Inside The EU CCTB/CCCTB Proposals

|

|

|

- Stephanie Elliott

- 5 years ago

- Views:

Transcription

1 Inside The EU CCTB/CCCTB Proposals Prof. dr. J.L. van de Streek There is a lot going on 1

2 History Topics General policy objectives Personal and material scope Main characteristics of the tax base Specific balance sheet items Anti-BEPS aspects Consoldiation and formulary apportionment History 1999 EU Council provided a revolutionary mandate to the Commission Technical Working Group 2011 CCCTB proposal Discussions in preparatory Council bodies 2016 Relaunched CCTB/CCCTB proposal 2

3 General policy objectives Stimulating growth and investment Reducing administrative burden for companies No transfer pricing One-stop-shop Super-deduction for R&D expenses Allowance for growth and investment Cross-border loss relief General policy objectives Enhancing the fairness of the corporate income tax Mandatory for large companies Sharing formula ensures taxation where value is created TP cannot be used as aggressive tax planning tool within EU Strict anti-beps measures 3

4 Commission s view My request (ATAD1) under the EU transparency regulation Although the decision-making process related to the adoption of that Directive is finalized, as you recall in your request, the negations on these issues are not totally completed. The issues covered by these documents, namely controlled foreign companies, are controversial among Member States but remain key to achieving the objectives of the Commission's corporate tax initiatives. 4

5 Yellow cards Mandatory system for large companies Legal form requirement Subject to tax requirement Size requirement Consolidated worldwide group revenue > EUR 750 MIO Group requirement 5

6 Optional system for SME s Legal form requirement Subject to tax requirement No cross-border element required Option to apply CCTB for 5 years CCTB requires no all-in/all-out approach CCCTB requires additional choice All-in/all-out (!) Multiple CIT systems 6

7 Example 2CTB Example 3CTB 7

8 Material scope CCTB Issues subject to national corporate income tax Flexibility Tax rates Deduction for gifts and donations to charitable bodies Deduction of in-house pension funds Definition third country PE Non-regulated issues Specific interest deduction limitations National group taxation regimes? 8

9 Example A few general principles and no link to IAS/IFRS Autonomous profit definition Not linked to IAS/IFRS No starting point No fall back system Self-proclaimed principles Realization principle Accruals principle Consistent manner principle 9

10 Calculation of the tax base Profit & loss account based definition Tax base = revenues -/- exempt revenues -/- deductible expenses -/- other deductible items No tax balance sheet Business purpose test for deductibility of costs Arm s length standard Foreign income and participation exemption Three categories of foreign income PE income Income from major shareholdings (10%) Interest, royalties and income from portfolio shares Relationship with double tax treaties Intra-EU Tax treaties with third countries Article 351 TFEU? 10

11 Treatment of foreign income under CCTB Tax treaties with third countries? 11

12 Allowance for growth and investment Half-baked ACE Modeled on Aiuto alla Crescita Economica Reduction of debt/equity bias Rate = interest Eurobond + 2% risk premium Equity increases Equity decreases Example Start CCTB equity end of

13 Super deduction R&D-expenses Regular deduction at incurrence 50% additional deduction up to EUR 20 MIO R&D-expenses per year 100% additional deduction for start-ups 25% additional deduction for R&Dexpenses exceeding EUR 20 MIO Basic research, applied research and experimental development Novelty-degree not defined Loss relief Unlimited carry forward However, limitations already being discussed Anti-loss trading rule Change of ownership Major change of activity Cross-border losses First-tier subsidiaries and PE s Recapture, ultimately end of year 5 13

14 Example Specific balance sheet items Individually depreciable assets Pooled assets Non-depreciable assets Stocks and work in progress Financial assets held for trading Long-term contracts Provisions Bad debts Hedging instruments 14

15 Individually depreciable assets Commercial, office and other buildings 40 years Industrial buildings 25 years Other long-life fixed tangible assets (useful life 15 years): 15 years Medium-life fixed tangible assets (8 useful life 15 years): 8 years Fixed intangible assets: legal protection period or otherwise 15 years Pooled assets Germany, Finland, Lithuania, Sweden and UK already do it! Short-life fixed assets (1 useful life < 8 years) Fixed depreciation rate 25% Built-in roll-over relief Proceeds of disposed pooled asset is tax exempt However, pooled deprecation basis 15

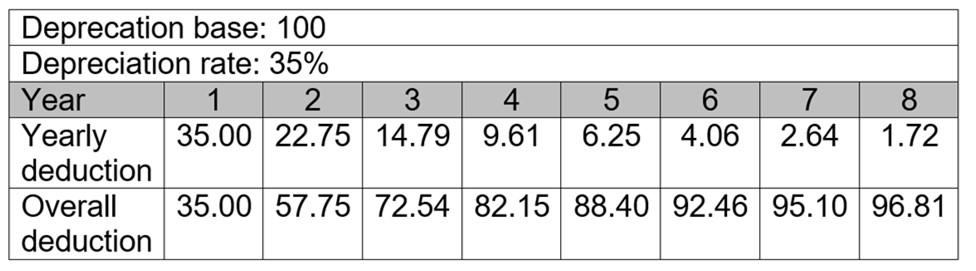

16 Example Higher depreciation rate? (35%) 16

17 Non-depreciable assets Fixed tangible asses not subject to wear and tear and/or obsolescence Financial assets However, deduction for exceptional decrease in value ( financial assets) Force majeure Criminal activities Recapture in in case of value increase Stocks and work-in-progress Valuation at direct cost of net realizable value, whichever is lower Interchangeable goods and services FIFO LIFO Weighted average costs Why does the Commission allow LIFO? IAS/IFRS and US GAAP 17

18 Financial assets and liabilities held for trading Mark-to-market treatment Trading items Held principally for the purpose of selling or repurchasing in in the short term; or Part of a portfolio of identified financial instruments and there is a pattern of shortterm profitmaking Participation exemption switched-off Long-term contracts Contract term > 12 months Concluded for the purpose of manufacturing, installing of constructing, or performing services Percentage of completion method Completion percentage = cost incurred / overall estimated costs Expert evaluation skipped 18

