Welcome to the City of Virginia Beach. Opportunity Zone Open House. February 20, 2019 Zeiders Theater

|

|

|

- Rudolf Phillips

- 5 years ago

- Views:

Transcription

1 Welcome to the City of Virginia Beach Opportunity Zone Open House February 20, 2019 Zeiders Theater

2 City of Virginia Beach Opportunity Zone Resources Steven Harrison

3 YesVirginiaBeach.com/OZ

4 YesVirginiaBeach.com/OZ

5 YesVirginiaBeach.com/OZ Resources Zone Reports IRS Guidelines Investment Example Prospectus Contacts

6

7 AN OVERVIEW OF QUALIFIED OPPORTUNITY ZONES Todd D. Rothlisberger and Stephan J. Lipskis Poole Brooke Plumlee PC (757) Columbus St., Suite 100 Virginia Beach, VA

8 Legal Disclaimer Any accounting, business or tax advise contained in this communication, including attachments and enclosures, is not intended as a thorough, in depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties. If desired, Poole Brooke Plumlee PC would be pleased to perform the requisite research relevant to your specific situation and provide you with a detailed written analysis. Such an engagement may be the subject of a separate engagement letter that would define the scope and limits of the desired consultation services.

9 TOPICS ADDRESSED Background on the change in the tax law What is a qualified opportunity zone How to identify a qualified opportunity zone Why consider investing in a qualified opportunity zone.

10 BACKGROUND OF THE LAW The potential for these investments came into existence with the Tax Cuts and Jobs Act of 2017 (TCJA) approved on December 22, Proposed Regulations were published by the IRS on October 29, Those proposed regulations were subject to a 60 day public comment period so it remains to be seen if there will be any significant changes to the regulations before, or if, they become final. The public hearing on the comments was postponed due to the government shutdown. The Qualified Opportunity Zone/Fund idea behind the law has broad bipartisan support and has been studied/considered for many years prior to inclusion with the TCJA.

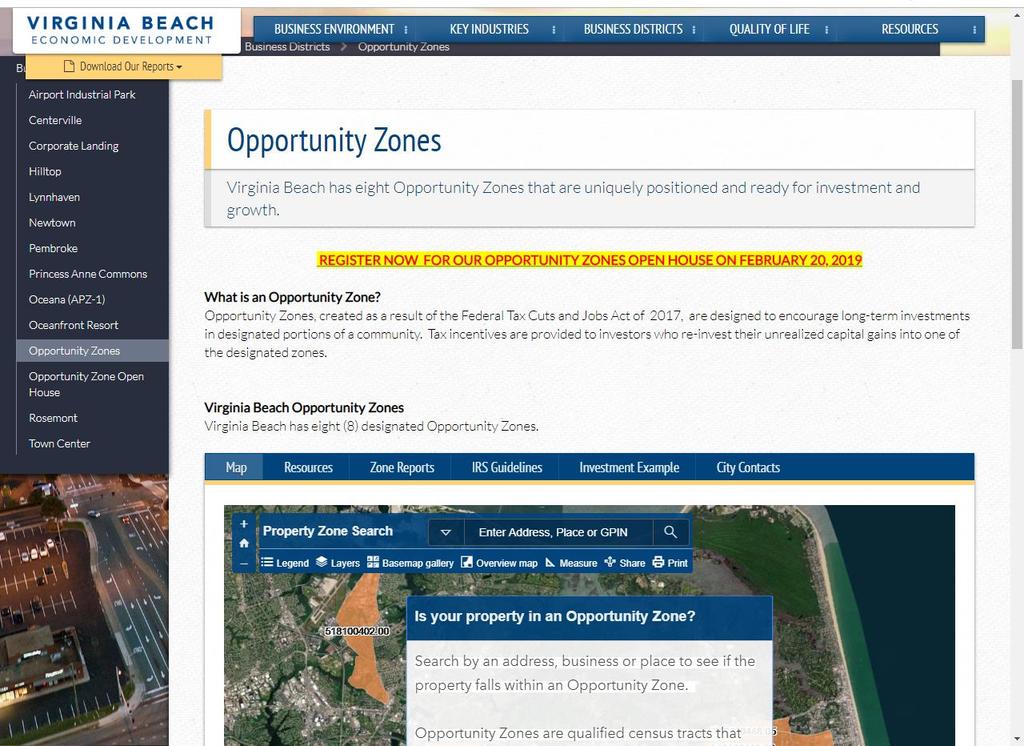

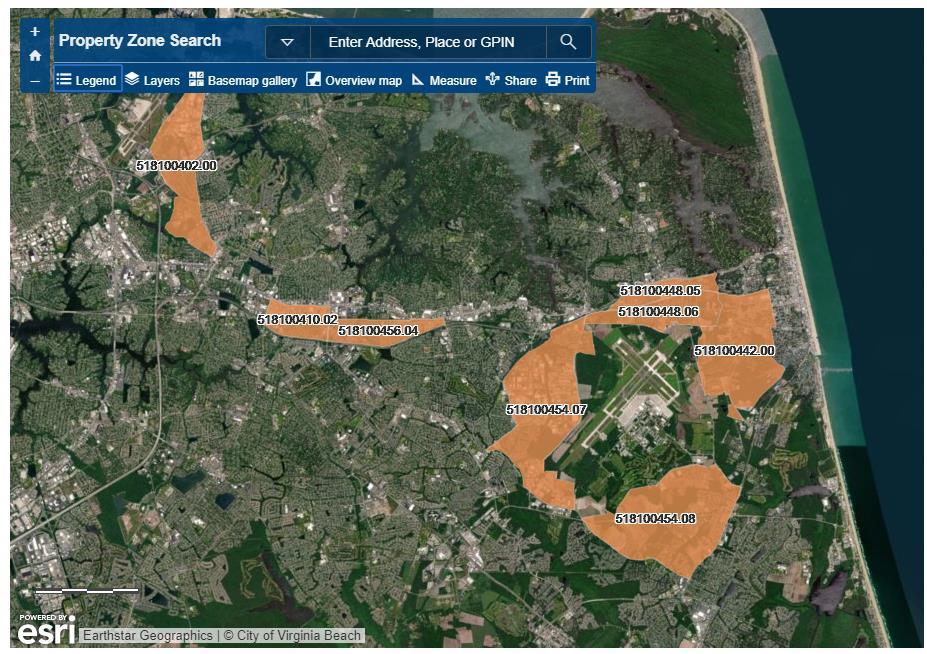

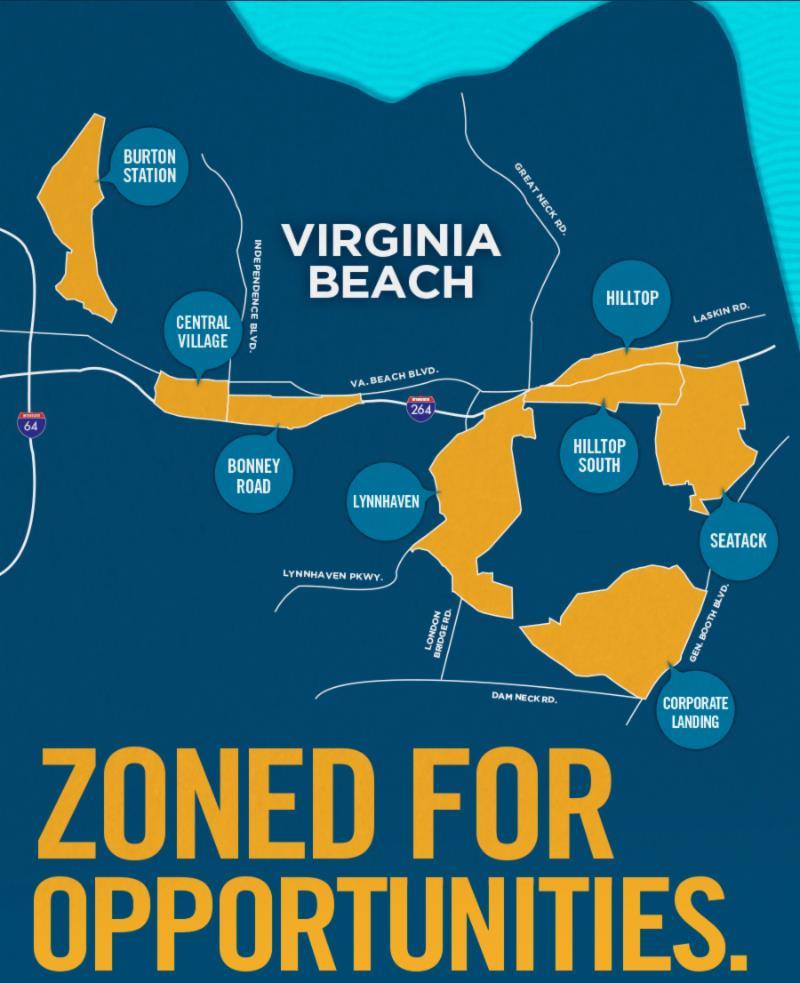

11 WHAT IS A QUALIFIED OPPORTUNITY ZONE In short, qualified opportunity zones are designated low-income areas. Each state was allowed to propose certain areas to be designated as a qualified opportunity zone. The zones are delineated by census tract. There were an estimated 41,000 potential zones nationwide. The purpose of establishing a zone is to encourage investment, and specifically long-term investment, in historically economically distressed communities. There are zones located throughout theunited States and its territories. Locally, there are three in Chesapeake, four in Hampton, seven in Newport News, sixteen in Norfolk, eight in Portsmouth, one in Suffolk, and eight in Virginia Beach.

12 HOW WERE ZONES DECIDED? All eligible census tracts were submitted to the respective states for nomination as QOZs. States nominated select QOZs from the list of eligible census tracts (different priorities/processes for each state in selecting). Federal government accepted all nominated tracts from the states. Future zones may be added or be available depending on retention of this program and new income data for census tracts

13 DESIGNATED ZONES IN VIRGINIA BEACH Virginia Virginia Beach Virginia Virginia Beach Virginia Virginia Beach Virginia Virginia Beach Virginia Virginia Beach Virginia Virginia Beach Virginia Virginia Beach Virginia Virginia Beach Low-Income Community Low-Income Community Low-Income Community Low-Income Community Low-Income Community Low-Income Community Low-Income Community Low-Income Community

14 HOW TO IDENTIFY A QUALIFIED OPPORTUNITY ZONE This website has a function that allows you to search any address to determine if it is in a qualified zone.

15 WHY INVEST IN A QUALIFIED OPPORTUNITY ZONE? There are two main tax advantages. You can defer the capital gains tax on the sale of an asset if sales proceeds are invested in a qualified opportunity fund. You can reduce the amount of capital gains tax paid on the deferred amount invested within the qualified opportunity fund if you hold the assets for at least five years. If you hold an asset for 5 years or longer, you increase your basis by 10% of the deferred gain; If you hold an asset for 7 years or longer, you increase your basis by 15% of the deferred gain; If you hold the investment for 10 years or more, upon disposition you may elect to increase the basis in that asset to 100% of the Fair Market Value. This effectively means that you pay NO capital gains tax on the appreciation in the investment if you hold that investment for at least 10 years. The last day to make the increase in basis election under the proposed regulations is December 31, 2047.

16 THINGS TO CONSIDER FOR INVESTMENT Appealing Investment within a Qualified Opportunity Zone Re-organization of physical business structures (need for new office, facility, etc.) Liquidation event creating capital gains Sale of secondary residence that does not qualify as primary residence Transaction poorly suited to 1031 exchange Remember Makes a good deal better, but does not make a bad deal good!

17 COMPARISON TO 1031 EXCHANGES 1031 Exchange Assets available to qualify for the exchange is limited to real estate. Gain on sale of capital asset deferred until subsequent sale of replacement asset. (unlimited deferral). Must reinvest the full amount of the sale to defer the gain. Replacement Property must be identified within 45 days of the initial sale. Closing on the replacement property must occur within 180 days of the initial sale. Replacement property must be of like kind of the property sold. Gain can be deferred successively, but will be due on the ultimate sale. Qualified Opportunity Zone Deferral can apply to virtually all capital gain assets. Must recognize the initial deferred gain at the end of (required end ofdeferral) Only required to reinvest the gain to avoid current taxation. Return of basis is untaxed. 180 days to invest in replacement. If going through a qualified opportunity fund, potentially another 180 days for that fund to invest, and perhaps longer with working capital safe harbor. No like kind requirement. Only qualified zone requirements Gain on replacement can be eliminated if investment held for 10 years.

18 WHAT GAINS AND WHAT TAXPAYERS ARE ELIGIBLE TO CLAIM THE CAPITAL GAINS DEFERRAL Any gain that is to be treated as capital gain for Federal Income Tax purposes is eligible for deferral They can be long-term, short-term, capital gains of any type including distributions from a mutual fund. Eligible gains include capital gains from actual, or deemed, sales or exchanges if the gain would be recognized not later than December 31, The sale or exchange generating the gain cannot be to a person related to the taxpayer. The gain deferred cannot exceed the amount invested in the qualified opportunity fund within 180 days from the date of the sale or exchange that generated the gain. You can split your investment into multiple parts provided each of the parts meets the 180-day deadline. Virtually any entity that recognizes capital gains for federal income tax purposes is eligible to defer the gain individuals, C Corporations, Regulated Investment Companies, Real Estate Investment Trusts, partnerships, and other pass-through entities (S-Corps). Partners and other pass-through owners can elect their own deferral if the partnership or passthrough entity does not elect to defer on the entity level.

19 WHAT IS A QUALIFIED OPPORTUNITY FUND (QOF)? The qualified opportunity fund is the investment vehicle that allows you to invest money into the qualified opportunity zone. You must purchase an eligible interest in a qualified opportunity fund to be eligible for tax deferral. You must purchase an equity interest in the qualified opportunity fund (i.e. common or preferred stock, LLC membership interest or partnership interest). You cannot purchase a debt instrument asthe qualifying eligible interest. Deemed contributions of money (such as in the context of some partnerships) also do not qualify.

20 REQUIREMENTS FOR THE FUND QOFs that are corporations or partnerships for tax purposes will be allowed to self-certify. There will be no pre-registration requirement. The QOF chooses the first month it is to be treated as a QOF. If it fails to choose, the first month of initial taxable year will be treated as the first month the entity is a QOF. CAUTION: A DEFERRAL ELECTION CAN ONLY BE MADE FOR AN INVESTMENT TO AN ENTITY THAT IS A QOF. THEREFORE, THE QOF CANNOT CHOOSE AN INITIAL MONTH THAT IS AFTER THE DATE OF THE INVESTMENT.

21 OZ Investment Structures Virginia Beach OZ Open House February 20, 2019 Jenny H. Connors

22 OZ Funds > Investment in an OZ Fund What is an OZ Fund? Investment vehicle that: Is a corporation or tax partnership for federal income tax purposes Holds at least 90% of its assets in OZ Property 22

23 The Asset Test > The 90% Asset Test Based on the average percentage of OZ Property held on: The last day of the first 6-month period of the taxable year of the OZ Fund, and The last day of the taxable year of the OZ Fund Ex. calendar-year taxpayer: June 30th and December 31 st If formed after 1 st of year, based on first 6-month period of taxable year If taxable year less than 6 months, only tested on last day of taxable year OZ Funds measure assets using financial statement values or, if none, cost 33

24 OZ Fund Certification > Certifying as an OZ Fund OZ Funds self-certify by filing an IRS Form Form 8996 Filed with timely federal income tax return for the year of OZ Fund certification OZ Fund selects month when OZ Fund status commences» If not, defaults to first month of taxable year» If OZ Investment made before OZ Fund commencement date, it is not an eligible OZ Investment 44

25 OZ Property > What is OZ Property? OZ Business Property (Direct Ownership) OZ Stock (Indirect Ownership) OZ Partnership Interests (Indirect Ownership) 55

26 OZ Fund Direct Ownership Structure Direct Structure 10% of Assets: Cash and other nonqualified financial property Intangibles Nonqualifying tangible property OZ Fund OZ Business Property 90% of Assets: Tangible property used in trade or business Acquired by purchase after 12/31/17 Original use in OZ or substantially improved Substantially all located in OZ during substantially all of holding period 66

27 OZ Fund Indirect Ownership Structure Indirect Structure Max 5% of assets Nonqualified financial property (excluding reasonable working capital) OZ Fund OZ Business (No Sin Business) 90% of Assets in OZ Partnership Interests (acquired after 12/31/17 for cash) 50% gross income attributable to the active conduct of trade or business in OZ Unlimited intangibles if substantial portion used in active conduct of business in OZ At least 70% of tangible assets must be OZ Business Property 77

28 Direct Vs. Indirect Structure Gross income requirement Direct None Indirect At least 50% derived from the active conduct of trade or business Permitted intangibles Working capital allowance Together with nonqualified financial property (e.g., working capital), limited to10% of OZ Fund assets Together with intangible assets, limited to 10% of OZ Fund assets, no safe harbor No limit if used in the active conduct of QO Business Reasonable working capital permitted (plus 31+ month safe harbor) Prohibited activities None Sin businesses Tangible property requirement At least 90% of assets must be tangible property None 88

29 Key Structuring Considerations > Key Provisions Purchase Excludes acquisitions of property from related parties Substantial Improvement Occurs when, over a 30-month period, beginning after the date of acquisition, additions to basis by QO Fund exceed an amount equal to the adjusted basis of the property at the beginning of the 30-month period. In the case of real estate, cost of land excluded from this calculation, lowering threshold 99

30 Key Structuring Considerations > Key Provisions Active Conduct Term yet to be defined Presumably, higher threshold for indirect structure businesses Sin Business Country club, massage parlor, hot tub facility, racetrack, health club or store the principal purpose of which is to sell alcoholic beverages for consumption off premises No prohibition against these businesses in direct structure 1010

31 Key Structuring Considerations > Key Provisions Reasonable Working Capital Safe Harbor Available for OZ Businesses (Indirect Structure)» Permits OZ Businesses to hold reasonable amounts of working capital for a period of up to 31 months To satisfy safe harbor, must develop a written plan that:» Identifies the financial property» Provides a plan for the financial property» Includes a written schedule for the deployment of financial property consistent with ordinary course of business operations 111

32 Mixed OZ Funds > Mixed Use Funds OZ Investment and non-oz Investment in OZ Fund treated as two separate investments Tax deferral and exclusion only apply to qualifying OZ Investment Requires tracking of eligible and non-eligible OZ Investments Deemed contributions to a partnership under Code Section 752 do not constitute non-oz Investments giving rise to mixed-use OZ Fund 1212

33 Questions & Contact Information Jenny H. Connors Please note: This presentation contains general, condensed summaries of actual legal matters, statutes and opinions for information purposes. It is not meant to be and should not be construed as legal advice. Individuals with particular needs on specific issues should retain the services of competent counsel. 1313

34 Qualified Opportunity Zone Businesses MARK DESROCHES, CPA

35 Business Investment QOZ Small business start ups can be less capital intensive Ease of moving or expanding into an opportunity zone Business valuations using multiple of earnings can generate a greater return Benefits held more than 10 years would be tax-free New asset class

36 Self Certification and Semi-Annual Tests Any corporation or partnership (including preexisting entities) can self certify to become a QOF Identity the first taxable year and first month the eligible entity wishes to be a QOF Comply with the 90% asset test required of QOFs Complete and attach Form 8996 with their tax return

37 QO Zone Business Property QO Zone Stock QO Zone partnership interest QO Zone business property Tangible real and personal property purchased after December 31, 2017 that is for used in an opportunity zone Original use of tangible property commences with use of property in the Opportunity Zone OR The business substantially improves the property during any 30 month period

38 Qualified Opportunity Zone Business (QOZB) Requirements 70% of the tangible property (real and personal) must be used in the opportunity zone 50% of the total gross income is derived from the active conduct of the business in an opportunity zone A substantial portion of the intangible property of the entity is used in the active conduct of the business Under 5% of the business property is attributable to nonqualified financial property which excludes reasonable working capital

. QOZ Subsidiary must be owned by QOF and must meet the requirements of a QOZB")

39 The 70% Substantially All Rule & QOZ Subsidiary In order for the taxpayer to be considered a Qualified Opportunity Zone Business (QOZB), substantially all or at least 70% of the tangible property owned or leased by the taxpayer must be QO Zone Business Property (QOZBP). QOZ Subsidiary must be owned by QOF and must meet the requirements of a QOZB

40 The Combined Structure By combining the 90% asset test for the QOF and the 70% substantially all test for the QOZB, the investment can have more other assets on hand to potentially diversify their investments In this scenario, the QOF would invest in a subsidiary QOZB, who would then invest in the qualified opportunity zone business property. QOF 90% Rule QOZB 70% Rule QOZBP

41 The Combined Structure

42 A reasonable amount of working capital can be kept on hand by an opportunity zone business and not count against them in the calculation of qualified business property 31-Month Working Capital Safe Harbor

43 1 2 3 For a QOZB, the amount held in working capital would count towards satisfying the 50% gross income test and the substantial portion of intangible property test being used in the active conduct of the business The 31-month working capital safe harbor will provide comfort to developers and investors concerned about the 180 day timeline of getting capital gains from the QOF and into opportunity zone property In the proposed regulations, there is no stipulated limit to how much money a company or fund can hold in working capital assets

44 31-Month Working Capital Safe Harbor Requirements The amount of working capital must be designated in writing for the acquisition, construction, and/or substantial improvement of tangible property in a QO Zone. Must have a written schedule consistent with the ordinary startup of a trade or business for the expenditure of the working capital assets. Capital must have been actually used in a manner that is substantially consistent with the above written designation and schedule.

45 Business Start Up Example Top Burger, Inc. Equal Partnership $200,000 $200,000 $400,000 QOF A QOZB $200,000 QOF B

46 Technology Startup Incubator A startup incubator, which houses numerous earlystage startup businesses in one setting, is a natural fit for the opportunity zone program. These highly scalable technology companies can hit it big (in which case you wouldn t pay the capital gains tax upon sale of your equity interest)

47 Pharmaceutical Drug development and other investment ideas that involve heavy research and development in the hopes to eventually land a key breakthrough or patent also lend themselves to the opportunity zone program. The downside is the same, but the upside can be significantly higher by reducing the capital gain expense you would normally have to incur when selling a higher appreciated asset.

48 Business Example: Government Contracts Secure Tech, Inc. Hires Key staff Relocates into OZ Secures Government Contract Outside Investors Invest in Secure Tech Secure Tech Grows

49 Both the franchisee and the franchisor looking to expand in an opportunity zone location can roll capital gains (either their own or outside investors ) into a QOF Both parties substantially improve the property After 10 years, the franchisor can sell his interest in the franchise to a new owner and pay no capital gains tax on the sale Franchise Benefits The Opportunity Zone program allows franchisee more incentive (ease of raising equity, higher after tax return on capital)

50 Mark DesRoches

51 Welcome to the City of Virginia Beach Opportunity Zone Open House February 20, 2019 Zeiders Theater

Investing in Opportunity Act IIOA 2017 Tax Cuts & Jobs Act

Investing in Opportunity Act IIOA 2017 Tax Cuts & Jobs Act Tara Sherbert, CEO of The Sherbert Group The Sherbert Group is a unique integration of companies that provide valuable tax, accounting, investment

Investing in Opportunity Act IIOA 2017 Tax Cuts & Jobs Act Tara Sherbert, CEO of The Sherbert Group The Sherbert Group is a unique integration of companies that provide valuable tax, accounting, investment

Tax Benefits of Investing in Opportunity Zones

Tax Benefits of Investing in Opportunity Zones Bradley J. Sklar ASCPA Montgomery, Alabama Opportunity Zones Created as part of the Tax Cut and Jobs Act of 2017 Purpose of Opportunity Zones To generate

Tax Benefits of Investing in Opportunity Zones Bradley J. Sklar ASCPA Montgomery, Alabama Opportunity Zones Created as part of the Tax Cut and Jobs Act of 2017 Purpose of Opportunity Zones To generate

Taking Advantage of Opportunity Zones: A Panel Discussion. Presented by Buchanan Ingersoll & Rooney Tampa October 2018

Taking Advantage of Opportunity Zones: A Panel Discussion Presented by Buchanan Ingersoll & Rooney Tampa October 2018 Florida Opportunity Zones Potential to eliminate poverty Areas with business activity

Taking Advantage of Opportunity Zones: A Panel Discussion Presented by Buchanan Ingersoll & Rooney Tampa October 2018 Florida Opportunity Zones Potential to eliminate poverty Areas with business activity

Puerto Rico designated as an Opportunity Zone

Puerto Rico designated as an Opportunity Zone Francisco Luis, CPA, JD Tax Partner February 2019 DISCLAIMER: This presentation and its content do not constitute advice. Attendants should not act solely

Puerto Rico designated as an Opportunity Zone Francisco Luis, CPA, JD Tax Partner February 2019 DISCLAIMER: This presentation and its content do not constitute advice. Attendants should not act solely

Treasury Releases Proposed Regulations on Tax Incentives for Investment in Designated Zones

October 2018 OPPORTUNITY ZONES Treasury Releases Proposed Regulations on Tax Incentives for Investment in Designated Zones On Friday, October 19, 2018, Treasury issued much-anticipated guidance in the

October 2018 OPPORTUNITY ZONES Treasury Releases Proposed Regulations on Tax Incentives for Investment in Designated Zones On Friday, October 19, 2018, Treasury issued much-anticipated guidance in the

Overview Snell & Wilmer

Overview History of Opportunity Zone Program Opportunity Zones Qualification and Designation Tax Benefits of the Opportunity Zone Program Opportunity Funds What are the rules, how do you qualify? Opportunity

Overview History of Opportunity Zone Program Opportunity Zones Qualification and Designation Tax Benefits of the Opportunity Zone Program Opportunity Funds What are the rules, how do you qualify? Opportunity

K E Y N O T E S P E A K E R S

K E Y N O T E S P E A K E R S R o b e r t W i e b e, C P A Ro b e r t W @ w h h c p a s. c o m B e n H u b b e ll, C P A Be n H @ w h h c p a s. c o m 2 P R E S E N T A T I O N O U T L I N E 1. History

K E Y N O T E S P E A K E R S R o b e r t W i e b e, C P A Ro b e r t W @ w h h c p a s. c o m B e n H u b b e ll, C P A Be n H @ w h h c p a s. c o m 2 P R E S E N T A T I O N O U T L I N E 1. History

The Eagerly Awaited Opportunity Zone Regulations: What Do They Tell Us and What Do We Still Need to Figure Out?

The Eagerly Awaited Opportunity Zone Regulations: What Do They Tell Us and What Do We Still Need to Figure Out? Lisa M. Starczewski, Esq. Co-Chair, Tax Section & Opportunity Zones Team Buchanan Ingersoll

The Eagerly Awaited Opportunity Zone Regulations: What Do They Tell Us and What Do We Still Need to Figure Out? Lisa M. Starczewski, Esq. Co-Chair, Tax Section & Opportunity Zones Team Buchanan Ingersoll

OPPORTUNITY ZONES GAIN DEFERRAL AND ELIMINATION ADAM M. COHEN

OPPORTUNITY ZONES GAIN DEFERRAL AND ELIMINATION ADAM M. COHEN COLORADO OPPORTUNITY ZONES 2 OPPORTUNITY ZONE BENEFITS 1. Initial Gain Deferral 2. Initial Gain Reduction 3. O-Zone Gain Elimination 3 GAIN

OPPORTUNITY ZONES GAIN DEFERRAL AND ELIMINATION ADAM M. COHEN COLORADO OPPORTUNITY ZONES 2 OPPORTUNITY ZONE BENEFITS 1. Initial Gain Deferral 2. Initial Gain Reduction 3. O-Zone Gain Elimination 3 GAIN

Real Estate Journal TM

Real Estate Journal TM Reproduced with permission from, V. 34, 11, p. 214, 11/07/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com The Eagerly Awaited Opportunity

Real Estate Journal TM Reproduced with permission from, V. 34, 11, p. 214, 11/07/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com The Eagerly Awaited Opportunity

Investing in Opportunity Zones

Investing in Opportunity Zones for the 2018 Defense Communities National Summit Gregory Clements Partner, Dover Novogradac & Company LLP gregory.clements@novoco.com Taxpayers can get capital gains tax

Investing in Opportunity Zones for the 2018 Defense Communities National Summit Gregory Clements Partner, Dover Novogradac & Company LLP gregory.clements@novoco.com Taxpayers can get capital gains tax

National Housing & Rehabilitation Association Spring Developers Forum

National Housing & Rehabilitation Association Spring Developers Forum May 7-8, 2018 Marina del Rey, CA Sponsors: Leveraging Qualified Opportunity Zones: Development & Finance Strategies Laura Burns Eagle

National Housing & Rehabilitation Association Spring Developers Forum May 7-8, 2018 Marina del Rey, CA Sponsors: Leveraging Qualified Opportunity Zones: Development & Finance Strategies Laura Burns Eagle

Investing in Opportunity Act

Investing in Opportunity Act MODERATOR John Sciarretti Novogradac & Company LLP PANELISTS Joseph Bredehoft Husch Blackwell Jonathan Goldstein Advantage Capital Neil Faden Manatt, Phelps & Phillips LLP

Investing in Opportunity Act MODERATOR John Sciarretti Novogradac & Company LLP PANELISTS Joseph Bredehoft Husch Blackwell Jonathan Goldstein Advantage Capital Neil Faden Manatt, Phelps & Phillips LLP

ANALYSIS OF QUALIFIED OPPORTUNITY ZONES

March 15, 2018 Updated May 10, 2018 ANALYSIS OF QUALIFIED OPPORTUNITY ZONES This document provides a detailed analysis of the newly created tax incentives for investments in Qualified Opportunity Zones

March 15, 2018 Updated May 10, 2018 ANALYSIS OF QUALIFIED OPPORTUNITY ZONES This document provides a detailed analysis of the newly created tax incentives for investments in Qualified Opportunity Zones

Guidance on Opportunity Zone Structuring & Capital Gain Deferral DECEMBER 12, 2018

Guidance on Opportunity Zone Structuring & Capital Gain Deferral DECEMBER 12, 2018 New IRC 1400Z-1 & 2 The new IRC 1400Z-1 & -2 establish an entirely novel & completely different regimen for deferring

Guidance on Opportunity Zone Structuring & Capital Gain Deferral DECEMBER 12, 2018 New IRC 1400Z-1 & 2 The new IRC 1400Z-1 & -2 establish an entirely novel & completely different regimen for deferring

Investment in Federal Opportunity Zones

Investment in Federal Opportunity Zones Opportunity Zones Overview What is the basic concept behind the legislation? A new community development program established by Congress that encourages long-term

Investment in Federal Opportunity Zones Opportunity Zones Overview What is the basic concept behind the legislation? A new community development program established by Congress that encourages long-term

Qualified Opportunity Zone Funds Structuring and Implementing Tax-Advantaged Fund Transactions February 26, 2019

Qualified Opportunity Zone Funds Structuring and Implementing Tax-Advantaged Fund Transactions February 26, 2019 John Schrier 646.971.5554 john.schrier@sscinc.com Mark Leeds 212.506.2499 mleeds@mayerbrown.com

Qualified Opportunity Zone Funds Structuring and Implementing Tax-Advantaged Fund Transactions February 26, 2019 John Schrier 646.971.5554 john.schrier@sscinc.com Mark Leeds 212.506.2499 mleeds@mayerbrown.com

INSIGHT: The Eagerly Awaited Opportunity Zone Regulations: What Do They Tell Us and What Do We Still Need to Figure Out?

bloombergbna.com Reproduced with permission. Published October 23, 2018. Copyright 2018 The Bureau of National Affairs, Inc. 800-372-1033. For further use, please visit http://www.bna.com/copyright-permission-request/

bloombergbna.com Reproduced with permission. Published October 23, 2018. Copyright 2018 The Bureau of National Affairs, Inc. 800-372-1033. For further use, please visit http://www.bna.com/copyright-permission-request/

1. Where are Opportunity Zones (OZs) in California?

in California?") An Overview 1 1. Where are Opportunity Zones (OZs) in California? Opportunity Zones provide a new tool for investors, fund managers and communities by utilizing privately sourced funds into eligible economic

An Overview 1 1. Where are Opportunity Zones (OZs) in California? Opportunity Zones provide a new tool for investors, fund managers and communities by utilizing privately sourced funds into eligible economic

Qualified Opportunity Zone Businesses

Qualified Opportunity Zone Businesses PANELISTS Annette Stevenson Novogradac & Company LLP Glenn A. Graff Applegate & Thorne-Thomsen, P.C. Jay Darby Sullivan & Worcester LLP Kelly Longwell Coats Rose Greg

Qualified Opportunity Zone Businesses PANELISTS Annette Stevenson Novogradac & Company LLP Glenn A. Graff Applegate & Thorne-Thomsen, P.C. Jay Darby Sullivan & Worcester LLP Kelly Longwell Coats Rose Greg

Critical New Insights on Proposed Opportunity Zone Regulations NOVEMBER 7, 2018

Critical New Insights on Proposed Opportunity Zone Regulations NOVEMBER 7, 2018 To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

Critical New Insights on Proposed Opportunity Zone Regulations NOVEMBER 7, 2018 To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

Opportunity Zones Tax incentives for investing in low-income communities

Opportunity Zones Tax incentives for investing in low-income communities Overview > Established by Tax Cut and Jobs Act of 2017 > 8,700 zones in the US (11% of the country) > Only capital gains can be

Opportunity Zones Tax incentives for investing in low-income communities Overview > Established by Tax Cut and Jobs Act of 2017 > 8,700 zones in the US (11% of the country) > Only capital gains can be

A PRIMER ON THE NEW FEDERAL QUALIFIED OPPORTUNITY ZONE PROVISIONS*

A PRIMER ON THE NEW FEDERAL QUALIFIED OPPORTUNITY ZONE PROVISIONS* By: Alveno N. Castilla and Ashley N. Wicks** Background For many years, the Internal Revenue Code has provided various incentives aimed

A PRIMER ON THE NEW FEDERAL QUALIFIED OPPORTUNITY ZONE PROVISIONS* By: Alveno N. Castilla and Ashley N. Wicks** Background For many years, the Internal Revenue Code has provided various incentives aimed

October 31, Summary of Opportunity Zone Proposed Regulations. Table of Contents

Schuyler M. Moore D: 310.201.7559 F: 310.201.4444 SMoore@ggfirm.com October 31, 2018 To Colleagues, Friends, and Clients: Re: Summary of Opportunity Zone Proposed Regulations This letter provides a summary

Schuyler M. Moore D: 310.201.7559 F: 310.201.4444 SMoore@ggfirm.com October 31, 2018 To Colleagues, Friends, and Clients: Re: Summary of Opportunity Zone Proposed Regulations This letter provides a summary

Opportunity Zones. US Federal Tax Rules CPA María de los A. Rivera

The Puerto Rico Chamber of Commerce and the Puerto Rico Builders Association present What are they, how do they work and what are the opportunities? US Federal Tax Rules CPA María de los A. Rivera #tucamaraena

The Puerto Rico Chamber of Commerce and the Puerto Rico Builders Association present What are they, how do they work and what are the opportunities? US Federal Tax Rules CPA María de los A. Rivera #tucamaraena

IRS Publishes Opportunity Zone Proposed Regulations: The First Important Step in the Structuring of OZ Funds

Qualified Opportunity Zone Funds OCTOBER 2018 NO. 2 IRS Publishes Opportunity Zone Proposed Regulations: The First Important Step in the Structuring of OZ Funds As part of the Tax Cuts and Jobs Act (the

Qualified Opportunity Zone Funds OCTOBER 2018 NO. 2 IRS Publishes Opportunity Zone Proposed Regulations: The First Important Step in the Structuring of OZ Funds As part of the Tax Cuts and Jobs Act (the

Opportunity Zone Program Tax Cuts and Jobs Act

Opportunity Zone Program Tax Cuts and Jobs Act Marc L. Schultz (602) 382-6358 mschultz@swlaw.com Jason Brinkley (303) 634-2066 jbrinkley@swlaw.com Nicole Ament (303) 223-1174 nament@bhfs.com 1 Overview

Opportunity Zone Program Tax Cuts and Jobs Act Marc L. Schultz (602) 382-6358 mschultz@swlaw.com Jason Brinkley (303) 634-2066 jbrinkley@swlaw.com Nicole Ament (303) 223-1174 nament@bhfs.com 1 Overview

OPPORTUNITY ZONES: MORE THAN A PRIMER

OPPORTUNITY ZONES: MORE THAN A PRIMER Presented to: National Multifamily Housing Council September 13, 2018 CohnReznick LLP OPPORTUNITY ZONES: MORE THAN A PRIMER Steven M. Friedman steve.friedman@cohnreznick.com

OPPORTUNITY ZONES: MORE THAN A PRIMER Presented to: National Multifamily Housing Council September 13, 2018 CohnReznick LLP OPPORTUNITY ZONES: MORE THAN A PRIMER Steven M. Friedman steve.friedman@cohnreznick.com

IRC 199A Deduction for Qualified Business Income

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

The Opportunity in Opportunity Zones

The Opportunity in Opportunity Zones Alex Flachsbart 7.10.2018 aflachsbart@balch.com Presentation Roadmap Program History and Zone Selection How the Program Works Basics of the OZ Incentive Definitions

The Opportunity in Opportunity Zones Alex Flachsbart 7.10.2018 aflachsbart@balch.com Presentation Roadmap Program History and Zone Selection How the Program Works Basics of the OZ Incentive Definitions

Opportunity Zone Basics CDBA Peer Forum and Membership Meeting June 6, 2018

Opportunity Zone Basics 2018 CDBA Peer Forum and Membership Meeting June 6, 2018 The Objective 2 To get investors to invest in low income communities In general, Opportunity Zones are 25% (or 25, if more)

Opportunity Zone Basics 2018 CDBA Peer Forum and Membership Meeting June 6, 2018 The Objective 2 To get investors to invest in low income communities In general, Opportunity Zones are 25% (or 25, if more)

Opportunity Zones Overview: Basics and Concepts

Opportunity Zones Overview: Basics and Concepts Ryan Brunton Husch Blackwell LLP ryan.brunton@huschblackwell.com RJ McArthur Plante Moran RJ.McArthur@plantemoran.com Benefits of the Opportunity Zone Incentive

Opportunity Zones Overview: Basics and Concepts Ryan Brunton Husch Blackwell LLP ryan.brunton@huschblackwell.com RJ McArthur Plante Moran RJ.McArthur@plantemoran.com Benefits of the Opportunity Zone Incentive

Opportunity Zones: The Latest

Opportunity Zones: The Latest November 15, 2018 National Development Council 2 Agenda Why invest in an Opportunity Zone fund? How did Opportunity Zones come to be? Steps in the Opportunity Zone Process

Opportunity Zones: The Latest November 15, 2018 National Development Council 2 Agenda Why invest in an Opportunity Zone fund? How did Opportunity Zones come to be? Steps in the Opportunity Zone Process

Tax Incentives for Investments in Opportunity Zones: New Regulations Provide Clarity and More Questions

Tax Incentives for Investments in Opportunity Zones: New Regulations Provide Clarity and More Questions October 30, 2018 The 2017 Federal Tax Reform bill enacted a new set of tax incentives for investments

Tax Incentives for Investments in Opportunity Zones: New Regulations Provide Clarity and More Questions October 30, 2018 The 2017 Federal Tax Reform bill enacted a new set of tax incentives for investments

The IRS Issues First Batch of Proposed Opportunity Fund Regulations

The IRS Issues First Batch of Proposed Opportunity Fund Regulations TAX IRS PROPOSED OPPORTUNITY FUND REGULATIONS The IRS Issues First Batch of Proposed Opportunity Fund Regulations The Internal Revenue

The IRS Issues First Batch of Proposed Opportunity Fund Regulations TAX IRS PROPOSED OPPORTUNITY FUND REGULATIONS The IRS Issues First Batch of Proposed Opportunity Fund Regulations The Internal Revenue

Opportunity Zones Investments in Operating Businesses

Opportunity Zones Investments in Operating Businesses PANELISTS Michael Kressig Novogradac & Company LLP Chris Schultz Launch Pad Rick Holliday Factory OS Jonathan Goldstein Advantage Capital Operating

Opportunity Zones Investments in Operating Businesses PANELISTS Michael Kressig Novogradac & Company LLP Chris Schultz Launch Pad Rick Holliday Factory OS Jonathan Goldstein Advantage Capital Operating

ARIZONA COMMERCE AUTHORITY OPPORTUNITY FUNDS GUIDANCE UPDATE

ARIZONA COMMERCE AUTHORITY OPPORTUNITY FUNDS GUIDANCE UPDATE ACA MISSION The mission of the Arizona Commerce Authority is to grow and strengthen Arizona s economy and facilitate the creation of quality

ARIZONA COMMERCE AUTHORITY OPPORTUNITY FUNDS GUIDANCE UPDATE ACA MISSION The mission of the Arizona Commerce Authority is to grow and strengthen Arizona s economy and facilitate the creation of quality

QUALIFIED OPPORTUNITY ZONES AN INTRODUCTION TO A NEW TAX INCENTIVE FOR INVESTORS

QUALIFIED OPPORTUNITY ZONES AN INTRODUCTION TO A NEW TAX INCENTIVE FOR INVESTORS Vance Maultsby, CPA Huselton, Morgan & Maultsby, P.C. October 25, 2018 Traverse City, Michigan 1 EXTERNAL DISCLAIMER This

QUALIFIED OPPORTUNITY ZONES AN INTRODUCTION TO A NEW TAX INCENTIVE FOR INVESTORS Vance Maultsby, CPA Huselton, Morgan & Maultsby, P.C. October 25, 2018 Traverse City, Michigan 1 EXTERNAL DISCLAIMER This

First round of proposed regulations issued for opportunity zones

First round of proposed regulations issued for opportunity zones A trending aspect of the Tax Cuts and Jobs Act (TCJA) is the creation of a new incentive, Opportunity zones, intended to direct new investments

First round of proposed regulations issued for opportunity zones A trending aspect of the Tax Cuts and Jobs Act (TCJA) is the creation of a new incentive, Opportunity zones, intended to direct new investments

Welcome to the Land of OZ: A Basic Overview of the Opportunity Zones Incentive

Welcome to the Land of OZ: A Basic Overview of the Opportunity Zones Incentive MODERATOR Brent Parker Novogradac & Company LLP PANELISTS Catalina Vielma Boston Financial Investment Management Tony Alfieri

Welcome to the Land of OZ: A Basic Overview of the Opportunity Zones Incentive MODERATOR Brent Parker Novogradac & Company LLP PANELISTS Catalina Vielma Boston Financial Investment Management Tony Alfieri

Understanding the benefits and challenges of Opportunity Zones

Understanding the benefits and challenges of Opportunity Zones Tuesday, Nov. 27, 2018 2:00-3:00 pm ET We will be starting soon Please disable pop-up blocking software before viewing this webcast Speakers

Understanding the benefits and challenges of Opportunity Zones Tuesday, Nov. 27, 2018 2:00-3:00 pm ET We will be starting soon Please disable pop-up blocking software before viewing this webcast Speakers

IRS Issues Proposed Regulations on Qualified Opportunity Funds

IRS Issues Proposed Regulations on Qualified Opportunity Funds Proposed Regulations Would Clarify a Number of Threshold Issues But Also Leave Many Other Issues to be Resolved by Future Guidance SUMMARY

IRS Issues Proposed Regulations on Qualified Opportunity Funds Proposed Regulations Would Clarify a Number of Threshold Issues But Also Leave Many Other Issues to be Resolved by Future Guidance SUMMARY

Opportunity Zone Funds Offer New Tax Incentive for Long-Term Investment in Low-Income Communities

08 / 01 / 18 If you have any questions regarding the matters discussed in this memorandum, please contact the attorneys listed on the last page or call your regular Skadden contact. The Tax Cuts and Jobs

08 / 01 / 18 If you have any questions regarding the matters discussed in this memorandum, please contact the attorneys listed on the last page or call your regular Skadden contact. The Tax Cuts and Jobs

Opportunity Zones. for Real Estate Investors. Michael Lortz, CPA, LEED AP (503)

") Opportunity Zones for Real Estate Investors Michael Lortz, CPA, LEED AP (503) 221 0141 mlortz@gmco.com March 6, 2019 Disclaimer The purpose of this presentation is to provide information, rather than advice

Opportunity Zones for Real Estate Investors Michael Lortz, CPA, LEED AP (503) 221 0141 mlortz@gmco.com March 6, 2019 Disclaimer The purpose of this presentation is to provide information, rather than advice

th St. NW, Suite Washington, DC

Summary of the U.S. Treasury and Internal Revenue Service s guidance for investing in Opportunity Zones This is the first of several proposed federal regulations and guidance documents to be released before

Summary of the U.S. Treasury and Internal Revenue Service s guidance for investing in Opportunity Zones This is the first of several proposed federal regulations and guidance documents to be released before

Qualified Opportunity Zones

Qualified Opportunity Zones 2018 OCAH Affordable Housing Conference August 22, 2018 Presented by: Nancy Morton, CPA Justin D. Rumer, JD Cheryl Denney Dauby O Connor & Zaleski, LLC McAfee & Taft 501 Congressional

Qualified Opportunity Zones 2018 OCAH Affordable Housing Conference August 22, 2018 Presented by: Nancy Morton, CPA Justin D. Rumer, JD Cheryl Denney Dauby O Connor & Zaleski, LLC McAfee & Taft 501 Congressional

2018 Income Tax Update - Commercial Real Estate

2018 Income Tax Update - Commercial Real Estate Stephen M. Lukinovich, CPA, PFS, CVA Andrew J. Ackermann, CPA, CVA Kentucky Commercial Real Estate Conference Louisville, KY October 30, 2018 Tax Cuts and

2018 Income Tax Update - Commercial Real Estate Stephen M. Lukinovich, CPA, PFS, CVA Andrew J. Ackermann, CPA, CVA Kentucky Commercial Real Estate Conference Louisville, KY October 30, 2018 Tax Cuts and

Recent Developments & Observations

ADAM M. COHEN is a Partner with Holland & Hart LLP in Denver, Colorado. SARAH RITCHEY HARADON is an Associate with Holland & Hart LLP in Denver, Colorado. Recent Developments & Observations Qualified Opportunity

ADAM M. COHEN is a Partner with Holland & Hart LLP in Denver, Colorado. SARAH RITCHEY HARADON is an Associate with Holland & Hart LLP in Denver, Colorado. Recent Developments & Observations Qualified Opportunity

Qualified Opportunity Zones

Qualified Opportunity Zones Welcome and Introductions Molly R. Bryson, Partner 202.661.7638 brysonm@ballardspahr.com Wendi L. Kotzen, Partner 215.864.8305 kotzenw@ballardspahr.com Douglas M. Fox, Partner

Qualified Opportunity Zones Welcome and Introductions Molly R. Bryson, Partner 202.661.7638 brysonm@ballardspahr.com Wendi L. Kotzen, Partner 215.864.8305 kotzenw@ballardspahr.com Douglas M. Fox, Partner

Client Alert October 30, 2018

Tax News and Developments North America Client Alert October 30, 2018 New IRS Guidance Opens Door to Use of Qualified Opportunity Zones Tax reform introduced significant tax incentives for investments

Tax News and Developments North America Client Alert October 30, 2018 New IRS Guidance Opens Door to Use of Qualified Opportunity Zones Tax reform introduced significant tax incentives for investments

ARIZONA OPPORTUNITY ZONES

July 18, 2018 ARIZONA OPPORTUNITY ZONES ARIZONA COMMERCE AUTHORITY OPPORTUNITY ZONES-WHAT ARE THEY? A mechanism to convert passive investment dollars into active investment dollars in underserved areas

July 18, 2018 ARIZONA OPPORTUNITY ZONES ARIZONA COMMERCE AUTHORITY OPPORTUNITY ZONES-WHAT ARE THEY? A mechanism to convert passive investment dollars into active investment dollars in underserved areas

Opportunity Zones Program: Qualified Funds and Related Tax Incentives

Opportunity Zones Program: Qualified Funds and Related Tax Incentives Kyla M. Ehrisman, JD, MBA Alan Lincoln, MBA, CCIM Mick Law P.C. LLO August 17, 2018 The Opportunity Zones Program was created as part

Opportunity Zones Program: Qualified Funds and Related Tax Incentives Kyla M. Ehrisman, JD, MBA Alan Lincoln, MBA, CCIM Mick Law P.C. LLO August 17, 2018 The Opportunity Zones Program was created as part

Opportunity Zones: A Preliminary Examination

Opportunity Zones: A Preliminary Examination MAY 2018 The Tax Cuts and Jobs Act of 2017 (the Act ) made significant changes to U.S. federal tax law. One of these changes was the establishment of a new

Opportunity Zones: A Preliminary Examination MAY 2018 The Tax Cuts and Jobs Act of 2017 (the Act ) made significant changes to U.S. federal tax law. One of these changes was the establishment of a new

Opportunity Zones. How to capitalize the funds and get OZ equity into a project

Opportunity Zones How to capitalize the funds and get OZ equity into a project CONNECT WITH US Presenter Michael Ross President, Principal +1 (512) 975 7290 michael.ross@bakertilly.com Michael Ross, president

Opportunity Zones How to capitalize the funds and get OZ equity into a project CONNECT WITH US Presenter Michael Ross President, Principal +1 (512) 975 7290 michael.ross@bakertilly.com Michael Ross, president

Real estate markets. Opportunity knocks in tax-advantaged Opportunity Zones in the US

Opportunity knocks in tax-advantaged Opportunity Zones in the US Chief Investment Office Americas, Wealth Management 18 May 2018 3:31 pm BST Jonathan Woloshin, CFA, Head Americas Equities, jonathan.woloshin@ubs.com;

Opportunity knocks in tax-advantaged Opportunity Zones in the US Chief Investment Office Americas, Wealth Management 18 May 2018 3:31 pm BST Jonathan Woloshin, CFA, Head Americas Equities, jonathan.woloshin@ubs.com;

QUALIFIED OPPORTUNITY ZONES WHAT EVERY TRUSTS AND ESTATES LAWYER SHOULD KNOW

QUALIFIED OPPORTUNITY ZONES WHAT EVERY TRUSTS AND ESTATES LAWYER SHOULD KNOW Knoxville Estate Planning Council January 17, 2019 Presented by: Michael L. Duffy Director; Strategic Wealth Advisory Group

QUALIFIED OPPORTUNITY ZONES WHAT EVERY TRUSTS AND ESTATES LAWYER SHOULD KNOW Knoxville Estate Planning Council January 17, 2019 Presented by: Michael L. Duffy Director; Strategic Wealth Advisory Group

International Economic Development Council Webinar. Opportunity Zones 201

International Economic Development Council Webinar Opportunity Zones 201 THE PATH TO PASSAGE Washington Can Work The Tax Cuts and Jobs Act (H.R. 1) was signed into law by President Trump on December 22,

International Economic Development Council Webinar Opportunity Zones 201 THE PATH TO PASSAGE Washington Can Work The Tax Cuts and Jobs Act (H.R. 1) was signed into law by President Trump on December 22,

Opportunity Zones Webinar Q&A

From a webinar hosted by CCC on June 19, 2018 Disclaimer: The responses to the Q&A do not constitute investment advice and do not purport to identify all risks or material considerations which should be

From a webinar hosted by CCC on June 19, 2018 Disclaimer: The responses to the Q&A do not constitute investment advice and do not purport to identify all risks or material considerations which should be

Lowell and Lawrence, Massachusetts Renewal Communities Incentives

Lowell and Lawrence, Massachusetts Renewal Communities Incentives An Initiative of the U. S. Department of Housing and Urban Development based on tax incentives authorized by the Community Renewal Tax

Lowell and Lawrence, Massachusetts Renewal Communities Incentives An Initiative of the U. S. Department of Housing and Urban Development based on tax incentives authorized by the Community Renewal Tax

March 9, RE Recommendations for Guidance on Opportunity Zones. Dear Mr. Dinwiddie:

March 9, 2018 Mr. Scott Dinwiddie Associate Chief Counsel Income Tax & Accounting Internal Revenue Service 1111 Constitution Avenue, NW Washington, DC 20224 RE s for Guidance on Opportunity Zones Dear

March 9, 2018 Mr. Scott Dinwiddie Associate Chief Counsel Income Tax & Accounting Internal Revenue Service 1111 Constitution Avenue, NW Washington, DC 20224 RE s for Guidance on Opportunity Zones Dear

Opportunity Zones & Funds

Opportunity Zones & Funds Presented by: Paul Speyer January 3, 2019 Overview of Opportunity Zones & Funds Set up as part of the Tax Cuts and Jobs Act of 2017 Program was established as a way to motivate

Opportunity Zones & Funds Presented by: Paul Speyer January 3, 2019 Overview of Opportunity Zones & Funds Set up as part of the Tax Cuts and Jobs Act of 2017 Program was established as a way to motivate

The 2017 Tax Reform Act: What Lawyers Should Know

The 2017 Tax Reform Act: What Lawyers Should Know Mark E. Gingrich, CPA, J.D. Tax Member Chris J. Harris, CPA, J.D. Tax Senior I Agenda I. 20% deduction under Sec. 199A II. Depreciation / like-kind exchange

The 2017 Tax Reform Act: What Lawyers Should Know Mark E. Gingrich, CPA, J.D. Tax Member Chris J. Harris, CPA, J.D. Tax Senior I Agenda I. 20% deduction under Sec. 199A II. Depreciation / like-kind exchange

Opportunity Zones offer new tax incentives. What you need to know about Opportunity Zones

offer new tax incentives What you need to know about Opportunity Zones Danny McKeithen, Partner Rebecca Stork, Associate 2018 (US) LLP All Rights Reserved. This communication is for general informational

offer new tax incentives What you need to know about Opportunity Zones Danny McKeithen, Partner Rebecca Stork, Associate 2018 (US) LLP All Rights Reserved. This communication is for general informational

ACTION: Notice of proposed rulemaking and notice of public hearing. SUMMARY: This document contains proposed regulations that provide guidance under

This document has been submitted to the Office of the Federal Register (OFR) for publication and is currently pending placement on public display at the OFR and publication in the Federal Register. The

This document has been submitted to the Office of the Federal Register (OFR) for publication and is currently pending placement on public display at the OFR and publication in the Federal Register. The

Treasury Regs. DATES: Written (including electronic) comments must be received by [INSERT DATE 60 DAYS AFTER DATE

comments must be received by [INSERT DATE 60 DAYS AFTER DATE") Treasury Regs [4830-01-p] DEPARTMENT OF TREASURY Internal Revenue Service 26 CFR Part I [REG-115420-18] RIN 1545-BP03 Investing in Qualified Opportunity Funds AGENCY: Internal Revenue Service (IRS), Treasury.

Treasury Regs [4830-01-p] DEPARTMENT OF TREASURY Internal Revenue Service 26 CFR Part I [REG-115420-18] RIN 1545-BP03 Investing in Qualified Opportunity Funds AGENCY: Internal Revenue Service (IRS), Treasury.

Introduction and Background

IRS REG 115420-18 Comments by Girard Miller, a Laguna Niguel, CA angel investor, regarding Opportunity Zones for startup businesses, and angel/venture investment groups November 19, 2018 Executive Summary:

IRS REG 115420-18 Comments by Girard Miller, a Laguna Niguel, CA angel investor, regarding Opportunity Zones for startup businesses, and angel/venture investment groups November 19, 2018 Executive Summary:

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Qualified Opportunity Zones and Tax Credits: Capital Gain Deferral Mechanisms Under New Section 1400Z IRC 45D(e) Requirements, Step-Up in Basis,

Presenting a live 90-minute webinar with interactive Q&A Qualified Opportunity Zones and Tax Credits: Capital Gain Deferral Mechanisms Under New Section 1400Z IRC 45D(e) Requirements, Step-Up in Basis,

U. S. Dept. of Housing and Urban Development & The Internal Revenue Service

Tax Incentives for Community Renewal Webcast U. S. Dept. of Housing and Urban Development & The Internal Revenue Service 1 EZ Designation Extension EZ/RC Locator Employment Credits Work Opportunity Tax

Tax Incentives for Community Renewal Webcast U. S. Dept. of Housing and Urban Development & The Internal Revenue Service 1 EZ Designation Extension EZ/RC Locator Employment Credits Work Opportunity Tax

Opportunity Zone Proposed Regulations Provide the Certainty Anxious Investors, Developers, and Entrepreneurs Have Been Seeking

23 October 2018 Practice Groups: Public Policy and Law Tax Real Estate Investment Management Opportunity Zone Proposed Regulations Provide the Certainty Anxious Investors, Developers, and Entrepreneurs

23 October 2018 Practice Groups: Public Policy and Law Tax Real Estate Investment Management Opportunity Zone Proposed Regulations Provide the Certainty Anxious Investors, Developers, and Entrepreneurs

Opportunity Zones: Tax Benefits & Issues. Presented by:

Opportunity Zones: Tax Benefits & Issues Presented by: Doug Garner, CPA - Tax Manager Rick Westerfield, CPA - Tax Shareholder Xin Xin, CPA - Tax Shareholder 2 Opportunity Zones: Purpose The Internal Revenue

Opportunity Zones: Tax Benefits & Issues Presented by: Doug Garner, CPA - Tax Manager Rick Westerfield, CPA - Tax Shareholder Xin Xin, CPA - Tax Shareholder 2 Opportunity Zones: Purpose The Internal Revenue

Federal Register / Vol. 83, No. 209 / Monday, October 29, 2018 / Proposed

Federal Register / Vol. 83, No. 209 / Monday, October 29, 2018 / Proposed Rules 54279 FAA has issued an advisory notice to airmen (NOTAM KICZ A0031/17) advising U.S. operators in Afghanistan airspace to

Federal Register / Vol. 83, No. 209 / Monday, October 29, 2018 / Proposed Rules 54279 FAA has issued an advisory notice to airmen (NOTAM KICZ A0031/17) advising U.S. operators in Afghanistan airspace to

Combining Opportunity Zones with Tax Credits

Combining Opportunity Zones with Tax Credits MODERATOR Nicolo Pinoli Novogradac & Company LLP PANELISTS Fred Copeman Boston Financial Investment Management, LP Craig Nolte Federal Reserve Bank Of San Francisco

Combining Opportunity Zones with Tax Credits MODERATOR Nicolo Pinoli Novogradac & Company LLP PANELISTS Fred Copeman Boston Financial Investment Management, LP Craig Nolte Federal Reserve Bank Of San Francisco

September 12, Opportunity Zone Overview. Qualified Opportunity Fund Benefits

September 12, 2018 Opportunity Zone Overview The Tax Cuts and Jobs Act established new Internal Revenue Code Sections 1400Z-1 and 1400Z-2, providing special tax benefits for Opportunity Zones. These sections

September 12, 2018 Opportunity Zone Overview The Tax Cuts and Jobs Act established new Internal Revenue Code Sections 1400Z-1 and 1400Z-2, providing special tax benefits for Opportunity Zones. These sections

Window of Opportunity: The IRS Issues Initial Guidance on Qualified Opportunity Zone Rules

Article Window of Opportunity: The IRS Issues Initial Guidance on Qualified Opportunity Zone Rules By David Burton, Mark Leeds, Zal Kumar and Maria Carolina Grecco 1 It is extremely rare that a section

Article Window of Opportunity: The IRS Issues Initial Guidance on Qualified Opportunity Zone Rules By David Burton, Mark Leeds, Zal Kumar and Maria Carolina Grecco 1 It is extremely rare that a section

Gain Deferral Using Qualified Opportunity Zone Investment Strategies

Legal Update August 2, 2018 Gain Deferral Using Qualified Opportunity Zone Investment Strategies This Legal Update provides an overview of the Qualified Opportunity Zone rules. 1 These rules provide for

Legal Update August 2, 2018 Gain Deferral Using Qualified Opportunity Zone Investment Strategies This Legal Update provides an overview of the Qualified Opportunity Zone rules. 1 These rules provide for

Opportunity Zones. Unlock new opportunities. November kpmg.com

Opportunity Zones Unlock new opportunities November 2018 kpmg.com Contents Executive summary 2 About the authors 4 Do well, do good 5 What is a Qualified Opportunity Zone? 6 The potential tax benefits

Opportunity Zones Unlock new opportunities November 2018 kpmg.com Contents Executive summary 2 About the authors 4 Do well, do good 5 What is a Qualified Opportunity Zone? 6 The potential tax benefits

Real Estate Journal TM

Real Estate Journal TM Reproduced with permission from, Vol. 34 No. 11, 11/07/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com IRS Guidance Permits Opportunity

Real Estate Journal TM Reproduced with permission from, Vol. 34 No. 11, 11/07/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com IRS Guidance Permits Opportunity

November 26, Dear Mr. Dinwiddie:

November 26, 2018 Mr. Scott Dinwiddie Associate Chief Counsel Income Tax & Accounting CC:PA:LPD:PR (REG-115420-18), room 5203, Internal Revenue Service, PO Box 7604, Ben Franklin Station, Washington, DC

November 26, 2018 Mr. Scott Dinwiddie Associate Chief Counsel Income Tax & Accounting CC:PA:LPD:PR (REG-115420-18), room 5203, Internal Revenue Service, PO Box 7604, Ben Franklin Station, Washington, DC

Tax Credits for Small Wineries. Winery and Wine Distribution Law

Tax Credits for Small Wineries Winery and Wine Distribution Law Marc R. Greenough Foster Pepper PLLC Quincy, Washington August 5, 2008 Tax Credits for Small Wineries Under the Internal Revenue Code of

Tax Credits for Small Wineries Winery and Wine Distribution Law Marc R. Greenough Foster Pepper PLLC Quincy, Washington August 5, 2008 Tax Credits for Small Wineries Under the Internal Revenue Code of

WHAT ARE OPPORTUNITY ZONES?

WHAT ARE OPPORTUNITY ZONES? Low-income, distressed census tracts where investors can receive significant tax breaks and deferrals for investments Can be used for a variety of economic development projects

WHAT ARE OPPORTUNITY ZONES? Low-income, distressed census tracts where investors can receive significant tax breaks and deferrals for investments Can be used for a variety of economic development projects

IMPACT OF THE NEW TAX LAW ON BUSINESS STRUCTURING

IMPACT OF THE NEW TAX LAW ON BUSINESS STRUCTURING Disclaimer This whitepaper is for informational purposes only and not intended as substitute for professional advice. Every situation is different. Please

IMPACT OF THE NEW TAX LAW ON BUSINESS STRUCTURING Disclaimer This whitepaper is for informational purposes only and not intended as substitute for professional advice. Every situation is different. Please

WHAT ARE OPPORTUNITY ZONES?

WHAT ARE OPPORTUNITY ZONES? Low-income, distressed census tracts where investors can receive significant tax breaks and deferrals for investments Can be used for a variety of economic development projects

WHAT ARE OPPORTUNITY ZONES? Low-income, distressed census tracts where investors can receive significant tax breaks and deferrals for investments Can be used for a variety of economic development projects

145 Qualified Opportunity Zones and Treatment of Capital Gain Reinvested in Qualified Opportunity Zones

145 Qualified Opportunity Zones and Treatment of Capital Gain Reinvested in Qualified Opportunity Zones NEW LAW EXPLAINED Creation of qualified opportunity zones. A population census tract that is a low-income

145 Qualified Opportunity Zones and Treatment of Capital Gain Reinvested in Qualified Opportunity Zones NEW LAW EXPLAINED Creation of qualified opportunity zones. A population census tract that is a low-income

Community Development Financial Institutions. Fund

equality U.S. Department of the Treasury equality INVESTMENT Community Development Financial Institutions invest neighborhood Fund New Markets Tax Credits: 2003 Allocation Application CDFI Fund Mission

equality U.S. Department of the Treasury equality INVESTMENT Community Development Financial Institutions invest neighborhood Fund New Markets Tax Credits: 2003 Allocation Application CDFI Fund Mission

Don t Let 2018 Be Taxing:

Don t Let 2018 Be Taxing: How Changes to the Tax Laws Change How We Counsel Businesses March 15, 2018 Agenda Introduction C corporation overview Pass-through overview Comparison 2 Introduction Types of

Don t Let 2018 Be Taxing: How Changes to the Tax Laws Change How We Counsel Businesses March 15, 2018 Agenda Introduction C corporation overview Pass-through overview Comparison 2 Introduction Types of

Cincinnati, OH August 22, 2018

Opportunity Zones Cincinnati, OH August 22, 2018 Opportunity Zones Washington Square Park Cincinnati, OH The Opportunity Zones tax incentive was established by Congress in the 2017 Tax Cut and Jobs Act

Opportunity Zones Cincinnati, OH August 22, 2018 Opportunity Zones Washington Square Park Cincinnati, OH The Opportunity Zones tax incentive was established by Congress in the 2017 Tax Cut and Jobs Act

UNDERSTANDING OPPORTUNITY ZONES & HUBZONES

UNDERSTANDING OPPORTUNITY ZONES & HUBZONES Wednesday, November 7, 2018, 1:00PM-2:30PM Williams County Community Offices, Conference Room A&B 1425 East High Street, Bryan OH 43506 Nate Green, Director of

UNDERSTANDING OPPORTUNITY ZONES & HUBZONES Wednesday, November 7, 2018, 1:00PM-2:30PM Williams County Community Offices, Conference Room A&B 1425 East High Street, Bryan OH 43506 Nate Green, Director of

Opportunity Zones. A Brief Overview June 19, John Heppolette Citi Community Capital Co-Head. Jeffrey Jaeger Principal. Lisa Brill Partner

A Brief Overview June 19, 2018 Opportunity Zones Lisa Brill Partner Jeffrey Jaeger Principal John Heppolette Citi Community Capital Co-Head Michael Novogradac Partner Citi Community Capital Welcome To

A Brief Overview June 19, 2018 Opportunity Zones Lisa Brill Partner Jeffrey Jaeger Principal John Heppolette Citi Community Capital Co-Head Michael Novogradac Partner Citi Community Capital Welcome To

State of Minnesota HOUSE OF REPRESENTATIVES

This Document can be made available in alternative formats upon request 02/16/2017 State of Minnesota HOUSE OF REPRESENTATIVES 1303 NINETIETH SESSION H. F. No. Authored by Albright, Vogel, Davids and Mahoney

This Document can be made available in alternative formats upon request 02/16/2017 State of Minnesota HOUSE OF REPRESENTATIVES 1303 NINETIETH SESSION H. F. No. Authored by Albright, Vogel, Davids and Mahoney

White Paper on Opportunity Zones

White Paper on Opportunity Zones SEPTEMBER 2018 Prepared by: Aaron Deitz, PORTFOLIO MANAGER Elias Bachmann, DIRECTOR OF PRIVATE INVESTMENTS & PORTFOLIO MANAGER Report Overview Here at BSW, we proactively

White Paper on Opportunity Zones SEPTEMBER 2018 Prepared by: Aaron Deitz, PORTFOLIO MANAGER Elias Bachmann, DIRECTOR OF PRIVATE INVESTMENTS & PORTFOLIO MANAGER Report Overview Here at BSW, we proactively

Opportunity Zone Workforce Housing Vignette

Opportunity Zone Workforce Housing Vignette In collaboration with Kirkland Ellis LLP and Ernst Young LLP November 13, The views, opinions, statements, analysis and information contained in these materials

Opportunity Zone Workforce Housing Vignette In collaboration with Kirkland Ellis LLP and Ernst Young LLP November 13, The views, opinions, statements, analysis and information contained in these materials

Backdoor Roth. Combining After-tax Contributions with Roth Conversions to Optimize 401(k) Plans. December Fidelity Benefits Consulting

Plans. December Fidelity Benefits Consulting") Fidelity Benefits Consulting Backdoor Roth Combining After-tax Contributions with Roth Conversions to Optimize 401(k) Plans December 018 What s Inside Understanding the basics We have heard many plan sponsors

Fidelity Benefits Consulting Backdoor Roth Combining After-tax Contributions with Roth Conversions to Optimize 401(k) Plans December 018 What s Inside Understanding the basics We have heard many plan sponsors

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal The Tax Act of 2017: H.R. 1 The Tax Cuts and Jobs Act short title was stricken An Act to provide for reconciliation

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal The Tax Act of 2017: H.R. 1 The Tax Cuts and Jobs Act short title was stricken An Act to provide for reconciliation

FOR BROKER/DEALER/PRODUCER USE ONLY. NOT TO BE REPRODUCED OR SHOWN TO THE PUBLIC.

Business Planning The Pension Protection Act of 2006 The discussion of taxation in this material is the Genworth Financial companies' interpretation of current tax law and is not intended as tax advice.

Business Planning The Pension Protection Act of 2006 The discussion of taxation in this material is the Genworth Financial companies' interpretation of current tax law and is not intended as tax advice.

The Tax Cuts and Jobs Act1 (TCJA) made

made") Significant Provisions of the Tax Cuts and Jobs Act Affecting Closely Held Businesses and Their Owners by Gerald A. Shanker The Tax Cuts and Jobs Act1 (TCJA) made significant changes to the Internal Revenue

Significant Provisions of the Tax Cuts and Jobs Act Affecting Closely Held Businesses and Their Owners by Gerald A. Shanker The Tax Cuts and Jobs Act1 (TCJA) made significant changes to the Internal Revenue

Opportunity Zone Financial Examples. City of Virginia Beach (757) September 19, 2018

September 19, 2018") Opportunity Zone Financial Examples Ronald D Berkebile rberkebi@vbgov.com City of Virginia Beach (757) 385-2902 September 19, 2018 Opportunity Zone Example Programs and Assumptions Programs: Five-year

Opportunity Zone Financial Examples Ronald D Berkebile rberkebi@vbgov.com City of Virginia Beach (757) 385-2902 September 19, 2018 Opportunity Zone Example Programs and Assumptions Programs: Five-year

Qualified Opportunity Zones and Tax Credit Incentives Under the Tax Cuts and Jobs Act

Qualified Opportunity Zones and Tax Credit Incentives Under the Tax Cuts and Jobs Act James O. Lang and Justin J. Mayor * The authors discuss a significant new economic development tool created under the

Qualified Opportunity Zones and Tax Credit Incentives Under the Tax Cuts and Jobs Act James O. Lang and Justin J. Mayor * The authors discuss a significant new economic development tool created under the

M E M O R A N D U M. To: Friends of Duval & Stachenfeld Date: August 16, Duval & Stachenfeld Real Estate and Tax Practice Groups

M E M O R A N D U M To: Friends of Duval & Stachenfeld Date: August 16, 2018 From: Duval & Stachenfeld Real Estate and Tax Practice Groups Subject: Your Opportunity Zone Roadmap: How to set up a Qualified

M E M O R A N D U M To: Friends of Duval & Stachenfeld Date: August 16, 2018 From: Duval & Stachenfeld Real Estate and Tax Practice Groups Subject: Your Opportunity Zone Roadmap: How to set up a Qualified

State of Minnesota HOUSE OF REPRESENTATIVES

This Document can be made available in alternative formats upon request 02/16/2017 03/09/2017 State of Minnesota HOUSE OF REPRESENTATIVES 1303 NINETIETH SESSION H. F. No. Authored by Albright, Vogel, Davids

This Document can be made available in alternative formats upon request 02/16/2017 03/09/2017 State of Minnesota HOUSE OF REPRESENTATIVES 1303 NINETIETH SESSION H. F. No. Authored by Albright, Vogel, Davids

WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES

Tax Reform: WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES Presented By: JOHN HELLER, CPA Manager Tax Services Group Agenda We will cover: Review Corporate Tax Changes Business Deduction Changes

Tax Reform: WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES Presented By: JOHN HELLER, CPA Manager Tax Services Group Agenda We will cover: Review Corporate Tax Changes Business Deduction Changes