A Taxing NAPS Dilemma

|

|

|

- Francine Russell

- 5 years ago

- Views:

Transcription

1 A Taxing NAPS Dilemma

2 Do you know your NAPS Branch Tax Status?

3 How to check your NAPS Branch Tax Status Call the IRS tax exempt section at: Write the IRS at: (877) Internal Revenue Service TE/GE EO Determinations Office PO Box 2508 Cincinnati OH 45201

4 Why Become A Tax Exempt 501(c)(5)? Tax-exempt organizations do not pay federal income taxes on revenue in excess of expenses May not be required to pay State income taxes Most financial institutions waive banking fees IRS Form 990, 990-EZ or 990-N (epostcard) may be simpler than annual Corporate Form 1120 or Partnership Form 1065, K-1 and Schedule E If you do not choose to become tax-exempt then consider election as corporation over partnership

5 Tax Exempt 501(c)(5) Responsibilities Prior to 2007 tax filing not mandated for most nonprofits In 2007 law changed - every non-profit had to file tax returns for 3 consecutive years A non-profit (tax-exempt) organization that failed to file the required IRS 990, 990-EZ, 990-N (e-postcard) for three consecutive years automatically lost its taxexempt status After December 31, 2012 must reapply for non-profit

6 Tax Exempt 501(c)(5) Tax-exempt General Information Majority of states do not allow 501(c)(5) tax-exempt organizations to avoid paying state sales tax (Check State rules) Some state laws Non-Profit organization may not be sued Tax Exempt 501(c)(5) organizations do not allow for tax deduction contributions There is a cost to file for non-profit/tax exemption

7 Cost to File for Tax Exemption Internal Revenue Service charges the following User Fees: $400 for an organization that has average gross receipts of less than $10,000 for the preceding four years $850 for all other organizations Most NAPS branches will fall in the $850 user fee category