19 Provisions Present or future legal obligation arising from previous activities/transactions No provision Constructive obligations Contingent losses Future cost increases Reliable estimation of future expenses Discount rate set at Euribor Bad-debts Two conditions for deductibility It is probable that the debt will not be paid off wholly of partially; and The taxpayer has taken all reasonable steps to pursue payment Large number of similar debt-claims Case-by-case approach skipped No deduction for related party debt! 19

20 Hedging instruments Gains and losses on a hedging instrument follow tax treatment hedged item Examples Hedged item is participation Hedged item is financial asset held for trading Two conditions hedging relationship Formally designated and documented Highly effective Anti-beps measures General interest deduction limitation Threshold EUR 3 MIO (CCCTB: EUR 5 MIO) Switch-over clause Highly controversial Controlled foreign companies Important to eliminate TP planning towards 3 rd countries Mismatches General anti-abuse clause 20

21 Formation of a consolidated group (1) Formation of a consolidated group (2) 21

22 Formation of a consolidated group (3) Formation of a consolidated group (4) 22

23 Qualifying subsidiaries Consolidation method and effects Adding-up individual tax bases Intra-group transactions are recorded at cost No arm's length pricing No withholding taxation No comprehensive unity approach Case-by-case approach Article 69(1) CCCTB Article 9(4) CCTB 23

24 Sharing formula Massachusetts formula Assets Labour Sales Uniform formula Modified versions for financial sector, oil extraction and production sector and international transport sector Safeguard clause for unfair results Labour factor Both payroll and number of employees (50%/50%) Included in the labour factor of the group member that pays salary Definition employee depends on local law Anti-factor shifting Intra-group outsourcing External outsourcing 24

25 Asset factor Fixed tangible assets owned, rented or leased Value for tax purposes Included in the asset factor of the group member that is the economic owner Anti-factor shifting Intangibles excluded Intra-group leasing/renting External sale Sales factor Most controversial factor! Sales by destination Where the dispatch of transport of goods to the acquirer ends Where services are physically carried out or actually supplied Spread throw back rule for nowhere sales Passive income excluded, unless earned in the ordinary course of a trade or business 25

26 Principal taxpayer One-stop-shop Principal tax authority Forum shopping? How to solve disagreements between Member States? Principal tax authority vs. local tax authorities Audits and rulings Appeals White paper on the future of Europe (1 March 2017) 1. Carrying on 2. Nothing but the single market 3. Those who want to do more 4. Doing less more efficiently 5. Doing much more together 26

1. Carrying on 2.")

27 White paper on the future of Europe (1 March 2017) 1. Carrying on 2. Nothing but the single market 3. Those who want to do more 4. Doing less more efficiently 5. Doing much more together 27

C(C)CTB 28 February CORIT

CTB 28 February CORIT") C(C)CTB 28 February 2017 Agenda Introduction Determination of the tax base Anti tax avoidance legislation Consolidation and allocation One-stop-shop Political and practical perspectives Introduction Challenges

C(C)CTB 28 February 2017 Agenda Introduction Determination of the tax base Anti tax avoidance legislation Consolidation and allocation One-stop-shop Political and practical perspectives Introduction Challenges

EU Developments: C(C)CTB and corporate tax reform

CTB and corporate tax reform") EU Developments: C(C)CTB and corporate tax reform 27 October 2016 Introduction On 25 October, the European Commission published a corporate tax reform package that provides three new proposals: To provide

EU Developments: C(C)CTB and corporate tax reform 27 October 2016 Introduction On 25 October, the European Commission published a corporate tax reform package that provides three new proposals: To provide

Common (Consolidated) Corporate Tax Base what are the next steps?

Corporate Tax Base what are the next steps?") Common (Consolidated) Corporate Tax Base what are the next steps? Uwe Ihli, Head of Sector, DG TAXUD D1.003, European Commission IFA Austria, 8 October 2018, Vienna Main objectives for the taxation in

Common (Consolidated) Corporate Tax Base what are the next steps? Uwe Ihli, Head of Sector, DG TAXUD D1.003, European Commission IFA Austria, 8 October 2018, Vienna Main objectives for the taxation in

Trends I Netherlands moves away from fiscal offshore industry

1 Trends I Netherlands moves away from fiscal offshore industry The Netherlands is slowly but surely steering away from facilitating the use of its corporate income tax system by companies that are set

1 Trends I Netherlands moves away from fiscal offshore industry The Netherlands is slowly but surely steering away from facilitating the use of its corporate income tax system by companies that are set

https://dm.eesc.europa.eu/eescdocumentsearch/pages/opinionsresults.aspx?k=eco%2f419

Council of the European Union Brussels, 5 October 2017 (OR. en) Interinstitutional Files: 2016/0336 (CNS) 2016/0337 (CNS) 12848/17 FISC 210 COVER NOTE From: To: Subject: General Secretariat of the Council

Council of the European Union Brussels, 5 October 2017 (OR. en) Interinstitutional Files: 2016/0336 (CNS) 2016/0337 (CNS) 12848/17 FISC 210 COVER NOTE From: To: Subject: General Secretariat of the Council

BEPS and ATAD: Where do we stand?

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

The European Commission (EC) published four new draft European Union (EU) Directives on 25 October 2016 with proposals to:

published four new draft European Union (EU) Directives on 25 October 2016 with proposals to:") EU tax proposals seek to harmonise corporate tax bases, apply formulary apportionment, further address hybrid mismatches and improve tax dispute resolution 23 November 2016 In brief The European Commission

EU tax proposals seek to harmonise corporate tax bases, apply formulary apportionment, further address hybrid mismatches and improve tax dispute resolution 23 November 2016 In brief The European Commission

Proposal for a COUNCIL DIRECTIVE. on a Common Consolidated Corporate Tax Base (CCCTB) {SWD(2016) 341 final} {SWD(2016) 342 final}

{SWD(2016) 341 final} {SWD(2016) 342 final}") EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 683 final 2016/0336 (CNS) Proposal for a COUNCIL DIRECTIVE on a Common Consolidated Corporate Tax Base (CCCTB) {SWD(2016) 341 final} {SWD(2016) 342

EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 683 final 2016/0336 (CNS) Proposal for a COUNCIL DIRECTIVE on a Common Consolidated Corporate Tax Base (CCCTB) {SWD(2016) 341 final} {SWD(2016) 342

Tax Obstacles in Cross Border Planning

International Fiscal Association USA Branch New York Region Fall Meeting Thursday, December 1, 2016 Tax Obstacles in Cross Border Planning Colleen O Neill Ernst & Young LLP Maarten P. Maaskant PricewaterhouseCoopers

International Fiscal Association USA Branch New York Region Fall Meeting Thursday, December 1, 2016 Tax Obstacles in Cross Border Planning Colleen O Neill Ernst & Young LLP Maarten P. Maaskant PricewaterhouseCoopers

Common (Consolidated) Corporate Tax Base A Personal View

Corporate Tax Base A Personal View") Common (Consolidated) Corporate Tax Base A Personal View Christoph Spengel, University of Mannheim / ZEW IFA Austria,, Vienna Agenda 1. C(C)CTB: Institutional Background and Re-Launch 2016 2. Quantitative

Common (Consolidated) Corporate Tax Base A Personal View Christoph Spengel, University of Mannheim / ZEW IFA Austria,, Vienna Agenda 1. C(C)CTB: Institutional Background and Re-Launch 2016 2. Quantitative

TEXTS ADOPTED. having regard to the Commission proposal to the Council (COM(2016)0683),

0683),") European Parliament 2014-2019 TEXTS ADOPTED P8_TA(2018)0087 Common Consolidated Corporate Tax Base * European Parliament legislative resolution of 15 March 2018 on the proposal for a Council directive

European Parliament 2014-2019 TEXTS ADOPTED P8_TA(2018)0087 Common Consolidated Corporate Tax Base * European Parliament legislative resolution of 15 March 2018 on the proposal for a Council directive

PUBLIC /14 VI/df 1 DGG2B LIMITE EN. Councilofthe EuropeanUnion Brussels,19November2014 (OR.en) 15756/14. InterinstitutionalFile: 2011/0058(CNS)

15756/14. InterinstitutionalFile: 2011/0058(CNS)") ConseilUE Councilofthe EuropeanUnion Brussels,19November2014 (OR.en) InterinstitutionalFile: 2011/0058(CNS) PUBLIC 15756/14 LIMITE FISC197 NOTE From: To: Presidency WorkingPartyonTaxQuestions -DirectTaxation

ConseilUE Councilofthe EuropeanUnion Brussels,19November2014 (OR.en) InterinstitutionalFile: 2011/0058(CNS) PUBLIC 15756/14 LIMITE FISC197 NOTE From: To: Presidency WorkingPartyonTaxQuestions -DirectTaxation

The Controlled Foreign Company Regime in the EU CCTB Proposal

The Controlled Foreign Company Regime in the EU CCTB Proposal Werner Haslehner Professor for European and International Tax Law ATOZ Chair for European and International Taxation University of Luxembourg

The Controlled Foreign Company Regime in the EU CCTB Proposal Werner Haslehner Professor for European and International Tax Law ATOZ Chair for European and International Taxation University of Luxembourg

EU state aid and other developments. 18 November 2016

EU state aid and other developments 18 November 2016 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer

EU state aid and other developments 18 November 2016 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer

The Arm s Length Standard: a Blind Spot in the CC(C)TB Proposals. Amsterdam, 27 January First Critical Analysis Prof.dr. D.S.

TB Proposals. Amsterdam, 27 January First Critical Analysis Prof.dr. D.S.") The Arm s Length Standard: a Blind Spot in the CC(C)TB Proposals Amsterdam, 27 January 2017 The Return of the CC(C)TB: First Critical Analysis Prof.dr. D.S. Smit Menu for the next 20 minutes What arm s

The Arm s Length Standard: a Blind Spot in the CC(C)TB Proposals Amsterdam, 27 January 2017 The Return of the CC(C)TB: First Critical Analysis Prof.dr. D.S. Smit Menu for the next 20 minutes What arm s

Common Corporate Tax Base (CCTB) and Common Consolidated Corporate Tax Base (CCCTB)

and Common Consolidated Corporate Tax Base (CCCTB)") POSITION PAPER 22 nd February 2017 Common Corporate Tax Base (CCTB) and Common Consolidated Corporate Tax Base (CCCTB) 1 2 3 KEY MESSAGES A Common EU Consolidated Corporate Tax Base (CCCTB), has the potential,

POSITION PAPER 22 nd February 2017 Common Corporate Tax Base (CCTB) and Common Consolidated Corporate Tax Base (CCCTB) 1 2 3 KEY MESSAGES A Common EU Consolidated Corporate Tax Base (CCCTB), has the potential,

GERMANY GLOBAL GUIDE TO M&A TAX: 2017 EDITION

GERMANY 1 GERMANY INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Germany has recently seen some legislative developments

GERMANY 1 GERMANY INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Germany has recently seen some legislative developments

STEP Silicon Valley Ireland: Gateway to Accessing the EU Market

STEP Silicon Valley Ireland: Gateway to Accessing the EU Market Mark O Sullivan and Pat English August 17, 2016 Financial Times 2012-2015 Matheson is ranked in the FT s top 10 European law firms 2015.

STEP Silicon Valley Ireland: Gateway to Accessing the EU Market Mark O Sullivan and Pat English August 17, 2016 Financial Times 2012-2015 Matheson is ranked in the FT s top 10 European law firms 2015.

Tackling Aggressive Tax Planning in the European Union - Recent Developments

Tackling Aggressive Tax Planning in the European Union - Recent Developments Dr Christiana HJI Panayi Senior Lecturer in Tax Law Queen Mary University of London 1 Important recent developments Digital

Tackling Aggressive Tax Planning in the European Union - Recent Developments Dr Christiana HJI Panayi Senior Lecturer in Tax Law Queen Mary University of London 1 Important recent developments Digital

Cyprus Tax Update. Kyiv May 2018

Cyprus Tax Update Kyiv May 2018 Today s agenda 1. Snapshot of Cyprus tax system 2. Developments affecting the Cyprus tax regime 3. Selected developments : a) ATAD b) TP 4. Selected structures 5. Expected

Cyprus Tax Update Kyiv May 2018 Today s agenda 1. Snapshot of Cyprus tax system 2. Developments affecting the Cyprus tax regime 3. Selected developments : a) ATAD b) TP 4. Selected structures 5. Expected

European Commission publishes Anti Tax Avoidance Package

28 January 2016 - Number 65 Brazil Desk e-mail bulletin European Commission publishes Anti Tax Avoidance Package On 28 January 2016 the European Commission published an Anti Tax Avoidance Package containing

28 January 2016 - Number 65 Brazil Desk e-mail bulletin European Commission publishes Anti Tax Avoidance Package On 28 January 2016 the European Commission published an Anti Tax Avoidance Package containing

Common (Consolidated) Corporate Tax Base The EC s re-launch proposals for a Council Directive on a CCTB (685) and a CCCTB (683) of 25 October 2016

Corporate Tax Base The EC s re-launch proposals for a Council Directive on a CCTB (685) and a CCCTB (683) of 25 October 2016") Common (Consolidated) Corporate Tax Base The EC s re-launch proposals for a Council Directive on a CCTB (685) and a CCCTB (683) of 25 October 2016 Prof. Dr. Luc De Broe (KU Leuven) Holder of the Deloitte

Common (Consolidated) Corporate Tax Base The EC s re-launch proposals for a Council Directive on a CCTB (685) and a CCCTB (683) of 25 October 2016 Prof. Dr. Luc De Broe (KU Leuven) Holder of the Deloitte

The OECD s 3 Major Tax Initiatives

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

2 National tax systems: Structure and recent developments

Ireland Structure and development of tax revenues Table IE.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Ranking Revenue (billion euros) A. Structure by type of

Ireland Structure and development of tax revenues Table IE.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Ranking Revenue (billion euros) A. Structure by type of

ROMANIA GLOBAL GUIDE TO M&A TAX: 2018 EDITION

ROMANIA 1 ROMANIA INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? The new Romanian Fiscal Code, in force starting 1 January

ROMANIA 1 ROMANIA INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? The new Romanian Fiscal Code, in force starting 1 January

BUDGET DAY CORPORATE AND INTERNATIONAL TAXATION

NEWSFLASH SEPTEMBER 2018 BUDGET DAY 2018 - CORPORATE AND INTERNATIONAL TAXATION This week, Budget Day 2018 in the Netherlands brought a collection of fiscal legislative proposals which might have an impact

NEWSFLASH SEPTEMBER 2018 BUDGET DAY 2018 - CORPORATE AND INTERNATIONAL TAXATION This week, Budget Day 2018 in the Netherlands brought a collection of fiscal legislative proposals which might have an impact

Base erosion & profit shifting (BEPS) 25 May 2016

25 May 2016") Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Dutch Tax Bill 2019: what will change?

1 Dutch Tax Bill 2019: what will change? On 18 September 2018, the Dutch government presented a number of tax measures as part of the 2019 budget proposals. The key measures are: Abolition of withholding

1 Dutch Tax Bill 2019: what will change? On 18 September 2018, the Dutch government presented a number of tax measures as part of the 2019 budget proposals. The key measures are: Abolition of withholding

BEPS - Current Status of Implementation in EU Countries. Prof. Guglielmo Maisto 1 March 2019

BEPS - Current Status of Implementation in EU Countries Prof. Guglielmo Maisto 1 March 2019 1 Pillar I COHERENCE Action 2 Neutralizing Hybrid Mismatch Arrangements Action 3 CFC Rules Action 4 Interest

BEPS - Current Status of Implementation in EU Countries Prof. Guglielmo Maisto 1 March 2019 1 Pillar I COHERENCE Action 2 Neutralizing Hybrid Mismatch Arrangements Action 3 CFC Rules Action 4 Interest

INCEPTION IMPACT ASSESSMENT

TITLE OF THE INITIATIVE LEAD DG RESPONSIBLE UNIT AP NUMBER LIKELY TYPE OF INITIATIVE INCEPTION IMPACT ASSESSMENT Re-launch of the Common Consolidated Corporate Tax Base (CCCTB) DG TAXUD.D DATE OF ROADMAP

TITLE OF THE INITIATIVE LEAD DG RESPONSIBLE UNIT AP NUMBER LIKELY TYPE OF INITIATIVE INCEPTION IMPACT ASSESSMENT Re-launch of the Common Consolidated Corporate Tax Base (CCCTB) DG TAXUD.D DATE OF ROADMAP

EU Anti-Tax Avoidance Directive 2: hybrid mismatches with third countries

EU Anti-Tax Avoidance Directive 2: hybrid mismatches with third countries On February 21, 2017 the EU Member States reached agreement on a Directive that will amend the Anti-Tax Avoidance Directive (Council

EU Anti-Tax Avoidance Directive 2: hybrid mismatches with third countries On February 21, 2017 the EU Member States reached agreement on a Directive that will amend the Anti-Tax Avoidance Directive (Council

LUXEMBOURG GLOBAL GUIDE TO M&A TAX: 2018 EDITION

LUXEMBOURG 1 LUXEMBOURG INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Corporate income tax ( CIT ) rate The CIT rate

LUXEMBOURG 1 LUXEMBOURG INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Corporate income tax ( CIT ) rate The CIT rate

COMPARISON OF EUROPEAN HOLDING COMPANY REGIMES

COMPARISON OF EUROPEAN HOLDING COMPANY REGIMES This analysis provides an indicative guide only and advice from appropriate country specialists should always be sought. Particular attention should be given

COMPARISON OF EUROPEAN HOLDING COMPANY REGIMES This analysis provides an indicative guide only and advice from appropriate country specialists should always be sought. Particular attention should be given

The EU draft anti-avoidance directive (ATAD) A focus on CFC rules from a Swiss perspective

A focus on CFC rules from a Swiss perspective") The EU draft anti-avoidance directive (ATAD) A focus on CFC rules from a Swiss perspective Prof. Dr. Robert Danon Professor of Swiss and International Tax Law at the University of Lausanne Of counsel,

The EU draft anti-avoidance directive (ATAD) A focus on CFC rules from a Swiss perspective Prof. Dr. Robert Danon Professor of Swiss and International Tax Law at the University of Lausanne Of counsel,

PUBLIC EXPLANATORYNOTES

ConseilUE Councilofthe EuropeanUnion Brussels,19November2014 (OR.en) InterinstitutionalFile: 2011/0058(CNS) PUBLIC 15756/14 ADD1 LIMITE FISC197 NOTE From: To: Presidency WorkingPartyonTaxQuestions -DirectTaxation

ConseilUE Councilofthe EuropeanUnion Brussels,19November2014 (OR.en) InterinstitutionalFile: 2011/0058(CNS) PUBLIC 15756/14 ADD1 LIMITE FISC197 NOTE From: To: Presidency WorkingPartyonTaxQuestions -DirectTaxation

Public consultation on the Re-launch of the Common Consolidated Corporate Tax Base (CCCTB)

") Case Id: 5a071abb-ae23-4826-ad80-b98d1501271a Date: 05/01/2016 21:33:39 Public consultation on the Re-launch of the Common Consolidated Corporate Tax Base (CCCTB) Fields marked with are mandatory. 1 Introduction

Case Id: 5a071abb-ae23-4826-ad80-b98d1501271a Date: 05/01/2016 21:33:39 Public consultation on the Re-launch of the Common Consolidated Corporate Tax Base (CCCTB) Fields marked with are mandatory. 1 Introduction

Cyprus Country Profile

Cyprus Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

Cyprus Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL. Building a fair, competitive and stable corporate tax system for the EU

EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 682 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Building a fair, competitive and stable corporate tax system

EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 682 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Building a fair, competitive and stable corporate tax system

ATRiD: Harmonizing the rules on the allocation of taxing rights within the EU and in the relations with third countries

ATRiD: Harmonizing the rules on the allocation of taxing rights within the EU and in the relations with third countries Paolo Arginelli 1This contribution lays down a general plan for what the EU should

ATRiD: Harmonizing the rules on the allocation of taxing rights within the EU and in the relations with third countries Paolo Arginelli 1This contribution lays down a general plan for what the EU should

Taxation of cross-border mergers and acquisitions

Taxation of cross-border mergers and acquisitions Cyprus kpmg.com/tax KPMG International Cyprus Introduction The Income Tax Law No.118 (I) 2002 introduced major reforms of Cyprus s tax system at the time

Taxation of cross-border mergers and acquisitions Cyprus kpmg.com/tax KPMG International Cyprus Introduction The Income Tax Law No.118 (I) 2002 introduced major reforms of Cyprus s tax system at the time

- Simplification rule for pure intermediary companies : remuneration

Theme Source of law Object / Date of application PAST CHANGES Impact / Comments 1. Transfer Pricing Article 56 of the Luxembourg Income Tax Law (LIR) and paragraph 171 Abgabenordnung Introduction of the

Theme Source of law Object / Date of application PAST CHANGES Impact / Comments 1. Transfer Pricing Article 56 of the Luxembourg Income Tax Law (LIR) and paragraph 171 Abgabenordnung Introduction of the

Memorandum. 1. Introduction

Memorandum TO FROM AFP Prof. dr. J.L. van de Streek* REF 18232381-v1 DATE 4 March 2015 RE State of play CCCTB - spring 2015 1. Introduction On 16 March 2011 the European Commission published its Proposal

Memorandum TO FROM AFP Prof. dr. J.L. van de Streek* REF 18232381-v1 DATE 4 March 2015 RE State of play CCCTB - spring 2015 1. Introduction On 16 March 2011 the European Commission published its Proposal

Cyprus Country Profile

Cyprus Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

Cyprus Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

International Tax Primer. Third Edition. Brian J. Arnold

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

Dutch Tax Bill 2018: what will change?

1 Dutch Tax Bill 2018: what will change? The Dutch government has presented its Tax Bill 2018. Three amendments are particularly relevant for multinationals, international investors and investment funds

1 Dutch Tax Bill 2018: what will change? The Dutch government has presented its Tax Bill 2018. Three amendments are particularly relevant for multinationals, international investors and investment funds

EU Commission approves enhancements to Madeira International Business Center Tax Regime

3 September 2013 EU Commission approves enhancements to Madeira International Business Center Tax Regime Executive summary On 2 July 2013, the EU Commission issued a decision allowing Portugal to increase

3 September 2013 EU Commission approves enhancements to Madeira International Business Center Tax Regime Executive summary On 2 July 2013, the EU Commission issued a decision allowing Portugal to increase

INTRODUCTION 2019 TAX PLAN

2019 DUTCH TAX PLAN INTRODUCTION During Budget Day (18 September 2018) in the Netherlands a number tax plans were published. Please find below a selection of the most relevant proposals PERSONAL INCOME

2019 DUTCH TAX PLAN INTRODUCTION During Budget Day (18 September 2018) in the Netherlands a number tax plans were published. Please find below a selection of the most relevant proposals PERSONAL INCOME

IBFD Course Programme International Tax Planning after BEPS and the MLI

IBFD Course Programme International Tax Planning after BEPS and the MLI Summary Recent developments such as the BEPS project and the Multilateral Instrument in international taxation, but also unilateral

IBFD Course Programme International Tax Planning after BEPS and the MLI Summary Recent developments such as the BEPS project and the Multilateral Instrument in international taxation, but also unilateral

Residual Profit Allocation Proposal

Residual Profit Allocation Proposal Michael Devereux July 14, 2016 Aim Incremental change to existing separate accounting system Aim to reduce: opportunities for profit shifting sensitivity of location

Residual Profit Allocation Proposal Michael Devereux July 14, 2016 Aim Incremental change to existing separate accounting system Aim to reduce: opportunities for profit shifting sensitivity of location

Tax footprint report 2017

Tax Footprint 2017 Tax footprint report 2017 This tax footprint report is a non-audited report, where Kemira publishes its global tax policy and key tax figures. Kemira s quantitative tax analysis is prepared

Tax Footprint 2017 Tax footprint report 2017 This tax footprint report is a non-audited report, where Kemira publishes its global tax policy and key tax figures. Kemira s quantitative tax analysis is prepared

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

International Tax Netherlands Highlights 2018

International Tax Netherlands Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS/IFRS/Dutch GAAP. Financial statements must

International Tax Netherlands Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS/IFRS/Dutch GAAP. Financial statements must

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS)

") Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

2 National tax systems: Structure and recent developments

2 National tax systems: Structure and recent developments United Kingdom Structure and development of tax revenues Table UK.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

2 National tax systems: Structure and recent developments United Kingdom Structure and development of tax revenues Table UK.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

What s New in the 2016 US Model Treaty?

What s New in the 2016 US Model Treaty? Panelists: Lori Hellkamp, Jones Day Danielle Rolfes, U.S. Treasury Department David G. Shapiro, Saul Ewing LLP Gretchen Sierra, Deloitte Tax LLP Jason Yen, U.S.

What s New in the 2016 US Model Treaty? Panelists: Lori Hellkamp, Jones Day Danielle Rolfes, U.S. Treasury Department David G. Shapiro, Saul Ewing LLP Gretchen Sierra, Deloitte Tax LLP Jason Yen, U.S.

Tax & Legal Weekly Alert

Tax & Legal Weekly Alert 2-6 April 2018 In this issue: Major changes to the Tax Code Law no. 72/2018, Government Emergency Ordinance no. 18/2018, Government Emergency Ordinance no. 25/2018 amended recently

Tax & Legal Weekly Alert 2-6 April 2018 In this issue: Major changes to the Tax Code Law no. 72/2018, Government Emergency Ordinance no. 18/2018, Government Emergency Ordinance no. 25/2018 amended recently

Principles of International Taxation

Overview and Learning Objectives This tax course is designed to provide participants with the essentials of international taxation. The first three days are dedicated to the fundamental concepts relevant

Overview and Learning Objectives This tax course is designed to provide participants with the essentials of international taxation. The first three days are dedicated to the fundamental concepts relevant

Skatteverket International Tax Planning 2016 CORIT

Skatteverket International Tax Planning Agenda Introduction General remarks on International Tax Planning Analysis of International Tax Planning Models and Indicators International IP Tax Planning and

Skatteverket International Tax Planning Agenda Introduction General remarks on International Tax Planning Analysis of International Tax Planning Models and Indicators International IP Tax Planning and

RSM InterTax Tax Insights February Belgian corporate income tax reform

RSM InterTax Tax Insights February 2018 Belgian corporate income tax reform Most of the measures announced by the 2017 Belgian summer agreement were finally adopted in the Law of 25 December 2017 on the

RSM InterTax Tax Insights February 2018 Belgian corporate income tax reform Most of the measures announced by the 2017 Belgian summer agreement were finally adopted in the Law of 25 December 2017 on the

Tax Provisions in Administration s FY 2016 Budget Proposals

Tax Provisions in Administration s FY 2016 Budget Proposals International February 2015 kpmg.com HIGHLIGHTS OF INTERNATIONAL TAX PROVISIONS IN THE ADMINISTRATION S FISCAL YEAR 2016 BUDGET KPMG has prepared

Tax Provisions in Administration s FY 2016 Budget Proposals International February 2015 kpmg.com HIGHLIGHTS OF INTERNATIONAL TAX PROVISIONS IN THE ADMINISTRATION S FISCAL YEAR 2016 BUDGET KPMG has prepared

Finland. Structure and development of tax revenues. National tax systems: Structure and recent developments. Table FI.1: Tax Revenue (% of GDP)

") Finland Structure and development of tax revenues Table FI.1: Tax Revenue (% of GDP) 00 003 004 005 006 007 008 009 010 011 01 013 Ranking Revenue (billion euros) A. Structure by type of tax Indirect taxes

Finland Structure and development of tax revenues Table FI.1: Tax Revenue (% of GDP) 00 003 004 005 006 007 008 009 010 011 01 013 Ranking Revenue (billion euros) A. Structure by type of tax Indirect taxes

IMF Revenue Mobilizations and Development Conference: Session on Business Taxation. Alan Carter (ITD) Washington DC, April 18, 2011

Washington DC, April 18, 2011") IMF Revenue Mobilizations and Development Conference: Session on Business Taxation Alan Carter (ITD) Washington DC, April 18, 2011 International Business Tax Issues - Why are international tax issues important?

IMF Revenue Mobilizations and Development Conference: Session on Business Taxation Alan Carter (ITD) Washington DC, April 18, 2011 International Business Tax Issues - Why are international tax issues important?

Welcome to the EFS-seminar. BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt

Welcome to the EFS-seminar BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt Rotterdam February 3, 2016 Agenda Seminar An update on the transfer pricing

Welcome to the EFS-seminar BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt Rotterdam February 3, 2016 Agenda Seminar An update on the transfer pricing

To the Finance Standing Committee of the Lower House of Parliament Mr. R.F. Berck P.O. Box EA THE HAGUE. Amsterdam, 15 November 2016

To the Finance Standing Committee of the Lower House of Parliament Mr. R.F. Berck P.O. Box 20018 2500 EA THE HAGUE Amsterdam, 15 November 2016 Subject: Comments from the Committee on Legislative Proposals

To the Finance Standing Committee of the Lower House of Parliament Mr. R.F. Berck P.O. Box 20018 2500 EA THE HAGUE Amsterdam, 15 November 2016 Subject: Comments from the Committee on Legislative Proposals

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

Japan. Introduction Taxable income. 1. Corporate Income Tax Type of tax system Taxable persons

This chapter is based on information available up to 1 January 2010. Introduction Taxes in Japan are imposed by both the national government and local authorities. Companies are subject to corporation

This chapter is based on information available up to 1 January 2010. Introduction Taxes in Japan are imposed by both the national government and local authorities. Companies are subject to corporation

BEPS: What does it mean for funds and asset managers?

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

Latvia Country Profile

Latvia Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Latvia EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

Latvia Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Latvia EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

POSITION PAPER EU CONSULTATION ON FAIR TAXATION OF THE DIGITAL ECONOMY

Opinion Statement FC 10/2017 POSITION PAPER EU CONSULTATION ON FAIR TAXATION OF THE DIGITAL ECONOMY Prepared by the CFE Fiscal Committee Submitted to the EU Institutions on 6 December 2017 The CFE (Confédération

Opinion Statement FC 10/2017 POSITION PAPER EU CONSULTATION ON FAIR TAXATION OF THE DIGITAL ECONOMY Prepared by the CFE Fiscal Committee Submitted to the EU Institutions on 6 December 2017 The CFE (Confédération

US Taxation- A Primer

WIRC of the ICAI- Seminar Series on Global Updates- I US Taxation- A Primer Presented by : 7 th May, 2011 CA. Shishir Lagu Session Overview Introduction Corporate Tax Overview Federal Income Tax State

WIRC of the ICAI- Seminar Series on Global Updates- I US Taxation- A Primer Presented by : 7 th May, 2011 CA. Shishir Lagu Session Overview Introduction Corporate Tax Overview Federal Income Tax State

International Tax Poland Highlights 2018

International Tax Poland Highlights 2018 Investment basics: Currency Polish Zloty (PLN) Foreign exchange control None (generally) for transactions with EU, EEA, OECD and some other countries. Permission

International Tax Poland Highlights 2018 Investment basics: Currency Polish Zloty (PLN) Foreign exchange control None (generally) for transactions with EU, EEA, OECD and some other countries. Permission

Headquarter Jurisdictions Around the World: A Comparison

Headquarter Jurisdictions Around the World: A Comparison 2017 Austria Belgium Cyprus Dubai Hong Kong Ireland Luxembourg The Netherlands Portugal Singapore Spain Switzerland United Kingdom Headquarter jurisdictions

Headquarter Jurisdictions Around the World: A Comparison 2017 Austria Belgium Cyprus Dubai Hong Kong Ireland Luxembourg The Netherlands Portugal Singapore Spain Switzerland United Kingdom Headquarter jurisdictions

Tax Management International Forum

Tax Management International Forum Comparative Tax Law for the International Practitioner Reproduced with permission from Tax Management International Forum, 38 FORUM 14, 6/5/17. Copyright 姝 2017 by The

Tax Management International Forum Comparative Tax Law for the International Practitioner Reproduced with permission from Tax Management International Forum, 38 FORUM 14, 6/5/17. Copyright 姝 2017 by The

THE TAXATION OF PRIVATE EQUITY IN ITALY

THE TAXATION OF PRIVATE EQUITY IN ITALY 1 Index 1 INTRODUCTION 3 1.1 Tax environment 5 1.2 Taxation system 5 1.2.1 Corporate Income Tax IRES 6 1.2.2 Regional Production Tax IRAP 9 2 TAXATION OF ITALIAN

THE TAXATION OF PRIVATE EQUITY IN ITALY 1 Index 1 INTRODUCTION 3 1.1 Tax environment 5 1.2 Taxation system 5 1.2.1 Corporate Income Tax IRES 6 1.2.2 Regional Production Tax IRAP 9 2 TAXATION OF ITALIAN

2017 Professional Practice Update Investment Fund Industry

2017 Professional Practice Update Investment Fund Industry 1 March 2017, Luxembourg Agenda 08:30 09:00 Registration & breakfast 09:00 09:05 Chairperson s opening remarks Jason Rea, Chairperson, ABIAL 09:05

2017 Professional Practice Update Investment Fund Industry 1 March 2017, Luxembourg Agenda 08:30 09:00 Registration & breakfast 09:00 09:05 Chairperson s opening remarks Jason Rea, Chairperson, ABIAL 09:05

BELGIUM GLOBAL GUIDE TO M&A TAX: 2018 EDITION

BELGIUM 1 BELGIUM INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? A major corporate income tax reform has been published

BELGIUM 1 BELGIUM INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? A major corporate income tax reform has been published

IBFD Course Programme Principles of International Taxation

IBFD Course Programme Principles of International Taxation Need a good base to start your career in international tax? This course will provide the essential knowledge you need and give you the confidence

IBFD Course Programme Principles of International Taxation Need a good base to start your career in international tax? This course will provide the essential knowledge you need and give you the confidence

BUSINESS IN THE UK A ROUTE MAP

1 BUSINESS IN THE UK A ROUTE MAP 18 chapter 02 Anyone wishing to set up business operations in the UK for the first time has a number of options for structuring those operations. There are a number of

1 BUSINESS IN THE UK A ROUTE MAP 18 chapter 02 Anyone wishing to set up business operations in the UK for the first time has a number of options for structuring those operations. There are a number of

LIVE WEBCAST UPDATE ON BEPS PROJECT. 26 May :00pm 2:00pm (CEST)

") LIVE WEBCAST UPDATE ON BEPS PROJECT 26 May 2014 1:00pm 2:00pm (CEST) Speakers Pascal Saint-Amans Director, Centre for Tax Policy and Administration Raffaele Russo Head of BEPS Project Marlies de Ruiter

LIVE WEBCAST UPDATE ON BEPS PROJECT 26 May 2014 1:00pm 2:00pm (CEST) Speakers Pascal Saint-Amans Director, Centre for Tax Policy and Administration Raffaele Russo Head of BEPS Project Marlies de Ruiter

Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

1. OECD publishes 77 comments on transfer pricing guidelines for intra-group services, dispute resolution

1. OECD publishes 77 comments on transfer pricing guidelines for intra-group services, dispute resolution The OECD published 77 responses to its request for suggestions on how to improve the OECD transfer

1. OECD publishes 77 comments on transfer pricing guidelines for intra-group services, dispute resolution The OECD published 77 responses to its request for suggestions on how to improve the OECD transfer

Fair taxation of the digital European Commission DG TAXUD. economy

Fair taxation of the digital European Commission DG TAXUD economy The issue at stake Difficulty to tax/ opportunities for tax avoidance Lack of a level playing field and distortion of competition Less

Fair taxation of the digital European Commission DG TAXUD economy The issue at stake Difficulty to tax/ opportunities for tax avoidance Lack of a level playing field and distortion of competition Less

International Tax Belgium Highlights 2018

International Tax Belgium Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements Belgian GAAP. IFRS is mandatory for consolidated

International Tax Belgium Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements Belgian GAAP. IFRS is mandatory for consolidated

OECD releases final BEPS package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

A8-0189/ Proposal for a directive (COM(2016)0026 C8-0031/ /0011(CNS)) Text proposed by the Commission

0026 C8-0031/ /0011(CNS)) Text proposed by the Commission") 3.6.2016 A8-0189/ 001-091 AMDMTS 001-091 by the Committee on Economic and Monetary Affairs Report Hugues Bayet Rules against tax avoidance practices A8-0189/2016 (COM(2016)0026 C8-0031/2016 2016/0011(CNS))

3.6.2016 A8-0189/ 001-091 AMDMTS 001-091 by the Committee on Economic and Monetary Affairs Report Hugues Bayet Rules against tax avoidance practices A8-0189/2016 (COM(2016)0026 C8-0031/2016 2016/0011(CNS))

Proposed Amendments to the Interests and Royalties Directive 2003/49/EC : Toward an harmonization with the Parent / Subsidiary Directive

Proposed Amendments to the Interests and Royalties Directive 2003/49/EC : Toward an harmonization with the Parent / Subsidiary Directive Vincent Agulhon April 13, 2012 1 I - Directive 2003/49/EC : The

Proposed Amendments to the Interests and Royalties Directive 2003/49/EC : Toward an harmonization with the Parent / Subsidiary Directive Vincent Agulhon April 13, 2012 1 I - Directive 2003/49/EC : The

International Tax Slovenia Highlights 2018

International Tax Slovenia Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Bank accounts may be held and repatriation payments made in any currency. Accounting principles/financial

International Tax Slovenia Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Bank accounts may be held and repatriation payments made in any currency. Accounting principles/financial

Switzerland. Investment basics

Switzerland Diego Weder Director Tel: +1 212 492 4432 diweder@deloitte.com Investment basics Currency Swiss Franc (CHF) Foreign exchange control restrictions are imposed on the import or export of capital.

Switzerland Diego Weder Director Tel: +1 212 492 4432 diweder@deloitte.com Investment basics Currency Swiss Franc (CHF) Foreign exchange control restrictions are imposed on the import or export of capital.

KPMG. To Achim Pross Head, International Co-operation and Tax Administration Division OECD/CTPA. Date 30 April 2015

KPMG International To Achim Pross Head, International Co-operation and Tax Administration Division OECD/CTPA Date From KPMG s Global International Tax Services Professionals Ref KPMG OECD CFC Action 3

KPMG International To Achim Pross Head, International Co-operation and Tax Administration Division OECD/CTPA Date From KPMG s Global International Tax Services Professionals Ref KPMG OECD CFC Action 3

Hot topics Treasury seminar

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

An overview of the main issues that emerged at the fourth meeting of the subgroup on assets (SG1)

") EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Analyses and tax policies Analysis and Coordination of tax policies Brussels, 19 May 2006 Taxud E1 MH/FF CCCTB\WP\032\doc\en Orig. EN

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Analyses and tax policies Analysis and Coordination of tax policies Brussels, 19 May 2006 Taxud E1 MH/FF CCCTB\WP\032\doc\en Orig. EN

Germany. Structure and development of tax revenues. National tax systems: Structure and recent developments. Table DE.1: Tax Revenue (% of GDP)

") Germany Structure and development of tax revenues Table DE.1: Tax Revenue (% of GDP) 00 003 004 005 006 007 008 009 010 011 01 013 Ranking Revenue (billion euros) A. Structure by type of tax Indirect taxes

Germany Structure and development of tax revenues Table DE.1: Tax Revenue (% of GDP) 00 003 004 005 006 007 008 009 010 011 01 013 Ranking Revenue (billion euros) A. Structure by type of tax Indirect taxes

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February AM PM Conrad Hotel, Hong Kong

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

International Tax Greece Highlights 2018

International Tax Greece Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Capital controls are in force and certain limitations still apply on bank withdrawals and bank transfers

International Tax Greece Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Capital controls are in force and certain limitations still apply on bank withdrawals and bank transfers

U.S. Tax Legislation Corporate and International Provisions. Corporate Law Provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

Hybrid mismatches with third countries

Briefing EU Legislation in Progress CONTENTS Background Parliament s starting position Council starting position Proposal Preparation of the proposal The changes the proposal would bring Views Advisory

Briefing EU Legislation in Progress CONTENTS Background Parliament s starting position Council starting position Proposal Preparation of the proposal The changes the proposal would bring Views Advisory

The International Tax Landscape

and EU Tax Reforms How will Ireland, Luxembourg, Netherlands and Switzerland Reform Their Tax Systems to Comply?, Loyens & Loeff NV, PricewatershouseCoopers, PricewaterhouseCoopers 67 th Annual Tax Conference

and EU Tax Reforms How will Ireland, Luxembourg, Netherlands and Switzerland Reform Their Tax Systems to Comply?, Loyens & Loeff NV, PricewatershouseCoopers, PricewaterhouseCoopers 67 th Annual Tax Conference

International Tax Portugal Highlights 2018

International Tax Portugal Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Portugal does not have exchange controls and there are no restrictions on the import or export

International Tax Portugal Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Portugal does not have exchange controls and there are no restrictions on the import or export

Global Tax Trends Impact on US MNCs. December 1, 2017

Global Tax Trends Impact on US MNCs December 1, 2017 1 Panel Panelists Michael J. Caballero, Partner, Covington & Burling LLP, Washington, DC Robert B. Stack, Managing Director, Washington National and

Global Tax Trends Impact on US MNCs December 1, 2017 1 Panel Panelists Michael J. Caballero, Partner, Covington & Burling LLP, Washington, DC Robert B. Stack, Managing Director, Washington National and

ACTL Conference on REITs

ACTL Conference on REITs Recent tax treaty developments and their implications for REITs November 14, 2014 Prof. Arnaud de Graaf degraaf@law.eur.nl 0.0- Introduction 1. REITs in cross-border context 2.

ACTL Conference on REITs Recent tax treaty developments and their implications for REITs November 14, 2014 Prof. Arnaud de Graaf degraaf@law.eur.nl 0.0- Introduction 1. REITs in cross-border context 2.