AASTHI (GIS BASED PROPERTY TAX SYSTEM) Dept of Urban Development Govt. of Karnataka. Directorate of Municipal Administration

|

|

|

- Coleen Francis

- 5 years ago

- Views:

Transcription

1 AASTHI (GIS BASED PROPERTY TAX SYSTEM) Directorate of Municipal Administration Dept of Urban Development Govt. of Karnataka

2 Agenda Taxation Systems CVS method of Property Tax in Karnataka Municpal Reforms AASTHI (GIS BASED PROPERTY TAX SYSTEM)

3 TAXATION SYSTEMS

4 Why Taxation? The main obligatory functions of the Urban Local Bodies are as follows. Drinking water supply. Street light facilities. Sanitation work. Providing Roads, Drains, Culverts etc

5 Why Taxation? There must be a source of income to provide the above amenities.. Constitution of India empowered State Government to levy Tax on Land and Building by providing an entry at item No. 49 in list II of seventh schedule there in

6 Characteristics of Good taxation System Transparent Assessment of Taxes No Discretionary power Low Tax to avoid the incentive to evade Ensure Equity between classes of tax payers High Penalties for tax evaders

7 Annual Rental Value Annual Rental Value is the rental value which a building is likely to fetch The annual ratable value was calculated on the annual gross rent. The rate of tax for each category of ULBs was as follows. Corporation 20% - 25% CMC 20% TMC/TP 15%

8 Annual Rental Value Rental Based valuation Plagued by rent control acts There was no formal course of training for these Assessors nor are any specific steps taken to ensure objectivity of the assessment. These Assessors were appointed to the ULBs once in Five years for revision of assessment. Discretionary powers to the Officials

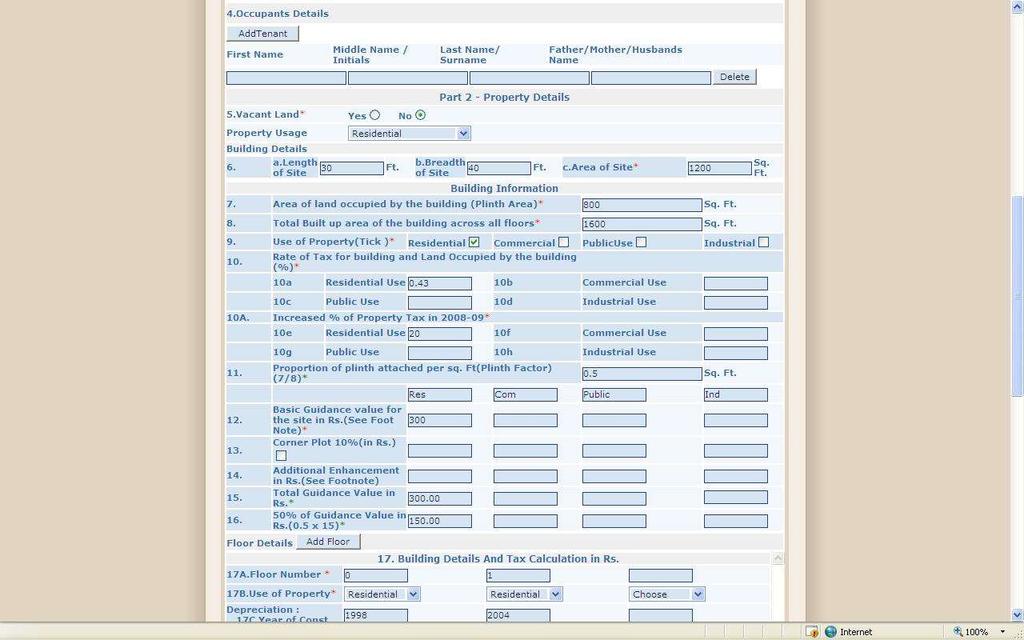

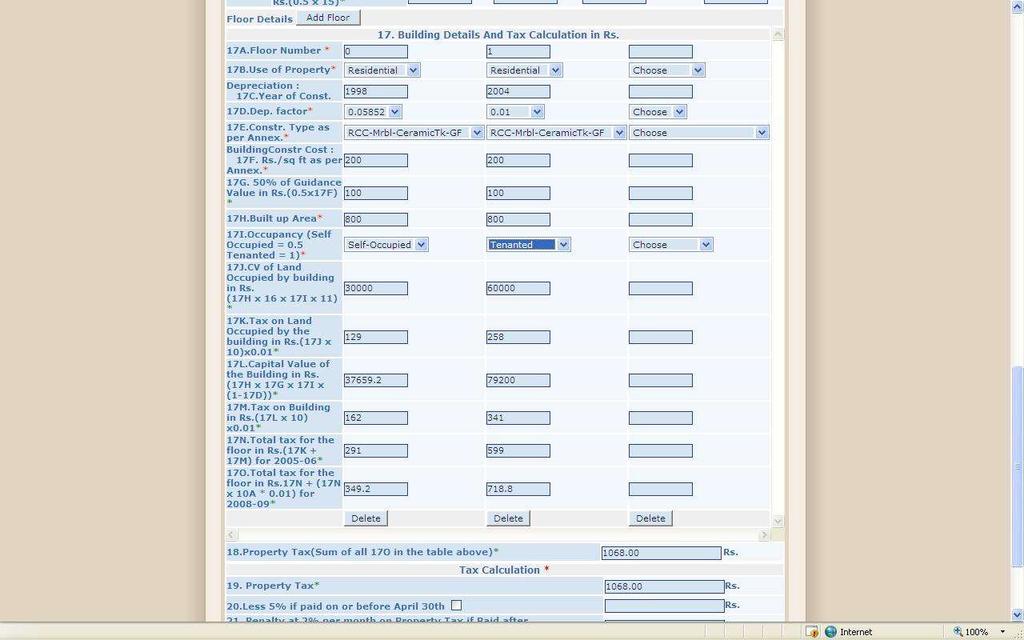

9 CVS Other taxation Systems Capital Values System (CVS) : Market Value of the Property Unit Area Method (UAM) Basic Tax is based on Plinth/Carpet Area

10 Main Factors for CVS Location Usage ( Residential/Commercial/Industrial/Public) Occupancy (Self Occupied/ Tenanted) Construction Type ( Based on the type of construction used for the Building) Depreciation Factor (How old is the building)

11 CVS METHOD OF PROPERTY TAX IN KARNATAKA

12 Property Tax Reforms Self Assessment based on Capital Value System introduced on with the following Intentions Comply with the Court Directives Increasing Own Tax Revenues Transparency in the Tax Calculation

13 Property Tax Reforms Property tax is levied on building and vacant land situated within the municipal area. The property tax is based on valuation of the property. There are two methods of valuation of property. For the purpose of purchase or compulsory acquisition of land the valuation is based on the actual market value of the property. For the purpose of taxation the valuation is based on market value guidelines published under section 45B of the Stamp Act. (taxable capital value of property.)

14 Property Tax on Building The calculation of property tax may be made simple using the following formula: - Building Value = cost of erection of building x Plinth area of the building Depreciation of building = Depreciation quotient based on age of building x Building Value Capital value of land = Market value of land per square feet x Area of the land Taxable capital value of building = Capital value of land + Building Value Depreciation of building Property tax = Rate of property tax x Taxable capital value of building

15 Rate of tax for Commercial Properties section 101 (2)(a) of Karnataka Municipalities Act 1964 and section 108 (2)(a) of Karnataka Municipal Corporation Act Population Minimum Rate Maximum Rate < 1 Lakh Population >1 Lakh Population 0.5% 0.9% 0.5% 2%

16 Rate of tax for Residential Properties Section 101 2(b) of Karnataka Municipalities Act 1964 and section 108(2)(b) of Karnataka Municipal corporation Act 1976 Population Minimum Rate Maximum Rate < 1 Lakh Population >1 Lakh Population 0.3% 0.6% 0.3% 1%

17 Rate of tax for Vacant Lands Section 101 (2)(A) Exemption from payment of Property Tax for vacant land situated within the Municipal Area having population of less than one lakh. Section 101 (2)(c)(d)(e) of Karnataka Municipalities Act 1964 & section 108 (2)(c) (d)(e) of Karnataka Municipal Corporation Act 1976 Population Minimum Rate Maximum Rate < sq. Ft 0.1% 0.5% >= and < sq. Ft 0.025% 0.1% >= sq. Ft 0.01% 0.1%

18 Method of Assessment and property Tax Section 102 of Karnataka Municipalities Act 1964 & section 109 of Karnataka Municipal Corporation Act 1976 The taxable capital value of such land shall be assessed having regard to the Market value guidelines and properties published under section 45B of Karnataka stamp Act 1957 Fifty percent discount is allowed with effect from , prior to that, at 100% of the Market value guide lines so fixed by the committee constituted under section 45B of Karnataka stamp Act This applies to vacant lands also which are liable for payment of tax

19 Depreciation at the time of assessment Depreciation is allowed to the buildings up to sixty years old, as per standard rate depreciation for buildings as prescribed by the PWD Department Government of Karnataka vide PWD hand book vol 11 pages 55 & 56 of the edition 1958.

20 Rebate for self occupied building Section 103 of Karnataka Municipalities Act 1964 & section 109A of Karnataka Municipal Corporation Act % rebate is allowed for the self occupied building by the kathedras/owner of the respective buildings.

21 Rebate of 5% on the amount payable Section 105 (1) para (2) of Karnataka Municipalities Act 1964 & section 112A para (2) of Karnataka Municipal Corporation Act The owner or occupier who is liable to pay Tax, files the respective returns together with the bank challen for having paid the Property Tax within a month from the date of commencement of each financial year (i.e. with is 30th April of each year), shall be allowed a rebate of five percent on the Tax payable by them

22 ENHANCE THE PROPERTY TAX SECTION 102A of Karnataka Municipalities Act 1964 & section 109A of Karnataka Municipal Corporations Act The ULBs shall not be assessed each year thereafter but shall stand enhanced by 15% once in every three years commencing from the financial year but the ULBs may enhance property Tax up to 30% once in three years different rates of enhancement may be made to different areas and different class of buildings and lands. Provided further that the non assessment of property Tax under this section during the block period of three years, shall not be applicable to a building in respect of which, there is any addition alteration or variation to it.