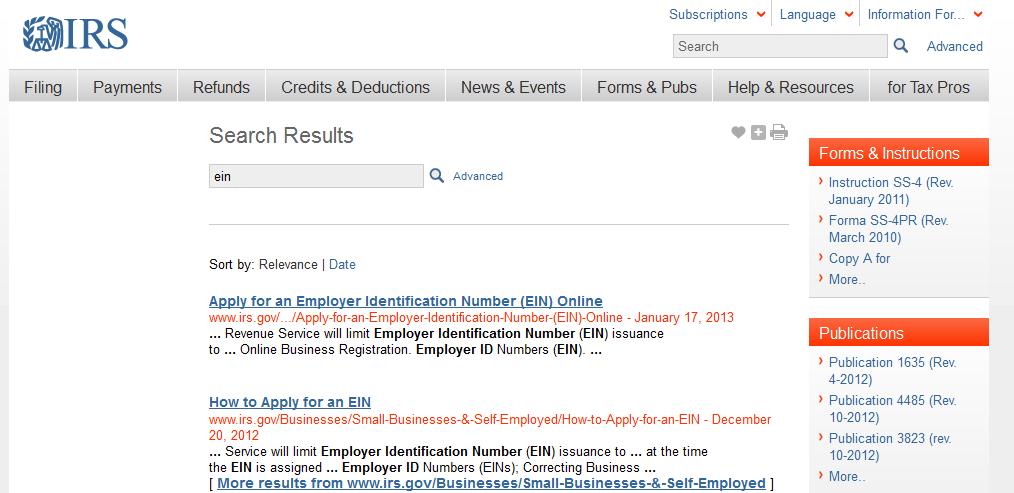

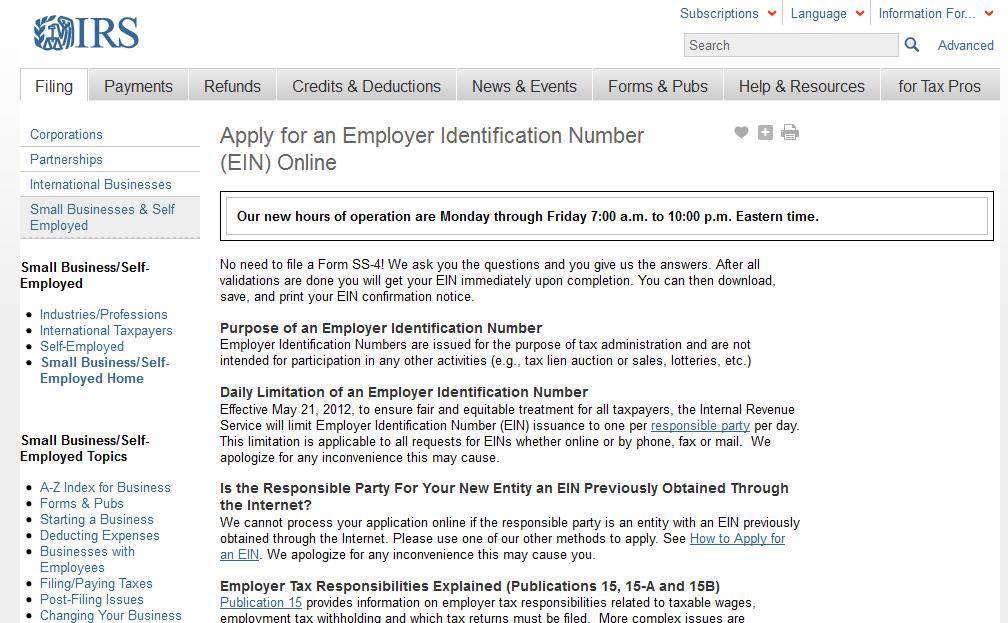

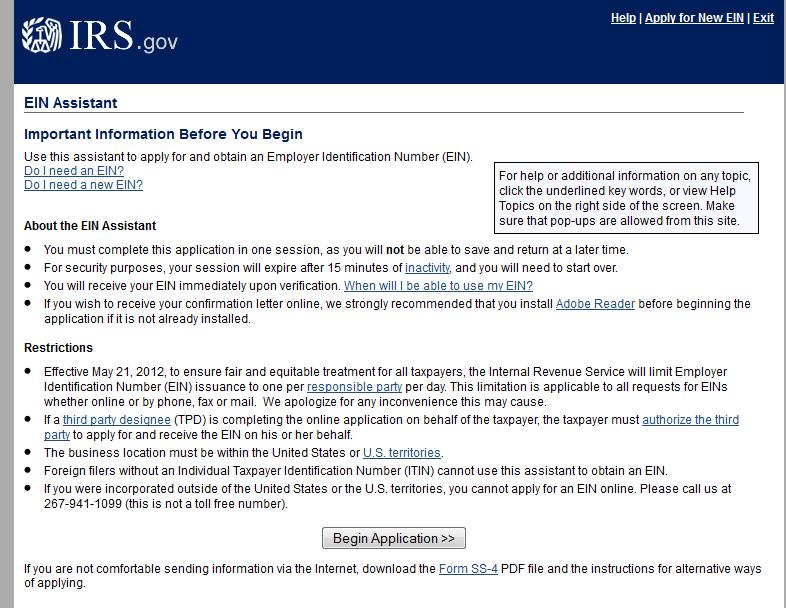

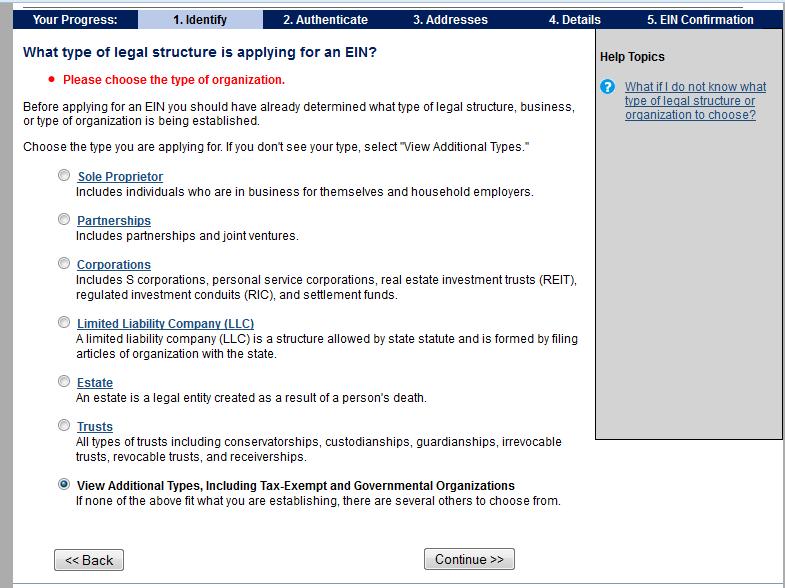

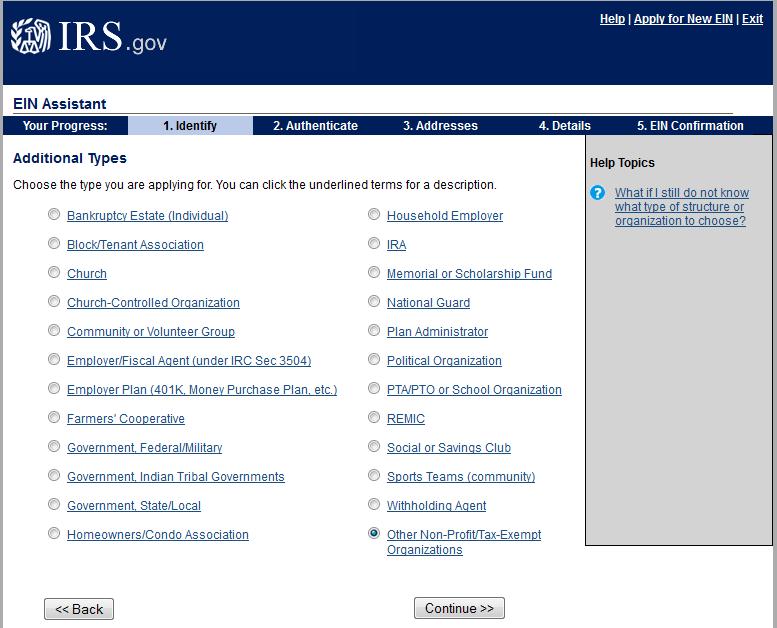

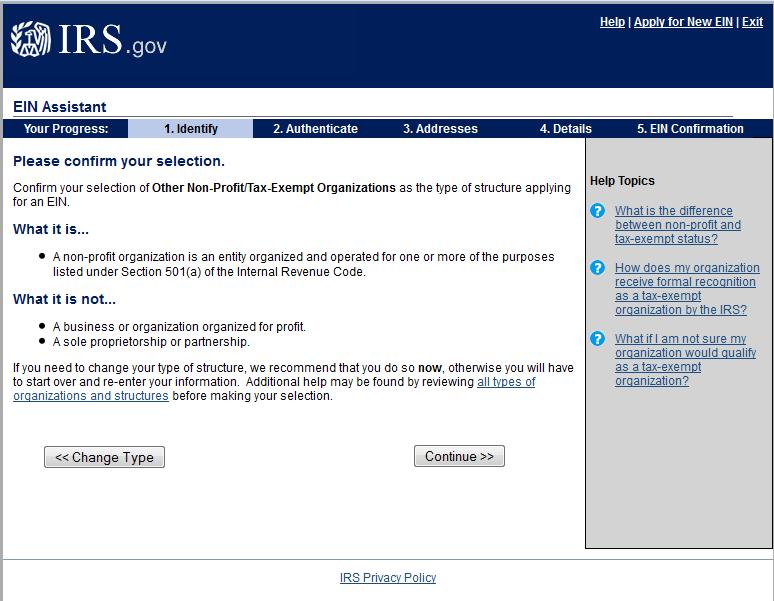

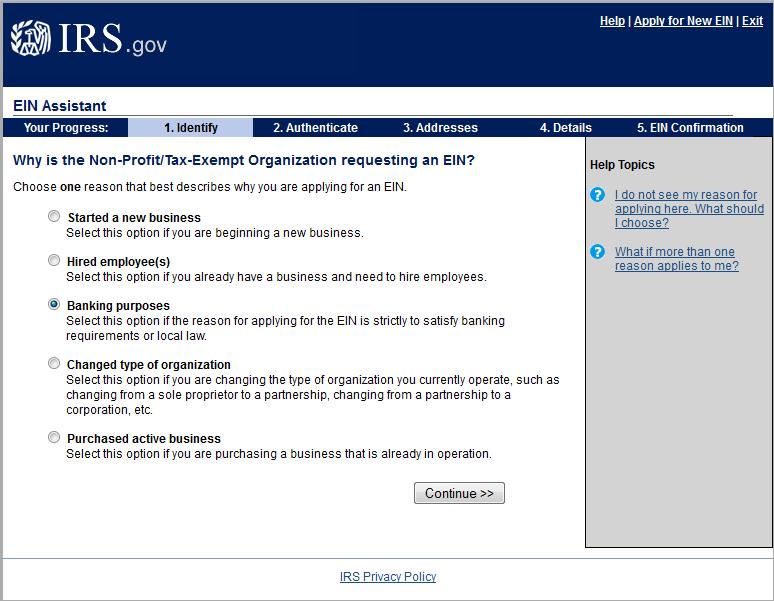

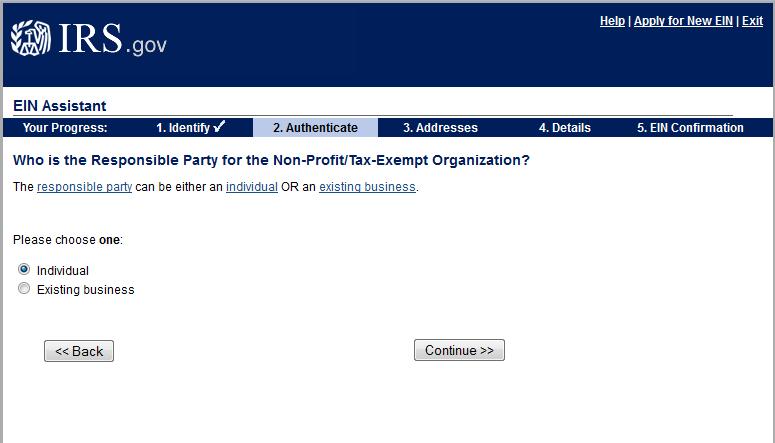

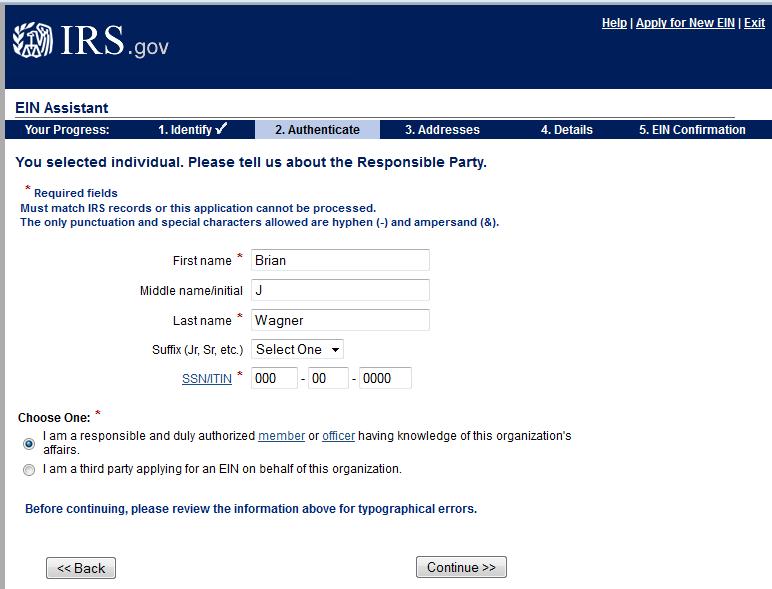

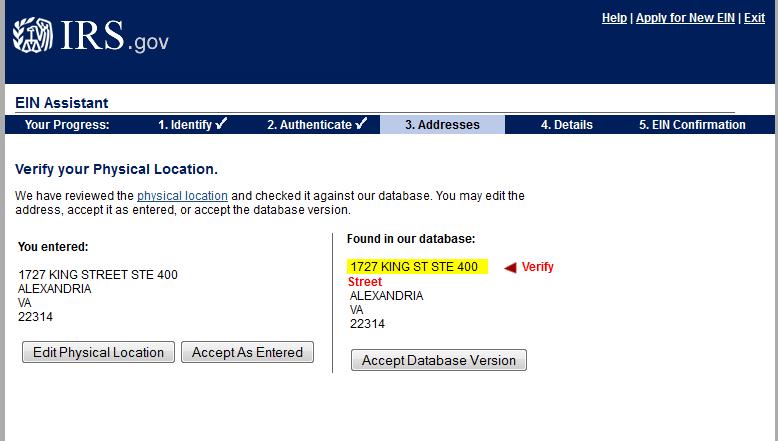

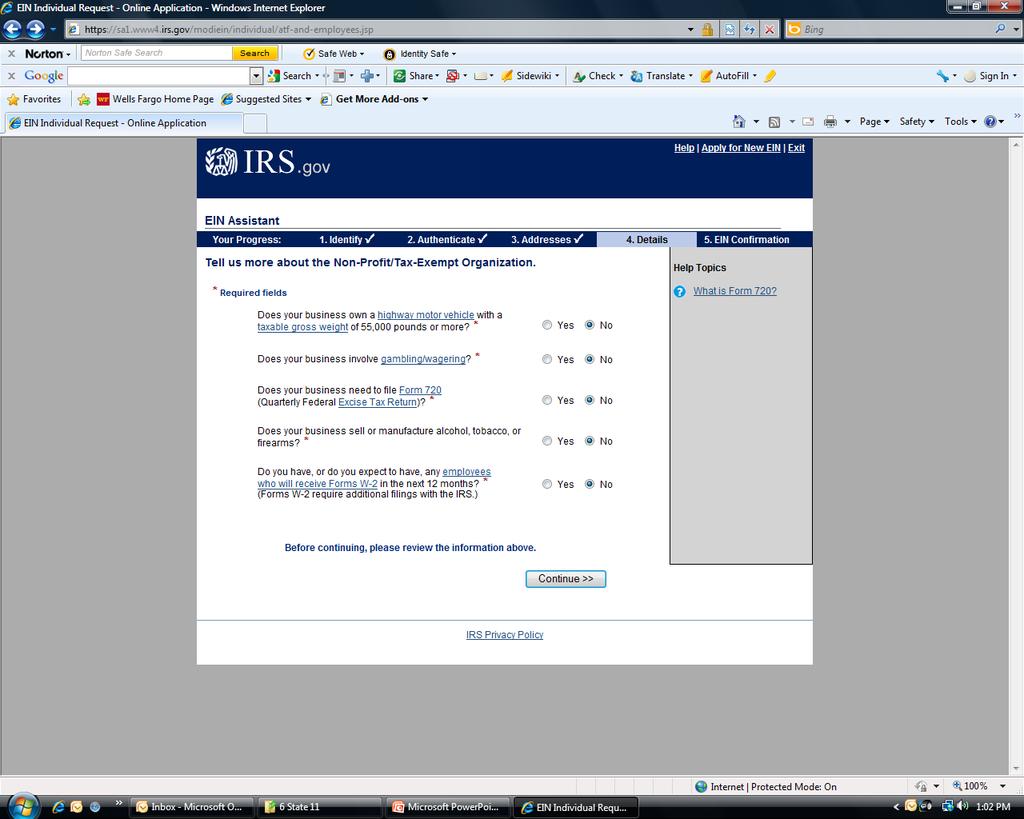

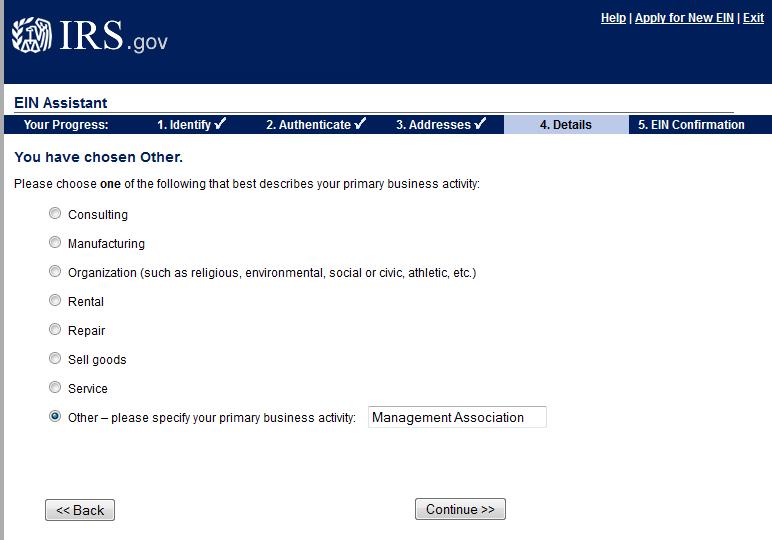

8 Elect Tax Exempt/Non-Profit - Where to Start? First Request an Employer Identification Number (EIN) if branch does not already have one SS-4 Application for Federal Employer Identification Number (EIN). May be requested online at Simplest way This is a free service offered by the Internal Revenue Service Check with your state if branch needs state number or charter In the IRS search type EIN SS4. Follow the instructions to apply on-line for EIN May also apply by mail a longer process

9 Elect Tax Exempt/Non-Profit - Where to Start?

10

11

12

13

14

15

16

17

18

19 Note: PO Box address is not acceptable

20

21

22

23

24

25

26 Elect Tax Exempt/Non-Profit - Where to Start? Second Form 1024 Application for Recognition of Exemption Under Section 501 Available on-line 18 page Form Complete only Pages 1 thru 5 & 9 NAPS HQ template available Mail all 18 pages NAPS HQ helpful instructions at Form 8718 User Fee for Exempt Organizations Available on-line

27 Elect Tax Exempt/Non-Profit - Where to Start? Third Mail IRS Forms 1024 & 8718 & supporting documentation Copy of Branch current Constitution & Bylaws Copy of your Branch Articles of Incorporation (If applicable) Copies of Branch Revenue & Expense Statements (Current Fiscal Year & past 3 years. (Matches Page 5/Form 1024) Copy of minutes from 2 recent branch meetings Copy of Branch newsletter (If applicable) Sign and date forms by an officer of the organization Mail Check/Money Order for User Fee payable to: United States Treasury

28 Information Necessary to File for Exemption Current Year to Date general ledger or financial report for NAPS Branch Three prior years of general ledger or financial report for NAPS Branch Assets Funds in Banks, Petty Cash, Investments, Fixed Assets (Value of Buildings, Vehicles, Furniture or Equipment, etc) Liabilities Money owed on debts or loans, etc.

29 Information Necessary to File for Exemption In Care Of person for Tax Matters Address for future correspondence of the organization (PO Box not Acceptable) All NAPS Branch Officers - Name, Address, Phone, Title, Annual Pay, Estimated Hours per week spent on NAPS activities Dated copy of the current Constitution and Bylaws of the NAPS Branch

30 Information Necessary to File for Exemption Dated copy of two previous newsletters of the NAPS Branch (If the branch prints a newsletter) Dated copy of the minutes of two previous meetings of the NAPS Branch (If no newsletter is published) Date the NAPS branch was formed or started (If not known contact NAPS HQ)

31 Elect Tax Exempt/Non-Profit Where to Mail Tax-Exempt Documents? Internal Revenue Service PO Box Covington KY

32 Tax Exempt/Non-Profit Your Branch is Approved Tax-Exempt/Non-Profit Now What?

Gross Receipts less than $50,000 Note: Annual NAPS DCO")

