BY CA MAYUR B NAYAK 1

|

|

|

- Harriet Patrick

- 5 years ago

- Views:

Transcription

1 BY CA MAYUR B NAYAK 1

2 Govt. should collect taxes from citizens the way a Bee collects Honey from the flowers - quietly without inflicting pain". -Chanakya BY CA MAYUR B NAYAK 2

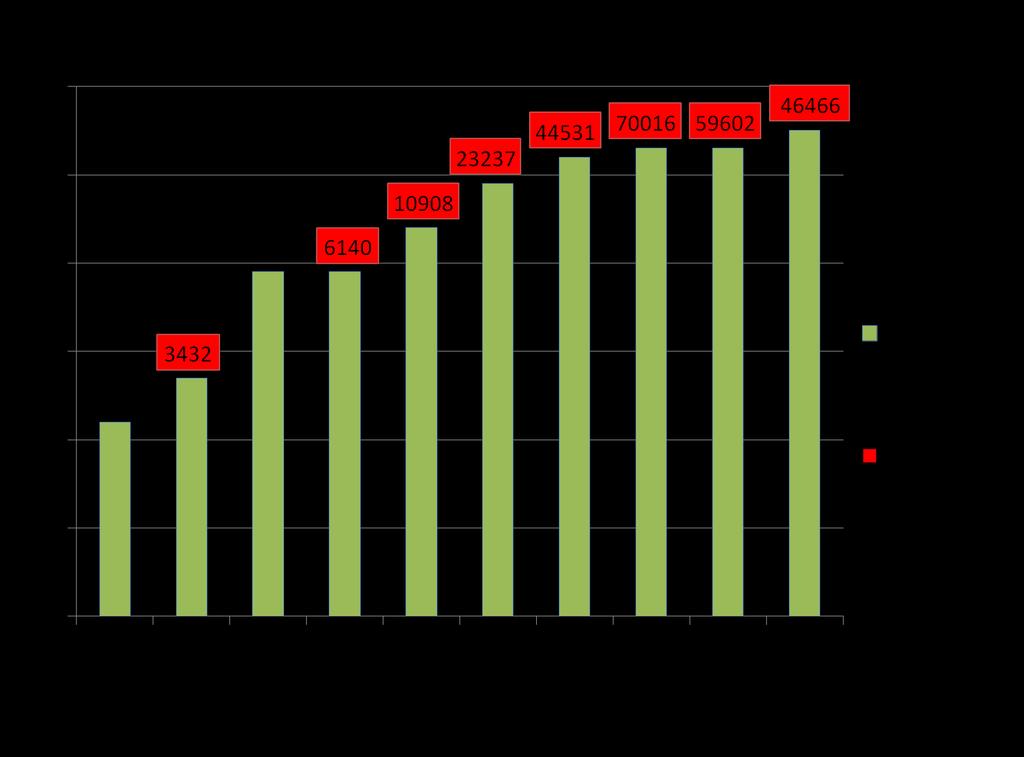

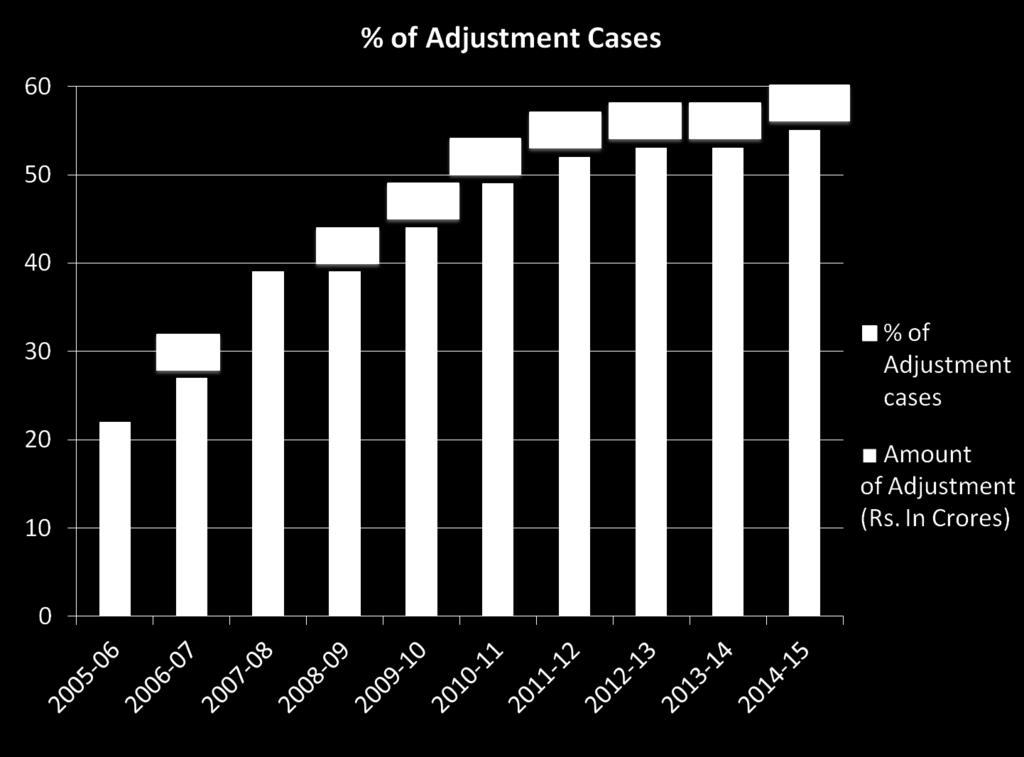

3 Financial Year Transfer pricing adjustments done in India No. of TP audits completed No of Adjustment cases % of Adjustment cases Amount of Adjustment (Rs. In Crore)

4

5 BY CA MAYUR B NAYAK 5

6 Introduction with effect from 1 st April 2012 Specified Domestic Transactions (SDT) between related parties exceeding Rs. 20 crore SDTs subject to Transfer Pricing Regulations as applicable to International Transactions Bench mark transactions using methods prescribed for Arm s Length Price (ALP) BY CA MAYUR B NAYAK 6

7 The genesis of DTP can be traced to the Supreme Court s decision in case of CIT v. Glaxo Smithkline Asia Pvt. Ltd. [26 th Oct. 2010] Existing provisions to curb the misuse of tax holiday provisions were arbitrary and insufficient. New provisions are expected to provide certainty and methods for determining ALP. Protecting the revenue of the Indian Government. BY CA MAYUR B NAYAK 7

8 CIT v. Glaxo Smithkline Asia Pvt. Ltd Facts Glaxo SmithKline (Asia) Reimbursement of cost* plus 5% Provides Finance, Marketing, Hr related Services Glaxo Smith Kline Consumer Healthcare Ltd ( GSKCH ) NOT Covered u/s 40A(2) *Cost towards services suggested by Firm of CAs BY CA MAYUR B NAYAK 8

9 Assessing Officer s Contention The reimbursement of cost by assessee is excessive or unreasonable and not for business purpose. Thus, he was of the opinion that part of the charges reimbursed is to be disallowed Held That No interference is called for as this exercise is revenue neutral Tribunal deleted the disallowance on the ground that there was no provision to disallow expenditure on the ground that it was excessive or unreasonable unless the case of the assessee falls within the scope of section 40A(2) BY CA MAYUR B NAYAK 9

10 COMPANY A - DISTRIBUTOR OF ROUGH DIAMONDS Goods/ Services TRANSFER SHOULD BE DONE AT ALP AE OF A COMPANY B MANUFACTURER OF POLISHED DIAMONDS USA INDIA AE Associated Enterprise ALP Arm s length price BY CA MAYUR B NAYAK 10

11 INDIA INDIA Shifting of Expenses/ Losses Company A Enjoying tax holiday - SEEPZ Related enterprise- Company B in Domestic tariff Area Shifting of Income/ Profits Tax Saving to the Group - Loss to Indian Revenue BY CA MAYUR B NAYAK 11

12 Particulars Co. A (Tax holiday) Income Income from related party Expenses Expense to related party CASE 1 : ALP - Co. B (Normal rates of tax) 200 Profit/ Loss Tax rate applicable 0% 32.45% Tax (200*32.45%) Tax to the group Particulars CASE 2 : Non ALP Co. A (Tax holiday) Income Income from related party Expenses Expense to related party Profit/ Loss Co. B (Normal rates of tax) 400 Tax rate applicable 0% 32.45% Tax - - Tax to the group NIL Tax saving to group- Loss to Indian Revenue BY CA MAYUR B NAYAK 12

13 Intent of TP Regulations INDIA INDIA Shifting of Expenses/ Losses Company A Loss Making Related enterprise- Company B in Domestic tariff Area Shifting of Income/ Profits Tax Saving to the Group - Loss to Indian Revenue BY CA MAYUR B NAYAK 13

200 Tax rate applicable 32.45% 32.45% Tax - 64.")

14 CASE 1: ALP NORMAL RATE OF TAX APPLICABLE TO BOTH THE COMPANIES (Both Cos. are in DTA) CASE 2 : Non ALP Particulars Co. A Co. B Particulars Co. A Co. B Income Income from related party Expenses Expense to related party Profit/ Loss (200) 200 Tax rate applicable 32.45% 32.45% Tax (200*32.45%) Tax to the group Income Income from related party Expenses Expense to related party Profit/ Loss (100) 100 Tax rate applicable 32.45% 32.45% Tax (100*32.45%) Tax to the group BY CA MAYUR B NAYAK

