Chapter New Law

|

|

|

- Candace Pope

- 5 years ago

- Views:

Transcription

1 Chapter New Law The Surface 1-11 Transportation and Veterans Health Care Choice Improvement Act of 2015 (7/31/15)

2 1-11 Modified Return Filing Dates and Extension Dates For 2016 Returns 1-13 Due Date Chart from AICPA (link)

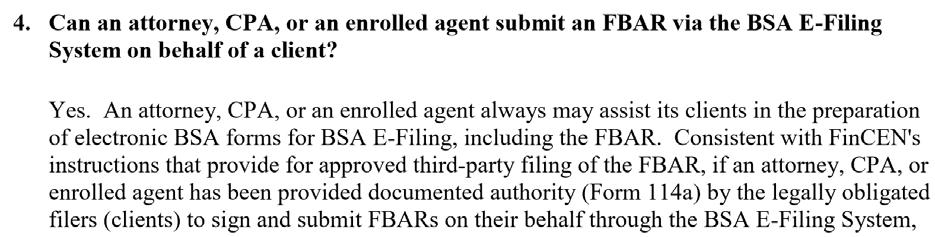

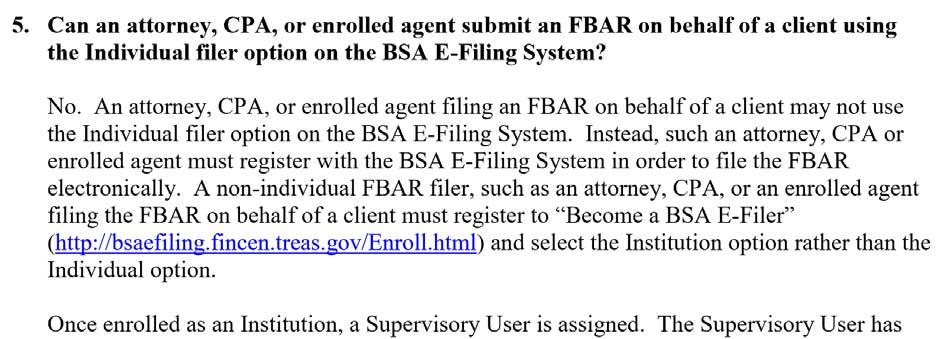

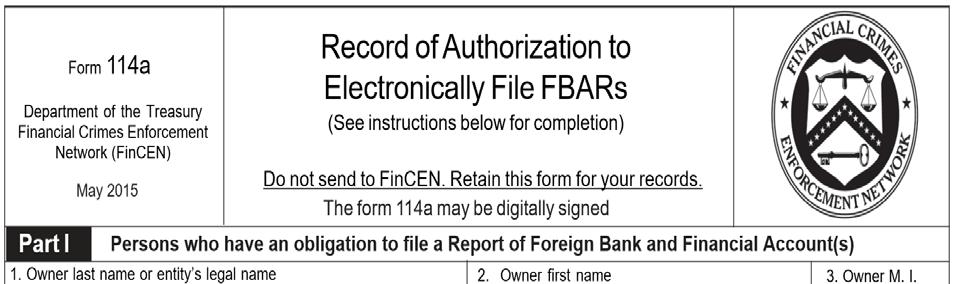

3 June 30 No Ext. April 15 Oct. 15 For returns for tax years beginning after Dec. 31, 2015 (2016 FBARS) 1-18 FBAR FAQ s

4

5 Basis Consistency For Estate Tax Property and Information 1-13 Reporting of Estate Tax Value Basis Consistency Requirement (Sec. 1014(f))

6 For estate tax returns filed after July 31, 2015, beneficiary s basis must not exceed estate tax value Underpayment of income tax due to inconsistent basis is subject to the 20- percent accuracyrelated penalty (section 6662(b)(8)).

7 Only applies if inclusion in the decedent s estate increased the estate tax liability 2015 Gross Estate filing threshold: $5.43 million

8 Estate Reporting Applies to 706s filed after July 31, 2015 (Sec. 6035) The executor of any estate required to file a return under section 6018(a) must furnish, both to the IRS and [the beneficiary of the property]

9 a statement identifying the value of each interest in such property as reported on such return and such other information with respect to such interest as the IRS may prescribe. (Section 6035(a)(1)) Due Date of Statement The IRS will prescribe the due date, but it can be no later than the earlier of 30 days after the Form 706 is required to be filed (including extensions), or 30 days after the 706 is filed (Sec. 6035(a)(3)(A))

10 Form 8971, Sch A Column B Description of property acquired from the decedent and the schedule and item number where reported on Form 706. If beneficiary acquired a partial interest in the property indicate the % acquired here. Column C Did this asset increase estate tax? Y/N

11 Column D Valuation Date Column E Estate Tax Value

12 Sec. 1014(a): [T]he basis of property in the hands of a person acquiring the property from a decedent or to whom the property passed from a decedent shall be the fair market value of the property at the date of the decedent's death, Reg (a): The purpose of section 1014 is, in general, to provide a basis for property acquired from a decedent which is equal to the value placed upon such property for purposes of the Federal estate tax.

13 Reg (b): Multiple Interests. Where more than one person has an interest in property acquired from a decedent, the basis of such property shall be determined and adjusted without regard to the multiple interests.. Form 8971, Schedule A Notice to Beneficiaries: You have received this schedule to inform you of the value of property you received from the estate of the decedent named above. Retain this schedule for tax reporting purposes. If the property increased the estate tax liability, IRC sec. 1014(f) applies, requiring the consistent reporting of basis information. For more information on determining basis, see IRC section 1014 and/or consult a tax professional

14 Notice Delay in Due Date of New Statement Notice For statements required to be filed before February 29, 2016, the due date under section 6035(a)(3) is delayed to February 29, 2016.

property from the estate?")

15 The notice does not delay the effective date of sec which applies to estate tax returns filed after July 15, 2015 DRAFT Part II How many beneficiaries received (or are expected to receive) property from the estate? For each beneficiary, provide the information requested below

Form")

16 Notice to Executors Only Schedule A to beneficiary. Form 8971 and each Sch A goes to IRS. Do not provide 8971 to beneficiary. Retain copies for estate s records. Open Question: 1-15 Observation Must estates that file (optionally) Form 706 solely to elect portability, file the new basis reports?

17 The statute authorizes the IRS to issue regulations as necessary to carry out [section 6035], including to property with regard to which no estate tax return is required to be filed The recently finalized regulations on portability declare that [a]n estate that elects portability will be considered, for purposes of subtitle B and subtitle F of the Internal Revenue Code (Code), to be required to file [an estate tax] return under section 6018(a). Reg (a)(1).

18 Section 6035 Reporting is in by Subtitle F The IRS is aware of the issue

19 JCT Revenue Estimate $1.542 billion over fiscal years Clarification of 6-Year Statute of Limitations with Overstatement of Basis.

20 An understatement of gross income by reason of an overstatement of unrecovered cost or other basis is an omission of gross income. Effective for returns filed after July 2015 or if S of L is open as of July 2015 More Information on Form 1098 With Respect to 1098s Furnished After

21 Due Feb. 29, 2016 if Paper Filed Due Feb. 28, 2017 if Paper Filed 2016 Form 1098

22 JCT Revenue Estimate = $1.806 billion 1-23 Prior Law First Effective in 2015

23 1-23 ABLE Act TYB on or after 1/1/2015 Eligible for ABLE Acct if entitled to social security benefits for blindness or disability before age 26 or

24 File a disability certification, which is a signed statement by a physician acknowledging disability or blindness before age 26 Doctor Certifies That:

25 the individual has a medically determinable physical or mental impairment, which results in marked and severe functional limitations, and which can be expected to result in death or which has lasted or can be expected to last for a continuous period of not less than 12 months, or is blind (sec. 529A(e)(2)(A)(i)) No age requirement to open the account as long as the eligible individual became disabled before age 26.

26 One ABLE account Per Beneficiary Maximum annual contribution is the gift tax exclusion amount ($14,000 in 2015) Tax Advantage

27 No deduction for contributions, but The ABLE account is not taxable and distributions are tax free if used for qualified disability expenses (QDEs). QDEs: Education, housing, transportation, employment training and support, assistive technology and personal support services, health, prevention and wellness,

28 financial management and administrative services, legal fees, expenses for oversight and monitoring, funeral and burial expenses, and other expenses approved by the Secretary. Prop. Regs. Preamble: qualified disability expenses should be broadly construed to permit the inclusion of basic living expenses and should not be limited to expenses for items for which there is a medical necessity

29 For example, expenses for common items such as smart phones could be considered qualified disability expenses if they are an effective and safe communication or navigation aid for a child with autism. The Non-Tax Advantage

30 ABLE account is generally disregarded for purposes of other means-tested federal programs: Medicaid, Supplemental Security Income (SSI) Social Security Disability Insurance (SSDI) Helpful because, for example, Medicaid and the SSI program benefits may be lost if an individual s assets exceed $2,000

31 Exception The ABLE Act allows disabled individuals to accumulate no more than $100,000 of assets without the loss of SSI benefits.

32 If the $100,000 limit is exceeded, SSI benefits are suspended not terminated; when the account balance falls below $100,000, SSI benefits are restored. Also, in the case of the SSI program, distributions for housing expenses are not disregarded.

33 However, ABLE accounts, when established, create a Medicaid lien for Medicaid benefits received after that date (claimed at death) The medicaid payback requirement is a disadvantage to ABLE accounts compared to to special needs trusts or 529 qualified tuition programs

34 A special needs trust (SNT), is not funded with money from the beneficiary, but: No dollar limits No payback for Medicaid benefits Cannot Use Another New State s LawABLE Act Program

35 2015 PATH ACT Can Use Another State s ABLE Act Program Can rollover from 529 Plan California ABLE Act Signed by Governor October 11, 2015 AB 449 SB 324

36 California Revenue and Taxation Code Change Sec For taxable years beginning on or after January 1, 2016, section 529A shall apply R&T Sec

37 A 2.5% penalty (instead of 10%) for distributions not used for disability expenses Welfare and Institutions Code Change New Section 4877 (10/11/2015) Official Announcement: will implement next year (2016)

Updates on ABLE Accounts & Special Needs Trusts

Updates on ABLE Accounts & Special Needs Trusts Mary E. O Byrne, MBA JD Baltimore County Bar Association O Byrne Law, LLC Estates & Trusts Section 1400 Front Avenue, Suite 303 February 28, 2018 Lutherville,

Updates on ABLE Accounts & Special Needs Trusts Mary E. O Byrne, MBA JD Baltimore County Bar Association O Byrne Law, LLC Estates & Trusts Section 1400 Front Avenue, Suite 303 February 28, 2018 Lutherville,

Form 8971; The Basics

January 10-13, 2016 Form 8971: The Basics 1 PRESENTATION TITLEE Disclaimer The information presented today is for educational purposes only and shall not be cited or relied upon as authority. 2 Basics

January 10-13, 2016 Form 8971: The Basics 1 PRESENTATION TITLEE Disclaimer The information presented today is for educational purposes only and shall not be cited or relied upon as authority. 2 Basics

How can I or my family member qualify for an ABLE account?

ABLE Fact Sheet Top ABLE Account Questions How can I or my family member qualify for an ABLE account? First, the individual s disability must have occurred before age 26. Second, the individual must essentially

ABLE Fact Sheet Top ABLE Account Questions How can I or my family member qualify for an ABLE account? First, the individual s disability must have occurred before age 26. Second, the individual must essentially

Montana ABLE Accounts. Theresa Baldry

Montana ABLE Accounts Theresa Baldry ABLE Act within Law: The Stephen Beck, Jr. Achieving a Better Life Experience (ABLE) Act: Created options for qualified individuals with disabilities and their families

Montana ABLE Accounts Theresa Baldry ABLE Act within Law: The Stephen Beck, Jr. Achieving a Better Life Experience (ABLE) Act: Created options for qualified individuals with disabilities and their families

Plan Disclosure Booklet

Plan Disclosure Booklet Administration and Trustee: The Oregon 529 Savings Board October 26, 2017 Amounts invested under the Oregon ABLE Savings Plan are not guaranteed or insured by the State of Oregon,

Plan Disclosure Booklet Administration and Trustee: The Oregon 529 Savings Board October 26, 2017 Amounts invested under the Oregon ABLE Savings Plan are not guaranteed or insured by the State of Oregon,

Special Needs Trusts and ABLE Accounts

Special Needs Trusts and ABLE Accounts Travis Finchum Special Needs Lawyers, P.A. Travis@SpecialNeedsLawyers.com SpecialNeedsLawyers.com GuardianTrusts.org Special Needs Trusts To benefit individuals with

Special Needs Trusts and ABLE Accounts Travis Finchum Special Needs Lawyers, P.A. Travis@SpecialNeedsLawyers.com SpecialNeedsLawyers.com GuardianTrusts.org Special Needs Trusts To benefit individuals with

STABLE Account 529A Savings Plan. Plan Disclosure Statement and Participation Agreement December 9, 2016

STABLE Account 529A Savings Plan Plan Disclosure Statement and Participation Agreement December 9, 2016 Accounts in the State Treasury Achieving a Better Life Experience ( STABLE ) Account Plan are not

STABLE Account 529A Savings Plan Plan Disclosure Statement and Participation Agreement December 9, 2016 Accounts in the State Treasury Achieving a Better Life Experience ( STABLE ) Account Plan are not

Program Disclosure Booklet. Administration and Trustee: The Maryland 529 Board

Program Disclosure Booklet Administration and Trustee: The Maryland 529 Board November 27, 2017 Investing in the Maryland ABLE program is an important decision. Please read the Program Disclosure Booklet

Program Disclosure Booklet Administration and Trustee: The Maryland 529 Board November 27, 2017 Investing in the Maryland ABLE program is an important decision. Please read the Program Disclosure Booklet

Plan Disclosure Booklet. Administration and Trustee: The Oregon 529 Savings Board

Plan Disclosure Booklet Administration and Trustee: The Oregon 529 Savings Board March 20, 2018 Amounts invested under the ABLE for ALL Savings Plan are not guaranteed or insured by the State of Oregon,

Plan Disclosure Booklet Administration and Trustee: The Oregon 529 Savings Board March 20, 2018 Amounts invested under the ABLE for ALL Savings Plan are not guaranteed or insured by the State of Oregon,

What is Maryland ABLE

What is Maryland ABLE Maryland ABLE accounts are a way for families and people with disabilities to save money without jeopardizing state or federal benefits, such as SSI, Medicaid, waiver services, etc.

What is Maryland ABLE Maryland ABLE accounts are a way for families and people with disabilities to save money without jeopardizing state or federal benefits, such as SSI, Medicaid, waiver services, etc.

Texas ABLE Program Disclosure Statement and Participation Agreement. As of April 26, 2018

Texas ABLE Program Disclosure Statement and Participation Agreement SM As of April 26, 2018 This page has been intentionally left blank. PROGRAM DISCLOSURE STATEMENT Before you open an Account in the Texas

Texas ABLE Program Disclosure Statement and Participation Agreement SM As of April 26, 2018 This page has been intentionally left blank. PROGRAM DISCLOSURE STATEMENT Before you open an Account in the Texas

The ABLE Act in 2016 July 19, 2016

1 The ABLE Act in 2016 July 19, 2016 Marty Ford Senior Executive Officer, Public Policy Robin Shaffert Senior Executive Officer, Individual and Family Support Nicole Jorwic Director, Rights Policy 2 The

1 The ABLE Act in 2016 July 19, 2016 Marty Ford Senior Executive Officer, Public Policy Robin Shaffert Senior Executive Officer, Individual and Family Support Nicole Jorwic Director, Rights Policy 2 The

SMD# RE: Implications of the ABLE Act for State Medicaid Programs. September 7, Dear State Medicaid Director:

DEPARTMENT OF HEALTH AND HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, MD 21244-1850 SMD# 17-002 RE: Implications of the ABLE Act for State

DEPARTMENT OF HEALTH AND HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, MD 21244-1850 SMD# 17-002 RE: Implications of the ABLE Act for State

Special Needs Planning The Arc of MA Transition Training

Special Needs Planning The Arc of MA Transition Training November 4, 2017 College of the Holy Cross Presented By: Theresa M. Varnet WORCESTER FRAMINGHAM CAPE COD MEDFIELD NEW BEDFORD PROVIDENCE Navigating

Special Needs Planning The Arc of MA Transition Training November 4, 2017 College of the Holy Cross Presented By: Theresa M. Varnet WORCESTER FRAMINGHAM CAPE COD MEDFIELD NEW BEDFORD PROVIDENCE Navigating

Craig C. Reaves and Mary Alice Jackson

Stetson University College of Law 2017 National Conference on Special Needs Trusts and Special Needs Planning Presented by Craig C. Reaves and Mary Alice Jackson Copyright 2017 Craig C. Reaves and Mary

Stetson University College of Law 2017 National Conference on Special Needs Trusts and Special Needs Planning Presented by Craig C. Reaves and Mary Alice Jackson Copyright 2017 Craig C. Reaves and Mary

AN INTRODUCTION TO ABLE ACCOUNTS AND THE NC ABLE PROGRAM September 19, 2018 (Rev. December 11, 2018)

") AN INTRODUCTION TO ABLE ACCOUNTS AND THE NC ABLE PROGRAM September 19, 2018 (Rev. December 11, 2018) Reid Chisholm Assistant General Counsel North Carolina Department of State Treasurer INTRODUCTION ABLE

AN INTRODUCTION TO ABLE ACCOUNTS AND THE NC ABLE PROGRAM September 19, 2018 (Rev. December 11, 2018) Reid Chisholm Assistant General Counsel North Carolina Department of State Treasurer INTRODUCTION ABLE

Special Needs Financial Planning ABLE Accounts

Special Needs Financial Planning ABLE Accounts What can ABLE Accomplish? Copyright The Arc Wisconsin, Kathleen Oberneder & Barbara S. Hughes March 2018 Securities and Advisory Services offered through

Special Needs Financial Planning ABLE Accounts What can ABLE Accomplish? Copyright The Arc Wisconsin, Kathleen Oberneder & Barbara S. Hughes March 2018 Securities and Advisory Services offered through

WHAT YOU DON T KNOW CAN HURT YOU

WHAT YOU DON T KNOW CAN HURT YOU Recent Developments in Estate, Long-Term Care & Special Needs Planning Presented by Elizabeth Q. Boehmcke, Esq. boehmcke@hooklawcenter.com Long-Term Care As of July 1,

WHAT YOU DON T KNOW CAN HURT YOU Recent Developments in Estate, Long-Term Care & Special Needs Planning Presented by Elizabeth Q. Boehmcke, Esq. boehmcke@hooklawcenter.com Long-Term Care As of July 1,

Analysis of Funding Options for Special Needs Planning

Analysis of Funding Options for Planning Payback Income 1 Created and Managed by Who can serve as ee Hire/Fire/Change ee Successor ees Authority to remove ee Authority to make investment decisions Control

Analysis of Funding Options for Planning Payback Income 1 Created and Managed by Who can serve as ee Hire/Fire/Change ee Successor ees Authority to remove ee Authority to make investment decisions Control

The ABLE Act: What does it mean for your practice?

The ABLE Act: What does it mean for your practice? Robert B. Fleming Fleming & Curti, PLC Tucson, Arizona www.flemingandcurti.com What is ABLE? The ABLE Act: Passed Congress in December Signed by President

The ABLE Act: What does it mean for your practice? Robert B. Fleming Fleming & Curti, PLC Tucson, Arizona www.flemingandcurti.com What is ABLE? The ABLE Act: Passed Congress in December Signed by President

THE GENERAL ASSEMBLY OF PENNSYLVANIA HOUSE BILL

PRINTER'S NO. 1 THE GENERAL ASSEMBLY OF PENNSYLVANIA HOUSE BILL No. Session of 01 INTRODUCED BY MARSHALL, O'NEILL, STEPHENS, D. MILLER, MURT, BARRAR, COHEN, D. COSTA, CUTLER, DAVIS, DRISCOLL, GIBBONS,

PRINTER'S NO. 1 THE GENERAL ASSEMBLY OF PENNSYLVANIA HOUSE BILL No. Session of 01 INTRODUCED BY MARSHALL, O'NEILL, STEPHENS, D. MILLER, MURT, BARRAR, COHEN, D. COSTA, CUTLER, DAVIS, DRISCOLL, GIBBONS,

Interplay of Tax and Eligibility Rules in 529 Accounts and ABLE Accounts. Stephen W. Dale, JD, LL.M

2017 National Conference on Special Needs Planning and Special Needs Trusts Interplay of Tax and Eligibility Rules in 529 Accounts and ABLE Accounts Stephen W. Dale, JD, LL.M Interplay of Tax and Eligibility

2017 National Conference on Special Needs Planning and Special Needs Trusts Interplay of Tax and Eligibility Rules in 529 Accounts and ABLE Accounts Stephen W. Dale, JD, LL.M Interplay of Tax and Eligibility

To all your abilities, now add the ability to save.

To all your abilities, now add the ability to save. To all of your abilities, now add the ability to save. The Achieving a Better Life Experience Act (ABLE) of 2014 allows individuals with disabilities

To all your abilities, now add the ability to save. To all of your abilities, now add the ability to save. The Achieving a Better Life Experience Act (ABLE) of 2014 allows individuals with disabilities

Via Electronic Mail: Enclosure: ACTEC Comments on Notice /IRC 6035 and 1014(f)

") January 19, 2016 Office of Chief Counsel (Passthroughs and Special Industries) CC:PA:LPD:PR (Notice 2015-57) Room 5203 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington, DC 20044 Via

January 19, 2016 Office of Chief Counsel (Passthroughs and Special Industries) CC:PA:LPD:PR (Notice 2015-57) Room 5203 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington, DC 20044 Via

COMPARISON OF 529 ABLE ACCOUNTS, SPECIAL NEEDS TRUSTS AND POOLED SPECIAL NEEDS TRUSTS

COMPARISON OF 529 ABLE ACCOUNTS, SPECIAL NEEDS TRUSTS AND POOLED SPECIAL NEEDS TRUSTS LAW OFFICE OF RANDY HOPE STEEN, LTD. WWW.RSTEENLAW.COM Able Account Who is Eligible? Are there the age restrictions?

COMPARISON OF 529 ABLE ACCOUNTS, SPECIAL NEEDS TRUSTS AND POOLED SPECIAL NEEDS TRUSTS LAW OFFICE OF RANDY HOPE STEEN, LTD. WWW.RSTEENLAW.COM Able Account Who is Eligible? Are there the age restrictions?

Arizona s ABLE Plan. az-able.com

Arizona s ABLE Plan az-able.com What is ABLE? Federal legislation passed 2014 Creates tax-advantaged investment accounts for individuals with disabilities Assets in your account do not affect eligibility

Arizona s ABLE Plan az-able.com What is ABLE? Federal legislation passed 2014 Creates tax-advantaged investment accounts for individuals with disabilities Assets in your account do not affect eligibility

Vermont s ABLE Plan: Offered in Partnership with STABLE Accounts.

Vermont s ABLE Plan: Offered in Partnership with STABLE Accounts www.vermontable.com Disclosure This Webinar is provided by Kirsten Murphy Executive Director Vermont Developmental Disabilities Council

Vermont s ABLE Plan: Offered in Partnership with STABLE Accounts www.vermontable.com Disclosure This Webinar is provided by Kirsten Murphy Executive Director Vermont Developmental Disabilities Council

SPECIAL NEEDS TRUSTS

SPECIAL NEEDS TRUSTS Special Needs Trust (SNT): type of trust designed to protect a beneficiary who is disabled, enabling them to receive governmental benefits: Supplemental Security Income-automatically

SPECIAL NEEDS TRUSTS Special Needs Trust (SNT): type of trust designed to protect a beneficiary who is disabled, enabling them to receive governmental benefits: Supplemental Security Income-automatically

Special Needs Financial Planning ABLE Accounts What can ABLE Accomplish?

Special Needs Financial Planning ABLE Accounts What can ABLE Accomplish? Securities and Advisory Services offered through JW Cole Financial, a registered investment advisor. Member FINRA/SIPC. Crescendo

Special Needs Financial Planning ABLE Accounts What can ABLE Accomplish? Securities and Advisory Services offered through JW Cole Financial, a registered investment advisor. Member FINRA/SIPC. Crescendo

Internal Revenue Code Section 6662(j) Imposition of accuracy-related penalty on underpayments.

Imposition of accuracy-related penalty on underpayments.") Internal Revenue Code Section 6662(j) Imposition of accuracy-related penalty on underpayments. CLICK HERE to return to the home page (a) Imposition of penalty. If this section applies to any portion of

Internal Revenue Code Section 6662(j) Imposition of accuracy-related penalty on underpayments. CLICK HERE to return to the home page (a) Imposition of penalty. If this section applies to any portion of

ABLE United Deeper Dive into ABLE Accounts. John Finch Director ABLE United Florida Prepaid College Board

ABLE United Deeper Dive into ABLE Accounts John Finch Director ABLE United Florida Prepaid College Board Objectives Achieving a Better Life Experience. Overview of ABLE Act ABLE United Specifics Distinctions

ABLE United Deeper Dive into ABLE Accounts John Finch Director ABLE United Florida Prepaid College Board Objectives Achieving a Better Life Experience. Overview of ABLE Act ABLE United Specifics Distinctions

Ohio s ABLE Plan. stableaccount.com

Ohio s ABLE Plan stableaccount.com What is ABLE? Federal legislation passed 2014 Creates tax-advantaged investment accounts for individuals with disabilities Assets in your account do not affect eligibility

Ohio s ABLE Plan stableaccount.com What is ABLE? Federal legislation passed 2014 Creates tax-advantaged investment accounts for individuals with disabilities Assets in your account do not affect eligibility

Information Reporting and Civil Penalties (in a Nutshell)

") I. In General Information Reporting and Civil Penalties (in a Nutshell) By Lucy S. Lee, Esq. Caplin & Drysdale, Chartered Washington, D.C. 2008 Lucy S. Lee The Internal Revenue Code (the Code ) 1 generally

I. In General Information Reporting and Civil Penalties (in a Nutshell) By Lucy S. Lee, Esq. Caplin & Drysdale, Chartered Washington, D.C. 2008 Lucy S. Lee The Internal Revenue Code (the Code ) 1 generally

The Arc of Texas Master Pooled Trust and the ABLE Act

The Arc of Texas Master Pooled Trust and the ABLE Act How To Save Money and Protect Benefits Haley D. Greer, J.D. Chief Master Pooled Trust Officer What we will talk about today 1. What are the Future

The Arc of Texas Master Pooled Trust and the ABLE Act How To Save Money and Protect Benefits Haley D. Greer, J.D. Chief Master Pooled Trust Officer What we will talk about today 1. What are the Future

WHAT IS ABLE? Medicaid SSI. ABLE Accounts do not affect eligibility for benefits programs

WHAT IS ABLE? ABLE Act of 2014 created savings and investment accounts for individuals with disabilities ABLE Accounts do not affect eligibility for benefits programs SSI Medicaid WHAT IS ABLE? ABLE Accounts

WHAT IS ABLE? ABLE Act of 2014 created savings and investment accounts for individuals with disabilities ABLE Accounts do not affect eligibility for benefits programs SSI Medicaid WHAT IS ABLE? ABLE Accounts

Supplemental Needs Trusts & Related Estate Planning

Supplemental Needs Trusts & Related Estate Planning Presentation for Hydrocephalus Association 12 th National Conference 440 Milwaukee Ave., Suite 200, Lincolnshire, Illinois 60069 PHONE (847) 793-2484

Supplemental Needs Trusts & Related Estate Planning Presentation for Hydrocephalus Association 12 th National Conference 440 Milwaukee Ave., Suite 200, Lincolnshire, Illinois 60069 PHONE (847) 793-2484

SUPPLEMENT DATED JANUARY 2018 TO THE NEW YORK ABLE SAVINGS PROGRAM DISCLOSURE BOOKLET AND PARTICIPATION AGREEMENT DATED AUGUST 2017

SUPPLEMENT DATED JANUARY 2018 TO THE NEW YORK ABLE SAVINGS PROGRAM DISCLOSURE BOOKLET AND PARTICIPATION AGREEMENT DATED AUGUST 2017 This Supplement describes important changes and amends the Disclosure

SUPPLEMENT DATED JANUARY 2018 TO THE NEW YORK ABLE SAVINGS PROGRAM DISCLOSURE BOOKLET AND PARTICIPATION AGREEMENT DATED AUGUST 2017 This Supplement describes important changes and amends the Disclosure

Special Needs Life Planning

Special Needs Life Planning Making a Good Life Possible Blaine P. Brockman, Esq. The ARC of Ohio Summer Conference June 16, 2017 A Special Needs Life Birth and Early Childhood Due to birth complications,

Special Needs Life Planning Making a Good Life Possible Blaine P. Brockman, Esq. The ARC of Ohio Summer Conference June 16, 2017 A Special Needs Life Birth and Early Childhood Due to birth complications,

Ten Topics to Consider for Your Estate Planning Conference

Ten Topics to Consider for Your Estate Planning Conference Laura Akins Attorney, The Witcher Law Firm www.billwitcher.com 150 E. Ponce de Leon Ave., Ste. 300 Decatur, GA 30030 (404) 371 5080 1. Do you

Ten Topics to Consider for Your Estate Planning Conference Laura Akins Attorney, The Witcher Law Firm www.billwitcher.com 150 E. Ponce de Leon Ave., Ste. 300 Decatur, GA 30030 (404) 371 5080 1. Do you

Form Specified Individual. The Instructions to Form 8938 define a Specified Individual as: A U.S. Citizen.

Form 8938 On March 18, 2010, the Foreign Account Tax Compliance Act ( FATCA ) was enacted as part of the Hiring Incentives to Restore Employment ( HIRE ) Act. Section 511 of FATCA creates new Internal

Form 8938 On March 18, 2010, the Foreign Account Tax Compliance Act ( FATCA ) was enacted as part of the Hiring Incentives to Restore Employment ( HIRE ) Act. Section 511 of FATCA creates new Internal

NYSBA CLE Estate Planning and Will Drafting April 20, 2016, Rochester, NY

NYSBA CLE Estate Planning and Will Drafting April 20, 2016, Rochester, NY Lifetime Giving, Minors and Incapacitated Beneficiaries Supplemental Outline, Rochester, NY Prepared by: Albert B. Kukol Levene

NYSBA CLE Estate Planning and Will Drafting April 20, 2016, Rochester, NY Lifetime Giving, Minors and Incapacitated Beneficiaries Supplemental Outline, Rochester, NY Prepared by: Albert B. Kukol Levene

ABLE Accounts: What Trusts and Estates Lawyers Need to Know

Magazine May/June 2017 Volume 31, No. 3 ABLE Accounts: What Trusts and Estates Lawyers Need to Know Bernard A. Krooks Bernard A. Krooks is a founding partner of Littman Krooks in New York, New York, and

Magazine May/June 2017 Volume 31, No. 3 ABLE Accounts: What Trusts and Estates Lawyers Need to Know Bernard A. Krooks Bernard A. Krooks is a founding partner of Littman Krooks in New York, New York, and

ABLE United Account Basics

ABLE United Account Basics Florida s Qualified ABLE Program Presented by: Emily Read How to: Ask Questions ABLE Accounts What is ABLE? Achieving a Better Life Experience. o The Stephen Beck, Jr. Achieving

ABLE United Account Basics Florida s Qualified ABLE Program Presented by: Emily Read How to: Ask Questions ABLE Accounts What is ABLE? Achieving a Better Life Experience. o The Stephen Beck, Jr. Achieving

2015 NEW DEVELOPMENTS LETTER

2015 NEW DEVELOPMENTS LETTER INTRODUCTION Over the past several years, we have experienced tax changes and developments at a much faster pace than just a few years ago. Consequently, keeping abreast of

2015 NEW DEVELOPMENTS LETTER INTRODUCTION Over the past several years, we have experienced tax changes and developments at a much faster pace than just a few years ago. Consequently, keeping abreast of

H. R IN THE HOUSE OF REPRESENTATIVES

I TH CONGRESS ST SESSION H. R. 0 To amend the Internal Revenue Code of to provide for the establishment of ABLE accounts for the care of family members with disabilities, and for other purposes. IN THE

I TH CONGRESS ST SESSION H. R. 0 To amend the Internal Revenue Code of to provide for the establishment of ABLE accounts for the care of family members with disabilities, and for other purposes. IN THE

Spousal Rollover (con t)

") Spousal Rollover (con t) If the beneficiary of the retirement asset was a trust whose sole beneficiary was the spouse and where spouse is the trustee or has withdrawal power over the trust assets, then

Spousal Rollover (con t) If the beneficiary of the retirement asset was a trust whose sole beneficiary was the spouse and where spouse is the trustee or has withdrawal power over the trust assets, then

The Achieving a Better Life Experience (ABLE) Act

Act") The Achieving a Better Life Experience (ABLE) Act is a new law that lets a person with a disability and that person s family put money into a special tax-advantaged account. The ABLE Act will allow people

The Achieving a Better Life Experience (ABLE) Act is a new law that lets a person with a disability and that person s family put money into a special tax-advantaged account. The ABLE Act will allow people

DON T PUT YOUR MONEY IN YOUR MATTRESS! Learning different ways to plan for your family s future

DON T PUT YOUR MONEY IN YOUR MATTRESS! Learning different ways to plan for your family s future Dreams & Futures 1 We all have dreams For millions of Americans, we dream and plan of Owning a home Having

DON T PUT YOUR MONEY IN YOUR MATTRESS! Learning different ways to plan for your family s future Dreams & Futures 1 We all have dreams For millions of Americans, we dream and plan of Owning a home Having

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

SUPPLEMENT A. IRC 1014(f): Basis Must Be Consistent With Estate Tax Return

: Basis Must Be Consistent With Estate Tax Return") SUPPLEMENT A IRC 1014(f): Basis Must Be Consistent With Estate Tax Return For purposes of this section (1) In General. The basis of any property to which subsection (a) [of IRC 1014] applies shall not

SUPPLEMENT A IRC 1014(f): Basis Must Be Consistent With Estate Tax Return For purposes of this section (1) In General. The basis of any property to which subsection (a) [of IRC 1014] applies shall not

Improving the Quality of Life with a Trust / MinnesotABLE Account

Improving the Quality of Life with a Trust / MinnesotABLE Account Lutheran Social Service of Minnesota April 2018 Larry Piumbroeck Outreach Representative Kimberly Watson Director Pooled Trust Services

Improving the Quality of Life with a Trust / MinnesotABLE Account Lutheran Social Service of Minnesota April 2018 Larry Piumbroeck Outreach Representative Kimberly Watson Director Pooled Trust Services

OKLAHOMA S ABLE PLAN. okstable.org

OKLAHOMA S ABLE PLAN okstable.org WHAT IS ABLE? ABLE Act of 2014 created savings and investment accounts for individuals with disabilities ABLE Accounts do not affect eligibility for benefits programs

OKLAHOMA S ABLE PLAN okstable.org WHAT IS ABLE? ABLE Act of 2014 created savings and investment accounts for individuals with disabilities ABLE Accounts do not affect eligibility for benefits programs

THE ARC OF TEXAS MASTER POOLED TRUST AND THE ABLE ACT: HOW TO SAVE MONEY WITHOUT SACRIFICING SSI

THE ARC OF TEXAS MASTER POOLED TRUST AND THE ABLE ACT: HOW TO SAVE MONEY WITHOUT SACRIFICING SSI Haley D. Greer, J.D.- Chief Master Pooled Trust Officer Kyle Piccola- Chief Government and Community Affairs

THE ARC OF TEXAS MASTER POOLED TRUST AND THE ABLE ACT: HOW TO SAVE MONEY WITHOUT SACRIFICING SSI Haley D. Greer, J.D.- Chief Master Pooled Trust Officer Kyle Piccola- Chief Government and Community Affairs

OHIO S ABLE PLAN. stableaccount.com

OHIO S ABLE PLAN stableaccount.com WHAT IS ABLE? ABLE Act of 2014 created savings and investment accounts for individuals with disabilities ABLE Accounts do not affect eligibility for benefits programs

OHIO S ABLE PLAN stableaccount.com WHAT IS ABLE? ABLE Act of 2014 created savings and investment accounts for individuals with disabilities ABLE Accounts do not affect eligibility for benefits programs

DESCRIPTION OF THE CHAIRMAN S MODIFICATION TO THE CHAIRMAN S MARK OF THE TAX CUTS AND JOBS ACT

DESCRIPTION OF THE CHAIRMAN S MODIFICATION TO THE CHAIRMAN S MARK OF THE TAX CUTS AND JOBS ACT Scheduled for Markup Before the SENATE COMMITTEE ON FINANCE on November 15, 2017 Prepared by the Staff of

DESCRIPTION OF THE CHAIRMAN S MODIFICATION TO THE CHAIRMAN S MARK OF THE TAX CUTS AND JOBS ACT Scheduled for Markup Before the SENATE COMMITTEE ON FINANCE on November 15, 2017 Prepared by the Staff of

The Arc of Texas Master Pooled Trust and the ABLE Act

The Arc of Texas Master Pooled Trust and the ABLE Act How To Save Money and Protect Benefits HALEY D. GREER Chief Master Pooled Trust Officer KYLE PICCOLA Chief Government and Community Affairs Officer

The Arc of Texas Master Pooled Trust and the ABLE Act How To Save Money and Protect Benefits HALEY D. GREER Chief Master Pooled Trust Officer KYLE PICCOLA Chief Government and Community Affairs Officer

Estate Planning, Medi-Cal, Advance Directives & Special Needs Trusts

Estate Planning, Medi-Cal, Advance Directives & Special Needs Trusts B R U C E A. F E D E R, E S Q. K A T O, F E D E R & S U Z U K I, L L P 6 8 5 M A R K E T S T R E E T, S U I T E 5 4 0 S A N F R A N

Estate Planning, Medi-Cal, Advance Directives & Special Needs Trusts B R U C E A. F E D E R, E S Q. K A T O, F E D E R & S U Z U K I, L L P 6 8 5 M A R K E T S T R E E T, S U I T E 5 4 0 S A N F R A N

6/21/17. Life Advantages, LLC

Life Advantages, LLC Attorneys John F. Kearns III & Rebecca A. Hajosy Kearns & Kearns PC 1121 New Britain Ave West Hartford, CT 06110 (860) 233-1281 www.kearnsandkearns.com Kearns & Kearns PC helps our

Life Advantages, LLC Attorneys John F. Kearns III & Rebecca A. Hajosy Kearns & Kearns PC 1121 New Britain Ave West Hartford, CT 06110 (860) 233-1281 www.kearnsandkearns.com Kearns & Kearns PC helps our

The Essentials of Special Needs Planning

The Essentials of Special Needs Planning Lesley M. Mehalick, J.D., LL.M. and Alissa B. Gorman, J.D., LL.M. McAndrews Law Office, P.C. Berwyn, PA I. Introduction a. What is Special Needs Planning? i. Estate

The Essentials of Special Needs Planning Lesley M. Mehalick, J.D., LL.M. and Alissa B. Gorman, J.D., LL.M. McAndrews Law Office, P.C. Berwyn, PA I. Introduction a. What is Special Needs Planning? i. Estate

Impact of Tax Reform on ABLE Accounts and Special Needs Trusts: Guidance for Elder Law Attorneys

Presenting a live 90-minute webinar with interactive Q&A Impact of Tax Reform on ABLE Accounts and Special Needs Trusts: Guidance for Elder Law Attorneys THURSDAY, SEPTEMBER 27, 2018 1pm Eastern 12pm Central

Presenting a live 90-minute webinar with interactive Q&A Impact of Tax Reform on ABLE Accounts and Special Needs Trusts: Guidance for Elder Law Attorneys THURSDAY, SEPTEMBER 27, 2018 1pm Eastern 12pm Central

The Arc of Texas Master Pooled Trust and the ABLE Act

The Arc of Texas Master Pooled Trust and the ABLE Act How To Save Money and Protect Benefits Haley D. Greer, J.D. Chief Master Pooled Trust Officer What we will talk about today 1. What are the Tools in

The Arc of Texas Master Pooled Trust and the ABLE Act How To Save Money and Protect Benefits Haley D. Greer, J.D. Chief Master Pooled Trust Officer What we will talk about today 1. What are the Tools in

Enable Savings Plan PRESENTATION SUBTITLE HERE

Enable Savings Plan PRESENTATION SUBTITLE HERE Monday, March 7, 2016 October 2016 1 What is ABLE: an Overview Achieving a Better Life Experience (ABLE) Act Became federal law in December 2014 Authorized

Enable Savings Plan PRESENTATION SUBTITLE HERE Monday, March 7, 2016 October 2016 1 What is ABLE: an Overview Achieving a Better Life Experience (ABLE) Act Became federal law in December 2014 Authorized

Funding the Future: The ABLE Act and Special Needs Planning P R E S E N T E D B Y

Funding the Future: The ABLE Act and Special Needs Planning P R E S E N T E D B Y SUPPLEMENTAL SECURITY INCOME SSI Resource Rules Countable resource limit: $2,000 single, $3,000 couple Exempt resources:

Funding the Future: The ABLE Act and Special Needs Planning P R E S E N T E D B Y SUPPLEMENTAL SECURITY INCOME SSI Resource Rules Countable resource limit: $2,000 single, $3,000 couple Exempt resources:

PLANNING FOR YOUR FINANCIAL FUTURE:

PLANNING FOR YOUR FINANCIAL FUTURE: How A Special Needs Trust, Master Pooled Trust, Miller Trust & ABLE Accounts Can Help! HALEY D. GREER Chief Master Pooled Trust Officer What we will talk about today

PLANNING FOR YOUR FINANCIAL FUTURE: How A Special Needs Trust, Master Pooled Trust, Miller Trust & ABLE Accounts Can Help! HALEY D. GREER Chief Master Pooled Trust Officer What we will talk about today

Individual Taxation and Planning

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

WHAT ARE THE BENEFITS OF ABLE?

ABLE Act of 2014 created savings and investment accounts for individuals with disabilities WHAT IS ABLE? Creates tax-advantaged investment accounts for individuals with disabilities Assets in your account

ABLE Act of 2014 created savings and investment accounts for individuals with disabilities WHAT IS ABLE? Creates tax-advantaged investment accounts for individuals with disabilities Assets in your account

The New York City Bar Association, through its Committee on Estate and Gift Taxation

CONTACT POLICY DEPARTMENT MARIA CILENTI 212.382.6655 mcilenti@nycbar.org ELIZABETH KOCIENDA 212.382.4788 ekocienda@nycbar.org REPORT OF THE ESTATE AND GIFT TAXATION COMMITTEE ON PROPOSED REGULATIONS UNDER

CONTACT POLICY DEPARTMENT MARIA CILENTI 212.382.6655 mcilenti@nycbar.org ELIZABETH KOCIENDA 212.382.4788 ekocienda@nycbar.org REPORT OF THE ESTATE AND GIFT TAXATION COMMITTEE ON PROPOSED REGULATIONS UNDER

20 Speen Street, Suite 101 Framingham, MA Telephone: Facsimile:

20 Speen Street, Suite 101 Framingham, MA 01701 Telephone: 508-861-3453 Facsimile: 508-861-3690 www.specialneeds-law.com ABLE Accounts 1 June 3, 2016 Since the enactment of federal legislation authorizing

20 Speen Street, Suite 101 Framingham, MA 01701 Telephone: 508-861-3453 Facsimile: 508-861-3690 www.specialneeds-law.com ABLE Accounts 1 June 3, 2016 Since the enactment of federal legislation authorizing

THE AMERICAN LAW INSTITUTE Continuing Legal Education. Estate Planning for the Family Business Owner

917 THE AMERICAN LAW INSTITUTE Continuing Legal Education Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law and the ABA Section of Taxation

917 THE AMERICAN LAW INSTITUTE Continuing Legal Education Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law and the ABA Section of Taxation

Please file this Supplement to the Enable Savings Plan Program Disclosure Statement with your records

Please file this Supplement to the Enable Savings Plan Program Disclosure Statement with your records ENABLE SAVINGS PLAN PROGRAM DISCLOSURE STATEMENT DATED AUGUST 27, 2017 SUPPLEMENT NUMBER ONE This Supplement

Please file this Supplement to the Enable Savings Plan Program Disclosure Statement with your records ENABLE SAVINGS PLAN PROGRAM DISCLOSURE STATEMENT DATED AUGUST 27, 2017 SUPPLEMENT NUMBER ONE This Supplement

Session 1: Estate Planning Hot Topics: 2016

Session 1: Estate Planning Hot Topics: 2016 Christopher T. Rogers In this presentation we will review several current estate planning/estate tax topics, including (i) an introduction to the Beneficiary

Session 1: Estate Planning Hot Topics: 2016 Christopher T. Rogers In this presentation we will review several current estate planning/estate tax topics, including (i) an introduction to the Beneficiary

The New Consistent Basis and Value Reporting Rules

The New Consistent Basis and Value Reporting Rules Jennifer R. Pierce INTRODUCTION The Surface Transportation and Veterans Health Care Choice Improvement Act of 2015 1014(f) ( basis consistency requirement)

The New Consistent Basis and Value Reporting Rules Jennifer R. Pierce INTRODUCTION The Surface Transportation and Veterans Health Care Choice Improvement Act of 2015 1014(f) ( basis consistency requirement)

2017 National Conference on Special Needs Planning and Special Needs Trusts. Saving Income Taxes with Qualified Disability Trusts Bradley J.

2017 National Conference on Special Needs Planning and Special Needs Trusts Saving Income Taxes with Qualified Disability Trusts Bradley J. Frigon Law Offices of Bradley J. Frigon 6500 S. Quebec St. Suite

2017 National Conference on Special Needs Planning and Special Needs Trusts Saving Income Taxes with Qualified Disability Trusts Bradley J. Frigon Law Offices of Bradley J. Frigon 6500 S. Quebec St. Suite

403(b) ORP PLAN DOCUMENT FOR. Eastern Kentucky University

ORP PLAN DOCUMENT FOR. Eastern Kentucky University") 403(b) ORP PLAN DOCUMENT FOR Eastern Kentucky University TABLE OF CONTENTS Page Preamble 1 Article I Definitions 2 Article II Eligibility 8 Article III Contribution and Allocation 10 Article IV Determination

403(b) ORP PLAN DOCUMENT FOR Eastern Kentucky University TABLE OF CONTENTS Page Preamble 1 Article I Definitions 2 Article II Eligibility 8 Article III Contribution and Allocation 10 Article IV Determination

IRS relaxes bona fide residency test for individuals living in US territories

IRS relaxes bona fide residency test for individuals living in US territories Authors: Mark Strong, Senior Manager, Private Client Services, Ernst & Young LLP (McLean, VA) Ashley Weyenberg, Manager, Private

IRS relaxes bona fide residency test for individuals living in US territories Authors: Mark Strong, Senior Manager, Private Client Services, Ernst & Young LLP (McLean, VA) Ashley Weyenberg, Manager, Private

Impact of 2017 Tax Act on Individuals. From The Editors

Impact of 2017 Tax Act on Individuals From The Editors On December 22, 2017, President Trump signed into law the most extensive tax legislation since 1986, resulting in sweeping changes to the tax system,

Impact of 2017 Tax Act on Individuals From The Editors On December 22, 2017, President Trump signed into law the most extensive tax legislation since 1986, resulting in sweeping changes to the tax system,

2017 Fingertip Tax Guide

2017 Fingertip Tax Guide INCOME TAXES 2017 If Taxable Income Is: 1 Married Filing Jointly Estates and Trusts Single $0 $18,650 $0 + 10% $0 $18,650 $75,900 $1,865 + 15% $18,650 $75,900 $153,100 $10,452.50

2017 Fingertip Tax Guide INCOME TAXES 2017 If Taxable Income Is: 1 Married Filing Jointly Estates and Trusts Single $0 $18,650 $0 + 10% $0 $18,650 $75,900 $1,865 + 15% $18,650 $75,900 $153,100 $10,452.50

FINANCING LONG TERM CARE: PROTECTING THE HOME

FINANCING LONG TERM CARE: PROTECTING THE HOME Prepared by Emily S. Starr The Law Office of Ciota, Starr & Vander Linden LLP 625 Main Street Seven State Street Fitchburg, MA 01420 Worcester, MA 01609 (978)

FINANCING LONG TERM CARE: PROTECTING THE HOME Prepared by Emily S. Starr The Law Office of Ciota, Starr & Vander Linden LLP 625 Main Street Seven State Street Fitchburg, MA 01420 Worcester, MA 01609 (978)

FILICE INSURANCE 401(K) EMPLOYEE SAVINGS PLAN SUMMARY PLAN DESCRIPTION

EMPLOYEE SAVINGS PLAN SUMMARY PLAN DESCRIPTION") FILICE INSURANCE 401(K) EMPLOYEE SAVINGS PLAN SUMMARY PLAN DESCRIPTION TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?...1 What information does this Summary provide?...1 ARTICLE

FILICE INSURANCE 401(K) EMPLOYEE SAVINGS PLAN SUMMARY PLAN DESCRIPTION TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?...1 What information does this Summary provide?...1 ARTICLE

Highlights from the 199A Proposed Regulations

Highlights from the 199A Proposed Regulations August 13, 2018 Kristine A. Tidgren Treasury and the IRS released IRC 199A proposed regulations, REG-107892-18, on August 8, 2018. The regulations will not

Highlights from the 199A Proposed Regulations August 13, 2018 Kristine A. Tidgren Treasury and the IRS released IRC 199A proposed regulations, REG-107892-18, on August 8, 2018. The regulations will not

NEIGHBORHOOD LEGAL SERVICES, INC.

NEIGHBORHOOD LEGAL SERVICES, INC. EQUAL JUSTICE FOR ALL Main-Seneca Building 237 Main Street Suite 400 Buffalo, New York 14203-2794 TEL. (716) 847-0650 FAX (716) 847-0227 TDD (716) 847-1322 www.nls.org

NEIGHBORHOOD LEGAL SERVICES, INC. EQUAL JUSTICE FOR ALL Main-Seneca Building 237 Main Street Suite 400 Buffalo, New York 14203-2794 TEL. (716) 847-0650 FAX (716) 847-0227 TDD (716) 847-1322 www.nls.org

CC:PA:LPD:PR (REG ) Courier s Desk Internal Revenue Service 1111 Constitution Avenue, N.W. Washington, DC

Courier s Desk Internal Revenue Service 1111 Constitution Avenue, N.W. Washington, DC") COMMITTEE ON ESTATE AND GIFT TAXATION PAUL A. FERRARA CHAIR 114 WEST 47 TH STREET NEW YORK, NY 10036 Phone: (212) 852-2817 paul.a.ferrara@ustrust.com JOHN BATTERTON SECRETARY 114 WEST 47 TH STREET NEW

COMMITTEE ON ESTATE AND GIFT TAXATION PAUL A. FERRARA CHAIR 114 WEST 47 TH STREET NEW YORK, NY 10036 Phone: (212) 852-2817 paul.a.ferrara@ustrust.com JOHN BATTERTON SECRETARY 114 WEST 47 TH STREET NEW

Roth IRA Disclosure Statement

Roth IRA Disclosure Statement Mail or fax completed form to: P.O. Box 1555, Des Moines, IA 50306-1555 Fax: 866 709 3922 Contact us: Annuity Customer Contact Center Tel: 888 266 8489 www.atheneannuity.com

Roth IRA Disclosure Statement Mail or fax completed form to: P.O. Box 1555, Des Moines, IA 50306-1555 Fax: 866 709 3922 Contact us: Annuity Customer Contact Center Tel: 888 266 8489 www.atheneannuity.com

IRS Issues Proposed ABLE Act Regulations

1667 K Street NW, Suite 640 Washington D.C., 20006 Phone: (202) 296.2040 Fax: (202) 296.2047 IRS Issues Proposed ABLE Act Regulations Friday June 19th, the Internal Revenue Service (IRS) released the highly

1667 K Street NW, Suite 640 Washington D.C., 20006 Phone: (202) 296.2040 Fax: (202) 296.2047 IRS Issues Proposed ABLE Act Regulations Friday June 19th, the Internal Revenue Service (IRS) released the highly

.02 Unearned Income of Minor Children Taxed as if Parent's Income ("Kiddie Tax") .05 Hope and Lifetime Learning Credits 25A

.05 Hope and Lifetime Learning Credits 25A") Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.602: Tax forms and instructions. (Also Part I, 1, 23, 24, 25A, 32, 42, 59, 63, 68, 132, 135, 137, 146, 151, 170, 213, 220, 221, 512, 513,

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.602: Tax forms and instructions. (Also Part I, 1, 23, 24, 25A, 32, 42, 59, 63, 68, 132, 135, 137, 146, 151, 170, 213, 220, 221, 512, 513,

Retirement & Savings Issues Chapter 5 pp National Income TAX Workbook

Retirement & Savings Issues Chapter 5 pp. 127-156 2018 National Income TAX Workbook 1 Retirement & Savings Issues p. 127 1. Rollovers, Conversions, Recharacterizations 2. Taxation of Plan Loans and Loan

Retirement & Savings Issues Chapter 5 pp. 127-156 2018 National Income TAX Workbook 1 Retirement & Savings Issues p. 127 1. Rollovers, Conversions, Recharacterizations 2. Taxation of Plan Loans and Loan

EXEMPT ORGANIZATIONS. A. Unrelated Business Income Tax

EXEMPT ORGANIZATIONS A. Unrelated Business Income Tax 1. Clarification of unrelated business income tax treatment of entities exempt from tax under section 501(a) (sec. 5001 of the House bill and sec.

EXEMPT ORGANIZATIONS A. Unrelated Business Income Tax 1. Clarification of unrelated business income tax treatment of entities exempt from tax under section 501(a) (sec. 5001 of the House bill and sec.

CHS/COMMUNITY HEALTH SYSTEMS, INC. STANDARD 401(K) PLAN SUMMARY PLAN DESCRIPTION JANUARY 1, 2014

PLAN SUMMARY PLAN DESCRIPTION JANUARY 1, 2014") CHS/COMMUNITY HEALTH SYSTEMS, INC. STANDARD 401(K) PLAN SUMMARY PLAN DESCRIPTION JANUARY 1, 2014 TABLE OF CONTENTS PAGE INTRODUCTION TO YOUR PLAN What kind of Plan is this?... 1 What information does this

CHS/COMMUNITY HEALTH SYSTEMS, INC. STANDARD 401(K) PLAN SUMMARY PLAN DESCRIPTION JANUARY 1, 2014 TABLE OF CONTENTS PAGE INTRODUCTION TO YOUR PLAN What kind of Plan is this?... 1 What information does this

Supported Decision-Making and Financial Decisions Webinar 06/29/2015 1

Supported Decision-Making and Financial Decisions Webinar 06/29/2015 1 From Theory to Practice: Supported Decision-Making and Financial Decisions National Resource Center for Supported Decision- Making

Supported Decision-Making and Financial Decisions Webinar 06/29/2015 1 From Theory to Practice: Supported Decision-Making and Financial Decisions National Resource Center for Supported Decision- Making

EOI SERVICE COMPANY, INC. RETIREMENT & SAVINGS PLAN SUMMARY PLAN DESCRIPTION

EOI SERVICE COMPANY, INC. RETIREMENT & SAVINGS PLAN SUMMARY PLAN DESCRIPTION TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?... 1 What information does this Summary provide?... 1

EOI SERVICE COMPANY, INC. RETIREMENT & SAVINGS PLAN SUMMARY PLAN DESCRIPTION TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?... 1 What information does this Summary provide?... 1

PROBATE QUESTIONNAIRE

CATHERINE E. DAVEY, J.D., LL.M. Post Office Box 941251 Maitland, Florida 32794-1251 Telephone (407) 645-4833 Facsimile (407) 645-4832 PROBATE QUESTIONNAIRE 1. LEGAL NAME OF DECEDENT: PERMANENT RESIDENCE

CATHERINE E. DAVEY, J.D., LL.M. Post Office Box 941251 Maitland, Florida 32794-1251 Telephone (407) 645-4833 Facsimile (407) 645-4832 PROBATE QUESTIONNAIRE 1. LEGAL NAME OF DECEDENT: PERMANENT RESIDENCE

Chapter 8: Education and Able Planning. 1 08: Education & Able Planning

Page 103-133 Chapter 8: Education and Able Planning 1 Learning Objectives Page 103-133 Upon completion of this seminar, participants should be able to Identify the deduction, credits, exclusions, and investments

Page 103-133 Chapter 8: Education and Able Planning 1 Learning Objectives Page 103-133 Upon completion of this seminar, participants should be able to Identify the deduction, credits, exclusions, and investments

Advanced Markets Because You Asked

Advanced Markets Because You Asked June 2007 Answers to Questions Frequently Asked of the Advanced Markets Group The Impact of Section 409A on Nonqualified Deferred Compensation Plans Advanced Markets

Advanced Markets Because You Asked June 2007 Answers to Questions Frequently Asked of the Advanced Markets Group The Impact of Section 409A on Nonqualified Deferred Compensation Plans Advanced Markets

DOLLAR FINANCIAL GROUP RETIREMENT PLAN SUMMARY PLAN DESCRIPTION

DOLLAR FINANCIAL GROUP RETIREMENT PLAN SUMMARY PLAN DESCRIPTION TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?...1 What information does this Summary provide?...1 ARTICLE I PARTICIPATION

DOLLAR FINANCIAL GROUP RETIREMENT PLAN SUMMARY PLAN DESCRIPTION TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?...1 What information does this Summary provide?...1 ARTICLE I PARTICIPATION

2011 Federal & California Tax Update for Individuals

CALIFORNIA CPA EDUCATION FOUNDATION 2011 Federal & California Tax Update for Individuals Gary R. McBride & Thomas C. Daley January 2012 Supplement 2012 Busy Season Look-Out List Foreign Asset Reporting:

CALIFORNIA CPA EDUCATION FOUNDATION 2011 Federal & California Tax Update for Individuals Gary R. McBride & Thomas C. Daley January 2012 Supplement 2012 Busy Season Look-Out List Foreign Asset Reporting:

.01 Tax Rate Tables 1(a)-(e) .02 Unearned Income of Minor Children Taxed as if Parent s 1(g) Income ("Kiddie Tax") .03 Adoption Credit 23

-(e) .02 Unearned Income of Minor Children Taxed as if Parent s 1(g) Income (Kiddie Tax) .03 Adoption Credit 23") Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.602. Tax forms and instructions. (Also Part I, 1, 23, 24, 25A, 32, 42, 59, 62, 63, 68, 132, 135, 137, 146, 148, 151, 170, 179, 213, 220,

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.602. Tax forms and instructions. (Also Part I, 1, 23, 24, 25A, 32, 42, 59, 62, 63, 68, 132, 135, 137, 146, 148, 151, 170, 179, 213, 220,

Federal Tax Update 63rd Annual Institute on Taxation Tuesday, November 15, :30am - 9:45am

Federal Tax Update 63rd Annual Institute on Taxation Tuesday, November 15, 2016 8:30am - 9:45am By: Peter X. Bellanti, CPA Amato, Fox & Company PC 36 Niagara Street Tonawanda, NY 14150 (716) 694-0336 Email

Federal Tax Update 63rd Annual Institute on Taxation Tuesday, November 15, 2016 8:30am - 9:45am By: Peter X. Bellanti, CPA Amato, Fox & Company PC 36 Niagara Street Tonawanda, NY 14150 (716) 694-0336 Email

TEAM HEALTH, INC., 401(K) PLAN SUMMARY PLAN DESCRIPTION

PLAN SUMMARY PLAN DESCRIPTION") TEAM HEALTH, INC., 401(K) PLAN SUMMARY PLAN DESCRIPTION TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?... 1 What information does this Summary provide?... 1 ARTICLE I PARTICIPATION

TEAM HEALTH, INC., 401(K) PLAN SUMMARY PLAN DESCRIPTION TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN What kind of Plan is this?... 1 What information does this Summary provide?... 1 ARTICLE I PARTICIPATION

Tax Cuts and Jobs Act

Tax Cuts and Jobs Act Three-year holding period for LTCG treatment on on certain partnership profits interest received in connection with the performance of investment services 1.2 2 Tax Nonresident Partner

Tax Cuts and Jobs Act Three-year holding period for LTCG treatment on on certain partnership profits interest received in connection with the performance of investment services 1.2 2 Tax Nonresident Partner

SPECIAL NEEDS TRUST GUIDELINES

SPECIAL NEEDS TRUST GUIDELINES The essential purpose of a Special Needs Trust is to improve the quality of an individual s life without disqualifying them from eligibility to receive public benefits. The

SPECIAL NEEDS TRUST GUIDELINES The essential purpose of a Special Needs Trust is to improve the quality of an individual s life without disqualifying them from eligibility to receive public benefits. The