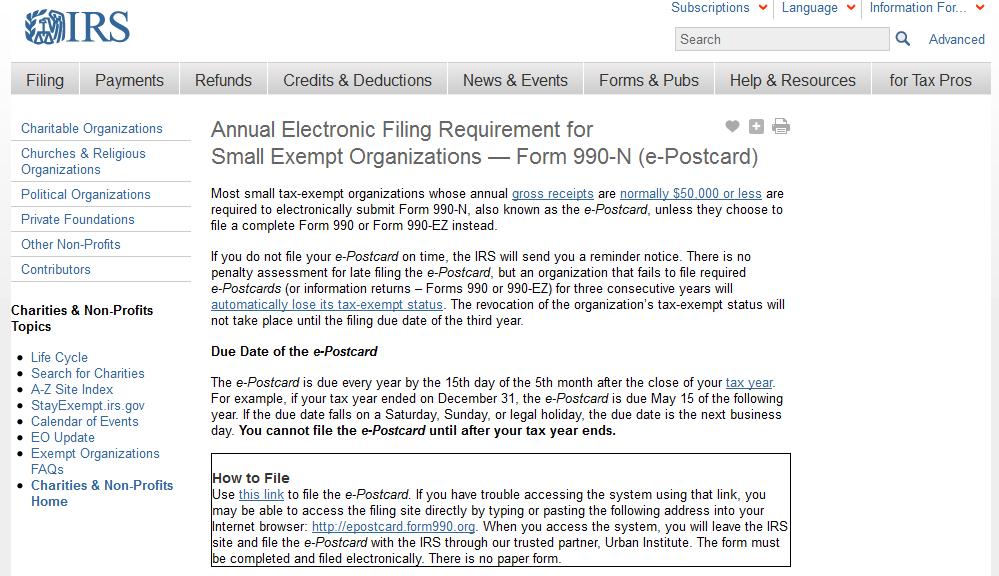

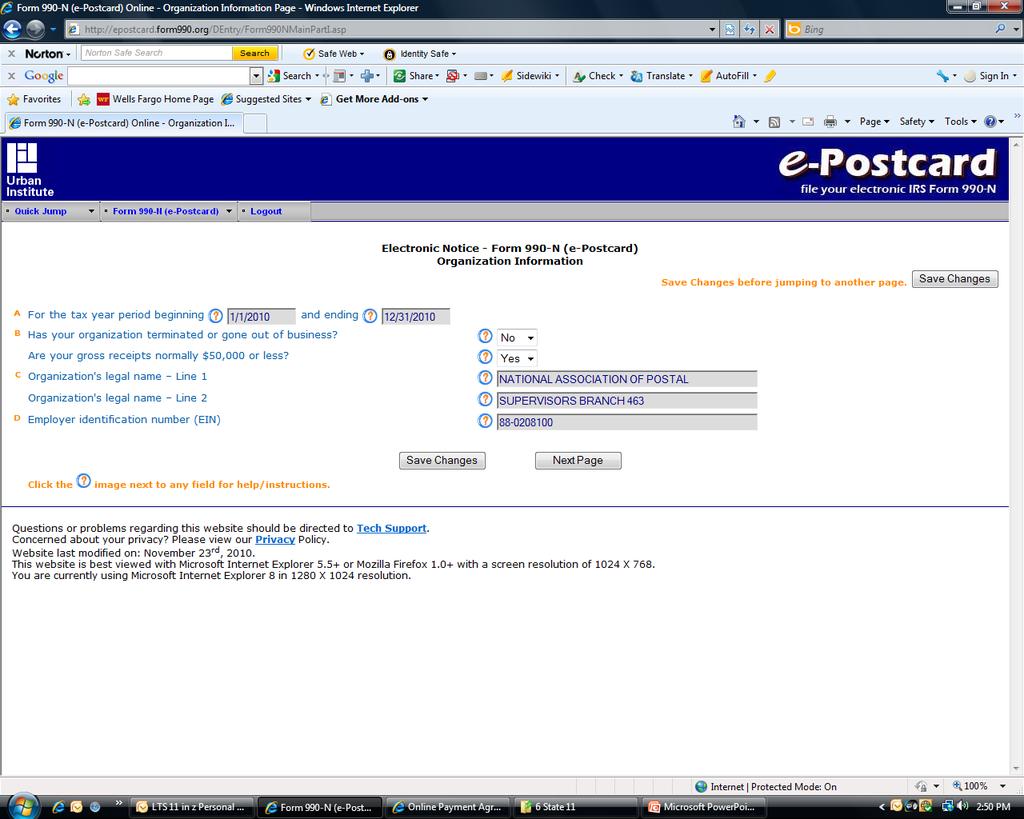

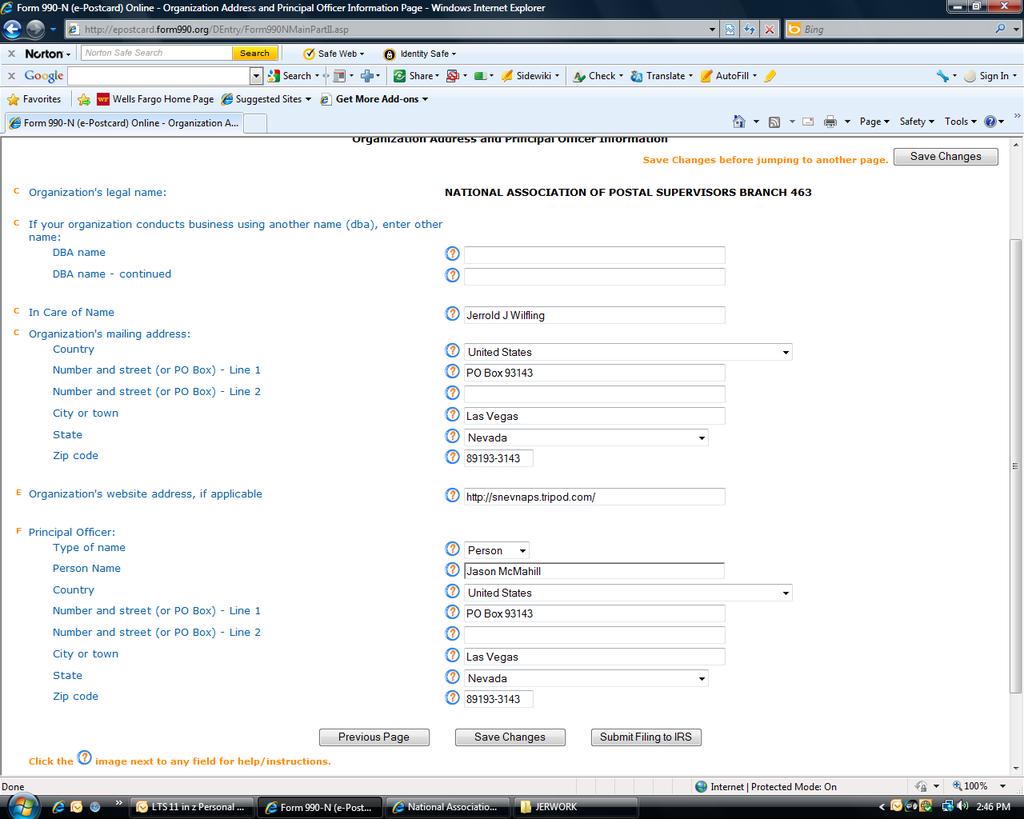

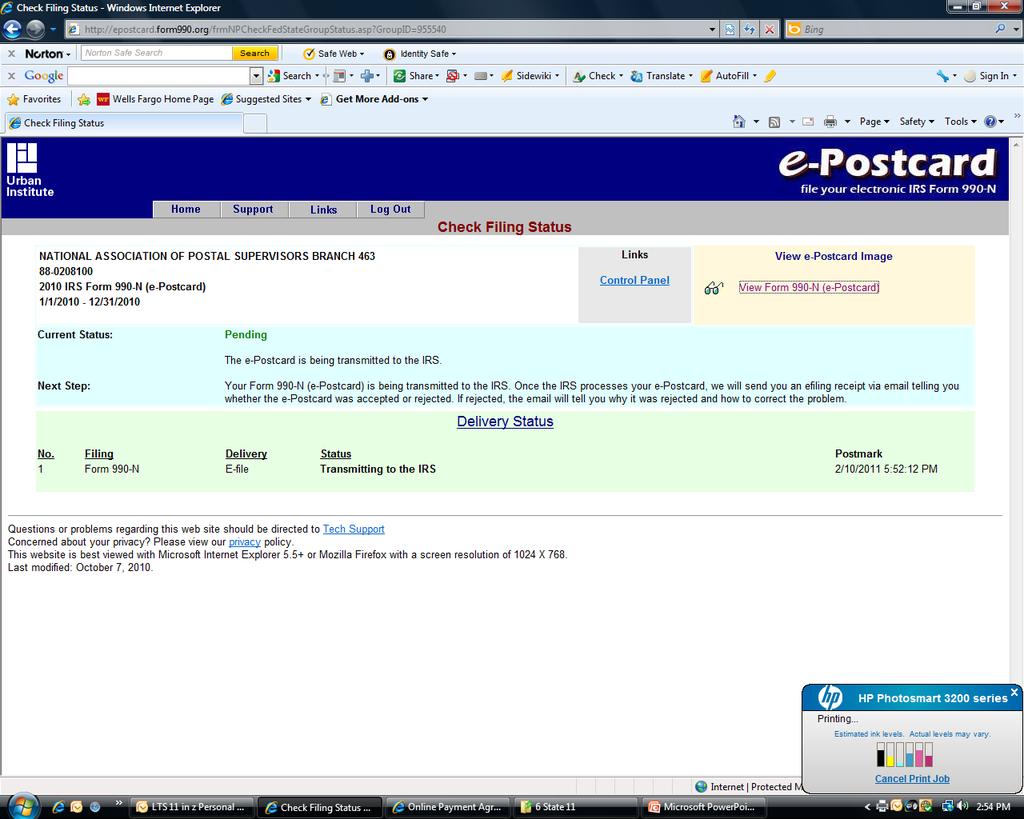

33 Annual IRS Filing Requirements Tax Exempt Organizations are required to file one of the following Forms by the 15 th day of the 5 th Month at the end of branch Fiscal Year: Form 990 Gross Receipts over $200,000 Form 990-EZ Gross Receipts over $50,000 up to $200,000 Electronic Form 990-N (epostcard) Gross Receipts less than $50,000 Note: Annual NAPS DCO 1099

34 Where to find 990 e-postcard Help?

35

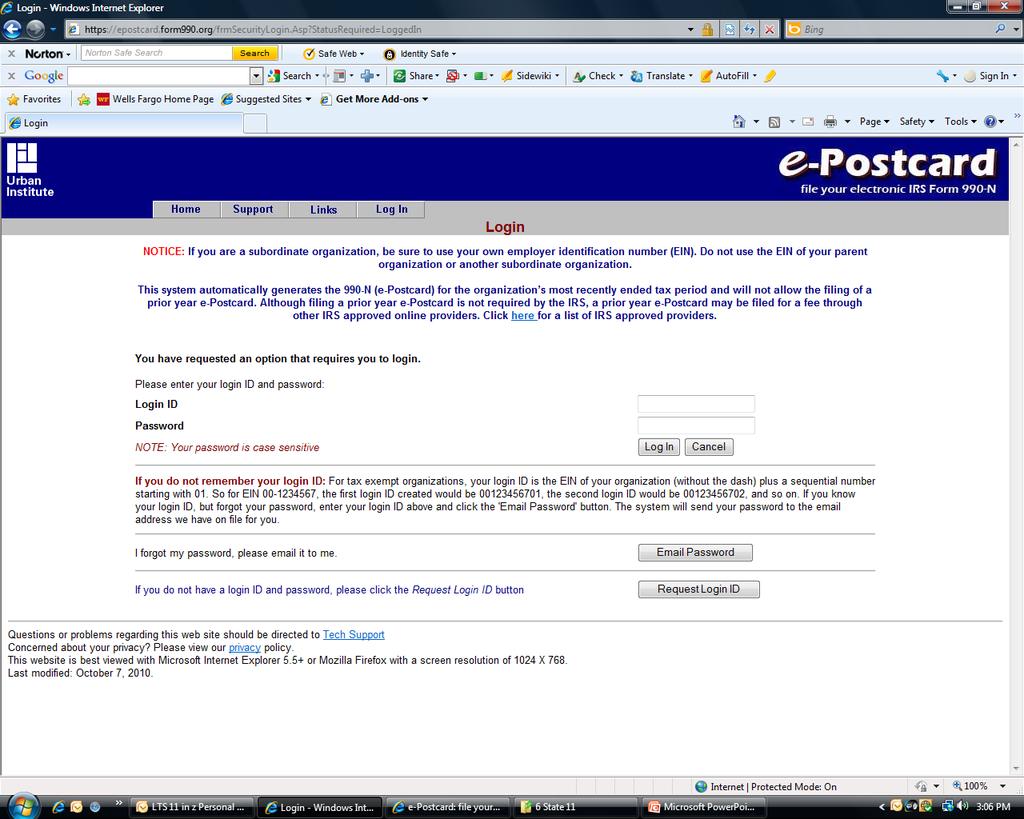

36 990-N (e-postcard) :

37 Leave IRS Site

38 How to file a 990 e-postcard Less than $50,000 in receipts

39

40

41

42

43 Due Date of the e-postcard The e-postcard is due every year by the 15th day of the 5th month after the close of your tax year For example, if your tax year ended on December 31, the e-postcard is due by May 15 of the following year If the due date falls on a Saturday, Sunday, or legal holiday, the due date is the next business day You cannot file the e-postcard until after your Fiscal Year ends

44 Forms to File for State Income Tax Tax-exempt/Non-Profit NAPS branches contact State Department of Revenue to determine income tax filing requirements. Each State is different. Example 1: IL Department of Revenue does not require a branch tax return to be filed, if NAPS Branch files a Federal 990 Form. Example 2: IL Department of Revenue requires an IL 990-T to be completed if a Federal 990-T is filed. Note: 990-T only!

45 File! File! File! Your Branch Taxes An organization that fails to file required e-postcards (or information returns Forms 990 or 990-EZ) for three consecutive years will automatically lose its tax-exempt status. The revocation of the organization s tax-exempt status will not take place until the filing due date of the third year. If you do not file your e-postcard on time, the IRS may assess your branch a late fee.

46 Don t Panic. Get Started! How? Establish Branch Accounting Method Manage Branch Records Do financial audits & reports Keep Branch Minutes Establish/update Branch Constitution & Bylaws Retain Branch Records

47 Accounting Methods Organizations may file annual returns on a Calendar Year basis or a Fiscal Year basis Organization may maintain their books and records on a Cash Method or an Accrual Method Cash Method record income when received and expenses when paid Accrual Method record income when earned and expenses when incurred

48 Accounting Methods Most NAPS branches maintain their records on a Calendar Year Basis January 1 through December 31 Most NAPS branches maintain their records on a Cash Method of Accounting Income received & expenses paid

Items Purchased for Resale Expenses Employment Tax Records Assets")

49 Managing Branch Records Maintain the following records on a manual general ledger or a computer accounting Program like Quickbooks: Gross Receipts (DCO Deposits NAPS DCO 1099) Items Purchased for Resale Expenses Employment Tax Records Assets Liabilities

50 Permanent Records Record Retention Applications for Tax Exempt Status and Federal Identification Numbers The Determination Letter recognizing the Organizations Tax Exemption Status from IRS and State Agencies Organizations Constitution and Bylaws, including amendments or updates

51 Records Retention Minimum Requirement Income Tax Returns should be kept for three years plus the current year General Ledgers and/or Financial Reports should be kept for three years plus the current year Records may be kept indefinitely if the organization chooses

52 Employment Records Form 1099 must be issued to any Officer or Member who is compensated an amount of $600 or more per year Form W-2 must be issued to any Officer or Member who is compensated as an employee of the Tax Exempt Organization, where taxes are withheld and transmitted to the IRS Reimbursements for expenses are exempt from this requirement Stipend/Salaries/Gratuities for officers? Be careful. Stipend for reimbursement of incidental expenses?

53 Reporting Changes to IRS A Tax Exempt Organization that is required to file a Form 990 or Form 990-EZ must report name, address, structural and operational changes on its annual return A Tax Exempt Organization that is only required to file an electronic Form 990-N, may report these type of changes by writing to: Internal Revenue Service TE/GE EO Determinations Office PO Box 2508 Cincinnati OH 45201

54 Change of In Care of Person All organizations must have an In Care Of person and/or responsible person for tax matters: Sign Tax Exempt Application Forms Sign Annual Tax and Information Returns In Care Of person should be one of the following individuals in each NAPS Branch: President, Treasurer or Secretary or Secretary/Treasurer

55 Change of Address or In Care Of Person Important Note: When Officers of NAPS Branches change, the following information must be reported to the Internal Revenue Service: To change the address of the NAPS Branch for Tax Records File IRS Form 8822 To change the name and address of the In Care Of person for the NAPS Branch File IRS Form 8822

56 Un-Taxing the Dilemma Contact NAPS HQ Secretary/Treasurer: To request a template/semi-completed IRS Form 1024 For assistance in final completion of IRS Form 1024 With general inquiries/questions about IRS Non-Profit & Tax-Exempt forms NAPS HQ recommends a branch contact tax professionals for all complicated tax issues related to branch tax filing.

