Assessment of Various Entities (Revision)

|

|

|

- Beverley Walker

- 5 years ago

- Views:

Transcription

1 CA Final Direct Tax 1 Assessment of Various Entities (Revision) Assessment of Companies: Tax on income from life insurance business: (Section 115B) - Profits and gains derived from the business of life insurance computed in accordance with the First Schedule to the Income-tax Act, 1961, - Income-tax payable (i) Life insurance business included - At the rate of 12½% and (ii) Balance - Regular Rate - Not be subject to MAT. Section 115A: 1. Where the income of a non-corporate non-resident or a foreign company consists of: (i) dividends (other than dividends referred to in section 115-O) (ii) interest received from Government or from an Indian concern on monies borrowed or debt incurred by the Government or the Indian concern in foreign currency; or (iii) income received in respect of units purchased in foreign currency of a mutual fund the same will be taxed at 20%. However, the following interest income would be subject to a concessional rate of 5% on gross interest: (i) Interest income received by a non-corporate non-resident or a foreign company from an infrastructural fund (ii) Interest received by a foreign company or a non-corporate non-resident, in respect of borrowing made by an Indian company or business trust in foreign currency from sources outside India between and or by way of issue of long-term infrastructure bonds between and or by way of issue of long-term bonds between and (194LC) (iii) Distributed income, taxable in the hands of non-resident unit holders of a business trust. (194LBA) 2. No deduction 3. Shall not furnish a return of their income if the total income consisted only of the income referred above, and the tax deductible at source has been deducted from such income. 4. Where the total income of a non-corporate non-resident or a foreign company includes royalty or fees for technical services, other than income referred to in section 44DA(1), received from Government or an Indian concern in pursuance of an agreement made, the same will be subject to the following conditions: (a) such agreement must be made with an Indian concern ; (b) the agreement must be approved by the Central Government, or (c) where it relates to a matter included in the industrial policy for the time being in force. Section 115AB: (1) Where the total income of an overseas financial organisation (Off -shore Fund) includes the following incomes namely: (a) income received in respect of units purchased in foreign currency, or (b) income by way of long term capital gains arising from the transfer of units purchased in foreign currency, the same will be taxed at the rate of 10%. (No Deduction)

2 CA Final Direct Tax 2 Section 115AC: 1. Where the total income of a non-resident includes the following types of income namely, (a) income by way of interest on bonds of an Indian company issued in accordance with such scheme as may be notified by the Government or on bonds of a public sector company, sold by the Government, and purchased by him in foreign currency; or (b) income by way of dividends (other than dividends referred to in section 115-O) on Global Depository Receipts (c) income by way of long-term capital gains arising from the above bonds or GDRs. The income-tax will be at the rate of 10% on the above income. (No deduction) (No Indexation) (If only income & TDS, then NO ROI) Section 115ACA: This section applies to resident individuals who are employees of an Indian company engaged in specified knowledge based industry or service, or its subsidiary engaged in specified knowledge based industry or service. Income-tax payable shall be the aggregate of: (i) 10% of income by way of dividends (other than dividends referred to in section 115-O) in respect of Global Depository Receipts of an Indian company purchased in foreign currency in accordance with such employees stock option scheme as the Central Government may, notify, (ii) 10%, in case of long-term capital gains arising from the transfer of the aforesaid Global Depository Receipts. (No deduction) (No Indexation) Section 115AD: Foreign Institutional Investor, income-tax payable shall be the aggregate of the following: (1) 20% of the income (other than income by way of dividends referred to in section 115-O) However, 194LD, income-tax is payable@5% of gross income. (2) 30% of the short-term capital gains. However, 111A is to be calculated at 15%. (3) 10% of long term capital gains. (No deduction) (No Indexation) Section 115BBD: Dividends received by Indian companies from specified foreign companies to be subject to a concessional rate of 15% Specified foreign company means a foreign company in which the Indian company holds 26% or more in nominal value of the equity share capital of the company. Section 47A: Section 47A provides that where the transfer of a capital asset between a parent company and its hundred per cent subsidiary company has been exempted from any charge to capital gains tax by virtue of provisions of section 47 such exemption will be revoked in either of the two under noted cases by an order of rectification under section 155(7A) of the Income-tax Act, (i) Within a period of eight years from the date of the transfer the capital asset in question is converted by the transferee company into or as, stock -in-trade of its business; or (ii) within a period of eight years from the date of the transfer the parent company or its nominee or as the case may be, the holding company ceases to hold the whole of the share capital of the subsidiary company.

3 CA Final Direct Tax 3 Minimum Alternate Tax on companies [Section 115JB]: As per section 115JB(1), in case of company (domestic or foreign), if the income-tax payable on the total income computed under the Income-tax Act, 1961 is less than 18.5% of its book profit, such book profit shall be deemed to be the total income of the assessee and the tax payable by the assessee on such total income shall be the amount of income-tax at the rate of 18.5% (add surcharge & Cess asapplicable). Section 115JB requires companies to prepare their profit and loss account for the relevant previous year in accordance with the provisions of the Act governing such company. For computing the book profit, the net profit shall be increased by the following amounts if debited to the profit and loss account: (a) income-tax paid or payable, and the provision therefor; or [It may be noted that income-tax includes: (1) dividend distribution tax / tax on distributed income; (2) interest; (3) surcharge; (4) education cess; and (5) secondary and higher education cess] (b) amount carried to any reserves; or (c) amounts set aside to provision for meeting liabilities other than ascertained liabilities; or (d) amount of provision for losses of subsidiary companies; or (e) amount of dividends paid or proposed; or (f) amount of expenditure relatable to any income to which section 10 [other than section 10(38)] or 11 or 12 apply; or (fa) amount of expenditure relatable to income, being share of the assessee in the income of an AOP or BOI, on which no income-tax is payable in accordance with the provisions of section 86; or (fb) the amount or amounts of expenditure relatable to income accruing or arising to an assessee, being a foreign company, from: (A) the capital gains arising on transactions in securities; or (B) the interest, royalty or fees for technical services chargeable to tax at the rate or rates specified in Chapter XII, if the income-tax payable thereon in accordance with the provisions of the Act, other than the provisions of this Chapter, is at a rate less than 18.5%; or (fc) the amount representing notional loss on transfer of a capital asset, being share or a special purpose vehicle to a business trust in exchange of units allotted by that trust or the amount representing notional loss resulting from any change in carrying amount of said units or the amount of loss on transfer of such units; or (g) the amount of depreciation; or (h) the amount of deferred tax and provision therefor; or (i) the amount set aside as provision for diminution in the value of any asset. Further, the net profit shall also be increased by the amount standing in revaluation reserve relating to the revalued asset on the retirement or disposal of such asset, in case the same is not credited to the profit and loss account. Also, when units of business trust are actually transferred, the amount of gain on such transfer has to be added to compute the book profit, since notional gains on transfer of share of a special purpose vehicle to a business trust in exchange for the units of the business trust and notional gains resulting from change in carrying amount of such units have been deducted earlier to compute book profit. The amount of gain has to be computed by taking into consideration the cost of shares exchanged with the units of the business trust, in a case where the shares are carried at cost. In a case where the shares