23 Penalty

24 Penalty Levy of penalty at 2% Vide Section 105 (8) of Karnataka Municipalities Act 1964 & section 112A (5)(a) of Karnataka Municipal Corporation Act 1976: Levy of penalty of Rs 100/- : Section 105 (5) (c) of Karnataka Municipalities Act 1964 & section 112A (5)(c) of Karnataka Municipal Corporation Act Levy of penalty at two times. Vide section 105(b) of Karnataka Municipalities Act of 1964 & section 112A (5)(b) of Karnataka Municipal Corporation Act 1976

25 Levy of penalty on unlawful buildings:- Section 107 of Karnataka Municipalities Act 1964 and Rule 22 of the Karnataka Municipalities Taxation Rules 2002 & section 112-C of Karnataka Municipal Corporations Act 1976 and Rule 12 of Karnataka Municipal Corporations Taxation amendment Rules For any unlawful construction or reconstruction of any building or part a building. Unlawful means. Without obtaining permission under the provisions of KM Act Layout formed with out approval under the relevant law as prescribed under Town and country planning Act. Land in breach of any provisions of the KM Act 1964 or any rule or bye law made there under or any direction or requisitions lawfully given or made under KM Act 1964 a rule ruler or bye-law.

26 Levy of penalty on unlawful buildings:- For these types and un law full, the concerned persons shall be liable to pay every year a penalty which shall be equal to twice the property tax levlable on such building, so long as it remains as unlawful constructions without prejudice any proceedings which may be instituted against the concerned in respect of such unlawful constructions, but such levy and collection of penalty shall not be construed as regularization of such unlawful construction or reconstruction.

27 Challenges in Implementing CVS Completely vacant land s are taxed Appurtenant land is taxed. Determination of capital value based on 45B. Based one time transaction Increases several fold within small span of years Not properly fixed. Tax will become very high 28

28 Overcoming the challenges Completely vacant land needs to be taxed Tax on appurtenant land abolished Municipal council given powers to vary 45 B values up to certain limit for property taxation from Tax Fixed for three years (an option to increase the tax by % every 3 years). For to , Property Tax restricted to 2 times of ARV property Tax (Reasonable as most ULBs had not revised property tax for more than 7 years)

29 MUNICIPAL REFORMS

30 Urban scenario in Karnataka Categories of Urban Local Bodies in State City Corporations 09 City Municipal Councils (0.5 to 3.0 lakhs population) 42 Total 213 ULBs Town Panchayaths (0.1 to 0.2 lakhs population) 68 Town Municipal Councils (0.20 to 0.50 lakhs population) 94

31 Good Governance Competent and Qualified Manpower Sound Financial System Efficient planning & Budgeting Assets Management Optimum Resource Mobilization Coordination & Good Team Work Use of IT to improve efficiency / Monitoring of service delivery

32 Good Governance Contd... Citizens Participation Transparent Citizen Interface Timely redressal of Citizen Grievances Reducing direct Citizen Officer interface Respect for Human Right

33 Background The Urban Development Department, GoK through the Directorate of Municipal Administration launched Municipal Reforms along with Computerization of all Urban Local Bodies in the year 2004 With Financial assistance from the Asian Development Bank (for NNP) and World Bank (for KMRP) To upgrade all ULBs from the existing manual system to Computer based systems, thus streamlining ULB s Municipal functions through process re-engineering and use of IT tools and Technologies Towards smoother delivery of municipal services to the citizens of Karnataka Municipal Reforms Cell

34 MUNICIPAL REFORMS CELL Municipal Reforms Cell

35 Municipal Reforms Cell Exclusive cell under DMA Co-ordination with project partners Rolling out of Application Operations and Maintenance of Centralized Database Managed by Professionals hired from the market directly Hand holding and training of ULBs staff Municipal Reforms Cell

HR Reforms")

36 Various Reforms Initiatives (through egovernance tools) HR Reforms Accounting Reforms Reforms in Service Delivery Performance Monitoring Municipal Reforms Cell

37 Reforms in Service Delivery Phase-I (being implemented) GIS based property tax Public grievances and redressal (PGR) Birth & Death Registration and Certification ULB websites Phase-II (to be taken up) e-procurement Building plan approval Trade license Ward works Water tariff Municipal Reforms Cell

")

38 AASTHI (GIS BASED PROPERTY TAX SYSTEM)

39 Municipal Reforms Cell

40 Why reforms in property tax.? Issues faced by the department Low rate of filing the property tax returns High accumulation of arrears Negligible penalty for not filing the return. Improper assessment of Property tax by ULB Officials which was causing huge Revenue loss to the ULB Large number of properties were unassesed and not brought under Tax net Delay in preparing the list of defaulters Delay in preparing notices to defaulters Problems in identification of unassessed properties. Poor rate of Tax collection & inaction on mounting arrears No uniform procedure of taxation Lack of procedural compliance to the act, Taxation principles followed by some ULBs were not in accordance with Act Tampering of records Inaccurate and inconsistent details and data provided by ULB Geographically widespread casing problem in monitoring of ULB Tax performance Property records were maintained in manual DCB registers Registers had details of only assessed properties. Out of which, many properties were wrongly assessed

41 Need for reforms in property tax. Issues from the perspective of citizens/service users Delay in issuing property tax extract to citizens Non service of hand written property tax notices to the Property owners by Bill Collector every year Possibilities of tampering the property details entered manually in paper form Calculation & clerical Errors in Taxation by Bill Collectors & Revenue Officers. Issues faced by the government Discrepancies in reported figures from ULBs Lack of timely information about property details from ULBs Inaccurate projections of Property Tax demand which was one of the main source of revenue of ULBs Monitoring Collection efficiency across 213 ULBs difficult Tampering of Manual records, misplacement of records Manual Data was Inaccurate

42 Municipal Reforms Cell

Maps Identification of each property outlines on property level Area (ward) maps")

43 Steps involved are. Street Naming Street Numbering Property Numbering Preparation of City Maps Preparation of Area (ward) Maps Identification of each property outlines on property level Area (ward) maps Data entry of Form C - MIS Digitization of Area (ward) maps - GIS Property details linking with digitized map Collection of Data [Form - C] Municipal Reforms Cell

44 SUPERVISION OF SURVEY WORK SURVEY OF PROPERTIES

45 SOURCE For Extracting GIS Layers Image From Google or Wikimapia SOI TOPOSHEET 1:50000 scale ULB Base Map

46 Sample Maps Base Map ULB Base Map Digital ULB Base Map Digitised Base Map Closer Look

47 Sample Maps Base Map Digitised Base Map Superimposed over Satellite Image

48 Sample Maps Block Map Over Image

49 Sample Maps Property Field Survey Map Property Field Survey Map Zoom Digitised Property Blocks

50 Municipal Reforms Cell

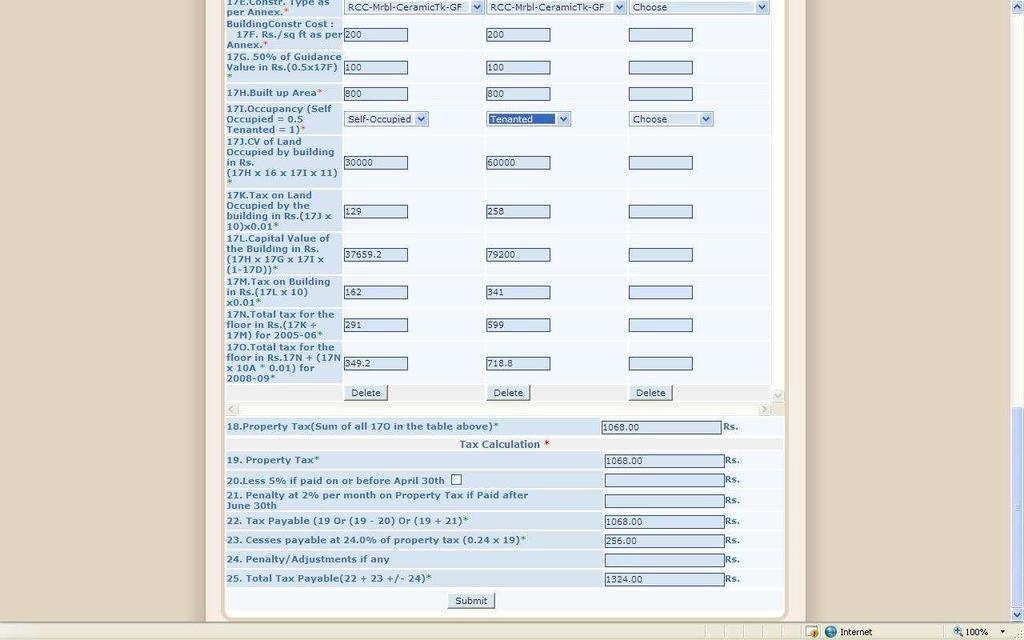

51 at ULB ULB Base map preparation which includes City Boundary, Ward Boundary, Block Boundary and Street Network Data in Municipal Books/SAS Hiring and Training locally hired Survey Assistants and ULB Engineers on Street naming and Property Numbering Validate and Augment the Data with DCB (CY + last 5 years) Amalgamate Data Capture MIS Attributes Field Survey Create a Unique ID for Each Property Draw Property Polygons with PID on Ward/Block Maps Data Entry by Locally Hired Data Entry Operators Data Validation by Revenue Staff MRC SOI

52 at SOI Digitization of Maps submitted by ULB Validation of Street naming, Numbering and Property Numbering MRC

53 at MRC ULB SOI MIS Data GIS Data Integrate GIS and MIS database Verification and Validation of Data Notice to Citizens Verification and Validation of Data Data on Production Continuous Data Updating

54 After initiative - Present scenario Sound Database of all properties available with the ULB Information about collection of property tax at any point of time Tracking of defaulters Helps in infrastructure planning Quick information about various types of properties in ULB Municipal Reforms Cell

55 Identified unassessed properties No of ULBs Impact of the Project No of properties as per MAR 19 No of unassessed properties identified % increase in no of properties brought under tax net 213 ULBs % PROPERTY TAX DEMAND PRE & POST Aasthi IMPLEMENTATION ( Amount in lakhs ) Before After Name of the ULB Demand Demand Amount of Increase in demand % Increase Gokak Nippani Channapattana Hassan