15 any expenditure in respect of which payment has been made or is to be made to a person referred to in 40A(2)(b) any of these transactions, not being an international transaction any transaction referred to in section 80A any transfer of goods or services referred to in section 80-IA(8) any business transacted between the assessee and other person as referred to in 80-IA(10) any transaction, referred to in any other section under Chapter VI-A or section 10AA, to which provisions of section 80-IA(8) or 80 IA(10) are applicable any other transaction as may be prescribed Y CA MAYUR B NAYAK aggregate of such transactions in the previous year exceeds a sum of twenty crore rupees 15

16 Section 40A(2)(b)(i): any relative ASSESSEE (INDIVIDUAL) RELATIVE Section 40A(2)(b)(ii): any director of the co. or any relative of such director COMPANY DIRECTOR MR. A RELATIVE MRS. A Covered transaction BY CA MAYUR B NAYAK 16

17 ASSESSEE 20% or more voting power or profits INDIVIDUAL HAVING SUBSTANTIAL INTEREST MR. A RELATIVE OF MR. A Covered transaction Section 40A(2)(b)(iii): Any individual or relative of the individual having substantial interest in the business or profession of the assessee BY CA MAYUR B NAYAK 17

(b)(iv): any company having substantial interest in business or profession of the assessee or")

18 ASSESSEE 20% or more voting power or profits COMPANY A HAVING SUBSTANTIAL INTEREST Covered transaction DIRECTOR MR. B RELATIVE OF MR. B COMPANY C COMPANY A HAVING SUBSTANTIAL INTEREST 20% or more voting power or profits Section 40A(2)(b)(iv): any company having substantial interest in business or profession of the assessee or director of such company or any relative of such director or any other Co. in which first mentioned Co. has substantial interest BY CA MAYUR B NAYAK 18

19 ASSESSEE 20% or more voting power or profits MR. A HAVING SUBSTANTIAL INTEREST- DIRECTOR OF COMPANY A RELATIVE OF MR. A Covered transactions ANY OTHER DIRECTOR OF COMPANY A - MR. B RELATIVE OF MR. B Section 40A(2)(b)(v): A company of which a director has a substantial interest in business or profession of the assessee or any director of such company or any relative of such director BY CA MAYUR B NAYAK 19

20 ANY PERSON HAVING BUSINESS OR PROFESSION 20% or more voting power or profits ASSESSEE MR A HAVING SUBSTANTIAL INTEREST OR RELATIVE OF MR A HAVING SUBSTANTIAL INTEREST Section 40A(2)(b)(vi): (A) any person who carries on a business or profession where the assessee (individual) or any relative of such individual has substantial interest BY CA MAYUR B NAYAK 20

21 ANY PERSON HAVING BUSINESS OR PROFESSION 20% or more voting power or profits 20% or more voting power or profits 20% or more voting power or profits ASSESSEE COMPANY A HAVING SUBSTANTIAL INTEREST OR DIRECTOR OF COMPANY A -MR B HAVING SUBSTANTIAL INTEREST OR RELATIVE OF MR. B - HAVING SUBSTANTIAL INTEREST Section 40A(2)(b)(vi): (B) any person who carries on a business or profession where the assessee (company) or any director or any relative of such director has substantial interest BY CA MAYUR B NAYAK 21

22 Co. A Co. B Co. C Co. D Co. E BY CA MAYUR B NAYAK 22

23 Co. A & Co. B =? Co. A & Co. C =? Co. B & Co. C =? Co. B & Co. D =? Co. C & Co. E =? Co. A & Co. D =? Co. A & Co. E =? Co. D & Co. E =? Co. C & Co. D =? Co. B & Co. E =? BY CA MAYUR B NAYAK 23

24 Anti-avoidance provision Transactions of goods or services by the assessee between its two businesses one of which is eligible for a tax holiday and the other not so eligible must be at market value Rationale - To prevent assessee from inflating profits in a tax holiday unit, undertaking or a company and showing losses in non-tax holiday enterprises. BY CA MAYUR B NAYAK 24

25 Where any goods or services held for the purposes of the eligible business are transferred to any other business carried on by the assessee, or where any goods or services held for the purposes of any other business carried on by the assessee are transferred to the eligible business and, in either case, the consideration, if any, for such transfer as recorded in the accounts of Where it appears to the assessing officer that, owing to the close connection between the assessee carrying on the eligible business to which this section applies and any other person, or for any other reason, the course of business between them is so arranged that the business transacted between them produces to the assessee more than the the eligible business does not ordinary profits which might be correspond to the market value of such goods or services as on the date transfer, then, for the purpose of the expected to arise in such eligible business, the Assessing Officer shall, in computing the profits and gains of deduction under this section, the such eligible business for the profits and gains of such eligible business shall be computed as if the transfer, in either, had been made at the market value of such goods or services as on that date. purposes of the deduction under this section, take the amount of profits as may be reasonably deemed to have been derived therefrom. 25 BY CA MAYUR B NAYAK

26 Applicability: Goods or services held by the eligible business are transferred to any other business carried on by the assessee or goods or services held by any other business of the assessee are transferred to the eligible business. The consideration for such transfer as recorded in the accounts of the eligible business must correspond to the market value of such goods or services. BY CA MAYUR B NAYAK 26

27 In relation to any goods or services sold or supplied (Table A) The price that such goods or services would fetch if these were sold by the undertaking or unit or enterprise or eligible business in the open market, subject to statutory or regulatory restrictions, if any. In relation to any goods or services acquired (Table B) The price that such goods or services would cost if these were acquired by the undertaking or unit or enterprise or eligible business from the open market, subject to statutory or regulatory restrictions, if any. For value > Rs. 20 Crore (Table C) In relation to any goods or services sold, supplied or acquired means the arm's length price as defined in clause (ii) of section 92F of such goods or services, if it is a specified domestic transaction referred to in section 92BA. Provisions of Table A and B would continue to apply to all transactions below Rs. 20 Cr. as provisions of DTP would apply to transactions exceeding Rs. 20 Cr. w.e.f. A.Y BY CA MAYUR B NAYAK BACK 27

28 FMV ALP No method Documentation is not required Tax Audit report Assessing Officer Six methods Documentation is required Report of an accountant to be furnished u/s 92E BY CA MAYUR B NAYAK 28

29 Eligible business : Eligible Business means business by an undertaking, unit or an enterprise which is eligible for the deduction under this section. This section provides 100% tax break for ten consecutive assessment years out of fifteen years beginning from the year in which the undertaking or the enterprise develops or operates and maintains or develops, operates and maintains any infrastructure facility or telecommunication services Industrial park or special economic zone generates power or commences transmission or distribution of power or undertakes substantial renovation and modernization of the existing transmission and distribution lines. BY CA MAYUR B NAYAK BACK 29

30 If the consideration is not at market value : For the purposes of the deduction under this section, the profits and gains of such eligible business shall be computed as if the transfer, in either case, had been made at the market value of such goods or services as on that date. BY CA MAYUR B NAYAK 30

31 Section 80 IA(8) : Section 80-IA (10): Transactions between eligible and non- eligible businesses of the same assessee Business transacted with any person by an assessee carrying on eligible business generates more than ordinary profits owing to the close connection between them SDT amounting to more than Rs. 20 crore: The discretionary powers of AO are replaced and provided that ALP as defined in section 92F(ii) would be applicable SDT amounting to less than Rs. 20 crore: Discretionary powers of the AO would continue to apply. BY CA MAYUR B NAYAK 31

32 Sr. No. Section Particulars (i) 10A Special Provisions in respect of newly established undertakings in Free Trade Zone, etc. (ii) 10AA Special Provisions in respect of newly established undertakings in Special Economic Zones. (iii) 10B Special Provisions in respect of newly established hundred per cent export oriented undertakings. BY CA MAYUR B NAYAK 32

33 Sr. No. Section Particulars (iv) 80-IA Deductions in respect of profits and gains from industrial undertakings or enterprises engaged in infrastructure development etc. Nature of Tax Payer covered: Infrastructure developers. Developers of Industrial park. Telecommunication service providers. Producers or distributors of power. BY CA MAYUR B NAYAK 33

34 Sr. No. Section Particulars (v) 80-IB Deductions in respect of profits and gains from certain industrial undertakings other than infrastructure development undertakings. Nature of Tax payer covered: Small scale industry engaged in operating Cold storage plant Company carrying on scientific research and development Multiplex theaters and convention centre Industrial undertaking in Industrially backward state as mentioned in VIII Schedule (ex: Jammu and Kashmir ) Eligible housing projects. Eligible hospitals. Eligible Hotels Commercial production of mineral oil and Natural Gas 34 BY CA MAYUR B NAYAK

(vii) 80-ID Deductions in respect of profits and gains from business of hotels and convention centres in specified area.")

