Personal Income Tax Update. AGA Winter Seminar 2013 Nathan Abbott, CISA, CFE, EA

|

|

|

- Archibald Golden

- 5 years ago

- Views:

Transcription

1 Personal Income Tax Update AGA Winter Seminar 2013 Nathan Abbott, CISA, CFE, EA

2 The Easy Stuff

3 Inflation Adjustments

4 Inflation Adjustments

5 Inflation Adjustments

6 Inflation Adjustments Social Security Maximum earnings subject to SS $110,100 Maximum employee pays is $4, Retire before Full retirement age max amount $14,640 before paying back benefits In the year full retirement age $38,880

7

8 Income Tax Update Fiscal Cliff Extenders Bush Tax Cuts Expiration Health Care Tax Effects

9 TAX Year 2011 AMT State Sales Tax Deductions Tuition & Fees Deductions Qualified Education Expense Deduction Mortgage Insurance Premium Deduction Qualified Charitable IRA Distribution

10 AMT Alternative Minimum Tax [AMT] AMT Patch

11 AMT AMT exemption amounts for 2011 will revert to pre-2001 levels of $33,750 for single, $45,000 for MFJ, and $22,500 for MFS Without the patch, the government estimates that as many as 80% of taxpayers with incomes between $100,000 and $200,000 would have owed the AMT on their 2010 returns

12 Itemize Deductions State Sales tax deductions Mortgage insurance premium deduction [PMI] Qualified charitable IRA distributions

13 Education Deductions Tuition and fees deduction Qualified education expense deduction

14 Tax Year 2013 Tax rate hike Phase-out of itemized deductions Earned income credit Child tax credit American opportunity credit Adoption assistance income exclusion Marriage penalty Capital Gains Payroll tax holiday

15 Bush Tax Cuts 10% 15% 28% 33% 35% 2012 Tax Rates 2013 Tax Rates 15% 28% 31% 36% 39.5%

16 Itemize Deductions Phase-out of itemized deductions and personal exemptions

17 Earned Income Credit The EIC benefit will decrease for many taxpayers. First, the overall calculation reverts to pre-2001 law. Also, the maximum benefit available will be for families with two children instead of three.

18 Child Tax Credit Starting in 2013, the child tax credit amount will be $500 per child (reduced from the current $1,000 per child) and refundability will be limited to families with three or more children and who meet other qualifications

19 Education Credit The American opportunity credit enhancement to the Hope credit is set to expire at the end of Beginning in 2013, this credit will revert to the regular Hope credit rules, including a twoyear availability limitation and a maximum credit of $1,800. The credit is also nonrefundable.

20 Adoption Under current law, employees may exclude employer provided adoption assistance payments from income. This exclusion will expire at the end of 2012 making the benefit subject to both income and payroll taxes. Because the exclusion cannot be claimed on the tax return until the adoption is finalized, individuals that received payments in a year before 2012 may be unable to exclude those assistance payments if the adoption is not finalized until 2013.

21 Marriage Penalty The break for the MFJ 15% tax bracket will be 167% of the single tax bracket, rather than 200% as under current law. Likewise, the standard deduction will be 167% rather than 200% of the standard deduction for singles

22 Capital Gains 2012 Long-Term Rates 0% 15% 2013 Long Term Rates 10% 20% All dividends will be taxed at ordinary income tax rates rather than favorable capital gain rates.

23 Payroll Tax The 2% reduction in the social security tax that we have all enjoyed for the past two years

24 ATRA The Senate and House have passed HR 8, the American Taxpayer Relief Act of 2012 (ATRA) AMT relief (the AMT patch) has been made permanent

25 ATRA 2 Year Extenders Deduction for state and local general sales tax 170(b)(1)(E) an itemized deduction (Schedule A) for sales tax in lieu of state income tax. Qualified charitable contributions 408(d)(8)(F) tax-free rollovers of up to $100,000 from IRAs to qualified charitable organizations Qualified mortgage insurance premiums deductible as home mortgage interest

26 ATRA 2 Year Extenders Tax-exempt employer-provided transit benefits 132(f) qualified employer-provided mass transit passes are excluded from employees gross income. Nonbusiness energy property credit 25C up to $500 maximum lifetime credit for qualified energy efficient home improvements (windows, furnaces, etc.). Electric drive vehicle credits 30D up to $2,500 credit for two-and three-wheeled plug-in electric vehicles. Expanded section 179 deduction The maximum deduction was scheduled to decrease to $139,000 (phaseout starting at $560,000).

27 EXTENDED FOR ONE YEAR: 2013 Qualified principal residence indebtedness exclusion 108(a)(1) cancellation of debt of up to $2 million on a qualified principal residence is excluded from gross income. Bonus depreciation 50% bonus depreciation expired remains in effect for property placed in service during 2013.

28 PERMANENT EXTENSION OF BUSH TAX CUTS Tax rate and bracket system 1 the current rates of 10%, 15%, 25%, 28%, 33%, and 35% have been made permanent. The pre-2001 rate of 39.6% applies to taxable incomes over $400,000 ($425,000 HOH, $450,000 MFJ, $225,000 MFS). These thresholds will be inflation adjusted after 2013 Marriage penalty relief 1 the standard deduction and the lower (10% and 15%) tax bracket cut-offs for joint filers remain at 200% of the single filer amounts

29 PERMANENT EXTENSION OF BUSH TAX CUTS Capital gains and dividends 1 the current rates for net long-term capital gains and qualified dividends of 0% and 15% have been made permanent. The pre-2001 rate of 20% applies to taxpayers with taxable incomes over $400,000 ($425,000 HOH, $450,000 MFJ, $225,000 MFS). These thresholds will be inflation adjusted after 2013 Phase out of personal exemptions and itemized deductions (PEP and PEASE) 68 and 151(d) the phaseouts (reductions) of personal exemptions and itemized deductions are permanently repealed for taxpayers with AGI over $250,000 ($275,000 HOH, $300,000 MFJ, $150,000 MFS). These thresholds will be inflation adjusted after 2013

30 PERMANENT EXTENSION OF BUSH TAX CUTS Adoption credit 23 the expanded credit under the 2001 Tax Act has been made permanent. The expanded credit is $10,000 (to be adjusted for inflation; the maximum 2012 credit is $12,650) and expenses are deemed paid for children with special needs. The provisions for employerprovided adoption assistance are made permanent as well. Note: the refundability feature of ACA expired after 2011 and has not been extended. Child tax credit 24 the maximum $1,000 child tax credit and additional child tax credit per child have been made permanent. Also see the section on Temporary Extension of 2009 Tax Breaks (below) for other child tax credit relief.

31 PERMANENT EXTENSION OF BUSH TAX CUTS Dependent care credit 21 the maximum expense on which the credit is calculated will remain permanently at $3,000 for one child ($6,000 for two children) and the maximum percentage will remain at 35%. Thus the maximum credit will be $1,050 ($2,100 for two children) Earned income credit 32 the higher phaseout range for joint filers and other 2001 Tax Act modifications are permanently extended. Also see the section on Temporary Extension of 2009 Tax Breaks for other EITC relief.

