Annual Tax Briefing Participants. From: Mecklenburg County Office of the Tax Collector Date: July Tax Billing Information

|

|

|

- Joleen Gordon

- 5 years ago

- Views:

Transcription

1 To: Annual Tax Briefing Participants From: Mecklenburg County Office of the Tax Collector Date: July 2018 RE: 2018 Tax Billing Information The attached packet contains information that is useful when answering taxpayer questions regarding real estate or personal property tax bills. Please use this packet and CD as your reference materials. The following information is provided in this packet: I. Tax Cycle and Other Important Tax Information II. Jurisdiction Rate Chart III. Payment Options IV. Annual Tax Billing FAQs V. Sample Bills VI. Maps For additional questions, please feel free to contact Bobby Hopkins, Ashley Levy or Veronica Trice. Thank you, Bobby Hopkins Ashley Levy Veronica Trice

2 TAX CYCLE AND OTHER IMPORTANT INFORMATION Dates What to expect? January 1, 2018 July 27, 2018 Real Estate is listed from the deed with owner of record. NCGS (d) Real Estate, Personal Property tax bills, and Property Tax Notifications are expected to be mailed to the owner of record as of January 1, July 27, 2018 September 1, 2018 Property Tax Notification Letters are expected to be mailed to the owner of record as of January 1, Real Estate and Personal Property Tax Bills are due. NCGS (a) January 7, 2019 All tax bill payments are due to avoid interest. January 8, 2019 Interest begins to accrue on delinquent Real Estate and Personal Property tax bills. February 2019 Delinquent Real Estate and Personal Property taxpayers will be notified that they may be advertised in the local newspaper. NCGS (b1) 225,601 Real Estate and Personal Property tax bills will be mailed on July 27, ,609 Property Tax Notifications will be mailed the week of July 27, For certain properties whose value or tax records are still being processed by the County Assessor s Office the respective tax bills will subsequently be mailed as they are processed. Examples of these bills include, but are not limited to, properties changing value in 2018 as a result of new construction or other factors. Mecklenburg County does not grant discounts on early payments.

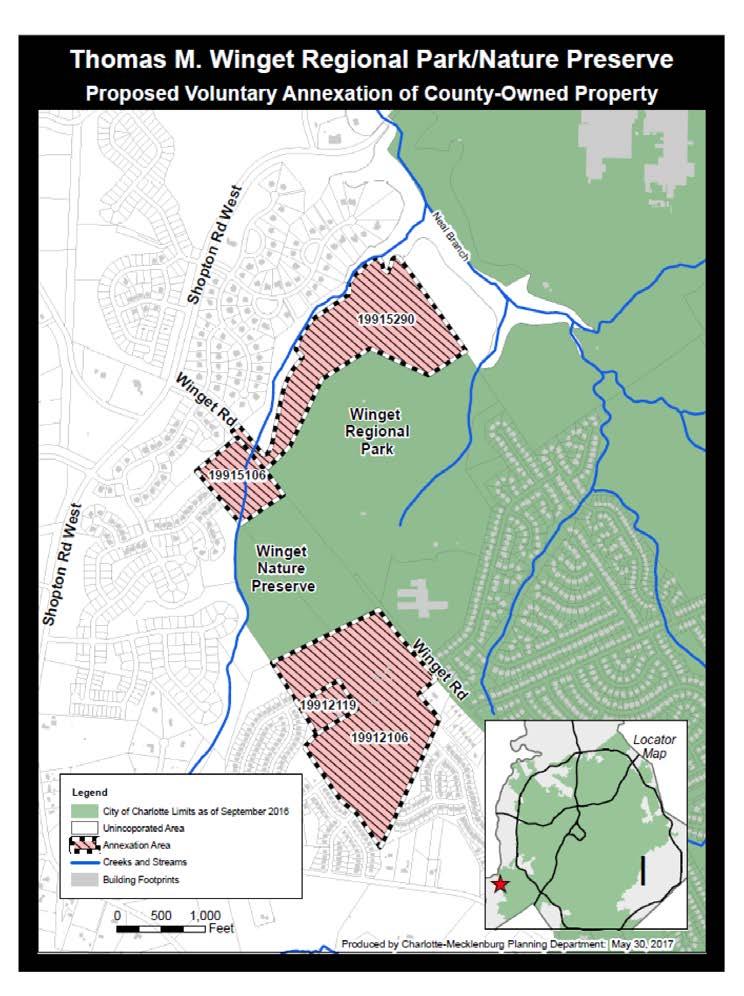

3 Mecklenburg County does not waive interest on late payments. Period for which Taxes are Levied NCGS 143C-1-1(d)(14) Taxes are levied for the operation of the local government from July 1 through June 30, which is Mecklenburg County s and the municipalities fiscal year. Last Day to Pay on Holiday or Weekend NCGS If January 5 th falls on a weekend or holiday, the next business day will be the last day to pay before interest begins to accrue for Real Estate and Personal Property tax bills. NOTE: January 5 th does fall on a weekend this year. Interest Accrual - NCGS (a)(1)(2) Delinquent 2018 Real Estate and Personal Property tax bills will accrue interest on January 8, 2019 at a rate of 2% for January and ¾% each month thereafter, beginning on the 1 st day of the month. Postmark Date NCGS (d) Tax payments submitted by mail will be deemed received as of the date shown on the postmark affixed by the Unites States Postal Service. All tax payments submitted by mail without a USPS- affixed postmark, including metered stamped tax payments, will be deemed as received on the day it is received in the office. Real Estate and Personal Property Tax Notices - NCGS Mecklenburg County is not required to mail notices for Real Estate and Personal Property tax bills. Effective June 30, 2018, the Charlotte City Council adopted a series of ordinances approving annexations of several city and county owned properties. The annexations are: o Tuckaseegee Airport Area o Old Moore s Chapel o Castleford Reserve o Sutton Farms o Berewick Commons o ByrumNC 160 o Reedy Creek o Winget o Rocky River MPV The Town of Davidson annexed an area effective July 10, The annexation is: o Kenmare Subdivision

4 For additional information about annexations, visit In FY12, Mecklenburg County established five Fire Protection Service Districts for properties located within the unincorporated area of Mecklenburg County. The five Fire Protection Service Districts are: Charlotte, Cornelius, Davidson, Huntersville, and Mint Hill. Prior to FY12, fire protection costs were paid for by all taxpayers within Mecklenburg County. While all residents of the County will have full fire protection, the details of which fire unit would respond to a service need depends on the location of the property and various contracts with Mecklenburg County, the cities and towns, and different volunteer fire departments. The cost of fire protection services varies by districts. Not all Fire Protection Service District tax rates are the same. Below are the FY16 Fire Protection Service District tax rates and billing codes: Fire District Tax Rate Billing Codes City of Charlotte $0.080 Fire (MCH) Cornelius $0.057 Fire (MCN) Davidson $0.085 Fire (MDV) Huntersville $0.050 Fire (MHT) Mint Hill $0.080 Fire (MMH) Property owners in unincorporated Mecklenburg County pay for police services through the Law Enforcement Service District (LESD) tax. Effective July 1, 2018 Mecklenburg County established six (6) LESDs in the unincorporated area of the County and abolished the countywide LESD. The newly established LESD taxes replace the former LESD tax. Property owners in the unincorporated area will find the LESD tax included on this bill in the Bill Line Items section. The description will appear as POLICE (Jurisdiction) TAX. Police District Tax Rate Billing Codes City of Charlotte $ POLICE (MCH) TAX Cornelius $ POLICE (MCN) TAX Davidson $ POLICE (MDV) TAX Huntersville $ POLICE (MHT) TAX Mint Hill $ POLICE (MMH) TAX Pineville $ POLICE (MPN) TAX The tax brochure includes additional information such as Mecklenburg County property taxes account for 62.5% of County funds. The tax brochure provides revenue and budget summaries for Mecklenburg County and the surrounding municipalities. To view the tax brochure and tax rates visit

5

6 PAYMENT OPTIONS Below is a sample copy of the Payment Options full page insert for this year s annual billing. Please note: there are five ways to pay a Real Estate and Personal Property tax bill.

