2015 Gear Up 1040 Individual Tax

|

|

|

- Lucy Freeman

- 5 years ago

- Views:

Transcription

1 2015 Gear Up 1040 Individual Tax Melanie Mogg CPA MelanieMogg Copyright 2009 Thomson Reuters/Gear Up. All rights reserved.

2 Today s Topics Net investment income tax (NIIT) Investment income Passive & rental activities Sale of principal residence Foreclosures and COD AMT Personal tax credits

3 Chapter 10: Net Investment Income Tax Page 141 After two tax seasons of dealing with this we might actually understand better. 3

4 2013 Statistics of Income 6.3 billion tax for.9% Medicare 2.8 million returns 16.5 billion tax for NIIT 3 million returns Averages: $2,250 for 9% Medicare $5,500 for 3.8% NIIT

5 Sample Did you know that if you sell your house after 2012 you will pay a 3.8% sales tax on it? That's $3,800 on a $100,000 home etc. When did this happen? It's in the healthcare bill. REAL ESTATE SALES TAX TO GO INTO EFFECT 2013 (Part of HC Bill)

6 Worksheet page 141

7 3.8% NIIT Rate Applies to taxpayers with higher MAGI: Joint $250,000 Thresholds NOT indexed for inflation Head of Household $225,000 Single $200,000

8 Example 1 Page The Adams are married with MAGI of $275,000 and net investment income of $50,000. The tax is imposed on the lesser of: a.) Net investment income ($50,000) or b.) MAGI over $250,000 ($275,000-$250,000 = $25,000) The tax is $25,000 x 3.8% = $950

9 Example 2: 14 The Adams are married with MAGI of $375,000 and net investment income of $50,000. The tax is imposed on the lesser of: a.) Net investment income ($50,000) or b.) MAGI over $250,000 ($375,000-$250,000 = $125,000) The tax is $50,000 x 3.8% = $1,900

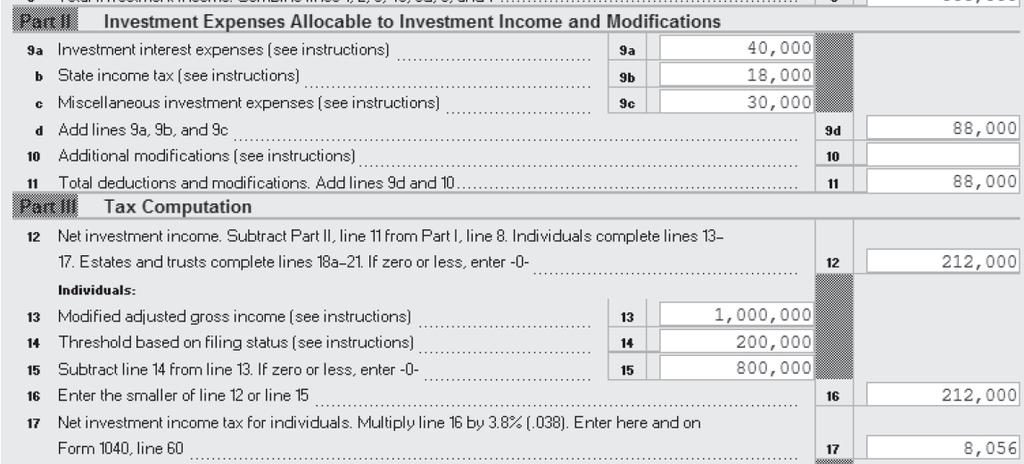

10 Example 3: 14 The Adams are married with MAGI of $1,000,000 and net investment income of $50,000. The tax is imposed on the lesser of: a.) Net investment income ($50,000) or b.) MAGI over $250,000 ($1,000,000-$250,000 = $750,000) The tax is $50,000 x 3.8% = $1,900

11 3 Buckets Analogy Bonus Wages SE Income Interest, Dividends, Rental, Passive T&B Commodities & FI SS, Retirement, UC, alimony, & non-passive T&B income or Gains & RE Professional Payroll NIIT Exempt filename 11

12 Example 2015: 14 Page 146 Bud has the following: Capital gain 10,000 Capital loss (40,000) Net loss (30,000) The net loss is limited to 3,000 for both regular and NII purposes. If Bud has $5,000 of dividend income his investment income before deductions would be $2,000.

13 Example 2016: 14 Page 146 Bud has the following in the following year: Capital gain 30,000 Capital loss c/o (27,000) Net gain 3,000 If Bud has $6,000 of dividend income his investment income before deductions would be $9,000.

14 Example: Page Heine has the following: 1231 gain 21,000 Capital loss (15,000) Net gain 6,000 Annuity income is presumed to be nonqualifying and subject to NIIT. For NIIT purposes, he is allowed to use the full 15,000 capital loss to offset the annuity.

15 Errata pages

16 S Corporation Materially participates No 3.8% on OI line 1 No 0.9% on OI Salary subject to 0.9% S Corporation Does not materially participate Subject to 3.8% on line 1 OI No 0.9% (assume no salary) Partnership/ LLC Materially participates No 3.8% on OI line 1 Subject to 0.9% on line 14 SE income Partnership/ LLC Does not materially participate Subject to 3.8% on line 1 OI No 0.9% on OI C Corporation Materially participates or not. Dividends subject to 3.8% Salary subject to 0.9%

17 Comprehensive example: 146 Page 149

18 Comprehensive example: 150 4

19 Comprehensive example: 150

20 ACA Concerns Additional Medicare Tax (earned income) AGI and MAGI have NO effect Retirement contributions have no effect S Corp has advantages here as long as reasonable wages paid.

21 ACA Concerns Net Investment Income Tax (NIIT) AGI or MAGI DO impact the assessment of this tax Retirement savings reduce AGI, reducing exposure Tax efficient investing to reduce gain recognition Muni s offer triple tax-free Roth conversions while in modest bracket reduce future exposure Like-kind exchanges, installment sales can defer NIIT

22 Chapter 11: Interest & Dividends Page 155 New investment vehicles and reporting are creating a headache for us preparers.