4 CA Final Direct Tax 4 are carried at a value other than the cost through profit and loss account, the carrying amount of shares at the time of exchange would be taken into consideration for computing the amount of gain. The amount of gain on such transfer, if any, credited to profit and loss account will be reduced. The net profit shall be reduced by the following amounts: (i) amount withdrawn from any reserve or provision, if any, such amount is credited to the profit and loss account. (ii) amount of income to which section 10 [other than section 10(38)] or 11 or 12 apply, if such amount is credited to the profit and loss amount; (iia) the amount of depreciation debited to the profit and loss account (excluding the claim of depreciation on account of revaluation of assets); (iib) the amount withdrawn from the revaluation reserve and credited to the profit and loss account, to the extent it does not exceed the amount of depreciation on revaluation of assets;(iic) the amount of income, being the share of the assessee in the income of an AOP or BOI, on which no income-tax is payable in accordance with the provisions of section 86, if any such amount is credited to the profit and loss account; or (iid) the amount of income accruing or arising to an assessee, being a foreign company, from: (A) the capital gains arising on transactions in securities; or (B) the interest, royalty or fees for technical services chargeable to tax at the rate or rates specified in Chapter XII, if such income is credited to the profit and loss account and the income-tax payable thereon in accordance with the provisions of the Income-tax Act, 1961, other than the provisions of Chapter XII-B, is at a rate less than 18.5%; or (iie) the amount representing: (A) the notional gain on transfer of a capital asset, being a share of a SPV to a business trust in exchange of units allotted by the business trust; (B) notional gain resulting from any change in carrying amount of said units; or (C) gain on transfer of such units, if any, credited to profit and loss account; (iif) the amount of loss on transfer of units acquired in exchange of shares of SPV computed by taking into account the cost of the shares exchanged with the units, where the shares are carried at cost. In case shares are carried at a value other than cost through profit and loss account, the amount of loss on transfer of such units has to be computed by taking into account the carrying amount of the shares at the time of exchange; (iii) amount of brought forward loss or unabsorbed depreciation, whichever is less as per books of account. The loss shall not include depreciation; If either the figure of brought forward loss or unabsorbed depreciation is NIL, no deduction will be allowed from the book profit of the relevant year; (vii) amount of profits of a sick industrial company (BIFR company) commencing from the previous year in which the company became sick and ending with the assessment year during which the entire net worth becomes positive. (viii) the amount of deferred tax, if any such amount is credited to the profit and loss account.

5 CA Final Direct Tax 5 Set-off of credit of tax paid under section 115JB [Section 115JAA]: (1) In any assessment year in relation to the deemed income under section 115JB(1), the excess of tax so paid over and above the tax payable under the other provisions of the Income-tax Act, 1961, will be allowed as tax credit in the subsequent years. (2) The tax credit is, therefore, the difference between the tax paid under section 115JB(1) and the tax payable on the total income computed in accordance with the other provisions of the Act. (3) The tax credit shall be allowed to be set off in a year in which tax becomes payable on the total income computed in accordance with provisions of the Act other than section 115JB. Tax on distributed profit of domestic companies: Chapter XII D [Section 115-O]: Flat rate of 15% + Surcharge (12%) + Cess (3%) [Gross up] A holding company receiving dividend from its subsidiary company can reduce the same from dividends declared, distributed or paid by it. The NPS Trust is exempted from the applicability of dividend distribution tax in respect of dividend paid to any person for, or on behalf of, the NPS Trust. This tax must be paid to the credit of the Central Government within fourteen days from the date of (a) declaration of any dividend or (b) distribution of any dividend or (c) payment of any dividend, whichever is earliest. Simple for every month or part thereof on the amount of such tax for the period beginning from the date following the date on which the tax was payable and ending with the date on which the tax is actually paid. Section 115QA: (1) Distributed income (i.e., consideration paid by the company for buyback of its own unlisted shares which is in excess of the sum received by the company at the time of issue of such shares) would be subject to additional income tax@20% (plus surcharge@12% and education cess@2% and secondary and higher education cess@1%) in the hands of the domestic company. (2) 14 days (3) Simple for every month or part Section 115VA: Computation of profits and gains from the business of operating qualifying ships: 1. It is optional for a qualifying company, 2. for the income from the business of operating qualifying ships, 3. to compute its income as per tonnage tax scheme, or 4. to compute its income as per normal provisions of the Act. Section 115VC: Qualifying Company: A company is a qualifying company if: (a) it is an Indian company; (b) the place of effective management (i.e., where decisions take place) of the company is in India; (c) it owns at least one qualifying ship; and (d) the main object of the company is to carry on the business of operating ships.

a valid certificate in respect of such ship indicating its net tonnage is in force, but does not include, (i) a sea going ship or vessel if the main purpose for")

6 CA Final Direct Tax 6 Section 115VD: Qualifying Ship: A ship is a qualifying ship if: (a) it is a sea going ship or vessel of 15 net tones or more; (b) it is a ship registered in India or having licence to operate in India; and (c) a valid certificate in respect of such ship indicating its net tonnage is in force, but does not include, (i) a sea going ship or vessel if the main purpose for which it is used is the provisions of goods or services of a kind normally provided on land; (ii) fishing vessels; (iii) factory ship (iv) pleasure crafts (v) harbor and river ferries; (vi) offshore installations i.e. rigs oil; (vii) a qualifying ship which is used as a fishing vessel for a period of more than thirty days during a previous year. Section 115VG: Computation of Tonnage Income: Tonnage Income from each qualifying ship = Daily tonnage income x No. of days the ship is operated in the previous year Qualifying ship having Amount of Daily tonnage Net tonnage Income Upto, 1, 000 Rs. 70 for each 100 tons Exceeding 1, 000 but not more Rs. 700 plus Rs. 53 for each 100 tons than 10, 000 exceeding 1, 000 tons Exceeding 10, 000 but not more Rs. 5, 470 plus Rs. 42 for each 100 tons than 25, 000 Exceeding 25, 000 exceeding 10, 000 tons Rs. 11, 770 plus Rs. 29 for each 100 tons exceeding 25, 000 tons. Tonnage shall be rounded off to the nearest multiple of 100 tons No deduction or set off of any loss shall be allowed in computing the tonnage income under this Chapter. Section 115VO: Exclusion from Provisions of section 115JB Conversion of an Indian branch of foreign company into an Indian subsidiary company [Chapter XII-BB] [Section 115JG]: If the conditions notified by the Central Government in this behalf are satisfied, then capital gains arising from such conversion would not be chargeable to tax in the assessment year relevant to the previous year in which such conversion takes place. Tax on distributed income of mutual funds [Chapter XII-E]: 115R [+ Surcharge (12%) + Cess (3%)] [Gross up] [14 Days] [Simple Interest 1% Per Month or part thereof]

![2014]: (i) Redemption of units or repurchase of units would not attract levy of tax under section 115R(2) as such income is not in the nature of income distributed to the unit holders and hence, lies](/docs-images/87/96965308/images/7-1.jpg "outside the purview of this section.")

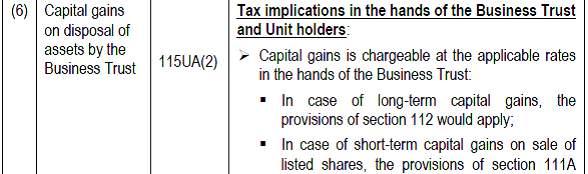

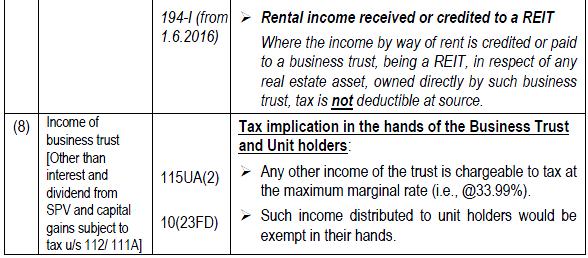

7 CA Final Direct Tax 7 Clarification regarding scope of additional income-tax on distributed income under section 115R [Circular No. 6/2014, dated ]: (i) Redemption of units or repurchase of units would not attract levy of tax under section 115R(2) as such income is not in the nature of income distributed to the unit holders and hence, lies outside the purview of this section. (iii) Since issue of bonus units is not akin to distribution of income by way of dividend, the same would not be subject to additional income tax under section 115R. Levy of additional income-tax on income distributed by securitization trusts [Chapter XII EA] Related Provisions: [115TA, 115TB and 115TC] Section 10(23DA) exempts any income of a securitization trust from the activity of securitization. [+ Surcharge (12%) + Cess (3%)] [14 Days] [Simple Interest 1% Per Month or part thereof] Computation of additional income-tax payable under section 115TA Scheme for taxation of Real Estate Investment Trust (REIT) and Infrastructure Investment Trust (Invit) [Chapter XII-FA Section 115UA]:

8 CA Final Direct Tax 8

9 CA Final Direct Tax 9

10 CA Final Direct Tax 10

![CA Final Direct Tax 11 Special Taxation Regime for Investment Funds [Sections 115UB & 10(23FB)]: The total income of the investment fund is chargeable to tax as follows: Investment Fund Rate of tax A](/docs-images/87/96965308/images/11-0.jpg "company or a firm Rate or rates specified in the Finance Act of the relevant year (30% for A.Y.")