32 PERMANENT EXTENSION OF BUSH TAX CUTS Coverdell ESAs 530 expanded education savings account provisions allowing a $2,000 annual contribution per student for qualified elementary, secondary, and higher education expenses has been made permanent. Student loan interest deduction 221 expanded provisions of the 2001 Tax Act, including the availability of the deduction for an unlimited number of years and deductibility of interest on voluntary payments have been made permanent.

33 TEMPORARY TAX CUTS American opportunity credit (AOC) 25A(i) the expanded Hope credit up to $2,500, partially refundable, and available for the first four years of higher education is extended through 2017 Child tax credit 24 in addition to the permanent extension of the 2001/2003 features, the lower refundability threshold of $3,000 will be available through 2017 Earned income credit 32 in addition to the permanent extension of the 2001/2003 provisions, expanded phaseout for joint filers and a higher credit for families with three or more children remain available through 2017

34 Health Care Law In 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) and the Health Care and Education Reconciliation Act of 2010 into law

35

36 Tax Year 2010

37 Small Employer Insurance Credit Credit is up to 35% of health cost small business * Currently about 4.4 million small businesses that provide employee health insurance are eligible for the credit [per Kaiser health]

38 Tax Year 2011

39 FSA & HSA Flexible Spending Account Limited to prescription drugs Health Savings Account Penalty on nonqualified HSA distributions 10% to 20%

40 Medical Expense Deduction For clients less than age 65, the threshold for deduction of qualified medical expenses on form 1040, Schedule A is raised to 10% of federal AGI

41 Medical Loss Ratio Beginning in 2011, insurance companies are required to spend a specified percentage of policyholders premiums on medical care and quality improvement activities, meeting a medical los ratio (MLR) standard. Insurance companies that do not meet the MLR standard are required to provide rebates to their individual policyholders and premium reductions to their group policyholders in July, 2012.

42 Tax Year 2012

43 W-2 Employees who issued more than 250 forms for 2011 must report their employee health insurance premium costs in box 12 using code DD YOU ARE NOT TAXED ON THIS AMOUNT. This is for informational purpose only for NOW

44 Open Enrollment Health insurers must provide employees with a uniform Summary of Benefits and coverage during their open enrollment

45 Tax Year 2013

46 Investment Tax A new tax of 3.8% applies to net investment income for clients with modified AGI in excess of $200,000. Net investment income includes interest, dividends, and capital gains. This only applies to taxable gain.

47 Medicare Tax The Medicare tax increases by.9% to 2.35% on earned income exceeding $200,000, the tax remains at 1.45% on earned income below these thresholds

48 FSA & HSA Flexible Spending Account Maximum contribution $2500 Health Savings Account Maximum contribution $2500

49 Tax Year 2014

50 Health Insurance Plans Plans must provide coverage for certain types of preventive care Plans may no longer include an annual or lifetime maximum cap on paid expenses Clients may continue to cover adult children under age 27 Clients who have Medicare prescription drug coverage (Medicare Part D) received a $250 rebate in 2010.

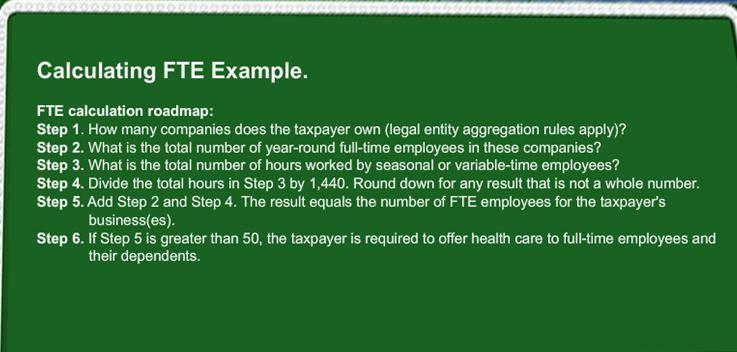

51 Individual Requirement Beginning in January 2014, the health care law requires U.S. citizens and lawful residents to be covered by minimum essential health insurance for themselves and their dependents or pay a penalty tax

52 Exceptions to Requirement Coverage may be obtained through: An employer A government-sponsored health plan, such as Medicaid/Medicare A state-based health insurance exchange Private health insurance purchased in the open market

53 Individual Requirement Qualified employer coverage must meet 3 key standards: Minimum essential coverage -That standard has not yet been defined Affordable - Premiums may not exceed 9.5% of wages Adequate -The plan must pay for a minimum of 60% of covered medical expenses

54 Government Plans Qualified sponsored health plans: Medicaid and expanded Medicaid Medicare Children s Health Insurance Program (CHIP) TRICARE and TRICARE for life Veterans Affairs healthcare program Health care plan for members of the Peace Corps

55 Health Insurance Exchange Cannot be denied for pre-existing condition Four benefit levels: Bronze 60% payment Silver 70% payment Gold 80% payment Platinum 90% payment Annual out-of-pocket payment $5,950 Individual; $11,900 family

56 Tax Penalty For 2014 the larger of either: 1% of household income $95 /$47.50/$285 For 2015: 2% of household income $325 /$162.50/$975 max For % of household income $695 / $347.50/ $2,085 max

57 Exemptions to penalty Income below the filing requirement Less than three months of noncoverage *Determination of coverage is made month-tomonth on the last day of each month.

58 FTE Employers with 50 or more FTE employees must offer insurance Determining FTE: Safe harbor Number of employees with a minimum of 120 hours in the month

59

60 Example 1 ABC Industries LLC has 80 FTE employees and is thus required to offer health insurance coverage to its 31 full-time employees. The business leadership decides to pay the penalty rather than offer coverage. Because the penalty only applies to the number of full-time employees over 30, their penalty is $2,000. ($2,000 X 1 Fulltime employee = $2,000)

61 Example 2 XYZ Distribution LLP has 100 FTE employees and is required to offer health insurance coverage to its 35 full-time employees. However, the coverage the company offers does not meet the key standards and XYZ must pay a penalty as a result. To calculate the fine, you need to know how many of the full-time employees purchased coverage through the exchange and received premium assistance. Assuming that 10 did so (the rest may have coverage through the employer s plan even though it doesn t meet the standards, a spouses plan, purchased through the exchange but did not receive premium assistance, or opted to go without coverage) the penalty is $30,000 ($3,000 X 10 Employees who purchased insurance = $30,000) However, the penalty may not exceed $10,000. ($2,000 X 5 full-time employees over 30 threshold = $10,000)

Expiring Tax Provisions

Expiring Tax Provisions The term Bush-era tax cuts or Bush tax cuts is often used to describe the tax related reductions that were contained in legislation enacted by Congress in 2001 and 2003, the Economic

Expiring Tax Provisions The term Bush-era tax cuts or Bush tax cuts is often used to describe the tax related reductions that were contained in legislation enacted by Congress in 2001 and 2003, the Economic

Middle Class Tax Relief Act of 2012

Middle Class Tax Relief Act of 2012 Two major bills enacting tax cuts for individuals expire at the end of 2010: the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA); and the Jobs and

Middle Class Tax Relief Act of 2012 Two major bills enacting tax cuts for individuals expire at the end of 2010: the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA); and the Jobs and

An Overview of the Tax Provisions in the American Taxpayer Relief Act of 2012

An Overview of the Tax Provisions in the American Taxpayer Relief Act of 2012 Margot L. Crandall-Hollick Analyst in Public Finance January 10, 2013 CRS Report for Congress Prepared for Members and Committees

An Overview of the Tax Provisions in the American Taxpayer Relief Act of 2012 Margot L. Crandall-Hollick Analyst in Public Finance January 10, 2013 CRS Report for Congress Prepared for Members and Committees

The Patient Protection and Affordable Care Act

Patient Protection and Affordable Care Act-Tax Implications and Expiring Tax Provisions in 2014 Arkansas Chapter HFMA October 31, 2014 Presented by John Ed Welch, Partner, CPA The Patient Protection and

Patient Protection and Affordable Care Act-Tax Implications and Expiring Tax Provisions in 2014 Arkansas Chapter HFMA October 31, 2014 Presented by John Ed Welch, Partner, CPA The Patient Protection and

Re: 2012 American Taxpayer Relief Act (ATRA)

") 50 W Mashta Drive, Suite 6 Key Biscayne, FL 33149 Tel: (305) 361-1014 Fax: (305) 361-7078 www.lancaster-cpas.com JANUARY 2nd, 2013 Re: 2012 American Taxpayer Relief Act (ATRA) Dear Friends, After much

50 W Mashta Drive, Suite 6 Key Biscayne, FL 33149 Tel: (305) 361-1014 Fax: (305) 361-7078 www.lancaster-cpas.com JANUARY 2nd, 2013 Re: 2012 American Taxpayer Relief Act (ATRA) Dear Friends, After much

Tax Changes for 2016: A Checklist

Tax Changes for 2016: A Checklist Welcome, 2016! As the New Year rolls around, it's always a sure bet that there will be changes to current tax law and 2016 is no different. From health savings accounts

Tax Changes for 2016: A Checklist Welcome, 2016! As the New Year rolls around, it's always a sure bet that there will be changes to current tax law and 2016 is no different. From health savings accounts

American Taxpayer Relief Act of 2012 Workshop

American Taxpayer Relief Act of 2012 Workshop John Kilroy, CPA, CFP May 14, 2013 Agenda Estate, Gift and GST provisions Individual Income Tax provisions Trust and Estate Income Tax provisions Business

American Taxpayer Relief Act of 2012 Workshop John Kilroy, CPA, CFP May 14, 2013 Agenda Estate, Gift and GST provisions Individual Income Tax provisions Trust and Estate Income Tax provisions Business

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now Rich Shavell, CPA, CVA, CCIFP Shavell & Company, P.A. info@shavell.net www.shavell.net 1 THE DISCLAIMER Information provided herein

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now Rich Shavell, CPA, CVA, CCIFP Shavell & Company, P.A. info@shavell.net www.shavell.net 1 THE DISCLAIMER Information provided herein

Brackets (seven) - Taxable Income Single Filers. Between $9,525 and $38,700. Between $2,550 and $9,150. Between $157,500 and $200,000

- Taxable Income Single Filers. Between $9,525 and $38,700. Between $2,550 and $9,150. Between $157,500 and $200,000") Individual Taxes (Which Would Expire After 2025) Brackets (seven) - Taxable Income Single Filers Up to $9,525 Between $9,525 and $38,700 Between $38,700 and $82,500 Between $200,000 and $500,000 Above

Individual Taxes (Which Would Expire After 2025) Brackets (seven) - Taxable Income Single Filers Up to $9,525 Between $9,525 and $38,700 Between $38,700 and $82,500 Between $200,000 and $500,000 Above

Client Newsletter. 551 West 78th Street, Ste. 204, P.O. Box 254 Chanhassen, MN Office: Fax:

Client Newsletter 2015 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: RODENZ ACCOUNTING & TAX SERVICE LLC Accounting Business Consulting Tax Preparation Payroll Services Darrell E. Rodenz Certified Public Accountant

Client Newsletter 2015 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: RODENZ ACCOUNTING & TAX SERVICE LLC Accounting Business Consulting Tax Preparation Payroll Services Darrell E. Rodenz Certified Public Accountant

Re: 2012 Year-End Tax Planning for Individuals

Re: 2012 Year-End Tax Planning for Individuals To Our Valued Clients and Friends: Year-end tax planning is always complicated by the uncertainty that the following year may bring and 2012 is no exception.

Re: 2012 Year-End Tax Planning for Individuals To Our Valued Clients and Friends: Year-end tax planning is always complicated by the uncertainty that the following year may bring and 2012 is no exception.

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

American Taxpayer Relief Act of 2012 Changes Effective in New Law Before Law Change Date Page 1 Alternative Minimum Tax (AMT) Individuals AMT

Individuals AMT") American Taxpayer Relief Act of 202 Changes Effective in 202 Effective QF New Law Before Law Change Date Page Alternative Minimum Tax (AMT) Individuals AMT 2-3 For 202, the AMT exemption amounts are: $50,600

American Taxpayer Relief Act of 202 Changes Effective in 202 Effective QF New Law Before Law Change Date Page Alternative Minimum Tax (AMT) Individuals AMT 2-3 For 202, the AMT exemption amounts are: $50,600

(married filing jointly) indexed for inflation in future years.

indexed for inflation in future years.") 2 AMERICAN TAXPAYER RELIEF ACT OF 2012 excess of the applicable threshold. These thresholds will be indexed for inflation in future years. Because the tax rates are permanent, for 2013 you can employ the

2 AMERICAN TAXPAYER RELIEF ACT OF 2012 excess of the applicable threshold. These thresholds will be indexed for inflation in future years. Because the tax rates are permanent, for 2013 you can employ the

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS Following are income tax items that could affect your return for 2014. Please review and make sure you have alerted your tax consultant for all of

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS Following are income tax items that could affect your return for 2014. Please review and make sure you have alerted your tax consultant for all of

Year-End Tax Tips for Individuals

Year-End Tax Tips for Individuals New tax legislation has brought greater certainty to year-end planning, but also created new challenges. There is still time to set up an appointment for year-end planning.

Year-End Tax Tips for Individuals New tax legislation has brought greater certainty to year-end planning, but also created new challenges. There is still time to set up an appointment for year-end planning.

