e-commerce and Transfer Pricing

|

|

|

- Eleanore Janis Manning

- 6 years ago

- Views:

Transcription

1 e-commerce and Transfer Pricing Richard Hiemstra 20 November 2017

2 Contents The digital economy Corporate Tax: what is the issue? Google and Amazon EU Commission Communication Existing rules Longer Term and Shorter term solutions Issues and concerns Final statements

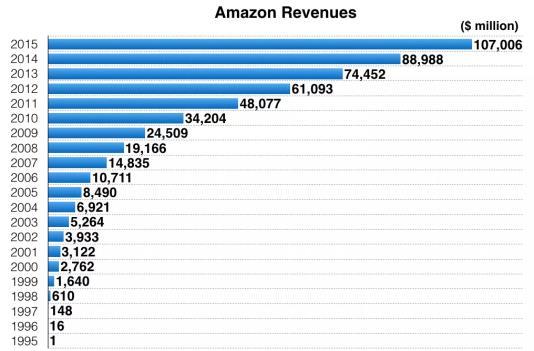

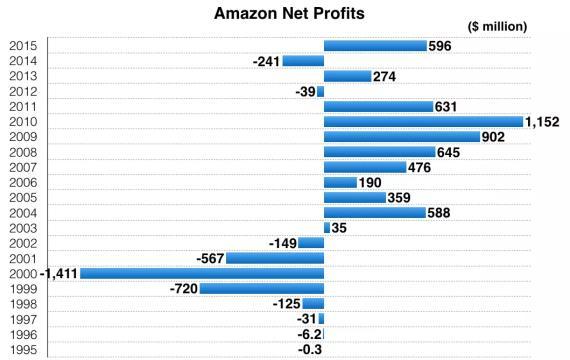

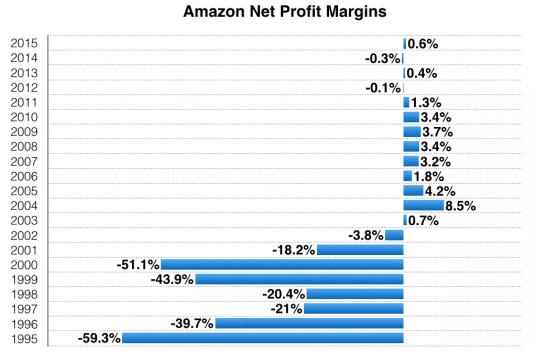

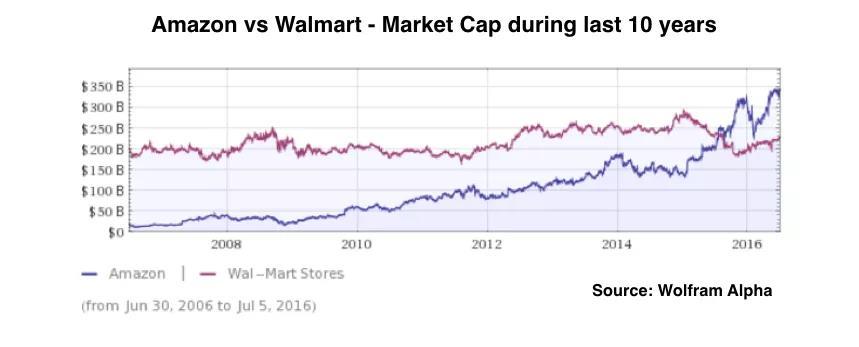

3 The digital economy is here to stay They have critical mass in the top 20 of companies with the largest market cap. And dominate it. e-commerce is growing faster than regular business.

4 Key characteristics of e-commerce Limited physical presence Conduct business activity remotely Exponential growth Winner takes all Volatility Start-up losses Value per employee 25m per employee 77m per employee 345m per employee

5 What is the corporate tax issue of e-commerce? Base erosion e-commerce companies avoid taxation via aggressive tax schemes OR Non-ability to tax e-commerce companies cannot be taxed where they do business A business driven by intangibles can opt for double non-taxation Without physical presence in the end market, taxation rights do not exist

6 Google and Amazon CSA IP fee Structures Routine operations in European end-markets European Hub without IP (Ire/Lux) Non-taxed IP owner of non-us IP IP Cost Sharing Arrangement US tax deferral structure Counter measures BEPS 8-10 EU state aid claims UK Diverted Profit Tax ( Google tax )

7 Communication European Commission A Fair and Efficient Tax System in the European Union for the Digital Single Market Existing tax rules designed for brick and mortar businesses Digital business models rely less on physical presence Significant economic presence: Internet sales Advertisement income Data collection Two questions: Where to tax? (nexus) and What to tax? (value creation)

8 Existing rules 1. Taxable presence Legal entities Physical PE Agency PE Where to tax 2. Transfer pricing At arm s length principle Dealings between related parties (i.e. entities with taxable presence) What to tax Fair allocation of taxation rights

9 Existing rules 1. Taxable presence Legal entities Physical PE Agency PE Where to tax 2. Transfer pricing At arm s length principle Dealings between related parties (i.e. entities with taxable presence) What to tax Fair allocation of taxation rights

10 Longer term solution Where to tax Introduction of Virtual PE for significant economic presence What to tax Formula apportionment for hard to value intangibles How to implement The CCCTB proposal offers the basis to address these challenges

11 Shorter term solutions What Equalisation tax on turnover if insufficiently taxed Withholding tax on digital transactions from non-residents Levy on revenues generated from the provision of digital services or advertisement activity How Appropriate level is deemed to be the EU Set example to the world

12 Issues and concerns Double taxation Turnover tax and credits Turnover tax and profit level Virtual PE exemptions At arm s length principle & formula apportionment (CCCTB) Definition significant economic presence Europe vs Rest of World

13 Exponential growth; profit realization vs profit expectation

14 Exponential growth and profitability Key questions: At what moment in time is it appropriate to start taxing? Exponential revenue growth Net profitable NOLs Net profitable Revenue based levy Contingent to profit? Credits?

15 Virtual PE & CCCTB vs At arm s length principle ALP? Virtual PE/CCCTB Virtual PE/CCCTB Key questions: How would the principles of the Google/Amazon structures work with the Virtual PE/CCCTB solution? At arm s length principle or lookthrough principle? Effective taxation in the residence state relevant? How to deal with NOLs in light of effective taxation?

