Econ 2230: Public Economics. Lecture 21: Subsidizing giving

|

|

|

- Spencer Wells

- 6 years ago

- Views:

Transcription

1 Econ 2230: Public Economics Lecture 21: Subsidizing giving

2 Subsidizing charitable giving 1. Tax subsidy a) Characterizing the US deduction for charitable donations b) Optimal subsidy c) Intended and unintended consequences d) Price elasticity of giving e) Salience 2. Matching a. Difference between subsidy versus match b. Price elasticity of giving g under match c. Reconciling response from experimental and non-experimental data

3 1a. Tax subsidy for charitable giving Deductions of charitable giving: Individuals can deduct the value of contributions to non-profits Gifts of property are deductible but services are not Deductions can not exceed 50% of adjusted gross income Deduction only given to those who itemize One of the largest tax expenditures of the US government 2005 deductions of nearly $200 billion

4

5 1a. Tax subsidy for charitable giving Why provide deductions for charitable giving? Positive externalities associated with charitable giving. Can reduce problem by offering a subsidy Enables government support to organizations that they otherwise are prevented from supporting What is the government funding through the subsidy?

6

7

8 1.b. Subsidizing charitable giving Theoretical questions: Should we have such a subsidy? How large should such a subsidy be? What are the key determinants of the optimal subsidy? Saez (2004): Optimal level of subsidies depends on four factors: 1. The price elasticity of the contribution good; the optimal subsidy should rise with the price elasticity 2. Size of externality associated with provision ( particularly important for public goods the government cannot fund) 3. Crowding out: subsidy should be greater for goods for which private donations are crowded out by ypublic provision 4. Redistribution: contributions concentrated at the bottom of the income distribution should be subsidized more heavily than those concentrated at the top

9

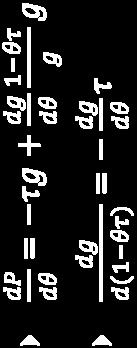

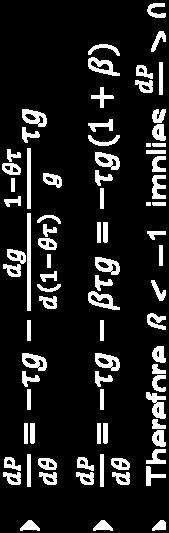

10 One public good

11 Optimal subsidy Suppose two public goods: private donations fund one, government revenue funds another public good Subsidy may be justifiable if external benefit of privately funded d charity exceed those of the public good provided by the government Equivalent to saying marginal value of charitable good (λ) greater than public good Criteria: 1. λ - externality of provision 2. β - price elasticity of giving 3. Crowding out 4. Redistribution 5. Other factors?

12 1.c. Unintended consequences Is it sufficient to consider the response in giving? Gruber (2004) Pay or pray? The impact of charitable subsidies on religious attendance Examine effect of subsidy on religiosity (giving and participation) Justification for religious subsidy Religious organizations provide transfers to low income Provide low income an opportunity to attend religious services Government prevented from direct support How does the tax subsidy influence giving and religious participation? If subsidy decreases attendance then may reduce the externalities the subsidy was thought to have.

13 1.c. Unintended consequences (Gruber, 2004) Theory: giving and attending Substitutes (Azzi and Ehrenber, 1975) Individuals id allocate resources between religious i and secular commodities to maximize lifetime and afterlife utility Complements Need to attend to give. Warm glow relies on visibility Empirical evidence: Complements: positive correlation between attendance and contributions (e.g., Olson and Caddell,1994). Omitted variable? Substitutes: United Church of Christ congregations, the congregations with the highest per capita financial giving were the congregations that were losing members most rapidly (Olson and Caddell,1994). Omitted variable?

14 1.c. Unintended consequences (Gruber, 2004) Theory: giving and attending Substitutes (Azzi and Ehrenber, 1975) Individuals allocate resources between religious and secular commodities to maximize lifetime and afterlife utility Complements Need to attend to give. Warm glow relies on visibility Empirical evidence: Complements: positive correlation between attendance and contributions (e.g., Olson and Caddell,1994). Omitted variable? more religious more likely to attend and give Substitutes: United Church of Christ congregations, the congregations with the highest h per capita financial i giving i were the congregations that were losing members most rapidly (Olson and Caddell,1994). Omitted variable? natural life cycle, those that remain are those most dedicated.

15 1.c. Unintended consequences (Gruber, 2004) Exploit variation in the subsidization over time, across income groups, across states to identify effect of subsidy on giving and attending General Social Survey, nationally representative sample since 1972, on religious attendance Consumer Expenditure Survery (CEX) nationally representative sample on giving activity TAXSIM to calculate cu ate deductions (It allows one to calculate cu ate federal and state income tax liabilities from survey data)

16 Gruber (2004) finding

17 Gruber (2004) finding

18

19 1.c. Unintended consequences Gruber (2004) 1% increase in religious giving decreases religious participation by 1.1% Crucial to evaluate the overall welfare effects of extending deductions to religious giving May not be sufficient to examine price elasticity if the objective is to achieve certain external effects

20 1.d. How responsive is giving to the price of giving? Prince and File 1994, survey of 200 big donors awareness of tax advantages was ranked the third most important motivator for making a charitable donation Aggregate data despite substantial changes in the marginal tax rates during the 1980's the share of income donated remained fairly constant. suggest little if any response to price changes. Look at subgroups: Look at those for whom the price of giving increased and those for whom it decreased

21 1.d. Are deductions treasury efficient? β=-1 1 Cross-sectional data: Existing studies have estimated price elasticity β and γ income elasticity log(g) = α + β log(1 - t) + γ log y + ε Cross sectional results γ = 0.8, β = (Feldstein and Taylor 1976, Clotfelter 1985) General cross sectional results <β β < Problem with cross sectional data?

22 1.d. Are deductions treasury efficient? β=-1 1 Cross-sectional data: Existing studies have estimated price elasticity β and γ income elasticity log(g) = α + β log(1 - t) + γ log y + ε Cross sectional results γ = 0.8, β = (Feldstein and Taylor 1976, Clotfelter 1985) General cross sectional results <β β < Problem with cross sectional data? difficult to separately identify the effect of changes in income from that of prices. Since the marginal tax rate increases with income, one cannot determine whether a positive correlation between giving and income is caused by people giving more when they face a higher h income or when they face a lower price.

23 1.d. Are deductions treasury efficient? β=-1 1 Panel data: Randolph (1995): 10-year panel of tax-return data : period with two major tax reforms Income elasticity: larger in the long-term than in the short-term. Limited response to temporary changes in income Price elasticity: donors time their giving to take advantage of temporary changes in the tax prices, whereas permanent changes in price have a small effect. Finds short-term term elasticities: 1.2; long-term elasticities: Concern that tax incentives merely affect the timing of giving rather than, as intended, the level of giving.

24 1.d. Are deductions treasury efficient? β=-1 1 Auten, Sieg and Clotfelter (2002) use a similar (although longer) panel of tax payers, but employ a different estimation technique. Analysis capitalizes on restrictions placed on the covariance matrices of income and price by assumptions of the permanent income hypothesis Confirm finding that the permanent income elasticity exceeds that of the temporary one. Permanent price elasticity of (very small temporary effect)

25 1.d. Are deductions treasury efficient? β=-1 1 Bakija and Heim (2010) Follow on strand on papers trying to account for anticipated permanent changes in tax law. This literature typically finds small persistent price elasticities and larger transitory price elasticities, but with wide confidence intervals. Panel of over 550,000 disproportionately high-income tax returns ( ) Deals with expectations; allowing people at different income levels to have different degrees responsiveness to taxation and different time paths of unobservable influences on giving Permanent price elasticity 0.7

26 1.d. Are deductions treasury efficient? β=-1 1 The sensitivity of the estimates to the estimation technique and the identification strategy has left the literature unsettled as to the true values of price and income elasticities iti Are there ways in which we could increase response to the subsidy? Is the deduction salient?

