TAX PLANNING GUIDE Year-round strategies to make the tax laws work for you Spott, Lucey & Wall, Inc. CERTIFIED PUBLIC ACCOUNTANTS 601 Montgomery Street Suite 1400 San Francisco, CA 94111 www.spottluceywall-cpas.com

TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU

2017-2018 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU Possible tax law changes on the horizon With Donald Trump in the White House and Republicans maintaining a majority

2017-2018 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU Possible tax law changes on the horizon With Donald Trump in the White House and Republicans maintaining a majority

Year-end Tax Moves for 2017

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

WEALTH MANAGEMENT 2016 FINANCIAL PLANNING LIMITS AND TAX RATE SCHEDULES

WEALTH MANAGEMENT 2016 FINANCIAL PLANNING LIMITS AND TAX RATE SCHEDULES Building success together. One advisor at a time. Addressing the complexities of financial planning with your most valuable clients

WEALTH MANAGEMENT 2016 FINANCIAL PLANNING LIMITS AND TAX RATE SCHEDULES Building success together. One advisor at a time. Addressing the complexities of financial planning with your most valuable clients

901 East Cary Street, Suite 1100, Richmond, VA

2017 Tax Planning & Reference Guide The 2017 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

2017 Tax Planning & Reference Guide The 2017 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU

2017-2018 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU Possible tax law changes on the horizon Depending on what happens in Congress, we could have some dramatic changes in

2017-2018 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU Possible tax law changes on the horizon Depending on what happens in Congress, we could have some dramatic changes in

Tax Planning Guide Year-round strategies to make the tax laws work for you

2010 2011 Tax Planning Guide Year-round strategies to make the tax laws work for you For tax planning, the only certainty is uncertainty As our country starts to recover from the recession, we re confronted

2010 2011 Tax Planning Guide Year-round strategies to make the tax laws work for you For tax planning, the only certainty is uncertainty As our country starts to recover from the recession, we re confronted

Personal Income Tax Update. AGA Winter Seminar 2013 Nathan Abbott, CISA, CFE, EA

Personal Income Tax Update AGA Winter Seminar 2013 Nathan Abbott, CISA, CFE, EA The Easy Stuff Inflation Adjustments Inflation Adjustments Inflation Adjustments Inflation Adjustments Social Security Maximum

Personal Income Tax Update AGA Winter Seminar 2013 Nathan Abbott, CISA, CFE, EA The Easy Stuff Inflation Adjustments Inflation Adjustments Inflation Adjustments Inflation Adjustments Social Security Maximum

Before we get to specific suggestions, here are two important considerations to keep in mind.

To Our Clients and Friends As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. With the fate of many of the long favored tax breaks

To Our Clients and Friends As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. With the fate of many of the long favored tax breaks

2013 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS

INTRODUCTION 2013 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS As the end of 2013 approaches, it s time to consider planning moves that could reduce your 2013 taxes. Year-end planning is particularly important

INTRODUCTION 2013 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS As the end of 2013 approaches, it s time to consider planning moves that could reduce your 2013 taxes. Year-end planning is particularly important

TAX UPDATE TAX CUTS & JOBS ACT (2018) Add l Elderly & Blind Joint & Surviving Spouse: $1,300

Add l Elderly & Blind Joint & Surviving Spouse: $1,300") TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

You may wish to carefully examine your records to determine if you may be missing any of these deductions.

2018 tax planning and tax changes Re: Planning 2018: Tax Consequences for Self-Employed Individuals Dear Client: Owning your own business can be very rewarding, both personally and financially. Being the

2018 tax planning and tax changes Re: Planning 2018: Tax Consequences for Self-Employed Individuals Dear Client: Owning your own business can be very rewarding, both personally and financially. Being the

Tax planning is as essential as ever

2 014-2 015 TAX PLANNING GUIDE Year-round strategies to make the tax laws work for you Tax planning is as essential as ever At the beginning of 2013, many tax rates and breaks were made permanent. The

2 014-2 015 TAX PLANNING GUIDE Year-round strategies to make the tax laws work for you Tax planning is as essential as ever At the beginning of 2013, many tax rates and breaks were made permanent. The

Arthur Lander C.P.A., P.C. A professional corporation

A Arthur Lander C.P.A., P.C. A professional corporation 300 N. Washington St. #104 Alexandria, Virginia 22314 phone: (703) 486-0700 fax: (703) 527-7207 YEAR-END TAX PLANNING FOR INDIVIDUALS Once again,