2009 Economic Stimulus Act

2009 Economic Stimulus Act On February 17, President Obama signed into law the American Recovery and Reinvestment Act of 2009 (the 2009 Economic Stimulus Act). This new legislation was passed to aid our

2009 Economic Stimulus Act On February 17, President Obama signed into law the American Recovery and Reinvestment Act of 2009 (the 2009 Economic Stimulus Act). This new legislation was passed to aid our

What the New Tax Laws Mean to You

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

2016 Year-End Tax Planning Letter

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

Barn Report. A Dairy Keeper Resource

Barn Report. A Dairy Keeper Resource January 20, 2012 Report 12.017 A Laundry List of 2011 Tax Law Changes This page was last updated January 10, 2011. Please check back regularly as the tax laws will

Barn Report. A Dairy Keeper Resource January 20, 2012 Report 12.017 A Laundry List of 2011 Tax Law Changes This page was last updated January 10, 2011. Please check back regularly as the tax laws will

Year End Tax Planning for Individuals

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Individual Taxation and Planning

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

Summary of Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010

Summary of Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 Cross References HR 4853 Update Overview The President signed into law the Tax Relief, Unemployment Insurance,

Summary of Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 Cross References HR 4853 Update Overview The President signed into law the Tax Relief, Unemployment Insurance,

2017 Income Tax Developments

2017 Income Tax Developments Presented To: Delaware Tax Institute Presented by: Karly A. Laughlin, CPA Manager Tax & Small Business www.belfint.com Researched & Compiled by: Michael D. Kelly, CPA 302.573.3955

2017 Income Tax Developments Presented To: Delaware Tax Institute Presented by: Karly A. Laughlin, CPA Manager Tax & Small Business www.belfint.com Researched & Compiled by: Michael D. Kelly, CPA 302.573.3955

HOUSE TAX REFORM PROPOSAL INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Tax Cuts and Jobs Act bill, as approved by the House Ways and Means Committee on November 9, 2017. This chart highlights

The following chart sets forth some of the provisions affecting individuals in the Tax Cuts and Jobs Act bill, as approved by the House Ways and Means Committee on November 9, 2017. This chart highlights

FASB Looks to. Leslie F. Seidman, FASB Chair. Annual Tax Update Marriage and Taxes Estate Tax Portability Tax Preferences for Education

www.cpaj.com December 2011 FASB Looks to the Future Leslie F. Seidman, FASB Chair Annual Tax Update Marriage and Taxes Estate Tax Portability Tax Preferences for Education T A X A T I O N federal taxation

www.cpaj.com December 2011 FASB Looks to the Future Leslie F. Seidman, FASB Chair Annual Tax Update Marriage and Taxes Estate Tax Portability Tax Preferences for Education T A X A T I O N federal taxation

Individual Provisions Under the Tax Cuts and Jobs Act Compared to Previous Tax Law

Reduction & Simplification of Individual Income Tax Rates Individual rates on ordinary income (1) Seven brackets with top rate of 39.6 percent # Seven brackets with top rate of 37 percent #^ Unearned income

Reduction & Simplification of Individual Income Tax Rates Individual rates on ordinary income (1) Seven brackets with top rate of 39.6 percent # Seven brackets with top rate of 37 percent #^ Unearned income

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM:

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: A publication of the Minnesota Association of Public Accountants The Minnesota Association of Public Accountants has prepared this newsletter.

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: A publication of the Minnesota Association of Public Accountants The Minnesota Association of Public Accountants has prepared this newsletter.

TAX CUTS AND JOBS ACT (H.R. 1), 2018 A CLOSER LOOK PREPARED BY: ADIL A. BALOCH, CPA; CTRS. Accurate Records and Tax Services, Inc.

, 2018 A CLOSER LOOK PREPARED BY: ADIL A. BALOCH, CPA; CTRS. Accurate Records and Tax Services, Inc.") TAX CUTS AND JOBS ACT (H.R. 1), 2018 A CLOSER LOOK PREPARED BY: ADIL A. BALOCH, CPA; CTRS Accurate Records and Tax Services, Inc. 18562 Office Park Dr. Montgomery Village, MD 20886 (301) 519-1445 info@aabcpa.com

TAX CUTS AND JOBS ACT (H.R. 1), 2018 A CLOSER LOOK PREPARED BY: ADIL A. BALOCH, CPA; CTRS Accurate Records and Tax Services, Inc. 18562 Office Park Dr. Montgomery Village, MD 20886 (301) 519-1445 info@aabcpa.com

Tax Cuts and Jobs Act. Durham Chamber of Commerce Public Policy Meeting January 9, 2018

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

2018 Year-End Tax Planning for Individuals

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

2018 tax planning guide

Advanced Planning 2018 tax planning guide We are committed to helping you confirm that your current and future tax strategy supports your larger financial goals. Advice. Beyond investing. Your financial

Advanced Planning 2018 tax planning guide We are committed to helping you confirm that your current and future tax strategy supports your larger financial goals. Advice. Beyond investing. Your financial

Congress Passes Fiscal Cliff Act

Congress Passes Fiscal Cliff Act Pulling back from the fiscal cliff at the 13th hour, Congress preserved most of the George W. Bush-era tax cuts and extended many other lapsed tax provisions. The Senate

Congress Passes Fiscal Cliff Act Pulling back from the fiscal cliff at the 13th hour, Congress preserved most of the George W. Bush-era tax cuts and extended many other lapsed tax provisions. The Senate

2014 AFFORDABLE CARE ACT (OBAMA CARE)

") 2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

Prepared by the Staff of the JOINT COMMITTEE ON TAXATION. December 10, 2010 JCX-55-10

TECHNICAL EXPLANATION OF THE REVENUE PROVISIONS CONTAINED IN THE TAX RELIEF, UNEMPLOYMENT INSURANCE REAUTHORIZATION, AND JOB CREATION ACT OF 2010 SCHEDULED FOR CONSIDERATION BY THE UNITED STATES SENATE

TECHNICAL EXPLANATION OF THE REVENUE PROVISIONS CONTAINED IN THE TAX RELIEF, UNEMPLOYMENT INSURANCE REAUTHORIZATION, AND JOB CREATION ACT OF 2010 SCHEDULED FOR CONSIDERATION BY THE UNITED STATES SENATE

2013 TAX AND FINANCIAL PLANNING TABLES. An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning.

2013 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning. WHAT YOU WILL SEE IN THIS BROCHURE 2013 Income Tax Changes Tax Rates

2013 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning. WHAT YOU WILL SEE IN THIS BROCHURE 2013 Income Tax Changes Tax Rates

American Recovery and Reinvestment Act of 2009 (Enacted February 17, 2009)

") Individuals Tax Credits American Opportunity Tax Credit (formerly the Hope Credit) 2009 & 2010 The Hope education credit is renamed the American Opportunity Tax credit and modified by: Increasing the credit

Individuals Tax Credits American Opportunity Tax Credit (formerly the Hope Credit) 2009 & 2010 The Hope education credit is renamed the American Opportunity Tax credit and modified by: Increasing the credit

Provisions of Tax Cuts and Jobs Act

Provisions of Tax Cuts and Jobs Act i Contents Introduction to the Course... 1 Course Learning Objectives... 1 Domain 1 Provisions of Tax Cuts and Jobs Act... 2 Introduction... 2 Domain 1 Learning Objectives...

Provisions of Tax Cuts and Jobs Act i Contents Introduction to the Course... 1 Course Learning Objectives... 1 Domain 1 Provisions of Tax Cuts and Jobs Act... 2 Introduction... 2 Domain 1 Learning Objectives...