35 Sr. No. Section Particulars (vi) 80-IAB Deductions in respect of profits and gains by an undertaking or enterprise engaged in development of Special Economic Zone. (Nature of Tax payer - Developers of SEZ) (vii) 80-ID Deductions in respect of profits and gains from business of hotels and convention centres in specified area. (viii) 80-IE Special Provisions in respect of certain undertakings in North- Eastern States. (ix) 80JJA Deductions in respect of profits and gains from business of (x) collecting and processing of bio-degradable waste. 80JJAA Deductions in respect of employment of new workmen. BY CA MAYUR B NAYAK 35

36 Summary of Coverage of Domestic Transfer Pricing Section Coverage Transactions with 40A(2) Expenditure Related Parties as defined 80A and 80IA(8) Income and Expenditure Between Different Business units of same tax payer 80IA (10) Profits Close Connection BY CA MAYUR B NAYAK 36

37 Safe Harbour Rules BY CA MAYUR B NAYAK 37

38 Overview The Central Board of Direct Taxes (CBDT) has released a new set of simplified Transfer Pricing (TP) documentation Rules for domestic transactions Safe harbour means circumstances in which the income tax authorities shall accept the transfer price as declared by the assessee. BY CA MAYUR B NAYAK 38

39 Overview Safe Harbour is a Transfer Pricing provision applying to a specific category of tax payers/transactions. These rules are optional in nature and can be opted for by filling Form 3CEFAB on before due date for filing return of income. The safe harbour rules are valid for each assessment year in which the eligible assessee has entered into eligible SDT and it is treated as validly exercised. BY CA MAYUR B NAYAK 39

40 Rules for Safe Harbour Rules 10 TH- Definitions 10 THA- Eligible Assessee 10 THB- Eligible Specified Domestic Transactions 10 THC- Safe Harbour 10 THD- Procedure BY CA MAYUR B NAYAK 40

41 Which are the Eligible Domestic Transactions? Rule 10THB : Eligible Specified Domestic Transaction means a specified domestic transaction undertaken by an eligible assessee and which comprises of i. Supply of Electricity ii. iii. iv. Transmission of Electricity Wheeling of electricity Purchase of milk or milk products by a co-operative society from its members. BY CA MAYUR B NAYAK 41

42 Who are the Eligible Assessee? Rule 10THA: The eligible assessee means a person who has exercised a valid option for application of safe harbour rules in accordance with the provisions of rule 10THC and i. Is a government company engaged in the business of generation, supply, transmission or distribution of electricity ii. Is a co-operative society engaged in procuring and marketing milk and milk products BY CA MAYUR B NAYAK 42

43 Evaluation of Transactions Sr. No. Eligible specified Transactions 1 Supply of Electricity, transmission of electricity, wheeling of electricity referred in clauses (i), (ii) or (iii) of rule 10THB, as the case may be Safe Harbour Ratios The tariff in respect of supply of electricity, transmission of electricity, wheeling of electricity, as the case may be, is determined [or the methodology for determination of the tariff is approved] by the Appropriate Commission in accordance with the provisions of the Electricity Act, 2003 (36 of 2003). BY CA MAYUR B NAYAK 43

44 Evaluation of Transactions Sr. No. Eligible specified Transactions 2 Purchase of milk or milk products as referred to in clause (iv) of Rule 10THB Safe Harbour Ratios The price of milk or milk products is determined at a rate which is fixed on the basis of the quality of milk, namely, fat content and Solid Not FAT (SNF) content of milk ; and (a) The said rate is irrespective of the,- (i) the quantity of milk procured; (ii) the percentage of shares held by the members in the cooperative society; (iii) the voting power held by the members in the society; and (b) Such prices are routinely declared by the cooperative society in a transparent manner and are available in public domain BY CA MAYUR B NAYAK 44

45 Some Important Points Once Safe Harbour rules are chosen, the assessee is not eligible for comparability adjustment or for a +/-3% benefit while adjusting the ALP (Arm s Length Price). The provisions of section 92D and 92E apply irrespective of the fact that the assessee has opted for safe harbour rules. BY CA MAYUR B NAYAK 45

46 Procedure : Filing of Form 3CEFB AO verifies whether Eligible Assessee Eligible Specified Transaction DOUBTFUL Yes Safe Harbour option available AO will provide notice for submission of required documents inadequate Adequate Safe Harbour option available Option to file objection to Principal Commissioner within 15 Days Principal Commissioner passes appropriate orders within 2 months BY CA MAYUR B NAYAK 46

: TPO shall issue a notice to the assessee requiring him to produce any evidence in support of the computation of ALP.")

47 Section 92CA(1): Assessing Officer (AO) may refer the computation of ALP to the TPO with the previous approval of the Commissioner. Section 92CA(2): TPO shall issue a notice to the assessee requiring him to produce any evidence in support of the computation of ALP. Section 92CA(3): TPO shall by order in writing, determine the ALP and send a copy to the AO and to the assessee. BY CA MAYUR B NAYAK 47

48 Section 92CA(3A): An order under sub-section (3) may be made by TPO at any time before 60 days prior to the date on which the limitation under section 153 or 153B expires. Provided that if the period of limitation available to TPO is less than 60 days then such remaining period shall be extended to 60 days. Section 92CA(4): The AO shall proceed to compute the total income of the assessee in conformity with the ALP as so determined by the TPO. BY CA MAYUR B NAYAK 48

: Power to call information.")

49 Section 92CA(7): The following powers of a TPO are also applicable to domestic transactions: Section 131(1):Powers regarding discovery and inspection, summons, production of evidence, issuing commission. Section 133A: Power of survey. Section 133(6): Power to call information. BY CA MAYUR B NAYAK 49

50 Section 144C(15)(b): Reference to Dispute Resolution Panel(DRP) AO shall forward a draft of the proposed order of assessment to the eligible assessee if he proposes to make any variation in the income or loss returned which is prejudicial to his interest. Here eligible assessee means any person in whose case order u/s 92CA is passed BY CA MAYUR B NAYAK 50

51 BY CA MAYUR B NAYAK 51

52 Relating to the assessee enterprise Description of the ownership structure Profile of the multinational group of which the assessee is a part Broad description of the business and the industry Nature and Terms (including prices) of SDT entered into with each associate Enterprise Description of the Functions preformed, Assets employed, and Risks assumed i.e. (FAR Analysis) Record of the economic and market analyses, forecasts, budgets or any other financial estimates Record of uncontrolled transactions for analyzing comparability BY CA MAYUR B NAYAK 52

53 Relating to the Associated enterprise (AE) Broad description of the business and the industry Description of the functions preformed, risks assumed and assets employed Relating to ALP Description of methods considered for determining the ALP Record of the actual working carried out for determining the ALP Assumptions, policies and price negotiations, if any Details of adjustments BY CA MAYUR B NAYAK 53

54 BY CA MAYUR B NAYAK 54

55 Identification of SDTs Analyzing the legal structure of the Group Obtaining a list of related parties Verifying the list of transactions with related parties maintained by the assessee Verifying Board minutes for increase in investment in group companies/ other companies that could lead to substantial interest. Verifying the transactions with the related parties in accordance with the provisions of Specified Domestic Transactions under Section 92BA. Verifying sample copy of invoices, debit notes, ledger accounts of related parties and other back up documents. BY CA MAYUR B NAYAK 55

56 Implications of SDTs Review the agreements/ documents in support of the current inter company pricing/ allocations Analyze whether the current pricing policy of the group are in line with the Arm s Length principle Technical assessment of the arrangements to evaluate applicability of SDT provisions and possible approach for establishing ALP for the arrangements where SDT applies BY CA MAYUR B NAYAK 56

57 Further steps: Classification of SDT Conducting FAR Analysis Selection of appropriate method Benchmarking BY CA MAYUR B NAYAK 57

58 BY CA MAYUR B NAYAK 58

59 Section Impact Quantum of Penalty 271AA Failure to maintain any information or documents as required u/s 92D(1) or 92D(2) Failure of reporting a transaction Maintaining or furnishing an incorrect information or document 2% of the value of transaction 271G Failure to furnish information or document u/s 92D(3). 271BA Failure to furnish a report of an accountant as required by 92E 271(1)(c) Adjustment to tax payer s income during assessment 2% of the value of transaction Rs. 1,00, % to 300% of tax on adjusted amount BY CA MAYUR B NAYAK 59

60 BY CA MAYUR B NAYAK 60

Determination of ALP such other method as may be prescribed BY CA MAYUR B")

61 Resale Price Method (RPM) Cost Plus Method (CPM) Profit Split Method (PSM) Transactional net margin method (TNMM) Comparable Uncontrolled Price Method (CUP) Determination of ALP such other method as may be prescribed BY CA MAYUR B NAYAK 61

62 Comparable - Price Most direct method for determination of ALP Classified into Internal CUP and External CUP Method will be applicable in case of Similar Products, Similar conditions Most appropriate method in case of the following: Interest charged on loan Sale and Purchase of goods and services Royalty payment Commission BY CA MAYUR B NAYAK 62

63 Direct method Comparable - Gross Income Method will be applicable in case of Similar functions, Similar product group Most appropriate method in case where the controlled party is a Distributor BY CA MAYUR B NAYAK 63

64 Comparable Gross Income Method will be applicable in case of Most appropriate method in case of the following: Similar functions Similar product group Sale of finished / semifinished goods or services BY CA MAYUR B NAYAK 64

65 Comparable Profit Most appropriate method in case of the following: Joint Research and Development Development of joint Intellectual Property Rights Certain Financial Transactions BY CA MAYUR B NAYAK 65

66 Comparable Operating Income Most appropriate method in case of the following: Manufacture / distribution of finished goods Provision of services BY CA MAYUR B NAYAK 66

67 BY CA MAYUR B NAYAK 67

68 Transactions Appropriate method Documentation required Issues 1) Purchase of Goods Comparable uncontrolled price (CUP) method CUP analysis along with supporting documentation Agreement/ invoices between the parties _ 2) Salary and Bonuses paid to the partners 3) Interest payment Whether the limit as per Section 40(b) will be appropriate for determination of ALP? Comparable uncontrolled price (CUP) method Benchmarking study of Interest rates Agreement between the parties Source of funds BY CA MAYUR B NAYAK 68 _

69 Various Transactions and their appropriate method for determining ALP and issues Transactions Appropriate method Documentation required Issues 4) Remuneration and Sitting fees paid to the Directors _ Approvals from remuneration committee and general meeting for managerial remuneration Whether the limit as per Chapter XIII of Companies Act will be appropriate or determination of ALP? 5) Reimbursement of expenses _ Copy of invoices raised on third parties for which costs are reimbursed 6) Rent payment _ Agreement between the parties BY CA MAYUR B NAYAK 69

70 As per the definition of related parties of Section 40A(2)(b) Direct relations OR Indirect relations? In case of transfer of land whether rates mentioned in ready reckoner considered as ALP? Apprehensions are expressed about nonavailability of comparative data for determination of ALP Will DTP reduce or increase litigation? BY CA MAYUR B NAYAK 70

71 BY CA MAYUR B NAYAK 71

72 Maintaining and keeping information and documents Arm s Length Price Filing of Form 3CEB Losing excessive income tax benefits Possibility of double taxation Assessment by Transfer pricing officer (TPO) Penalty BY CA MAYUR B NAYAK 72

73 BY CA MAYUR B NAYAK 73

74 An Indian company having substantial interest of more than 20% in a Company outside India but less than 26%. Provisions of International Transfer Pricing will not be applicable on transactions between the two companies, but will provisions of Domestic Transfer Pricing applicable? BY CA MAYUR B NAYAK 74

Rs.")

75 Company XYZ has entered into the following transactions : Rent given to Company A ( substantial interest of Company XYZ) Rs. 5 crore Remuneration paid to Director and Managing Director Rs. 6 crore Sold goods to Company B (substantial interest of Company A) Rs. 10 crore Will DTP provisions be applicable? BY CA MAYUR B NAYAK 75

76 76

CA TIRTHESH M. BAGADIYA

DOMESTIC TRANSFER PRICING CA TIRTHESH M. BAGADIYA 1 1 Introduction Previously TP applicable only to international transactions By virtue of Finance Act, 2012, TP provision ambit has been extended to Specified

DOMESTIC TRANSFER PRICING CA TIRTHESH M. BAGADIYA 1 1 Introduction Previously TP applicable only to international transactions By virtue of Finance Act, 2012, TP provision ambit has been extended to Specified

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA DOMESTIC TRANSFER PRICING PROVISIONS CA.T. P. OSTWAL 21st September 2012 1 Introduction TP was earlier limited to International Transactions The Finance Act

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA DOMESTIC TRANSFER PRICING PROVISIONS CA.T. P. OSTWAL 21st September 2012 1 Introduction TP was earlier limited to International Transactions The Finance Act

Specified Domestic Transactions Coverage and Analysis. S P Singh

Specified Domestic Transactions Coverage and Analysis S P Singh August 2012 Introduction The Finance Act 2012, extends the scope of Transfer Pricing provision to Specified Domestic Transactions ( SDT )

Specified Domestic Transactions Coverage and Analysis S P Singh August 2012 Introduction The Finance Act 2012, extends the scope of Transfer Pricing provision to Specified Domestic Transactions ( SDT )

DOMESTIC TRANSFER PRICING. By CA Ramesh S Iyer

DOMESTIC TRANSFER PRICING By CA Ramesh S Iyer 04-08-2013 1 Reasons for introduction The SC in the case of CIT vs. Glaxo Smithkline Asia Pvt Ltd [2010]195Taxman 35(SC) recommended introduction of domestic

DOMESTIC TRANSFER PRICING By CA Ramesh S Iyer 04-08-2013 1 Reasons for introduction The SC in the case of CIT vs. Glaxo Smithkline Asia Pvt Ltd [2010]195Taxman 35(SC) recommended introduction of domestic

B S R & Co. LLP. Specified Domestic Transactions. Pankil Sanghvi Director. 10 October 2015

Specified Domestic Transactions B S R & Co. LLP Pankil Sanghvi Director 10 October 2015 1 Background Genesis of Domestic Transfer Pricing Regulations Supreme Court (SC) in the case of CIT v Glaxo SmithKline

Specified Domestic Transactions B S R & Co. LLP Pankil Sanghvi Director 10 October 2015 1 Background Genesis of Domestic Transfer Pricing Regulations Supreme Court (SC) in the case of CIT v Glaxo SmithKline

CONTENTS. Introduction to Transfer Pricing. Transfer Pricing Litigation Statistics. Introduction to Domestic Transfer Pricing

DOMESTIC TRANSFER PRICING CONTENTS Introduction to Transfer Pricing Transfer Pricing Litigation Statistics Introduction to Domestic Transfer Pricing Section 40A(2)(b), 80IA(8) & 80IA(10) Relationships,

DOMESTIC TRANSFER PRICING CONTENTS Introduction to Transfer Pricing Transfer Pricing Litigation Statistics Introduction to Domestic Transfer Pricing Section 40A(2)(b), 80IA(8) & 80IA(10) Relationships,

Applicability of Transfer Pricing to Specified Domestic Transactions

Applicability of Transfer Pricing to Specified Domestic Transactions Outline Introduction Overview of provisions Analysis of provisions Impact on taxpayers Way forward & EY approach Page 2 Abbreviations

Applicability of Transfer Pricing to Specified Domestic Transactions Outline Introduction Overview of provisions Analysis of provisions Impact on taxpayers Way forward & EY approach Page 2 Abbreviations

September 1, By: CA. Gaurav Garg

September 1, 2012 By: CA. Gaurav Garg Transfer pricing bleeding ground for the corporate but breeding ground for consultants Transfer pricing addition in first six years equal to addition made addition

September 1, 2012 By: CA. Gaurav Garg Transfer pricing bleeding ground for the corporate but breeding ground for consultants Transfer pricing addition in first six years equal to addition made addition

Transfer Pricing Law

Transfer Pricing Law 1 Presentation Compiled By Akshay Kenkre Gaurav Garg Tejas Dharwadkar What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services,

Transfer Pricing Law 1 Presentation Compiled By Akshay Kenkre Gaurav Garg Tejas Dharwadkar What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services,

The Chamber of Tax Consultants

The Chamber of Tax Consultants Case Studies on Domestic Transfer Pricing w.r.t section 80A/80IA/10AA including its bench marking Presentation by Yogesh Thar April 29, 2016 1 Genesis of Transfer Pricing

The Chamber of Tax Consultants Case Studies on Domestic Transfer Pricing w.r.t section 80A/80IA/10AA including its bench marking Presentation by Yogesh Thar April 29, 2016 1 Genesis of Transfer Pricing

Workshop on Basics in Transfer Pricing. Domestic Transfer Pricing By

Workshop on Basics in Transfer Pricing Domestic Transfer Pricing By CA Praveen Ranka Introduction SDT The Intent The Finance Act, 2012 extended applicability of transfer pricing provisions to Specified

Workshop on Basics in Transfer Pricing Domestic Transfer Pricing By CA Praveen Ranka Introduction SDT The Intent The Finance Act, 2012 extended applicability of transfer pricing provisions to Specified

Issues in Domestic Transfer Pricing including various methods for determining ALP

Issues in Domestic Transfer Pricing including various methods for determining ALP Rakesh Alshi, Anand Thacker - 6 th October 2014 2014 Deloitte Haskins & Sells LLP 1 Contents 1. Specified Domestic Transactions

Issues in Domestic Transfer Pricing including various methods for determining ALP Rakesh Alshi, Anand Thacker - 6 th October 2014 2014 Deloitte Haskins & Sells LLP 1 Contents 1. Specified Domestic Transactions

DOMESTIC TRANSFER PRICING REGULATIONS

DOMESTIC TRANSFER PRICING REGULATIONS (Taxation of specified domestic transactions in India) By B. D. Jokhakar & Co. Chartered Accountants INDIA TABLE OF CONTENTS Sr. No. Topic Page no. I INTRODUCTION

DOMESTIC TRANSFER PRICING REGULATIONS (Taxation of specified domestic transactions in India) By B. D. Jokhakar & Co. Chartered Accountants INDIA TABLE OF CONTENTS Sr. No. Topic Page no. I INTRODUCTION

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

TRANSFER PRICING. 19 th July, July-14 1

TRANSFER PRICING 19 th July, 2014 19-July-14 1 TRANSFER PRICING AND ITS FUTURE PROSPECTS Due to the increasing trend in globalization of Indian business, transfer pricing will remain foremost on the agenda

TRANSFER PRICING 19 th July, 2014 19-July-14 1 TRANSFER PRICING AND ITS FUTURE PROSPECTS Due to the increasing trend in globalization of Indian business, transfer pricing will remain foremost on the agenda

CONTENT. Mulund CPE Study Circle of ICAI. Domestic Transfer Pricing Applicability & Overview 15/6/2013. CA Paras K Savla

Mulund CPE Study Circle of ICAI Domestic Transfer Pricing Applicability & Overview 15/6/2013 CA Paras K Savla CONTENT Introduction Specified domestic transactions Illustrations Procedures ALP under other

Mulund CPE Study Circle of ICAI Domestic Transfer Pricing Applicability & Overview 15/6/2013 CA Paras K Savla CONTENT Introduction Specified domestic transactions Illustrations Procedures ALP under other

Domestic Transfer Pricing

Domestic Transfer Pricing By CA Nihar Jambusaria Central Council Member ICAI {Mumbai} Overview Transfer pricing (referred to as TP) regulations introduced in India in 2001, previously covered only cross

Domestic Transfer Pricing By CA Nihar Jambusaria Central Council Member ICAI {Mumbai} Overview Transfer pricing (referred to as TP) regulations introduced in India in 2001, previously covered only cross

Domestic Transfer Pricing Provisions

Domestic Transfer Pricing Provisions Ameya Kunte April 4, 2014 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP

Domestic Transfer Pricing Provisions Ameya Kunte April 4, 2014 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP

(Applicability & impact Analysis) By:-

By:-") Domestic Transfer Pricing (Applicability & impact Analysis) By:- Surana Maloo & Co. Chartered Accountants 2 nd Floor, Aakash Ganga Complex, Parimal Under Bridge, Nr Suvidha Shopping Center, Paldi, Ahmedabad-

Domestic Transfer Pricing (Applicability & impact Analysis) By:- Surana Maloo & Co. Chartered Accountants 2 nd Floor, Aakash Ganga Complex, Parimal Under Bridge, Nr Suvidha Shopping Center, Paldi, Ahmedabad-

Domestic Transfer Pricing

Domestic Transfer Pricing Ameya Kunte 20 March 2015 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP Framework SDT

Domestic Transfer Pricing Ameya Kunte 20 March 2015 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP Framework SDT

TRANSFER PRICING - DOMESTIC TRANSACTIONS AN INSIGHT GAURAV SHAH OCTOBER 2012

1 TRANSFER PRICING - DOMESTIC TRANSACTIONS AN INSIGHT GAURAV SHAH OCTOBER 2012 Table of Contents Introduction to Transfer Pricing International Transfer Pricing Background Domestic Transfer Pricing Differences

1 TRANSFER PRICING - DOMESTIC TRANSACTIONS AN INSIGHT GAURAV SHAH OCTOBER 2012 Table of Contents Introduction to Transfer Pricing International Transfer Pricing Background Domestic Transfer Pricing Differences

TRANSFER PRICING IN INDIA DOMESTIC TRANSACTION AN ADDED DIMENSION For Jallandhar Branch Of NIRC Of. By: CA Krishan Vrind Jain Dated 08/08/2013

TRANSFER PRICING IN INDIA DOMESTIC TRANSACTION AN ADDED DIMENSION For Jallandhar Branch Of NIRC Of ICAI By: CA Krishan Vrind Jain Dated 08/08/2013 Finance Minister s speech on the rational for introducing

TRANSFER PRICING IN INDIA DOMESTIC TRANSACTION AN ADDED DIMENSION For Jallandhar Branch Of NIRC Of ICAI By: CA Krishan Vrind Jain Dated 08/08/2013 Finance Minister s speech on the rational for introducing

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

Transfer Pricing of Domestic Transactions & Provisions of. or Complimentary. 7 December 2013 Rajan Vora

Transfer Pricing of Domestic Transactions & Provisions of Section 40A(2)(b) Contradictory or Complimentary 7 December 2013 Rajan Vora Outline Rationale for introducing transfer pricing Brief background

Transfer Pricing of Domestic Transactions & Provisions of Section 40A(2)(b) Contradictory or Complimentary 7 December 2013 Rajan Vora Outline Rationale for introducing transfer pricing Brief background

Future of TP. Documentation & Certification. 7th October Presented by- CA Dilip Gupta

Future of TP Documentation & Certification 7th October 2017 Presented by- CA Dilip Gupta Journey of TP regulations in India Major Milestones Final Rules on Range and multiple year data concept Introduction

Future of TP Documentation & Certification 7th October 2017 Presented by- CA Dilip Gupta Journey of TP regulations in India Major Milestones Final Rules on Range and multiple year data concept Introduction

Domestic Transfer Pricing

Domestic Transfer Pricing September 15, 2012 CA Darpan Mehta Agenda 1 Domestic TP Transactions 2 Case Study 3 Way Forward Slide 2 Transactions Slide 3 Intent of Indian Transfer Pricing (TP) Regulations

Domestic Transfer Pricing September 15, 2012 CA Darpan Mehta Agenda 1 Domestic TP Transactions 2 Case Study 3 Way Forward Slide 2 Transactions Slide 3 Intent of Indian Transfer Pricing (TP) Regulations

Specific Domestic Transactions. Documentation & Audit Report Requirements Key concern Areas. 22 November 2013

Specific Domestic Transactions Documentation & Audit Report Requirements Key concern Areas 22 November 2013 Agenda Requirements at glace Key issues relating to applicability to various entities Transactions

Specific Domestic Transactions Documentation & Audit Report Requirements Key concern Areas 22 November 2013 Agenda Requirements at glace Key issues relating to applicability to various entities Transactions

SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria

-Nihar Jambusaria") SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria TP Regulations to apply to certain Specified Domestic Transactions [New Section 92BA] TP provisions are applicable to the following Domestic

SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria TP Regulations to apply to certain Specified Domestic Transactions [New Section 92BA] TP provisions are applicable to the following Domestic

Overview of Transfer Pricing

Overview of Transfer Pricing Contents Legislative framework Transfer pricing study Assessment and Litigation Key Recent Developments Page 2 Transfer Pricing in India- Background April 1, 2001 onwards Comprehensive

Overview of Transfer Pricing Contents Legislative framework Transfer pricing study Assessment and Litigation Key Recent Developments Page 2 Transfer Pricing in India- Background April 1, 2001 onwards Comprehensive

DOMESTIC TRANSFER PRICING

12 October 2014 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

12 October 2014 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

Domestic Transfer Pricing (India)

") Domestic Transfer Pricing (India) After the grand success of International Transfer pricing, through which huge transfer pricing orders slapped on companies with cross-border operations in the last financial

Domestic Transfer Pricing (India) After the grand success of International Transfer pricing, through which huge transfer pricing orders slapped on companies with cross-border operations in the last financial

Transfer Pricing Backdrop in. Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016

Transfer Pricing Backdrop in India Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016 Presentation Outline Introduction ti Transfer Pricing Regulations in India Arms

Transfer Pricing Backdrop in India Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016 Presentation Outline Introduction ti Transfer Pricing Regulations in India Arms

DOMESTIC TRANSFER PRICING

17 November 2013 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

17 November 2013 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

Domestic Transfer Pricing in India

Domestic Transfer Pricing in India By (Partner) SBR & CO. Chartered Accountants P a g e 1 After the grand success of International Transfer pricing, through which huge transfer pricing orders slapped on

Domestic Transfer Pricing in India By (Partner) SBR & CO. Chartered Accountants P a g e 1 After the grand success of International Transfer pricing, through which huge transfer pricing orders slapped on

An overview of Transfer Pricing

An overview of Transfer Pricing CTC Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing CTC Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

IN THE HIGH COURT OF GUJARAT AT AHMEDABAD. SPECIAL CIVIL APPLICATION NO of 2017

IN THE HIGH COURT OF GUJARAT AT AHMEDABAD SPECIAL CIVIL APPLICATION NO. 19073 of 2017 FOR APPROVAL AND SIGNATURE: HONOURABLE MR.JUSTICE AKIL KURESHI and HONOURABLE MR.JUSTICE B.N. KARIA ==========================================================

IN THE HIGH COURT OF GUJARAT AT AHMEDABAD SPECIAL CIVIL APPLICATION NO. 19073 of 2017 FOR APPROVAL AND SIGNATURE: HONOURABLE MR.JUSTICE AKIL KURESHI and HONOURABLE MR.JUSTICE B.N. KARIA ==========================================================

Introduction to Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

d e vreser st ighr lla

Article 7 and 9 of the model conventions including International and Domestic TP Beginners Study Course on International Taxation July 4, 2015 Neha Arora 2 Contents Article 7 of the Model Convention Approaches

Article 7 and 9 of the model conventions including International and Domestic TP Beginners Study Course on International Taxation July 4, 2015 Neha Arora 2 Contents Article 7 of the Model Convention Approaches

Did you know! Transactions M.2 Safe harbour rules M.3 Dispute resolution panel

M Transfer pricing Doing business in India 209 Did you know! India has emerged as the world s number one, along with the US, in annual solar power generation. In wind power production, when it comes to

M Transfer pricing Doing business in India 209 Did you know! India has emerged as the world s number one, along with the US, in annual solar power generation. In wind power production, when it comes to

DOMESTIC TRANSFER PRICING CONFERENCE

DOMESTIC TRANSFER PRICING CONFERENCE Importance of FAR & Comparability; Selection of the Most Appropriate Method and Issues in disclosure in new Form 3CEB from SDT perspective 19 October 2013 Pramod Joshi

DOMESTIC TRANSFER PRICING CONFERENCE Importance of FAR & Comparability; Selection of the Most Appropriate Method and Issues in disclosure in new Form 3CEB from SDT perspective 19 October 2013 Pramod Joshi

TRANSFER PRICING DATED CA. Ashwani Rastogi, New Delhi

TRANSFER PRICING DATED 8.6.2017 1 India has signed the historic multilateral convention to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS), at Paris with More than

TRANSFER PRICING DATED 8.6.2017 1 India has signed the historic multilateral convention to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS), at Paris with More than

Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer

CA. Vispi T. Patel, CA. Rajiv Shah and CA.Kejal Visharia Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer INTERNATIONAL PRICING PROVISIONS TRANSFER Introduction

CA. Vispi T. Patel, CA. Rajiv Shah and CA.Kejal Visharia Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer INTERNATIONAL PRICING PROVISIONS TRANSFER Introduction

BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING

CONTENTS BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING CHAPTER 1 : INTRODUCTION 3 CHAPTER 2 : FEATURES OF THE TRANSFER PRICING REGIME UNDER CHAPTER X 10 CHAPTER 3 : TRANSFER PRICING PROVISIONS OF CHAPTER

CONTENTS BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING CHAPTER 1 : INTRODUCTION 3 CHAPTER 2 : FEATURES OF THE TRANSFER PRICING REGIME UNDER CHAPTER X 10 CHAPTER 3 : TRANSFER PRICING PROVISIONS OF CHAPTER

Overview of Transfer Pricing Regulations. CA Akshay Kenkre

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

TRANSFER PRICING. By Yethi Remella

TRANSFER PRICING By Yethi Remella 1. INTRODUCTION 2. INCOME TAX ACT, SECTION 92 3. FORM 3CEB Introduction What is Transfer Pricing? What is the Importance of TP in Income Tax? Transfer Pricing - Term Costing

TRANSFER PRICING By Yethi Remella 1. INTRODUCTION 2. INCOME TAX ACT, SECTION 92 3. FORM 3CEB Introduction What is Transfer Pricing? What is the Importance of TP in Income Tax? Transfer Pricing - Term Costing

Rajeev Pai, Chief Financial Officer JSW Steel Limited

Rajeev Pai, Chief Financial Officer JSW Steel Limited Setting of Enterprise Resource Planning (ERP) based system and key challenges Accounting Standards and Regulatory compliance and Challenges thereof

Rajeev Pai, Chief Financial Officer JSW Steel Limited Setting of Enterprise Resource Planning (ERP) based system and key challenges Accounting Standards and Regulatory compliance and Challenges thereof

JGARG. Economic Advisors. Tri Nagar Keshav Puram Study Circle Of North India Regional Council. By: CA. Gaurav Garg

JGARG Economic Advisors Tri Nagar Keshav Puram Study Circle Of North India Regional Council By: CA. Gaurav Garg Warm-up Indian TP Regulations Arm s Length Principle The Tax Treaty Aspect Meaning of Associated

JGARG Economic Advisors Tri Nagar Keshav Puram Study Circle Of North India Regional Council By: CA. Gaurav Garg Warm-up Indian TP Regulations Arm s Length Principle The Tax Treaty Aspect Meaning of Associated

Transfer Pricing in India Examining inter-company cross-border transactions

Transfer Pricing in India Examining inter-company cross-border transactions 1 Contents Background and history Meaning of International transaction Specified Domestic Transaction Arm s Length Price Associated

Transfer Pricing in India Examining inter-company cross-border transactions 1 Contents Background and history Meaning of International transaction Specified Domestic Transaction Arm s Length Price Associated

Special provisions relating to certain income of non residents, Introduction to transfer pricing, APA, Double taxation Relief. CA Kiran J.

Special provisions relating to certain income of non residents, Introduction to transfer pricing, APA, Double taxation Relief CA Kiran J. Nisar 1 Chapter XIIA : Special Provision relating to certain income

Special provisions relating to certain income of non residents, Introduction to transfer pricing, APA, Double taxation Relief CA Kiran J. Nisar 1 Chapter XIIA : Special Provision relating to certain income

Bombay Chartered Accountants Society. Vispi T. Patel Vispi T. Patel & Associates

FAR Analysis, Selection of Most Appropriate Method, Application of Methods (CUP & RPM) and Case Studies with reference to Specified Domestic Transactions Bombay Chartered Accountants Society Vispi T. Patel

FAR Analysis, Selection of Most Appropriate Method, Application of Methods (CUP & RPM) and Case Studies with reference to Specified Domestic Transactions Bombay Chartered Accountants Society Vispi T. Patel

Domestic Transfer Pricing

Table of Contents DOMESTIC TRANSFER PRICING Benchmarking and Reporting requirements Study Circle Meeting CA Gaurav Shah 15 th June 2013 Domestic Transfer Pricing Benchmarking Analysis Transfer Pricing

Table of Contents DOMESTIC TRANSFER PRICING Benchmarking and Reporting requirements Study Circle Meeting CA Gaurav Shah 15 th June 2013 Domestic Transfer Pricing Benchmarking Analysis Transfer Pricing

The Chamber of Tax Consultants

The Chamber of Tax Consultants 3 rd Domestic Transfer Pricing Conference Tax incentives and domestic transfer pricing Sanjay Kapadia Assisted by Nisha Shah 19 October 2013 Meaning of Specified Domestic

The Chamber of Tax Consultants 3 rd Domestic Transfer Pricing Conference Tax incentives and domestic transfer pricing Sanjay Kapadia Assisted by Nisha Shah 19 October 2013 Meaning of Specified Domestic

Landmark Decisions on Transfer Pricing

Landmark Decisions on Transfer Pricing CITC Amol Tibrewal Vispi T. Patel & Associates 11 April 2014 Global Vantedge - Delhi Tribunal (ITA No 2763 & 2764/DEL/2009) Facts of the case Assessee provided IteS

Landmark Decisions on Transfer Pricing CITC Amol Tibrewal Vispi T. Patel & Associates 11 April 2014 Global Vantedge - Delhi Tribunal (ITA No 2763 & 2764/DEL/2009) Facts of the case Assessee provided IteS

Transfer Pricing. Recent Trends & Key Developments. PHD Chamber International Tax Conference September 04, 2014 New Delhi. Statement of Credentials 1

Transfer Pricing Recent Trends & Key Developments PHD Chamber International Tax Conference September 04, 2014 New Delhi Statement of Credentials 1 SESSION DETAILS Topic: Transfer Pricing Recent Trends

Transfer Pricing Recent Trends & Key Developments PHD Chamber International Tax Conference September 04, 2014 New Delhi Statement of Credentials 1 SESSION DETAILS Topic: Transfer Pricing Recent Trends

JGARG. Tri Nagar Keshav Puram Study Circle Of North India Regional Council. By: CA. Gaurav Garg. Economic Advisors

JGARG Economic Advisors Tri Nagar Keshav Puram Study Circle Of North India Regional Council By: CA. Gaurav Garg Compliance Requirement Information/ Document Penalties JGarg Economic Advisors Pvt. Ltd.

JGARG Economic Advisors Tri Nagar Keshav Puram Study Circle Of North India Regional Council By: CA. Gaurav Garg Compliance Requirement Information/ Document Penalties JGarg Economic Advisors Pvt. Ltd.

Transfer Pricing Audit and Issuance of Form 3CEB. Kedar Karve 10 October 2015 Application No. 65

Transfer Pricing Audit and Issuance of Form 3CEB Kedar Karve 10 October 2015 Application No. 65 0 Contents 1 2 3 4 5 Brief Overview of Transfer Pricing Regulations in India Section 92E of Income-tax Act,

Transfer Pricing Audit and Issuance of Form 3CEB Kedar Karve 10 October 2015 Application No. 65 0 Contents 1 2 3 4 5 Brief Overview of Transfer Pricing Regulations in India Section 92E of Income-tax Act,

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

FINANCE ACT, EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE ACT, Explanatory notes to the provisions of the Finance Act, 2011

FINANCE ACT, 2011 - EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE ACT, 2011 CIRCULAR NO. 02/2012 [F. NO.142/01/2012-SO(TPL)], DATED 22-5-2012 Explanatory notes to the provisions of the Finance Act,

FINANCE ACT, 2011 - EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE ACT, 2011 CIRCULAR NO. 02/2012 [F. NO.142/01/2012-SO(TPL)], DATED 22-5-2012 Explanatory notes to the provisions of the Finance Act,

Issues in Transfer Pricing

Issues in Transfer Pricing Vaishali Mane Chartered Accountant, Mumbai 2017 Grant Thornton India LLP. All rights reserved. 1 Contents 1 Transfer Pricing - Basic 2 Recent Developments in Transfer Pricing

Issues in Transfer Pricing Vaishali Mane Chartered Accountant, Mumbai 2017 Grant Thornton India LLP. All rights reserved. 1 Contents 1 Transfer Pricing - Basic 2 Recent Developments in Transfer Pricing

T. P. Ostwal & Associates (Regd.) Key Budget Proposal Budget 2012 CHARTERED ACCOUNTANTS

Key Budget Proposal Budget 2012 CHARTERED ACCOUNTANTS") IMPORTANT AMENDMENTS & MAJOR DIRECT TAX PROPOSALS IN FINANCE BILL, 2012 CORPORATE TAX No change in the head corporate tax. Extension of sunset date for tax holiday for power sector to 2013; Initial depreciation

IMPORTANT AMENDMENTS & MAJOR DIRECT TAX PROPOSALS IN FINANCE BILL, 2012 CORPORATE TAX No change in the head corporate tax. Extension of sunset date for tax holiday for power sector to 2013; Initial depreciation

An overview of Transfer Pricing

An overview of Transfer Pricing Vispi T. Patel Vispi T. Patel & Associates March 14, 2015 1 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations

An overview of Transfer Pricing Vispi T. Patel Vispi T. Patel & Associates March 14, 2015 1 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations

Transfer Pricing Theory & Practice CA Hari Om Jindal October 7, 2017

Transfer Pricing Theory & Practice CA Hari Om Jindal (hojindal@yahoo.co.in) October 7, 2017 Nothing in this paper should be construed or treated as legal advice. Whilst we endeavor to ensure that the information

Transfer Pricing Theory & Practice CA Hari Om Jindal (hojindal@yahoo.co.in) October 7, 2017 Nothing in this paper should be construed or treated as legal advice. Whilst we endeavor to ensure that the information

TRANSFER PRICING UNDER INCOME TAX ACT, N.Madhan B.Com., CA & Grad CWA. 22 August 2015

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS. S.R. Wadhwa, Advocate 1

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS S.R. Wadhwa, Advocate 1 BY: S.R. Wadhwa Ph. No. 9810414433 Email: wadhwasr@hotmail.com Website: wadhwataxconsultant.com S.R. Wadhwa,

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS S.R. Wadhwa, Advocate 1 BY: S.R. Wadhwa Ph. No. 9810414433 Email: wadhwasr@hotmail.com Website: wadhwataxconsultant.com S.R. Wadhwa,

Appeal, Set comm., DRP Etc Mock Test IGP-CS CA Vivek Gaba

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

Transfer Pricing and Other Provisions to Check Avoidance of Tax

16 Transfer Pricing and Other Provisions to Check Avoidance of Tax Question 1 State the consequences that would follow if the Assessing Officer makes adjustment to arm s length price in international transactions

16 Transfer Pricing and Other Provisions to Check Avoidance of Tax Question 1 State the consequences that would follow if the Assessing Officer makes adjustment to arm s length price in international transactions

Audit of Domestic Transfer Pricing

Audit of Domestic Transfer Pricing Prakash Udeshi B.Com, FCA, CS, CMA KALARIA & SAMPAT Chartered Accountants Ahmedabad Applicability - SDT The Finance Act 2012 extended the scope of Transfer Pricing provision

Audit of Domestic Transfer Pricing Prakash Udeshi B.Com, FCA, CS, CMA KALARIA & SAMPAT Chartered Accountants Ahmedabad Applicability - SDT The Finance Act 2012 extended the scope of Transfer Pricing provision

BUDGET 2016 SONALEE GODBOLE

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

Methods of determining ALP

Methods of determining ALP -Eric Mehta 1 August 2011 Concept of Transfer Pricing 1 August 2011 Page 2 Transfer Pricing Concept of transfer pricing A price between unrelated parties is known as the arm

Methods of determining ALP -Eric Mehta 1 August 2011 Concept of Transfer Pricing 1 August 2011 Page 2 Transfer Pricing Concept of transfer pricing A price between unrelated parties is known as the arm

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

Methods of determining ALP

3 rd Intensive Study Course on Transfer Pricing Methods of determining ALP CA Vishwanath Kane 16 February 2013 Agenda Introduction Transfer Pricing Methods Overview Applicability of Transfer Pricing Methods

3 rd Intensive Study Course on Transfer Pricing Methods of determining ALP CA Vishwanath Kane 16 February 2013 Agenda Introduction Transfer Pricing Methods Overview Applicability of Transfer Pricing Methods

Case Study on Splitting up/ reconstruction of business of old unit

Case Studies Case Study on Splitting up/ reconstruction of business of old unit Case Study 1: XYZ India Ltd, is engaged in the business of developing softwares. The company already has an established software

Case Studies Case Study on Splitting up/ reconstruction of business of old unit Case Study 1: XYZ India Ltd, is engaged in the business of developing softwares. The company already has an established software

Transfer Pricing Methods and Selection of Most Appropriate Method. Vaishali Mane Partner Grant Thornton India LLP Mumbai

Transfer Pricing Methods and Selection of Most Appropriate Method Vaishali Mane Partner Grant Thornton India LLP Mumbai Agenda Transfer Pricing Quick background Arm's Length Principle Overview of Methods

Transfer Pricing Methods and Selection of Most Appropriate Method Vaishali Mane Partner Grant Thornton India LLP Mumbai Agenda Transfer Pricing Quick background Arm's Length Principle Overview of Methods

Transfer Pricing - Filing of Form 3CEB & Practical Issues November 11, CA Vikram R. B.Com., FCA.

12 November 2014 Transfer Pricing - Filing of Form 3CEB & Practical Issues November 11, 2017 CA Vikram R. B.Com., FCA. 98841 91001 vikram@vcmv.in Transfer Pricing Introduction in India Finance Minister

12 November 2014 Transfer Pricing - Filing of Form 3CEB & Practical Issues November 11, 2017 CA Vikram R. B.Com., FCA. 98841 91001 vikram@vcmv.in Transfer Pricing Introduction in India Finance Minister

Solved Scanner. (Solution of December ) CMA Inter Group - I (Syllabus-2012) Paper - 7 : Direct Taxation

CMA Inter Group - I (Syllabus-2012) Paper - 7 : Direct Taxation") Solved Scanner (Solution of December - 2016) CMA Inter Group - I (Syllabus-2012) Paper - 7 : Direct Taxation [Chapter - 21] Objective Questions 1. (a), (b), (c) (5 marks each) (a) (i) ` 10,000 (ii) ` 5,00,000

Solved Scanner (Solution of December - 2016) CMA Inter Group - I (Syllabus-2012) Paper - 7 : Direct Taxation [Chapter - 21] Objective Questions 1. (a), (b), (c) (5 marks each) (a) (i) ` 10,000 (ii) ` 5,00,000

TRANSFER PRICING. - to be AWARE or BEWARE?

TRANSFER PRICING - to be AWARE or BEWARE? E-Venue: The Institute of Cost Accountants of India Webinar ( 10.01.2018 ) By CMA Chiranjib Das, FCMA, ACA, M.Com Presentation Plan (1) Transfer Pricing an Overview

TRANSFER PRICING - to be AWARE or BEWARE? E-Venue: The Institute of Cost Accountants of India Webinar ( 10.01.2018 ) By CMA Chiranjib Das, FCMA, ACA, M.Com Presentation Plan (1) Transfer Pricing an Overview

Issues Involving Comparability and Profit Based Methods in Transfer Pricing

G L O B A L T R A N S F E R P R I C I N G S E R V I C E S Issues Involving Comparability and Profit Based Methods in Transfer Pricing International Taxation Conference 2008 December 5, 2008 T A X Uday

G L O B A L T R A N S F E R P R I C I N G S E R V I C E S Issues Involving Comparability and Profit Based Methods in Transfer Pricing International Taxation Conference 2008 December 5, 2008 T A X Uday

FINAL CA May 2018 DIRECT TAXATION

FINAL CA May 2018 DIRECT TAXATION Test Code F 90 Branch: MULTIPLE Date: (50 Marks) compulsory. Note: All questions are Question 1 (10 marks) Computation of Book Profit for levy of MAT under section 115JB

FINAL CA May 2018 DIRECT TAXATION Test Code F 90 Branch: MULTIPLE Date: (50 Marks) compulsory. Note: All questions are Question 1 (10 marks) Computation of Book Profit for levy of MAT under section 115JB

Transfer Pricing Perspective Pharmaceuticals Industry 20 September 2014

www.pwc.in Transfer Pricing Perspective Pharmaceuticals Industry 20 Contents Transfer Pricing environment Key TP Issues Recent Developments Best Practices Slide 2 Transfer Pricing Environment Slide 3 Global

www.pwc.in Transfer Pricing Perspective Pharmaceuticals Industry 20 Contents Transfer Pricing environment Key TP Issues Recent Developments Best Practices Slide 2 Transfer Pricing Environment Slide 3 Global

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX

![GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX](/thumbs/90/104493159.jpg "GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX") [TO BE PUBLSIHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

[TO BE PUBLSIHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

[2012] 18 taxmann.com 256 (Article)

![[2012] 18 taxmann.com 256 (Article)](/thumbs/75/72354143.jpg "[2012] 18 taxmann.com 256 (Article)") [2012] 18 taxmann.com 256 (Article) Convergence between Transfer Pricing and Customs Valuation in the Indian context Introduction KARTHIK SUNDARAM Advocate - Madras High Court 1 1. Transactions globally

[2012] 18 taxmann.com 256 (Article) Convergence between Transfer Pricing and Customs Valuation in the Indian context Introduction KARTHIK SUNDARAM Advocate - Madras High Court 1 1. Transactions globally

Recent Transfer Pricing Developments

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

WIRC INTENSIVE COURSE ON TRANSFER PRICING

1 WIRC INTENSIVE COURSE ON TRANSFER PRICING (From 1.08.2011 to 12.08.2011) I. INTRODUCTION What is Transfer Pricing? OVERVIEW OF TRANSFER PRICING By Nilesh Patel; Ex-IRS Officer, CPA(USA) Ph: 9819060323

1 WIRC INTENSIVE COURSE ON TRANSFER PRICING (From 1.08.2011 to 12.08.2011) I. INTRODUCTION What is Transfer Pricing? OVERVIEW OF TRANSFER PRICING By Nilesh Patel; Ex-IRS Officer, CPA(USA) Ph: 9819060323

Transfer Pricing compliances, Litigation update and Dispute resolution. - CA Mithilesh

Transfer Pricing compliances, Litigation update and Dispute resolution - CA Mithilesh 09553111131 Overview Concept and Rationale of TP Applicability International Transaction Meaning of Associated Enterprise

Transfer Pricing compliances, Litigation update and Dispute resolution - CA Mithilesh 09553111131 Overview Concept and Rationale of TP Applicability International Transaction Meaning of Associated Enterprise

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I Date: Fri, 04/22/2016-15:02 Ajay Kering (Direct or, Grant Thornt on India LLP) Dinesh Ramnani (Manager, Grant Thornt on India LLP) This

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I Date: Fri, 04/22/2016-15:02 Ajay Kering (Direct or, Grant Thornt on India LLP) Dinesh Ramnani (Manager, Grant Thornt on India LLP) This

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE COMPILED BY: CA.ARUN GUPTA ca.arungupta77@gmail.com A. Rates of Taxes: 1. It is proposed to make the following changes in tax rates: In case of Resident

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE COMPILED BY: CA.ARUN GUPTA ca.arungupta77@gmail.com A. Rates of Taxes: 1. It is proposed to make the following changes in tax rates: In case of Resident

IN THE INCOME TAX APPELLATE TRIBUNAL B BENCH : BANGALORE

IN THE INCOME TAX APPELLATE TRIBUNAL B BENCH : BANGALORE BEFORE SHRI GEORGE GEORGE K., JUDICIAL MEMBER AND SHRI A. MOHAN ALANKAMONY, ACCOUNTANT MEMBER ITA No. 131/Bang/2010 Assessment year : 2004-05 Intel

IN THE INCOME TAX APPELLATE TRIBUNAL B BENCH : BANGALORE BEFORE SHRI GEORGE GEORGE K., JUDICIAL MEMBER AND SHRI A. MOHAN ALANKAMONY, ACCOUNTANT MEMBER ITA No. 131/Bang/2010 Assessment year : 2004-05 Intel

Functional Analysis, Comparability Analysis and Economic Analysis. Vispi T. Patel Vispi T. Patel & Associates

Functional Analysis, Comparability Analysis and Economic Analysis Vispi T. Patel Vispi T. Patel & Associates February 6, 2016 AGENDA Arm s Length Price and its computation Functional, Asset and Risk Analysis

Functional Analysis, Comparability Analysis and Economic Analysis Vispi T. Patel Vispi T. Patel & Associates February 6, 2016 AGENDA Arm s Length Price and its computation Functional, Asset and Risk Analysis

Salient features of Direct Tax Proposals of Union Budget 2011

Salient features of Direct Tax Proposals of Union Budget 2011 RATES OF INCOME-TAX FOR THE ASSESSMENT YEAR 2012-13 o Tax slab rates have been changed for individuals and HUF, which is given by way of a

Salient features of Direct Tax Proposals of Union Budget 2011 RATES OF INCOME-TAX FOR THE ASSESSMENT YEAR 2012-13 o Tax slab rates have been changed for individuals and HUF, which is given by way of a

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE A PRESENTATION BY AKHILESH RANJAN DIRECTOR OF INCOME TAX (INTERNATIONAL TAXATION), NEW DELHI 02.12.2005 HISTORICALLY Concept of transfer pricing always there

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE A PRESENTATION BY AKHILESH RANJAN DIRECTOR OF INCOME TAX (INTERNATIONAL TAXATION), NEW DELHI 02.12.2005 HISTORICALLY Concept of transfer pricing always there

GUIDE TO TRANSFER PRICING BACKGROUNDER. (i)

") GUIDE TO TRANSFER PRICING BACKGROUNDER (i) First Edition : November 2016 Price : Rs. 120/-- (Excluding postage) THE INSTITUTE OF COMPANY SECRETARIES OF INDIA All rights reserved. No part of this book may

GUIDE TO TRANSFER PRICING BACKGROUNDER (i) First Edition : November 2016 Price : Rs. 120/-- (Excluding postage) THE INSTITUTE OF COMPANY SECRETARIES OF INDIA All rights reserved. No part of this book may

Transfer Pricing Scope and Jurisdiction. Presentation By. - S.P. Singh - Manoj Pardasani

Transfer Pricing Scope and Jurisdiction Presentation By - S.P. Singh - Manoj Pardasani For private circulation amongst participants in NIRC s Seminar on Transfer Pricing on 13 June 2015 at Delhi Contents

Transfer Pricing Scope and Jurisdiction Presentation By - S.P. Singh - Manoj Pardasani For private circulation amongst participants in NIRC s Seminar on Transfer Pricing on 13 June 2015 at Delhi Contents

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria

![Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria](/thumbs/90/101594279.jpg "Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria") Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

TAX AUDIT POINTS TO BE CONSIDERED

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

DIRECT TAXES AND INDIRECT TAXES UPDATES APPLICABLE FOR DECEMBER 2012 EXAMINATION FOR EXECUTIVE & PROFESSIONAL PROGRAMME

DIRECT TAXES AND INDIRECT TAXES UPDATES APPLICABLE FOR DECEMBER 2012 EXAMINATION FOR EXECUTIVE & PROFESSIONAL PROGRAMME *Disclaimer- This document has been prepared purely for academics purposes only and

DIRECT TAXES AND INDIRECT TAXES UPDATES APPLICABLE FOR DECEMBER 2012 EXAMINATION FOR EXECUTIVE & PROFESSIONAL PROGRAMME *Disclaimer- This document has been prepared purely for academics purposes only and

Practical aspects - Documentation, Benchmarking and Transfer Pricing Analysis IT/ITES, KPO and Engineering. Vaishali Mane Mumbai

Practical aspects - Documentation, Benchmarking and Transfer Pricing Analysis IT/ITES, KPO and Engineering Vaishali Mane Mumbai Agenda Transfer Pricing A quick background Operation Challenges Litigation

Practical aspects - Documentation, Benchmarking and Transfer Pricing Analysis IT/ITES, KPO and Engineering Vaishali Mane Mumbai Agenda Transfer Pricing A quick background Operation Challenges Litigation

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH L, MUMBAI BEFORE SHRI R.S.SYAL (A.M) & SHRI N.V.VASUDEVAN(J.M) ITA NO.5779/MUM/07(A.Y ) Vs.

& SHRI N.V.VASUDEVAN(J.M) ITA NO.5779/MUM/07(A.Y ) Vs.") IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH L, MUMBAI BEFORE SHRI R.S.SYAL (A.M) & SHRI N.V.VASUDEVAN(J.M) ITA NO.5779/MUM/07(A.Y.2003-04) The ACIT, Range 8(3), Room No.204, 2 nd Floor, Aaykay Bhavan,

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH L, MUMBAI BEFORE SHRI R.S.SYAL (A.M) & SHRI N.V.VASUDEVAN(J.M) ITA NO.5779/MUM/07(A.Y.2003-04) The ACIT, Range 8(3), Room No.204, 2 nd Floor, Aaykay Bhavan,

Special provision in respect of newly established undertakings in free trade zone, etc.

Special provision in respect of newly established undertakings in free trade zone, etc. 10A. (1) Subject to the provisions of this section, a deduction of such profits and gains as are derived by an undertaking

Special provision in respect of newly established undertakings in free trade zone, etc. 10A. (1) Subject to the provisions of this section, a deduction of such profits and gains as are derived by an undertaking

Details required in Form 3CD relevant to Computation of Income

Information for Tax Audit Report AY - 214-215 12 Whether Profit and Loss Account includes profit on assessable on presumptive basis If Yes, provide Details and Style of Business Nature of Business Sec

Information for Tax Audit Report AY - 214-215 12 Whether Profit and Loss Account includes profit on assessable on presumptive basis If Yes, provide Details and Style of Business Nature of Business Sec

A BILL to give effect to the financial proposals of the Central Government for the financial year

FINANCE BILL, 2012* Bill No. 11 of 2012 A BILL to give effect to the financial proposals of the Central Government for the financial year 2012-2013. BE it enacted by Parliament in the Sixty-third Year

FINANCE BILL, 2012* Bill No. 11 of 2012 A BILL to give effect to the financial proposals of the Central Government for the financial year 2012-2013. BE it enacted by Parliament in the Sixty-third Year