7 The online and telephone payment options are handled by Forte Payment Systems. Forte Payment Systems telephone payment option number is The online payment link is With Forte Payment Systems, taxpayers can now pay multiple bills at one time. Taxpayers no longer have to select the type of bill he or she wishes to pay. If a taxpayer elects to pay by echeck, he or she is required to enter their bank account number twice, which will help reduce the number of returned checks due to incorrect account information. Forte Payment Systems has a standard service fee for all credit card and debit card payments. Credit card and debit card payments are charged a service fee of 2.35% of the amount of the tax bill or a minimum fee of $1.95. The service fee is not charged or collected by Mecklenburg County. The service fee is charged by Forte Payment Systems per merchant service agreement. Forte Payment Systems customer service can be reached at or by visiting

8 FREQUENTLY ASKED TAX COLLECTION QUESTIONS Q: What can cause my taxes to increase? A: Taxes may increase from the prior year for any one of the following reasons: 1. A change in the tax rate by the Charlotte City Council and/or Town or County Commissioners. 2. The assessed value increases due to reappraisal or if certain improvements are made. 3. Additional taxable property was acquired (real or personal). 4. Property is subject to both city and county taxes due to annexation. 5. The solid waste fee is increased or newly applicable. Q: Why did I not get a real estate tax bill? A: There are several reasons for not receiving a tax bill; including: 1. Those properties under formal assessment review will not receive a tax bill until that review is completed. 2. The bills for taxes that are in escrow are sent to the mortgage company. 3. Incorrect address. 4. In the case of a sale after January 1 st, the previous owners would have received the tax bill (the County sends new owners a letter notifying them of the taxes due). Q: Can I appeal my real estate assessment when I get the tax bill? A: No. An assessment must be appealed by May 11 th or within thirty (30) days after receipt of a change of assessment notice. Q: Can I appeal my Individual Personal Property (IPP) assessment when I get the tax bill? A: Yes, if no previous notice of value has been created (per audit discovery), then the tax bill will serve as the official notification of value. A taxpayer can appeal his or her IPP assessment within thirty (30) days after the date of the official notice of value. Q: If I sold my house during the year, why did I get a tax bill? A: Because North Carolina tax law requires that the tax bill is sent to the owner of record as of January 1 st. This tax bill should be returned to the Office of the Tax Collector with the new owner s name and address if available. Q: How did the County determine my house value? A: The Tax Assessor assesses the value of all taxable property by the first of each year. The assessed value is based on the market value as of the last reappraisal. Home values may increase or decrease if there was a change in the home structure such as a home renovation, flood or fire damage.

9 Q: I cannot pay my taxes, what should I do? A: Property taxes are not based on ability to pay or income. Property taxes are an ad valorem tax. You should contact the Office of the Tax Collector ( ) prior to the tax bill becoming delinquent and for further information. Q: Is there any tax relief for elderly or disabled property owners? A: Yes. There are several programs created by the North Carolina General Statutes. Please contact the County Assessor s Office at (704) for details. There are strict qualifications and application deadlines for these programs and they are not retroactive for previous year tax obligations. For those programs based on disability, the required certifications have to come from a physician and not from agencies such as the Social Security Administration. Q: Does this tax bill include all of my property taxes for the year? A: This tax bill is for the taxable property owned, real and personal, that is reflected on the tax bill. Q: What does unincorporated mean and why is it unincorporated? A: Unincorporated means that an area is not within the city limits of any city or town within Mecklenburg County. It is unincorporated because the area has not been annexed by a municipality, nor has it applied to become a municipality. Q: What qualifies as Individual Personal Property? A: Boats and other water craft, airplanes, unlicensed vehicles, multiyear/permanent tag vehicles/trailers, campers, income producing farm equipment, manufactured mobile homes (with wheels/hitch), and other such properties. Q: What qualifies as Business Personal Property? A: Office equipment, machinery, furniture and fixtures, leasehold improvements, computer equipment, software, supplies, business motor vehicles, etc. Q: When should I list Individual or Business Personal Property with the Tax Assessor? A: Owners of personal property must list with the Tax Assessor s Office during the month of January each year. A 10% late listing penalty will be charged for anyone listing after January 31 st of each year. An extension to list property can be requested, in writing, during the regular listing period for good cause for business personal property. Q: How is the assessment determined for Individual and Business Personal Property? A: Personal property is assessed at fair market value by the Tax Assessor s Office on January 1 st each year. For Business Personal Property, depreciation tables are applied to the original cost to arrive at the current market value.

10 FREQUENTLY ASKED LAW ENFORCEMENT/FIRE SERVICE DISTRICT TAX QUESTIONS Q: Are taxes being used for police services in unincorporated areas? Does this mean police services will be increased in these areas? A: Police services in the unincorporated areas are provided by the Charlotte-Mecklenburg Police Department. The Chief of Police decides the necessary level of service required to meet the public safety needs of each police district. In the unincorporated areas, police services are paid for by the use of a separate tax rate so residents of the unincorporated areas pay directly for the police services they receive. Q: Why is there a separate tax rate for the unincorporated areas? A: A state law passed in 1996 allows the County to levy a separate tax rate in unincorporated areas for police services delivered to those residents. The reason is because police services are not included in the County tax rate. Q: How are police services billed for residents of Charlotte and other towns? A: Police services for residents of Charlotte and other towns are billed as part of his or her municipal property tax; it is combined within the overall tax rate. Q: Will police services be billed independently by individual police stations? A: No. Police services will be billed as part of the property tax bill by either the municipality or the County, depending upon where you live. Q: How much of my taxes actually go to pay for police services in unincorporated areas? A: The unincorporated tax rate is $1.0378, of which $ is used to fund police services provided within the unincorporated areas. Q: I live in a town. Does that mean that my County tax bill includes money to pay for police services throughout the County and Charlotte? No. You pay for police services provided in your town through the tax billing done by your town. The police services paid by the Law Enforcement Service District County tax rate are for residents of the unincorporated areas only. Q: What are Fire Protection Service Districts? A: Each property within the unincorporated areas of Mecklenburg County is contained in one of five (5) Fire Protection Service Districts. A Fire Protection Service District tax is charged to the property owners within each district. There is a separate tax rate for each fire district depending on the costs of providing fire protection services to that district. Residents of each district pay the costs of fire protection being

11 provided in his or her area. Prior to 2012, all Mecklenburg County property owners paid fire protection costs for unincorporated areas. Please refer to the tax rate chart and maps in this briefing. The tax rates are subject to change each fiscal year (July 1 June 30) and annexation may affect applicability. The Fire Protection Services District Tax is a Mecklenburg County tax and it is charged on the annual tax bill for the property.

12 FREQUENTLY ASKED SOLID WASTE FEE QUESTIONS Q: Who decided to impose the solid waste fee? A: The decision on setting the solid waste fee is made by elected officials. Q: My property is exempt from ad valorem tax. Why did I get billed for the solid waste fee? A: The County s $27.50 solid waste fee applies to taxable and exempt properties within Mecklenburg County. The same applies for the City of Charlotte s solid waste fee of $46.06 for single-family homes and multi-family homes, and the Town of Huntersville s solid waste fee of $84.00 for single-family homes. The Town of Davidson solid waste fee is $201 per single-family home and varies for multifamily homes. Please refer to the tax rate chart for more information. Q: How do I know that the solid waste fee I pay is used to dispose of my trash? A: If you live within the Charlotte city limits, or the Huntersville or Davidson town limits, the fee you pay is directly related to the cost of disposing your trash. Q: Why are there two solid waste fees on my bill? A: There is a municipality solid waste fee in Charlotte, Huntersville, and Davidson as well as a Mecklenburg County solid waste fee. Q: Will I have to pay a fee every time I go to drop off my trash, recyclable materials, and/or yard waste? A: The County s annual solid waste fee allows homeowners, at no cost, to self-haul and dispose of their household trash to the County s disposal centers. The only item that does involve additional cost is yard waste. Q: Why do I have to pay a solid waste fee when my taxes are used to pay for collection of trash? A: The cost of trash collection and disposal are separate costs. Charlotte, Huntersville, and Davidson property taxes are used to pay for collection services within the city/town limits. The Charlotte, Huntersville, and Davidson solid waste fees are used to pay for the disposal of trash at the landfill. Q: Does the solid waste fee also include all towns within the County? A: Yes. It includes all of the towns within the County. Q: What happens if I do not pay the solid waste fee? A: The tax lien will remain on the property and the property is subject to enforced collections. Q: Why is the solid waste fee not considered a tax?

13 The elected officials determined that a fee would allow the tax rate to remain lower, and would be a clearer indicator of the cost for the services of trash disposal and recycling. Q: Why are the County and Municipality solid waste fees different? The County solid waste fee is used to pay for recycling and waste reduction services and facilities. The Charlotte, Huntersville, and Davidson solid waste fees are used to pay for disposal of trash collected within the respective municipalities. These services have different costs.

