Rajeev Pai, Chief Financial Officer JSW Steel Limited

|

|

|

- Ashley Tate

- 6 years ago

- Views:

Transcription

1 Rajeev Pai, Chief Financial Officer JSW Steel Limited

2 Setting of Enterprise Resource Planning (ERP) based system and key challenges Accounting Standards and Regulatory compliance and Challenges thereof Reporting to owners / shareholders

3 Setting of ERP based Financial system and challenges

4 An ERP system is an attempt to integrate all functions across a company to a single computer system to serve all functions specific needs. It provides integrated database and custom-designed report systems. It adopts a set of best practices for carrying out all business processes.

5 Integrated financial information Integrated customer order information Standardization and optimization of operational processes Standardization of various information and report

6 Internal Benefits Integration of information enhances financial and internal controls A real-time system Increased productivity and reduced operating costs Improved internal communication Foundation for future improvement

7 External Benefits Improved customer service and order fulfillment Improved communication with suppliers and customers Enhanced competitive position Increased sales and profits

8 Resistance to change Limitation on customization of ERP system due to inconsistency with existing business processes Cost of implementation (hardware, software, training, consulting) and maintenance Impact on organizational structure (front office vs. back office, product lines, etc.) Interface to other software systems Implementation timelines Availability of internal technical knowledge and resources Education and training Implementation strategy and execution

9 Accounting Standards (AS), Regulatory compliance and Key Challenges

10 Why Accounting Standards? - To harmonize the diverse accounting policies and practices in use in India - To enables the users to interpret the reported information in a better way. - Uniform adoption and disclosure of accounting policies AS consists of detailed rules to be adopted for accounting treatment of various items before the presentation of financial statements.

11 AS 1 to to 1995 AS 16 to to 2007 (7) As 30 to 32 After 2007 (Yet to be notified)

12 Statutes e.g. Companies Act, etc. - Schedule VI, Companies (Accounting Standards) Rules, 2006, etc. SEBI / RBI Regulations, etc. Accounting Standard Board (ASB) of Institute of Chartered Accountants of India (ICAI) Framework Accounting Standards (AS) Accounting Standard Interpretations (ASI) Guidance notes (GN) Various accounting announcements Expert Advisory Opinion (EAC) ICAI Technical Guides ICAI Monographs ICAI Research publications

13 Section 210A Constitution of National Advisory Committee on Accounting Standards (NACAS) Section 211 P&L, Balance Sheet to comply with the Accounting Standards Accounting Standards as may be prescribed by the Central Government Till that time, standards issued by ICAI to be followed Formation of NACAS Committee - Headed by Shri Y. H. Malegam as Chairman and representatives from various bodies viz. ICAI, ICSI, RBI, SEBI etc. NACAS recommended Standards 1 to 7 and 9 to 29 (AS 8 R&D part of AS 26)

14 IND-AS accounting standard equivalent to IFRS have been issued by NACAS in India however the adoption of these standards have been postponed. Companies Act has amended the presentation of financials statements by issuing Revised Schedule VI for the financial years beginning from Revised Schedule VI has brought the disclosure of financial statements more or less in accordance with IFRS.

15 Other Regulatory compliances

16 Key Compliances: - Adoption of audited annual accounts at AGM and filing (XBRL) thereof within 30 days of AGM - Maintenance of register under various section of the Companies Act (example - register of investments, charges etc) - Filing of various forms with ROC (like appointment of directors, allotment of shares etc) - Compliance with minimum number of board meetings, audit committee (if applicable), shareholder meetings etc. and maintenance of various records thereof - Defines power within which Board of directors to act upon - Cost Audit Report, if applicable, to be filed within 180 days from end of financial year.

17 Key Compliances: - Transfer pricing International & Domestic Transfer Pricing - Tax audit and Filing of Annual Income Tax return - Payment of Advance Tax - TDS Compliance

18

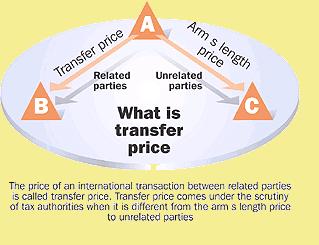

19 Transfer Pricing 19

20 What is Transfer Pricing Analysis The process of determining what is the arm s length price for a transaction (or a group of similar transactions) 20

21 TP was earlier limited to International Transactions The Finance Act 2012, extends the scope of TP provision to Specified Domestic Transactions between related parties w.e.f. 1 April 2012 Obligation now on taxpayer to report/ document and substantiate the arm s length nature of such transactions

22 Transfer Pricing - Domestic Intent of Indian TP Regulations (Domestic transactions) India Shifting of expenses/losses India Tax Exemption Indian Co. Tax Holiday undertaking Related Enterprise in Domestic Tariff Area (DTA) Shifting of income/profits Tax Saving for the Group Loss to Indian revenue 22

23 Section 92BA Meaning of Specified Domestic Transactions (SDT) (inserted by Finance Act, 2012 w.e.f. AY i.e. current FY) For the purposes of this section and sections 92, 92C, 92D and 92E, specified domestic transaction in case of an assessee means any of the following transactions, not being an international transaction, namely:- (i) any expenditure in respect of which payment has been made or is to be made to a person referred to in section 40A(2)(b); (ii) any transaction referred to in section 80A; (iii) any transfer of goods or services referred to in sub-section (8) of section 80-IA; (iv) any business transacted between the assessee and other person as referred to in section 80-IA (10); (v) any transaction, referred to in any other section under Chapter VIA or section 10AA, to which provisions of section 80-IA(8) or section 80-IA(10) are applicable; or (vi) any other transaction as may be prescribed, and where the aggregate of such transactions entered into by the assessee in the previous year exceeds a sum of five crore rupees. 23

24 Computation of Arm s Length Price by applying the most appropriate method out of Comparable Uncontrolled Price (CUP) Resale Price Method (RPM) Cost Plus Method (CPM) Transaction Net Margin Method (TNMM) Profit Split Method (PSM)

25 Challenges Type of payments/ transactions Salary and Bonuses paid to the partners Remuneration paid to the Directors Transfer of land Joint Development agreements Challenges Benchmarking? Whether the limit as mentioned in section 40 (b) would be the ALP? Benchmarking? Whether the limit as mentioned in Schedule XIII would be the ALP? Whether the rates mentioned in the ready reckoner be considered as ALP? Benchmarking? Project management fees Benchmarking? Allocation of expenses between the same taxpayer having an eligible unit and non-eligible unit Definition of Related Party Whether these allocation would be SDT Sec 80-IA(10)? Directly v/s Indirectly 25

26 Key Compliances Service Tax Applicable on all services except negative list Excise Duty Applicable on goods manufactured Custom Duty Applicable on import of goods Sales Tax/VAT Applicable on Sale of goods (inter state and intra state) Compliance includes timely filing of returns, payment of taxes etc

