Lecture Materials STRATEGIC LEADERSHIP ISSUES

|

|

|

- Evelyn Boone

- 5 years ago

- Views:

Transcription

1 Lecture Materials STRATEGIC LEADERSHIP ISSUES Philip Smith President Gerrish McCreary Smith, Consultants and Attorneys Memphis, Tennessee August 4, 2016

2

3

4 GERRISH MCCREARY SMITH Consultants and Attorneys You can view or download Philip Smith s materials for the 2016 session of the Graduate School of Banking at the University of Wisconsin from our website at Follow us on

5 BIOGRAPHICAL INFORMATION PHILIP K. SMITH. Mr. Smith is the President and a member of the Board of Directors of the Memphis-based law firm of Gerrish McCreary Smith, PC, and its affiliated bank consulting firm, Gerrish McCreary Smith Consultants, LLC. Mr. Smith's legal and consulting practice places special emphasis on bank mergers and acquisitions, financial analysis, acquisition and ownership planning for boards of directors, strategic planning for boards of directors, regulatory matters, bank holding company formations and use, securities law concerns, new bank formations, S corporations, going private transactions and other matters of importance to banks and financial institutions. He is a frequent speaker to boards of directors and a presenter at numerous banking seminars. He received his undergraduate business degree and Masters of Business Administration degree from the Fogelman School of Business and Economics at The University of Memphis and his law degree from the Cecil C. Humphreys School of Law at The University of Memphis. He is authoring a monthly electronic newsletter, The Chairman s Forum Newsletter, which discusses key topics impacting financial institutions and, specifically, the role of the Chairman. Mr. Smith is a Summa Cum Laude graduate of the Barret School of Banking where he has been a member of the faculty. He has also served as a member of the faculty of the Pacific Coast Banking School, the Colorado Graduate School of Banking, the Southwestern Graduate School of Banking and the Wisconsin Graduate School of Banking. Gerrish McCreary Smith Consultants, LLC and Gerrish McCreary Smith, PC, Attorneys offer consulting, financial advisory and legal services to community banks nationwide in the following areas: strategic planning; mergers and acquisitions, both financial analysis and legal services; dealing with the regulators, particularly involving troubled banks, memoranda of understanding, cease and desist orders, consent orders and compliance; structuring and formation of bank holding companies; capital planning; employee stock ownership plans, leveraged ESOPs, KSOPs and incentive compensation packages; directors and officers liability; new bank formations; S corporation formations; going private transactions; and public and private securities offerings. Gerrish McCreary Smith, PC, Attorneys has been ranked as high as third nationally by number of transactions in bank mergers and acquisitions. GERRISH McCREARY SMITH, PC, ATTORNEYS GERRISH McCREARY SMITH CONSULTANTS, LLC 700 Colonial Road, Suite Colonial Road, Suite 200 Memphis, Tennessee Memphis, Tennessee (901) (901) psmith@gerrish.com psmith@gerrish.com

6 GERRISH McCREARY SMITH CONSULTANTS, LLC GERRISH McCREARY SMITH, PC, ATTORNEYS CONSULTING FINANCIAL ADVISORY LEGAL Mergers & Acquisitions Analysis of Business and Financial Issues Target Identification and Potential Buyer Evaluation Preparation and Negotiation of Definitive Agreements Preparation of Regulatory Applications Due Diligence Reviews Tax Analysis Securities Law Compliance Leveraged Buyouts Anti-Takeover Planning Going Private Transactions Financial Modeling and Analysis Transaction Pricing Analysis Fairness Opinions Bank and Thrift Holding Company Formations Structure and Formation Ownership and Control Planning New Product and Service Advice Preparation of Regulatory Applications Financial Modeling and Analysis New Bank and Thrift Organizations Organizational and Regulatory Advice Business Plan Creation Preparation of Financial Statement Projections Preparation of the Interagency Charter and Federal Deposit Insurance Application Private Placements and Public Stock Offerings Development of Bank Policies Financial Modeling and Analysis Financial Statement Projections Business and Strategic Plans Ability to Pay Analysis Net Present Value and Internal Rate of Return Analysis Mergers and Acquisitions Analysis Subchapter S Election Analysis Bank Regulatory Guidance and Examination Preparation Preparation of Regulatory Applications Examination Planning and Preparation Regulatory Compliance Matters Charter Conversions Subchapter S Conversions and Elections Financial and Tax Analysis and Advice Reorganization Analysis and Restructuring Cash-Out Mergers Stockholders Agreements Financial Modeling and Analysis Strategic Planning Retreats Customized Director and Officer Retreats Long-Term Business Planning Assistance and Advice in Implementing Strategic Plans Business and Strategic Plan Preparation and Analysis Director Education Capital Planning and Raising Private Placements and Public Offerings of Securities Bank Stock Loans Capital Plans Problem Banks and Thrifts Issues Examiner Dispute Resolution Negotiation of Memoranda of Understanding and Consent Orders Negotiation and Litigation of Administrative Enforcement Actions Defense of Directors in Failed Bank Litigation Management Evaluations and Plans Failed Institution Acquisitions New Capital Raising and Capital Plans Appeals of Material Supervisory Determinations Executive Compensation and Employee Benefit Plans Employee Stock Ownership Plans 401(k) Plans Leveraged ESOP Transactions Incentive Compensation and Stock Option Plans Employment Agreements-Golden Parachutes Profit Sharing and Pension Plans General Corporate Matters Corporate Governance Planning and Advice Recapitalization and Reorganization Analysis and Implementation Taxation Tax Planning Tax Controversy Negotiation and Advice Estate Planning for Community Bank Executives Wills, Trusts, and Other Estate Planning Documents Estate Tax Savings Techniques Probate Other Public Speaking Engagements for Banking Industry Groups (i.e., Conventions, Schools, Seminars, and Workshops) Publisher of Books and Newsletters Regarding Banking and Financial Services Issues

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23 Corporate Governance Warning Signs Tough questions regarded as undesirable Corporate minutes are useless CEO shields Board from the management team Gerrish McCreary Smith Consultants and Attorneys Conclusion Primary job is to enhance shareholder value Corporate governance is here to stay Strategic planning obligation includes corporate governance For non-public companies, do what makes sense Gerrish McCreary Smith Consultants and Attorneys GERRISH MCCREARY SMITH Consultants and Attorneys 16

24

25

26 BOARD GOVERNANCE TABLE OF CONTENTS PAGE 10 Commandments for Community Bank Corporate Governance... 1 Developments in Corporate Governance... 5 Changes under the Dodd-Frank Act... 5 Developments under the Sarbanes-Oxley Act Further Developments since the Release of the Report Developments in the Director Community... 17

27 10 COMMANDMENTS FOR COMMUNITY BANK CORPORATE GOVERNANCE Corporate governance for large or small institutions is constantly evolving. Corporate governance is simply a fancy way to refer to the inter-workings of the bank or bank holding company at its highest level of board of directors, board committees and senior management. On July 30, 2002, the President signed into law the Sarbanes-Oxley Act. This Act specifically provides a variety of corporate governance and other requirements for bank holding companies reporting to the Securities and Exchange Commission ( SEC ) pursuant to the Securities Exchange Act of This basically means that any company that files 10-Ks, 10-Qs and the like must comply with the requirements of the new Act. In 2010, President Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act which adds a host of new rules, rights and requirements that must be understood by bank boards. For non-reporting companies, a review and analysis, or in many cases an overhaul, of the corporate governance processes is also likely necessary. The following 10 commandments will provide food for thought in those specific areas that will begin to need focus. I. THOU SHALT REALIZE, THE TIMES, THEY ARE A CHANGIN! Just as Sarbanes-Oxley did over a decade ago, the passage of the Dodd-Frank Act in 2010 has added, and will continue to add, a host of rules related to corporate governance for SEC reporting companies. For non-reporting companies, they provide a road map. It is likely also a road map that the regulators will be utilizing to guide non-reporting banks to the land of sound corporate governance. It is likely that the regulators for non-reporting banks will adopt as policy, or at least as expectation, requirements from both Sarbanes-Oxley and Dodd-Frank, particularly as it relates to independence of Directors and the function of audit, compensation and nominating committees. II. THOU SHALT ESTABLISH AN EFFECTIVE, CAPABLE AND RELIABLE BOARD OF DIRECTORS. Every community bank or bank holding company should have an effective, reliable and capable board of directors. This means individuals with integrity who are qualified and successful in their own fields and who have the capacity, understanding and interest to focus on the financial services industry. That means that a majority of your board of directors should be truly outside, independent directors. Outside, independent directors will have some stock ownership (you really don t want somebody running the company who has no financial interest) but would otherwise be independent, not work for the company, not borrow money from the company, and be able to provide independent advice. The board must be effective and should meet in executive session at least monthly without the CEO, even if he or she is a member of the board. The board should also set the long-term strategy, policy and values for the organization. It should not micro manage. Philip K. Smith Copyright GERRISH McCREARY SMITH Consultants and Attorneys

