South African Reward Association. Tax Update Budget 2018/19

|

|

|

- Alannah Hart

- 5 years ago

- Views:

Transcription

1 South African Reward Association Tax Update Budget 2018/19

2 Events Tax and Cost to Company Workshop What happens after package determined (art vs. science) 14 & 15 August Johannesburg

3 Tax Morality

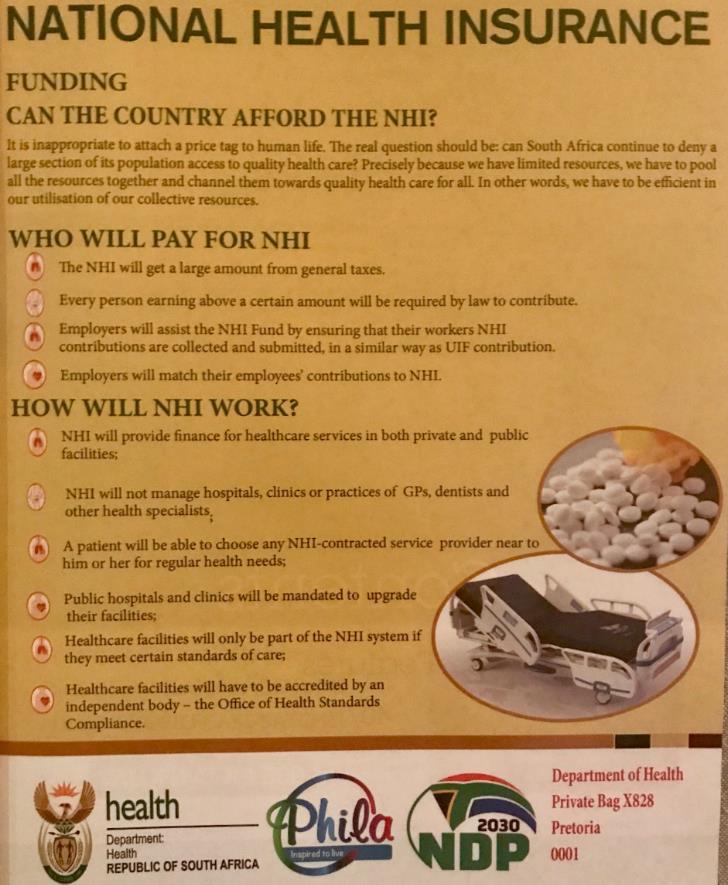

4 National Health Insurance No Budget Announcement

5

6 Retirement Reform & Social Security Promulgated 01 March 2019 (3 rd time) Thorny issue of compulsory preservation

7 Who Pays?

8 Tax Tables

9 Higher Tax Due to Incorrect Inflationary Adjustment (Inflation 5,3%)

10 Assumed Total Kilometers 20,000 and Business Kilometers 15,000 Travel Allowance Claim Adjustment

11 Medical Aid Credits Over the next three years, below-inflation increases in medical tax credits will help government to fund the rollout of national health insurance. The medical tax credit will be reviewed after the Davis Tax Committee presents its recommendations.

12 Example (Shared)

13 Employee Personal Inflation Increase 15% (01 April 2018) VAT exemptions removed and increase ad valorem duty (01 April 2018). There 19 zero-rated food items (include dried beans, samp, maize meal and rice) to be reduced. Fuel price

to reflect the original policy intent that only brown bread and whole wheat brown bread will be zero-rated.")

14 More Wealthy or Healthy, More VAT The 19 zero-rated food items are only meant to cover basic food items. As of 1 April 2018, government proposes to amend the VAT Act (1991) to reflect the original policy intent that only brown bread and whole wheat brown bread will be zero-rated. Products such as rye or low GI bread, which in South Africa are much more expensive and tend to be consumed by richer households, will not be zero-rated.

15 Ad Valorem Increase Effective 1 April 2018, the maximum ad valorem excise duty for motor vehicles will be increased from 25 per cent to 30 per cent. The classification of cellular telephones will be updated to include smart phones to ensure they attract ad valorem excise duties. In addition, the ad valorem excise duty rates, now at 5 per cent and 7 per cent, will be increased to 7 per cent and 9 per cent, ensuring that households spending more on luxury goods contribute proportionately more to revenue Government will also consult on a proposal to replace the flat rate for cellphones with a progressive rate structure based on the value of the phone.

16 Fuel Price (04 April 2018) Employee Personal Inflation Increase

17 Standard Adjustments New Subsistence Table (01 March 2018). Incidental costs R128 per day Meals and Incidental R416 per day Updated per country list (highest appears Angola USD303 per day) Housing abatement increase from R to R (company owned housing). Official interest rate will be 7.75% (soon to increase)

18 Unchanged Retirement Withdrawal Rates Capital Gains 18% Retirement withdrawal rates (normal vs retrenchment / death)

19 Budget Specific Tax Amendments

20 Fruitless and Wasteful Expenditure To ensure proper governance of public entities and encourage accountability, government proposes that losses or expenditure classified as fruitless and wasteful will not qualify for a tax deduction.

21 Splitting Medical Credits The medical tax credit consists of two components: medical scheme fees for approved medical scheme contributions and additional medical expenses for out-of-pocket medical payments. Government is concerned that some taxpayers may be excessively benefiting from this rebate, specifically in instances where multiple taxpayers contribute toward the medical scheme or expenses of another person (for example, adult children jointly contributing to their elderly mother s medical scheme). Where taxpayers carry a share of the medical scheme, contribution or medical cost, it is proposed that the medical tax credit should also be apportioned between the various contributors.

22 Removing of fringe benefit for preferential interest rates to employees for housing In 2014, legislative changes were made to remove the fringe benefit that previously applied to employees with remuneration below R for the acquisition of low-cost housing with a value below R In line with government policy to promote the provision of housing, it is proposed that the relief from this fringe benefit tax be extended to loans at preferential interest rates, which are solely for housing use, made to employees who satisfy the same remuneration criteria for loans with a value of less than R Note Important Announcement for Employee Housing Scheme Low Interest Loans now allowed with no fringe benefit tax Craig Rocher s Savings Calculation = R592,223 (R450,000 10% 20 years)

23 South African Expatriates Working Abroad Tax treatment of contributions to retirement funds situated outside South Africa: The Income Tax Act currently exempts all retirement benefits from a foreign source for employment rendered outside of South Africa from taxation. The interaction of this exemption with double taxation agreements and other provisions of the Income Tax Act will be reviewed to ensure that the principle of allowing deductible contributions only incases where benefits are taxable isupheld. Note Important change impacting many South African expatriates working internationally. Must look at retirement fund implications.