27 1.e. Salience Response to taxes and subsidies depend on how salient they are People are not fully aware of the taxes they face? Chetty, Looney, and Kroft (2009) test this assumption and generalize theory to allow for salience effects Test whether salience (visibility of tax-inclusive price) affects behavioral responses to commodity taxation Does effect of a tax on demand depend on whether it is included in posted price? Experiment Non-experimental data

28 Chetty, Looney, and Kroft (2009) Experiment manipulating salience of sales tax implemented at a supermarket that belongs to a major grocery chain 30% of products sold in store are subject to sales tax Posted tax-inclusive prices on shelf for subset of products subject to sales tax (7.375% in this city) Data: Scanner data on price and weekly quantity sold by product

29

30 Classroom survey Individuals are aware of the magnitude of the sales tax Students were asked to choose two items from image Asked to report Total bill due at the register for these two items

31 Field experiment Quasi-experimental difference-in-differences Treatment group: Products: Cosmetics, Deodorants, and Hair Care Accessories (relatively high price and high price elasticity) Store: One large store in Northern California Time period: 3 weeks (February 22, March 15, 2006) Control groups: Products: Other prods. in same aisle (toothpaste, skin care, shave) of the store Stores: same products at two nearby stores similar in demographic characteristics Time period: prior to intervention calendar year 2005 and first 6 weeks of 2006

32 Chetty, Looney, and Kroft (2009)

33 Chetty, Looney, and Kroft (2009) Experimental period Period prior to experiment

34 Chetty, Looney, and Kroft (2009) Sale of non treatment products increased by 0.8 units during treatment Experimental period Period prior to experiment

35 Chetty, Looney, and Kroft (2009)

36 Chetty, Looney, and Kroft (2009)

37 Chetty, Looney, and Kroft (2009)

38 Chetty, Looney, and Kroft (2009)

39 Chetty, Looney, and Kroft (2009)

40 Chetty, Looney, and Kroft (2009) Evaluate response Posting tax inclusive prices decreases demand by 8% Price elasticity of demand range from 1 to 1.5 Tax-inclusive price reduced demand by nearly same amount as a percent price increase Vast majority of customers do not take sales tax into account Non-experimental data Compare effects of price changes and tax changes Alcohol subject to two state-level taxes in the U.S.: Excise tax: included in price Sales tax: added at register, not shown in posted price Exploiting state-level changes in these two taxes

41 Chetty, Looney, and Kroft (2009)

42 Chetty, Looney, and Kroft (2009)

43 Chetty and Saez, 2009 Salience of income taxation Examine Earned Income Tax Credit (EITC) The EITC is the largest cash transfer program for low income families in the United States and it generates large marginal subsidies or taxes on the earnings of recipients. A refundable tax credit primarily for individuals and couples with qualifying children. For tax year 2010: maximum EIC for a person or couple without qualifying children is $457 with one qualifying child is $3,050 with two qualifying children is $5,036 with three or more qualifying children is $5,666

44

45 Chetty and Saez, H&R Block offices in Chicago metro area; 43,000 EITC clients 1,461 tax professionals implemented experiment Tax Season 2007: Jan. 1 to April 15, 2007 EITC clients randomly assigned to control or treatment group Control group: standard tax preparation procedure Only mentions the EITC amount, with no info on EITC structure Treatment

46

47

48

49

50 One potential explanation for this response is that the non-compliers are tax professionals who framed the EITC incentive effects as being small relative to the benefits of earning a higher income

51 1.e. Salience Salience plays a key role in determining response to taxation or subsidies Accounting for the limited salience Thaler and Sunstein (2008) propose a Charity Debit Card Can be used only for charitable donations Provides statement on deduction Summary statement sent straight to IRS for deductions One way of determining response to salient tax deductions is the lab

52 2. Matching Government provided incentives typically provided in the form of deductions. Private incentives in the form of matches Experimental evidence typically examine matches. Attraction is that cost salient in experimental studies a. Are rebates and subsidies equivalent? Eckel and Grossman (2003) b. How does the magnitude of the match influence giving? Meier (2007) Karlan and List (2007), Karlan, List, and Shafir (2010) c. Reconciling evidence from experimental and non-experimental data

53 Next: Matching Groups: Norms, Institutions and sorting: Elinor Ostrom, Governing the Commons,, chapter 3, Governing the Commons: The Evolution of Institutions for Collective Action Theodore Bergstrom, The Uncommon Insight of Elinor Ostrom, Scandinavian Journal of Economics, 2010 Ahn, T.K., Mark Isaac and Timothy C. Salmon. Coming and Going: Experiments on Endogenous Group Sizes for Excludable Public Goods. Journal of Public Economics, Vol. 93, No. 1-2 (2009): Ahn, T.K., Mark Isaac and Timothy C. Salmon.Endogenous Group Formation, Journal of Public Economic Theory, Vol 10. No. 2 (2008) Sutter, Matthias, Stefan D. Haigner, and Martin G. Kocher Choosing the Carrot or the Stick? Endogenous Institutional Choice in Social Dilemma Situations. Cinyabuguma, Matthias, Talbot Page, and Louis Putterman Cooperation under the Threat of Expulsion in a Public Goods Experiment. Journal of Public Economics, 89: Ehrhart, Karl-Martin, and Claudia Keser Mobility and Cooperation: On the Run. Gürerk, Özgür, Bernd Irlenbusch, and Bettina Rockenbach The Competitive Advantage of Sanctioning Institutions. Science, 312(5770):

Chetty, Looney, and Kroft Salience and Taxation: Theory and Evidence Amy Finkelstein E-ZTax: Tax Salience and Tax Rates

LECTURE: TAX SALIENCE AND BEHAVIORAL PUBLIC FINANCE HILARY HOYNES UC DAVIS EC230 Papers: Chetty, Looney, and Kroft Salience and Taxation: Theory and Evidence Amy Finkelstein E-ZTax: Tax Salience and Tax

LECTURE: TAX SALIENCE AND BEHAVIORAL PUBLIC FINANCE HILARY HOYNES UC DAVIS EC230 Papers: Chetty, Looney, and Kroft Salience and Taxation: Theory and Evidence Amy Finkelstein E-ZTax: Tax Salience and Tax

WORKING PAPER SERIES

March 2010 No.3 The Price Elasticity of Charitable Giving: Does the Form of Tax Relief Matter? Prof Kimberley Scharf (Warwick) and Dr Sarah Smith (Bristol) WORKING PAPER SERIES Centre for Competitive Advantage

March 2010 No.3 The Price Elasticity of Charitable Giving: Does the Form of Tax Relief Matter? Prof Kimberley Scharf (Warwick) and Dr Sarah Smith (Bristol) WORKING PAPER SERIES Centre for Competitive Advantage

Sarah K. Burns James P. Ziliak. November 2013

Sarah K. Burns James P. Ziliak November 2013 Well known that policymakers face important tradeoffs between equity and efficiency in the design of the tax system The issue we address in this paper informs

Sarah K. Burns James P. Ziliak November 2013 Well known that policymakers face important tradeoffs between equity and efficiency in the design of the tax system The issue we address in this paper informs