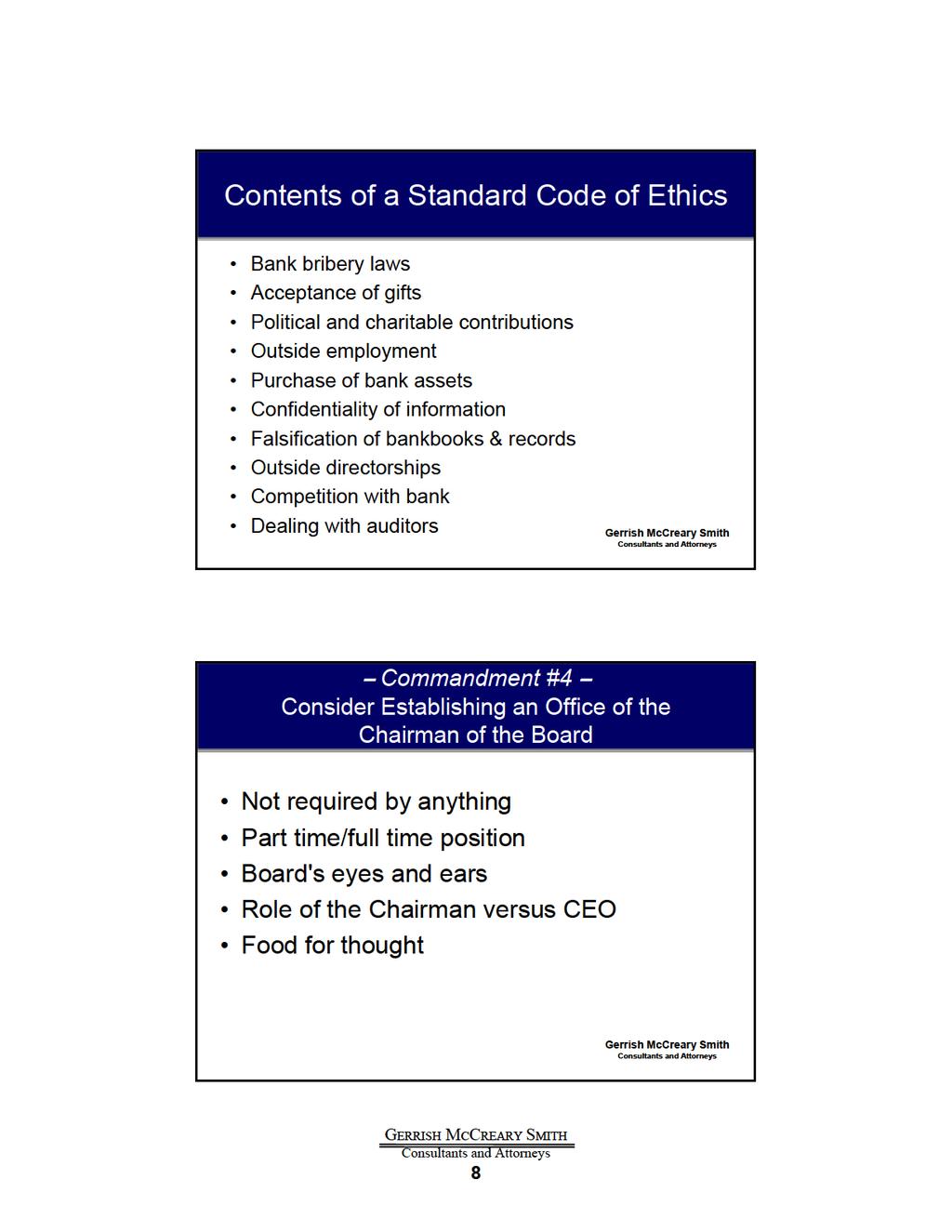

28 For public companies, under Sarbanes-Oxley, in order to be considered an "independent" director, the director cannot (a) accept any consulting, advisory or other compensation or fee from the company (other than usual director fees) or (b) be an affiliated person at the company or any subsidiary of the company. An affiliated person generally means any person directly or indirectly owning, controlling, or holding the power to vote 10% or more of the outstanding voting securities of the company. Should a director borrow from his own bank? Sarbanes-Oxley, for publicly reporting bank holding companies and banks, allows director loans pursuant to Regulation O. The question still remains, should a director borrow from his own bank. The following are the pros and cons on this issue. PROS CONS 1. Directors are generally the most successful 1. Loans result in enhanced regulatory scrutiny business people in the community 2. The most financially stable 2. Inadvertent violation of Regulation O subjects all board members to potential penalties 3. Known to the bank 3. A director's financial trouble means regulatory trouble for the bank 4. Have some ownership interest in the bank 4. Easier to get a director on the board than off, even in a troubled situation 5. Suffer peer pressure to repay the loan Should a director borrow from his or her own bank? The answer is a resounding "probably". Should all directors receive, simply due to their membership on the board, approval of a line of credit or some inherent right to borrow? Absolutely not! III. THOU SHALT ESTABLISH A CORPORATE CODE OF ETHICS FOR THE BANK OR BANK HOLDING COMPANY. SEC reporting banks and bank holding companies are not required to have a code of ethics policy, but if an SEC reporting company does not have such a policy, it must explain why. Given the perception that many bank failures are a result of failures at the board level, it is more prudent to have one. While no banking law or regulation requires a formal policy governing the ethical conduct of bank officers and employees, you can expect examiners to inquire about the existence of such a policy. And, should the bank encounter problems with insider activities, you can be sure examiners will require one. At a minimum, a code of ethics policy should address: a. Conflicts of interest b. Bank bribery laws c. Acceptance of gifts d. Political contributions e. Outside employment f. Purchases of bank assets 2 GERRISH McCREARY SMITH Consultants and Attorneys

29 g. Confidentiality of bank and customer information h. Falsification of bank books and records i. Outside directorships j. Competition with the bank for business opportunities k. Dealing with auditors As Yogi Berra said, if you don t know where you are going, you will wind up someplace else. If corporate ethics, values and the like are not established at the top, at the board level, and used to govern the operations of the company, both from a long-term strategy and a daily basis through executive management, then executive management certainly cannot anticipate that the rank and file will follow such a code on their own. Establish a workable, reliable and realistic corporate code of ethics for the way the corporation will conduct business internally and externally. IV. THOU SHALT CONSIDER ESTABLISHING AN OFFICE OF THE CHAIRMAN OF THE BOARD. Several large organizations are considering establishing an Office of the Chairman of the Board. This will be a paid, fulltime position. It will be compensated only by salary and not subject to any type of supervisory authority by the executive management of the company. A full-time Chairman of the Board will report only to the board and will be the board s eyes and ears on a daily basis in connection with the workings of the company. While this certainly may not be feasible for many smaller community banks, it is still a concept worth exploring with respect to having a truly independent board chairman. Under current regulations, listed companies are required to disclose why they chose to combine or separate the offices of Chairman and CEO. If the offices are combined, the company must disclose whether it has a lead independent director. V. THOU SHALT HAVE AN EFFECTIVE AND OPERATING AUDIT COMMITTEE, COMPENSATION COMMITTEE, NOMINATING COMMITTEE AND RISK COMMITTEE. The audit committee, compensation committee and nominating committee should be composed of all independent outside directors of the company. The risk committee should be chaired by an independent outside director. These committees should have access to attorneys and consultants, paid for by the company other than the corporation s normal counsel and consultants. Clearly, under Sarbanes-Oxley Act for SEC reporting companies, the audit committee is entitled to such representation independently. The audit committee should directly retain the auditors and set the scope of the engagement. The committee should also monitor outside non-audit work performed for the company by the auditors. 3 GERRISH McCREARY SMITH Consultants and Attorneys

30 Banking regulations currently require that banks with assets of $500 million or more, but less than $1 billion, must have a board level audit committee composed of outside directors, a majority of whom must be independent of management. And, banks with assets of $1 billion or more must have an independent board level audit committee comprised entirely of outside directors who are independent of the management of the institution. The audit committee of these larger institutions is primarily responsible for ensuring that an annual independent audit is conducted. The committee is responsible for selecting and engaging the auditor. Once the audit is completed, the committee should receive and review the audit report ensuring that audit deficiencies are addressed. While these stringent requirements do not apply to smaller banks, they too, should ensure that the audit committee functions independently of management. While this is not always possible in smaller institutions, independence should be the objective. The SEC has recently issued rules required under the Dodd-Frank Act that direct the national securities exchanges to implement reforms related to Compensation Committees. Among them are rules related to the hiring of consultants by Compensation Committees and factors to help determine the independence of a director/committee member. The independent nature of the compensation committee and nominating committee are also critical. The compensation committee should not be a rubber stamp for management. The nominating committee should consider establishing an evaluation system for board members. Simply because you are a board member elected at the last election, you should not automatically be re-elected at the current annual meeting. VI. THOU SHALT CONSIDER EFFECTIVE BOARD COMPENSATION. Directors, particularly with their new duties, responsibilities and liabilities, should be fairly compensated, although, admittedly, directors will never be compensated for the risk. Should directors receive equity interests? Many do. Should directors receive additional compensation for serving on some of the critical committees, such as audit, compensation and nominating? Probably so. If the bank or bank holding company s goal is to attract and retain the highest quality employees, it should also be to attract, retain and maintain the highest quality of directors. VII. THOU SHALT ASSURE CONTINUING EDUCATION FOR DIRECTORS. The financial services industry is moving rapidly in a number of different directions. It is critical, even for the smallest institution, that directors be educated about the options and opportunities for the institution. Only then can they make wise choices with respect to its effective long-term strategies. 4 GERRISH McCREARY SMITH Consultants and Attorneys