11 CA Final Direct Tax 11 Special Taxation Regime for Investment Funds [Sections 115UB & 10(23FB)]: The total income of the investment fund is chargeable to tax as follows: Investment Fund Rate of tax A company or a firm Rate or rates specified in the Finance Act of the relevant year (30% for A.Y ) Other than a company or a Firm Maximum marginal rate Levy of Alternate Minimum Tax (AMT) on all persons claiming profit-linked deductions, other than companies [Chapter XII-BA Sections 115JC to 115JF]: % of adjusted total income. - Any person other than acompany, who has claimed deduction under any section (other than section 80P) included in Chapter VI-A under the heading C Deductions in respect of certain incomes or under section 10AA would be subject to AMT. - The provisions of AMT would, however, not be applicable to an individual, HUF, AOP, BOI, whether incorporated or not, or artificial juridical person, if the adjusted total income of such person does not exceed Rs. 20 lakh. - Investment-linked tax deduction claimed under section 35AD also falls within the scope of alternate minimum tax. Adjusted total income would mean the total income before giving effect to Chapter XII:BA as increased by the deductions claimed, if any, under: (1) any section (other than section 80P) included in Chapter VI -A under the heading C Deductions in respect of certain incomes ; (2) section 10AA; and (3) section 35AD, as reduced by the depreciation allowable under section 32, as if no deduction under section 35AD was allowed in respect of the asset for which such deduction is claimed. Tax credit for AMT [Section 115JD]: AMT paid in excess of the regular income-tax payable under the provisions of the Income taxact, 1961 for the year would be eligible for credit to be carried forward and set off against income-tax payable in the later year to the extent of excess of regular income-tax payable under the provisions of the Act over the AMT payable in that year. AMT credit can be carried forward for set-off upto a maximum period of 10 assessment years succeeding the assessment year in which the credit becomes allowable.

12 CA Final Direct Tax 12 Assessment of a Individuals: Section 115BB: Gross winnings from lotteries, crossword puzzles, races includinghorse races (other than income from the activity of owning and maintaining racehorses), card games and other games of any sort or from gambling or betting of any nature whatsoever shall be chargeable to income-tax at a flat rate of 30% on the gross winnings. Section 115BBA: Total income of an assessee, (a) being a sportsman (including an athlete), who is not a citizen of India and is a nonresident, includes any income received or receivable by way of participation in any game or sport or advertisement or contribution of articles in relation to any game or sport in India in newspapers, magazines, journals. (b) being a non-resident sports association or institution, includes any amount guaranteed to be paid or payable to such association or institution in relation to any game or sport played in India. (c) being an entertainer, who is not a citizen of India and is a non-resident, includes any income received or receivable from his performance in India. The income-tax payable on above: 20% (No deduction) (No ROI if above only income & TDS ) Special provisions relating to certain incomes of non-residents - Chapter XII A: - Concessional method of taxation of certain specified income of non-residents Indian. - Foreign exchange asset means any specified asset which the assessee has acquired, purchased with or subscribed to in convertible foreign exchange. Such specified assets are as follows: (a) shares in an Indian company. (b) debentures issued by an Indian company which is not a private company as defined in the Companies Act, (c) deposits with a non-private Indian company. (d) any specified securities of Central Government. (e) units of the Unit Trust of India. Section 115E: Income-tax on investment income at the rate of 20%; Income-tax on long-term capital gains at the rate of 10% Section 115F: Where the non-resident Indian transfers the original foreign exchange asset and within a period of six months of such a transfer deposits or invests the whole or part of the net consideration in: (a) any specified asset or (b) any notified savings certificates referred to in section 10(4B) then, the capital gains arising on such a transfer will be dealt with as follows : If the cost of the new asset, referred to in (a) or (b) above, is not less than the net consideration in respect of the original asset the whole of such capital gain shall be exempt. If such cost is less than the net consideration, the exemption will be limited to: Total capital gain x Cost of new asset Net Consideration Where the new asset is transferred or converted (otherwise than by transfer) into money, within a period of three years from the date of its acquisition, the capital gain, exempted as above, shall be chargeable as long term capital gain of the previous year in which the new asset is transferred or converted. (No ROI if above only income & TDS )

13 CA Final Direct Tax 13 Assessment of Hindu Undivided Families: HUF consists of all males lineally descended from a common ancestor and includes their wives and daughters. The relation of a HUF does not arise from a contract but arises from status. Some members of the HUF are called co-parceners. A Hindu Coparcenary includes those persons who acquire an interest in joint family property by birth. It may be noted that only the coparceners have a right to partition. However, other female members of the family, for example, wife or daughter -in-law of a coparcener are not eligible for such coparcenary rights. The income of a HUF is to be assessed in the hands of the HUF and not in the hands of any of its members. This is because HUF is a separate and a distinct tax entity. Partition of HUF There are two types of partition. They are: (1) Total partition is a partition by which the entire family property is divided amongst the coparceners. After the total partition, the HUF ceases to exist as such. When a claim of total partition of HUF has been made by any member of the HUF on behalf of the HUF, the Assessing Officer shall inquire into such claim. If partition has been effected in the previous year, the total income of the HUF for the previous year up to the date of partition shall be assessed as income of the HUF. Every member of the HUF is jointly and severally liable for payment of tax on such assessed income of the HUF. The several liability of a member would be proportionate to the share of joint family property allotted to him on such partition. (2) Partial partition is a partition which is partial as regards either the persons constituting the joint family or as regards the properties belonging to the joint family or both. However, partial partitionsare not recognized for tax purposes. Such family will continue to be assessed as if no such partial partition has been effected. Every member of the HUF, immediately before such partial partition, and the HUF shall be jointly and severally liable for any sum payable under the Act. The several liability of a member would be proportionate to the share of joint family property allotted to him on such partial partition. Where the funds of a HUF are invested in a company or a partnership firm, the dividends or share of profits are generally taxable as the income of the family. In such a case the fee, salary, commission or other remuneration received by the Karta, or any member of the family, in his capacity as director or partner would also be taxable as income of the family. The reasons for this treatment are as follows: (1) The income is earned by the detriment to the joint family funds. (2) It is earned with the aid of joint family funds. (3) There is real and sufficient connection between the investment of the joint family funds and the income by way of remuneration earned. However, where the income is earned by the karta or any other member of the family by the exercise of the personal skill the income should be assessed in their individual hands even if some detriment is caused to the family funds, say, by way of loan, guarantee etc. whose role is only secondary.

14 CA Final Direct Tax 14 Salary paid to Karta for managing the family s business: If remuneration is paid to the Karta of Hindu undivided family under a valid agreement which is bona fide and in the interest of and expedient for the business of the family and the payment is genuine and not excessive, such remuneration would be an expenditure laid out wholly and exclusively for the purpose of the business of the family and would be allowable as an expenditure. Salary paid to member: A Hindu undivided family can be allowed to deduct salaries paid to member of the family if the payment is made as a matter of commercial or business expediency, but the service rendered must be to the family. Assessment of firms/llps and their partners: Partnership Firm Assessed As Such (PFAS) [Section 184]: Conditions to be fulfilled: (i) Firm should be evidenced by an instrument. (ii) Individual shares of partners must be specified in the instrument. (iii) Certified copy of the instrument should accompany the first return of income of a firm. Instrument shall be certified in writing by all partners other than minors. (iv) If there is any change in the constitution of the firm or profit -sharing ratio during any previous year, a certified copy of the revised instrument of partnership should be filed along with the return of income of the relevant assessment year. Section 167C: In case of liquidation of an LLP, where tax due from the LLP cannot be recovered, every person who was a partner of the LLP at any time during the relevant previous year will be jointly and severally liable for payment of tax unless he proves that non-recovery cannot be attributed to any gross neglect, misfeasance or breach of duty on his part in relation to the affairs of the LLP. Conversion of company into a LLP: Section 47(xiiib) provides that: (1) any transfer of a capital asset or intangible asset by a private company or unlisted public company to a LLP; or (2) any transfer of a share or shares held in a company by a shareholder on conversion of a company into a LLP in accordance with section 56 and section 57 of the Limited Liability Partnership Act, 2008, shall not be regarded as a transfer for the purposes of levy of capital gains tax under section 45, subject to fulfillment of certain conditions. Further, the successor LLP would be allowed to carry forward and set-off the business loss and unabsorbed depreciation of the predecessor company [Section 72A(6A)]. These conditions are as follows: (1) the total sales, turnover or gross receipts in business of the company should not exceed Rs. 60 lakh in any of the three preceding previous years; (2) the shareholders of the company become partners of the LLP in the same proportion as their shareholding in the company; (3) no consideration other than share in profit and capital contribution in the LLP arises to the shareholders; (4) the erstwhile shareholders of the company continue to be entitled to receive at least 50% of the profits of the LLP for a period of 5 years from the date of conversion;