14 FREQUENTLY ASKED ONLINE AND TELEPHONE PAYMENT QUESTIONS Q: How do I make a payment over the internet or telephone? A: The online payment system can be accessed at The telephone payment system can be accessed by dialing (800) echeck may be used on the online payment system and the telephone payment system. Have your 24-digit tax bill number and credit/debit card or checking account information available. Please follow all instructions and print a copy of your confirmation number if making an online payment or write your confirmation number down if making a telephone payment. Q: How is it possible to make an online or telephone payment? A: The Mecklenburg County Office of the Tax Collector has entered into an agreement with Forte Payment Systems to provide taxpayers this automated payment service. Forte charges a service fee to the taxpayer for all credit/debit card transactions, but there is no service fee for using an electronic check (echeck). Q: Tell me more about the service fee. A: Mecklenburg County does not charge a service fee for processing an online or telephone payment transaction. Forte, however, does charge a service fee for credit/debit card transactions. You will be informed of the amount of the fee before authorizing payment. This fee is in addition to any charges, such as interest, that may be assessed by the credit card issuer. Note: Forte is a publicly held for-profit company. In order to cover operating costs, security costs, and the costs associated with servicing thousands of transactions, a service fee is charged. Q: Does Mecklenburg County receive any portion of the service fee? A: No. This service fee is not part of your tax; therefore, Mecklenburg County does not receive any portion of the service fee. When paying online or via telephone, please allow up to two business days for your payment to be posted. Q: What credit cards can I use? A: American Express, Discover, MasterCard, and Visa. Q: Can I use my debit card? A: Yes. If your debit card has the MasterCard or Visa logo, then you can use your debit card to submit an online or telephone payment. The debit card must be able to be used without a personal identification number (PIN).

15 Q: What will I receive as confirmation of payment? A: You will be provided a confirmation number at the end of your payment transaction. You will also receive an confirmation. The confirmation number, and , along with your credit card or banking statement will serve as your payment confirmation. Q: How secure is my payment information that is used to make my payment? A: Forte uses the best encryption technology available. Credit/debit card and checking account information is not passed to any government entity, nor is it stored anywhere on their site.

16 FREQUENTLY ASKED ONLINE BILL PAY PAYMENT QUESTIONS Q: How can I make a payment through my bank s online bill payment service? A: Note: Not recommended for tax payments. Any interest accrued due to a rejected payment cannot be removed from the tax bill. Online bill pay services vary by each banking or financial institution. Most banking institutions do not recommend payment of taxes through their services due to the fact that taxes have a delinquency date upon which interest will accrue if payment is not received. In order to pay taxes via a bill pay service, the taxpayer must enter the complete, 24-digit tax bill number in the Account Number Field. This number must reflect the current bill number for the taxes that the taxpayer wishes to pay. This bill number is different for every parcel, car, boat, etc. and changes each year. It is the responsibility of the taxpayer to ensure that the correct, 24-digit bill number is entered. The Office of the Tax Collector encourages taxpayers to use the online payment system at Q: What happens if I fail to enter the correct, 24-digit tax bill number? A: The payment will be rejected and returned to the taxpayer s banking institution. Q: What happens if I enter a 24-digit tax bill number that has been paid? A: The payment will be rejected and returned to the taxpayer s banking institution. Q: What happens if I fail to enter the 24-digit tax bill number into the correct Account Number Field? A: The payment will be rejected and returned to the taxpayer s banking institution. Q: What happens if the payment is returned to my bank? A: Your bank will credit your account. However, your tax bill remains unpaid and if payment is not received by the Office of the Tax Collector prior to the date the bill becomes delinquent, interest will accrue. Once accrued, interest cannot be waived. Q: Will I receive credit for the date I attempted to pay the tax? A: No. It is the responsibility of the taxpayer to ensure that payment is made correctly to the Office of the Tax Collector. Payment is not deemed as received until the funds have reached the Office of the Tax Collector. Payments received on or after the date of delinquency (January 6, 2018) will result in interest being assessed.

17

18

19

20

21

22

23

24 Castleford Reserve

25 Sutton Farms

26

27

28

29

30

31

![Commented [DCA1]: Typically, the map here](/docs-images/87/95758329/images/32-0.jpg "shows the fire districts, not the VFD")

32 Commented [DCA1]: Typically, the map here shows the fire districts, not the VFD boundaries.

33

34

35

FY Property Taxes

FY 2012-2013 Office of the Tax Collector Mecklenburg County, NC Mecklenburg Charlotte Cornelius Davidson Huntersville Matthews Mint Hill Pineville What do property taxes pay for? When you call the police

FY 2012-2013 Office of the Tax Collector Mecklenburg County, NC Mecklenburg Charlotte Cornelius Davidson Huntersville Matthews Mint Hill Pineville What do property taxes pay for? When you call the police

FY Property Taxes

How do I pay my taxes? There are five ways to pay your real estate and personal property taxes. A convenience fee is charged for the Internet and phone options that require a credit/debit card or echeck.

How do I pay my taxes? There are five ways to pay your real estate and personal property taxes. A convenience fee is charged for the Internet and phone options that require a credit/debit card or echeck.

FY Property Taxes

How do I pay my taxes? There are five ways to pay your real estate and personal property taxes. A convenience fee is charged for the Internet and phone options that require a credit/debit card or echeck.

How do I pay my taxes? There are five ways to pay your real estate and personal property taxes. A convenience fee is charged for the Internet and phone options that require a credit/debit card or echeck.

FY Property Taxes

How do I pay my taxes? There are fi ve ways to pay your real estate and personal property taxes. A convenience fee is charged for the Internet and phone options that require a credit/debit card or echeck.

How do I pay my taxes? There are fi ve ways to pay your real estate and personal property taxes. A convenience fee is charged for the Internet and phone options that require a credit/debit card or echeck.

Property Taxes

How do I pay my taxes? There are five ways to pay your real estate and personal property taxes. A convenience fee will be charged for the Internet and phone options that require a credit/debit card or

How do I pay my taxes? There are five ways to pay your real estate and personal property taxes. A convenience fee will be charged for the Internet and phone options that require a credit/debit card or

2019 Property Tax Calendar

PROPERTY TAX BULLETIN NO. 175 DECEMBER 2018 2019 Property Tax Calendar Christopher B. McLaughlin This calendar lists deadlines for the 2019 20 tax year established by the Machinery Act. Duties for which

PROPERTY TAX BULLETIN NO. 175 DECEMBER 2018 2019 Property Tax Calendar Christopher B. McLaughlin This calendar lists deadlines for the 2019 20 tax year established by the Machinery Act. Duties for which

Mecklenburg County Fire Protection Service Districts Report

Mecklenburg County Fire Protection Service Districts Report February 21, 2012 1 Part 1: Overview Background and Justification The County proposes a new funding vehicle for delivery of fire protection services

Mecklenburg County Fire Protection Service Districts Report February 21, 2012 1 Part 1: Overview Background and Justification The County proposes a new funding vehicle for delivery of fire protection services

2018 Property Tax Calendar

PROPERTY TAX BULLETIN NO. 173 DECEMBER 2017 2018 Property Tax Calendar Christopher B. McLaughlin This calendar lists deadlines for the 2018 19 tax year established by the Machinery Act. Duties for which

PROPERTY TAX BULLETIN NO. 173 DECEMBER 2017 2018 Property Tax Calendar Christopher B. McLaughlin This calendar lists deadlines for the 2018 19 tax year established by the Machinery Act. Duties for which

This AGREEMENT, made and entered the day of, 2013, by and W I T N E S S E T H:

NORTH CAROLINA PASQUOTANK COUNTY This AGREEMENT, made and entered the day of, 2013, by and between Pasquotank County (hereinafter referred to as County), and the City of Elizabeth City (hereinafter referred

NORTH CAROLINA PASQUOTANK COUNTY This AGREEMENT, made and entered the day of, 2013, by and between Pasquotank County (hereinafter referred to as County), and the City of Elizabeth City (hereinafter referred

FACTS ABOUT BUSINESS PROPERTY ASSESSMENTS. LESLIE MORGAN Shasta County Assessor-Recorder

FACTS ABOUT BUSINESS PROPERTY ASSESSMENTS LESLIE MORGAN Shasta County Assessor-Recorder Shasta County does not discriminate on the basis of disability. Our ADA Coordinator may be reached at 530-225-5515;

FACTS ABOUT BUSINESS PROPERTY ASSESSMENTS LESLIE MORGAN Shasta County Assessor-Recorder Shasta County does not discriminate on the basis of disability. Our ADA Coordinator may be reached at 530-225-5515;

TAX COLLECTOR'S NOTICE: CITY OF NORWALK, CONNECTICUT

TAX COLLECTOR'S NOTICE: CITY OF NORWALK, CONNECTICUT Notice is hereby given that TAXES on the grand list of October 1, 2010 are DUE AND PAYABLE on January 1, 2012. The last day on which to pay without

TAX COLLECTOR'S NOTICE: CITY OF NORWALK, CONNECTICUT Notice is hereby given that TAXES on the grand list of October 1, 2010 are DUE AND PAYABLE on January 1, 2012. The last day on which to pay without

Table of Contents FOR ADDITIONAL INFORMATION, PLEASE CONTACT:

Important Information About This Summary This document briefly summarizes recent substantive changes to Arizona's tax laws. The bills addressed herein were approved by Arizona's Legislature and signed