31 VIII. THOU SHALT ESTABLISH PROCEDURES FOR BOARD SUCCESSION. A critical issue of corporate governance is to make sure qualified board members are available. This involves issues of succession. Does the holding company have a mandatory retirement age that is actually enforced? Does a board self-evaluation process exist to rid the board of deadwood? Does the company have a plan to maintain a fully staffed board of directors with capable people, no matter what the ages, as it moves forward for the next several years? All of these must be planned for and addressed under the umbrella of corporate governance. The failure to have a plan will result in the failure to have board succession in most cases. IX. THOU SHALT DISCLOSE, DISCLOSE, DISCLOSE. Publicly held (greater than 2,000 shareholders) banks and bank holding companies will find that disclosure will be quicker and more onerous than in the past. Even for private companies and banks, those with less than 2,000 shareholders, disclosure needs to be stepped up. This may be through quarterly letters to your shareholders. But some means of communication, though not legally required, will go a long way toward furthering the confidence of your shareholders in your institution. X. THOU SHALT RECOGNIZE THAT YOUR DUTY IS TO ESTABLISH CORPORATE GOVERNANCE PROCEDURES THAT WILL SERVE TO ENHANCE SHAREHOLDER VALUE. The primary job of the board of directors is to enhance the value of the shares held by its shareholders. This is generally done through growing earnings, providing an adequate return on equity, providing liquidity in the shares and some type of cash flow off the shares within an overall strategy established by the board. Corporate governance procedures should be designed to enhance the long-term value for the shareholders. DEVELOPMENTS IN CORPORATE GOVERNANCE Changes under the Dodd-Frank Act On July 21st of 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act ( Dodd- Frank Act ) was signed into law. In addition to overhauling the financial services regulatory regime, the Dodd-Frank Act advances the further federalization of corporate governance regulation by building on prior public policy embodied in Sarbanes-Oxley. The Dodd-Frank Act s corporate governance provisions are not limited to financial services sector companies, but apply generally to publicly reporting companies. Many of the provisions are to be implemented by requiring the national securities exchanges and associations to modify listing standards to encapsulate these requirements. The principle executive compensation and corporate governance changes in the Act include: 5 GERRISH McCREARY SMITH Consultants and Attorneys

32 Say on Pay and Say on Golden Parachute Provisions. (Section 951) The Dodd-Frank Act added new Sections 14A(a) and 14A(b) to the Securities Exchange Act, which were incorporated into the SEC s rules in These require public companies to provide their shareholders with a non-binding vote ( say-onpay ) on the compensation of their executives, as well as on golden parachute severance arrangements in connection with mergers and other similar transactions, at least every three years. The frequency of the say-on-pay vote is to be determined by a separate shareholder resolution no less frequently than every six years. The first say-on-pay vote which determines the frequency of the say-onpay vote must occur in the proxy, consent or authorization materials for the first annual shareholder meeting occurring after January 21, The say-on-pay vote is not binding on the company or its board and cannot be construed as overruling any decision made by the company or the board. The say-on-pay vote does not create any additional legal duties for the Board and does not limit a shareholder s ability to include executive compensation proposals in proxy materials. Any proxy, consent or authorization materials for a meeting seeking shareholder approval of an acquisition, merger, or disposition of substantially all of the company s assets to include a separate non-binding shareholder resolution approving certain payments made in connection with the transaction. In light of the non-binding nature of the vote, and in order to allow shareholders to learn how often a company will provide the say-on-pay vote, the rule also revises Form 8-K to require disclosure of the results of the vote on the frequency of future say-on-pay votes. This Form 8-K is required no later than 150 calendar days after the date of the annual meeting in which the vote took place. The SEC adopted a temporary exemption so that smaller reporting companies (those with a public float of less than $75 million) are not required to conduct say-on-pay and frequency votes until annual meetings occurring on or after January 21, As with other issuers, smaller reporting companies are required to conduct the shareholder advisory vote on golden parachute compensation once the rules are effective. The delayed compliance date for smaller reporting companies is designed to allow those companies to observe how the rules operate for other companies, and should allow them to better prepare for implementation. 6 GERRISH McCREARY SMITH Consultants and Attorneys

33 Compensation Committee Reforms. (Section 952) As directed by the Dodd-Frank Act, in June 2012, the SEC adopted rules directing the National Securities Exchanges to adopt certain listing standards related to the compensation committee of a company s Board of Directors, as well as its compensation advisors. The exchanges are required to adopt listing standards that require each member of a company s compensation committee (or, if there is no compensation committee, any individual or committee overseeing executive compensation matters) to be a member of the Board of Directors and to be independent. The exchanges are to consider factors such as: Sources of compensation of a Director, including any consulting, advisory or compensatory fee paid by the company to such member of the Board of Directors. Whether the member of the Board of Directors of a company is affiliated with the company, a subsidiary of the company or an affiliate of a subsidiary of the company. Listing standards adopted by the exchanges must provide that the compensation committee of a listed company: May, in its sole discretion, retain or obtain the advice of a compensation advisor. Is directly responsible for the appointment, payment and oversight of compensation advisors. Must be appropriately funded by the listed company. The listing standards must provide that a compensation committee may select a compensation consultant, legal counsel or other advisor only after considering the following six independence factors: Whether the compensation advisor s employer is providing any other services to the listed company. How much the compensation consulting company has received fees from the company, as a percentage of that person s total revenue. What policies and procedures have been adopted by the compensation consulting company to prevent conflicts of interest? Whether the compensation advisor has any business or personal relationship with the member of the compensation committee. Whether the compensation advisor owns any stock of the company. 7 GERRISH McCREARY SMITH Consultants and Attorneys

34 Whether the compensation advisor or consulting company has any business or personal relationships with the listed company s executive officers. The final rules require the exchanges to exempt the following five categories of companies from the independence requirements: Controlled companies. Limited partnerships. Companies in bankruptcy proceedings. Open-end management investment companies registered under the Investment Company Act of Any foreign private-issuer that discloses in its annual report the reasons that the foreign private-issuer does not have an independent compensation committee. Implementation of a Claw-back Policy. (Section 954) Section 10D to the Exchange Act requires the SEC to direct the national securities exchanges to require companies to implement a policy to claw-back executive payments that were made based on improper financial statements. To be listed on an exchange, a company will have to disclose incentive based compensation tied to financial information required to be reported under the securities laws and implement a policy to claw-back any such compensation that was paid to current or former executive officers during the three-year period preceding the date for which the company must prepare an accounting restatement. Hedging Disclosures. (Section 955) Companies must disclose in their proxy statement whether any employee or director is permitted to engage in hedging activities involving company stock. Require Enhanced Pay-for-Performance and Pay Equity Disclosures. (Section 956) Proxy statements must disclose the relationship between executive compensation actually paid and the company s financial performance, taking into account any change in the value of stock and any dividends or distributions. Proxy statements (and other SEC filings containing compensation disclosures) will also be required to show the ratio of the median total annual compensation of all employees other than the CEO, to the CEO s total annual compensation. 8 GERRISH McCREARY SMITH Consultants and Attorneys

35 Prohibition on Discretionary Voting. (Section 957) The Act amends Section 6(b) of the Exchange Act to require that the national securities exchanges prohibit proxy voting by a broker in connection with the election of directors (other than a vote with respect to the uncontested election of a member of the board of any registered investment company), executive compensation or any other significant matter, as determined by the SEC, unless the beneficial owner of the security has specifically instructed the broker to vote in such way. The New York Stock Exchange amended NYSE Rule 452 in order to carry out the requirements of Section 957 of the Dodd-Frank Act. Because the Exchange previously prohibited member organizations from voting uninstructed shares if the matter voted on is the election of Directors, the amendment prohibits member organizations from voting uninstructed shares if the matter voted on relates to executive compensation. The amendment clarifies that a matter relating to executive compensation would include, among other things, the items referred to in Section 14A of the Exchange Act (added by Section 951 of the Dodd-Frank Act), including the advisory vote to approve the compensation of the Directors, a vote on the frequency of such say on pay vote, and an advisory vote to approve any type of compensation that is based on or otherwise relates to an acquisition, merger, consolidation, sale, or other disposition of all or substantially all of the assets of an issuer and the aggregate total of all such compensation that may be paid or become payable to or on behalf of an executive officer. Proxy Access Rights. (Section 971) The Act affirms that the SEC may promulgate rules permitting the use by a shareholder of company proxy materials to nominate director candidates. The Act does not require the SEC to adopt proxy access rules and it explicitly authorizes the SEC to exempt companies from any requirements that it does adopt after taking into account considerations such as whether the requirements would disproportionately burden small companies. The SEC proposed a proxy access rule in August, 2010 that was vacated by the U.S. Court of Appeals for the District of Columbia in July The SEC has yet to propose a new proxy access rule. Chairman and CEO disclosures. (Section 972) The Act amends Section 14B of the Securities Exchange Act to direct the SEC to issue rules requiring companies to disclose in their annual proxy statements the reasons why the company has chosen to combine or separate the Chairman of the Board and CEO positions. Similar disclosure is required under current SEC rules, so it is unclear whether this provision will result in any additional disclosure requirements. 9 GERRISH McCREARY SMITH Consultants and Attorneys

