A SIGNATURE PROGRAM OF INDIANA GRANTMAKERS ALLIANCE

|

|

|

- Martin James

- 6 years ago

- Views:

Transcription

1 A SIGNATURE PROGRAM OF INDIANA GRANTMAKERS ALLIANCE

2 VERY SCARY (AND NOT SO SCARY) GIFTS October 31, 2013 Phil Purcell, JD Vice President, Ball State Foundation GIFT Legal Consultant *Not to be revised or edited without the written consent of Phil Purcell or the GIFT Team

3 Cemetery Funds Son of Accelerated CRT Ghoul and Shark-Fin CLT Tales from the Darkside: Gift Annuities and Life Insurance Control from the Grave: Donor Restrictions The Devil is in the Details!

4 CEMETERY FUNDS

5 CEMETERY FUNDS Cemetery companies are tax exempt per IRC Section 501(c)(13). Therefore, cemetery companies not eligible to become a designated fund to award grants for general administrative expenses. But eligible for field-of-interest fund for ONLY charitable purposes. Note: Gifts directly to cemetery funds qualify for an income tax (but not estate tax) charitable deduction per special statute. Rev. Rul

6 GRANTS TO CEMETERY COMPANIES Requires expenditure responsibility (ER). Must be paid for charitable purposes or programs of the cemetery such as: 1. Beautifying the community 2. Improving public areas 3. Replacing deteriorating headstones 4. Historic preservation 5. Educating the community about history

7 EXPENDITURE RESPONSIBILITY (ER) No payment to maintain a specific lot or crypt. Follow the five steps of expenditure responsibility!

8 FIVE STEPS OF ER 1. Pre Grant Inquiry: Reasonable investigation of grantee to confirm that grant will be used for charitable purpose. 2. Written Agreement: Spelling out the charitable purpose that grant will be used for. Also to prohibit non-charitable uses of grant. 8

9 FIVE STEPS OF ER 3. Separate Account: Grantee must keep grant funds in separate financial account from all noncharitable funds. 4. Regular Reports: Grantee must provide regular reports on the charitable use of the granted funds Reporting: Community foundation should report all grants requiring ER including name of grantee, dollar amounts and charitable purposes. Use Schedule O to explain details.

10 QUESTIONS?

11 SON OF ACCELERATED CHARITABLE REMAINDER TRUST

12 LONG TERM RETIREMENT PLANNING WITH CHARITABLE REMAINDER TRUSTS

13 BASICS OF CRTS Operated pursuant to a trust document that complies with state and federal law. IRC 664. See model CRT template documents provided by IRS ( to offer a safe harbor so long as substantially followed. Counsel can add state trust code powers of trustee, etc.

14 BASICS OF CRTS Donor and/or others designated by donor receive income for life or a term of years not to exceed 20 years. Fixed income payout percentage between 5% and 50%. Established during life or at death. Remainder to charity is irrevocable. But donor may retain right to change the recipient charity(ies) Does charity disclose this fact?

15 TAX BENEFITS OF A CRT Income tax charitable deduction for present value of charity s future interest. Income tax deduction value must be at least 10% of original value of donated cash or assets. Donated cash or assets removed from taxable estate. Assets donated to CRT are sold without capital gains tax liability since CRT is a tax-exempt trust.

16 Standard Unitrust (SCRUT). Net Income Unitrust (NICRUT). Net Income with Make-Up Unitrust (NIMCRUT). Flip CRT (begins as NICRUT or NIMCRUT and flips to a SCRUT). Annuity Trust (CRAT). TYPES OF CRTS

17 PLANNING OPPORTUNITIES Sell assets without capital gains tax. Transforms non-income producing property into income for retirement or for loved ones. Trust document may define income to include realized capital gain at the discretion of the trustee. As trust principal value grows, so does income with unitrusts. Removes worry of property management.

18 FLIP CRT Flip from NICRUT or NIMCRUT to SCRUT. Treas. Reg (a)(1)(i)(c). Excellent vehicle to deal with real estate that may be slow to sell. Get income tax deduction when property is donated to trust. Pay income when asset is sold and proceeds reinvested and trust flips.

19 Triggered on a specific date or by an occurrence which is not discretionary or within the control of any person. The regulations provide specific examples. Treas. Reg (a)(1)(i)(c).

20 SON OF AN ACCELERATED CRT Donate appreciated stock % payout for 2-4 years. Stock not sold right away. Borrow $ or forward sales contract to provide cash for first 1-2 years of payout. Tax -free return of principal. Escape gain, receive income tax deduction. Little or nothing left for charity!

21 FULL MONTY/CHUTZPAH CRT Original Accelerated CRT concept was prohibited by amendments to IRC Sec. 664 in 1997 and 1998 (e.g., 10% minimum deduction, 50% maximum payout, etc.). Treasury Decision 8926 prohibits Son of Accelerated CRT.

22 MINIMUM CHARITABLE DEDUCTION RULE: EXAMPLE $100,000 donated to CRT Calculated deduction must be at least 10% x $100,000 = $10,000 Otherwise, CRT will not qualify for federal income, gift and estate tax benefits!

23 QUESTIONS?

24 GHOUL CHARITABLE LEAD TRUST

25 Charitable Lead Trusts This image cannot currently be displayed. This image cannot currently be displayed. Charity 1 Gift Donors Charity 2 At end of trust term, the principal is given to individuals named by donor

26 EXAMPLE $1,000,000 donated to 20 year charitable lead annuity trust 5% payout; 7% total return on assets 2% Adjusted Federal Mid-term rate (Nov 2013) $1,819,910 calculated to family at end of trust $1,000,000 million paid to charity during term $182,430 taxable gift to heirs

27 TAX SAVINGS Gift/estate tax savings increase as does % payout and term of payments. No gift/estate tax when trust assets received by heirs freeze technique. Lifetime or testamentary transfers. Lifetime trust: No step-up in basis for heirs. But compare estate with capital gains tax rates! Testamentary trust: Step-up in basis.

28 WHEN AFT DROPS Increase in tax deduction for Remainder Interest in Residence or Farm. Reduction in gift or estate tax liability for Charitable Lead Trust. Minimum impact on CRUTs. Gift Annuity income value increases but deduction decreases. Charitable Remainder Annuity Trust tax deduction decreases. Beware 10% deduction limit and 5% probability test.

29 ER OR GHOUL CLAT Format: Link payout from CLAT to a recruited (for a fee?) young person with a nominally long life expectancy who, in reality, is not well. Gift tax paid at much reduced rate than if an older person (e.g., parent) had been the measuring life. Prohibited by Treasury Decision 8923.

30 JAWS!!

31 SHARK-FIN CLAT: JAWS!? Nominal early payments. Back-Loaded large balloon payments. Maximize early growth to allow for more to heirs. Zero-out gift/estate tax. Life insurance investment to pay balloon.

32 SHARK-FIN CLAT IRS form annotations allow variable payments - but no specific guidance. Authority suggests de minimis payments may be disregarded and that variable payments must be reconsidered annually. Potential self-dealing if charity s payments are at risk by back loading investments. Estate Planning Journal, October 2010.

33 QUESTIONS?

34 TALES FROM THE DARKSIDE

35 CHARITABLE GIFT ANNUITY Contract between donor and charity. Donor gives assets, charity provides fixed and guaranteed income for 1 or 2 lives. Rates of return: American Council on Gift Annuities Rate assumptions: life expectancy, market growth, costs. for current rates and state laws.

36 GIFT ANNUITY RATES Age % Age % Age % Age % Age % Age % Age %

37 GIFT ANNUITY BENEFIT Fixed income for life at attractive rates. Current income tax charitable deduction. Tax-free return of principal. Spread of capital gains tax. Removal from estate tax. Note: Potential gift tax if paid to persons other than donor or spouse.

38 PHILANTHROPY PROTECTION ACT 1995/1997 Class action lawsuit over gift annuities as violation of Sherman Anti-Trust Law. New disclosure requirements for gift annuities and trust investments. Provide disclosure before closure of gift annuity: summary of assets and liabilities. Audited financial statement not required.

list gift annuities as a Top Ten Scam.")

39 GIFT ANNUITY STATE REGULATIONS Charity bankruptcy in Arizona. North American Securities Administrators Association (NASAA) list gift annuities as a Top Ten Scam. Summary of state laws: Not regulated in Indiana per IC

40 TRICK OR TREAT? COMMISSIONS FOR GIFT ANNUITIES Payment to financial advisor by charity for referral of gift annuity donors. Aggressive marketing. Violates Ethical Standards. See White Paper at

41 COMMISSIONS FOR GIFT ANNUITIES: PROBLEMS 1. Potential SEC regulation. 2. State insurance licensing. 3. State securities regulation. 4. Potential reduction of deduction. 5. Reduces charitable residual. 6. State solicitation laws.

42 VERY SCARY! National Community Foundation of New Life International founded by Norvell Olive has paid commissions for gift annuity referrals. No longer soliciting gift annuities. National Foundation of America (NFOA), Richard and Susan Olive, officers. Tennessee Department of Commerce and Insurance obtained control of NFOA for doing insurance business without certificate of authority. Also, NFOA has not received 501(c)(3) status. Other states involved. rce/documents/nfoa_receiver ship_order_ pdf

43 REINSURANCE Insurance company pays charity for right to death benefit of policies. Insurance company pays annuitant. Charity still legally obligated to pay if insurance company cannot. Charity may receive significantly less than the residual projected by ACGA. A financial investment decision! Beware overly cautious board of directors.

44 QUESTIONS?

45 GIFTS OF LIFE INSURANCE: THE GOOD Charity as Beneficiary only. Charity as Owner and Beneficiary with no loan. Gift of Existing Policy which has an outstanding loan.

46 CHARITY BENEFICIARY ONLY Charity may be primary or contingent beneficiary. No income tax charitable deduction. Qualifies for estate tax charitable deduction.

.")

47 CHARITY OWNER AND BENEFICIARY (NO LOANS) New Policy: Charitable deduction for premium paid (subject to AGI limit). In Force Policy: Charitable deduction for lesser of donor s basis and policy s interpolated terminal reserve. IRC Sec. 170(e). Paid Up Policy: Lesser of basis or replacement cost. Term Policy: Deduction for unused premium.

48 CHARITY OWNER AND BENEFICIARY (NO LOANS) Cash gives to charity to cover premium: 50% AGI deduction limit so long as no legally binding commitment by charity to pay. Helpful for charity to receive premium notices to assure annual payments. Idea: Donate stock that is used by charity to pay premium. Premium paid directly to insurance to companycould be 30% limit. A gift for the benefit of a charity.

49 CHARITY OWNER AND BENEFICIARY (LOAN) Deemed a bargain sale. Donor s basis is allocated between the sale portion and the gift portion of the transaction on a pro rata basis. Treas. Reg Donor s adjusted basis allocable to the gift portion is deemed to be deducible gift to charity.

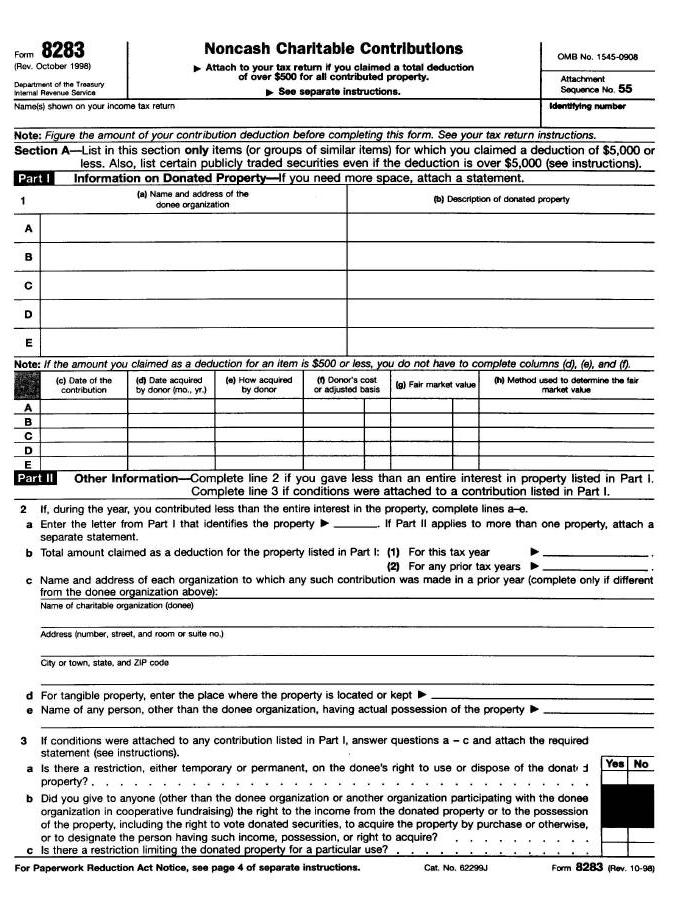

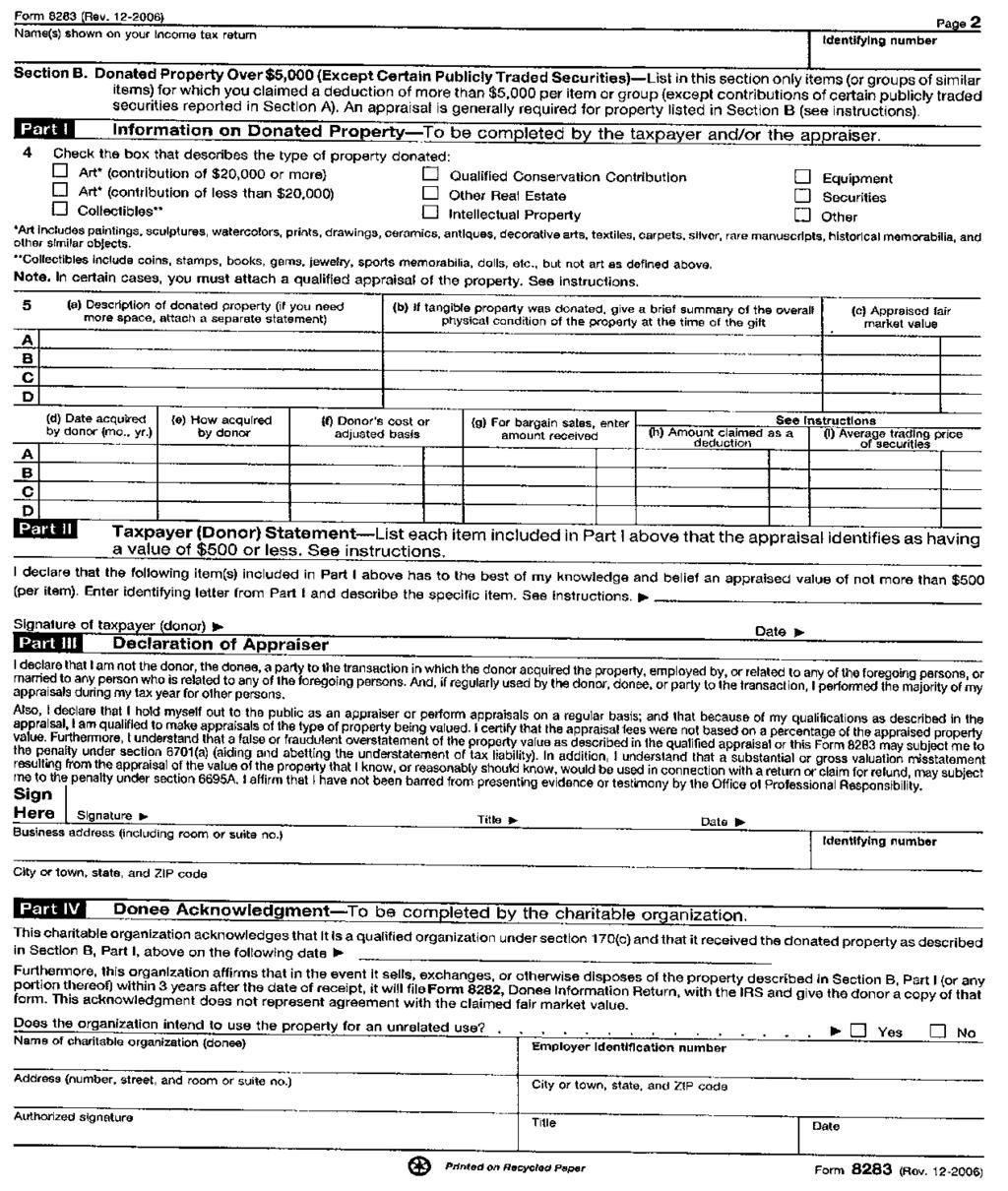

50 CLAIMING THE CHARITABLE DEDUCTION Indiana: Charity has insurable interest in donors: Indiana Code Sec Written acknowledgement describing the donated policy. IRS Form 8283: Noncash Charitable Contributions. Qualified independent appraisal? IRS Form 712: Life Insurance Statement IRS Form 8282: Donee Information Return.

51 LIFE INSURANCE: THE POTENTIALLY BAD AND UGLY!

52 THE POTENTIALLY BAD AND UGLY! Premium Financed: loan to pay premiums Group insured: board members, others Commercial annuities: depends on contract date Charitable reverse split dollar: charity and family as beneficiaries legally prohibited! See Life Insurance Valuation Guidelines at

53 QUESTIONS?

54 CONTROL FROM THE GRAVE! DEALING WITH DONOR RESTRICTIONS

.")

55 WHAT IS A CHARITABLE GIFT? To qualify for tax benefits: income tax charitable deduction, capital gains tax savings. Definition of gift : Intent plus objective test (i.e., actual transfer to qualified charitable organization). No return benefit or quid pro quo. U.S. v. American Bar Endowment, 477 U.S. 105 (1986).

56 NO STRINGS ATTACHED Deduction denied if conduit for a person. PLR Deduction denied if donor asserts inappropriate control or personal benefit. No deduction if gift is to be returned if restriction unfulfilled (right of reverter, right of first refusal). Ferguson, 21 B.T.A (1930).

57 DONOR ADVISED FUNDS U.S. v. Mosley, Northern District of California (2003). Charitable income tax deductions claimed for six-figure gifts to DAF held by National Heritage Foundation. Grants from DAF to pay tuition for education at private school of donor s child. Criminal tax evasion: jail and financial penalties.

.")

58 IRS PUBLICATION 526: CHARITABLE CONTRIBUTIONS No deduction for gift of time/services. No deduction for loan of property. No deduction for gifts of partial interest in property - with specific exceptions for split interest gifts (e.g., charitable remainder trust, etc.). Gift of ordinary income property limited to basis (e.g., gift of art by artist).

59 CASE STUDY: THE ART OF THE STEAL Bequest: Dr. Albert C. Barnes. Billion $ art collection. Merion, PA : remain in location. Bankrupt museum: Move? Court rules: Move it! Doctrines of cy pres and equitable deviation. Montgomery County, Pennsylvania Orphan's Court (2004).

60 DEALING WITH RESTRICTIONS Document donor intent and purpose as clearly as possible. Suggest a Plan B or Plan C. Always remember the importance of the variance power!

61 QUESTIONS?

62 THE DEVIL IS IN THE DETAILS!

63 IRS PUBLICATION 1771: ACKNOWLEDGEMENT Requirements for gift receipts: 1. Name of charity recipient. 2. Date of gift (disputed requirement). 3. Dollar value if cash gift. 4. Description if non-cash gift. 5. Value of goods or services received by donor if above de minimis token, OR 6. Statement: No goods or services received in exchange for gift.

64 GIFT RECEIPTS Tax Court denied a $23,000 charitable income tax deduction, even though IRS conceded charitable gifts were made. Charity did not add phrase "you received no goods or services" on receipt. Law does not allow for corrections after the due date for income tax return. Durden v. Commissioner, T.C. Memo (May 17, 2012).

65 NON-CASH GIFTS: FEDERAL REQUIREMENTS IRS Forms 8283 (donor) and 8282 (charity): Disclosure of value and subsequent sale of non-cash gifts. Pension Protection Act of New guidance by IRS re: qualified appraisal and appraiser. See

66 VALUATION OF NON-CASH GIFTS U.S. Tax Court acknowledged property worth over $18 million (and not over-valued) was donated to a charitable remainder trust. ENTIRE charitable deduction disallowed - appraisal requirements not satisfied. No independent appraisal and not all information provided on Mohamed v. Commissioner, T.C. Memo (May 29, 2012).

67

68

69 GIFTS OF TANGIBLE PERSONAL PROPERTY If use is unrelated to mission, then deduction is limited to lesser of FMV and cost basis. Examples: Grain, livestock, artwork, equipment. Applies to gifts for charity auctions. Special rule for automobile gifts

70 SALE OF DONATED PROPERTY IRS Form 8282: Reporting proceeds of sale of donated property by charitable organization. Filed if property is sold within three years of date of gift. IRS audit red flag if value of claimed for charitable deduction significantly exceeds the charitable organization s sale value.

71

72

73 If the claimed charitable deduction exceeds $5,000, then a qualified independent appraisal is required of donor. Exception for publicly traded stock. Other exceptions. Donor pays for appraisal. See IRS Publication 561. VALUATION

74

75 GIFT OF BONDS Income tax charitable deduction for full current fair market value of bonds. Complete escape of capital gains tax. Gift to a charitable remainder trust or in exchange for a gift annuity. Pays income to donor and/or loved ones. Income tax charitable deduction for present value. Escape capital gains tax.

76 GIFTS OF S STOCK: WARNINGS 1. The donor s charitable deduction is likely not fair market value. Similar to gift by partnership, i.e., must be reduced by potential gain in property. Note: Fair market value allowed for gifts at death. 2. Charity will owe unrelated business income tax on income earned by the S Corp if stock is not redeemed or sold. 3. Charitable remainder and lead trusts accepting S stock disqualifies S status.

77 GIFTS OF TIME SHARES Gift of a contract right. Requires independent valuation if deduction claimed over $5,000. Due diligent review of time share fees, maintenance costs, insurance, rights of tenant and land owner relative to timing of use, use by others, marketability, etc.

78 QUESTIONS?

79 THANKS FOR THE MUMMYRIES! R.I.P. SAMMY TERRY!

80

Using Your Assets to Promote your Values. Lawrence M. Lehmann, JD, AEP, CAP Lehmann Norman & Marcus LC

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Kingdom Advisors Charitable Giving Tool Kit

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA Tel: (310) Fax: (310)

Fax: (310)") Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA 90067 Tel: (310) 553-8844 Fax: (310) 553-5165 jgeida@weinstocklaw.com IRC 170(c), a contribution or gift to or for the

Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA 90067 Tel: (310) 553-8844 Fax: (310) 553-5165 jgeida@weinstocklaw.com IRC 170(c), a contribution or gift to or for the

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

Planned Giving. For Beginners

Planned Giving For Beginners What is Planned Giving? The integration of personal, financial and estate planning goals using lifetime or testamentary charitable giving with benefits to the donor ANNUAL

Planned Giving For Beginners What is Planned Giving? The integration of personal, financial and estate planning goals using lifetime or testamentary charitable giving with benefits to the donor ANNUAL

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

Charitable Remainder Trust

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life or a period of years. At the end

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life or a period of years. At the end

Charitable Planning CLIENT GUIDE

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Remainder Trust

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life, or for a period of years (not

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life, or for a period of years (not

Charitable Trusts. Charitable Trusts

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

Comprehensive Charitable Planning

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Irrevocable Gift Vehicles

2014 Western Regional Planned Giving Conference P R I M E R S E C T I O N I I I : I R R E V O C A B L E P L A N N E D G I F T S C H A R I T A B L E G I F T A N N U I T I E S L I F E I N S U R A N C E C

2014 Western Regional Planned Giving Conference P R I M E R S E C T I O N I I I : I R R E V O C A B L E P L A N N E D G I F T S C H A R I T A B L E G I F T A N N U I T I E S L I F E I N S U R A N C E C

Stupid Charitable Tricks:

Stupid Charitable Tricks: Charitable Planning Mistakes I Have Seen Ramsay Slugg November, 2017 Disclosure (use this if the next slide N/A) IMPORTANT: This presentation is designed to provide general information

Stupid Charitable Tricks: Charitable Planning Mistakes I Have Seen Ramsay Slugg November, 2017 Disclosure (use this if the next slide N/A) IMPORTANT: This presentation is designed to provide general information

A Guide to Planned Giving

A Guide to Planned Giving ~ Boys & Girls Clubs ~ 2 - A Guide to Plan Giving What is Planned Giving? The integration of personal, financial and estate planning goals with lifetime or testamentary charitable

A Guide to Planned Giving ~ Boys & Girls Clubs ~ 2 - A Guide to Plan Giving What is Planned Giving? The integration of personal, financial and estate planning goals with lifetime or testamentary charitable

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Charitable Gifting: Overview and Tax Implications. Overview. Tax Implications - Charitable Deduction Rules

Overview Charitable Gifting: Overview and Tax Implications The desire to assist a charitable organization must be a primary motive for making a gift; if no charitable inclination exists, charitable giving

Overview Charitable Gifting: Overview and Tax Implications The desire to assist a charitable organization must be a primary motive for making a gift; if no charitable inclination exists, charitable giving

WHAT S NEW IN PLANNED GIVING AND WHY PRESENTED TO THE TAMPA BAY PLANNED GIVING COUNCIL NOVEMBER 15, 2000

WHAT S NEW IN PLANNED GIVING AND WHY PRESENTED TO THE TAMPA BAY PLANNED GIVING COUNCIL NOVEMBER 15, 2000 BY LINDA SUZZANNE GRIFFIN, J.D., LL.M., C.P.A. LINDA SUZZANNE GRIFFIN, P.A. 1455 COURT STREET CLEARWATER,

WHAT S NEW IN PLANNED GIVING AND WHY PRESENTED TO THE TAMPA BAY PLANNED GIVING COUNCIL NOVEMBER 15, 2000 BY LINDA SUZZANNE GRIFFIN, J.D., LL.M., C.P.A. LINDA SUZZANNE GRIFFIN, P.A. 1455 COURT STREET CLEARWATER,

CHARITABLE GIFTS. A charitable gift has a number of different tax benefits, which benefits differ if the gift is made during life or at death.

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

numer cal anal ysi shown, esul nei her guar ant ees nor ect ons, and act ual esul may gni cant Any assumpt ons est es, on, her val ues hypot het cal

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Charitable Gifting: Overview and Tax Implications

Charitable Gifting: Overview and Tax Implications Overview The desire to assist a charitable organization must be a primary motive for making a gift; if a charitable inclination does not exist, charitable

Charitable Gifting: Overview and Tax Implications Overview The desire to assist a charitable organization must be a primary motive for making a gift; if a charitable inclination does not exist, charitable

Philip M. Purcell, JD Consultant for Philanthropy Copyright All rights reserved

Top Ten (or More) Legal Issues for Community Foundations Philip M. Purcell, JD Consultant for Philanthropy pmpurcell@outlook.com Copyright 2017@ All rights reserved Top Ten (or) More 1. 2. 3. 4. 5. 6.

Top Ten (or More) Legal Issues for Community Foundations Philip M. Purcell, JD Consultant for Philanthropy pmpurcell@outlook.com Copyright 2017@ All rights reserved Top Ten (or) More 1. 2. 3. 4. 5. 6.

CHARITABLE PLANNING. Illinois State Bar Association Trust & Estate Section Estate Planning: Hot Topics. Chicago, Illinois October 10, 2013

CHARITABLE PLANNING Illinois State Bar Association Trust & Estate Section Estate Planning: Hot Topics Chicago, Illinois October 10, 2013 James A. Nepple Nepple Law, PLC 1515 Fifth Avenue, Suite 320 Moline,

CHARITABLE PLANNING Illinois State Bar Association Trust & Estate Section Estate Planning: Hot Topics Chicago, Illinois October 10, 2013 James A. Nepple Nepple Law, PLC 1515 Fifth Avenue, Suite 320 Moline,

Thursday, September WRM# 14-35

Thursday, September 4 2014 WRM# 14-35 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms.

Thursday, September 4 2014 WRM# 14-35 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms.

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives. 41st Annual MPGC Conference November 15-16, 2017

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

Donations of Complex Assets to the LDS Church. Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT (801)

") Donations of Complex Assets to the LDS Church Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT 84111 (801) 323-5946 bandrewsen@kmclaw.com Overview of Presentation What is a complex asset? Almost

Donations of Complex Assets to the LDS Church Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT 84111 (801) 323-5946 bandrewsen@kmclaw.com Overview of Presentation What is a complex asset? Almost

charitable contributions

charitable contributions Your ability to control when and how you make charitable contributions can lower your income tax bill, effectively reducing the actual cost of any gift you make, while fulfilling

charitable contributions Your ability to control when and how you make charitable contributions can lower your income tax bill, effectively reducing the actual cost of any gift you make, while fulfilling

1/22/2013. Charitable Giving 2013 and Beyond. Today s Agenda. Who Gave in 2011? The Charitable Giving Environment

Charitable Giving 2013 and Beyond January 22, 2013 The Rivers Club 8:00 a.m. 10:00 a.m. Registration begins at 7:30 a.m. Today s Agenda The Charitable Giving Environment Understanding Complex Charitable

Charitable Giving 2013 and Beyond January 22, 2013 The Rivers Club 8:00 a.m. 10:00 a.m. Registration begins at 7:30 a.m. Today s Agenda The Charitable Giving Environment Understanding Complex Charitable

Charitable Giving and Beyond. January 22, 2013 The Rivers Club 8:00 a.m. 10:00 a.m. Registration begins at 7:30 a.m.

Charitable Giving 2013 and Beyond January 22, 2013 The Rivers Club 8:00 a.m. 10:00 a.m. Registration begins at 7:30 a.m. Today s Agenda The Charitable Giving Environment Understanding Complex Charitable

Charitable Giving 2013 and Beyond January 22, 2013 The Rivers Club 8:00 a.m. 10:00 a.m. Registration begins at 7:30 a.m. Today s Agenda The Charitable Giving Environment Understanding Complex Charitable

2016 Charitable Giving Review

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

Understanding CRTs. A Summary of Charitable Remainder Trusts (CRTs) VLC

VLC") Understanding CRTs A Summary of Charitable Remainder Trusts (CRTs) VLC0439-0917 GET READY FOR RETIREMENT If your retirement planning objectives include lifetime income planning, estate tax reduction, 1

Understanding CRTs A Summary of Charitable Remainder Trusts (CRTs) VLC0439-0917 GET READY FOR RETIREMENT If your retirement planning objectives include lifetime income planning, estate tax reduction, 1

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

CRTs in Midlife Crisis: Terminating, Accelerating and Fixing Charitable Remainder Trusts

CRTs in Midlife Crisis: Terminating, Accelerating and Fixing Charitable Remainder Trusts David Wheeler Newman Mitchell Silberberg & Knupp LLP CRTs in Midlife Crisis: Terminating, Accelerating and Fixing

CRTs in Midlife Crisis: Terminating, Accelerating and Fixing Charitable Remainder Trusts David Wheeler Newman Mitchell Silberberg & Knupp LLP CRTs in Midlife Crisis: Terminating, Accelerating and Fixing

Presented by Richard D. Cirincione 677 Broadway Albany, NY Direct: Fax:

Presented by Richard D. Cirincione 677 Broadway Albany, NY 12207 Direct: 518-447-3389 Fax: 518-867-4789 646 Plank Road, Suite 206 Clifton Park, New York 12065 518-383-9200 518-867-4789 facsimile cirincione@mltw.com

Presented by Richard D. Cirincione 677 Broadway Albany, NY 12207 Direct: 518-447-3389 Fax: 518-867-4789 646 Plank Road, Suite 206 Clifton Park, New York 12065 518-383-9200 518-867-4789 facsimile cirincione@mltw.com

The Advisor s Guide to Donating Illiquid Assets

The Advisor s Guide to Donating Illiquid Assets by Barbara Benware Vice President, Investment Oversight and Risk and Denise Schuh Director, Charitable Strategies Group About the authors: Barbara Benware

The Advisor s Guide to Donating Illiquid Assets by Barbara Benware Vice President, Investment Oversight and Risk and Denise Schuh Director, Charitable Strategies Group About the authors: Barbara Benware

Giving Today to Guarantee Tomorrow: A Lesson in Charitable Giving

Giving Today to Guarantee Tomorrow: A Lesson in Charitable Giving A careful review of the various ways to structure charitable gifts can help make your gifts more meaningful, both to you and to the charities

Giving Today to Guarantee Tomorrow: A Lesson in Charitable Giving A careful review of the various ways to structure charitable gifts can help make your gifts more meaningful, both to you and to the charities

SHOULD CHARITABLE GIVING BE A PART OF MY ESTATE PLAN?

by Layne T. Rushforth Summary Charitable contributions not only entitle the donor to an income-tax deduction, but may also accomplish certain estate-planning objectives. Such contributions can be made

by Layne T. Rushforth Summary Charitable contributions not only entitle the donor to an income-tax deduction, but may also accomplish certain estate-planning objectives. Such contributions can be made

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER Patricia M. Annino, Attorney Prince Lobel Tye LLP Birmingham Estate Planning Council May 20, 2016 WHY IS IT IMPORTANT? Closely held business owners

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER Patricia M. Annino, Attorney Prince Lobel Tye LLP Birmingham Estate Planning Council May 20, 2016 WHY IS IT IMPORTANT? Closely held business owners

Planned Giving 101 The Basics or So, this is how we ll build our endowment! A Presentation for 2014 Management Conference Magic and Mayhem

Planned Giving 101 The Basics or So, this is how we ll build our endowment! A Presentation for 2014 Management Conference Magic and Mayhem by James E. Gillespie, President & CEO of P.O. Box 50332 Indianapolis,

Planned Giving 101 The Basics or So, this is how we ll build our endowment! A Presentation for 2014 Management Conference Magic and Mayhem by James E. Gillespie, President & CEO of P.O. Box 50332 Indianapolis,

Life Income Gifts 4/19/2016. How a Life Income Gift Works. Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation

Life Income Gifts Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation How a Life Income Gift Works Gift Donor Life Income Gift Remainder to Charity Income tax deduction

Life Income Gifts Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation How a Life Income Gift Works Gift Donor Life Income Gift Remainder to Charity Income tax deduction

GOOD CHOICES: WHEN TO CHOOSE BETWEEN A GIFT ANNUITY OR CHARITABLE REMAINDER TRUST

GOOD CHOICES: WHEN TO CHOOSE BETWEEN A GIFT ANNUITY OR CHARITABLE REMAINDER TRUST NATIONAL CAPITAL GIFT PLANNING COUNCIL S 18TH ANNUAL PLANNED GIVING DAYS CONFERENCE MAY 14, 2010 All rights reserved Presented

GOOD CHOICES: WHEN TO CHOOSE BETWEEN A GIFT ANNUITY OR CHARITABLE REMAINDER TRUST NATIONAL CAPITAL GIFT PLANNING COUNCIL S 18TH ANNUAL PLANNED GIVING DAYS CONFERENCE MAY 14, 2010 All rights reserved Presented

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

EXPLORING THE FUTURE OF GIFT PLANNING 2017 WESTERN REGIONAL PLANNED GIVING CONFERENCE

EXPLORING THE FUTURE OF GIFT PLANNING 2017 WESTERN REGIONAL PLANNED GIVING CONFERENCE Charitable Gift Annuities: sticking your toe in the water Beginner Track 2:00-3:15, Thursday, June 1, 2017 (Beginning

EXPLORING THE FUTURE OF GIFT PLANNING 2017 WESTERN REGIONAL PLANNED GIVING CONFERENCE Charitable Gift Annuities: sticking your toe in the water Beginner Track 2:00-3:15, Thursday, June 1, 2017 (Beginning

Charitable Remainder Trusts

Charitable Remainder Trusts LIFE INCOME GIFTS In the simplest terms, a life income gift is a plan that allows a donor to make a contribution to charity and receive an income in return. Depending upon the

Charitable Remainder Trusts LIFE INCOME GIFTS In the simplest terms, a life income gift is a plan that allows a donor to make a contribution to charity and receive an income in return. Depending upon the

A Guide to Planned Giving

A Guide to Planned Giving 2 Dear Friend, Are you looking for ways to save on your taxes this year through charitable giving? Would you like to avoid capital gains tax on the sale of your appreciated assets?

A Guide to Planned Giving 2 Dear Friend, Are you looking for ways to save on your taxes this year through charitable giving? Would you like to avoid capital gains tax on the sale of your appreciated assets?

A Guide to Planned Giving

A Guide to Planned Giving - A Guide to Plan Giving What is Planned Giving? The integration of personal, financial and estate planning goals with lifetime or testamentary charitable giving. An opportunity

A Guide to Planned Giving - A Guide to Plan Giving What is Planned Giving? The integration of personal, financial and estate planning goals with lifetime or testamentary charitable giving. An opportunity

The best-laid philanthropic plans sometimes go astray. Priorities

Professional TAX & ESTATE PLANNING Notes 1 2 3 4 If you think a colleague would like to receive complimentary copies of Professional Notes, or if you d like past issues, e-mail us at mds@nyct-cfi.org.

Professional TAX & ESTATE PLANNING Notes 1 2 3 4 If you think a colleague would like to receive complimentary copies of Professional Notes, or if you d like past issues, e-mail us at mds@nyct-cfi.org.

Pointers in Selecting Assets to Fund Charitable Trusts

Pointers in Selecting Assets to Fund Charitable Trusts Publication: Estate Planning Magazine Charitable trusts will continue to be an important part of the thoughtful estate planner's repertoire in our

Pointers in Selecting Assets to Fund Charitable Trusts Publication: Estate Planning Magazine Charitable trusts will continue to be an important part of the thoughtful estate planner's repertoire in our

RBC Wealth Management December 14, 2010

Matthew E. Kehoe, CFP, AWM Vice President - Financial Consultant 57 River Street Suite 102 Wellesley, MA 02481 781-263-1029 888-760-8177 m.kehoe@rbc.com www.rbcfc.com/matthew.kehoe Charitable Giving Page

Matthew E. Kehoe, CFP, AWM Vice President - Financial Consultant 57 River Street Suite 102 Wellesley, MA 02481 781-263-1029 888-760-8177 m.kehoe@rbc.com www.rbcfc.com/matthew.kehoe Charitable Giving Page

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ Fax

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

2018 Federal Tax Pocket Guide

2018 Federal Tax Pocket Guide For Advisers and Planners n Federal Individual Income Tax n Income Tax on Estates and Trusts n Federal Corporation Tax n Federal Income Tax on Capital Gains n Federal Alternative

2018 Federal Tax Pocket Guide For Advisers and Planners n Federal Individual Income Tax n Income Tax on Estates and Trusts n Federal Corporation Tax n Federal Income Tax on Capital Gains n Federal Alternative

Charitable Giving: Tax Benefits and Strategies

Charitable Giving: Tax Benefits and Strategies CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM Contents 1 Introduction 2 Overview of Tax Benefits 3 Tax Treatment of Gifts

Charitable Giving: Tax Benefits and Strategies CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM Contents 1 Introduction 2 Overview of Tax Benefits 3 Tax Treatment of Gifts

Adventures in Charitable Planning. Robert W. Dietz, CFA Director Wealth Strategies

2018 Adventures in Charitable Planning Robert W. Dietz, CFA Director Wealth Strategies robert.dietz@bernstein.com Bernstein does not provide tax, legal, or accounting advice. In considering the information

2018 Adventures in Charitable Planning Robert W. Dietz, CFA Director Wealth Strategies robert.dietz@bernstein.com Bernstein does not provide tax, legal, or accounting advice. In considering the information

Marty Langley 210 West Millbrook Rd. Raleigh, NC Charitable Giving

Marty Langley 210 West Millbrook Rd. Raleigh, NC 27609 919-841-9642 Marty.Langley@RaymondJames.com Charitable Giving Page 2 of 7 Charitable Giving When developing your estate plan, you can do well by doing

Marty Langley 210 West Millbrook Rd. Raleigh, NC 27609 919-841-9642 Marty.Langley@RaymondJames.com Charitable Giving Page 2 of 7 Charitable Giving When developing your estate plan, you can do well by doing

Charitable Lead Trusts in the New Tax Landscape

Charitable Lead Trusts in the New Tax Landscape Northern California Planned Giving Planned Giving Conference May 4, 2018 Vivian U. Redsar, Esq. Manatt, Phelps & Phillips, LLP Sarah Copeland Jordan Park

Charitable Lead Trusts in the New Tax Landscape Northern California Planned Giving Planned Giving Conference May 4, 2018 Vivian U. Redsar, Esq. Manatt, Phelps & Phillips, LLP Sarah Copeland Jordan Park

TAX ISSUES IN INTERNATIONAL PHILANTHROPY. Ellen E. Halfon, Esq. Jones Day September 24, 2010

TAX ISSUES IN INTERNATIONAL PHILANTHROPY Ellen E. Halfon, Esq. Jones Day September 24, 2010 I. General Tax Hurdles for Direct Gifts/Grants to Foreign Charities A. Individuals federal income tax charitable

TAX ISSUES IN INTERNATIONAL PHILANTHROPY Ellen E. Halfon, Esq. Jones Day September 24, 2010 I. General Tax Hurdles for Direct Gifts/Grants to Foreign Charities A. Individuals federal income tax charitable

Introduction. 1. Bequests Charitable Gift Annuity Charitable Remainder Annuity Trust Charitable Remainder Unitrus 6-7

Introduction. 1 Bequests..... 1-2 Charitable Gift Annuity.. 2-4 Charitable Remainder Annuity Trust... 5-6 Charitable Remainder Unitrus 6-7 Charitable Lead Trust.....7-8 Gifts of Retirement Plan Assets.

Introduction. 1 Bequests..... 1-2 Charitable Gift Annuity.. 2-4 Charitable Remainder Annuity Trust... 5-6 Charitable Remainder Unitrus 6-7 Charitable Lead Trust.....7-8 Gifts of Retirement Plan Assets.

GEORGIA STATE UNIVERSITY FOUNDATION, INC.

GEORGIA STATE UNIVERSITY FOUNDATION, INC. Policy number/name: 2.4 Gift Acceptance Policy Title IV, Planned Giving Issuing date: 6/4/2008 Effective date: 6/4/2008 Policy approved by: Board of Trustees Governance

GEORGIA STATE UNIVERSITY FOUNDATION, INC. Policy number/name: 2.4 Gift Acceptance Policy Title IV, Planned Giving Issuing date: 6/4/2008 Effective date: 6/4/2008 Policy approved by: Board of Trustees Governance

Donation receipt for full amount Straightforward transactions Satisfaction of seeing gift at work today

Types of Gifts Type of Gift Gift of Cash Available for immediate use Liquid No risk Donation receipt for full amount Straightforward transactions Satisfaction of seeing gift at work today Cash Cheque Credit

Types of Gifts Type of Gift Gift of Cash Available for immediate use Liquid No risk Donation receipt for full amount Straightforward transactions Satisfaction of seeing gift at work today Cash Cheque Credit

Charitable Giving for Entrepreneurs after TCJA

Charitable Giving for Entrepreneurs after TCJA Brian T. Whitlock, CPA, JD, LLM THE GLOBAL FOODBANKING NETWORK Agenda Overview of charitable giving pre-tcja Review TCJA Changes Impacting Charitable Giving

Charitable Giving for Entrepreneurs after TCJA Brian T. Whitlock, CPA, JD, LLM THE GLOBAL FOODBANKING NETWORK Agenda Overview of charitable giving pre-tcja Review TCJA Changes Impacting Charitable Giving

Select Portfolio Management, Inc. December 06, 2007

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Charitable Giving If

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Charitable Giving If

Charitable Giving Options for 2018 and Beyond. Tama Brooks Klosek Klosek & Associates PLLC Planned Giving Council of Houston April 26, 2018

Charitable Giving Options for 2018 and Beyond Tama Brooks Klosek Klosek & Associates PLLC Planned Giving Council of Houston April 26, 2018 TAMA BROOKS KLOSEK Tama has a tax practice focused on both the

Charitable Giving Options for 2018 and Beyond Tama Brooks Klosek Klosek & Associates PLLC Planned Giving Council of Houston April 26, 2018 TAMA BROOKS KLOSEK Tama has a tax practice focused on both the

A Topic You Love to Hate: Putting Your Gift Policies in Order

, LLC A Topic You Love to Hate: Putting Your Gift Policies in Order Brian M. Sagrestano, JD, CFRE Gift Planning Development, LLC 100 Chestnut Place New Hartford, NY 13413 P: 315.292.1335 F: 315.292.7001

, LLC A Topic You Love to Hate: Putting Your Gift Policies in Order Brian M. Sagrestano, JD, CFRE Gift Planning Development, LLC 100 Chestnut Place New Hartford, NY 13413 P: 315.292.1335 F: 315.292.7001

Gift Acceptance Policies and Guidelines

Gift Acceptance Policies and Guidelines Lutheran Legacy Foundation, a not for profit corporation organized under the laws of the State of Illinois encourages the solicitation and acceptance of gifts to

Gift Acceptance Policies and Guidelines Lutheran Legacy Foundation, a not for profit corporation organized under the laws of the State of Illinois encourages the solicitation and acceptance of gifts to

Leaving a Legacy. Your Guide to Charitable Giving

Leaving a Legacy Your Guide to Charitable Giving About Stifel Stifel is a full-service Investment firm with a distinguished history of providing securities brokerage, investment banking, trading, investment

Leaving a Legacy Your Guide to Charitable Giving About Stifel Stifel is a full-service Investment firm with a distinguished history of providing securities brokerage, investment banking, trading, investment

Selecting Assets for Charitable Gifts Outright and in Trust

Selecting Assets for Charitable Gifts Outright and in Trust TABLE OF CONTENTS Planning Outright Gifts of Long-Term Capital Gain Property.................. 3 Publicly Traded Securities........................

Selecting Assets for Charitable Gifts Outright and in Trust TABLE OF CONTENTS Planning Outright Gifts of Long-Term Capital Gain Property.................. 3 Publicly Traded Securities........................

Mastering Complex Giving. Tips & Strategies on Using Charitable Planning for Enhancing your Practice

Mastering Complex Giving Tips & Strategies on Using Charitable Planning for Enhancing your Practice The Leading Independent Donor Advised Fund Choice Since 1993 Table of Contents For many advisors, discussing

Mastering Complex Giving Tips & Strategies on Using Charitable Planning for Enhancing your Practice The Leading Independent Donor Advised Fund Choice Since 1993 Table of Contents For many advisors, discussing

THE UNIVERSITY FOUNDATION CALIFORNIA STATE UNIVERSITY, CHICO. Gift Acceptance Policy. Approved 10/6/16

Approved 10/6/16 Table of Contents I. BACKGROUND... 1 II. POLICY STATEMENT... 1 A. General... 1 B. Gift Acceptance Committee... 1 C. Types of Acceptable Gifts... 3 D. Criteria Governing the Acceptance

Approved 10/6/16 Table of Contents I. BACKGROUND... 1 II. POLICY STATEMENT... 1 A. General... 1 B. Gift Acceptance Committee... 1 C. Types of Acceptable Gifts... 3 D. Criteria Governing the Acceptance

Estate Planning and Charitable Giving: Three Real Life Case Studies

Estate Planning and Charitable Giving: Three Real Life Case Studies Gordon Fischer, JD, CAP Gordon Fischer Law Firm, PC August 31, 2016 Extra page CHARITABLE GIVING and ESTATE PLANNING IOWA STATE UNIVERSITY

Estate Planning and Charitable Giving: Three Real Life Case Studies Gordon Fischer, JD, CAP Gordon Fischer Law Firm, PC August 31, 2016 Extra page CHARITABLE GIVING and ESTATE PLANNING IOWA STATE UNIVERSITY

Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More

FOR LIVE PROGRAM ONLY Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 18, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY Form 5227 Reporting: Mastering Compliance With Charitable Split-Interest Trusts, NIIT Calculations, and More THURSDAY, AUGUST 18, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Planned Giving Glossary

Planned Giving Glossary Here follow short descriptions of various planned giving terms and vehicles. Today s presentation only goes so far in describing various gift types. These pages are meant for later

Planned Giving Glossary Here follow short descriptions of various planned giving terms and vehicles. Today s presentation only goes so far in describing various gift types. These pages are meant for later

New Developments: Charitable Remainder Trusts in the New Economic Environment

American Bar Association Section of Real Property, Trust & Estate Law 20th Annual Spring Symposia Trust & Estate Symposium Charitable Planning and Exempt Organization Group Program Thursday, April 30,

American Bar Association Section of Real Property, Trust & Estate Law 20th Annual Spring Symposia Trust & Estate Symposium Charitable Planning and Exempt Organization Group Program Thursday, April 30,

Fund Agreements: Best Practices. Phil Purcell, JD Consultant for Philanthropy, LLC Copyright rights reserved

Fund Agreements: Best Practices Phil Purcell, JD Consultant for Philanthropy, LLC pmpurcell@outlook.com Copyright 2017@All rights reserved Outline Fund Agreement (FA) Basics What should a FA say? Special

Fund Agreements: Best Practices Phil Purcell, JD Consultant for Philanthropy, LLC pmpurcell@outlook.com Copyright 2017@All rights reserved Outline Fund Agreement (FA) Basics What should a FA say? Special

ALI-ABA Course of Study Charitable Giving Techniques

383 ALI-ABA Course of Study Charitable Giving Techniques Cosponsored by the ABA Section of Real Property, Trust and Estate Law and the ABA Section of Taxation June 10-11, 2010 New York, New York Charitable

383 ALI-ABA Course of Study Charitable Giving Techniques Cosponsored by the ABA Section of Real Property, Trust and Estate Law and the ABA Section of Taxation June 10-11, 2010 New York, New York Charitable

Charitable Remainder Trusts

Charitable Remainder Trusts Calculations and Examples Charitable Remainder Trust Summary of Benefits 2 Actuarial Calculations 3 Text Description 4 CRUT/Sell/Keep Comparison Summary of Benefits 5 Cash Flow

Charitable Remainder Trusts Calculations and Examples Charitable Remainder Trust Summary of Benefits 2 Actuarial Calculations 3 Text Description 4 CRUT/Sell/Keep Comparison Summary of Benefits 5 Cash Flow

Charitable Planned Giving Strategies

Charitable Planned Giving Strategies Courtesy of: Yellowstone Boys & Girls Ranch Foundation, Inc. This presentation was prepared for educational purposes only. It must not be used as a basis for tax or

Charitable Planned Giving Strategies Courtesy of: Yellowstone Boys & Girls Ranch Foundation, Inc. This presentation was prepared for educational purposes only. It must not be used as a basis for tax or

Mary Carter Financial Services April 17, 2018

Mary Carter Financial Services An Independent Firm Mary Carter, ChFC, CFP 131 2nd Avenue North Suite 200 Jacksonville Beach, FL 32250 904-246-0346 mary.carter@raymondjames.com marycarterfinancialservices.com

Mary Carter Financial Services An Independent Firm Mary Carter, ChFC, CFP 131 2nd Avenue North Suite 200 Jacksonville Beach, FL 32250 904-246-0346 mary.carter@raymondjames.com marycarterfinancialservices.com

Arthritis Foundation Texas Chapter Planned Giving Seminar May 20, 2010 PLANNING WITH CHARITABLE REMAINDER TRUSTS

I. Generally. Arthritis Foundation Texas Chapter Planned Giving Seminar May 20, 2010 PLANNING WITH CHARITABLE REMAINDER TRUSTS R. Thomas Groves, Jr. Jackson Walker L.L.P. 901 Main Street, Suite 6000 Dallas,

I. Generally. Arthritis Foundation Texas Chapter Planned Giving Seminar May 20, 2010 PLANNING WITH CHARITABLE REMAINDER TRUSTS R. Thomas Groves, Jr. Jackson Walker L.L.P. 901 Main Street, Suite 6000 Dallas,

A Guide to. Planned Giving

A Guide to Planned Giving If your life has been touched by Special Olympics, and you want to give back, the SOMO Endowment Fund is a great place to start. In this booklet, you ll learn about planned giving

A Guide to Planned Giving If your life has been touched by Special Olympics, and you want to give back, the SOMO Endowment Fund is a great place to start. In this booklet, you ll learn about planned giving

CHAPTER 16 Charitable Gift Transfers

CHAPTER 16 Charitable Gift Transfers Charitable contribution options (p.2): - Cash - Appreciated property - Bargain sale to charity - Horizontal split interest gifts: (1) income interest retained, and

CHAPTER 16 Charitable Gift Transfers Charitable contribution options (p.2): - Cash - Appreciated property - Bargain sale to charity - Horizontal split interest gifts: (1) income interest retained, and

Top 10 Income Tax Planning Ideas for 2013

Top 10 Income Tax Planning Ideas for 2013 Presented by: Robert S. Keebler, CPA, MST, AEP(Distinguished) Ph: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com Ideas 1. Bracket Management 2.

Top 10 Income Tax Planning Ideas for 2013 Presented by: Robert S. Keebler, CPA, MST, AEP(Distinguished) Ph: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com Ideas 1. Bracket Management 2.

Business Interests: Planning Considerations

Business Interests: Planning Considerations Business owners have unusual opportunities when it comes to making gifts to The First Church of Christ, Scientist. They have the flexibility of giving from their

Business Interests: Planning Considerations Business owners have unusual opportunities when it comes to making gifts to The First Church of Christ, Scientist. They have the flexibility of giving from their

2011 Charitable Giving Review

TAX-EXEMPT ORGANIZATIONS edwardswildman.com taxexempt.edwardswildman.com 2011 Charitable Giving Review With the end of the year approaching rapidly, we would like to take this opportunity to provide you

TAX-EXEMPT ORGANIZATIONS edwardswildman.com taxexempt.edwardswildman.com 2011 Charitable Giving Review With the end of the year approaching rapidly, we would like to take this opportunity to provide you

Charitable Remainder Annuity Trust Presentation Input Screen

Charitable Remainder Annuity Trust Presentation Input Screen Annuity Trust Questions Gift Asset Questions Case Name ----- NEW CASE ----- Gift Asset Type Cash Name for Reports Betty Anthropist Value of

Charitable Remainder Annuity Trust Presentation Input Screen Annuity Trust Questions Gift Asset Questions Case Name ----- NEW CASE ----- Gift Asset Type Cash Name for Reports Betty Anthropist Value of

S Corporations Corporations that have elected to be taxed as passthrough entities under subchapter S of the IRC

For non-cash donations of $5,000 or greater, the donor must obtain a qualified appraisal by a qualified appraiser as described under IRC 170(f)(11)(E). These guidelines will be considered satisfied if

For non-cash donations of $5,000 or greater, the donor must obtain a qualified appraisal by a qualified appraiser as described under IRC 170(f)(11)(E). These guidelines will be considered satisfied if

From Lindsey W. Duvall. Duvall Law Firm, LLC. 147 Old Solomons Island Road Suite 306 Annapolis MD

Uncovering Charitable Planning Opportunities Volume 7, Issue 11 Charitable giving is discretionary spending. It is affected by both the economy and the income tax rates. Not surprisingly, charitable giving

Uncovering Charitable Planning Opportunities Volume 7, Issue 11 Charitable giving is discretionary spending. It is affected by both the economy and the income tax rates. Not surprisingly, charitable giving

Finding cures. Saving children. If you would like to receive printed copies of this, please contact us at or

OFFERED TO YOU BY ST. JUDE CHILDREN'S RESEARCH HOSPITAL Finding cures. Saving children. If you would like to receive printed copies of this, please contact us at 1-800-395-4341 or giftplanning@stjude.org

OFFERED TO YOU BY ST. JUDE CHILDREN'S RESEARCH HOSPITAL Finding cures. Saving children. If you would like to receive printed copies of this, please contact us at 1-800-395-4341 or giftplanning@stjude.org

Flexible Giving and Your Will

Flexible Giving and Your Will Making Gifts in Your Will Many of our supporters choose to make gifts in their wills. The advantages are undeniable. These gifts are simple, straightforward, and familiar.