24 South African Expatriates Working Abroad Align tax treatment of preservation funds upon emigration Upon formal emigration an individual is able to withdraw the full value of their retirement annuity, after paying the applicable taxes. Government will consider aligning the tax treatment of different types of retirement fund withdrawals in such circumstances. Note Risk and cost assessment for South Africans abroad (surprising how many non compliant!) Additional tax cost was main reason for postponing new law to 01 March Employer comments for not just expatriates, but even localised hires who are expatriates.

25 Fund Transfers It is proposed that transfers to pension preservation and provident preservation funds be catered for in the legislation. Rectifying tax anomalies on the transfer of retirement funds: The transfer of fund amounts between, or within, retirement funds at the same employer has inadvertently led to a tax liability for members, due to the current wording of the legislation. In principle, there should be no additional tax consequence for members if the transfers refer to amounts that have already been contributed to the retirement fund. Legislative amendments will be retrospectively introduced to correct these unintended tax liabilities.

26 Adjusting Official Rate of Interest The official rate of interest is the current repurchase rate plus 100 basis points (7.75 per cent). This rate is used to quantify the fringe benefit of low interest rate loans provided by employers and the amount of a donation for low interest loans to trusts by connected persons. Given that interest rates lower than prime are now uncommon, it is proposed that the official rate be increased to a level closer to the prime rate of interest. This would allow the benefit of lower rates to be measured with reference to a rate that approximates the rate offered by commercial banks to low-risk clients.) Who is still doing this? National Credit Regulator (NCR) compliance barrier.

27 Important New Developments Past Year

28 UIF No longer tax exempt 01 March employees under a contract of employment contemplated in section 18 (2) of the Skills Development Act, 1998 (Act 97 of 1998), and their employers (Learnership exemption) an employee and his or her employer, where that employee has entered the Republic for the purpose of carrying out a contract of service, apprenticeship or learnership within the Republic if upon the termination thereof the employer is required by law or by the contract of service, apprenticeship or learnership, as the case may be, or by any other agreement or undertaking, to repatriate that person, or if that person is so required to leave the Republic (Expatriate exemption) Note Registration for expatriates Many employers get learnership claims incorrect

29 ETI Binding General Ruling 44, 13 October 2017, Meaning of 160 hours for purposes of section 4(1)(b). Binding General Ruling 47, 05 March 2018, Meaning of monthly remuneration for employers remunerating employees on a weekly or fortnightly basis.

30 Subsistence Ruling 291 (24 January 2018)

31 Relocation Costs BPR 186 Settling-in Allowance, 22 November 2017 (confirms once-off repealed) Exempt Bond registration and legal fees paid in respect of a new residence that has been purchased; Transfer duty paid in respect of the new residence; Cancellation fees paid for bond cancellation on previous residence; and Agent s commission paid on sale of previous residence New school uniforms; Replacement of curtains; Motor vehicle registration fees; and Telephone, water and electricity connection. Now taxable (no more allowances) Payments to reimburse the employee for loss on the sale of a previous residence during transfer; and Architect s fees for the design or alteration of a new residence.

32 Approved Section 18A PBO s PBO%27s.aspx 18,995 entities

33 2019 IRP5 Codes on Important Items The following codes must be applied for 2018/19 (August 2018 and February 2019) submissions New Codes The new exemption thresholds for bursaries or scholarships provided by employers to assist disabled persons One new code to report the dividend category which is defined to be remuneration In respect of travel reimbursements, the reporting rules for two of the existing codes have been changed, and a new code has been added.

34 Bursary Codes Normal Bursaries Exempt Basic Education: 3815 Exempt Further Education: 3821

35

36 QUALIFICATION DESCRIPTION BURSARY TAX LIMIT PER CHILD PER ANNUM School Grade R - Grade 12 R20 000,00 NQF 1 General Certificate R20 000,00 NQF 2 Elementary Certificate R20 000,00 NQF 3 Intermediate Certificate R20 000,00 NQF 4 National Certificate R20 000,00 NQF 5 Higher Certificate R20 000,00 NQF 6 Diploma/Advanced Certificate R20 000,00 NQF 7 Bachelor's Degree/Advanced Diploma R60 000,00 NQF 8 Bachelor Honours Degree/ Postgraduate Diploma R60 000,00 NQF 9 Master's Degree R60 000,00 NQF 10 Doctoral Degree (Professional) R60 000,00

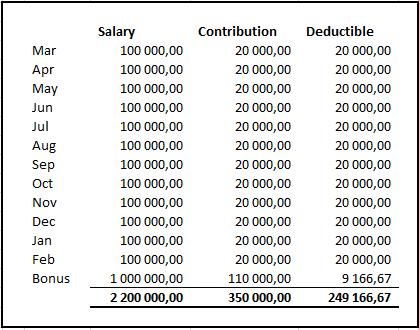

37 Example #1

38 Example #2

39 Rem Guys Always Do The Calculation

40 Dividends As Normal Remuneration Effective from 1 March 2017, amendments were made to the Income Tax Act to introduce anti avoidance measures dealing with schemes where restricted shares in terms of section 8C are allocated to employees through employee share based incentive schemes. As a remedy, the 1 March 2017 amendments added three categories of dividends that are Employment related to the definition of remuneration, and a fourth category has now been added as paragraph (g)(iv) to the definition of remuneration from 1 March The new dividend category must be reported on a tax certificate as Code Employers must apply for directives (application form (IRP3(s)) that specify the PAYE that must be withheld from dividends that are not exempt (paragraph (dd), (ii), (jj) and (kk) of the proviso of section 10(1)(k)(i)) Payroll Authors Group

41 Employee Travel Reimbursement Subject to PAYE Employees tax and reimbursement of travel expenses To facilitate and simplify the calculation and administration of employees tax, it is proposed that only the portion of the travel expenses reimbursed by an employer that exceeds the rate or distance fixed by the Minister of Finance by notice in the Gazette in terms of the current law should be regarded as remuneration for purposes of determining employees tax. Code 3703 still applicable but for all travel Everyone should keep a logbook (?) No more up to 12,000km tax free reimbursement Below limit everything is exempt, but no travel allowance and must be below limit

42 Example

43 Employee Travel Reimbursement Subject to PAYE No code 3701 (travel allowance / fuel card) and 3703 allowed Should normal employees have travel allowance? Only reimbursement = tax free Allowance = can claim against cost of vehicle Calculate! Company vehicle remains mathematically best option for above 60% - 65% business travel. No brainer where above 80% business?

