Correcting Depreciation Form 3115 Line-By-Line. ihmlisa

|

|

|

- Annis Conley

- 6 years ago

- Views:

Transcription

1 Form 3115 Line-By-Line ihmlisa

2 This text has been prepared with due diligence. However, the possibility of mechanical or human error does exist and the author accepts no responsibility or liability regarding this material and its use. This text is not intended or written by the practitioner to be used, and cannot be used by a taxpayer or a tax return preparer, for the purpose of of avoiding penalties that may be be imposed. The The text text is is not not intended to address to address every every situation situation that that may may arise. arise. Consult Consult additional sources sources of information, of as needed, as needed, to determine to determine the the solution solution to tax to tax questions. This publication is designed to provide accurate and authoritative information on the subject of federal tax laws. It is presented with the understanding that the author is not engaged in rendering legal or accounting services. Copyright 2017 by Karen Lisa Ihm, Joyner, EA, EA, Coronado, El Cajon, CA. CA Reprinting and Lisa Ihm, any EA, part Coronado, of this text CA. or Reprinting use without any the part express of this written text or permission use without of Lisa the Ihm express is prohibited. written permission of Lisa Ihm is prohibited.

3 Table of Contents How To Correct Depreciation Errors... 1 When is an amended return appropriate?... 1 When must you file a Change in Accounting Method?... 1 Advantages of Form (a) Adjustment... 2 How to calculate adjustment... 2 When to report adjustment... 2 Where to report adjustment... 3 Automatic Change Request Procedures... 3 Automatic Change Not Allowed... 3 Designated Change Number (DCN)... 3 DCN 7 and DCN DCN Filing the Form page form only specific pages required copies must be filed... 4 NEW filing address for copy... 5 Due date... 5 No acknowledgment... 5 Can you still file Form 3115 to make changes relating to new repair regs?... 5 Marked-Up Form Cessation of Business (Line 4)... 7 Special provision for depreciation corrections... 7 Returns Under Examination (Line 6)... 9 Automatic change request generally not allowed... 9 Allowed in specific circumstances... 9 How to request consent... 9 Under examination defined... 9 Does audit relate to proposed Form 3115 change?... 9 Audit Protection (Line 7) Audit protection generally applies DCNs to which audit protection does not apply Items under exam... 10

4 3-month window day window period Method not before director Change resulting in a negative adjustment CAP Other Audit protection at end of exam No audit protection if applied new regs prospectively Changes Within Last 5 Years (Line 11) Automatic change procedure not allowed Attachments Multiple Items & Multiple Businesses (Line 15) Unrelated business require separate forms Multiple rental properties are related DCN list shows permitted concurrent changes Some increases, some decreases Designated Change Numbers List Determining Asset Class - From Pub Form 3115 Shortcuts Examples Sample Completed Full CA Conformity? Amending Form Form 3115 Attachment Worksheet for... 36

5 How To Correct Depreciation Errors When an error is discovered on a prior return, first instinct is to amend the return and make the correction. However, when the error involves depreciation calculations, amending the previously filed return is often not the correct, or most advantageous, way to proceed. 1 When is an amended return appropriate? You can file an amended return (1040X) to correct the amount of depreciation claimed in any of the following situations: You claimed the incorrect amount because of a mathematical error. You claimed the incorrect amount because of a posting error. You have not adopted a method of accounting for property placed in service in tax years ending after December 29, Generally, you adopt a method of accounting for depreciation by: 1. Using a permissible method of determining depreciation when you file your first tax return, or 2. Using the same impermissible method of determining depreciation in two or more consecutively filed tax returns. When must you file a Change in Accounting Method? If the depreciation correction cannot be made on an amended return (usually because you used the incorrect method on 2 or more returns), the change is made by filing Form Advantages of Form 3115 Using a Form 3115 rather than a 1040X is generally advantageous for several reasons: 1. It effectively eliminates the statute of limitations for claiming a refund. 2. It eliminates interest on prior year deduction overstatements. 3. It delays payment of tax by allowing corrections of prior year deduction overstatements to be spread out over 4 years. 1 Reg (e)

6 481(a) Adjustment The amount of the adjustment resulting from correcting the depreciation deduction from prior returns is referred to as a Code Section 481(a) adjustment. 481(a) adjustments represent the aggregate amount of net income or expense that would have been reported in the tax years before the year of change if the taxpayer had used the correct or new method in those earlier years. 2 2 How to calculate adjustment The 481(a) adjustment is generally computed by comparing the amounts reported in prior years and the amounts that would have been reported if the taxpayer had used the correct or new method in those years. 3 The 481(a) adjustment is computed ignoring the statute of limitations on assessment and collection of tax. 4 (Go back to the beginning of time.) When to report adjustment Decrease in income The entire deduction is taken in the year the error is discovered. 5 Increase in income The 481(a) adjustment period is 4 tax years for a net positive adjustment (i.e., increase in taxable income). 1/4 of the adjustment is added to income each year. However, if the increase in taxable income is less than $50,000 6 the taxpayer may elect to include the entire adjustment in the year of change (the year the error is discovered), rather than spread it out over 4 years. (The limit prior to 2014 was $25,000.) Applicant under audit The 481(a) adjustment period is two taxable years (year of change and next taxable year) for a positive 481(a) adjustment for a change in method of accounting requested when a taxpayer is under examination, unless the rules for a change filed in a 3-month window, 120-day window, or method not before the director applies. 7 (See discussion of taxpayers under audit later.) Out of business A taxpayer who ceases to engage in a trade or business must take the remaining balance of any 481(a) adjustment into account in computing taxable income in the tax year of the cessation or termination. 8 Therefore, if a building that was being depreciated is sold, the remaining 481(a) adjustment must be taken into consideration in the year of sale. 2 IRS Letter Ruling IRS Letter Ruling Superior Coach of FL, Inc.; Rev Proc Rev Proc as modified by Rev Proc and Rev Proc , Section 7.03(3)(c) 7 Rev Proc , Section 7.03(3)(b) 8 Rev Proc , Section 7.03(4)(a)

7 Where to report adjustment The adjustment is reported on Line 26 of Form 3115 and on the same form or schedule where the original error occurred. This will generally be Schedule E, but might also be Schedule C or F, Form 2106, etc. 3 Automatic Change Request Procedures In most instances, you use the automatic change request procedures to change the method of accounting for depreciation. 9 There is no fee required by the IRS for an automatic change request. The IRS does not acknowledge receipt or acceptance of your request. Automatic Change Not Allowed The automatic change procedures generally cannot be used, or are subject to special limitations, in the following cases: 1. Taxpayer has returns under audit 2. Filed a Form 3115 within the last 5 years 3. Cessation of business (but special allowance for depreciation deductions) Designated Change Number (DCN) Each change eligible for the automatic change procedures has been assigned a DCN. Those numbers can be found in the chart at the end of the Form 3115 instructions. DCN 7 and DCN 107 These two DCNs will be used most often for depreciation corrections. DCN 7 is a change from an impermissible to a permissible method of depreciation. DCN 107 is the same, but for disposed property. Common depreciation corrections include: 1. Depreciation never claimed (this is not a permissible method, so DCN 7 will be used) 2. Land depreciated (this is not a permissible method, so DCN 7 will be used) 3. Basis in inherited property not adjusted to FMV at date of death (taxpayer is effectively not depreciating part of the basis of the property, which is not a permissible method, so DCN 7 will be used) In all of these examples, if the property was disposed of before the filing of the Form 3115, then DCN 107 is used rather than DCN 7. DCN 8 A change from a permissible method to another permissible method is reported using DCN 8. The most common reason this DCN would be used is to change from item accounting for specific assets to multiple asset accounting (pooling or bulk asset accounts) for the same assets, or vice versa. Some other specific changes are allowed Revenue Procedure , Revenue Procedure Rev Proc , Section 6.02(4)

8 Filing the Form page form only specific pages required When the IRS modified the Form 3115 at the end of 2015, they did not shorten it, but they did add some reference charts making it clear that a taxpayer is only required to complete the parts of the form that relate to their specific change. 4 We will usually file Form 3115 using the automatic change procedures, so Parts I, II, and IV must be completed. Part III can be skipped. Depreciation corrections require completion of only Schedule E. All other schedules can be skipped. 2 copies must be filed A second copy must be sent by mail to Covington, KY. That copy cannot be filed electronically. 11 Form 3115 revised December 2015 instructions

9 NEW filing address for copy For 2015 the address for automatic change requests delivered by mail has changed from Ogden, UT to 201 West Rivercenter Blvd., PIN Team Mail Stop 97, Covington, KY Forms sent by private delivery service should be sent to the same address. 5 Due date Form 3115 has the same due date as the tax return to which it relates. An automatic extension of 6 months from the due date (excluding any extension) is granted to file a Form 3115 under the automatic change procedures provided the taxpayer: 12 a) Timely filed (including extensions) its original federal income tax return. b) Files an amended return within the 6-month extension period, c) Attached the original Form 3115 to the amended return, d) Files a signed copy of the Form 3115 with the IRS in Covington, KY no later than the date the original is filed with the amended return, e) Attaches a statement to the Form 3115 that it is being filed pursuant to (b) of the Procedure and Administration Regulations. No acknowledgment The IRS does not send an acknowledgement of receipt for a Form 3115 (original or copy) filed under the automatic change procedures. 13 No news is good news! Can you still file Form 3115 to make changes relating to new repair regs? If a taxpayer made the election under Rev Proc to apply the new repair regs only in taxable years beginning on or after January 1, 2014, then they cannot file a Form 3115 (after 2014) to apply the new regs to old items (prior to 2014) on their depreciation schedules. There was no formal election statement required to make the election under Rev Proc , so there is debate about whether the taxpayer automatically made the election by failing to file a Form 3115 in 2014; if they did, then they cannot file a Form 3115 in a year after 2014 to clean-up their pre-2014 depreciation schedule. Some argue that if no election statement was attached to the 2014 return, then no election was made, and the taxpayer would be able to file a 3115 in a year after 2014 to clean-up pre-2014 depreciation schedules. 12 Rev Proc , Section 6.03(4) 13 Rev Proc , Section 6.03(1)(c)

