TOOLS OF THE TRADE A New Look at Estate and Gift Planning Following Recent Law Changes

|

|

|

- Ethan Ball

- 6 years ago

- Views:

Transcription

1 TOOLS OF THE TRADE A New Look at Estate and Gift Planning Following Recent Law Changes 2012 Federal Tax Clinic Tuscaloosa, Alabama November 15, 2012 C. Fred Daniels Cabaniss, Johnston, Gardner, Dumas & O Neal LLP 2001 Park Place North, Suite 700 Birmingham, Alabama (205) cfd@cabaniss.com

2 SPEAKER C. FRED DANIELS C. Fred Daniels is a partner in the Birmingham, Alabama office of Cabaniss, Johnston, Gardner, Dumas, & O Neal LLP, where his practice is concentrated in the areas of estates and trusts, tax litigation, and closely-held businesses. He received his B.S. degree from Auburn University, his J.D. degree from the University of Alabama, and his LL.M. degree in Taxation from New York University. Mr. Daniels has been the lead trial and appellate counsel in numerous estate, gift and income tax cases including O Neal v. United States, 258 F.3d 1265 (11th Cir. 2001) (establishing that, in the Eleventh Circuit, claims against a decedent are to be valued for estate tax purposes based solely on facts known at death) and Cleveland v. Compass Bank, 652 So. 2d 1134 (Ala. 1994) (establishing that, in Alabama, state law governs the source of payment of state estate taxes on QTIP trusts). Mr. Daniels is a Fellow in the American College of Trust and Estate Counsel (Regent, Past Alabama State Chair; Past Chair of State Chairs Steering Committee) and is a Member of the Alabama Law Institute. He is Past Chairman of the Tax Section of the Alabama Bar Association, and he served as an Alabama Bar Delegate to the Southeastern Region IRS Liaison Committee and an Alabama Bar Delegate to the Southeastern Region IRS Exempt Plan, Exempt Organizations Liaison Committee. Mr. Daniels is a coauthor of Planning for Beneficiaries of IRAs and Qualified Plans: Essential Concepts and Useful Forms, 22 ACTEC Notes 125 (1996). He was a member of the Alabama Law Institute committees that revised Alabama s General Partnership Act (chairman), Estate Tax Apportionment Act (reporter), Business Entities Act, Professional Corporations Act, and Uniform Transfers to Minors Act. Mr. Daniels was chairman of the committee that drafted the comprehensive revision of Alabama s corporate income tax laws in 1985 and was a member of the committee that drafted the revision of Alabama s individual income tax laws in In addition to being listed in Best Lawyers in the fields of Corporate Law, Employee Benefits Law, Tax Law, and Trusts and Estates, he was recently named by Alabama Super Lawyers magazine as one of the top 50 attorneys in Alabama and by Best Lawyers as 2010 Lawyer of the Year in Trusts and Estates.

3 Table of Contents Page I. INTRODUCTION A. Where Are We and How Did We Get Here? B. Planning Prior to TRUIRA II. PORTABILITY; GREAT FOR CLIENTS, DANGER FOR ADVISORS A. Doubling of the Applicable Exclusion Amount B. Calculation of DSUEA C. Estate Tax Return Requirement D. Serial Spouses E. DSUEA Audits F. Traps for the Unwary G. Continued Desirability of Credit Shelter Trusts H. Clauses Concerning the Filing of Estate Tax Returns III. DISCLAIMER TRUSTS A. Sample Language B. Some Circumstances that Suggest the Use of Disclaimer Trusts C. Pitfalls IV. TOTAL RETURN TRUSTS A. Total Return Trust Structure B. Additional Features and Considerations C. Marital Deduction Trusts D. Sample Language V. CLAWBACKS VI. FORMULA ALLOCATION AND WANDRY DEFINED VALUE CLAUSES A. Formula Allocation Clauses B. Wandry or Formula Transfer Clauses C. The Proctor Problem D. Planning VII. NON-RECIPROCAL TRUSTS A. The Reciprocal Trust Doctrine B. The Levy Case C. Non-Reciprocal Trust Strategies D. Exercise of Power of Appointment in Favor of the Donor Spouse VIII. GIFTS TO PARENT S TRUSTS A. Structure of the Trust B. Tax Effect of the Gifts (i)

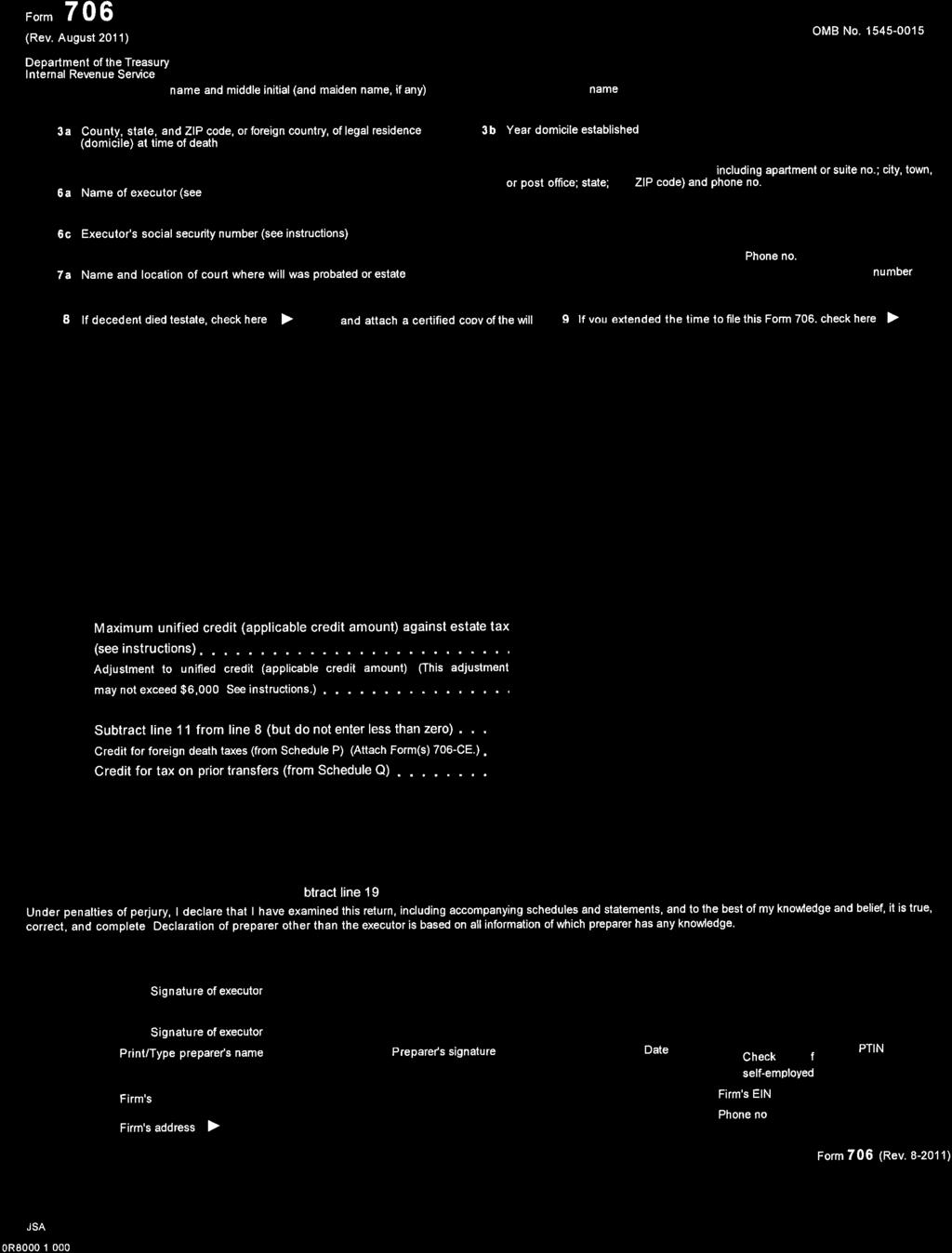

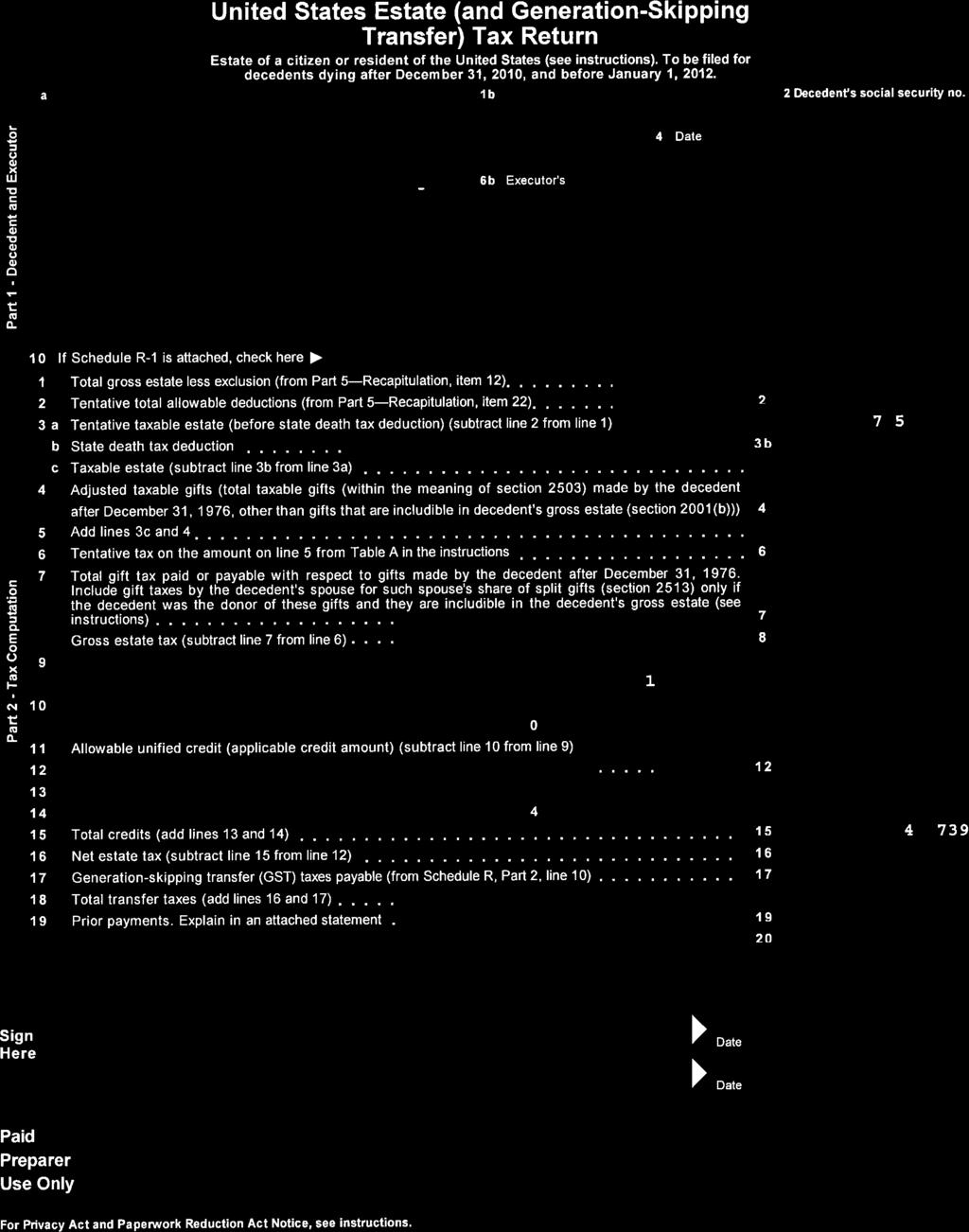

4 IX. SUPERCHARGED CREDIT SHELTER TRUSTS. SM A. Structure of the Supercharged Credit Shelter Trust. SM B. Grantor Trust Treatment for the Credit Shelter Trust C. Effect of Creditor Rights D. Income Tax Basis Following Death of First Spousal Beneficiary X. PLANNING FOR THE CREDIT FOR TAX ON PRIOR TRANSFERS A. Property not Included in Second Decedent Estate B. Application to Life Interests C. Percentage Limitations D. Limitations Based Upon Amount of Tax Appendix "A" Pages 1 and 4 of IRS Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return and related instructions Appendix "B" IRS Worksheet for Schedule Q Credit for Tax on Prior Transfers and related forms (ii)

5 TOOLS OF THE TRADE A New Look at Estate and Gift Planning Following Recent Law Changes I. INTRODUCTION. C. Fred Daniels * The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 ( TRUIRA 2010 ) increased the estate tax exclusion amount to $5,000,000 for decedents dying in 2011 and 2012 and indexed it for inflation. There is a possibility that the $5,000,000 applicable exclusion amount might continue after It is not likely that it will be reduced below $3,500,000, although a failure by Congress to act will result in a $1,000,000 applicable exclusion amount. A. Where Are We and How Did We Get Here? It is often perceived that only in the last decade has the estate tax been constantly changing. As indicated in the table below, there have only been two periods when there was not constant change 1948 to 1976 and 1987 to Excluded Year Amount Rates 1916 $50,000 1% to 10% 1917 $50,000 2% to 25% $50,000 1% to 25% $50,000 1% to 40% 1924 Gift tax added $100,000 1% to 20% $50,000 1% to 45% * Unless otherwise indicated Section references refer to the Internal Revenue Code of 1986, as amended; and Regulation references refer to sections of the Treasury Regulations. The reader is cautioned that there can be uncertainty in the interpretation and application of tax and other law, and much of what is expressed herein is the opinion of the author and others. The reader must make an independent determination as to the proper interpretation and application of tax and other law to the matters discussed herein. The reader is further cautioned not to rely on forms and clauses in these materials as is but to determine independently the appropriateness of each form and clause together with its compliance with applicable law

6 1934 $50,000 1% to 60% $40,000 2% to 70% 1940 $40,000 2% to 70% plus 10% surtax 1941 $40,000 3% to 77% $60,000 3% to 77% % marital deduction enacted 1977 $120,000 18% to 70% Gift and estate tax unified Minimum marital deduction of $250, $134,000 18% to 70% 1979 $147,000 18% to 70% 1980 $161,000 18% to 70% 1981 $175,000 18% to 70% 1982 $225,000 18% to 65% unlimited marital deduction Qualified disclaimers authorized 1983 $275,000 18% to 60% 1984 $325,000 18% to 55% 1985 $400,000 18% to 55% 1986 $500,000 18% to 55% GST enacted $600,000 37% to 55% % surtax over $10,000, $625,000 37% to 55% 1999 $650,000 37% to 55% $675,000 37% to 55% 2002 $1,000,000 41% to 50% 2003 $1,000,000 41% to 49% 2004 $1,500,000 45% to 48% 2005 $1,500,000 18% to 47% 2006 $2,000,000 46% 2007 $2,000,000 45% 2008 $2,000,000 45% 2009 $3,500,000 45% 2010 $5,000,000 35% or no tax if elected 2011 $5,000,000 35% 2012 $5,120,000 35% B. Planning Prior to TRUIRA Marital Formula Wills. The 50% marital deduction was added to the estate tax law in 1948 for non-community property, and it led to - 2 -

7 marital formula wills for couples whose combined net worth exceeded what was then $60, exemption from estate tax. 1 (a) (b) (c) Formulas Prior to From 1948 until 1977, the basic marital formula was to give 50% of the so-called adjusted taxable estate to what is now called a credit shelter trust and to give the remainder outright to the spouse or to a marital deduction trust that included a general power of appointment. 2 This practice created the need to equalize a husband s and wife s separate estates, but equalization often involved gift tax consequences because the gift tax marital deduction was only 50%, not unlimited. Formulas from 1977 to The 1976 Tax Reform Act increased the marital deduction to the greater of $250,000 or 50%. Marital formulas were modified accordingly. Formulas after the Unlimited Marital Deduction. The Economic Recovery Act of 1981 added the unlimited marital deduction effective 1982, and the formula changed dramatically. The predominant formula allocated the maximum exempt amount to the credit shelter trust and the balance, if any to the surviving spouse. 2. QTIP Trusts. The Economic Recovery Tax Act of 1981 extended the marital deduction to qualified terminal interest property ( QTIP ). Thereafter, martial trusts tended to be in the form of QTIP trusts instead of pay-all-income trusts coupled with a general power of appointment. 3. Lifetime Gifts and Unification. There was an independent gift tax until 1977 that had a $30, lifetime exclusion and rates that were three-fourths of the estate tax rates. This resulted in an incentive to use the lifetime exclusion rather than lose it and also to take 1 The theory of the 50% marital deduction was to give decedents in common law states the same tax advantage that was attained in community property states. Joint income tax returns were added at the same time for the same reason. Without these changes, the tax laws were an incentive for common law states to change to community property, and many did. 2 Qualified terminal interest property ( QTIP ) trusts were not available until

8 advantage of the lower gift tax rates. The 1976 Tax Reform Act unified the estate tax and the gift tax by replacing the gift tax and estate tax exclusions with a unified credit against the combined taxes and increasing the amount exempted in annual steps from $60, in 1976 to $175, in Various enactments since then gradually increased the exempt amount to $5,120,000, after the 2012 inflation adjustment. Unification eliminated the differential between estate and gift tax rates. (a) (b) Gifts of Future Income and Growth. Notwithstanding unification, lifetime gifts continue to remove future income and growth for the donor s estate, which is a valuable technique. Eliminate the Tax on a Tax. The estate tax base includes the funds that a decedent s estate uses to pay the estate tax, i.e., a tax on a tax. If a gift is made that results in the payment of gift tax and the donor outlives the gift by three years, the gift tax is excluded from the transfer tax base, thereby eliminating the tax on tax. See 2035(b) (inclusion of gift tax on gifts made during 3 years before death). 4. Life Insurance. (a) Spouse as Life Insurance Owner and Beneficiary. Because the estate tax marital deduction was only 50% until 1977, it was popular for an insured s spouse to be designated as the owner and beneficiary of the insured s life insurance. This ceased to be useful in 1982 when the marital deduction became unlimited.. (b) Irrevocable Life Insurance Trusts. A prevailing technique throughout most of the history of the estate tax has been the irrevocable life insurance trust. They were made more effective by the Ninth Circuit Court of Appeals decision in Crummey v. Comm r, 397 F.2d 82 (9 th Cir. 1968), that confirmed that trust additions coupled with a withdrawal were present gifts that qualify for $13,000 annual gift tax exclusion. 5. Disclaimer Trust Planning. If a couple s combined estate was close to the exempted amount, one technique that has been available since 1982 is to devise the estate to the surviving spouse, but provide that, - 4 -

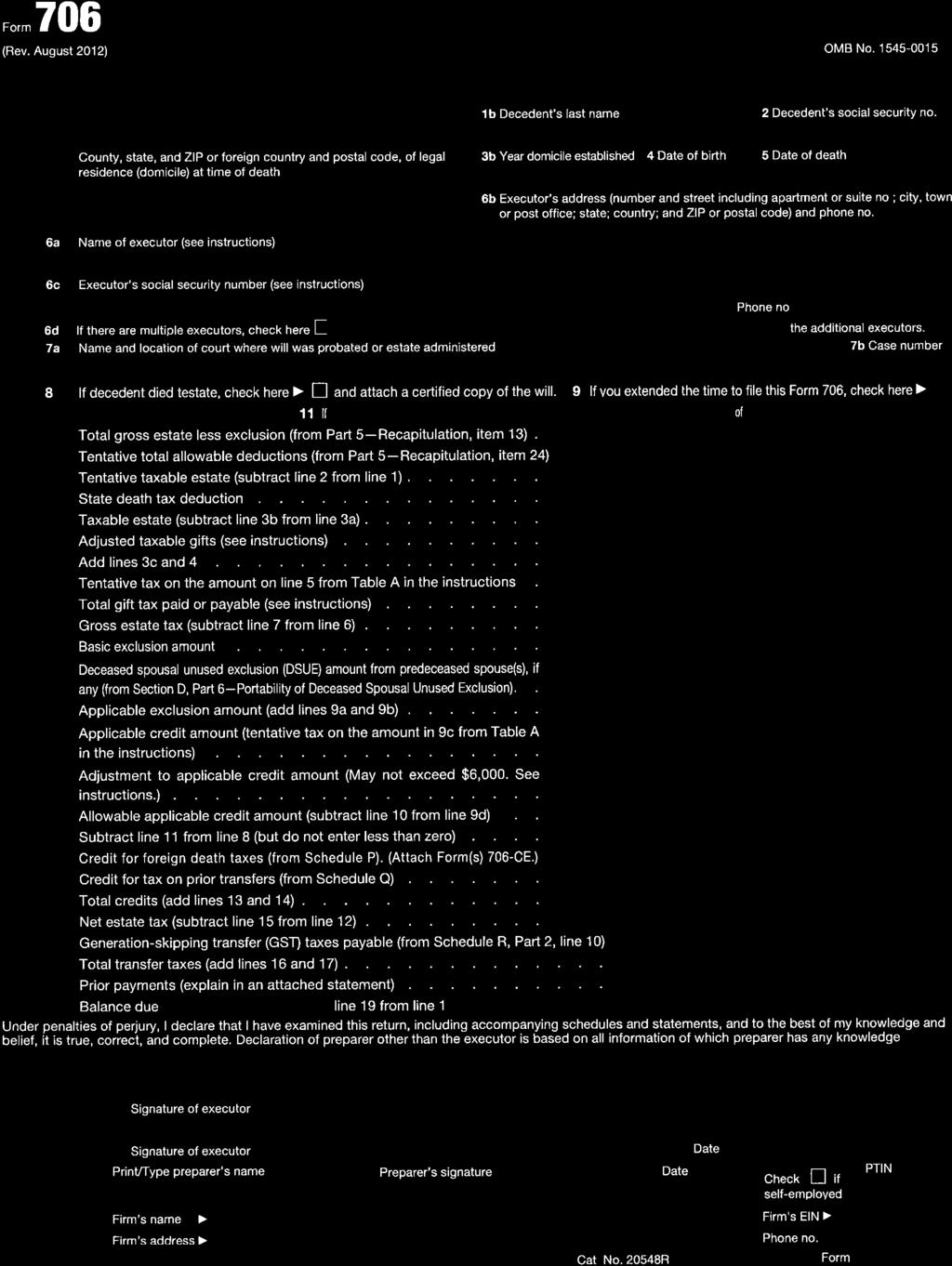

9 if the spouse disclaims, the disclaimed assets are devised to a credit shelter trust. See Generation-Skipping. The Tax Reform Act of 1986 added the generation skipping-transfer tax and its exemption. This resulted in complex dynasty trusts designed to utilize the GST exemption. II. PORTABILITY; GREAT FOR CLIENTS, DANGER FOR ADVISORS. Commentators often claim that husbands and wives exemptions from estate tax are twice the exclusion amount. A $5,000,000 exclusion amount supposedly means that a husband and wife have $10,000,000 exempt from estate tax. 3 To double the exemption prior to 2011, however, it was necessary that the assets be properly titled between the husband and wife and that the first spouse to die have a marital formula will a will that contained a credit shelter trust to which an amount equal to the decedent spouse s exclusion amount was devised. The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 ( TRUIRA 2010 ) attempts to achieve the same result without trusts and to simplify the preservation of both spouses exclusion amounts by introducing portability. However, practitioners representing small estates, preparing pre-nuptial agreements or seeking a substantial wrongful death award for a decedent s spouse may find themselves in the cross-hairs of a malpractice action if they fail to recognize the weaknesses of estate tax portability. Temporary regulations on the portability of a deceased spousal unused exclusion ( DSUEA ) amount for estate and gift tax purposes were issued on June 15, (REG ). The text of the temporary regulations also serves as proposed regulations. A. Doubling of the Applicable Exclusion Amount. TRUIRA 2010 amended 2010(c) to provide that the surviving spouse s estate tax applicable exclusion amount is the sum of the surviving spouse s basic exclusion amount ($5,000,000, indexed beginning in 2012 for inflation from 2010), plus a deceased spousal unused exclusion amount ( DSUEA ). 2010(c)(2), as amended by TRUIRA (a). 3 The $5,000,000 applicable exclusion amount was increased to $5,120,000 in 2012 by an inflation adjustment. For the purpose of simplicity, this discussion of portability generally ignores the inflation adjustment and refers to the applicable exclusion amount as $5,000,000 in all relevant years

10 1. Application to Gifts. Portability also applies to the gift tax exemption. 2505(a)(1), as amended by TRUIRA (b)(1). Thus, the surviving spouse can take the decedent s DSUEA into account when determining the surviving spouse s gift or estate tax liability. Reg T(a) and T(a). 2. Not Available for Generation-Skipping Transfer Taxes. The generation-skipping transfer tax exemption is not portable. CAVEAT: A credit shelter trust with generation-skipping tax features must still be used to take advantage of the GST exemption of the first spouse to die. B. Calculation of DSUEA. DSUEA generally is the deceased spouse s basic exclusion amount (e.g., $5,000,000 in 2010, $5,120,000 in 2011) in excess of the sum of the deceased spouse s taxable estate plus adjusted taxable gifts other than taxable gifts on which the deceased spouse paid gift tax. 2010(c)(4)(B)(ii); Reg T(c)(1) and (2). 1. Examples. The following examples illustration the DSUEA calculation. (a) No Non-Marital Gifts. If a decedent who made no lifetime adjusted taxable gifts dies in 2012 and leaves his or her entire estate to the surviving spouse, the decedent s taxable estate will be $0.00 due to the estate tax marital deduction. (i) (ii) If there are no adjusted taxable gifts, the DSUEA is $5,120,000, irrespective of the size of the deceased spouse s estate. The surviving spouse then has a $10,240,000 exemption from estate tax if he or she dies in 2012, not just $5,120,000. (b) Testamentary Non-Marital Gift. If the deceased spouse in the above example had left $200,000 to his or her children and the balance to the spouse, the DSUEA would be $4,920,000, because the deceased spouse s taxable estate would have been $200,

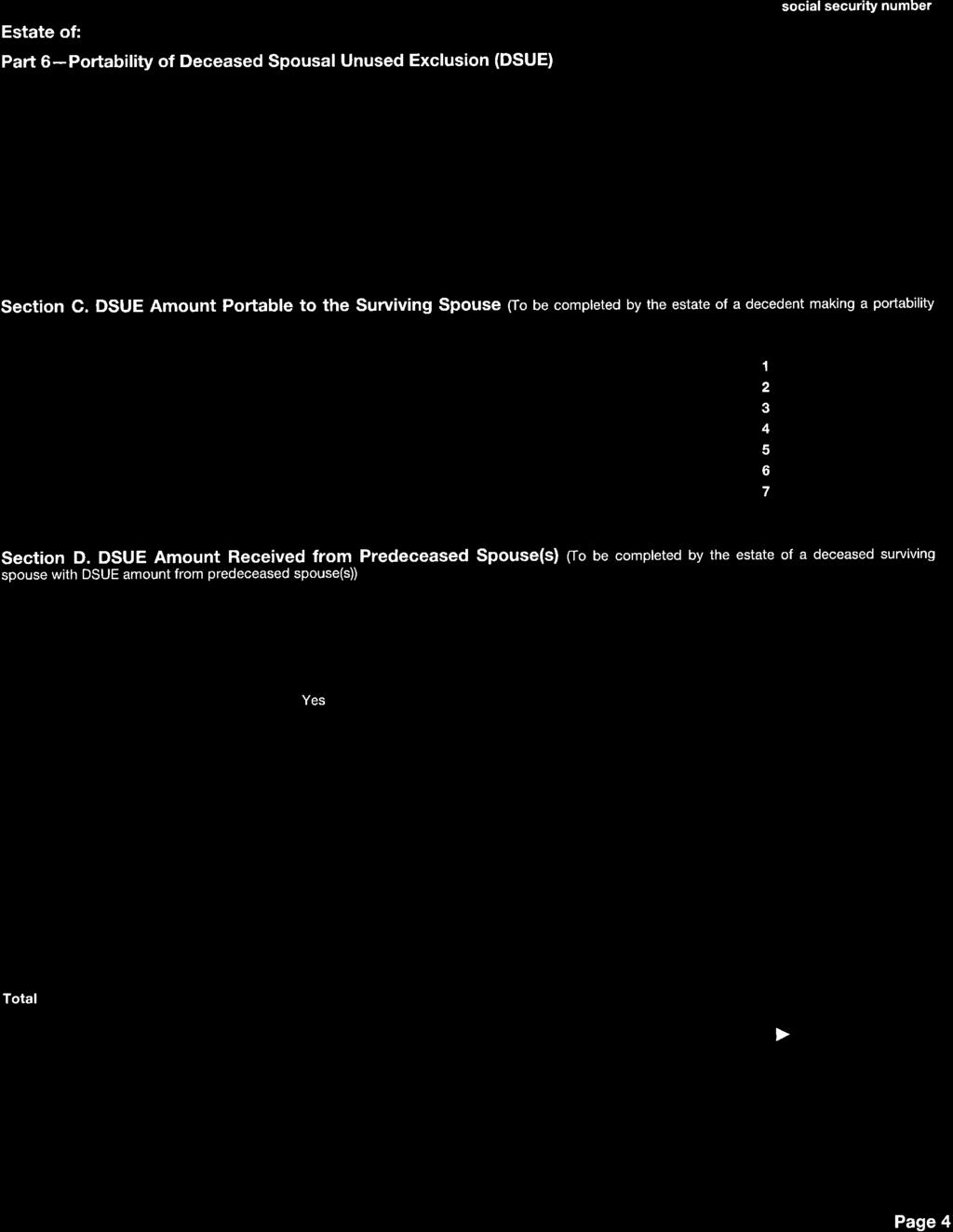

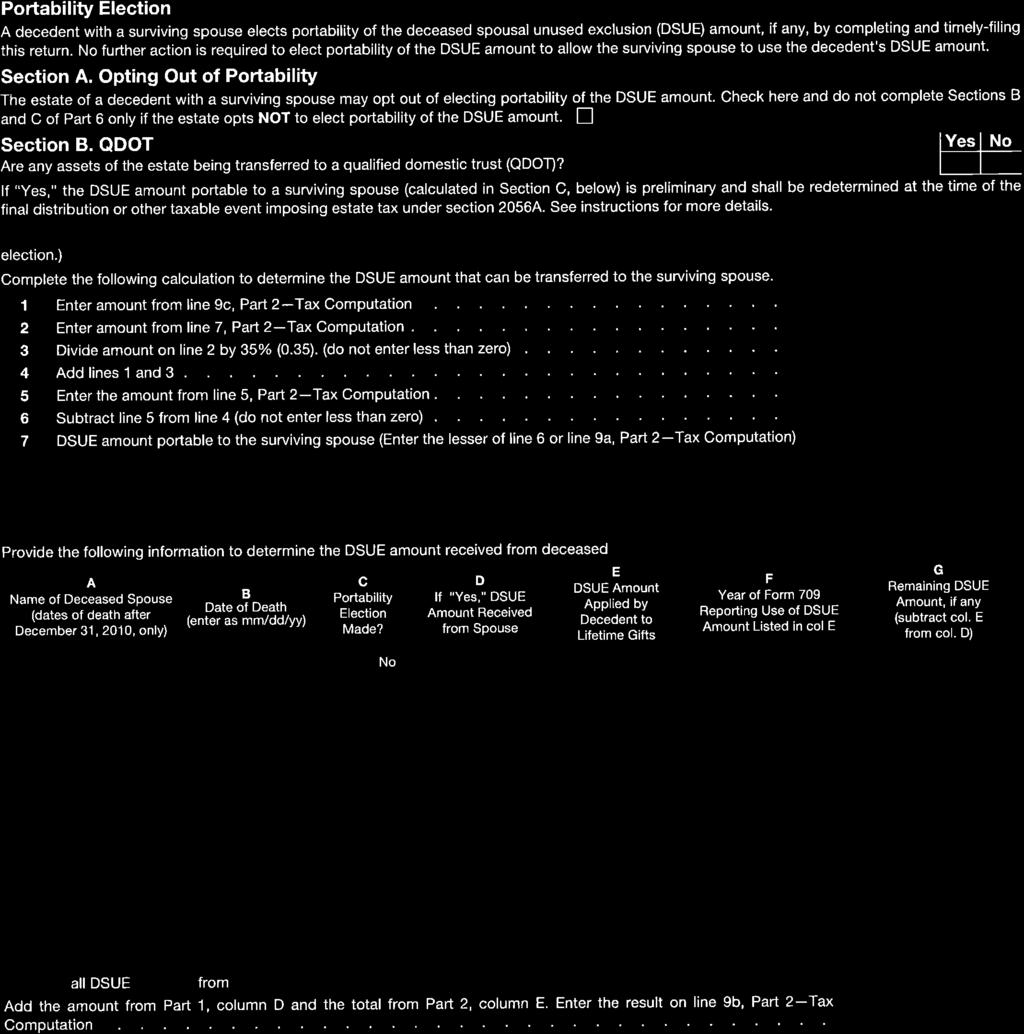

11 (c) (d) Inter Vivos and Testamentary Non-Marital Gifts. If the deceased spouse in the above examples had also made a $1,000,000 adjusted taxable gift in 2002 (when the applicable exclusion amount was $1,000,000), the DSUEA would be $3,920,000 ($5,120,000 - $200,000 testamentary gift to children - $1,000,000 adjusted taxable gifts). Inter Vivos Gifts that Required Payment of Gift Tax. If the deceased spouse in the above examples had also made a $1,500,000 adjusted taxable gift in 2002, the DSUEA is still $3,920,000 ($5,120,000 - $1,000,000 adjusted taxable gifts - $200,000 testamentary gift to children) because the $500,000 portion of the $1,500,000 adjusted taxable gift that was taxed in 2002 is ignored. See Reg T(c)(5), Example Using the DSUEA. Line 9(b) on the first page of the 2012 contains an entry to claim the DSUEA. The amount to be claimed is calculated on page 4 at Section D, Part 6 Portability of Deceased Spousal Unused Exclusion. 4 See Appendix A. 3. Effect of Tax Credits. The temporary regulations do not address the impact of available credits 2013 credit for tax on prior transfers, 2014 credit for foreign death taxes, and 2015 credit for death taxes on remainders. The Treasury and the IRS requested comments to assist in issuing future guidance. 4. No Indexing for Inflation. Although TRUIRA 2010 indexes the applicable estate tax exclusion amount, DSUEA acquired from a predeceased spouse is not indexed for inflation following his or her death. 5. Possibility of Re-Enactment. Although portability is to expire on December 31, 2013, the President s budget proposals call for it to be continued indefinitely thereafter. PREDICTION: Because the same result can be obtained by using a credit shelter trust, the Congressional revenue estimate for continuing portability is that there is no revenue loss, thus enhancing the likelihood for reenactment. 4 The 2012 Estate Tax Return form, revised August, 2012, was posted October 4, The instructions were posted October 12,

12 C. Estate Tax Return Requirement. A deceased spouse s DSUEA is not available unless the deceased spouse s estate files an estate tax return and makes an election to permit the surviving spouse to utilize the unused exemption. 2010(c)(5)(A), as amended by TRUIRA (a); Notice , I.R.B Portability Elected by Making Required Computation on Estate Tax Return. The election is not made by checking a box on the return. Instead, the election is made by including the DSUEA computation on the estate tax return. Reg T(b)(1). A transitional rule provides that the IRS will deem the required computation of the decedent s DSUEA amount to have been made on an estate tax return that is considered complete and properly prepared. Notice (a) (b) (c) Part 6 Portability of Deceased Spousal Unused Exclusion (DSUE), page 4 of the 2012 IRS Form 706 sets forth schedules for the computation. The temporary regulations clarified that, after the IRS revised the prescribed form for the estate tax return to expressly include the computation of the DSUEA amount, executors that previously filed an estate tax return pursuant to the transitional rule are not required to file a supplemental estate tax return using the revised form. The estate tax return must be timely filed, including extensions actually granted. Reg T(a). Although estate tax returns are not required for gross estates that are less than the applicable exclusion amount, timely filing for portability purposes is determined as though the deceased spouse s gross estate exceed the applicable exclusion amount. 2. Complete and Properly Prepared Estate Tax Return. An estate tax return prepared in accordance with all applicable requirements is considered a complete and properly-prepared estate tax return. Reg T(a)(7)(i). 3. Electing Out of Portability. An election out of portability is made by an affirmative statement on the estate tax return signifying the decision to have the portability election not apply. Reg T(a)(3). Although there is not a box on the 2012 IRS Form 706 to - 8 -

13 elect portability, Section A of Part 6 has a check block to elect out of portability. Not filing a timely return is also considered to be an affirmative statement signifying the decision not to make a portability election. 4. Reduced Reporting Requirements for Certain Property. If an estate tax return is not otherwise required, the executor does not have to report the value of certain property that qualifies for the marital or charitable deduction. Reg T(a)(7)(ii). (a) (b) Information Required. Instead, the executor will only report the description, ownership, and beneficiary of the property, along with other information necessary to establish the right of the estate to the marital or charitable deduction. Reg T(a)(7)(ii). Exceptions. Limited reporting for marital or charitable deduction property is not available if (i) (ii) (iii) (iv) The value of the property relates to, affects, or is needed to determine, the value passing from the decedent to another recipient (e.g., there is a formula bequest); The value of the property is needed to determine the estate s eligibility for the provisions of 2032, 2032A, 6166, or another provision (these relate to alternate valuation, special valuation of farm property, and extension of time to pay); Less than the entire value of an interest in property includible in the decedent s gross estate is marital deduction or charitable deduction property (e.g., charitable remainder trusts); or A partial disclaimer or partial qualified terminable interest property (QTIP) election is made with respect to a bequest, devise, or transfer of property includible in the gross estate, part of which is marital deduction or charitable deduction property. 5. Person Who Files the Return. The return is filed by an executor or administrator who is appointed, qualified, and acting within the - 9 -

14 United States, within the meaning of Reg T(a)(6)(i). (a) (b) (c) No Executor Appointed. If an executor has not been appointed, a person in actual or constructive possession of any property of the decedent (i.e., a non-appointed executor) may file the estate tax return on behalf of the estate of the decedent and elect portability. Reg T(a)(6)(ii). Multiple Non-Appointed Executors. A portability election made by a non-appointed executor cannot be superseded by a contrary election made by another non-appointed executor of that same decedent s estate (unless such other non-appointed executor is the successor of the non-appointed executor who made the election). Reg T(a)(6)(ii). Surviving Spouse. A surviving spouse who is not appointed as the deceased spouse s executor cannot file the return if an executor has been appointed. D. Serial Spouses. If there are multiple marriages, only the most recent deceased spouse s (i.e., the last deceased spouse ) unused exemption can be used by the surviving spouse. 2010(c)(5)(B)(i), as amended. 1. Only One Last Deceased Spouse. Assume that the first spouse to die died in 2010 with only $100,000 of assets which is devised to his or her surviving spouse. The DSUEA is $5,000,000.00, and the surviving spouse s exclusion increased to $10,000, Second Deceased Spouse Cancels First Deceased Spouse s DSUEA. If the surviving spouse in the preceding example remarries and the new spouse dies with an taxable estate in excess of $5,000,000 in 2011, there will be no DSUEA. Because the second spouse is the last deceased spouse, the surviving spouse loses the benefit of the first deceased spouse s DSUEA, and his or her exemption is only $5,000,000 in A Second Spouse Who is Still Living is not the Last Deceased Spouse. The temporary regulations explain that the term last deceased spouse is the most recently deceased individual who was married to the surviving spouse at that individual s death. Reg

15 T(d)(5). Merely remarrying does not eliminate the DSUEA acquired from a prior spouse unless and until the new spouse dies before the death of the surviving spouse. 4. Application to Inter Vivos Gifts. If a surviving spouse makes a taxable gift, the surviving spouse s last deceased spouse is identified on the date of the taxable gift for purposes of determining a surviving spouse s applicable exclusion amount. Reg T(a). In other words, the gift tax availability of DSUEA acquired from the deceased first spouse is not lost upon remarriage until the new spouse dies. (a) (b) Ordering Rules. If a surviving spouse makes a taxable gift, the DSUEA from the decedent who is the last deceased spouse of the surviving spouse is applied against the surviving spouse s taxable gifts before the surviving spouse s basic exclusion amount is applied. Reg T(b). In other words, the DSUEA available to a surviving spouse or to his or her estate for calculations on the returns includes both: (i) the DSUEA from the surviving spouse s last deceased spouse, plus (ii) any DSUEA actually applied to taxable gifts pursuant to the extent the DSUEA so applied was from a decedent who no longer is the last deceased spouse. Reg T(c) and T(b). Use DSUEA Before it is Lost. OBSERVATION: A wealthy spouse who remarries may want to make gifts that use the DSUEA before his or her new spouses dies. E. DSUEA Tax Audits. If the personal representative of the first spouse to die files an estate tax return and makes the election, the IRS may examine the gift and estate tax returns of the predeceased spouse at any time to determine the DSUEA available for the surviving spouse. 2010(c)(5)(B), as amended by TRUIRA (a); Reg T(a), T(d), T(d), and T(e). 1. The examination cannot be made to assert a deficiency in estate or gift taxes for the predeceased spouse beyond the normal statute of limitations

16 2. The temporary regulations allow the decedent s estate full availability of the decedent s applicable exclusion amount until the final estate tax liability of the decedent is computed. 3. The returns and return information of a deceased spouse may be disclosed to the surviving spouse or the surviving spouse s estate as appropriate under section 6103 for purposes of an examination. Reg T(d). The temporary regulations are silent as to whether the returns and return information can be obtained from the IRS to use in preparing the surviving spouse s returns. 4. It is critical that the decedent s records be preserved and available to the surviving spouse and his or her estate. CAVEAT: The decision of who will preserve the information as well as where and how it will be preserved is a major decision. F. Traps for the Unwary. Many personal representatives will assume that there is no need to file an estate tax return if the first spouse to die has a relatively small estate. However, the surviving spouse will lose the benefit of the deceased spouse s DSUEA unless the return is filed. 1. Example. Assume that the first spouse to die died in 2010 with only $100,000 of assets which he or she devised to his or her surviving spouse. The surviving spouse has $8,900,000 in assets. (a) (b) If no estate tax return is filed for the first spouse to die, the surviving spouse s estate tax exclusion amount will only be $5,000,000, and $1,400,000 in estate taxes will be owed (assuming the current 35% tax rate). If the estate tax return is filed, however, the surviving spouse will have a $10,000,000 exclusion amount and there will be no estate taxes. 2. Example. Assume a spouse is killed under terrible circumstances, and the potential for a multimillion dollar wrongful death verdict is high. If the personal representative sues for $10,000,000, he or she may be advised that there is no need to file an estate tax return because wrongful death proceeds in Alabama are exempt from both income tax and estate tax. However, if all $10,000,000 is recovered and paid to the surviving spouse, the surviving spouse at his or her

17 death will have a $10,000,000 estate which otherwise would have been non-taxable had the personal representative of the pre-deceased spouse s estate filed an estate tax return and made the election. 3. Example. Assume that the surviving spouse has a small net worth, but he or she will inherit a substantial sum following the deaths of his or her parents. The surviving spouse might find that he or she needs the DSUEA that was available when his or her spouse died. G. Continued Desirability of Credit Shelter Trusts. Because of portability, many persons will assume that credit shelter trusts are no longer needed. This may be a mistake. 1. Example. Assume a spouse with $10,000,000 of assets devises his or her entire estate outright to his or her surviving spouse. Because of portability, the deceased spouse s DSUEA will be available to the surviving spouse, thereby resulting in a $10,000,000 applicable credit amount for the surviving spouse. If the surviving spouse remarries and the second spouse dies first, however, the $5,000,000 DSUEA from the first spouse s estate is lost. 2. Example. If, instead, the deceased spouse s will left the first $5,000,000 to a credit shelter trust and the surviving spouse remarries, he or she can acquire the DSUEA of his or her second spouse should their second spouse predeceased them and still exclude the $5,000,000 in the credit shelter trust in addition. 3. Disclaimer Trusts. If a couple hesitates to include credit shelter trusts in their wills, it may be desirable to include disclaimer trusts so the surviving spouse can change his or her decision when the first spouse dies. H. Clauses Concerning the Filing of Estate Tax Returns. Filing the return may be complicated when there is a second marriage, and the husband and wife have children by prior marriages. If the spouse with the minimal assets dies first, his or her children will have little incentive, if any, to incur the expense, time and difficulty of filing an estate tax. Recognizing that there is potential to save as much as $1,750,000 (i.e., DSUEA of $5,000,000 time 35% tax rate), the children of the deceased spouse might even demand that the surviving spouse share the potential benefit by a compensating payment to the estate of the first spouse to die

18 1. Deducting the Expense. Will clauses can address whether the deceased spouse s estate or the surviving spouse will pay the expense of preparing the return. Because the deceased spouse s estate necessarily will not owe estate tax, the expense cannot be taken as an estate tax deduction. If it is paid by the deceased spouse s estate, it can be deducted on the estate s income tax return. If it is paid by the surviving spouse, it is likely not deductible on any return. 2. Pre-Nuptial Agreements. It might be advisable to enter into a prenuptial agreement that requires the estate of the first spouse to die to file an estate tax return and make the election upon the request of the surviving spouse. The surviving spouse might also want a provision whereby the surviving spouse can be named as the personal representative under these circumstances. In return, the estate of the first spouse to die may want to require the surviving spouse to pay all expenses associated with the estate tax return and defend any tax audit at his or her expense. The following is sample language that might be used: Deceased Spousal Unused Exclusion Amount. Notwithstanding the foregoing, Mr. Got-Nuthin agrees that the personal representative of his estate will, at Miss Lottas-Money s request, timely file any and all documents necessary to make the election provided in 2010(c)(5) of the Internal Revenue Code of 1986, as amended by 303(a) of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010, or any similar or corresponding law, for the deceased spousal unused exclusion amount with respect to Mr. Got-Nuthin s estate to be available to be taken into account by Miss Lottas-Money and her estate. Said documents may include, but are not necessarily limited to, an estate tax return for Mr. Got- Nuthin s estate even if his estate does not owe any Federal estate tax at his death. If Miss Lottas-Money makes said request and Mr. Got-Nuthin s estate would otherwise not be required to file an estate tax return or other necessary documents in order to make the election, Miss Lottas-Money shall make the arrangements for the preparation of said estate tax return (or necessary documents in connection with said election) and

19 pay the cost of preparing said estate tax return or other documentation and all other costs incurred in connection with said election. Mr. Got-Nuthin s personal representative shall fully cooperate with the preparation, execution and filing of the necessary documents (including said estate tax return) and shall promptly furnish all documents and information as shall be reasonably requested for that purpose. 3. Will Provisions. A low net worth spouse might want to consider a clause similar to the following to assist the survivor. A determination must be as to whether the cost will be paid by the low net worth spouse s estate or by the surviving spouse. Deceased Spousal Unused Exclusion Amount Election. I direct that, upon the request of my surviving spouse, my executor shall do all things necessary to make a valid election to allow my surviving spouse to have the benefit of my deceased spousal unused exclusion amount, to the greatest extent permitted under applicable federal estate tax law. [My surviving spouse shall have no obligation to make any payment to my estate or to the other beneficiaries of my estate in order for my executor to make or because my executor has made this election, nor shall any equitable adjustment be made with respect to the dispositions under my estate because my executor makes this election.] The cost of making this election, including the costs of filing any tax returns required to make this election, shall be [charged solely against the residue of my estate] or [paid by my surviving spouse]. 4. Advising Personal Representatives. Although it may seem obvious in many estates that the personal representative will be unwilling to spend the money and endure the difficulty required to file an estate tax return, it is desirable in all estates of a first spouse to die for the professional advising the personal representative to discuss portability and have the personal representative decline to prepare the return. It is also advisable to document the discussion. Sample language to include in a letter for this purpose can be as simple as the following: Although the estate is below the $5,120, threshold for filing an estate tax return, we fully discussed

20 the effect of portability of s $5,120, estate tax exemption amount. If you file an estate tax return, the unused portion of s exemption will be added to your estate tax exemption amount. Although this is a valuable opportunity, you decided not to file an estate tax return and to forego the portability of the exemption. III. DISCLAIMER TRUSTS. If there is uncertainty whether to use a marital formula will, the decision came be postponed until the death of the first spouse to die. The technique is to devise the residue to the spouse, and then provide that any portion that is disclaimed is devised to a credit shelter trust that benefits the spouse. A. Sample Language. The following is a typical disclaimer clause gift: Gift to My Spouse. I give, devise and bequeath the residue of my estate to my spouse, outright and free of trust, if my spouse survives me. Effect of Qualified Disclaimer by My Spouse. If my spouse makes a qualified disclaimer of any part or all of the residue, the disclaimed property shall be transferred and paid over to the Trustee of the Family Trust, the principal provisions of which are set forth in Article hereof, to be held or disposed of in accordance with the provisions thereof. B. Some Circumstances that Suggest the Use of Disclaimer Trusts. Circumstances where disclaimer trusts are frequently used include the following: 1. Concern About Reduction in Applicable Exclusion Amount. Husband and wife are in their seventies, and each has $2,000,000. They do not want to use a credit-shelter trust if the applicable exclusion amount remains at $5,000,000, but they are concerned that it might be reduced to $3,500, or less

21 2. Concern Because Net Worth is Growing. Husband and wife are young professionals, and each has already accumulated $1,500,000. Although their combined net worth is only $3,000,000, they reasonably anticipate that their net worth will continue to grow to exceed the applicable exclusion amount by a substantial amount. They do not want to limit themselves to portability as their only solution to possible estate taxes. 3. Concern Due to Potential Inheritance. Husband and wife have moderate estates but anticipate inheriting significant amounts. 4. Concern That Surviving Spouse Will Remarry. Husband and wife are in their fifties, and their combined net worth is substantially in excess of $10,000,000. If they live into their seventies or later, they believe they will rely on portability to use both applicable exclusion amounts. However, if one dies in the near future, they recognize that the survivor is young enough that he or she is likely to remarry and lose the benefit of the deceased spouse unused exclusion amount. C. Pitfalls. Pitfalls frequently encountered when using disclaimer techniques include the following: 1. Diminished Mental Capacity. By the time the first spouse dies, the surviving spouse s mental capacity might have diminished to the point that the ability to make a qualified disclaimer is questionable. 2. Reluctance to Make Major Decisions. The first year after a spouse s death is not a good time to make major decisions. A qualified disclaimer has to be made within nine months of death. IV. TOTAL RETURN TRUSTS. Traditional trusts frequently instruct trustees to pay net income but retain principal. The dividend yield in 1980 on the Standard & Poor s 500 Index was almost 6%. Now, it is around 2%. If a 1.25% trustee fee is subtracted, net income falls to 0.75% before income taxes. If the trustee invests in non-dividend paying stocks like Microsoft, the effect of the trustee fee creates negative net income even when the value of the trust grows substantially. Many people feel that a steady return of 4% or 5% coupled with a principal growth to compensate for inflation is a better result. This led to the concept of total return trusts or unitrusts

22 A. Total Return Trust Structure. A typical total return trust provides that the trustee is to pay a unitrust amount of based upon a fixed percentage (typically between 3% to 5%) of the value of the trust each year instead of net income. If the income plus growth in normal years is more than the unitrust amount, the beneficiary will receive a reasonably steady return while principal grows to compensation for inflation. For example, if a $100,000 trust has income plus growth of 6% per year, and the unitrust percentage is 4%, the adjustment for inflation is illustrated as follows: Beginning Ending Year Balance Return Payout Balance 1 100, , (4,000.00) 102, , , (4,080.00) 104, , , (4,161.60) 106, , , (4,244.83) 108, , , (4,329.73) 110, , , (4,416.32) 112, , , (4,504.65) 114, , , (4,594.74) 117, B. Additional Features and Considerations. Matters to consider in addition to the unitrust percentage included the following: 1. Smoothing Period. Peaks and valleys can be smoothed by using a moving average value of trust assets instead of the current year value. For example, net asset value might be based upon a three average. 2. Personal Use Assets. Personal use assets might be excluded from the calculation of the value of the assets. 3. Principal Invasions. The trustee can be authorized to invade principal if the unitrust amount is insufficient for the beneficiary s needs

23 C. Marital Deduction Trusts. Reg (b)-1 contemplates total return trusts as qualifying for the gift tax and estate tax marital deductions by defining income for that purpose as a unitrust amount if the governing state law authorizes income to be defined in that manner. 1. The Regulation. The provision in the regulation includes the following: Sec (b)-1 Definition of income.... However, an allocation of amounts between income and principal pursuant to applicable local law will be respected if local law provides for a reasonable apportionment between the income and remainder beneficiaries of the total return of the trust for the year, including ordinary and tax-exempt income, capital gains, and appreciation. For example, a state statute providing that income is a unitrust amount of no less than 3% and no more than 5% of the fair market value of the trust assets, whether determined annually or averaged on a multiple year basis, is a reasonable apportionment of the total return of the trust.... (emphasis added) 2. The Local Law Requirement. Although a majority of the states now have local law provisions permitting income to be defined as a unitrust amount, Alabama does not. However, the Alabama Law Institute has drafted a unitrust statute to be introduced in the 2013 the Alabama Legislature session. It not only authorizes unitrust definitions of income, it permits existing income trusts to convert to unitrusts. Until then, trusts desiring to qualify for the marital deduction must continue to provide for the distribution of the greater of net income or the unitrust amount. D. Sample Language. The following language that can be used to coordinate a marital deduction trust and a credit shelter trust in a state without a unitrust statute:

24 TOTAL RETURN MARITAL TRUST (No local statute) Distributions During Lifetime of My Spouse. During the lifetime of my spouse, the Trustee shall pay to or for the benefit of my spouse the entire net income from this trust in installments convenient to my spouse, at least annually. If the net income of the trust is less than five percent (5%) of the average net fair market value of the assets of the trust, the Trustee shall pay to or for the benefit of my spouse an amount from the principal of the trust equal to the excess of (i) five percent (5%) of such average net fair market value of the assets, over (ii) the net income from the trust, said payments to be made in installments convenient to my spouse, preferably monthly in arrears but at least annually. The payments hereunder shall accrue from the date of my death. In determining the amount to be paid from principal for a short year, the Trustee shall prorate the same on a daily basis. No payment of principal otherwise due hereunder, however, shall be made after my spouse s death. Additional Payments from Principal. If at any time during the lifetime of my spouse, the foregoing payments from the trust are insufficient for the health, maintenance, support, and education of my spouse, the Trustee shall pay to or for the benefit of my spouse such additional sum or sums out of the principal of the trust as the Trustee, in the sole discretion of the Trustee, shall deem necessary or desirable for said purposes. My primary concern during the continuation of the trust is the health, maintenance, support, and education of my spouse rather than the preservation of principal for ultimate distribution to the remaindermen, and the Trustee shall not consider the interest of the remaindermen when making decisions concerning investments, distributions or any other matter. Tangible Property. I anticipate that the assets of the trust may include, in whole or part, an interest in my homeplace and perhaps other tangible property, which I wish to be available for my spouse. Accordingly, in addition to the foregoing, the Trustee may make available for the use of my spouse rent-free any tangible real or personal property owned by the trust. Such property made available for the use of my

25 spouse rent-free, however, shall not be included in the fair market value of the trust assets when determining the average net fair market value of the assets of the trust under this Article. Average Net Fair Market Value. It is my intent that the average net fair market value of the assets of the trust shall be the average of the net fair market values of the trust assets determined as of the close of the last business day of each of the three (3) preceding years of the trust. In the case of the first year of the trust, however, it shall be based solely on the initial net fair market value of the assets. For the second year, it shall be based upon the average of the initial net fair market value of the assets and the net fair market value of the assets as of the close of the last business day of the first year of the trust. For the third year, it shall be based upon the average of the initial net fair market value of the assets and the net fair market values as of the close of the last business days of the first and second year of the trust. The average net fair market value shall be determined by the Trustee in the Trustee s sole and absolute discretion, and the decision of the Trustee as to such value shall be final and binding on all persons. Trustee s Discretion. The Trustee may, in the Trustee s sole and absolute discretion, from time to time, determine the following: Notwithstanding the net fair market values of one or more trust assets may be determined on days other than the last business day of the year if the Trustee determines that different valuation days are more appropriate; Average net fair market value shall be adjusted by the Trustee to reflect the effect of additions to the trust or distributions of additional payments from the payments; Reasonable estimates may be used to value non-liquid assets or hard to value assets; and

26 Any other matter that is necessary or desirable for the proper functioning of the trust that is not inconsistent with the terms herein. Disposition of Undistributed Income at My Death. Upon the death of my spouse, the Trustee shall transfer and pay over any accumulated or undistributed income, but not the principal, of the trust to such person or persons, including the estate of my spouse, as my spouse may appoint and direct pursuant to this general power of appointment hereby granted. Any unappointed portion of such income together with the remainder of the trust shall be disposed of as hereinafter provided. TOTAL RETURN FAMILY TRUST Distributions During Lifetime of My Spouse. It my goal for the distributions to be made from the this trust will, when added to the distributions from the Marital Trust, result in aggregate distributions from both trusts in an amount that equals five percent (5%) of the average net fair market value of the assets of both trusts. Accordingly, during the lifetime of my spouse, the Trustee shall pay to or for the benefit of my spouse from the net income and principal of this trust an amount equal to (i) five percent (5%) of the average net fair market value of the assets of this trust, minus (ii) that portion of the net income of the Marital Trust that exceeds five percent (5%) of the average net fair market value of the assets of the Marital Trust as determined in accordance with the provisions of the Marital Trust, said payments to be made in installments convenient to my spouse, preferably monthly in arrears but at least annually. The payments hereunder shall accrue from the date of my death. In determining the amount to be paid, the Trustee shall prorate the same on a daily basis for a short year. No payments otherwise due hereunder, however, shall be made after my spouse s death. Additional Payments from Principal. If at any time during the lifetime of my spouse, the foregoing payments from the trust are insufficient for the health, maintenance, support, and education of my spouse, the Trustee shall pay to or for the benefit of my spouse such additional sum or sums out of the principal of the trust as the Trustee, in the sole

27 discretion of the Trustee, shall deem necessary or desirable for said purposes. My primary concern during the continuation of the trust is the health, maintenance, support, and education of my spouse rather than the preservation of principal for ultimate distribution to the remaindermen, and the Trustee shall not consider the interest of the remaindermen when making decisions concerning investments, distributions or any other matter. Tangible Property. I anticipate that the assets of the trust may include, in whole or part, an interest in my homeplace and perhaps other tangible property, which I wish to be available for my spouse. Accordingly, in addition to the foregoing, the Trustee may make available for the use of my spouse rent-free any tangible real or personal property owned by the trust. Such property made available for the use of my spouse rent-free, however, shall not be included in the fair market value of the trust assets when determining the average net fair market value of the assets of the trust under this Article. Average Net Fair Market Value. It is my intent that the average net fair market value of the assets of the trust shall be the average of the net fair market values of the trust assets determined as of the close of the last business day of each of the three (3) preceding years of the trust. In the case of the first year of the trust, however, it shall be based solely on the initial net fair market value of the assets. For the second year, it shall be based upon the average of the initial net fair market value of the assets and the net fair market value of the assets as of the close of the last business day of the first year of the trust. For the third year, it shall be based upon the average of the initial net fair market value of the assets and the net fair market values as of the close of the last business days of the first and second year of the trust. The average net fair market value shall be determined by the Trustee in the Trustee s sole and absolute discretion, and the decision of the Trustee as to such value shall be final and binding on all persons. Trustee s Discretion. The Trustee may, in the Trustee s sole and absolute discretion, from time to time, determine the following:

28 Notwithstanding the net fair market values of one or more trust assets may be determined on days other than the last business day of the year if the Trustee determines that different valuation days are more appropriate; Average net fair market value shall be adjusted by the Trustee to reflect the effect of additions to the trust or distributions of additional payments from the payments; Reasonable estimates may be used to value non-liquid assets or hard to value assets; and Any other matter that is necessary or desirable for the proper functioning of the trust that is not inconsistent with the terms herein. V. CLAWBACKS. No gift tax will be owed if a taxpayer who has not made prior taxable gifts makes a $5,120, taxable gift during There is uncertainty as to what happens, however, when the taxpayer dies if the applicable credit amount is reduced to $3,500, or $1,000, for 2013 and later years. As presently enacted, the savings is clawed back when the taxpayer dies. However, the Treasury s Green Book states that clawback was not intended, and this is expected to be clarified in future legislation. If so, a taxpayer can avoid transfer taxes on $1,620, or $4,120,000.00, as the case may be, by using the $5,120, applicable exclusion amount during VI. FORMULA ALLOCATION AND WANDRY DEFINED VALUE CLAUSES. Gifts or sales of non-publicly traded interests in businesses almost always involve some uncertainty as to value for gift tax purposes. Five cases in recent years have shown the way to establish value in a manner that makes it difficult for the IRS to contest the value. It appears advisable to make gifts or sales that might involve a gift element by using defined value clauses instead of identifying a specific number of shares, number of units or percentage

29 A. Formula Allocation Clauses. A formula allocation clause allocates the gifted or sold interest among taxable transferees (e.g., family members) and non-taxable transferees (e.g., charities, spouses, QTIP trusts, incomplete gift trusts, and zeroed-out GRATs) using a formula based upon the intended taxable value instead of a specific number of shares, number of units or percentage. If the IRS asserts the value of the gifted or sold interest is higher than that the determined by the parties, the increase in value passes to the non-taxable transferees, and no additional gift tax is paid. 1. Illustration. A typical formula allocation clause might be something similar to the following: I hereby transfer and assign my 80% interest in Capstone Land Management, Ltd, to my son and the Community Foundation of Birmingham, Alabama. My son is to receive that portion of the 80% interest that has a fair market value of $5,120, The Community Foundation of Birmingham, Alabama is to receive that portion of the 80% interest that has a fair market value in excess of $5,120, The foregoing provision should then be completed using either a confirmation agreement clause or a finally determined clause. (a) Confirmation Agreements. A confirmation agreement clause might be similar to the following: The determination of said fair market value shall be made by my son and the Community Foundation of Birmingham, Alabama. For this purpose, the fair market value of the Assigned Partnership Interest as of the date of this Assignment Agreement shall be the price at which the Assigned Partnership Interest would change hands as of the date of this Assignment Agreement between a hypothetical willing buyer and a hypothetical willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts. Any dispute with respect to the allocation

30 of the Assigned Partnership Interests among Assignees shall be resolved by arbitration. See McCord v. Comm r, 461 F.3d 614 (5th Cir. 2006), rev g, 120 T.C. 358 (2003) (upheld a defined value sale/gift transfer.); Hendrix v. Comm r, T.C. Memo (June 15, 2011) (also upheld a defined value sale/gift transfer). (b) Finally Determined Clauses. A finally determined clause might be similar to the following: The fair market value of the Assigned Partnership Interest as of the date of this Assignment Agreement shall be the value thereof as finally determined for federal estate or gift tax purposes. See Estate of Petter v. Comm r, T.C. Memo , aff d 653 F.3d 1012 (9th Cir. 2011); Estate of Christiansen v. Comm r, 130 T.C. 1 (2008), aff d, 586 F.3d 1061 (8 th Cir. 2009) (defined value disclaimer so that assets in excess of a defined value passed to charities). B. Wandry or Formula Transfer Clauses. Wandry v. Comm r T.C. Memo (2012) goes much further by eliminating the excess gift to the non-taxable transferee. It should be used when the taxpayer is unwilling to designate a non-taxable transferee as the donee of a portion of the interest. 1. Illustration. The following is a modified version of the clause used in Wandry: I hereby assign and transfer as gifts, effective as of December 1, 2012, a sufficient number of my Units in Capstone Land Management, LLC, so that the fair market value of such Units for federal gift tax purposes shall be $5,120,000. Although the number of Units gifted is fixed on the date of the gift, that number is based on the fair market value of the gifted Units, which cannot be known on the date of the gift but must be determined after such date based on all relevant information as of that date. Furthermore, the value

31 determined is subject to challenge by the Internal Revenue Service ( IRS ). I intend to have a goodfaith determination of such value made by an independent third-party professional experienced in such matters and appropriately qualified to make the determination. Nevertheless, if after the number of gifted Units is determined based on such valuation, the IRS challenges such valuation, the number of gifted Units shall be adjusted accordingly so that the value of the number of Units gifted as finally determined for federal gift tax purposes equals $5,120,000, said adjustment to be made in the same manner as a federal estate tax formula marital deduction amount would be adjusted for a valuation redetermination. 2. Appeal. Whether a Wandry clause is preferable to a formula allocation clause will not be clear until there has been an appeal of the Tax Court s decision. Although the government recently filed a notice of appeal of Wandry to the Tenth Circuit Court of Appeals, it is not clear whether a decision was made by the government to prosecute the appeal or if the notice was filed merely to obtain additional time to consider whether the appeal should be pursued. C. The Proctor Issue. Comm r v. Procter, 142 F.2d 824 (4th Cir. 1944), involved an assignment that provided if any part of the transfer is subject to gift tax, the excess property that is decreed by the court to be subject to gift tax shall automatically be deemed not to be included in the conveyance and shall remain the property of the donor. To determine what is valid and what is not, the Tax Court in Wandry focused on the distinction between a savings clause, which is not valid, and a formula clause, which is valid. A savings clause is void because it the donor, as in Proctor, tries to take property back. In contrast, a formula clause merely transfers a fixed set of rights with uncertain value. This is the same as the formula marital deduction clauses that have been utilized since D. Planning. A couple of potential pitfalls to avoid that were identified in Wandry include the following:

32 1. Correctly Described What Was Transferred. The gift tax return should correctly describe what is given. It is Units having a value of $5,120,000, not 2,350 units, even though the valuation report may indicate that 2,350 units have a value of $5,200, Obtain a Contemporaneous Valuation. The valuation report should be obtained promptly. Some firms refuse to prepare gift tax returns if the valuation report is not obtained within 90 days of the transfer. VII. NON-RECIPROCAL TRUSTS. A couple may want to use their $5,120, applicable exclusion amounts during 2012 but retain access to the gifted assets. One way to do this is for the husband to create a $5,120, trust for the wife and for the wife to create a $5,120, trust for the husband. If so, the reciprocal trust doctrine might undermine the effectiveness of the gifts. A. The Reciprocal Trust Doctrine. United States v. Estate of Grace, 395 U.S. 316 (1969), involve a husband who created a trust that provide income to his wife for life followed by a similar trust created by the wife fifteen days later. The Supreme Court held that the trust created for the husband by the wife should be included in the husband s gross estate under an earlier version of 2036 because the trusts were identical and created essentially at the same time. Under the Court s theory, the husband essentially was the grantor of the trust nominally created by the wife. Under 2036(a)(1), a trust is included in a grantor s estate if the grantor retained the right to the income for life. For a further discussion of Grace and the reciprocal trust doctrine, see G. Slade, THE EVOLUTION OF THE RECIPROCAL TRUST DOCTRINE SINCE GRACE AND ITS CURRENT APPLICATION IN ESTATE PLANNING, 17 Tax Mgmt. Est. Gifts & Tr. J. 71 (1992). B. The Levy Case. The Tax Court revisted the reciprocal trust doctrine in Levy v. Comm r, 46 T.C.M. (CCH) 910 (1983). There, a husband and wife created trusts on the same day that gave each other an income interest. The trusts were not identical because one of them provided its spousal beneficiary a limited power of appointment to its spousal beneficiary, and the other trust did not

33 1. Importance of Different Provisions. In determining that the reciprocal trust doctrine did not apply due to this difference, the court referenced the following language from Grace: The reciprocal trust doctrine does not purport to reach transfers in trust which create different interests and which change the effective position of each party vis a vis the [transferred] property The IRS Concession. Significantly, the IRS conceded in Levy that the wife s limited power of appointment in the wife, if valid, prevented the two trusts from being interrelated and, therefore, subject to the reciprocal trust doctrine. Although it is not precedential, the IRS has embraced Levy. See PLR C. Non-Reciprocal Trust Strategies. Strategies to avoid the application of the reciprocal trust doctrine include the following: 1. Create at Different Times. Create the trusts at different times separated by months, not days as in Grace. Even if the terms of two trusts are identical, the reciprocal trust doctrine should still not apply if the trusts are not created in the same time frame. See Grace, 395 U.S. at 316 (emphasizing that the trusts were interrelated because of the parallel terms and because created within a 15-day period). 2. Different Limited Powers of Appointments. As in Levy, one trust might contain a limited power of appointment while the other would not. In the alternative, both trusts might have limited powers of appointment but exercisable in favor of different classes of appointees and, perhaps, might be exercisable only with the consent of a non-adverse party). 3. Different Distribution Directions. One trust might be a pay all income or pay a unitrust amount for a spouse and the other might be a sprinkle trust for the other spouse and their descendants. 4. Different Trustees. The trusts might have significantly different trustees, such as a bank trustee for one and individual trustee for the other

34 5. Trustee Portability. The trusts might have different portability provisions for changing trustees. In the alternative, one might have provisions to change trustees and the other might not have such provisions. 6. Different Powers of Principal Invasion. One trust might provide that other resources of the spouse beneficiary should be taken into account when invade principal and the other might direct that the existence of other resources is irrelevant. 7. Fund with Different Assets. The trusts might be funded with different assets and with different values. For example, one trust might be funded with real estate or a closely held business interest, and the other might be funded with marketable securities and cash. D. Exercise of Power of Appointment in Favor of the Donor Spouse. Although distributions from the trusts are available for the family through distributions from each trust to its respective spousal beneficiary, the inclusion of a provision to provide benefits to the donor spouse following the death of the beneficiary spouse will result in inclusion of the trust in the donor spouse s estate as a 2036 retained life estate or a 2038 revocable transfer. However, there should be no inclusion if the donee spouse exercises a power of appointment at a later date to create a successive trust for the donor spouse, unless the exercise of the power of appointment was pursuant to a pre-existing agreement or plan to do so. The analysis is as follows: 1. Section Section 2036 only applies to transfers where the decedent retains the prohibited interest. See, e.g., United States v. O Malley, 383 U.S. 627 (1966). Section 2036(a) provides as follows: Sec Transfers with retained life estate (a) General rule. The value of the gross estate shall include the value of all property to the extent of any interest therein of which the decedent has at any time made a transfer (except in case of a bona fide sale for an adequate and full consideration in money or money s worth), by trust or otherwise, under which he has retained for his life or for any period not ascertain

35 able without reference to his death or for any period which does not in fact end before his death (1) the possession or enjoyment of, or the right to the income from, the property, or (2) the right, either alone or in conjunction with any person, to designate the persons who shall possess or enjoy the property or the income therefrom. By not including provisions for the benefit of the grantor spouse, there will be no retention even if the first beneficiary spouse adds provisions at a later date. 2. Section Section 2038 is not limited to a retained right, but instead, it applies to certain powers without regard to when or from what source the decedent acquired such power. It states Sec Revocable transfers (a) In general. The value of the gross estate shall include the value of all property. (1) Transfers after June 22, To the extent of any interest therein of which the decedent has at any time made a transfer (except in case of a bona fide sale for an adequate and full consideration in money or money s worth), by trust or otherwise, where the enjoyment thereof was subject at the date of his death to any change through the exercise of a power (in whatever capacity exercisable) by the decedent alone or by the decedent in conjunction with any other person (without regard to when or from what source the decedent acquired such power), to alter, amend, revoke, or terminate, or where any such power is relinquished during the 3 year period ending on the date of the decedent s death. The interpretation of 2038(a)(1) is that it is directed at situations where the transferor-decedent set the machinery in motion that

36 purposefully allows fiduciary powers over the property interest to subsequently return to the transferor-decedent. Estate of Skifter v. Comm r, 468 F.2d 699 (2d Cir. 1972); Estate of Reed v. United States, Civil No (M.D. Fla., May 7, 1975); Rev. Rul , C.B Absent a pre-agreed plan for the first beneficiary spouse to exercise the power of appointment in favor of the grantor spouse, 2038(a)(1) should not apply. VIII. GIFTS TO PARENT S TRUSTS. A wealthy taxpayer with one or both parents alive who do not have substantial wealth (i.e., net worth less than their applicable exclusion amounts) can make $13, annual gifts ($14, beginning in 2014) in trust to take use the parents applicable exclusion amounts for the benefit of the wealthy taxpayer s descendants. A. Structure of the Trust. Typical provisions for a parent s trust include the following: 1. The parent is given a Crummey withdrawal rights so that the gifts will qualify for the $13, annual gift exclusion for present interest gifts. 2. Distributions to the parent are limited to a narrow standard that takes into account other resources available to the party. The expectation is that the trustee likely will never make any distribution to the parent. 3. The parent is given a narrow general power of appointment. For example, the power of appointment might be limited to the creditors of the parent s estate. If difficulties later developed (e.g., the parent develops mild to moderate dementia or becomes under the influence of a person with improper motives), the parent will not be able to appoint the trust to a different individual. 4. Upon the parent s death, the remainder of the trust will pass tax free (due to the small size of the parent s estate) to the wealthy taxpayer s descendants, usually in a generation-skipping trust. 5. The wealthy taxpayer will retain a right that results in a grantor trust, such as a 675(4)(C) non-fiduciary power to reacquire the trust

37 corpus by substituting other property of an equivalent value. This further leverages the transfer. B. Tax Effect of the Gifts. The tax results of the parental trust typically are the following: 1. By using Crummey withdrawal rights and limiting each year s gift to the $13, annual gift exclusion for present interest gifts, the additions to the parental trust do not use any of the wealthy taxpayer s gift tax exclusion amount, estate tax exclusion amount or generation-skipping transfer tax exemption. 2. By creating grantor trust status, the parent does not pay income tax on the trust s taxable income. The wealthy taxpayer s payment of the income tax further enhances the transfer tax free growth of the trust, i.e., the assets that ultimately pass to the wealthy taxpayer s descendants. 3. By giving the parent a general power of appointment, the trust assets will be included in the parent s estate when he or she dies. (a) (b) If the parent s net worth inclusive of the trust is still less than the parent s estate tax applicable exclusion amounts, the trust assets will pass estate tax free to the wealthy taxpayer s descendants or trusts for their benefit. If the parent s net worth inclusive of the trust is still less than the parent s remaining generation-skipping transfer tax exemption, the trust assets will pass free of the generationskipping transfer tax. IX. SUPERCHARGED CREDIT SHELTER TRUSTS. SM The ultimate credit-shelter trust for a surviving spouse who has more than adequate wealth is one that does not make distributions to the spouse yet results in the surviving spouse bearing the income tax burden under the grantor trust rules. 5 5 Mitchell M. Gans, Jonathan G. Blattmachr, and Diana S. C. Zeydel refer to this as a Supercharged Credit Shelter Trust SM. Their excellent article on this topic is Mitchell M. Gans, Jonathan G. Blattmachr, and Diana S. C. Zeydel, SUPERCHARGED CREDIT SHELTER

38 The surviving spouse s payment of the income tax permits the trust estate to grow income tax free. Moreover, during the surviving spouse s lifetime, income can be distributed to descendants without incurring gift tax if it is a sprinkle trust. However, a credit-shelter trust created under the will of the first spouse to die cannot be a grantor trust for the surviving spouse because the surviving spouse is not the grantor. Supercharging refers to a technique to create a credit-shelter trust that will be a grantor trust. A. Structure of the Supercharged Credit Shelter Trust. SM The desired result can be achieved through the use of an inter vivos QTIP trust. The technique is as follows: 1. The grantor spouse creates an inter vivos QTIP trust for donee spouse. (a) (b) The grantor spouse is a spouse with substantial wealth. The plan is structured on the assumption that the grantor spouse may be the second spouse to die and will become the beneficiary of a credit shelter trust. The donee spouse is the spouse who the plan assumes might be the first to die. The trust is structured so that the donee spouse will be treated as creating the credit-shelter trust for estate tax purposes even though he or she is not the person who actually creates the trust. The additional goal, however, is for the grantor spouse, instead of the donee spouse, to be treated as the grantor of the credit-shelter trust for income tax purposes. 2. The grantor will make a QTIP election when creating the trust for the donee spouse. The election must be made on a timely filed gift tax return. Late elections cannot be made. TRUST SM, 52 Probate & Property, July/August Most of the observations and suggestions in this section reflect ideas presented in their article as well as discussions with Mr. Blattmachr. Supercharged Credit Shelter Trust SM is a servicemark of Prof. Gans, Mr. Blattmachr, and Ms. Zeydel, who have granted permission for it to be used without charge provided appropriate attribution is given to them for its use

39 3. As a QTIP trust, the trust qualifies for the gift tax marital deduction, and no gift tax is payable upon creation of the trust. 4. Also because of the QTIP election, the trust is included in the donee spouse s gross estate if the donee spouse dies first While both spouses are alive, the trust is deemed to be wholly owned by the grantor because a grantor is treated as holding all powers or interests held by his or her spouse. 671(e)(1). A grantor is deemed to own a trust where he or she has retained the right to the income and principal of the trust. 676 and 677. Therefore, all of the trust s taxable income (whether allocated to accounting income or to principal) is taxed to the grantor spouse. 6. Assuming the donee spouse is the first to die, the inter vivos QTIP trust will provide that an amount equal to the donee spouse s remaining applicable credit amount is left to a credit-shelter trust for the benefit of the grantor spouse. 7. The assets of the inter vivos QTIP trust are included in the donee spouse s gross estate upon the donee spouse s death (a) (b) However, no estate tax is owed due to the donee spouse s remaining applicable credit amount. Assets in excess of the donee spouse s remaining applicable credit amount can be structured to pass to or for the benefit of the grantor spouse in a form that qualifies for the estate tax marital deduction. If so, no estate tax is owed. 8. The credit shelter trust is not included in the grantor spouse s gross estate. Although 2036 ordinarily includes trust assets in a grantor s gross estate if the grantor is a beneficiary, the QTIP regulations prohibit the IRS from invoking 2036 or 2038 in the surviving spouse s estate in the case of such a lifetime QTIP. See Reg (f)-1(f), ex. 11. B. Grantor Trust Treatment for the Credit Shelter Trust. For income tax purposes, not estate tax purposes, the trust continues to be the grantor spouse s grantor trust after the donee spouse s death if the trustee has discretion to make distributions of income and principal to the grantor spouse. See 676 and 677. It does not matter that it was included

40 in the donee spouse s gross estate under 2044 for estate tax purposes. See Reg (e)(5). The regulation provides that, in the absence of someone exercising a general power of appointment over the trust, the original grantor s status as the grantor continues. C. Effect of Creditor Rights. In most, but not all, states, a grantor s creditors can reach assets if the grantor is entitled or eligible in the discretion of a trustee to receive distributions from a trust that he or she has created. See Restatement (3d) of Trusts The ability of a grantor s creditors to reach trust assets typically results in inclusion of the trust in the gross estate under See, e.g., Outwin v. Comm r, 76 T.C. 153 (1981), acq C.B. 1; Palozzi v. Comm r, 23 T.C. 182 (1954), acq C.B 4; Estate of Paxton v. Comm r, 86 T.C. 785 (1986); Rev. Rul , C.B Although the QTIP regulations preclude the IRS from invoking 2036 and 2038 in this context, they do not preclude the application of 2041, which concerns powers of appointment. See Reg (f)-1(f), ex. 11. These leaves open the risk of inclusion in the grantor s gross estate, and the plan should be structured so that 2041 does not apply to the credit shelter trust created for the grantor spouse s benefit out of the inter vivos QTIP trust he or she created for the first spousal beneficiary. 1. Use of Ascertainable Standards. Section 2041 can be negated through the use of an ascertainable standard relating to health, education, maintenance, or support. If distributions from the credit shelter trust to the grantor spouse are limited by an ascertainable standard, 2041 will not apply even if creditors can access the trust s assets under state law. In states permitting creditors access, creditors are typically only able to reach the amount that the trustee could distribute to the grantor under a maximum exercise of discretion. See, e.g., Vanderbilt Creditor Corp. v. Chase Manhattan Bank, NA, 473 N.Y.S.2d 242 (App. Div. 1984); comment f to Restatement (3d) of Trusts 60. Because Code 2041 excludes from the definition of a general power of appointment a right to property circumscribed by such a standard, including an appropriate standard would preclude the application of Form Trust in an Asset Protection State. The trust can be formed under the laws of a state that does not permit the grantor s creditors to access trust assets (e.g., Alaska, Delaware, Nevada, Rhode Island, South Dakota, Utah, and, to a limited extent, Oklahoma). See, e.g., Estate of German v. United States, 7 Ct. Cl. 641 (1985) (no estate

41 tax inclusion in estate of grantor who was eligible to receive income and corpus from the trust because her creditors could not attach the trust property under the law under which the trust was created). D. Income Tax Basis Following Death of First Spousal Beneficiary. It is not clear whether the basis of the assets in the QTIP trust is stepped up at the death of the donee spouse. 1. The income tax basis of QTIP property included in a decedent s estate under 2044 is its estate tax value. Section 1014(b)(10) provides the following in this regard: Sec Basis of property acquired from a decedent * * * * * (b) Property acquired from the decedent. For purposes of subsection (a), the following property shall be considered to have been acquired from or to have passed from the decedent: * * * * * (10) Property includible in the gross estate of the decedent under section 2044 (relating to certain property for which marital deduction was previously allowed). In any such case, the last 3 sentences of paragraph (9) shall apply as if such property were described in the first sentence of paragraph (9). 2. Because the grantor spouse is the deemed owner of the trust s assets before the death of the donee spouse and will be the deemed owner of the assets in the credit shelter trust, there may be a question whether the grantor-trust rules or the step-up-in basis rule of 1014(b)(10) should govern due to a theory that the assets were owned by the grantor spouse at all times for income tax purposes It appears that the step up in basis rule should control because 1014(b)(10), in providing for a basis adjustment in the case of all QTIPs, does not set forth an exception to the rule with regard to inter vivos QTIP trusts

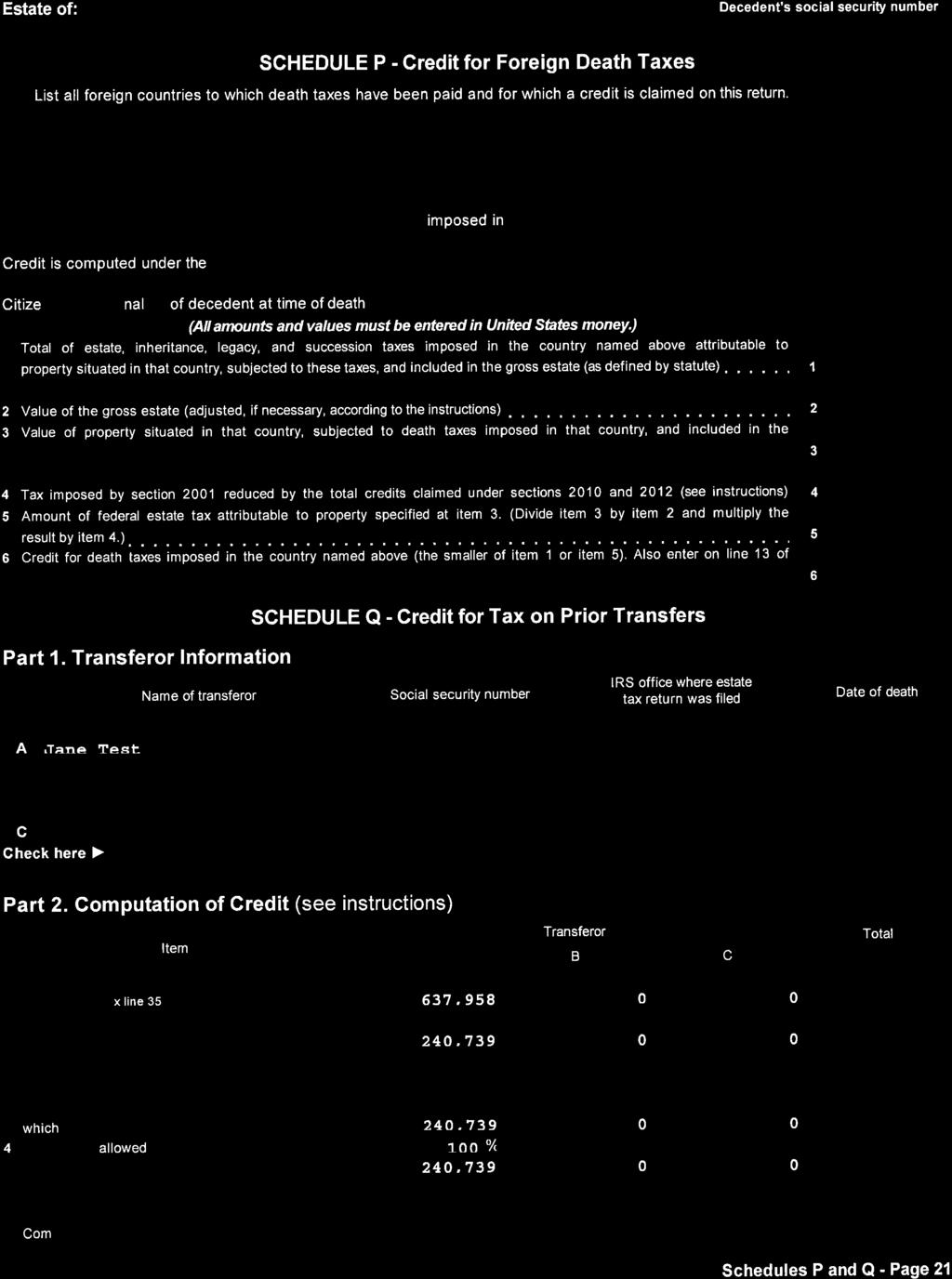

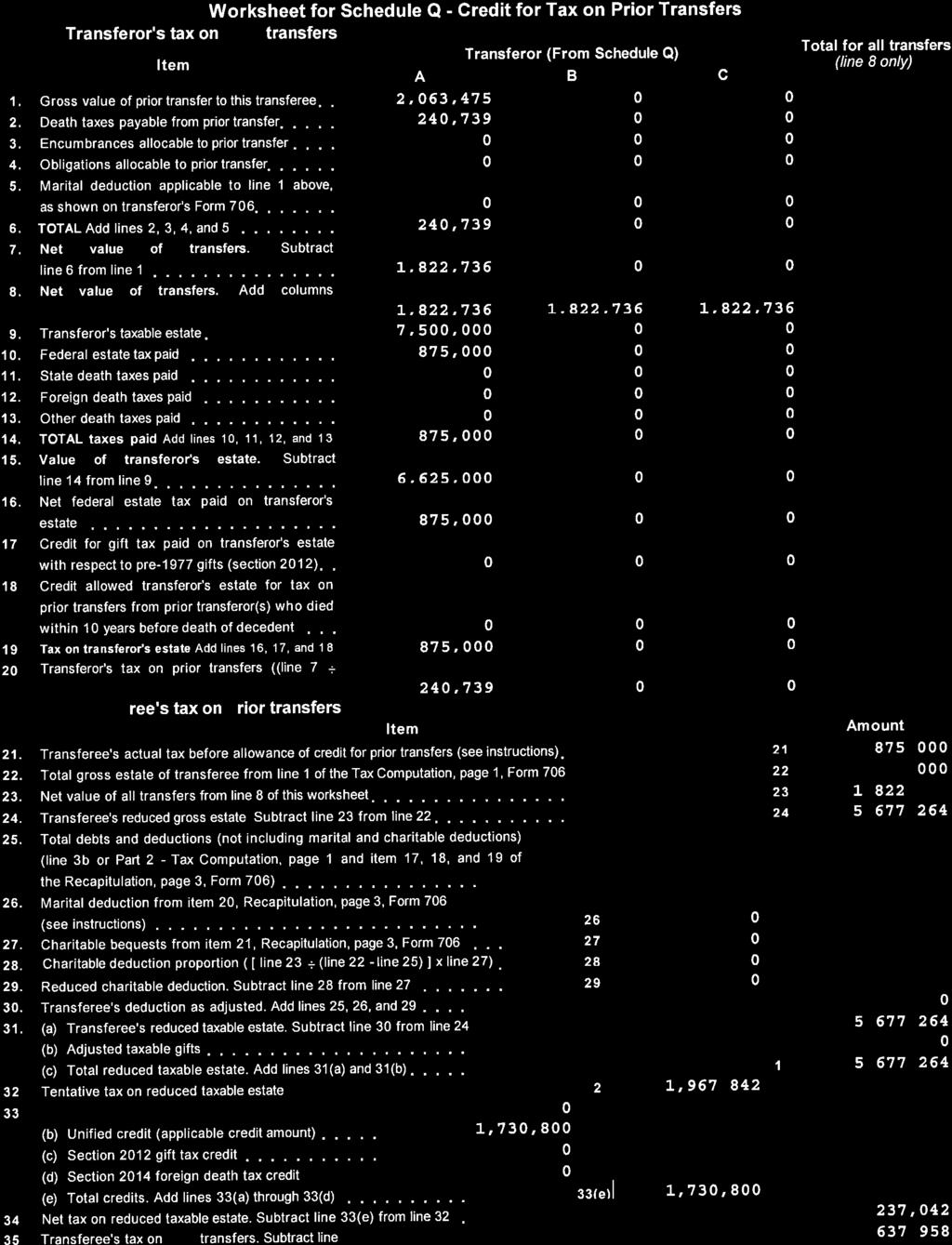

42 X. PLANNING FOR THE CREDIT FOR TAX ON PRIOR TRANSFERS. Before the unlimited marital deduction was added by the Economic Recovery Tax of 1981, estates of the first spouses to die routinely paid estate tax because the estate tax exemption was only $60, Because the surviving spouse most often died within ten years, the 2013 credit for tax on prior transfers was used with regularity. Although this has changed, there are still planning opportunities for the use of this credit. A. Property not Included in Second Decedent Estate. There is a mistaken belief that the credit is not available unless the property from the prior decedent s estate is included in the second decedent s gross estate. However, the regulations provided the following: Sec Credit for tax on prior transfers. (a) In general. A credit is allowed under section 2013 against the Federal estate tax imposed on the present decedent s estate for Federal estate tax paid on the transfer of property to the present decedent from a transferor who died within ten years before, or within two years after, the present decedent s death. See section for definition of the terms property and transfer. There is no requirement that the transferred property be identified in the estate of the present decedent or that the property be in existence at the time of the decedent s death. It is sufficient that the transfer of the property was subjected to Federal estate tax in the estate of the transferor and that the transferor died within the prescribed period of time.... (emphasis added) B. Application to Life Interests. Thus, a pay-all-income interest in a trust can trigger the credit for the surviving spouse s estate even though the interest is excluded from the surviving spouse s estate. This can be achieved by using a pay-all-income credit shelter trust and a QTIP trust that does not make the QTIP election. 1. Example. Assume the following facts: Jane died February 15, 2011 when her husband, George, was age 73, and her net estate was $7,500, $5,000, was left to