2017 Employees & Payroll Withholding

|

|

|

- Gabriel Austin

- 6 years ago

- Views:

Transcription

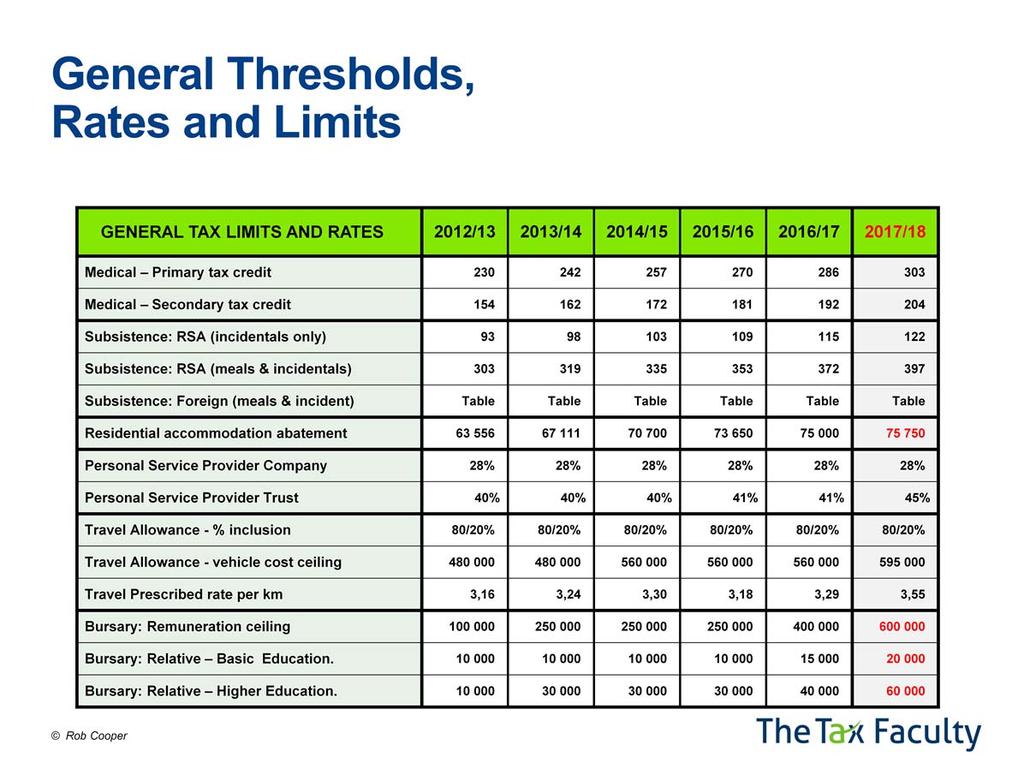

1 2017 Employees & Payroll Withholding Presented by Rob Cooper Rob Cooper is the Director of Legislation at Sage VIP Payroll & HR. As one of the company s founders, he has an in-depth understanding of the impact of legislation on the HR and payroll software industry. Over the last 20 years, his focus has been on the diverse legislation that governs the employment and payroll industry. Rob is a founding member and the current chairman of the Payroll Authors Group of South Africa, a body that liaises with statutory bodies on behalf of payroll system suppliers, and is a respected presenter at seminars and workshops around the country.

2 Programme: 08:15 08:55 Registration 09:00 10: Employees & Payroll Withholding 10:30 10:50 Tea Break (20 mins) 10:50 13: Employees & Payroll Withholding 13:00 Conclusion

3 0

4 1

5 2

6 3

7 4

8 5

9 6

10 7

11 27. Section 11 of the Income Tax Act, 1962, is hereby amended (b) by the substitution in paragraph (i)(bb)of the proviso to paragraph (k) for item (B) of the following item: (B) taxable income (other than in respect of any retirement fund lump sum benefit, retirement fund lump sum withdrawal benefit and severance benefit) as determined before allowing any deduction under this paragraph and section 18A; ; and (c) by the addition in to the proviso to paragraph (k) after paragraph (iv) of the following paragraph: (v) any deduction in terms of this paragraph must apply for the purpose of determining the total amount of taxable income, before any deduction in terms of section 18A or the inclusion of any taxable capital gain of the person, whether derived from the carrying on of any trade or otherwise;. 8

12 The amendment to paragraph 12D of the Seventh Schedule: (b) by the substitution in subparagraph (1) in the definition of retirement funding income for paragraph (a) of the following paragraph: (a) in relation to any employee or the holder of an office (including a member of a body of persons whether or not established by or in terms of any law) who in respect of his or her employment derives any income constituting remuneration as defined in paragraph 1 of the Fourth Schedule and who is a member of or, as an employee, contributes to a pension fund or provident fund established for the benefit of employees of the employer, from whom such income is derived, [that part of the employee s said income as] the income that is taken into account in the determination of the contributions made by the employer or the pension fund or provident fund for the benefit of the employee to such pension fund or provident fund in terms of the rules of the fund; or. 9

13 Section 11(k)(i) Deduction for contributions to any retirement fund: The total deduction to be allowed in terms of this paragraph must not in the year of assessment exceed the lesser of (aa) R ; or (bb) 27,5% of

14 11

15 Settling-in Relocation expenses in the Future If the employer agrees to assist with any one or more of the three categories of relocation expenses (transport, settling-in and alternative accommodation), there are three options 1. Pay the suppliers directly (no fringe benefit because these expenses are exempt) 2. Reimburse the employee if the employee has paid directly and supplies proof of the expenses 3. Pay a taxable relocation allowance and report as code 3713 (Taxable Allowance). Employees who pay for these expenses directly cannot claim them on assessment there is no deduction provision available. 12

16 13

17 The Formula method uses the formula: (A B) x C/100 x D/12 Where: A = the remuneration proxy B = R (the tax threshold for an under 65 year old taxpayer for 2015) C = 17 unless the accommodation consists of at least 4 rooms and - = 18 if unfurnished and power or fuel is supplied by the employer = 18 if furnished and no power or fuel is supplied by the employer = 19 if furnished and power or fuel is supplied by the employer D = the number of months that the employee is entitled to the accommodation Use the lesser of the Formula method and the Expenditure method if - o the full ownership of the accommodation does not vest in the employer, and o the employer provides accommodation obtained at arm s length from an unconnected person 14

18 Tax Certificate codes for Bursaries Both the exempt and the non-exempt portion of the bursary must be in the payroll for the fringe benefit calculation of the portion that was not exempted, and for tax certificate reporting Code 3809 (Basic education bursary taxable) Code 3815 (Basic education bursary non-taxable) Code 3820 (Higher education bursary taxable) Code 3821 (Higher education bursary non-taxable). 15