Flexible Giving and Your Will Making Gifts in Your Will Many of our supporters choose to make gifts in their wills. The advantages are undeniable. These gifts are simple, straightforward, and familiar.

For a more detailed overview, see Charitable Remainder Trusts, 2. Treas. Regs (a)(5)(i).

(5)(i).") Two CRUTs and a CLAT: Using Split Interest Charitable Trusts to Defer Gain and Eliminate Estate Taxes Terence Condren & Thomas Cosinuke December 3, 2015 1. Framing the Discussion a. "True charity is the

Two CRUTs and a CLAT: Using Split Interest Charitable Trusts to Defer Gain and Eliminate Estate Taxes Terence Condren & Thomas Cosinuke December 3, 2015 1. Framing the Discussion a. "True charity is the

Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More

Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More Navigating the New Reporting Requirements and Avoiding Compliance Errors WEDNESDAY, MAY 14, 2014, 1:00-2:50 pm

Revised Form 5227 Reporting: Charitable Split-Interest Trusts, NIIT Calculations, and More Navigating the New Reporting Requirements and Avoiding Compliance Errors WEDNESDAY, MAY 14, 2014, 1:00-2:50 pm

Gift Acceptance Policy

Gift Acceptance Policy This Gift Acceptance Policy (the Policy ) governs the solicitation, acceptance, and acknowledgment of charitable gifts to the Vail Valley Foundation, which shall include Vail Valley

Gift Acceptance Policy This Gift Acceptance Policy (the Policy ) governs the solicitation, acceptance, and acknowledgment of charitable gifts to the Vail Valley Foundation, which shall include Vail Valley

PRACTICAL CHARITABLE PLANNING EXAMPLES THAT DON T REQUIRE YOU TO BE A TAX EXPERT. THE ABCS OF CRATS, CRUTS, CLATS AND CLUTS.

PRACTICAL CHARITABLE PLANNING EXAMPLES THAT DON T REQUIRE YOU TO BE A TAX EXPERT. THE ABCS OF CRATS, CRUTS, CLATS AND CLUTS. IS THE ALPHABET REALLY THAT DIFFICULT? HOW TO PROVIDE FOR YOUR FURRY FRIENDS!

PRACTICAL CHARITABLE PLANNING EXAMPLES THAT DON T REQUIRE YOU TO BE A TAX EXPERT. THE ABCS OF CRATS, CRUTS, CLATS AND CLUTS. IS THE ALPHABET REALLY THAT DIFFICULT? HOW TO PROVIDE FOR YOUR FURRY FRIENDS!

GIFT ACCEPTANCE POLICIES AND GUIDELINES

GIFT ACCEPTANCE POLICIES AND GUIDELINES PKD Foundation, a not-for-profit organization organized under the laws of the State of Missouri, encourages the solicitation and acceptance of gifts to the PKD Foundation

GIFT ACCEPTANCE POLICIES AND GUIDELINES PKD Foundation, a not-for-profit organization organized under the laws of the State of Missouri, encourages the solicitation and acceptance of gifts to the PKD Foundation

4/26/2018 (c) William P. Streng 1

William P. Streng 1") CHAPTER 16 Charitable Gift Transfers Circumstances where charitable gifts are of significant interest to clients: 1) Clients have no direct descendants. 2) Clients have substantial assets and genuine charitable

CHAPTER 16 Charitable Gift Transfers Circumstances where charitable gifts are of significant interest to clients: 1) Clients have no direct descendants. 2) Clients have substantial assets and genuine charitable

September / Use of Life Insurance in Charitable Planning (Part Two) A Note to our Readers: Inside this issue: I. CHARITABLE REMAINDER TRUST

A Note to our Readers: Inside this issue: I. CHARITABLE REMAINDER TRUST") September / 2006 Use of Life Insurance in Charitable Planning (Part Two) Inside this issue: I. CHARITABLE REMAINDER TRUST II. CHARITABLE LEAD TRUST III. CHARITABLE GIFT ANNUITY IV. WEALTH REPLACEMENT TRUST

September / 2006 Use of Life Insurance in Charitable Planning (Part Two) Inside this issue: I. CHARITABLE REMAINDER TRUST II. CHARITABLE LEAD TRUST III. CHARITABLE GIFT ANNUITY IV. WEALTH REPLACEMENT TRUST

Charitable Trusts David Nunheimer The Small Business & Estate Planning Law Group 26 George Ryder Road West Chatham, MA

Maximizing Wealth While Minimizing Taxes Charitable Trusts David Nunheimer The Small Business & Estate Planning Law Group 26 George Ryder Road West Chatham, MA 508-945-1000 1 Charitable Planning Is the

Maximizing Wealth While Minimizing Taxes Charitable Trusts David Nunheimer The Small Business & Estate Planning Law Group 26 George Ryder Road West Chatham, MA 508-945-1000 1 Charitable Planning Is the

CHAPTER 16 Charitable Gift Transfers

CHAPTER 16 Charitable Gift Transfers Circumstances where charitable gifts are of significant interest: 1) Clients have no direct descendants. 2) Clients have substantial assets and genuine charitable objectives.

CHAPTER 16 Charitable Gift Transfers Circumstances where charitable gifts are of significant interest: 1) Clients have no direct descendants. 2) Clients have substantial assets and genuine charitable objectives.

Don t Forget Gifts of Tangible Personal Property

Don t Forget Gifts of Tangible Personal Property PG Calc Feature Article, August 2013 Except for museums that are accustomed to receiving gifts of art and artifacts, charities tend to focus on gifts of

Don t Forget Gifts of Tangible Personal Property PG Calc Feature Article, August 2013 Except for museums that are accustomed to receiving gifts of art and artifacts, charities tend to focus on gifts of

The Charitable Lead Trust

Chapter 44 The Charitable Lead Trust Scott Gunderson (Reno, Nevada) Would you like to support one or more charities at your death without reducing your children s or grandchildren s inheritance? Would

Chapter 44 The Charitable Lead Trust Scott Gunderson (Reno, Nevada) Would you like to support one or more charities at your death without reducing your children s or grandchildren s inheritance? Would

Estate Planning Through Charitable Gifting

Donna Sheehy, CFP 29605 US Highway 19 Suite 250 Clearwater, FL 33761 727-943-8813 dsheehy@harborfs.com www.investdonna.com Estate Planning Through Charitable Gifting Call today for a personal consultation

Donna Sheehy, CFP 29605 US Highway 19 Suite 250 Clearwater, FL 33761 727-943-8813 dsheehy@harborfs.com www.investdonna.com Estate Planning Through Charitable Gifting Call today for a personal consultation

Charitable Remainder Annuity Trust. Planned Charitable Giving Using a Split-Interest Trust

Charitable Remainder Annuity Trust Planned Charitable Giving Using a Split-Interest Trust CRAT Overview Lifetime transfer of cash or property in trust in exchange for annuity interest payable over (a)

Charitable Remainder Annuity Trust Planned Charitable Giving Using a Split-Interest Trust CRAT Overview Lifetime transfer of cash or property in trust in exchange for annuity interest payable over (a)