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings Raj Chetty, Harvard and NBER John N. Friedman, Harvard and NBER Emmanuel Saez, UC Berkeley and NBER April

Using Differences in Knowledge Across Neighborhoods to Uncover the Impacts of the EITC on Earnings Raj Chetty, Harvard and NBER John N. Friedman, Harvard and NBER Emmanuel Saez, UC Berkeley and NBER April

The impact of charitable subsidies on religious giving and attendance: Evidence from panel data

The impact of charitable subsidies on religious giving and attendance: Evidence from panel data April 17, 2012 Abstract In the United States, charitable contributions can be deducted from taxable income

The impact of charitable subsidies on religious giving and attendance: Evidence from panel data April 17, 2012 Abstract In the United States, charitable contributions can be deducted from taxable income

The Impact of Taxation on Charitable Giving

The Impact of Taxation on Charitable Giving Leora Friedberg and Tianying He University of Virginia March 2015 We are grateful to Murat Demirci, Don Fullerton, John Pepper, Bruce Reynolds, and Sarah Turner

The Impact of Taxation on Charitable Giving Leora Friedberg and Tianying He University of Virginia March 2015 We are grateful to Murat Demirci, Don Fullerton, John Pepper, Bruce Reynolds, and Sarah Turner

HOW DOES CHARITABLE GIVING RESPOND TO INCENTIVES AND INCOME? NEW ESTIMATES FROM PANEL DATA. Jon Bakija and Bradley T. Heim

National Tax Journal, June 2011, 64 (2, Part 2), 615 650 HOW DOES CHARITABLE GIVING RESPOND TO INCENTIVES AND INCOME? NEW ESTIMATES FROM PANEL DATA Jon Bakija and Bradley T. Heim We estimate the elasticity

National Tax Journal, June 2011, 64 (2, Part 2), 615 650 HOW DOES CHARITABLE GIVING RESPOND TO INCENTIVES AND INCOME? NEW ESTIMATES FROM PANEL DATA Jon Bakija and Bradley T. Heim We estimate the elasticity

Julio Videras Department of Economics Hamilton College

LUCK AND GIVING Julio Videras Department of Economics Hamilton College Abstract: This paper finds that individuals who consider themselves lucky in finances donate more than individuals who do not consider

LUCK AND GIVING Julio Videras Department of Economics Hamilton College Abstract: This paper finds that individuals who consider themselves lucky in finances donate more than individuals who do not consider

Capital Gains Realizations of the Rich and Sophisticated

Capital Gains Realizations of the Rich and Sophisticated Alan J. Auerbach University of California, Berkeley and NBER Jonathan M. Siegel University of California, Berkeley and Congressional Budget Office

Capital Gains Realizations of the Rich and Sophisticated Alan J. Auerbach University of California, Berkeley and NBER Jonathan M. Siegel University of California, Berkeley and Congressional Budget Office

Salience and Taxation: Evidence and Policy Implications

Salience and Taxation: Evidence and Policy Implications Testimony for the Committee of Finance United States Senate Hearing on How Do Complexity, Uncertainty and Other Factors Impact Responses to Tax Incentives?

Salience and Taxation: Evidence and Policy Implications Testimony for the Committee of Finance United States Senate Hearing on How Do Complexity, Uncertainty and Other Factors Impact Responses to Tax Incentives?

Tax Incidence January 22, 2015

Tax ncidence January 22, 2015 The Question deally: Howtaxesaffectthewelfarefordifferentindividuals; how is the burden of taxation distributed among individuals? Practically: Which group (sellers-buyers,

Tax ncidence January 22, 2015 The Question deally: Howtaxesaffectthewelfarefordifferentindividuals; how is the burden of taxation distributed among individuals? Practically: Which group (sellers-buyers,

Empirical public economics (31.3, 7.4, seminar questions) Thor O. Thoresen, room 1125, Friday

Thor O. Thoresen, room 1125, Friday") 1 Empirical public economics (31.3, 7.4, seminar questions) Thor O. Thoresen, room 1125, Friday 10-11 tot@ssb.no, t.o.thoresen@econ.uio.no 1 Reading Thor O. Thoresen & Trine E. Vattø (2015). Validation

1 Empirical public economics (31.3, 7.4, seminar questions) Thor O. Thoresen, room 1125, Friday 10-11 tot@ssb.no, t.o.thoresen@econ.uio.no 1 Reading Thor O. Thoresen & Trine E. Vattø (2015). Validation

Taxation of Earnings and the Impact on Labor Supply and Human Capital. Discussion by Henrik Kleven (LSE)

") Taxation of Earnings and the Impact on Labor Supply and Human Capital Discussion by Henrik Kleven (LSE) The Empirical Foundations of Supply Side Economics The Becker Friedman Institute, September 2013

Taxation of Earnings and the Impact on Labor Supply and Human Capital Discussion by Henrik Kleven (LSE) The Empirical Foundations of Supply Side Economics The Becker Friedman Institute, September 2013

Julia Bredtmann RWI, and IZA, Germany. Cons. Pros. Keywords: private philanthropy, time and money donations, government spending, crowding out

Julia Bredtmann RWI, and IZA, Germany Does government spending crowd out voluntary labor and donations? There is little evidence that government spending crowds out private charitable donations of time

Julia Bredtmann RWI, and IZA, Germany Does government spending crowd out voluntary labor and donations? There is little evidence that government spending crowds out private charitable donations of time

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics

Henrik Jacobsen Kleven London School of Economics") LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

LABOR SUPPLY RESPONSES TO TAXES AND TRANSFERS: PART I (BASIC APPROACHES) Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Finance (EC426): Lent 2013 AGENDA Efficiency cost

1 Excess burden of taxation

1 Excess burden of taxation 1. In a competitive economy without externalities (and with convex preferences and production technologies) we know from the 1. Welfare Theorem that there exists a decentralized

1 Excess burden of taxation 1. In a competitive economy without externalities (and with convex preferences and production technologies) we know from the 1. Welfare Theorem that there exists a decentralized

THE DESIGN OF THE INDIVIDUAL ALTERNATIVE

00 TH ANNUAL CONFERENCE ON TAXATION CHARITABLE CONTRIBUTIONS UNDER THE ALTERNATIVE MINIMUM TAX* Shih-Ying Wu, National Tsing Hua University INTRODUCTION THE DESIGN OF THE INDIVIDUAL ALTERNATIVE minimum

00 TH ANNUAL CONFERENCE ON TAXATION CHARITABLE CONTRIBUTIONS UNDER THE ALTERNATIVE MINIMUM TAX* Shih-Ying Wu, National Tsing Hua University INTRODUCTION THE DESIGN OF THE INDIVIDUAL ALTERNATIVE minimum

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income Hilary Hoynes, UC Berkeley Ankur Patel US Treasury April 2015 Overview The U.S. social safety net for

Effective Policy for Reducing Inequality: The Earned Income Tax Credit and the Distribution of Income Hilary Hoynes, UC Berkeley Ankur Patel US Treasury April 2015 Overview The U.S. social safety net for

Hilary Hoynes UC Davis EC230. Taxes and the High Income Population

Hilary Hoynes UC Davis EC230 Taxes and the High Income Population New Tax Responsiveness Literature Started by Feldstein [JPE The Effect of MTR on Taxable Income: A Panel Study of 1986 TRA ]. Hugely important

Hilary Hoynes UC Davis EC230 Taxes and the High Income Population New Tax Responsiveness Literature Started by Feldstein [JPE The Effect of MTR on Taxable Income: A Panel Study of 1986 TRA ]. Hugely important