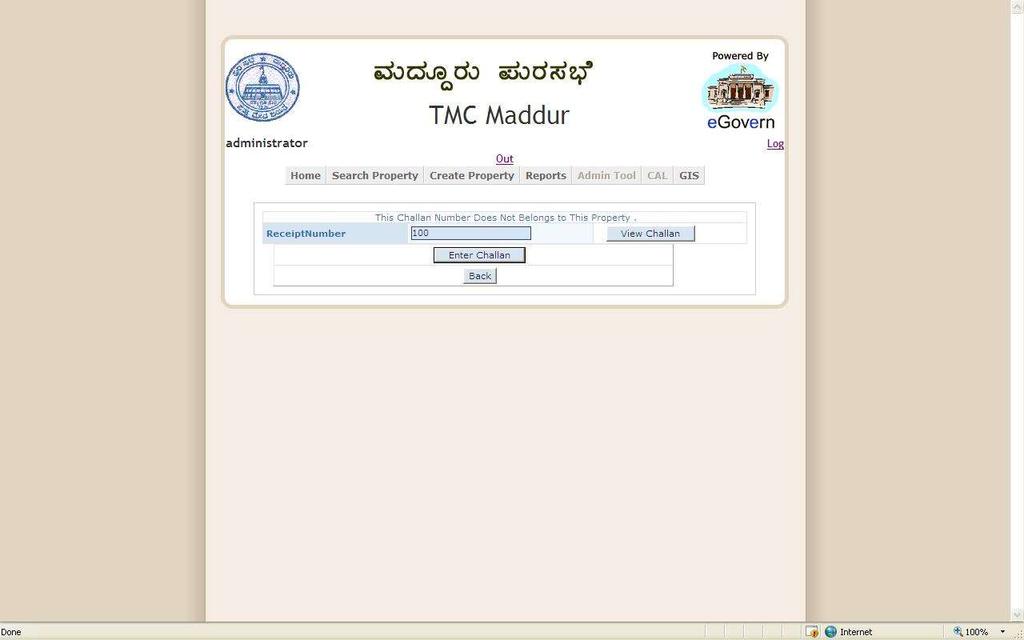

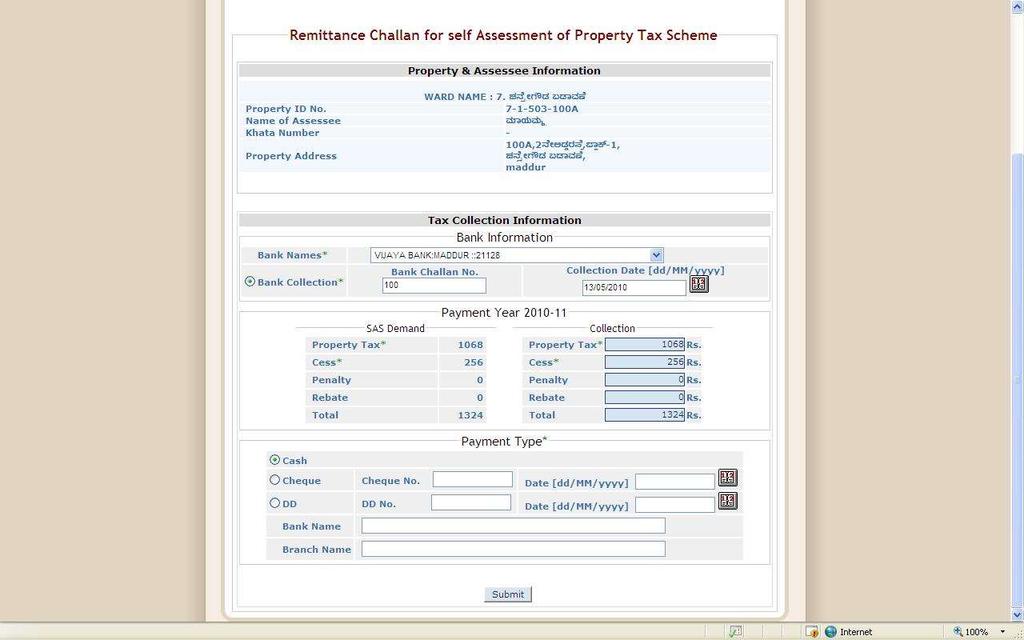

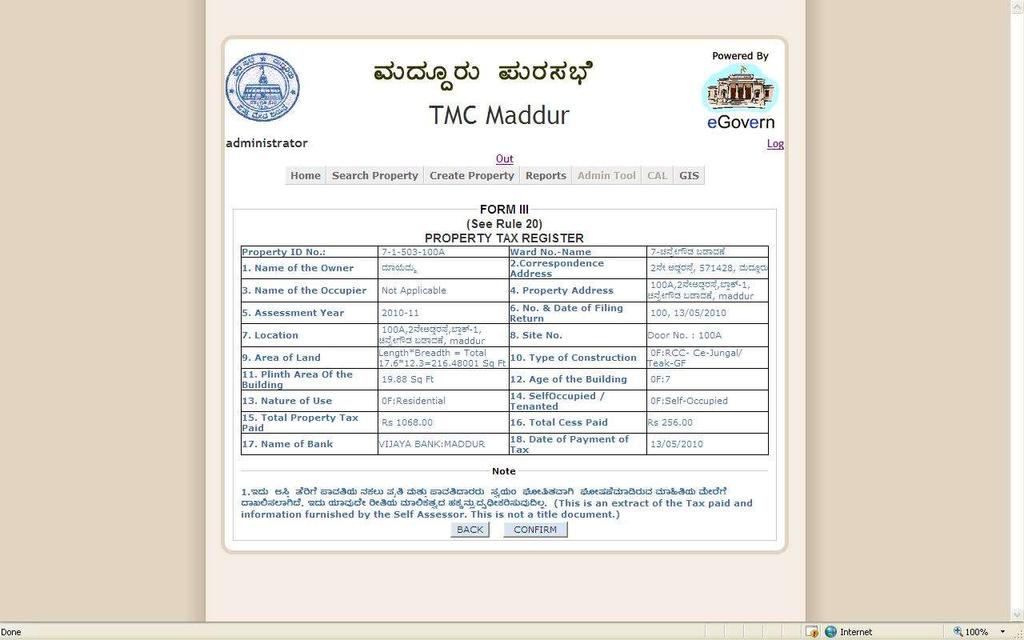

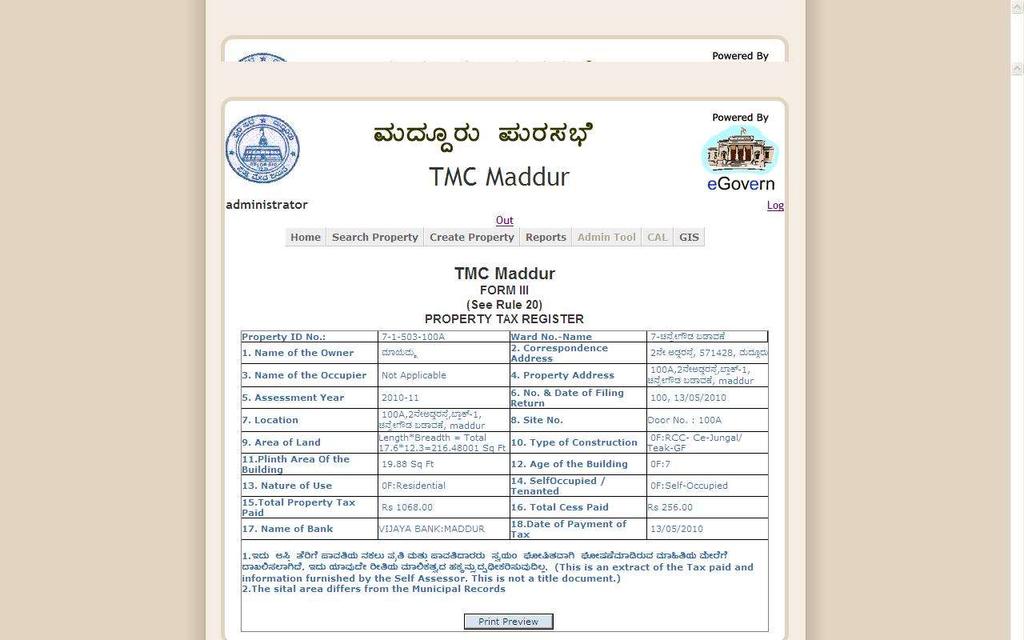

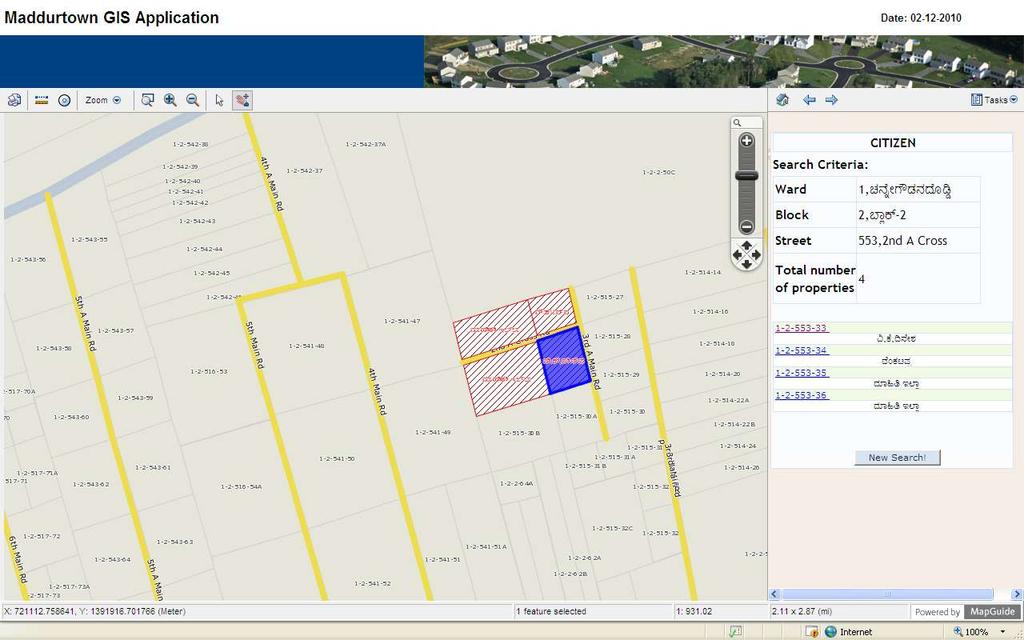

56 Aasthi GIS Based PTIS Application

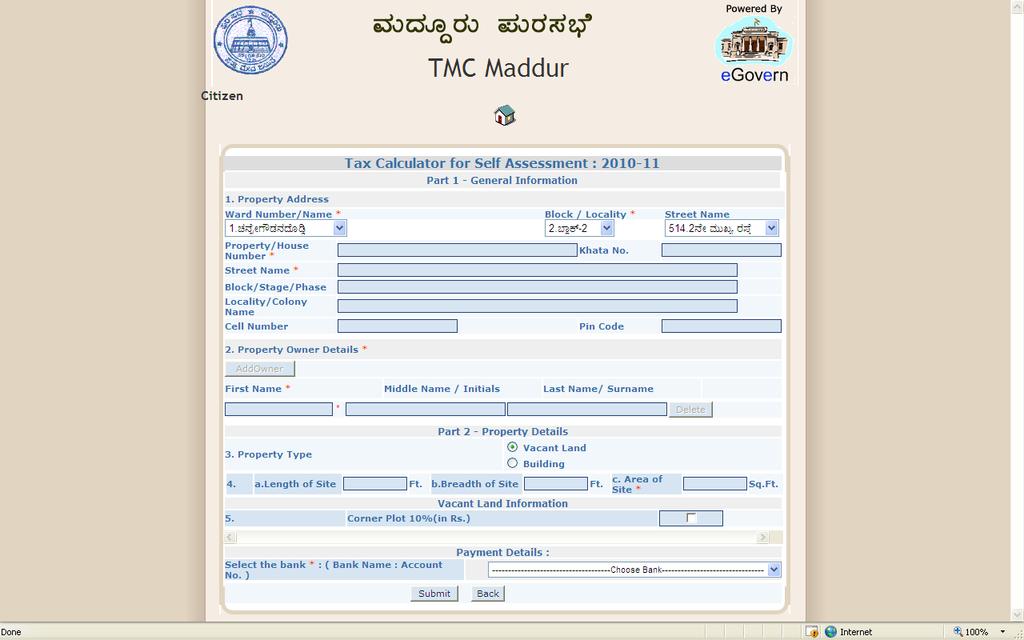

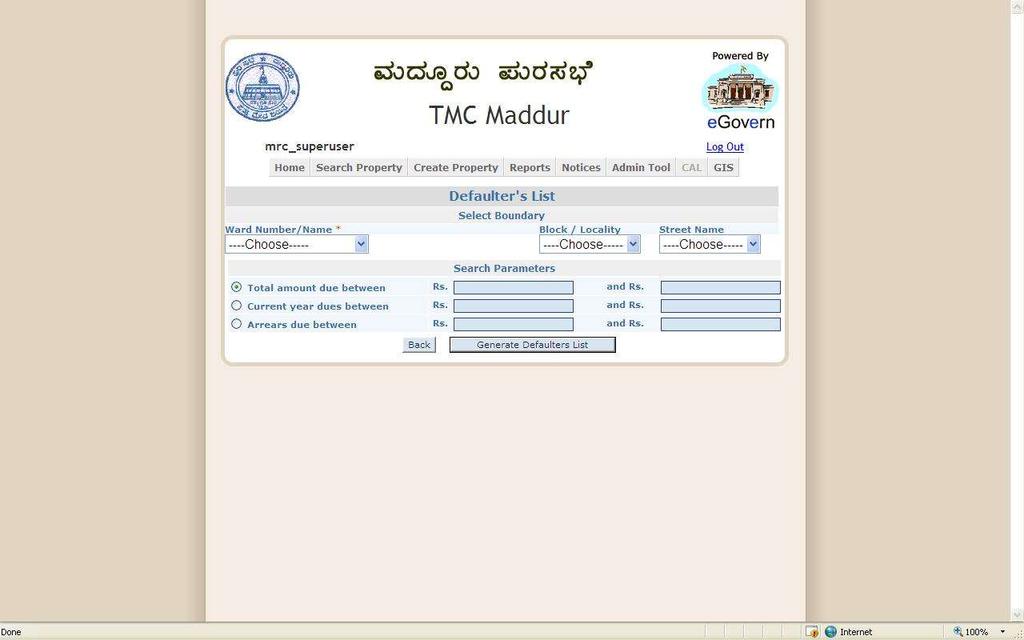

57 Processes Simplified (Services Covered) Assessment of property & property record creation Minimizing the chances of property record tampering Property tax payment by Citizen Real time data on collection of property tax by the ULB Easy search & analysis of property & tax related data Tracking of default on property tax payment Over the counter issuing of Khatha Extract Automatic calculation of Property tax demand Online property tax calculator for the citizen Policy/System uniformity across 213 ULBs Cost saving associated with property tax collection

58 Application access Flow

59 Administrator Login

60 Application access Flow

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75 Phase II Features of Aasthi Implemented Computing automatic property tax demand GIS. -Property tax Demand Calculation from DCB report from the year DCB Report at Different ULB Boundary levels -Demand Adjustment due to Property Modifications -Demand Adjustments due to any Write offs -Auto Rebate and Cess calculation if any. -Penalties are auto calculated. Automatic generation of demand notices and seizure notices -CAL notices are generated on 1 st July every year for Tax default Properties. -Demand Notice is generated if tax is not paid within 30 days from the time of CAL notice served -Seizure notice is generated if tax is not paid within 30 days from the time of Demand notice served Online Property Tax Calculator -Helps Citizen to calculate their Property Tax -Citizen has to furnish their property Location and Property Details -System will calculate the Property tax and shows the detail Property tax calculation.

76

77 ULB Level DCB

78

79

80

81

82

83 Thank you

Frequently Asked Questions On Unit Area Assessment System

Frequently Asked Questions On Unit Area Assessment System Q. How does the Kolkata Municipal Corporation determines property tax under the current system? A. Generally, Annual Valuation (AV) of a property

Frequently Asked Questions On Unit Area Assessment System Q. How does the Kolkata Municipal Corporation determines property tax under the current system? A. Generally, Annual Valuation (AV) of a property

URBAN REFORMS AGENDA AT ULB LEVEL

1. Mandatory Reforms at City Level Commitment as per the MoA for the current financial year a) Implementation of Accounting Reforms URBAN REFORMS AGENDA AT ULB LEVEL Progress made during the Quarter Installed

1. Mandatory Reforms at City Level Commitment as per the MoA for the current financial year a) Implementation of Accounting Reforms URBAN REFORMS AGENDA AT ULB LEVEL Progress made during the Quarter Installed

