Welcome to VITA! Thank you for Volunteering!

|

|

|

- Rodger Adams

- 6 years ago

- Views:

Transcription

1 Welcome to VITA! Thank you for Volunteering!

2 This is our 4th year serving Washtenaw County Last year: We prepared 596 households Federal and State Most received refunds averaging just under $2000! That s more money coming into Washtenaw County There was more demand for assistance than we could cover.

3 What is VITA? VITA Program offers free tax help to people who make $54,000 or less & need assistance preparing their own tax returns. IRS-certified volunteers provide free basic income tax return preparation with electronic filing to qualified individuals in local communities.

4 We are a fusion site UWWC offers two options for free tax preparation: 1. VITA We prepare the return for the taxpayer using software you will be trained on. 2. Facilitated Self Assistance (FSA) Also known as MyFreeTaxes.com Taxpayer (TP) prepares own return using software and support.

5 How VITA works 1. Prior to their appointment taxpayers are pre-screened for eligibility 2. Taxpayers receive a letter detailing what to bring to their appointment as well as an intake form (13614-C, see example in packet) 3. Taxpayers first meet with a greeter/screener ensures they have all of their proper documents, their intake form is complete. 4. Taxpayers are assigned a tax preparer based on their returns certification level (Basic, Advanced, Foreign Student, etc.) 5. Tax preparers interviews client, reviews documents and prepare return. 6. All returns are reviewed by a second volunteer known as a quality reviewer (QR). QR volunteers must be certified to the level of return they are reviewing. 7. Client goes to exit table to receive copy of return, any paper-filed returns are printed out, signed & mailing instructions provided as well as fills out exit survey.

6 Tax Time Saving Initiative 1. (New for 2017) UWWC is encouraging individuals to save a portion of their refund 1. Taxpayers that split their refund to purchase $100 in saving bonds, open a MyRA account, or fund a saving account and taking a saving pledge will receive a gift card instantly and be entered into a drawing to win additional prizes. 2. To qualify taxpayers must be receiving the EITC or Home Heating Credit 2. What is MyRA? 1. Accessing MyRA can be done in TaxSlayer 2. Can be funded by their tax refund 3. Has the same tax benefits as a Roth IRA

7 FSA Software Model MyFreeTaxes.com Free federal returns; free state returns in all 50 states Income limit is $64,000 (individual or family income) Anyone can use this, from any computer! Hotline is available, and IRS-certified volunteers may be, to assist with tax questions and/or computer issues.

8 MyFreeTaxes User Support MyFreeTaxes Helpline : My-Tx-Help All clients using MyFreeTaxes.com supported by MyFreeTaxes Helpline Hours of Operation: 10am 8pm EST support is available 24/7 with 24 hour response time Live Chat support available during hours of operation Support provided for system navigation, tax preparation & if necessary other wrap-around services

9 General Information -How to make appointments -Season Schedule -Roles -Certification Requirements -IRS Link and Learn -After Certifying -Recap

10 How to Make Appointments Know someone who needs VITA s help? Have them call (734) or visit uwgive.org/mytaxes

11 Current Schedule Volunteer Shifts Wednesdays 5-8:30pm (Hamilton Crossing, February Only) Thursdays 5-8:30pm Saturdays 9am-1pm Saturdays 1pm-5pm Starting February 2th & continuing until April 15

12 Roles for VITA volunteers There are 4 roles for VITA volunteers: 1. Greeters must be complete Ethics and Intake certification tests 2. Tax Return Preparers must be certified at least to the basic level, & preferably to the advanced level using IRS s Link & Learn Certification program 3. Tax Return Reviewers must be certified at least to the advanced level using IRS s Link & Learn Certification program 4. Site Coordinators need additional training & have VITA experience.

13 Certification Requirements Depending on your role there are various certification tests All test questions can be found in Publication 6744 All VITA volunteers must complete Volunteer Standards of Conduct Test and the Intake/Interview and Quality Review Test. Each test contain 10 regular and 10 re-take questions. Please review all. Return preparers must complete either the basic or advanced certification test. We recommend all preparers certify at advanced

14 VITA Tax Preparer Certification 4011 & 4704FS New for 2017

15 IRS Link and Learn Certification can be completed at the IRS Link and Learn Website Select the VITA/TCE Central Link to access the testing site You have only two chances to pass your test, you can submit questions and your test answers for review to Once you have certified, please print your Volunteer Standards of Conduct Agreement and a PDF to the above Please save PDF as LastNameFirstInitial.pdf

16 After Certifying Sign up for at least 3 shifts ASAP with United Way. We need 2 greeters, 2 reviewers & preparers per shift. We are taking appointments for clients now, so signing up early helps us match clients to volunteers meeting their language or certification needs.

17 Recap For links to certification resources and webpages, go to Send all questions to Send your Volunteer Agreement form to the same address Sign up for shifts asap

18 Quality Site Requirement What you need to know about the intake and interview process?

19 Intake & Interview Process Form C is mandatory for all VITA/TCE sites See the Form C Job Aid Remember: 1. Screen for eligibility- Completed prior to appointment 2. Check identity- Greeters and preparers must check IDs 3. Check completed intake sheet for errors 4. Review supporting documents 5. Use probing questions 6. Unsure responses must be changed to Yes or No 7. Confirm the return is within program scope & your training 8. Conduct a quality review after return is prepared Lesson 2 Screening & Interviewing 19

20 Interview Techniques How do you? Build rapport Ask effective questions Use active listening skills Overcome communication barriers Important questions: Who lives in your house/apartment? Months/years in each home? Dependent relationship(s)? Marital status as of December 31? Lesson 2 Screening & Interviewing 20

21 Resources & Reminder Necessary tools for Screening & Interviewing (will be on your computer on-site): Form C, Intake/Interview & Quality Review Sheet Publication 4012, Volunteer Resource Guide Publication 17, Your Federal income Tax for Individuals Safeguard all TP information it is private & confidential Lesson 2 Screening & Interviewing 21

22 Tax Law Lesson 3 Filing Basics 22

23 Who Must File a Tax Return? What helps determine if an individual must file? Intake Form C Refer to Pub 4012, Charts A, B, & C, on pp A-1 to A- 3, tab A Net earnings from Self-employment income over $400 In what situations would an individual want to file if they are not required to? Find examples in Pub 4012, Tab A, Chart D FAFSA! Lesson 3 Filing Basics 23

24 Verifying TP Identity What are acceptable identity documents to verify identity? See the Tip in Pub 4491 What are acceptable Taxpayer Identification Numbers (TINs)? Enter names & identification numbers accurately Mistakes in data entry can result in processing delays See Pub 4012 (Tab N, Pages N-4-6), TaxWise Online Interview, for ID entries Verify TP information to protect against identity theft Remind TPs correct information necessary for age-related tax benefits Out of scope: TPs who cannot substantiate identity send them to FSA side. Lesson 3 Filing Basics 24

, Frequent TP Inquiries")

25 Administrative Questions? FAQ answers: Pub 4012 (Tab P, Page P-5), Frequent TP Inquiries Pub 17 Index Lesson 3 Filing Basics 25

26 Who s your family /in your household? This issue touches many areas of the tax return, 4 big ones are: 1. Filing Status (qualifying for more advantageous head of household ) 2. Dependency Exemptions (can someone claim a person as a dependent on their tax return) 3. EITC (tax credit for working poor is larger if you have qualifying children) & Child Tax Credits 4. ACA (Shared responsibility payment penalty ) Definitions are different for each, & some are not intuitive (for example, in some cases your brother is your child ). Use the resources & never guess. 26

27 The Five Filing Statuses Find relevant TP information on Form C, Part II: Marital Status & Household Information Filing status impacts: 1. Calculation of income tax 2. Amount of the standard deduction 3. Allowance or limitation of certain credits & deductions Use Filing Status Wizard function on in TaxSlayer if you are unsure of their filing status Pub 4012 (Tab B), Determination of Filing Status Decision Tree, pp B-1 through B-3 Pub 17, Chapter 2, Filing Status provides details Lesson 4 Filing Status 27

28 Filing Status- Decision Tree 28

, Filing Status Interview Tips Lesson 4 Filing")