23 Dividend Rates 2015 Taxpayers in 15% or below: 0% Most taxpayers below threshold: same at 15% Some taxpayers with higher income: 20% - see thresholds. Joint $464,850 Head of Household $439,000 Single $413,200

24 Chapter 12: Capital Gains Page 169 Understanding how the dividend/capital gains rate is affected by deductions. 24

25 Capital Gain Rates 2015 Taxpayers in 15% or below: 0% Most taxpayers below threshold: same at 15% Some taxpayers with higher income: 20% - see thresholds. Joint $464,850 Head of Household $439,000 Single $413,200

26 High NW tax calculation 2011: Line 43 (Taxable Income) $9,007,705 Line 9b (Dividends) 2,221,956 Capital Gains 6,810,176 Qualifying D & CG $9,032,132 Taxed at zero (69,000) Taxed at 15% 8,938,705 Tax $1,340,806

27 2013 tax calculation: Line 43 (Taxable Income) $9,007,705 All QD & CG 72,500 taxed at zero 0 177,500 taxed at 15% 56, ,000 taxed at 18.8% 37,600 8,557,705 taxed at 23.8% 2,036,734 Total tax: $2,130,959

28 Increase? 2013 tax 2,130, tax 1,340,806 Increase 790, ,153 = 58.93% 1,340,806

29 Double Benefit Taxable Ord. LTCG Income Rates Rates $74,900 25% 15% 15% 0% $18,450 10% 0% 2015 Rates - MFJ

30 Double Benefit Taxable Ord. LTCG After Income Rates Rates Before $10,000 IRA $74,900 25% 15% $40,000 LTCG 15% 0% $40,000 LTCG 15% 0% 15% 0% $50,000 Ord. 15% $40,000 Ord. 15% $18,450 10% 0% 10% 10%

31 Double Benefit on lowest marginal rate: Before After C.G. 15% - 0% 15% O.I. 15% Total 30% $40,000 LTCG $50,000 Ord. 20% 15% 15% $40,000 LTCG $40,000 Ord. 15% 0% 15% 10% 10%

32 Double Benefit at highest marginal rate: C.G. 20% 15% 5% O.I. 39.6% Total 44.6%

33 2015 Projection Client is 60, a retired physician 2 million in taxable investments 1.2 million in retirement accounts Projected 2015 income: 8k interest 13k Q dividends 17k Capital gains

34 2015 Projection AGI $33,000 ID (10,000) EX ( 4,000) TI $19,000 Tax $0 How much to convert to ROTH?

35 2015 Schedule D: 171

36 Chapter 13: Passive and Rental Activities - Page 185 Passive takes on a new role with the addition of the 3.8% Medicare tax on passive trades or businesses.

37 The Tax Reform Act of 1986:

38 187

39 TC Memo page decision on a family matter. Carryback claim was over 5 million on losses generated in 2008 and carried back to Loads of family drama and accusations caused one member of the families testimony to be not credible. Ruled non-passive.

40 TC Memo Submitted 1,936 hours to employer. Submitted generic calendar in 2009 for 2008 rental activities and claimed he only worked 32 hours for his employer. We need not accept petitioner s testimony and may and do reject it because of the many indicia of unreliability.

41 TC Memo Had previously been audited on the issue of passive losses and RE professional. Submitted calendar showing hours without travel time. Travel to 12 rentals was approximately minutes. IRS refused revised log with travel time.

42 197 RE Professional & NIIT If RE professional (750 hours & 50%) AND meet safe harbor of 500+ hours in rental activities, not subject to NIIT Note: May need grouping to meet. Non-rental activity does not count.

43 NIIT Simplified Method 202 Can only use if 1. Sum of all NIIT items are < 5% of all separately stated items and total gain/ loss < 5 million or 2. Gain is less than 250,000

44 How much of the gain is 203 NII? investment income = NUMERATOR Sec items DENOMINATOR All items Regular tax gain (loss) 44

45 Page 193

46 Chapter 14: Installment Sales - Page 211 Harder than ever to make the decision to elect out when a capital gain is involved.

47 20% 91%

48 Chapter 15: Debt Forgiveness & Foreclosures - Page 219 In retrospect, I should have seen this coming. How could someone making $60,000 afford a $380,000 mortgage?

49 Loan Proceeds Theory A = L + OE (20) (20)

50 Loan Proceeds Theory A = L + OE (20) + 20

51 Form 1099-A indicates a sale: 220

52 Potential ordinary income: 220

53 Must file Form 982: 221

54 Recourse Debt 222 Purchase Cost Down Pay Mortgage $300,000 $30,000 $270,000 Surrender FMV Mortgage Balance 230,000 $260,000 Debt Discharge Debt Forgiveness Income $30,000

55 Recourse Debt 222 Purchase Cost Down Pay Mortgage $300,000 $30,000 $270,000 Surrender FMV Mortgage Balance $230,000 $260,000 Debt Discharge Deemed Sale Net Gain (Loss) Debt Forgiveness Income ($70,000) ($55,000) $30,000 Deemed Sale Loss Equals 70,000

56 Recourse Debt 222 Purchase Cost Down Pay Mortgage $300,000 $30,000 $270,000 Surrender FMV Mortgage Balance $130,000 $260,000 Debt Discharge Deemed Sale Net Gain (Loss) Debt Forgiveness Income ($170,000) ($55,000) $130,000 Deemed Sale Loss Equals 170,000

57 Nonrecourse Debt 222 Purchase Cost Down Pay Mortgage $300,000 $30,000 $270,000 Surrender FMV Mortgage Balance $230,000 $260,000 Debt Discharge Deemed Sale Net Gain (Loss) ($40,000) Debt Forgivenes s Income $0

58 Separating the tax impact: Loan Type Recourse Nonrecourse Selling price = FMV Debt forgiveness = Note - FMV Selling price = Note balance

59 223 Form 982 excluded discharges:

60 Qualified Real Property A = L + OE (20) (20)

61 Special Rules for Principal Residence 230 Qualified Principal Residence Debt excludable from income: 1. Applies to discharges for calendar years In the event the taxpayer restructures their acquisition debt or lose the residence through foreclosure or short sale

62 Chapter 16: Sale of a Principal Residence - Page 233 Now more than ever it is crucial to determine a principal residence in contrast to a residence.

63 NIIT & Residences Excludable gain is not included in NII Taxable gain is included in NII Second home gain is included in NII

64 235 Guinan Year Wisconsin Georgia Arizona 9/97-9/ /96-9/ /95-9/ /94-9/ /93-9/

65 Where Do I Live? If a taxpayer alternates between 2 properties, the property that the taxpayer uses a majority of the time during the year ordinarily will be considered the taxpayer's principal residence.