CHECKLIST OF REFORM E-GOVERNANCE

CHECKLIST OF REFORM E-GOVERNANCE Objective: Scheme of Urban infrastructure Development in Satellite Towns around Seven Megacities, requires certain reforms to be undertaken by Towns/Cities in E-Governance.

CHECKLIST OF REFORM E-GOVERNANCE Objective: Scheme of Urban infrastructure Development in Satellite Towns around Seven Megacities, requires certain reforms to be undertaken by Towns/Cities in E-Governance.

All municipalities, including single-tier, lower-tier and upper-tier municipalities must complete Schedule 24.

SCHEDULE 24: Payments-In-Lieu of Taxation General Information All municipalities, including single-tier, lower-tier and upper-tier municipalities must complete Schedule 24. Upper-tiers report only Upper-tier

SCHEDULE 24: Payments-In-Lieu of Taxation General Information All municipalities, including single-tier, lower-tier and upper-tier municipalities must complete Schedule 24. Upper-tiers report only Upper-tier

Reforms in Fiscal and Monetary Policies: The Road Ahead. Reforms in Property Taxation in India: Where Do We Stand? By

Foundation for Public Economics and Policy Research, Delhi International Seminar on Reforms in Fiscal and Monetary Policies: The Road Ahead December 9, 2006 Presentation on Reforms in Property Taxation

Foundation for Public Economics and Policy Research, Delhi International Seminar on Reforms in Fiscal and Monetary Policies: The Road Ahead December 9, 2006 Presentation on Reforms in Property Taxation

Property Tax Enumeration Using GIS

Property Tax Enumeration Using GIS DIANA YOHANNAN 1, JANKI ADHVARYU 2 1 Student, CEPT University 2 Student, CEPT University Kasturbhai Lalbhai Campus, University Road, Navrangpura, Ahmedabad, Gujarat 380009

Property Tax Enumeration Using GIS DIANA YOHANNAN 1, JANKI ADHVARYU 2 1 Student, CEPT University 2 Student, CEPT University Kasturbhai Lalbhai Campus, University Road, Navrangpura, Ahmedabad, Gujarat 380009

WELCOME e-govenance IN ULGs OF KERALA

WELCOME e-govenance IN ULGs OF KERALA C.RADHAKRISHNA KURUP JOINT DIRECTOR OF URBAN AFFAIRS, KERALA Initiatives Information Kerala Mission-IKM estd.in 1998 is responsible for computerization Of LSGs Developed

WELCOME e-govenance IN ULGs OF KERALA C.RADHAKRISHNA KURUP JOINT DIRECTOR OF URBAN AFFAIRS, KERALA Initiatives Information Kerala Mission-IKM estd.in 1998 is responsible for computerization Of LSGs Developed

TAXATION ON SALE AND PURCHASE OF PROPERTY REAL ESTATE SUMMIT 2016

TAXATION ON SALE AND PURCHASE OF PROPERTY BRIEF INTRODUCTION Service tax is presently calculated at the rate of 15% of the gross value of the property. But as there is a government abatement of 75% (increased

TAXATION ON SALE AND PURCHASE OF PROPERTY BRIEF INTRODUCTION Service tax is presently calculated at the rate of 15% of the gross value of the property. But as there is a government abatement of 75% (increased

Short title, extent and commencement. Definitions.