Chapter Tax Compliance Requirements

Chapter Tax Compliance Requirements Federal tax law provides income tax exemption to nonprofit organizations. The Pension Protection Act of 2006 created the requirement for small orgaizatrions, defined

Chapter Tax Compliance Requirements Federal tax law provides income tax exemption to nonprofit organizations. The Pension Protection Act of 2006 created the requirement for small orgaizatrions, defined

SOUTH CAROLINA. End of the Year Duties for Treasurers Candace Leggett, SCPTA Treasurer 2013 SCPTA Convention Saturday, May 4, 2013

SOUTH CAROLINA End of the Year Duties for Treasurers Candace Leggett, SCPTA Treasurer 2013 SCPTA Convention Saturday, May 4, 2013 Let s Talk About Money Management Reports and IRS Regulations Insurance

SOUTH CAROLINA End of the Year Duties for Treasurers Candace Leggett, SCPTA Treasurer 2013 SCPTA Convention Saturday, May 4, 2013 Let s Talk About Money Management Reports and IRS Regulations Insurance

Federal Financial Requirements

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

Organizational Guidelines for Friendship Force Clubs in the USA Effective Date: June 23, 2017

Organizational Guidelines for Friendship Force Clubs in the USA Effective Date: June 23, 2017 Friendship Force clubs are independent organizations with each club responsible for developing and maintaining

Organizational Guidelines for Friendship Force Clubs in the USA Effective Date: June 23, 2017 Friendship Force clubs are independent organizations with each club responsible for developing and maintaining

Federal Tax-Exempt Status 501(c)(3) Organizations

(3) Organizations") Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

Thank you! 7/26/2011 For information purposes only. NOT LEGAL OR TAX ADVICE.

On July 14, a webinar called How to reinstate and maintain your IRS tax exempt status was conducted. Weʹre sorry to report that some of the information was inaccurate. The presenters did present accurate

On July 14, a webinar called How to reinstate and maintain your IRS tax exempt status was conducted. Weʹre sorry to report that some of the information was inaccurate. The presenters did present accurate

Information for Sumner County School Support Organizations

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

IMPORTANT TAX AND FIDELITY BOND INFORMATION

AMERICAN LEGION AUXILIARY NATIONAL HEADQUARTERS IMPORTANT TAX AND FIDELITY BOND INFORMATION This information is intended to assist Units, Departments, Districts/Counties/Councils in understanding their

AMERICAN LEGION AUXILIARY NATIONAL HEADQUARTERS IMPORTANT TAX AND FIDELITY BOND INFORMATION This information is intended to assist Units, Departments, Districts/Counties/Councils in understanding their

FRATERNITY OF ALPHA ZETA - FAQ ABOUT TAXES AND THE FORM 990

FRATERNITY OF ALPHA ZETA - FAQ ABOUT TAXES AND THE FORM 990 2018 Table of Contents FAQ Overview 2 Your Chapter s Tax Responsibility 3 Tax Designation 6 Filing the Form 990 7 Fundraising and Donations as

FRATERNITY OF ALPHA ZETA - FAQ ABOUT TAXES AND THE FORM 990 2018 Table of Contents FAQ Overview 2 Your Chapter s Tax Responsibility 3 Tax Designation 6 Filing the Form 990 7 Fundraising and Donations as

Thinking About Changing Your Name?

This article presents general guidelines for Georgia nonprofit organizations as of the date written and should not be construed as legal advice. Always consult an attorney to address your particular situation.

This article presents general guidelines for Georgia nonprofit organizations as of the date written and should not be construed as legal advice. Always consult an attorney to address your particular situation.

Annual Electronic Filing Requirement Small Exempt Organizations Form 990-N

Annual Electronic Filing Requirement Small Exempt Organizations Form 990-N Utilized For ALL ENTITIES (Councils, Courts, Assembly s, Chapter s, Inter-City s, Inter-Districts, District Conferences, State

Annual Electronic Filing Requirement Small Exempt Organizations Form 990-N Utilized For ALL ENTITIES (Councils, Courts, Assembly s, Chapter s, Inter-City s, Inter-Districts, District Conferences, State

Federation of Genealogical Societies. by Cath Madden Trindle, CG. Supplemental Page

Society Strategies Federation of Genealogical Societies P.O. Box 200940 Austin TX 78720-0940 Series Set IV Number 5 August 2010 Set IV Strategies for Treasurers by Cath Madden Trindle, CG Supplemental

Society Strategies Federation of Genealogical Societies P.O. Box 200940 Austin TX 78720-0940 Series Set IV Number 5 August 2010 Set IV Strategies for Treasurers by Cath Madden Trindle, CG Supplemental

Local Section Finances

Local Section Finances Local sections, like the national association, must incur expenses, manage their budgets, pay bills, and deal with tax issues. The following information provides the basic requirements

Local Section Finances Local sections, like the national association, must incur expenses, manage their budgets, pay bills, and deal with tax issues. The following information provides the basic requirements

Kentucky Extension Homemakers Association

Kentucky Extension Homemakers Association April 12, 2010 KEHA Leaders and FCS Agents, In 2007, the Internal Revenue Service (IRS) changed filing requirements for non profit organizations. For the past

Kentucky Extension Homemakers Association April 12, 2010 KEHA Leaders and FCS Agents, In 2007, the Internal Revenue Service (IRS) changed filing requirements for non profit organizations. For the past

May PTA President and Treasurer,

May 2013 PTA President and Treasurer, Please read this entire notice. It includes pertinent information on tax laws that if overlooked may result in IRS fines. Even seasoned officers should take the time

May 2013 PTA President and Treasurer, Please read this entire notice. It includes pertinent information on tax laws that if overlooked may result in IRS fines. Even seasoned officers should take the time

Sumner County School Support Organizations

Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information Additional information and resources for School Support Organizations may be found

Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information Additional information and resources for School Support Organizations may be found

Treasurer s Guide. Chapter Leadership Training. NMA...THE Leadership Development Organization

Treasurer s Guide Chapter Leadership Training NMA...THE Leadership Development Organization January 2017 Chapter Leader Training TREASURER S GUIDE NMA THE Leadership Development Organization 2210 Arbor

Treasurer s Guide Chapter Leadership Training NMA...THE Leadership Development Organization January 2017 Chapter Leader Training TREASURER S GUIDE NMA THE Leadership Development Organization 2210 Arbor

501(c)(3) for Parent Groups. The Basics

(3) for Parent Groups. The Basics") 501(c)(3) for Parent Groups The Basics Do 501(c)(3), tax exemption, and nonprofit all mean the same thing? People tend to use these terms interchangeably, but they have distinct definitions. 501(c)(3)

501(c)(3) for Parent Groups The Basics Do 501(c)(3), tax exemption, and nonprofit all mean the same thing? People tend to use these terms interchangeably, but they have distinct definitions. 501(c)(3)

Council Tax-Exempt Status Workshop

1902-2002 Purpose: To review the requirements for securing and maintaining Internal Revenue Service Section 501(c)(3) tax-exempt status for a Navy League council. Learning Objectives: 1. To review the

1902-2002 Purpose: To review the requirements for securing and maintaining Internal Revenue Service Section 501(c)(3) tax-exempt status for a Navy League council. Learning Objectives: 1. To review the

Instructions for Reinstatement of Tax-Exempt Status

Instructions for Reinstatement of Tax-Exempt Status Dear Local PTA: The IRS has issued letters revoking the tax-exempt status of numerous organizations, including many local PTAs, for failure to file information

Instructions for Reinstatement of Tax-Exempt Status Dear Local PTA: The IRS has issued letters revoking the tax-exempt status of numerous organizations, including many local PTAs, for failure to file information

(c)(3) Applying for 501(c)(3) Tax-Exempt Status,

(3) Applying for 501(c)(3) Tax-Exempt Status,") Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

Applicable Sections: Revenue Procedure SECTION 1. PURPOSE

Applicable Sections: 26 CFR 1.6033-2. Returns by exempt organizations (taxable years beginning after December 31, 1969) and returns by certain nonexempt organizations (taxable years beginning after December

Applicable Sections: 26 CFR 1.6033-2. Returns by exempt organizations (taxable years beginning after December 31, 1969) and returns by certain nonexempt organizations (taxable years beginning after December

Chapter Tax Filing Requirements

Chapter Tax Filing Requirements Purpose of Document Provide guidance to chapter officers regarding requirement for yearly tax filling to maintain nonprofit status. Provide guidance regarding Senior Chapter

Chapter Tax Filing Requirements Purpose of Document Provide guidance to chapter officers regarding requirement for yearly tax filling to maintain nonprofit status. Provide guidance regarding Senior Chapter

HOTV ByLaws. File for Status. Bank Account. Record Retention. Heart of the Valley 501C3 Investigation Report. ByLaws. Requirements: Mission Statement:

Legal Requirements Slides before 1st Section Divider Requirements: Heart of the Valley 501C3 Investigation Report HOTV ByLaws Mission Statement: File for Status ByLaws Incorporation Bank Account Record

Legal Requirements Slides before 1st Section Divider Requirements: Heart of the Valley 501C3 Investigation Report HOTV ByLaws Mission Statement: File for Status ByLaws Incorporation Bank Account Record

FRISCO INDEPENDENT SCHOOL DISTRICT

FRISCO INDEPENDENT SCHOOL DISTRICT STUDENT SERVICES BOOSTER CLUB REQUIREMENTS AND OPERATIONAL GUIDELINES 2017-2018 FOREWORD Frisco Independent School District recognizes the importance of parent and community

FRISCO INDEPENDENT SCHOOL DISTRICT STUDENT SERVICES BOOSTER CLUB REQUIREMENTS AND OPERATIONAL GUIDELINES 2017-2018 FOREWORD Frisco Independent School District recognizes the importance of parent and community

A Primer on Chapter Financial Management. Washington State HR Council Pam Gibbons, Treasurer June 2015

A Primer on Chapter Financial Management Washington State HR Council Pam Gibbons, Treasurer June 2015 Where to Start Bylaws Must be approved by SHRM and voted on by Board First step in getting legal Tax

A Primer on Chapter Financial Management Washington State HR Council Pam Gibbons, Treasurer June 2015 Where to Start Bylaws Must be approved by SHRM and voted on by Board First step in getting legal Tax

Despite the government shutdown, the IRS confirmed that it will process tax returns beginning January 28, 2019.