66 235 Guinan Year Wisconsin Georgia Arizona 9/97-9/ /96-9/ /95-9/ /94-9/ /93-9/

67 Where Did Guinan Live? Banking both Mail both Cars both Children neither state No Wisconsin Income Tax Return Driver s licenses Georgia & Arizona Lecturer at Georgia colleges

68 Example: Scott 237 Tax Basis = $280,000 Land at Conversion = 60,000 Bldg at Conversion = $200,000 $60,000 Suspended Basis = $ 20,000 $20,000 $200,000

69 Sold for a loss: Conversion value Original Cost $280,000 Conversion Value $260,000 Depreciation Taken Adjusted Basis for Gain Adjusted Basis for Loss Sale Price Realized Gain / (Loss) $16,000 $264,000 $244,000 $210,000 -$34,000 If the property is sold for a loss the basis for sale is the conversion value plus post capital expenditures

70 Sold for a gain: Original cost Original Cost $280,000 Conversion Value $260,000 Depreciation Taken $16,000 Adjusted Basis for Gain Adjusted Basis for Loss Sale Price Realized Gain / (Loss) $264,000 $244,000 $270,000 $6,000

71 Sold for in-between: Original Cost $280,000 Conversion Value $260,000 Depreciation Taken $16,000 Adjusted Basis for Gain $264,000 Adjusted Basis for Loss $244,000 Sale Price $260,000 Realized Gain / (Loss) $0 In event the gain basis produces a loss and the loss basis produces a gain ZERO gain or loss is realized.

72 Page 241 Partial Home Exclusion Change in place of employment Health reasons Unforeseen circumstances

73 Non-qualified Use

74 243 Non-qualified Use aggregate period of nonqualifying use total period of ownership

75 Conversion requires allocation: Page 243 Jeb! purchased a vacation home in January It was not rented nor used as a principal residence until he moved into the home in January January 2015 he sells the residence realizing a $120,000 gain.

76 Conversion to residence old law 2 of last 5 years used as residence? Yes Qualified for full exclusion.

77 4 years non-qualified use 243 aggregate period of nonqualifying use = 4 total period of ownership = OR 40%

78 3 years non-qualified use 243 aggregate period of nonqualifying use = 3 total period of ownership = OR 33.33%

79 2 years non-qualified use 243 aggregate period of nonqualifying use = 2 total period of ownership = OR 25%

80 1 year non-qualified use 243 aggregate period of nonqualifying use = 1 total period of ownership = OR 14.3%

81 Page 247 Comparison HECM 1. Collateral 2. No payments 3. Unlimited until I of 4 events HELOC or Loan 1. Income & credit 2. Fixed Payments req d 3. Limited term

82 The trouble with quotes on the internet is that it s difficult to determine whether or not they are genuine. - Abraham Lincoln 82

83 Personal Credits - Page 251 Expect increased scrutiny on EITC. TIGTA report August 2013 reported 21 25% error rate.

84 History of EITC Signed by Ford as part of the Tax Reduction Act of 1975 Temporary to offset SS tax and rising food and energy prices Made permanent in Expanded by Reagan as part of The Tax Reform Act of 1986

85 History of EITC The EITC was further expanded in 1990, 1993 and The American Recovery and Reinvestment Act (2009) expanded the EITC temporarily for 2 groups. Married couples and families with 3+ children. These enhancements were set to expire in 2013 but were extended through 2017 by the American Tax Relief Act of 2012.

86 86

87 2014 Earned Income Tax Credit Parameters (Source: IRS) Filing Status No Children One Child Two Children Three or More Children Single or Head of Household Earned Income Level for Max Credit $6,480 $9,720 $13,650 $13,650 Maximum Credit $496 $3,305 $5,460 $6,143 Earned Income Level When Phase out Begins Earned Income Level When Phase-out Ends (Credit Equals Zero) $8,110 $17,830 $17,830 $17,830 $14,590 $38,511 $43,756 $46,997 Married Filing Jointly Earned Income Level for Max Credit $6,480 $9,720 $13,650 $13,650 Maximum Credit $496 $3,305 $5,460 $6,143 Earned Income Level When Phase-out Begins Earned Income Level When Phase out Ends (Credit Equals Zero) $13,540 $23,260 $23,260 $23,260 $20,020 $43,941 $49,186 $52,427 Add l Marg. Rate 7.65% 16% 21% 21% 87

88 Chapter 18: Alternative Minimum Tax - Page 263 What causes AMT? Surprisingly it is mostly a function of lowered regular tax rates, increased exemptions and personal credits.

89 AMT Exemptions Statutory S/HoH $33,750 MFJ $45,000 MFS $22, Perm S/HoH $50,600 MFJ $78,750 MFS $39,375 AMT Exemptions will now be indexed for inflation!!!! 89

90 AMT Exemptions Page 264

91 Marginal rate during phase-out: Marginal rate during exemption phase out is 35% * 28% = 35%

92 Buddy s Law: Handle every stressful situation like a dog If you can't eat it or play with it, Just pee on it and walk away

93

Year-End Tax Planning Summary December 2015

Year-End Tax Planning Summary December 2015 Overview Thanks to the continued political gridlock in Washington, 2015 did not see comprehensive tax reform. However, on December 18th, Congress passed the

Year-End Tax Planning Summary December 2015 Overview Thanks to the continued political gridlock in Washington, 2015 did not see comprehensive tax reform. However, on December 18th, Congress passed the

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 Year-End Income Tax Planning for Individuals December 2017

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

2013 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS

INTRODUCTION 2013 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS As the end of 2013 approaches, it s time to consider planning moves that could reduce your 2013 taxes. Year-end planning is particularly important

INTRODUCTION 2013 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS As the end of 2013 approaches, it s time to consider planning moves that could reduce your 2013 taxes. Year-end planning is particularly important

Partner Self- Employment Income

2-29 Partner Self- Employment Income FICA on wages is all on labor SECA is on labor and capital 1 Partner SE Income General Rule: Distributive share of income and guaranteed payments to partners are SE

2-29 Partner Self- Employment Income FICA on wages is all on labor SECA is on labor and capital 1 Partner SE Income General Rule: Distributive share of income and guaranteed payments to partners are SE

Individual Tax Planning 2015 & Beyond

Individual Tax Planning 2015 & Beyond Tax Bracket Comparison 2015 & 2012 2015 MARRIED FILING JOINT 2012 MARRIED FILING JOINT 10% - up to $18,450 10% - up to $17,400 15% - $18,451 - $74,900 15% - $17,401

Individual Tax Planning 2015 & Beyond Tax Bracket Comparison 2015 & 2012 2015 MARRIED FILING JOINT 2012 MARRIED FILING JOINT 10% - up to $18,450 10% - up to $17,400 15% - $18,451 - $74,900 15% - $17,401

KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017

OF 2017") KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017 New tax laws resulting from the TCJA represent the most significant changes in our tax structure in more than 30 years. Most provisions for individuals