10 Marked-Up Form

11 Cessation of Business (Line 4) Cessation of a business generally disqualifies a taxpayer from requesting a change in accounting method using the automatic change request procedures Special provision for depreciation corrections However, this provision does not apply when the requested change is a correction in depreciation. 15 If the taxpayer is terminating his business, answer the question Yes and attach a statement explaining why he can still use the automatic change request procedures. A sample statement could state: Revenue Procedure Section 6.01 states that the eligibility rule in section 5.01(1)(d) of Rev Proc does not apply to DCN 7 or DCN 107. (DCN 7 is a change from an impermissible to a permissible method of depreciation. DCN 107 is the same, but for disposed property.) 14 Rev Proc Section 5.01(1)(d) 15 Rev Proc Section 6.01(2)

12 8

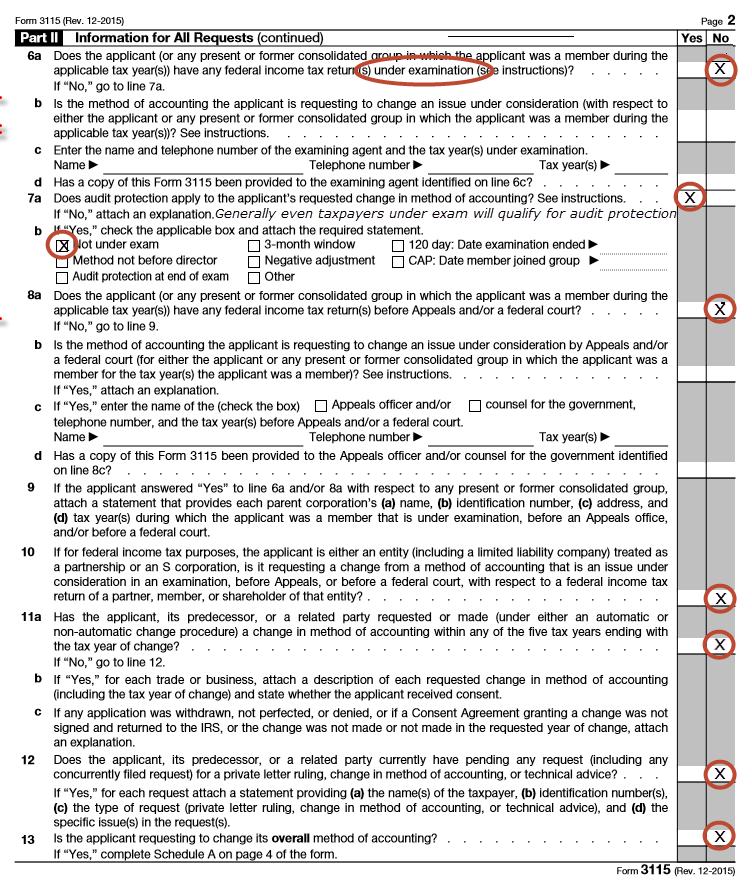

13 Returns Under Examination (Line 6) Automatic change request generally not allowed Generally, if a taxpayer s return is under audit, they do not qualify to use the automatic change request procedures, unless the IRS director consents to the filing of an application to change. 9 Allowed in specific circumstances The director will consent to the filing of the application under the automatic change request procedures unless, in the director s opinion, the method of accounting to be changed would ordinarily be included as an item of adjustment in the year(s) for which the taxpayer is under exam. 16 For example, the director will consent to a filing of an application for a change from a clearly permissible method of accounting, or for an asset placed in service after the year under exam. The director s consent is limited to consent to file the application, and does not constitute the director s agreement to, or approval of, the requested change. How to request consent The request is made by requesting technical advice, and because technical advice is issued to assist field offices, it is the field office (auditor) that determines whether to request technical advice. While a case is under the jurisdiction of a Director, a taxpayer may request an issue be referred to the Associate (Chief Counsel) office for technical advice. The request may be oral or written and should be directed to the field office. If denied, appeal procedures are available. 17 Under examination defined The applicant is under examination if they have received any contact in any manner by a representative of the IRS, for the purpose of scheduling or conducting any type of examination of the return. 18 (If the exam has been scheduled but has not yet begun, the applicant is considered under examination. If a letter has been received asking the taxpayer to contact the IRS to set up the exam, the applicant is under examination. If a CP 2000 letter has been received and has not yet been reconciled, the taxpayer is under examination.) Does audit relate to proposed Form 3115 change? Generally, the applicant s method of accounting (the reason for filing the Form 3115) is an issue under consideration if the examining agent has given the taxpayer written notification specifically citing the treatment of the item as an issue under consideration. If no adjustment is proposed for the item during the exam, and the auditor does not put the issue in suspense for later review related to another year, then the item is no longer considered to be an item under examination. 16 Rev Proc , Sec Rev Proc , Section 5 18 Rev Proc , Section 3.18

14 10 Audit protection generally applies Audit protection generally applies when an application for change in accounting method is granted. Audit Protection (Line 7) DCNs to which audit protection does not apply Those changes to which audit protection does not apply are noted in the chart of DCNs provided at the end of the Form 3115 instructions. If that chart does not specifically say that audit protection is not provided, then audit protection is provided. Items under exam Special rules apply to taxpayers under exam, but they may still qualify for audit protection in specific circumstances. 3-month window The 3-month window is the period from the 15 th day of the 7 th month (usually July) to the 15 th day of the 10 th month (usually October) following the close of the applicant s tax year. Audit protection applies if: A. Taxpayer has been under exam for at least 12 months as of the first day of the 3- month window, and B. The change being requested is not an issue under consideration. 120-day window period The 120-day window is the 120-day period following the date an exam ends, regardless of whether a subsequent exam has commenced. An applicant qualifies for audit protection if: A. They file Form 3115 during the 120-day window, and B. The change being requested is not an issue under consideration. Method not before director The present method is not before the director when it is: A. A change from a clearly permissible method of accounting, or B. A change to property placed in service after the year under exam. Change resulting in a negative adjustment If the change results in additional income being reported, then audit protection generally applies. (This would be the case if depreciation adjustments were overstated in prior years.) CAP CAP applies only to consolidated group members participating in the compliance assurance process (CAP).

15 11 The List of Automatic Changes may provide audit protection in specific cases. Attach a Other statement citing the guidance providing audit protection. Audit protection at end of exam If none of the other categories applies, this box should generally be checked. The applicant may receive audit protection at the end of the exam, provided the examining agent does not propose an adjustment for the same item and the method of accounting for that same item is not an issue under consideration. No audit protection if applied new regs prospectively A small business taxpayer choosing the option of calculating a 481(a) adjustment that takes into account only amounts paid or incurred, and dispositions, in taxable years beginning on or after January 1, 2014, does not receive audit protection for taxable years beginning prior to January 1, Changes Within Last 5 Years (Line 11) Automatic change procedure not allowed An applicant generally is not eligible to file under the automatic change procedures if they made or requested a prior item change (for the same item) or a prior overall method change within the five tax years ending with the requested year of change. The national office will consider the taxpayer s explanation for requesting consent to again change its method of accounting for that same item in determining whether to grant consent for the current request Rev Proc , Section 2 20 Rev Proc , Section 11.02(2)