Bollenbacher and Associates Certified Public Accountants Taxpayer Relief Act

Bollenbacher and Associates Certified Public Accountants 2012 Taxpayer Relief Act Highlights of the 2012 Taxpayer Relief Act (1) the elimination of EGTRRA sunsetting (Bush Tax Cuts), (2) tax rate increases

Bollenbacher and Associates Certified Public Accountants 2012 Taxpayer Relief Act Highlights of the 2012 Taxpayer Relief Act (1) the elimination of EGTRRA sunsetting (Bush Tax Cuts), (2) tax rate increases

Davis & associates, p.a. Certified Public Accountants and Consultants

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

209 FEDERAL TAX RATES Davis & Associates, p.a. Certified Public Accountants and Consultants 97 Washingtonian Boulevard, Suite 550 Gaithersburg, Maryland 20878 Phone: 30.963.6696 Fax: 30.963.6693 www.daviscpas.com

2017 vs Key Facts and Figures

2017 vs. 2018 Key Facts and Figures Note: We highlighted the information that changed between 2017 and 2018 with a box. * 2018 numbers are based on the Tax Cuts and Jobs Act (TCJA) of 2017. (Note: the

2017 vs. 2018 Key Facts and Figures Note: We highlighted the information that changed between 2017 and 2018 with a box. * 2018 numbers are based on the Tax Cuts and Jobs Act (TCJA) of 2017. (Note: the

HEALTHCARE TAX UPDATE SEPTEMBER 28, 2012

HEALTHCARE TAX UPDATE SEPTEMBER 28, 2012 1 AGENDA 1. Expiring individual income tax cuts? 2012 Election. 2. Tax provisions of the Affordable Care Act. 3. Schedule H State of New Jersey hospitals and American

HEALTHCARE TAX UPDATE SEPTEMBER 28, 2012 1 AGENDA 1. Expiring individual income tax cuts? 2012 Election. 2. Tax provisions of the Affordable Care Act. 3. Schedule H State of New Jersey hospitals and American

Tax Law Changes 2018

Tax Law Changes 2018 Standard Deduction Standard deduction increased to $24,000 MFJ and QW $18,000 HoH $12,000 Single and MFS Pub 4012 Tab F-1 Additional standard deduction amount for age 65 and older

Tax Law Changes 2018 Standard Deduction Standard deduction increased to $24,000 MFJ and QW $18,000 HoH $12,000 Single and MFS Pub 4012 Tab F-1 Additional standard deduction amount for age 65 and older

Presented by: Timothy A. George, CPA, MST, CCIFP

Tax Implications of Obamacare Presented by: Timothy A. George, CPA, MST, CCIFP 2 Players Club Drive, Suite 100, Charleston, West Virginia 25311 Office: (304) 343-4188 Fax: (304) 344-5035 20 Plus New Taxes

Tax Implications of Obamacare Presented by: Timothy A. George, CPA, MST, CCIFP 2 Players Club Drive, Suite 100, Charleston, West Virginia 25311 Office: (304) 343-4188 Fax: (304) 344-5035 20 Plus New Taxes

TAX UPDATE TAX CUTS & JOBS ACT (2018) Add l Elderly & Blind Joint & Surviving Spouse: $1,300

Add l Elderly & Blind Joint & Surviving Spouse: $1,300") TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

Tax Cuts and Jobs Act (TCJA)

") Tax Cuts and Jobs Act (TCJA) Presented by: Rachel Pappy Partner, Attorney Outline Repeal of personal exemptions Increase of standard deduction Repeal of pease limitations Limitation of state and local

Tax Cuts and Jobs Act (TCJA) Presented by: Rachel Pappy Partner, Attorney Outline Repeal of personal exemptions Increase of standard deduction Repeal of pease limitations Limitation of state and local

HEALTH CONCEPTS AND TAX CONSIDERATIONS

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

14 HEALTH CONCEPTS AND TAX CONSIDERATIONS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Recognize the features of health insurance policies that have been mandated by

HEALTH CARE REFORM UPDATE

HEALTH CARE REFORM UPDATE The Health Care Reform Train Don t Be Left Standing at the Station Hope is Not an Effective Planning Solution TUESDAY NOVEMBER 13, 2012 Todd Tigges, Principal, UHY LLP Gregory

HEALTH CARE REFORM UPDATE The Health Care Reform Train Don t Be Left Standing at the Station Hope is Not an Effective Planning Solution TUESDAY NOVEMBER 13, 2012 Todd Tigges, Principal, UHY LLP Gregory

Individual Income Tax Planning

18401 Murdock Circle Suite B Port Charlotte, FL 33948 941-627-4774 linda.cross@raymondjames.com www.raymondjames.com/sommervillegroup 2012 Key Numbers June 2012 Individual Income Tax Planning Adoption

18401 Murdock Circle Suite B Port Charlotte, FL 33948 941-627-4774 linda.cross@raymondjames.com www.raymondjames.com/sommervillegroup 2012 Key Numbers June 2012 Individual Income Tax Planning Adoption

Selected Tax Issues Under Patient Protection and Affordable Care Act (PPACA)

") Selected Tax Issues Under Patient Protection and Affordable Care Act (PPACA) J. Clark Pendergrass Lanier Ford Shaver & Payne P.C. 2101 West Clinton Ave., Suite 102 Huntsville, AL 35805 256-535-1100 jcp@lanierford.com

Selected Tax Issues Under Patient Protection and Affordable Care Act (PPACA) J. Clark Pendergrass Lanier Ford Shaver & Payne P.C. 2101 West Clinton Ave., Suite 102 Huntsville, AL 35805 256-535-1100 jcp@lanierford.com

Individual Taxes. TAX CUTS & JOBS ACT OF Tax Brackets: 7 Tax Brackets: 7 Tax Brackets: 4 Tax Brackets:

COMPARISON OF CURRENT TAX LAW VS. TAX CUTS AND JOBS ACT Individual Taxes Ordinary Income Tax Brackets (Single Tax Brackets Shown) 10%: $0 - $9,325 15%: $9,326 - $37,950 25%: $37,951 - $91,900 28%: $91,901

COMPARISON OF CURRENT TAX LAW VS. TAX CUTS AND JOBS ACT Individual Taxes Ordinary Income Tax Brackets (Single Tax Brackets Shown) 10%: $0 - $9,325 15%: $9,326 - $37,950 25%: $37,951 - $91,900 28%: $91,901

TAX CUTS AND JOBS ACT OF 2017

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Income, Gift, and Estate Tax Update Philip E. Harris 1 and Linda E. Curry 2

Income, Gift, and Estate Tax Update Philip E. Harris 1 and Linda E. Curry 2 Table of Contents I. Income Tax Rates... 1 A. Regular Income Tax... 1 1. Marriage Penalty Relief... 1 2. Long-Term Capital Gains...

Income, Gift, and Estate Tax Update Philip E. Harris 1 and Linda E. Curry 2 Table of Contents I. Income Tax Rates... 1 A. Regular Income Tax... 1 1. Marriage Penalty Relief... 1 2. Long-Term Capital Gains...

What Are We Covering Today?