KEY PROVISIONS OF THE TAX CUTS AND JOBS ACT (TCJA) OF 2017 New tax laws resulting from the TCJA represent the most significant changes in our tax structure in more than 30 years. Most provisions for individuals

Year End Tax Planning for Individuals

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

WSRP, LLC Salt Lake City UT, Lehi UT & Las Vegas NV

Background on WSRP The firm began in 1985 with 6 people. Now the firm has over 100 + professionals and one of the largest CPA firms in Utah. Offices in SLC, Lehi, Las Vegas, and Ogden shortly. We primarily

Background on WSRP The firm began in 1985 with 6 people. Now the firm has over 100 + professionals and one of the largest CPA firms in Utah. Offices in SLC, Lehi, Las Vegas, and Ogden shortly. We primarily

Time Investment Gains and Losses

To Our Clients and Friends: The federal income tax rates for 2015 are the same as last year: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. However, the rate bracket beginning and ending points are increased

To Our Clients and Friends: The federal income tax rates for 2015 are the same as last year: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. However, the rate bracket beginning and ending points are increased

SDK s Annual Tax Update

Welcome SDK s Annual Tax Update Welcome from your host Dennis Bidwell dbidwell@sdkcpa.com Agenda Tax Rate Changes (Jennifer Stavish) New 3.8% Medicare Tax (Ryan Churness) Repair Regulations (Laurie Waterman)

Welcome SDK s Annual Tax Update Welcome from your host Dennis Bidwell dbidwell@sdkcpa.com Agenda Tax Rate Changes (Jennifer Stavish) New 3.8% Medicare Tax (Ryan Churness) Repair Regulations (Laurie Waterman)

Chapter 16: Sale of Residence. 16: Sale of Residence

Page 255-272 Chapter 1 Learning Objectives Page 255-272 Upon completion of this seminar, participants should be able to Determine if the exclusion or the reduced exclusion applies. Apply rules for nonqualified

Page 255-272 Chapter 1 Learning Objectives Page 255-272 Upon completion of this seminar, participants should be able to Determine if the exclusion or the reduced exclusion applies. Apply rules for nonqualified

What s New That Affects You? A Snapshot of Tax Law for Your Return

What s New That Affects You? A Snapshot of Tax Law for Your Return As is typical for an election year, no big tax changes that will affect 2016 tax returns came out of Washington. However, there has been

What s New That Affects You? A Snapshot of Tax Law for Your Return As is typical for an election year, no big tax changes that will affect 2016 tax returns came out of Washington. However, there has been

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's 1065 Deskbook. Twenty fifth Edition (October 2014)

") Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's 1065 Deskbook Twenty fifth Edition (October 2014) Highlights of this Edition The following are some of the important

Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's 1065 Deskbook Twenty fifth Edition (October 2014) Highlights of this Edition The following are some of the important

2017 Year-End Tax Reminders

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

Income Tax Planning for 2015 and Beyond

Income Tax Planning for 2015 and Beyond Presented by: Michael A. Fritton, CPA 3925 River Crossing Pkwy, Suite 300 Indianapolis, IN 46240 317.472.2200 / 800.469.7206 somersetcpas.com AGENDA Where we are

Income Tax Planning for 2015 and Beyond Presented by: Michael A. Fritton, CPA 3925 River Crossing Pkwy, Suite 300 Indianapolis, IN 46240 317.472.2200 / 800.469.7206 somersetcpas.com AGENDA Where we are

Tax Cuts and Jobs Act. Durham Chamber of Commerce Public Policy Meeting January 9, 2018

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Individual Taxation and Planning

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

TAX CUTS AND JOB ACT OF 2017 Highlights

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017 SUMMARY FOR 2017 NEW TAX LAW Publication Date: March 2017 Field of Studies: Level: Taxes Basic Cpe Hours: 3 Prerequisites: Advanced Preparation: None None Type

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017 SUMMARY FOR 2017 NEW TAX LAW Publication Date: March 2017 Field of Studies: Level: Taxes Basic Cpe Hours: 3 Prerequisites: Advanced Preparation: None None Type

WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014

Page 1 of 5 WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014 The IRS has electronically released final tax forms and instructions for the 2014 tax year, including Forms 1040, 1040-A, and 1040-EZ, along with some

Page 1 of 5 WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014 The IRS has electronically released final tax forms and instructions for the 2014 tax year, including Forms 1040, 1040-A, and 1040-EZ, along with some

Tax Cuts & Jobs Act Your Questions Answered

Tax Cuts & Jobs Act Your Questions Answered 1 Presented By 2 Our Panel of Experts Tom Judge CPA, MBA Founding Partner Rob Strachan Principal 3 Our Panel of Experts Matt Hochstetler Attorney Estate Planning,

Tax Cuts & Jobs Act Your Questions Answered 1 Presented By 2 Our Panel of Experts Tom Judge CPA, MBA Founding Partner Rob Strachan Principal 3 Our Panel of Experts Matt Hochstetler Attorney Estate Planning,

Tangible Property Regulations and Tax Update for the Oil and Gas Industry

and Tax Update for the Oil and Gas Industry Laura Roman, CPA, CMAP Partner, Tax and Strategic Business Services 0 Repair Regulations Affect almost all taxpayers Govern capitalizing and deducting expenditures

and Tax Update for the Oil and Gas Industry Laura Roman, CPA, CMAP Partner, Tax and Strategic Business Services 0 Repair Regulations Affect almost all taxpayers Govern capitalizing and deducting expenditures

2017 INDIVIDUAL TAX PLANNING

2017 INDIVIDUAL TAX PLANNING We hope that you are looking forward to the Holiday Season. It is hard to believe that it is mid-december and this year is quickly ending. If you ve been following the news

2017 INDIVIDUAL TAX PLANNING We hope that you are looking forward to the Holiday Season. It is hard to believe that it is mid-december and this year is quickly ending. If you ve been following the news

2016 Year-End Tax Planning Letter

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

Top Producer Seminar

Top Producer Seminar Are You Ready for A Wild Tax Ride? Paul Neiffer, CPA CliftonLarsonAllen, LLP January 30, 2014 CLAconnect.com Are You ready for a Wild Tax Ride? Topics The Deceptively High 2013 Tax

Top Producer Seminar Are You Ready for A Wild Tax Ride? Paul Neiffer, CPA CliftonLarsonAllen, LLP January 30, 2014 CLAconnect.com Are You ready for a Wild Tax Ride? Topics The Deceptively High 2013 Tax

American Taxpayer Relief Act of 2012 Workshop

American Taxpayer Relief Act of 2012 Workshop John Kilroy, CPA, CFP May 14, 2013 Agenda Estate, Gift and GST provisions Individual Income Tax provisions Trust and Estate Income Tax provisions Business

American Taxpayer Relief Act of 2012 Workshop John Kilroy, CPA, CFP May 14, 2013 Agenda Estate, Gift and GST provisions Individual Income Tax provisions Trust and Estate Income Tax provisions Business

Client Letter: Year-End Tax Planning for 2018 (Individuals)

") Client Letter: Year-End Tax Planning for 2018 (Individuals) Just as the daylight hours are getting shorter, so is the time for fine tuning any last-minute strategies to lower your 2018 tax bill. Unlike

Client Letter: Year-End Tax Planning for 2018 (Individuals) Just as the daylight hours are getting shorter, so is the time for fine tuning any last-minute strategies to lower your 2018 tax bill. Unlike

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

THE AGENDA YEAR END TAX PLANNING

YEAR END TAX PLANNING TUESDAY, DECEMBER 8, 2015 PRESENTED BY: JOE CAWLEY, CPA, PRINCIPAL-JOECAWLEY@BSSF.COM JOHN WEIDMAN, CPA, PRINCIPAL-JOHNWEIDMAN@BSSF.COM PHONE NUMBER-(717)761-7171 1 THE AGENDA Part

YEAR END TAX PLANNING TUESDAY, DECEMBER 8, 2015 PRESENTED BY: JOE CAWLEY, CPA, PRINCIPAL-JOECAWLEY@BSSF.COM JOHN WEIDMAN, CPA, PRINCIPAL-JOHNWEIDMAN@BSSF.COM PHONE NUMBER-(717)761-7171 1 THE AGENDA Part

Year-End Tax Planning Letter

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

KEIR EDUCATIONAL RESOURCES

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

Provisions of Tax Cuts and Jobs Act

Provisions of Tax Cuts and Jobs Act i Contents Introduction to the Course... 1 Course Learning Objectives... 1 Domain 1 Provisions of Tax Cuts and Jobs Act... 2 Introduction... 2 Domain 1 Learning Objectives...

Provisions of Tax Cuts and Jobs Act i Contents Introduction to the Course... 1 Course Learning Objectives... 1 Domain 1 Provisions of Tax Cuts and Jobs Act... 2 Introduction... 2 Domain 1 Learning Objectives...

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Tax strategies for higher-income taxpayers

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

American Taxpayer Relief Act Explained New Phone Number Summer Vacation

August 2013 American Taxpayer Relief Act Explained New Phone Number Summer Vacation We moved last week thank you to our old landlord Costco for 8 ½ great years! We are open for business; our new location

August 2013 American Taxpayer Relief Act Explained New Phone Number Summer Vacation We moved last week thank you to our old landlord Costco for 8 ½ great years! We are open for business; our new location

DRAFT AS OF August 7, 2013

Form 8960 Department of the Treasury Internal Revenue Service (99) Name(s) shown on Form 1040 or Form 1041 Net Investment Income Tax Individuals, Estates, and Trusts Attach to Form 1040 or Form 1041. Information

Form 8960 Department of the Treasury Internal Revenue Service (99) Name(s) shown on Form 1040 or Form 1041 Net Investment Income Tax Individuals, Estates, and Trusts Attach to Form 1040 or Form 1041. Information

You may wish to carefully examine your records to determine if you may be missing any of these deductions.

2018 tax planning and tax changes Re: Planning 2018: Tax Consequences for Self-Employed Individuals Dear Client: Owning your own business can be very rewarding, both personally and financially. Being the

2018 tax planning and tax changes Re: Planning 2018: Tax Consequences for Self-Employed Individuals Dear Client: Owning your own business can be very rewarding, both personally and financially. Being the

TOOLBOX CS PRODUCT PROFILE QUICK ACCESS TO KEY UTILITIES MEET CLIENT NEEDS WITH A WEALTH OF TOOLS FINANCIAL CALCULATORS CS PROFESSIONAL SUITE

PRODUCT PROFILE TOOLBOX CS CS PROFESSIONAL SUITE QUICK ACCESS TO KEY UTILITIES ToolBox CS, puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout

PRODUCT PROFILE TOOLBOX CS CS PROFESSIONAL SUITE QUICK ACCESS TO KEY UTILITIES ToolBox CS, puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout

2017 Year-End Tax Planning

2017 Year-End Tax Planning If you've been following the news out of Washington, you probably know that for the first time in decades, tax reform is a real possibility. Given that both the House and the

2017 Year-End Tax Planning If you've been following the news out of Washington, you probably know that for the first time in decades, tax reform is a real possibility. Given that both the House and the

2013 NEW DEVELOPMENTS LETTER

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

Tax Genius. limiting total contribution deductions to 50% of AGI was increased to 60%, allowing a slightly larger deduction in some cases.

Tax Genius 2018 Pocket Tax Guide Online Edition It has been a busy time for tax-related news and upcoming changes. We have compiled many of the tax changes, deductions and tax rates for easy reference

Tax Genius 2018 Pocket Tax Guide Online Edition It has been a busy time for tax-related news and upcoming changes. We have compiled many of the tax changes, deductions and tax rates for easy reference

Medicare taxes for higher-income taxpayers

Medicare taxes for higher-income taxpayers Facts and planning considerations to help manage your tax liability Begin planning now You ll especially want to discuss these tax provisions with your Financial

Medicare taxes for higher-income taxpayers Facts and planning considerations to help manage your tax liability Begin planning now You ll especially want to discuss these tax provisions with your Financial

IMPACT OF THE ELECTION President-Elect Trump proposes significant changes to the tax law including:

December 2016 To Our Clients and Friends: While many of you are making plans for year-end holidays, what should not be overlooked this time of year is year-end tax planning, especially considering the

December 2016 To Our Clients and Friends: While many of you are making plans for year-end holidays, what should not be overlooked this time of year is year-end tax planning, especially considering the

Personal Income Tax Update. AGA Winter Seminar 2013 Nathan Abbott, CISA, CFE, EA

Personal Income Tax Update AGA Winter Seminar 2013 Nathan Abbott, CISA, CFE, EA The Easy Stuff Inflation Adjustments Inflation Adjustments Inflation Adjustments Inflation Adjustments Social Security Maximum

Personal Income Tax Update AGA Winter Seminar 2013 Nathan Abbott, CISA, CFE, EA The Easy Stuff Inflation Adjustments Inflation Adjustments Inflation Adjustments Inflation Adjustments Social Security Maximum

Tax Cuts and Jobs Act of 2017

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

New Tax Rules for 2018 What You Need to Know to Reduce Your Tax Burden

New Tax Rules for 2018 What You Need to Know to Reduce Your Tax Burden 1 The Sarian Group Key Takeaways from the Tax Cuts and Jobs Act of 2017 The new tax laws represent the most significant changes in

New Tax Rules for 2018 What You Need to Know to Reduce Your Tax Burden 1 The Sarian Group Key Takeaways from the Tax Cuts and Jobs Act of 2017 The new tax laws represent the most significant changes in

Your Comprehensive Guide to 2013 Year-End Tax Planning

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Tax Planning Letter

2014-2015 Tax Planning Letter Dear Valued Client: Year-end tax planning is especially challenging this year because Congress has yet to act on a host of tax breaks that expired at the end of 2013. Some

2014-2015 Tax Planning Letter Dear Valued Client: Year-end tax planning is especially challenging this year because Congress has yet to act on a host of tax breaks that expired at the end of 2013. Some

THE OWNER OPERATOR S GUIDE TO. The Tax Cuts and Jobs Act of Prepared by

THE OWNER OPERATOR S GUIDE TO The Tax Cuts and Jobs Act of 2017 Prepared by Tip: Click on any of the chapters below to skip ahead to that section. TABLE OF CONTENTS Introduction...3 Pass Through Entities...3

THE OWNER OPERATOR S GUIDE TO The Tax Cuts and Jobs Act of 2017 Prepared by Tip: Click on any of the chapters below to skip ahead to that section. TABLE OF CONTENTS Introduction...3 Pass Through Entities...3

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA)

") Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

Checklist for Individuals Reducing the NIIT

Checklist for Individuals Reducing the NIIT 1. Reducing net investment income (NII) and MAGI General Observations a. Assuming that a taxpayer is subject to the net investment income tax (NIIT) in the first

Checklist for Individuals Reducing the NIIT 1. Reducing net investment income (NII) and MAGI General Observations a. Assuming that a taxpayer is subject to the net investment income tax (NIIT) in the first

2007 AND 2008 INFLATION-ADJUSTED TAX RATES

2007 AND 2008 INFLATION-ADJUSTED TAX RATES STANDARD DEDUCTION Filing Status Single $5,350 $5,450 Married, filing jointly/ss $10,700 $10,900 Head of household $7,850 $8,000 Married, filing separately $5,350

2007 AND 2008 INFLATION-ADJUSTED TAX RATES STANDARD DEDUCTION Filing Status Single $5,350 $5,450 Married, filing jointly/ss $10,700 $10,900 Head of household $7,850 $8,000 Married, filing separately $5,350

Product Profile ToolBox CS CS Professional Suite. Quick Access to Key Utilities. Meet Client Needs with a Wealth of Tools. Financial Calculators

Product Profile ToolBox CS CS Professional Suite Quick Access to Key Utilities ToolBox CS puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout the

Product Profile ToolBox CS CS Professional Suite Quick Access to Key Utilities ToolBox CS puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout the

Tax strategies for higher-income taxpayers

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

2018/2019 INCOME TAX UPDATE. Chicago Volunteer Legal Services Foundation. Chicago, Illinois February 21, 2019

2018/2019 INCOME TAX UPDATE Chicago Volunteer Legal Services Foundation Chicago, Illinois February 21, 2019 Lawrence R. Krupp Wipfli LLP 100 Tri-State International Suite 300 Lincolnshire, IL 60069 Telephone:

2018/2019 INCOME TAX UPDATE Chicago Volunteer Legal Services Foundation Chicago, Illinois February 21, 2019 Lawrence R. Krupp Wipfli LLP 100 Tri-State International Suite 300 Lincolnshire, IL 60069 Telephone:

Oil and Gas Tax Issues. Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP

Oil and Gas Tax Issues Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP Arnett Carbis Toothman llp 2018 Depletion and Ways to Compute What is depletion and what is its

Oil and Gas Tax Issues Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP Arnett Carbis Toothman llp 2018 Depletion and Ways to Compute What is depletion and what is its

Medicare taxes for higher-income taxpayers

Medicare taxes for higher-income taxpayers Many changes from the 2010 health care reform are now in effect Begin planning now You ll especially want to discuss these tax provisions with your Financial

Medicare taxes for higher-income taxpayers Many changes from the 2010 health care reform are now in effect Begin planning now You ll especially want to discuss these tax provisions with your Financial

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

5/29/ TAX CUTS AND JOBS ACT OVERVIEW. Individual Tax. Introduction-Individual Provisions. Dauphin County Bar Association May 30, 2018

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

Client Newsletter. 551 West 78th Street, Ste. 204, P.O. Box 254 Chanhassen, MN Office: Fax:

Client Newsletter 2015 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: RODENZ ACCOUNTING & TAX SERVICE LLC Accounting Business Consulting Tax Preparation Payroll Services Darrell E. Rodenz Certified Public Accountant

Client Newsletter 2015 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: RODENZ ACCOUNTING & TAX SERVICE LLC Accounting Business Consulting Tax Preparation Payroll Services Darrell E. Rodenz Certified Public Accountant

Tax Cuts & Jobs Act (TCJA)

") Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Financial Intelligence

Financial Intelligence Volume 14 Issue 1 Tax Changes and Planning Considerations in 2018 and Beyond by Brent Yanagida, CFP, EA On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs

Financial Intelligence Volume 14 Issue 1 Tax Changes and Planning Considerations in 2018 and Beyond by Brent Yanagida, CFP, EA On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs

TAX CUTS AND JOBS ACT OF 2017

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2016 www.cordascocpa.com INTRODUCTION 2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS It s that time of year again.

2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2016 www.cordascocpa.com INTRODUCTION 2016 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS It s that time of year again.