16 Significant economic presence Threshold of online revenue Absolute amount Relative to overall revenues Amount of advertisement income Absolute amount Relative to overall revenues How to deal with indirect earning models Data collection and resale of data outside EU

17 Closing statements Still a long way to go But things can move faster than expected BEPS Increased media attention And not always in the direction as expected

The European Commission Is Attempting a Radical Change to How Digital Transactions Are Taxed Throughout the EU

The European Commission Is Attempting a Radical Change to How Digital Transactions Are Taxed Throughout the EU October 20, 2017 On 21 September 2017, the European Commission issued a fact sheet outlining

The European Commission Is Attempting a Radical Change to How Digital Transactions Are Taxed Throughout the EU October 20, 2017 On 21 September 2017, the European Commission issued a fact sheet outlining

16 March :00 16:00 (CET)

") 16 March 2018 15:00 16:00 (CET) Join the discussion Ask questions and comment throughout the webcast: CTP.Contact@oecd.org @OECDtax or #OECDTaxTalks 2015 Action 1 Report Digitalisation of the economy,

16 March 2018 15:00 16:00 (CET) Join the discussion Ask questions and comment throughout the webcast: CTP.Contact@oecd.org @OECDtax or #OECDTaxTalks 2015 Action 1 Report Digitalisation of the economy,

The OECD s 3 Major Tax Initiatives

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

Fair taxation of the digital European Commission DG TAXUD. economy

Fair taxation of the digital European Commission DG TAXUD economy The issue at stake Difficulty to tax/ opportunities for tax avoidance Lack of a level playing field and distortion of competition Less

Fair taxation of the digital European Commission DG TAXUD economy The issue at stake Difficulty to tax/ opportunities for tax avoidance Lack of a level playing field and distortion of competition Less

Taxation & the Digital Economy

Taxation & the Digital Economy John Muiruri - Partner Muiruri Macharia & Associates Email : jmuiruri@muirurimacharia.com Digital Economy Key Terms BEPS : Base Erosion & Profit Shifting (BEPS) is the result

Taxation & the Digital Economy John Muiruri - Partner Muiruri Macharia & Associates Email : jmuiruri@muirurimacharia.com Digital Economy Key Terms BEPS : Base Erosion & Profit Shifting (BEPS) is the result

REQUEST FOR INPUT ON WORK REGARDING THE TAX CHALLENGES OF THE DIGITALISED ECONOMY

OECD c/o Mr. David Bradburry 2 Rue André Pascal 75775 Paris France Author Phone Telefax E-Mail Date Pe/JT E 09/17 +49 30 278 76 310 +49 30 278 76 799 trommer@dstv.de 18.10.2071 REQUEST FOR INPUT ON WORK

OECD c/o Mr. David Bradburry 2 Rue André Pascal 75775 Paris France Author Phone Telefax E-Mail Date Pe/JT E 09/17 +49 30 278 76 310 +49 30 278 76 799 trommer@dstv.de 18.10.2071 REQUEST FOR INPUT ON WORK

Permanent Establishment through Digital Presence Will it work?

Permanent Establishment through Digital Presence Will it work? Himanshu Parekh 8 December 2018 Background BEPS Action Plan 1 Digital Economy is a result of Information and Communication Technology Technologies

Permanent Establishment through Digital Presence Will it work? Himanshu Parekh 8 December 2018 Background BEPS Action Plan 1 Digital Economy is a result of Information and Communication Technology Technologies

Digital Economy. Dr. Amar Mehta October Chambers Of Tax Consultant, Mumbai.

Digital Economy Chambers Of Tax Consultant, Mumbai Dr. Amar Mehta October 2018 Categories 1 OECD s BEPS Action 1 Final Report 4 Digital PE: The EU Version 7 Italy 2 OECD s BEPS Interim Report Action 1

Digital Economy Chambers Of Tax Consultant, Mumbai Dr. Amar Mehta October 2018 Categories 1 OECD s BEPS Action 1 Final Report 4 Digital PE: The EU Version 7 Italy 2 OECD s BEPS Interim Report Action 1

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 21.3.2018 COM(2018) 146 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Time to establish a modern, fair and efficient taxation standard

EUROPEAN COMMISSION Brussels, 21.3.2018 COM(2018) 146 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Time to establish a modern, fair and efficient taxation standard

VIRTUAL PERMANENT ESTABLISHMENT Presented by Mustapha Ndajiwo UNISA/FIRS

VIRTUAL PERMANENT ESTABLISHMENT Presented by Mustapha Ndajiwo UNISA/FIRS INTRODUCTION PERMANENT ESTABLISHMENT The profits of an enterprise of a Contracting State shall be taxable only in that state unless

VIRTUAL PERMANENT ESTABLISHMENT Presented by Mustapha Ndajiwo UNISA/FIRS INTRODUCTION PERMANENT ESTABLISHMENT The profits of an enterprise of a Contracting State shall be taxable only in that state unless

Georgia Stamatelou Partner, Head of Tax 19 April 2018

Taxation and Challenges of the Digital Economy Georgia Stamatelou Partner, Head of Tax 19 April 2018 Agenda Digital Economy in the EU: Commission s proposals Important Milestones The Various Initiatives

Taxation and Challenges of the Digital Economy Georgia Stamatelou Partner, Head of Tax 19 April 2018 Agenda Digital Economy in the EU: Commission s proposals Important Milestones The Various Initiatives

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC Agenda The current environment and the case for change Australian measures most

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC Agenda The current environment and the case for change Australian measures most

Taxation of digital economy

Taxation of digital economy CA Jasdeep Sahni WIRC 15 December 2018 Contents Conventional commerce Digital economy India tax considerations Summing up 2 Conventional commerce Conventional commerce Retailers

Taxation of digital economy CA Jasdeep Sahni WIRC 15 December 2018 Contents Conventional commerce Digital economy India tax considerations Summing up 2 Conventional commerce Conventional commerce Retailers

SEMINAR ON TRANSFER PRICING 23rd September, Valuation Approaches and their applicability under Transfer Pricing. CA Siddharth Banwat