36 Exemptions from Sarbanes-Oxley Internal Control Requirements (Section 989G) The Act makes permanent exemptions for smaller public companies that are not "accelerated filers" or "large accelerated filers" from compliance with the internal control auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of It also directs the SEC to study ways of reducing the burden of Section 404(b) compliance on companies with market capitalizations between $75 million and $250 million while maintaining investor protections for such companies. Developments under the Sarbanes-Oxley Act The SEC s Advisory Committee on Smaller Public Companies was established to assess the current regulatory system on smaller companies, in particular the Sarbanes-Oxley Act of The Committee s report, issued April 23, 2006 and modified on September 7, 2007, includes a number of recommended changes for the Act s application to smaller companies. The following materials provide an overview of the Committee s recommendations by category. A. SCALING REGULATIONS FOR SMALLER COMPANIES Primary Recommendation The Committee recommends establishing a new system of size-based regulation for smaller public companies. Smaller companies would be defined according to the following criteria: the total present value ( market capitalization ) of the company; a measurement system that s been specially created to help scale regulations; a measurement system that is self-calibrating; a standardized method for computing a company s market capitalization; a date for determining the company s market capitalization; and clear and firm boundaries between size classes, and rules on companies transitions between the classes. The Committee recommends developing specific, size-based regulation for companies in the lowest 6% of U.S. equity market capitalization. These are divided into microcap and smallcap companies, as follows: Microcap companies have a market capitalization that places them in the lowest 1%. Smallcap companies have a market capitalization that places them in the next lowest 1% to 5%. 10 GERRISH McCREARY SMITH Consultants and Attorneys

37 B. COMPANIES INTERNAL CONTROL OVER FINANCIAL REPORTING 1. Primary Recommendations The Committee first recommends that, until the SEC creates a suitable assessment of internal reporting controls for micro- and smallcap companies, those companies should be exempt from Section 404 requirements, as long as they do the following: Follow Exchange Act guidelines relating to audit committees; Adopt a code of ethics applicable to all directors, officers, and employees; and Disclose the code of ethics as provided in SEC regulations. The Committee recommends that the SEC confirm and clarify the existing requirements regarding internal controls that apply to two classes of companies: Microcap companies with less than $125 million in annual revenue; and smallcap companies with less than $10 million in annual product revenue. These internalcontrol regulations require: that the companies maintain an effective system of internal control over financial reporting; that they disclose any modifications to their internal control over financial reporting, and the relevant consequences of the modifications; that their CEO and CFO certify such disclosures; and that they have their management report on any known material weaknesses. The Committee recommends that certain micro- and smallcap companies be temporarily exempt from external auditor involvement in the Section 404 process, as long as they comply with corporate governance standards 1-4 in the recommendation above. This would apply to: Smallcap companies that have less than $250 million in annual revenues, but more than $10 million in annual product revenues; and Microcap companies that have between $125 million and $250 million in annual revenues. The internal-controls requirement should be changed to a more cost-effective standard, called ASX, providing for an external audit of internal controls. 11 GERRISH McCREARY SMITH Consultants and Attorneys

38 2. Secondary Recommendations The Committee also recommends that the SEC: Provide additional help with the assessment and design of internal controls, and request that COSO and the PCAOB provide such help as well; Make processes related to internal controls more cost-effective; and Assess if and when it would be advisable to reevaluate and consider amending AS2. The SEC is requested to determine the necessary internal-controls structure so that COSO can strengthen it, in light of COSO s role in the standard-setting process in this type of reporting. The Commission should also ask the PCAOB to address the ability to rely on compensating controls and describe ways to reduce compliance costs related to information technology controls, as well as provide guidance on how management may assess internal controls efficiently and if ASX is required, additional guidance on how management may assess internal controls efficiently and in satisfaction with the requirements of the external auditor. The Commission should also provide additional guidance by clarifying considerations and encouraging cost effectiveness relating to management s design and assessment of internal controls. C. CAPITAL FORMATION, CORPORATE GOVERNANCE AND DISCLOSURE 1. Primary Recommendations In regard to the scaled disclosure accommodations that are currently available to small business issuers under Regulation S-B: Incorporate the accommodations into Regulation S-K; Make the accommodations available to all microcap companies; and Stop prescribing separate specialized disclosure forms for smaller companies. In regard to the primary scaled financial statement accommodations currently available to small business issuers under Regulation S-B: Incorporate them into Regulation S-K or Regulation S-X; and Make them available to all microcap and smallcap companies. Allow all reporting companies on a national securities exchange, NASDAQ or the OTCBB to be eligible to use Form S-3, if: 12 GERRISH McCREARY SMITH Consultants and Attorneys

39 They have been reporting under the Exchange Act for at least one year, and They are current in their reporting at the time of filing. Adopt policies that encourage sharing research on smaller public companies. Adopt a new private-offering exemption from the registration requirements of the Securities Act. This exemption should: Allow more solicitation and advertising, for transactions in which the purchaser does not need all the protections of the Securities Act s registration requirements; and Relax the prohibitions in Rule 502(c) under the Securities Act to parallel the test the waters model of Rule 254 under that Act. Create, in cooperation with other agencies, a streamlined NASD registration process for finders, M&A advisors and institutional private placement practitioners. 2. Secondary Recommendations Amend SEC Rule 12g5-1 to interpret the phrase held of record in Exchange Act Sections 12(g) and 15(d) to mean held by actual beneficial holders. Make information filed under Rule 15c2-11 publicly available. Form a task force to discuss ways to streamline governmental filings. These should include: Standardized filing requirements for filings involving substantially similar information, such as financial statements; and Extending incorporation by reference privileges to other governmental filings containing substantially equivalent information. Allow companies, with full disclosure, to compensate market-makers for working on the filing of a Form 211. Consider upgrading or replacing the EDGAR system, so that smaller public companies can make SEC filings without the need for third party intervention. Make it easier for microcap companies to exit the Exchange Act reporting system. Increase the disclosure threshold of Securities Act Rule 701(e) from $5 million to $20 million. 13 GERRISH McCREARY SMITH Consultants and Attorneys

40 Extend the access equals delivery model to a broader range of SEC filings. Shorten the integration safe harbor from six months to 30 days. Clarify the loan prohibition in Section 402 of the Sarbanes-Oxley Act. Increase uniformity and cooperation between federal and state regulatory systems by: defining the term qualified purchaser in the Securities Act, and making the NASDAQ Capital Market and OTCBB stocks covered securities under NSMIA. Either clarify the interpretation, or amend the language, of the integration safe harbor established under Rule 152. A registered IPO should be allowed to begin immediately after the completion of an otherwise valid private offering, as long as the stated purpose of the private offering was to raise capital with which to fund the IPO process. To help smaller companies, the SEC should: D. ACCOUNTING STANDARDS Commit more resources and professional staff to a help desk to provide assistance to smaller public companies; and Publish guidance on reporting and legal requirements aimed at assisting smaller public companies. 1. Primary Recommendations The Committee recommends developing a safe-harbor protocol for transaction accounting. This should protect preparers from regulatory or legal action when the protocol is appropriately followed in good faith. In implementing new accounting standards, the FASB already allows private companies extended effective dates; these same dates should be allowed to microcap companies. Provide additional guidance for all public companies on the topic of materiality related to previously issued financial statements. Implement a de minimis exception in the application of the SEC s auditor independence rules. 14 GERRISH McCREARY SMITH Consultants and Attorneys

41 2. Secondary Recommendations It is recommended that non-big Four firms be included in committees, public forums, and other venues that would increase the awareness of these firms in the marketplace. This will promote competition and increase the perception of choice in selecting audit firms. The SEC should formally encourage the FASB to continue pursuing objectivesbased accounting standards. Simplicity and ease of application should be key considerations in establishing these standards. The PCAOB should require annual continuing professional education, covering SEC-specific topics, for firms that wish to practice before the SEC. Finally, the SEC should monitor the state of auditor-client interactions in evaluating internal controls over financial reporting; if warranted, take further action to improve the situation. Further Developments Since the Release of the Report. On May 10, 2006, the SEC held round table discussions to take under consideration the recommendations provided to the SEC by its Advisory Committee on Smaller Public Companies. On May 17, 2006, the SEC announced its next step for Sarbanes-Oxley implementation. Specifically, it announced a series of actions it intends to take to improve the implementation of Section 404 in internal control requirements of the Sarbanes-Oxley Act of These actions included issuing SEC guidance for companies and working with the Public Company Accounting Oversight Board ( PCAOB ) on revisions of its internal control auditing standard. It anticipated the actions will also include SEC inspections of PCAOB efforts to improve Section 404 oversight and a brief further postponement of the Section 404 requirements for the smallest company filers. Specific actions taken by the SEC since its round table discussions include: Guidance for Companies. In June 2007, the SEC issued guidance for management on how to complete its assessment of internal control over financial reporting, as required by Section 404(a) of the Sarbanes-Oxley Act. This voluntary guidance addresses identifying financial reporting risks, evaluating risk control measures, and reporting internal control effectiveness. This guidance is available on the SEC s webpage at 15 GERRISH McCREARY SMITH Consultants and Attorneys