Important Information About This Summary This document briefly summarizes recent substantive changes to Arizona's tax laws. The bills addressed herein were approved by Arizona's Legislature and signed

FY 2016 FY 2017 FY 2017 FY 2018 Percent Ad Valorem Taxes

Ad Valorem Taxes Ad Valorem Taxes are taxes paid on real and personal property located within the Village s corporate limits. Taxes for real and personal property, excluding motor vehicles, are levied

Ad Valorem Taxes Ad Valorem Taxes are taxes paid on real and personal property located within the Village s corporate limits. Taxes for real and personal property, excluding motor vehicles, are levied

TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES

PTO TM #16-01 TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES PURPOSE: This transmittal memorandum contains changes to the Department of Revenue Rules within the Property Tax Oversight Program. RULE

PTO TM #16-01 TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES PURPOSE: This transmittal memorandum contains changes to the Department of Revenue Rules within the Property Tax Oversight Program. RULE

Department of. Assessment & Taxation

Department of Assessment & Taxation About Your Assessor s Office Your Assessor would like you to know about his role in the Oregon system of local government finance. Many people think assessors work directly

Department of Assessment & Taxation About Your Assessor s Office Your Assessor would like you to know about his role in the Oregon system of local government finance. Many people think assessors work directly

FREQUENTLY ASKED QUESTIONS ASSESSOR S OFFICE

FREQUENTLY ASKED QUESTIONS ASSESSOR S OFFICE Q: What do Assessors do? A: Assessors are required by Massachusetts law to value all real and personal property within their community. They value every property,

FREQUENTLY ASKED QUESTIONS ASSESSOR S OFFICE Q: What do Assessors do? A: Assessors are required by Massachusetts law to value all real and personal property within their community. They value every property,

Rules and Regulations

Rules and Regulations Mecklenburg County Ordinance to Require the Source Separation of Designated Materials from the Municipal Solid Waste Stream for the Purpose of Participation in a Recycling Program

Rules and Regulations Mecklenburg County Ordinance to Require the Source Separation of Designated Materials from the Municipal Solid Waste Stream for the Purpose of Participation in a Recycling Program

Financial Sources & Uses

Financial Sources & Uses Financial Sources and Uses The Salute to Veterans Parade was held on November 8, 2014 to showcase local middle and high school bands, the Junior Reserve Officer Training Corps

Financial Sources & Uses Financial Sources and Uses The Salute to Veterans Parade was held on November 8, 2014 to showcase local middle and high school bands, the Junior Reserve Officer Training Corps

2016 Mecklenburg County, North Carolina

FISCAL YEAR 2016 Mecklenburg County, North Carolina BUDGET In Brief www.mecklenburgcountync.gov EXECUTIVE SUMMARY Mecklenburg County s Fiscal Year 2016 Adopted Budget totals $1.57 billion; a $42.4 million

FISCAL YEAR 2016 Mecklenburg County, North Carolina BUDGET In Brief www.mecklenburgcountync.gov EXECUTIVE SUMMARY Mecklenburg County s Fiscal Year 2016 Adopted Budget totals $1.57 billion; a $42.4 million

GUIDE TO PROPERTY TAXES

NEW JERSEY HOMEOWNER S GUIDE TO PROPERTY TAXES ASSOCIATION OF MUNICIPAL ASSESSORS OF NEW JERSEY Property taxes are top of mind for many New Jersey homeowners. The state has the highest property taxes in

NEW JERSEY HOMEOWNER S GUIDE TO PROPERTY TAXES ASSOCIATION OF MUNICIPAL ASSESSORS OF NEW JERSEY Property taxes are top of mind for many New Jersey homeowners. The state has the highest property taxes in

IC Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies

IC 6-1.1-17 Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies IC 6-1.1-17-0.5 Exclusion by county auditor of certain assessed value on tax duplicate; county auditor reduction

IC 6-1.1-17 Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies IC 6-1.1-17-0.5 Exclusion by county auditor of certain assessed value on tax duplicate; county auditor reduction

ORDINANCE NUMBER 1174

ORDINANCE NUMBER 1174 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF PERRIS, COUNTY OF RIVERSIDE, STATE OF CALIFORNIA, ACTING IN ITS CAPACITY AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO.

ORDINANCE NUMBER 1174 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF PERRIS, COUNTY OF RIVERSIDE, STATE OF CALIFORNIA, ACTING IN ITS CAPACITY AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO.

Gaston County 2017 Small Business Grant Program

Gaston County 2017 Small Business Grant Program Small Business Investment Grant Program GASTON COUNTY The Gaston County Board of Commissioners has supported economic development for more than twenty years

Gaston County 2017 Small Business Grant Program Small Business Investment Grant Program GASTON COUNTY The Gaston County Board of Commissioners has supported economic development for more than twenty years

NC General Statutes - Chapter 105 Article 20 1

Article 20. Approval, Preparation, Disposition of Records. 105-318. Forms for listing, appraising, and assessing property. The Department of Revenue may design and prescribe the books and forms to be used

Article 20. Approval, Preparation, Disposition of Records. 105-318. Forms for listing, appraising, and assessing property. The Department of Revenue may design and prescribe the books and forms to be used

IC Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies

IC 6-1.1-17 Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies IC 6-1.1-17-0.5 Exclusion by county auditor of certain assessed value on tax duplicate; county auditor reduction

IC 6-1.1-17 Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies IC 6-1.1-17-0.5 Exclusion by county auditor of certain assessed value on tax duplicate; county auditor reduction

FY15 APPROPRIATIONS. Specific highlights for the General Fund, Special Capital

FY15 APPROPRIATIONS The following sections will provide highlights on changes to budgeted appropriations from FY14 to FY15. OPERATING BUDGET HIGHLIGHTS The total Operating Budget for FY15 has increased

FY15 APPROPRIATIONS The following sections will provide highlights on changes to budgeted appropriations from FY14 to FY15. OPERATING BUDGET HIGHLIGHTS The total Operating Budget for FY15 has increased

MECKLENBURG COUNTY. Assessor s Office Real Estate Division

MECKLENBURG COUNTY Assessor s Office Real Estate Division Dear Sir/Madam, Enclosed is a 2013 application/audit review for Low-Income Homestead Exclusion, the Disabled Veteran Exclusion, and the Circuit

MECKLENBURG COUNTY Assessor s Office Real Estate Division Dear Sir/Madam, Enclosed is a 2013 application/audit review for Low-Income Homestead Exclusion, the Disabled Veteran Exclusion, and the Circuit

FISCAL YEAR RECOMMENDED BUDGET STRATEGY FOR SUCCESS MECKLENBURG COUNTY, NORTH CAROLINA

FISCAL YEAR 2017 RECOMMENDED BUDGET STRATEGY FOR SUCCESS MECKLENBURG COUNTY, NORTH CAROLINA 1 Purpose of Presentation Provide an overview of the FY2017 Recommended Budget Revenue Estimates Service Districts

FISCAL YEAR 2017 RECOMMENDED BUDGET STRATEGY FOR SUCCESS MECKLENBURG COUNTY, NORTH CAROLINA 1 Purpose of Presentation Provide an overview of the FY2017 Recommended Budget Revenue Estimates Service Districts

Important Tax Reminders

2018 Property Tax Guide Important Tax Reminders All exemptions must be filed with the Cherokee County Tax Assessors office by April 1 of the current tax year in order to take effect during the following

2018 Property Tax Guide Important Tax Reminders All exemptions must be filed with the Cherokee County Tax Assessors office by April 1 of the current tax year in order to take effect during the following

TOWN OF WINDSOR UTILITY BILLING POLICIES AND PROCEDURES

TOWN OF WINDSOR UTILITY BILLING POLICIES AND PROCEDURES 301 Walnut Street Windsor, Colorado 80550 phone 970-674-2400 fax 970-674-2456 www.windsorgov.com Contents Section 1. Utility Billing Policy 3 Section

TOWN OF WINDSOR UTILITY BILLING POLICIES AND PROCEDURES 301 Walnut Street Windsor, Colorado 80550 phone 970-674-2400 fax 970-674-2456 www.windsorgov.com Contents Section 1. Utility Billing Policy 3 Section

ORDINANCE NUMBER 1104

ORDINANCE NUMBER 1104 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF PERRIS ACTING IN ITS CAPACITY AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO. 2001-3 (NORTH PERRIS PUBLIC SAFETY) OF THE

ORDINANCE NUMBER 1104 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF PERRIS ACTING IN ITS CAPACITY AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO. 2001-3 (NORTH PERRIS PUBLIC SAFETY) OF THE

Ad Valorem Taxes. Description of Revenue Source. Revenue Assumptions

Ad Valorem Taxes Ad Valorem Taxes are taxes paid on real and personal property located within the Village s corporate limits. Taxes for real and personal property, excluding motor vehicles, are levied