PART I GOVERNMENT OF PUNJAB DEPARTMENT OF LEGAL AND LEGISLATIVE AFFAIRS, PUNJAB NOTIFICATION The 19th April, 2018 No.12-Leg./2018.-The following Act of the Legislature of the State of Punjab received the

PART I GOVERNMENT OF PUNJAB DEPARTMENT OF LEGAL AND LEGISLATIVE AFFAIRS, PUNJAB NOTIFICATION The 19th April, 2018 No.12-Leg./2018.-The following Act of the Legislature of the State of Punjab received the

The Corporation of the Town of Essex. By-Law Number additional charges for Municipal, County. and Education purposes for the year 2017

' The Corporation of the Town of Essex Being a by-law to establish tax rates and additional charges for Municipal, County and Education purposes for the year 217 Whereas Section 29( 1) of the Municipal

' The Corporation of the Town of Essex Being a by-law to establish tax rates and additional charges for Municipal, County and Education purposes for the year 217 Whereas Section 29( 1) of the Municipal

SCHEDULE 22: Municipal and School Board Taxation

SCHEDULE 22: Municipal and School Board Taxation General Information All municipalities, including single-tier, lower-tier and upper-tier municipalities must complete Schedule 22. Upper-tiers report only

SCHEDULE 22: Municipal and School Board Taxation General Information All municipalities, including single-tier, lower-tier and upper-tier municipalities must complete Schedule 22. Upper-tiers report only

Implications of the GST for the States, ULBs and the PRIs

DISCLAIMER: Implications of the GST for the States, ULBs and the PRIs The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe

DISCLAIMER: Implications of the GST for the States, ULBs and the PRIs The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 8

: 1 : 263 RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question Paper

: 1 : 263 RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question Paper

T R A N S F O R M AT I O N A L I N I T I AT I V E S U P D AT E B O A R D O F S U P E R V I S O R S M E E T I N G J U N E 7,

T R A N S F O R M AT I O N A L I N I T I AT I V E S U P D AT E B O A R D O F S U P E R V I S O R S M E E T I N G J U N E 7, 2 0 1 7 SIGNIFICANT PROGRESS ACCOMPLISHED IMPROVE LONG-TERM STRUCTURAL REALIGNMENT

T R A N S F O R M AT I O N A L I N I T I AT I V E S U P D AT E B O A R D O F S U P E R V I S O R S M E E T I N G J U N E 7, 2 0 1 7 SIGNIFICANT PROGRESS ACCOMPLISHED IMPROVE LONG-TERM STRUCTURAL REALIGNMENT

Part A - Compulsory For All 1 Name of Municipal Corporation/Municipal Council & Nagar Panchyat 2 Ward No. & Block No.

PROPERTY TAX RETURN, PUNJAB SELF ASSESSMENT FORM (Punajb Municipal Act, 1911 under section 68(1) and Punjab Municipal Corporation Act, 1976 under section 112-A (1) Unit Number of Property H/Tax Account

PROPERTY TAX RETURN, PUNJAB SELF ASSESSMENT FORM (Punajb Municipal Act, 1911 under section 68(1) and Punjab Municipal Corporation Act, 1976 under section 112-A (1) Unit Number of Property H/Tax Account

DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS

Page 1 of 8 DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS What is GST? Goods and Services Tax (GST) is one indirect tax for the whole Nation, which will make India one

Page 1 of 8 DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS What is GST? Goods and Services Tax (GST) is one indirect tax for the whole Nation, which will make India one

THE MYSORE PAPER MILLS LTD (A Government of Karnataka Undertaking)

") THE MYSORE PAPER MILLS LTD (A Government of Karnataka Undertaking) No FFR/DF/RM/2017-18/109 CIN : L99999KA1936SGC000173 Office of the Director (Forests) MPM.Ltd., Paper Town, Bhadravathi Phone : (O) 08282

THE MYSORE PAPER MILLS LTD (A Government of Karnataka Undertaking) No FFR/DF/RM/2017-18/109 CIN : L99999KA1936SGC000173 Office of the Director (Forests) MPM.Ltd., Paper Town, Bhadravathi Phone : (O) 08282

Instructions for filling ITR-1 SAHAJ A.Y

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Taxes on Sales, Trade, etc.

OVERVIEW This Report contains 28 paragraphs, including three Performance Audits relating to non/short levy of taxes, duties, interest and penalty, etc., involving ` 255 crore. Some of the major findings

OVERVIEW This Report contains 28 paragraphs, including three Performance Audits relating to non/short levy of taxes, duties, interest and penalty, etc., involving ` 255 crore. Some of the major findings

COUNTY OF CATTARAUGUS INDUSTRIAL DEVELOPMENT AGENCY UNIFORM TAX EXEMPTION POLICY

COUNTY OF CATTARAUGUS INDUSTRIAL DEVELOPMENT AGENCY UNIFORM TAX EXEMPTION POLICY SECTION 1. PURPOSE AND AUTHORITY. Pursuant to Section 874(4)(a) of Title One of Article 18-A of the General Municipal Law,

COUNTY OF CATTARAUGUS INDUSTRIAL DEVELOPMENT AGENCY UNIFORM TAX EXEMPTION POLICY SECTION 1. PURPOSE AND AUTHORITY. Pursuant to Section 874(4)(a) of Title One of Article 18-A of the General Municipal Law,

H 8091 S T A T E O F R H O D E I S L A N D

LC00 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO PUBLIC UTILITIES AND CARRIERS -- E- GEOGRAPHIC INFORMATION SYSTEM (GIS) AND TECHNOLOGY

LC00 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO PUBLIC UTILITIES AND CARRIERS -- E- GEOGRAPHIC INFORMATION SYSTEM (GIS) AND TECHNOLOGY

URBAN REVITALIZATION PLAN

9.01 Title 9.10 Qualifications for Eligibility 9.02 Adoption of Plan 9.11 Tax Exemption Schedule 9.03 Basis of Plan 9.12 Application Requirements 9.04 Revitalization of Land Assessed as Agricultural 9.13

9.01 Title 9.10 Qualifications for Eligibility 9.02 Adoption of Plan 9.11 Tax Exemption Schedule 9.03 Basis of Plan 9.12 Application Requirements 9.04 Revitalization of Land Assessed as Agricultural 9.13

Amnesty Scheme {Chapter VI of Finance Act,2013} Presented By CA Avinash Poddar

Amnesty Scheme {Chapter VI of Finance Act,2013} Presented By CA Avinash Poddar Contents Brief Introduction of Tax Structure Constitutional Validity of Amnesty Schemes Need and Purpose of Amnesty Scheme

Amnesty Scheme {Chapter VI of Finance Act,2013} Presented By CA Avinash Poddar Contents Brief Introduction of Tax Structure Constitutional Validity of Amnesty Schemes Need and Purpose of Amnesty Scheme

VAT Information System*

116 Compendium of e-governance Initiatives CHAPTER in India 9 VAT Information System* M.M. Shrivastava Commissioner of Commercial Taxes, Govt. of Gujarat Office of Commissioner of Commercial Taxes, Sales

116 Compendium of e-governance Initiatives CHAPTER in India 9 VAT Information System* M.M. Shrivastava Commissioner of Commercial Taxes, Govt. of Gujarat Office of Commissioner of Commercial Taxes, Sales

To establish a policy that guides City assessment review activities to help ensure stability and accuracy of the assessment base.

EFFECTIVE: June 1, 2007 REPLACES: new PAGE: 1 of 13 POLICY STATEMENT: To establish a policy that guides City assessment review activities to help ensure stability and accuracy of the assessment base. PURPOSE:

EFFECTIVE: June 1, 2007 REPLACES: new PAGE: 1 of 13 POLICY STATEMENT: To establish a policy that guides City assessment review activities to help ensure stability and accuracy of the assessment base. PURPOSE:

2016 NASCIO Recognition Award Submission Budget Forecasting Function (BFF)

") STATE OF CALIFORNIA California Department of Corrections and Rehabilitation Enterprise Information Services Business Information System Program Initiation: July 2014 Completion: May 2015 2016 NASCIO Recognition

STATE OF CALIFORNIA California Department of Corrections and Rehabilitation Enterprise Information Services Business Information System Program Initiation: July 2014 Completion: May 2015 2016 NASCIO Recognition

Public Financial Management & Accountability in Urban Local Bodies

Over the years there has been a decline of local self government institutions in India in terms of inadequate devolution of powers and poor management and governance. There has been a complete lack of

Over the years there has been a decline of local self government institutions in India in terms of inadequate devolution of powers and poor management and governance. There has been a complete lack of

1. All existing revenue sources of the Urban Council

1. All existing revenue sources of the Urban Council Name of Legislation For Urban Councils Under Urban Council Ordinance Applicable Section Section 158 (2) (a) section Schedule Number 04 Section 158 (2)

1. All existing revenue sources of the Urban Council Name of Legislation For Urban Councils Under Urban Council Ordinance Applicable Section Section 158 (2) (a) section Schedule Number 04 Section 158 (2)

Proposed Amendments in GST Law

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Service Tax Voluntary Compliance Encouragement Scheme, 2013

Service Tax Voluntary Compliance Encouragement Scheme, 2013 CHAPTER VI OF FINANCE ACT, 2013 Service Tax Voluntary Compliance Encouragement Scheme, 2013 104. Short title. This Scheme may be called the Service

Service Tax Voluntary Compliance Encouragement Scheme, 2013 CHAPTER VI OF FINANCE ACT, 2013 Service Tax Voluntary Compliance Encouragement Scheme, 2013 104. Short title. This Scheme may be called the Service

WATERWORKS BYLAW BYLAW NO

WATERWORKS BYLAW BYLAW NO. 07-030 This consolidation is a copy of a bylaw consolidated under the authority of section 139 of the Community Charter. (Consolidated on July 13, 2015 up to Bylaw No. 15-049)

WATERWORKS BYLAW BYLAW NO. 07-030 This consolidation is a copy of a bylaw consolidated under the authority of section 139 of the Community Charter. (Consolidated on July 13, 2015 up to Bylaw No. 15-049)

6. Property Rates in Indonesia 1

Role of Property Taxes within Indonesia 6. Property Rates in Indonesia 1 Property taxes in Indonesia in FY 1999/2000 generated Rp. 3.3 trillion (or approximately US$356 million). In 1999/2000, property

Role of Property Taxes within Indonesia 6. Property Rates in Indonesia 1 Property taxes in Indonesia in FY 1999/2000 generated Rp. 3.3 trillion (or approximately US$356 million). In 1999/2000, property

TITLE 5 MUNICIPAL FINANCE AND TAXATION 1

Change 12, August 4, 2015 5-1 TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 CHAPTER 1. MISCELLANEOUS. 2. REAL PROPERTY TAXES. 3. PRIVILEGE TAXES GENERALLY. 4. WHOLESALE BEER TAX. 5. RENTAL TAX ON TELEPHONE