42 Revisions to Auditing Standard No. 2. In July 2007, the SEC replaced PCAOB Auditing Standard No. 2 with Auditing Standard No. 5, which provides standards and guidance to independent auditors as they evaluate internal controls over financial reporting under Section 404 of the Sarbanes-Oxley Act. According to the SEC, Auditing Standard No. 5: Reduces the number of mandatory requirements in order to encourage more open and tailored communication with management and audit committees; Scales the complexity of the audit according to the size and complexity of the institution; Eliminates busy work and focuses on matters that will have the greatest impact on the company s internal control over financial reporting; and Adopts a principles-based approach in determining whether to use a third party s work product by considering factors such as objectivity and competence of the third parties. SEC Oversight of PCAOB Inspection Program. As part of the SEC s oversight of the PCAOB, the Commission staff inspects all aspects of the PCAOB s operations, including its inspection program. Among other things, the staff will examine whether the PCAOB inspections of audit firms have been effective encouraging implementation of the principles outlined in the PCAOB s May 1, 2006 statement. Extension of Compliance for Non-accelerated Filers. Due to smaller public companies disproportionate costs of complying with Section 404 of the Sarbanes-Oxley Act, the SEC initially postponed the effective date of its rules implementing Section 404 for smaller public companies (non-accelerated filers). This extension was intended to permit non-accelerated filers and the auditors to have the benefit of the management guidance the SEC issued in In September 2010, the SEC amended its rules pursuant to the Dodd-Frank Act to exempt nonaccelerated filers from the requirements to include an attestation report of the company s public accounting firm in its Annual Report. Non-accelerated filers are still required to include in their Annual Report a Report of Management regarding internal control of financial reporting. In April 2012, the President signed the JOBS Act into law, which mitigates the negative impact of Sarbanes-Oxley on smaller companies. Provisions of the JOBS Act impacting Sarbanes-Oxley include: 16 GERRISH McCREARY SMITH Consultants and Attorneys

43 Shareholder Threshold for Registration (Sections 501 and 601). The JOBS Act amended the Securities Exchange Act of 1934 to increase the securities registration threshold for bank holding companies from 500 shareholders to 2,000 shareholders and increasing the deregistration threshold for bank holding companies from 300 shareholders to 1,200 shareholders. By increasing the registration and deregistration thresholds, the JOBS Act effectively limits Sarbanes- Oxley s applicability to more companies. Exemption for Emerging Growth Companies (Section 102). The JOBS Act exempts companies with less than $1 billion in revenue from Sarbanes-Oxley Section 404(b) requirements for the first five years after the company s initial public offering. Developments in the Director Community In 2008, the National Association of Corporate Directors formulated what they call the Key Agreed Principles to Strengthen Corporate Governance. These principles are rightfully rooted in the desire of long-term value creation for the shareholder, as well as the accountability of management to the board and the board to the shareholders. These Key Agreed Principles to Strengthen Corporate Governance, in no particular order, include: Board Responsibility for Governance This principle emphasizes the fact that the board has the duty to design and implement an effective governance structure. The governance structure should operate in such a way that the board meets and fulfills this duty to the shareholders. Corporate Governance Transparency It is not only the board s responsibility to ensure a governance structure is in place, but also to ensure the highest possible level of transparency in the way that it operates. Oftentimes transparency is more important than the strict adherence to any certain set of best practices recommendations. Director Competency and Commitment The governance structure should be designed in such a way that the competency and commitment of the boar members is constantly guaranteed. 17 GERRISH McCREARY SMITH Consultants and Attorneys

44 Board Accountability and Objectivity The governance structures and practices should also ensure that the board remains ultimately accountable to the shareholders. Furthermore, the objectivity of the directors should also be made certain via the governance structure. Independent Board Leadership The governance structure should be designed in such a way that the board has some form of leadership distinct from members of the management team. Integrity, Ethics, and Responsibility The governance structure should cultivate an appropriate corporate culture that values integrity, ethics, and corporate social responsibility. Attention to Information, Agenda, and Strategy The governance structure and policies should be designed in a way that promotes the determination of board priorities, bearing in mind the obligation to shareholders. The determination of these priorities should produce a subsequent agenda as well as informational needs, and assist in the board s focus on strategy and associated risks. Protection Against Board Entrenchment The governance structure and practice should encourage the board to constantly refresh itself. Shareholder Input in Board Selection The shareholders are to whom the board owes a duty, and as is such, the governance structure should encourage some kind of meaningful involvement on their part in the selection of new directors. Shareholder Communications The governance structure and practices should be designed and implemented in a way that encourages communication with shareholders. These Key Agreed Principles to Strengthen Corporate Governance should act as a sort of checklist for the board in the design and implementation of a governance structure. They are in no way, shape, or form meant to be exhaustive, but they certainly do hit squarely upon what makes for a strong governance structure. G GERRISH McCREARY SMITH Consultants and Attorneys

WSGR ALERT PRESIDENT TO SIGN FINANCIAL OVERHAUL BILL. Corporate Governance and Executive Compensation Update. I. Corporate Governance

WSGR ALERT JULY 2010 PRESIDENT TO SIGN FINANCIAL OVERHAUL BILL Corporate Governance and Executive Compensation Update On July 15, 2010, after months of deliberation, Congress passed a comprehensive financial

WSGR ALERT JULY 2010 PRESIDENT TO SIGN FINANCIAL OVERHAUL BILL Corporate Governance and Executive Compensation Update On July 15, 2010, after months of deliberation, Congress passed a comprehensive financial

Dodd-Frank Corporate Governance

Dodd-Frank Corporate Governance 1 The Dodd-Frank Wall Street Reform and Consumer Protection Act: Executive Compensation and Corporate Governance Reforms, SEC Disclosure and Proxy Access Implications for

Dodd-Frank Corporate Governance 1 The Dodd-Frank Wall Street Reform and Consumer Protection Act: Executive Compensation and Corporate Governance Reforms, SEC Disclosure and Proxy Access Implications for

Vincent A. Vietti Partner

Vincent A. Vietti Partner Princeton, NJ Tel: 609.896.4571 Fax: 609.896.1469 vvietti@foxrothschild.com Vince is an experienced corporate lawyer and is the co-chair of the firm s Public Companies Practice.

Vincent A. Vietti Partner Princeton, NJ Tel: 609.896.4571 Fax: 609.896.1469 vvietti@foxrothschild.com Vince is an experienced corporate lawyer and is the co-chair of the firm s Public Companies Practice.

Corporate Governance and Executive Compensation Provisions in the Dodd-Frank Act

June 29, 2010 Corporate Governance and Executive Compensation Provisions in the Dodd-Frank Act On June 25, 2010, a House and Senate conference committee negotiating the blueprint for the reform of the

June 29, 2010 Corporate Governance and Executive Compensation Provisions in the Dodd-Frank Act On June 25, 2010, a House and Senate conference committee negotiating the blueprint for the reform of the

8/20/2002. Changes from the Initial NYSE Proposal Morrison & Foerster LLP. All Rights Reserved.

NYSE Adopts Changes to its Corporate Governance and Listing Standards; Differences between Current NYSE and Nasdaq Proposals and Sarbanes-Oxley Act Requirements 8/20/2002 Corporate, Financial Institutions

NYSE Adopts Changes to its Corporate Governance and Listing Standards; Differences between Current NYSE and Nasdaq Proposals and Sarbanes-Oxley Act Requirements 8/20/2002 Corporate, Financial Institutions

Comparison of the Frank and Dodd Bills

March 19, 2010 Congressional Watch: Senator Dodd Introduces Financial Stability Bill Calling for SEC Proxy Access Authority and Other Governance and Executive Compensation Reforms On March 15, 2010, Senator

March 19, 2010 Congressional Watch: Senator Dodd Introduces Financial Stability Bill Calling for SEC Proxy Access Authority and Other Governance and Executive Compensation Reforms On March 15, 2010, Senator

The Sarbanes-Oxley Act of 2002: Impact on and Considerations for Financial Institutions

LAST UPDATED SEPTEMBER 20, 2003 : Impact on and Considerations for Financial Institutions Gibson, Dunn & Crutcher LLP Gibson, Dunn & Crutcher lawyers are available to assist clients in addressing any questions

LAST UPDATED SEPTEMBER 20, 2003 : Impact on and Considerations for Financial Institutions Gibson, Dunn & Crutcher LLP Gibson, Dunn & Crutcher lawyers are available to assist clients in addressing any questions

Corporate Governance Under the Dodd-Frank Wall Street Reform & Consumer Protection Act