19 16

20 Note In order to evaluate the learnership incentive more effectively in the future, National Treasury and SARS are discussing the best way in which to collect more information on claims and learners. The intention is to make this reporting compulsory for claimants of the learnership tax incentive. When the Unemployment Insurance Amendment Act becomes effective (see discussion in a later Chapter in this workbook), contributions will have to be paid for all learners, and these individuals will then be able to claim unemployment benefits. 17

21 18

22 An equity instrument is defined in section 8C(7) as: " a share or member's interest in a company, and includes- an option to acquire such share, part of a share or member's interest; any financial instrument that is convertible to a share or member's interest; and any contractual right or obligation the value of which is determined directly or indirectly with reference to a share or member's interest" A restricted equity instrument is an: Equity instrument that is restricted in a manner that prevents the individual from freely disposing of that equity instrument at market value, or which is not deliverable to the taxpayer until a specified event is satisfied. 19

23 The underlying problem as described by the Explanatory Memorandum: Section 8C is based on the implicit assumption that the full value of the equity shares underlying a restricted equity instrument will vest in the employee when the restrictions fall away. 20

24 Section 10(1)(k)(i) exempts dividends from income tax (in which case they are subject to a dividends tax of 15% (20% from 22 February 2017)), but a proviso excludes nine categories of dividends from exemption. By no longer being exempt from income, these nine categories of dividends are therefore included in income and subject to income tax. Three of the nine categories of dividends have now been added to the definition of remuneration: Any amount received by or accrued to that person by way of a dividend contemplated in- (i) paragraph (dd) of the proviso to section 10(1)(k)(i); (ii) paragraph (ii) of the proviso to section 10(1)(k)(i); (iii) paragraph (jj) of the proviso to section 10(1)(k)(i); The three categories of dividends that are now included in remuneration are paragraphs (dd), (ii) and (jj) of the proviso to section 10(1)(k)(i). 21

25 Key questions to ask to determine if there is a risk of possible dividend inclusion in remuneration 1. Are the dividends being paid on non-equity shares or hybrid equity instruments, or to beneficiaries of a trust holding such shares or instruments? 2. Are the dividends being paid in respect of employment to persons holding anything other than shares or restricted equity instruments? 3. Are the dividends being paid to the holders of restricted equity instruments, and those dividends relate to a share buy-back or redemption, or a company winding up? 4. Is the dividend being paid in the form of an equity instrument? If you answer yes to any of these questions, then you will need to consider the rules very carefully, as the dividend may be subject to PAYE instead of dividends tax. This needs to be picked up early, so that dividends tax is not deducted from the payment of the dividend. The above rules provided courtesy of Dan Foster, who is a director of Webber Wentzel Attorneys 22

26 23

27 SARS BGR 40: Independence is central to the NED s role and is interpreted to mean the absence of undue influence and bias. The independent role of the NED results in SARS considering an NED to be a director who is not involved in the daily management or operations of a company, but simply attends, provides objective judgment, and votes at board meetings. Income Tax Act definition: director, in relation to a close corporation, means any person who in respect of such close corporation holds any office or performs any functions similar to the office or functions of a director of a company other than a close corporation; 24

28 remuneration means any amount of income which is paid or is payable to any person by way of any salary, leave pay, wage, overtime pay, bonus, gratuity, commission, fee, etc. but not including any amount paid in respect of services rendered by any person (other than a person who is not a resident ) in the course of any trade carried on by him independently of the person by whom such amount is paid : Provided that a person shall not be deemed to carry on a trade independently if the services are required to be performed mainly at the premises of the person by whom such amount is paid and the person who rendered the services is subject to the control or supervision of any other person as to the manner in which his or her duties are performed or as to his hours of work: Provided further 25

29 Fourth Schedule Employee Definition: employee means (a) any person who receives any remuneration (g) any director of a private company who is not included in terms of paragraph (a); 26

30 Fourth Schedule Employee Definition: employee means (a) any person who receives any remuneration (g) any director of a private company who is not included in terms of paragraph (a); 27

31 Note the following when planning the implementation of the requirements of the BGRs - 1. NEDs who accounted for VAT prior to 1 st June 2017: If PAYE was withheld, can review their PAYE withholding before 28 th February If PAYE was not withheld, need take no action this is correct in terms of the BGRs. 2. NEDs who did not account for VAT prior to 1 st June 2017 and who should have: If PAYE was withheld, NEDs will not be required to account for VAT in respect of director s fees received prior to 1 June 2017 (SARS notice on 14 th February 2016). If PAYE was not withheld, it was not clear at the time of writing whether SARS will take action retrospectively. With this last uncertainty in mind, NEDs and their employers must decide whether or not to start PAYE withholding until 1 June 2017 (the NED can request voluntary withholding of PAYE), as this will ensure that the NED will not be penalised for not accounting for VAT. 28

32 29

33 (a) where an employer employs and pays remuneration to a qualifying employee for at least 160 hours in a month, means the amount paid or payable to the qualifying employee by the employer in respect of a month; or (b) where an employer employs a qualifying employee and pays remuneration to that employee for less than 160 hours in a month, means an amount calculated in terms of section 7(5);. (i) where the employee is employed and paid remuneration for at least 160 hours in a month, the amount of R2 000 in respect of a month; or (ii) where the employee is employed and paid remuneration for less than 160 hours in a month, an amount that bears to the amount of R2 000 the same ratio as 160 hours bears to the number of hours that the employee was employed for by that employer in that month.. 30

34 If the payroll is processed monthly, then for permanent employees, the employed hours should be the average working hours per month. For example for a 40-hour week, the average hours per month are 173 hours (8 x 5 x 4,33 = 173,33). For a 45-hour week, they are 195 hours (45 x 4,3333). Note that the method of calculating the average working hours per month is based on section 35(3) of the Basic Conditions of Employment Act that specifies that the ratio between weeks and months is four and one-third on average over a year (mathematically this factor is calculated by dividing 52 weeks by 12 months). If the payroll is processed weekly or fortnightly, then for permanent employees, the employed hours are the number of hours per week multiplied by the number of weeks in the month. The principle is that it is the number of weeks in the month that determines the total amount paid for the month. For an 8-hour day, 5-day week employment arrangement, the employed hours per month will be: 160 hours (for a 4-week month) 200 hours (for a 5-week month). 31

35 The Basic Conditions of Employment Act defines wage as: the amount of money paid or payable to an employee in respect of ordinary hours of work or, if they are shorter, the hours an employee ordinarily works in a day or week; 32

36 33

37 34

38 35

39 36

40 37

41 38

42 39

43 40

44 41

45 42

40% in 2003 (for 13 years) 41% in 2016 (for 1 years) 45% in 2017 (for?")