Change 12, August 4, 2015 5-1 TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 CHAPTER 1. MISCELLANEOUS. 2. REAL PROPERTY TAXES. 3. PRIVILEGE TAXES GENERALLY. 4. WHOLESALE BEER TAX. 5. RENTAL TAX ON TELEPHONE

GST & YOU. Tally Solutions Pvt. Ltd. All Rights Reserved 2. Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

Punjab Government Gazette

26 Regd. No. NW CH-22 Regd. No. CHD/0092/2009-2011 Punjab Government Gazette EXTRAORDINARY Published by Authority CHANDIGARH, WEDNESDAY, APRIL 06, 2011 (CHAITRA 16, 1933 SAKA) LEGISLATIVE SUPPLEMENT Contents

26 Regd. No. NW CH-22 Regd. No. CHD/0092/2009-2011 Punjab Government Gazette EXTRAORDINARY Published by Authority CHANDIGARH, WEDNESDAY, APRIL 06, 2011 (CHAITRA 16, 1933 SAKA) LEGISLATIVE SUPPLEMENT Contents

CHAPTER 11-9 TAX INCREMENTAL DISTRICTS

CHAPTER 11-9 TAX INCREMENTAL DISTRICTS 11-9-1 Definition of terms. 11-9-2 Municipal powers related to districts. 11-9-3 Planning commission hearing on creation of district--notice. 11-9-4 Recommendation

CHAPTER 11-9 TAX INCREMENTAL DISTRICTS 11-9-1 Definition of terms. 11-9-2 Municipal powers related to districts. 11-9-3 Planning commission hearing on creation of district--notice. 11-9-4 Recommendation

Summary o. f findings, Conclusion and suggestions

Summary o. f findings, Conclusion and suggestions CHAPTER-IX SUMMARY OF FINDINGS, CONCLUSION AND SUGGESTIONS In this chapter, an attempt is made to highlight the major inferences with a view of provide

Summary o. f findings, Conclusion and suggestions CHAPTER-IX SUMMARY OF FINDINGS, CONCLUSION AND SUGGESTIONS In this chapter, an attempt is made to highlight the major inferences with a view of provide

Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state.

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

Thiruvananthapuram Corporation

Thiruvananthapuram Corporation 07-November-08 Johnson K George IAS Secretary http://www.corporationoftrivandrum.in JnNURM PROGRESS 1 Structure of the Presentation ULB Level Reform State Level Optional

Thiruvananthapuram Corporation 07-November-08 Johnson K George IAS Secretary http://www.corporationoftrivandrum.in JnNURM PROGRESS 1 Structure of the Presentation ULB Level Reform State Level Optional

SyNoPSIS of the FINaNce BILL, 2017

SyNoPSIS of the FINaNce BILL, 2017 By PaRaS KocHaR, advocate The following changes in the finance bill has been proposed by the Hon ble Finance Minister to the Income Tax Act, 1961 from 01-04-2017 TAX

SyNoPSIS of the FINaNce BILL, 2017 By PaRaS KocHaR, advocate The following changes in the finance bill has been proposed by the Hon ble Finance Minister to the Income Tax Act, 1961 from 01-04-2017 TAX

Delivering on Our Commitments

2018 Business and Financial Plan Delivering on Our Commitments Mission Statement The Saskatchewan Assessment Management Agency develops, regulates and delivers a stable, cost-effective assessment system

2018 Business and Financial Plan Delivering on Our Commitments Mission Statement The Saskatchewan Assessment Management Agency develops, regulates and delivers a stable, cost-effective assessment system

TAX INCREMENT FINANCING ACT - OMNIBUS AMENDMENTS Act of Dec. 16, 1992, P.L. 1240, No. 164 Cl. 64 Session of 1992 No

TAX INCREMENT FINANCING ACT - OMNIBUS AMENDMENTS Act of Dec. 16, 1992, P.L. 1240, No. 164 Cl. 64 Session of 1992 No. 1992-164 HB 2439 AN ACT Amending the act of July 11, 1990 (P.L.465, No.113), entitled

TAX INCREMENT FINANCING ACT - OMNIBUS AMENDMENTS Act of Dec. 16, 1992, P.L. 1240, No. 164 Cl. 64 Session of 1992 No. 1992-164 HB 2439 AN ACT Amending the act of July 11, 1990 (P.L.465, No.113), entitled

The Institute of Cost Accountants of India. (Statutory body under an Act of Parliament)

") The Institute of Cost Accountants of India (Statutory body under an Act of Parliament) Suggestions and Feedback from Stakeholders and General Public submitted to CBDT on New Direct Tax Law General Information

The Institute of Cost Accountants of India (Statutory body under an Act of Parliament) Suggestions and Feedback from Stakeholders and General Public submitted to CBDT on New Direct Tax Law General Information

Part 1: General. Existing Revenue Sources of the Municipal Council. List of Revenue Sources. Name of Legislation

Part 1: General 1' all existing revenue sources of Municipal Council Existing Revenue Sources of the Municipal Council Table 1 indicates all existing revenue sources of the Municipal Council together with

Part 1: General 1' all existing revenue sources of Municipal Council Existing Revenue Sources of the Municipal Council Table 1 indicates all existing revenue sources of the Municipal Council together with

TOWN OF SMITHFIELD JOB DESCRIPTION FINANCE DIRECTOR / TAX COLLECTOR

TOWN OF SMITHFIELD JOB DESCRIPTION FINANCE DIRECTOR / TAX COLLECTOR GENERAL SUMMARY: The Tax Collector/ is in charge with the ultimate responsibility of organizing, directing and coordinating all phases

TOWN OF SMITHFIELD JOB DESCRIPTION FINANCE DIRECTOR / TAX COLLECTOR GENERAL SUMMARY: The Tax Collector/ is in charge with the ultimate responsibility of organizing, directing and coordinating all phases

State Policy on Chhattisgarh Special Economic Zone. Government of Chhattisgarh. Department of Commerce and Industries

(1) State Policy on Chhattisgarh Special Economic Zone Government of Chhattisgarh Department of Commerce and Industries 1.0 Preamble 1.1 Where as for augmenting infrastructure facilities for export production

(1) State Policy on Chhattisgarh Special Economic Zone Government of Chhattisgarh Department of Commerce and Industries 1.0 Preamble 1.1 Where as for augmenting infrastructure facilities for export production

BUDGET 2016 SONALEE GODBOLE

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

Tax essentials for Individuals

Tax Rates The income tax rates are: Taxable Income for Men & Rate Taxable Income for Senior Rate Women Citizen Up to Rs. 2,00,000 Nil Up to Rs. 2,50,000 Nil 2,00,001 to 5,00,000 10% 2,50,001 to 5,00,000

Tax Rates The income tax rates are: Taxable Income for Men & Rate Taxable Income for Senior Rate Women Citizen Up to Rs. 2,00,000 Nil Up to Rs. 2,50,000 Nil 2,00,001 to 5,00,000 10% 2,50,001 to 5,00,000

TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 CHAPTER 1 MISCELLANEOUS

5-1 CHAPTER 1. MISCELLANEOUS. 2. REAL PROPERTY TAXES. 3. PRIVILEGE TAXES. 4. WHOLESALE BEER TAX. 5. HOTEL/MOTEL TAX. TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 5-101. Fiscal year. 5-102. Depositories for

5-1 CHAPTER 1. MISCELLANEOUS. 2. REAL PROPERTY TAXES. 3. PRIVILEGE TAXES. 4. WHOLESALE BEER TAX. 5. HOTEL/MOTEL TAX. TITLE 5 MUNICIPAL FINANCE AND TAXATION 1 5-101. Fiscal year. 5-102. Depositories for

JAMMU & KASHMIR. 1. Structure

S ales Tax S vsiem s In India: A P rofile JAMMU & KASHMIR The levy of sales tax in the State of Jammu & Kashmir is governed by the provisions of the Central Sales Tax Act. 1956, and the Jammu & Kashmir

S ales Tax S vsiem s In India: A P rofile JAMMU & KASHMIR The levy of sales tax in the State of Jammu & Kashmir is governed by the provisions of the Central Sales Tax Act. 1956, and the Jammu & Kashmir

Chapter-20 Role of IFAs - Managers Check List

Chapter-20 Role of IFAs - Managers Check List BSNL, India For Internal Circulation Only 1 Functions of Internal Finance Advisers A. Finance & Budget: 1. To establish appropriate local procedures to have

Chapter-20 Role of IFAs - Managers Check List BSNL, India For Internal Circulation Only 1 Functions of Internal Finance Advisers A. Finance & Budget: 1. To establish appropriate local procedures to have

CHAPTER-5 MUNICIPAL FINANCES. 5.1 The financial position of ULBs in Assam is such that they are

CHAPTER-5 MUNICIPAL FINANCES 5.1 The financial position of ULBs in Assam is such that they are hardly in a position to provide quality civic services to the urban dwellers. As per 2001 census, Assam is

CHAPTER-5 MUNICIPAL FINANCES 5.1 The financial position of ULBs in Assam is such that they are hardly in a position to provide quality civic services to the urban dwellers. As per 2001 census, Assam is

KARNATAKA POWER CORPORATION LIMITED YELAHANKA COMBINED CYCLE POWER PLANT (CIN: U85110KA1970SGC001919)

") KARNATAKA POWER CORPORATION LIMITED YELAHANKA COMBINED CYCLE POWER PLANT (CIN: U85110KA1970SGC001919) Office of the Executive Engineer (Civil) -2 Yelahanka Combined Cycle Power Plant Doddaballapur Road,

KARNATAKA POWER CORPORATION LIMITED YELAHANKA COMBINED CYCLE POWER PLANT (CIN: U85110KA1970SGC001919) Office of the Executive Engineer (Civil) -2 Yelahanka Combined Cycle Power Plant Doddaballapur Road,

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of The People of the State of Michigan enact:

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of 1980 AN ACT to prevent urban deterioration and encourage economic development and activity and to encourage neighborhood revitalization and historic preservation;

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of 1980 AN ACT to prevent urban deterioration and encourage economic development and activity and to encourage neighborhood revitalization and historic preservation;

REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By CA Sandip Agrawal Sandip Satyanarayan & Co Chartered Accountants

By CA Sandip Agrawal Sandip Satyanarayan & Co Chartered Accountants") REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By BRIEF INTRODUCTION TO GST GST is a Tax on Goods and services and it is proposed to be a comprehensive indirect tax levy on manufacture,

REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By BRIEF INTRODUCTION TO GST GST is a Tax on Goods and services and it is proposed to be a comprehensive indirect tax levy on manufacture,

Description of the Sample and Limitations of the Data

Section 3 Description of the Sample and Limitations of the Data T his section describes the 2008 Corporate sample design, sample selection, data capture, data cleaning, and data completion. The techniques

Section 3 Description of the Sample and Limitations of the Data T his section describes the 2008 Corporate sample design, sample selection, data capture, data cleaning, and data completion. The techniques

POS No.1 Fund released under 12 th & 13 th Finance Commission Observations.

POS No.1 Fund released under 12 th & 13 th Finance Commission Observations. 1 It may please be stated the criteria for Finance Department allocated Rs.157.80 allocation of fund under 12 th Finance crore

POS No.1 Fund released under 12 th & 13 th Finance Commission Observations. 1 It may please be stated the criteria for Finance Department allocated Rs.157.80 allocation of fund under 12 th Finance crore

REQUEST FOR PROPOSAL FOR APPOINTMENT OF CHARTERED ACCOUNTANTS/FIRM ON CONTRACT BASIS. Real Estate Regulatory Authority, Karnataka

Real Estate Regulatory Authority, Karnataka No. 1-1/15, 2 ND Floor, Silver Jubilee Block, Unity Building, C.S.I. Compound, 3 rd Cross, Mission Road, Bengaluru-560027 REQUEST FOR PROPOSAL FOR APPOINTMENT

Real Estate Regulatory Authority, Karnataka No. 1-1/15, 2 ND Floor, Silver Jubilee Block, Unity Building, C.S.I. Compound, 3 rd Cross, Mission Road, Bengaluru-560027 REQUEST FOR PROPOSAL FOR APPOINTMENT

SENATE, No STATE OF NEW JERSEY. 216th LEGISLATURE INTRODUCED FEBRUARY 11, 2016

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Senator ANTHONY R. BUCCO District (Morris and Somerset) SYNOPSIS Requires 0-day grace period prior to accrual of interest

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Senator ANTHONY R. BUCCO District (Morris and Somerset) SYNOPSIS Requires 0-day grace period prior to accrual of interest

Bhopal: Dated 5 th May 2006

Bhopal: Dated 5 th May 2006 No. 1192/MPERC/2006. In exercise of the powers conferred by section 181 (g) read with section 32(3) of the Electricity Act, 2003 enacted by the parliament, the Madhya Pradesh

Bhopal: Dated 5 th May 2006 No. 1192/MPERC/2006. In exercise of the powers conferred by section 181 (g) read with section 32(3) of the Electricity Act, 2003 enacted by the parliament, the Madhya Pradesh

NORTH EASTERN REGION CAPITAL CITIES DEVELOPMENT INVESTMENT PROGRAMME (LOAN NO 2528-IND & 2834-IND)

") NORTH EASTERN REGION CAPITAL CITIES DEVELOPMENT INVESTMENT PROGRAMME (LOAN NO 2528-IND & 2834-IND) PROJECT IMPLEMENTATION STATUS FOR SHILLONG-MEGHALAYA (7 th May 2012) TRANCHE I STATUS A. CONSTRUCTING

NORTH EASTERN REGION CAPITAL CITIES DEVELOPMENT INVESTMENT PROGRAMME (LOAN NO 2528-IND & 2834-IND) PROJECT IMPLEMENTATION STATUS FOR SHILLONG-MEGHALAYA (7 th May 2012) TRANCHE I STATUS A. CONSTRUCTING

Section - 271, Income-tax Act,

1 of 7 29-Feb-16 2:37 PM Section - 271, Income-tax Act, 1961-2015 35 [Failure to furnish returns, comply with notices, concealment of income, etc. 36 271. 36a (1) If the 37 [Assessing] Officer or the 38

1 of 7 29-Feb-16 2:37 PM Section - 271, Income-tax Act, 1961-2015 35 [Failure to furnish returns, comply with notices, concealment of income, etc. 36 271. 36a (1) If the 37 [Assessing] Officer or the 38

COUNTY GOVERNMENTS PUBLIC FINANCE MANAGEMENT Transition ACT

LAWS OF KENYA COUNTY GOVERNMENTS PUBLIC FINANCE MANAGEMENT Transition ACT Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org County Governments

LAWS OF KENYA COUNTY GOVERNMENTS PUBLIC FINANCE MANAGEMENT Transition ACT Published by the National Council for Law Reporting with the Authority of the Attorney-General www.kenyalaw.org County Governments

FISCAL IMPACT ANALYSIS FOR THE REDEVELOPMENT PLAN FOR THE CHENEY/HAGERTY/KUSHNER TRACT TOWNSHIP OF CRANBURY MIDDLESEX COUNTY, NEW JERSEY.

FISCAL IMPACT ANALYSIS FOR THE REDEVELOPMENT PLAN FOR THE CHENEY/HAGERTY/KUSHNER TRACT TOWNSHIP OF CRANBURY MIDDLESEX COUNTY, NEW JERSEY Prepared by: Phillips Preiss Grygiel LLC Planning and Real Estate

FISCAL IMPACT ANALYSIS FOR THE REDEVELOPMENT PLAN FOR THE CHENEY/HAGERTY/KUSHNER TRACT TOWNSHIP OF CRANBURY MIDDLESEX COUNTY, NEW JERSEY Prepared by: Phillips Preiss Grygiel LLC Planning and Real Estate

INCOME-TAX AND BASED ON FINANCE ACT, FINANCE ACT, 2007 WITH NOTES 49 I.T. NOTES 69 I.T. NOTES 97 I.T. NOTES I.T. NOTES 139 I.T.

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

2016 PERSONAL INCOME TAX WORKSHEET

2016 PERSONAL INCOME TAX WORKSHEET TAXPAYER DETAILS Title Tax File Number Surname of Birth First Name Best Contact Number ( ) Other Name/s Or Mobile Telephone Occupation (not Title) Residential Address

2016 PERSONAL INCOME TAX WORKSHEET TAXPAYER DETAILS Title Tax File Number Surname of Birth First Name Best Contact Number ( ) Other Name/s Or Mobile Telephone Occupation (not Title) Residential Address

Area/locality; Town/City/District; State; Country. Pin code is mandatory. Tick mark the appropriate box for residential status. For non-residents cert

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

UNIFORM TAX EXEMPTION POLICY

UCIDA Ulster County Industrial Development Agency UNIFORM TAX EXEMPTION POLICY SECTION 1. PURPOSE AND AUTHORITY. Pursuant to Section 874(4)(a) of Title One of Article 18-A of the General Municipal Law

UCIDA Ulster County Industrial Development Agency UNIFORM TAX EXEMPTION POLICY SECTION 1. PURPOSE AND AUTHORITY. Pursuant to Section 874(4)(a) of Title One of Article 18-A of the General Municipal Law

Assessor Tami Little, County Assessor Development Services Building 150 Beavercreek Road Oregon City, Oregon

Assessor Tami Little, County Assessor Development Services Building 150 Beavercreek Road Oregon City, Oregon 97045 503-655-8671 Website Address: http://www.clackamas.us/at/ 1 This page intentionally left

Assessor Tami Little, County Assessor Development Services Building 150 Beavercreek Road Oregon City, Oregon 97045 503-655-8671 Website Address: http://www.clackamas.us/at/ 1 This page intentionally left

CHAPTER IV : LAND REVENUE

CHAPTER IV : LAND REVENUE 4.1 Results of Audit Test check of records of land revenue conducted during the year 2002-2003 revealed under assessment, short levy, loss of revenue etc., amounting to Rs 441.18

CHAPTER IV : LAND REVENUE 4.1 Results of Audit Test check of records of land revenue conducted during the year 2002-2003 revealed under assessment, short levy, loss of revenue etc., amounting to Rs 441.18

1. Risk of regularizing illegal connections

1. Risk of regularizing illegal connections Background: This is an example of a contract provision for mitigating the risk of converting illegal connections to legal connections in a 300,000 population

1. Risk of regularizing illegal connections Background: This is an example of a contract provision for mitigating the risk of converting illegal connections to legal connections in a 300,000 population

Government of karnataka R F D. (Results-Framework Document) for. Department of Housing ( )

for. Department of Housing ( )") Government of karnataka R F D (Results-Framework Document) for Department of Housing (2015-2016) Confirmation mail of RFD Submission has been sent to the user's email Id: jdplanningudd@hotmail.com and

Government of karnataka R F D (Results-Framework Document) for Department of Housing (2015-2016) Confirmation mail of RFD Submission has been sent to the user's email Id: jdplanningudd@hotmail.com and

RESOLUTION NO

RESOLUTION NO. 2016- A RESOLUTION OF THE BOARD OF DIRECTORS OF THE SADDLE CREEK COMMUNITY SERVICES DISTRICT ADOPTING INTENDED BALLOT LANGUAGE, AND CALLING AND PROVIDING FOR A SPECIAL MAILED BALLOT ELECTION

RESOLUTION NO. 2016- A RESOLUTION OF THE BOARD OF DIRECTORS OF THE SADDLE CREEK COMMUNITY SERVICES DISTRICT ADOPTING INTENDED BALLOT LANGUAGE, AND CALLING AND PROVIDING FOR A SPECIAL MAILED BALLOT ELECTION

Service Level Agreement between MPAC and Ontario Municipalities

Service Level Agreement between MPAC and Ontario Municipalities 1. Purpose This Service Level Agreement is a statement of MPAC s commitment to all Municipalities to maintain high performance standards

Service Level Agreement between MPAC and Ontario Municipalities 1. Purpose This Service Level Agreement is a statement of MPAC s commitment to all Municipalities to maintain high performance standards

GUIDE TO PROPERTY TAXES

NEW JERSEY HOMEOWNER S GUIDE TO PROPERTY TAXES ASSOCIATION OF MUNICIPAL ASSESSORS OF NEW JERSEY Property taxes are top of mind for many New Jersey homeowners. The state has the highest property taxes in