Corporate Governance Under the Dodd-Frank Wall Street Reform & Consumer Protection Act John Brantley, Partner, Bracewell & Giuliani LLP October 22, 2010 The Law in Context Corporate governance has been

Corporate Governance Under the Dodd-Frank Wall Street Reform & Consumer Protection Act John Brantley, Partner, Bracewell & Giuliani LLP October 22, 2010 The Law in Context Corporate governance has been

ENHANCING SHAREHOLDER VALUE WITH OR WITHOUT SALE

ENHANCING SHAREHOLDER VALUE WITH OR WITHOUT SALE The Role of the Board and Management Organizational Techniques to Enhancing Value The Current M&A Environment Philip K. Smith President Gerrish Smith Tuck,

ENHANCING SHAREHOLDER VALUE WITH OR WITHOUT SALE The Role of the Board and Management Organizational Techniques to Enhancing Value The Current M&A Environment Philip K. Smith President Gerrish Smith Tuck,

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER PURPOSE The purpose of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of First Hawaiian, Inc. (the Company ) is to oversee the accounting and financial

AUDIT COMMITTEE CHARTER PURPOSE The purpose of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of First Hawaiian, Inc. (the Company ) is to oversee the accounting and financial

Jumpstart Our Business Startups Act Makes Significant Changes to Capital Formation, Disclosure and Registration Requirements

Legal Update April 5, 2012 Jumpstart Our Business Startups Act Makes Significant Changes to Capital Formation, The Jumpstart Our Business Startups Act, or JOBS Act, was signed by President Obama on April

Legal Update April 5, 2012 Jumpstart Our Business Startups Act Makes Significant Changes to Capital Formation, The Jumpstart Our Business Startups Act, or JOBS Act, was signed by President Obama on April

Course Materials ENHANCING SHAREHOLDER VALUE: WITH OR WITHOUT SALE

Course Materials ENHANCING SHAREHOLDER VALUE: WITH OR WITHOUT SALE Philip K. Smith President, PC Memphis, Tennessee psmith@gerrish.com 91-767-9 July 31 August 2, 217 Enhancing Shareholder Value: With

Course Materials ENHANCING SHAREHOLDER VALUE: WITH OR WITHOUT SALE Philip K. Smith President, PC Memphis, Tennessee psmith@gerrish.com 91-767-9 July 31 August 2, 217 Enhancing Shareholder Value: With

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF MINERALS TECHNOLOGIES INC.

I. PURPOSE The primary purposes of the Audit Committee (the Committee ) are to: 1. Assist the Board of Directors (the Board ) in its oversight of (i) the integrity of the Company s financial statements,

I. PURPOSE The primary purposes of the Audit Committee (the Committee ) are to: 1. Assist the Board of Directors (the Board ) in its oversight of (i) the integrity of the Company s financial statements,

Co r p o r at e a n d

Co r p o r at e a n d Securities Law Update July 2010 Analysis of the Dodd-Frank Wall Street Reform Act Executive Compensation, Corporate Governance and Enforcement Provisions of the Dodd-Frank Act Affecting

Co r p o r at e a n d Securities Law Update July 2010 Analysis of the Dodd-Frank Wall Street Reform Act Executive Compensation, Corporate Governance and Enforcement Provisions of the Dodd-Frank Act Affecting

Foreign Private Issuers and the Corporate Governance and Disclosure Provisions

Electronically reprinted from Volume 24 Number 9, September 2010 Foreign Private Issuers and the Corporate Governance and Disclosure Provisions While the impact of the executive compensation and corporate

Electronically reprinted from Volume 24 Number 9, September 2010 Foreign Private Issuers and the Corporate Governance and Disclosure Provisions While the impact of the executive compensation and corporate

Impacts of the Dodd-Frank Wall Street Reform and Consumer Protection Act on Executive Compensation and Corporate. Governance THOUGHT LEADERSHIP

THOUGHT LEADERSHIP Alerts Service Securities & Corporate Governance Professionals Craig A. Adoor St. Louis: 314.345.6407 craig.adoor@ James M. Ash Kansas City: 816.983.8137 james.ash@ Steven R. Barrett

THOUGHT LEADERSHIP Alerts Service Securities & Corporate Governance Professionals Craig A. Adoor St. Louis: 314.345.6407 craig.adoor@ James M. Ash Kansas City: 816.983.8137 james.ash@ Steven R. Barrett

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER Purpose: The Audit Committee (the Committee ) is a standing committee of the Board. The Committee s purpose is to assist the Board in carrying out its oversight responsibilities

AUDIT COMMITTEE CHARTER Purpose: The Audit Committee (the Committee ) is a standing committee of the Board. The Committee s purpose is to assist the Board in carrying out its oversight responsibilities

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS These Frequently Asked Questions should be read together with our Frequently Asked Questions

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS These Frequently Asked Questions should be read together with our Frequently Asked Questions

TCG BDC II, INC. AUDIT COMMITTEE CHARTER. the quality and integrity of the Company s financial statements;

TCG BDC II, INC. AUDIT COMMITTEE CHARTER I. PURPOSE The purposes of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of TCG BDC II, Inc. and its subsidiaries (collectively, the

TCG BDC II, INC. AUDIT COMMITTEE CHARTER I. PURPOSE The purposes of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of TCG BDC II, Inc. and its subsidiaries (collectively, the

FANNIE MAE CORPORATE GOVERNANCE GUIDELINES

FANNIE MAE CORPORATE GOVERNANCE GUIDELINES 1. The Roles and Responsibilities of the Board and Management On September 6, 2008, the Director of the Federal Housing Finance Authority, or FHFA, our safety

FANNIE MAE CORPORATE GOVERNANCE GUIDELINES 1. The Roles and Responsibilities of the Board and Management On September 6, 2008, the Director of the Federal Housing Finance Authority, or FHFA, our safety

NASD and NYSE Rulemaking: Relating to Corporate Governance

Home Previous Page NASD and NYSE Rulemaking: Relating to Corporate Governance SECURITIES AND EXCHANGE COMMISSION (Release No. 34-48745; File Nos. SR-NYSE-2002-33, SR-NASD-2002-77, SR- NASD-2002-80, SR-NASD-2002-138,

Home Previous Page NASD and NYSE Rulemaking: Relating to Corporate Governance SECURITIES AND EXCHANGE COMMISSION (Release No. 34-48745; File Nos. SR-NYSE-2002-33, SR-NASD-2002-77, SR- NASD-2002-80, SR-NASD-2002-138,

Executive Compensation and the Wall Street Reform and Consumer Protection Act

A Timely Analysis of Legal Developments In This Issue: July 2010 On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173), which is primarily

A Timely Analysis of Legal Developments In This Issue: July 2010 On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173), which is primarily

The Dodd-Frank Wall Street Reform and Consumer Protection Act

07.27.2010 The Dodd-Frank Wall Street Reform and Consumer Protection On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection (the ). The primary objective

07.27.2010 The Dodd-Frank Wall Street Reform and Consumer Protection On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection (the ). The primary objective

The following shall be the principal recurring duties of the Committee in carrying out its oversight responsibility.

AEVI GENOMIC MEDICINE, INC. AUDIT COMMITTEE CHARTER 1. PURPOSE The Audit Committee (the Committee ) of the Board of Directors (the Board ) of Aevi Genomic Medicine, Inc. (the Company ) has the oversight

AEVI GENOMIC MEDICINE, INC. AUDIT COMMITTEE CHARTER 1. PURPOSE The Audit Committee (the Committee ) of the Board of Directors (the Board ) of Aevi Genomic Medicine, Inc. (the Company ) has the oversight

MONDELĒZ INTERNATIONAL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER. Effective January 26, 2015

Purpose. MONDELĒZ INTERNATIONAL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER Effective January 26, 2015 The Audit Committee (the Committee ) of the Board of Directors (the Board ) of Mondelēz International,

Purpose. MONDELĒZ INTERNATIONAL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER Effective January 26, 2015 The Audit Committee (the Committee ) of the Board of Directors (the Board ) of Mondelēz International,

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS PURPOSE The primary purpose of the Audit Committee (the Committee ) is to assist the Board of Directors (the Board ) in fulfilling

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS PURPOSE The primary purpose of the Audit Committee (the Committee ) is to assist the Board of Directors (the Board ) in fulfilling

EXECUTIVE COMPENSATION AND CORPORATE GOVERNANCE PROVISIONS IN THE DODD-FRANK U.S. FINANCIAL REGULATORY REFORM BILL

June 30, 2010 EXECUTIVE COMPENSATION AND CORPORATE GOVERNANCE PROVISIONS IN THE DODD-FRANK U.S. FINANCIAL REGULATORY REFORM BILL To Our Clients and Friends: On June 30, 2010, the U.S. House of Representatives

June 30, 2010 EXECUTIVE COMPENSATION AND CORPORATE GOVERNANCE PROVISIONS IN THE DODD-FRANK U.S. FINANCIAL REGULATORY REFORM BILL To Our Clients and Friends: On June 30, 2010, the U.S. House of Representatives

CHARTER OF AUDIT COMMITTEE OF THE BOARD OF DIRECTORS (as amended through November 13, 2012)

") CENTURYLINK, INC. CHARTER OF AUDIT COMMITTEE OF THE BOARD OF DIRECTORS (as amended through November 13, 2012) I. SCOPE OF RESPONSIBILITY A. General Subject to the limitations noted in Section VI, the primary

CENTURYLINK, INC. CHARTER OF AUDIT COMMITTEE OF THE BOARD OF DIRECTORS (as amended through November 13, 2012) I. SCOPE OF RESPONSIBILITY A. General Subject to the limitations noted in Section VI, the primary

Act language and concepts. David T. Mittelman

The Sarbanes-Oxley Act language and concepts David T. Mittelman The Sarbanes-Oxley Act of 2002 Public Company Accounting Reform and Corporate Responsibility Generally seen as the most comprehensive revision

The Sarbanes-Oxley Act language and concepts David T. Mittelman The Sarbanes-Oxley Act of 2002 Public Company Accounting Reform and Corporate Responsibility Generally seen as the most comprehensive revision

AUDIT COMMITTEE CHARTER OF KBR, INC. (as of December 7, 2016)

") AUDIT COMMITTEE CHARTER OF KBR, INC. (as of December 7, 2016) Article I. Purpose The Audit Committee (the Committee ) of KBR, Inc. (the Corporation ) is appointed by the Board of Directors of the Corporation

AUDIT COMMITTEE CHARTER OF KBR, INC. (as of December 7, 2016) Article I. Purpose The Audit Committee (the Committee ) of KBR, Inc. (the Corporation ) is appointed by the Board of Directors of the Corporation

Requirements for Public Company Boards

Public Company Advisory Group Requirements for Public Company Boards Including IPO Transition Rules November 2016 Introduction. 1 The Role and Authority of Independent Directors. 2 The Definition of Independent

Public Company Advisory Group Requirements for Public Company Boards Including IPO Transition Rules November 2016 Introduction. 1 The Role and Authority of Independent Directors. 2 The Definition of Independent

The principal purposes of the Audit Committee (Committee) of the Board of Directors (Board) of Vistra Energy Corp.

of the Board of Directors (Board) of Vistra Energy Corp.") VISTRA ENERGY CORP. AUDIT COMMITTEE CHARTER I. PURPOSES OF THE COMMITTEE The principal purposes of the Audit Committee (Committee) of the Board of Directors (Board) of Vistra Energy Corp. (Company) are

VISTRA ENERGY CORP. AUDIT COMMITTEE CHARTER I. PURPOSES OF THE COMMITTEE The principal purposes of the Audit Committee (Committee) of the Board of Directors (Board) of Vistra Energy Corp. (Company) are

Fried, Frank, Harris, Shriver & Jacobson August 26, 2003

August 26, 2003 Timeline Effective Dates for Implementing The Sarbanes-Oxley Act of 2002 ("SOX") and New and Proposed SEC, NYSE & Nasdaq Rules for Non-U.S. Issuers Disclosure 1. CEO/CFO certification A.

August 26, 2003 Timeline Effective Dates for Implementing The Sarbanes-Oxley Act of 2002 ("SOX") and New and Proposed SEC, NYSE & Nasdaq Rules for Non-U.S. Issuers Disclosure 1. CEO/CFO certification A.

SEC PUBLISHES FINAL RULES REGARDING AUDITOR INDEPENDENCE

January 31, 2003 SEC PUBLISHES FINAL RULES REGARDING AUDITOR INDEPENDENCE On January 28, 2003, the SEC published its final rules pursuant to Section 208 of the Sarbanes- Oxley Act of 2002 (the Act ), which

January 31, 2003 SEC PUBLISHES FINAL RULES REGARDING AUDITOR INDEPENDENCE On January 28, 2003, the SEC published its final rules pursuant to Section 208 of the Sarbanes- Oxley Act of 2002 (the Act ), which

NYSE, NASDAQ and AMEX Publish Final Corporate Governance Rules

CORPORATE GOVERNANCE UPDATE DECEMBER 2003 NYSE, NASDAQ and AMEX Publish Final Corporate Governance Rules NYSE, NASDAQ and AMEX (the "SROs") have each recently published their final corporate governance

CORPORATE GOVERNANCE UPDATE DECEMBER 2003 NYSE, NASDAQ and AMEX Publish Final Corporate Governance Rules NYSE, NASDAQ and AMEX (the "SROs") have each recently published their final corporate governance

Sarbanes-Oxley Act. The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S. Issuers.

Sarbanes-Oxley Act The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S. Issuers www.lw.com Sarbanes-Oxley REPORT September 1, 2004 The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S.

Sarbanes-Oxley Act The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S. Issuers www.lw.com Sarbanes-Oxley REPORT September 1, 2004 The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S.

Q&A on the Dodd-Frank Wall Street Reform and Consumer Protection Act

27 July 2010 Financial Regulatory Reform Q&A on the Dodd-Frank Wall Street Reform and Consumer Protection Act What is the status of the Dodd-Frank Act? The Dodd-Frank Wall Street Reform and Consumer Protection

27 July 2010 Financial Regulatory Reform Q&A on the Dodd-Frank Wall Street Reform and Consumer Protection Act What is the status of the Dodd-Frank Act? The Dodd-Frank Wall Street Reform and Consumer Protection

New NYSE and NASDAQ Listing Rules Raise the Accountability of Company Boards and Compensation Committees Through Flexible Standards

New NYSE and NASDAQ Listing Rules Raise the Accountability of Company Boards and Compensation Committees Through Flexible Standards By Todd B. Pfister and Aubrey Refuerzo* On January 11, 2013, the U.S.

New NYSE and NASDAQ Listing Rules Raise the Accountability of Company Boards and Compensation Committees Through Flexible Standards By Todd B. Pfister and Aubrey Refuerzo* On January 11, 2013, the U.S.

FREQUENTLY ASKED QUESTIONS ABOUT RULE 144A EQUITY OFFERINGS

FREQUENTLY ASKED QUESTIONS ABOUT RULE 144A EQUITY OFFERINGS These FAQs relate specifically to Rule 144A equity offerings. Please refer to our Frequently Asked Questions About Rule 144A generally, and our

FREQUENTLY ASKED QUESTIONS ABOUT RULE 144A EQUITY OFFERINGS These FAQs relate specifically to Rule 144A equity offerings. Please refer to our Frequently Asked Questions About Rule 144A generally, and our

EVINE LIVE INC. AUDIT COMMITTEE CHARTER

EVINE LIVE INC. AUDIT COMMITTEE CHARTER I. PURPOSE, DUTIES, and RESPONSIBILITIES The audit committee (the Committee ) is established by the board of directors (the board ) of EVINE Live Inc. (the company

EVINE LIVE INC. AUDIT COMMITTEE CHARTER I. PURPOSE, DUTIES, and RESPONSIBILITIES The audit committee (the Committee ) is established by the board of directors (the board ) of EVINE Live Inc. (the company

Corporate Governance After the Dodd-Frank Act: Recent Developments

Corporate Governance After the Dodd-Frank Act: Recent Developments John C. Coffee, Jr. Cape Town, South Africa IOSCO Annual Meeting April, 2011 Slide 1 MAJOR DEVELOPMENTS 1. Proxy Access: 3% can now propose

Corporate Governance After the Dodd-Frank Act: Recent Developments John C. Coffee, Jr. Cape Town, South Africa IOSCO Annual Meeting April, 2011 Slide 1 MAJOR DEVELOPMENTS 1. Proxy Access: 3% can now propose

Meridian Client Update

VOLUME 3, ISSUE 13R OCTOBER 10, 2012 Meridian Client Update NYSE and NASDAQ Issue Proposed Listing Rules on Compensation Committee Independence Standards Over two years after the enactment of the Dodd-Frank

VOLUME 3, ISSUE 13R OCTOBER 10, 2012 Meridian Client Update NYSE and NASDAQ Issue Proposed Listing Rules on Compensation Committee Independence Standards Over two years after the enactment of the Dodd-Frank

SEC Proposes Say-on-Pay Rules

Securities Alert NOVEMBER 23 2010 SEC Proposes Say-on-Pay Rules Advisory Votes on Executive Compensation and Golden Parachute Compensation, and Frequency of the Executive Compensation Vote BY MEGAN N.

Securities Alert NOVEMBER 23 2010 SEC Proposes Say-on-Pay Rules Advisory Votes on Executive Compensation and Golden Parachute Compensation, and Frequency of the Executive Compensation Vote BY MEGAN N.