15 CA Final Direct Tax 15 (5) all assets and liabilities of the company become the assets and liabilities of the LLP; and (6) no amount is paid, either directly or indirectly, to any partner out of the accumulated profit of the company for a period of 3 years from the date of conversion. However, if subsequent to the transfer, any of the above conditions are not complied with, the capital gains not charged under section 45 would be deemed to be chargeable to tax in the previous year in which the conditions are not complied with, in the hands of the LLP or the shareholder of the predecessor company, as the case may be [Section 47A(4)]. The tax credit under section 115JAA for MAT paid by the company under section 115JB would not be allowed to the successor LLP [Sub-section (7) of section 115JAA]. The aggregate depreciation allowable to the Predecessor Company and successor LLP shall not exceed, in any previous year, the depreciation calculated at the prescribed rates as if the conversion had not taken place. Such depreciation shall be apportioned between the predecessor company and the successor LLP in the ratio of the number of days for which the assets were used by them [Section 32(1)]. Computation of total income of AOP/BOI and PFAOP [Section 67A]: In computing the total income, salary, bonus, commission, remuneration or interest paid to partners/members will not be allowed. However in the case of payment of interest the following provisions will apply: Explanation 1: If interest is paid by an AOP/BOI to any member who was also paid interest to the AOP/BOI then only that amount of interest paid by the AOP/BOI will be disallowed in its assessment which is in excess of the interest paid by the member to the AOP/BOI. Explanation 2: If an individual is a member of an AOP/BOI in a representative capacity, then interest paid by the AOP/BOI to such individual in his personal capacity the interest payment will be allowed. Explanation 3: If interest is paid to a member who is member in a personal capacity but such interest is received by him in representative capacity, the interest payment will be allowed. Computation of tax where shares of members in AOP/BOI are unknown [Section 167B]: Tax on the total income would be computed as follows: - If individual share of any partner is not known, tax will be levied at the maximum marginal rate, or at a higher rate. - If individual share of a partner is known but total income of any member/partner exceeds the basic exemption limit, then the firm will pay tax at the maximum marginal rate. - If individual share of a partner is known and no member/partner has total income exceeding the basic exemption limit, the firm will pay tax at the rates applicable to an individual. Computation of member s/partner s share in the total income of association of persons/aop firm [Section 67A]: A member s share in the income of an association of persons/aop firm (wherein the shares of members are determinate/known) will be computed as follows: (a) Any interest, salary, bonus, commission, remuneration, etc. paid to a member/ partner during the previous year will be deducted from the total income of the association, and the balance will be apportioned among the members in proportion to their respective shares. (b) If the amount apportioned to a member/partner as per (a) is a profit, any interest, salary, etc. paid to him by the association or AOP firm during the previous year will be added to

16 CA Final Direct Tax 16 that amount and the aggregate sum will be such member s/partner s share in the income of the AOP/AOP firm. (c) If the amount apportioned to a member/partner as per (a) is a loss, any interest, salary, etc., paid to him by the association or AOP firm will be deducted from the amount of loss and the balance sum will be such member s/partner s share in the income of the AOP/AOP firm. The share of a member in the income/loss of the AOP/AOP firm will, for the purposes of assessment, be apportioned under the various heads of income in the same manner in which income/loss of the association has been determined under each head. Any interest paid by a member on capital borrowed by him for the purpose of investment in the AOP/AOP firm will be allowed as deduction from share while computing his income under Profits and gains of business or profession. Assessment of share in the hands of member/partner [Section 86]: - A member s/partner s share in the total income of an association of persons/aop firm will be treated as follows: - If an AOP/AOP firm has paid tax at the maximum marginal rate, or a higher rate, the partner s share in the total income of the firm will not be included in his total income and will be exempt. - If the AOP/AOP firm has paid tax at regular rates applicable to an individual, the member s/partner s share in the income of the association/aop firm will be included in his total income for rate purposes only. In other words, the member/partner will be allowed rebate at the average rate in respect of such share. If the AOP/AOP firm has not paid tax on its total income, the member s/partner s share in the total income of the association/aop firm will be included in his total income and taxed at regular rates.

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

13 Assessment of Various Entities

13 Assessment of Various Entities 13.1 Assessment of Companies 13.1.1 Meaning of Company for purposes of income-tax: Under the Income-tax Act, 1961, the term company has a much wider meaning than what

13 Assessment of Various Entities 13.1 Assessment of Companies 13.1.1 Meaning of Company for purposes of income-tax: Under the Income-tax Act, 1961, the term company has a much wider meaning than what

THE FINANCE BILL, 2015

BILL No. 26 OF THE FINANCE BILL, (AS INTRODUCED IN LOK SABHA) THE FINANCE BILL, ARRANGEMENT OF CLAUSES CHAPTER I PRELIMINARY CLAUSES 1. Short title and commencement. CHAPTER II RATES OF INCOME-TAX 2. Income-tax.

BILL No. 26 OF THE FINANCE BILL, (AS INTRODUCED IN LOK SABHA) THE FINANCE BILL, ARRANGEMENT OF CLAUSES CHAPTER I PRELIMINARY CLAUSES 1. Short title and commencement. CHAPTER II RATES OF INCOME-TAX 2. Income-tax.

CA Final Course Chapter 7 Direct Tax Laws Chapter 13 Unit 2 Rajendra Prasad Talluri B.Com; CA; Grad CWA

CA Final Course Chapter 7 Direct Tax Laws Chapter 13 Unit 2 Rajendra Prasad Talluri B.Com; CA; Grad CWA Meaning: Person includes an Individual [Sec (2(31)] ; And the term individual has not been defined

CA Final Course Chapter 7 Direct Tax Laws Chapter 13 Unit 2 Rajendra Prasad Talluri B.Com; CA; Grad CWA Meaning: Person includes an Individual [Sec (2(31)] ; And the term individual has not been defined

13 ASSESSMENT OF VARIOUS ENTITIES

13 ASSESSMENT OF VARIOUS ENTITIES AMENDMENTS BY THE FINANCE ACT, 2015 (a) Special Taxation Regime for Investment Funds [Sections 115UB & 10(23FB)] Related amendment in sections: 115U, 139 & 194LBB (i)

13 ASSESSMENT OF VARIOUS ENTITIES AMENDMENTS BY THE FINANCE ACT, 2015 (a) Special Taxation Regime for Investment Funds [Sections 115UB & 10(23FB)] Related amendment in sections: 115U, 139 & 194LBB (i)

CA Final Direct taxes Flow charts May 2017

CA Final Direct taxes Flow charts May 2017 Amended by FA 2016 Along with all important circulars and notifications up to 31.10.2016 CA N. Rajasekhar M.com FCA DISA (ICAI) Chennai. 9444019860 rajdhost@yahoo.com

CA Final Direct taxes Flow charts May 2017 Amended by FA 2016 Along with all important circulars and notifications up to 31.10.2016 CA N. Rajasekhar M.com FCA DISA (ICAI) Chennai. 9444019860 rajdhost@yahoo.com

EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE ACT, 2013

CIRCULAR NO.03/2014 F. No. 142/24/2013-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) ******* Dated, the 24 th January, 2013 EXPLANATORY NOTES TO THE

CIRCULAR NO.03/2014 F. No. 142/24/2013-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) ******* Dated, the 24 th January, 2013 EXPLANATORY NOTES TO THE

SURENDER KR. SINGHAL & CO

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

FINANCE (NO.2) ACT, 2014 EXPLANATORY NOTES TO THE PROVISIONS OF SAID ACT AMENDMENTS AT A GLANCE

ACT, 2014 EXPLANATORY NOTES TO THE PROVISIONS OF SAID ACT AMENDMENTS AT A GLANCE") FINANCE (NO.2) ACT, 2014 EXPLANATORY NOTES TO THE PROVISIONS OF SAID ACT Section/Schedule CIRCULAR NO.1/2015 [F.NO.142/13/2014 TPL], DATED 21 1 2015 AMENDMENTS AT A GLANCE Finance (No.2) Act, 2014 First

FINANCE (NO.2) ACT, 2014 EXPLANATORY NOTES TO THE PROVISIONS OF SAID ACT Section/Schedule CIRCULAR NO.1/2015 [F.NO.142/13/2014 TPL], DATED 21 1 2015 AMENDMENTS AT A GLANCE Finance (No.2) Act, 2014 First

EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE(No.2) ACT, 2014

ACT, 2014") CIRCULAR NO. 01/2015 F. No. 142/13/2014-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) ******* Dated, the 21st January, 2015 EXPLANATORY NOTES TO THE

CIRCULAR NO. 01/2015 F. No. 142/13/2014-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) ******* Dated, the 21st January, 2015 EXPLANATORY NOTES TO THE

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

(A) received from the Government in pursuance of an agreement made by the non-resident/ foreign company with the Government, or

received from the Government in pursuance of an agreement made by the non-resident/ foreign company with the Government, or") Section 115A - 10% on Royalty and FTS Where the total income of a foreign company or a non-resident includes any income by way of royalty or fees for technical services other than the income referred to

Section 115A - 10% on Royalty and FTS Where the total income of a foreign company or a non-resident includes any income by way of royalty or fees for technical services other than the income referred to

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment

INTRODUCTION WHO IS LIABLE TO PAY MAT

CONTENTS I-9 Chapter-heads I-5 DIVISION ONE MINIMUM ALTERNATE TAX (MAT) 1 INTRODUCTION 1.1 History of Minimum Alternate Tax (MAT) 3 1.2 Rationale for MAT 4 1.3 Salient features of MAT Regime u/s 115JB

CONTENTS I-9 Chapter-heads I-5 DIVISION ONE MINIMUM ALTERNATE TAX (MAT) 1 INTRODUCTION 1.1 History of Minimum Alternate Tax (MAT) 3 1.2 Rationale for MAT 4 1.3 Salient features of MAT Regime u/s 115JB

FINAL CA May 2018 DIRECT TAXATION

FINAL CA May 2018 DIRECT TAXATION Test Code F 90 Branch: MULTIPLE Date: (50 Marks) compulsory. Note: All questions are Question 1 (10 marks) Computation of Book Profit for levy of MAT under section 115JB

FINAL CA May 2018 DIRECT TAXATION Test Code F 90 Branch: MULTIPLE Date: (50 Marks) compulsory. Note: All questions are Question 1 (10 marks) Computation of Book Profit for levy of MAT under section 115JB

1.1 Overview of income-tax law in India

1 Basic Concepts 1.1 Overview of income-tax law in India Income-tax is a tax levied on the total income of the previous year of every person. A person includes an individual, Hindu Undivided Family (HUF),

1 Basic Concepts 1.1 Overview of income-tax law in India Income-tax is a tax levied on the total income of the previous year of every person. A person includes an individual, Hindu Undivided Family (HUF),

DEDUCTION, COLLECTION AND RECOVERY OF TAX

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

Budget 2018 An overview. CA C Ramadurai FCA Membership no Chartered Accountant

Budget 2018 An overview Membership no 027220 Chartered Accountant Finance Bill 2018 Analysis of Direct Tax amendments By CA Chandrasekaran Ramadurai M.Com; FCA; ACMA Chartered Accountant Insolvency Professional

Budget 2018 An overview Membership no 027220 Chartered Accountant Finance Bill 2018 Analysis of Direct Tax amendments By CA Chandrasekaran Ramadurai M.Com; FCA; ACMA Chartered Accountant Insolvency Professional

A BILL to give effect to the financial proposals of the Central Government for the financial year

FINANCE BILL, 2012* Bill No. 11 of 2012 A BILL to give effect to the financial proposals of the Central Government for the financial year 2012-2013. BE it enacted by Parliament in the Sixty-third Year

FINANCE BILL, 2012* Bill No. 11 of 2012 A BILL to give effect to the financial proposals of the Central Government for the financial year 2012-2013. BE it enacted by Parliament in the Sixty-third Year

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

UNDERSTANDING-- TAXATION SYSTEM

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 3 5 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The outer effects affecting

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 3 5 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The outer effects affecting

Income Tax Act DIVISION ONE 1 DIVISION TWO 2

Income Tax Act SECTION DIVISION ONE 1 Income-tax Act, 1961 Arrangement of Sections I-3 Text of the Income-tax Act, 1961 as amended by the Finance (No. 2) Act, 2014 1.1 Appendix : Text of remaining provisions

Income Tax Act SECTION DIVISION ONE 1 Income-tax Act, 1961 Arrangement of Sections I-3 Text of the Income-tax Act, 1961 as amended by the Finance (No. 2) Act, 2014 1.1 Appendix : Text of remaining provisions

CA Final Paper 7 Direct Tax Laws Ch13 Unit1 CA Sudhindra Kumar Jain

CA Final Paper 7 Direct Tax Laws Ch13 Unit1 CA Sudhindra Kumar Jain 2 Definition Section 2(17) In Which Public Are Substantially Interested Section 2(18) Indian Company Section 2(26) Domestic Company Section

CA Final Paper 7 Direct Tax Laws Ch13 Unit1 CA Sudhindra Kumar Jain 2 Definition Section 2(17) In Which Public Are Substantially Interested Section 2(18) Indian Company Section 2(26) Domestic Company Section

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba 1. Power to impose income tax on agriculture income is with a) Central government b) State government c) Partly with central government and partly with state

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba 1. Power to impose income tax on agriculture income is with a) Central government b) State government c) Partly with central government and partly with state

Tax deducted at source For the Financial year

Tax deducted at source For the Financial year 2016-17 A summary list of tax deductible from a resident, a nonresident and other persons CA K. Balachandran FCA, Coimbatore TDS summary for the AY 2017-18

Tax deducted at source For the Financial year 2016-17 A summary list of tax deductible from a resident, a nonresident and other persons CA K. Balachandran FCA, Coimbatore TDS summary for the AY 2017-18

Brief Note on Provisions of Section 194A(3)(v) relating to Co-operative Banks

(v) relating to Co-operative Banks") Brief Note on Provisions of Section 194A(3)(v) relating to Co-operative Banks Section 194A of the Income-tax Act, 1961 ( the Act ) was introduced through the Finance Act, 1967 with effect from 1 st April,

Brief Note on Provisions of Section 194A(3)(v) relating to Co-operative Banks Section 194A of the Income-tax Act, 1961 ( the Act ) was introduced through the Finance Act, 1967 with effect from 1 st April,

J.M.PATEL COLLEGE OF COMMERCE 1

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 Taxation 2 3 5 4 6 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 Taxation 2 3 5 4 6 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The

1

TAX & LEGAL & GENERAL INFORMATION A. Taxation on investing in Mutual Funds As per the taxation laws in force as at the date of this Scheme Information Document and the enactment of Finance Bill 2008,,the

TAX & LEGAL & GENERAL INFORMATION A. Taxation on investing in Mutual Funds As per the taxation laws in force as at the date of this Scheme Information Document and the enactment of Finance Bill 2008,,the

Finance Bill, 2015 Direct Tax Highlights

Finance Bill, 2015 Direct Tax Highlights Bansi S. Mehta & Co. All the following amendment are made effective from Assessment Years 2016-17, unless specifically mentioned otherwise. I - Residential Status,

Finance Bill, 2015 Direct Tax Highlights Bansi S. Mehta & Co. All the following amendment are made effective from Assessment Years 2016-17, unless specifically mentioned otherwise. I - Residential Status,

INCOME TAX. -COPY OF- CIRCULAR NO.19/2015 Dated 27 th November, 2015

INCOME TAX -COPY OF- CIRCULAR NO.19/2015 Dated 27 th November, 2015 F.No.142/14/2015-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) New Delhi ** ** **

INCOME TAX -COPY OF- CIRCULAR NO.19/2015 Dated 27 th November, 2015 F.No.142/14/2015-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) New Delhi ** ** **

Major direct tax proposals in Finance Bill, 2017

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

ARTICLE. On Finance Bill (Budget) Proposals 2013 Income Tax Act, 1961 By CA. SATISH AGARWAL

Proposals 2013 Income Tax Act, 1961 By CA. SATISH AGARWAL") ARTICLE On Finance Bill (Budget) Proposals 0 Income Tax Act, 96 By CA. SATISH AGARWAL Mobile : +99808957 Phone : +95769 Office : 9/4, East Patel Nagar, (Near Jaypee Sidharthe Hotel) New Delhi - 0008 :

ARTICLE On Finance Bill (Budget) Proposals 0 Income Tax Act, 96 By CA. SATISH AGARWAL Mobile : +99808957 Phone : +95769 Office : 9/4, East Patel Nagar, (Near Jaypee Sidharthe Hotel) New Delhi - 0008 :

INTRODUCTION OF TAX PLANNING

INTRODUCTION OF TAX PLANNING UNIT 1 STRUCTURE OF THE CHAPTER 1.1 Introduction 1.2 Meaning of Planning 1.3 Meaning of Management 1.4 Meaning of Evasion 1.5 Meaning of Avoidance 1.6 Basics 1.7 Summary 1.8

INTRODUCTION OF TAX PLANNING UNIT 1 STRUCTURE OF THE CHAPTER 1.1 Introduction 1.2 Meaning of Planning 1.3 Meaning of Management 1.4 Meaning of Evasion 1.5 Meaning of Avoidance 1.6 Basics 1.7 Summary 1.8

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

1 Taxation of Individuals,

1 Taxation of Individuals, Partnership Firms/LLP and Companies! Basic Concepts and Taxation of Individuals! Taxation of Companies. This Chapter includes! Taxation of Firm/Limited Liability Partnership

1 Taxation of Individuals, Partnership Firms/LLP and Companies! Basic Concepts and Taxation of Individuals! Taxation of Companies. This Chapter includes! Taxation of Firm/Limited Liability Partnership

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and

![thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and](/thumbs/74/69854896.jpg "thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and") ACT FINANCE ACT *Finance Act, 2011 [8 OF 2011] An Act to give effect to the financial proposals of the Central Government for the financial year 2011-2012. BE it enacted by Parliament in the Sixty-second

ACT FINANCE ACT *Finance Act, 2011 [8 OF 2011] An Act to give effect to the financial proposals of the Central Government for the financial year 2011-2012. BE it enacted by Parliament in the Sixty-second

Capital gains. 45. (1) Any profits or gains arising from the transfer of a capital asset effected in the previous year shall, save as otherwise

Any profits or gains arising from the transfer of a capital asset effected in the previous year shall, save as otherwise") Capital gains. 45. (1) Any profits or gains arising from the transfer of a capital asset effected in the previous year shall, save as otherwise provided in sections 54, 54B, 54D, 54E, 54EA, 54EB, 54F,

Capital gains. 45. (1) Any profits or gains arising from the transfer of a capital asset effected in the previous year shall, save as otherwise provided in sections 54, 54B, 54D, 54E, 54EA, 54EB, 54F,

TAX RECKONER

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

FINANCE BILL He has proposed to revise the tax slabs upwards as under:

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

Web:

PRESENTED ON 1st FEB 2017 HIGHLIGHTS 1 A Rates of Income-tax Rates of income-tax in respect of income liable to tax for the assessment year 2017-18. Rates for deduction of income-tax at source during the

PRESENTED ON 1st FEB 2017 HIGHLIGHTS 1 A Rates of Income-tax Rates of income-tax in respect of income liable to tax for the assessment year 2017-18. Rates for deduction of income-tax at source during the

Appeal, Set comm., DRP Etc Mock Test IGP-CS CA Vivek Gaba

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

Circular The Schedule of dates for filing income-tax returns is given below:

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Total turnover/ Gross receipts 30% 30% of FY > Rs 50 Cr No change in rate of Surcharge

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

MINISTRY OF LAW AND JUSTICE (Legislative Department)

") MINISTRY OF LAW AND JUSTICE (Legislative Department) New Delhi, the 28th May, 2012/Jyaistha 7, 1934 (Saka) The following Act of Parliament received the assent of the President on the 28th May, 2012 and

MINISTRY OF LAW AND JUSTICE (Legislative Department) New Delhi, the 28th May, 2012/Jyaistha 7, 1934 (Saka) The following Act of Parliament received the assent of the President on the 28th May, 2012 and

Chapter 8 Income under the Head "Income from Other Sources"

Chapter 8 Income under the Head "Income from Other Sources" 1. Basis of Charge Section 56(1) Income of every kind which is not exempt shall be chargeable to income-tax under the head "Income from Other

Chapter 8 Income under the Head "Income from Other Sources" 1. Basis of Charge Section 56(1) Income of every kind which is not exempt shall be chargeable to income-tax under the head "Income from Other

Income Tax Changes made in Income Tax Provisions in the Union Budget which would affect Salaried Class

Income Tax 2013-14 Changes made in Income Tax Provisions in the Union Budget 2013-14 which would affect Salaried Class A. RATES OF INCOME-TAX I. Rates of income-tax in respect of income liable to tax for

Income Tax 2013-14 Changes made in Income Tax Provisions in the Union Budget 2013-14 which would affect Salaried Class A. RATES OF INCOME-TAX I. Rates of income-tax in respect of income liable to tax for

Rates of Taxes. Rates for deduction of Income

CA Mohan S. Phadke Rates of Taxes I. Rates of Income Tax in respect of income liable to tax for the assessment year 2013-14 a) In respect of income of all categories of assessees liable to tax for the

CA Mohan S. Phadke Rates of Taxes I. Rates of Income Tax in respect of income liable to tax for the assessment year 2013-14 a) In respect of income of all categories of assessees liable to tax for the

FINANCE ACT, EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE ACT, Explanatory notes to the provisions of the Finance Act, 2011

FINANCE ACT, 2011 - EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE ACT, 2011 CIRCULAR NO. 02/2012 [F. NO.142/01/2012-SO(TPL)], DATED 22-5-2012 Explanatory notes to the provisions of the Finance Act,

FINANCE ACT, 2011 - EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE ACT, 2011 CIRCULAR NO. 02/2012 [F. NO.142/01/2012-SO(TPL)], DATED 22-5-2012 Explanatory notes to the provisions of the Finance Act,

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y. 2013-2014 AMENDMENTS IN FINANCE ACT, 2012 HAVING IMPACT ON TAX AUDIT REPORT Rule 12 From A.Y. 2013-14 inter-alia e-filing of Audit Reports u/s. 44AB (Tax Audit

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y. 2013-2014 AMENDMENTS IN FINANCE ACT, 2012 HAVING IMPACT ON TAX AUDIT REPORT Rule 12 From A.Y. 2013-14 inter-alia e-filing of Audit Reports u/s. 44AB (Tax Audit

Finance (No. 2) Bill 2014

Bill 2014") Finance (No. 2) Bill 2014 Proposed Income Tax Amendments Mr. R.N. LAKHOTIA Leading Income Tax Consultant & Author The Finance Minister presented the Finance (No.2) Bill 2014 along with the Union Budget

Finance (No. 2) Bill 2014 Proposed Income Tax Amendments Mr. R.N. LAKHOTIA Leading Income Tax Consultant & Author The Finance Minister presented the Finance (No.2) Bill 2014 along with the Union Budget

8 Income from other Sources

8 Income from other Sources 8.1 Introduction Any income, profits or gains includible in the total income of an assessee, which cannot be included under any of the preceding heads of income, is chargeable

8 Income from other Sources 8.1 Introduction Any income, profits or gains includible in the total income of an assessee, which cannot be included under any of the preceding heads of income, is chargeable

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

THE FINANCE BILL, 2011

Bill No. 8-F of 2011 THE FINANCE BILL, 2011 (AS PASSED BY THE HOUSES OF PARLIAMENT LOK SABHA ON 22ND MARCH, 2011 RAJYA SABHA ON 24TH MARCH, 2011) ASSENTED TO ON 8TH APRIL, 2011 ACT NO. 8 OF 2011 Bill No.

Bill No. 8-F of 2011 THE FINANCE BILL, 2011 (AS PASSED BY THE HOUSES OF PARLIAMENT LOK SABHA ON 22ND MARCH, 2011 RAJYA SABHA ON 24TH MARCH, 2011) ASSENTED TO ON 8TH APRIL, 2011 ACT NO. 8 OF 2011 Bill No.

Executive Summary of Finance Bill, 2014 Direct Taxes

* The applicable date being denotes the amendment is applicable w.e.f. A.Y. 2015-16 CLAUSE NO. OF FINANCE BILL SECTION NEW LAW APPLICABLE w.e.f.* BRIEF OF AMENDMENT 2 Tax Slabs Changes for Individual,

* The applicable date being denotes the amendment is applicable w.e.f. A.Y. 2015-16 CLAUSE NO. OF FINANCE BILL SECTION NEW LAW APPLICABLE w.e.f.* BRIEF OF AMENDMENT 2 Tax Slabs Changes for Individual,

Salient features of Direct Tax Proposals of Union Budget 2011

Salient features of Direct Tax Proposals of Union Budget 2011 RATES OF INCOME-TAX FOR THE ASSESSMENT YEAR 2012-13 o Tax slab rates have been changed for individuals and HUF, which is given by way of a

Salient features of Direct Tax Proposals of Union Budget 2011 RATES OF INCOME-TAX FOR THE ASSESSMENT YEAR 2012-13 o Tax slab rates have been changed for individuals and HUF, which is given by way of a

1. Tax on accumulated balance of recognised provident fund 111 To be computed in accordance with rule 9(1) of Part A of fourth Schedule 2. Short term

of Part A of fourth Schedule 2. Short term") Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Issues in Taxation of Income (Non-Corporate)

") Issues in Taxation of Income (Non-Corporate) By CA Mahavir Jain B.Com.; DISA; FCA Partner : JMT & Associates Email: jmtca301@gmail.com Issues in Taxation of Non-Corporate Income is a very vast subject.

Issues in Taxation of Income (Non-Corporate) By CA Mahavir Jain B.Com.; DISA; FCA Partner : JMT & Associates Email: jmtca301@gmail.com Issues in Taxation of Non-Corporate Income is a very vast subject.

Paper 4: Taxation. Section A: Income-tax Law. Applicability of the Finance Act, Assessment Year etc. for November, 2018 Examination

Paper 4: Taxation Section A: Income-tax Law Applicability of the Finance Act, Assessment Year etc. for November, 2018 Examination The provisions of income-tax law, as amended by the Finance Act, 2017,

Paper 4: Taxation Section A: Income-tax Law Applicability of the Finance Act, Assessment Year etc. for November, 2018 Examination The provisions of income-tax law, as amended by the Finance Act, 2017,

Chapter - 7 Income under the Head "Capital Gains"

Chapter - 7 Income under the Head "Capital Gains" Basis of Charge Section 45(1) Any profits or gains arising from the transfer of a capital asset effected in the previous year, shall be chargeable to income-tax

Chapter - 7 Income under the Head "Capital Gains" Basis of Charge Section 45(1) Any profits or gains arising from the transfer of a capital asset effected in the previous year, shall be chargeable to income-tax

1 APPLICABILITY OF MAT

CONTENTS Chapter-heads I-5 MAT/AMT Ready Reckoner I-21 DIVISION ONE MINIMUM ALTERNATE TAX (MAT) 1 APPLICABILITY OF MAT 1.1 History of Minimum Alternate Tax (MAT) 3 1.1-1 Comparative study of sections 115J,

CONTENTS Chapter-heads I-5 MAT/AMT Ready Reckoner I-21 DIVISION ONE MINIMUM ALTERNATE TAX (MAT) 1 APPLICABILITY OF MAT 1.1 History of Minimum Alternate Tax (MAT) 3 1.1-1 Comparative study of sections 115J,

TAMIL NADU GENERATION AND DISTRIBUTION CORPORATION LIMITED (ACCOUNTS BRANCH) 144, Anna Salai, (2 copies each for Accounts and

144, Anna Salai, (2 copies each for Accounts and") INCOME TAX SPECIAL TAMIL NADU GENERATION AND DISTRIBUTION CORPORATION LIMITED (ACCOUNTS BRANCH) From To K.Sundaravadhanam, B.Sc., ACA., ACS., All Superintending Engineers, Chief Financial Controller/General,

INCOME TAX SPECIAL TAMIL NADU GENERATION AND DISTRIBUTION CORPORATION LIMITED (ACCOUNTS BRANCH) From To K.Sundaravadhanam, B.Sc., ACA., ACS., All Superintending Engineers, Chief Financial Controller/General,

1 Taxation of Individuals, Partnership Firms/LLP and Companies

1 Taxation of Individuals, Partnership Firms/LLP and Companies Basic Concepts and Taxation of Individuals Taxation of Companies. This Chapter includes Taxation of Firm/Limited Liability Partnership (LLP)

1 Taxation of Individuals, Partnership Firms/LLP and Companies Basic Concepts and Taxation of Individuals Taxation of Companies. This Chapter includes Taxation of Firm/Limited Liability Partnership (LLP)

Instructions for filling out FORM ITR-3

Instructions for filling out FORM ITR-3 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-3 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Notes on clauses.

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

Income Ta Income Tax (A.Y (A.Y )

") 1 Income Tax (A.Y. 2011-12) 12) What is a Finance Bill? a) The Finance Bill incorporates all the financial proposals of the Government for the following year. b) It is ordinarily introduced in the Lok

1 Income Tax (A.Y. 2011-12) 12) What is a Finance Bill? a) The Finance Bill incorporates all the financial proposals of the Government for the following year. b) It is ordinarily introduced in the Lok

RECENT AMENDMENTS COMPUTATION OF TAX HOW TO COMPUTE REGULAR TAX

RECENT AMENDMENTS The amendments as applicable to AY 2014-15 are given below. These amendments have been incorporated at all relevant places in this book. For any clarification / suggestion, please feel

RECENT AMENDMENTS The amendments as applicable to AY 2014-15 are given below. These amendments have been incorporated at all relevant places in this book. For any clarification / suggestion, please feel

DIRECT TAX Every bit and piece of my work is dedicated to every sleepless night my mother has spent for me

Part A DIRECT TAX Every bit and piece of my work is dedicated to every sleepless night my mother has spent for me INDEX of Income Tax Amendments by FA, 2016 Chapter 1: Basic Concepts Particulars Rates

Part A DIRECT TAX Every bit and piece of my work is dedicated to every sleepless night my mother has spent for me INDEX of Income Tax Amendments by FA, 2016 Chapter 1: Basic Concepts Particulars Rates

Assessment Year

Assessment Year 2016-2017 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources Individual/HUF Firm Company Trust AOP/BOI/Co-op

Assessment Year 2016-2017 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources Individual/HUF Firm Company Trust AOP/BOI/Co-op

INCOME-TAX AND BASED ON FINANCE ACT, FINANCE ACT, 2007 WITH NOTES 49 I.T. NOTES 69 I.T. NOTES 97 I.T. NOTES I.T. NOTES 139 I.T.

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

Rates for tax deduction at source (TDS)

") Rates for tax deduction at source (TDS) [For Assessment year 18-19] Particulars 1. In the case of a person other than a company 1.1 where the person is resident in India- Section 192: Payment of salary

Rates for tax deduction at source (TDS) [For Assessment year 18-19] Particulars 1. In the case of a person other than a company 1.1 where the person is resident in India- Section 192: Payment of salary

MTP_ Final _Syllabus 2016_ June 2017_Set 2 Paper 16 Direct Tax Laws And International Taxation

Paper 16 Direct Tax Laws And International Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 16 Direct Tax Laws and International

Paper 16 Direct Tax Laws And International Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 16 Direct Tax Laws and International

DIRECT TAX LAWS AND INTERNATIONAL TAXATION

SYLLABUS - 2016 FINAL : PAPER - 16 DIRECT TAX LAWS AND INTERNATIONAL TAXATION FINAL STUDY NOTES The Institute of Cost Accountants of India CMA Bhawan, 12, Sudder Street, Kolkata - 700 016 First Edition

SYLLABUS - 2016 FINAL : PAPER - 16 DIRECT TAX LAWS AND INTERNATIONAL TAXATION FINAL STUDY NOTES The Institute of Cost Accountants of India CMA Bhawan, 12, Sudder Street, Kolkata - 700 016 First Edition

INTERMEDIATE (IPC) COURSE/ ACCOUNTING TECHNICIAN COURSE SUPPLEMENTARY STUDY PAPER TAXATION

COURSE/ ACCOUNTING TECHNICIAN COURSE SUPPLEMENTARY STUDY PAPER TAXATION") INTERMEDIATE (IPC) COURSE/ ACCOUNTING TECHNICIAN COURSE SUPPLEMENTARY STUDY PAPER - 2013 TAXATION [A discussion on the amendments made by the Finance Act, 2013 and significant Notifications & Circulars

INTERMEDIATE (IPC) COURSE/ ACCOUNTING TECHNICIAN COURSE SUPPLEMENTARY STUDY PAPER - 2013 TAXATION [A discussion on the amendments made by the Finance Act, 2013 and significant Notifications & Circulars

R-2. Amendments at a glance

R-2 Amendments at a glance Effected by the Finance ACT, 2018 $ Tax rates 0.11 Tax rates for the assessment years 2018-19 and 2019-20 are given in Referencer 1. 0.11-1 Income-tax - The following are the

R-2 Amendments at a glance Effected by the Finance ACT, 2018 $ Tax rates 0.11 Tax rates for the assessment years 2018-19 and 2019-20 are given in Referencer 1. 0.11-1 Income-tax - The following are the

Jagannath Institute of Management Sciences Lajpat Nagar. BBA Sem V Income Tax

Jagannath Institute of Management Sciences Lajpat Nagar BBA Sem V Income Tax UNIT- 1 Introduction and Important Definitions Introduction Basic concepts of Income Tax Act Income [Section 2(24)] Capital

Jagannath Institute of Management Sciences Lajpat Nagar BBA Sem V Income Tax UNIT- 1 Introduction and Important Definitions Introduction Basic concepts of Income Tax Act Income [Section 2(24)] Capital

1 APPLICABILITY OF MAT

CONTENTS Chapter-heads I-5 MAT/AMT Ready Reckoner I-21 DIVISION ONE MINIMUM ALTERNATE TAX (MAT) 1 APPLICABILITY OF MAT 1.1 History of Minimum Alternate Tax (MAT) 3 1.1-1 Comparative study of sections 115J,

CONTENTS Chapter-heads I-5 MAT/AMT Ready Reckoner I-21 DIVISION ONE MINIMUM ALTERNATE TAX (MAT) 1 APPLICABILITY OF MAT 1.1 History of Minimum Alternate Tax (MAT) 3 1.1-1 Comparative study of sections 115J,

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM. Test Code CIM 8174

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT- DT Test Code CIM 8174 BRANCH - () (Date :) Head Office :Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT- DT Test Code CIM 8174 BRANCH - () (Date :) Head Office :Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1

SALIENT FEATURES OF THE FINANCE BILL, [Relating to Direct Taxes]

![SALIENT FEATURES OF THE FINANCE BILL, [Relating to Direct Taxes]](/thumbs/77/76609678.jpg "SALIENT FEATURES OF THE FINANCE BILL, [Relating to Direct Taxes]") SALIENT FEATURES OF THE FINANCE BILL, 2013 1 [Relating to Direct Taxes] Published in 351 ITR (Journ.) p.61 (Part-5) - By S.K. Tyagi The Finance Bill, 2013, or the Union Budget, 2013-14, was presented in

SALIENT FEATURES OF THE FINANCE BILL, 2013 1 [Relating to Direct Taxes] Published in 351 ITR (Journ.) p.61 (Part-5) - By S.K. Tyagi The Finance Bill, 2013, or the Union Budget, 2013-14, was presented in

SUGGESTED SOLUTION IPCC May 2017 EXAM. Test Code - I N J

SUGGESTED SOLUTION IPCC May 2017 EXAM DIRECT TAXATION Test Code - I N J 1 0 7 3 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Answer-1

SUGGESTED SOLUTION IPCC May 2017 EXAM DIRECT TAXATION Test Code - I N J 1 0 7 3 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Answer-1

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

10 Aggregation of Income, Set-off and Carry Forward of Losses

10 Aggregation of Income, Set-off and Carry Forward of Losses 10.1 Aggregation of Income In certain cases, some amounts are deemed as income in the hands of the assessee though they are actually not in

10 Aggregation of Income, Set-off and Carry Forward of Losses 10.1 Aggregation of Income In certain cases, some amounts are deemed as income in the hands of the assessee though they are actually not in

Question 1. The Institute of Chartered Accountants of India

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

Basics of Income Tax

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

Budget Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013

Budget 2013 Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013 Index Direct Tax Proposals Implications of amendments proposed in the Finance Bill, 2013 2 Direct Tax Proposals

Budget 2013 Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013 Index Direct Tax Proposals Implications of amendments proposed in the Finance Bill, 2013 2 Direct Tax Proposals

Minimum Alternate Tax (MAT) (Chapter-XIIB {Section 115J/ JAA/ JB}) Articles. Objective behind the introduction of MAT: Background:

(Chapter-XIIB {Section 115J/ JAA/ JB}) Articles. Objective behind the introduction of MAT: Background:") Minimum Alternate Tax (MAT) (Chapter-XIIB {Section 115J/ JAA/ JB}) Objective behind the introduction of MAT: Normally, a comapny is liable to pay tax on the income computed in accordance with the provisions

Minimum Alternate Tax (MAT) (Chapter-XIIB {Section 115J/ JAA/ JB}) Objective behind the introduction of MAT: Normally, a comapny is liable to pay tax on the income computed in accordance with the provisions

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE COMPILED BY: CA.ARUN GUPTA ca.arungupta77@gmail.com A. Rates of Taxes: 1. It is proposed to make the following changes in tax rates: In case of Resident

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE COMPILED BY: CA.ARUN GUPTA ca.arungupta77@gmail.com A. Rates of Taxes: 1. It is proposed to make the following changes in tax rates: In case of Resident

ASSESSMENT OF AOP / BOI (Sec. 86)

") ASSESSMENT OF AOP / BOI (Sec. 86) The assessment of the members of AOP or BOI depends on whether the AOP or BOI is chargeable to tax at the maximum marginal rate or at slab rate or is not chargeable to

ASSESSMENT OF AOP / BOI (Sec. 86) The assessment of the members of AOP or BOI depends on whether the AOP or BOI is chargeable to tax at the maximum marginal rate or at slab rate or is not chargeable to

Interim Union Budget 2019 & Important changes for AY CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP

, FCA, FCS, FCMA, LL.B, MIMA, DISA, IP") Interim Union Budget 2019 & Important changes for AY 2019-20 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Nehru Place CPE Study Circle of NIRC of ICAI 7 th February 2019 INCOME