NEW JERSEY HOMEOWNER S GUIDE TO PROPERTY TAXES ASSOCIATION OF MUNICIPAL ASSESSORS OF NEW JERSEY Property taxes are top of mind for many New Jersey homeowners. The state has the highest property taxes in

Manufactured Housing Tax Liens

Texas Department of Housing and Community Affairs MANUFACTURED HOUSING DIVISION Manufactured Housing Tax Liens TDHCA Main Web Page To access the Manufactured Housing web page select MANUFACTURED HOUSING

Texas Department of Housing and Community Affairs MANUFACTURED HOUSING DIVISION Manufactured Housing Tax Liens TDHCA Main Web Page To access the Manufactured Housing web page select MANUFACTURED HOUSING

FINANCE BILL He has proposed to revise the tax slabs upwards as under:

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of The People of the State of Michigan enact:

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of 1980 AN ACT to prevent urban deterioration and encourage economic development and activity and to encourage neighborhood revitalization and historic preservation;

THE TAX INCREMENT FINANCE AUTHORITY ACT Act 450 of 1980 AN ACT to prevent urban deterioration and encourage economic development and activity and to encourage neighborhood revitalization and historic preservation;

PENALTY, INTEREST & SURVEY (TDS) 12/02/2011 SANGHVI SANGHVI & SANGHVI

12/02/2011 SANGHVI SANGHVI & SANGHVI") 12/02/2011 SANGHVI SANGHVI & SANGHVI 1 PENAL AND OTHER CONSEQUENCES FOR NON- COMPLIANCE WITH THE PROVISIONS OF TDS DISALLOWANCE OF EXPENDITURE Sec. 40(a)(i) : Expenditure in respect of certain payments

12/02/2011 SANGHVI SANGHVI & SANGHVI 1 PENAL AND OTHER CONSEQUENCES FOR NON- COMPLIANCE WITH THE PROVISIONS OF TDS DISALLOWANCE OF EXPENDITURE Sec. 40(a)(i) : Expenditure in respect of certain payments

ANNEXURE-I QUESTIONNAIRE FOR CORPORATE HEADS

ANNEXURE-I QUESTIONNAIRE FOR CORPORATE HEADS Name of the Respondent: _ Organization: Designation: _ E-Mail id: _ Contact No.: _ GENERAL 1. Respondent s corporate information; 1.1 State the type of industry

ANNEXURE-I QUESTIONNAIRE FOR CORPORATE HEADS Name of the Respondent: _ Organization: Designation: _ E-Mail id: _ Contact No.: _ GENERAL 1. Respondent s corporate information; 1.1 State the type of industry

IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY by CA Sudin Sabnis

FORMS FOR AY by CA Sudin Sabnis") IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY 2018-19 by CA Sudin Sabnis Why filing correct Income Tax Return is important Law of the land Losses and Tax holiday Refunds Stich in time saves

IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY 2018-19 by CA Sudin Sabnis Why filing correct Income Tax Return is important Law of the land Losses and Tax holiday Refunds Stich in time saves

Circular The Schedule of dates for filing income-tax returns is given below:

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Presentation on section 80IBA of Income Tax Act (amended) along with Alternate Minimum Tax

along with Alternate Minimum Tax") Deduction of 100% profits to Affordable Housing Projects Where the gross total income of an assessee includes any profits and gains derived from the business of developing and building housing projects,

Deduction of 100% profits to Affordable Housing Projects Where the gross total income of an assessee includes any profits and gains derived from the business of developing and building housing projects,

2017 PERSONAL INCOME TAX WORKSHEET

2017 PERSONAL INCOME TAX WORKSHEET TAXPAYER DETAILS Title Tax File Number Surname Date of Birth First Name Best Contact Number ( ) Other Name/s Or Mobile Telephone Occupation (not Title) Residential Address

2017 PERSONAL INCOME TAX WORKSHEET TAXPAYER DETAILS Title Tax File Number Surname Date of Birth First Name Best Contact Number ( ) Other Name/s Or Mobile Telephone Occupation (not Title) Residential Address

Tax essentials for Individuals

Tax Rates The income tax rates are: Taxable Income for Men Rate Taxable Income for Women Rate Up to Rs. 1,80,000 Nil Up to Rs. 1,90,000 Nil 1,80,001 to 5,00,000 10% 1,90,001 to 5,00,000 10% 5,00,001 to

Tax Rates The income tax rates are: Taxable Income for Men Rate Taxable Income for Women Rate Up to Rs. 1,80,000 Nil Up to Rs. 1,90,000 Nil 1,80,001 to 5,00,000 10% 1,90,001 to 5,00,000 10% 5,00,001 to

VAT CONCEPT AND ITS APPLICATION IN GST

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

Current Tax Structure in India

History of GST More than 150 countries have already introduced GST. France was the first country to introduce GST system in 1954. Typically it is a single rate system but two/three rate systems are also

History of GST More than 150 countries have already introduced GST. France was the first country to introduce GST system in 1954. Typically it is a single rate system but two/three rate systems are also

City of Schenectady IDA UNIFORM TAX EXEMPTION POLICY. Agency shall mean the City of Schenectady Industrial Development Agency.

UNIFORM TAX EXEMPTION POLICY I. PURPOSE AND AUTHORITY Pursuant to Section 874(4)(a) of Title One of Article 18-A of the General Municipal Law (the "Act"), the Schenectady County Industrial Development

UNIFORM TAX EXEMPTION POLICY I. PURPOSE AND AUTHORITY Pursuant to Section 874(4)(a) of Title One of Article 18-A of the General Municipal Law (the "Act"), the Schenectady County Industrial Development

IMPORTANT DATES DIRECT TAXES. TDS / TCS returns are to be filed Quarterly.

IMPORTANT DATES DIRECT TAXES TDS / TCS returns are to be filed Quarterly. QUARTER ENDING DUE DATE 30 TH JUNE 15 TH JULY 30 TH SEPTEMBER 15 TH OCTOBER 31 ST DECEMBER 15 TH JANUARY 31 ST MARCH 15 TH MAY

IMPORTANT DATES DIRECT TAXES TDS / TCS returns are to be filed Quarterly. QUARTER ENDING DUE DATE 30 TH JUNE 15 TH JULY 30 TH SEPTEMBER 15 TH OCTOBER 31 ST DECEMBER 15 TH JANUARY 31 ST MARCH 15 TH MAY

Town of Nipawin 2018 Municipal Property Tax Policy

Town of Nipawin 2018 Municipal Property Tax Policy Introduction Property tax is an important revenue source for the Town of Nipawin and funds both operational and capital needs for general operations (all

Town of Nipawin 2018 Municipal Property Tax Policy Introduction Property tax is an important revenue source for the Town of Nipawin and funds both operational and capital needs for general operations (all

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime

Provisions in GST Regime") Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

PlanPlus ( A tool for Decentralized and Integrated District Planning

PlanPlus (http://planningonline.gov.in) A tool for Decentralized and Integrated District Planning 1 TFC BRGF Planning currently done in silos (scheme-based) Funding NREGS Gram Panchayat Own Funds May not

PlanPlus (http://planningonline.gov.in) A tool for Decentralized and Integrated District Planning 1 TFC BRGF Planning currently done in silos (scheme-based) Funding NREGS Gram Panchayat Own Funds May not

Municipal Government Act Review

What We Heard: A Summary of Consultation Input Assessment and Taxation Technical Session Held in Edmonton on February 5, 2014 Released on June 12, 2014 Developed by KPMG for Alberta Municipal Affairs Contents

What We Heard: A Summary of Consultation Input Assessment and Taxation Technical Session Held in Edmonton on February 5, 2014 Released on June 12, 2014 Developed by KPMG for Alberta Municipal Affairs Contents

Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages

212.05 Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages in the business of selling tangible personal property

212.05 Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages in the business of selling tangible personal property

Dated Aizawl, the 1 st Feb., 2018.

No.J.21011/1/2017-TAX/Vol-III(iv) GOVERNMENT OF MIZORAM TAXATION DEPARTMENT... N O T I F I C A T I O N Dated Aizawl, the 1 st Feb., 2018. In exercise of the powers conferred by section 164 of the Central

No.J.21011/1/2017-TAX/Vol-III(iv) GOVERNMENT OF MIZORAM TAXATION DEPARTMENT... N O T I F I C A T I O N Dated Aizawl, the 1 st Feb., 2018. In exercise of the powers conferred by section 164 of the Central

Total turnover/ Gross receipts 30% 30% of FY > Rs 50 Cr No change in rate of Surcharge

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

Internet Banking Provisions

Internet Banking Provisions Terms and Conditions of Hong Kong General Terms and Conditions of i-bank Service Article 1. (Purpose) The purpose of this General Terms and Conditions is to set forth terms

Internet Banking Provisions Terms and Conditions of Hong Kong General Terms and Conditions of i-bank Service Article 1. (Purpose) The purpose of this General Terms and Conditions is to set forth terms

Agreement with the University of Toronto for Voluntary Payments Relating to its Revenue-Producing Properties

STAFF REPORT ACTION REQUIRED Agreement with the University of Toronto for Voluntary Payments Relating to its Revenue-Producing Properties Date: September 30, 2013 To: From: Wards: Reference Number: Government

STAFF REPORT ACTION REQUIRED Agreement with the University of Toronto for Voluntary Payments Relating to its Revenue-Producing Properties Date: September 30, 2013 To: From: Wards: Reference Number: Government

POLICY FOR VACANCY REFUND APPLICATIONS 03/16/06

519-449-2451 Fax: 519-449-2454 1-888-250-2297 Taxation Division 26 Park Ave P.O. Box 160 Burford ON, N0E 1A0 POLICY FOR VACANCY REFUND APPLICATIONS 03/16/06 Purpose It is the policy of the Council that

519-449-2451 Fax: 519-449-2454 1-888-250-2297 Taxation Division 26 Park Ave P.O. Box 160 Burford ON, N0E 1A0 POLICY FOR VACANCY REFUND APPLICATIONS 03/16/06 Purpose It is the policy of the Council that

H 5209 S T A T E O F R H O D E I S L A N D

LC000 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO TAXATION - LEVY AND ASSESSMENT OF LOCAL TAXES Introduced By: Representative Michael

LC000 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO TAXATION - LEVY AND ASSESSMENT OF LOCAL TAXES Introduced By: Representative Michael