AVERY DENNISON CORPORATION AUDIT AND FINANCE COMMITTEE CHARTER *

AVERY DENNISON CORPORATION AUDIT AND FINANCE COMMITTEE CHARTER * Purpose The Audit & Finance Committee ( Committee ) is appointed by the Board to assist the Board with its oversight responsibilities in

AVERY DENNISON CORPORATION AUDIT AND FINANCE COMMITTEE CHARTER * Purpose The Audit & Finance Committee ( Committee ) is appointed by the Board to assist the Board with its oversight responsibilities in

Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession. Learning Objective 2-1

Chapter 2 The CPA Profession. Learning Objective 2-1") Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of: A) each state. B) the Financial

Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of: A) each state. B) the Financial

not have participated in the preparation of the Company s or any of its subsidiaries financial statements at any time during the past three years;

SABRE CORPORATION AUDIT COMMITTEE CHARTER I. Statement of Purpose The Audit Committee (the Committee ) is a standing committee of the Board of Directors (the Board ). The purpose of the Committee is to

SABRE CORPORATION AUDIT COMMITTEE CHARTER I. Statement of Purpose The Audit Committee (the Committee ) is a standing committee of the Board of Directors (the Board ). The purpose of the Committee is to

Audit, Finance & Risk Committee TERMS OF REFERENCE FOR THE AUDIT, FINANCE & RISK COMMITTEE

TERMS OF REFERENCE FOR THE AUDIT, FINANCE & RISK COMMITTEE I. CONSTITUTION There shall be a committee, to be known as the (the Committee ), of the Board of Directors (the Board ) of Enbridge Inc. (the

TERMS OF REFERENCE FOR THE AUDIT, FINANCE & RISK COMMITTEE I. CONSTITUTION There shall be a committee, to be known as the (the Committee ), of the Board of Directors (the Board ) of Enbridge Inc. (the

GENESIS ENERGY, LLC BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER

GENESIS ENERGY, LLC BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER I. PURPOSE The Audit Committee (the Committee ) is appointed by the board of managers (the Board, and each member of the Board, a director

GENESIS ENERGY, LLC BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER I. PURPOSE The Audit Committee (the Committee ) is appointed by the board of managers (the Board, and each member of the Board, a director

A Director s Guide to the Final Nasdaq Corporate Governance Rules. Table of Contents. Introduction and Use of this Guide.. 3

Table of Contents Introduction and Use of this Guide.. 3 Implementation of New Rules 4 Board of Directors Provisions.... 4 Majority Independent Directors and Independence Definition Executive Sessions

Table of Contents Introduction and Use of this Guide.. 3 Implementation of New Rules 4 Board of Directors Provisions.... 4 Majority Independent Directors and Independence Definition Executive Sessions

CORPORATE GOVERNANCE POLICIES AND PROCEDURES MANUAL OCTOBER 27, 2016

CORPORATE GOVERNANCE POLICIES AND PROCEDURES MANUAL OCTOBER 27, 2016 - 2 - TASEKO MINES LIMITED (the Company ) Corporate Governance Policies and Procedures Manual (the Manual ) Amended Effective October

CORPORATE GOVERNANCE POLICIES AND PROCEDURES MANUAL OCTOBER 27, 2016 - 2 - TASEKO MINES LIMITED (the Company ) Corporate Governance Policies and Procedures Manual (the Manual ) Amended Effective October

SARAH E. COGAN, CYNTHIA COBDEN, BRYNN D. PELTZ, DAVID E. WOHL & MARISA VAN DONGEN

SEC ADOPTS FINAL RULES APPLICABLE TO REGISTERED INVESTMENT COMPANIES UNDER THE SARBANES-OXLEY ACT: SHAREHOLDER REPORTS, FINANCIAL EXPERTS AND CODES OF ETHICS SARAH E. COGAN, CYNTHIA COBDEN, BRYNN D. PELTZ,

SEC ADOPTS FINAL RULES APPLICABLE TO REGISTERED INVESTMENT COMPANIES UNDER THE SARBANES-OXLEY ACT: SHAREHOLDER REPORTS, FINANCIAL EXPERTS AND CODES OF ETHICS SARAH E. COGAN, CYNTHIA COBDEN, BRYNN D. PELTZ,

DIAMOND OFFSHORE DRILLING, INC. AUDIT COMMITTEE CHARTER

DIAMOND OFFSHORE DRILLING, INC. AUDIT COMMITTEE CHARTER (as amended and restated on February 2, 2018) Purpose The primary function of the Audit Committee (the Committee ) is to assist the Board of Directors

DIAMOND OFFSHORE DRILLING, INC. AUDIT COMMITTEE CHARTER (as amended and restated on February 2, 2018) Purpose The primary function of the Audit Committee (the Committee ) is to assist the Board of Directors

Dodd-Frank Application of Corporate Governance, Securities Reform and Disclosure Requirements to Public Companies

Dodd-Frank Application of Corporate Governance, Securities Reform and Disclosure Requirements to Public Companies September 29, 2010 Overview The scope of the recently enacted Dodd-Frank Wall Street Reform

Dodd-Frank Application of Corporate Governance, Securities Reform and Disclosure Requirements to Public Companies September 29, 2010 Overview The scope of the recently enacted Dodd-Frank Wall Street Reform

PDC ENERGY, INC. AUDIT COMMITTEE CHARTER. Amended and Restated September 18, 2015

PDC ENERGY, INC. AUDIT COMMITTEE CHARTER Amended and Restated September 18, 2015 1. Purpose. The Board of Directors (the Board ) of PDC Energy, Inc. (the Company ) has duly established the Audit Committee

PDC ENERGY, INC. AUDIT COMMITTEE CHARTER Amended and Restated September 18, 2015 1. Purpose. The Board of Directors (the Board ) of PDC Energy, Inc. (the Company ) has duly established the Audit Committee

As revised at the September 23, 2013 Board of Directors Meeting

As revised at the September 23, 2013 Board of Directors Meeting PURPOSE The Audit and Finance Committee ( AFC ) is appointed by the Board of Directors (the Board ) to assist the Board (1) in fulfilling

As revised at the September 23, 2013 Board of Directors Meeting PURPOSE The Audit and Finance Committee ( AFC ) is appointed by the Board of Directors (the Board ) to assist the Board (1) in fulfilling

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER Purpose The Audit Committee is appointed by the Board of Directors (the Board ) to assist the Board in monitoring (1) the integrity of the financial statements of the Company, (2)

AUDIT COMMITTEE CHARTER Purpose The Audit Committee is appointed by the Board of Directors (the Board ) to assist the Board in monitoring (1) the integrity of the financial statements of the Company, (2)

Audit Committee Charter

ESTERLINE TECHNOLOGIES CORPORATION Audit Committee Charter Purpose and Authority It is the policy of this Company to have an Audit Committee (the Committee ) of the Board of Directors to assist the Board

ESTERLINE TECHNOLOGIES CORPORATION Audit Committee Charter Purpose and Authority It is the policy of this Company to have an Audit Committee (the Committee ) of the Board of Directors to assist the Board

SEC Approves Changes to NYSE s and Nasdaq s Listing Standards Regarding Compensation Committees and Compensation Advisers

SEC Approves Changes to NYSE s and Nasdaq s Listing Standards Regarding Compensation Committees and Compensation Advisers The Securities and Exchange Commission ( SEC ) recently approved rule changes to

SEC Approves Changes to NYSE s and Nasdaq s Listing Standards Regarding Compensation Committees and Compensation Advisers The Securities and Exchange Commission ( SEC ) recently approved rule changes to

Sarbanes-Oxley Update: Impact on Public Companies, Management, and Audit Committees. W. Lynn Loden Deloitte & Touche LLP

Sarbanes-Oxley Update: Impact on Public Companies, Management, and Audit Committees W. Lynn Loden Deloitte & Touche LLP Dynamic and Defining Times The Sarbanes-Oxley Act of 2002 (the Act ) Unprecedented

Sarbanes-Oxley Update: Impact on Public Companies, Management, and Audit Committees W. Lynn Loden Deloitte & Touche LLP Dynamic and Defining Times The Sarbanes-Oxley Act of 2002 (the Act ) Unprecedented

2018 proxy statements

SEC Financial Reporting Series 2018 proxy statements An overview of the requirements and observations about current practice Contents 1 Overview... 1 1.1 Section highlights... 2 1.2 EY publications and

SEC Financial Reporting Series 2018 proxy statements An overview of the requirements and observations about current practice Contents 1 Overview... 1 1.1 Section highlights... 2 1.2 EY publications and

UNITEDHEALTH GROUP BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER (November 8, 2016)

") UNITEDHEALTH GROUP BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER (November 8, 2016) INTRODUCTION AND PURPOSE UnitedHealth Group Incorporated (the "Company") is a publicly-held company and operates in a complex,

UNITEDHEALTH GROUP BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER (November 8, 2016) INTRODUCTION AND PURPOSE UnitedHealth Group Incorporated (the "Company") is a publicly-held company and operates in a complex,

SEC ISSUES FINAL RULES FOR AUDIT COMMITTEES OF LISTED COMPANIES

CLIENT MEMORANDUM SEC ISSUES FINAL RULES FOR AUDIT COMMITTEES OF LISTED COMPANIES Last week, the Securities and Exchange Commission (the SEC ) issued final rules 1 to implement Section 301 of the Sarbanes-Oxley

CLIENT MEMORANDUM SEC ISSUES FINAL RULES FOR AUDIT COMMITTEES OF LISTED COMPANIES Last week, the Securities and Exchange Commission (the SEC ) issued final rules 1 to implement Section 301 of the Sarbanes-Oxley