SEMINAR ON TRANSFER PRICING 23rd September, 2017 Valuation Approaches and their applicability under Transfer Pricing WHAT IS VALUATION? WHAT IS VALUE? A value in exchange is a hypothetical price and the

SEMINAR ON TRANSFER PRICING 23rd September, 2017 Valuation Approaches and their applicability under Transfer Pricing WHAT IS VALUATION? WHAT IS VALUE? A value in exchange is a hypothetical price and the

European Commission releases package on taxation of the digital economy

European Commission releases package on taxation of the digital economy On March 21, 2018, the European Commission issued a package on a Fair and Effective Tax System in the EU for the Digital Single Market,

European Commission releases package on taxation of the digital economy On March 21, 2018, the European Commission issued a package on a Fair and Effective Tax System in the EU for the Digital Single Market,

Korean Tax Update BEPS Implementation

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

TAX EFFICIENT GLOBAL SUPPLY CHAINS IN 2018

TAX EFFICIENT GLOBAL SUPPLY CHAINS IN 2018 Michael Hardgrove Paul Flignor June 14, 2018 www.dlapiper.com 0 1 Global Supply Chain: Transactional Flow and Principal Concepts Global Supply Chain: Operational

TAX EFFICIENT GLOBAL SUPPLY CHAINS IN 2018 Michael Hardgrove Paul Flignor June 14, 2018 www.dlapiper.com 0 1 Global Supply Chain: Transactional Flow and Principal Concepts Global Supply Chain: Operational

Short Term Measures The EU Digital Services Tax (DST) Proposal v. The Indian Equalisation Levy

Proposal v. The Indian Equalisation Levy") Short Term Measures The EU Digital Services Tax (DST) Proposal v. The Indian Equalisation Levy Sriram Govind, LL.M. Foundation for International Taxation International Taxation Conference, 2018 December

Short Term Measures The EU Digital Services Tax (DST) Proposal v. The Indian Equalisation Levy Sriram Govind, LL.M. Foundation for International Taxation International Taxation Conference, 2018 December

Digital Sector Based Own Resource conclusions reached by the EC Expert Group and OECD-BEPS Action Plan on taxation and the digital economy

Digital Sector Based Own Resource conclusions reached by the EC Expert Group and OECD-BEPS Action Plan on taxation and the digital economy Directorate-General Communications Networks, Content & Technology

Digital Sector Based Own Resource conclusions reached by the EC Expert Group and OECD-BEPS Action Plan on taxation and the digital economy Directorate-General Communications Networks, Content & Technology

Fair Taxation of the Digital Economy: What is Fair? 2018 KPMG EMA Tax Summit Rome

Fair Taxation of the Digital Economy: What is Fair? 2018 KPMG EMA Tax Summit Rome Panel Chris Morgan Head of Global Tax Policy E: christopher.morgan@kpmg.co.uk Robert Van der Jagt Chairman of KPMG's EU

Fair Taxation of the Digital Economy: What is Fair? 2018 KPMG EMA Tax Summit Rome Panel Chris Morgan Head of Global Tax Policy E: christopher.morgan@kpmg.co.uk Robert Van der Jagt Chairman of KPMG's EU

BEPS and ATAD: Where do we stand?

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, XXX COM(2017) 547 COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL A Fair and Efficient Tax System in the European Union for the Digital Single

EUROPEAN COMMISSION Brussels, XXX COM(2017) 547 COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL A Fair and Efficient Tax System in the European Union for the Digital Single

Diverted Profits Tax Guidance. Guidance 10 December 2014

Diverted Profits Tax Guidance Guidance 10 December 2014 1 Contents Page Introduction Chapter 1 Chapter 2 Chapter 3 Introduction & Overview Application of Diverted Profits Tax Diverted Profits Tax - processes.

Diverted Profits Tax Guidance Guidance 10 December 2014 1 Contents Page Introduction Chapter 1 Chapter 2 Chapter 3 Introduction & Overview Application of Diverted Profits Tax Diverted Profits Tax - processes.

Engaging title in Green Descriptive element in Blue 2 lines if needed

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

Analysis of Intellectual Property Tax Planning Strategies of Multinationals and the Impact of the BEPS Project

Analysis of Intellectual Property Tax Planning Strategies of Multinationals and the Impact of the BEPS Project Dr Ranjana Gupta Auckland University of Technology 1 Introduction The global economy and the

Analysis of Intellectual Property Tax Planning Strategies of Multinationals and the Impact of the BEPS Project Dr Ranjana Gupta Auckland University of Technology 1 Introduction The global economy and the

BEPS - Current Status of Implementation in EU Countries. Prof. Guglielmo Maisto 1 March 2019

BEPS - Current Status of Implementation in EU Countries Prof. Guglielmo Maisto 1 March 2019 1 Pillar I COHERENCE Action 2 Neutralizing Hybrid Mismatch Arrangements Action 3 CFC Rules Action 4 Interest

BEPS - Current Status of Implementation in EU Countries Prof. Guglielmo Maisto 1 March 2019 1 Pillar I COHERENCE Action 2 Neutralizing Hybrid Mismatch Arrangements Action 3 CFC Rules Action 4 Interest

IMPACT OF TAX ON M&A. Simon Fletcher 14 October 2016

IMPACT OF TAX ON M&A Simon Fletcher AGENDA 1. Tax environment 2. Recent developments 3. Impact on M&A 4. Questions Disclaimer: this presentation is intended to be for general guidance on matters of interest,

IMPACT OF TAX ON M&A Simon Fletcher AGENDA 1. Tax environment 2. Recent developments 3. Impact on M&A 4. Questions Disclaimer: this presentation is intended to be for general guidance on matters of interest,

International Tax Primer. Third Edition. Brian J. Arnold

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury International Tax Policy Forum and Institute of Economic Law Conference

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury International Tax Policy Forum and Institute of Economic Law Conference

Global Tax Trends Impact on US MNCs. December 1, 2017

Global Tax Trends Impact on US MNCs December 1, 2017 1 Panel Panelists Michael J. Caballero, Partner, Covington & Burling LLP, Washington, DC Robert B. Stack, Managing Director, Washington National and

Global Tax Trends Impact on US MNCs December 1, 2017 1 Panel Panelists Michael J. Caballero, Partner, Covington & Burling LLP, Washington, DC Robert B. Stack, Managing Director, Washington National and

Common (Consolidated) Corporate Tax Base what are the next steps?