2017 vs Key Facts and Figures

2017 vs. 2018 Key Facts and Figures Note: We highlighted the information that changed between 2017 and 2018 with a box. * 2018 numbers are based on the Tax Cuts and Jobs Act (TCJA) of 2017. (Note: the

2017 vs. 2018 Key Facts and Figures Note: We highlighted the information that changed between 2017 and 2018 with a box. * 2018 numbers are based on the Tax Cuts and Jobs Act (TCJA) of 2017. (Note: the

Tax Cuts and Jobs Act 2017 HR 1

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

2018 Year-End Tax Reminders

2018 Year-End Tax Reminders Family Office Resources Income Tax Beginning in 2018, the standard deduction for single filers is $12,000 (up from $6,500 in 2017) and $24,000 for married taxpayers who file

2018 Year-End Tax Reminders Family Office Resources Income Tax Beginning in 2018, the standard deduction for single filers is $12,000 (up from $6,500 in 2017) and $24,000 for married taxpayers who file

Tax Season Reference Guide. Tool for preparing 2017 tax returns

Tax Season Reference Guide Tool for preparing tax returns Quick Reference Guide A tool for preparing returns At the close of every year, NATP s Tax Knowledge Center pulls together a list of common facts

Tax Season Reference Guide Tool for preparing tax returns Quick Reference Guide A tool for preparing returns At the close of every year, NATP s Tax Knowledge Center pulls together a list of common facts

2018 Year-End Tax Planning for Individuals

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Integrity Accounting

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM:

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: A publication of the Minnesota Association of Public Accountants The Minnesota Association of Public Accountants has prepared this newsletter.

Client Newsletter 2018 TAX HIGHLIGHTS WITH COMPLIMENTS FROM: A publication of the Minnesota Association of Public Accountants The Minnesota Association of Public Accountants has prepared this newsletter.

Proposed Reduction to Section 956 Income Inclusions by Domestic Corporations Owning CFC Stock

In This Issue 1 Proposed Reduction to Section 956 Income Inclusions by Domestic Corporations Owning CFC Stock 2 Minimizing Exposure to Five Possible Taxes 4 Decedent Transferred Partnership Interests,

In This Issue 1 Proposed Reduction to Section 956 Income Inclusions by Domestic Corporations Owning CFC Stock 2 Minimizing Exposure to Five Possible Taxes 4 Decedent Transferred Partnership Interests,

Withholding Certificate for Pension or Annuity Payments

Web 10-17 PURPOSE Form NC 4P is for North Carolina residents who are recipients of income from pensions, annuities, and certain other deferred compensation plans. Use the form to tell payers whether you

Web 10-17 PURPOSE Form NC 4P is for North Carolina residents who are recipients of income from pensions, annuities, and certain other deferred compensation plans. Use the form to tell payers whether you

Individual Year-End Tax Planning for 2016

Individual Year-End Tax Planning for 2016 It is getting to be that time of year where we should meet to review your tax situation for 2016. Proper year-end planning can help alleviate any unnecessary tax

Individual Year-End Tax Planning for 2016 It is getting to be that time of year where we should meet to review your tax situation for 2016. Proper year-end planning can help alleviate any unnecessary tax

TIPS FOR TRADERS ON PREPARING 2018 TAX RETURNS

1/4/2019 Copyright 2019 @ GreenTraderTax.com TIPS FOR TRADERS ON PREPARING 2018 TAX RETURNS Jan. 9, 2019 @ 12:00 pm EST (Interactive Brokers Webinar) 1 1/4/2019 Copyright 2019 @ GreenTraderTax.com 2 CPA

1/4/2019 Copyright 2019 @ GreenTraderTax.com TIPS FOR TRADERS ON PREPARING 2018 TAX RETURNS Jan. 9, 2019 @ 12:00 pm EST (Interactive Brokers Webinar) 1 1/4/2019 Copyright 2019 @ GreenTraderTax.com 2 CPA

TAX UPDATE TAX CUTS & JOBS ACT (2018) Add l Elderly & Blind Joint & Surviving Spouse: $1,300

Add l Elderly & Blind Joint & Surviving Spouse: $1,300") TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

Tax Cuts & Jobs Act Individuals

Tax Cuts & Jobs Act Individuals Holt & Patterson, LLC 260 Chesterfield Ind. Blvd. Chesterfield, MO 63005 (636)530-1040 1 http://holtpatterson.com/ Tax Cuts & Jobs Act Individuals 2 Holt & Patterson, LLC

Tax Cuts & Jobs Act Individuals Holt & Patterson, LLC 260 Chesterfield Ind. Blvd. Chesterfield, MO 63005 (636)530-1040 1 http://holtpatterson.com/ Tax Cuts & Jobs Act Individuals 2 Holt & Patterson, LLC

2014 YEAR-END TAX PLANNING

Page 1 of 5 2014 YEAR-END TAX PLANNING Year-end tax planning is especially challenging this year because Congress has yet to act on a host of tax breaks which expired at the end of 2013. Some of these

Page 1 of 5 2014 YEAR-END TAX PLANNING Year-end tax planning is especially challenging this year because Congress has yet to act on a host of tax breaks which expired at the end of 2013. Some of these

Re: 2012 Year-End Tax Planning for Individuals

Re: 2012 Year-End Tax Planning for Individuals To Our Valued Clients and Friends: Year-end tax planning is always complicated by the uncertainty that the following year may bring and 2012 is no exception.

Re: 2012 Year-End Tax Planning for Individuals To Our Valued Clients and Friends: Year-end tax planning is always complicated by the uncertainty that the following year may bring and 2012 is no exception.

Federal Income Tax Quick Reference

Federal Income Tax Quick Reference In alphabetical order Alimony For divorce decrees entered into after December 31, 2018, alimony will not be taxable income for the recipient and alimony will not be deduction

Federal Income Tax Quick Reference In alphabetical order Alimony For divorce decrees entered into after December 31, 2018, alimony will not be taxable income for the recipient and alimony will not be deduction

Estate Planning and Income Tax Considerations After the American Taxpayer Relief Act of 2012

_j _) _rml LJ-u-1.1 i Estate Planning and Income Tax Considerations After the American Taxpayer Relief Act of 2012 Robert Gardner May 22, 2013 C D BAKEILDONELSON,LJK txh'eliaiic Legislative History Economic

_j _) _rml LJ-u-1.1 i Estate Planning and Income Tax Considerations After the American Taxpayer Relief Act of 2012 Robert Gardner May 22, 2013 C D BAKEILDONELSON,LJK txh'eliaiic Legislative History Economic

Social Security and Medicare funding

Chapter 14 Looking Forward 1 Social Security and Medicare funding Medicare projected date of HI Trust Fund depletion is 2030, four years later than projected in last year s report Social Security - After

Chapter 14 Looking Forward 1 Social Security and Medicare funding Medicare projected date of HI Trust Fund depletion is 2030, four years later than projected in last year s report Social Security - After

Tax Reform The Tax Cuts and Jobs Act March 2, 2018

FPA of Greater Indiana Tax Reform The Tax Cuts and Jobs Act March 2, 2018 Presented by: William R. Owen, Jr. CPA, CFP BGBC Partners, LLP 300 N. Meridian Street Indianapolis, IN 46204 (317) 860-1092 FPA