January 17, 2019 To: Officers of ACS Local Sections From: Rosalee Lewis, Senior Tax Manager, Tax Compliance & Reporting RE: Tax Information Update Another year has passed and, once again, it is time to

January 17, 2019 To: Officers of ACS Local Sections From: Rosalee Lewis, Senior Tax Manager, Tax Compliance & Reporting RE: Tax Information Update Another year has passed and, once again, it is time to

Fiscal Fitness for Units: A Guide for Treasurers

Fiscal Fitness for Units: A Guide for Treasurers October 25 th, 2017 Sean M. Hannam NYS PTA Treasurer treasurer@nyspta.org What is a Treasurer? The Treasurer plays a key role in the ongoing operation of

Fiscal Fitness for Units: A Guide for Treasurers October 25 th, 2017 Sean M. Hannam NYS PTA Treasurer treasurer@nyspta.org What is a Treasurer? The Treasurer plays a key role in the ongoing operation of

Transitional Relief under Internal Revenue Code 6033(j) for Small. This notice provides transitional relief for certain small organizations that have

for Small. This notice provides transitional relief for certain small organizations that have") Part III - Administrative, Procedural, and Miscellaneous Transitional Relief under Internal Revenue Code 6033(j) for Small Organizations Notice 2011-43 This notice provides transitional relief for certain

Part III - Administrative, Procedural, and Miscellaneous Transitional Relief under Internal Revenue Code 6033(j) for Small Organizations Notice 2011-43 This notice provides transitional relief for certain

PTO/Booster Club Financial Guidelines

PTO/Booster Club Financial Guidelines Revised August 2015 Accounting Procedures Parent Organizations/Booster Clubs should include written instructions on the recording of accounting transactions in their

PTO/Booster Club Financial Guidelines Revised August 2015 Accounting Procedures Parent Organizations/Booster Clubs should include written instructions on the recording of accounting transactions in their

INSTRUCTIONS FOR REGISTRATION STATEMENT (COR-92) AND ADDITIONAL DOCUMENTATION NEEDED FOR INITIAL REGISTRATION

AND ADDITIONAL DOCUMENTATION NEEDED FOR INITIAL REGISTRATION") INSTRUCTIONS FOR REGISTRATION STATEMENT (COR-92) AND ADDITIONAL DOCUMENTATION NEEDED FOR INITIAL REGISTRATION Instructions for completing Initial Registration and form: This form, along with several other

INSTRUCTIONS FOR REGISTRATION STATEMENT (COR-92) AND ADDITIONAL DOCUMENTATION NEEDED FOR INITIAL REGISTRATION Instructions for completing Initial Registration and form: This form, along with several other

A PTA can only engage in an insubstantial amount of lobbying activity.

Most PTAs are classified as taxexempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are exempt under Section 501(c)(3) of the IRC is that

Most PTAs are classified as taxexempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are exempt under Section 501(c)(3) of the IRC is that

Financial Reports and Certification and IRS Electronic Filing Overview

Financial Reports and Certification and IRS Electronic Filing Overview April Powers-Matthews, Treasurer Kevin Coleman, Financial Secretary Blacks In Government Region XI Council 1 Financial Reports and

Financial Reports and Certification and IRS Electronic Filing Overview April Powers-Matthews, Treasurer Kevin Coleman, Financial Secretary Blacks In Government Region XI Council 1 Financial Reports and

Gross receipts $200,000, or total assets $500,

To: Officers of ACS Divisions From: Rosalee Lewis, Tax Manager, Tax Compliance & Reporting RE: Tax Information Update Another year has passed and, once again, it is time to prepare information and income

To: Officers of ACS Divisions From: Rosalee Lewis, Tax Manager, Tax Compliance & Reporting RE: Tax Information Update Another year has passed and, once again, it is time to prepare information and income

Financial Reports and Certification and IRS Electronic Filing Overview

Financial Reports and Certification and IRS Electronic Filing Overview April Powers-Matthews, Treasurer Kevin Coleman, Financial Secretary Region XI Council 1 Financial Reports and Certification and IRS

Financial Reports and Certification and IRS Electronic Filing Overview April Powers-Matthews, Treasurer Kevin Coleman, Financial Secretary Region XI Council 1 Financial Reports and Certification and IRS

2015 Federal Tax Returns

2015 Federal Tax Returns All Knights of Columbus subordinate units in the United States must file an annual informational tax return (IRS Form 990) with the Internal Revenue Service (IRS). This memorandum

2015 Federal Tax Returns All Knights of Columbus subordinate units in the United States must file an annual informational tax return (IRS Form 990) with the Internal Revenue Service (IRS). This memorandum

The Business of Running a Shelter or Rescue: Organization Document Filing Requirements

The Business of Running a Shelter or Rescue: Organization Document Filing Requirements Adrienne Linnell, MAC Treasurer September 30, 2018 First, The IRS 990 Not a tax filing; a report of activities and

The Business of Running a Shelter or Rescue: Organization Document Filing Requirements Adrienne Linnell, MAC Treasurer September 30, 2018 First, The IRS 990 Not a tax filing; a report of activities and

BOOSTER CLUB TRAINING. Department of Athletics Temple Independent School District

BOOSTER CLUB TRAINING Department of Athletics Temple Independent School District Booster Club Website www.wildcatstrong.com Hover over Wildcat HQ Select Booster Clubs Board Policy GE Local The Board is

BOOSTER CLUB TRAINING Department of Athletics Temple Independent School District Booster Club Website www.wildcatstrong.com Hover over Wildcat HQ Select Booster Clubs Board Policy GE Local The Board is

How to Get Your Nonprofit Back in Good Standing

How to Get Your Nonprofit Back in Good Standing Texas nonprofits are subject to numerous complicated laws and regulations, filing and reporting requirements. Failure to comply with these requirements can

How to Get Your Nonprofit Back in Good Standing Texas nonprofits are subject to numerous complicated laws and regulations, filing and reporting requirements. Failure to comply with these requirements can

Show Me the Money! Financial & Fiduciary Responsibili9es for Leaders

Show Me the Money! Financial & Fiduciary Responsibili9es for Leaders Rodney Rowe, Secretary Treasurer, Educa9on Minnesota Michael Roehl, CFO, Educa9on Minnesota COMPETENCY: BUSINESS Competency progression

Show Me the Money! Financial & Fiduciary Responsibili9es for Leaders Rodney Rowe, Secretary Treasurer, Educa9on Minnesota Michael Roehl, CFO, Educa9on Minnesota COMPETENCY: BUSINESS Competency progression

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT General information Financial policies and controls Fundraising Reporting Learning from the past District policies and procedures Q&A NOTE: This presentation is

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT General information Financial policies and controls Fundraising Reporting Learning from the past District policies and procedures Q&A NOTE: This presentation is

(c)(3) Compliance Guide for 501(c)(3) Public Charities,

(3) Compliance Guide for 501(c)(3) Public Charities,") Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Compliance Guide for 501(c)(3) Public Charities, Inside: Activities that may jeopardize a charity s exempt status, Federal information returns, tax

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Compliance Guide for 501(c)(3) Public Charities, Inside: Activities that may jeopardize a charity s exempt status, Federal information returns, tax

Parent Support Organizations Mandatory Training August 18, 2018

Parent Support Organizations Mandatory Training August 18, 2018 Vnet & GPS Finance TRAINING AGENDA I. Purpose of Training II. Definition and Role of the Parent Support Organization (PSO) A. Types B. Role

Parent Support Organizations Mandatory Training August 18, 2018 Vnet & GPS Finance TRAINING AGENDA I. Purpose of Training II. Definition and Role of the Parent Support Organization (PSO) A. Types B. Role

Attention: The IRS is Revising Publication 4302, A Charity s Guide to Car Donations

Attention: The IRS is Revising Publication 4302, A Charity s Guide to Car Donations The IRS is in the process of revising Publication 4302 dated August 2004. This version does not include the tax law changes

Attention: The IRS is Revising Publication 4302, A Charity s Guide to Car Donations The IRS is in the process of revising Publication 4302 dated August 2004. This version does not include the tax law changes

Internal Revenue Service Compliance Guide for 501(c)(3) Public Charities

(3) Public Charities") Internal Revenue Service Compliance Guide for 501(c)(3) Public Charities Federal tax law provides tax benefits to nonprofit organizations recognized as exempt from federal income tax under section 501(c)(3)

Internal Revenue Service Compliance Guide for 501(c)(3) Public Charities Federal tax law provides tax benefits to nonprofit organizations recognized as exempt from federal income tax under section 501(c)(3)

B O O S T E R T R E A S U R E R W O R KS H O P

B O O S T E R T R E A S U R E R W O R KS H O P 2018 CHARACTERISTICS: Desire to serve with other Boosters, the school, and ultimately the students Computer literate - - must know how to use Excel, QuickBooks,

B O O S T E R T R E A S U R E R W O R KS H O P 2018 CHARACTERISTICS: Desire to serve with other Boosters, the school, and ultimately the students Computer literate - - must know how to use Excel, QuickBooks,

Activities that may jeopardize exempt status. Federal information returns, tax returns or notices that must be filed. Recordkeeping why, what, when

(a) Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Compliance Guide for Tax-Exempt Organizations (other than 501(c)(3) Public Charities and Private Foundations) Covers:

(a) Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Compliance Guide for Tax-Exempt Organizations (other than 501(c)(3) Public Charities and Private Foundations) Covers:

PO Box 34002<;1 N~-!.TN <;1 1.g.I"':/cf. org (6L5) 36q.240q

36q.240q") GefA GENERAL COU~,jCIL ON finai',ce t\nd ADMINI') - RATION THE UNITED METHODIST CHURCH PO Box 34002

GefA GENERAL COU~,jCIL ON finai',ce t\nd ADMINI') - RATION THE UNITED METHODIST CHURCH PO Box 34002

A Charity s Guide to. Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible contributions.

Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations A Charity s Guide to Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible

Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations A Charity s Guide to Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible

Compliance Guide for Tax-Exempt Organizations

INTERNAL REVENUE SERVICE TAX-EXEMPT AND GOVERNMENT ENTITIES EXEMPT ORGANIZATIONS, Compliance Guide for Tax-Exempt Organizations (Other than 501(c)(3) Public Charities and Private Foundations), Inside:

INTERNAL REVENUE SERVICE TAX-EXEMPT AND GOVERNMENT ENTITIES EXEMPT ORGANIZATIONS, Compliance Guide for Tax-Exempt Organizations (Other than 501(c)(3) Public Charities and Private Foundations), Inside:

IPMA-HR Chapter &Region Accounting Manual

IPMA-HR Chapter &Region Accounting Manual Issued July 2014 1 P age Basic Financial Statements As Chapter/Region Treasurer you will be generally be concerned with two basic financial statements: balance

IPMA-HR Chapter &Region Accounting Manual Issued July 2014 1 P age Basic Financial Statements As Chapter/Region Treasurer you will be generally be concerned with two basic financial statements: balance

North American Derivatives Exchange, Inc., 311 South Wacker Drive, Suite 2675, Chicago, IL 60606

Jaime M. Walsh +1 (312) 884-0927 Jaime.walsh@nadex.com January 7, 2016 Via CFTC Portal Submissions Mr. Christopher Kirkpatrick Secretary of the Commission Office of the Secretariat Commodity Futures Trading

Jaime M. Walsh +1 (312) 884-0927 Jaime.walsh@nadex.com January 7, 2016 Via CFTC Portal Submissions Mr. Christopher Kirkpatrick Secretary of the Commission Office of the Secretariat Commodity Futures Trading

Booster Organization Handbook

Booster Organization Handbook Contents Steps to Start a Booster Organization Step 1 Organize Step 2 Take Care of Legalities Step 3 Create a Financial System Step 4 Apply for Booster Recognition with your

Booster Organization Handbook Contents Steps to Start a Booster Organization Step 1 Organize Step 2 Take Care of Legalities Step 3 Create a Financial System Step 4 Apply for Booster Recognition with your

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

VICE PRESIDENT - FINANCE This is your PACKET FOR NEW OFFICERS

Congratulations on your election as VICE PRESIDENT - FINANCE This is your PACKET FOR NEW OFFICERS What s inside? Everything you need to know for your position. We want to assist you towards full understanding

Congratulations on your election as VICE PRESIDENT - FINANCE This is your PACKET FOR NEW OFFICERS What s inside? Everything you need to know for your position. We want to assist you towards full understanding

Ruritan. Handbook. Club Treasurer s. Revised 8/17. Ruritan Club. Club Treasurer

Ruritan Club Treasurer s Handbook Ruritan Club Club Treasurer Revised / CLUB TREASURER Duties and Responsibilities. Serving as a member of the board of directors and finance committee.. Serving as custodian

Ruritan Club Treasurer s Handbook Ruritan Club Club Treasurer Revised / CLUB TREASURER Duties and Responsibilities. Serving as a member of the board of directors and finance committee.. Serving as custodian

Instructions Forming a California Corporation

Contact Information State Business: Entities Department: California Secretary of State Business Entities Mailing Address: PO Box 944260 Sacramento, CA 94244-2600 Physical Address: Phone: 916.657.5448 Facsimile:

Contact Information State Business: Entities Department: California Secretary of State Business Entities Mailing Address: PO Box 944260 Sacramento, CA 94244-2600 Physical Address: Phone: 916.657.5448 Facsimile:

FOR SUBORDINATE EVANGELISTIC/RELIGIOUS ORGANIZATION CHARTERS For year ending

FOR SUBORDINATE EVANGELISTIC/RELIGIOUS ORGANIZATION CHARTERS For year ending Dear Chartered (Subordinate) Ministry, Greetings, in the precious name of our Lord, Jesus Christ! We praise God for the privilege

FOR SUBORDINATE EVANGELISTIC/RELIGIOUS ORGANIZATION CHARTERS For year ending Dear Chartered (Subordinate) Ministry, Greetings, in the precious name of our Lord, Jesus Christ! We praise God for the privilege

August 5, Via CFTC Portal Submissions

August 5, 2016 Via CFTC Portal Submissions Mr. Christopher Kirkpatrick Secretary of the Commission Office of the Secretariat Commodity Futures Trading Commission 3 Lafayette Centre 1155 21 st Street, N.W.

August 5, 2016 Via CFTC Portal Submissions Mr. Christopher Kirkpatrick Secretary of the Commission Office of the Secretariat Commodity Futures Trading Commission 3 Lafayette Centre 1155 21 st Street, N.W.

Guidebook Chartering a State Chapter of VUFT

Guidebook Chartering a State Chapter of VUFT Version 1.0 6/7/08 Version 1.0 6/7/08 Guidebook Chartering a State Chapter of VUFT Introduction Veterans United For Truth, Inc. (hereinafter VUFT) is incorporated

Guidebook Chartering a State Chapter of VUFT Version 1.0 6/7/08 Version 1.0 6/7/08 Guidebook Chartering a State Chapter of VUFT Introduction Veterans United For Truth, Inc. (hereinafter VUFT) is incorporated

STATE COUNCIL/CHAPTER TREASURER HANDBOOK

STATE COUNCIL/CHAPTER TREASURER HANDBOOK By VEITNAM VETERANS OF AMERICA, INC And VVA CONFERENCE OF STATE COUNCIL PRESIDENTS Adopted at the Conference of State Council Presidents Meeting April 10, 2003

STATE COUNCIL/CHAPTER TREASURER HANDBOOK By VEITNAM VETERANS OF AMERICA, INC And VVA CONFERENCE OF STATE COUNCIL PRESIDENTS Adopted at the Conference of State Council Presidents Meeting April 10, 2003

Edmond Public Schools. Sanctioned Organizations

Edmond Public Schools Sanctioned Organizations Contact Information for EPS Jeanise Wynn, Business Manager Phone: (405) 340-2881 Email: jeanise.wynn@edmondschools.net Debbie Smith, Executive Assistant Phone:

Edmond Public Schools Sanctioned Organizations Contact Information for EPS Jeanise Wynn, Business Manager Phone: (405) 340-2881 Email: jeanise.wynn@edmondschools.net Debbie Smith, Executive Assistant Phone:

Instructions Forming a Michigan Corporation

Contact Information State Business: Entities Department: Michigan Department of Licensing & Regulatory Affairs Bureau of Commercial Services Mailing Address: PO Box 30054 Lansing, MI 48909-7554 Physical

Contact Information State Business: Entities Department: Michigan Department of Licensing & Regulatory Affairs Bureau of Commercial Services Mailing Address: PO Box 30054 Lansing, MI 48909-7554 Physical

E. HOW TO ELECTRONICALLY FILE IRS FORM 1023-EZ

E. HOW TO ELECTRONICALLY FILE IRS FORM 1023-EZ An organization that wants to apply for recognition of its tax-exempt status as a Section 501(c)(3) organization needs to complete a Form 1023, Application

E. HOW TO ELECTRONICALLY FILE IRS FORM 1023-EZ An organization that wants to apply for recognition of its tax-exempt status as a Section 501(c)(3) organization needs to complete a Form 1023, Application

SUPPLEMENTAL FORMS TO THE OPERATIONS MANUAL

SUPPLEMENTAL FORMS TO THE OPERATIONS MANUAL UPDATED 2017 Last Update 03/14/2017 1 TABLE OF CONTENTS SECTION 1: Setting up your business (church). 3-4 SECTION 2: Online Access for Churches and Ministers...

SUPPLEMENTAL FORMS TO THE OPERATIONS MANUAL UPDATED 2017 Last Update 03/14/2017 1 TABLE OF CONTENTS SECTION 1: Setting up your business (church). 3-4 SECTION 2: Online Access for Churches and Ministers...

Wylie Independent School District. Booster Club Guidelines

Wylie Independent School District Booster Club Guidelines Wylie ISD Booster Club Guidelines Contents UIL Booster Club Guidelines... 4 Role of Booster Clubs... 5 District Booster Clubs Shall:... 5 District

Wylie Independent School District Booster Club Guidelines Wylie ISD Booster Club Guidelines Contents UIL Booster Club Guidelines... 4 Role of Booster Clubs... 5 District Booster Clubs Shall:... 5 District

Chapter Treasurer s Handbook

Chapter Treasurer s Handbook NATIONAL ASSOCIATION OF WOMEN IN CONSTRUCTION THIS HANDBOOK IS THE PROPERTY OF YOUR NAWIC CHAPTER. PLEASE PASS ON TO THE APPROPRIATE PERSON WHEN YOUR TERM AS TREASURER IS OVER.

Chapter Treasurer s Handbook NATIONAL ASSOCIATION OF WOMEN IN CONSTRUCTION THIS HANDBOOK IS THE PROPERTY OF YOUR NAWIC CHAPTER. PLEASE PASS ON TO THE APPROPRIATE PERSON WHEN YOUR TERM AS TREASURER IS OVER.

Regarding Your Assembly's 2017 Federal and State Tax Filing Requirements

2018 TAX ALERT After you have been informed by Vickie Garcia your Assembly's 2017 Annual IRS Financial Report is correct, you may file your Forms 199N e-postcard a RRF-1. Regarding Your Assembly's 2017

2018 TAX ALERT After you have been informed by Vickie Garcia your Assembly's 2017 Annual IRS Financial Report is correct, you may file your Forms 199N e-postcard a RRF-1. Regarding Your Assembly's 2017

Make check payable to : United States Treasury

In 2006 a bill was passed by congress requiring that Non Profit Organizations submit their 990: Tax Return for Non Profit Organizations, even if no revenue was generated. This bill went into effect in

In 2006 a bill was passed by congress requiring that Non Profit Organizations submit their 990: Tax Return for Non Profit Organizations, even if no revenue was generated. This bill went into effect in

American Podiatric Medical Association Component Registration and Reporting Requirements with the IRS and State Record Offices

April 25, 2017 American Podiatric Medical Association Component Registration and Reporting Requirements with the IRS and State Record Offices Richard Riley Foley & Lardner LLP Washington DC Basic Requirements

April 25, 2017 American Podiatric Medical Association Component Registration and Reporting Requirements with the IRS and State Record Offices Richard Riley Foley & Lardner LLP Washington DC Basic Requirements

STATE/PROVINCIAL TREASURER Example Job Description and Guidelines

STATE/PROVINCIAL TREASURER Example Job Description and Guidelines This position s example job description includes references as stated in the International and State Bylaws, and the Compilation of International

STATE/PROVINCIAL TREASURER Example Job Description and Guidelines This position s example job description includes references as stated in the International and State Bylaws, and the Compilation of International

4-H CLUB TREASURER S RECORD BOOK

4-H CLUB TREASURER S RECORD BOOK Name of Club: County: Year: Officers: President: Vice President: Secretary: Treasurer: Other: 4-H TREASURER Congratulations on your new responsibility as 4-H treasurer.

4-H CLUB TREASURER S RECORD BOOK Name of Club: County: Year: Officers: President: Vice President: Secretary: Treasurer: Other: 4-H TREASURER Congratulations on your new responsibility as 4-H treasurer.