Ad Valorem Taxes Ad Valorem Taxes are taxes paid on real and personal property located within the Village s corporate limits. Taxes for real and personal property, excluding motor vehicles, are levied

Office of the Tax Collector

FY2017-2019 STRATEGIC BUSINESS PLAN Office of the Tax Collector, North Carolina STRATEGIC BUSINESS PLAN Office of the Tax Collector OUR VISION The Office of the Tax Collector's vision is to serve the community

FY2017-2019 STRATEGIC BUSINESS PLAN Office of the Tax Collector, North Carolina STRATEGIC BUSINESS PLAN Office of the Tax Collector OUR VISION The Office of the Tax Collector's vision is to serve the community

SPECIAL ASSESSMENT DISTRICTS HANDBOOK

SPECIAL ASSESSMENT DISTRICTS HANDBOOK ADOPTED BY THE HIGHLANDS COUNTY BOARD OF COUNTY COMMISSIONERS November 18, 2003 Special Assessment Districts Handbook of Highlands County Table of Contents SECTION

SPECIAL ASSESSMENT DISTRICTS HANDBOOK ADOPTED BY THE HIGHLANDS COUNTY BOARD OF COUNTY COMMISSIONERS November 18, 2003 Special Assessment Districts Handbook of Highlands County Table of Contents SECTION

The Commonwealth of Massachusetts

State Tax Form 96 Revised 11/2016 The Commonwealth of Massachusetts Name of City or Town 17 22 37 41 42&43 Assessors Use only Date Received Application. Parcel Id. SENIOR -- SURVIVING SPOUSE OR MINOR --

State Tax Form 96 Revised 11/2016 The Commonwealth of Massachusetts Name of City or Town 17 22 37 41 42&43 Assessors Use only Date Received Application. Parcel Id. SENIOR -- SURVIVING SPOUSE OR MINOR --

Premier Community Bank!

Welcome to Premier Community Bank! A guide to understanding the transfer of your Winneconne AnchorBank accounts to Premier Community Bank Find enclosed: Key dates and account change information Commonly

Welcome to Premier Community Bank! A guide to understanding the transfer of your Winneconne AnchorBank accounts to Premier Community Bank Find enclosed: Key dates and account change information Commonly

Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

The Taxpayers Guide to Brooklyn Taxes

The Taxpayers Guide to Brooklyn Taxes Jocelyne Ruffo - Revenue Collector April Lamothe - Assistant Revenue Collector Telephone # (860) 779-3411, option 5 Fax # 779-7853 Tax Collector PO Box 253 Brooklyn,

The Taxpayers Guide to Brooklyn Taxes Jocelyne Ruffo - Revenue Collector April Lamothe - Assistant Revenue Collector Telephone # (860) 779-3411, option 5 Fax # 779-7853 Tax Collector PO Box 253 Brooklyn,

This AGREEMENT, made and entered this the-3

NORTH CAROLINA ORANGE COUNTY This AGREEMENT, made and entered this the-3 day of ~, 2006, by and among Orange County (hereinafter referred to ljcomfty), Town ofcarrboro, Town of Chapel Hill, and Town of

NORTH CAROLINA ORANGE COUNTY This AGREEMENT, made and entered this the-3 day of ~, 2006, by and among Orange County (hereinafter referred to ljcomfty), Town ofcarrboro, Town of Chapel Hill, and Town of

FY15 REVENUES. FY 14 Adopted Taxes. General Fund $ $ $753.50

BROWARD COUNTY BUDGET-IN-BRIEF FY15 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments,

BROWARD COUNTY BUDGET-IN-BRIEF FY15 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments,

Online Presentment and Payment FAQ s

General Online Presentment and Payment FAQ s What are some of the benefits of receiving my bill electronically? It is convenient, saves time, reduces errors, allows you to receive bills anywhere at any

General Online Presentment and Payment FAQ s What are some of the benefits of receiving my bill electronically? It is convenient, saves time, reduces errors, allows you to receive bills anywhere at any

Administration of Arkansas Property Tax

FSCDC16 Administration of Arkansas Property Tax Wayne Miller Extension Economist - Agricultural Economics and Community Development John Zimpel Research, Development and Technical Support, Arkansas Assessment

FSCDC16 Administration of Arkansas Property Tax Wayne Miller Extension Economist - Agricultural Economics and Community Development John Zimpel Research, Development and Technical Support, Arkansas Assessment

Frequently Asked Questions

General Insurance Questions Frequently Asked Questions What insurance products are available through my agent? Our Agents can sell and service the following insurance products: personal automobile, business

General Insurance Questions Frequently Asked Questions What insurance products are available through my agent? Our Agents can sell and service the following insurance products: personal automobile, business

BASIC FINANCIAL STATEMENTS

BASIC FINANCIAL STATEMENTS Exhibit A STATEMENT OF NET ASSETS JUNE 30, 2012 Surry County Primary Government Tourism and Governmental Business-Type Development Activities Activities Total Authority Assets:

BASIC FINANCIAL STATEMENTS Exhibit A STATEMENT OF NET ASSETS JUNE 30, 2012 Surry County Primary Government Tourism and Governmental Business-Type Development Activities Activities Total Authority Assets:

applies and therefore levy the tax on a lower base. The cap may be raised by adoption of a resolution or ordinance under T.C.A. ' (a)(2).

(2).") Sales Tax Handbook TENNESSEE LAW 1 Voters have a choice in financing local government needs WHO CAN HAVE IT? Under the 1963 Local Option Revenue Act (found in Tennessee Code Annotated, Sections 67-6-701,

Sales Tax Handbook TENNESSEE LAW 1 Voters have a choice in financing local government needs WHO CAN HAVE IT? Under the 1963 Local Option Revenue Act (found in Tennessee Code Annotated, Sections 67-6-701,

PROPERTY TAX 101 PRESENTED BY: TORRANCE COUNTY ASSESSOR - BETTY CABBER HIDALGO COUNTY TREASURER - TYLER MASSEY

PROPERTY TAX 101 PRESENTED BY: TORRANCE COUNTY ASSESSOR - BETTY CABBER HIDALGO COUNTY TREASURER - TYLER MASSEY What does all of this mean!? ASSESSMENTS RESIDENTAL NON RESIDENTIAL PERSONAL PROPERTY PROTEST

PROPERTY TAX 101 PRESENTED BY: TORRANCE COUNTY ASSESSOR - BETTY CABBER HIDALGO COUNTY TREASURER - TYLER MASSEY What does all of this mean!? ASSESSMENTS RESIDENTAL NON RESIDENTIAL PERSONAL PROPERTY PROTEST

Cash and investments $ 605,231,424 $ 21,810,533 $ 627,041,957 $ 4,640,569 $ 5,605,829 $ 10,269,116. Other capital assets, net of.

A - 1 MECKLENBURG COUNTY, NORTH CAROLINA STATEMENT OF NET ASSETS (DEFICIT) JUNE 30, 2007 ASSETS Primary Government Component Units Public Library Mecklenburg Mecklenburg of Charlotte and Emergency County

A - 1 MECKLENBURG COUNTY, NORTH CAROLINA STATEMENT OF NET ASSETS (DEFICIT) JUNE 30, 2007 ASSETS Primary Government Component Units Public Library Mecklenburg Mecklenburg of Charlotte and Emergency County

City of Timmins Tax and Water Collections Frequently Asked Tax Questions. Who is responsible for Property Assessment & Taxation?