46 The history of changes to the top personal tax marginal rate: 50% in 1987 (for 12 years) 45% in 1999 (for four years) 40% in 2003 (for 13 years) 41% in 2016 (for 1 years) 45% in 2017 (for? years ) 43

47 44

48 45

49 46

50 47

51 48

52 49

Tax and ETI Amendments 2017/2018

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

18% of taxable income % of taxable income above % of taxable income above

Important Note If your Sage One Payroll software is already in March 2016, your year-to-date amounts will recalculate when you do a start of period into April, unless you make any changes on an employee

Important Note If your Sage One Payroll software is already in March 2016, your year-to-date amounts will recalculate when you do a start of period into April, unless you make any changes on an employee

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

Tax, ETI and UIF Amendments 2018/2019

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

PAYROLL TAX POCKET GUIDE. A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa.

PAYROLL TAX POCKET GUIDE 2019 2020 A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside

PAYROLL TAX POCKET GUIDE 2019 2020 A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON ACCOMMODATION

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

South African Reward Association. Tax Update Budget 2018/19

South African Reward Association Tax Update Budget 2018/19 Events Tax and Cost to Company Workshop What happens after package determined (art vs. science) 14 & 15 August 2018 - Johannesburg Tax Morality

South African Reward Association Tax Update Budget 2018/19 Events Tax and Cost to Company Workshop What happens after package determined (art vs. science) 14 & 15 August 2018 - Johannesburg Tax Morality

Payroll Tax Pocket Guide 2017/18

Payroll Tax Pocket Guide 2017/18 A complete reference guide covering legislative matters that affect the HR & payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside RSA

Payroll Tax Pocket Guide 2017/18 A complete reference guide covering legislative matters that affect the HR & payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside RSA

D-BIT Payroll. Employees Remuneration for UIF, SDL, PAYE. D-BIT SYSTEMS (Pty) Ltd D-BIT Systems (Pty) Ltd) 2/24/2012, 3:18 PM

Ltd D-BIT Systems (Pty) Ltd) 2/24/2012, 3:18 PM") D-BIT SYSTEMS (Pty) Ltd RegNo: 87/033407 D-Bit Building 18 Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 156 South Africa D-BIT Payroll Employees for UIF, SDL, PAYE 01... D-BIT Systems (Pty)

D-BIT SYSTEMS (Pty) Ltd RegNo: 87/033407 D-Bit Building 18 Bosbok Rd Boskruin South Africa PO Box 1950 Randpark Ridge 156 South Africa D-BIT Payroll Employees for UIF, SDL, PAYE 01... D-BIT Systems (Pty)

EXPLANATORY MEMORANDUM

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 2 EXPLANATORY MEMORANDUM ON THE UNEMPLOYMENT INSURANCE CONTRIBUTIONS BILL, 2001 Currently, the unemployment

Payroll Pocket Guide. as at March A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa

Payroll Pocket Guide as at March 2013 A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa Quick Reference Subsistence Allowance Travel inside RSA

Payroll Pocket Guide as at March 2013 A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa Quick Reference Subsistence Allowance Travel inside RSA

University of Pretoria. LEARNING AREA 6: Fringe Benefits Lecture 38-41

University of Pretoria LEARNING AREA 6: Fringe Benefits Lecture 38-41 1 Recap Due to the nature of Simpiwe s work, he travels to clients quite often as he needs to audit on site. Simpiwe stays 10km from

University of Pretoria LEARNING AREA 6: Fringe Benefits Lecture 38-41 1 Recap Due to the nature of Simpiwe s work, he travels to clients quite often as he needs to audit on site. Simpiwe stays 10km from

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY Foreword This document is a general guide dealing with the PAYE responsibility

GUIDE ON THE EMPLOYEES' TAX RESPONSIBILITIES REGARDING CREW IN THE BROADCAST, TECHNICAL PRODUCTION & LIVE EVENTS INDUSTRY Foreword This document is a general guide dealing with the PAYE responsibility

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2018 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 13 Page 1 of 56 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

Tax tables 2019/2020 (year of assessment ending 29 February 2020)

") BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

BUDGET SPEECH 2019/2020 ALL YOU NEED TO KNOW Tax tables 2019/2020 (year of assessment ending 29 February 2020) Income tax: Individuals and special trusts Taxable income Rates of tax 0-195 850 18 % of taxable

REPUBLIC OF SOUTH AFRICA

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

IN RESPECT OF FRINGE BENEFITS

GUIDE FOR EMPLOYERS IN RESPECT OF (2016 TAX YEAR) 1 PURPOSE 3 2 SCOPE 3 3 OBLIGATIONS OF THE EMPLOYER 3 4 BENEFITS GRANTED TO RELATIVES OF EMPLOYEES AND OTHERS 4 5 TAXABLE BENEFITS 4 5.1 ACQUISITION OF

GUIDE FOR EMPLOYERS IN RESPECT OF (2016 TAX YEAR) 1 PURPOSE 3 2 SCOPE 3 3 OBLIGATIONS OF THE EMPLOYER 3 4 BENEFITS GRANTED TO RELATIVES OF EMPLOYEES AND OTHERS 4 5 TAXABLE BENEFITS 4 5.1 ACQUISITION OF

PAYE and Fringe benefit

PAYE and Fringe benefit 1 Definitions - Employer Par 1 Fourth Schedule Employer (Par 1 of Fourth Schedule ) Any person who pays or is liable to pay to any person any amount by way of remuneration. Including

PAYE and Fringe benefit 1 Definitions - Employer Par 1 Fourth Schedule Employer (Par 1 of Fourth Schedule ) Any person who pays or is liable to pay to any person any amount by way of remuneration. Including

Government Gazette REPUBLIC OF SOUTH AFRICA

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 511 Cape Town 8 January 2008 No. 30656 THE PRESIDENCY No. 39 8 January 2008 It is hereby notified that the President has assented to the following Act,

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 511 Cape Town 8 January 2008 No. 30656 THE PRESIDENCY No. 39 8 January 2008 It is hereby notified that the President has assented to the following Act,

REPUBLIC OF SOUTH AFRICA DRAFT EXPLANATORY MEMORANDUM ON THE TAXATION LAWS AMENDMENT BILL, July 2014

REPUBLIC OF SOUTH AFRICA DRAFT EXPLANATORY MEMORANDUM ON THE TAXATION LAWS AMENDMENT BILL, 2014 17 July 2014 [W.P. - 14] 1 TABLE OF CONTENTS EXPLANATION OF MAIN AMENDMENTS 1. INCOME TAX: INDIVIDUALS, SAVINGS

REPUBLIC OF SOUTH AFRICA DRAFT EXPLANATORY MEMORANDUM ON THE TAXATION LAWS AMENDMENT BILL, 2014 17 July 2014 [W.P. - 14] 1 TABLE OF CONTENTS EXPLANATION OF MAIN AMENDMENTS 1. INCOME TAX: INDIVIDUALS, SAVINGS

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee.