Corporate Tax Base what are the next steps?") Common (Consolidated) Corporate Tax Base what are the next steps? Uwe Ihli, Head of Sector, DG TAXUD D1.003, European Commission IFA Austria, 8 October 2018, Vienna Main objectives for the taxation in

Common (Consolidated) Corporate Tax Base what are the next steps? Uwe Ihli, Head of Sector, DG TAXUD D1.003, European Commission IFA Austria, 8 October 2018, Vienna Main objectives for the taxation in

Discussion on amendments to Agency PE rules in Budget 2018

Discussion on amendments to Agency PE rules in Budget 2018 Jimit Devani July 2018 Agenda Concept of Permanent Establishment (PE) BEPS Action Plan 7 India budget update Consequence of PE Way forward Recent

Discussion on amendments to Agency PE rules in Budget 2018 Jimit Devani July 2018 Agenda Concept of Permanent Establishment (PE) BEPS Action Plan 7 India budget update Consequence of PE Way forward Recent

The Arm s Length Standard: a Blind Spot in the CC(C)TB Proposals. Amsterdam, 27 January First Critical Analysis Prof.dr. D.S.

TB Proposals. Amsterdam, 27 January First Critical Analysis Prof.dr. D.S.") The Arm s Length Standard: a Blind Spot in the CC(C)TB Proposals Amsterdam, 27 January 2017 The Return of the CC(C)TB: First Critical Analysis Prof.dr. D.S. Smit Menu for the next 20 minutes What arm s

The Arm s Length Standard: a Blind Spot in the CC(C)TB Proposals Amsterdam, 27 January 2017 The Return of the CC(C)TB: First Critical Analysis Prof.dr. D.S. Smit Menu for the next 20 minutes What arm s

BEPS, SPILLOVERS, ETC.: CURRENT ISSUES IN INTERNATIONAL CORPORATE TAXATION

BEPS, SPILLOVERS, ETC.: CURRENT ISSUES IN INTERNATIONAL CORPORATE TAXATION Michael Keen JTA-IFA Tokyo, April 10 2015 See IMF (2014), Spillovers in international corporate taxation Views should not be attributed

BEPS, SPILLOVERS, ETC.: CURRENT ISSUES IN INTERNATIONAL CORPORATE TAXATION Michael Keen JTA-IFA Tokyo, April 10 2015 See IMF (2014), Spillovers in international corporate taxation Views should not be attributed

Intellectual property in the age of BEPS

Intellectual property in the age of BEPS Tax Executives Institute Michigan Chapter Detroit 28 October 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

Intellectual property in the age of BEPS Tax Executives Institute Michigan Chapter Detroit 28 October 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS)

") Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Diverted Profits Tax. The Royal Society 6-9 Carlton House Terrace London SW1Y 5AG. 08 January 2015

Diverted Profits Tax The Royal Society 6-9 Carlton House Terrace London SW1Y 5AG 08 January 2015 Agenda 09.00 09.30 Registration 09.30 09.35 Open - Aidan Reilly (HMRC) 09.35 09.45 Policy Context and Overview

Diverted Profits Tax The Royal Society 6-9 Carlton House Terrace London SW1Y 5AG 08 January 2015 Agenda 09.00 09.30 Registration 09.30 09.35 Open - Aidan Reilly (HMRC) 09.35 09.45 Policy Context and Overview

Practical Implications of BEPS

www.pwc.com/il Practical Implications of BEPS Vered Kirshner, Tax Partner, PwC Israel Ben Blumenfeld, Tax and Transfer Pricing Senior Manager, PwC Israel Aim of BEPS Action plan backed by the OECD and

www.pwc.com/il Practical Implications of BEPS Vered Kirshner, Tax Partner, PwC Israel Ben Blumenfeld, Tax and Transfer Pricing Senior Manager, PwC Israel Aim of BEPS Action plan backed by the OECD and

Emerging trends in BEPS arena

For private circulation only October 2018 01 Emerging trends in BEPS arena Background OECD s BEPS Project was launched after one of the most severe financial and economic crisis period during 2008, with

For private circulation only October 2018 01 Emerging trends in BEPS arena Background OECD s BEPS Project was launched after one of the most severe financial and economic crisis period during 2008, with

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February AM PM Conrad Hotel, Hong Kong

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS)

") 22 July 2013 OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS) Executive summary On 19 July 2013, the Organisation for Economic Cooperation and Development (OECD) issued its much-anticipated

22 July 2013 OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS) Executive summary On 19 July 2013, the Organisation for Economic Cooperation and Development (OECD) issued its much-anticipated

Working Party on Tax Questions (Direct Taxation CCTB) Challenges of the digital economy for direct taxation - State of play and the way forward

Challenges of the digital economy for direct taxation - State of play and the way forward") Brussels, 11 October 2017 WK 11067/2017 INIT LIMITE FISC ECOFIN MEETING DOCUMENT From: To: Subject: Presidency Working Party on Tax Questions (Direct Taxation CCTB) Challenges of the digital economy for

Brussels, 11 October 2017 WK 11067/2017 INIT LIMITE FISC ECOFIN MEETING DOCUMENT From: To: Subject: Presidency Working Party on Tax Questions (Direct Taxation CCTB) Challenges of the digital economy for

Table of Contents. Part I La Brienza Winery: Tax Trouble in Wine Country. Chapter 1 Introduction: The Vital Role of Tax in Global Management

Table of Contents Part I La Brienza Winery: Tax Trouble in Wine Country Chapter 1 Introduction: The Vital Role of Tax in Global Management La Brienza Winery, Present Day...3 The Two Objectives of International

Table of Contents Part I La Brienza Winery: Tax Trouble in Wine Country Chapter 1 Introduction: The Vital Role of Tax in Global Management La Brienza Winery, Present Day...3 The Two Objectives of International

Subject: Request for input on work regarding the tax challenges of the digitalized economy

1 Rue Euler 75008 Paris France Tel: +33 1 70 75 01 90 www.nera.com OECD TFDE VIA EMAIL (TFDE@oecd.org) Subject: Request for input on work regarding the tax challenges of the digitalized economy Comments