29 Single On the last day of 2016 TP was: Not married Legally separated or divorced, or Widowed before first day of tax year, not remarried within the year May qualify for more beneficial tax status Pub 4012 (Tab B), Filing Status Interview Tips Lesson 4 Filing Status 29

30 Married Filing Jointly This filing status generally is the most beneficial One return is filed covering both spouses On the last day of 2016 TPs: Were married & live together Live apart but not legally separated or divorced Separated but divorce decree not final, or Widow(er) not remarried during 2016 Lesson 4 Filing Status 30

31 Married Filing Separately Taxes are generally higher for this status Some credits unavailable, some reduced Advantage, no joint & several liability Some TPs file separately to avoid potential refund offset due to spouse s outstanding debts Suggest Form 8379, Injured Spouse Allocation For the complete list of special rules, see Pub 17, Filing Status Lesson 4 Filing Status 31

32 Head of Household A TP may qualify if he or she: Is unmarried or considered unmarried on 12/31/16, and; Paid 50% or more of the cost of keeping up a home for 2016, and; Had a qualifying person living with them more than half the year (except for temporary absences) Qualifying person: Can be child, parent, or other relative See Pub 4012 (Tab B), Who is a Qualifying Person Lesson 4 Filing Status 32

33 Head of Household - Keeping Up a Home In general, the Head of Household status is for unmarried taxpayers who paid more than 1/2 the cost of keeping up a home for a qualifying person who lived with them in the home more than 1/ Valid household expenses include: Rent, mortgage interest, real estate taxes Home insurance, repairs, utilities Food eaten in the home Welfare or other public assistance payments are not considered amounts that the taxpayer provides to keep up a home. These payments must be included in the total cost of keeping up the home to determine if the taxpayer paid over half the cost. 33

34 Head of Household qualifying person A qualifying person is defined as: A qualifying child A married child who can be claimed as a dependent A dependent parent A qualifying relative who lived with the taxpayer more than half the year and is one of the relatives listed in the Volunteer Resource Guide (Tab C), Interview Tips, or Table 2: Dependency Exemption for Qualifying Relative, Step 2 (Page C-6) The qualifying person for Head of Household filing status must always be related to the taxpayer. A person may qualify as a qualifying relative for a dependency exemption, but not qualify the taxpayer for the Head of Household filing status. Refer to the Volunteer Resource Guide (Tab B, Page B-3), Who is a Qualifying Person Qualifying You to File as Head of Household? 34

35 Hypos Correct Filing Status Michael provided all the cost of keeping up his home for the year. Michael's son Justin lived with him the entire year. Justin is not disabled, 22 & was not a full-time student in Although Justin only worked part-time, he made too much money for Michael to be able to claim a dependency exemption for him. Can Michael file Head of Household? NO Nancy is single & lives alone. Nancy's mother, Maxine, lives alone in another city. Maxine receives social security payments, but has no other income. Nancy pays all of the costs of keeping up the home her mother lives in, & provides over half her support. Nancy can claim a dependency exemption for her mother. Can Nancy file Head of Household? YES 35

36 Married & Living Apart with Dependent Child Some married TPs may be considered unmarried only for filing Head of Household if they: 1. File a return separate from their spouse 2. Paid >50% cost of keeping up their home 3. Lived apart from their spouse during the entire last 6 months of 2016, & 4. Provided the main home for more than 1/2 the year of a qualifying dependent child, stepchild, or authorized foster child Lesson 4 Filing Status 36

37 Single or Head of Household? A TP may qualify for Head of Household status if the spouse is a nonresident alien Interactive Tax Assistant: What is My Filing Status? Lesson 4 Filing Status 37

Dependency qualifications apply to child Lesson 4 Filing")

38 Qualifying Widow(er) with Dependent Child As beneficial as Married Filing Jointly Available for only 2 years following year of spouse s death TP would use Married Filing Jointly or Married Filing Separately in the year of spouse s death (if not remarried) Dependency qualifications apply to child Lesson 4 Filing Status 38

39 Summary There are 5 filing statuses: Single, Married Filing Jointly, Married Filing Separately, Head of Household, & Qualifying Widow(er) with Dependent Child Choose the filing status that results in the lowest tax HEAVILY TESTED ON CERTIFICATION EXAMS Lesson 4 Filing Status 39

40 Personal Exemptions 40

41 Personal Exemptions What are exemptions? A dollar amount that can be deducted from a TP s total income, thereby reducing their taxable income. Personal exemptions Claimed for self (& possibly spouse) Dependency exemptions Claimed for qualifying dependents Lesson 5 Personal Exemptions 41

Answer must be no to claim personal exemption Resources: Pub 4012 (Tab C, Page C-2), Personal Exemption Interview Tips Interactive Tax Assistant: Personal &")

42 Rules for Personal Exemption Can anyone claim you or your spouse as a dependent on their tax return? (Not does anyone!) Answer must be no to claim personal exemption Resources: Pub 4012 (Tab C, Page C-2), Personal Exemption Interview Tips Interactive Tax Assistant: Personal & Spousal Exemptions Lesson 5 Personal Exemptions 42

43 Spouses (continued) Divorced, Separated, Same-Sex & Common Law TPs cannot claim an exemption for a (former) spouse from whom they are divorced or legally separated No difference same- or opposite- sex marriages. Deceased spouse claimed as personal exemption if TP: Did not remarry by December 31, 2016, & Was not divorced or legally separated from their spouse on the date of death, & Would have been able to claim the exemption under the rules for a joint or separate return Pub 17, Chapter 3, Personal Exemptions & Dependents Lesson 5 Personal Exemptions 43

44 Dependency Exemptions 44

45 Dependency Exemption A TP can claim one exemption for each qualified dependent, thereby reducing their taxable income Who may be claimed as a dependent? 1. Qualifying child 2. Qualifying relative Lesson 6 Dependency Exemptions 45

46 Dependents 3 tests apply to both qualifying child & qualifying relative: 1. Dependent TP person who COULD BE a dependent on someone else s tax return cannot claim a dependent exemption 2. Joint return person filing a joint return cannot be claimed as a dependent, & 3. Citizen or resident dependent must be a U.S. citizen, U.S. resident alien, U.S. national, or a resident of Canada or Mexico Lesson 6 Dependency Exemptions 46

, Interview Tips for Dependency Exemption Lesson 6")

47 Qualifying Child Tests Five additional tests for a qualifying child: 1. Relationship 2. Age 3. Residency 4. Support 5. Qualifying child of more than one person Review Pub 4012 (Tab C, Page C-5), Interview Tips for Dependency Exemption Lesson 6 Dependency Exemptions 47

48 Qualifying Child - Relationship Test To meet this test, the child must be: Taxpayer's son, daughter, stepchild, foster child (placed by an authorized placement agency), or a descendant (for example, a grandchild) of any of them, or Adopted child is treated the same as a natural child. This includes a child who was lawfully placed with the taxpayer for legal adoption. Taxpayer's brother, sister, half-brother, half-sister, stepbrother, stepsister, or a descendant (for example, niece or nephew) of any of them 48

49 Qualifying Child - Age Test To meet this test, the child must be: Under age 19 as of 12/31/2016 & younger than the taxpayer (or the taxpayer's spouse, if filing jointly), or A full-time student under the age of 24 as of 12/31/16 & younger than the taxpayer (or spouse, if filing jointly), or Any age if permanently & totally disabled at any time of the year 49

50 Qualifying Child Residency Test Child must have lived with TP more than 1/2 of Taxpayer's home is any location where they regularly live; need not be a traditional home. For example, child who lived with TP for more than ½ the year in one or more homeless shelters meets residency test. Exceptions to the Residency Test Child considered to live with TP during periods when either child or TP is temporarily absent due to illness, education, business, vacation or military service. Child who was born (or died) during 2016 is treated as having lived with TP all year, if child lived in TP's home the entire time child was alive. Do not confuse this test with citizenship or resident test. 50

51 Qualifying Child- Support Test Child cannot have provided more than 1/2 of child s own support during This test different from support test for qualifying relative. A person's own funds not support unless funds actually spent for support. If taxpayer is unsure whether child provided more than 1/2 of child s own support, review Worksheet for Determining Support in Volunteer Resource Guide (Tab C, Page C-9) together. 51

52 Qualifying Child Of More Than 1 Person Test Although a child could meet conditions to be the qualifying child of more than 1 person, only 1 TP can claim that child as a qualifying child for the following tax benefits: 1. Dependency exemption 2. Child tax credits 3. Head of Household filing status 4. Credit for child & dependent care expenses 5. Exclusion from income for dependent care benefits 6. Earned income credit 52

53 Qualifying Child Of More Than 1 Person Test If 2 TPs have the same qualifying child, only 1 TP can claim all 6 benefits for that particular child. They cannot agree to split these benefits. (Exception: if special rule applies for child of unmarried, divorced, separated or living apart parents). 53

, Children of Divorced or Separated Parents or Parents Who Live Apart Custodial parents can revoke a release of claim to exemption they previously provided to")

54 Children of Divorced or Separated Parents Special rules apply What is the difference between custodial & noncustodial parent? See table 3 in Pub 4012 (Tab C), Children of Divorced or Separated Parents or Parents Who Live Apart Custodial parents can revoke a release of claim to exemption they previously provided to the noncustodial parent on Form 8332 Lesson 6 Dependency Exemptions 54

, Interview Tips for Qualifying Relative Pub 4012 (Tab C, Page C-9), Worksheet for Determining Support Lesson 6")

55 Qualifying Relative Tests Four tests for a qualifying relative: 1. Not a qualifying child 2. Member of household or relationship 3. Gross income 4. Support Review Pub 4012 (Tab C, Page C-6), Interview Tips for Qualifying Relative Pub 4012 (Tab C, Page C-9), Worksheet for Determining Support Lesson 6 Dependency Exemptions 55

56 Qualifying Relative Not Qualifying Child Rule A child is not considered the TP's qualifying relative if the child is the TP's qualifying child, or is the qualifying child of another TP. Exception: When the child's parent (or other person for whom the child is a qualifying child) is not required to file a U.S. income tax return & either: Does not file a return, or Only files to get a refund of income tax withheld or estimated tax paid 56

57 Member of Household or Relationship Test The person must either: Live as a member of the TP's household all year, or Be related to the TP in one of the following ways: Child, stepchild, foster child or a descendant of any of them Brother, sister, stepbrother or stepsister Father, mother, grandparent or other direct ancestor, but not foster parent Stepfather or stepmother Son or daughter of the TP's brother or sister (niece or nephew) Brother or sister of the TP's father or mother (uncle or aunt) Son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law Any of these relationships that were established by marriage are not ended by death or divorce. 57

58 Member of Household or Relationship Test An unrelated person who lived with the TP for the entire year can also meet the member of household or relationship test, BUT: A person is still considered to live with the TP as a member of the household during periods when that person, or the TP, is temporarily absent due to special circumstances such as illness, education, business, vacation, military service, or placement in a nursing home. Cousins can meet the relationship test for qualifying relative only if they live with the TP for the entire year. 58

59 Qualifying Relative Gross Income Test Dependent's gross income for 2016 must be less than the personal exemption amount ($4,050 for 2016). GI is all income in the form of money, property, & services that is not exempt from tax. Specific examples are found in Publication 17, Personal Exemptions & Dependents. Test applies only to qualifying relatives, not qualifying children. State benefit payments such as welfare, Temporary Assistance for Needy Families (TANF), food stamps, Medicaid, or housing assistance considered support provided by the state, not TP. Social security benefits received by a child & used for support are considered provided by the child. 59

60 Qualifying Relative Support Test TP must have provided more than 50% of the person's total support for Note that this support test is different from the support test for a qualifying child. When calculating the amount of total support, TPs should compare their contributions with the entire amount of support the person received from all sources (such as taxable income, tax-exempt income, & loans). 60

61 All those Kids Cheatsheet 61

")

62 Earned Income Credit (EIC) 62

63 What is the EIC? A refundable tax credit available to eligible TPs who do not earn high incomes Qualifying TPs can receive a refund even if they have no filing requirement, owe no tax, & had no income tax withheld 2016: Maximum EIC for families with three or more children is $6,269 HEAVILY TESTED ON CERTIFICATION EXAMS HEAVILY SOUGHT BY CLIENTS AND SOME TRY TO GAME SYSTEM WITH SELF EMPLOYMENT INCOME. Lesson 29 Earned Income Credit (EIC) 63

, Summary of EIC Eligibility Requirements; focus on Part A & Part D Avoid common EIC filing errors: Incorrectly")

64 Qualifying for the EIC Three sets of rules: 1. General eligibility rules for everyone 2. Rules for TPs with one or more qualifying children 3. Rules for TPs who do not have a qualifying child Review Pub 4012 (Tab I, Page I-2), Summary of EIC Eligibility Requirements; focus on Part A & Part D Avoid common EIC filing errors: Incorrectly reported income Incorrectly reported SSNs Married TPs incorrectly filing as Single or Head of Household Claiming a non-qualifying child Lesson 29 Earned Income Credit (EIC) 64

65 Qualifying for the EIC What are some example of earned income that may qualify TPs for the EIC? Wages, salaries, tips, & other taxable employee pay Taxable long-term disability benefits received prior to minimum retirement age Nontaxable combat pay; compare the EIC amount with & without this pay before electing to include it in earned income See Pub 4012 (Tab I, Page I-1) Earned Income Table for a complete list Watch out for self employed with no expenses, round numbers!! Lesson 29 Earned Income Credit (EIC) 65

: Summary of EIC Eligibility Requirements, Part B EIC General Eligibility Rules Interview Tips EIC with a Qualifying Child Interview Tips Qualifying Child of More than One")

66 Rules for Taxpayers with Qualifying Children Claiming a child who is not a qualifying child is one of the most common EIC errors; make sure you apply the rules correctly. Review Pub 4012 (Tab I): Summary of EIC Eligibility Requirements, Part B EIC General Eligibility Rules Interview Tips EIC with a Qualifying Child Interview Tips Qualifying Child of More than One Person Lesson 29 Earned Income Credit (EIC) 66

67 Rules for Taxpayers Without Qualifying Children Rules are presented in Pub 4012 (Tab I) Part C, & in the Interview Tips Must be at least age 25 but under age 65 as of December 31 Cannot be the dependent of another person Check Part I, question 10 on Form C Must have lived in the U. S. more than half the year Lesson 29 Earned Income Credit (EIC) 67

have EIC disallowed in a prior year?")

68 Calculating the Tax Credit Check Part V, question 4 on Form C: Did you (or your spouse) have EIC disallowed in a prior year? If yes, see the special rules in Pub 4012 (Tab I, Page I-2), Disallowance of the Earned Income Credit TaxWise will calculate the amount of EIC Lesson 29 Earned Income Credit (EIC) 68

69 EIC Summary The earned income credit (EIC) computation is based on filing status, number of qualifying children, earned income, & adjusted gross income. Certain individuals with no children may also qualify. By using the intake & interview sheet, the interview tips in the Volunteer Resource Guide, & correctly filling out the EIC worksheets, most common errors can be avoided. Lesson 29 Earned Income Credit (EIC) 69

70 Unique Filing Status & Exemption Situations 70

71 Determining Alien Status Nonresident aliens taxed differently from resident aliens See Pub 4012 (Tab L), ITIN returns Determining Residency Status decision tree Green card test An individual with a green card is, for tax purposes, a resident alien But not the only test! Lesson 7 Unique Filing Status & Exemption Situations 71

72 Determining Alien Status Substantial presence test physically present in the U.S. at least: 31 days during the current year, & 183 days during the 3-year period that includes the current year & the two years immediately before, counting: All days in current year (2016) 1/3 of days in previous year 1/6 of days in second year before current year An individual who meets these requirement is, for tax purposes, a resident alien Lesson 7 Unique Filing Status & Exemption Situations 72

73 Exemption for Nonresident Alien Spouse What are two ways a citizen or resident alien who is married to a nonresident alien can claim the personal exemption for their spouse? 1. Treat the spouse as resident alien on a joint return, or 2. Treat the spouse as a nonresident alien on a Head of Household or Married Filing Separately return. TPs must declare in writing that they are choosing to treat a spouse as a resident alien on a joint return. Lesson 7 Unique Filing Status & Exemption Situations 73

74 Dependency Exemptions Resident Aliens The dependency tests for a qualifying relative or qualifying child apply in the same way to citizens or resident aliens There may be unique issues with the support test & the citizen/resident test. Refer to: Pub 4012 (Tab C) Interview Tips - Personal Exemptions Pub 17, Chapter 3, Citizen or Resident Test Interactive Tax Assistant: Who Can I Claim as a Dependent? & How Much Can I Deduct for Each Exemption I Claim? Special rules for children born overseas & adopted children Lesson 7 Unique Filing Status & Exemption Situations 74

75 Out of Scope: Taxpayers with F, J, M, or Q visas, unless there is a volunteer at your site with Foreign Student certification Unmarried nonresident aliens who do not meet the green card or substantial presence test Can refer these TPs to FSA Lesson 4 Filing Status 75

76 Income from Form 1040, Lines

Gifts & inheritances Exempt income Earned Received for work, such as wages, business income Unearned Interest income from investments Review Pub")

77 Determining Taxable & Nontaxable Income What are the differences between taxable & nontaxable income? Nontaxable (excludable) Gifts & inheritances Exempt income Earned Received for work, such as wages, business income Unearned Interest income from investments Review Pub 4012 (Tab D) for examples Lesson 8 Income from Form 1040 Lines

78 Determining Taxable & Nontaxable Income Remember: Volunteers probe taxpayers to determine all sources of income whether or not reported on a W-2 or other form! Lesson 8 Income from Form 1040 Lines

79 Reporting Wages, Salaries, Tips, etc. Form W-2: Issued to employees by January 31, reports wages & other compensation Pub 4012 (Tab D, Page D-7-8) How/Where to Enter Income Pub 4012 (Tab D, Page D-9-10) Form W-2 Instructions D-3 shows how to enter income from certain forms in Tax slayer Lesson 8 Income from Form 1040 Lines

80 Reporting Wages, Salaries, Tips, etc. Remember: Household employees earning less than $1,700 may not receive a Form W-2, but the income must be reported Self-employed TPs who receive tips should include their tips in gross receipts on Schedule C Lesson 8 Income from Form 1040 Lines

Educational Benefits Lesson 8")

81 Taxable Scholarship Income Taxable scholarship income may be reported on Form W-2 & Form 1098-T Note, not all scholarships are income, but the excess over eligible expenses is. If the TP did not receive a Form W-2, the taxable amount should still be reported Form 1098-T income is reported as shown on pg D-45 Pub 4012 Review Pub 4012 (Tab J) Educational Benefits Lesson 8 Income from Form 1040 Lines

82 Interest Income Interest income (unearned income) is reported on Form 1099-INT if large enough ask if other interest was received. Common sources: savings accounts, CDs, saving certificates, government bonds, interest on insurance proceeds, loan interest See 4012 Tab D, Page D-12 for how to enter in Taxslayer Lesson 8 Income from Form 1040 Lines

83 State & Local Tax Refunds On Form 1099-G, refund will be in box 2 Report only if: TP itemized deductions last year, & Received an income tax benefit. Do not report if state sales tax was deducted in 2015 Taxable refund is reported on Form 1040, line 10 See Pub 4012, p D-11 for how to enter in Taxslayer Lesson 8 Income from Form 1040 Lines

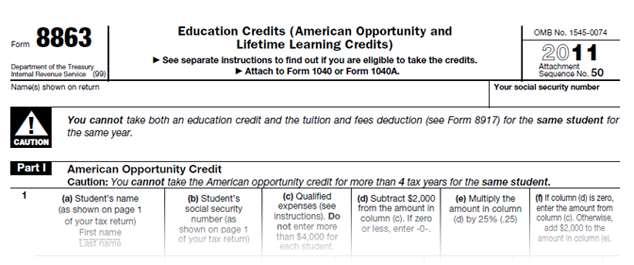

84 Alimony Do not confuse with Child Support! Getting information about alimony Form C Pub 4012 (Tab E, pg E-5) Lesson 8 Income from Form 1040 Lines

85 Out of Scope for this Lesson: TPs with income from the following sources reported on Form 1040: Other gains/losses (line 14) Farm income (line 18) Dependent child under the age of 18 (age 24 if a full-time student), who has investment income of more than $2000 Casualty losses Accrual method for reporting income TPs who buy or sell bonds between interest payment dates Form 1099-INT, box 9 Adjustments needed for any of the amounts listed on Form 1099-OID, or if the TP should have received Form 1099-OID but did not receive one Form 1099-DIV, boxes 2b, 2c, 2d, 8, 9 State or local income tax refunds received in 2016 for a tax year other than 2015 Alimony/divorce agreements executed before 1985 Minister tax returns with parsonage/housing allowance Lesson 8 Income from Form 1040 Lines

86 Business Income See Tab D, pg D for Instructions on entering business income and deductions. 86

87 Income Social Security Benefits; Form 1040 Line 20a 87

88 Social Security & Railroad Retirement Benefits Social security benefits: Old-age, survivor, & disability insurance (OASDI) Workers compensation Monthly retirement Reported on Form SSA-1099 See Pub 4012, pg D27-28 for how to enter in Taxslayer Intake & Interview Sheet Lesson 14 Income Social Security Benefits; Form 1040 Line 20a 88

89 Finding the Taxable Portion of Social Security The taxable amount, if any, depends upon: Filing status & other reportable income Whether the benefits were the TP s only source of income If the benefits were the only source of income, the benefits are generally not taxable, & the TP need not file a federal income tax return. If the TP received other income, Taxslayer will calculate the taxable portion. Lesson 14 Income Social Security Benefits; Form 1040 Line 20a 89

90 Standard Deduction & Itemizing Deductions 90

, Standard Deduction for Most People Pub 4012 (Tab F), Interview Tips for persons not eligible for the Standard Deduction Lesson 19 Standard Deduction & Tax")

91 Deductions Use interview techniques & other tools to determine if the standard deduction or itemizing will result in the largest possible deduction for the TP. Pub 4012 (Tab F), Standard Deduction for Most People Pub 4012 (Tab F), Interview Tips for persons not eligible for the Standard Deduction Lesson 19 Standard Deduction & Tax Computation 91

92 Age & Blindness Standard deduction is higher for a TP or spouse 65 or older, or if one or both spouses are blind Use Pub 4012 (Tab F), Standard Deduction Chart for People Born Before January 2, 1952 or Who Are Blind Chart, as a guide to computing the standard deduction Taxslayer will compute if you enter the information properly. Lesson 19 Standard Deduction & Tax Computation 92

93 Taxpayers Who Can be Claimed as Dependents A lower standard deduction is offered for an individual who can be claimed as a dependent on another s tax return Form C has a check box for a dependent being claimed by another TP. But the taxpayer may not know! Use Tab C of Form 4012 to help explain. Lesson 19 Standard Deduction & Tax Computation 93

94 Standard Deduction vs. Itemizing Examples of types of expenses that generally warrant itemizing deductions: Large out-of-pocket medical & dental expenses State & local income taxes, real estate taxes, and/or personal property taxes Mortgage interest Gifts to charity Casualty, theft, & certain other miscellaneous deductions Lesson 19 Standard Deduction & Tax Computation 94

95 Deductions Who Must Itemize TPs who cannot take standard deduction & must itemize: 1. Filing as Married Filing Separately & the spouse itemizes 2. Nonresident or dual-status alien (not married to U.S. citizen at the end of the year) Refer to the Standard Deduction Worksheet Line 40 from either Pub 17 or Form 1040 Instructions Lesson 19 Standard Deduction & Tax Computation 95

96 Who Should Itemize? TPs should itemize if total allowable deductions are higher than the standard deduction amount TPs ineligible for standard deduction should itemize deductions Refer to Pub 4012 (Tab F) Persons Not Eligible for the Standard Deduction Interview Tips for help in determining if a TP qualifies for a standard deduction Refer to Pub 4012 (Tab F) Interview Tips Itemized Deductions to help determine if a TP should try to itemize TaxSlayer will automatically select the larger of itemized versus standard deduction Lesson 20 Itemized Deductions 96

97 Taxes that May be Deductible Certain taxes may be deductible if paid by the TP during 2016, such as: State & local taxes Real estate taxes Personal property taxes Michigan Auto Registrations Other taxes (foreign income taxes, etc.) Refer to Pub 17, Which Taxes Can You Deduct table for more information Lesson 20 Itemized Deductions 97

98 Interest Paid Certain types of interest are deductible, such as: Mortgage interest Points paid as a form of interest Investment interest (out of scope) Refer to the flowcharts in Pub 17, Is My Home Mortgage Interest Fully Deductible? & Are My Points Fully Deductible? for more information Private Mortgage Insurance (PMI) may be deductible Student Loan interest does NOT go On schedule A, it is reported on 1040, under Adjustments Lesson 20 Itemized Deductions 98

99 Gifts to Charity TPs may deduct charitable contributions (donations or gifts) to qualified organizations ONLY IF THEY ITEMIZE. Exempt Organizations Select Check is an online tool for searching for organizations that are eligible to receive tax-deductible charitable contributions TPs are required to keep receipts & records of all their contributions Refer to Pub 17, Contributions, & Pub 4012 (Tab F, Page F-5 && 8), Schedule A Itemized Deductions, for more information Lesson 20 Itemized Deductions 99

100 Education Benefits 100

101 Education Benefits Introduction Education credit amounts are based on qualified education expenses paid during 2016 For an overview of education credits, see Pub 4012 (Tab J), Education Benefits To help guide your interview, use Pub 4012 (Tab J), Education Credits Disqualifying conditions include if a TP: Can be claimed as dependent on someone else s return Files as Married Filing Separately Has an AGI above the limit for the TP s filing status Was a nonresident alien for any part of 2016, & did not elect to be treated as a resident alien for tax purposes Lesson 23 Education Credits 101

102 Dependents / Eligible Institutions To claim the credit for a student s qualified expenses, the TP must claim the student as a dependent Expenses must have been paid to an eligible educational institution A searchable database of all accredited schools is available at Lesson 23 Education Credits 102

103 Qualifying Expenses Qualified education expenses are tuition & certain related expenses required for attendance at an eligible educational institution The definition for certain related expenses differs between the lifetime learning credit & the American opportunity credit Necessary proof of expenses includes such documents as receipts or Form 1098-T, Tuition Statement, issued by the school Qualified expenses must be reduced by the amount of any tax-free educational assistance TPs receive TPs can claim payments that were prepaid for the academic period that begins in the first three months of the next year Lesson 23 Education Credits 103

104 American Opportunity Tax Credit Available for the first 4 years of college per eligible student The credit covers 100% of the first $2,000 & 25% of the second $2,000 of eligible expenses, up to the amount of tax or a maximum of $2,500 40% of the credit is a refundable credit See Form 8863 Instructions for more information Lesson 23 Education Credits 104

105 Lifetime Learning Credit The credit is 20% of the first $10,000 of eligible expenses, up to the amount of tax or a maximum of $2,000 The credit is non-refundable Eligible students are not required to be enrolled at least half-time or in a degree program, & a felony drug conviction is not a disqualification Refer to Pub 4012 (Tab J), Education Benefits for basic requirements Lesson 23 Education Credits 105

106 Choosing Between the Credits / No Double Benefits TPs cannot receive multiple benefits for the same student s expenses TPs have several options for claiming education expenses: 1. American opportunity credit or lifetime learning credit 2. Tuition & fees deduction 3. Itemizing on Schedule A 4. Reporting as business expenses on Schedules C or C-EZ Lesson 23 Education Credits 106

107 Child Tax Credits 107

108 1. Child and Dependent Care Credit Allows TPs to reduce their tax by a portion of their child and dependent care expenses. Credit may be claimed by TPs who, work or look for work and pay someone to take care of their qualifying person. A qualifying person is a: Qualifying child under 13 Spouse who is incapable of self-care Dependent who is incapable of self-care The credit ranges from 20% to 35% of the taxpayer's expenses. The percentage is based on the taxpayer's earned income and adjusted gross income. The amount of the credit cannot be more than the amount of income tax on the return. It can reduce an individual's tax to $0, but it will not give the taxpayer a refund. 108

109 1. Child and Dependent Care Credit Spouse is considered working if going to school full time. Can claim amounts paid to family members, but not dependent s parents or TP s dependents. Must have taxpayer ID number for care provider. No exceptions! See Pub 4012 (Tab G, Pages G3-5) 109

110 2&3 Child Tax Credit/Additional Child Tax Credit Child tax credit allows TPs to claim a nonrefundable tax credit of up to $1,000 per child TPs who claim the child tax credit, but do not qualify for the full amount, may be able to also take the refundable additional child tax credit by completing Form 8812, Additional Child Tax Credit Review Pub 4012 (Tab G, Pages G8-9), Child Tax Credit Lesson 25 Child Tax Credit 110

111 Calculating the Credits Taxslayer will automatically calculate the credits, provided you have correctly completed the: Dependent section of the Main Information Screen Form 1040 through the retirement savings contribution credit line Part I of Form 5695, & Schedule R Lesson 25 Child Tax Credit 111

112 Payments 112

, Form 1040, Page 2 Other Taxes & Payments See Pub 505, Tax Withholding & Estimated Tax, for more information Lesson 28 Payments")

113 Federal Income Tax Withheld The total federal income tax withheld is entered in the Payments section of Form 1040, line 62 Use interview techniques & Form C to determine the payments & credits to report Review Pub 4012 (Tab H), Form 1040, Page 2 Other Taxes & Payments See Pub 505, Tax Withholding & Estimated Tax, for more information Lesson 28 Payments 113

114 Estimated Tax Payments Estimated tax includes income tax & self-employment tax If estimated payments are not paid when required, or amounts are insufficient, a penalty could be imposed From Form C & interview, determine if TPs paid estimated tax; if yes, ask to see the TP s Form 1040-ES For more information about estimated taxes, refer to Form 1040-ES Lesson 28 Payments 114

115 Amounts Applied from Previous Year TPs who overpay income taxes for 1 tax year can apply all or part of their refund to next year s tax From Form C & interview, determine if TPs overpaid income tax last year & if they applied any part of it to this tax year; if yes, ask to see the 2015 return to verify the amount Add the amount to the estimated tax payments Lesson 28 Payments 115

,")

116 Payments & Extensions Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return, extends the time to file until Oct. 15 An extension must be filed electronically or on paper by the due date of the return If taxes due are not paid by April 18, TPs may owe interest & penalties Review Pub 4012 (Tab M, Page M-5), Filing for an Extension Using TaxSlayer Lesson 28 Payments 116

117 Refund & Amount of Tax Owed 117

118 Refund or Tax Due Form 8888, Allocation of Refund, is used to deposit a refund into up to three bank accounts For more information, review Pub 4012 (Tab K): Page K-15, Split Refund Option Page K-14, Pointers for Direct Deposit of Refunds Page K-16-17, Balance Due Returns Double-check accuracy of routing & account numbers for direct deposit refunds Refund status can be checked at Where s My Refund feature on or calling Lesson 30 Refund & Amount of Tax Owed 118

119 U.S. Savings Bonds TPs may purchase U.S. savings bonds with their tax refunds for themselves or for co-owners, such as children or grandchildren Form 8888 is used to buy savings bonds Series I bonds are sold at face value & accrue interest until redeemed or until they reach their final maturity in 30 years Series I bonds pay interest based on a combination of a fixed rate & a semiannual inflation rate Lesson 30 Refund & Amount of Tax Owed 119

120 Amount Owed Payment options for taxes owed are: Check or money order submitted with Form 1040-V, Payment Voucher Electronic funds withdrawal Credit card Electronic Federal Tax Payment System (EFTPS) Cash if paid in person (new) Lesson 30 Refund & Amount of Tax Owed 120

121 Amount Owed Review Pub 4012 (Tab K), Balance Due Returns whenever you prepare a return that has an amount owed TPs who cannot pay the full amount owed may request one of the following agreements: 1. Pay in full within 60 or 120 days with no fee 2. Monthly installment payments using Form 9465, Installment Agreement Request, with a fee Balance due payments must be made by the April 18 th filing due date to avoid penalties & interest NOT DATE OF EFILING. Lesson 30 Refund & Amount of Tax Owed 121

122 Estimated Tax Penalty Estimated tax penalty may apply for underpayment of estimated taxes Most TPs must make estimated tax payments if they expect to owe at least $1,000 in tax (after subtracting withholding & credits) Leave line 77 blank; if a penalty is due, the IRS will figure the amount & send the TP a notice Recommend client change withholding amounts on Forms W-4 & W-4P Lesson 30 Refund & Amount of Tax Owed 122

123 Third Party Designees TPs may choose to authorize another person to discuss their tax return with the IRS Volunteer tax preparers must never be designated as the 3rd party designee Lesson 30 Refund & Amount of Tax Owed 123

124 Identity Protection The IRS Identity Protection PIN (IP PIN) is a unique 6 digit number that is assigned annually to victims of identity theft for use when filing their federal tax return to show that taxpayer is the rightful filer of the return. For the 2016 filing season, IRS expects to provide more than 1.2 million IP PINs. The IP PIN will allow these individuals to avoid delays in filing returns and receiving refunds. When assisting taxpayers who are victims or may be victims of identity theft at VITA/TCE site, you should: If an IP PIN was issued to primary taxpayer you should ensure the IP PIN is input correctly on the tax return. If the Taxpayer received an IP PIN but did not bring it with them. 1. Complete tax return for the taxpayer. 2. Provide taxpayer with a complete copy of the tax return (Provide two copies if the taxpayer will mail the tax return.) 124

125 Identity Protection When assisting taxpayers who are victims or may be victims of identity theft at VITA/TCE site, Tab P, page P-4. Also, contact site coordinator for help with State identity theft. 125

126 Completing the Return 126

127 Signing Form 1040 Quality review must be done before TP signs the return/chooses PIN. Advise TPs they are ultimately responsible for information on their return. Signing their return guarantees TPs have examined the return & schedules for accuracy. The return is not considered valid, & refunds are not issued, unless it is signed. (TaxSlayer uses e-signature.) Note Identity Protection PIN at bottom of Form Lesson 31 Quality Review of the Tax Return 127

128 Printing & Storing Returns TPs must receive copy of their tax return. To prepare packet: Print appropriate client letter (efile or paper file) and check appropriate boxes Print the entire return using TaxSlayer Ensure names & social security numbers are legible on every sheet Assemble the packet starting with client letter, 1040V, if any, Form 1040, followed by each form, schedule, & attachment in order, based on the sequence number; then state return(s) with similar sequence. Show TP printed copy of return, & verify key information is correct Print a second copy Advise TPs to keep tax-related documents for at least 3 years Show TP text on letter describing how to track refunds. Review Pub 4012: Tab K, Page K-25, Distributing Copies of the Return Lesson 32 Concluding the Interview 128

129 Completing the Return 1. Run diagnostics on the return, address any issues you can; explain review process to client 2. Change status on TS to Ready for review and mark whiteboard 3. After review assemble the return & all necessary documentation; Go over letter with client and ask if questions; send client to exit table. 4. Change return status to Completed. Note in taxpayer diary any special issues or why not completed. If not complete, use Needs more info status. Lesson 31 Quality Review of the Tax Return 129

130 THE END THANK YOU FOR YOUR ATTENTION!

Nonrefundable Credits

Nonrefundable Credits TaxSlayer Navigation: Federal Section>Deductions>Credits Menu Select for Form 1116, Foreign Tax Credit Select for Form 2441 Child Tax Credit. See Child Tax Credit Tip & Interview

Nonrefundable Credits TaxSlayer Navigation: Federal Section>Deductions>Credits Menu Select for Form 1116, Foreign Tax Credit Select for Form 2441 Child Tax Credit. See Child Tax Credit Tip & Interview

This applies even if another person does not actually claim the taxpayer as a dependent. A taxpayer who

Personal Exemptions Introduction Identifying and entering the correct number of exemptions is a critical component of completing taxpayers returns, because each allowable exemption reduces their taxable

Personal Exemptions Introduction Identifying and entering the correct number of exemptions is a critical component of completing taxpayers returns, because each allowable exemption reduces their taxable

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010 The federal Earned Income Tax Credit is designed to boost the wages of working families. The following questions and answers will

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010 The federal Earned Income Tax Credit is designed to boost the wages of working families. The following questions and answers will

TY2017 VITA Basic Certification Test - Study Guide

Scenario 1: Albright TY2017 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Scenario 1: Albright TY2017 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Nonrefundable Credits

nrefundable Credits Link to Form 1116, Foreign Tax Credit page 1, if required. Link to Form 2441, page 1. Link to Form 8863. See Education Benefits tab. Link to Form 8880. See Child Tax Credit Tip and

nrefundable Credits Link to Form 1116, Foreign Tax Credit page 1, if required. Link to Form 2441, page 1. Link to Form 8863. See Education Benefits tab. Link to Form 8880. See Child Tax Credit Tip and

2017 Basic Certification Study and Reference Guide

2017 Basic Certification Study and Reference Guide 1 P age Basic Scenario 1: Calvin and Betty Albright 1. Qualifying health insurance coverage also known as minimum essential coverage or MEC under the

2017 Basic Certification Study and Reference Guide 1 P age Basic Scenario 1: Calvin and Betty Albright 1. Qualifying health insurance coverage also known as minimum essential coverage or MEC under the

TY2018 VITA Basic Certification Test - Study Guide

Scenario 1: Arnold TY2018 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Scenario 1: Arnold TY2018 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Earned Income Credit i

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Federal Income Taxes. Today s Approach. Your Tax Knowledge. Process. Process Continued. Filing Requirements. Fall 2014 VITA Training

Federal Income Taxes Fall 2014 VITA Training Dr. Cathy Bowen Dr. Barbara Yener Today s Approach Use Form 1040 and common tax forms to discuss key areas of completing a tax return for VITA taxpayers. Not

Federal Income Taxes Fall 2014 VITA Training Dr. Cathy Bowen Dr. Barbara Yener Today s Approach Use Form 1040 and common tax forms to discuss key areas of completing a tax return for VITA taxpayers. Not

Earned Income Table. Earned Income for EIC, Additional Child Tax Credit and Dependent Care Credit. Common EIC Filing Errors

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from selfemployment Gross

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from selfemployment Gross

C Consumer Information on the Earned Income Tax Credit

APPENDIX C Consumer Information on the Earned Income Tax Credit The Earned Income Credit: A Powerful Benefit for People Who Work What is the Earned Income Credit (EIC)? The EIC is a tax benefit for working

APPENDIX C Consumer Information on the Earned Income Tax Credit The Earned Income Credit: A Powerful Benefit for People Who Work What is the Earned Income Credit (EIC)? The EIC is a tax benefit for working

Earned Income Credit (EIC)

") Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2013 Returns Contents What's New for 2013... 3 Reminders... 3 Chapter

Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2013 Returns Contents What's New for 2013... 3 Reminders... 3 Chapter

QUESTIONS AND ANSWERS ABOUT THE CHILD AND DEPENDENT CARE TAX CREDIT TAX YEAR 2011

QUESTIONS AND ANSWERS ABOUT THE CHILD AND DEPENDENT CARE TAX CREDIT TAX YEAR 2011 The federal Child and Dependent Care Tax Credit can help working families pay for the child care they need to work. The

QUESTIONS AND ANSWERS ABOUT THE CHILD AND DEPENDENT CARE TAX CREDIT TAX YEAR 2011 The federal Child and Dependent Care Tax Credit can help working families pay for the child care they need to work. The

REFUNDABLE TAX CREDITS NOT LIMITED TO TAX LIABILITY

REFUNDABLE TAX CREDITS NOT LIMITED TO TAX LIABILITY FORM 1040 page 2 Non-refundable credits Refundable credits Refundable credits Line 66a Earned income credit (EIC or EITC) Line 67 Additional child tax

REFUNDABLE TAX CREDITS NOT LIMITED TO TAX LIABILITY FORM 1040 page 2 Non-refundable credits Refundable credits Refundable credits Line 66a Earned income credit (EIC or EITC) Line 67 Additional child tax

Arizona Form 2012 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2012 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2012 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

ELIGIBLE. Earned Income Credit (EIC)

") Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2003 Returns?ARE YOU ELIGIBLE Look inside for... Detailed Examples Eligibility

Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2003 Returns?ARE YOU ELIGIBLE Look inside for... Detailed Examples Eligibility

The Earned Income Tax Credit

The Earned Income Tax Credit WHAT IS THE EARNED INCOME TAX CREDIT? The Earned Income Tax Credit (EITC) is a benefit for working people who have low to moderate income. It reduces the amount of taxes you

The Earned Income Tax Credit WHAT IS THE EARNED INCOME TAX CREDIT? The Earned Income Tax Credit (EITC) is a benefit for working people who have low to moderate income. It reduces the amount of taxes you

Earned Income Table. Earned Income

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross

Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

The Health Care Assister s Guide to Tax Rules

The Health Care Assister s Guide to Tax Rules Determining Income & Households for Medicaid and Premium Tax Credits Center on Budget and Policy Priorities Authors January Angeles and Tara Straw Acknowledgements

The Health Care Assister s Guide to Tax Rules Determining Income & Households for Medicaid and Premium Tax Credits Center on Budget and Policy Priorities Authors January Angeles and Tara Straw Acknowledgements

Advanced Volunteer Summary Chart

on Marital Status and Household Information Marital Status and Household Information 1. 1. Filing Status Social Security Cards (or SSA- 1099, ITIN) 2. Dependents List and Total Number of Exemptions Wages,

on Marital Status and Household Information Marital Status and Household Information 1. 1. Filing Status Social Security Cards (or SSA- 1099, ITIN) 2. Dependents List and Total Number of Exemptions Wages,

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

Figuring your Taxes and Credits

Figuring your Taxes and Credits This self-study explains how to figure your tax and how to figure the tax of certain children who have more than $2,100 of unearned income. Also discussed are various tax

Figuring your Taxes and Credits This self-study explains how to figure your tax and how to figure the tax of certain children who have more than $2,100 of unearned income. Also discussed are various tax

IRS Federal Income Tax Publications provided by efile.com

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

Earned Income Table. Earned Income

Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross income of a statutory

Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross income of a statutory

Property Tax Refund (Credit) Claim. You must file this form, or Arizona Form 204, by April 17, 2018.

Claim. You must file this form, or Arizona Form 204, by April 17, 2018.") DO NOT STAPLE ANY ITEMS TO THE CLAIM. Arizona Form 140PTC You must file this form, or Arizona Form 204, by April 17, 2018. 82F Check box 82F if filing under extension 95 Check box 95 if amending claim

DO NOT STAPLE ANY ITEMS TO THE CLAIM. Arizona Form 140PTC You must file this form, or Arizona Form 204, by April 17, 2018. 82F Check box 82F if filing under extension 95 Check box 95 if amending claim

1/19/2017. Agenda. Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law)

Overview of Credits (1 hour Tax Law)") Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law) January 19, 2017 Agenda Overview of the Child Tax Credit Additional Child Tax Credit American Opportunity Credit

Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law) January 19, 2017 Agenda Overview of the Child Tax Credit Additional Child Tax Credit American Opportunity Credit

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

THE TAXATION OF INDIVIDUALS AND FAMILIES

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

Understanding Your Tax Basics

Understanding Your Tax Basics No matter what the season or your unique circumstances, when it comes to your taxes, planning usually pays off in a lower tax bill. The following is provided so that you may

Understanding Your Tax Basics No matter what the season or your unique circumstances, when it comes to your taxes, planning usually pays off in a lower tax bill. The following is provided so that you may

CESAs Coverdell Education Savings Accounts. Questions & Answers

CESAs Coverdell Education Savings Accounts Questions & Answers What is a Coverdell Education Savings Account? A Coverdell Education Savings Account is a type of tax-preferred savings and investment account

CESAs Coverdell Education Savings Accounts Questions & Answers What is a Coverdell Education Savings Account? A Coverdell Education Savings Account is a type of tax-preferred savings and investment account

CHAPTER 2 SOLUTIONS END OF CHAPTER MATERIAL

Solutions Manual Discussion Questions CHAPTER 2 SOLUTIONS END OF CHAPTER MATERIAL 1. What is a for AGI deduction? Give three examples. Learning Objective: 02-01 Topic: Form 1040 and 1040A Difficulty: 1

Solutions Manual Discussion Questions CHAPTER 2 SOLUTIONS END OF CHAPTER MATERIAL 1. What is a for AGI deduction? Give three examples. Learning Objective: 02-01 Topic: Form 1040 and 1040A Difficulty: 1

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

Earned Income Credit

Earned Income Credit Major update Earned Income Credit Pub 4491 Lesson 30 Pub 4012 Tab I needed for 2017 law change (disaster relief) Refundable Credit A refundable credit can generate a refund even if

Earned Income Credit Major update Earned Income Credit Pub 4491 Lesson 30 Pub 4012 Tab I needed for 2017 law change (disaster relief) Refundable Credit A refundable credit can generate a refund even if

All Rights Reserved The Phoenix Tax Group

All Rights Reserved 2017 The Phoenix Tax Group United States Public Laws, Federal Regulations and decisions of administrative and executive agencies and courts of the United States, are in the public domain.

All Rights Reserved 2017 The Phoenix Tax Group United States Public Laws, Federal Regulations and decisions of administrative and executive agencies and courts of the United States, are in the public domain.

Coverdell Education Savings Account (ESA)

") 7. Coverdell Education Savings Account (ESA) Introduction If your modified adjusted gross income (MAGI) is less than $110,000 ($220,000 if filing a joint return), you may be able to establish a Coverdell

7. Coverdell Education Savings Account (ESA) Introduction If your modified adjusted gross income (MAGI) is less than $110,000 ($220,000 if filing a joint return), you may be able to establish a Coverdell

a Taxable interest. Attach Schedule B if required... 8a b Tax-exempt interest. Do not include on line 8a...

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Standard Deductions. MACRS Recovery Periods. Tax Preparers Due Diligence Requirements for EITC Medical Savings Accounts (MSA)

") Tax Preparers Due Diligence Requirements for EITC Paid preparers who file EITC returns or claims for refunds for clients must meet four due diligence requirements. Those who fail to do so can be assessed

Tax Preparers Due Diligence Requirements for EITC Paid preparers who file EITC returns or claims for refunds for clients must meet four due diligence requirements. Those who fail to do so can be assessed

INSTRUCTIONS IRS NOTE: THIS BOOKLET DOES NOT CONTAIN TAX FORMS. makes doing your taxes faster and easier.

1040 NOTE: THIS BOOKLET DOES NOT CONTAIN TAX FORMS INSTRUCTIONS 2013 makes doing your taxes faster and easier. Get a faster refund, reduce errors, and save paper. For more information on IRS e-file and

1040 NOTE: THIS BOOKLET DOES NOT CONTAIN TAX FORMS INSTRUCTIONS 2013 makes doing your taxes faster and easier. Get a faster refund, reduce errors, and save paper. For more information on IRS e-file and

CSS/Financial Aid PROFILE Early Application Instructions.

CSS/Financial Aid PROFILE 2013-14 Early Application Instructions www.collegeboard.org INSTRUCTIONS Read the instructions as you fill out the PROFILE Early Application. Mistakes will delay the processing

CSS/Financial Aid PROFILE 2013-14 Early Application Instructions www.collegeboard.org INSTRUCTIONS Read the instructions as you fill out the PROFILE Early Application. Mistakes will delay the processing

To obtain these cards call or go to

Thank you for making an appointment with the United Way of Washtenaw County VITA tax clinic. Please review this letter to ensure you are prepared for your appointment. What if I need to cancel or change

Thank you for making an appointment with the United Way of Washtenaw County VITA tax clinic. Please review this letter to ensure you are prepared for your appointment. What if I need to cancel or change

Basic Certification Test: Study Guide for Tax Year 2017

Basic Certification Test: Study Guide for Tax Year 2017 TRAINING PRACTICE PROBLEMS 2018 i The items in parentheses refer to sections or page numbers in Publication 4012, Volunteer Resource Guide. It s

Basic Certification Test: Study Guide for Tax Year 2017 TRAINING PRACTICE PROBLEMS 2018 i The items in parentheses refer to sections or page numbers in Publication 4012, Volunteer Resource Guide. It s

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES 2 STARTING A BUSINESS 3 CHILDREN: Exemptions, Credits And Income Shifting Techniques Children invariably mean you will need to incur additional,

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES 2 STARTING A BUSINESS 3 CHILDREN: Exemptions, Credits And Income Shifting Techniques Children invariably mean you will need to incur additional,

Foreign Student and Scholar Volunteer Tax Return Preparation. VITA Training 1

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

GLOSSARY. November 15, 2015 (corrected)

") GLOSSARY ACA Patient Protection and Affordable Care Act ACTC Additional child tax credit AGI Adjusted gross income AMT Alternative minimum tax AOC American Opportunity credit, formerly HOPE education credit

GLOSSARY ACA Patient Protection and Affordable Care Act ACTC Additional child tax credit AGI Adjusted gross income AMT Alternative minimum tax AOC American Opportunity credit, formerly HOPE education credit

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES 2 STARTING A BUSINESS 3 CHILDREN: Exemptions, Credits And Income Shifting Techniques Children invariably mean making additional, often significant,

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES 2 STARTING A BUSINESS 3 CHILDREN: Exemptions, Credits And Income Shifting Techniques Children invariably mean making additional, often significant,

2017 Advanced Certification Study and Reference Guide

2017 Advanced Certification Study and Reference Guide Note: Where used in the following, QRG means Quick Reference Guide ( mini manual ); Manual means the Ladder Up Volunteer Training Manual; in both cases

2017 Advanced Certification Study and Reference Guide Note: Where used in the following, QRG means Quick Reference Guide ( mini manual ); Manual means the Ladder Up Volunteer Training Manual; in both cases

Welcome & Happy New Year Refresher Training 5-8 Jan 2016 Part 2

Welcome & Happy New Year Refresher Training 5-8 Jan 2016 Part 2 1 Review of Tax Laws and TaxWise Use 2 Elements of Fed 1040 & MA Form 1 Tax Returns Taxpayer information (incl health ins.) Dependents Filing

Welcome & Happy New Year Refresher Training 5-8 Jan 2016 Part 2 1 Review of Tax Laws and TaxWise Use 2 Elements of Fed 1040 & MA Form 1 Tax Returns Taxpayer information (incl health ins.) Dependents Filing

VITA/TCE Training. Preparing a Return in Practice Lab

The National Tax Training Committee has modified this manual to more accurately reflect Tax-Aide policies and scope and to clarify instructions that relate to Practice Lab versus the desktop version of

The National Tax Training Committee has modified this manual to more accurately reflect Tax-Aide policies and scope and to clarify instructions that relate to Practice Lab versus the desktop version of

Intake/Interview & Quality Review Training Filing Season

Intake/Interview & Quality Review Training 2018 Filing Season Publication 5101 (Rev. 10-2017) Catalog Number 64024A Department of the Treasury Internal Revenue Service www.irs.gov 1 The Objectives of this

Intake/Interview & Quality Review Training 2018 Filing Season Publication 5101 (Rev. 10-2017) Catalog Number 64024A Department of the Treasury Internal Revenue Service www.irs.gov 1 The Objectives of this

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

216 Medical Savings Accounts (MSA) 216 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,45-6,7 Maximum Out of Pocket Self-Only Coverage 4,45 Family Coverage 8,15 STANDARD DEDUCTIONS

216 Medical Savings Accounts (MSA) 216 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,45-6,7 Maximum Out of Pocket Self-Only Coverage 4,45 Family Coverage 8,15 STANDARD DEDUCTIONS

Page 2 Page 7 Page 10 Page 12 ONLY $449. Save $200 Off Retail!

All seven of the following tests must be met in order for a taxpayer to claim another person as a dependent in 0. Test numbers through vary depending joint return with a spouse. This rule does not apply

All seven of the following tests must be met in order for a taxpayer to claim another person as a dependent in 0. Test numbers through vary depending joint return with a spouse. This rule does not apply

New Preparer Part FILING SEASON FOR TY 2017

New Preparer Part 1 2018 FILING SEASON FOR TY 2017 Welcome and Introductions Thank you for volunteering Mechanics Restrooms, breaks Ask questions at any time Overview of training materials IRS Training

New Preparer Part 1 2018 FILING SEASON FOR TY 2017 Welcome and Introductions Thank you for volunteering Mechanics Restrooms, breaks Ask questions at any time Overview of training materials IRS Training

Taxpayer Questionnaire

First : Last : Taxpayer Questionnaire PERSONAL INFORMATION Primary Taxpayer M.I.: S.S.N. : Birthdate: Taxpayer's PIN: Home Phone: Work Phone: Cell Phone: Occupation: Email Address: Dependent on another

First : Last : Taxpayer Questionnaire PERSONAL INFORMATION Primary Taxpayer M.I.: S.S.N. : Birthdate: Taxpayer's PIN: Home Phone: Work Phone: Cell Phone: Occupation: Email Address: Dependent on another

Important Changes for 2017

Due Date of Return The due date for filing a 2017 return is Tuesday, April 17, 2018. This is because April 15, 2018 is a Sunday and Emancipation Day, a legal holiday in the District of Columbia, is observed

Due Date of Return The due date for filing a 2017 return is Tuesday, April 17, 2018. This is because April 15, 2018 is a Sunday and Emancipation Day, a legal holiday in the District of Columbia, is observed

2018 Publication 4012, VITA/TCE Resource Guide

2018 Publication 4012, VITA/TCE Resource Guide Publication 4012 B-4 In the second text box, in the left margin of the page, change Line 21 to: B-7A Schedule 1 Make a pen/ink change in Publication 4012.

2018 Publication 4012, VITA/TCE Resource Guide Publication 4012 B-4 In the second text box, in the left margin of the page, change Line 21 to: B-7A Schedule 1 Make a pen/ink change in Publication 4012.

Adjustments to Income

Adjustments to Income Pub 4491 Lesson 18 Pub 4012 Tab E Adjusted Gross Income Total Income minus Adjustments = Adjusted Gross Income (AGI) 2 1 Intake/Interview 3 A2 In-Scope Adjustments Educator expenses

Adjustments to Income Pub 4491 Lesson 18 Pub 4012 Tab E Adjusted Gross Income Total Income minus Adjustments = Adjusted Gross Income (AGI) 2 1 Intake/Interview 3 A2 In-Scope Adjustments Educator expenses

Department of the Treasury - Internal Revenue Service Intake/Interview & Quality Review Sheet

Form 13614-C (October 2018) You will need: Tax Information such as Forms W-2, 1099, 1098, 1095. Social security cards or ITIN letters for all persons on your tax return. Picture ID (such as valid driver's

Form 13614-C (October 2018) You will need: Tax Information such as Forms W-2, 1099, 1098, 1095. Social security cards or ITIN letters for all persons on your tax return. Picture ID (such as valid driver's

Tax Determination, Payments, and Reporting Procedures

CCH Essentials of Federal Income Taxation Tax Determination, Payments, and Reporting Procedures 2002, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://tax.cchgroup.com Taxpayer Filing

CCH Essentials of Federal Income Taxation Tax Determination, Payments, and Reporting Procedures 2002, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://tax.cchgroup.com Taxpayer Filing

CSS/Financial Aid PROFILE Early Application School Year

Section A --- Student s Information 1. Student s Name: Last Name First Name M.I. 2. Student s permanent mailing address: Street address City Zip or Postal Code Country 3. Student s preferred telephone

Section A --- Student s Information 1. Student s Name: Last Name First Name M.I. 2. Student s permanent mailing address: Street address City Zip or Postal Code Country 3. Student s preferred telephone

Tax Withholding and Estimated Tax

This publication was cited in a footnote at the Bradford Tax Institute. ClLICK HERE to go to the home page. Department of the Treasury Internal Revenue Service Publication 505 Cat. No. 15008E Tax Withholding

This publication was cited in a footnote at the Bradford Tax Institute. ClLICK HERE to go to the home page. Department of the Treasury Internal Revenue Service Publication 505 Cat. No. 15008E Tax Withholding

Tax Benefits for Higher Education

Department of the Treasury Internal Revenue Service Publication 970 (Rev. December 1998) Cat. No. 25221V Tax Benefits for Higher Education Contents Introduction... 1 Education Tax Credits... 2 Rules That

Department of the Treasury Internal Revenue Service Publication 970 (Rev. December 1998) Cat. No. 25221V Tax Benefits for Higher Education Contents Introduction... 1 Education Tax Credits... 2 Rules That

Overview of the Tax Structure