16 12

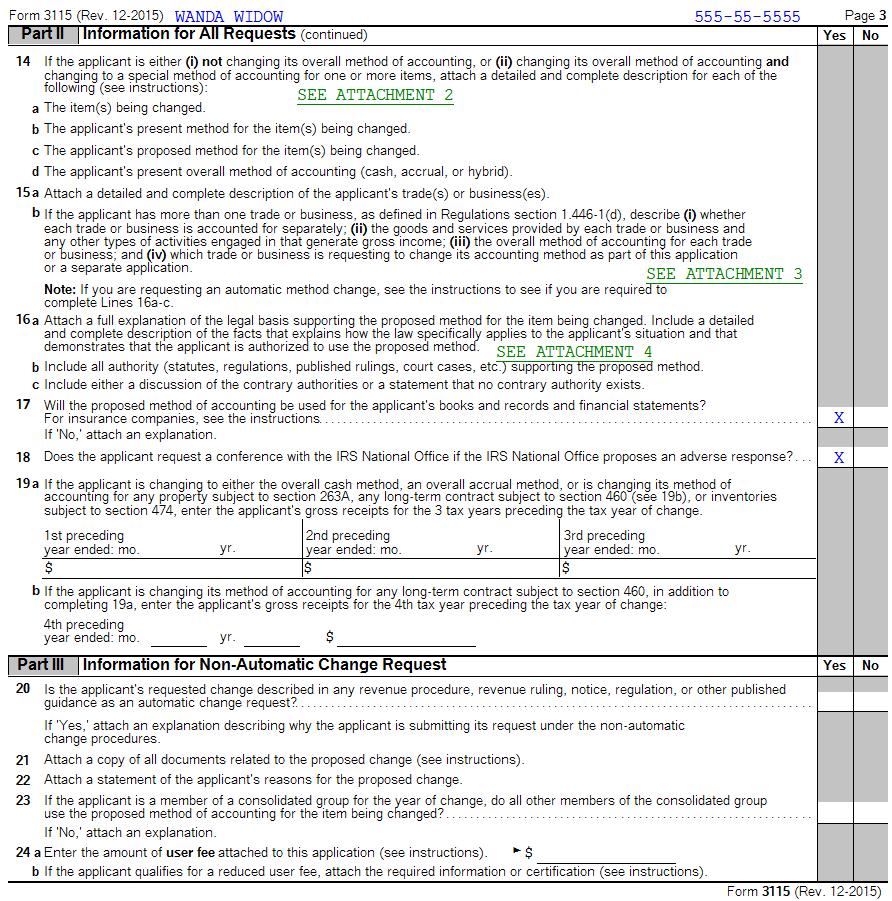

17 13 Throughout the Form 3115 there are lines that ask for detailed information about the change. Most of the requested information is already on your depreciation schedule, so save substantial time by simply typing See Statement Attached into every one of those lines, and attach the current correct depreciation schedule to the return, with the following added notations: Attachments A. Attach copy of new current correct depreciation schedule 1. Above the Prior Depreciation column, add the word Correct. (Since this is the correct current year depreciation schedule, you should have entered the prior depreciation as if it had been correctly claimed. 2. Make another column titled Actual Prior Dep. In that column enter the depreciation actually claimed by the taxpayer in prior years. 3. Cross out Current Depreciation and make the title of that column Section 481(a) adjustment. Do the math and enter the amount of the correction for each asset in that column. 4. To the left of the asset name, make a column titled Asset Class. Enter the asset class from Pub 946. (Applicable pages are reproduced later in this text.) Real estate does not have an asset class, so enter None, or if your property header does not state the type of property, enter the type of property (i.e. residential rental, commercial, etc.). B. Attach a statement including the information requested. A fillable Excel version of the Form 3115 Attachment Worksheet can be downloaded from my website at

18 14

19 15 Unrelated business require separate forms A taxpayer may ordinarily request only one change in method of accounting on a Form 3115, but if changes are related, they may appear on the same form. As an example, if the rental building was depreciated using the wrong basis, and the land was also depreciated, both changes can appear on the same Form 3115 (as can all other changes related to that property and other rental properties that are a part of the same business). Separate Forms 3115 are required if changes are made in 2 businesses that are separate and distinct. 21 Multiple Items & Multiple Businesses (Line 15) Multiple rental properties are related Several rental properties do not constitute several businesses even though the rental properties are each reported on a separate Schedule E, so if the land was depreciated on 2 separate rental properties, both corrections can be reported on one Form 3115, but detail must be provided to show how much of the adjustment goes to each of the properties (that detail is already on the depreciation schedule you created). DCN list shows permitted concurrent changes The List of Automatic Changes describes particular changes in method of accounting that a taxpayer is required or permitted to request on a single Form Some increases, some decreases If corrections are being made to 2 or more depreciable items, and some of the changes result in increases to income and some result in decreases to income, 2 adjustments are made: 1. All increases to income are added together 2. All decreases to income are added together The decreases to income are all included in the year the error is discovered. The increases to income are spread over 4 years (unless the total is less than $50,000 and an election is made to report the entire adjustment in the current year). 21 Rev Proc , Section Rev Proc , Section 6.03(1)(b)

20 16 Form 3115, pages 5, 6, & 7 intentionally deleted because they are not required for a change in depreciation.

21 Designated Change Numbers List 17

22 18

.")

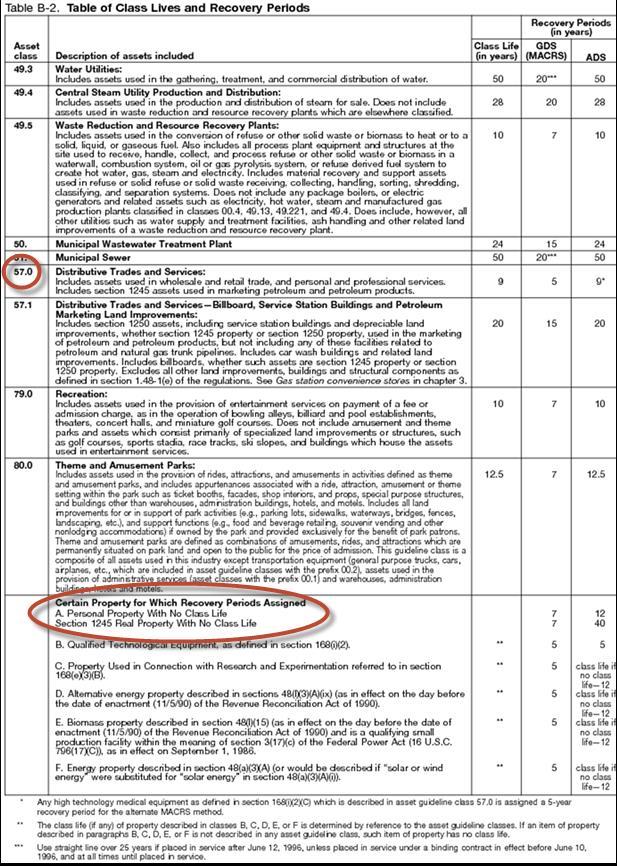

23 19 Form 3115 requires that you enter the asset class for each item changed. The asset class is NOT the recovery period (3, 5, 7, 27.5, 39 years). The asset classes are listed in the depreciation publication, Pub 946 (which you haven t opened since 1987 when you memorized all the class lives). Determining Asset Class - From Pub 946

24 20

25 21 This 8 page form contains question after question that does not apply to typical taxpayers requesting an automatic change in accounting method to correct depreciation, and the technical language used makes it impossible to quickly read the questions to determine which ones apply, and the instructions are even worse. Form 3115 Shortcuts The marked-up Form 3115 provides a quick and easy-to-follow guide for completion of the form. Use a simpler worksheet attachment Using a standardized worksheet to provide the detail required in several areas of the form eliminates the need to read through 8 pages of forms and enter the same information in several different formats. Simply type See Statement Attached into the Form 3115 anywhere that it asks for typed-in information. The example to follow includes a worksheet for this purpose. An Excel version of the worksheet can be downloaded free of charge from my website at Create a Template Complete a Form Take screen shots of the completed input, and you or support staff can use that as a guide to quickly enter the required information into your software program for any client needing a Form 3115.

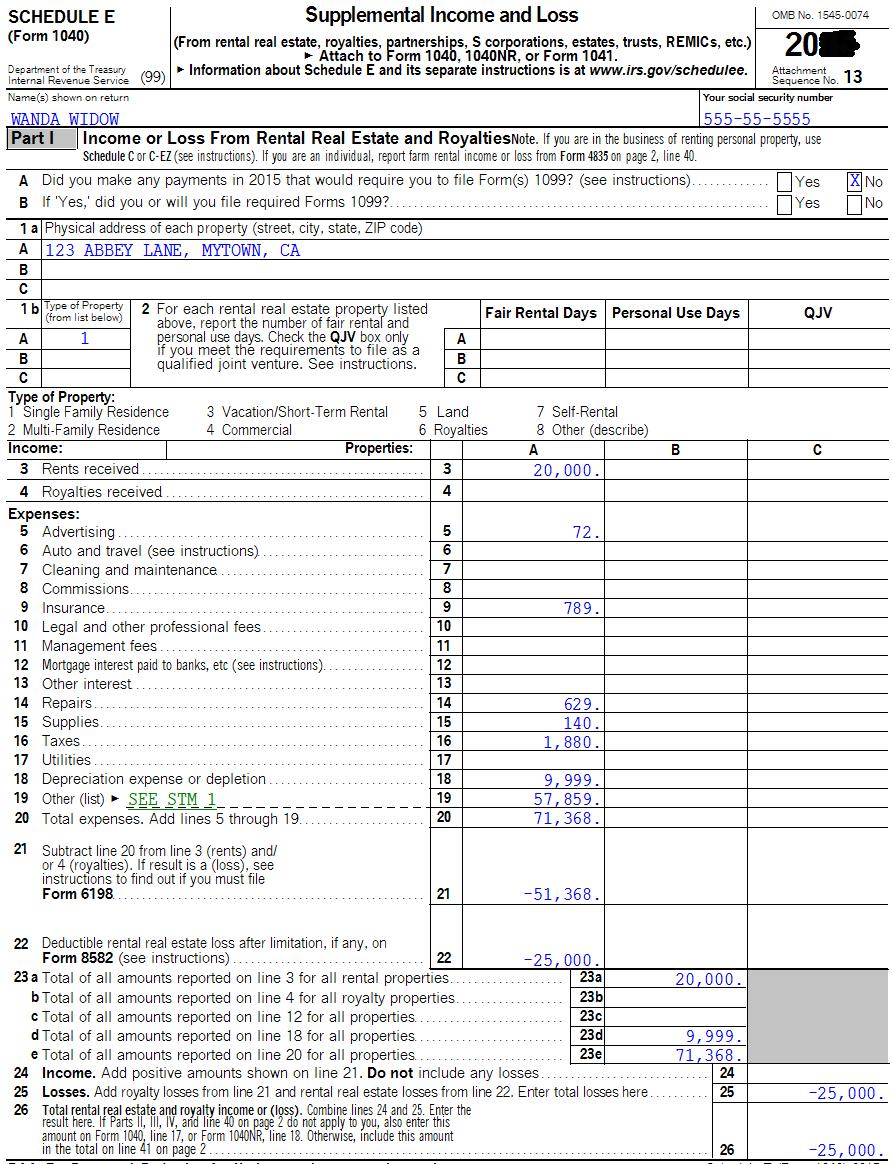

26 Examples The following are examples of a change in method of accounting for depreciation. 22 Example 1 Missed Deduction A change from an impermissible method of determining depreciation for depreciable property, if the impermissible method was used in two or more consecutively filed tax returns. Wanda Widow is a new client Errors discovered before return prepared Rental property was fully depreciated Husband died 6 years ago Step-up in basis was overlooked FMV of building at date of death was $275,000 FMV of land at date of death was $200,000 File Form 3115 The statute of limitations does not apply. Calculate the correct depreciation, back to the beginning of time. The 481(a) adjustment is the difference between the depreciation actually claimed and what the correct depreciation should have been.