27 Payment of Service Tax - by 5 th of succeeding month - For March month by 31 st March ST 3 Returns has to be e-filed half-yearly Period Due Date April to September 25 th October October to March 25 th April 27

28 Form Description Who is require to file Time limit ER-1 Monthly return by large units Manufacturers not eligible for SSI concession 10 th of following mth. ER-2 Return by EOU EOU units 10 th of following mth. ER-3 Quarterly return by SSI Assesses availing SSI concession ER-4 ER-5 ER-6 ER-7 Annual financial information statement Information relating to principal inputs Monthly return of receipts & consumption of each of Principal Inputs Annual Install capacity statement Assesses paying duty of Rs. One crore or more per annum through PLA. Assesses paying duty of Rs. One crore or more per annum through PLA and manufacturing goods under specified tariff heading Assesses who is required to submit ER-5 return All assessee 20 th of following qtr. Annually, by 30 th Nov. of succeeding year. Annually, by 30 th April of current year. 10 th of following month Annually on or before 30 th April. 28

29 SEBI Act (Applicable to listed entities ) - Corporate Governance Report (Clause 49) - Quarterly standalone and consolidated financial statements (clause 41) - Shareholding pattern (Clause 35) Others - Compliance with respect to compliance with Factories Act and other applicable labor legislations. - Compliance with Foreign Exchange Management Act. - Compliance with Environment Laws. - Compliance with Employers Provident Fund and Miscellaneous Provisions Act, 1952, Payment of Bonus Act, Payment of Gratuity Act etc.

30 - Ensuring that the financials are prepared in accordance with the measurement and disclosures requirement of accounting standards - Various Assumptions made in preparation of financial statements - Frequent changes in rules and regulations - Multiple Acts/ regulators increase cost of compliance and litigations. For example in case indirect tax, tax is levied at various instances such excise on manufactured, service tax on services and VAT/Sales Tax on sale of goods which can be substituted by a single act like Goods and Service Tax (GST) Act. Govt. of India is already contemplating for implementation of the same.

31 To submit annual report containing Corporate Governance, Business Sustainability Report, Management Discussion and Analysis alongwith audited financial statements. Intimation to shareholders on key updates through press release, advertisement in newspapers etc Maintenance and making available to shareholders of various statutory registers and documents as defined under various laws.

32 Voluntary disclosures like Guidance on profitability of the company Current status and key updates to Investor and Analyst through meet.

33 Thank You.

Domestic Transfer Pricing

Domestic Transfer Pricing By CA Nihar Jambusaria Central Council Member ICAI {Mumbai} Overview Transfer pricing (referred to as TP) regulations introduced in India in 2001, previously covered only cross

Domestic Transfer Pricing By CA Nihar Jambusaria Central Council Member ICAI {Mumbai} Overview Transfer pricing (referred to as TP) regulations introduced in India in 2001, previously covered only cross

DOMESTIC TRANSFER PRICING. By CA Ramesh S Iyer

DOMESTIC TRANSFER PRICING By CA Ramesh S Iyer 04-08-2013 1 Reasons for introduction The SC in the case of CIT vs. Glaxo Smithkline Asia Pvt Ltd [2010]195Taxman 35(SC) recommended introduction of domestic

DOMESTIC TRANSFER PRICING By CA Ramesh S Iyer 04-08-2013 1 Reasons for introduction The SC in the case of CIT vs. Glaxo Smithkline Asia Pvt Ltd [2010]195Taxman 35(SC) recommended introduction of domestic

Transfer Pricing of Domestic Transactions & Provisions of. or Complimentary. 7 December 2013 Rajan Vora

Transfer Pricing of Domestic Transactions & Provisions of Section 40A(2)(b) Contradictory or Complimentary 7 December 2013 Rajan Vora Outline Rationale for introducing transfer pricing Brief background

Transfer Pricing of Domestic Transactions & Provisions of Section 40A(2)(b) Contradictory or Complimentary 7 December 2013 Rajan Vora Outline Rationale for introducing transfer pricing Brief background

CA TIRTHESH M. BAGADIYA

DOMESTIC TRANSFER PRICING CA TIRTHESH M. BAGADIYA 1 1 Introduction Previously TP applicable only to international transactions By virtue of Finance Act, 2012, TP provision ambit has been extended to Specified

DOMESTIC TRANSFER PRICING CA TIRTHESH M. BAGADIYA 1 1 Introduction Previously TP applicable only to international transactions By virtue of Finance Act, 2012, TP provision ambit has been extended to Specified

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA DOMESTIC TRANSFER PRICING PROVISIONS CA.T. P. OSTWAL 21st September 2012 1 Introduction TP was earlier limited to International Transactions The Finance Act

INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA DOMESTIC TRANSFER PRICING PROVISIONS CA.T. P. OSTWAL 21st September 2012 1 Introduction TP was earlier limited to International Transactions The Finance Act

DOMESTIC TRANSFER PRICING CONFERENCE

DOMESTIC TRANSFER PRICING CONFERENCE Importance of FAR & Comparability; Selection of the Most Appropriate Method and Issues in disclosure in new Form 3CEB from SDT perspective 19 October 2013 Pramod Joshi

DOMESTIC TRANSFER PRICING CONFERENCE Importance of FAR & Comparability; Selection of the Most Appropriate Method and Issues in disclosure in new Form 3CEB from SDT perspective 19 October 2013 Pramod Joshi

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

TRANSFER PRICING - DOMESTIC TRANSACTIONS AN INSIGHT GAURAV SHAH OCTOBER 2012

1 TRANSFER PRICING - DOMESTIC TRANSACTIONS AN INSIGHT GAURAV SHAH OCTOBER 2012 Table of Contents Introduction to Transfer Pricing International Transfer Pricing Background Domestic Transfer Pricing Differences

1 TRANSFER PRICING - DOMESTIC TRANSACTIONS AN INSIGHT GAURAV SHAH OCTOBER 2012 Table of Contents Introduction to Transfer Pricing International Transfer Pricing Background Domestic Transfer Pricing Differences

Issues in Domestic Transfer Pricing including various methods for determining ALP

Issues in Domestic Transfer Pricing including various methods for determining ALP Rakesh Alshi, Anand Thacker - 6 th October 2014 2014 Deloitte Haskins & Sells LLP 1 Contents 1. Specified Domestic Transactions

Issues in Domestic Transfer Pricing including various methods for determining ALP Rakesh Alshi, Anand Thacker - 6 th October 2014 2014 Deloitte Haskins & Sells LLP 1 Contents 1. Specified Domestic Transactions

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

Future of TP. Documentation & Certification. 7th October Presented by- CA Dilip Gupta

Future of TP Documentation & Certification 7th October 2017 Presented by- CA Dilip Gupta Journey of TP regulations in India Major Milestones Final Rules on Range and multiple year data concept Introduction

Future of TP Documentation & Certification 7th October 2017 Presented by- CA Dilip Gupta Journey of TP regulations in India Major Milestones Final Rules on Range and multiple year data concept Introduction

Domestic Transfer Pricing

Table of Contents DOMESTIC TRANSFER PRICING Benchmarking and Reporting requirements Study Circle Meeting CA Gaurav Shah 15 th June 2013 Domestic Transfer Pricing Benchmarking Analysis Transfer Pricing

Table of Contents DOMESTIC TRANSFER PRICING Benchmarking and Reporting requirements Study Circle Meeting CA Gaurav Shah 15 th June 2013 Domestic Transfer Pricing Benchmarking Analysis Transfer Pricing

DOMESTIC TRANSFER PRICING REGULATIONS

DOMESTIC TRANSFER PRICING REGULATIONS (Taxation of specified domestic transactions in India) By B. D. Jokhakar & Co. Chartered Accountants INDIA TABLE OF CONTENTS Sr. No. Topic Page no. I INTRODUCTION

DOMESTIC TRANSFER PRICING REGULATIONS (Taxation of specified domestic transactions in India) By B. D. Jokhakar & Co. Chartered Accountants INDIA TABLE OF CONTENTS Sr. No. Topic Page no. I INTRODUCTION

Bombay Chartered Accountants Society. Vispi T. Patel Vispi T. Patel & Associates

FAR Analysis, Selection of Most Appropriate Method, Application of Methods (CUP & RPM) and Case Studies with reference to Specified Domestic Transactions Bombay Chartered Accountants Society Vispi T. Patel

FAR Analysis, Selection of Most Appropriate Method, Application of Methods (CUP & RPM) and Case Studies with reference to Specified Domestic Transactions Bombay Chartered Accountants Society Vispi T. Patel

BY CA MAYUR B NAYAK 1

BY CA MAYUR B NAYAK 1 Govt. should collect taxes from citizens the way a Bee collects Honey from the flowers - quietly without inflicting pain". -Chanakya BY CA MAYUR B NAYAK 2 Financial Year Transfer

BY CA MAYUR B NAYAK 1 Govt. should collect taxes from citizens the way a Bee collects Honey from the flowers - quietly without inflicting pain". -Chanakya BY CA MAYUR B NAYAK 2 Financial Year Transfer

Transfer Pricing in India Examining inter-company cross-border transactions

Transfer Pricing in India Examining inter-company cross-border transactions 1 Contents Background and history Meaning of International transaction Specified Domestic Transaction Arm s Length Price Associated

Transfer Pricing in India Examining inter-company cross-border transactions 1 Contents Background and history Meaning of International transaction Specified Domestic Transaction Arm s Length Price Associated

Specified Domestic Transactions Coverage and Analysis. S P Singh

Specified Domestic Transactions Coverage and Analysis S P Singh August 2012 Introduction The Finance Act 2012, extends the scope of Transfer Pricing provision to Specified Domestic Transactions ( SDT )

Specified Domestic Transactions Coverage and Analysis S P Singh August 2012 Introduction The Finance Act 2012, extends the scope of Transfer Pricing provision to Specified Domestic Transactions ( SDT )

Overview of Transfer Pricing

Overview of Transfer Pricing Contents Legislative framework Transfer pricing study Assessment and Litigation Key Recent Developments Page 2 Transfer Pricing in India- Background April 1, 2001 onwards Comprehensive

Overview of Transfer Pricing Contents Legislative framework Transfer pricing study Assessment and Litigation Key Recent Developments Page 2 Transfer Pricing in India- Background April 1, 2001 onwards Comprehensive

BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING

CONTENTS BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING CHAPTER 1 : INTRODUCTION 3 CHAPTER 2 : FEATURES OF THE TRANSFER PRICING REGIME UNDER CHAPTER X 10 CHAPTER 3 : TRANSFER PRICING PROVISIONS OF CHAPTER

CONTENTS BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING CHAPTER 1 : INTRODUCTION 3 CHAPTER 2 : FEATURES OF THE TRANSFER PRICING REGIME UNDER CHAPTER X 10 CHAPTER 3 : TRANSFER PRICING PROVISIONS OF CHAPTER

Audit of Domestic Transfer Pricing

Audit of Domestic Transfer Pricing Prakash Udeshi B.Com, FCA, CS, CMA KALARIA & SAMPAT Chartered Accountants Ahmedabad Applicability - SDT The Finance Act 2012 extended the scope of Transfer Pricing provision

Audit of Domestic Transfer Pricing Prakash Udeshi B.Com, FCA, CS, CMA KALARIA & SAMPAT Chartered Accountants Ahmedabad Applicability - SDT The Finance Act 2012 extended the scope of Transfer Pricing provision

Introduction to Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria

-Nihar Jambusaria") SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria TP Regulations to apply to certain Specified Domestic Transactions [New Section 92BA] TP provisions are applicable to the following Domestic

SPECIFIED DOMESTIC TRANSACTION SECTION 40a(2) -Nihar Jambusaria TP Regulations to apply to certain Specified Domestic Transactions [New Section 92BA] TP provisions are applicable to the following Domestic

September 1, By: CA. Gaurav Garg

September 1, 2012 By: CA. Gaurav Garg Transfer pricing bleeding ground for the corporate but breeding ground for consultants Transfer pricing addition in first six years equal to addition made addition

September 1, 2012 By: CA. Gaurav Garg Transfer pricing bleeding ground for the corporate but breeding ground for consultants Transfer pricing addition in first six years equal to addition made addition

An overview of Transfer Pricing

An overview of Transfer Pricing CTC Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing CTC Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

B S R & Co. LLP. Specified Domestic Transactions. Pankil Sanghvi Director. 10 October 2015

Specified Domestic Transactions B S R & Co. LLP Pankil Sanghvi Director 10 October 2015 1 Background Genesis of Domestic Transfer Pricing Regulations Supreme Court (SC) in the case of CIT v Glaxo SmithKline

Specified Domestic Transactions B S R & Co. LLP Pankil Sanghvi Director 10 October 2015 1 Background Genesis of Domestic Transfer Pricing Regulations Supreme Court (SC) in the case of CIT v Glaxo SmithKline

Transfer Pricing Methods and Selection of Most Appropriate Method. Vaishali Mane Partner Grant Thornton India LLP Mumbai

Transfer Pricing Methods and Selection of Most Appropriate Method Vaishali Mane Partner Grant Thornton India LLP Mumbai Agenda Transfer Pricing Quick background Arm's Length Principle Overview of Methods

Transfer Pricing Methods and Selection of Most Appropriate Method Vaishali Mane Partner Grant Thornton India LLP Mumbai Agenda Transfer Pricing Quick background Arm's Length Principle Overview of Methods

Domestic Transfer Pricing

Domestic Transfer Pricing September 15, 2012 CA Darpan Mehta Agenda 1 Domestic TP Transactions 2 Case Study 3 Way Forward Slide 2 Transactions Slide 3 Intent of Indian Transfer Pricing (TP) Regulations

Domestic Transfer Pricing September 15, 2012 CA Darpan Mehta Agenda 1 Domestic TP Transactions 2 Case Study 3 Way Forward Slide 2 Transactions Slide 3 Intent of Indian Transfer Pricing (TP) Regulations

TRANSFER PRICING DATED CA. Ashwani Rastogi, New Delhi

TRANSFER PRICING DATED 8.6.2017 1 India has signed the historic multilateral convention to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS), at Paris with More than

TRANSFER PRICING DATED 8.6.2017 1 India has signed the historic multilateral convention to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS), at Paris with More than

DOMESTIC TRANSFER PRICING

17 November 2013 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

17 November 2013 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

Transfer Pricing Backdrop in. Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016

Transfer Pricing Backdrop in India Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016 Presentation Outline Introduction ti Transfer Pricing Regulations in India Arms

Transfer Pricing Backdrop in India Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016 Presentation Outline Introduction ti Transfer Pricing Regulations in India Arms

d e vreser st ighr lla

Article 7 and 9 of the model conventions including International and Domestic TP Beginners Study Course on International Taxation July 4, 2015 Neha Arora 2 Contents Article 7 of the Model Convention Approaches

Article 7 and 9 of the model conventions including International and Domestic TP Beginners Study Course on International Taxation July 4, 2015 Neha Arora 2 Contents Article 7 of the Model Convention Approaches

Arm s Length Principle. Kavita Sethia Gambhir

Arm s Length Principle Kavita Sethia Gambhir January 2017 Introduction 2 Background Economic Globalization Multinational Structure Different Objectives Top Management/Key Personnel Shareholders Tax Authorities

Arm s Length Principle Kavita Sethia Gambhir January 2017 Introduction 2 Background Economic Globalization Multinational Structure Different Objectives Top Management/Key Personnel Shareholders Tax Authorities

TRANSFER PRICING. 19 th July, July-14 1

TRANSFER PRICING 19 th July, 2014 19-July-14 1 TRANSFER PRICING AND ITS FUTURE PROSPECTS Due to the increasing trend in globalization of Indian business, transfer pricing will remain foremost on the agenda

TRANSFER PRICING 19 th July, 2014 19-July-14 1 TRANSFER PRICING AND ITS FUTURE PROSPECTS Due to the increasing trend in globalization of Indian business, transfer pricing will remain foremost on the agenda

Domestic Transfer Pricing in India

Domestic Transfer Pricing in India By (Partner) SBR & CO. Chartered Accountants P a g e 1 After the grand success of International Transfer pricing, through which huge transfer pricing orders slapped on

Domestic Transfer Pricing in India By (Partner) SBR & CO. Chartered Accountants P a g e 1 After the grand success of International Transfer pricing, through which huge transfer pricing orders slapped on

Domestic Transfer Pricing Provisions

Domestic Transfer Pricing Provisions Ameya Kunte April 4, 2014 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP

Domestic Transfer Pricing Provisions Ameya Kunte April 4, 2014 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP

Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer

CA. Vispi T. Patel, CA. Rajiv Shah and CA.Kejal Visharia Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer INTERNATIONAL PRICING PROVISIONS TRANSFER Introduction

CA. Vispi T. Patel, CA. Rajiv Shah and CA.Kejal Visharia Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer INTERNATIONAL PRICING PROVISIONS TRANSFER Introduction

DOMESTIC TRANSFER PRICING

12 October 2014 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

12 October 2014 WIRC of ICAI: J B Nagar CPE Study Circle INTRODUCTION [ 3] COVERAGE & IMPLICATIONS [ 8] DOCUMENTATION & CERTIFICATION [15] ISSUES & CASE STUDIES [29] KEY TAKEAWAYS [40] Page 2 Introduction

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

Transfer Pricing. Recent Trends & Key Developments. PHD Chamber International Tax Conference September 04, 2014 New Delhi. Statement of Credentials 1

Transfer Pricing Recent Trends & Key Developments PHD Chamber International Tax Conference September 04, 2014 New Delhi Statement of Credentials 1 SESSION DETAILS Topic: Transfer Pricing Recent Trends

Transfer Pricing Recent Trends & Key Developments PHD Chamber International Tax Conference September 04, 2014 New Delhi Statement of Credentials 1 SESSION DETAILS Topic: Transfer Pricing Recent Trends

TRANSFER PRICING IN INDIA DOMESTIC TRANSACTION AN ADDED DIMENSION For Jallandhar Branch Of NIRC Of. By: CA Krishan Vrind Jain Dated 08/08/2013

TRANSFER PRICING IN INDIA DOMESTIC TRANSACTION AN ADDED DIMENSION For Jallandhar Branch Of NIRC Of ICAI By: CA Krishan Vrind Jain Dated 08/08/2013 Finance Minister s speech on the rational for introducing

TRANSFER PRICING IN INDIA DOMESTIC TRANSACTION AN ADDED DIMENSION For Jallandhar Branch Of NIRC Of ICAI By: CA Krishan Vrind Jain Dated 08/08/2013 Finance Minister s speech on the rational for introducing

Specific Domestic Transactions. Documentation & Audit Report Requirements Key concern Areas. 22 November 2013

Specific Domestic Transactions Documentation & Audit Report Requirements Key concern Areas 22 November 2013 Agenda Requirements at glace Key issues relating to applicability to various entities Transactions

Specific Domestic Transactions Documentation & Audit Report Requirements Key concern Areas 22 November 2013 Agenda Requirements at glace Key issues relating to applicability to various entities Transactions

Domestic Transfer Pricing (India)

") Domestic Transfer Pricing (India) After the grand success of International Transfer pricing, through which huge transfer pricing orders slapped on companies with cross-border operations in the last financial

Domestic Transfer Pricing (India) After the grand success of International Transfer pricing, through which huge transfer pricing orders slapped on companies with cross-border operations in the last financial

CONTENTS. Introduction to Transfer Pricing. Transfer Pricing Litigation Statistics. Introduction to Domestic Transfer Pricing

DOMESTIC TRANSFER PRICING CONTENTS Introduction to Transfer Pricing Transfer Pricing Litigation Statistics Introduction to Domestic Transfer Pricing Section 40A(2)(b), 80IA(8) & 80IA(10) Relationships,

DOMESTIC TRANSFER PRICING CONTENTS Introduction to Transfer Pricing Transfer Pricing Litigation Statistics Introduction to Domestic Transfer Pricing Section 40A(2)(b), 80IA(8) & 80IA(10) Relationships,

Domestic Transfer Pricing

Domestic Transfer Pricing Ameya Kunte 20 March 2015 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP Framework SDT

Domestic Transfer Pricing Ameya Kunte 20 March 2015 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP Framework SDT

(Applicability & impact Analysis) By:-

By:-") Domestic Transfer Pricing (Applicability & impact Analysis) By:- Surana Maloo & Co. Chartered Accountants 2 nd Floor, Aakash Ganga Complex, Parimal Under Bridge, Nr Suvidha Shopping Center, Paldi, Ahmedabad-

Domestic Transfer Pricing (Applicability & impact Analysis) By:- Surana Maloo & Co. Chartered Accountants 2 nd Floor, Aakash Ganga Complex, Parimal Under Bridge, Nr Suvidha Shopping Center, Paldi, Ahmedabad-

CONTENT. Mulund CPE Study Circle of ICAI. Domestic Transfer Pricing Applicability & Overview 15/6/2013. CA Paras K Savla

Mulund CPE Study Circle of ICAI Domestic Transfer Pricing Applicability & Overview 15/6/2013 CA Paras K Savla CONTENT Introduction Specified domestic transactions Illustrations Procedures ALP under other

Mulund CPE Study Circle of ICAI Domestic Transfer Pricing Applicability & Overview 15/6/2013 CA Paras K Savla CONTENT Introduction Specified domestic transactions Illustrations Procedures ALP under other

CBDT Draft Rules on "range concept" and "multiple year data" - A boon or bane?

CBDT Draft Rules on "range concept" and "multiple year data" - A boon or bane? Date: May 25,2015 Keyur Shah (Part ner, Financial Services T ransfer Pricing, EY) Jaiman Pat el (Direct or, Financial Services

CBDT Draft Rules on "range concept" and "multiple year data" - A boon or bane? Date: May 25,2015 Keyur Shah (Part ner, Financial Services T ransfer Pricing, EY) Jaiman Pat el (Direct or, Financial Services

The Chamber of Tax Consultants

The Chamber of Tax Consultants Case Studies on Domestic Transfer Pricing w.r.t section 80A/80IA/10AA including its bench marking Presentation by Yogesh Thar April 29, 2016 1 Genesis of Transfer Pricing

The Chamber of Tax Consultants Case Studies on Domestic Transfer Pricing w.r.t section 80A/80IA/10AA including its bench marking Presentation by Yogesh Thar April 29, 2016 1 Genesis of Transfer Pricing

Methods of determining ALP

3 rd Intensive Study Course on Transfer Pricing Methods of determining ALP CA Vishwanath Kane 16 February 2013 Agenda Introduction Transfer Pricing Methods Overview Applicability of Transfer Pricing Methods

3 rd Intensive Study Course on Transfer Pricing Methods of determining ALP CA Vishwanath Kane 16 February 2013 Agenda Introduction Transfer Pricing Methods Overview Applicability of Transfer Pricing Methods

FINANCIAL LITERACY FOR DIRECTORS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA. 16 th December 2017, IOD

FINANCIAL LITERACY FOR DIRECTORS 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain Annual Report Director s Report Auditor s Report Financial Statements Balance

FINANCIAL LITERACY FOR DIRECTORS 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain Annual Report Director s Report Auditor s Report Financial Statements Balance

PROCTER & GAMBLE HYGIENE AND HEALTH CARE LIMITED RELATED PARTY TRANSACTION POLICY

PROCTER & GAMBLE HYGIENE AND HEALTH CARE LIMITED RELATED PARTY TRANSACTION POLICY PREAMBLE: The Procter & Gamble Company s Worldwide Business Conduct Manual provides that all employees and directors must

PROCTER & GAMBLE HYGIENE AND HEALTH CARE LIMITED RELATED PARTY TRANSACTION POLICY PREAMBLE: The Procter & Gamble Company s Worldwide Business Conduct Manual provides that all employees and directors must

Functional Analysis, Comparability Analysis and Economic Analysis. Vispi T. Patel Vispi T. Patel & Associates

Functional Analysis, Comparability Analysis and Economic Analysis Vispi T. Patel Vispi T. Patel & Associates February 6, 2016 AGENDA Arm s Length Price and its computation Functional, Asset and Risk Analysis

Functional Analysis, Comparability Analysis and Economic Analysis Vispi T. Patel Vispi T. Patel & Associates February 6, 2016 AGENDA Arm s Length Price and its computation Functional, Asset and Risk Analysis

JGARG. Economic Advisors. Tri Nagar Keshav Puram Study Circle Of North India Regional Council. By: CA. Gaurav Garg

JGARG Economic Advisors Tri Nagar Keshav Puram Study Circle Of North India Regional Council By: CA. Gaurav Garg Warm-up Indian TP Regulations Arm s Length Principle The Tax Treaty Aspect Meaning of Associated

JGARG Economic Advisors Tri Nagar Keshav Puram Study Circle Of North India Regional Council By: CA. Gaurav Garg Warm-up Indian TP Regulations Arm s Length Principle The Tax Treaty Aspect Meaning of Associated

Issues in Transfer Pricing

Issues in Transfer Pricing Vaishali Mane Chartered Accountant, Mumbai 2017 Grant Thornton India LLP. All rights reserved. 1 Contents 1 Transfer Pricing - Basic 2 Recent Developments in Transfer Pricing

Issues in Transfer Pricing Vaishali Mane Chartered Accountant, Mumbai 2017 Grant Thornton India LLP. All rights reserved. 1 Contents 1 Transfer Pricing - Basic 2 Recent Developments in Transfer Pricing

TRANSFER PRICING. - to be AWARE or BEWARE?

TRANSFER PRICING - to be AWARE or BEWARE? E-Venue: The Institute of Cost Accountants of India Webinar ( 10.01.2018 ) By CMA Chiranjib Das, FCMA, ACA, M.Com Presentation Plan (1) Transfer Pricing an Overview

TRANSFER PRICING - to be AWARE or BEWARE? E-Venue: The Institute of Cost Accountants of India Webinar ( 10.01.2018 ) By CMA Chiranjib Das, FCMA, ACA, M.Com Presentation Plan (1) Transfer Pricing an Overview

Ind-AS Implementation Issues. Himanshu Kishnadwala

Ind-AS Implementation Issues Himanshu Kishnadwala What is I-GAAP? Accounting Standards in India Till 2006, Standards issued by ASB of ICAI were to be followed Companies (Accounting Standards) Rules, notified

Ind-AS Implementation Issues Himanshu Kishnadwala What is I-GAAP? Accounting Standards in India Till 2006, Standards issued by ASB of ICAI were to be followed Companies (Accounting Standards) Rules, notified

Applicability of Transfer Pricing to Specified Domestic Transactions

Applicability of Transfer Pricing to Specified Domestic Transactions Outline Introduction Overview of provisions Analysis of provisions Impact on taxpayers Way forward & EY approach Page 2 Abbreviations

Applicability of Transfer Pricing to Specified Domestic Transactions Outline Introduction Overview of provisions Analysis of provisions Impact on taxpayers Way forward & EY approach Page 2 Abbreviations

Workshop on Basics in Transfer Pricing. Domestic Transfer Pricing By

Workshop on Basics in Transfer Pricing Domestic Transfer Pricing By CA Praveen Ranka Introduction SDT The Intent The Finance Act, 2012 extended applicability of transfer pricing provisions to Specified

Workshop on Basics in Transfer Pricing Domestic Transfer Pricing By CA Praveen Ranka Introduction SDT The Intent The Finance Act, 2012 extended applicability of transfer pricing provisions to Specified

Transfer Pricing Principles By Wilfred Alambo KPMG Advisory Services Limited

Transfer Pricing Principles By Wilfred Alambo KPMG Advisory Services Limited Introduction, African overview and TP methods Table of contents 1. Background & introduction 2. Overview TP in Africa 3. TP

Transfer Pricing Principles By Wilfred Alambo KPMG Advisory Services Limited Introduction, African overview and TP methods Table of contents 1. Background & introduction 2. Overview TP in Africa 3. TP

Bangladesh Transfer Pricing Regulations Finance Act, 2014

30 October 2014 Global Tax Alert News from Transfer Pricing EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

30 October 2014 Global Tax Alert News from Transfer Pricing EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

Transfer Pricing and Other Provisions to Check Avoidance of Tax

16 Transfer Pricing and Other Provisions to Check Avoidance of Tax Question 1 State the consequences that would follow if the Assessing Officer makes adjustment to arm s length price in international transactions

16 Transfer Pricing and Other Provisions to Check Avoidance of Tax Question 1 State the consequences that would follow if the Assessing Officer makes adjustment to arm s length price in international transactions

The Chamber of Tax Consultants

The Chamber of Tax Consultants 3 rd Domestic Transfer Pricing Conference Tax incentives and domestic transfer pricing Sanjay Kapadia Assisted by Nisha Shah 19 October 2013 Meaning of Specified Domestic

The Chamber of Tax Consultants 3 rd Domestic Transfer Pricing Conference Tax incentives and domestic transfer pricing Sanjay Kapadia Assisted by Nisha Shah 19 October 2013 Meaning of Specified Domestic

An overview of Transfer Pricing

An overview of Transfer Pricing Vispi T. Patel Vispi T. Patel & Associates March 14, 2015 1 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations

An overview of Transfer Pricing Vispi T. Patel Vispi T. Patel & Associates March 14, 2015 1 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations

Tax Audit Few Problem Areas and Impact of Recent Amendments

1867 Tax Audit Few Problem Areas and Impact of Recent Amendments Tax audit season is round the corner now. So, it is important to clear few problem areas faced by tax auditors and the impact of recent

1867 Tax Audit Few Problem Areas and Impact of Recent Amendments Tax audit season is round the corner now. So, it is important to clear few problem areas faced by tax auditors and the impact of recent

Transfer Pricing Law

Transfer Pricing Law 1 Presentation Compiled By Akshay Kenkre Gaurav Garg Tejas Dharwadkar What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services,

Transfer Pricing Law 1 Presentation Compiled By Akshay Kenkre Gaurav Garg Tejas Dharwadkar What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services,

Corporate Taxes - An Overview. 5 th MSOP :ICSI-Hyderabad Chapter. Ankem Sri Prasad Chief Tax Officer - Deloitte U.S. India Offices

Corporate Taxes - An Overview 5 th MSOP :ICSI-Hyderabad Chapter Ankem Sri Prasad Chief Tax Officer - Deloitte U.S. India Offices March 26, 2012 The best things in life are free, but soon, the government

Corporate Taxes - An Overview 5 th MSOP :ICSI-Hyderabad Chapter Ankem Sri Prasad Chief Tax Officer - Deloitte U.S. India Offices March 26, 2012 The best things in life are free, but soon, the government

ACCOUNTING & TAXATION ISSUES RELATING TO CAPITAL MARKET TRANSACTIONS CAPITAL MARKET TRANSACTIONS

ACCOUNTING & TAXATION ISSUES RELATING TO CAPITAL MARKET TRANSACTIONS CAPITAL MARKET TRANSACTIONS CASH MARKET DERIVATIVE MARKET DELIVERY DAILY JOBBING FUTURE OPTIONS BASED (NO DELIVERY) INDEX STOCKS INDEX

ACCOUNTING & TAXATION ISSUES RELATING TO CAPITAL MARKET TRANSACTIONS CAPITAL MARKET TRANSACTIONS CASH MARKET DERIVATIVE MARKET DELIVERY DAILY JOBBING FUTURE OPTIONS BASED (NO DELIVERY) INDEX STOCKS INDEX

Transfer Pricing Country Summary Russia

Page 1 of 6 Transfer Pricing Country Summary Russia 16 November 2015 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines The TP rules are fixed in the Russian Tax Code (Part 1). Furthermore,

Page 1 of 6 Transfer Pricing Country Summary Russia 16 November 2015 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines The TP rules are fixed in the Russian Tax Code (Part 1). Furthermore,

Transfer Pricing Country Summary Pakistan

Page 1 of 7 Transfer Pricing Country Summary Pakistan July 2018 Page 2 of 7 Legislation Existence of Transfer Pricing Laws/Guidelines There is a general anti-avoidance rule in the Pakistani tax law that

Page 1 of 7 Transfer Pricing Country Summary Pakistan July 2018 Page 2 of 7 Legislation Existence of Transfer Pricing Laws/Guidelines There is a general anti-avoidance rule in the Pakistani tax law that

Transfer Pricing Country Summary India

Page 1 of 13 Transfer Pricing Country Summary India April 2018 Page 2 of 13 Legislation Existence of Transfer Pricing Laws/Guidelines Section 92 of the Income-tax Act, 1961 requires international transactions

Page 1 of 13 Transfer Pricing Country Summary India April 2018 Page 2 of 13 Legislation Existence of Transfer Pricing Laws/Guidelines Section 92 of the Income-tax Act, 1961 requires international transactions

TRANSFER PRICING UNDER INCOME TAX ACT, N.Madhan B.Com., CA & Grad CWA. 22 August 2015

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

TRANSFER PRICING. By Yethi Remella

TRANSFER PRICING By Yethi Remella 1. INTRODUCTION 2. INCOME TAX ACT, SECTION 92 3. FORM 3CEB Introduction What is Transfer Pricing? What is the Importance of TP in Income Tax? Transfer Pricing - Term Costing

TRANSFER PRICING By Yethi Remella 1. INTRODUCTION 2. INCOME TAX ACT, SECTION 92 3. FORM 3CEB Introduction What is Transfer Pricing? What is the Importance of TP in Income Tax? Transfer Pricing - Term Costing

[2012] 18 taxmann.com 256 (Article)

![[2012] 18 taxmann.com 256 (Article)](/thumbs/75/72354143.jpg "[2012] 18 taxmann.com 256 (Article)") [2012] 18 taxmann.com 256 (Article) Convergence between Transfer Pricing and Customs Valuation in the Indian context Introduction KARTHIK SUNDARAM Advocate - Madras High Court 1 1. Transactions globally

[2012] 18 taxmann.com 256 (Article) Convergence between Transfer Pricing and Customs Valuation in the Indian context Introduction KARTHIK SUNDARAM Advocate - Madras High Court 1 1. Transactions globally

Landmark Decisions on Transfer Pricing

Landmark Decisions on Transfer Pricing CITC Amol Tibrewal Vispi T. Patel & Associates 11 April 2014 Global Vantedge - Delhi Tribunal (ITA No 2763 & 2764/DEL/2009) Facts of the case Assessee provided IteS

Landmark Decisions on Transfer Pricing CITC Amol Tibrewal Vispi T. Patel & Associates 11 April 2014 Global Vantedge - Delhi Tribunal (ITA No 2763 & 2764/DEL/2009) Facts of the case Assessee provided IteS

Voices on Reporting. Quarterly updates. October Contents. Updates relating to Ind AS. Updates relating to the Companies Act, 2013

Voices on Reporting Quarterly updates October 2017 Contents Updates relating to Ind AS Updates relating to the Companies Act, 2013 Updates relating to SEBI regulations Other regulatory updates 01 18 25

Voices on Reporting Quarterly updates October 2017 Contents Updates relating to Ind AS Updates relating to the Companies Act, 2013 Updates relating to SEBI regulations Other regulatory updates 01 18 25

Transfer Pricing - Filing of Form 3CEB & Practical Issues November 11, CA Vikram R. B.Com., FCA.

12 November 2014 Transfer Pricing - Filing of Form 3CEB & Practical Issues November 11, 2017 CA Vikram R. B.Com., FCA. 98841 91001 vikram@vcmv.in Transfer Pricing Introduction in India Finance Minister

12 November 2014 Transfer Pricing - Filing of Form 3CEB & Practical Issues November 11, 2017 CA Vikram R. B.Com., FCA. 98841 91001 vikram@vcmv.in Transfer Pricing Introduction in India Finance Minister

DCB BANK LIMITED Policy on Related Party Transactions Version 4.0

DCB BANK LIMITED Policy on Related Party Transactions Version 4.0 1 Glossary of Abbreviations used in this Document ACB AS ESOP ICAI KMP LODR NRCB RBI RPTs SEBI Audit Committee of the Board Accounting

DCB BANK LIMITED Policy on Related Party Transactions Version 4.0 1 Glossary of Abbreviations used in this Document ACB AS ESOP ICAI KMP LODR NRCB RBI RPTs SEBI Audit Committee of the Board Accounting

Issues Involving Comparability and Profit Based Methods in Transfer Pricing

G L O B A L T R A N S F E R P R I C I N G S E R V I C E S Issues Involving Comparability and Profit Based Methods in Transfer Pricing International Taxation Conference 2008 December 5, 2008 T A X Uday

G L O B A L T R A N S F E R P R I C I N G S E R V I C E S Issues Involving Comparability and Profit Based Methods in Transfer Pricing International Taxation Conference 2008 December 5, 2008 T A X Uday

RBI defers the effective date for implementation of Ind AS for banks to 1 April 2019

29 Regulatory updates 30 RBI defers the effective date for implementation of Ind AS for banks to 1 April 2019 On 5 April 2018, the Reserve Bank of India (RBI) through its press release deferred the implementation

29 Regulatory updates 30 RBI defers the effective date for implementation of Ind AS for banks to 1 April 2019 On 5 April 2018, the Reserve Bank of India (RBI) through its press release deferred the implementation

CS Professional Programme Solution June Paper - 6 Module-III Advanced Tax Laws and Practice Part-A

CS Professional Programme Solution June - 2013 Paper - 6 Module-III Advanced Tax Laws and Practice Part-A Answer: 2013 - June [1] (a) (i) Ch-14 The statement is True. As per Section 115 BBD, dividend from

CS Professional Programme Solution June - 2013 Paper - 6 Module-III Advanced Tax Laws and Practice Part-A Answer: 2013 - June [1] (a) (i) Ch-14 The statement is True. As per Section 115 BBD, dividend from

Methods of determining ALP

Methods of determining ALP -Eric Mehta 1 August 2011 Concept of Transfer Pricing 1 August 2011 Page 2 Transfer Pricing Concept of transfer pricing A price between unrelated parties is known as the arm

Methods of determining ALP -Eric Mehta 1 August 2011 Concept of Transfer Pricing 1 August 2011 Page 2 Transfer Pricing Concept of transfer pricing A price between unrelated parties is known as the arm

GOODS & SERVICES TAX / IDT UPDATE 31

GOODS & SERVICES TAX / IDT UPDATE 31 E-way Bill Mechanism Following decisions were taken by the GST council in the 24 th GST Council meeting for implementation of nationwide e-way Bill system : i) The

GOODS & SERVICES TAX / IDT UPDATE 31 E-way Bill Mechanism Following decisions were taken by the GST council in the 24 th GST Council meeting for implementation of nationwide e-way Bill system : i) The

Overview of Transfer Pricing Regulations. CA Akshay Kenkre

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

SEMINAR ON TRANSFER PRICING 23rd September, Valuation Approaches and their applicability under Transfer Pricing. CA Siddharth Banwat

SEMINAR ON TRANSFER PRICING 23rd September, 2017 Valuation Approaches and their applicability under Transfer Pricing WHAT IS VALUATION? WHAT IS VALUE? A value in exchange is a hypothetical price and the

SEMINAR ON TRANSFER PRICING 23rd September, 2017 Valuation Approaches and their applicability under Transfer Pricing WHAT IS VALUATION? WHAT IS VALUE? A value in exchange is a hypothetical price and the

I. VARIOUS OPTIONS FOR CONVERGENCE WITH IFRSs IN INDIA

P I. VARIOUS OPTIONS FOR CONVERGENCE WITH IFRSs IN INDIA 1. Background 1.1 International Financial Reporting Standards (IFRSs), issued by the International Accounting Standards Board (IASB), which are

P I. VARIOUS OPTIONS FOR CONVERGENCE WITH IFRSs IN INDIA 1. Background 1.1 International Financial Reporting Standards (IFRSs), issued by the International Accounting Standards Board (IASB), which are

Special provisions relating to certain income of non residents, Introduction to transfer pricing, APA, Double taxation Relief. CA Kiran J.

Special provisions relating to certain income of non residents, Introduction to transfer pricing, APA, Double taxation Relief CA Kiran J. Nisar 1 Chapter XIIA : Special Provision relating to certain income

Special provisions relating to certain income of non residents, Introduction to transfer pricing, APA, Double taxation Relief CA Kiran J. Nisar 1 Chapter XIIA : Special Provision relating to certain income

Changes in Financial Statements and Auditor s Report. Presentation By CA Anil Sharma

Changes in Financial Statements and Auditor s Report Presentation By CA Anil Sharma Sec 129- Financial Statement The financial statement shall : be in the form in Schedule III and comply with the accounting

Changes in Financial Statements and Auditor s Report Presentation By CA Anil Sharma Sec 129- Financial Statement The financial statement shall : be in the form in Schedule III and comply with the accounting

AMENDMENTS IN SEBI LISTING AND DISCLOSURE REQUIREMENTS REGULATIONS (CA P.N. SHAH AND CS AMRUTA AVASARE)

") AMENDMENTS IN SEBI LISTING AND DISCLOSURE REQUIREMENTS REGULATIONS (CA P.N. SHAH AND CS AMRUTA AVASARE) Securities And Exchange Board of India (SEBI) had appointed a Committee under the Chairmanship of

AMENDMENTS IN SEBI LISTING AND DISCLOSURE REQUIREMENTS REGULATIONS (CA P.N. SHAH AND CS AMRUTA AVASARE) Securities And Exchange Board of India (SEBI) had appointed a Committee under the Chairmanship of

MANUBHAI & SHAH LLP Maker Bhavan # 2, CHARTERED ACCOUNTANTS

MANUBHAI & SHAH LLP Maker Bhavan # 2, CHARTERED ACCOUNTANTS 18, New Marine Lines, Mumbai 400020. Tel. 66333558/59/60 Fax: 66333561 www.msglobal.co.in E-mail: infomumbai@msglobal.co.in AMENDMENTS IN SEBI

MANUBHAI & SHAH LLP Maker Bhavan # 2, CHARTERED ACCOUNTANTS 18, New Marine Lines, Mumbai 400020. Tel. 66333558/59/60 Fax: 66333561 www.msglobal.co.in E-mail: infomumbai@msglobal.co.in AMENDMENTS IN SEBI

Case Study on Splitting up/ reconstruction of business of old unit

Case Studies Case Study on Splitting up/ reconstruction of business of old unit Case Study 1: XYZ India Ltd, is engaged in the business of developing softwares. The company already has an established software

Case Studies Case Study on Splitting up/ reconstruction of business of old unit Case Study 1: XYZ India Ltd, is engaged in the business of developing softwares. The company already has an established software

Answer to MTP_Intermediate_Syllabus 2012_Dec2017_Set 2 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria

![Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria](/thumbs/90/101594279.jpg "Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria") Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

GUIDE TO TRANSFER PRICING BACKGROUNDER. (i)

") GUIDE TO TRANSFER PRICING BACKGROUNDER (i) First Edition : November 2016 Price : Rs. 120/-- (Excluding postage) THE INSTITUTE OF COMPANY SECRETARIES OF INDIA All rights reserved. No part of this book may

GUIDE TO TRANSFER PRICING BACKGROUNDER (i) First Edition : November 2016 Price : Rs. 120/-- (Excluding postage) THE INSTITUTE OF COMPANY SECRETARIES OF INDIA All rights reserved. No part of this book may

Voices on Reporting. 4 October KPMG.com/in

Voices on Reporting 4 October 2017 KPMG.com/in 2017 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

Voices on Reporting 4 October 2017 KPMG.com/in 2017 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 11

Clarification Bulletin 11") Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 11 Ind AS Transition Facilitation Group (ITFG) of Ind AS Implementation Committee has been constituted for providing clarifications on

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 11 Ind AS Transition Facilitation Group (ITFG) of Ind AS Implementation Committee has been constituted for providing clarifications on

33 rd Regional Conference of WIRC of ICAI. Interplay Reporting on Audit under Companies Act & Income Tax Act. CA Kamlesh Vikamsey

33 rd Regional Conference of WIRC of ICAI Interplay Reporting on Audit under Companies Act & Income Tax Act 25.08.2018 Evolution of Accounting Standards vis-à-vis Companies Act 1857 First Companies Act

33 rd Regional Conference of WIRC of ICAI Interplay Reporting on Audit under Companies Act & Income Tax Act 25.08.2018 Evolution of Accounting Standards vis-à-vis Companies Act 1857 First Companies Act

TRAINING ON TRANSFER PRICING. Income Tax Workshop DATE: 12th 13th April 2018 VENUE: Grand Regency Hotel Nairobi

TRAINING ON TRANSFER PRICING Income Tax Workshop DATE: 12th 13th April 2018 VENUE: Grand Regency Hotel Nairobi 1 www.kra.go.ke 18/04/2018 INTRODUCTION TO TRANSFER PRICING What is Transfer Pricing? Prices

TRAINING ON TRANSFER PRICING Income Tax Workshop DATE: 12th 13th April 2018 VENUE: Grand Regency Hotel Nairobi 1 www.kra.go.ke 18/04/2018 INTRODUCTION TO TRANSFER PRICING What is Transfer Pricing? Prices

Transfer Pricing compliances, Litigation update and Dispute resolution. - CA Mithilesh

Transfer Pricing compliances, Litigation update and Dispute resolution - CA Mithilesh 09553111131 Overview Concept and Rationale of TP Applicability International Transaction Meaning of Associated Enterprise

Transfer Pricing compliances, Litigation update and Dispute resolution - CA Mithilesh 09553111131 Overview Concept and Rationale of TP Applicability International Transaction Meaning of Associated Enterprise

Amounts not deductible.

Amounts not deductible. 40. Notwithstanding anything to the contrary in sections 30 to 38 the following amounts shall not be deducted in computing the income chargeable under the head Profits and gains

Amounts not deductible. 40. Notwithstanding anything to the contrary in sections 30 to 38 the following amounts shall not be deducted in computing the income chargeable under the head Profits and gains

The Managing Director/ Executive Director/ Administrator of all the Stock Exchanges

Neelam Bhardwaj General Manager Corporation Finance Department Division of Issues and Listing Phone: +91 2644 9350 Email: neelamb@sebi.gov.in SEBI/CFD/DIL/LA/1/2009/24/04 April 24, 2009 The Managing Director/

Neelam Bhardwaj General Manager Corporation Finance Department Division of Issues and Listing Phone: +91 2644 9350 Email: neelamb@sebi.gov.in SEBI/CFD/DIL/LA/1/2009/24/04 April 24, 2009 The Managing Director/