FPA of Greater Indiana Tax Reform The Tax Cuts and Jobs Act March 2, 2018 Presented by: William R. Owen, Jr. CPA, CFP BGBC Partners, LLP 300 N. Meridian Street Indianapolis, IN 46204 (317) 860-1092 FPA

United States: Summary of key 2014 and 2015 federal tax rates and limits

www. pwcias.com United States: Summary of key 2014 and 2015 federal tax rates and limits January 2015 In brief The following is a high-level summary of some key individual tax rates and applicable limits

www. pwcias.com United States: Summary of key 2014 and 2015 federal tax rates and limits January 2015 In brief The following is a high-level summary of some key individual tax rates and applicable limits

2009 Economic Stimulus Act

2009 Economic Stimulus Act On February 17, President Obama signed into law the American Recovery and Reinvestment Act of 2009 (the 2009 Economic Stimulus Act). This new legislation was passed to aid our

2009 Economic Stimulus Act On February 17, President Obama signed into law the American Recovery and Reinvestment Act of 2009 (the 2009 Economic Stimulus Act). This new legislation was passed to aid our

10/8/2018. First major tax reform since Signed into law by President Donald Trump on December 22, 2017.

First major tax reform since 1986. Signed into law by President Donald Trump on December 22, 2017. 1 Introduction n Changes n Personal side: set to expire 12/31/2025 n Business side: mostly permanent n

First major tax reform since 1986. Signed into law by President Donald Trump on December 22, 2017. 1 Introduction n Changes n Personal side: set to expire 12/31/2025 n Business side: mostly permanent n

Tax Law Changes 2018

Tax Law Changes 2018 Standard Deduction Standard deduction increased to $24,000 MFJ and QW $18,000 HoH $12,000 Single and MFS Pub 4012 Tab F-1 Additional standard deduction amount for age 65 and older

Tax Law Changes 2018 Standard Deduction Standard deduction increased to $24,000 MFJ and QW $18,000 HoH $12,000 Single and MFS Pub 4012 Tab F-1 Additional standard deduction amount for age 65 and older

Tax Law & Scope Changes Carl Kantner As of December 3, 2018

Tax Law & Scope Changes 2018 Carl Kantner As of December 3, 2018 Tax-Aide Scope Manual The authority for Tax-Aide scope questions Manual for Tax Year 2018 issued November 28 Located in Portal Library under

Tax Law & Scope Changes 2018 Carl Kantner As of December 3, 2018 Tax-Aide Scope Manual The authority for Tax-Aide scope questions Manual for Tax Year 2018 issued November 28 Located in Portal Library under

What the New Tax Laws Mean to You

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

*Brackets adjusted for inflation in future years Long Term Capital Gains & Dividends Taxable income up to $413,200/$457,600 0% - 15%*

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

Tax Cuts and Jobs Act of 2017 (TCJA) Key Individual Tax Provisions

Key Individual Tax Provisions") Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Robert A Cowen Certified Public Accountant year end Tax planning for individuals

Robert A Cowen Certified Public Accountant 2017 year end Tax planning for individuals The end of the year is just a month away. It is good time to start to think about year-end planning. If you have been

Robert A Cowen Certified Public Accountant 2017 year end Tax planning for individuals The end of the year is just a month away. It is good time to start to think about year-end planning. If you have been

NATIONAL SOCIETY OF TAX PROFESSIONALS TAX CUTS AND JOBS ACT H.R.1 COMPARISON OF HOUSE AND SENATE BILLS AS OF DECEMBER 6, 2017

NATIONAL SOCIETY OF TAX PROFESSIONALS TAX CUTS AND JOBS ACT H.R.1 COMPARISON OF HOUSE AND SENATE BILLS AS OF DECEMBER 6, 2017 PROVISION: HOUSE BILL SENATE BILL 1. Individual Tax Rates 12%, 25%, 35%, 39.6%.

NATIONAL SOCIETY OF TAX PROFESSIONALS TAX CUTS AND JOBS ACT H.R.1 COMPARISON OF HOUSE AND SENATE BILLS AS OF DECEMBER 6, 2017 PROVISION: HOUSE BILL SENATE BILL 1. Individual Tax Rates 12%, 25%, 35%, 39.6%.

Presented by: Timothy A. George, CPA, MST, CCIFP

Tax Implications of Obamacare Presented by: Timothy A. George, CPA, MST, CCIFP 2 Players Club Drive, Suite 100, Charleston, West Virginia 25311 Office: (304) 343-4188 Fax: (304) 344-5035 20 Plus New Taxes

Tax Implications of Obamacare Presented by: Timothy A. George, CPA, MST, CCIFP 2 Players Club Drive, Suite 100, Charleston, West Virginia 25311 Office: (304) 343-4188 Fax: (304) 344-5035 20 Plus New Taxes

2018 TAX AND FINANCIAL PLANNING TABLES

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

TAX CUTS AND JOBS ACT (H.R. 1), 2018 A CLOSER LOOK PREPARED BY: ADIL A. BALOCH, CPA; CTRS. Accurate Records and Tax Services, Inc.

, 2018 A CLOSER LOOK PREPARED BY: ADIL A. BALOCH, CPA; CTRS. Accurate Records and Tax Services, Inc.") TAX CUTS AND JOBS ACT (H.R. 1), 2018 A CLOSER LOOK PREPARED BY: ADIL A. BALOCH, CPA; CTRS Accurate Records and Tax Services, Inc. 18562 Office Park Dr. Montgomery Village, MD 20886 (301) 519-1445 info@aabcpa.com

TAX CUTS AND JOBS ACT (H.R. 1), 2018 A CLOSER LOOK PREPARED BY: ADIL A. BALOCH, CPA; CTRS Accurate Records and Tax Services, Inc. 18562 Office Park Dr. Montgomery Village, MD 20886 (301) 519-1445 info@aabcpa.com

Middle Class Tax Relief Act of 2012

Middle Class Tax Relief Act of 2012 Two major bills enacting tax cuts for individuals expire at the end of 2010: the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA); and the Jobs and

Middle Class Tax Relief Act of 2012 Two major bills enacting tax cuts for individuals expire at the end of 2010: the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA); and the Jobs and

PAL and Section 1411

PAL and Section 1411 By Thomas C. Nice September 23, 2014 The Net Investment Income ( NII ) Tax of IRC Section 1411 applies to real estate income if the income is passive, or not from an IRC Section 162

PAL and Section 1411 By Thomas C. Nice September 23, 2014 The Net Investment Income ( NII ) Tax of IRC Section 1411 applies to real estate income if the income is passive, or not from an IRC Section 162