Individual & Business Tax Planning Update November 9, 2011 HMWC CPAs & Business Advisors What Are We Covering Today? 2011 Legislation Update Individuals Business Tax Planning Strategies Individuals Business

Individual & Business Tax Planning Update November 9, 2011 HMWC CPAs & Business Advisors What Are We Covering Today? 2011 Legislation Update Individuals Business Tax Planning Strategies Individuals Business

Arthur Lander C.P.A., P.C. A professional corporation

A Arthur Lander C.P.A., P.C. A professional corporation 300 N. Washington St. #104 Alexandria, Virginia 22314 phone: (703) 486-0700 fax: (703) 527-7207 YEAR-END TAX PLANNING FOR INDIVIDUALS Once again,

A Arthur Lander C.P.A., P.C. A professional corporation 300 N. Washington St. #104 Alexandria, Virginia 22314 phone: (703) 486-0700 fax: (703) 527-7207 YEAR-END TAX PLANNING FOR INDIVIDUALS Once again,

N/A. Kiddie Tax Various bracket thresholds Ordinary and capital gains rates applicable to trusts and estates

We have prepared a summary of the House and the Senate versions of the proposed tax reform bill. Once they reach an agreement on a final bill, we will update the summary as needed. House Bill (H. R. 1)

We have prepared a summary of the House and the Senate versions of the proposed tax reform bill. Once they reach an agreement on a final bill, we will update the summary as needed. House Bill (H. R. 1)

Tax Inflation Numbers 2018 & 2019

Tax Inflation Numbers 2018 & 2019 Standard Deduction Filing Status Single 12,000 12,200 MFJ/QW 24,000 24,400 HOH 18,000 18,350 MFS 12,000 12,200 Additional Standard Deduction (Age 65 or older or Blind)

Tax Inflation Numbers 2018 & 2019 Standard Deduction Filing Status Single 12,000 12,200 MFJ/QW 24,000 24,400 HOH 18,000 18,350 MFS 12,000 12,200 Additional Standard Deduction (Age 65 or older or Blind)

Federal Income Tax Changes 2018

Federal Income Tax Changes 2018 i Copyright 2018 by 1040 Education LLC ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT

Federal Income Tax Changes 2018 i Copyright 2018 by 1040 Education LLC ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT

The Affordable Care Act Update

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview of Presentation 1. 2010 2014 Provisions overview

The Affordable Care Act Update Presented by: The Union Labor Life Insurance Company SOLUTIONS FOR THE UNION WORKPLACE SPECIALTY INSURANCE INVESTMENTS Overview of Presentation 1. 2010 2014 Provisions overview

TAX CUT AND JOBS ACT OF INDIVIDUAL PROPOSALS

Reduction of rates Married Filing Joint () (Surviving Spouse) $0 90,000 $91,000 260,000 $260,001 1,000,000 Over $1,000,000 $0 45,000 $45,001 130,000 $130,001 500,000 Over $500,000 Head of Household ()

Reduction of rates Married Filing Joint () (Surviving Spouse) $0 90,000 $91,000 260,000 $260,001 1,000,000 Over $1,000,000 $0 45,000 $45,001 130,000 $130,001 500,000 Over $500,000 Head of Household ()

2017 Year-End Tax Planning for Individuals

2017 Year-End Tax Planning for Individuals As 2017 draws to a close, there is still time to reduce your 2017 tax bill and plan ahead for 2018. This letter highlights several potential tax-saving opportunities

2017 Year-End Tax Planning for Individuals As 2017 draws to a close, there is still time to reduce your 2017 tax bill and plan ahead for 2018. This letter highlights several potential tax-saving opportunities

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017 SUMMARY FOR 2017 NEW TAX LAW Publication Date: March 2017 Field of Studies: Level: Taxes Basic Cpe Hours: 3 Prerequisites: Advanced Preparation: None None Type

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017 SUMMARY FOR 2017 NEW TAX LAW Publication Date: March 2017 Field of Studies: Level: Taxes Basic Cpe Hours: 3 Prerequisites: Advanced Preparation: None None Type

Integrity Accounting

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Key Numbers 2017 Presented by Nancy LaPointe

Key Numbers 2017 Presented by Nancy LaPointe Individual Income Tax Unmarried Individuals (other than Surviving Spouses and Heads of Household) $9,325 or less 10% of taxable income Over $9,325 to $37,950

Key Numbers 2017 Presented by Nancy LaPointe Individual Income Tax Unmarried Individuals (other than Surviving Spouses and Heads of Household) $9,325 or less 10% of taxable income Over $9,325 to $37,950

THE AFFORDABLE CARE ACT...2

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

Table of Contents THE AFFORDABLE CARE ACT...2 Health Insurance Marketplace (Exchange)...3 Metallic Levels...4 Catastrophic Plans...4 Individual Mandate...5 Subsidies...5 Open Enrollment Period...6 Special

President Obama signed a multi-billion

2010 TAX RELIEF/JOB CREATION ACT December 21, 2010 HIGHLIGHTS Reduced Individual Tax Rates Reduced Capital Gains/ Dividend Tax Rates $1,000 Child Tax Credit AOTC And Other Education Incentives Two-Year

2010 TAX RELIEF/JOB CREATION ACT December 21, 2010 HIGHLIGHTS Reduced Individual Tax Rates Reduced Capital Gains/ Dividend Tax Rates $1,000 Child Tax Credit AOTC And Other Education Incentives Two-Year

SK Wealth Management, LLC November 18, 2014

SK Wealth Management, LLC Jason Archambault, CFP, CPA/PFS Managing Member 55 Dorrance Street Providence, RI 02903 401-331-1575 jarchambault@skwealth.com http://skwealth.com 2015 Key Numbers SKWealth clients

SK Wealth Management, LLC Jason Archambault, CFP, CPA/PFS Managing Member 55 Dorrance Street Providence, RI 02903 401-331-1575 jarchambault@skwealth.com http://skwealth.com 2015 Key Numbers SKWealth clients

Senator Kerry s Tax Proposals. Leonard E. Burman and Jeffrey Rohaly 1 Revised July 23, 2004

Senator Kerry s Tax Proposals Leonard E. Burman and Jeffrey Rohaly 1 Revised July 23, 2004 This note provides a very preliminary summary and distributional analysis of Senator Kerry s tax proposals. Some

Senator Kerry s Tax Proposals Leonard E. Burman and Jeffrey Rohaly 1 Revised July 23, 2004 This note provides a very preliminary summary and distributional analysis of Senator Kerry s tax proposals. Some

How Compliant is Your Organization? PPACA Updates and Our New Normal.

Broader Perspective. Business Solutions. How Compliant is Your Organization? PPACA Updates and Our New Normal. Presented by: Jacqueline Roth Assistant Vice President March 20, 2013 1 A Brief History The

Broader Perspective. Business Solutions. How Compliant is Your Organization? PPACA Updates and Our New Normal. Presented by: Jacqueline Roth Assistant Vice President March 20, 2013 1 A Brief History The

e4 Brokerage, LLC th St. South Suite C Fargo, ND

e4 Brokerage, LLC 2280 45th St. South Suite C Fargo, ND 58104 701-356-1270 866-356-3203 sbergee@e4brokerage.com www.e4brokerage.com 2017 Tax Facts Guide 1/01/2017 Page 1 of 28, see disclaimer on final

e4 Brokerage, LLC 2280 45th St. South Suite C Fargo, ND 58104 701-356-1270 866-356-3203 sbergee@e4brokerage.com www.e4brokerage.com 2017 Tax Facts Guide 1/01/2017 Page 1 of 28, see disclaimer on final

Tax Season Reference Guide. Tool for preparing 2017 tax returns

Tax Season Reference Guide Tool for preparing tax returns Quick Reference Guide A tool for preparing returns At the close of every year, NATP s Tax Knowledge Center pulls together a list of common facts

Tax Season Reference Guide Tool for preparing tax returns Quick Reference Guide A tool for preparing returns At the close of every year, NATP s Tax Knowledge Center pulls together a list of common facts

Tax Law Snapshot for Individuals 2014 Filing Season

Tax Law Snapshot for Individuals 2014 Filing Season (480) 776-3358 1237 S. Val Vista Dr. Suite 206 Mesa, AZ 85204-6401 (480) 323-2474 fax kboudreau@bcsbs.net Taxes Contract Financial Management Financial

Tax Law Snapshot for Individuals 2014 Filing Season (480) 776-3358 1237 S. Val Vista Dr. Suite 206 Mesa, AZ 85204-6401 (480) 323-2474 fax kboudreau@bcsbs.net Taxes Contract Financial Management Financial

Tax Inflation Numbers 2017 & 2018

Tax Inflation Numbers 2017 & 2018 Standard Deduction Filing Status Single 6,350 12,000 MFJ/QW 12,700 24,000 HOH 9,350 18,000 MFS 6,350 12,000 Additional Standard Deduction (Age 65 or older or Blind) Filing

Tax Inflation Numbers 2017 & 2018 Standard Deduction Filing Status Single 6,350 12,000 MFJ/QW 12,700 24,000 HOH 9,350 18,000 MFS 6,350 12,000 Additional Standard Deduction (Age 65 or older or Blind) Filing

2011 Tax Guide. What You Need to Know About the New Rules

2011 Tax Guide What You Need to Know About the New Rules Tax Guide 2011 This guide is not intended to be tax advice and should not be treated as such. Each individual s tax situation is different. You

2011 Tax Guide What You Need to Know About the New Rules Tax Guide 2011 This guide is not intended to be tax advice and should not be treated as such. Each individual s tax situation is different. You

HASHEM and SIMMS, PLLC CERTIFIED PUBLIC ACCOUNTANTS

HASHEM and SIMMS, PLLC CERTIFIED PUBLIC ACCOUNTANTS George K. Hashem, CPA Tyler W. Simms, CPA December 2, 2015 Dear Client: As 2015 draws to a close, there is still time to reduce your 2015 tax bill and

HASHEM and SIMMS, PLLC CERTIFIED PUBLIC ACCOUNTANTS George K. Hashem, CPA Tyler W. Simms, CPA December 2, 2015 Dear Client: As 2015 draws to a close, there is still time to reduce your 2015 tax bill and

Your Comprehensive Guide to 2013 Year-End Tax Planning

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014

provisions effective January 1, 2014") The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

The New Health Care Landscape Today s Agenda Health Care Reform under the Patient Protection and Affordable Care Act ( PPACA ) provisions effective January 1, 2014 Exchanges and Qualified Health Plans

2015 PATH Act: What all Taxpayers Need to Know

2015 PATH Act: What all Taxpayers Need to Know AUTHORS Loree Dubois, CPA Laura H. Yalanis, CPA,MST Loree is the Chair of the Firm s Corporate Tax Group and Co-Chair of the Firms Healthcare Services Group.

2015 PATH Act: What all Taxpayers Need to Know AUTHORS Loree Dubois, CPA Laura H. Yalanis, CPA,MST Loree is the Chair of the Firm s Corporate Tax Group and Co-Chair of the Firms Healthcare Services Group.

American Health Care Act (House-Passed Bill)

") This chart compares the to provisions of both the House-passed and the Senate Discussion Draft, called the. This chart is current as of June 26, 2017. Individual shared responsibility penalty for not having

This chart compares the to provisions of both the House-passed and the Senate Discussion Draft, called the. This chart is current as of June 26, 2017. Individual shared responsibility penalty for not having

LAST CHANCE TO REDUCE 2018 INCOME TAXES

LAST CHANCE TO REDUCE 2018 INCOME TAXES Presented by: James J. Holtzman, CFP Wealth Advisor and Shareholder with Legend Financial Advisors, Inc. JAMES J. HOLTZMAN, CFP James J. Holtzman, CFP, is a Wealth

LAST CHANCE TO REDUCE 2018 INCOME TAXES Presented by: James J. Holtzman, CFP Wealth Advisor and Shareholder with Legend Financial Advisors, Inc. JAMES J. HOLTZMAN, CFP James J. Holtzman, CFP, is a Wealth

November 6, Comprehensive Tax Reform Proposal Released HR1 Tax Cuts and Jobs Bill, November 2,

November 6, 2017 Comprehensive Tax Reform Proposal Released... 2 HR1 Tax Cuts and Jobs Bill, November 2, 2017... 2 2017 Loscalzo Institute, a Kaplan Company Current Federal Tax Developments 2 Comprehensive

November 6, 2017 Comprehensive Tax Reform Proposal Released... 2 HR1 Tax Cuts and Jobs Bill, November 2, 2017... 2 2017 Loscalzo Institute, a Kaplan Company Current Federal Tax Developments 2 Comprehensive

Congress has approved, and President

TAX RELIEF/JOB CREATION ACT Of 2010 December 16, 2010 HIGHLIGHTS Reduced Individual Tax Rates Reduced Capital Gains/ Dividend Tax Rates $1,000 Child Tax Credit AOTC And Other Education Incentives Two-Year

TAX RELIEF/JOB CREATION ACT Of 2010 December 16, 2010 HIGHLIGHTS Reduced Individual Tax Rates Reduced Capital Gains/ Dividend Tax Rates $1,000 Child Tax Credit AOTC And Other Education Incentives Two-Year

SENATE TAX REFORM PROPOSAL INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only

The following chart sets forth some of the provisions affecting individuals in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only

WHAT TAX REFORM MEANS FOR SMALL BUSINESSES & PASS-THROUGH ENTITIES. Julie Peters, Attorney Polston Tax Resolution & Accounting

WHAT TAX REFORM MEANS FOR SMALL BUSINESSES & PASS-THROUGH ENTITIES Julie Peters, Attorney Polston Tax Resolution & Accounting TAX CUT AND JOBS ACT The new tax law, called the Tax Cut and Jobs Act (TCJA),

WHAT TAX REFORM MEANS FOR SMALL BUSINESSES & PASS-THROUGH ENTITIES Julie Peters, Attorney Polston Tax Resolution & Accounting TAX CUT AND JOBS ACT The new tax law, called the Tax Cut and Jobs Act (TCJA),

2016 Federal Income Tax Planning

Weller Group LLC Timothy Weller, CFP CERTIFIED FINANCIAL PLANNER 6206 Slocum Road Ontario, NY 14519 315-524-8000 tim@wellergroupllc.com www.wellergroupllc.com 2016 Federal Income Tax Planning March 06,

Weller Group LLC Timothy Weller, CFP CERTIFIED FINANCIAL PLANNER 6206 Slocum Road Ontario, NY 14519 315-524-8000 tim@wellergroupllc.com www.wellergroupllc.com 2016 Federal Income Tax Planning March 06,

AFFORDABLE CARE ACT: STATUS CHART Health Plans

AFFORDABLE CARE ACT: STATUS CHART Health Plans July 2017 TODD MARTIN, PARTNER 612.335.1409 todd.martin@stinson.com Table of Contents Page ACA Coverage Mandates... 1 ACA Insurance Market Rules... 5 ACA

AFFORDABLE CARE ACT: STATUS CHART Health Plans July 2017 TODD MARTIN, PARTNER 612.335.1409 todd.martin@stinson.com Table of Contents Page ACA Coverage Mandates... 1 ACA Insurance Market Rules... 5 ACA

2016 vs Key Facts and Figures

2016 vs. 2017 Key Facts and Figures Keir Educational Resources compiled the following key facts and figures for the CFP Certification Examination to assist you with your preparation for this comprehensive

2016 vs. 2017 Key Facts and Figures Keir Educational Resources compiled the following key facts and figures for the CFP Certification Examination to assist you with your preparation for this comprehensive

INDIVIDUAL YEAR END NEWSLETTER DEC 2018

INDIVIDUAL YEAR END NEWSLETTER DEC 2018 LUONGO & ASSOCIATES, PC (301) 952-9437 WWW.LUONGOCPA.COM Unlike recent years, in which the tax rules have been fairly stable, 2018 brings extensive changes not seen

INDIVIDUAL YEAR END NEWSLETTER DEC 2018 LUONGO & ASSOCIATES, PC (301) 952-9437 WWW.LUONGOCPA.COM Unlike recent years, in which the tax rules have been fairly stable, 2018 brings extensive changes not seen

SAVE 2018 INCOME TAXES! LAST MINUTE TAX PLANNING TIPS. Presented by: James J. Holtzman, CFP

SAVE 2018 INCOME TAXES! LAST MINUTE TAX PLANNING TIPS Presented by: James J. Holtzman, CFP JAMES J. HOLTZMAN, CFP James J. Holtzman, CFP, is a Wealth Advisor and Shareholder with Legend Financial Advisors,

SAVE 2018 INCOME TAXES! LAST MINUTE TAX PLANNING TIPS Presented by: James J. Holtzman, CFP JAMES J. HOLTZMAN, CFP James J. Holtzman, CFP, is a Wealth Advisor and Shareholder with Legend Financial Advisors,

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the INDIVIDUALS

Tax Briefing Tax Cuts and Jobs Act December 16, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Top Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Tax Briefing Tax Cuts and Jobs Act December 16, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Top Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Tax Cuts and Jobs Act of 2017 (TCJA) Key Individual Tax Provisions

Key Individual Tax Provisions") Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

06/29/2015_830 AM. Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction

Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction Overview of ACA Healthcare Reform in 2015 What s on the Horizon Potential Legislative Actions Patient Protection and

Healthcare Reform How Will Your Business be Affected in 2015 and Beyond? Introduction Overview of ACA Healthcare Reform in 2015 What s on the Horizon Potential Legislative Actions Patient Protection and

Health Care Reform: What s In Store for Employer Health Plans?

Health Care Reform: What s In Store for Employer Health Plans? April 21, 2010 Presented by: Sue O. Conway sconway@wnj.com (616) 752-2153 Norbert F. Kugele nkugele@wnj.com (616) 752-2186 Copyright 2010

Health Care Reform: What s In Store for Employer Health Plans? April 21, 2010 Presented by: Sue O. Conway sconway@wnj.com (616) 752-2153 Norbert F. Kugele nkugele@wnj.com (616) 752-2186 Copyright 2010

IMPACT OF THE ELECTION President-Elect Trump proposes significant changes to the tax law including:

December 2016 To Our Clients and Friends: While many of you are making plans for year-end holidays, what should not be overlooked this time of year is year-end tax planning, especially considering the

December 2016 To Our Clients and Friends: While many of you are making plans for year-end holidays, what should not be overlooked this time of year is year-end tax planning, especially considering the

An Employer s Guide to Health Care Reform

An Employer s Guide to Health Care Reform Background On March 23, 2010, President Obama signed into law the Patient Protection and Affordable Care Act (PPACA). Less than a week later, Congress passed the

An Employer s Guide to Health Care Reform Background On March 23, 2010, President Obama signed into law the Patient Protection and Affordable Care Act (PPACA). Less than a week later, Congress passed the

HASHEM and SIMMS, PLLC CERTIFIED PUBLIC ACCOUNTANTS

HASHEM and SIMMS, PLLC CERTIFIED PUBLIC ACCOUNTANTS George K. Hashem, CPA Tyler W. Simms, CPA December 2, 2014 Dear Client: As 2014 draws to a close, there is still time to reduce your 2014 tax bill and

HASHEM and SIMMS, PLLC CERTIFIED PUBLIC ACCOUNTANTS George K. Hashem, CPA Tyler W. Simms, CPA December 2, 2014 Dear Client: As 2014 draws to a close, there is still time to reduce your 2014 tax bill and

2017 Federal Income Tax Planning

ABC Financial Planning Michael A. Licciardi Professional Planner 77 Gilcreast Rd Suite 2004 603-965-3065 x106 Mike@apsusa.com www.myabcplan.com 2017 Federal Income Tax Planning March 21, 2017 Page 1 of

ABC Financial Planning Michael A. Licciardi Professional Planner 77 Gilcreast Rd Suite 2004 603-965-3065 x106 Mike@apsusa.com www.myabcplan.com 2017 Federal Income Tax Planning March 21, 2017 Page 1 of

Individual income tax provision highlights

Legislative Update Tax Cuts and Jobs Act Individual income tax provision highlights On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act (P.L. 115-97). Highlights of the key

Legislative Update Tax Cuts and Jobs Act Individual income tax provision highlights On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act (P.L. 115-97). Highlights of the key

Health Care Reform: Be Prepared for 2014

Health Care Reform: Be Prepared for 2014 Your Health Care Reform Team: Moderator Eboni Britt POMCO Group Marketing Manager Co-presenter Jessica Marabella POMCO Group Account Manager Co-presenter Amy Zell

Health Care Reform: Be Prepared for 2014 Your Health Care Reform Team: Moderator Eboni Britt POMCO Group Marketing Manager Co-presenter Jessica Marabella POMCO Group Account Manager Co-presenter Amy Zell

After a weekend of intense negotiations

FISCAL CLIFF TAX LEGISLATION January 1, 2013 Highlights Sunset of EGTRRA s Reduced Individual Income Tax Rates Lower AMT Exemption Amounts Sunset of JGTRRA s Reduced Capital Gains/Dividends Tax Rates Expiration

FISCAL CLIFF TAX LEGISLATION January 1, 2013 Highlights Sunset of EGTRRA s Reduced Individual Income Tax Rates Lower AMT Exemption Amounts Sunset of JGTRRA s Reduced Capital Gains/Dividends Tax Rates Expiration