Summary The Administration s 2010 and 2011 budget outlines contain a proposal to cap the value of itemized deductions at 28%, for high-income taxpayer

Charitable Contributions: The Itemized Deduction Cap and Other FY2011 Budget Options Jane G. Gravelle Senior Specialist in Economic Policy Donald J. Marples Specialist in Public Finance March 18, 2010

Charitable Contributions: The Itemized Deduction Cap and Other FY2011 Budget Options Jane G. Gravelle Senior Specialist in Economic Policy Donald J. Marples Specialist in Public Finance March 18, 2010

THE EFFECT OF THE CAPITAL GAINS TAX ON DONATIONS OF CASH AND APPRECIATED ASSETS

THE EFFECT OF THE CAPITAL GAINS TAX ON DONATIONS OF CASH AND APPRECIATED ASSETS A Thesis submitted to the Faculty of the Graduate School of Arts & Sciences of Georgetown University in partial fulfillment

THE EFFECT OF THE CAPITAL GAINS TAX ON DONATIONS OF CASH AND APPRECIATED ASSETS A Thesis submitted to the Faculty of the Graduate School of Arts & Sciences of Georgetown University in partial fulfillment

Lecture 3: Tax Incidence and Efficiency Costs of Taxation

1 50 Lecture 3: Tax Incidence and Efficiency Costs of Taxation Stefanie Stantcheva Fall 2017 19.1 Tax Incidence C H A P T E R 1 9 T H E E Q U I T Y I M P L I C A T I O N S O F T A X A T I O N : T A X

1 50 Lecture 3: Tax Incidence and Efficiency Costs of Taxation Stefanie Stantcheva Fall 2017 19.1 Tax Incidence C H A P T E R 1 9 T H E E Q U I T Y I M P L I C A T I O N S O F T A X A T I O N : T A X

Nudges and Learning: Evidence from Informational Interventions for Low-Income Taxpayers

Nudges and Learning: Evidence from Informational Interventions for Low-Income Taxpayers Day Manoli UT-Austin & NBER Nick Turner US Treasury January 2016 Abstract Can one-time informational interventions

Nudges and Learning: Evidence from Informational Interventions for Low-Income Taxpayers Day Manoli UT-Austin & NBER Nick Turner US Treasury January 2016 Abstract Can one-time informational interventions

The model is estimated including a fixed effect for each family (u i ). The estimated model was:

. The estimated model was:") 1. In a 1996 article, Mark Wilhelm examined whether parents bequests are altruistic. 1 According to the altruistic model of bequests, a parent with several children would leave larger bequests to children

1. In a 1996 article, Mark Wilhelm examined whether parents bequests are altruistic. 1 According to the altruistic model of bequests, a parent with several children would leave larger bequests to children

Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 29, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact Fatoumata

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 29, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact Fatoumata

Empirical Approaches in Public Finance. Hilary Hoynes EC230. Outline of Lecture:

Lecture: Empirical Approaches in Public Finance Hilary Hoynes hwhoynes@ucdavis.edu EC230 Outline of Lecture: 1. Statement of canonical problem a. Challenges for causal identification 2. Non-experimental

Lecture: Empirical Approaches in Public Finance Hilary Hoynes hwhoynes@ucdavis.edu EC230 Outline of Lecture: 1. Statement of canonical problem a. Challenges for causal identification 2. Non-experimental

The federal estate tax allows a deduction for every dollar

The Estate Tax and Charitable Bequests: Elasticity Estimates Using Probate Records The Estate Tax and Charitable Bequests: Elasticity Estimates Using Probate Records Abstract - This paper uses data from

The Estate Tax and Charitable Bequests: Elasticity Estimates Using Probate Records The Estate Tax and Charitable Bequests: Elasticity Estimates Using Probate Records Abstract - This paper uses data from

Jon Bakija Williams College Williamstown, MA

How Does Charitable Giving Respond to Incentives and Income? Panel Estimates with State Tax Identification, Predictable Tax Changes, and Heterogeneity by Income Jon Bakija Williams College Williamstown,

How Does Charitable Giving Respond to Incentives and Income? Panel Estimates with State Tax Identification, Predictable Tax Changes, and Heterogeneity by Income Jon Bakija Williams College Williamstown,

Nonprofit organizations are becoming a large and important

Nonprofit Taxable Activities, Production Complementarities, and Joint Cost Allocations Nonprofit Taxable Activities, Production Complementarities, and Joint Cost Allocations Abstract - Nonprofit organizations

Nonprofit Taxable Activities, Production Complementarities, and Joint Cost Allocations Nonprofit Taxable Activities, Production Complementarities, and Joint Cost Allocations Abstract - Nonprofit organizations

Closed book/notes exam. No computer, calculator, or any electronic device allowed.

Econ 131 Spring 2017 Emmanuel Saez Final May 12th Student Name: Student ID: GSI Name: Exam Instructions Closed book/notes exam. No computer, calculator, or any electronic device allowed. No phones. Turn

Econ 131 Spring 2017 Emmanuel Saez Final May 12th Student Name: Student ID: GSI Name: Exam Instructions Closed book/notes exam. No computer, calculator, or any electronic device allowed. No phones. Turn

TAX EXPENDITURES Fall 2012

TAX EXPENDITURES 14.471 - Fall 2012 1 Base-Broadening Strategies for Tax Reform: Eliminate Existing Deductions Retain but Scale Back Existing Deductions o Income-Related Clawbacks o Cap on Rate for Deductions

TAX EXPENDITURES 14.471 - Fall 2012 1 Base-Broadening Strategies for Tax Reform: Eliminate Existing Deductions Retain but Scale Back Existing Deductions o Income-Related Clawbacks o Cap on Rate for Deductions

Econ 551 Government Finance: Revenues Winter 2018

Econ 551 Government Finance: Revenues Winter 2018 Given by Kevin Milligan Vancouver School of Economics University of British Columbia Lecture 8c: Taxing High Income Workers ECON 551: Lecture 8c 1 of 34

Econ 551 Government Finance: Revenues Winter 2018 Given by Kevin Milligan Vancouver School of Economics University of British Columbia Lecture 8c: Taxing High Income Workers ECON 551: Lecture 8c 1 of 34

Peer Effects in Retirement Decisions

Peer Effects in Retirement Decisions Mario Meier 1 & Andrea Weber 2 1 University of Mannheim 2 Vienna University of Economics and Business, CEPR, IZA Meier & Weber (2016) Peers in Retirement 1 / 35 Motivation

Peer Effects in Retirement Decisions Mario Meier 1 & Andrea Weber 2 1 University of Mannheim 2 Vienna University of Economics and Business, CEPR, IZA Meier & Weber (2016) Peers in Retirement 1 / 35 Motivation

Labour Supply and Taxes

Labour Supply and Taxes Barra Roantree Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic how should

Labour Supply and Taxes Barra Roantree Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic how should

How Changes in Tax Rates Might Affect Itemized Charitable Deductions. The Center on Philanthropy at Indiana University March 2009

Executive Summary How Changes in Tax Rates Might Affect Itemized Charitable Deductions The Center on Philanthropy at Indiana University March 2009 President Obama s budget proposal for 2010 and beyond

Executive Summary How Changes in Tax Rates Might Affect Itemized Charitable Deductions The Center on Philanthropy at Indiana University March 2009 President Obama s budget proposal for 2010 and beyond

Empirical Evidence and Earnings Taxation:

Empirical Evidence and Earnings Taxation: Lessons from the Mirrlees Review ES World Congress August 2010 Richard Blundell University College London and Institute for Fiscal Studies Institute for Fiscal

Empirical Evidence and Earnings Taxation: Lessons from the Mirrlees Review ES World Congress August 2010 Richard Blundell University College London and Institute for Fiscal Studies Institute for Fiscal

Topic 1: Policy Design: Unemployment Insurance and Moral Hazard

Introduction Trade-off Optimal UI Empirical Topic 1: Policy Design: Unemployment Insurance and Moral Hazard Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 39 Introduction Trade-off

Introduction Trade-off Optimal UI Empirical Topic 1: Policy Design: Unemployment Insurance and Moral Hazard Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 39 Introduction Trade-off

Closed book/notes exam. No computer, calculator, or any electronic device allowed.