44 NED Fees PAYE and VAT Binding General Ruling (Issue 2) on VAT for Non- Executive Directors Are allowed to work through company (SCA case) Financial statements VAT and PAYE FAQ on BGR 40 & 41 (19 August 2017) Consider information note

45 R350,000 limit (not increased) Commentary in the TLAB 1017 The proposed spreading of the R350,000 annual cap on retirement fund contributions for PAYE purposes means that a person who exceeds the R29,167 monthly cap in a single month but not in others will not be able to benefit from unused amounts in the other months. R remains unchanged R29, per monthly maximum

46 Example

47 Important Items Coming Year

48 Tax Court Cases Coming Year Employee Gifts (wedding, birthdays, conference bags, secretary days) Tax return professional fees and expatriate tax calculations fringe benefit tax (KPMG)

49 Voluntary vs Involuntary Retrenchment Have you terminated any employees 2017/18 due to operational requirements. What is voluntary (full tax) vs. involuntary retrenchment (R500,000 exemption table)? Remains uncertain SARS considering policy. IT13726 (Port Elizabeth Tax Court) Judge Elna Revelas (retrenchment or dismissal)

50 Expatriates are not happy Amending foreign employment income-tax exemption in respect of South African residents 183-and-60 day rule saved 01 March 2020 only 1 st R1m exempt Then normal tax and tax credits (where applicable) Fringe benefits & Allowances not exempt Currency differences no tax relief financial emigration clear way to break tax residency

51 Thank You

Tax, ETI and UIF Amendments 2018/2019

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Tax tables 2019/2020 (year of assessment ending 29 February 2020)

") BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

PAYROLL TAX POCKET GUIDE. A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa.

PAYROLL TAX POCKET GUIDE 2019 2020 A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside

PAYROLL TAX POCKET GUIDE 2019 2020 A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside

ON THE SCALES 7 OF 2018 NATIONAL BUDGET 2018

ON THE SCALES 7 OF 2018 NATIONAL BUDGET 2018 On 21 February 2018, Minister Malusi Gigaba presented his National Budget speech. The speech was presented within a framework of renewal, hope and optimism,

ON THE SCALES 7 OF 2018 NATIONAL BUDGET 2018 On 21 February 2018, Minister Malusi Gigaba presented his National Budget speech. The speech was presented within a framework of renewal, hope and optimism,

NEWS FLASH - February 2016

NEWS FLASH - February 2016 Africa: South Africa CRS TAX POCKET GUIDE 2016/2017 it is important that Employers note the following TAX RATES (TAX YEAR ENDING 28 FEBRUARY 2017) Individuals and special trusts

NEWS FLASH - February 2016 Africa: South Africa CRS TAX POCKET GUIDE 2016/2017 it is important that Employers note the following TAX RATES (TAX YEAR ENDING 28 FEBRUARY 2017) Individuals and special trusts

Budget Highlights 2018

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS. Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

Tax and ETI Amendments 2017/2018

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

South African Income Tax Guide for 2013/2014

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

2017 Employees & Payroll Withholding

2017 Employees & Payroll Withholding Presented by Rob Cooper Rob Cooper is the Director of Legislation at Sage VIP Payroll & HR. As one of the company s founders, he has an in-depth understanding of the

2017 Employees & Payroll Withholding Presented by Rob Cooper Rob Cooper is the Director of Legislation at Sage VIP Payroll & HR. As one of the company s founders, he has an in-depth understanding of the

SARS Tax Guide 2014 / 2015

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16.

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

Tax guide 2018/2019 TAX FACTS

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

18% of taxable income % of taxable income above % of taxable income above

Important Note If your Sage One Payroll software is already in March 2016, your year-to-date amounts will recalculate when you do a start of period into April, unless you make any changes on an employee

Important Note If your Sage One Payroll software is already in March 2016, your year-to-date amounts will recalculate when you do a start of period into April, unless you make any changes on an employee

BUDGET 2019 TAX GUIDE

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

Payroll Tax Pocket Guide 2017/18

Payroll Tax Pocket Guide 2017/18 A complete reference guide covering legislative matters that affect the HR & payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside RSA

Payroll Tax Pocket Guide 2017/18 A complete reference guide covering legislative matters that affect the HR & payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside RSA

Quick Tax Guide 2013/14 Simplicity from complexity

Quick Tax Guide 2013/14 Simplicity from complexity Income Tax for Individuals Tax rates and rebates Individuals, Estates & Special Trusts 1 (Year ending 28 February 2014) Taxable income as exceeds But

Quick Tax Guide 2013/14 Simplicity from complexity Income Tax for Individuals Tax rates and rebates Individuals, Estates & Special Trusts 1 (Year ending 28 February 2014) Taxable income as exceeds But

INCOME TAX: INDIVIDUALS AND TRUSTS

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

Budget Speech 2018: Implications for Retirement Funds

Edition 4 of 2018: February 2018 Budget Speech 2018: Implications for Retirement Funds SA s Finance Minister Malusi Gigaba delivered the National Budget speech on 21 February 2018. This publication summarises

Edition 4 of 2018: February 2018 Budget Speech 2018: Implications for Retirement Funds SA s Finance Minister Malusi Gigaba delivered the National Budget speech on 21 February 2018. This publication summarises

Payroll Pocket Guide. as at March A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa

Payroll Pocket Guide as at March 2013 A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa Quick Reference Subsistence Allowance Travel inside RSA

Payroll Pocket Guide as at March 2013 A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa Quick Reference Subsistence Allowance Travel inside RSA

Next >> Driving progress Quick Tax Guide 2018/19

Next >> Driving progress Quick Tax Guide 2018/19 South Africa Contents... 1 and Rebates... 1... 1... 2 and Allowances... 3... 4 Severance and Retirement Fund Lump Sum... 4... 5... 5... 6... 7... 7... 7...

Next >> Driving progress Quick Tax Guide 2018/19 South Africa Contents... 1 and Rebates... 1... 1... 2 and Allowances... 3... 4 Severance and Retirement Fund Lump Sum... 4... 5... 5... 6... 7... 7... 7...

Change, the new certainty

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

Tax data card 2018/2019

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

SAPA - ANNUAL PAYE UPDATE BREAKFAST, Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014

SAPA - ANNUAL PAYE UPDATE BREAKFAST, 2014 Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014 Content Chapter 4 Annexure C Davis Tax Review Committee Miscellaneous 1 Content: Chapter

SAPA - ANNUAL PAYE UPDATE BREAKFAST, 2014 Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014 Content Chapter 4 Annexure C Davis Tax Review Committee Miscellaneous 1 Content: Chapter

South African Reward Associa3on

South African Reward Associa3on Budget Update 2012 Tax Law Changes 01 March 2012 Ac3on List for 2012 Jerry Botha jerry@taxconsul3ng.co.za 082 899 6118 Landscape 1999/2000 = 579 Pages Since then = 1,868

South African Reward Associa3on Budget Update 2012 Tax Law Changes 01 March 2012 Ac3on List for 2012 Jerry Botha jerry@taxconsul3ng.co.za 082 899 6118 Landscape 1999/2000 = 579 Pages Since then = 1,868

Guide. for. Income Tax & other taxes for Individuals. Tax Thresholds, Tax Rates & Tax Rebates

Guide for Income Tax & other taxes for Individuals South Africa has a hybrid tax system i.e. residents are taxed on their world-wide income (residence-based system of taxation) and non-residents are taxed

Guide for Income Tax & other taxes for Individuals South Africa has a hybrid tax system i.e. residents are taxed on their world-wide income (residence-based system of taxation) and non-residents are taxed

This booklet is published by PKF Publishers (Pty) Ltd for and on behalf of. chartered accountants & business advisers

Ltd for and on behalf of. chartered accountants & business advisers") BUDGET PROPOSALS 1 Tax-Preferred Savings Accounts Tax-preferred savings accounts, as a measure to encourage household savings, will proceed. These accounts will have an initial annual contribution limit

BUDGET PROPOSALS 1 Tax-Preferred Savings Accounts Tax-preferred savings accounts, as a measure to encourage household savings, will proceed. These accounts will have an initial annual contribution limit

Financial Leadership through Professional Excellence 2017/2018 TAX CARD. Telephone + 27 (0) Facsimile + 27 (0)

Facsimile + 27 (0)") Financial Leadership through Professional Excellence 2017/2018 TAX CAD Telephone + 27 (0) 21 683 4834 Facsimile + 27 (0) 86 541 2872 www.mdacc.co.za mdacc@mdacc.co.za MD House Greenford Office Estate Off

Financial Leadership through Professional Excellence 2017/2018 TAX CAD Telephone + 27 (0) 21 683 4834 Facsimile + 27 (0) 86 541 2872 www.mdacc.co.za mdacc@mdacc.co.za MD House Greenford Office Estate Off

2016/2017 TAX CARD. Financial Leadership through Professional Excellence. Telephone + 27 (0) Facsimile + 27 (0)

Facsimile + 27 (0)") Financial Leadership through Professional Excellence 2016/2017 TAX CAD Telephone + 27 (0) 21 683 4834 Facsimile + 27 (0) 86 541 2872 www.mdacc.co.za mdacc@mdacc.co.za MD House Greenford Office Estate Off

Financial Leadership through Professional Excellence 2016/2017 TAX CAD Telephone + 27 (0) 21 683 4834 Facsimile + 27 (0) 86 541 2872 www.mdacc.co.za mdacc@mdacc.co.za MD House Greenford Office Estate Off

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

Next >> Quick Tax Guide 2019/20 South Africa. Making an impact that matters

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters Contents... 1...1...1...2...3...4 Severance and Retirement Fund Lump Sum...4... 5...5...6...7...7...7...7... 8...8...8...9...9...9...9...10...10...10...10...10...11...

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters Contents... 1...1...1...2...3...4 Severance and Retirement Fund Lump Sum...4... 5...5...6...7...7...7...7... 8...8...8...9...9...9...9...10...10...10...10...10...11...

BAKER TILLY GREENWOODS

BAKER TILLY GREENWOODS CHARTERED ACCOUNTANTS PRACTICE PROFILE Baker Tilly Greenwoods was established in 1946. The firm has expanded over the years and practises in all major fields of Accounting, Auditing

BAKER TILLY GREENWOODS CHARTERED ACCOUNTANTS PRACTICE PROFILE Baker Tilly Greenwoods was established in 1946. The firm has expanded over the years and practises in all major fields of Accounting, Auditing

D-BIT Payroll. Employees Remuneration for UIF, SDL, PAYE. D-BIT SYSTEMS (Pty) Ltd D-BIT Systems (Pty) Ltd) 2/24/2012, 3:18 PM

Ltd D-BIT Systems (Pty) Ltd) 2/24/2012, 3:18 PM") D-BIT SYSTEMS (Pty) Ltd RegNo: 87/033407 D-Bit Building 18 Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 156 South Africa D-BIT Payroll Employees for UIF, SDL, PAYE 01... D-BIT Systems (Pty)

D-BIT SYSTEMS (Pty) Ltd RegNo: 87/033407 D-Bit Building 18 Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 156 South Africa D-BIT Payroll Employees for UIF, SDL, PAYE 01... D-BIT Systems (Pty)

Budget Highlight 2017

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

A measured budget, but tax base still under pressure

A measured budget, but tax base still under pressure In line with the hopeful message delivered in the State of the Nation address by the President, the Minister of Finance delivered a measured budget

A measured budget, but tax base still under pressure In line with the hopeful message delivered in the State of the Nation address by the President, the Minister of Finance delivered a measured budget

LEGAL UPDATE: 2014/15 BUDGET HIGHLIGHTS

LEGAL UPDATE: 2014/15 BUDGET HIGHLIGHTS Introduction In his fifth and final national budget speech under the current administration of President Jacob Zuma, Finance Minister Pravin Gordhan began by quoting

LEGAL UPDATE: 2014/15 BUDGET HIGHLIGHTS Introduction In his fifth and final national budget speech under the current administration of President Jacob Zuma, Finance Minister Pravin Gordhan began by quoting

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

18 August 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

companies from 33% to 28%. This booklet is published by FHPKF Publishers (Pty) Ltd for and on behalf of chartered accountants & business advisers

Ltd for and on behalf of chartered accountants & business advisers") BUDGET PROPOSALS 1 Dividends Tax A dividend withholding tax will replace STC from 1 April 2012 at a rate of 15%. 2 Capital Gains Tax As from 1 March 2012, the inclusion rate for individuals and special

BUDGET PROPOSALS 1 Dividends Tax A dividend withholding tax will replace STC from 1 April 2012 at a rate of 15%. 2 Capital Gains Tax As from 1 March 2012, the inclusion rate for individuals and special

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

BUDGET PROPOSALS 2 BURSARIES & SCHOLARSHIPS 14 CAPITAL GAINS TAX (CGT) 22 CAPITAL INCENTIVE ALLOWANCES 31 COMPANIES & CLOSE CORPORATIONS 6 CRITICAL

22 CAPITAL INCENTIVE ALLOWANCES 31 COMPANIES & CLOSE CORPORATIONS 6 CRITICAL") INDEX PAGE BUDGET PROPOSALS 2 BURSARIES & SCHOLARSHIPS 14 CAPITAL GAINS TAX (CGT) 22 CAPITAL INCENTIVE ALLOWANCES 31 COMPANIES & CLOSE CORPORATIONS 6 CRITICAL PAYMENT DATES 8 DEDUCTIONS & ALLOWANCES INDIVIDUALS

INDEX PAGE BUDGET PROPOSALS 2 BURSARIES & SCHOLARSHIPS 14 CAPITAL GAINS TAX (CGT) 22 CAPITAL INCENTIVE ALLOWANCES 31 COMPANIES & CLOSE CORPORATIONS 6 CRITICAL PAYMENT DATES 8 DEDUCTIONS & ALLOWANCES INDIVIDUALS

BBR VAN DER GRIJP & ASSOCIATES

BB VAN DE GIJP & ASSOCIATES CHATEED ACCOUNTANTS (S.A.) P. O. BOX 1448 1106 COUTYAD egistration: 920 932 E SOMESET WEST 7129 GANTS CENTE, STAND 7140 Tel: (021) 854 9060 Knysna Office: P.O. Box 2602 3 Hill

BB VAN DE GIJP & ASSOCIATES CHATEED ACCOUNTANTS (S.A.) P. O. BOX 1448 1106 COUTYAD egistration: 920 932 E SOMESET WEST 7129 GANTS CENTE, STAND 7140 Tel: (021) 854 9060 Knysna Office: P.O. Box 2602 3 Hill

An automated tax clearance system will be implemented this year. 4 Employment Incentive

BUDGET PROPOSALS 1 Retirement Savings Reforms An employer s contribution to retirement funds on behalf of an employee will be treated as a taxable fringe benefit in the hands of the employee. Individuals

BUDGET PROPOSALS 1 Retirement Savings Reforms An employer s contribution to retirement funds on behalf of an employee will be treated as a taxable fringe benefit in the hands of the employee. Individuals

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

Paper P6 (ZAF) Advanced Taxation (South Africa) Thursday 7 December Professional Level Options Module

Advanced Taxation (South Africa) Thursday 7 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Thursday 7 December 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Professional Level Options Module Advanced Taxation (South Africa) Thursday 7 December 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Tax rates for natural persons and special trusts 2018/2019 tax year

We are at a moment in the history of our nation when the people, through their determination, have started to turn the country around Now is the time for all of us to work together, in honour of Nelson

We are at a moment in the history of our nation when the people, through their determination, have started to turn the country around Now is the time for all of us to work together, in honour of Nelson

ON THE SCALES 18 OF The Draft Taxation Laws Amendment Bill 2018

ON THE SCALES 18 OF 2018 The Draft Taxation Laws Amendment Bill 2018 National Treasury has issued the draft Taxation Laws Amendment Bill 2018 ( draft TLAB ) for comment. It includes some of the proposed

ON THE SCALES 18 OF 2018 The Draft Taxation Laws Amendment Bill 2018 National Treasury has issued the draft Taxation Laws Amendment Bill 2018 ( draft TLAB ) for comment. It includes some of the proposed

RE: CALL FOR COMMENT: DRAFT TAXATION LAWS AMENDMENT BILL ( TLAB )

") 5 August 2013 Ms N. Mpotulo The National Treasury 240 Vermuelen Street PRETORIA 0001 Ms A. Collins Legal & Policy The South African Revenue Service Lehae La SARS PRETORIA 8000 BY E-MAIL: nomfanelo.mpotulo@treasury.gov.za

5 August 2013 Ms N. Mpotulo The National Treasury 240 Vermuelen Street PRETORIA 0001 Ms A. Collins Legal & Policy The South African Revenue Service Lehae La SARS PRETORIA 8000 BY E-MAIL: nomfanelo.mpotulo@treasury.gov.za

Tax Professional Knowledge Competency Assessment

Tax Professional Knowledge Competency Assessment JUNE 2016 Paper 2 Instructions to Candidates 1. This competency assessment paper consists of four questions. 2. Answer each question in a separate answer

Tax Professional Knowledge Competency Assessment JUNE 2016 Paper 2 Instructions to Candidates 1. This competency assessment paper consists of four questions. 2. Answer each question in a separate answer

Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TAX)

") Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TA) 2011 2012 2013 TA YEAR SITE limit Only > 65 years : R540pa R45pm Only for > 65 years : R540pa R45pm Only for > 65 years : Tax Rebates

Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TA) 2011 2012 2013 TA YEAR SITE limit Only > 65 years : R540pa R45pm Only for > 65 years : R540pa R45pm Only for > 65 years : Tax Rebates

bulletin PAPILSKY HURWITZ 2014/2015 CHARTERED ACCOUNTAN TS (SA)

") bulletin 2014/2015 PAPILSKY HURWITZ CHARTERED ACCOUNTAN TS (SA) IMPORTANT amendments to the income tax act, current tax RATes and allowances and other general points of interest Papilsky Hurwitz 1st Floor,

bulletin 2014/2015 PAPILSKY HURWITZ CHARTERED ACCOUNTAN TS (SA) IMPORTANT amendments to the income tax act, current tax RATes and allowances and other general points of interest Papilsky Hurwitz 1st Floor,

INTERCODE PAYROLL V5.0.0 RELEASE NOTES

INTERCODE PAYROLL V5.0.0 RELEASE NOTES BEFORE INSTALLING THE UPDATE It is recommended that you make backup copies of all your existing employer files before you install any updates to Intercode Payroll.

INTERCODE PAYROLL V5.0.0 RELEASE NOTES BEFORE INSTALLING THE UPDATE It is recommended that you make backup copies of all your existing employer files before you install any updates to Intercode Payroll.

EMPLOYEE BENEFIT UPDATE

EMPLOYEE BENEFIT UPDATE jerry@taxconsulting.co.za 0828996118 B e n e f i t T r e e Your Benefit Tree School Fees Classic Life Stages Buy House Start Family Retire Graduate Marry Benefit Environment Regulation

EMPLOYEE BENEFIT UPDATE jerry@taxconsulting.co.za 0828996118 B e n e f i t T r e e Your Benefit Tree School Fees Classic Life Stages Buy House Start Family Retire Graduate Marry Benefit Environment Regulation

Quick Start Guide to Payroll Tax Year-End

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

These transactions are to be reviewed in order to determine whether additional anti-tax avoidance measures are required.

Below is a summary of the tax proposals that were delivered by Finance Minister Pravin Gordhan at the National Budget address on 24 February 2016. This is a high level overview of the changes. Capital

Below is a summary of the tax proposals that were delivered by Finance Minister Pravin Gordhan at the National Budget address on 24 February 2016. This is a high level overview of the changes. Capital

Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016

No. 3 of 2017 February 2017 Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016 A. The Taxation Laws Amendment Act No. 15 of 2016 was promulgated in Government Gazette No. 40562 on 19 January 2017.

No. 3 of 2017 February 2017 Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016 A. The Taxation Laws Amendment Act No. 15 of 2016 was promulgated in Government Gazette No. 40562 on 19 January 2017.

Paper P6 (ZAF) Advanced Taxation (South Africa) Thursday 8 December Professional Level Options Module

Advanced Taxation (South Africa) Thursday 8 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Thursday 8 December 2016 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Professional Level Options Module Advanced Taxation (South Africa) Thursday 8 December 2016 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

September 2015 PAYE Reconciliation Communication

0800 00 7277 sars.gov.za September 2015 PAYE Reconciliation Communication 1. Clarification of source codes The following amendments to descriptions and explanations of source codes should be noted (amendments

0800 00 7277 sars.gov.za September 2015 PAYE Reconciliation Communication 1. Clarification of source codes The following amendments to descriptions and explanations of source codes should be noted (amendments

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee.

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee. Q How can PAYE be deducted from an accrual? Income that accrues in one tax

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee. Q How can PAYE be deducted from an accrual? Income that accrues in one tax

Hope and confidence come from energetic involvement and a willingness to

27 February 2013 Compiled by Group Taxation This document is distributed as a service to the Liberty group via the internal e-mail system. It deals with broad-ranging tax developments of relevance to the

27 February 2013 Compiled by Group Taxation This document is distributed as a service to the Liberty group via the internal e-mail system. It deals with broad-ranging tax developments of relevance to the

Increased Personal Income Tax Rates

flash Alert A Publication for Global Mobility and Tax Professionals by KPMG s Global Mobility Services Practice South Africa Personal Tax Rate, Fringe Benefit Changes in Budget 2015 by KPMG, South Africa

flash Alert A Publication for Global Mobility and Tax Professionals by KPMG s Global Mobility Services Practice South Africa Personal Tax Rate, Fringe Benefit Changes in Budget 2015 by KPMG, South Africa

Attorneys. Financial and Taxation Directory 2005/2006

Attorneys Financial and Taxation Directory 2005/2006 CONTENTS South African Taxation Highlights of the 2005/2006 Budget 2-4 Calculation of Tax Payable 5 Tables of Normal Tax Payable 6-7 Comparison of 2006

Attorneys Financial and Taxation Directory 2005/2006 CONTENTS South African Taxation Highlights of the 2005/2006 Budget 2-4 Calculation of Tax Payable 5 Tables of Normal Tax Payable 6-7 Comparison of 2006

Tax data card 2013/2014

Tax data card 2013/2014 Contents Interest rates 1 Individuals and trusts 1 Companies 4 Capital allowances 5 Capital gains tax 6 Tax Administration Act penalties 7 Value-added tax 8 Other taxes, duties

Tax data card 2013/2014 Contents Interest rates 1 Individuals and trusts 1 Companies 4 Capital allowances 5 Capital gains tax 6 Tax Administration Act penalties 7 Value-added tax 8 Other taxes, duties

SA s rich likely to bear brunt of expected tax increases

Budget 2015 Background to budget SA s rich likely to bear brunt of expected tax increases Having already announced a raft of austerity measures five months into his position, Finance Minister Nhlanhla

Budget 2015 Background to budget SA s rich likely to bear brunt of expected tax increases Having already announced a raft of austerity measures five months into his position, Finance Minister Nhlanhla

training (pty) ltd Tax Guide

ltd Tax Guide") training (pty) ltd. 2016-2017 Tax Guide CONTENTS INCOME TAX RATES Natural person or special trust... 2 TAX REBATES Rebates for individuals... 2 Medical aid contributions and medical expenses... 2 TAX THRESHOLDS...

training (pty) ltd. 2016-2017 Tax Guide CONTENTS INCOME TAX RATES Natural person or special trust... 2 TAX REBATES Rebates for individuals... 2 Medical aid contributions and medical expenses... 2 TAX THRESHOLDS...

2018 BUDGET SAICA TAX COMMENTARY AND SUMMARY

2018 BUDGET SAICA TAX COMMENTAY AND SUMMAY CONTENTS 1. INTODUCTION... 3 2. BUDGET HIGHLIGHTS... 3 3. FOCUS ON IMPOVING TAX ADMINISTATION AND TAX MOALITY... 4 4. INDIVIDUALS AND TUSTS... 4 Personal income

2018 BUDGET SAICA TAX COMMENTAY AND SUMMAY CONTENTS 1. INTODUCTION... 3 2. BUDGET HIGHLIGHTS... 3 3. FOCUS ON IMPOVING TAX ADMINISTATION AND TAX MOALITY... 4 4. INDIVIDUALS AND TUSTS... 4 Personal income

Paper F6 (ZAF) Taxation (South Africa) Tuesday 4 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (South Africa) Tuesday 4 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (South Africa) Tuesday 4 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Fundamentals Level Skills Module Taxation (South Africa) Tuesday 4 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

- 2 - INCOME TAX RATES Rate of normal income tax on taxable income of any natural person or special trust: 2014/2015

TAX GUIDE 2014-2015 - 1 - CONTENTS INCOME TAX RATES, REBATES AND THRESHOLDS 2 WEAR AND TEAR ALLOWANCES General 3 Capital allowances 3 RESIDENCE BASIS OF TAXATION Resident 4 Non-resident 4 INTEREST AND

TAX GUIDE 2014-2015 - 1 - CONTENTS INCOME TAX RATES, REBATES AND THRESHOLDS 2 WEAR AND TEAR ALLOWANCES General 3 Capital allowances 3 RESIDENCE BASIS OF TAXATION Resident 4 Non-resident 4 INTEREST AND

ATX ZAF. Advanced Taxation South Africa (ATX ZAF) Strategic Professional Options. Tuesday 4 December 2018

Strategic Professional Options. Tuesday 4 December 2018") Strategic Professional Options Advanced Taxation South Africa (ATX ZAF) Tuesday 4 December 2018 ATX ZAF ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A

Strategic Professional Options Advanced Taxation South Africa (ATX ZAF) Tuesday 4 December 2018 ATX ZAF ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A

Financial and Taxation Directory 2006/2007

Financial and Taxation Directory 2006/2007 Cliffe Dekker is part of DLA Piper Group, an alliance of legal practices CONTENTS South African Taxation Highlights of the 2006/2007 Budget 2-5 Calculation of

Financial and Taxation Directory 2006/2007 Cliffe Dekker is part of DLA Piper Group, an alliance of legal practices CONTENTS South African Taxation Highlights of the 2006/2007 Budget 2-5 Calculation of

Paper P6 (ZAF) Advanced Taxation (South Africa) Thursday 10 December Professional Level Options Module

Advanced Taxation (South Africa) Thursday 10 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Thursday 10 December 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This question paper is divided into two sections:

Professional Level Options Module Advanced Taxation (South Africa) Thursday 10 December 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This question paper is divided into two sections:

Making l ght work? Taxometer 2015/2016

Making l ght work? Taxometer 2015/2016 Contents Individuals and trusts 1 Companies 4 Capital allowances 5 Capital gains tax 6 Tax Administration Act penalties 7 Value-added tax 8 Other taxes, duties and

Making l ght work? Taxometer 2015/2016 Contents Individuals and trusts 1 Companies 4 Capital allowances 5 Capital gains tax 6 Tax Administration Act penalties 7 Value-added tax 8 Other taxes, duties and

FINANCIAL & TAXATION. Directory 2017 / 2018

FINANCIAL & TAXATION Directory 2017 / 2018 BDO IN SOUTH AFRICA We are the South African member firm of BDO International. The global BDO network provides audit, tax and advisory services in 157 countries,

FINANCIAL & TAXATION Directory 2017 / 2018 BDO IN SOUTH AFRICA We are the South African member firm of BDO International. The global BDO network provides audit, tax and advisory services in 157 countries,

Statement issued by NUMSA National Executive Committee, February :

SARA BUDGET UPDATE Budget 2009/10 Statement issued by NUMSA National Executive Committee, February 18 2010: The National Union of Metal Workers of South Africa listened to the Budget Speech by the Minister

SARA BUDGET UPDATE Budget 2009/10 Statement issued by NUMSA National Executive Committee, February 18 2010: The National Union of Metal Workers of South Africa listened to the Budget Speech by the Minister

This booklet is published by PKF Publishers (Pty) Ltd for and on behalf of. chartered accountants & business advisers

Ltd for and on behalf of. chartered accountants & business advisers") BUDGET PROPOSALS 1 VAT Rate As from 1 April 2018, the VAT rate increases from 14% to 15%. 2 Donations Tax As from 1 March 2018, the rate increases to 25% for donations above R30 million. 3 Estate Duty

BUDGET PROPOSALS 1 VAT Rate As from 1 April 2018, the VAT rate increases from 14% to 15%. 2 Donations Tax As from 1 March 2018, the rate increases to 25% for donations above R30 million. 3 Estate Duty

% 28% funds Trusts 45% 45% Small Business Funding Entities 28% 28%

- 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 25 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS 2 Micro businesses 27

- 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 25 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS 2 Micro businesses 27

1 Strategising for growth BUDGET 2017/2018 SUMMARY OF MAJOR FEATURES Tax proposals Companies and close corporations The rate of normal tax remains

1 Strategising for growth BUDGET 2017/2018 SUMMARY OF MAJOR FEATURES Tax proposals Companies and close corporations The rate of normal tax remains unchanged at 28% in respect of years of assessment ending

1 Strategising for growth BUDGET 2017/2018 SUMMARY OF MAJOR FEATURES Tax proposals Companies and close corporations The rate of normal tax remains unchanged at 28% in respect of years of assessment ending

PAYE and Fringe benefit

PAYE and Fringe benefit 1 Definitions - Employer Par 1 Fourth Schedule Employer (Par 1 of Fourth Schedule ) Any person who pays or is liable to pay to any person any amount by way of remuneration. Including

PAYE and Fringe benefit 1 Definitions - Employer Par 1 Fourth Schedule Employer (Par 1 of Fourth Schedule ) Any person who pays or is liable to pay to any person any amount by way of remuneration. Including

SOUTH AFRICAN TAX GUIDE 2018/19

INDIVIDUAL - TAX ATES SOUTH AFICAN TAX GUIDE 2018/19 2015/16 Year of assessment ending 28 February 2019: Taxable Income 0-195 850 195 851-305 850 305 851-423 300 423 301-555 600 555 601-708 310 708 311-1

INDIVIDUAL - TAX ATES SOUTH AFICAN TAX GUIDE 2018/19 2015/16 Year of assessment ending 28 February 2019: Taxable Income 0-195 850 195 851-305 850 305 851-423 300 423 301-555 600 555 601-708 310 708 311-1

TAX PROFESSIONAL OCCUPATIONAL CERTIFICATE: Initial Test of Competency RPL Assessment SAQA ID: July Paper 1: Questions 1 and 2 SOLUTIONS

OCCUPATIONAL CERTIFICATE: TAX PROFESSIONAL SAQA ID: 93624 Initial Test of Competency RPL Assessment July 207 Paper : Questions and 2 SOLUTIONS CANDIDATE NUMBER Instructions to Candidates. This competency

OCCUPATIONAL CERTIFICATE: TAX PROFESSIONAL SAQA ID: 93624 Initial Test of Competency RPL Assessment July 207 Paper : Questions and 2 SOLUTIONS CANDIDATE NUMBER Instructions to Candidates. This competency

WESTERN CAPE De Waterkant Building 10 Helderberg Street Stellenbosch PO Box 920 Stellenbosch 7599

DIRECTORS Pieter-Jan Bestbier, Jock de Jager, André du Plessis, Fran du Plessis, Jana Goosen, Francois Joubert, Iaan Marx, Stephan Pretorius, Lehandi Swanepoel, Johann van Rensburg, Erlo Vos. WESTERN CAPE

DIRECTORS Pieter-Jan Bestbier, Jock de Jager, André du Plessis, Fran du Plessis, Jana Goosen, Francois Joubert, Iaan Marx, Stephan Pretorius, Lehandi Swanepoel, Johann van Rensburg, Erlo Vos. WESTERN CAPE

University of Pretoria. LEARNING AREA 6: Fringe Benefits Lecture 38-41

University of Pretoria LEARNING AREA 6: Fringe Benefits Lecture 38-41 1 Recap Due to the nature of Simpiwe s work, he travels to clients quite often as he needs to audit on site. Simpiwe stays 10km from

University of Pretoria LEARNING AREA 6: Fringe Benefits Lecture 38-41 1 Recap Due to the nature of Simpiwe s work, he travels to clients quite often as he needs to audit on site. Simpiwe stays 10km from

It is proposed to delink the diesel refund from the VAT system. Due to the significant disputes over record-keeping, clarity will be provided.

Tax Guide 2015/2016 BUDGET PROPOSALS 1 Medical Expense Tax Credit To alleviate the burden for taxpayers older than 65 years, it is proposed that the medical expense tax credit be taken into account for

Tax Guide 2015/2016 BUDGET PROPOSALS 1 Medical Expense Tax Credit To alleviate the burden for taxpayers older than 65 years, it is proposed that the medical expense tax credit be taken into account for

CENTRE O F TAX EXCELLENCE TAX GUIDE 2014 / 15.

CENTRE O F TAX EXCELLENCE TAX GUIDE 2014 / 15 www.saipa.co.za TAX GUIDE 2014/15 CONTENTS BUDGET SUMMARY...4 RESIDENCE BASIS TAXATION... 7 Tax Rates: Individuals... 9 Tax rates: Trusts... 9 Tax rates: Companies...

CENTRE O F TAX EXCELLENCE TAX GUIDE 2014 / 15 www.saipa.co.za TAX GUIDE 2014/15 CONTENTS BUDGET SUMMARY...4 RESIDENCE BASIS TAXATION... 7 Tax Rates: Individuals... 9 Tax rates: Trusts... 9 Tax rates: Companies...

Wealth Associates. TAX Guide 2019/20 Tax year. Independence. Continuity. Value.

Wealth Associates TAX Guide 2019/20 Tax year Independence. Continuity. Value. Independence. Continuity. Value. BUDGET PROPOSALS 1 Personal Income Tax The personal income tax brackets have not been changed.

Wealth Associates TAX Guide 2019/20 Tax year Independence. Continuity. Value. Independence. Continuity. Value. BUDGET PROPOSALS 1 Personal Income Tax The personal income tax brackets have not been changed.

TAXATION IN SOUTH AFRICA 2016/7

Retirement Fund March 2016 TAXATION IN SOUTH AFRICA 2016/7 Your Retirement - Our Passion Sentinel Retirement Fund Reg No 12/8/1215 Sentinel House 1 Sunnyside Drive Sunnyside Park PARKTOWN 2193 P O Box

Retirement Fund March 2016 TAXATION IN SOUTH AFRICA 2016/7 Your Retirement - Our Passion Sentinel Retirement Fund Reg No 12/8/1215 Sentinel House 1 Sunnyside Drive Sunnyside Park PARKTOWN 2193 P O Box

International Tax South Africa Highlights 2018

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

Discussion Points 1. Tax Treatment of Group Risk Contributions 2. Tax Treatment of Retirement Fund Contributions 3. What will Retirement Funds and Gro

The Evolving Landscape of Retirement Funds and Group Risk Schemes in SA Discussion Points 1. Tax Treatment of Group Risk Contributions 2. Tax Treatment of Retirement Fund Contributions 3. What will Retirement

The Evolving Landscape of Retirement Funds and Group Risk Schemes in SA Discussion Points 1. Tax Treatment of Group Risk Contributions 2. Tax Treatment of Retirement Fund Contributions 3. What will Retirement

Paper F6 (ZAF) Taxation (South Africa) Thursday 8 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (South Africa) Thursday 8 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (South Africa) Thursday 8 December 2016 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

Fundamentals Level Skills Module Taxation (South Africa) Thursday 8 December 2016 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

Tax Guide

2017-2018 Tax Guide - 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 24 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS

2017-2018 Tax Guide - 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 24 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS

Paper P6 (ZAF) Advanced Taxation (South Africa) Friday 15 June Professional Level Options Module

Advanced Taxation (South Africa) Friday 15 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Friday 15 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Professional Level Options Module Advanced Taxation (South Africa) Friday 15 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

chartered accountants & business advisers TAX GUIDE 2011/2012 right size. right people. right answers.

chartered accountants & business advisers TAX GUIDE 2011/2012 right size. right people. right answers. INDEPENDENT OFFICES IN SOUTHERN AFRICA SOUTH AFRICA Bloemfontein 46 First Avenue Westdene 9301 Tel

chartered accountants & business advisers TAX GUIDE 2011/2012 right size. right people. right answers. INDEPENDENT OFFICES IN SOUTHERN AFRICA SOUTH AFRICA Bloemfontein 46 First Avenue Westdene 9301 Tel

BGR DE JAGER BOSHOFF BGR DE VILLIERS BGR PYPER TURNER BGR ALLUVIUM TAX GUIDE BGR BROODRYK KOTZÉ BGR JACOBS GRIESSEL

TAX GUIDE 2018 2019 2018 2019 SERVICES PROVIDED: AUDIT AND ASSURANCE Statutory Audit and other assurance engagements Agreed upon procedures Due Diligence Investigations Design, implementation and review

TAX GUIDE 2018 2019 2018 2019 SERVICES PROVIDED: AUDIT AND ASSURANCE Statutory Audit and other assurance engagements Agreed upon procedures Due Diligence Investigations Design, implementation and review

Progression & Stability

Progression & Stability Navigate your next step Budget 2018/9 Tax Guide kpmg.co.za 1 Turning data and knowledge into value across a client s organisation. Harnessing the power of technology and unlocking

Progression & Stability Navigate your next step Budget 2018/9 Tax Guide kpmg.co.za 1 Turning data and knowledge into value across a client s organisation. Harnessing the power of technology and unlocking

OCCUPATIONAL CERTIFICATE: TAX TECHNICIAN SAQA ID: Knowledge Competency Assessment. November 2016 Paper 1 CANDIDATE NUMBER.

OCCUPATIONAL CERTIFICATE: TAX TECHNICIAN SAQA ID: 94098 Knowledge Competency Assessment November 2016 Paper 1 CANDIDATE NUMBER P a g e 1 P a g e 2 Instructions to Candidates 1. This competency assessment

OCCUPATIONAL CERTIFICATE: TAX TECHNICIAN SAQA ID: 94098 Knowledge Competency Assessment November 2016 Paper 1 CANDIDATE NUMBER P a g e 1 P a g e 2 Instructions to Candidates 1. This competency assessment

Responsible 2015/6 BUDGET WATCH GAP. for the Common Good. KPMG s 2016 BudgetWatch. kpmg.co.za

MIND Responsible KPMG S 2015/6 THEWITH BUDGET WATCH Tax GAP for the Common Good KPMG s 2016 BudgetWatch Tax With Reference KPMG s Guide 2016/7Tax Guide kpmg.co.za African Tax Solution Centre Yes, we have

MIND Responsible KPMG S 2015/6 THEWITH BUDGET WATCH Tax GAP for the Common Good KPMG s 2016 BudgetWatch Tax With Reference KPMG s Guide 2016/7Tax Guide kpmg.co.za African Tax Solution Centre Yes, we have

EXPLANATORY MEMORANDUM

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

YPNO[ WLVWSL YPNO[ ZPaL YPNO[ ZVS\[PVUZ YEARS C H A N TA N. t D AV I D S T A RS ;H_.\PKL

95 AY YE A RS 19 7 Rt 5 01 N &T R ED R TE TS C H A N TA N OU RS ACC U D ITO ) &A (S A CA BAN DUR -2 HA AC LO t D AV I D S T YEARS R 9 YPNO[ WLVWSL YPNO[ ZPaL YPNO[ ZVS\[PVUZ 22 1922-2017 ;H_.\PKL BUDGET

95 AY YE A RS 19 7 Rt 5 01 N &T R ED R TE TS C H A N TA N OU RS ACC U D ITO ) &A (S A CA BAN DUR -2 HA AC LO t D AV I D S T YEARS R 9 YPNO[ WLVWSL YPNO[ ZPaL YPNO[ ZVS\[PVUZ 22 1922-2017 ;H_.\PKL BUDGET