1 Rue Euler 75008 Paris France Tel: +33 1 70 75 01 90 www.nera.com OECD TFDE VIA EMAIL (TFDE@oecd.org) Subject: Request for input on work regarding the tax challenges of the digitalized economy Comments

Principles of International Tax Planning

Overview and Learning Objectives This course is aimed at analysing the fundamentals of international tax planning in a structured and consistent manner, deepening the knowledge of tax planning techniques

Overview and Learning Objectives This course is aimed at analysing the fundamentals of international tax planning in a structured and consistent manner, deepening the knowledge of tax planning techniques

Proposal for a COUNCIL DIRECTIVE. on the common system of a digital services tax on revenues resulting from the provision of certain digital services

EUROPEAN COMMISSION Brussels, 21.3.2018 COM(2018) 148 final 2018/0073 (CNS) Proposal for a COUNCIL DIRECTIVE on the common system of a digital services tax on revenues resulting from the provision of certain

EUROPEAN COMMISSION Brussels, 21.3.2018 COM(2018) 148 final 2018/0073 (CNS) Proposal for a COUNCIL DIRECTIVE on the common system of a digital services tax on revenues resulting from the provision of certain

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, XXX COM(2017) 547/2 COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL A Fair and Efficient Tax System in the European Union for the Digital Single

EUROPEAN COMMISSION Brussels, XXX COM(2017) 547/2 COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL A Fair and Efficient Tax System in the European Union for the Digital Single

32nd Annual Asia Pacific Tax Conference November 2016 JW Marriott Hotel Hong Kong

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong Alternative A: Source country taxation, evolving PE rules and unilateral measures Chair: Gary Sprague, Palo Alto

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong Alternative A: Source country taxation, evolving PE rules and unilateral measures Chair: Gary Sprague, Palo Alto

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud

and EU measures against aggressive tax planning and tax fraud") The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

Tax Obstacles in Cross Border Planning

International Fiscal Association USA Branch New York Region Fall Meeting Thursday, December 1, 2016 Tax Obstacles in Cross Border Planning Colleen O Neill Ernst & Young LLP Maarten P. Maaskant PricewaterhouseCoopers

International Fiscal Association USA Branch New York Region Fall Meeting Thursday, December 1, 2016 Tax Obstacles in Cross Border Planning Colleen O Neill Ernst & Young LLP Maarten P. Maaskant PricewaterhouseCoopers

Tax Issues related to the Digitalization of the Economy: Report

Distr.: General 5 April 2019 Original: English Committee of Experts on International Cooperation in Tax Matters Eighteenth session New York, 23-26 April 2019 Item 3 (j) of the provisional agenda Tax Issues

Distr.: General 5 April 2019 Original: English Committee of Experts on International Cooperation in Tax Matters Eighteenth session New York, 23-26 April 2019 Item 3 (j) of the provisional agenda Tax Issues

15445/17 AS/AR/mpd 1 DG G 2B

Council of the European Union Brussels, 5 December 2017 (OR. en) 15445/17 FISC 346 ECOFIN 1092 OUTCOME OF PROCEEDINGS From: General Secretariat of the Council To: Delegations No. prev. doc.: 15175/17 Subject:

Council of the European Union Brussels, 5 December 2017 (OR. en) 15445/17 FISC 346 ECOFIN 1092 OUTCOME OF PROCEEDINGS From: General Secretariat of the Council To: Delegations No. prev. doc.: 15175/17 Subject:

Future of tax in a digital economy: Are you prepared? The Dbriefs International Tax series

Future of tax in a digital economy: Are you prepared? The Dbriefs International Tax series Claudio Cimetta / Li Qun Gao / William Marshall 1 June 2017 Agenda The digital economy Tax challenges of the digital

Future of tax in a digital economy: Are you prepared? The Dbriefs International Tax series Claudio Cimetta / Li Qun Gao / William Marshall 1 June 2017 Agenda The digital economy Tax challenges of the digital

AN APPRAISAL OF THE PROPOSED DST. A study commissioned by CCIA 20 September 2018

AN APPRAISAL OF THE PROPOSED DST A study commissioned by CCIA 20 September 2018 DST: What, why and the two problems What A new 3% tax on certain digital activities: i) Online advertising revenues, ii)

AN APPRAISAL OF THE PROPOSED DST A study commissioned by CCIA 20 September 2018 DST: What, why and the two problems What A new 3% tax on certain digital activities: i) Online advertising revenues, ii)

Internet Taxation. Francis Bloch. Toulouse, Postal Conference, April 16, Université Paris 1 and PSE

Internet Taxation Francis Bloch Université Paris 1 and PSE Toulouse, Postal Conference, April 16, 2016 Bloch (PSE) Internet Taxation April 1, 2016 1 / 29 Introduction Taxation of Internet Platforms Internet

Internet Taxation Francis Bloch Université Paris 1 and PSE Toulouse, Postal Conference, April 16, 2016 Bloch (PSE) Internet Taxation April 1, 2016 1 / 29 Introduction Taxation of Internet Platforms Internet

Diverted Profits Tax. Key points

Diverted Profits Tax Given the publicity surrounding the practices of multinationals in particular a number of the large US technology corporations - in structuring their affairs to minimise their tax

Diverted Profits Tax Given the publicity surrounding the practices of multinationals in particular a number of the large US technology corporations - in structuring their affairs to minimise their tax

Corporate tax and the digital economy Response by the Chartered Institute of Taxation

Corporate tax and the digital economy Response by the Chartered Institute of Taxation 1 Introduction 1.1 We refer to the government s position paper on Corporate tax and the digital economy published in

Corporate tax and the digital economy Response by the Chartered Institute of Taxation 1 Introduction 1.1 We refer to the government s position paper on Corporate tax and the digital economy published in

New Israeli Tax Guidance on On line Activity of Foreign Companies

April 2015. Newsletter No. 194977 New Israeli Tax Guidance on On line Activity of Foreign Companies General The Israeli Tax Authority ("ITA") recently published a new draft circular (the equivalent of

April 2015. Newsletter No. 194977 New Israeli Tax Guidance on On line Activity of Foreign Companies General The Israeli Tax Authority ("ITA") recently published a new draft circular (the equivalent of