City of Timmins Tax and Water Collections Frequently Asked Tax Questions Who is responsible for Property Assessment & Taxation? Provincial and municipal governments and the Municipal Property Assessment

City of Timmins Tax and Water Collections Frequently Asked Tax Questions Who is responsible for Property Assessment & Taxation? Provincial and municipal governments and the Municipal Property Assessment

PERSONAL PROPERTY TAX RELIEF ACT SPECIAL REVIEW SEPTEMBER 2004

PERSONAL PROPERTY TAX RELIEF ACT SPECIAL REVIEW SEPTEMBER 2004 EXECUTIVE SUMMARY We have completed our study of the Personal Property Tax Relief Act (the Act) as amended by Chapter 1 of the Act of Assembly

PERSONAL PROPERTY TAX RELIEF ACT SPECIAL REVIEW SEPTEMBER 2004 EXECUTIVE SUMMARY We have completed our study of the Personal Property Tax Relief Act (the Act) as amended by Chapter 1 of the Act of Assembly

State-Collected Local Taxes: Basis of Distribution

State-Collected Local Taxes: Basis of Distribution PREPARED BY THE NORTH CAROLINA LEAGUE OF MUNICIPALITIES -- MARCH 2018 Powell Bill Funds Distribution Schedule: Powell Bill proceeds are distributed twice

State-Collected Local Taxes: Basis of Distribution PREPARED BY THE NORTH CAROLINA LEAGUE OF MUNICIPALITIES -- MARCH 2018 Powell Bill Funds Distribution Schedule: Powell Bill proceeds are distributed twice

DUTIES AND FUNCTIONS OF THE ASSESSOR S OFFICE. Adrianna S. Hedwall, CCMA II Assessor

DUTIES AND FUNCTIONS OF THE ASSESSOR S OFFICE Adrianna S. Hedwall, CCMA II Assessor On the first day of Assessor s School we are taught 3 things. The assessment date is always October 1 st, assessments

DUTIES AND FUNCTIONS OF THE ASSESSOR S OFFICE Adrianna S. Hedwall, CCMA II Assessor On the first day of Assessor s School we are taught 3 things. The assessment date is always October 1 st, assessments

Chapter 2 Books, Records, Accounts and Vouchers

Public Records Authority Chapter 2 Books, Records, Accounts and Vouchers 1. Ch. 66, Ch. 4 7(26) and 950 CMR 32.01-32.09 regulate access to public records. 2. Public records include all books, papers, maps,

Public Records Authority Chapter 2 Books, Records, Accounts and Vouchers 1. Ch. 66, Ch. 4 7(26) and 950 CMR 32.01-32.09 regulate access to public records. 2. Public records include all books, papers, maps,

Property Tax Refund (Credit) Claim. You must file this form, or Arizona Form 204, by April 17, 2018.

Claim. You must file this form, or Arizona Form 204, by April 17, 2018.") DO NOT STAPLE ANY ITEMS TO THE CLAIM. Arizona Form 140PTC You must file this form, or Arizona Form 204, by April 17, 2018. 82F Check box 82F if filing under extension 95 Check box 95 if amending claim

DO NOT STAPLE ANY ITEMS TO THE CLAIM. Arizona Form 140PTC You must file this form, or Arizona Form 204, by April 17, 2018. 82F Check box 82F if filing under extension 95 Check box 95 if amending claim

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2011 H 1 HOUSE BILL 861. Short Title: Local Option Tax Menu. (Public)

") GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 H HOUSE BILL Short Title: Local Option Tax Menu. (Public) Sponsors: Referred to: Representative Michaux (Primary Sponsor). For a complete list of Sponsors,

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 H HOUSE BILL Short Title: Local Option Tax Menu. (Public) Sponsors: Referred to: Representative Michaux (Primary Sponsor). For a complete list of Sponsors,

Department of Public Works Water & Sewer Divisions. Water & Sewer Divisions Customer Service Policy & Procedure Manual

Department of Public Works Customer Service Page 1 I. Application for Service Anyone may apply for water and/or sewer service to a property provided they are the owner, owner s agent, or an occupant of

Department of Public Works Customer Service Page 1 I. Application for Service Anyone may apply for water and/or sewer service to a property provided they are the owner, owner s agent, or an occupant of

ALAMEDA COUNTY ASSESSMENT APPEALS BOARD AND EQUALIZATION HEARING OFFICER INSTRUCTION BOOKLET

ALAMEDA COUNTY ASSESSMENT APPEALS BOARD AND EQUALIZATION HEARING OFFICER INSTRUCTION BOOKLET OFFICE OF THE CLERK-ADMINISTRATOR ASSESSMENT APPEALS BOARD P. O. BOX 1499 OAKLAND, CA 94612-1499 (510) 272-3854

ALAMEDA COUNTY ASSESSMENT APPEALS BOARD AND EQUALIZATION HEARING OFFICER INSTRUCTION BOOKLET OFFICE OF THE CLERK-ADMINISTRATOR ASSESSMENT APPEALS BOARD P. O. BOX 1499 OAKLAND, CA 94612-1499 (510) 272-3854

BOROUGH OF AVALON NOTES TO FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2000

Note 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Description of Financial Reporting Entity - The Borough of Avalon is a seashore community located on the Atlantic Ocean in the County of Cape May, State

Note 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Description of Financial Reporting Entity - The Borough of Avalon is a seashore community located on the Atlantic Ocean in the County of Cape May, State

The changes in the bill are not expected to have an impact on state revenues.

Department Technical Bill March 28, 2003 Separate Official Fiscal Note Requested Yes No Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 759 (Abrams)/ S.F. 1007 (Moua)

Department Technical Bill March 28, 2003 Separate Official Fiscal Note Requested Yes No Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 759 (Abrams)/ S.F. 1007 (Moua)

BASIC FINANCIAL STATEMENTS

BASIC FINANCIAL STATEMENTS 16 Exhibit A STATEMENT OF NET ASSETS JUNE 30, 2009 Primary Government Governmental Business-Type Activities Activities Total Assets: Cash and investments $ 24,006,801 $ 2,319,359

BASIC FINANCIAL STATEMENTS 16 Exhibit A STATEMENT OF NET ASSETS JUNE 30, 2009 Primary Government Governmental Business-Type Activities Activities Total Assets: Cash and investments $ 24,006,801 $ 2,319,359

Real Estate Bill: Taxpayer Information

Taxpayer Information Real Estate Bill: There are two types of taxes: Current Taxes: Taxes paid on or before December 31 st of the current Tax Year Delinquent Taxes: Taxes paid after December 31 st of the

Taxpayer Information Real Estate Bill: There are two types of taxes: Current Taxes: Taxes paid on or before December 31 st of the current Tax Year Delinquent Taxes: Taxes paid after December 31 st of the

RESOLUTION NUMBER 3415

RESOLUTION NUMBER 3415 A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF PERRIS, ACTING AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO. 2001-3 (NORTH PERRIS PUBLIC SAFETY) OF THE CITY OF PERRIS,

RESOLUTION NUMBER 3415 A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF PERRIS, ACTING AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO. 2001-3 (NORTH PERRIS PUBLIC SAFETY) OF THE CITY OF PERRIS,

ASSESSOR S CALENDAR. Assessor Submits Tax Numbers The assessor must provide a list of tax numbers to be recorded by the county recorder without fee.

CONTINUOUS MONTHLY (JANUARY MAY) JANUARY 1 Assessor Submits Tax Numbers The assessor must provide a list of tax numbers to be recorded by the county recorder without fee. Land Sale Certificate The director

CONTINUOUS MONTHLY (JANUARY MAY) JANUARY 1 Assessor Submits Tax Numbers The assessor must provide a list of tax numbers to be recorded by the county recorder without fee. Land Sale Certificate The director

MARION COUNTY FY BUDGET BY DEPARTMENT ASSESSOR ASSESSOR/TAX. Special Projects MISSION STATEMENT

/TAX Chief Deputy Assessor/Tax Collector Assessor/Tax Collector Valuation Appraisal Tax Collection Cartography Administration Commercial/ Industrial/ Personal Property Appraisal Farm Appraisal Special

/TAX Chief Deputy Assessor/Tax Collector Assessor/Tax Collector Valuation Appraisal Tax Collection Cartography Administration Commercial/ Industrial/ Personal Property Appraisal Farm Appraisal Special

RULES OF THE TENNESSEE STATE BOARD OF EQUALIZATION CHAPTER TAX RELIEF TABLE OF CONTENTS

RULES OF THE TENNESSEE STATE BOARD OF EQUALIZATION CHAPTER 0600-03 TAX RELIEF TABLE OF CONTENTS 0600-03-.01 Determination of Reimbursable or 0600-03-.08 Income Requirement Local Property Taxes Provided

RULES OF THE TENNESSEE STATE BOARD OF EQUALIZATION CHAPTER 0600-03 TAX RELIEF TABLE OF CONTENTS 0600-03-.01 Determination of Reimbursable or 0600-03-.08 Income Requirement Local Property Taxes Provided

HARNETT COUNTY Request for Proposals Harnett County 2022 Real Property Reappraisal. Date: March 25, I. Introduction:

HARNETT COUNTY Request for Proposals Harnett County 2022 Real Property Reappraisal Date: March 25, 2019 I. Introduction: Harnett County is soliciting Proposals (Bids) from qualified firms (hereinafter

HARNETT COUNTY Request for Proposals Harnett County 2022 Real Property Reappraisal Date: March 25, 2019 I. Introduction: Harnett County is soliciting Proposals (Bids) from qualified firms (hereinafter

Plainfield Community Consolidated School District #202 LOCAL PROPERTY TAX TOPICS, INFORMATION, AND THE 2016 TAX

Plainfield Community Consolidated School District #202 LOCAL PROPERTY TAX TOPICS, INFORMATION, AND THE 2016 TAX LEVY 1 Table of Contents I. Overview of the Tax Levy and Extension Process II. Calculating

Plainfield Community Consolidated School District #202 LOCAL PROPERTY TAX TOPICS, INFORMATION, AND THE 2016 TAX LEVY 1 Table of Contents I. Overview of the Tax Levy and Extension Process II. Calculating

WHEREAS, notice of the public hearing was duly given as required by Section of the Act or has been duly waived by the property owner; and

RESOLUTION NUMBER 4983 A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF PERRIS, ACTING AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO. 2001-3 (NORTH PERRIS PUBLIC SAFETY) OF THE CITY OF PERRIS,

RESOLUTION NUMBER 4983 A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF PERRIS, ACTING AS THE LEGISLATIVE BODY OF COMMUNITY FACILITIES DISTRICT NO. 2001-3 (NORTH PERRIS PUBLIC SAFETY) OF THE CITY OF PERRIS,

GENERAL FUND TAX SUPPORT 100% 100% 100%

TAX COLLECTOR The Tax Collector bills, collects and distributes all taxes for the County, Municipalities, Tourist Development Council, School Board, and taxing districts. The Tax Collector issues licenses

TAX COLLECTOR The Tax Collector bills, collects and distributes all taxes for the County, Municipalities, Tourist Development Council, School Board, and taxing districts. The Tax Collector issues licenses

Assessments, Reappraisals and Millage Rates. Taxable Property. FSPPC114 Administration of Arkansas Property Tax

FSPPC114 Administration of Arkansas Property Tax Property tax is an important source of revenue for local governments, including school districts and county and city governments. Revenue generated by the

FSPPC114 Administration of Arkansas Property Tax Property tax is an important source of revenue for local governments, including school districts and county and city governments. Revenue generated by the

Abatements and Refunds

Abatements and Refunds Janeen Ogden Colorado Division of Property Taxation CCTA Conference Colorado Springs, Colorado June 29, 2010 1 Abatements & Refunds Definitions Need for Abatements History of Abatement

Abatements and Refunds Janeen Ogden Colorado Division of Property Taxation CCTA Conference Colorado Springs, Colorado June 29, 2010 1 Abatements & Refunds Definitions Need for Abatements History of Abatement

LOCAL HAZARD MITIGATION PLAN UPDATE CHECKLIST

D LOCAL HAZARD MITIGATION PLAN UPDATE CHECKLIST This section of the Plan includes a completed copy of the Local Hazard Mitigation Checklist as provided by the North Carolina Division of Emergency Management.

D LOCAL HAZARD MITIGATION PLAN UPDATE CHECKLIST This section of the Plan includes a completed copy of the Local Hazard Mitigation Checklist as provided by the North Carolina Division of Emergency Management.

THANK YOU FOR CHOOSING SUGAR & BRUNO! WE RE THRILLED TO HAVE YOU AS A CUSTOMER AND WE LOOK FORWARD TO WORKING WITH OUR FOR MANY YEARS TO COME!

NEW CUSTOMER FORM Sugar and Bruno, Inc. 7260 Georgetown Road Indianapolis, Indiana 46268 www.sugarandbruno.com PH: 317.991.4422 FX: 317.293.5886 THANK YOU FOR CHOOSING SUGAR & BRUNO! WE RE THRILLED TO

NEW CUSTOMER FORM Sugar and Bruno, Inc. 7260 Georgetown Road Indianapolis, Indiana 46268 www.sugarandbruno.com PH: 317.991.4422 FX: 317.293.5886 THANK YOU FOR CHOOSING SUGAR & BRUNO! WE RE THRILLED TO

OFFICE OF JOE G. TEDDER, CFC Tax Collector for Polk County, Florida

OFFICE OF JOE G. TEDDER, CFC Tax Collector for Polk County, Florida The Guiding Principles are our organization s beliefs. They help us understand: MISSION What we do VISION Where we are going SHARED VALUES

OFFICE OF JOE G. TEDDER, CFC Tax Collector for Polk County, Florida The Guiding Principles are our organization s beliefs. They help us understand: MISSION What we do VISION Where we are going SHARED VALUES

FACTS ABOUT AIRCRAFT & BOAT ASSESSMENTS. LESLIE MORGAN Shasta County Assessor-Recorder

FACTS ABOUT AIRCRAFT & BOAT ASSESSMENTS LESLIE MORGAN Shasta County Assessor-Recorder Shasta County does not discriminate on the basis of disability. Our ADA Coordinator may be reached at 530-225-5515;

FACTS ABOUT AIRCRAFT & BOAT ASSESSMENTS LESLIE MORGAN Shasta County Assessor-Recorder Shasta County does not discriminate on the basis of disability. Our ADA Coordinator may be reached at 530-225-5515;

The APR will vary with the market based on the Prime Rate. Option A

VISA/MASTERCARD CARDHOLDER AGREEMENT AND DISCLOSURE STATEMENT M-122374 (10/17) TINKER FEDERAL CREDIT UNION VISA/MASTERCARD Interest Rates and Interest Charges ANNUAL PERCENTAGE RATE (APR) for Purchases

VISA/MASTERCARD CARDHOLDER AGREEMENT AND DISCLOSURE STATEMENT M-122374 (10/17) TINKER FEDERAL CREDIT UNION VISA/MASTERCARD Interest Rates and Interest Charges ANNUAL PERCENTAGE RATE (APR) for Purchases

Local Taxes and Tax Collection

16 Local Taxes and Tax Collection The most significant local tax legislation enacted by the 2006 General Assembly affects the collection of delinquent property taxes. Beginning with the 2006 07 tax year,

16 Local Taxes and Tax Collection The most significant local tax legislation enacted by the 2006 General Assembly affects the collection of delinquent property taxes. Beginning with the 2006 07 tax year,

Appendix A: Overview of Illinois property tax system

Appendix A: Overview of Illinois property tax system Across Illinois, more than 6,000 units of government billed taxpayers a total of $29.8 billion in 2017, $19.2 billion of which was billed to residential

Appendix A: Overview of Illinois property tax system Across Illinois, more than 6,000 units of government billed taxpayers a total of $29.8 billion in 2017, $19.2 billion of which was billed to residential

NHTCA New Tax Collector Training Series. The Tax Year

NHTCA New Tax Collector Training Series The Tax Year Property Tax Collection By the Book Warrants & Billing Forms of Payment Collections Other Taxes Land Use Change Tax (LUCT) Yield Taxes Doomage Excavation

NHTCA New Tax Collector Training Series The Tax Year Property Tax Collection By the Book Warrants & Billing Forms of Payment Collections Other Taxes Land Use Change Tax (LUCT) Yield Taxes Doomage Excavation

August 2017 Legal Calendar

1 Assessor On or before this date, the assessor must forward approved homestead exemption applications and a copy of the certification of disability status to the Tax Commissioner. 77-3517(1) 1 Assessor

1 Assessor On or before this date, the assessor must forward approved homestead exemption applications and a copy of the certification of disability status to the Tax Commissioner. 77-3517(1) 1 Assessor

INFORMATION FOR THE MIDDLEBOROUGH TAXPAYER

INFORMATION FOR THE MIDDLEBOROUGH TAXPAYER The Board of Assessors Anthony Freitas, Chairman Paula Burdick Frederick Eayrs and Barbara Erickson, M.A.A. Assessor/Appraiser Town of Middleborough Assessors

INFORMATION FOR THE MIDDLEBOROUGH TAXPAYER The Board of Assessors Anthony Freitas, Chairman Paula Burdick Frederick Eayrs and Barbara Erickson, M.A.A. Assessor/Appraiser Town of Middleborough Assessors

TOWN OF LILLINGTON FISCAL YEAR (FY) BUDGET MESSAGE

BUDGET MESSAGE") TOWN OF LILLINGTON June 13, 2017 Mayor Glenn McFadden Mayor Pro Tempore Judy Breeden Commissioner Rupert Langdon Commissioner Dianne Johnson Commissioner Marshall Page Commissioner Paul Phillips FISCAL

TOWN OF LILLINGTON June 13, 2017 Mayor Glenn McFadden Mayor Pro Tempore Judy Breeden Commissioner Rupert Langdon Commissioner Dianne Johnson Commissioner Marshall Page Commissioner Paul Phillips FISCAL

Department of Revenue Analysis of H.F (Abrams)/ S.F (Moua) As Proposed to be Amended. General Fund $0 $0 $0 $0

/ S.F (Moua) As Proposed to be Amended. General Fund $0 $0 $0 $0") Department Policy Bill March 15, 2004 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 2552 (Abrams)/ S.F. 2716 (Moua) As Proposed

Department Policy Bill March 15, 2004 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 2552 (Abrams)/ S.F. 2716 (Moua) As Proposed

CAROLE KEETON STRAYHORN,

Truth-In-Taxation A Guide for Setting School District Tax Rates July 2006 CAROLE KEETON STRAYHORN, Texas Comptroller TEXAS PROPERTY TAX Truth-In-Taxation A Guide for Setting School District Tax Rates

Truth-In-Taxation A Guide for Setting School District Tax Rates July 2006 CAROLE KEETON STRAYHORN, Texas Comptroller TEXAS PROPERTY TAX Truth-In-Taxation A Guide for Setting School District Tax Rates

Title 36: TAXATION. Chapter 908: DEFERRED COLLECTION OF HOMESTEAD PROPERTY TAXES. Table of Contents Part 9. TAXPAYER BENEFIT PROGRAMS...

Title 36: TAXATION Chapter 908: DEFERRED COLLECTION OF HOMESTEAD PROPERTY TAXES Table of Contents Part 9. TAXPAYER BENEFIT PROGRAMS... Section 6250. DEFINITIONS... 3 Section 6251. DEFERRAL OF TAX ON HOMESTEAD;

Title 36: TAXATION Chapter 908: DEFERRED COLLECTION OF HOMESTEAD PROPERTY TAXES Table of Contents Part 9. TAXPAYER BENEFIT PROGRAMS... Section 6250. DEFINITIONS... 3 Section 6251. DEFERRAL OF TAX ON HOMESTEAD;

APPLICATION FOR PROPERTY TAX RELIEF

STATE OF NORTH CAROLINA Henderson County North Carolina - Year 2018 APPLICATION FOR PROPERTY TAX RELIEF ELDERLY OR DISABLED EXCLUSION (G.S. 105-277.1), DISABLED VETERAN EXCLUSION (G.S. 105-277.1C), or

STATE OF NORTH CAROLINA Henderson County North Carolina - Year 2018 APPLICATION FOR PROPERTY TAX RELIEF ELDERLY OR DISABLED EXCLUSION (G.S. 105-277.1), DISABLED VETERAN EXCLUSION (G.S. 105-277.1C), or

Georgia Department of Revenue GATO Tax Assessors and Tax Commissioners

GATO 2018 Tax Assessors and Tax Commissioners Danny Forsyth Compliance Specialist 1 Kenny Colson Compliance Specialist 3 Local Government Services Division Georgia Department of Revenue January 1 st

GATO 2018 Tax Assessors and Tax Commissioners Danny Forsyth Compliance Specialist 1 Kenny Colson Compliance Specialist 3 Local Government Services Division Georgia Department of Revenue January 1 st

IC Chapter 41. Cumulative Fund Tax Levy Procedures

IC 6-1.1-41 Chapter 41. Cumulative Fund Tax Levy Procedures IC 6-1.1-41-1 Application of chapter Sec. 1. This chapter applies to establishing and imposing a tax levy for cumulative funds under the following:

IC 6-1.1-41 Chapter 41. Cumulative Fund Tax Levy Procedures IC 6-1.1-41-1 Application of chapter Sec. 1. This chapter applies to establishing and imposing a tax levy for cumulative funds under the following:

CTAS e-li. Published on e-li ( November 28, 2018 Trustee's Records

Published on e-li (http://eli.ctas.tennessee.edu) November 28, 2018 Dear Reader: The following document was created from the CTAS electronic library known as e-li. This online library is maintained daily

Published on e-li (http://eli.ctas.tennessee.edu) November 28, 2018 Dear Reader: The following document was created from the CTAS electronic library known as e-li. This online library is maintained daily

FY16 REVENUES. FY 15 Adopted Taxes. General Fund $ $ $ Voter Approved Debt Service $37.30 $36.90 $37.50

FY16 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments, federal and state grants,

FY16 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments, federal and state grants,

Combining & Individual Fund Statements & Schedules

Combining & Individual Fund Statements & Schedules Provides detailed statements for the nonmajor Special Revenue and Capital Projects Funds and the Agency Fiduciary Funds, budget to actual schedules for

Combining & Individual Fund Statements & Schedules Provides detailed statements for the nonmajor Special Revenue and Capital Projects Funds and the Agency Fiduciary Funds, budget to actual schedules for

MI Connection Communications System (A North Carolina Interlocal Agency)

") MI Connection Communications System (A North Carolina Interlocal Agency) Financial Statements For the Year Ended June 30, 2014 TABLE OF CONTENTS Page No. INDEPENDENT AUDITORS REPORT... 1 MANAGEMENT'S DISCUSSION

MI Connection Communications System (A North Carolina Interlocal Agency) Financial Statements For the Year Ended June 30, 2014 TABLE OF CONTENTS Page No. INDEPENDENT AUDITORS REPORT... 1 MANAGEMENT'S DISCUSSION

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2011 SESSION LAW HOUSE BILL 129

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2011 SESSION LAW 2011-84 HOUSE BILL 129 AN ACT TO PROTECT JOBS AND INVESTMENT BY REGULATING LOCAL GOVERNMENT COMPETITION WITH PRIVATE BUSINESS. Whereas, certain

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2011 SESSION LAW 2011-84 HOUSE BILL 129 AN ACT TO PROTECT JOBS AND INVESTMENT BY REGULATING LOCAL GOVERNMENT COMPETITION WITH PRIVATE BUSINESS. Whereas, certain

INTRODUCTION. Transmittal Letter Executive Summary FY2016 Budget Roadmap

Introduction INTRODUCTION On May 28, 2015, County Manager Dena Diorio presented her FY2016 Recommended Budget to the Board of County Commissioners in the chamber of the Government Center. Transmittal Letter

Introduction INTRODUCTION On May 28, 2015, County Manager Dena Diorio presented her FY2016 Recommended Budget to the Board of County Commissioners in the chamber of the Government Center. Transmittal Letter

Department of Revenue Analysis of H.F. 751 (Abrams) / S.F. 748 (Belanger) As Proposed to Be Amended

/ S.F. 748 (Belanger) As Proposed to Be Amended") Governor s Tax Bill Original and Supplemental Proposals April 4, 2003 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 751 (Abrams)

Governor s Tax Bill Original and Supplemental Proposals April 4, 2003 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 751 (Abrams)

10 SB 346/AP A BILL TO BE ENTITLED AN ACT

SB 346/AP Senate Bill 346 By: Senators Rogers of the 21st, Williams of the 19th, Thompson of the 33rd, Seabaugh of the 28th, Butterworth of the 50th and others AS PASSED A BILL TO BE ENTITLED AN ACT 1

SB 346/AP Senate Bill 346 By: Senators Rogers of the 21st, Williams of the 19th, Thompson of the 33rd, Seabaugh of the 28th, Butterworth of the 50th and others AS PASSED A BILL TO BE ENTITLED AN ACT 1

This handbook is an on-line publication of the Vermont League of Cities and Towns Municipal Assistance Center.

This handbook is an on-line publication of the Vermont League of Cities and Towns Municipal Assistance Center. Please be aware that the electronic versions of VLCT handbooks are not exact reproductions

This handbook is an on-line publication of the Vermont League of Cities and Towns Municipal Assistance Center. Please be aware that the electronic versions of VLCT handbooks are not exact reproductions

Online Presentment and Payment FAQ s

General Online Presentment and Payment FAQ s What are some of the benefits of receiving my bill electronically? It is convenient, saves time, reduces errors, allows you to receive bills anywhere at any

General Online Presentment and Payment FAQ s What are some of the benefits of receiving my bill electronically? It is convenient, saves time, reduces errors, allows you to receive bills anywhere at any

ADOPTION OF FISCAL YEAR 2006 OPERATING AND CAPITAL BUDGETS

ADOPTION OF FISCAL YEAR 2006 OPERATING AND CAPITAL BUDGETS Agenda Item Title: Adoption of Fiscal Year 2006 Operating and Capital Budgets Specific Action Requested: That the Board of Commissioners adopts

ADOPTION OF FISCAL YEAR 2006 OPERATING AND CAPITAL BUDGETS Agenda Item Title: Adoption of Fiscal Year 2006 Operating and Capital Budgets Specific Action Requested: That the Board of Commissioners adopts

January 2013 Session of the Connecticut General Assembly. Public Act No (Substitute Senate Bill No. 70)

") January 2013 Session of the Connecticut General Assembly Public Act No. 13-48 (Substitute Senate Bill No. 70) AN ACT RESTORING BENEFITS TO VETERANS DISCHARGED UNDER "DON'T ASK, DON'T TELL" Section 1 of

January 2013 Session of the Connecticut General Assembly Public Act No. 13-48 (Substitute Senate Bill No. 70) AN ACT RESTORING BENEFITS TO VETERANS DISCHARGED UNDER "DON'T ASK, DON'T TELL" Section 1 of

Motor Vehicle Excise Information

Motor Vehicle Excise Information Our office has produced this booklet as a public service. There may be other offices to contact for specific information regarding your excise tax bill. The following offices

Motor Vehicle Excise Information Our office has produced this booklet as a public service. There may be other offices to contact for specific information regarding your excise tax bill. The following offices