A Arthur Lander C.P.A., P.C. A professional corporation 300 N. Washington St. #104 Alexandria, Virginia 22314 phone: (703) 486-0700 fax: (703) 527-7207 YEAR-END TAX PLANNING FOR INDIVIDUALS Once again,

Integrity Accounting

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

2018 tax planning tables

2018 tax planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value 2018 important deadlines Last day to January 16 Pay fourth-quarter 2017 federal individual

2018 tax planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value 2018 important deadlines Last day to January 16 Pay fourth-quarter 2017 federal individual

e4 Brokerage, LLC th St. South Suite C Fargo, ND

e4 Brokerage, LLC 2280 45th St. South Suite C Fargo, ND 58104 701-356-1270 866-356-3203 sbergee@e4brokerage.com www.e4brokerage.com 2017 Tax Facts Guide 1/01/2017 Page 1 of 28, see disclaimer on final

e4 Brokerage, LLC 2280 45th St. South Suite C Fargo, ND 58104 701-356-1270 866-356-3203 sbergee@e4brokerage.com www.e4brokerage.com 2017 Tax Facts Guide 1/01/2017 Page 1 of 28, see disclaimer on final

2017 year-end tax guide Possible tax law changes on the horizon

2017 year-end tax guide Possible tax law changes on the horizon With Donald Trump in the White House and Republicans maintaining a majority in Congress comes the possibility of some dramatic changes in

2017 year-end tax guide Possible tax law changes on the horizon With Donald Trump in the White House and Republicans maintaining a majority in Congress comes the possibility of some dramatic changes in

U.S. Tax Reform FINANCIAL PLANNING IMPLICATIONS OF THE U.S. TAX REFORM MEASURE

PRICE POINT December 2017 Timely intelligence and analysis for our clients. U.S. Tax Reform FINANCIAL PLANNING IMPLICATIONS OF THE U.S. TAX REFORM MEASURE KEY POINTS The U.S. tax reform measure will have

PRICE POINT December 2017 Timely intelligence and analysis for our clients. U.S. Tax Reform FINANCIAL PLANNING IMPLICATIONS OF THE U.S. TAX REFORM MEASURE KEY POINTS The U.S. tax reform measure will have

TAX CUTS AND JOBS ACT OF 2017

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Individual & Business Tax Planning Update

Individual & Business Tax Planning Update November 14, 2013 HMWC CPAs & Business Advisors Presented by: Curtis Campbell Janet Anderson Joel Jorrisch DID YOU KNOW? 2 1 2013 MARKS THE 100 TH ANNIVERSARY

Individual & Business Tax Planning Update November 14, 2013 HMWC CPAs & Business Advisors Presented by: Curtis Campbell Janet Anderson Joel Jorrisch DID YOU KNOW? 2 1 2013 MARKS THE 100 TH ANNIVERSARY

Tax Planning Guide. Year-round strategies to make the tax laws work for you

2016-2017 Tax Planning Guide Year-round strategies to make the tax laws work for you For tax planning, the only certainty is uncertainty Last December, many valuable tax breaks were made permanent by the

2016-2017 Tax Planning Guide Year-round strategies to make the tax laws work for you For tax planning, the only certainty is uncertainty Last December, many valuable tax breaks were made permanent by the

2011 tax planning tables

2011 tax planning tables 2011 important deadlines Last day to Jan. 18 Pay fourth-quarter 2010 federal individual estimated income tax Jan. 25 Buy in to close a short-against-the-box position (regular-way

2011 tax planning tables 2011 important deadlines Last day to Jan. 18 Pay fourth-quarter 2010 federal individual estimated income tax Jan. 25 Buy in to close a short-against-the-box position (regular-way

What Are We Covering Today?

Individual & Business Tax Planning Update November 9, 2011 HMWC CPAs & Business Advisors What Are We Covering Today? 2011 Legislation Update Individuals Business Tax Planning Strategies Individuals Business

Individual & Business Tax Planning Update November 9, 2011 HMWC CPAs & Business Advisors What Are We Covering Today? 2011 Legislation Update Individuals Business Tax Planning Strategies Individuals Business

Individual year-end planning and tax law updates

Individual yearend planning and tax law updates October 29, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 1 Presenters

Individual yearend planning and tax law updates October 29, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 1 Presenters

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM:

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: A publication of the Minnesota Association of Public Accountants The Minnesota Association of Public Accountants has prepared this newsletter.

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: A publication of the Minnesota Association of Public Accountants The Minnesota Association of Public Accountants has prepared this newsletter.

FEBRUARY 2018 A FEW ITEMS CONCERNING INCOME TAXES AFTER 2017

FEBRUARY 2018 A FEW ITEMS CONCERNING INCOME TAXES AFTER 2017 The Tax Cuts and Jobs Act, hailed as the largest tax reform in over 30 years, was signed into law by the President on December 22, 2017. Unlike

FEBRUARY 2018 A FEW ITEMS CONCERNING INCOME TAXES AFTER 2017 The Tax Cuts and Jobs Act, hailed as the largest tax reform in over 30 years, was signed into law by the President on December 22, 2017. Unlike

Individual Tax Projection & Tax Reduction W&A Rev

Individual Tax Projection & Tax Reduction Guide @ W&A 256R North Washington Street Falls Church, VA 22046-3435 Telephone: 703 356-5005 Fax: 703 356-5955 Email: Pete@lowtaxsolutions.com www.lowtaxsolutions.com

Individual Tax Projection & Tax Reduction Guide @ W&A 256R North Washington Street Falls Church, VA 22046-3435 Telephone: 703 356-5005 Fax: 703 356-5955 Email: Pete@lowtaxsolutions.com www.lowtaxsolutions.com

Individual Year-End Tax Planning for 2016

Individual Year-End Tax Planning for 2016 It is getting to be that time of year where we should meet to review your tax situation for 2016. Proper year-end planning can help alleviate any unnecessary tax

Individual Year-End Tax Planning for 2016 It is getting to be that time of year where we should meet to review your tax situation for 2016. Proper year-end planning can help alleviate any unnecessary tax

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

YEAR-END TAX PLANNING LETTER

YEAR-END TAX PLANNING LETTER SUBMITTED BY Huntsville I Pensacola www.anglincpa.com Dear Clients and Friends, As 2018 draws to a close, there is still time to reduce your 2018 tax bill and plan ahead for

YEAR-END TAX PLANNING LETTER SUBMITTED BY Huntsville I Pensacola www.anglincpa.com Dear Clients and Friends, As 2018 draws to a close, there is still time to reduce your 2018 tax bill and plan ahead for

e-pocket TAX TABLES 2016 and 2017 Quick Links: 2016 Income and Payroll Tax Rates 2017 Income and Payroll Tax Rates

e-pocket TAX TABLES 2016 and 2017 Quick Links: 2016 Income and Payroll Tax Rates 2017 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

e-pocket TAX TABLES 2016 and 2017 Quick Links: 2016 Income and Payroll Tax Rates 2017 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

TAX GUIDE PLANNING YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU

2018 2019 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU It s a new day for tax planning On December 22, 2017, the most sweeping tax legislation since the Tax Reform Act of

2018 2019 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU It s a new day for tax planning On December 22, 2017, the most sweeping tax legislation since the Tax Reform Act of

Tax Cuts and Jobs Act 2017 HR 1

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

2018 year-end tax guide

2018 year-end tax guide It s a new day for tax planning CONTENTS Year-to-date review 2 Executive compensation 8 Investing 11 Real estate 17 Business ownership 21 Charitable giving 24 Family and education

2018 year-end tax guide It s a new day for tax planning CONTENTS Year-to-date review 2 Executive compensation 8 Investing 11 Real estate 17 Business ownership 21 Charitable giving 24 Family and education

Client Letter: Year-End Tax Planning for 2018 (Individuals)

") Client Letter: Year-End Tax Planning for 2018 (Individuals) Just as the daylight hours are getting shorter, so is the time for fine tuning any last-minute strategies to lower your 2018 tax bill. Unlike

Client Letter: Year-End Tax Planning for 2018 (Individuals) Just as the daylight hours are getting shorter, so is the time for fine tuning any last-minute strategies to lower your 2018 tax bill. Unlike

Year-end Tax Planning Letter

December 2011 Year-end Tax Planning Letter To Our Clients and Friends: As we approach year end, it s again time to focus on last-minute tax planning changes that you might want to consider to benefit you

December 2011 Year-end Tax Planning Letter To Our Clients and Friends: As we approach year end, it s again time to focus on last-minute tax planning changes that you might want to consider to benefit you

e-pocket TAX TABLES Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax

e-pocket TAX TABLES Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security Benefits Personal

e-pocket TAX TABLES Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security Benefits Personal