Proposal for a COUNCIL DIRECTIVE. laying down rules relating to the corporate taxation of a significant digital presence

EUROPEAN COMMISSION Brussels, 21.3.2018 COM(2018) 147 final 2018/0072 (CNS) Proposal for a COUNCIL DIRECTIVE laying down rules relating to the corporate taxation of a significant digital presence {SWD(2018)

EUROPEAN COMMISSION Brussels, 21.3.2018 COM(2018) 147 final 2018/0072 (CNS) Proposal for a COUNCIL DIRECTIVE laying down rules relating to the corporate taxation of a significant digital presence {SWD(2018)

E-Commerce structures & tax issues

E-Commerce structures & tax issues CA Jasdeep Sahni WIRC, Mumbai 1 September 2018 Contents Traditional commerce E- commerce and related tax considerations Recent amendments under the Income-tax Act, 1961

E-Commerce structures & tax issues CA Jasdeep Sahni WIRC, Mumbai 1 September 2018 Contents Traditional commerce E- commerce and related tax considerations Recent amendments under the Income-tax Act, 1961

de Nederlandse Orde van Belastingadviseurs The Dutch Association of Tax Advisers

de Nederlandse Orde van Belastingadviseurs The Dutch Association of Tax Advisers To the European Commission January 2, 2018 Subject: European Commission s Public Consultation on Fair Taxation of the Digital

de Nederlandse Orde van Belastingadviseurs The Dutch Association of Tax Advisers To the European Commission January 2, 2018 Subject: European Commission s Public Consultation on Fair Taxation of the Digital

Global Tax Webcast. Taxation of the Digital Economy: an Asia Pacific perspective on the recent developments. KPMG Asia Pacific Tax Centre

Global Tax Webcast Taxation of the Digital Economy: an Asia Pacific perspective on the recent developments KPMG Asia Pacific Tax Centre May 15, 2018 Speakers Grant Wardell-Johnson, Leader, Australian Tax

Global Tax Webcast Taxation of the Digital Economy: an Asia Pacific perspective on the recent developments KPMG Asia Pacific Tax Centre May 15, 2018 Speakers Grant Wardell-Johnson, Leader, Australian Tax

OECD releases final BEPS package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

Tackling Aggressive Tax Planning in the European Union - Recent Developments

Tackling Aggressive Tax Planning in the European Union - Recent Developments Dr Christiana HJI Panayi Senior Lecturer in Tax Law Queen Mary University of London 1 Important recent developments Digital

Tackling Aggressive Tax Planning in the European Union - Recent Developments Dr Christiana HJI Panayi Senior Lecturer in Tax Law Queen Mary University of London 1 Important recent developments Digital

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

Lund University. Profit-allocation based on value creation in the digital economy. Tim Theunis

Lund University School of Economics and Management Department of Business Law Profit-allocation based on value creation in the digital economy By Tim Theunis HARN60 Master Thesis Master s Programme in

Lund University School of Economics and Management Department of Business Law Profit-allocation based on value creation in the digital economy By Tim Theunis HARN60 Master Thesis Master s Programme in

Software and innovation deduction: Belgium is the place to be! 23 November 2017

Software and innovation deduction: Belgium is the place to be! 23 1 Innovation income deduction (adopted by the Chamber of Representatives on 2 February 2017) R&D incentives Innovation income deduction

Software and innovation deduction: Belgium is the place to be! 23 1 Innovation income deduction (adopted by the Chamber of Representatives on 2 February 2017) R&D incentives Innovation income deduction

COMMISSION RECOMMENDATION. of relating to the corporate taxation of a significant digital presence

EUROPEAN COMMISSION Brussels, 21.3.2018 C(2018) 1650 final COMMISSION RECOMMENDATION of 21.3.2018 relating to the corporate taxation of a significant digital presence EN EN COMMISSION RECOMMENDATION of

EUROPEAN COMMISSION Brussels, 21.3.2018 C(2018) 1650 final COMMISSION RECOMMENDATION of 21.3.2018 relating to the corporate taxation of a significant digital presence EN EN COMMISSION RECOMMENDATION of

Selling goods and services in the digital economy

Selling goods and services in the digital economy James Freed Principal KPMG LLP Chicago, IL jfreed@kpmg.com Andrew Street Global Indirect Tax / VAT Consulting Professional Amazon Inc. Chicago, IL streandr@amazon.com

Selling goods and services in the digital economy James Freed Principal KPMG LLP Chicago, IL jfreed@kpmg.com Andrew Street Global Indirect Tax / VAT Consulting Professional Amazon Inc. Chicago, IL streandr@amazon.com

Taxation of digital economy: does it require a fundamental change of approach?

Taxation of digital economy: does it require a fundamental change of approach? Pere M. Pons Dublin (Ireland), 19 September 2014 Disclaimer This presentation is a brief summary of the article Taxation of

Taxation of digital economy: does it require a fundamental change of approach? Pere M. Pons Dublin (Ireland), 19 September 2014 Disclaimer This presentation is a brief summary of the article Taxation of

Trends I Netherlands moves away from fiscal offshore industry

1 Trends I Netherlands moves away from fiscal offshore industry The Netherlands is slowly but surely steering away from facilitating the use of its corporate income tax system by companies that are set

1 Trends I Netherlands moves away from fiscal offshore industry The Netherlands is slowly but surely steering away from facilitating the use of its corporate income tax system by companies that are set

Hot topics Treasury seminar

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

other taxes (importance of corporation tax in Australia and in developing countries great than in other countries)

") OXFORD LAW Judith Freedman, Pinsent Masons Professor of Tax Law, Oxford University and Oxford Centre for Business Taxation, Crawford School of Public Policy Tax and Transfer Policy Institute, Canberra

OXFORD LAW Judith Freedman, Pinsent Masons Professor of Tax Law, Oxford University and Oxford Centre for Business Taxation, Crawford School of Public Policy Tax and Transfer Policy Institute, Canberra

Equalisation levy Genesis, Provisions and Interpretation Issues

Equalisation levy Genesis, Provisions and Interpretation Issues By Shaily Gupta, Senior Associate, Vaish Associates Advocates Email: shailygupta@vaishlaw.com 1. Digital Economy The new Economy 'Digital