27 Sample Completed Full

28 24

29 25

30 Pages 5, 6, & 7 were intentionally omitted, as they would be blank. 26

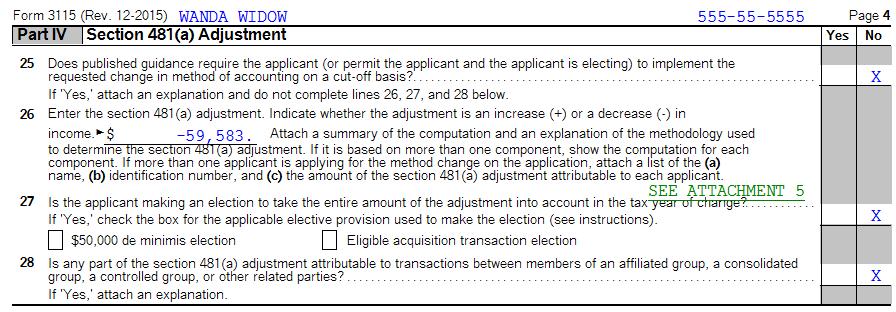

31 27 The $59,583 will be deducted in full in the year the error is discovered. Put the adjustment on Schedule E on the Other Expenses line. Use Section 481(a) adjustment as the description. Mail additional signed copy of Form 3115 to KY address.

32 28 Example 2 Deducted Too Much Depreciation Larry Landlord Owns 20 unit residential rental building Purchased for $1.4 million Depreciated entire cost Did not take out land Land was $84,000 Form 3115 makes correction all the way back to date of purchase even though older returns are out of statute. Larry Landlord s 3115 would be almost identical to Wanda Widow s, except that the amount entered in Part IV would be different and since the total amount of the positive adjustment is less than $50,000, Larry can elect to include the entire adjustment in the current year. If he made that election, he would answer Yes to Question 27 instead of No.

33 29 The excess depreciation claimed must be included in income, even though the statute of limitations for assessment of tax is closed for many of these years! The $27,877 of additional income is reported over 4 years, beginning in the year the error was discovered. He can elect to report all the income in one year because the amount is under $50,000 (limit increased from $25,000 by Rev Proc (3)(c)).

34 Example 1 Continued 2 Corrections. 30 Wanda Widow bought the lot next door to rental 3 years ago Paid $100,000 and depreciated it How would the 2 adjustments appear on Form 3115? Depreciated Land Did not depreciate building

35 31 Negative adjustment portion The $59,583 of missed deductions will all be deducted in the current year. Positive adjustment portion The $8,636 of overstated deductions on the land results in additional income. The income is reported over 4 years (the current year and the next 3 years), unless the additional income is less than $50,000 and the taxpayer elects to report all of the income in the current year.

36 32

adjustment in the current year, as she will pay no tax in")

37 Example 1 Continued 33 What if Wanda is in a $0 tax bracket? She should elect to report the entire positive 481(a) adjustment in the current year, as she will pay no tax in the current year and reporting the income in future years might result in tax. On Page 4 of Form 3115, check the box for Line 27 Yes and check the box for the $50,000 de minimis election. On the attached worksheet, be sure to answer the questions at the bottom appropriately.

38 34

39 35 Yes, but no CA Form 3115 CA generally allows the same adjustments under section 481(a) that are allowed on the federal return, does not have a separate Form If there are basis differences that result in a different CA 481(a) adjustment amount, make an adjustment on the California Schedule CA for the Schedule C, Schedule E, etc. CA Conformity? Amending Form 3115 If a taxpayer submits additional correspondence regarding its Form 3115 filed under the automatic change procedures (for example, a revised 481(a) adjustment or power of attorney), it must attach a copy of the additional correspondence behind a copy of page 1 of the previously filed Form 3115 and submit it to the IRS at the current address for submission of original Forms 3115.

40 Form 3115 Attachment Worksheet for 36 An Excel fill-in version of this worksheet can be downloaded from my website at

Form 3115 Line-by-Line

Form 3115 Line-by-Line All audio is streamed through your computer speakers. There will be several attendance verification questions during the LIVE webinar that must be answered via the online quiz at

Form 3115 Line-by-Line All audio is streamed through your computer speakers. There will be several attendance verification questions during the LIVE webinar that must be answered via the online quiz at

Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations

FOR LIVE PROGRAM ONLY Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations WEDNESDAY, MAY 4, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY Form 3115 Change in Accounting Method: Navigating the IRS Repair Regulations WEDNESDAY, MAY 4, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Accounting Method Changes Current and Future State. American Bar Association Section of Taxation Tax Accounting Committee January 21, 2011

Accounting Method Changes Current and Future State American Bar Association Section of Taxation Tax Accounting Committee January 21, 2011 George Blaine Associate Chief Counsel (Income Tax & Accounting)

Accounting Method Changes Current and Future State American Bar Association Section of Taxation Tax Accounting Committee January 21, 2011 George Blaine Associate Chief Counsel (Income Tax & Accounting)

26 C.F.R Changes in accounting periods and in methods of accounting

Part III Administrative, Procedural, and Miscellaneous 26 C.F.R. 601.204 Changes in accounting periods and in methods of accounting (Also Part I, 118, 162, 167, 168, 263A, 446, 451; 461, 471, 472, 481,

Part III Administrative, Procedural, and Miscellaneous 26 C.F.R. 601.204 Changes in accounting periods and in methods of accounting (Also Part I, 118, 162, 167, 168, 263A, 446, 451; 461, 471, 472, 481,

(4) Before afederal court. 14

Before afederal court. 14") 26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 446, 481; 1.446 1, 1.481 1, 1.481 4.) Rev. Proc. 97 27 TABLE OF CONTENTS PAGE SECTION 1. PURPOSE... 11.01 In general...

26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 446, 481; 1.446 1, 1.481 1, 1.481 4.) Rev. Proc. 97 27 TABLE OF CONTENTS PAGE SECTION 1. PURPOSE... 11.01 In general...

Foreign corporations: Procedures and pitfalls in adopting and changing methods of accounting for purposes of determining E&P

Foreign corporations: Procedures and pitfalls in adopting and changing methods of accounting for purposes of determining E&P Prepared by: Kate Abdoo, J.D., LL.M., Manager, McGladrey LLP 203.328.7101, kate.abdoo@mcgladrey.com

Foreign corporations: Procedures and pitfalls in adopting and changing methods of accounting for purposes of determining E&P Prepared by: Kate Abdoo, J.D., LL.M., Manager, McGladrey LLP 203.328.7101, kate.abdoo@mcgladrey.com

Form 3115 Application for Change in Accounting Method

Form 3115 Application for Change in Accounting Method (Rev. December 2015) Department of the Treasury Information about Form 3115 and its separate instructions is at www.irs.gov/form3115. Internal Revenue

Form 3115 Application for Change in Accounting Method (Rev. December 2015) Department of the Treasury Information about Form 3115 and its separate instructions is at www.irs.gov/form3115. Internal Revenue

Revenue Procedure 97-27

CLICK HERE to return to the home page Revenue Procedure 97-27 TABLE OF CONTENTS SECTION 1. PURPOSE.01 In general.02 Voluntary compliance.03 Significant changes SECTION 2. BACKGROUND.01 Change in method

CLICK HERE to return to the home page Revenue Procedure 97-27 TABLE OF CONTENTS SECTION 1. PURPOSE.01 In general.02 Voluntary compliance.03 Significant changes SECTION 2. BACKGROUND.01 Change in method

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS COMMENTS ON MODIFICATIONS TO REVENUE PROCEDURES AND

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS COMMENTS ON MODIFICATIONS TO REVENUE PROCEDURES 97-27 AND 2002-9 Developed by the Accounting Methods Change Task Force Paul K. Gibbs, Task Force Chair

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS COMMENTS ON MODIFICATIONS TO REVENUE PROCEDURES 97-27 AND 2002-9 Developed by the Accounting Methods Change Task Force Paul K. Gibbs, Task Force Chair

July 30, Ms. Lisa Zarlenga Tax Legislative Counsel Department of the Treasury 1500 Pennsylvania Avenue, N.W MT Washington, D.C.

Ms. Lisa Zarlenga Tax Legislative Counsel Department of the Treasury 1500 Pennsylvania Avenue, N.W. 3040 MT Washington, D.C. 20220 RE: Comments on the Definition of Issue under Consideration Certain Foreign

Ms. Lisa Zarlenga Tax Legislative Counsel Department of the Treasury 1500 Pennsylvania Avenue, N.W. 3040 MT Washington, D.C. 20220 RE: Comments on the Definition of Issue under Consideration Certain Foreign

Chief Counsel Advice on the Acceleration of a 481(a) Adjustment

Adjustment") Office of Chief Counsel Internal Revenue Service Memorandum Number: 200935024 Release Date: 8/28/2009 CC:ITA:6, LFNOLANII PREF-127815-09 UILC: 446.19-00, 472.06-00, 481.06-00, 481.07-00 date: August 17,

Office of Chief Counsel Internal Revenue Service Memorandum Number: 200935024 Release Date: 8/28/2009 CC:ITA:6, LFNOLANII PREF-127815-09 UILC: 446.19-00, 472.06-00, 481.06-00, 481.07-00 date: August 17,

Instructions for Form 990-BL

Instructions for Form 990-BL (Rev. December 2008) Information and Initial Excise Tax Return for Black Lung Benefit Trusts and Certain Related Persons Department of the Treasury Internal Revenue Service

Instructions for Form 990-BL (Rev. December 2008) Information and Initial Excise Tax Return for Black Lung Benefit Trusts and Certain Related Persons Department of the Treasury Internal Revenue Service

IRS Guidance - Errors on Form 5498 by Custodian May Cause Tax Trouble For Everyone

Published Since 1984 ALSO IN THIS ISSUE Final Review 2014 Form 5498, Page 2 CWF s Guide for the IRS Distribution Codes For Box 7 of the 2015 Form 1099-R, Page 6 Using K Code on Form 1099-R, Page 8 Collin

Published Since 1984 ALSO IN THIS ISSUE Final Review 2014 Form 5498, Page 2 CWF s Guide for the IRS Distribution Codes For Box 7 of the 2015 Form 1099-R, Page 6 Using K Code on Form 1099-R, Page 8 Collin

Bankruptcy How Does it Affect Form 1040?

How Does it Affect Form 1040? For Excel worksheets with formulas go to: www.lisaihm.com User name: lisaihm Password is case sensitive: CODintheREALWORLD This text has been prepared with due diligence.

How Does it Affect Form 1040? For Excel worksheets with formulas go to: www.lisaihm.com User name: lisaihm Password is case sensitive: CODintheREALWORLD This text has been prepared with due diligence.

IRA Contribution Limits for 2018 Unchanged at $5,500 and $6,500; 401(k) Limits Do Change

Limits Do Change") Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Recent Developments in Tax Accounting. Dwight Mersereau

Recent Developments in Tax Accounting Dwight Mersereau Agenda Revised Accounting Method Change Procedures Expense Recognition Fines & Penalties Section 199 Update on Tangible Property Regulations 1 Revised

Recent Developments in Tax Accounting Dwight Mersereau Agenda Revised Accounting Method Change Procedures Expense Recognition Fines & Penalties Section 199 Update on Tangible Property Regulations 1 Revised

Plan Sponsor Administrative Manual

Plan Sponsor Administrative Manual V 3.1 Sponsor Access Website January 2017 Table of Contents Welcome Overview... p 5 How to Use this Manual... p 5 Enrollment Overview... p 7 Online Enrollment Description...

Plan Sponsor Administrative Manual V 3.1 Sponsor Access Website January 2017 Table of Contents Welcome Overview... p 5 How to Use this Manual... p 5 Enrollment Overview... p 7 Online Enrollment Description...

2015 Continuing Education Course. THE TAX INSTITUTE th St Bakersfield CA THE TAX INSTITUTE S ANNUAL CPE COURSE 15HR COURSE

THE TAX INSTITUTE 424 18 th St Bakersfield CA 93301. 2015 Continuing Education Course THE TAX INSTITUTE S ANNUAL CPE COURSE 15HR COURSE IRS # N56QT-T-00018-15-S, N56QT-U-00017-15-S, & N56QT-E-00019-15-S

THE TAX INSTITUTE 424 18 th St Bakersfield CA 93301. 2015 Continuing Education Course THE TAX INSTITUTE S ANNUAL CPE COURSE 15HR COURSE IRS # N56QT-T-00018-15-S, N56QT-U-00017-15-S, & N56QT-E-00019-15-S

ALSO IN THIS ISSUE. The 2004 IRS Form Inherited IRAs and Checkbox 11 (Required Minimum Distribution) on Form 5498

on Form 5498") April 2005 Published Since 1984 ALSO IN THIS ISSUE Completing the 2004 Form 5498-SA, Page 3 Question and Answer, Page 3 Additional Discussion of Automatic Rollover Rules, Page 4 A Planning Technique, Page

April 2005 Published Since 1984 ALSO IN THIS ISSUE Completing the 2004 Form 5498-SA, Page 3 Question and Answer, Page 3 Additional Discussion of Automatic Rollover Rules, Page 4 A Planning Technique, Page

Capital Asset Taxation Introduction

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Common BAS errors. General.

Page 1 of 8 Common BAS errors General Including wages and superannuation contributions as purchases at G11 Including wages and superannuation contributions as purchases at G11 Lodgment of blank forms Lodgment

Page 1 of 8 Common BAS errors General Including wages and superannuation contributions as purchases at G11 Including wages and superannuation contributions as purchases at G11 Lodgment of blank forms Lodgment

Sage Bank Services User's Guide

Sage 300 2017 Bank Services User's Guide This is a publication of Sage Software, Inc. Copyright 2016. Sage Software, Inc. All rights reserved. Sage, the Sage logos, and the Sage product and service names

Sage 300 2017 Bank Services User's Guide This is a publication of Sage Software, Inc. Copyright 2016. Sage Software, Inc. All rights reserved. Sage, the Sage logos, and the Sage product and service names

Application for Change in Accounting Method OMB No

1/22/15 Sample Form 3115 - Be sure to see the included comments and read Rev. Proc. 2014-16. Also see TD 9636 for references to method changes such as 1.162-4(b) and 1.263(a)-3(q)+ see 3115 instructions.

1/22/15 Sample Form 3115 - Be sure to see the included comments and read Rev. Proc. 2014-16. Also see TD 9636 for references to method changes such as 1.162-4(b) and 1.263(a)-3(q)+ see 3115 instructions.

2015 NATIONAL INCOME TAX WORKBOOK

2015 NATIONAL INCOME TAX WORKBOOK Updates Individual Shared Responsibility Payment (pages 475-478) As noted in the Practitioner Note on page 476 of the 2015 National Income Tax Workbook, the August 25,

2015 NATIONAL INCOME TAX WORKBOOK Updates Individual Shared Responsibility Payment (pages 475-478) As noted in the Practitioner Note on page 476 of the 2015 National Income Tax Workbook, the August 25,

CPA Says Error, IRS Says Method March 17, 2008

CPA Says Error, IRS Says Method March 17, 2008 Feed address for Podcast subscription: http://feeds.feedburner.com/edzollarstaxupdate Home page for Podcast: http://ezollars.libsyn.com 2008 Edward K. Zollars,

CPA Says Error, IRS Says Method March 17, 2008 Feed address for Podcast subscription: http://feeds.feedburner.com/edzollarstaxupdate Home page for Podcast: http://ezollars.libsyn.com 2008 Edward K. Zollars,

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years Brown, TC Memo 2016-82 The Tax Court has held that IRS was not wrong to reject, based on several failings by

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years Brown, TC Memo 2016-82 The Tax Court has held that IRS was not wrong to reject, based on several failings by

Revenue Procedure

CLICK HERE to return to the home page Revenue Procedure 2002-19 SECTION 1. PURPOSE This revenue procedure modifies Rev. Proc. 97-27 (1997-1 C.B. 680) which provides procedures under which taxpayers may

CLICK HERE to return to the home page Revenue Procedure 2002-19 SECTION 1. PURPOSE This revenue procedure modifies Rev. Proc. 97-27 (1997-1 C.B. 680) which provides procedures under which taxpayers may

Sage Bank Services User's Guide. May 2017

Sage 300 2018 Bank Services User's Guide May 2017 This is a publication of Sage Software, Inc. 2017 The Sage Group plc or its licensors. All rights reserved. Sage, Sage logos, and Sage product and service

Sage 300 2018 Bank Services User's Guide May 2017 This is a publication of Sage Software, Inc. 2017 The Sage Group plc or its licensors. All rights reserved. Sage, Sage logos, and Sage product and service

Supplement: Estates. Support.DrakeSoftware.com

Supplement: Estates Support.DrakeSoftware.com 828.524.8020 Drake Tax User s Manual Tax Year 2017 Supplement: Estates (706) support.drakesoftware.com (828) 524-8020 Drake Tax Manual Supplement: Estates

Supplement: Estates Support.DrakeSoftware.com 828.524.8020 Drake Tax User s Manual Tax Year 2017 Supplement: Estates (706) support.drakesoftware.com (828) 524-8020 Drake Tax Manual Supplement: Estates

Current Federal Tax Developments

Current Federal Tax Developments Week of August 6, 2018 Edward K. Zollars, CPA (Licensed in Arizona) CURRENT FEDERAL TAX DEVELOPMENTS WEEK OF AUGUST 6, 2018 2018 Kaplan, Inc. Published in 2018 by Kaplan

Current Federal Tax Developments Week of August 6, 2018 Edward K. Zollars, CPA (Licensed in Arizona) CURRENT FEDERAL TAX DEVELOPMENTS WEEK OF AUGUST 6, 2018 2018 Kaplan, Inc. Published in 2018 by Kaplan

User guide for employers not using our system for assessment

For scheme administrators User guide for employers not using our system for assessment Workplace pensions CONTENTS Welcome... 6 Getting started... 8 The dashboard... 9 Import data... 10 How to import a

For scheme administrators User guide for employers not using our system for assessment Workplace pensions CONTENTS Welcome... 6 Getting started... 8 The dashboard... 9 Import data... 10 How to import a

July 9, Re: Comments on Modifications to Rev. Proc and Dear Mr. Keyso:

July 9, 2013 Mr. Andrew Keyso, Jr. Associate Chief Counsel (Income Tax & Accounting) Internal Revenue Service 1111 Constitution Avenue, N.W. Washington, D.C. 20224 Re: Comments on Modifications to Rev.

July 9, 2013 Mr. Andrew Keyso, Jr. Associate Chief Counsel (Income Tax & Accounting) Internal Revenue Service 1111 Constitution Avenue, N.W. Washington, D.C. 20224 Re: Comments on Modifications to Rev.

Street Address. PRIMARY Beneficiary(ies) % Column MUST total 100% % Name Mailing Address Relationship Birth Date SS #

% Column MUST total 100% % Name Mailing Address Relationship Birth Date SS #") TRADITIONAL IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address

TRADITIONAL IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2012 NAME AND ADDRESS

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2012 NAME AND ADDRESS First name Spouse s first name (To be used by resident taxpayers only) Initial Initial Last name Last name Your

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2012 NAME AND ADDRESS First name Spouse s first name (To be used by resident taxpayers only) Initial Initial Last name Last name Your

Capital Gain or Loss. Form 1040 Line 13 Pub 4012 Tab D Pages Pub 4491 Part 3 Lesson 11

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

General Information for 401k Plan Participant

General Information for 401k Plan Participant Welcome to our 401(k) Guide for the Plan Participant! The information contained on this site was designed and developed by various governmental agencies, and

General Information for 401k Plan Participant Welcome to our 401(k) Guide for the Plan Participant! The information contained on this site was designed and developed by various governmental agencies, and

Overview. It is basically a History report!

General Ledger Overview The Service Assistant s General Ledger report presents a synopsis of all transactions during aspecified period of time, giving dollar amounts posted as both a credit and debit.

General Ledger Overview The Service Assistant s General Ledger report presents a synopsis of all transactions during aspecified period of time, giving dollar amounts posted as both a credit and debit.

This notice requires you by law to send us a

Partnership Tax Return for the year ended 5 April 2014 Tax reference Date Issue address HM Revenue & Customs office address Telephone This notice requires you by law to send us a tax return giving details

Partnership Tax Return for the year ended 5 April 2014 Tax reference Date Issue address HM Revenue & Customs office address Telephone This notice requires you by law to send us a tax return giving details

Preparer (other than filer/applicant) Signature of individual preparing the application and date

Signature of individual preparing the application and date") Form 3115 (Rev. December 2003) Application for Change in Accounting Method OMB No. 1545-0152 Department of the Treasury Internal Revenue Service Name of filer (name of parent corporation if a consolidated

Form 3115 (Rev. December 2003) Application for Change in Accounting Method OMB No. 1545-0152 Department of the Treasury Internal Revenue Service Name of filer (name of parent corporation if a consolidated

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2011 NAME AND ADDRESS

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2011 NAME AND ADDRESS First name Spouse s first name (To be used by resident taxpayers only) Initial Initial Last name Last name Your

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2011 NAME AND ADDRESS First name Spouse s first name (To be used by resident taxpayers only) Initial Initial Last name Last name Your

Updates to Automatic Accounting Method Change Procedures

Updates to Automatic Accounting Method Change Procedures On January 10, 2011, the IRS issued new procedures (Rev. Proc. 2011-14) applicable to automatic changes in accounting method. Rev. Proc. 2011-14

Updates to Automatic Accounting Method Change Procedures On January 10, 2011, the IRS issued new procedures (Rev. Proc. 2011-14) applicable to automatic changes in accounting method. Rev. Proc. 2011-14

Gleim EA Review Updates to Part Edition, 1st Printing April 2016

Page 1 of 6 Gleim EA Review Updates to Part 3 2016 Edition, 1st Printing April 2016 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. This

Page 1 of 6 Gleim EA Review Updates to Part 3 2016 Edition, 1st Printing April 2016 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. This

IRS FORM 944. Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps.

IRS FORM 944 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 944:

IRS FORM 944 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 944:

Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

ERIC P WALLACE CPA TPR TOOLS AND TEMPLATES - TABLE OF CONTENTS. Section Listing: Number Description. Index Number. Name of the Document.

Eric P. Wallace LLC (1/16/2017) 1 ERIC P WALLACE CPA TPR TOOLS AND TEMPLATES - TABLE OF CONTENTS Copyright Eric P. Wallace LLC, January 2017 TPR (Tangible Property Regulations) Tools and Templates (items

Eric P. Wallace LLC (1/16/2017) 1 ERIC P WALLACE CPA TPR TOOLS AND TEMPLATES - TABLE OF CONTENTS Copyright Eric P. Wallace LLC, January 2017 TPR (Tangible Property Regulations) Tools and Templates (items

Application for Change in Accounting Method OMB No

Form 3115 (Rev. December 2009) Department of the Treasury Internal Revenue Service Name of filer (name of parent corporation if a consolidated group) (see instructions) Application for Change in Accounting

Form 3115 (Rev. December 2009) Department of the Treasury Internal Revenue Service Name of filer (name of parent corporation if a consolidated group) (see instructions) Application for Change in Accounting

Partner s Instructions for Schedule K-1 (Form 1065-B) Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only)

Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only)") 2008 Partner s Instructions for Schedule K-1 (Form 1065-B) Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only) Section references are to the Internal Revenue Code

2008 Partner s Instructions for Schedule K-1 (Form 1065-B) Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only) Section references are to the Internal Revenue Code

Instructions for Form 1128

Instructions for Form 1128 (Rev. January 2008) Application To Adopt, Change, or Retain a Tax Year Department of the Treasury Internal Revenue Service Section references are to the Internal Regulations

Instructions for Form 1128 (Rev. January 2008) Application To Adopt, Change, or Retain a Tax Year Department of the Treasury Internal Revenue Service Section references are to the Internal Regulations

VisionVPM General Ledger Module User Guide

VisionVPM General Ledger Module User Guide Version 1.0 VisionVPM user documentation is continually being developed. For the most up-to-date documentation please visit the VisionVPM website at www.visionvpm.com

VisionVPM General Ledger Module User Guide Version 1.0 VisionVPM user documentation is continually being developed. For the most up-to-date documentation please visit the VisionVPM website at www.visionvpm.com

Debtors Account Validity Help

Debtors Account Validity Help An Account Validity is run prior to sending out the monthly accounts. This ensures that the correct billing is sent to the Families, if there are any errors they must be corrected

Debtors Account Validity Help An Account Validity is run prior to sending out the monthly accounts. This ensures that the correct billing is sent to the Families, if there are any errors they must be corrected

UCAA Expansion Application Insurer User Guide December 2017

UCAA Expansion Application Insurer User Guide December 2017 2017 National Association of Insurance Commissioners All rights reserved. Revised Edition National Association of Insurance Commissioners NAIC

UCAA Expansion Application Insurer User Guide December 2017 2017 National Association of Insurance Commissioners All rights reserved. Revised Edition National Association of Insurance Commissioners NAIC

.02 Changes to 481(a) Spread Period for Negative 481(a) Adjustments. (1) Section 5.02(3)(a) of Rev. Proc is modified to read as follows:

Spread Period for Negative 481(a) Adjustments. (1) Section 5.02(3)(a) of Rev. Proc is modified to read as follows:") 26 CFR 601.204: Changes in accounting periods and methods of accounting. (Also Part I, 446, 481; 1.446 1, 1.481 1, 1.481 4.) Rev. Proc. 2002 19 SECTION 1. PURPOSE This revenue procedure modifies Rev. Proc.

26 CFR 601.204: Changes in accounting periods and methods of accounting. (Also Part I, 446, 481; 1.446 1, 1.481 1, 1.481 4.) Rev. Proc. 2002 19 SECTION 1. PURPOSE This revenue procedure modifies Rev. Proc.

Default Management Reporting System (DMRS) Correcting Event Failures and the Failed Submitted Events Report Job Aid

Correcting Event Failures and the Failed Submitted Events Report Job Aid") Default Management Reporting System (DMRS) Correcting Event Failures and the Failed Submitted Events Report Job Aid 2016 Fannie Mae. Trademarks of Fannie Mae. Version 2, Page 1 Table of Contents Purpose...

Default Management Reporting System (DMRS) Correcting Event Failures and the Failed Submitted Events Report Job Aid 2016 Fannie Mae. Trademarks of Fannie Mae. Version 2, Page 1 Table of Contents Purpose...

IRS FORM 941. Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps.

IRS FORM 941 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 941:

IRS FORM 941 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 941:

Employee Plans Compliance Resolution System: Revenue Procedure

What Can Go Wrong, but More Importantly, How to Correct It! Monday, April 29, 2013 Barbara M. Clough, QPA, QKA, Director of Plan Administration, Blue Ridge ESOP Associates Avaneesh Bhagat, IRS Employee

What Can Go Wrong, but More Importantly, How to Correct It! Monday, April 29, 2013 Barbara M. Clough, QPA, QKA, Director of Plan Administration, Blue Ridge ESOP Associates Avaneesh Bhagat, IRS Employee

Presented by: Alexander Bagne, JD, CPA, MBA, CCSP President ICS Tax, LLC October 27,

Presented by: Alexander Bagne, JD, CPA, MBA, CCSP President ICS Tax, LLC October 27, 2017 www.ics-tax.com Taxpayers and tax professionals use accounting method changes as a powerful mechanism to implement

Presented by: Alexander Bagne, JD, CPA, MBA, CCSP President ICS Tax, LLC October 27, 2017 www.ics-tax.com Taxpayers and tax professionals use accounting method changes as a powerful mechanism to implement

Partnership Tax Return 2018 for the year ended 5 April 2018 ( )

") Partnership Tax Return 2018 for the year ended 5 April 2018 (2017 18) Tax reference Date Issue address HM Revenue and Customs office address Telephone For Reference This notice requires you by law to send

Partnership Tax Return 2018 for the year ended 5 April 2018 (2017 18) Tax reference Date Issue address HM Revenue and Customs office address Telephone For Reference This notice requires you by law to send

New Accounting Method Rules for Small Business Taxpayers Under IRC 448

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

FOR LIVE PROGRAM ONLY New Accounting Method Rules for Small Business Taxpayers Under IRC 448 THURSDAY, FEBRUARY 7, 2019, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

LENDER SOFTWARE PRO USER GUIDE

LENDER SOFTWARE PRO USER GUIDE You will find illustrated step-by-step examples in these instructions. We recommend you print out these instructions and read at least pages 4 to 20 before you start using

LENDER SOFTWARE PRO USER GUIDE You will find illustrated step-by-step examples in these instructions. We recommend you print out these instructions and read at least pages 4 to 20 before you start using

Do your taxes online with H&R Block. Do your taxes online with H&R Block. Do your taxes online with H&R Block.

Send Friend (2004) FDFRNDOL-1WV 1.0 Send a friend to us. We'll thank you both with cash! 5 for you. 10 for your friend! Easy-to-follow instructions: 1. 2. 3. Give one of the forms below to a friend and

Send Friend (2004) FDFRNDOL-1WV 1.0 Send a friend to us. We'll thank you both with cash! 5 for you. 10 for your friend! Easy-to-follow instructions: 1. 2. 3. Give one of the forms below to a friend and

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2011 NAME AND ADDRESS

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2011 NAME AND ADDRESS First name Spouse s first name (To be used by nonresident and part-year resident taxpayers only) Initial

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2011 NAME AND ADDRESS First name Spouse s first name (To be used by nonresident and part-year resident taxpayers only) Initial

Clickheretoview thethirdquarter2014issue

Clickheretoview thethirdquarter2014issue Tax Controversy Corner A Second Chance to Get it Right: Section 9100 Relief for Missed Elections By Megan L. Brackney A taxpayer who fails to make a timely election

Clickheretoview thethirdquarter2014issue Tax Controversy Corner A Second Chance to Get it Right: Section 9100 Relief for Missed Elections By Megan L. Brackney A taxpayer who fails to make a timely election

Refund Application Checklist

Refund Application Checklist Before completing your application: Have you read the CalSTRS publication, Refund: Consider the Consequences, available at CalSTRS.com/publications? Have you watched the CalSTRS

Refund Application Checklist Before completing your application: Have you read the CalSTRS publication, Refund: Consider the Consequences, available at CalSTRS.com/publications? Have you watched the CalSTRS

Oregon Personal Income Tax

Oregon Personal Income Tax Electronic Filing Handbook For Software Developers and Tax Preparers Tax Year 2008 Published by Oregon Department of Revenue 10/08/2008 2:38 PM 1 Oregon Electronic Filing Business

Oregon Personal Income Tax Electronic Filing Handbook For Software Developers and Tax Preparers Tax Year 2008 Published by Oregon Department of Revenue 10/08/2008 2:38 PM 1 Oregon Electronic Filing Business

Revenue Procedure 98-1

Revenue Procedure 98-1 Reprinted from IR Bulletin 1998-1 Dated January 5, 1998 Procedures for Issuing Rulings, Determination Letters, and Information Letters, and for Entering Into Closing Agreements on

Revenue Procedure 98-1 Reprinted from IR Bulletin 1998-1 Dated January 5, 1998 Procedures for Issuing Rulings, Determination Letters, and Information Letters, and for Entering Into Closing Agreements on

2017 Continuing Education Course. THE TAX INSTITUTE th St Bakersfield CA THE TAX INSTITUTE S ANNUAL CPE COURSE 20HR COURSE

THE TAX INSTITUTE. 424 18 th St Bakersfield CA 93301. 2017 Continuing Education Course THE TAX INSTITUTE S ANNUAL CPE COURSE 20HR COURSE CTEC # 1007-CE-0017; IRS # N56QT-T-00027-17-S, N56QT-U-00028-17-S,

THE TAX INSTITUTE. 424 18 th St Bakersfield CA 93301. 2017 Continuing Education Course THE TAX INSTITUTE S ANNUAL CPE COURSE 20HR COURSE CTEC # 1007-CE-0017; IRS # N56QT-T-00027-17-S, N56QT-U-00028-17-S,

Employee Plans Compliance Resolution System: Revenue Procedure

Employee Plans Compliance Resolution System: Revenue Procedure 2013-12 Thelma Diaz IRS Employee Plans Voluntary Compliance Thelma.C.Diaz@irs.gov EPCRS Employee Plans Compliance Resolution System (EPCRS)

Employee Plans Compliance Resolution System: Revenue Procedure 2013-12 Thelma Diaz IRS Employee Plans Voluntary Compliance Thelma.C.Diaz@irs.gov EPCRS Employee Plans Compliance Resolution System (EPCRS)

If a joint return, spouse s first name and initial Last name Spouse s social security number

Form Department of the Treasury Internal Revenue Service 1040A U.S. Individual Income Tax Return (99) 2016 Your first name and initial Last name IRS Use Only Do not write or staple in this space. OMB No.

Form Department of the Treasury Internal Revenue Service 1040A U.S. Individual Income Tax Return (99) 2016 Your first name and initial Last name IRS Use Only Do not write or staple in this space. OMB No.

State of New Jersey Department of Education Division of Administration & Finance Office of School Finance

2016-2017 State of New Jersey Department of Education Division of Administration & Finance Office of School Finance Audit Summary Online Technical Manual Table of Contents Purpose.. 3 Submission dates....

2016-2017 State of New Jersey Department of Education Division of Administration & Finance Office of School Finance Audit Summary Online Technical Manual Table of Contents Purpose.. 3 Submission dates....

This publication is one of a series of practicals that

PRACTICAL WAR TAX RESISTANCE #1 Controlling Federal Income Tax Withholding This publication is one of a series of practicals that offer ideas, tips, and information for individuals who want to cut off

PRACTICAL WAR TAX RESISTANCE #1 Controlling Federal Income Tax Withholding This publication is one of a series of practicals that offer ideas, tips, and information for individuals who want to cut off

This Notice requires you by law to send us a Tax

Partnership Tax Return for the year ended 5 April 2009 Tax reference Date Issue address HM Revenue & Customs office address SA800 Telephone This Notice requires you by law to send us a Tax Return, and

Partnership Tax Return for the year ended 5 April 2009 Tax reference Date Issue address HM Revenue & Customs office address SA800 Telephone This Notice requires you by law to send us a Tax Return, and

TaxSlayer Training Webinar March 1, NOTE: A recording of this webinar is now available at:

TaxSlayer Training Webinar March 1, 2017 NOTE: A recording of this webinar is now available at: http://tinyurl.com/h4cywvm Introduction to webinar and welcome by Jay Wiedwald. A pdf of the slides can be

TaxSlayer Training Webinar March 1, 2017 NOTE: A recording of this webinar is now available at: http://tinyurl.com/h4cywvm Introduction to webinar and welcome by Jay Wiedwald. A pdf of the slides can be

Rev. Proc I.R.B. 678 April 1, 2002

26 CFR 601.105: Examination of returns and claims for refund, credit, or abatement; determination of correct tax liability. (Also Part 1, 446, 481; 1.446 1, 1.481 1) Rev. Proc. 2002 18 SECTION 1. PURPOSE...680.01

26 CFR 601.105: Examination of returns and claims for refund, credit, or abatement; determination of correct tax liability. (Also Part 1, 446, 481; 1.446 1, 1.481 1) Rev. Proc. 2002 18 SECTION 1. PURPOSE...680.01

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Fiduciary Income Tax for Estates

PBI Electronic Publication # EP-2669 Fiduciary Income Tax for Estates Paula M. Jones, Esquire McCarter & English, LLP Philadelphia A chapter from Post Mortem Estate Planning Pub. No. 4643, published June

PBI Electronic Publication # EP-2669 Fiduciary Income Tax for Estates Paula M. Jones, Esquire McCarter & English, LLP Philadelphia A chapter from Post Mortem Estate Planning Pub. No. 4643, published June

IRS. 401(k) Plan Checklist. If you answered No to any of the above questions, you may have made a mistake in the

Plan Checklist. If you answered No to any of the above questions, you may have made a mistake in the") 401(k) Plan Checklist This checklist is not a complete description of all For Business Owner s Use plan requirements, and should not be used as a (do not send this worksheet to the IRS) substitute for

401(k) Plan Checklist This checklist is not a complete description of all For Business Owner s Use plan requirements, and should not be used as a (do not send this worksheet to the IRS) substitute for

Street Address. City, State, ZIP

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

ProSystem fx. Consolidated. Electronic Filing. Quick Start Guide

ProSystem fx Electronic Filing Consolidated Electronic Filing Quick Start Guide January 2015 Copyright 2015, CCH INCORPORATED. A Wolters Kluwer business. All Right Reserved. Material in this publication

ProSystem fx Electronic Filing Consolidated Electronic Filing Quick Start Guide January 2015 Copyright 2015, CCH INCORPORATED. A Wolters Kluwer business. All Right Reserved. Material in this publication

Estate Tax Form M706 Instructions 2010

Estate Tax Form M706 Instructions 2010 For estates of decedents whose dates of death are in calendar year 2010 Questions? You can find forms and information, including answers to frequently asked questions

Estate Tax Form M706 Instructions 2010 For estates of decedents whose dates of death are in calendar year 2010 Questions? You can find forms and information, including answers to frequently asked questions

Using FastCensus for Plan Sponsors

Using FastCensus for Plan Sponsors FastCensus is a secure, online tool for Plan Sponsors to access, edit, validate and submit census data to their Third Party Administrator for the purposes of year-end

Using FastCensus for Plan Sponsors FastCensus is a secure, online tool for Plan Sponsors to access, edit, validate and submit census data to their Third Party Administrator for the purposes of year-end

QuickBooks. For Evaluation Only. Premier 2015 Level 2. Courseware MasterTrak Accounting Series

QuickBooks Premier 2015 Level 2 Courseware 1702-1 MasterTrak Accounting Series QuickBooks Premier 2015 Level 2 Lesson 2: Banking and Credit Cards Lesson Objectives In this lesson you will learn how to

QuickBooks Premier 2015 Level 2 Courseware 1702-1 MasterTrak Accounting Series QuickBooks Premier 2015 Level 2 Lesson 2: Banking and Credit Cards Lesson Objectives In this lesson you will learn how to

Page 1 The TaxWise (UTS) phone number has been changed for us, It is now

phone number has been changed for us, It is now") AARP Tax-Aide Counselor Reference Manual This contains all changes to be applied to the 9/23/2009 version. This will then be version 3 Cover- Cross out CA2 in the title. Add Tax Year 2009. This manual

AARP Tax-Aide Counselor Reference Manual This contains all changes to be applied to the 9/23/2009 version. This will then be version 3 Cover- Cross out CA2 in the title. Add Tax Year 2009. This manual

State of Maryland Department of Labor, Licensing and Regulation Division of Unemployment Insurance Contributions Unit

Larry Hogan Governor Boyd K. Rutherford Lt. Governor State of Maryland Department of Labor, Licensing and Regulation Division of Unemployment Insurance Contributions Unit Quarterly Contribution & Employment

Larry Hogan Governor Boyd K. Rutherford Lt. Governor State of Maryland Department of Labor, Licensing and Regulation Division of Unemployment Insurance Contributions Unit Quarterly Contribution & Employment

Instructions for Form 8283

Instructions for Form 8283 (Rev. December 2006) Noncash Charitable Contributions Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Instructions for Form 8283 (Rev. December 2006) Noncash Charitable Contributions Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Income Tax Planning for IRAs & Qualified Plans

Income Tax Planning for IRAs & Qualified Plans Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Foundation Concepts Tax Brackets 2 Foundation Concepts General Income Tax Treatment Tax Deduction

Income Tax Planning for IRAs & Qualified Plans Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Foundation Concepts Tax Brackets 2 Foundation Concepts General Income Tax Treatment Tax Deduction

Office of the Commissioner of Banks

Office of the Commissioner of Banks REPORT TO THE GENERAL ASSEMBLY ON PAYDAY LENDING February 22, 2001 I. Consumer Complaints REPORT OF THE COMMISSIONER OF BANKS TO THE NORTH CAROLINA GENERAL ASSEMBLY

Office of the Commissioner of Banks REPORT TO THE GENERAL ASSEMBLY ON PAYDAY LENDING February 22, 2001 I. Consumer Complaints REPORT OF THE COMMISSIONER OF BANKS TO THE NORTH CAROLINA GENERAL ASSEMBLY

TABLE OF CONTENTS. .03 Farmers cooperatives. .01 A request made during the course of an examination

Rev. Proc. 2000 2 TABLE OF CONTENTS SECTION 1. WHAT IS THE p. 77 PURPOSE OF THIS REVENUE PROCEDURE? SECTION 2. WHAT IS p. 78 TECHNICAL ADVICE? SECTION 3. ON WHAT ISSUES p. 78 MAY TECHNICAL ADVICE BE REQUESTED

Rev. Proc. 2000 2 TABLE OF CONTENTS SECTION 1. WHAT IS THE p. 77 PURPOSE OF THIS REVENUE PROCEDURE? SECTION 2. WHAT IS p. 78 TECHNICAL ADVICE? SECTION 3. ON WHAT ISSUES p. 78 MAY TECHNICAL ADVICE BE REQUESTED

Partnership Tax Return 2017 for the year ended 5 April 2017 ( )

") Partnership Tax Return 2017 for the year ended 5 April 2017 (2016 17) Tax reference Date Issue address HM Revenue & Customs office address Telephone For Reference This notice requires you by law to send

Partnership Tax Return 2017 for the year ended 5 April 2017 (2016 17) Tax reference Date Issue address HM Revenue & Customs office address Telephone For Reference This notice requires you by law to send

Frank Aragona Trust v. Commissioner: Guidance at Last on The Material Participation Standard for Trusts? By Dana M. Foley 1

Frank Aragona Trust v. Commissioner: Guidance at Last on The Material Participation Standard for Trusts? By Dana M. Foley 1 Nearly a year after the enactment of the 3.8% Medicare Tax, taxpayers and fiduciaries

Frank Aragona Trust v. Commissioner: Guidance at Last on The Material Participation Standard for Trusts? By Dana M. Foley 1 Nearly a year after the enactment of the 3.8% Medicare Tax, taxpayers and fiduciaries

Estate Tax Form M706 Instructions 2012

Estate Tax Form M706 Instructions 2012 For estates of decedents whose dates of death are in calendar year 2012 Questions? You can find forms and information, including answers to frequently asked questions

Estate Tax Form M706 Instructions 2012 For estates of decedents whose dates of death are in calendar year 2012 Questions? You can find forms and information, including answers to frequently asked questions

NH Tax-Aide NH Form DP-10 Reference 2017 Returns

This document provides general information about NH state taxes and preparing state returns on TaxSlayer ( TSO ), and specific instructions for preparing the NH DP-10 using TSO and forms on the NH DRA

This document provides general information about NH state taxes and preparing state returns on TaxSlayer ( TSO ), and specific instructions for preparing the NH DP-10 using TSO and forms on the NH DRA

Capital Gain or Loss. Introduction. Capital Asset Taxation. Introduction. Capital Asset Taxation. What is a Capital Asset

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2013 NAME AND ADDRESS

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2013 NAME AND ADDRESS First name Spouse s first name (To be used by nonresident and part-year resident taxpayers only) Initial

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2013 NAME AND ADDRESS First name Spouse s first name (To be used by nonresident and part-year resident taxpayers only) Initial

How to Prepare Form 8868 to Get an Extension of Time to File Form 990 / 990-EZ / 990-T

How to Prepare Form 8868 to Get an Extension of Time to File Form 990 / 990-EZ / 990-T The Plain Language Instructions that Should Have Come With the Form by David B. McRee, CPA http://www.form990help.com

How to Prepare Form 8868 to Get an Extension of Time to File Form 990 / 990-EZ / 990-T The Plain Language Instructions that Should Have Come With the Form by David B. McRee, CPA http://www.form990help.com

Rev. Proc SECTION 1. PURPOSE

Rev. Proc. 91-51 SECTION 1. PURPOSE This revenue procedure tells taxpayers how to obtain consent to change their method of accounting for certain sales of mortgage loans (mortgages) from a method that

Rev. Proc. 91-51 SECTION 1. PURPOSE This revenue procedure tells taxpayers how to obtain consent to change their method of accounting for certain sales of mortgage loans (mortgages) from a method that

2015 Federal Tax Returns

2015 Federal Tax Returns All Knights of Columbus subordinate units in the United States must file an annual informational tax return (IRS Form 990) with the Internal Revenue Service (IRS). This memorandum

2015 Federal Tax Returns All Knights of Columbus subordinate units in the United States must file an annual informational tax return (IRS Form 990) with the Internal Revenue Service (IRS). This memorandum

PUBLIC DISCLOSURE COPY

Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) For calendar year 2014 or other tax year beginning, 2014, and ending, 20. Department of

Exempt Organization Business Income Tax Return OMB No. 1545-0687 Form 990-T (and proxy tax under section 6033(e)) For calendar year 2014 or other tax year beginning, 2014, and ending, 20. Department of

Income Tax and 1099 Preparation and Reporting

Income Tax and 1099 Preparation and Reporting Preparing income tax forms and 1099s are two of the most common ways in which practitioners become involved with their clients' QuickBooks data. This guide

Income Tax and 1099 Preparation and Reporting Preparing income tax forms and 1099s are two of the most common ways in which practitioners become involved with their clients' QuickBooks data. This guide

Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should