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee. Q How can PAYE be deducted from an accrual? Income that accrues in one tax

PAYE must be deducted by an employer from remuneration paid to an employee when the income accrues or is paid to the employee. Q How can PAYE be deducted from an accrual? Income that accrues in one tax

TAXATION LAWS AMENDMENT BILL

REPUBLIC OF SOUTH AFRICA TAXATION LAWS AMENDMENT BILL (As introduced in the National Assembly (proposed section 77)) (The English text is the offıcial text of the Bill) (MINISTER OF FINANCE) [B 13 14]

REPUBLIC OF SOUTH AFRICA TAXATION LAWS AMENDMENT BILL (As introduced in the National Assembly (proposed section 77)) (The English text is the offıcial text of the Bill) (MINISTER OF FINANCE) [B 13 14]

DRAFT TAXATION LAWS AMENDMENT BILL

DRAFT TAXATION LAWS AMENDMENT BILL RELEASE The draft Taxation Laws Amendment Bill, 2014, is hereby published for comment. The draft legislation gives effect to matters presented by the Minister of Finance

DRAFT TAXATION LAWS AMENDMENT BILL RELEASE The draft Taxation Laws Amendment Bill, 2014, is hereby published for comment. The draft legislation gives effect to matters presented by the Minister of Finance

RE: CALL FOR COMMENT: DRAFT TAXATION LAWS AMENDMENT BILL ( TLAB )

") 5 August 2013 Ms N. Mpotulo The National Treasury 240 Vermuelen Street PRETORIA 0001 Ms A. Collins Legal & Policy The South African Revenue Service Lehae La SARS PRETORIA 8000 BY E-MAIL: nomfanelo.mpotulo@treasury.gov.za

5 August 2013 Ms N. Mpotulo The National Treasury 240 Vermuelen Street PRETORIA 0001 Ms A. Collins Legal & Policy The South African Revenue Service Lehae La SARS PRETORIA 8000 BY E-MAIL: nomfanelo.mpotulo@treasury.gov.za

SAPA - ANNUAL PAYE UPDATE BREAKFAST, Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014

SAPA - ANNUAL PAYE UPDATE BREAKFAST, 2014 Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014 Content Chapter 4 Annexure C Davis Tax Review Committee Miscellaneous 1 Content: Chapter

SAPA - ANNUAL PAYE UPDATE BREAKFAST, 2014 Johannesburg 28 February 2014 Durban 4 March 2014 Cape Town 6 March 2014 Content Chapter 4 Annexure C Davis Tax Review Committee Miscellaneous 1 Content: Chapter

ND Employment-related taxes

71 ND Employment-related taxes Contents Introductory provision ND 1 What this subpart does PAYE rules and PAYE payments Introductory provisions ND 2 ND 3 ND 4 ND 5 PAYE rules and their application PAYE

71 ND Employment-related taxes Contents Introductory provision ND 1 What this subpart does PAYE rules and PAYE payments Introductory provisions ND 2 ND 3 ND 4 ND 5 PAYE rules and their application PAYE

REPUBLIC OF SOUTH AFRICA

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2017 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 TABLE OF CONTENTS 1 2 3 4 5 5.1 5.2 5.3 5.4 6 6.1 6.2 7 7.1 7.2

Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016

No. 3 of 2017 February 2017 Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016 A. The Taxation Laws Amendment Act No. 15 of 2016 was promulgated in Government Gazette No. 40562 on 19 January 2017.

No. 3 of 2017 February 2017 Taxation Laws Amendment Acts No. 15 of 2016 & 16 of 2016 A. The Taxation Laws Amendment Act No. 15 of 2016 was promulgated in Government Gazette No. 40562 on 19 January 2017.

TAX UPDATE SEMINAR APRIL / MAY 2017

TAX UPDATE SEMINAR APRIL / MAY 2017 OVERVIEW Budget Speech Chapter 4 and Annexure C. Recent Rulings. Taxation Laws Amendment Act, 2016 ( 2016 TLA ). Recent Case Law. Amendments set out in Tax Administration

TAX UPDATE SEMINAR APRIL / MAY 2017 OVERVIEW Budget Speech Chapter 4 and Annexure C. Recent Rulings. Taxation Laws Amendment Act, 2016 ( 2016 TLA ). Recent Case Law. Amendments set out in Tax Administration

GOVERNMENT GAZETTE OF THE REPUBLIC OF NAMIBIA. N$2.00 WINDHOEK - 30 April 2010 No Parliament Government Notice

GOVERNMENT GAZETTE OF THE REPUBLIC OF NAMIBIA N$2.00 WINDHOEK - 30 April 2010 No. 4475 CONTENTS Page GOVERNMENT NOTICE No. 87 Promulgation of Income Tax Amendment Act, 2010 (Act No. 5 of 2010), of the

GOVERNMENT GAZETTE OF THE REPUBLIC OF NAMIBIA N$2.00 WINDHOEK - 30 April 2010 No. 4475 CONTENTS Page GOVERNMENT NOTICE No. 87 Promulgation of Income Tax Amendment Act, 2010 (Act No. 5 of 2010), of the

International Tax South Africa Highlights 2018

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR)

") EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

EXTERNAL GUIDE GUIDE FOR EMPLOYERS IN RESPECT OF EMPLOYEES TAX (2016 TAX YEAR) GUIDE FOR EMPLOYERS IN RESPECT OF Revision 12 Page 1 of 55 PAYE-GEN-01-G10 TABLE OF CONTENTS 1 2 3 4 5 QUICK REFERENCE CARD

Government Gazette REPUBLIC OF SOUTH AFRICA

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 4 Cape Town 2 November No. 33726 STATE PRESIDENT'S OFFICE No. 24 2 November It is hereby notified that the President has assented to the following Act,

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 4 Cape Town 2 November No. 33726 STATE PRESIDENT'S OFFICE No. 24 2 November It is hereby notified that the President has assented to the following Act,

Government Gazette REPUBLIC OF SOUTH AFRICA. Vol. 475 Cape Town 24 January 2005 No

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 475 Cape Town 24 January 2005 No. 27188 THE PRESIDENCY No. 46 24 January 2005 It is hereby notified that the President has assented to the following Act,

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 475 Cape Town 24 January 2005 No. 27188 THE PRESIDENCY No. 46 24 January 2005 It is hereby notified that the President has assented to the following Act,

South African Reward Associa3on

South African Reward Associa3on Budget Update 2012 Tax Law Changes 01 March 2012 Ac3on List for 2012 Jerry Botha jerry@taxconsul3ng.co.za 082 899 6118 Landscape 1999/2000 = 579 Pages Since then = 1,868

South African Reward Associa3on Budget Update 2012 Tax Law Changes 01 March 2012 Ac3on List for 2012 Jerry Botha jerry@taxconsul3ng.co.za 082 899 6118 Landscape 1999/2000 = 579 Pages Since then = 1,868

Quick Start Guide to Payroll Tax Year-End

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

E-Book Quick Start Guide to Payroll Tax Year-End Best practices for preparing, processing, and planning year-end payroll activity Contents Introduction Phase 1: Preparing for Tax Year-End Phase 2: Processing

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

NEWS FLASH - February 2016

NEWS FLASH - February 2016 Africa: South Africa CRS TAX POCKET GUIDE 2016/2017 it is important that Employers note the following TAX RATES (TAX YEAR ENDING 28 FEBRUARY 2017) Individuals and special trusts

NEWS FLASH - February 2016 Africa: South Africa CRS TAX POCKET GUIDE 2016/2017 it is important that Employers note the following TAX RATES (TAX YEAR ENDING 28 FEBRUARY 2017) Individuals and special trusts

THE PRESIDENCY. No June 2001

THE PRESIDENCY No. 550 20 June 2001 It is hereby notified that the Acting President has assented to the following Act which is hereby published for general information: - NO. 5 OF 2001: TAXATION LAWS AMENDMENT

THE PRESIDENCY No. 550 20 June 2001 It is hereby notified that the Acting President has assented to the following Act which is hereby published for general information: - NO. 5 OF 2001: TAXATION LAWS AMENDMENT

2017 Budget and Tax Update

2017 Budget and Tax Update Presented by Nico Theron MTP(SA), BCom Law (cum laude), BCom Honours Taxation, MCom Taxation (SA and International Tax) Nico, a partner at Tax Consulting South Africa, has been

2017 Budget and Tax Update Presented by Nico Theron MTP(SA), BCom Law (cum laude), BCom Honours Taxation, MCom Taxation (SA and International Tax) Nico, a partner at Tax Consulting South Africa, has been

Taxation (F6) Lesotho (LSO) June & December 2017

Lesotho (LSO) June & December 2017") Taxation (F6) Lesotho (LSO) June & December 2017 This syllabus and study guide is designed to help with planning study and to provide detailed information on what could be assessed in any examination session.

Taxation (F6) Lesotho (LSO) June & December 2017 This syllabus and study guide is designed to help with planning study and to provide detailed information on what could be assessed in any examination session.

Retirement Annuity Fund

Retirement Annuity Fund Background information... 3 Purpose... 3 Benefits of investing in a RA... 5 Definitions... 5 Member... 5 Nominee... 5 Dependant... 6 Beneficiary... 6 General information... 6 Registration...

Retirement Annuity Fund Background information... 3 Purpose... 3 Benefits of investing in a RA... 5 Definitions... 5 Member... 5 Nominee... 5 Dependant... 6 Beneficiary... 6 General information... 6 Registration...

INCOME TAX WORKSHOP Taxation of Individuals Presenter: Francis Kamau

INCOME TAX WORKSHOP Taxation of Individuals Friday, 7 th April 2017 Presenter: Francis Kamau Employee taxes Chargeable income For the purposes of section 3(2)(a)(ii), an amount paid to- a person who is,

INCOME TAX WORKSHOP Taxation of Individuals Friday, 7 th April 2017 Presenter: Francis Kamau Employee taxes Chargeable income For the purposes of section 3(2)(a)(ii), an amount paid to- a person who is,

Contents. Application INCOME TAX INTERPRETATION BULLETIN. INCOME TAX ACT Retiring Allowances

INCOME TAX INTERPRETATION BULLETIN NO.: IT-337R4 (Consolidated) DATE: February 1, 2006 SUBJECT: REFERENCE: INCOME TAX ACT Retiring Allowances Paragraph 60(j.1), subparagraph 56(1)(a)(ii) and the definition

INCOME TAX INTERPRETATION BULLETIN NO.: IT-337R4 (Consolidated) DATE: February 1, 2006 SUBJECT: REFERENCE: INCOME TAX ACT Retiring Allowances Paragraph 60(j.1), subparagraph 56(1)(a)(ii) and the definition

Government Gazette REPUBLIC OF SOUTH AFRICA

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE

SOUTH AFRICAN REVENUE SERVICE DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE Another helpful guide brought to you by the South African Revenue Service Preface Draft Guide to the Employment Tax Incentive The

SOUTH AFRICAN REVENUE SERVICE DRAFT GUIDE TO THE EMPLOYMENT TAX INCENTIVE Another helpful guide brought to you by the South African Revenue Service Preface Draft Guide to the Employment Tax Incentive The

BAKER TILLY GREENWOODS

BAKER TILLY GREENWOODS CHARTERED ACCOUNTANTS PRACTICE PROFILE Baker Tilly Greenwoods was established in 1946. The firm has expanded over the years and practises in all major fields of Accounting, Auditing

BAKER TILLY GREENWOODS CHARTERED ACCOUNTANTS PRACTICE PROFILE Baker Tilly Greenwoods was established in 1946. The firm has expanded over the years and practises in all major fields of Accounting, Auditing

- 2 - INCOME TAX RATES Rate of normal income tax on taxable income of any natural person or special trust: 2014/2015

TAX GUIDE 2014-2015 - 1 - CONTENTS INCOME TAX RATES, REBATES AND THRESHOLDS 2 WEAR AND TEAR ALLOWANCES General 3 Capital allowances 3 RESIDENCE BASIS OF TAXATION Resident 4 Non-resident 4 INTEREST AND

TAX GUIDE 2014-2015 - 1 - CONTENTS INCOME TAX RATES, REBATES AND THRESHOLDS 2 WEAR AND TEAR ALLOWANCES General 3 Capital allowances 3 RESIDENCE BASIS OF TAXATION Resident 4 Non-resident 4 INTEREST AND

2016 Automobile Rules. Computation of Personal Use

2016 Automobile Rules Computation of Personal Use 2016 Automobile Rules: Computation of Personal Use... 2 Exhibit 1A... 8 Exhibit 1B... 9 Exhibit 1C... 10 Exhibit 1D... 11 LEGAL NOTICE: The contents of

2016 Automobile Rules Computation of Personal Use 2016 Automobile Rules: Computation of Personal Use... 2 Exhibit 1A... 8 Exhibit 1B... 9 Exhibit 1C... 10 Exhibit 1D... 11 LEGAL NOTICE: The contents of

TAX GUIDE FOR MICRO BUSINESSES 2011/12

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

SOUTH AFRICAN REVENUE SERVICE TAX GUIDE FOR MICRO BUSINESSES 2011/12 Another helpful guide brought to you by the South African Revenue Service Foreword TAX GUIDE FOR MICRO BUSINESSES 2011/12 This guide

Government Gazette REPUBLIC OF SOUTH AFRICA

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 517 Cape Town 22 July 2008 No. 31267 THE PRESIDENCY No. 781 22 July 2008 It is hereby notified that the President has assented to the following Act, which

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 517 Cape Town 22 July 2008 No. 31267 THE PRESIDENCY No. 781 22 July 2008 It is hereby notified that the President has assented to the following Act, which

REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER 0 Initial Release A Scheepers GM Operational Services

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

AS-SDL-1 REVISION HISTORY REV DESCRIPTION OF CHANGE AUTHOR APPROVAL OWNER Initial Release A Scheepers GM Operational Services GM Operational Services 1 2 3 4 TYPE OF REFERENCE Legislation and Rules Administered

THE TAX PROFESSIONAL KNOWLEDGE COMPETENCY ASSESSMENT NOVEMBER 2013 SAMPLE PAPER 1 SUGGESTED SOLUTION

THE TAX PROFESSIONAL KNOWLEDGE COMPETENCY ASSESSMENT NOVEMBER 2013 SAMPLE PAPER 1 SUGGESTED SOLUTION Question Topic Marks 1 Various Advisory 50 2 VAT, CGT and Capital Allowances 30 3 Normal Tax Calculation

THE TAX PROFESSIONAL KNOWLEDGE COMPETENCY ASSESSMENT NOVEMBER 2013 SAMPLE PAPER 1 SUGGESTED SOLUTION Question Topic Marks 1 Various Advisory 50 2 VAT, CGT and Capital Allowances 30 3 Normal Tax Calculation

Government Gazette REPUBLIC OF SOUTH AFRICA

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 506 Cape Town 8 August 2007 No. 30157 THE PRESIDENCY No. 707 8 August 2007 It is hereby notified that the President has assented to the following Act, which

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 506 Cape Town 8 August 2007 No. 30157 THE PRESIDENCY No. 707 8 August 2007 It is hereby notified that the President has assented to the following Act, which

Tax guide 2018/2019 TAX FACTS

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

September 2015 PAYE Reconciliation Communication

0800 00 7277 sars.gov.za September 2015 PAYE Reconciliation Communication 1. Clarification of source codes The following amendments to descriptions and explanations of source codes should be noted (amendments

0800 00 7277 sars.gov.za September 2015 PAYE Reconciliation Communication 1. Clarification of source codes The following amendments to descriptions and explanations of source codes should be noted (amendments

DRAFT DRAFT INTERPRETATION NOTE DATE:

DRAFT DRAFT INTERPRETATION NOTE DATE: ACT : INCOME TAX ACT NO. 58 OF 1962 (the Act) SECTION : PARAGRAPHS 2(b), 2(e), 2(h), 6, 10 AND 13(1) OF THE SEVENTH SCHEDULE SUBJECT : TAXABLE BENEFIT USE OF EMPLOYER-PROVIDED

DRAFT DRAFT INTERPRETATION NOTE DATE: ACT : INCOME TAX ACT NO. 58 OF 1962 (the Act) SECTION : PARAGRAPHS 2(b), 2(e), 2(h), 6, 10 AND 13(1) OF THE SEVENTH SCHEDULE SUBJECT : TAXABLE BENEFIT USE OF EMPLOYER-PROVIDED

THE EMPLOYER S GUIDE TO PAY AS YOU EARN

THE EMPLOYER S GUIDE TO PAY AS YOU EARN Issued by, Taxpayers Services and Education Department July 2017 EMPLOYER S GUIDE TO P.A.Y.E CONTENTS PART I...1 1.0 PRELIMINARY INTERPRETATION...1 1.1 PURPOSE

THE EMPLOYER S GUIDE TO PAY AS YOU EARN Issued by, Taxpayers Services and Education Department July 2017 EMPLOYER S GUIDE TO P.A.Y.E CONTENTS PART I...1 1.0 PRELIMINARY INTERPRETATION...1 1.1 PURPOSE

Next >> Quick Tax Guide 2019/20 South Africa. Making an impact that matters

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters Contents... 1...1...1...2...3...4 Severance and Retirement Fund Lump Sum...4... 5...5...6...7...7...7...7... 8...8...8...9...9...9...9...10...10...10...10...10...11...

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters Contents... 1...1...1...2...3...4 Severance and Retirement Fund Lump Sum...4... 5...5...6...7...7...7...7... 8...8...8...9...9...9...9...10...10...10...10...10...11...

SARS Tax Guide 2014 / 2015

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS. Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

Tax data card 2018/2019

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

WESTERN CAPE De Waterkant Building 10 Helderberg Street Stellenbosch PO Box 920 Stellenbosch 7599

DIRECTORS Pieter-Jan Bestbier, Jock de Jager, André du Plessis, Fran du Plessis, Jana Goosen, Francois Joubert, Iaan Marx, Stephan Pretorius, Lehandi Swanepoel, Johann van Rensburg, Erlo Vos. WESTERN CAPE

DIRECTORS Pieter-Jan Bestbier, Jock de Jager, André du Plessis, Fran du Plessis, Jana Goosen, Francois Joubert, Iaan Marx, Stephan Pretorius, Lehandi Swanepoel, Johann van Rensburg, Erlo Vos. WESTERN CAPE

Financial and Taxation Directory 2006/2007

Financial and Taxation Directory 2006/2007 Cliffe Dekker is part of DLA Piper Group, an alliance of legal practices CONTENTS South African Taxation Highlights of the 2006/2007 Budget 2-5 Calculation of

Financial and Taxation Directory 2006/2007 Cliffe Dekker is part of DLA Piper Group, an alliance of legal practices CONTENTS South African Taxation Highlights of the 2006/2007 Budget 2-5 Calculation of

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16.

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

Tax Guide

2017-2018 Tax Guide - 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 24 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS

2017-2018 Tax Guide - 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 24 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS

training (pty) ltd Tax Guide

ltd Tax Guide") training (pty) ltd. 2016-2017 Tax Guide CONTENTS INCOME TAX RATES Natural person or special trust... 2 TAX REBATES Rebates for individuals... 2 Medical aid contributions and medical expenses... 2 TAX THRESHOLDS...

training (pty) ltd. 2016-2017 Tax Guide CONTENTS INCOME TAX RATES Natural person or special trust... 2 TAX REBATES Rebates for individuals... 2 Medical aid contributions and medical expenses... 2 TAX THRESHOLDS...

TAXATION OF EMPLOYEE EMOLUMENTS AND WITHHOLDING TAX OBLIGATIONS Presentation by: Mary Weru. Uphold public interest

TAXATION OF EMPLOYEE EMOLUMENTS AND WITHHOLDING TAX OBLIGATIONS Presentation by: Mary Weru Uphold public interest Presentation agenda Employee taxes Basis of taxation Residence rules Income subject to

TAXATION OF EMPLOYEE EMOLUMENTS AND WITHHOLDING TAX OBLIGATIONS Presentation by: Mary Weru Uphold public interest Presentation agenda Employee taxes Basis of taxation Residence rules Income subject to

401K PRO, INC. DEFINED CONTRIBUTION PROTOTYPE PLAN AND TRUST

401K PRO, INC. DEFINED CONTRIBUTION PROTOTYPE PLAN AND TRUST TABLE OF CONTENTS ARTICLE I DEFINITIONS ARTICLE II ADMINISTRATION 2.1 POWERS AND RESPONSIBILITIES OF THE EMPLOYER... 13 2.2 DESIGNATION OF ADMINISTRATIVE

401K PRO, INC. DEFINED CONTRIBUTION PROTOTYPE PLAN AND TRUST TABLE OF CONTENTS ARTICLE I DEFINITIONS ARTICLE II ADMINISTRATION 2.1 POWERS AND RESPONSIBILITIES OF THE EMPLOYER... 13 2.2 DESIGNATION OF ADMINISTRATIVE

% 28% funds Trusts 45% 45% Small Business Funding Entities 28% 28%

- 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 25 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS 2 Micro businesses 27

- 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 25 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS 2 Micro businesses 27

12I. Additional investment and training allowances in respect of industrial policy projects. (1) For the purposes of this section

For the purposes of this section") Section 12 I of the Income Tax Act No. 58 of 1962 SOURCE: Lexis Nexis Butterworths (24 May 2010) 12I. Additional investment and training allowances in respect of industrial policy projects. (1) For the

Section 12 I of the Income Tax Act No. 58 of 1962 SOURCE: Lexis Nexis Butterworths (24 May 2010) 12I. Additional investment and training allowances in respect of industrial policy projects. (1) For the

Tax Professional Knowledge Competency Assessment

Tax Professional Knowledge Competency Assessment JUNE 2016 Paper 2 Instructions to Candidates 1. This competency assessment paper consists of four questions. 2. Answer each question in a separate answer

Tax Professional Knowledge Competency Assessment JUNE 2016 Paper 2 Instructions to Candidates 1. This competency assessment paper consists of four questions. 2. Answer each question in a separate answer

Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TAX)

") Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TA) 2011 2012 2013 TA YEAR SITE limit Only > 65 years : R540pa R45pm Only for > 65 years : R540pa R45pm Only for > 65 years : Tax Rebates

Budget Speech 2011, 2012 & 2013 Quick Reference Summary Table (TA) 2011 2012 2013 TA YEAR SITE limit Only > 65 years : R540pa R45pm Only for > 65 years : R540pa R45pm Only for > 65 years : Tax Rebates

BUDGET 2019 TAX GUIDE

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

Professional Level Options Module, Paper P6 (ZAF)

") Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) December 2012 Answers Note: ACCA does not require candidates to quote section numbers or other statutory or case

Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) December 2012 Answers Note: ACCA does not require candidates to quote section numbers or other statutory or case

INCOME TAX: INDIVIDUALS AND TRUSTS

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

Change, the new certainty

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Res HD C2C A Better Pension System. Saving for Retirement: A Guide to the Tax Legislation. March Lud. CanadU

Res HD7105.45 C2C38 1988 A Better Pension System Saving for Retirement: A Guide to the Tax Legislation March 1988 Lud CanadU A Better Pension System 11 #1[1:14b5r111111 FOR Saving for Retirement: A Guide

Res HD7105.45 C2C38 1988 A Better Pension System Saving for Retirement: A Guide to the Tax Legislation March 1988 Lud CanadU A Better Pension System 11 #1[1:14b5r111111 FOR Saving for Retirement: A Guide

TAX UPDATE. For period: 1 January 2016 to 31 March Prepared by: Johan Kotze

TAX UPDATE For period: 1 January 2016 to 31 March 2016 Prepared by: Johan Kotze 3. 2 TABLE OF CONTENTS 1. INTRODUCTION 7 2. NATIONAL BUDGET 8 2.1. Personal income tax 8 2.2. Medical tax credits 9 2.3.

TAX UPDATE For period: 1 January 2016 to 31 March 2016 Prepared by: Johan Kotze 3. 2 TABLE OF CONTENTS 1. INTRODUCTION 7 2. NATIONAL BUDGET 8 2.1. Personal income tax 8 2.2. Medical tax credits 9 2.3.

Examiner s report F6 Taxation (LSO) June 2015

June 2015") Examiner s report F6 Taxation (LSO) June 2015 General Comments There were two sections to the examination paper and were compulsory. Section A consisted of 15 multiple choice questions (two marks each)

Examiner s report F6 Taxation (LSO) June 2015 General Comments There were two sections to the examination paper and were compulsory. Section A consisted of 15 multiple choice questions (two marks each)

Hope and confidence come from energetic involvement and a willingness to

27 February 2013 Compiled by Group Taxation This document is distributed as a service to the Liberty group via the internal e-mail system. It deals with broad-ranging tax developments of relevance to the

27 February 2013 Compiled by Group Taxation This document is distributed as a service to the Liberty group via the internal e-mail system. It deals with broad-ranging tax developments of relevance to the

Next >> Driving progress Quick Tax Guide 2018/19

Next >> Driving progress Quick Tax Guide 2018/19 South Africa Contents... 1 and Rebates... 1... 1... 2 and Allowances... 3... 4 Severance and Retirement Fund Lump Sum... 4... 5... 5... 6... 7... 7... 7...

Next >> Driving progress Quick Tax Guide 2018/19 South Africa Contents... 1 and Rebates... 1... 1... 2 and Allowances... 3... 4 Severance and Retirement Fund Lump Sum... 4... 5... 5... 6... 7... 7... 7...

GAP INC. DEFERRED COMPENSATION PLAN SUMMARY PLAN DESCRIPTION

GAP INC. DEFERRED COMPENSATION PLAN SUMMARY PLAN DESCRIPTION NOVEMBER 2016 ABOUT THIS BOOKLET The following is a Summary Plan Description ( SPD ) that describes the Gap Inc. Deferred Compensation Plan

GAP INC. DEFERRED COMPENSATION PLAN SUMMARY PLAN DESCRIPTION NOVEMBER 2016 ABOUT THIS BOOKLET The following is a Summary Plan Description ( SPD ) that describes the Gap Inc. Deferred Compensation Plan

FIS Business SystemsBUSINESS SYSTEMS LLC NON-STANDARDIZED GOVERNMENTAL401(a) PRE-APPROVED PLAN DRAFT - 1/24/19

PRE-APPROVED PLAN DRAFT - 1/24/19") FIS Business SystemsBUSINESS SYSTEMS LLC NON-STANDARDIZED GOVERNMENTAL401(a) PRE-APPROVED PLAN TABLE OF CONTENTS ARTICLE I DEFINITIONS ARTICLE II ADMINISTRATION 2.1 POWERS AND RESPONSIBILITIES OF THE EMPLOYER...

FIS Business SystemsBUSINESS SYSTEMS LLC NON-STANDARDIZED GOVERNMENTAL401(a) PRE-APPROVED PLAN TABLE OF CONTENTS ARTICLE I DEFINITIONS ARTICLE II ADMINISTRATION 2.1 POWERS AND RESPONSIBILITIES OF THE EMPLOYER...

RESTRICTED SHARE UNIT PLAN. December, 2013

RESTRICTED SHARE UNIT PLAN December, 2013 Amended and Restated March, 2014 TABLE OF CONTENTS ARTICLE 1 PURPOSE... 4 1.1 PURPOSE... 4 ARTICLE 2 DEFINITIONS... 4 2.1 DEFINITIONS... 4 2.2 INTERPRETATIONS...

RESTRICTED SHARE UNIT PLAN December, 2013 Amended and Restated March, 2014 TABLE OF CONTENTS ARTICLE 1 PURPOSE... 4 1.1 PURPOSE... 4 ARTICLE 2 DEFINITIONS... 4 2.1 DEFINITIONS... 4 2.2 INTERPRETATIONS...

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2009

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

SUPPLEMENT F SUPPLEMENT TO 1999 FIRSTENERGY CORP. PENSION PLAN RELATING TO NON-BARGAINING UNIT EMPLOYEES PREVIOUSLY COVERED UNDER THE GPU PLAN

SUPPLEMENT F SUPPLEMENT TO 1999 FIRSTENERGY CORP. PENSION PLAN RELATING TO NON-BARGAINING UNIT EMPLOYEES PREVIOUSLY COVERED UNDER THE GPU PLAN This Supplement hereby sets forth certain provisions of the

SUPPLEMENT F SUPPLEMENT TO 1999 FIRSTENERGY CORP. PENSION PLAN RELATING TO NON-BARGAINING UNIT EMPLOYEES PREVIOUSLY COVERED UNDER THE GPU PLAN This Supplement hereby sets forth certain provisions of the

bulletin PAPILSKY HURWITZ 2014/2015 CHARTERED ACCOUNTAN TS (SA)

") bulletin 2014/2015 PAPILSKY HURWITZ CHARTERED ACCOUNTAN TS (SA) IMPORTANT amendments to the income tax act, current tax RATes and allowances and other general points of interest Papilsky Hurwitz 1st Floor,

bulletin 2014/2015 PAPILSKY HURWITZ CHARTERED ACCOUNTAN TS (SA) IMPORTANT amendments to the income tax act, current tax RATes and allowances and other general points of interest Papilsky Hurwitz 1st Floor,

CONSOLIDATED TO 8 NOVEMBER 2017 LEGISLATION OF SEYCHELLES CHAPTER 273

CONSOLIDATED TO 8 NOVEMBER 2017 LEGISLATION OF SEYCHELLES CHAPTER 273 INCOME AND NON-MONETARY BENEFITS TAX ACT, 2010 [1st July 2010] Act 10 of 2010 SI 68 of 2010 SI 95 of 2010 SI 10 of 2011 SI 11 of 2011

CONSOLIDATED TO 8 NOVEMBER 2017 LEGISLATION OF SEYCHELLES CHAPTER 273 INCOME AND NON-MONETARY BENEFITS TAX ACT, 2010 [1st July 2010] Act 10 of 2010 SI 68 of 2010 SI 95 of 2010 SI 10 of 2011 SI 11 of 2011

BULLETIN PAPILSKY HURWITZ 2013/2014 CHARTERED ACCOUNTAN TS (SA)

") BULLETIN 2013/2014 PAPILSKY HURWITZ CHARTERED ACCOUNTAN TS (SA) CONTENTS Page Budget Proposals... 2 Company and Close Corporation Tax Rates... 3 Individuals... 3 Tax Tables... 3 Rebates... 3 Tax Thresholds...

BULLETIN 2013/2014 PAPILSKY HURWITZ CHARTERED ACCOUNTAN TS (SA) CONTENTS Page Budget Proposals... 2 Company and Close Corporation Tax Rates... 3 Individuals... 3 Tax Tables... 3 Rebates... 3 Tax Thresholds...

Global Mobility Services: Taxation of International Assignees Kenya

www.pwc.com/ke/en Global Mobility Services: Taxation of International Assignees Kenya People and Organisation Global Mobility Country Guide (Folio) Last Updated: May 2018 This document was not intended

www.pwc.com/ke/en Global Mobility Services: Taxation of International Assignees Kenya People and Organisation Global Mobility Country Guide (Folio) Last Updated: May 2018 This document was not intended

Budget Highlights 2018

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

DRAFT DRAFT INTERPRETATION NOTE DATE:

DRAFT DRAFT INTERPRETATION NOTE DATE: ACT : INCOME TAX ACT 58 OF 1962 (the Act) SECTION : SECTION 1(1), DEFINITION OF THE TERM GROSS INCOME FOURTH SCHEDULE TO THE ACT, PARAGRAPH 1 DEFINITIONS: REMUNERATION,

DRAFT DRAFT INTERPRETATION NOTE DATE: ACT : INCOME TAX ACT 58 OF 1962 (the Act) SECTION : SECTION 1(1), DEFINITION OF THE TERM GROSS INCOME FOURTH SCHEDULE TO THE ACT, PARAGRAPH 1 DEFINITIONS: REMUNERATION,

GOVERNMENT EMPLOYEES PENSION LAW AMENDMENT BILL

REPUBLIC OF SOUTH AFRICA GOVERNMENT EMPLOYEES PENSION LAW AMENDMENT BILL (As introduced in the National Assembly as a section 75 Bill; explanatory summary of Bill published in Government Gazette No 26676

REPUBLIC OF SOUTH AFRICA GOVERNMENT EMPLOYEES PENSION LAW AMENDMENT BILL (As introduced in the National Assembly as a section 75 Bill; explanatory summary of Bill published in Government Gazette No 26676

DÁIL ÉIREANN AN BILLE AIRGEADAIS 2005 FINANCE BILL 2005 LEASUITHE COISTE COMMITTEE AMENDMENTS

DÁIL ÉIREANN AN BILLE AIRGEADAIS 2005 FINANCE BILL 2005 LEASUITHE COISTE COMMITTEE AMENDMENTS [No. 1 of 2005] [1st March, 2005] [Printers Referrence] DÁIL ÉIREANN AN BILLE AIRGEADAIS 2005 ROGHCHOISTE FINANCE

DÁIL ÉIREANN AN BILLE AIRGEADAIS 2005 FINANCE BILL 2005 LEASUITHE COISTE COMMITTEE AMENDMENTS [No. 1 of 2005] [1st March, 2005] [Printers Referrence] DÁIL ÉIREANN AN BILLE AIRGEADAIS 2005 ROGHCHOISTE FINANCE

Interpretation Notes Register. All Taxes

Register All Taxes Publication 2001/11/30 IN 1 Provisional tax estimates Paragraph 19(3) of the Fourth Schedule 2009/03/17 IN 2 Foreign Dividends: Deductibility of Interest Section 11C Issue 1 2002/02/02

Register All Taxes Publication 2001/11/30 IN 1 Provisional tax estimates Paragraph 19(3) of the Fourth Schedule 2009/03/17 IN 2 Foreign Dividends: Deductibility of Interest Section 11C Issue 1 2002/02/02

South African Income Tax Guide for 2013/2014

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165