Econ 131 Spring 2017 Emmanuel Saez Final May 12th Student Name: Student ID: GSI Name: Exam Instructions Closed book/notes exam. No computer, calculator, or any electronic device allowed. No phones. Turn

Econ 131 Spring 2017 Emmanuel Saez Final May 12th Student Name: Student ID: GSI Name: Exam Instructions Closed book/notes exam. No computer, calculator, or any electronic device allowed. No phones. Turn

INTRODUCTION: ECONOMIC ANALYSIS OF TAX EXPENDITURES

National Tax Journal, June 2011, 64 (2, Part 2), 451 458 Introduction INTRODUCTION: ECONOMIC ANALYSIS OF TAX EXPENDITURES James M. Poterba Many economists and policy analysts argue that broadening the

National Tax Journal, June 2011, 64 (2, Part 2), 451 458 Introduction INTRODUCTION: ECONOMIC ANALYSIS OF TAX EXPENDITURES James M. Poterba Many economists and policy analysts argue that broadening the

TAXABLE INCOME RESPONSES. Henrik Jacobsen Kleven London School of Economics. Lecture Notes for MSc Public Economics (EC426): Lent Term 2014

: Lent Term 2014") TAXABLE INCOME RESPONSES Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Economics (EC426): Lent Term 2014 AGENDA The Elasticity of Taxable Income (ETI): concept and policy

TAXABLE INCOME RESPONSES Henrik Jacobsen Kleven London School of Economics Lecture Notes for MSc Public Economics (EC426): Lent Term 2014 AGENDA The Elasticity of Taxable Income (ETI): concept and policy

Empirical Evidence and Earnings Taxation: Lessons from the Mirrlees Review

Empirical Evidence and Earnings Taxation: Lessons from the Mirrlees Review EALE-SOLE June 2010 Richard Blundell University College London and Institute for Fiscal Studies Institute for Fiscal Studies Empirical

Empirical Evidence and Earnings Taxation: Lessons from the Mirrlees Review EALE-SOLE June 2010 Richard Blundell University College London and Institute for Fiscal Studies Institute for Fiscal Studies Empirical

ECON 4624 Income taxation 1/24

ECON 4624 Income taxation 1/24 Why is it important? An important source of revenue in most countries (60-70%) Affect labour and capital (savings) supply and overall economic activity how much depend on

ECON 4624 Income taxation 1/24 Why is it important? An important source of revenue in most countries (60-70%) Affect labour and capital (savings) supply and overall economic activity how much depend on

The Aggregate Implications of Regional Business Cycles

The Aggregate Implications of Regional Business Cycles Martin Beraja Erik Hurst Juan Ospina University of Chicago University of Chicago University of Chicago Fall 2017 This Paper Can we use cross-sectional

The Aggregate Implications of Regional Business Cycles Martin Beraja Erik Hurst Juan Ospina University of Chicago University of Chicago University of Chicago Fall 2017 This Paper Can we use cross-sectional

Strategic Timing of Charitable Giving

Strategic Timing of Charitable Giving Sara LaLumia Williams College December 3, 2016 DRAFT: Preliminary and incomplete. Abstract Gifts to charity are tax deductible for filers who itemize but not for filers

Strategic Timing of Charitable Giving Sara LaLumia Williams College December 3, 2016 DRAFT: Preliminary and incomplete. Abstract Gifts to charity are tax deductible for filers who itemize but not for filers

TAXES, TRANSFERS, AND LABOR SUPPLY. Henrik Jacobsen Kleven London School of Economics. Lecture Notes for PhD Public Finance (EC426): Lent Term 2012

: Lent Term 2012") TAXES, TRANSFERS, AND LABOR SUPPLY Henrik Jacobsen Kleven London School of Economics Lecture Notes for PhD Public Finance (EC426): Lent Term 2012 AGENDA Why care about labor supply responses to taxes and

TAXES, TRANSFERS, AND LABOR SUPPLY Henrik Jacobsen Kleven London School of Economics Lecture Notes for PhD Public Finance (EC426): Lent Term 2012 AGENDA Why care about labor supply responses to taxes and

Topic 2-3: Policy Design: Unemployment Insurance and Moral Hazard

Introduction Trade-off Optimal UI Empirical Topic 2-3: Policy Design: Unemployment Insurance and Moral Hazard Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 27 Introduction

Introduction Trade-off Optimal UI Empirical Topic 2-3: Policy Design: Unemployment Insurance and Moral Hazard Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 27 Introduction

The Impact of Taxes and Wasteful Government Spending on Giving

The Impact of Taxes and Wasteful Government Spending on Giving Roman M. Sheremeta a,b,* Neslihan Uler c,* a Weatherhead School of Management, Case Western Reserve University 11119 Bellflower Road, Cleveland,

The Impact of Taxes and Wasteful Government Spending on Giving Roman M. Sheremeta a,b,* Neslihan Uler c,* a Weatherhead School of Management, Case Western Reserve University 11119 Bellflower Road, Cleveland,

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS Joseph Rosenberg and Eugene Steuerle November 15, 2018 The federal tax treatment of charitable giving and the nonprofit sector

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS Joseph Rosenberg and Eugene Steuerle November 15, 2018 The federal tax treatment of charitable giving and the nonprofit sector

Taxation and International Migration of Superstars: Evidence from the European Football Market

Taxation and International Migration of Superstars: Evidence from the European Football Market Henrik Kleven (London School of Economics) Camille Landais (Stanford University) Emmanuel Saez (UC Berkeley)

Taxation and International Migration of Superstars: Evidence from the European Football Market Henrik Kleven (London School of Economics) Camille Landais (Stanford University) Emmanuel Saez (UC Berkeley)

C H A P T E R 1 9 T H E E Q U I T Y I M P L I C A T I O N S O F T A X A T I O N : T A X I N C I D E N C E

19.1 Tax Incidence C H A P T E R 1 9 T H E E Q U I T Y I M P L I C A T I O N S O F T A X A T I O N : T A X I N C I D E N C E Sources of federal government revenue, 1960 and 2008: Category: 1960 2008 Income

19.1 Tax Incidence C H A P T E R 1 9 T H E E Q U I T Y I M P L I C A T I O N S O F T A X A T I O N : T A X I N C I D E N C E Sources of federal government revenue, 1960 and 2008: Category: 1960 2008 Income

Volume 39, Issue 1. Tax Framing and Productivity: evidence based on the strategy elicitation

Volume 39, Issue 1 Tax Framing and Productivity: evidence based on the strategy elicitation Hamza Umer Graduate School of Economics, Waseda University Abstract People usually don't like to pay income tax

Volume 39, Issue 1 Tax Framing and Productivity: evidence based on the strategy elicitation Hamza Umer Graduate School of Economics, Waseda University Abstract People usually don't like to pay income tax

IGE: The State of the Literature

PhD Student, Department of Economics Center for the Economics of Human Development The University of Chicago setzler@uchicago.edu March 10, 2015 1 Literature, Facts, and Open Questions 2 Population-level

PhD Student, Department of Economics Center for the Economics of Human Development The University of Chicago setzler@uchicago.edu March 10, 2015 1 Literature, Facts, and Open Questions 2 Population-level

Public Economics. Lecture 4: Public goods and externalities. Marc Sangnier , Spring semester

Public Economics Lecture 4: Public goods and externalities Marc Sangnier marc.sangnier@univ-amu.fr 2012-2013, Spring semester Aix Marseille School of Economics 1 Introduction 2 Public goods 3 Externalities

Public Economics Lecture 4: Public goods and externalities Marc Sangnier marc.sangnier@univ-amu.fr 2012-2013, Spring semester Aix Marseille School of Economics 1 Introduction 2 Public goods 3 Externalities

The Price Elasticity of Charitable Giving: Reconciliation of Disparate Literatures

The Price Elasticity of Charitable Giving: Toward a Reconciliation of Disparate Literatures Daniel M. Hungerman University of Notre Dame and National Bureau of Economic Research Mark Ottoni-Wilhelm IUPUI

The Price Elasticity of Charitable Giving: Toward a Reconciliation of Disparate Literatures Daniel M. Hungerman University of Notre Dame and National Bureau of Economic Research Mark Ottoni-Wilhelm IUPUI

A Course in Environmental Economics: Theory, Policy, and Practice. Daniel J. Phaneuf and Till Requate

1 A Course in Environmental Economics: Theory, Policy, and Practice PART I: ECONOMICS AND THE ENVIRONMENT Daniel J. Phaneuf and Till Requate 1. Introduction to the Theory of Externalities 1.1 Market failure

1 A Course in Environmental Economics: Theory, Policy, and Practice PART I: ECONOMICS AND THE ENVIRONMENT Daniel J. Phaneuf and Till Requate 1. Introduction to the Theory of Externalities 1.1 Market failure

Extrinsic and Intrinsic Motivations for Tax Compliance: Evidence from a Field Experiment in Germany

Extrinsic and Intrinsic Motivations for Tax Compliance: Evidence from a Field Experiment in Germany Nadja Dwenger (MPI) Henrik Kleven (LSE) Imran Rasul (UCL) Johannes Rincke (Erlangen-Nuremberg) October

Extrinsic and Intrinsic Motivations for Tax Compliance: Evidence from a Field Experiment in Germany Nadja Dwenger (MPI) Henrik Kleven (LSE) Imran Rasul (UCL) Johannes Rincke (Erlangen-Nuremberg) October

Department of Economics Course Outline

Department of Economics Course Outline Term: Winter 2013 Course: Economics 653 [Public Revenue Analysis] Section: 01 Time: MWF 9:00 9:50 Place: SS 423 Instructor: Dr. Kenneth J. McKenzie Office: SS 452

Department of Economics Course Outline Term: Winter 2013 Course: Economics 653 [Public Revenue Analysis] Section: 01 Time: MWF 9:00 9:50 Place: SS 423 Instructor: Dr. Kenneth J. McKenzie Office: SS 452

The price elasticity of charitable giving: does the form of tax relief matter?

Int Tax Public Finance (2015) 22:330 352 DOI 10.1007/s10797-014-9306-3 The price elasticity of charitable giving: does the form of tax relief matter? Kimberley Scharf Sarah Smith Received: 7 March 2013

Int Tax Public Finance (2015) 22:330 352 DOI 10.1007/s10797-014-9306-3 The price elasticity of charitable giving: does the form of tax relief matter? Kimberley Scharf Sarah Smith Received: 7 March 2013

Economics 230a, Fall 2014 Lecture Note 11: Capital Gains and Estate Taxation

Economics 230a, Fall 2014 Lecture Note 11: Capital Gains and Estate Taxation Two taxes that deserve special attention are those imposed on capital gains and estates. Capital Gains Taxation Capital gains

Economics 230a, Fall 2014 Lecture Note 11: Capital Gains and Estate Taxation Two taxes that deserve special attention are those imposed on capital gains and estates. Capital Gains Taxation Capital gains

The Elasticity of Taxable Income During the 1990s: A Sensitivity Analysis

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Economics Department Faculty Publications Economics Department 2006 The Elasticity of Taxable During the 1990s: A Sensitivity

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Economics Department Faculty Publications Economics Department 2006 The Elasticity of Taxable During the 1990s: A Sensitivity

EC989 Behavioural Economics. Sketch solutions for Class 2

EC989 Behavioural Economics Sketch solutions for Class 2 Neel Ocean (adapted from solutions by Andis Sofianos) February 15, 2017 1 Prospect Theory 1. Illustrate the way individuals usually weight the probability

EC989 Behavioural Economics Sketch solutions for Class 2 Neel Ocean (adapted from solutions by Andis Sofianos) February 15, 2017 1 Prospect Theory 1. Illustrate the way individuals usually weight the probability

More Giving or More Givers? The Effects of Tax Incentives on Charitable Donations in the UK

6591 2017 Original Version: July 2017 This Version: January 2018 More Giving or More Givers? The Effects of Tax Incentives on Charitable Donations in the UK Miguel Almunia, Benjamin Lockwood, Kimberley

6591 2017 Original Version: July 2017 This Version: January 2018 More Giving or More Givers? The Effects of Tax Incentives on Charitable Donations in the UK Miguel Almunia, Benjamin Lockwood, Kimberley

Russell Ackoff Doctoral Student Fellowship for Research on Human Decision Processes and Risk Management: 2014 Application

Russell Ackoff Doctoral Student Fellowship for Research on Human Decision Processes and Risk Management: 2014 Application Influence of Income tax Shalena Srna Doctoral Student Marketing Department, The

Russell Ackoff Doctoral Student Fellowship for Research on Human Decision Processes and Risk Management: 2014 Application Influence of Income tax Shalena Srna Doctoral Student Marketing Department, The

Labour Supply, Taxes and Benefits

Labour Supply, Taxes and Benefits William Elming Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic

Labour Supply, Taxes and Benefits William Elming Introduction Effect of taxes and benefits on labour supply a hugely studied issue in public and labour economics why? Significant policy interest in topic

Exam. ECON 4624 Empirical Public Economics. (a) Consider the budget contraint in Figure 1 below. What are the expected effects on

Consider the budget contraint in Figure 1 below. What are the expected effects on") Exam ECON 4624 Empirical Public Economics This exercise set consists of five (5) pages. Exercise 1 (50%) Kostøl and Mogstad (2014, American Economic Review) study the impact of financial incentives on

Exam ECON 4624 Empirical Public Economics This exercise set consists of five (5) pages. Exercise 1 (50%) Kostøl and Mogstad (2014, American Economic Review) study the impact of financial incentives on

Designing Price Contracts for Boundedly Rational Customers: Does the Number of Block Matter?

Designing Price Contracts for Boundedly ational Customers: Does the Number of Block Matter? Teck H. Ho University of California, Berkeley Forthcoming, Marketing Science Coauthor: Noah Lim, University of

Designing Price Contracts for Boundedly ational Customers: Does the Number of Block Matter? Teck H. Ho University of California, Berkeley Forthcoming, Marketing Science Coauthor: Noah Lim, University of

UNINTENDED CONSEQUENCES OF A GRANT REFORM: HOW THE ACTION PLAN FOR THE ELDERLY AFFECTED THE BUDGET DEFICIT AND SERVICES FOR THE YOUNG

UNINTENDED CONSEQUENCES OF A GRANT REFORM: HOW THE ACTION PLAN FOR THE ELDERLY AFFECTED THE BUDGET DEFICIT AND SERVICES FOR THE YOUNG Lars-Erik Borge and Marianne Haraldsvik Department of Economics and

UNINTENDED CONSEQUENCES OF A GRANT REFORM: HOW THE ACTION PLAN FOR THE ELDERLY AFFECTED THE BUDGET DEFICIT AND SERVICES FOR THE YOUNG Lars-Erik Borge and Marianne Haraldsvik Department of Economics and

Economic incentives and gender identity

Economic incentives and gender identity Andrea Ichino European University Institute and University of Bologna Martin Olsson Research Institute of Industrial Economics (IFN) Barbara Petrongolo Queen Mary

Economic incentives and gender identity Andrea Ichino European University Institute and University of Bologna Martin Olsson Research Institute of Industrial Economics (IFN) Barbara Petrongolo Queen Mary

Investigation of tax benefits as a tool for stimulation of charity activities (on the example of the banking sector)

") CARF Luzern 2017 Controlling.Accounting.Risiko.Finanzen. Konferenzband Konferenz Homepage: www.hslu.ch/carf Investigation of tax benefits as a tool for stimulation of charity activities (on the example

CARF Luzern 2017 Controlling.Accounting.Risiko.Finanzen. Konferenzband Konferenz Homepage: www.hslu.ch/carf Investigation of tax benefits as a tool for stimulation of charity activities (on the example

Lecture 8: Public Goods

1 31 Lecture 8: Public Goods Stefanie Stantcheva Fall 2017 31 PUBLIC GOODS: DEFINITIONS Pure public goods: Goods that are perfectly non-rival in consumption and are non-excludable Non-rival in consumption:

1 31 Lecture 8: Public Goods Stefanie Stantcheva Fall 2017 31 PUBLIC GOODS: DEFINITIONS Pure public goods: Goods that are perfectly non-rival in consumption and are non-excludable Non-rival in consumption:

Unemployment Insurance and Worker Mobility

Unemployment Insurance and Worker Mobility Laura Kawano, Office of Tax Analysis, U. S. Department of Treasury Ryan Nunn, Office of Economic Policy, U.S. Department of Treasury Abstract After an involuntary

Unemployment Insurance and Worker Mobility Laura Kawano, Office of Tax Analysis, U. S. Department of Treasury Ryan Nunn, Office of Economic Policy, U.S. Department of Treasury Abstract After an involuntary

Labor Economics Field Exam Spring 2014

Labor Economics Field Exam Spring 2014 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Labor Economics Field Exam Spring 2014 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

The trade balance and fiscal policy in the OECD

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

ECON 652: Graduate Public Economics I

ECON 652: Graduate Public Economics I Lesley Turner Fall 2013 Week 1: Introduction and Course Overview Plan for Today 1. What is public economics (and why should you care)? 2. Semester road map What is

ECON 652: Graduate Public Economics I Lesley Turner Fall 2013 Week 1: Introduction and Course Overview Plan for Today 1. What is public economics (and why should you care)? 2. Semester road map What is

Department of Economics Course Outline

Department of Economics Course Outline Term: Winter 2014 Course: Economics 653 [Public Revenue Analysis] Section: 01 Time: TR 9:30 10:45 Place: SS 423 Instructor: Dr. Kenneth J. McKenzie Office: SS 452

Department of Economics Course Outline Term: Winter 2014 Course: Economics 653 [Public Revenue Analysis] Section: 01 Time: TR 9:30 10:45 Place: SS 423 Instructor: Dr. Kenneth J. McKenzie Office: SS 452

The Effect of the Working Income Tax Benefit on Labour Supply in Canada. Kourtney Koebel Dionne Pohler

The Effect of the Working Income Tax Benefit on Labour Supply in Canada Kourtney Koebel Dionne Pohler Working Income Tax Benefit Introduced by the federal government in 2007 (renamed Canada Workers Benefit

The Effect of the Working Income Tax Benefit on Labour Supply in Canada Kourtney Koebel Dionne Pohler Working Income Tax Benefit Introduced by the federal government in 2007 (renamed Canada Workers Benefit

How Does the Incentive Effect of the Charitable Deduction Vary Across Charities?

How Does the Incentive Effect of the Charitable Deduction Vary Across Charities? July 20, 2011 Michelle H. Yetman * and Robert J. Yetman ** We thank Jerry Auten, Brad Barber, Greg Giesler, John Graham,

How Does the Incentive Effect of the Charitable Deduction Vary Across Charities? July 20, 2011 Michelle H. Yetman * and Robert J. Yetman ** We thank Jerry Auten, Brad Barber, Greg Giesler, John Graham,

Volume Title: Federal Tax Policy and Charitable Giving. Volume URL:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Federal Tax Policy and Charitable Giving Volume Author/Editor: Charles T. Clotfelter Volume

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Federal Tax Policy and Charitable Giving Volume Author/Editor: Charles T. Clotfelter Volume

THE ELASTICITY OF TAXABLE INCOME Fall 2012

THE ELASTICITY OF TAXABLE INCOME 14.471 - Fall 2012 1 Why Focus on "Elasticity of Taxable Income" (ETI)? i) Captures Not Just Hours of Work but Other Changes (Effort, Structure of Compensation, Occupation/Career

THE ELASTICITY OF TAXABLE INCOME 14.471 - Fall 2012 1 Why Focus on "Elasticity of Taxable Income" (ETI)? i) Captures Not Just Hours of Work but Other Changes (Effort, Structure of Compensation, Occupation/Career

Strictness of Tax Compliance Norms: A Factorial Survey on the Acceptance of Inheritance Tax Evasion in Germany

Strictness of Tax Compliance Norms: A Factorial Survey on the Acceptance of Inheritance Tax Evasion in Germany Martin Abraham, Kerstin Lorek, Friedemann Richter, Matthias Wrede Rational Choice Sociology

Strictness of Tax Compliance Norms: A Factorial Survey on the Acceptance of Inheritance Tax Evasion in Germany Martin Abraham, Kerstin Lorek, Friedemann Richter, Matthias Wrede Rational Choice Sociology

What Do Big Data Tell Us About Why People Take Gig Economy Jobs?

What Do Big Data Tell Us About Why People Take Gig Economy Jobs? By Dmitri K. Koustas Why do households take gig economy jobs? There are now several studies examining labor supply of individuals of a particular

What Do Big Data Tell Us About Why People Take Gig Economy Jobs? By Dmitri K. Koustas Why do households take gig economy jobs? There are now several studies examining labor supply of individuals of a particular

Foreign Direct Investment and Economic Growth in Some MENA Countries: Theory and Evidence

Loyola University Chicago Loyola ecommons Topics in Middle Eastern and orth African Economies Quinlan School of Business 1999 Foreign Direct Investment and Economic Growth in Some MEA Countries: Theory

Loyola University Chicago Loyola ecommons Topics in Middle Eastern and orth African Economies Quinlan School of Business 1999 Foreign Direct Investment and Economic Growth in Some MEA Countries: Theory

The Effect of Anticipated Tax Changes on Intertemporal Labor Supply and the Realization of Taxable Income

The Effect of Anticipated Tax Changes on Intertemporal Labor Supply and the Realization of Taxable Income Adam Looney Monica Singhal July 2006 Abstract We use anticipated changes in tax rates associated

The Effect of Anticipated Tax Changes on Intertemporal Labor Supply and the Realization of Taxable Income Adam Looney Monica Singhal July 2006 Abstract We use anticipated changes in tax rates associated

Corporate Taxation. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Corporate Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 24 24.1 What Are Corporations and Why Do We Tax Them? 24.2 The Structure of the Corporate Tax 24.3 The

Corporate Taxation 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 24 24.1 What Are Corporations and Why Do We Tax Them? 24.2 The Structure of the Corporate Tax 24.3 The

Econ 219B Psychology and Economics: Applications (Lecture 6)

") Econ 219B Psychology and Economics: Applications (Lecture 6) Stefano DellaVigna February 28, 2007 Outline 1. Reference Dependence: Disposition Effect 2. Reference Dependence: Equity Premium 3. Reference

Econ 219B Psychology and Economics: Applications (Lecture 6) Stefano DellaVigna February 28, 2007 Outline 1. Reference Dependence: Disposition Effect 2. Reference Dependence: Equity Premium 3. Reference

Marginal Benefit Incidence of Pubic Health Spending: Evidence from Indonesian sub-national data

Marginal Benefit Incidence of Pubic Health Spending: Evidence from Indonesian sub-national data Ioana Kruse Menno Pradhan Robert Sparrow The 2010 IRDES Workshop on Applied Health Economics and Policy Evaluation

Marginal Benefit Incidence of Pubic Health Spending: Evidence from Indonesian sub-national data Ioana Kruse Menno Pradhan Robert Sparrow The 2010 IRDES Workshop on Applied Health Economics and Policy Evaluation

Smoke Gets in Your Eyes: Cigarette Tax Salience and Regressivity

Smoke Gets in Your Eyes: Cigarette Tax Salience and egressivity Jacob Goldin and Tatiana Homonoff December 16, 2010 Abstract ecent work suggests that consumers respond differently to taxes that are included

Smoke Gets in Your Eyes: Cigarette Tax Salience and egressivity Jacob Goldin and Tatiana Homonoff December 16, 2010 Abstract ecent work suggests that consumers respond differently to taxes that are included

THE SALIENCE OF COMPLEX TAX CHANGES: EVIDENCE FROM THE CHILD AND DEPENDENT CARE CREDIT EXPANSION

National Tax Journal, September 2015, 68 (3), 477 510 http://dx.doi.org/10.17310/ntj.2015.3.01 THE SALIENCE OF COMPLEX TAX CHANGES: EVIDENCE FROM THE CHILD AND DEPENDENT CARE CREDIT EXPANSION Benjamin

National Tax Journal, September 2015, 68 (3), 477 510 http://dx.doi.org/10.17310/ntj.2015.3.01 THE SALIENCE OF COMPLEX TAX CHANGES: EVIDENCE FROM THE CHILD AND DEPENDENT CARE CREDIT EXPANSION Benjamin

The Theory of Taxation and Public Economics

louis kaplow The Theory of Taxation and Public Economics a princeton university press princeton and oxford 01_Kaplow_Prelims_p00i-pxxii.indd iii Summary of Contents a Preface xvii 1. Introduction 1 PART

louis kaplow The Theory of Taxation and Public Economics a princeton university press princeton and oxford 01_Kaplow_Prelims_p00i-pxxii.indd iii Summary of Contents a Preface xvii 1. Introduction 1 PART

Tax Policy and Inequality

Tax Policy and Inequality Tax Policy Overview Damon Jones Harris School of Public Policy University of Chicago Jones Tax Policy: Part 1 1 / 78 Outline Tax Policy Overview Personal Income Tax Corporate

Tax Policy and Inequality Tax Policy Overview Damon Jones Harris School of Public Policy University of Chicago Jones Tax Policy: Part 1 1 / 78 Outline Tax Policy Overview Personal Income Tax Corporate

France. Gabrielle Fack & Camille Landais. April 25, 2011

Charitable giving and tax policy in the presence of tax cheating: Theory and evidence from the U.S. and France Gabrielle Fack & Camille Landais April 25, 2011 Abstract We develop a model of charitable

Charitable giving and tax policy in the presence of tax cheating: Theory and evidence from the U.S. and France Gabrielle Fack & Camille Landais April 25, 2011 Abstract We develop a model of charitable

Family Labor Supply and the Timing of Cash Transfers: Evidence from the Earned Income Tax Credit

Family Labor Supply and the Timing of Cash Transfers: Evidence from the Earned Income Tax Credit Tzu-Ting Yang March 16, 2015 Abstract This paper provides new evidence on how families adjust their labor

Family Labor Supply and the Timing of Cash Transfers: Evidence from the Earned Income Tax Credit Tzu-Ting Yang March 16, 2015 Abstract This paper provides new evidence on how families adjust their labor

Class 13 Question 2 Estimating Taxable Income Responses Using Danish Tax Reforms Kleven and Schultz (2014)

") Class 13 Question 2 Estimating Taxable Income Responses Using Danish Tax Reforms Kleven and Schultz (2014) Outline: 1) Background Information 2) Advantages of Danish Data 3) Empirical Strategy 4) Key Findings

Class 13 Question 2 Estimating Taxable Income Responses Using Danish Tax Reforms Kleven and Schultz (2014) Outline: 1) Background Information 2) Advantages of Danish Data 3) Empirical Strategy 4) Key Findings

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Tore Olsen, Harvard

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Tore Olsen, Harvard

Are Fiscal Incentives Towards Charitable Giving Efficient? Evidence from France

Are Fiscal Incentives Towards Charitable Giving Efficient? Evidence from France Gabrielle Fack (Harvard University and PSE) & Camille Landais (PSE) 1 Preliminary version. Please do not cite without author

Are Fiscal Incentives Towards Charitable Giving Efficient? Evidence from France Gabrielle Fack (Harvard University and PSE) & Camille Landais (PSE) 1 Preliminary version. Please do not cite without author

Keynesian Views On The Fiscal Multiplier

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

For students electing Macro (8702/Prof. Smith) & Macro (8701/Prof. Roe) option

& Macro (8701/Prof. Roe) option") WRITTEN PRELIMINARY Ph.D EXAMINATION Department of Applied Economics June. - 2011 Trade, Development and Growth For students electing Macro (8702/Prof. Smith) & Macro (8701/Prof. Roe) option Instructions

WRITTEN PRELIMINARY Ph.D EXAMINATION Department of Applied Economics June. - 2011 Trade, Development and Growth For students electing Macro (8702/Prof. Smith) & Macro (8701/Prof. Roe) option Instructions

Economic and Social Incentives for Tax Compliance: Evidence from a Field Experiment in Germany

Economic and Social Incentives for Tax Compliance: Evidence from a Field Experiment in Germany Nadja Dwenger (MPI) Henrik Kleven (LSE) Imran Rasul (UCL) Johannes Rincke (Univ. of Erlangen-Nuremberg) July

Economic and Social Incentives for Tax Compliance: Evidence from a Field Experiment in Germany Nadja Dwenger (MPI) Henrik Kleven (LSE) Imran Rasul (UCL) Johannes Rincke (Univ. of Erlangen-Nuremberg) July

Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact and forecasting

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 21, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact and forecasting

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 21, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact and forecasting

The Romer Model: Policy Implications

The Romer Model: Policy Implications Prof. Lutz Hendricks Econ520 February 16, 2017 1 / 29 Policies have level effects What are the effects of government policies? We may expect policies to affect saving

The Romer Model: Policy Implications Prof. Lutz Hendricks Econ520 February 16, 2017 1 / 29 Policies have level effects What are the effects of government policies? We may expect policies to affect saving