Form 5471 Substantial Compliance Rules: New IRS International Practice Unit Guidance

|

|

|

- Aron Jennings

- 6 years ago

- Views:

Transcription

1 Presenting a live 90-minute webinar with interactive Q&A Form 5471 Substantial Compliance Rules: New IRS International Practice Unit Guidance When Will the IRS Deem An International Tax Information Filing as Not "Substantially Complete"? TUESDAY, OCTOBER 24, pm Eastern 12pm Central 11am Mountain 10am Pacific Today s faculty features: Alison N. Dougherty, J.D., LL.M., Director, Aronson, Rockville, Md. Steven Toscher, Esq., Hochman Salkin Rettig Toscher & Perez, Beverly Hills, Calif. The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions ed to registrants for additional information. If you have any questions, please contact Customer Service at ext. 10. NOTE: If you are seeking CPE credit, you must listen via your computer phone listening is no longer permitted.

2 Tips for Optimal Quality FOR LIVE EVENT ONLY Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, you may listen via the phone: dial and enter your PIN when prompted. Otherwise, please send us a chat or sound@straffordpub.com immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. NOTE: If you are seeking CPE credit, you must listen via your computer phone listening is no longer permitted. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

3 Continuing Education Credits FOR LIVE EVENT ONLY In order for us to process your continuing education credit, you must confirm your participation in this webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar. A link to the Attendance Affirmation/Evaluation will be in the thank you that you will receive immediately following the program. For CPE credits, attendees must participate until the end of the Q&A session and respond to five prompts during the program plus a single verification code. In addition, you must confirm your participation by completing and submitting an Attendance Affirmation/Evaluation after the webinar and include the final verification code on the Affirmation of Attendance portion of the form. For additional information about continuing education, call us at ext. 35.

4 Hochman Salkin Rettig Toscher & Perez, P.C. and Aronson LLC for Strafford Form 5471 Substantial Compliance Rules: New IRS International Practice Unit Guidance When Will the IRS Deem an International Tax Information Filing as Not Substantially Complete? October 24, 2017 Hochman Salkin Rettig Toscher & Perez, P.C. Taxlitigator.com 9150 Wilshire Blvd, #300 Steven Toscher, Esq Aronson LLC Alison N. Dougherty Director, Tax Services Beverly Hills, CA

5 Meaning of Substantially Complete The Internal Revenue Service recently issued an International Practice Unit ( IPU ) providing guidance to its examining agents as to when a Foreign Information Reporting Form will be substantially complete and therefore considered adequate. If a taxpayer does not submit a substantially complete return, then penalties under IRC 6038, 6038A and 6046 may apply. Substantially complete and substantially incomplete are not defined in the Internal Revenue Code (IRC) or the regulations. International information returns must be substantially complete in order for the filer to have met its filing requirement. 5

6 Substantial Compliance Doctrine The substantial compliance doctrine is a judicial concept that applies to certain tax returns, elections and the substantiation of certain deductions. In some cases, courts require strict compliance with the statutory or regulatory requirements; in other situations, the courts will accept substantial compliance. While the concept of substantially complete has not been the subject of judicial review, the body of case law concerning the substantial compliance doctrine provides guide posts for how a court may interpret whether an international information return is substantially complete. After this exploration of the substantial compliance doctrine, we will discuss the available IRS informal guidance on substantially complete international information returns. This informal guidance, which consists of a Field Service Advice ( FSA ) and two Chief Counsel Advices ( CCA ), relates to Forms 5471 and Finally, we present examples that focus on what is required for a substantially complete international information return. 6

7 Strict Compliance Versus Substantial Compliance In determining whether a tax return satisfies a reporting requirement or whether a taxpayer has complied with a statute or regulatory requirement, there are two standards that may apply. The first requires strict compliance with the statute or regulatory requirement; the second requires substantial compliance. In analyzing the statute or regulatory requirement, the first step is to determine which standard applies. When determining which standard applies, courts may consider the following: If the particular information or requirement at issue is determined to be related to the substance or essence of the statute or regulation, then strict compliance is necessary. If, instead, the requirement is seen as procedural or directory then substantial compliance can apply. 7

8 Compliance with Respect to the Statutory Requirement of Filing an Income Tax Return Indiana Rolling Mills Co. v. Commissioner, 13 BTA 1141 (1928) dealt with the required signatures on a domestic corporate tax return. The statute (Section 239 of the Revenue Act of 1918) required that a corporate tax return be sworn to by the president or other principal officer and the treasurer or assistant treasurer. In Indiana Rolling Mills, the taxpayer s corporate return was sworn to by the vice president and secretary. The Service argued that the return was not a valid return for purposes of starting the statute of limitations. Although the dual signature requirement was repealed, this 1928 case was the first case to apply the substantial compliance doctrine to tax statutes. 8

9 Compliance with Respect to the Statutory Requirement of Filing an Income Tax Return (cont d) The court stated that a general rule of statutory construction is that those provisions that relate to the essence of the thing to be done are mandatory; those provisions that do not relate to the essence of the thing to be done are directory. Here, the essence of the statute was the making of an honest return by the corporation. If the requisite information is fairly and honestly given in a return sworn to by officers of the corporation who are familiar with its affairs, then the court determined that the taxpayer has substantially complied with the statute. The fact that the treasurer or assistant treasurer did not swear to the return did not go to the essence of the statute. In general, the Tax Court has required strict compliance where the requirement goes to the essence of the statute. The Tax Court has required only substantial compliance where the requirement does not go to the essence of the statute. 9

10 The Beard Test The Beard Test, 82 T.C. 777 (1984). In Beard the Tax Court has summarized the requirements for a tax return to be considered valid for purposes of beginning the statute of limitations on assessment: It provides sufficient data to calculate tax liability. The document must purport to be a return. There must be an honest and reasonable attempt to satisfy the requirements of the tax law. The taxpayer must sign the return under penalties of perjury. A return that meets these four requirements will be considered valid and trigger the running of the statute of limitations even if it contains other inaccuracies or omissions. 10

11 Compliance with Respect to the Statutory Requirement of Making an Election The substantial compliance doctrine is most commonly applied where a taxpayer attempts to make an election, but does not completely comply with the election requirements. Taylor v. Commissioner, 67 T.C (1977) dealt with an election that once was available under IRC 1251(b)(4)(B) in regard to gain from the disposition of property used in farming. Neither the taxpayer nor their advisors had read any of the published guidance concerning the making of the election. The court found that when the taxpayers filed their 1970 tax return, they subjectively believed that compliance with the accounting methods prescribed by IRC 1251(b)(4)(A) and the fact that they reported the gain from the sale of farm recapture property as long-term capital gain was an effective election under IRC 1251(b)(4). The Tax Court examined the statute at issue and determined that IRC 1251 was designed to prevent taxpayers from utilizing certain farm losses to convert ordinary income into capital gain. Such a recharacterization could be accomplished by requiring a portion of previously deducted farm losses to be characterized as ordinary losses on the sale of farm equipment. In order to avoid this re-characterization, a taxpayer had to follow certain accounting rules specified in IRC 1251(b)(4). The taxpayers in Taylor had followed these rules, but failed to include the statement required by the statute and regulations indicating that they chose this method. 11

12 Compliance with Respect to the Statutory Requirement of Making an Election (cont d) The Tax Court concluded that the essence of IRC 1251(b)(4) is to allow a farmer capital gains treatment if the farmer followed the accounting rules specified in IRC 1251(b)(4). The essence of the statute is that taxpayers compute taxable income from farming by using the methods specified. The election requirements assisted the IRS, but were directive. Therefore, the Tax Court concluded that the taxpayers had substantially complied by following the prescribed accounting methods and reporting the gain as long-term capital gain. 12

13 Compliance with the Substantiation Requirements in Treas. Reg A-13 An example of an issue that has been the subject of numerous cases is the requirement in Treas. Reg A-13(c)(2) that a taxpayer claiming a deduction for a charitable contribution of property worth more than $5,000 obtain a qualified appraisal, attach a fully completed appraisal summary and retain certain information (including the qualified appraisal itself). Bond v. Commissioner, 100 T.C. 32 (1993) is illustrative of such cases. In Bond, the taxpayers donated some blimps to charity. Taxpayers had an expert value the blimps and complete the Form 8283, Noncash Charitable Contributions, but the expert did not prepare a separate qualified appraisal. After an audit was opened, the expert provided information about his credentials to the IRS. The Tax Court determined that the only required information that was not provided by the taxpayer on the return was the expert s credentials and this information had been provided, once it was requested by the Service. The Tax Court examined whether the requirements in the regulations relate to the substance or essence of the statute. The Tax Court found that the purpose of the regulation was to provide information helpful to the Service in the 13

14 Compliance with the Substantiation Requirements in Treas. Reg A-13 (cont d) processing and auditing of returns on which charitable contributions are made. The regulation did not relate to the substance or essence of whether a charitable contribution was actually made, but instead alerted the IRS to the charitable contribution and required taxpayers to provide certain information. As a result, the regulatory requirement was held to be directory, rather than mandatory, and the taxpayer was held to have substantially complied. In cases that followed Bond v. Commissioner, there were varying degrees of noncompliance with the same regulation. In most of these other cases, the taxpayers were held not to have substantially complied because a critical element was missing. Examples include: Failing to get an appraisal, Failing to fill out Section B, Donated Property Over $5,000 (Except Publicly Traded Securities), of Form 8283, 14

15 Compliance with the Substantiation Requirements in Treas. Reg A-13 (cont d) Having someone without the relevant expertise complete the appraisal, Having an appraisal prepared outside the statutory window (including more than 60 days before the gift or after the return was filed), Including insufficient or inappropriate information in the appraisal or appraisal summary. In Bond v. Commissioner, the court found that the essence of the regulation was to alert the IRS to the charitable contribution. The Court found that the reporting requirements in the regulations were directory, and therefore the applicable standard was substantial compliance. 15

16 Conclusions About Substantial Compliance from Case Law While the focus of the discussion has been on cases in which substantial compliance applied, the courts have required strict compliance in cases where they determined the requirement related to the essence of the statute or regulation. An example is the requirement in IRC 170(f)(8) that the taxpayer obtain a contemporaneous written acknowledgement of a donation from the donee. Because obtaining this acknowledgement is part of the essence of IRC 170, courts have ruled that taxpayers must strictly comply with this requirement in order to claim the charitable contribution deduction. Substantial compliance generally applies to regulatory requirements. Strict compliance applies to statutory requirements. The analysis of whether there is compliance in this heavily litigated area is generally based on the facts and circumstances of the specific case. 16

17 Application of Substantial Compliance Doctrine by District Courts Following a 1990 case, Prussner v. United States, 896 F.2d 218 (7 th Cir. 1990) district courts and federal courts of appeals have generally applied the substantial compliance doctrine in a more restrictive way than the Tax Court. The decision in Prussner criticized the tendency of the Tax Court to broaden application of the substantial compliance doctrine wherever the taxpayer was in a sympathetic position. This tendency caused unwanted uncertainty for taxpayers, in the eyes of the Prussner court, and several circuits have followed Prussner in narrowing application of the substantial compliance doctrine. 17

18 Difference Between an Income Tax Return and an Information Return for Substantial Compliance Purposes In General Counsel Memorandum (GCM) Application of Section 6652(d) Penalty to Incomplete Forms 990-P and 4848, the Service considered whether section 6652(d)(1) would apply where entities required to file Forms 990-P and 4848 failed to provide all of the information required to be provided on those forms. In reaching the conclusion that the penalty is applicable under such circumstances, the GCM considers how information returns differ from income tax returns. The memo takes the position that cases concerning incomplete income tax returns are distinguishable from those concerning information returns because the goals of the two types of returns are different. Information reported on income tax returns is necessary to determine tax liability. As such, if a taxpayer omits information that is not necessary to determine tax liability, the return may be considered complete notwithstanding the omission. 18

19 Difference Between an Income Tax Return and an Information Return for Substantial Compliance Purposes (cont d) By contrast, information returns are required so that the Service can properly administer the revenue laws. If material information is left off an information return, such omission can impede the Service s ability to perform the duties placed on it by Congress. Because income tax and information returns serve different functions, the memo concludes that different rules should apply in determining whether or not a return is complete. 19

20 Substantial Compliance with Respect to International Information Returns Congress s intent in requiring taxpayers to report the information required to be reported on international information returns was to give the IRS more information about foreign entities with U.S. ties so that the IRS could determine if U.S. tax laws are being properly observed. In that regard, Congress enacted statutes requiring baseline information to be reported and gave the Secretary regulatory authority to determine the additional information required to be reported. IRC 6038 and 6038A provide penalties, respectively, for the failure to provide information in regard to (a) controlled corporations and partnerships and (b) certain foreign-owned corporations. The regulations under IRC 6038 provide that a taxpayer may be relieved from liability for the penalty if the IRS determines that such taxpayer substantially complied with the reporting requirements of IRC The regulations under IRC 6038A provide that a taxpayer who files a 20

21 Substantial Compliance with Respect to International Information Returns (cont d) substantially incomplete return is subject to penalty. Those regulations also provide that a taxpayer may be relieved from liability for the IRC 6038A penalty if the IRS determines that such taxpayer substantially complied with the reporting requirements of IRC 6038A. The regulations do not define the terms substantially complied or substantially incomplete. However, the Service has issued an FSA and two CCAs that explore these concepts. Failure to file complete returns may result in penalties. Regulations issued pursuant to IRC 6038 and 6038A provide specific rules that allow field examiners to consider whether the forms submitted have substantially complied with the reporting requirements (Forms 5471 and 5472) or are substantially incomplete (Form 5472) for purposes of the penalties imposed in those sections. The non-precedential advice that has been issued (and that is discussed below) applies only to these sections. 21

22 Substantial Compliance with Respect to International Information Returns (cont d) The judicial concept of substantial compliance, as discussed above, may apply to other international information returns (which do not have the same standards as those imposed under IRC 6038 and 6038A). Stated differently, absent a specific regulatory directive, only the judicial concept of substantial compliance would excuse anything less than strict compliance with a reporting requirement. A 1997 FSA discusses substantial compliance with respect to Form 5471, Information Return of U.S. Persons With Respect To Certain Foreign Corporations. FSA IRC 6038 Reporting Requirements. The FSA warns that even though the majority of the information may have been reported accurately and completely, this does not mean that there has been substantial compliance such that a taxpayer is relieved from liability for the IRC 6038 penalty. In the FSA, the U.S. taxpayer (UST) accurately reported the majority of the information, but it failed to accurately report major transactions with related parties. These types of related party transactions are important information for the IRS to evaluate in determining whether U.S. tax laws have been applied correctly. The FSA rejected the aggregate approach, under which a taxpayer would be considered to be in substantial compliance if it accurately reported a certain percentage of the information required to be reported on the Form Instead, it concluded that substantial compliance is measured on the basis of each significant item of information specified in IRC 6038(a)(1) for each individual Controlled Foreign Corporation (CFC). 22

23 Substantial Compliance with Respect to International Information Returns (cont d) Failure to accurately provide the information required by IRC 6038 may result in returns that are considered incomplete, even if most of the information on the form is correct. The taxpayer may be subject to penalties unless it can show reasonable cause or substantial compliance. CCA considered the meaning of the term substantially incomplete in regard to Form 5472, Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business, and as that term is used in Treas. Reg A-4(a)(1). The 2004 CCA considered whether a taxpayer s return would be considered substantially incomplete, and therefore subject to penalty, in a variety of different factual scenarios. 23

24 Substantial Compliance with Respect to International Information Returns (cont d) The CCA identifies two approaches that could be used to determine whether a return is substantially complete. The first is strict compliance, a rigorous interpretation of the rules that would treat virtually any substantive inaccuracy as rendering the return substantially incomplete. The second is a facts and circumstances approach. The CCA provides a list of seven factors that should be considered in a facts and circumstances analysis: 1. The magnitude of the underreporting, or of the over-reporting, of the erroneous reported transaction(s) in relation to the actual total amount of that reported type of transaction(s). 2. Whether the reporting corporation has reportable transactions other than the erroneous reported transaction(s) with the same related party and correctly reported such other transactions. 3. The magnitude of the erroneous reported transaction(s) in relation to all of the other reportable transactions as correctly reported. 24

25 Substantial Compliance with Respect to International Information Returns (cont d) 4. The magnitude of the erroneous reported transaction(s) in relation to the reporting corporation s volume of business and overall financial situation. 5. The significance of the erroneous reported transaction(s) to the reporting corporation s business in a broad functional sense. 6. Whether the erroneous reported transaction(s) occur(s) in the context of a significant ongoing transactional relationship with the related party. 7. Whether the erroneous reported transaction(s) is (are) reflected in the determination and computation of the reporting corporation s taxable income. Overall, these factors give informal guidance on measuring how significant the errors are. Keep in mind that estimates are allowed in completing Form 5472, if actual information is not readily available, but the estimates must be within prescribed limits. (The CCA assumes that the taxpayer did not estimate.) The 25

26 Substantial Compliance with Respect to International Information Returns (cont d) CCA uses a two-prong test in assessing substantial completeness: the magnitude of the errors and the effect of the noncompliance on the IRS s ability to efficiently audit the information required by the statute and regulations. The CCA cautions that no factor is necessarily more important than any other factor. The FSA and CCAs discussed above only provide informal guidance concerning substantial compliance and substantial completeness as those terms are used in the regulations under IRC 6038 and 6038A. As such, they don t apply to international information returns other than Forms 5471 and The substantial compliance defense to penalties described in the regulations under IRC 6038 and 6038A is available only to taxpayers who are subject to penalties under those sections. However, a court might apply the generally applicable substantial compliance doctrine discussed earlier to other international information returns. 26

27 Example 1- FSA Facts: UST filed separate Forms 5471 for a large number of Controlled Foreign Corporations (CFCs). Each Form 5471 reported much of the required information and included numerous pages of detailed financial information regarding financial condition, corporate stock structure, shareholders and results of operations. During exam, the Service identified significant understatements of purchases from and/or sales to some CFCs and related third parties (reported on Schedule M, Transactions Between Controlled Foreign Corporation and Shareholders or Other Related Persons) and significant inconsistencies in the reported earnings and profits of some CFCs. UST submitted most of the information required by IRC 6038 and related regulations. Other than the significant understatements, the information reported on the Forms 5471 was accurate and/or uncontested by the Service. Analysis: The information is mostly complete, but that doesn t mean that UST has substantially complied. The information that is missing or incorrect (to the tune of millions of dollars) is information that is the essence of the filing requirement. The related party information is a very important reason for requiring the Forms If a taxpayer is allowed to satisfy its filing requirements by accurately providing most of the information, it would have the opportunity to not provide or provide incorrect information with respect to very important categories. Conclusion: The FSA concluded that the UST did not substantially comply with the IRC 6038 reporting requirements. 27

28 Example 2 - CCA Facts: UST acquired controlling interest of a foreign parent corporation, which wholly owned the stock of multiple foreign corporations, for approximately four months of the tax year. Even though UST did not believe that it was required to file the forms, UST nevertheless timely filed Forms 5471 for certain foreign corporations. However, the forms were incomplete. Specifically, the amounts were not (a) reported in accordance with U.S. generally accepted accounting principles (GAAP) on Schedules C, Income Statement, and F, Balance Sheet, and (b) reported in U.S. currency on Schedules C and E, Income, War Profits, and Excess Profits Taxes Paid or Accrued. In addition, UST did not attach Schedule O, Organization or Reorganization of Foreign Corporations and Acquisitions and Dispositions of Its Stock, to the Forms Moreover, UST failed to file Forms 5471 for certain inactive or dormant foreign corporations. Analysis: There were a few issues addressed in the CCA. The first is UST s belief that it did not have to file the Forms That fact does not matter in determining substantial compliance, but may bolster the taxpayer s defense of reasonable cause. Second, UST failed to file required information, including Schedule O. Similar to Example 1, the information that is not supplied by UST is important. The failure to include Schedule O, by itself, is likely to cause the taxpayer to fail the substantial compliance test. The failure to convert the information into U.S. GAAP and U.S. dollars makes it difficult for the Service to audit. The Service s ability to audit efficiently is part of the goal of these reporting requirements. Conclusion: The CCA concluded that UST did not substantially comply with the IRC 6038 and 6046 reporting requirements. 28

29 Example 3 CCA Facts: UST is a reporting corporation as defined in Treas. Reg A-1(c). UST timely filed Form 5472 for transactions with its parent (Parent) for the tax years at issue. All information required by Treas. Reg A-2(b)(1) and (2) was included on the Form 5472 and estimates were not used. However, some transactions were erroneously reported. The CCA looked at whether the taxpayer had substantially complied with its reporting requirements. The magnitude of each erroneously reported transaction is substantial in relation to all other reportable transactions, as well as substantial in relation to UST s volume of business and overall financial situation. The CCA addressed four issues as to whether the Form 5472 was substantially complete: 1. UST over-reported amounts in Part IV of the Form 5472, reporting Purchases of Stock in Trade as $1,000X when the actual number was $500X. 2. UST reported amounts of intercompany accounts receivables not specifically required to be reported on Form 5472 and later corrected the Form 5472 to remove these amounts. 29

30 Example 3 CCA (cont d) 3. The amount reported on Form 5472 as the ending balance of related party loans did not match the opening balance on the next year s Form In addition, the opening balance of a loan was incorrectly reported. 4. UST over-reported one amount and under-reports another amount in Part IV of Form 5472 so that there was a relatively small aggregate difference between the correct total and what was reported. Analysis: As mentioned above, CCA lists seven factors which should be considered in determining whether the taxpayer has substantially complied. 1. Over-reporting constitutes inaccurate information and requires the IRS to determine the correct information. The fact that it is an overstatement, rather than an understatement, does not matter. The incorrect information hinders the IRS s ability to efficiently audit the Form 5472, if the error is material. Here, the 50% overstatement is of sufficient magnitude to violate the first, third and fourth factors. 30

31 Example 3 CCA (cont d) 2. The question is whether the Form 5472 as originally filed is substantially incomplete. The CCA assumes that $400X of intercompany receivables is erroneously included in Amounts Borrowed from Parent. The magnitude of the over-reporting is substantial because the overstatement is 40% of the transaction type and is substantial in relation to all other reportable transactions. The error violates the first, third and fourth factors. 3. Similar to 2, above, the magnitude of the over-reporting is 40%, which is significant. In addition, the loan has been in effect for at least two years, so it constitutes part of a significant, ongoing relationship between UST and a related party. This means that the first, third, fourth and sixth factors are violated. 4. In this example, we have relatively large offsetting mistakes, which result in a relatively small mistake on an aggregate basis. However, making multiple mistakes requires analyzing each mistake in isolation, as well as in the aggregate. Each mistake is significant in isolation, even if not in the aggregate, violating the first, third and fourth factors. The CCA concludes that the isolated mistakes cause the Form to be substantially incomplete, even if the Form is not substantially incomplete in aggregate. Conclusion: In each issue presented in the CCA, the magnitude of the incorrect reporting was substantial, the Form 5472 is substantially incomplete and the penalty should apply, unless UST has reasonable cause. 31

32

33 Form 5471 Substantial Compliance Rules: New IRS International Practice Unit Guidance Alison N. Dougherty Aronson LLC October 24, partnership-tax-return/

34 FORM 5471 INFORMATION RETURN OF U.S. PERSONS WITH RESPECT TO CERTAIN FOREIGN CORPORATIONS Examples of when a U.S. international information return filing is not substantially complete Errors apparent on the face of the Form 5471 return Errors beyond the face of the return Examples from the IRS International Practice Unit guidance 34

35 SCHEDULES REQUIRED TO BE ATTACHED TO FORM 5471 BASED ON APPLICABLE U.S. FILER CATEGORY 35

36 Examples of when a U.S. international information return is not substantially complete All required schedules are not attached or completed Overstatements or understatements of amounts that are required to be reported Incorrect or inaccurate information stated on the form All required information is not reported Financial statements that do not reflect an income statement with net income or loss that corresponds to the change in beginning to ending retained earnings or a balance sheet that does not balance 36

37 Examples of when a U.S. international information return is not substantially complete Related party transactions are not reported properly Correct boxes are not checked for Form 5471 filer categories Acquisitions and dispositions of foreign corporation stock are not reported Reorganizations of the foreign corporation are not reported Form 5472 direct and indirect foreign shareholders are not reflected Reference ID numbers for foreign parties are not provided 37

38 Errors apparent on the face of the Form 5471 information return Form 5471 Schedule F balance sheet does not balance Form 5471 Schedule C income statement net income does not correspond to change in beginning to ending retained earnings on Schedule F balance sheet Loans and receivables due from or payables due to related parties are on balance sheet but are not on Schedule M for Form 5471 Category 4 filer Loans due from or due to related parties are on Schedule M but not reported separately as related party loans on the balance sheet Schedule M reflects interest, dividend, rents, or royalty income or expense but those items are not reported separately on the balance sheet and there is no Subpart F income reported Form 5471 is filed for more than one related foreign corporation and Schedule M is not consistent Category 2 or 3 filer boxes are checked on page one but Schedule O is not attached, not complete, or wrong sections are filled out Schedule C income statement shows amount for tax provision but Schedule E does not reflect foreign taxes paid or accrued 38

39 Errors apparent on the face of the Form 5471 information return Schedule C income statement reflects passive income such as interest, dividends, rents, or royalties that does not qualify for the de minimis exception, there is current year E&P, and no current year Subpart F income is reported Schedule F balance sheet reflects loans due from U.S. shareholders, there is positive E&P, and no current year I.R.C. Section 956 inclusion is reported Form 5471 Schedule J does not reflect current year Subpart F or I.R.C. Section 956 inclusions which are reported on Schedule I Form 5471 Schedule J does not reflect current year distributions of non-previously taxed earnings and dividends are reflected on Schedule I Form 5471 Schedule J does not reflect accumulated amounts of prior year Subpart F or I.R.C. Section 956 inclusions Form 5471 Schedule J reports current year E&P in USD instead of foreign currency 39

40 Errors beyond the face of the Form 5471 information return Foreign corporation s financial statements are not properly converted into U.S. GAAP to be reported on the Form 5471 Foreign corporation s financial statements reported on Form 5471 are not properly converted from foreign currency to USD with the divide by convention or correct exchange rate Adequate books and records are not maintained to keep track of intercompany and related party loans, receivables, payables, and other transactions Calculations of CEP and AEP are not maintained from year to year Correct foreign tax pools are not calculated from year to year for U.S. shareholders that are C corporation parent companies of the foreign subsidiary corporation U.S. parent corporation does not correctly calculate and report the I.R.C. Section 78 gross up on dividends received from the foreign subsidiary corporation U.S. parent corporation does not correctly calculate and report the I.R.C. Section 902 or 960 deemed paid foreign tax credit for actual and deemed dividend distributions I.R.C. Section 1248 amounts are not properly calculated or reported for dispositions of CFC stock 40

41 Form 5471 Examples from the IRS International Practice Unit Guidance Example 1: FSA The taxpayer did not substantially comply with the Form 5471 reporting requirements. Significant understatements of purchases from and sales to some CFCs and related third parties reported on Schedule M Significant inconsistencies in the earnings and profits of some CFCS Other information reported on Form 5471 was accurate Example 2: CCA The taxpayer did not substantially comply with the Form 5471 reporting requirements. Schedule C income statement and Schedule F balance sheet not reported in accordance with U.S. GAAP Schedule O was not attached Forms 5471 not filed for certain inactive or dormant foreign corporations 41

42 Form 5472 Example from the IRS International Practice Unit Guidance Example 3: CCA The taxpayer did not substantially comply with the Form 5472 reporting requirement. Some transactions were reported erroneously Magnitude of each erroneously reported transaction was substantial in relation to all other reportable transactions, substantial in relation to the volume of business and overall financial situation Specific Errors: Taxpayer over-reported amounts in Part IV purchases of stock in trade as $1,000X when the actual amount was $500x Taxpayer incorrectly reported intercompany A/R not required and later corrected Form 5472 to remove them Ending balance of related party loans did not match the beginning balance on the next year s Form 5472 and the opening loan balance was incorrectly reported Taxpayer over-reported one amount and under-reported another amount. There was a relatively small aggregate difference between the correct total and what was reported. 42

43 Form 5472 Example from the IRS International Practice Unit Guidance Example 3: CCA The taxpayer did not substantially comply with the Form 5472 reporting requirement. Seven factors to consider in determining whether taxpayer has substantially complied. 1. The magnitude of the underreporting, or of the over-reporting, of the erroneous reported transactions in relation to the actual total amount of that reported type of transaction. 2. Whether the reporting corporation has reportable transactions other than the erroneous reported transactions with the same related party and correctly reported such other transactions 3. The magnitude of the erroneous reported transactions in relation to all of the other reportable transactions as correctly reported 4. The magnitude of the erroneous reported transactions in relation to the reporting corporation s volume of business and overall financial situation 5. The significance of the erroneous reported transactions to the reporting corporation s business in a broad functional sense 6. Whether the erroneous reported transactions occur in the context of a significant ongoing transactional relationship with the related party 7. Whether the erroneous reported transactions are reflected in the determination and computation of the reporting corporation s taxable income 43

44 FORM 5471 INFORMATION RETURN OF U.S. PERSONS WITH RESPECT TO CERTAIN FOREIGN CORPORATIONS 44

45 FORM 5471 U.S. Federal Reporting Requirement Applicable to U.S. Persons with Respect to Foreign Corporations U.S. person = U.S. citizen or resident U.S. partnership U.S. corporation an estate or a trust that is not a foreign estate or trust as defined in I.R.C. 7701(a)(31) Foreign corporation = Per se foreign corporation Any foreign entity with limited liability for all owners that is not an eligible entity with a Form 8832 check-the-box election in effect 45

46 FORM 5471 Who Must File? Category 2 Filer = 1. A U.S. citizen or resident who is an officer or a director of a foreign corporation and 2. A U.S. person has acquired 10% or an additional 10% of vote or value of the foreign corporation in one more transactions Category 3 Filer = 1. U.S. person who acquires stock which when added to stock already owned represents 10% of vote or value 2. U.S. person who acquires an additional 10% of vote or value 3. U.S. person who is a U.S. shareholder of a captive insurance company per I.R.C. 953(c) 4. U.S. person who becomes a U.S. person while meeting the 10% stock ownership requirement 5. U.S. person who disposes of sufficient stock to reduce ownership percentage to less than 10% 46

47 Category 4 Filer = FORM 5471 Who Must File? U.S. person who had control of a foreign corporation for an uninterrupted period of at least 30 days during the foreign corporation s annual accounting period Control = U.S. person owns more than 50% of vote or value of the foreign corporation at any time during the U.S. person s tax year U.S. person who controls a corporation which owns more than 50% of another corporation is considered to be in control of the other corporation 47

48 Category 5 Filer = FORM 5471 Who Must File? 1. U.S. shareholder who owns directly, indirectly or constructively at least 10% of a controlled foreign corporation (CFC) 2. for an uninterrupted period of 30 days or more during any tax year of the foreign corporation and 3. who owned the stock on the last day of that year Controlled Foreign Corporation = foreign corporation with more than 50% of the total combined vote or value owned directly, indirectly and constructively by U.S. shareholders who each own at least 10% of the voting stock 48

49 FORM 5471 Indirect and Constructive Ownership To determine U.S. shareholder and CFC status for Category 5 Apply I.R.C. 958(a) stock owned through foreign entities is treated as being owned proportionately Apply I.R.C. 958(b) the attribution rules of I.R.C. 318(a) apply with some modifications From family members - Individual owns stock owned by spouse, children, grandchildren and parents From partnerships stock is owned proportionately by partners From corporations if 10% or more is owned, stock owned by the corporation is owned proportionately To partnership partnership is considered to own the stock owned by the partner To corporation if 50% or more of a corporation is owned, the corporation will own the stock of the owner Limited attribution from nonresident individuals and entities If partnership or corporation owns more than 50% of voting stock it is considered to own 100% No re-attribution 49

50 FORM 5471 FILING EXCEPTIONS Multiple Filers Exception One U.S. person is allowed to file the Form 5471 for other persons who have the same filing requirements. Category 5 filer may file a joint Form 5471 with a Category 4 or another Category 5 filer. For Category 3 filers, the Form 5471 may only be filed by another person having an equal or greater interest by vote or value. The U.S. person who files the Form 5471 on behalf of others must complete item D on page one. All U.S. persons identified in item D on whose behalf the Form 5471 is filed must attach a statement to their U.S. Federal tax return. Separate Schedules I and M must be filed for each U.S. person on whose behalf the Form 5471 is being filed. 50

51 FORM 5471 FILING EXCEPTIONS Constructive Owners Exception A U.S. person described in Category 3, 4 or 5 is not required to file if the following conditions are met: 1. The U.S. person does not own a direct interest; 2. The U.S. person is required to file solely because of constructive ownership from another U.S. person; and 3. The U.S. person through which the indirect shareholder constructively owns an interest in the foreign corporation files Form 5471 to report all of the required information. The U.S. person claiming the constructive owners exception is not required to file a statement with the U.S. Federal tax return. 51

52 FORM 5471 FILING EXCEPTIONS Constructive Owners Exception A Category 2 filer is not required to file if: 1. A. The acquiring U.S. person files the Form 5471 as a Category 3 filer and B. Immediately after a reportable stock acquisition, three or fewer U.S. persons own 95% or more in value of the foreign corporation s stock OR 2. The acquiring U.S. person has a deemed acquisition as a constructive owner through attribution from another U.S. person who files the Form

53 FORM 5471 FILING EXCEPTIONS Constructive Owners Exception A Category 4 or 5 filer is not required to file if: 1. No direct or indirect ownership in the foreign corporation and 2. The Form 5471 is required to be filed solely because of constructive ownership from a nonresident alien 53

54 FORM 5471 PAGE ONE Top of first page foreign corporation s annual accounting period Required tax year for CFC is the majority U.S. shareholder s tax year Report information on Form 5471 based on foreign corporation s tax year that ends with or within U.S. shareholder s tax year Schedule O reports acquisitions, dispositions, organizations and reorganizations that occurred during the U.S. shareholder s tax year U.S. Filer s name, address and tax year end Item A U.S. filer s U.S. taxpayer identification number (SSN or FEIN) Item B U.S. filer categories 2, 3, 4 and 5 Item C U.S. filer s percentage of voting stock owned directly, indirectly and constructively at end of foreign corporation s annual accounting period Item D U.S. person on whose behalf Form 5471 is filed for multiple filers of same information, members of U.S. consolidated groups and constructive owners exceptions Item 1 Name, address, date of incorporation, country of incorporation, principal place of business, business activity code number, principal business activity, functional currency Item 1(b)(1) U.S. FEIN of foreign corporation, if any Item 1(b)(2) Reference ID number of foreign corporation is required if it does not have a U.S. FEIN Item 2(a) Name, address and identifying number of U.S. branch office or agent Item 2(b) U.S. taxable income and tax paid if foreign corporation files a U.S. Federal income tax return (Form 1120-F) Item 2(c) Name and address of foreign corporation s statutory or resident agent in country of incorporation Item 2(d) Name and address of person with custody of foreign corporation s books and records 54

55 FORM 5471 SCHEDULES A & B 55

56 FORM 5471 SCHEDULES A AND B Schedule A Stock of the Foreign Corporation Description of each class of stock Number of shares issued and outstanding at beginning and end of annual accounting period Schedule B U.S. Shareholders of Foreign Corporation Category 3 and 4 filers complete Schedule B for U.S. persons that owned directly or indirectly through foreign entities 10% or more in vote or value of any class of foreign corporation s stock during the annual accounting period Column (a) Name, address and identifying number of U.S. shareholder Column (b) Description of each class of stock held by U.S. shareholder Columns (c) and (d) Number of shares held at beginning and end of annual accounting period Column (e) Pro rata share of Subpart F income as a percentage 56

57 FORM 5471 SCHEDULE C INCOME STATEMENT 57

58 FORM 5471 SCHEDULE C INCOME STATEMENT Income statement should be reported in functional currency and translated into U.S. dollars based on the average exchange rate for the foreign corporation s tax year in accordance with U.S. GAAP. Functional currency net income or loss reported on line 21 Schedule C provides the starting point to determine current earnings and profits on Schedule H. Note that non-income taxes are reported on line 15 of Schedule C and income taxes deducted in accordance with U.S. GAAP are reported on line 20. Consider materiality when providing detail for other income and deductions Note lines 4, 5 and 6 could indicate potential Subpart F income. If parent and sub are both CFCs, present the parent s income statement on a stand-alone basis. 58

59 FORM 5471 SCHEDULE E INCOME TAXES PAID OR ACCRUED 59

60 FORM 5471 SCHEDULE E INCOME, WAR PROFITS AND EXCESS PROFITS TAXES PAID OR ACCRUED Income, war profits and excess profits taxes paid or accrued to United States, any foreign country or U.S. possession for the annual accounting period Accrual method taxpayers report amounts in the local currency and then translate to U.S. dollars based on average exchange rate for the tax year to which the tax relates unless an exception applies Translate to U.S. dollars based on exchange rate at time the taxes are paid if: The taxes are paid more than two years after the close of the tax year to which the taxes relate The taxes are paid in a tax year prior to the year to which they relate The taxes are denominated in a hyperinflationary currency The taxes are denominated in any currency other than the taxpayer s functional currency if the taxpayer makes an election under I.R.C. 986(a)(1)(D) U.S. dollar amount of foreign taxes will be included in foreign corporation s foreign tax pool relevant for calculating the I.R.C. Section 902 deemed paid foreign tax credit 60

61 FORM 5471 SCHEDULE F BALANCE SHEET 61

62 FORM 5471 SCHEDULE F BALANCE SHEET Balance sheet is reported and translated into U.S. dollars in accordance with U.S. GAAP. Line 5 loans to (U.S.) shareholders and other (U.S.) related persons may indicate a possible I.R.C. Section 956 inclusion if the foreign corporation has positive earnings and profits. Consider whether an appropriate interest rate is being charged on loans receivable due from and loans payable due to particularly for shareholders and other related persons. Significant line 1 cash amounts may indicate that FinCEN Form 114 Report of Foreign Bank and Financial Accounts (FBAR) should be filed if a U.S. shareholder owns more than 50% of foreign corporation or if U.S. officers and directors have signature authority over the foreign accounts. 62

63

64 FORM 5471 SCHEDULES G, H & I 64

65 FORM 5471 SCHEDULE G OTHER INFORMATION Statement required if foreign corporation owned 10% directly or indirectly of a foreign partnership Disclosure required to indicate ownership of interest in a trust or foreign disregarded entity Form 8858 must be attached by Category 4 or 5 filer of Form 5471 if foreign corporation is the tax owner of a foreign disregarded entity. Otherwise, a statement is attached by other filers. Disclosure for participation in cost sharing arrangement for development of intangibles 65

66 FORM 5471 SCHEDULE H CURRENT EARNINGS AND PROFITS (CEP) E&P is important to determine Amount of dividends I.R.C. Section 956 inclusion for investment in U.S. property Subpart F income inclusion I.R.C. Sections 902 and 960 deemed paid foreign tax credits I.R.C. Section 1248 recharacterization of gain on sale of CFC stock Report on line 1 the functional currency U.S. GAAP net income or loss from line 21 of Schedule C income statement Tax adjustments to calculate E&P Deferred tax expense Bad debt reserves Inventory reserves Advance payments Contingencies, severance and restructuring reserves Goodwill amortization Unrealized foreign currency exchange gain or loss Cumulative translation account Prior period adjustments Depreciation Unicap 66

67 FORM 5471 SCHEDULE I SUMMARY OF SHAREHOLDER S INCOME FROM FOREIGN CORPORATION A separate Schedule I is required for each U.S. shareholder who is a Category 4 or 5 filer on whose behalf the Form 5471 is filed. Line 1 reports the U.S. shareholder s share of Subpart F income translated at average exchange rate for CFC s tax year. Line 2 reports the U.S. shareholder s I.R.C. Section 956 inclusion from earnings invested in U.S. property translated at the spot rate on the last day of the CFC s tax year Line 7 reports the U.S. shareholder s share of dividends actually received (and not previously taxed as Subpart F income) translated at the spot rate on the date when the dividend was included in income. Line 8 reports exchange gain or loss recognized on actual distribution of previously taxed income. Answer questions regarding blocked and unblocked income 67

68 FORM 5471 SCHEDULE I SUMMARY OF SHAREHOLDER S INCOME FROM FOREIGN CORPORATION CFC S SUBPART F INCOME Subpart F income Foreign base company income Foreign personal holding income (interest, dividends, passive rents, royalties, net gains from property that produces this income and personal service contract income) Excluded are rents and royalties received from unrelated person and derived from active trade or business Excluded are dividends and interest received from related parties incorporated in same country as CFC Excluded are dividends, interest, rents and royalties received from related CFC if the amounts are not attributable to Subpart F income or U.S. ECI of the related CFC Foreign base company sales income CFC buys property from or sells to a related person Property is manufactured, produced, grown or extracted by a party other than the CFC outside the CFC s country of incorporation Property is sold for use, consumption or disposition outside CFC s country of incorporation Foreign base company services income Compensation, commission, fees or other income Derived from CFC s performance of technical, managerial, professional, scientific and like services CFC performs services for or on behalf of a related person The services are performed outside the CFC s country of incorporation Foreign base company oil related income (foreign source income derived from refining, processing, transporting, distributing or selling oil and gas or primary products derived from oil and gas) Other types of Subpart F income insurance income, international boycott income, illegal bribes and kickbacks 68

69 FORM 5471 SCHEDULE I SUMMARY OF SHAREHOLDER S INCOME FROM FOREIGN CORPORATION I.R.C. 956 INCLUSION INCOME I.R.C. 956 inclusion is the lesser of: the U.S. shareholder s pro rata share of CFC s applicable earnings, or the share of the average of the CFC s investments in U.S. property for the year as measured at the end of each quarter Investments in U.S. property include: Tangible property located in the United States Stock of a U.S. corporation An obligation with a U.S. issuer (bond, note, debenture, certificate, account receivable, note receivable, open account or other debt whether or not issued at a discount and whether interest or non-interest bearing) Exception for stock or debt of a U.S. corporation that is not a CFC shareholder and 25% or more of voting stock is not owned by CFC s U.S. shareholders Exception for account receivable for services paid within 60 days The right to use intangible property in the United States 69

70 FORM 5471 SCHEDULE I SUMMARY OF SHAREHOLDER S INCOME FROM FOREIGN CORPORATION FOREIGN CURRENCY EXCHANGE GAIN OR LOSS Foreign currency exchange gain or loss on distributions of previously taxed income is calculated as the difference between: The value of the distribution translated at the spot rate on the date of distribution, and The U.S. dollar amount at which the earnings were previously included in the U.S. shareholder s U.S. Federal taxable income Exchange gain or loss is ordinary income reportable as other income on the U.S. shareholder s U.S. Federal tax return 70

71 FORM 5471 SCHEDULE J ACCUMULATED EARNINGS & PROFITS (AEP) 71

72 FORM 5471 SCHEDULE J ACCUMULATED EARNINGS & PROFITS Report amounts on Schedule J in functional currency Column (a) Post-1986 undistributed E&P reports opening balance, current year additions and subtractions and closing balance Column (b) Pre-1987 E&P not previously taxed, distributed or deemed distributed Line 3 total CEP and AEP as of the close of the tax year before actual or deemed distributions during the year is the denominator of the fraction for the I.R.C. 902 deemed paid foreign tax credit calculation (local currency dividend/post-1986 E&P in local currency x post-1986 foreign tax pool translated into USD at average exchange rate unless taxpayer has elected to use the spot rate) Column (c) reports cumulative balance of previously taxed E&P resulting from I.R.C. 956 inclusions and Subpart F income 72

73 FORM 5471 SCHEDULE M TRANSACTIONS BETWEEN CFC AND SHAREHOLDERS OR OTHER RELATED PERSONS 73

74 FORM 5471 SCHEDULE M TRANSACTIONS BETWEEN CFC AND SHAREHOLDERS OR OTHER RELATED PERSONS Only Category 4 filers need to attach Schedule M to Form 5471 Report amounts in USD translated at average exchange rate for the year Report transactions between CFC and: U.S. filer Any U.S. or foreign corporation or partnership controlled by U.S. filer Any 10% or more U.S. shareholder of CFC other than U.S. filer Any 10% or more U.S. shareholder of any corporation controlling CFC IRS determines transfer pricing issues from Schedule M Schedule M may reflect Subpart F income (interest, dividends, rents, royalties, income from services or sales of property received) or I.R.C. 956 inclusion issues (amounts loaned by CFC to U.S. person or other accounts receivable due from U.S. person) Accrued amounts must be reported if accrual method CFC Lines 1-12 report amounts received by CFC Lines report amounts paid by CFC Dividends paid or received do not include those previously taxed under Subpart F Schedules should be maintained to reconcile amounts paid to and received from other related foreign corporations 74

75 FORM 5471 SCHEDULE M TRANSACTIONS BETWEEN CFC AND SHAREHOLDERS OR OTHER RELATED PERSONS Amounts borrowed and loaned (lines 19 and 20) should be shown as the highest amount during the year (not the beginning or ending balances) Do not report accounts payable as loans Include transactions between disregarded entities owned by the CFC and other entities in the controlled group in addition to activities of the CFC itself Activities between disregarded entities owned by the same CFC do not need to be reported Enter zeros if no activity for the year and do not leave Schedule M blank 75

76 FORM 5471 SCHEDULE O ORGANIZATION OR REORGANIZATION OF FOREIGN CORPORATION, AND ACQUISITIONS AND DISPOSITIONS OF ITS STOCK 76

77 FORM 5471 SCHEDULE O ORGANIZATION OR REORGANIZATION OF FOREIGN CORPORATION, AND ACQUISITIONS AND DISPOSITIONS OF ITS STOCK Schedule O, Part I is completed by Category 2 filers Report U.S. shareholders who have acquired 10% vote or value Schedule O Part II is completed by Category 3 filers Section A reports U.S. shareholder information Section B reports U.S. officers and directors Section C reports U.S. filer s acquisition information Section D reports U.S. filer s disposition information Report constructive dispositions such as sale of U.S. company with foreign subsidiary corporations, redemption, dilution and gifts Section E reports I.R.C. 351 transactions and reorganizations Description of assets, fair market value and basis of assets transferred to and by foreign corporation Section F requires statement if U.S. tax return filed in last three years, date of any reorganization in last four years and organization chart 77

78 FORM 5471 PENALTIES I.R.C. 6038(a) and Penalties for the failure to file Form 5471, Schedule M and Schedule O $10,000 USD failure to file penalty is automatically imposed for each late or incomplete Form 5471 Failure to file within 90 days after IRS notice to U.S. person, an additional $10,000 penalty per foreign corporation is charged for each 30-period or fraction thereof if failure continues up to maximum penalty of $50,000 per form per year I.R.C. 6038(c) - 10% reduction of foreign taxes available for credit under I.R.C. 901, 902 and 960 (not applicable for failure to file Schedule O) If failure continues 90 days or more after IRS mails notice, an additional 5% reduction is made for each 3-month period or fraction thereof if failure continues Limitation on this penalty is the greater of $10,000 or the income of the foreign corporation for its annual accounting period during with respect to which the failure occurs 78

79 FORM 5471 PENALTIES (Continued) Form 5471 penalties will apply to a U.S. person who agrees to have another person file on their behalf and all of the required information is not filed by the other person. I.R.C. 6662(j) 40% accuracy related penalty for underpayments of tax as a result of transactions involving an undisclosed specified foreign financial asset I.R.C. 6501(c)(8) Statute of limitations stays open indefinitely on entire U.S. Federal tax return when Form 5471 and required schedules are not filed Statute of limitations is extended to 3 years after the missing information is provided unless the failure is due to reasonable cause and not willful neglect 79

80 FORM 5471 NOT FILED FOR PRIOR YEARS How to resolve prior year delinquencies depends on whether the taxable income from the foreign corporation was reported on the U.S. shareholder s U.S. Federal tax return. All taxable income was reported with non-willful failure to file - Amend the prior year U.S. Federal tax return and attach the Form 5471 with a reasonable cause statement Not all taxable income was reported with non-willful failure to file Consider IRS Streamlined Domestic Offshore filing procedure with 5% penalty or IRS Streamlined Foreign Offshore filing procedure Not all taxable income was reported with willful or intentional failure to file Consider IRS Offshore Voluntary Disclosure Program Consider impact of failure to file FinCEN Form 114 (f/k/a TD F ) Foreign Bank Account Reports to report U.S. majority shareholder s or U.S. officer or director s financial interest in or signature authority over foreign accounts owned by the foreign corporation 80

81 FORM 5471 COMMON ISSUES 1. Present information consistently from year to year a. Schedule A and B beginning and ending shares outstanding b. Schedule F beginning and ending balance sheets c. Schedule J beginning balance of E&P and cumulative balances of previously taxed E&P from I.R.C. 956 inclusions and Subpart F income d. Schedule M reporting similar transactions each year 2. Report Subpart F income and I.R.C. 956 inclusions 3. Transfer pricing documentation to support related party transactions reported on Schedule M 81

82 CROSS-BORDER OWNERSHIP STRUCTURES FORM 5472 INFORMATION RETURN OF A 25% FOREIGN-OWNED U.S. CORPORATION OR A FOREIGN CORPORATION ENGAGED IN A U.S. TRADE OR BUSINESS 82

83 FORM 5472 INFORMATION RETURN OF A 25% FOREIGN-OWNED U.S. CORPORATION OR A FOREIGN CORPORATION ENGAGED IN A U.S. TRADE OR BUSINESS 83

84 FORM 5472 INFORMATION RETURN OF A 25% FOREIGN-OWNED U.S. CORPORATION OR A FOREIGN CORPORATION ENGAGED IN A U.S. TRADE OR BUSINESS Form 5472 is filed only when there is a reportable transaction between a reporting corporation and any U.S. or foreign related party Reporting corporation = 1. 25% foreign-owned U.S. corporation (by vote or value) 2. Foreign corporation engaged in a U.S. trade or business 3. U.S. disregarded entity wholly owned directly or indirectly by a nonresident foreign person (for tax years beginning after 12/31/2016) 84

85 NEW FORM 5472 FILING REQUIREMENT FOR U.S. DISREGARDED ENTITY OWNED SOLELY DIRECTLY OR INDIRECTLY BY ONE FOREIGN PERSON T.D New regulations New Form 5472 filing requirement for U.S. DREs with foreign owner applies for tax years beginning after 12/31/2016 and ending on or after 12/13/2017. U.S. DREs wholly owned by a foreign person will be required to obtain a U.S. FEIN and the foreign owner as a responsible party on the Form SS-4 will be required to obtain and provide either a U.S. FEIN, SSN (if eligible), or an ITIN. U.S. DRE is considered to be owned indirectly by one foreign person through a chain of other DREs or grantor trusts. 85

86 FORM 5472 INFORMATION RETURN OF A 25% FOREIGN-OWNED U.S. CORPORATION OR A FOREIGN CORPORATION ENGAGED IN A U.S. TRADE OR BUSINESS 25% Foreign-owned = at least one direct or indirect 25% foreign shareholder at any time during the tax year 25% foreign shareholder = a foreign person that owns directly or indirectly at least 25% of total vote or value of the corporation To determine 25% foreign shareholder and related parties, I.R.C. 318 attribution and constructive ownership rules apply (with modification for 10% threshold instead of 50% for attribution of stock ownership from corporations) 86

87 FORM 5472 INFORMATION RETURN OF A 25% FOREIGN-OWNED U.S. CORPORATION OR A FOREIGN CORPORATION ENGAGED IN A U.S. TRADE OR BUSINESS Form 5472 is filed only when there is a reportable transaction between a reporting corporation and any U.S. or foreign related party Related party = 1. Any direct or indirect 25% foreign shareholder of the reporting corporation 2. Any person who is related by more than 50% ownership to the reporting corporation 3. Any person who is related by more than 50% ownership to a 25% foreign shareholder of the reporting corporation 4. Any person who is related within the meaning of I.R.C

88 FORM 5472 INFORMATION RETURN OF A 25% FOREIGN-OWNED U.S. CORPORATION OR A FOREIGN CORPORATION ENGAGED IN A U.S. TRADE OR BUSINESS Form 5472 is filed only when there is a reportable transaction between a reporting corporation and any U.S. or foreign related party Reportable transaction = 1. Any transaction listed on Part IV for which monetary consideration was paid or received during the reporting corporation s tax year 2. Any transaction listed on Part IV for which part of the consideration was non-monetary or less than full consideration was paid or received 3. Transactions with U.S. DREs including capital contributions to and distributions of earnings from the U.S. DRE (for tax years beginning after 12/31/2016) 88

89 FORM 5472 FILING EXCEPTIONS A reporting corporation is not required to file Form 5472 if: 1. It had no reportable transactions 2. A U.S. person in control of a foreign related corporation files Form 5471 for the tax year to report information on Schedule M which shows all reportable transactions between the reporting corporation and the related party (the overlap rule) 3. The related corporation qualifies as a foreign sales corporation for the tax year and files Form 1120-FSC 4. A foreign corporation that otherwise would be required to file does not have a permanent establishment in the United States under an applicable U.S. income tax treaty and timely files Form 8333 Treaty-Based Return Position Disclosure 89

90 FORM 5472 FILING EXCEPTIONS A reporting corporation is not required to file Form 5472 if: 5. A foreign corporation whose gross income is exempt from U.S. Federal tax under I.R.C. Section 883 and timely and fully complies with the reporting requirements 6. Both the reporting corporation and the related party are not U.S. persons and the transactions will not generate in any tax year: U.S. source gross income or effectively connected income from a U.S. trade or business, or Any expense, loss or other deduction that is allocable or apportionable to such income 90

91 FORM 5472 CONSOLIDATED REPORTING If a reporting corporation is a member of an affiliated group filing a consolidated U.S. Federal income tax return then it can satisfy the requirements by filing a consolidated Form The common parent must attach a schedule stating which members of the U.S. affiliated group are reporting corporations and which of those members are joining in the consolidated Form 5472 filing. The schedule must show the name, address and FEIN of each member who is including transactions on Form A member of an affiliated group is not required to join in the consolidated Form 5472 filing just because other members do. 91

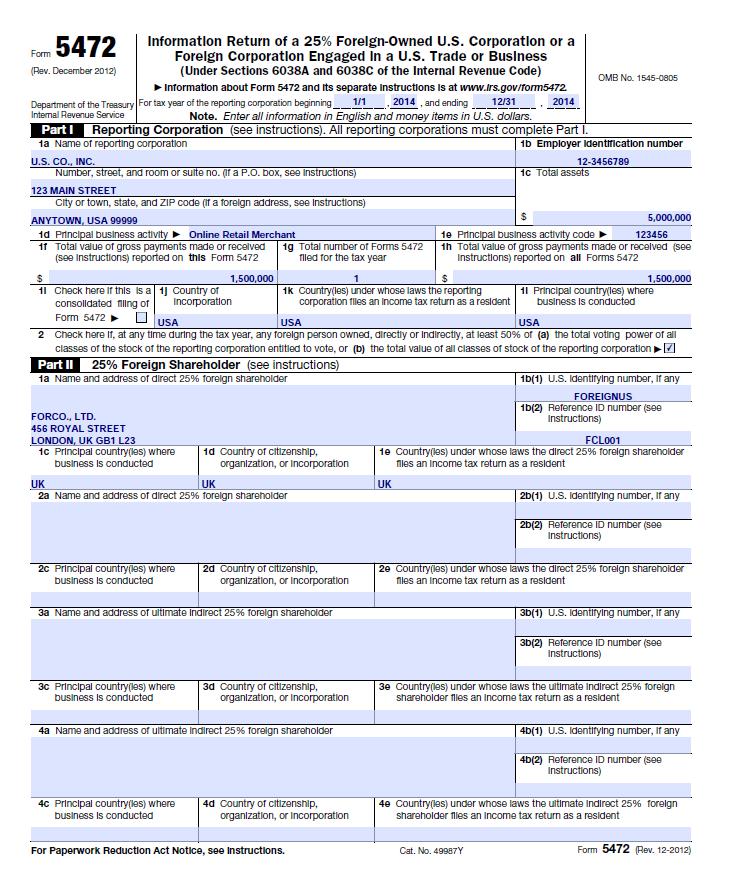

92 FORM 5472 PAGE TWO 92

93 FORM 5472 REPORTABLE TRANSACTIONS Inventory and tangible property transactions Rents and royalties Sales, leases, licenses, royalties, etc. of intangible property Compensation for different types of services Commissions Amounts loaned and borrowed Interest Premiums Platform contribution transactions Cost sharing transactions Other amounts Part IV lines 1 to 13 report amounts received by the reporting corporation Part IV lines 14 to 26 report amounts paid by the reporting corporation 93

94 FORM 5472 REPORTABLE TRANSACTIONS FOR TAX YEARS BEGINNING AFTER 12/31/2016 Solely for DREs, the new regulations expand the definition of reportable foreign related party transactions to include any transaction defined in U.S. Treas. Reg (i)(7) Includes amounts paid or received in connection with the formation, dissolution, acquisition, and dispositions of the DRE Includes contributions to and distributions from the DRE Examples clarify that the following transactions must be reported: Contributions to a domestic DRE from its foreign owner and distributions from a domestic DRE to its foreign owner Transactions between tiers of DREs with a single ultimate foreign owner are reportable related-party transactions 94

95 FORM 5472 REPORTABLE TRANSACTIONS Parts IV and V report monetary, nonmonetary and less than full consideration transactions between the reporting corporation and a foreign related party The terms paid and received include accrued payments and accrued receipts Do not complete Parts IV and V for transactions between the reporting corporation and a U.S. related party Part V Attach a schedule with a description of transaction sufficient to determine the nature and approximate monetary value of the transaction Should include a reasonable estimate of value 95

96 FORM 5472 WHEN AND WHERE TO FILE Attach Form 5472 to the reporting corporation s U.S. Federal tax return and file by the due date including extensions For tax years ending after 12/23/2014, Form 5472 cannot be filed separately from U.S. Federal tax return For tax years ending before 12/24/2014, Form 5472 must be filed timely even if U.S. Federal tax return is not filed timely 96

97 FORM 5472 PENALTIES $10,000 USD penalty per Form 5472 for the failure to file a substantially complete return or maintain records Additional $10,000 USD penalty per related party for the failure to file for each 30-day period that failure continues after 90 days since notification by IRS Statute of limitations stays open on entire U.S. Federal tax return unless it is possible to establish reasonable cause 97

98 FORM 5472 COMMON MISTAKES AND ISSUES Failure to properly classify the categories of intercompany transactions Reporting amounts paid by the reporting corporation on Part IV lines 1 through 13 and amounts received by the reporting corporation on Part IV lines 14 through 26 Failure to report reference IDs for 25% foreign shareholders and foreign related parties without U.S. FEIN Motivating taxpayers to disclose intercompany transactions Motivating foreign persons to disclose identifying information Substantially incomplete forms 98

99 FORM 5472 PREPARATION EXAMPLE Forco., Ltd. is a U.K. corporation which wholly owns U.S. Co., Inc. which is a U.S. subsidiary corporation. Forco., Ltd. manufactures widgets which it sells to its U.S. subsidiary corporation U.S. Co., Inc. U.S. Co., Inc. purchases $1,000,000 USD of widgets from its foreign parent corporation Forco., Ltd. U.S. Co., Inc. resells the widgets through its online retail business in the United States. U.S. Co., Inc. also performs market research in the United States for its foreign parent Forco., Ltd. to determine if the U.S. customers are fully satisfied with the quality of the widgets. Forco., Ltd. pays $500,000 USD to its U.S. subsidiary U.S. Co., Inc. as arm s length compensation for the services performed. 99

100 FORM 5472 PREPARATION EXAMPLE 100

101 FORM 5472 IRS INFORMATION REQUESTS IRS can request documentation of transactions between a reporting corporation and a foreign related party. If the requested documentation is not provided to the IRS from a foreign person, the IRS is permitted to determine the amount paid for or incurred by the reporting corporation with respect to the transactions at issue based on its own knowledge. The IRS could deny deductions of the reporting corporation due to lack of documentation. 101

102 FORM 5472 RECORD KEEPING REQUIREMENTS In addition to the Form 5472 filing requirement, there are recordkeeping requirements. U.S. Treas. Reg A-3. (1) I.R.C and 6038A. A reporting corporation must keep the permanent books of account or records as required by I.R.C that are sufficient to establish the correctness of the federal income tax return of the corporation, including information, documents, or records to the extent they may be relevant to determine the correct U.S. tax treatment of transactions with related parties. 102

103 FORM 5472 RECORD KEEPING REQUIREMENTS U.S. Treas. Reg A-1(h). Small corporation exception. A reporting corporation (other than an entity that is a reporting corporation as a result of being treated as a corporation under U.S. Treas. Reg (c)(2)(vi) of this chapter) that has less than $10,000,000 in U.S. gross receipts for a taxable year is not subject to U.S. Treas. Reg A-3 and A-5 for that taxable year. Such a corporation, however, remains subject to the information reporting requirements of U.S. Treas. Reg A-2 and the general record maintenance requirements of I.R.C For purposes of this paragraph, U.S. gross receipts includes all amounts received or accrued to the extent that such amounts are taken into account for the determination and computation of the gross income of the corporation. For purposes of this test, the U.S. gross receipts of all related reporting corporations shall be aggregated. 103

104 FORM 5472 RECORD KEEPING REQUIREMENTS (i) Safe harbor for reporting corporations with related party transactions of de minimis value. (1) In general. A reporting corporation (other than an entity that is a reporting corporation as a result of being treated as a corporation under U.S. Treas. Reg (c)(2)(vi)) is not subject to U.S. Treas. Reg A-3 and A-5 for any taxable year in which the aggregate value of all gross payments it makes to and receives from foreign related parties with respect to related party transactions (including monetary consideration, nonmonetary consideration, and the value of transactions involving less than full consideration) is not more than $5,000,000 and is less than 10 percent of its U.S. gross income. For purposes of this paragraph, U.S. gross income means the gross income reportable by the reporting corporation (or the aggregate gross income reportable by all related reporting corporations) for U.S. income tax purposes. Gross payments made to or received from foreign related parties cannot be netted; rather, the gross payments made to and received from foreign related parties are to be aggregated. Thus, for example, if a reporting corporation receives $4, of gross payments from a related party and makes $500,000 of gross payments to the same related party, it has aggregate gross payments of $5,200,000, and, therefore, does not qualify for the safe harbor under this paragraph. (2) Aggregate value of gross payments made or received. The aggregate value of gross payments made to (or received from) a foreign related party with respect to foreign related party transactions is determined by totaling the dollar amounts of foreign related party transactions as described in U.S. Treas. Reg A- 2(b)(3) and (4) on all Forms 5472 filed by the reporting corporation or related reporting corporations. 104

105 FORM 5472 RECORD KEEPING REQUIREMENTS Regulatory exceptions to the I.R.C. 6038A recordkeeping requirements and requirement to act as an agent for related parties for small corporations and corporations with de minimis related party transactions do not apply to U.S. DREs. The Form 5472 filing exception that applies when a U.S. person controls a related foreign corporation and files the Form 5471 with Schedule M to report related party transactions does not apply when a U.S. DRE is the reporting corporation. 105

106 ALISON N. DOUGHERTY DIRECTOR, TAX SERVICES ARONSON LLC Alison N. Dougherty provides tax services as a Director at Aronson LLC. Alison specializes in international tax reporting, compliance, consulting, planning, and structuring as a subject matter leader of Aronson s international tax practice. She has extensive experience assisting clients with U.S. tax reporting and compliance for offshore assets and foreign accounts. She provides outbound U.S. international tax guidance to U.S. individuals and businesses with activities in other countries. She also provides inbound U.S. international tax guidance to nonresident individuals and businesses with activities in the United States. She has worked extensively in the area of U.S. international tax reporting and compliance with the preparation of the U.S. Federal Forms 5471, 926, 8865, 8858, 5472, 1042, 1042-S, 8621, 8804, 8805, 8813, 8288, 8288-A, 8288-B, 1116, 1118, 1120-F, 1040-NR, 3520, 3520-A, 2555, 5713, 8832, 8833, 8840, 8843, 8854, 8938, and FBAR. She has counseled U.S. taxpayers regarding the outbound formation, capitalization, acquisition, operation, reorganization, and liquidation of foreign companies. She has significant experience with U.S. Federal nonresident tax withholding, foreign partner tax withholding, and FIRPTA withholding. She works closely with nonresident individuals and businesses regarding inbound U.S. real property investment. She often assists U.S. taxpayers with IRS amnesty program disclosures of offshore assets and foreign accounts. Alison completed the LL.M. (Master of Laws) in Securities and Financial Regulation in 2004 with academic distinction at Georgetown University Law Center. She completed the LL.M. (Master of Laws) in Taxation in 2000 and the Juris Doctor in 1999 at the University of Denver College of Law. She completed a Bachelor of Arts degree in Foreign Language in 1995 at Virginia Commonwealth University. Direct Main ADougherty@aronsonllc.com Aronson LLC 805 King Farm Blvd Third Floor Rockville, Maryland USA

Minaux LeRoi, CPA, MST, Senior Manager, Marcum, Miami Michel R. Stein, Principal, Hochman Salkin Rettig Toscher & Perez, Beverly Hills, Calif.

Presenting a 90-minute encore presentation with interactive Q&A Form 5471 Substantial Compliance Rules: IRS International Practice Unit Guidance Recognizing When the IRS Will Deem an International Tax

Presenting a 90-minute encore presentation with interactive Q&A Form 5471 Substantial Compliance Rules: IRS International Practice Unit Guidance Recognizing When the IRS Will Deem an International Tax

Mastering Form 5471 for Interests in Foreign Entities: Determining Ownership Share and Correct Filing Status

Mastering Form 5471 for Interests in Foreign Entities: Determining Ownership Share and Correct Filing Status TUESDAY, JUNE 23, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Mastering Form 5471 for Interests in Foreign Entities: Determining Ownership Share and Correct Filing Status TUESDAY, JUNE 23, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Mastering Form 5471 for Interests in Foreign Entities: Determining Ownership Share and Correct Filing Status

Mastering Form 5471 for Interests in Foreign Entities: Determining Ownership Share and Correct Filing Status TUESDAY, FEBRUARY 10, 2015, 1:00-2:50 PM EASTERN IMPORTANT INFORMATION This program is approved

Mastering Form 5471 for Interests in Foreign Entities: Determining Ownership Share and Correct Filing Status TUESDAY, FEBRUARY 10, 2015, 1:00-2:50 PM EASTERN IMPORTANT INFORMATION This program is approved

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies

FOR LIVE PROGRAM ONLY Mastering Form 5472: New Filing Requirements for Foreign Individuals, LLCs, and Companies THURSDAY, JULY 27, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM