2012 Deloitte Global Equity Plan Survey Sharing Value

|

|

|

- Madlyn Dorthy Morris

- 6 years ago

- Views:

Transcription

1 2012 Deloitte Global Equity Plan Survey Sharing Value Ohio Chapter NASPP Meeting Stephanie Linn, Deloitte Tax LLP Tammy Negrillo, Deloitte Tax LLP December 13, 2012

2 Agenda Introduction 2 Survey methodology and demographics 3 What types of plans are companies operating? 8 Why do companies operate specific plans? 13 Who participates in these plans? 19 How do companies manage their equity plans? 21 Country specific matters and challenges 36 Questions and contact information 40 1

3 Introduction, methodology, and participants The 2012 Deloitte Global Equity Survey provides an analysis of global equity plans operated by large multinational public or private companies. Responses received from 105 companies operating 270 equity plans Companies were headquartered in the following locations: Australia Canada Denmark Finland Germany Hong Kong Japan Luxembourg Netherlands Sweden UK U.S. As used in this document, Deloitte means Deloitte Tax LLP, a subsidiary of Deloitte LLP. Please see for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting. 2

The map shows the proportion of Survey participants by the region in which the companies headquarters are based.")

4 Introduction, methodology, and participants (cont.) The map shows the proportion of Survey participants by the region in which the companies headquarters are based. Responses were received from companies operating across a broad spectrum of industries. 17% 7% 62% 14% UK U.S. Rest of the world Europe 3

The following chart demonstrates the proportion of respondents (excluding two private companies) falling into four market")

5 Introduction, methodology, and participants (cont.) The following chart demonstrates the proportion of respondents (excluding two private companies) falling into four market capitalisation brackets. USD m Greater than 16,000m 4,800m - 16,000m 1,600m 4,800m Less than 1,600m 4

50% of companies")

6 Introduction, methodology, and participants (cont.) 50% of companies surveyed operate equity incentive plans in more than 20 countries 5

7 Polling question: Pressing issues What are your most pressing initiatives concerning your global equity plan? Determination of what types of plan to operate and where Determining award size for relevant populations Setting up/administrating tax favored plans Determining when and by which means to communicate to plan participants Implementing recharge agreements Managing compliance for mobile employees 6

8 Results of our 2012 Global Equity Plan Survey We have structured the results around five main themes: What types of plans are companies operating? How has this changed in recent years? Why do companies operate specific plans? Plan design and reasons for implementing a global equity plan Who participates in these plans? Is a global equity plan truly global, or is it sometimes too difficult or costly to offer in each country? How do companies manage their equity plans? How do companies manage the compliance and administration requirements? What forms of communications are used? How do companies respond to country specific changes? What country(s) are seeing the most change/in recent years? 7

9 What types of plans are companies operating? Free awards such as RSUs and PSPs are now the most common type of award across all regions. 8

There is a strong prevalence of share purchase type plans (either at a discount to market value or with a company")

10 What types of plans are companies operating? (cont.) There is a strong prevalence of share purchase type plans (either at a discount to market value or with a company match) in operation in the UK compared to any other type of plan. 9

The use of share options is strongest in the US compared to any")

11 What types of plans are companies operating? (cont.) The use of share options is strongest in the US compared to any other region. 10

Restricted stock plans make up 11% of broad based plans and 20% of executive plans across the rest of the")

12 What types of plans are companies operating? (cont.) Restricted stock plans make up 11% of broad based plans and 20% of executive plans across the rest of the world (including Europe), higher than for any other region. 11

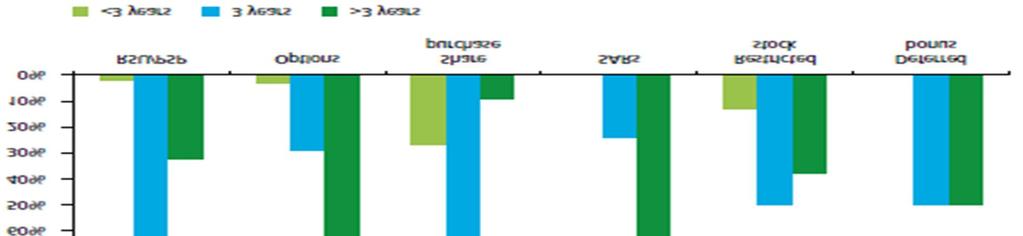

13 Length of vesting period 12

14 Why do companies operate equity plans? We asked companies to consider a range of factors that determine the reasons why they make awards to their employees and rank these according to importance We found that equity plans meet different needs depending on whether they are broad based or executive plans For both broad based and executive plans, the following factors were considered to be the most important: align the interests of employees with those of shareholders encourage share ownership utilize as retention mechanism For executives, incentivizing employees to achieve performance targets was equally important 13

15 Why do companies operate equity plans Executive plans 14

it is too complex to administer")

16 Tax Favored Plans 44% of respondents operate some form of qualified plan The main reasons why companies do not take advantage of local tax benefits were: companies do not have a significant number of employees to justify the costs or administration involved (50%) it is too complex to administer (33%) 15

17 Hot topic France Increase of employee and employer social contributions on qualified stock options and free shares. An additional budget act has been voted by the French Parliament on August16 th, The employer social contribution payable on the value of an option or share at the time of grant has been increased from 14% to 30%. The new taxation rate is applicable for options and free shares granted as from July 11 th It still remains advantageous for companies to remain in the scope of a French qualified plan. 30% rate is applicable on the taxable basis determined at the grant date, whereas in case of a non-qualified plan the social security rates would range from 26,5% to 45% of the gain realized at exercise date (for options) and at vesting date (for free shares). 16

18 Hot topic France In case of increase in value of the shares between grant and exercise/vesting, qualified plans will continue to offer cost saving opportunities for companies Assessing the 30% social contribution on the fair value of the options/shares in order to reduce the basis of this social contribution will increase the cost advantage for a company to remain in the scope of a French qualified plan. This rise complements changes that have already occurred since January 1, 2012: New reporting obligations applicable to stock options, free shares and BSPCEs Application of the withholding on gains related to grants made as from June 20, 2007 and resulting from the exercise of options / from the vesting of free shares realized by nonresidents as from April 1 st, 2011(OECD principles on gains sourcing) 17

19 Equity Plan Opportunities Identifying opportunities that deliver a greater after-tax benefit to participants at a lower out-of-pocket cost to the company Three Specific Opportunities to Consider: 1) Timing of taxation to the employee 2) Plan modifications to increase benefit for employee and/or reduce cost to employer 3) Type of equity award to be provided 18

20 Who participates in equity plans? The results suggested that the majority of companies (73%) used the same participation criteria globally to determine whether employees should participate in equity incentive plans. 19

21 Polling question: Communication What forms of communication does your company use in the operation of its equity plans? Newsletters Meetings/presentations Social Media (e.g., Facebook, Twitter) Outside administrator s website Booklets Intranet Other At what point during the equity cycle does your company communicate with its employees regarding their equity Award/Grant Moment of taxation (award/grant, vest, exercise) Changes in tax or regulatory requirements No communication 20

22 How do companies communicate their equity plans? Only 1% of companies currently use social media as a method of communicating with their employees; is by far the most frequently utilized method. 21

23 How do companies manage their equity plans? 52% of all companies confirmed that they did provide high level country-specific employee tax advice, with 15% of all companies including detailed information. A fewer number of European headquartered companies (40%) confirmed that they do not provide any type of tax specific advice to their employees. 22

24 Hot topic Japan 2013 equity reporting requirement Before Before January 2013: There were no employer reporting and/or income tax withholding requirements in Japan when employees who are tax residents of Japan received income from equity awards (e.g., stock options, performance shares, restricted stock units) from the foreign parent entity if the long-term incentive plan was administered outside of Japan. Instead, the employee was responsible for reporting the income from equity awards on his or her individual income tax return for the year in which the taxable event arose (due March 15 following the tax year end, December 31). Tax audits exposed cases of significant levels of under-reporting of equity income and therefore a new reporting requirement was implemented as part of the 2012 tax reforms in Japan. 23

25 Hot topic Japan 2013 equity reporting requirement After From January 2013 forward: Japanese subsidiaries that are owned (directly or indirectly) 50% or more by a foreign entity, and Japanese branches of foreign entities, will be required to submit annual equity reporting statement(s) to the Japanese National Tax Agency (NTA) detailing any income realized from equity awards (including cash awards where the underlying value of the award is based on share value) for Japanese tax resident employees and directors. The Japanese NTA requires a separate statement for each relevant employee. The statement is due by March 31 of the year following the year of income realization, with the first statement due March 31, 2013 for income earned in

26 Hot topic Japan 2013 equity reporting requirement - Addressing risk elements Potential Penalties: Failure to submit an equity reporting statement may attract the same penalties as failure to submit a Shiharai-choshuhyou (Annual Wage statement). The maximum allowable penalty is a prison sentence for the responsible party (i.e., the CEO) of the Japanese entity. Please note that in practice, the Japanese NTA has assessed financial penalties for failure to submit a wage statement. Typical penalties which have been levied are approximately 200, ,000 JPY (2,500 USD 6,400 USD) and vary based on the degree of failure (failure to submit one form being treated less severely than failure to submit one hundred). The extent to which the authorities may prosecute for failure to comply with the new requirement is unclear. Identification of non-disclosing individuals: Upon receipt of the equity reporting statement, the Japanese NTA will cross-reference the data received against individual income tax returns and will identify individuals who have failed to make the necessary disclosures. Beginning in 2013, if the Japanese NTA identify an underpayment of tax in one year, they will be able to look back up to 5 years to recover any unpaid tax and apply interest and penalties to the individual (if no withholding requirement applies). There may also be damage to the company s reputation with the Japanese NTA if the company is seen to have failed in its duty as an employer to inform employees that equity income should be disclosed in an employee s individual income tax return. 25

27 Obtaining professional advice on compliance issues 26

28 Increasing Corporate Tax Deductions Global Intercompany Recharge A U.S. employer can generally claim a deduction for the spread on equity-based compensation delivered to its U.S. employees: Fair Market Value of Stock at Acquisition - Price Paid by Employee to Acquire Shares (if any) Spread or Bargain Purchase Element For grants made to employees of foreign subsidiaries, the spread is generally NOT deductible for the U.S. employer (no employer/employee relationship) nor the foreign subsidiary (no economic cost) For most locations, a local tax deduction can be achieved by requiring the overseas employer to reimburse the U.S. company for the value of stock-based compensation awarded to its employees 27

29 Increasing Corporate Tax Deductions Global Intercompany Recharge (cont.) A global corporate recharge program can enhance the value of a company s global equity programs by: Obtaining tax deductions in jurisdictions where otherwise they might not be available Repatriating cash from subsidiaries to the parent company in a tax efficient manner (i.e. creation of positive cash flow) Favorably impacting company expenses awards under FAS123R Reducing global corporate tax rates, and Addressing global compliance issues and thus assisting with risk management 28

30 How do companies recharge? 57% of UK companies responded that they use the IFRS2 or equivalent accounting value as the cost on which they base their recharges. 29

31 Globally mobile employees What is an equity award trailing liability? An employee may be granted an equity award in one country, vest in that award in a second country, exercise in a third country, and ultimately sell the shares in a fourth country There could be employer reporting and withholding as well as individual tax implications in each jurisdiction Grant Vest Deemed Exercise Exercise Sale Stock options Belgium South Africa Singapore United Kingdom Chile 30

32 Globally mobile employees Changing compliance environment 1 Decreased revenue bases Decreasing revenue bases, along with technological improvements, create enhanced capacity and more potential challenges by tax authorities during audits, stricter enforcement of legislation, and less leniency in the negotiation of settlements and/or assessment of penalties. Decreases in company revenues result in less resources, technological and personnel, available to monitor and facilitate compliant operations. 1 Increased audit risk 4 Continuously changing 2 regulations 4 2 Challenge to keep current on Legislative constantly changing legislation, Compliance Increased updates scrutiny which increases exponentially as mobility creates need to understand interaction of regulations across jurisdictions. Public scrutiny (media and institutional shareholders) Commercial impact of negative publicity regarding non-compliant behaviors can have greater impact than fines/penalties assessed by regulators. 3 Acceptable risk profile 3 Management s risk tolerance Changes in management accountability and disclosure requirements have changed C-suite s perspective on what constitutes acceptable risk. Changing demographics for mobile employees impacts areas of focus. 31

33 Globally mobile employees - Why focus now? An international perspective There is an increasing need for governments to find new sources of revenue. According to the CIA World Fact Book 1, government spending exceeds revenues numerous countries, including: United Kingdom 26% Netherlands 12% Russia 22% United States 60% Japan 25% Ireland 94% India 47% 1 CIA World Fact Book 2011 Venezuela 26% Israel 12% Australia 11% 32

34 Cross-border compliance and equity Tightening rules Hong Kong Germany U.K. China Created rules in 2001 to tax gains upon departure of expats from Hong Kong Passed legislation in 2003 to tax gains realized by former residents Indicated intent to tax NR gains in 2003 Form 42 added to enable tracking Penalties charged for late submission of form Initial penalty of 300 per reportable event; further penalties of up to 60 per day Late or incorrect submissions affect the tax risk profile of the company Issued Circular 35 in 2005 to enable tracking of share awards New York/ Minnesota Stuckless case, 2006 Minnesota law change, 2008 United States France Japan Withholding on payments to nonresidents designated a Tier I issue in December 2008 French Supreme Court rules on stock option sourcing Withholding on nonresidents goes into effect Announced that certain Japanese branches and subsidiaries of foreign entities will be required to submit a report detailing equity compensation of resident employees 33

35 Globally mobile employees tracking movement 9% of U.S. companies do not track the movement of their mobile employees at all. 34

36 Globally mobile employees Withholding tax calculations 35

37 Polling question: Country headaches What countries pose the greatest challenges in terms of administering your plans or monitoring legislative updates? Australia China France Ireland UK Japan Other 36

38 Country specific matters Australia Companies were asked whether they had made changes to their granting practices since the 2009 changes. 38% of U.S. companies confirmed that they no longer grant stock options in Australia, whereas 75% of the rest of the world companies have not made changes to their granting practice. 37

39 Country specific matters China Tax registration (Circular 35) 60% of companies indicated that they were in the process of registering their plans with the local Chinese tax authorities 38

40 Country specific matters China (cont.) SAFE registration 59% of companies (85% of European headquartered companies) surveyed have already or are currently seeking SAFE approval 39

41 Questions?

42 Deloitte contact information Stephanie F. Linn Global Employer Services Deloitte Tax LLP Tel/Direct: Tammy J. Negrillo Global Employer Services Deloitte Tax LLP Tel/Direct:

43 This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

44 About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting. Member of Deloitte Touche Tohmatsu Limited

Global Plan Design: Trends and Strategies October 25, 2013

Global Plan Design: Trends and Strategies October 25, 2013 Mark Miller Tax Senior Manager, Deloitte Tax LLP Peter Simeonidis Tax Senior Manager, Deloitte Tax LLP Agenda Introductions Level Set Market Data

Global Plan Design: Trends and Strategies October 25, 2013 Mark Miller Tax Senior Manager, Deloitte Tax LLP Peter Simeonidis Tax Senior Manager, Deloitte Tax LLP Agenda Introductions Level Set Market Data

The Global Tax Reset 2017 Audit Committee Symposium

The Global Tax Reset Copyright 2017 Deloitte Development LLC. All rights reserved. 2017 Audit Committee Symposium Anticipate. Navigate. Focus. 1 The Global Tax Reset General context Multinational companies

The Global Tax Reset Copyright 2017 Deloitte Development LLC. All rights reserved. 2017 Audit Committee Symposium Anticipate. Navigate. Focus. 1 The Global Tax Reset General context Multinational companies

Best Practices in Managing a Globally Mobile Workforce. Deloitte Tax LLP

Best Practices in Managing a Globally Mobile Workforce Deloitte Tax LLP May 1, 2014 Agenda Introduction Current tax and regulatory environment Corporate tax consideration: Permanent establishment issues

Best Practices in Managing a Globally Mobile Workforce Deloitte Tax LLP May 1, 2014 Agenda Introduction Current tax and regulatory environment Corporate tax consideration: Permanent establishment issues

Update on recent tax & legal issues relating to global share plans. Andrew Moreton & Richard Wilson

Update on recent tax & legal issues relating to global share plans Andrew Moreton & Richard Wilson 29 September 2016 Introduction 2 Agenda Global updates of the last six months Key trends in employee share

Update on recent tax & legal issues relating to global share plans Andrew Moreton & Richard Wilson 29 September 2016 Introduction 2 Agenda Global updates of the last six months Key trends in employee share

GLOBAL SHARE PLANS WEBINAR 13 OCTOBER Matthew Emms David Gardner Emma Welland Rachel Tucker Jessica Pancamo Edouard de Raismes

GLOBAL SHARE PLANS WEBINAR 13 OCTOBER 2016 Matthew Emms David Gardner Emma Welland Rachel Tucker Jessica Pancamo Edouard de Raismes Agenda 1. Advantages /disadvantages of using an umbrella plan as opposed

GLOBAL SHARE PLANS WEBINAR 13 OCTOBER 2016 Matthew Emms David Gardner Emma Welland Rachel Tucker Jessica Pancamo Edouard de Raismes Agenda 1. Advantages /disadvantages of using an umbrella plan as opposed

Foreign Account Tax Compliance Act (FATCA)

") Foreign Account Tax Compliance Act (FATCA) Andrea Garcia Castelao November 18, 2013 Foreign Account Tax Compliance Act (FATCA) 0 2013 Deloitte Tax LLP FATCA Update Final FATCA regulations were released

Foreign Account Tax Compliance Act (FATCA) Andrea Garcia Castelao November 18, 2013 Foreign Account Tax Compliance Act (FATCA) 0 2013 Deloitte Tax LLP FATCA Update Final FATCA regulations were released

BEPS Actions implementation by country Actions 8-10 Transfer pricing

BEPS Actions implementation by country Actions 8-10 Transfer pricing On 5 October 2015, the G20/OECD published 13 final reports and an explanatory statement outlining consensus actions under the base erosion

BEPS Actions implementation by country Actions 8-10 Transfer pricing On 5 October 2015, the G20/OECD published 13 final reports and an explanatory statement outlining consensus actions under the base erosion

BIS International Locational Banking Statistics and International Consolidated Banking Statistics in Japan (end-june 2018)

") FOR RELEASE 8:5 A.M. September 14, 218 BIS International Locational Banking Statistics and International Consolidated Banking Statistics in Japan (end-june 218) I. BIS International Locational Banking

FOR RELEASE 8:5 A.M. September 14, 218 BIS International Locational Banking Statistics and International Consolidated Banking Statistics in Japan (end-june 218) I. BIS International Locational Banking

International Equity Awards: Granting to Employees Outside of Israel

International Equity Awards: Granting to Employees Outside of Israel April 13, 2015 Valerie Diamond Baker & McKenzie LLP Webinar Baker & McKenzie International is a Swiss Verein with member law firms around

International Equity Awards: Granting to Employees Outside of Israel April 13, 2015 Valerie Diamond Baker & McKenzie LLP Webinar Baker & McKenzie International is a Swiss Verein with member law firms around

New US income tax treaty and protocol with Italy enters into force

22 December 2009 International Tax Alert News and views from Foreign Tax Desks New US income tax treaty and protocol with Italy enters into force Executive summary On 16 December 2009, the United States

22 December 2009 International Tax Alert News and views from Foreign Tax Desks New US income tax treaty and protocol with Italy enters into force Executive summary On 16 December 2009, the United States

Key Issues in the Design of Capital Gains Tax Regimes: Taxing Non- Residents. 18 July 2014

Key Issues in the Design of Capital Gains Tax Regimes: Taxing Non- Residents 18 July 2014 How do we tax non-residents on capital income? Domestic design issues Tax treaty issues Interrelationship between

Key Issues in the Design of Capital Gains Tax Regimes: Taxing Non- Residents 18 July 2014 How do we tax non-residents on capital income? Domestic design issues Tax treaty issues Interrelationship between

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

Global Tax Reset Transfer Pricing Documentation Summary. February 2018

Global Tax Reset Transfer Pricing Summary February 2018 Global Tax Reset Transfer Pricing Summary Overview The Global Tax Reset Transfer Pricing Summary ( Guide ) compiles essential country-by-country

Global Tax Reset Transfer Pricing Summary February 2018 Global Tax Reset Transfer Pricing Summary Overview The Global Tax Reset Transfer Pricing Summary ( Guide ) compiles essential country-by-country

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars. Number of business days

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Designing Global Payroll and Benefit Programs. Fatima Laher and Maria Tsatas Deloitte LLP Randy Hahn Guberman Garson Segal LLP

Designing Global Payroll and Benefit Programs Fatima Laher and Maria Tsatas Deloitte LLP Randy Hahn Guberman Garson Segal LLP Agenda Evolving Payroll and Immigration landscape The Payroll Gap Analysis:

Designing Global Payroll and Benefit Programs Fatima Laher and Maria Tsatas Deloitte LLP Randy Hahn Guberman Garson Segal LLP Agenda Evolving Payroll and Immigration landscape The Payroll Gap Analysis:

Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation

Arm s Length Standard Global views within reach. Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation Transfer pricing continues to be the top enforcement

Arm s Length Standard Global views within reach. Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation Transfer pricing continues to be the top enforcement

The presentation will begin shortly. Audio will be streamed directly via your computer speakers. Enjoy the webcast!

The presentation will begin shortly. Audio will be streamed directly via your computer speakers. Enjoy the webcast! 2016 Concur, all rights reserved. Concur is a registered trademark of Concur Technologies,

The presentation will begin shortly. Audio will be streamed directly via your computer speakers. Enjoy the webcast! 2016 Concur, all rights reserved. Concur is a registered trademark of Concur Technologies,

Investor Profile. France Corporate

Investor Profile France Corporate 2017 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017. Any changes to legislation or

Investor Profile France Corporate 2017 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017. Any changes to legislation or

SADC Workshop on Statistics of International Trade in Services. FATS Compilation. Gaborone, Botswana January 2014

SADC Workshop on Statistics of International Trade in Services FATS Compilation Gaborone, Botswana 28 31 January 2014 Development of FATS Importance for assessing globalisation / mode 3 BOP trade in services:

SADC Workshop on Statistics of International Trade in Services FATS Compilation Gaborone, Botswana 28 31 January 2014 Development of FATS Importance for assessing globalisation / mode 3 BOP trade in services:

The Hunger Games: Surviving Global Administration Challenges

The Hunger Games: Surviving Global Administration Challenges Rachel Meyers, Product Communication Lead, E*TRADE Financial, US Sarah Papagelis, Sr. Corporate Paralegal, Sapient, US Jewon Wee, Managing Director,

The Hunger Games: Surviving Global Administration Challenges Rachel Meyers, Product Communication Lead, E*TRADE Financial, US Sarah Papagelis, Sr. Corporate Paralegal, Sapient, US Jewon Wee, Managing Director,

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets

Derivatives Markets") Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

11th Annual CEP and Silicon Valley NASPP Symposium March 24, Copyright 2015 CEP Institute 1

Agenda Plan summary and participation rate comparison Managing eligible participants Administrative Challenges of a Global ESPP Scott Barrall, CEP, Deloitte Tax LLP Veena Bhatia, CEP, Gilead Sciences,

Agenda Plan summary and participation rate comparison Managing eligible participants Administrative Challenges of a Global ESPP Scott Barrall, CEP, Deloitte Tax LLP Veena Bhatia, CEP, Gilead Sciences,

Moshe Bina, Senior Manager, International Taxation Department, Deloitte Israel

Moshe Bina, Senior Manager, International Taxation Department, Deloitte Israel Doing business in Japan Tax Aspects and a glance at BEPS Moshe Bina, Adv. September 6 th, 2015 Our main Topics. Country Domestic

Moshe Bina, Senior Manager, International Taxation Department, Deloitte Israel Doing business in Japan Tax Aspects and a glance at BEPS Moshe Bina, Adv. September 6 th, 2015 Our main Topics. Country Domestic

DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014

Quarterly Performance Report Q2 2014") DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds.

DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds.

Investor Profile. France FCP

Investor Profile France FCP 2017 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017. Any changes to legislation or treaties

Investor Profile France FCP 2017 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017. Any changes to legislation or treaties

DFA Global Equity Portfolio (Class F) Performance Report Q2 2017

Performance Report Q2 2017") DFA Global Equity Portfolio (Class F) Performance Report Q2 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q2 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2018

Performance Report Q3 2018") DFA Global Equity Portfolio (Class F) Performance Report Q3 2018 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2018 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q4 2017

Performance Report Q4 2017") DFA Global Equity Portfolio (Class F) Performance Report Q4 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q4 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2015

Performance Report Q3 2015") DFA Global Equity Portfolio (Class F) Performance Report Q3 2015 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2015 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises Kazakhstan, 2016 Brochure / report title goes here Section title goes here Documentation requirements

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises Kazakhstan, 2016 Brochure / report title goes here Section title goes here Documentation requirements

Foreign Account Tax Compliance Act (FATCA)

") Foreign Account Tax Compliance Act (FATCA) Impact Assessment on the Financial Services (Banking and Insurance) sectors and businesses in Trinidad and Tobago Presentation by the Bankers Association of Trinidad

Foreign Account Tax Compliance Act (FATCA) Impact Assessment on the Financial Services (Banking and Insurance) sectors and businesses in Trinidad and Tobago Presentation by the Bankers Association of Trinidad

Tax Working Group Information Release. Release Document. September taxworkingroup.govt.nz/key-documents

Tax Working Group Information Release Release Document September 2018 taxworkingroup.govt.nz/key-documents This paper contains advice that has been prepared by the Tax Working Group Secretariat for consideration

Tax Working Group Information Release Release Document September 2018 taxworkingroup.govt.nz/key-documents This paper contains advice that has been prepared by the Tax Working Group Secretariat for consideration

Global Business Barometer April 2008

Global Business Barometer April 2008 The Global Business Barometer is a quarterly business-confidence index, conducted for The Economist by the Economist Intelligence Unit What are your expectations of

Global Business Barometer April 2008 The Global Business Barometer is a quarterly business-confidence index, conducted for The Economist by the Economist Intelligence Unit What are your expectations of

Global Rewards Update New Zealand Changes to the Taxation of Employee Share Schemes

Global Employer Services November 2018 Global Rewards Update New Zealand Changes to the Taxation of Employee Share Schemes Background On March 29, 2018, new legislation was enacted in New Zealand, which

Global Employer Services November 2018 Global Rewards Update New Zealand Changes to the Taxation of Employee Share Schemes Background On March 29, 2018, new legislation was enacted in New Zealand, which

Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts

Derivatives Markets Turnover for April, 2007 and Amounts") Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts Outstanding as at June 30, 2007 January 4, 2008 Table

Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts Outstanding as at June 30, 2007 January 4, 2008 Table

The Global Equity Matrix

The Global Equity Matrix Cash Awards, Employee Stock Options, Stock Purchase Rights, Restricted Stock and Restricted Stock Units Argentina Denmark Israel Peru Sweden Australia Egypt Italy Philippines Switzerland

The Global Equity Matrix Cash Awards, Employee Stock Options, Stock Purchase Rights, Restricted Stock and Restricted Stock Units Argentina Denmark Israel Peru Sweden Australia Egypt Italy Philippines Switzerland

Recent challenges of global CFOs

Recent challenges of global CFOs Sandy Cockrell, Global leader and US national managing partner, CFO Program, Deloitte LLP March 16, 2017 Agenda Background Business environment Business risks and strategies

Recent challenges of global CFOs Sandy Cockrell, Global leader and US national managing partner, CFO Program, Deloitte LLP March 16, 2017 Agenda Background Business environment Business risks and strategies

Tax Executives Institute, Inc. / State Direct Tax

Tax Executives Institute, Inc. / State Direct Tax Steven Spaletto, Tax Managing Director, Deloitte Tax LLP Logan Wilkowich, Tax Senior Manager, Deloitte Tax LLP May 11, 2018 State Tax Implications of an

Tax Executives Institute, Inc. / State Direct Tax Steven Spaletto, Tax Managing Director, Deloitte Tax LLP Logan Wilkowich, Tax Senior Manager, Deloitte Tax LLP May 11, 2018 State Tax Implications of an

Export and import operations Tax & Legal, April 2017

Export and import operations Tax & Legal, April 2017 Export and import operations Tax & Legal, April 2017 Effective trading operations in Uzbekistan Today Uzbekistan actively develops international trading.

Export and import operations Tax & Legal, April 2017 Export and import operations Tax & Legal, April 2017 Effective trading operations in Uzbekistan Today Uzbekistan actively develops international trading.

China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation

Arm s Length Standard Global views within reach. China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation China s State Administration of Taxation (SAT)

Arm s Length Standard Global views within reach. China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation China s State Administration of Taxation (SAT)

GLOBAL HOT SPOTS. New Issues, Trends and Difficult Developments

GLOBAL HOT SPOTS New Issues, Trends and Difficult Developments Jo Garland, Manager Executive Remuneration and Employee Share Plans, Wesfarmers Erica Kidston, Senior Associate, Baker & McKenzie Jessica

GLOBAL HOT SPOTS New Issues, Trends and Difficult Developments Jo Garland, Manager Executive Remuneration and Employee Share Plans, Wesfarmers Erica Kidston, Senior Associate, Baker & McKenzie Jessica

17/10/2017. Circular 230 disclaimer. Payroll for International Assignments. Agenda. Your presenters

Circular 230 disclaimer Payroll for International Assignments 17 th Annual Virginia Statewide Payroll Conference October 13, 2017 Any tax advice contained herein was not intended or written to be used,

Circular 230 disclaimer Payroll for International Assignments 17 th Annual Virginia Statewide Payroll Conference October 13, 2017 Any tax advice contained herein was not intended or written to be used,

National Tax Agency, Japan

(Mutual Agreement Procedures) Report 214 When international double taxation arises from transfer pricing adjustments or other tax adjustments, the National Tax Agency ( NTA ) enters into Mutual Agreement

(Mutual Agreement Procedures) Report 214 When international double taxation arises from transfer pricing adjustments or other tax adjustments, the National Tax Agency ( NTA ) enters into Mutual Agreement

Permanent Establishment and Secondment Agreements Challenges of Linking Corporate and Individual Tax Issues for Global Mobile Employees

Permanent Establishment and Secondment Agreements Challenges of Linking Corporate and Individual Tax Issues for Global Mobile Employees In today s ever-changing global business arena, global mobility is

Permanent Establishment and Secondment Agreements Challenges of Linking Corporate and Individual Tax Issues for Global Mobile Employees In today s ever-changing global business arena, global mobility is

APA & MAP COUNTRY GUIDE 2017 CANADA

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

THIRD MEETING OF THE OECD FORUM ON TAX ADMINISTRATION

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT THIRD MEETING OF THE OECD FORUM ON TAX ADMINISTRATION 14-15 September 2006 Final Seoul Declaration CENTRE FOR TAX POLICY AND ADMINISTRATION 1 Sharing

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT THIRD MEETING OF THE OECD FORUM ON TAX ADMINISTRATION 14-15 September 2006 Final Seoul Declaration CENTRE FOR TAX POLICY AND ADMINISTRATION 1 Sharing

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Controlled Foreign Corporation

Controlled Foreign Corporation Certificate Course on International Taxation, Chennai Arpit Jain Director International Tax Background Spread of CFC legislation across the world in last 30-40 years US-perhaps

Controlled Foreign Corporation Certificate Course on International Taxation, Chennai Arpit Jain Director International Tax Background Spread of CFC legislation across the world in last 30-40 years US-perhaps

BEPS Action 13: Country implementation summary. Last updated: September 2, 2016

BEPS Action 13: implementation summary Last updated: September 2, 2016 0 Canada Draft legislation United States Mexico / MF / LF BEPS Action 13: implementation summary Sweden Peru Chile Bermuda / MF/LF

BEPS Action 13: implementation summary Last updated: September 2, 2016 0 Canada Draft legislation United States Mexico / MF / LF BEPS Action 13: implementation summary Sweden Peru Chile Bermuda / MF/LF

China s SAT publishes new rules on beneficial owners

World Tax Advisor Connecting you globally. 23 February 2018 China s SAT publishes new rules on beneficial owners On 3 February 2018, China s State Administration of Taxation (SAT) published new rules (Bulletin

World Tax Advisor Connecting you globally. 23 February 2018 China s SAT publishes new rules on beneficial owners On 3 February 2018, China s State Administration of Taxation (SAT) published new rules (Bulletin

IMPORTANT TAX INFORMATION

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

The OECD s Society at a Glance Simon Chapple OECD ELS/SPD Villa Vigoni, Italy, 9-11 th March 2011

The OECD s Society at a Glance 2 Simon Chapple OECD ELS/SPD Villa Vigoni, Italy, 9- th March 2 Reconceptualisation for 2: Internal reasons OECD growth from 3 to 34 countries Other major economies (e.g.

The OECD s Society at a Glance 2 Simon Chapple OECD ELS/SPD Villa Vigoni, Italy, 9- th March 2 Reconceptualisation for 2: Internal reasons OECD growth from 3 to 34 countries Other major economies (e.g.

Investor Profile. UK Corporate

Investor Profile UK Corporate 2017 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017. Any changes to legislation or treaties

Investor Profile UK Corporate 2017 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017. Any changes to legislation or treaties

Equity Income Sourcing and Compliance Issues for Mobile US and Non-US Employees

Equity Income Sourcing and Compliance Issues for Mobile US and Non-US Employees Authors: Valerie Diamond and Sinead Kelly August 30, 2017 Mobile Employee Equity Dilemma Over the last 10 years, how, when

Equity Income Sourcing and Compliance Issues for Mobile US and Non-US Employees Authors: Valerie Diamond and Sinead Kelly August 30, 2017 Mobile Employee Equity Dilemma Over the last 10 years, how, when

Actuarial Supply & Demand. By i.e. muhanna. i.e. muhanna Page 1 of

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Investor Profile. Irish Corporate 1 I N V E S T O R P R O F I L E

Investor Profile Irish Corporate 2017 1 I N V E S T O R P R O F I L E Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017.

Investor Profile Irish Corporate 2017 1 I N V E S T O R P R O F I L E Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017.

Challenges for Today s Short-Term Assignments

Point of view Challenges for Today s Short-Term Assignments Consulting. Outsourcing. Investments. Why is there an increasing trend for short-term assignments? What are the current challenges? How do companies

Point of view Challenges for Today s Short-Term Assignments Consulting. Outsourcing. Investments. Why is there an increasing trend for short-term assignments? What are the current challenges? How do companies

Employee Stock Plans: 2016 Year-End International Reporting Requirements

WHITE PAPER January 2017 Employee Stock Plans: 2016 Year-End International Reporting Requirements Year-end reporting requirements vary by jurisdiction for U.S. companies that provide stock plans to their

WHITE PAPER January 2017 Employee Stock Plans: 2016 Year-End International Reporting Requirements Year-end reporting requirements vary by jurisdiction for U.S. companies that provide stock plans to their

Anti-Money Laundering Compliance Issues

Anti-Money Laundering Compliance Issues 4th Annual Continuing Professional Development Event November 12, 2015 Presented by: Victoria Stuart Peter Moffatt 1 Introduction Compliance regime for reporting

Anti-Money Laundering Compliance Issues 4th Annual Continuing Professional Development Event November 12, 2015 Presented by: Victoria Stuart Peter Moffatt 1 Introduction Compliance regime for reporting

OECD s Base Erosion and Profit Shifting (BEPS) initiative and the Global Tax Reset Full results of fourth annual multinational survey August 2017

initiative and the Global Tax Reset Full results of fourth annual multinational survey August 2017") OECD s Base Erosion and Profit Shifting (BEPS) initiative and the Global Tax Reset Full results of fourth annual multinational survey August 2017 OECD s BEPS initiative full results of fourth annual multinational

OECD s Base Erosion and Profit Shifting (BEPS) initiative and the Global Tax Reset Full results of fourth annual multinational survey August 2017 OECD s BEPS initiative full results of fourth annual multinational

Chapter 2. Dispute Channels. 1. Overview of common dispute process

Chapter 2 Dispute Channels Suzan Arendsen * This chapter is based on information available up to 1 October 2010. 1. Overview of common dispute process Authorities worldwide increasingly consider transfer

Chapter 2 Dispute Channels Suzan Arendsen * This chapter is based on information available up to 1 October 2010. 1. Overview of common dispute process Authorities worldwide increasingly consider transfer

Global Withholding Tax

Global Withholding Tax Investor Profile Luxembourg FCP JANUARY 2018 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2016.

Global Withholding Tax Investor Profile Luxembourg FCP JANUARY 2018 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2016.

Avoiding Fraud and Corrupt Practices. Michael Steinberg IES Abroad AIEA Conference February 2014

Avoiding Fraud and Corrupt Practices Michael Steinberg IES Abroad AIEA Conference February 2014 Types of Corruption Bribery Bribery» E Extortion Embezzlement Grey Market Avoiding Fraud and Corrupt practices

Avoiding Fraud and Corrupt Practices Michael Steinberg IES Abroad AIEA Conference February 2014 Types of Corruption Bribery Bribery» E Extortion Embezzlement Grey Market Avoiding Fraud and Corrupt practices

Are You On Top of Tax Issues for Equity Plans?

Are You On Top of Tax Issues for Equity Plans? Suzie Bentley, Director, NVIDIA AmyLynn Flood, Partner, PwC Jennifer George, Director, PwC Sarah Hagberg, Senior Manager, Western Union Agenda Company Stats

Are You On Top of Tax Issues for Equity Plans? Suzie Bentley, Director, NVIDIA AmyLynn Flood, Partner, PwC Jennifer George, Director, PwC Sarah Hagberg, Senior Manager, Western Union Agenda Company Stats

France and Singapore sign revised income tax treaty

23 January 2015 International Tax Alert News from the Global Tax Desk Network EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

23 January 2015 International Tax Alert News from the Global Tax Desk Network EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

Indicator B3 How much public and private investment in education is there?

Education at a Glance 2014 OECD indicators 2014 Education at a Glance 2014: OECD Indicators For more information on Education at a Glance 2014 and to access the full set of Indicators, visit www.oecd.org/edu/eag.htm.

Education at a Glance 2014 OECD indicators 2014 Education at a Glance 2014: OECD Indicators For more information on Education at a Glance 2014 and to access the full set of Indicators, visit www.oecd.org/edu/eag.htm.

France clarifies tax treatment of international employees equity compensation

France clarifies tax treatment of international employees equity compensation The French tax authorities published two sets of long-awaited regulations on the equity compensation of internationally mobile

France clarifies tax treatment of international employees equity compensation The French tax authorities published two sets of long-awaited regulations on the equity compensation of internationally mobile

Headline Verdana Bold Qatar Tax Seminar 2016 Managing the sharp climb of tax expansion

Headline Verdana Bold Qatar Tax Seminar 2016 Managing the sharp climb of tax expansion December 14, 2016 Agenda Topic Overview of the Qatar Tax s System Corporate Tax Withholding Tax Practical Issues Questions

Headline Verdana Bold Qatar Tax Seminar 2016 Managing the sharp climb of tax expansion December 14, 2016 Agenda Topic Overview of the Qatar Tax s System Corporate Tax Withholding Tax Practical Issues Questions

Invesco Indexing Investable Universe Methodology October 2017

Invesco Indexing Investable Universe Methodology October 2017 1 Invesco Indexing Investable Universe Methodology Table of Contents Introduction 3 General Approach 3 Country Selection 4 Region Classification

Invesco Indexing Investable Universe Methodology October 2017 1 Invesco Indexing Investable Universe Methodology Table of Contents Introduction 3 General Approach 3 Country Selection 4 Region Classification

Issues surrounding business travellers. January Tax

January 2019 Tax 02 What is the issue? Global business travellers potentially trigger compliance and withholding obligations. These can be multiple obligations (income tax, social security, immigration,

January 2019 Tax 02 What is the issue? Global business travellers potentially trigger compliance and withholding obligations. These can be multiple obligations (income tax, social security, immigration,

15 Popular Q&A regarding Transfer Pricing Documentation (TPD) In brief. WTS strong presence in about 100 countries

In brief. WTS strong presence in about 100 countries") 15 Popular Q&A regarding Transfer Pricing Documentation (TPD) Contacts China Martin Ng Managing Partner Martin.ng@worldtaxservice.cn + 86 21 5047 8665 ext.202 Xiaojie Tang Manager Xiaojie.tang@worldtaxservice.cn

15 Popular Q&A regarding Transfer Pricing Documentation (TPD) Contacts China Martin Ng Managing Partner Martin.ng@worldtaxservice.cn + 86 21 5047 8665 ext.202 Xiaojie Tang Manager Xiaojie.tang@worldtaxservice.cn

Auscap Long Short Australian Equities Fund Newsletter June 2018

Auscap Long Short Australian Equities Fund Auscap Asset Management Limited Disclaimer: This newsletter contains performance figures and information in relation to the Auscap Long Short Australian Equities

Auscap Long Short Australian Equities Fund Auscap Asset Management Limited Disclaimer: This newsletter contains performance figures and information in relation to the Auscap Long Short Australian Equities

Re-inventing Global Liquidity Management: Can a multinational operate with minimal bank accounts?

Re-inventing Global Liquidity Management: Can a multinational operate with minimal bank accounts? Jim Scurlock Senior Manager Parimal Hemkar Director Agenda Microsoft Overview Life Cycle of the $ In House

Re-inventing Global Liquidity Management: Can a multinational operate with minimal bank accounts? Jim Scurlock Senior Manager Parimal Hemkar Director Agenda Microsoft Overview Life Cycle of the $ In House

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

World s Best Investment Bank Awards 2018

Global Finance will publish its selections for the 19th Annual World s Best Investment Banks in the April 2018 issue. Winners will be honored at an awards ceremony in New York City in March, and all award

Global Finance will publish its selections for the 19th Annual World s Best Investment Banks in the April 2018 issue. Winners will be honored at an awards ceremony in New York City in March, and all award

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts

Derivatives Markets Turnover for April, 2010 and Amounts") Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts Outstanding as at June 30, 2010 December 20, 2010 Table

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts Outstanding as at June 30, 2010 December 20, 2010 Table

Ireland Country Profile

Ireland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Ireland EU Member State Yes Double Tax Treaties With: Albania Armenia Australia

Ireland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Ireland EU Member State Yes Double Tax Treaties With: Albania Armenia Australia

Playing our part Pearson Tax report 2016

Playing our part Pearson Tax report 2016 Contents Introduction 2 Our global 4 Taxation principles 4 Tax incentives and arrangements 6 Tax havens 6 Governance & risk management 7 Tax department 8 Public

Playing our part Pearson Tax report 2016 Contents Introduction 2 Our global 4 Taxation principles 4 Tax incentives and arrangements 6 Tax havens 6 Governance & risk management 7 Tax department 8 Public

APA & MAP COUNTRY GUIDE 2017 UNITED STATES

APA & MAP COUNTRY GUIDE 2017 UNITED STATES Managing uncertainty in the new tax environment UNITED STATES KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance

APA & MAP COUNTRY GUIDE 2017 UNITED STATES Managing uncertainty in the new tax environment UNITED STATES KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance

Asia-Pacific update. TEI International Tax Planning Houston. 21 February 2017

Asia-Pacific update TEI International Tax Planning Houston 21 February 2017 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited,

Asia-Pacific update TEI International Tax Planning Houston 21 February 2017 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited,

IV Tax Administration in the Era of Globalization

IV The NTA promotes tax administration, including cooperation with foreign tax authorities to meet the era of globalization. As multinational enterprises conduct various cross-border economic activities

IV The NTA promotes tax administration, including cooperation with foreign tax authorities to meet the era of globalization. As multinational enterprises conduct various cross-border economic activities

Transfer pricing of intangibles

32E30000 - Tax Planning of International Enterprises Transfer pricing of intangibles Aalto BIZ / May 2, 2016 Petteri Rapo Alder & Sound Mannerheimintie 16 A FI-00100 Helsinki firstname.lastname@aldersound.fi

32E30000 - Tax Planning of International Enterprises Transfer pricing of intangibles Aalto BIZ / May 2, 2016 Petteri Rapo Alder & Sound Mannerheimintie 16 A FI-00100 Helsinki firstname.lastname@aldersound.fi

Summary of key findings

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

DIVERSIFICATION. Diversification

Diversification Helps you capture what global markets offer Reduces risks that have no expected return May prevent you from missing opportunity Smooths out some of the bumps Helps take the guesswork out

Diversification Helps you capture what global markets offer Reduces risks that have no expected return May prevent you from missing opportunity Smooths out some of the bumps Helps take the guesswork out

Foreign Direct Investment in the United States. Organization for International Investment

Foreign Direct Investment in the United States Organization for International Investment March 16, 2011 FOREIGN DIRECT INVESTMENT IN THE UNITED STATES Key Findings Foreign Direct Investment in the United

Foreign Direct Investment in the United States Organization for International Investment March 16, 2011 FOREIGN DIRECT INVESTMENT IN THE UNITED STATES Key Findings Foreign Direct Investment in the United

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

BRINKER CAPITAL DESTINATIONS TRUST

Important 2018 Tax Information Regarding Your Mutual s BRINKER CAPITAL DESTINATIONS TRUST The following tax information is furnished for informational purposes only. Please consult your tax advisor for

Important 2018 Tax Information Regarding Your Mutual s BRINKER CAPITAL DESTINATIONS TRUST The following tax information is furnished for informational purposes only. Please consult your tax advisor for

FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers

Communication on June 19 th 2014 last update: July 23 rd 2018 FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers Goal and legal framework of FATCA The

Communication on June 19 th 2014 last update: July 23 rd 2018 FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers Goal and legal framework of FATCA The

A short history of debt

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

FATCA Update May 2014

www.pwc.com The Basics Foreign Account Tax Compliance Act Purpose of Prevent and detect offshore tax evasion by US citizens Increased information reporting Enforced by withholding tax Effective begins

www.pwc.com The Basics Foreign Account Tax Compliance Act Purpose of Prevent and detect offshore tax evasion by US citizens Increased information reporting Enforced by withholding tax Effective begins

Overview of Transfer Pricing Regulations. CA Akshay Kenkre

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

PARVEST BOND BEST SELECTION WORLD EMERGING ( Sub-fund )

") This Product Highlights Sheet is an important document. Prepared on: 23.10.17 It highlights the key terms and risks of this investment product and complements the Prospectus 1 It is important to read the

This Product Highlights Sheet is an important document. Prepared on: 23.10.17 It highlights the key terms and risks of this investment product and complements the Prospectus 1 It is important to read the

Going Global: A Practical Survival Guide for Canadian Multinational Employers

Going Global: A Practical Survival Guide for Canadian Multinational Employers Baker & McKenzie LLP is a member firm of Baker & McKenzie International, a Swiss Verein with member law firms around the world.

Going Global: A Practical Survival Guide for Canadian Multinational Employers Baker & McKenzie LLP is a member firm of Baker & McKenzie International, a Swiss Verein with member law firms around the world.

All-Country Equity Allocator July 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

Practical guidance at Lexis Practice Advisor

Lexis Practice Advisor offers beginning-to-end practical guidance to support attorneys work in specific legal practice areas. Grounded in the real-world experience of expert practitioner-authors, our guidance

Lexis Practice Advisor offers beginning-to-end practical guidance to support attorneys work in specific legal practice areas. Grounded in the real-world experience of expert practitioner-authors, our guidance

Total tax contribution in 2012 A report on the economic contribution made by BBVA Group to public finances

1 Index 1 Introduction 2 Distribution of BBVA Group's tax payments by geographical area 3 Tax responsibility 4 5 Tax charged in the financial statements in 2012 6 Main conclusions 2 1 Introduction Tax

1 Index 1 Introduction 2 Distribution of BBVA Group's tax payments by geographical area 3 Tax responsibility 4 5 Tax charged in the financial statements in 2012 6 Main conclusions 2 1 Introduction Tax

Investor Profile. UK Pension Fund

Investor Profile UK Pension Fund 2017 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017. Any changes to legislation or

Investor Profile UK Pension Fund 2017 Disclaimer The information provided in this publication is for general information purposes only and is valid as at January 1, 2017. Any changes to legislation or