Instructions for Form 990-EZ

2009 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2009 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

INSTRUCTIONS 2015 ANNUAL RETURN

INSTRUCTIONS 2015 ANNUAL RETURN PLEASE READ THE ENTIRE INSTRUCTION BOOKLET BEFORE PROCEEDING Annual Returns are due on or before March 15, 2016 (Section 25070) By Code, you will be subject to a $3 per

INSTRUCTIONS 2015 ANNUAL RETURN PLEASE READ THE ENTIRE INSTRUCTION BOOKLET BEFORE PROCEEDING Annual Returns are due on or before March 15, 2016 (Section 25070) By Code, you will be subject to a $3 per

Corridor District of the North Carolina Conference The United Methodist Church

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

2018 BUSINESS TAX ORGANIZER

The following items are required to begin the preparation of your business tax returns. Please provide copies of documents which we can retain for our files. We encourage you to use Liscio to securely

The following items are required to begin the preparation of your business tax returns. Please provide copies of documents which we can retain for our files. We encourage you to use Liscio to securely

Checklist for Dissolving Your Business

Checklist for Dissolving Your Business This template is not intended as legal advice. Your organizational goals, purpose, values, and bylaws should drive the creation of this document. What is a corporate

Checklist for Dissolving Your Business This template is not intended as legal advice. Your organizational goals, purpose, values, and bylaws should drive the creation of this document. What is a corporate

NOTICE TO INTERESTED PARTIES OF THE SPEEDWAY RETIREMENT SAVINGS PLAN

This Notice to Interested Parties is required by the when an application is made by Speedway LLC for an advance determination on the tax qualification status of the Speedway Retirement Savings Plan. While

This Notice to Interested Parties is required by the when an application is made by Speedway LLC for an advance determination on the tax qualification status of the Speedway Retirement Savings Plan. While

Arizona PTA/PTSA Local Units and Councils Annual Financial Review Packet

Arizona Arizona PTA/PTSA Local Units and Councils Annual Financial Review Packet Upon completion of the annual financial review/professional audit, provide copies to the President, Vice President, Secretary

Arizona Arizona PTA/PTSA Local Units and Councils Annual Financial Review Packet Upon completion of the annual financial review/professional audit, provide copies to the President, Vice President, Secretary

Hindu Temple & Cultural Center of Wisconsin ACCOUNTING POLICIES AND PROCEDURES

Hindu Temple & Cultural Center of Wisconsin ACCOUNTING POLICIES AND PROCEDURES September 26, 2014 TABLE OF CONTENTS 1.00 BACKGROUND INFORMATION... 1 1.10 Tax Status & Purpose... 1 2.00 CHART OF ACCOUNTS...

Hindu Temple & Cultural Center of Wisconsin ACCOUNTING POLICIES AND PROCEDURES September 26, 2014 TABLE OF CONTENTS 1.00 BACKGROUND INFORMATION... 1 1.10 Tax Status & Purpose... 1 2.00 CHART OF ACCOUNTS...

Money Matters for ALL PTA Leaders

Money Matters for ALL PTA Leaders Pam Grigorian and Nicole Ponziani PTA 2016 Convention Leadership Training Money Matters to the Board Board members are expected to use good business judgement when making

Money Matters for ALL PTA Leaders Pam Grigorian and Nicole Ponziani PTA 2016 Convention Leadership Training Money Matters to the Board Board members are expected to use good business judgement when making

How to apply for an EIN (Employer Identification Number) for your Alpha Kappa Delta chapter:

for your Alpha Kappa Delta chapter:") How to apply for an EIN (Employer Identification Number) for your Alpha Kappa Delta chapter: If you are a new AKD chapter, please use the following instructions to apply for your chapter s EIN. This is

How to apply for an EIN (Employer Identification Number) for your Alpha Kappa Delta chapter: If you are a new AKD chapter, please use the following instructions to apply for your chapter s EIN. This is

Starting a Non-Profit Organization in Indiana. Filling Out the Forms

Starting a Non-Profit Organization in Indiana Filling Out the Forms Key Points Incorporating as a non-profit does not automatically result in 501(c)3 status or state sales and income tax exemption. These

Starting a Non-Profit Organization in Indiana Filling Out the Forms Key Points Incorporating as a non-profit does not automatically result in 501(c)3 status or state sales and income tax exemption. These

Treasurer s Glossary of Terms A

Treasurer s Glossary of Terms A Access - A database package that comes with Microsoft Office accrual basis accounting - A method of accounting where income is recognized when earned, even if not yet received,

Treasurer s Glossary of Terms A Access - A database package that comes with Microsoft Office accrual basis accounting - A method of accounting where income is recognized when earned, even if not yet received,

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Emily Robertson Attorney Robertson Law Office @RLOonNonprofits Amy Sinykin

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Emily Robertson Attorney Robertson Law Office @RLOonNonprofits Amy Sinykin

THE SCHOOL DISTRICT OF GREENVILLE COUNTY

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

Financial Update for PTOs and Booster Clubs

Financial Update for PTOs and Booster Clubs Beaufort County School District September 30, 2014 What Kind of PTO/Booster Club Parent are you? The Ruler 2 Starting a PTO, PTA, or Booster Club 3 Starting

Financial Update for PTOs and Booster Clubs Beaufort County School District September 30, 2014 What Kind of PTO/Booster Club Parent are you? The Ruler 2 Starting a PTO, PTA, or Booster Club 3 Starting

Friends of the Library Financial Policies

Note: This may seem to be overkill for such a small organization. The Executive Committee is proposing these policies to ensure that the 501(c)3 status which the IRS has given to the Friends will not be

Note: This may seem to be overkill for such a small organization. The Executive Committee is proposing these policies to ensure that the 501(c)3 status which the IRS has given to the Friends will not be

Introduction: Incorporation:

Introduction: Does your chapter have too much or too little money in the bank? Has your chapter raised money for the benefit of a charity or scholarship? Has your chapter had an independent financial review

Introduction: Does your chapter have too much or too little money in the bank? Has your chapter raised money for the benefit of a charity or scholarship? Has your chapter had an independent financial review

TREASURER Section 5. Louisiana

TREASURER 2017 2018 Section 5 Louisiana INTRODUCTION The treasurer is the authorized custodian of the funds of the association. However, the president, who bears full responsibility for the affairs of

TREASURER 2017 2018 Section 5 Louisiana INTRODUCTION The treasurer is the authorized custodian of the funds of the association. However, the president, who bears full responsibility for the affairs of

REPORTING SEASON IS HERE AGAIN!

CSEA LOCAL 1000 AFSCME / AFL-CIO 143 WASHINGTON AVENUE, ALBANY, NEW YORK 12210 M E M O R A N D U M TO: FROM: REGION, LOCAL AND UNIT TREASURERS WILLIAM WALSH, STATEWIDE TREASURER DATE: NOVEMBER 2016 RE:

CSEA LOCAL 1000 AFSCME / AFL-CIO 143 WASHINGTON AVENUE, ALBANY, NEW YORK 12210 M E M O R A N D U M TO: FROM: REGION, LOCAL AND UNIT TREASURERS WILLIAM WALSH, STATEWIDE TREASURER DATE: NOVEMBER 2016 RE:

Highlights of Council Fiscal Management

Highlights of Council Fiscal Management Good fiscal management is measured by maintaining sufficient resources in all funds and using them in order to deliver effective programs, eliminating or reducing

Highlights of Council Fiscal Management Good fiscal management is measured by maintaining sufficient resources in all funds and using them in order to deliver effective programs, eliminating or reducing

NOTICE TO INTERESTED PARTIES OF THE MARATHON PETROLEUM THRIFT PLAN

This Notice to Interested Parties is required by the when an application is made by MPC for an advance determination on the tax qualification status of the Marathon Petroleum Thrift Plan. While specific

This Notice to Interested Parties is required by the when an application is made by MPC for an advance determination on the tax qualification status of the Marathon Petroleum Thrift Plan. While specific

finance table of contents

Page 2 Introduction Welcome to PTA leadership! Overview 3 Duties of the treasurer 4 Contents of the treasurer s file 5 Records retention 7 Sample annual report 8 Sample monthly treasurer s report 9 Final

Page 2 Introduction Welcome to PTA leadership! Overview 3 Duties of the treasurer 4 Contents of the treasurer s file 5 Records retention 7 Sample annual report 8 Sample monthly treasurer s report 9 Final

Club Treasurer s Guide Altrusa International, Inc.

Club Treasurer s Guide Altrusa International, Inc. Updated April 2013 Notes About This Guide: This guide is meant to be a generic guide for each fiscal year. In some cases your Altrusa District may have

Club Treasurer s Guide Altrusa International, Inc. Updated April 2013 Notes About This Guide: This guide is meant to be a generic guide for each fiscal year. In some cases your Altrusa District may have

Tax Issues for Limited Liability Companies

Tax Issues for Limited Liability Companies What You Should Know About Limited Liability Companies... What is a Limited Liability Company? A Limited Liability Company (LLC) is a relatively new business

Tax Issues for Limited Liability Companies What You Should Know About Limited Liability Companies... What is a Limited Liability Company? A Limited Liability Company (LLC) is a relatively new business

FORM 990N INFORMATION

FORM 990N INFORMATION REGISTER & FILE AT: www.irs.gov/990n For filing fiscal y/e June 30, 2017, ALL clubs must register at website above. All United States Non-Profit organizations are required by the

FORM 990N INFORMATION REGISTER & FILE AT: www.irs.gov/990n For filing fiscal y/e June 30, 2017, ALL clubs must register at website above. All United States Non-Profit organizations are required by the

Financial Workshop. A Leader s first job is to protect the assets and the reputation of PTA. Mandatory Financial Training

Financial Workshop Mandatory Financial Training A Leader s first job is to protect the assets and the reputation of PTA. 2 1 Training Objectives Board/Treasurer Responsibilities Review Protecting Non Profit

Financial Workshop Mandatory Financial Training A Leader s first job is to protect the assets and the reputation of PTA. 2 1 Training Objectives Board/Treasurer Responsibilities Review Protecting Non Profit

SIERRA PACIFIC REGION

SIERRA PACIFIC REGION TREASURER S HANDBOOK 2017-2018 Soroptimist improves the lives of women and girls through programs leading to social and economic empowerment. Table of Contents FORWARD... 3 Club Treasurer

SIERRA PACIFIC REGION TREASURER S HANDBOOK 2017-2018 Soroptimist improves the lives of women and girls through programs leading to social and economic empowerment. Table of Contents FORWARD... 3 Club Treasurer

Indiana 4-H Program Policy and Procedures Frequently Asked Questions A Resource for 4-H Volunteers and Extension Educators

Indiana 4-H Program Policy and Procedures Frequently Asked Questions A Resource for 4-H Volunteers and Extension Educators 1. Why does 4-H have a different status than other youth organizations? The 4-H

Indiana 4-H Program Policy and Procedures Frequently Asked Questions A Resource for 4-H Volunteers and Extension Educators 1. Why does 4-H have a different status than other youth organizations? The 4-H