Equalisation levy Genesis, Provisions and Interpretation Issues By Shaily Gupta, Senior Associate, Vaish Associates Advocates Email: shailygupta@vaishlaw.com 1. Digital Economy The new Economy 'Digital

Foundation for International Taxation

Foundation for International Taxation 9 th December, 2017 Brief Presentation on A better & complete system of E-commerce Taxation CA Rashmin Sanghvi www.rashminsanghvi.com Important Notes: 1. This presentation

Foundation for International Taxation 9 th December, 2017 Brief Presentation on A better & complete system of E-commerce Taxation CA Rashmin Sanghvi www.rashminsanghvi.com Important Notes: 1. This presentation

IBFD Course Programme Principles of Transfer Pricing

IBFD Course Programme Principles of Transfer Pricing Overview and Learning Objectives On 5 October 2015, the OECD published its reports addressing base erosion and profit shifting (BEPS). This new guidance

IBFD Course Programme Principles of Transfer Pricing Overview and Learning Objectives On 5 October 2015, the OECD published its reports addressing base erosion and profit shifting (BEPS). This new guidance

CHALLENGES OF THE DIGITAL ECONOMY: AN OVERVIEW 1

Distr.: General 5 October 2017 Original: English Committee of Experts on International Cooperation in Tax Matters Fifteenth session Geneva, 17-20 October 2017 Agenda item 5(c)(ix) Tax consequences of the

Distr.: General 5 October 2017 Original: English Committee of Experts on International Cooperation in Tax Matters Fifteenth session Geneva, 17-20 October 2017 Agenda item 5(c)(ix) Tax consequences of the

EU Anti-Tax Avoidance Directive 2: hybrid mismatches with third countries

EU Anti-Tax Avoidance Directive 2: hybrid mismatches with third countries On February 21, 2017 the EU Member States reached agreement on a Directive that will amend the Anti-Tax Avoidance Directive (Council

EU Anti-Tax Avoidance Directive 2: hybrid mismatches with third countries On February 21, 2017 the EU Member States reached agreement on a Directive that will amend the Anti-Tax Avoidance Directive (Council

Three Smart Ways to Raise More Revenue

Three Smart Ways to Raise More Revenue Brief to House of Commons Finance Committee Pre-Budget Consultations in Advance of the 2017 Budget From Canadians for Tax Fairness August 2016 The federal government

Three Smart Ways to Raise More Revenue Brief to House of Commons Finance Committee Pre-Budget Consultations in Advance of the 2017 Budget From Canadians for Tax Fairness August 2016 The federal government

Taxing the Digital Economy: CIT and VAT

School of Law Taxing the Digital Economy: CIT and VAT RITA DE LA FERIA Professor of Tax Law, University of Leeds Global Tax 50 2015 and 2016 Outstanding Woman in Tax 2016 6 December 2017 Taxation in the

School of Law Taxing the Digital Economy: CIT and VAT RITA DE LA FERIA Professor of Tax Law, University of Leeds Global Tax 50 2015 and 2016 Outstanding Woman in Tax 2016 6 December 2017 Taxation in the

INDIA IMPORTANT CORPORATE TAX UPDATES

INDIA IMPORTANT CORPORATE TAX UPDATES Introduction Reducing tax litigation has been a key focus area for the Modi government. Several initiatives have been taken by the Central Board of Direct Taxes (the

INDIA IMPORTANT CORPORATE TAX UPDATES Introduction Reducing tax litigation has been a key focus area for the Modi government. Several initiatives have been taken by the Central Board of Direct Taxes (the

C(C)CTB 28 February CORIT

CTB 28 February CORIT") C(C)CTB 28 February 2017 Agenda Introduction Determination of the tax base Anti tax avoidance legislation Consolidation and allocation One-stop-shop Political and practical perspectives Introduction Challenges

C(C)CTB 28 February 2017 Agenda Introduction Determination of the tax base Anti tax avoidance legislation Consolidation and allocation One-stop-shop Political and practical perspectives Introduction Challenges

Action 8 Assure that transfer pricing outcomes are in in line with value creation

Action 8 Assure that transfer pricing outcomes are in in line with value creation Aim is to ensure that the attribution of value for tax purposes is consistent with economic activity generating that value.

Action 8 Assure that transfer pricing outcomes are in in line with value creation Aim is to ensure that the attribution of value for tax purposes is consistent with economic activity generating that value.

Study on Structures of Aggressive Tax Planning and Indicators

Study on Structures of Aggressive Tax Planning and Indicators Platform for Tax Good Governance 15 March 2016 Gaëtan Nicodème Context Fair and efficient corporate tax system: priority of the Commission

Study on Structures of Aggressive Tax Planning and Indicators Platform for Tax Good Governance 15 March 2016 Gaëtan Nicodème Context Fair and efficient corporate tax system: priority of the Commission

Proposal for a COUNCIL DIRECTIVE. laying down rules relating to the corporate taxation of a significant digital presence

EUROPEAN COMMISSION Brussels, XXX COM(2018) 147 2018/0072 (CNS) Proposal for a COUNCIL DIRECTIVE laying down rules relating to the corporate taxation of a significant digital presence {SWD(2018) 81} -

EUROPEAN COMMISSION Brussels, XXX COM(2018) 147 2018/0072 (CNS) Proposal for a COUNCIL DIRECTIVE laying down rules relating to the corporate taxation of a significant digital presence {SWD(2018) 81} -

Transfer pricing of intangibles

32E30000 - Tax Planning of International Enterprises Transfer pricing of intangibles Aalto BIZ / May 2, 2016 Petteri Rapo Alder & Sound Mannerheimintie 16 A FI-00100 Helsinki firstname.lastname@aldersound.fi

32E30000 - Tax Planning of International Enterprises Transfer pricing of intangibles Aalto BIZ / May 2, 2016 Petteri Rapo Alder & Sound Mannerheimintie 16 A FI-00100 Helsinki firstname.lastname@aldersound.fi

ADDRESSING THE TAX CHALLENGES OF THE DIGITALISATION OF THE ECONOMY

Base Erosion and Profit Shifting Project Public Consultation Document ADDRESSING THE TAX CHALLENGES OF THE DIGITALISATION OF THE ECONOMY 13 February 6 March 2019 OECD/G20 Base Erosion and Profit Shifting

Base Erosion and Profit Shifting Project Public Consultation Document ADDRESSING THE TAX CHALLENGES OF THE DIGITALISATION OF THE ECONOMY 13 February 6 March 2019 OECD/G20 Base Erosion and Profit Shifting

IBFD Course Programme Current Issues in International Tax Planning

IBFD Course Programme Current Issues in International Tax Planning Amsterdam, 14 16 June 2017 Summary This intermediate-level course provides participants with an in-depth understanding of the current

IBFD Course Programme Current Issues in International Tax Planning Amsterdam, 14 16 June 2017 Summary This intermediate-level course provides participants with an in-depth understanding of the current

Council of the European Union Brussels, 30 November 2017 (OR. en)

") Council of the European Union Brussels, 30 November 2017 (OR. en) 15175/17 FISC 320 ECOFIN 1064 'A' ITEM NOTE From: To: General Secretariat of the Council Council No. prev. doc.: 14843/17 Subject: Council

Council of the European Union Brussels, 30 November 2017 (OR. en) 15175/17 FISC 320 ECOFIN 1064 'A' ITEM NOTE From: To: General Secretariat of the Council Council No. prev. doc.: 14843/17 Subject: Council

Transfer Pricing Perspectives: The new normal: full TransParency. The post BEPS world in the automotive industry

The post BEPS world in the automotive industry 43 The automotive industry has followed a global footprint strategy since many years and it represents now the industry with the highest cross border intercompany

The post BEPS world in the automotive industry 43 The automotive industry has followed a global footprint strategy since many years and it represents now the industry with the highest cross border intercompany

Business sets out key principles for digital tax measures

Media Release Business sets out key principles for digital tax measures Paris, 21 st January 2019 Business at OECD has released a list of eleven principles for designing digital tax measures. At this crucial

Media Release Business sets out key principles for digital tax measures Paris, 21 st January 2019 Business at OECD has released a list of eleven principles for designing digital tax measures. At this crucial

The European Commission s Case. Kelly Stricklin-Coutinho Barrister, 39 Essex Chambers Visiting Lecturer, King s College London

The European Commission s Case Kelly Stricklin-Coutinho Barrister, 39 Essex Chambers Visiting Lecturer, King s College London Justified? Tax sovereignty Conflict as to new principle Retroactivity Legal

The European Commission s Case Kelly Stricklin-Coutinho Barrister, 39 Essex Chambers Visiting Lecturer, King s College London Justified? Tax sovereignty Conflict as to new principle Retroactivity Legal

BEPS Beyond Fortune 1000 October Armanino LLP amllp.com Armanino LLP amllp.com

BEPS Beyond Fortune 1000 October 2016 1 Armanino LLP amllp.com Armanino LLP amllp.com 1 BEPS Overview Timeline Pre-2013 - Organization for Economic Cooperation and Development (OECD) concern that existing

BEPS Beyond Fortune 1000 October 2016 1 Armanino LLP amllp.com Armanino LLP amllp.com 1 BEPS Overview Timeline Pre-2013 - Organization for Economic Cooperation and Development (OECD) concern that existing

Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

Re: USCIB Comments on HM Treasury s position paper on Corporate Tax and the Digital Economy

January 30, 2018 VIA EMAIL Timothy Power Deputy Director, Corporate Tax Team HM Treasury 1 Horse Guards Road London SW1A 2HQ digitalpaper@hmtreasury.gsi.gov.uk Re: USCIB Comments on HM Treasury s position

January 30, 2018 VIA EMAIL Timothy Power Deputy Director, Corporate Tax Team HM Treasury 1 Horse Guards Road London SW1A 2HQ digitalpaper@hmtreasury.gsi.gov.uk Re: USCIB Comments on HM Treasury s position

1. OECD publishes 77 comments on transfer pricing guidelines for intra-group services, dispute resolution

1. OECD publishes 77 comments on transfer pricing guidelines for intra-group services, dispute resolution The OECD published 77 responses to its request for suggestions on how to improve the OECD transfer

1. OECD publishes 77 comments on transfer pricing guidelines for intra-group services, dispute resolution The OECD published 77 responses to its request for suggestions on how to improve the OECD transfer

Planning for Intangible Property Migration in an Uncertain Environment. ABA Section of Taxation Mid Year Meeting January 25, 2013

Planning for Intangible Property Migration in an Uncertain Environment ABA Section of Taxation Mid Year Meeting January 25, 2013 1 Presenters Moderator Kenneth Christman, Ernst &Young Panelists Chris Bello,

Planning for Intangible Property Migration in an Uncertain Environment ABA Section of Taxation Mid Year Meeting January 25, 2013 1 Presenters Moderator Kenneth Christman, Ernst &Young Panelists Chris Bello,

Challenges of the U.S. and Mexico tax systems with regards to the cross-border digital economy. Dra. Lillian Sumi Imaoka

Challenges of the U.S. and Mexico tax systems with regards to the cross-border digital economy Dra. Lillian Sumi Imaoka Antilles Holding For Tax Administrations Digital Economy is not a single-industry

Challenges of the U.S. and Mexico tax systems with regards to the cross-border digital economy Dra. Lillian Sumi Imaoka Antilles Holding For Tax Administrations Digital Economy is not a single-industry

Developments in Europe Impact on US MNEs

Impact on US MNEs Tino Duttiné Partner - Frankfurt Norton Rose Fulbright LLP 8 May 2018 Todd Schroeder Partner - Dallas Norton Rose Fulbright (US) LLP Topics Introduction Update on State Aid Anti-Tax Avoidance

Impact on US MNEs Tino Duttiné Partner - Frankfurt Norton Rose Fulbright LLP 8 May 2018 Todd Schroeder Partner - Dallas Norton Rose Fulbright (US) LLP Topics Introduction Update on State Aid Anti-Tax Avoidance

The OECD s interim report on tax challenges arising from digitalisation: An overview

20 March 2018 Global Tax Alert The OECD s interim report on tax challenges arising from digitalisation: An overview EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax

20 March 2018 Global Tax Alert The OECD s interim report on tax challenges arising from digitalisation: An overview EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax