Investment deduction for R&D

|

|

|

- Dorthy Heath

- 5 years ago

- Views:

Transcription

Government Innovation and Investment")

1 Investment deduction for R&D Jan Pattyn Senior Director (Deloitte) Government Innovation and Investment Incentives Pieter Spinc le Consultant PhD (Deloitte) Government Innovation and Investment Incentives

2 Introduction 3 Definition of R&D 5 Investment deduction for R&D Introduction 14 Benefits and requirements 17 Conclusion 27 Contact details 29

3 2017 Deloitte Belgium Introduction

4 Introduction

5 Definition of R&D R & D cannot be taught, It can only be done. Haresh Sippy 2017 Deloitte Belgium

6 R&D Definition Law (Art WIB92 R&D types of activity) Fundamental Research Experimental or theoretical work undertaken primarily to acquire new knowledge of the underlying foundations of phenomena and observable facts, without any direct commercial application or use in view. Industrial Research The planned research or critical investigation aimed at the acquisition of new knowledge and skills for developing new products, processes or services or for bringing about a significant improvement in existing products, processes or services. It comprises the creation of components parts of complex systems, and may include the construction of prototypes in a laboratory environment or in an environment with simulated interfaces to existing systems as well as of pilot lines, when necessary for the industrial research and notably for generic technology validation Deloitte Belgium Experimental Development Acquiring, combining, shaping and using existing scientific, technological, business and other relevant knowledge and skills with the aim of developing new or improved products, processes or services. This may also include, for example, activities aiming at the conceptual definition, planning and documentation of new products, processes or services. Experimental development may comprise prototyping, demonstrating, piloting, testing and validation of new or improved products, processes or services in environments representative of real life operating conditions where the primary objective is to make further technical improvements on products, processes or services that are not substantially set. This may include the development of a commercially usable prototype or pilot which is necessarily the final commercial product and which is too expensive to produce for it to be used only for demonstration and validation purposes. Experimental development does not include routine or periodic changes made to existing products, production lines, manufacturing processes, services and other operations in progress, even if those changes may represent improvements.

7 R&D Definition Frascati (7 th ed. October 2015) R&D types of activity Basic Research Experimental or theoretical work undertaken primarily to acquire new knowledge of the underlying foundations of phenomena and observable facts, without any particular application or use in view Research and experimental development (R&D) comprise creative and systematic work undertaken in order to increase the stock of knowledge including knowledge of humankind, culture and society and to devise new applications of available knowledge Applied Research Original investigation undertaken in order to acquire new knowledge. It is, however, directed primarily towards a specific, practical aim or objective. Experimental Development Systematic work, drawing on knowledge gained from research and practical experience and producing additional knowledge, which is directed to producing new products or processes or to improving existing products or processes 2016 Deloitte Belgium

8 R&D Definition R&D criteria (Frascati manual) NOVEL To be aimed at new findings CREATIVE UNCERTAIN SYSTEMATIC CREATIVE To be based on original, not obvious, concepts and hypotheses UNCERTAIN To be uncertain about the final outcome SYSTEMATIC To be planned and budgeted RESEARCH AND DEVELOPMENT TRANSFERABLE AND/OR REPRODUCIBLE To lead to results that could be possibly reproduced 2016 Deloitte Belgium

9 R&D Definition R&D criteria (Frascati manual) Industry Knowledge CREATIVE Business Knowledge Novelty finding s UNCERTAIN SYSTEMATIC NOVEL To be aimed at new findings CREATIVE To be based on original, not obvious, concepts and hypotheses UNCERTAIN To be uncertain about the final outcome R&D must result in findings that are new to the business and not already in use in the industry. Can focus on reproducing existing results with discrepancies Cannot be activities undertaken to copy, imitate or reverse RESEARCH AND engineer (not novel knowledge) DEVELOPMENT SYSTEMATIC To be planned and budgeted TRANSFERABLE AND/OR REPRODUCIBLE To lead to results that could be possibly reproduced 2016 Deloitte Belgium

10 R&D Definition R&D criteria (Frascati manual) E x i s t i n g K n o w l e d g e New NOVEL To be aimed at new findings CREATIVE UNCERTAIN SYSTEMATIC CREATIVE To be based on original, not obvious, concepts and hypotheses UNCERTAIN To be uncertain about the final outcome R&D must have as an objective new concepts or ideas that improve on existing knowledge Can focus on new methods developed to perform common tasks Cannot be any routine change to products and processes or RESEARCH AND DEVELOPMENT be obvious SYSTEMATIC To be planned and budgeted TRANSFERABLE AND/OR REPRODUCIBLE To lead to results that could be possibly reproduced 2016 Deloitte Belgium

11 R&D Definition R&D criteria (Frascati manual) NOVEL To be aimed at new findings CREATIVE UNCERTAIN SYSTEMATIC CREATIVE To be based on original, not obvious, concepts and hypotheses UNCERTAIN To be uncertain about the final outcome What will be the outcome? SYSTEMATIC To be planned and budgeted R&D involves uncertainty, which means that the kind of outcome and the cost (including time allocation) cannot be precisely RESEARCH determined AND relative to the goals DEVELOPMENT TRANSFERABLE AND/OR REPRODUCIBLE To lead to results that could be possibly reproduced 2016 Deloitte Belgium

12 R&D Definition R&D criteria (Frascati manual) New NOVEL To be aimed at new findings CREATIVE UNCERTAIN 1 st 2 nd 3 rd 4 th SYSTEMATIC CREATIVE To be based on original, not obvious, concepts and hypotheses UNCERTAIN To be uncertain about the final outcome R&D is a formal activity that is performed systematically, meaning that it is conducted in a planned way, with records kept of both the process followed and the outcome. RESEARCH AND DEVELOPMENT SYSTEMATIC To be planned and budgeted TRANSFERABLE AND/OR REPRODUCIBLE To lead to results that could be possibly reproduced 2016 Deloitte Belgium

13 R&D Definition R&D criteria (Frascati manual) R&D 1 R&D 2 R&D 3 NOVEL To be aimed at new findings CREATIVE UNCERTAIN SYSTEMATIC CREATIVE To be based on original, not obvious, concepts and hypotheses UNCERTAIN To be uncertain about the final outcome Publication Patent Trade Secret R&D should result in the potential for the transfer of the new knowledge, ensuring its use and allowing other researchers to reproduce the results as part of their own R&D activities. SYSTEMATIC To be planned and budgeted Documentation is key! RESEARCH AND DEVELOPMENT TRANSFERABLE AND/OR REPRODUCIBLE To lead to results that could be possibly reproduced 2016 Deloitte Belgium

14 Investment deduction for R&D Introduction 2017 Deloitte Belgium

15 R&D Investment Deduction / Tax Credit Introduction Summary Art. 68 and 69 (art. 48 RD/ITC 92) 2017 Deloitte Belgium R&D investments & patents 13,5% - 20,5% deduction refundable tax credit Several conditions (R&D center, certificates, ) 4,5 to 7% net saving on R&D investments Direct -4.5% Investment costs Spread -7% Investment costs Companies that invest in R&D can benefit from an R&D investment deduction/r&d tax credit. The R&D investment deduction/tax credit applies to R&D investments capitalized in BE GAAP (tangible/intangible fixed assets); Option between one-shot or spread R&D investment deduction/tax credit; Requirement: a regional certificate confirming the absence of any negative impact on the environment of the new products or prospective technologies resulting out of the R&D activities has to be obtained; The accounting treatment of the R&D costs should be analyzed. Certainly considering the new European accounting directive and its implementation in Belgian law.

16 Investment deduction for R&D Benefits and investment requirements 2017 Deloitte Belgium

17 R&D Investment Deduction / Tax Credit Benefits and investment requirements Increased investment deduction 13.5%/20.5% x capitalised investment (Belgian GAAP) = deduction at 33.99% Carried forward Below the line reporting (IFRS/US GAAP) Tax credit 13.5%/20.5% x capitalised investment (Belgian GAAP) x 33.99% = credit Refundable if not used after 5 years Above the line reporting (IFRS/US GAAP) EBIT +++ 4,5% - 7% net saving on R&D investments Stick to choice! 2017 Deloitte Belgium

18 R&D Investment Deduction / Tax Credit Benefits and investment requirements Tax status (under Belgian GAAP) For tax-paying entities: same tax result For tax-loss entities: refund after 5 years = subsidy Reporting Above the line reporting for R&D Tax Credit under IFRS / US GAAP Notional Interest Deduction Gross NID basis minus (R&D tax credit) = adjusted NID basis versus no adjustment for increased investment deduction = not tax neutral 2017 Deloitte Belgium

19 R&D Investment Deduction / Tax Credit Benefits and investment requirements Belgian GAAP requirements Art. 95 RD January 30, 2001: Intangible fixed assets useful for the future activities of the company Art. 60 RD January 30, 2001: Intangible fixes assets may be capitalized at cost provided it does not exceed a prudent valuation of their utilization value or future return Research costs can not be capitalized since Jan 1, 2016 However, the Report to the King confirms that companies are still allowed to capitalize research costs to the extent that these costs are fully depreciated directly after capitalisation. Following elements need to be considered: 3 year depreciation period is required (and an excess depreciation needs to be triggered) for the R&D tax credit Clear differentiation is required between research costs and develoment costs (and consistent reporting is needed in e.g. the annual account, towards funding bodies, ) Could this position also apply for non-capitalized development costs? Development costs may normally be capitalized 2017 Deloitte Belgium

20 R&D Investment Deduction / Tax Credit Benefits and investment requirements CNC/CNC Advice 2016 / 16 Research costs always in P&L Development costs : may be capitalized upon conditions Usefullness of the product of process for the company should be proven; The product or process needs to be defined clearly and individualized; The cost should be related to the project and be identified seperately Technical feasibility of the project should be proven Financial feasibility should be proven Clear documentation will be required Alignment between IFRS rules and Belgian GAAP 2017 Deloitte Belgium

21 R&D Investment Deduction / Tax Credit Benefits and investment requirements Capitalized investments under BE GAAP only 1st Category: PATENTS Definition Law of March 24, 1984: A right of exploitation granted for any invention which is new and suitable for industrial application No specific certificate from Regions 13.5% only (no spread incentive) 2nd Category: R&D INVESTMENTS Investments that support the R&D of new products/ technologies With no or little impact on the environment Which are innovative for (at least) the Belgian market 2017 Deloitte Belgium

22 R&D Investment Deduction / Tax Credit Benefits and investment requirements R&D cost activation: If in the R&D costs includes depreciation related to intangibles which have already benefit from R&D tax credit, these depreciations should not be taken into consideration. No netting with wage tax reduction or other subsidy. Advance Tax Ruling Whether an investment qualifies can be subject to a ruling request Request + minimum of 90 working days 2017 Deloitte Belgium

23 R&D Investment Deduction / Tax Credit Benefits and investment requirements Certificate If investments are located in: Flemish Region: No due date but filing of 276U with tax return Walloon & Brussels Region: Accounting year N filing due date N + 3 months E.g. 31/12/2017 Due date 31/03/ /11/2017 Due date 28/02/2018 Energy saving tax credit Flemish Region: also applies a 3 months due date 2017 Deloitte Belgium

24 R&D Investment Deduction / Tax Credit Benefits and investment requirements FILE: Form plus Detail on R&D investments Details on products & technologies (proof innovative for Belgian market) Details on environment compliance (legislation + impact for certificate) Details on R&D staff Details on grants & subsidies (if any) TIMING of delivery of certificate depends on Region 2017 Deloitte Belgium

25 Conclusion 2017 Deloitte Belgium

26 Conclusion

27 Contact details 2017 Deloitte Belgium

28 Contact details - Jan Pattyn - Senior Director - jpattyn@deloite.com - M: Pieter Spinc le - Consultant PhD - pspinc le@deloitte.com - M:

Tax incentives on Research and Development (R&D) 16 September 2014

16 September 2014") www.pwc.com Tax incentives on Research and Development (R&D) 16 Belgian Branch reporters Marc De Mil International Tax Expert, Federal Public Service Finance Tom Wallyn Tax Director, Agenda 1.1 Introduction

www.pwc.com Tax incentives on Research and Development (R&D) 16 Belgian Branch reporters Marc De Mil International Tax Expert, Federal Public Service Finance Tom Wallyn Tax Director, Agenda 1.1 Introduction

Software and innovation deduction: Belgium is the place to be! 23 November 2017

Software and innovation deduction: Belgium is the place to be! 23 1 Innovation income deduction (adopted by the Chamber of Representatives on 2 February 2017) R&D incentives Innovation income deduction

Software and innovation deduction: Belgium is the place to be! 23 1 Innovation income deduction (adopted by the Chamber of Representatives on 2 February 2017) R&D incentives Innovation income deduction

METHODOLOGICAL EXPLANATION GOVERNMENT BUDGET ALLOCATIONS FOR RESEARCH AND DEVELOPMENT

METHODOLOGICAL EXPLANATION GOVERNMENT BUDGET ALLOCATIONS FOR RESEARCH AND DEVELOPMENT This methodological explanation relates to the data release: - Government budget allocations for research and development,

METHODOLOGICAL EXPLANATION GOVERNMENT BUDGET ALLOCATIONS FOR RESEARCH AND DEVELOPMENT This methodological explanation relates to the data release: - Government budget allocations for research and development,

Mutual Learning Exercise Administration and Monitoring of R&D tax incentives. Horizon 2020 Policy Support Facility

Mutual Learning Exercise Administration and Monitoring of R&D tax incentives Horizon 2020 Policy Support Facility EUROPEAN COMMISSION Directorate-General for Research & Innovation Directorate A Policy

Mutual Learning Exercise Administration and Monitoring of R&D tax incentives Horizon 2020 Policy Support Facility EUROPEAN COMMISSION Directorate-General for Research & Innovation Directorate A Policy

Project costs have to be actually incurred due to the project implementation, in order to be considered as eligible costs.

Financial issues Extract from the guide for BONUS applicants 1 8. How to prepare project budget? Only the real costs required for the implementation should be indicated in the planned budget for the project.

Financial issues Extract from the guide for BONUS applicants 1 8. How to prepare project budget? Only the real costs required for the implementation should be indicated in the planned budget for the project.

EMEA R&D incentives guide

EMEA R&D incentives guide February 2017 KPMG International 2 EMEA R&D incentives guide Contents EMEA R&D incentives overview 4 Related considerations 6 EMEA R&D incentives summary table 7 Austria 8 Belgium

EMEA R&D incentives guide February 2017 KPMG International 2 EMEA R&D incentives guide Contents EMEA R&D incentives overview 4 Related considerations 6 EMEA R&D incentives summary table 7 Austria 8 Belgium

Incentive Guidelines R&D Feasibility Studies

Incentive Guidelines R&D Feasibility Studies 2014-2020 Issue Date: 1 st November 2014 Version: 1 http://support.maltaenterprise.com Contents Incentive Guidelines 1 Contents 1 1. Introduction 2 1.1 Scope

Incentive Guidelines R&D Feasibility Studies 2014-2020 Issue Date: 1 st November 2014 Version: 1 http://support.maltaenterprise.com Contents Incentive Guidelines 1 Contents 1 1. Introduction 2 1.1 Scope

Doing Business in British Columbia/Canada

Doing Business in British Columbia/Canada Frank Schober Thora Sigurdson Ally Bharmal Introduction Robin Dhir Strategic Advisor, Fasken Martineau 1 Our Advantage Business-Friendly Legal Environment Low

Doing Business in British Columbia/Canada Frank Schober Thora Sigurdson Ally Bharmal Introduction Robin Dhir Strategic Advisor, Fasken Martineau 1 Our Advantage Business-Friendly Legal Environment Low

Client: Manufacturing Company Limited Year end: 31 Dec 2015 File no: M Lead schedule Y. 2 Audit programme Y. 3 Goodwill Y

Client: Manufacturing Company Limited Year end: 31 Dec 2015 File no: M0001 Ref: E E INTANGIBLE ASSETS 1 Lead schedule Y 2 Audit programme Y 3 Goodwill Y 4 Development expenditure Y 5 Ei Page 1 of 10 MCL

Client: Manufacturing Company Limited Year end: 31 Dec 2015 File no: M0001 Ref: E E INTANGIBLE ASSETS 1 Lead schedule Y 2 Audit programme Y 3 Goodwill Y 4 Development expenditure Y 5 Ei Page 1 of 10 MCL

Global Survey of R&D Tax Incentives

Global Survey of R&D Tax Incentives Updated on July 2011 Contents Preface Analysis of National R&D Incentives Australia Austria Belgium Brazil Canada China Czech Republic France Germany Hungary India Ireland

Global Survey of R&D Tax Incentives Updated on July 2011 Contents Preface Analysis of National R&D Incentives Australia Austria Belgium Brazil Canada China Czech Republic France Germany Hungary India Ireland

FASB Emerging Issues Task Force

EITF Issue No. 09-2 FASB Emerging Issues Task Force Issue No. 09-2 Title: Research and Development Assets Acquired and Contingent Consideration Issued In an Asset Acquisition Document: Issue Summary No.

EITF Issue No. 09-2 FASB Emerging Issues Task Force Issue No. 09-2 Title: Research and Development Assets Acquired and Contingent Consideration Issued In an Asset Acquisition Document: Issue Summary No.

Pirelli Intellectual Property Policy (or IPR) INTRODUCTION

INTRODUCTION") Pirelli Intellectual Property Policy (or IPR) INTRODUCTION The intellectual property rights, also referred to as IPRs (or Technological Know-How), are competitive tools for Pirelli, creating value for

Pirelli Intellectual Property Policy (or IPR) INTRODUCTION The intellectual property rights, also referred to as IPRs (or Technological Know-How), are competitive tools for Pirelli, creating value for

Information Sheet No. 66. The New Intellectual Property (IP) Tax Regime in Cyprus

Tax Regime in Cyprus") Information Sheet No. 66 The New Intellectual Property (IP) Tax Regime in Cyprus Introduction On 14 October 2016, the House of Representatives passed amendments to the Income Tax Law in order to align

Information Sheet No. 66 The New Intellectual Property (IP) Tax Regime in Cyprus Introduction On 14 October 2016, the House of Representatives passed amendments to the Income Tax Law in order to align

International Tax Belgium Highlights 2018

International Tax Belgium Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements Belgian GAAP. IFRS is mandatory for consolidated

International Tax Belgium Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements Belgian GAAP. IFRS is mandatory for consolidated

Solvay Group IFRS pro forma financial statements (insert to annual report 2002)

") Solvay Group 2002 IFRS pro forma financial statements (insert to annual report 2002) 2 Solvay Group/2002 IFRS pro forma financial statements Content 2002 IFRS PRO FORMA FINANCIAL STATEMENTS page 3 NOTES

Solvay Group 2002 IFRS pro forma financial statements (insert to annual report 2002) 2 Solvay Group/2002 IFRS pro forma financial statements Content 2002 IFRS PRO FORMA FINANCIAL STATEMENTS page 3 NOTES

Innovation Tax Incentives March 2017

www.pwc.ie Innovation Tax Incentives March 2017 1. R&D tax credit Regime Key Benefits Headline tax credit of 25% for expenditure on qualifying R&D activities Overall effective corporation tax credit of

www.pwc.ie Innovation Tax Incentives March 2017 1. R&D tax credit Regime Key Benefits Headline tax credit of 25% for expenditure on qualifying R&D activities Overall effective corporation tax credit of

Belgian R&D tax incentives

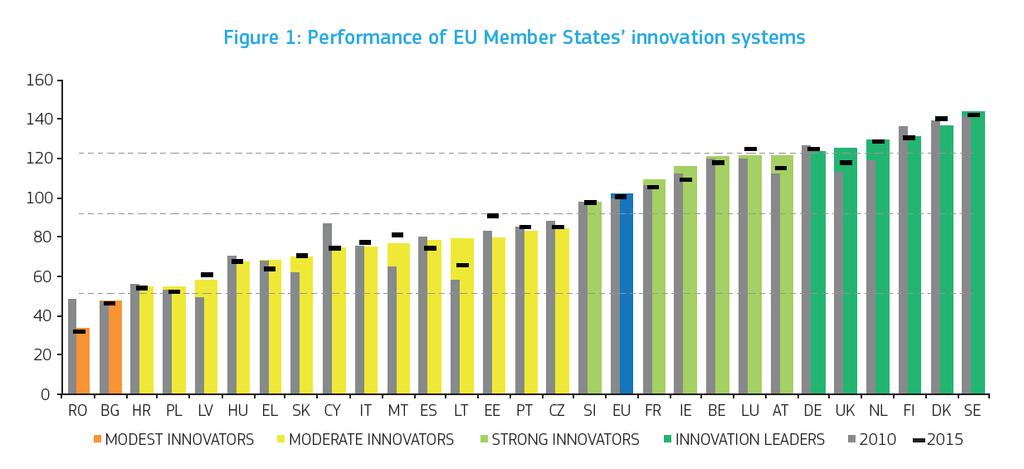

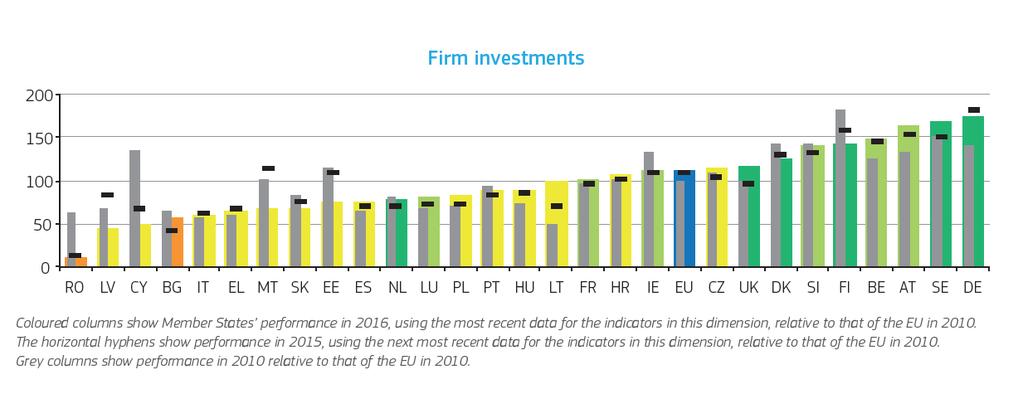

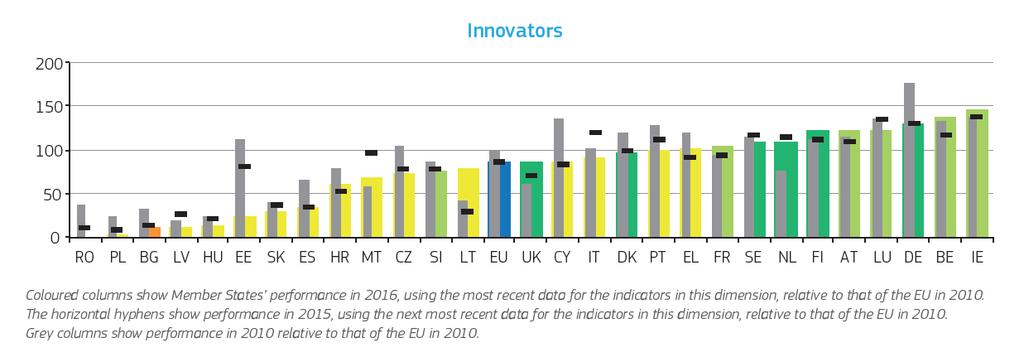

Belgian R&D tax incentives "What did Belgium choose to offer and why?" Brent Springael 18 May 2017 Key Figures Scoreboard Report 2016 EU Member States' Innovation Performance page 3 Scoreboard Report 2016

Belgian R&D tax incentives "What did Belgium choose to offer and why?" Brent Springael 18 May 2017 Key Figures Scoreboard Report 2016 EU Member States' Innovation Performance page 3 Scoreboard Report 2016

1. INTRODUCTION Accounting Requirements for Expenses Minor Amendments MAIN REQUIREMENTS... 4

Note presenting Opinion n 2011-09 of the 17 th October 2011 relating to the definition and the recognition of expenses and minor amendments to Standard 2 Expenses, Standard 12 renamed Non-Financial Liabilities

Note presenting Opinion n 2011-09 of the 17 th October 2011 relating to the definition and the recognition of expenses and minor amendments to Standard 2 Expenses, Standard 12 renamed Non-Financial Liabilities

Research and development tax credit legislation

21 December 2007 Special report from the Policy Advice Division of Inland Revenue Research and development tax credit legislation Legislation introducing a tax credit for eligible research and development

21 December 2007 Special report from the Policy Advice Division of Inland Revenue Research and development tax credit legislation Legislation introducing a tax credit for eligible research and development

Aleksandra Dyba University of Economics in Krakow

61 Aleksandra Dyba University of Economics in Krakow dyba@uek.krakow.pl Abstract Purpose development is nowadays a crucial global challenge. The European aims at building a competitive economy, however,

61 Aleksandra Dyba University of Economics in Krakow dyba@uek.krakow.pl Abstract Purpose development is nowadays a crucial global challenge. The European aims at building a competitive economy, however,

Belgium. Employee Stock Purchase Plans. Employment. Regulatory. Labor Concerns. Communications. Securities Compliance

Belgium Employee Stock Purchase Plans Employment Labor Concerns Communications To reduce the risk of potential claims from employees that they have entitlements under a Plan, employees should expressly

Belgium Employee Stock Purchase Plans Employment Labor Concerns Communications To reduce the risk of potential claims from employees that they have entitlements under a Plan, employees should expressly

Chapter 10 Property, Plant, and Equipment and Intangible Assets: Acquisition

Chapter 10 Property, Plant, and Equipment and Intangible Assets: Acquisition QUESTIONS FOR REVIEW OF KEY TOPICS Question 10 1 The difference between tangible and intangible long-lived, revenue-producing

Chapter 10 Property, Plant, and Equipment and Intangible Assets: Acquisition QUESTIONS FOR REVIEW OF KEY TOPICS Question 10 1 The difference between tangible and intangible long-lived, revenue-producing

PRINCE2. Number: PRINCE2 Passing Score: 800 Time Limit: 120 min File Version:

PRINCE2 Number: PRINCE2 Passing Score: 800 Time Limit: 120 min File Version: 1.0 Exam M QUESTION 1 Identify the missing word(s) from the following sentence. A project is a temporary organization that is

PRINCE2 Number: PRINCE2 Passing Score: 800 Time Limit: 120 min File Version: 1.0 Exam M QUESTION 1 Identify the missing word(s) from the following sentence. A project is a temporary organization that is

Tekes preliminary comments on the first draft of the General Block Exemption Regulation (published 8th of May 2013)

") 1 Tekes preliminary comments on the first draft of the General Block Exemption Regulation (published 8th of May 2013) This document contains Tekes comments on the first draft of the General Block Exemption

1 Tekes preliminary comments on the first draft of the General Block Exemption Regulation (published 8th of May 2013) This document contains Tekes comments on the first draft of the General Block Exemption

Available online at ScienceDirect. Procedia Economics and Finance 39 ( 2016 )

") Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 39 ( 2016 ) 399 411 3rd GLOBAL CONFERENCE on BUSINESS, ECONOMICS, MANAGEMENT and TOURISM, 26-28 November 2015, Rome,

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 39 ( 2016 ) 399 411 3rd GLOBAL CONFERENCE on BUSINESS, ECONOMICS, MANAGEMENT and TOURISM, 26-28 November 2015, Rome,

BELGIUM GLOBAL GUIDE TO M&A TAX: 2018 EDITION

BELGIUM 1 BELGIUM INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? A major corporate income tax reform has been published

BELGIUM 1 BELGIUM INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? A major corporate income tax reform has been published

Restated reporting Philips Group

Restated reporting Philips per quarter, first 3 quarters all amounts unless otherwise stated the data included in this report are unaudited financial reporting according to US GAAP unless otherwise stated

Restated reporting Philips per quarter, first 3 quarters all amounts unless otherwise stated the data included in this report are unaudited financial reporting according to US GAAP unless otherwise stated

Science and Technology Indicators

2011 Science and Technology Indicators R&D statistics Published by Address ISBN ISSN Nordic Institute for Studies in Innovation, Research and Education PB 5183, Majorstuen NO-0302. Visiting address: Wergelandsveien

2011 Science and Technology Indicators R&D statistics Published by Address ISBN ISSN Nordic Institute for Studies in Innovation, Research and Education PB 5183, Majorstuen NO-0302. Visiting address: Wergelandsveien

Black hole R&D expenditure

Black hole R&D expenditure A government discussion document Hon Steven Joyce Minister of Science and Innovation Hon Todd McClay Minister of Revenue First published in November 2013 by Policy and Strategy,

Black hole R&D expenditure A government discussion document Hon Steven Joyce Minister of Science and Innovation Hon Todd McClay Minister of Revenue First published in November 2013 by Policy and Strategy,

The R&D Tax Incentive. Federal funding support for Australian experimental R&D

The R&D Tax Incentive Federal funding support for Australian experimental R&D tem: R&D Tax R&D Incentive Tax Incentive The R&D Tax Incentive is a generous Federal Government programme Administered by AusIndustry

The R&D Tax Incentive Federal funding support for Australian experimental R&D tem: R&D Tax R&D Incentive Tax Incentive The R&D Tax Incentive is a generous Federal Government programme Administered by AusIndustry

Intellectual property rights in Luxembourg (IPR): tax exemption

: tax exemption") Intellectual property rights in Luxembourg (IPR): tax exemption Miami, November 3, 2011 Me Beatriz Garcia The tax attractiveness of Luxembourg regarding the intellectual property has increased by the introduction

Intellectual property rights in Luxembourg (IPR): tax exemption Miami, November 3, 2011 Me Beatriz Garcia The tax attractiveness of Luxembourg regarding the intellectual property has increased by the introduction

Managing Project Risk DHY

Managing Project Risk DHY01 0407 Copyright ESI International April 2007 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or

Managing Project Risk DHY01 0407 Copyright ESI International April 2007 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or

Subject: ED 2012/4 Classification and Measurement: Limited Amendments to IFRS 9

Mr. Hans Hoogervorst Chairman IASB 30 Cannon Street London EC4M 6XH United Kingdom Ref. G10507 FEB177093 Brussels, 27/03/2013 Subject: ED 2012/4 Classification and Measurement: Limited Amendments to IFRS

Mr. Hans Hoogervorst Chairman IASB 30 Cannon Street London EC4M 6XH United Kingdom Ref. G10507 FEB177093 Brussels, 27/03/2013 Subject: ED 2012/4 Classification and Measurement: Limited Amendments to IFRS

Research Article Design and Explanation of the Credit Ratings of Customers Model Using Neural Networks

Research Journal of Applied Sciences, Engineering and Technology 7(4): 5179-5183, 014 DOI:10.1906/rjaset.7.915 ISSN: 040-7459; e-issn: 040-7467 014 Maxwell Scientific Publication Corp. Submitted: February

Research Journal of Applied Sciences, Engineering and Technology 7(4): 5179-5183, 014 DOI:10.1906/rjaset.7.915 ISSN: 040-7459; e-issn: 040-7467 014 Maxwell Scientific Publication Corp. Submitted: February

Official Journal of the European Union

L 63/22 28.2.2004 COMMISSION REGULATION (EC) No 364/2004 of 25 February 2004 amending Regulation (EC) No 70/2001 as regards the extension of its scope to include aid for research and development THE COMMISSION

L 63/22 28.2.2004 COMMISSION REGULATION (EC) No 364/2004 of 25 February 2004 amending Regulation (EC) No 70/2001 as regards the extension of its scope to include aid for research and development THE COMMISSION

Choosing a Business Entity After the New Tax Act and Other Important Business Tax Changes Under the New Law

Tax Advisory January 2018 Choosing a Business Entity After the New Tax Act and Other Important Business Tax Changes Under the New Law A Five-Part Series Part I: General - The Choice of Entity Decision

Tax Advisory January 2018 Choosing a Business Entity After the New Tax Act and Other Important Business Tax Changes Under the New Law A Five-Part Series Part I: General - The Choice of Entity Decision

whitelightconsulting UK Patent Box how to get the most* out of it (*or as close to that as we can get)

") UK Patent Box how to get the most* out of it (*or as close to that as we can get) innovation minus protection equals donation WHAT IS THE PATENT BOX? From April 2013 HMRC launched a new tax incentive scheme

UK Patent Box how to get the most* out of it (*or as close to that as we can get) innovation minus protection equals donation WHAT IS THE PATENT BOX? From April 2013 HMRC launched a new tax incentive scheme

Fact Sheet Inventorship, Authorship and Ownership

European IPR Helpdesk Fact Sheet Inventorship, Authorship and Ownership March 2013 Introduction... 1 1 Ownership, Inventorship and Authorship... 2 2 The relevance of inventorship... 3 3 The relevance of

European IPR Helpdesk Fact Sheet Inventorship, Authorship and Ownership March 2013 Introduction... 1 1 Ownership, Inventorship and Authorship... 2 2 The relevance of inventorship... 3 3 The relevance of

Leslie Van den Branden Partner De Witte-Viselé Associates Kaasmarkt 24 B Brussels (Wemmel) Belgium 1 October 2013

Belgium 1 October 2013") Mr. Joseph Andrus Head, Transfer Pricing Unit OECD 2, rue andré pascal 75775 Paris Cedex 16 France Leslie Van den Branden Partner De Witte-Viselé Associates Kaasmarkt 24 B- 1780 Brussels (Wemmel) Belgium

Mr. Joseph Andrus Head, Transfer Pricing Unit OECD 2, rue andré pascal 75775 Paris Cedex 16 France Leslie Van den Branden Partner De Witte-Viselé Associates Kaasmarkt 24 B- 1780 Brussels (Wemmel) Belgium

Incentive Guidelines Tax Credits for R&D and Innovation

Incentive Guidelines Tax Credits for R&D and Innovation - Issue Date: 1 st June 2017 Version: 1 http://support.maltaenterprise.com Malta Enterprise provides interested applicants with support to facilitate

Incentive Guidelines Tax Credits for R&D and Innovation - Issue Date: 1 st June 2017 Version: 1 http://support.maltaenterprise.com Malta Enterprise provides interested applicants with support to facilitate

Peter S. Weissman Blank Rome LLP (202)

") Presentation for GW Business Plan Competition March 2014 Protecting Your Ideas and Brands with Patents and Trademarks Peter S. Weissman Blank Rome LLP (202) 772-5805 weissman@blankrome.com http://www.linkedin.com/in/pweissman

Presentation for GW Business Plan Competition March 2014 Protecting Your Ideas and Brands with Patents and Trademarks Peter S. Weissman Blank Rome LLP (202) 772-5805 weissman@blankrome.com http://www.linkedin.com/in/pweissman

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS APRIL 2018 CONTENTS Updates 2 Introduction 6 Conceptual Framework for Central Government Accounting 7 Standard 1 Financial Statements 24 Standard 2 Expenses 39 Standard

CENTRAL GOVERNMENT ACCOUNTING STANDARDS APRIL 2018 CONTENTS Updates 2 Introduction 6 Conceptual Framework for Central Government Accounting 7 Standard 1 Financial Statements 24 Standard 2 Expenses 39 Standard

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS March 2015 CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE Updates Public Sector Accounting Standards Council Date of Central Government Accounting Standards Opinion

CENTRAL GOVERNMENT ACCOUNTING STANDARDS March 2015 CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE Updates Public Sector Accounting Standards Council Date of Central Government Accounting Standards Opinion

B.6. Cost Contribution Arrangements

B.6. Cost Contribution Arrangements Introduction B.6.1. This chapter provides guidance on the use of cost contribution arrangements (CCAs) and the application of the arm s length principle to CCAs for

B.6. Cost Contribution Arrangements Introduction B.6.1. This chapter provides guidance on the use of cost contribution arrangements (CCAs) and the application of the arm s length principle to CCAs for

The research and development tax relief framework

Chapter 2 The research and development tax relief framework Contents Signposts Summary/key points 2.1 Background: the R & D tax relief framework 2.3 Current accounting definitions of R & D 2.6 Revenue

Chapter 2 The research and development tax relief framework Contents Signposts Summary/key points 2.1 Background: the R & D tax relief framework 2.3 Current accounting definitions of R & D 2.6 Revenue

COMPANY SNAPSHOT 08/26/2010 Last Closing Stock Price as of 08/25/2010: $10.22

Last Closing Stock Price as of 08/25/2010: $10.22 Company Snapshot This report presents a concise review of our DCF valuation and economic profitability analysis from our MaxVal model. Contributors Equity

Last Closing Stock Price as of 08/25/2010: $10.22 Company Snapshot This report presents a concise review of our DCF valuation and economic profitability analysis from our MaxVal model. Contributors Equity

FINANCIAL ECONOMIC ANALYSIS AND INTERPRETATION SECOND EDITION CHRIS HIGSON RIVINGTON

FINANCIAL STATEMENTS ECONOMIC ANALYSIS AND INTERPRETATION SECOND EDITION CHRIS HIGSON RIVINGTON Contents Chapter 1 Introduction Accounting 2 Return, Risk, Valuation 3 Using this book 4 Chapter 2 The Balance

FINANCIAL STATEMENTS ECONOMIC ANALYSIS AND INTERPRETATION SECOND EDITION CHRIS HIGSON RIVINGTON Contents Chapter 1 Introduction Accounting 2 Return, Risk, Valuation 3 Using this book 4 Chapter 2 The Balance

Taj s tax experts and engineers have compared the different R&D tax incentives in 13 OECD countries.

EXCLUSIVE STUDY R&D tax incentives: A ranking of the world s most Etude attractive exclusive regimes Taj R & D d e m y s t i f i e d On August 17, the Inspection Générale des Finances [general inspectorate

EXCLUSIVE STUDY R&D tax incentives: A ranking of the world s most Etude attractive exclusive regimes Taj R & D d e m y s t i f i e d On August 17, the Inspection Générale des Finances [general inspectorate

2. Intellectual Properties (IPs): Intangible properties protectable as to ownership under the laws of patent, copyright, trademark, or trade secret.

: Intangible properties protectable as to ownership under the laws of patent, copyright, trademark, or trade secret.") Introduction Approved by the Board of Trustees January 17, 2006 Central Washington University Intellectual Properties Policy It is important for Central Washington University (CWU) to provide uniform policies

Introduction Approved by the Board of Trustees January 17, 2006 Central Washington University Intellectual Properties Policy It is important for Central Washington University (CWU) to provide uniform policies

MODERN INNOVATIVE APPROACHES OF MEASURING BUSINESS PERFORMANCE

Integrated Economy and Society: Diversity, Creativity, and Technology 16 18 May 2018 Naples Italy Management, Knowledge and Learning International Conference 2018 Technology, Innovation and Industrial

Integrated Economy and Society: Diversity, Creativity, and Technology 16 18 May 2018 Naples Italy Management, Knowledge and Learning International Conference 2018 Technology, Innovation and Industrial

Source: OECD, Note: 2006 for Finland, United States, Canada and Ireland; 2004 for Switzerland, Netherlands, Australia, Italy and Turkey.

:(1) 280 : 10834 : : 1390 1... 2... 4....1 8....2 23....3 33... 34... :(1)....... -... و ش ج س ورایاسلا ی.. ()..... 1.. (GDP ).1 Source: OECD, 2007. Note: 2006 for Finland, United States, Canada and Ireland;

:(1) 280 : 10834 : : 1390 1... 2... 4....1 8....2 23....3 33... 34... :(1)....... -... و ش ج س ورایاسلا ی.. ()..... 1.. (GDP ).1 Source: OECD, 2007. Note: 2006 for Finland, United States, Canada and Ireland;

Updated reporting Philips Group

Updated reporting Philips Group all amounts in millions of euros unless otherwise stated all the data included in this report are unaudited financial reporting according to IFRS unless otherwise stated

Updated reporting Philips Group all amounts in millions of euros unless otherwise stated all the data included in this report are unaudited financial reporting according to IFRS unless otherwise stated

[COMPANY NAME] Research & Development Tax Credit Assessment n For tax year ended December 31, 20xx

![[COMPANY NAME] Research & Development Tax Credit Assessment n For tax year ended December 31, 20xx](/thumbs/81/83829128.jpg "[COMPANY NAME] Research & Development Tax Credit Assessment n For tax year ended December 31, 20xx") [COMPANY NAME] Research & Development Tax Credit Assessment n For tax year ended December 31, 20xx Prepared for ABC Manufacturing, Inc. Estimate for the Tax Year Ended December 31, 2015 Any tax advice

[COMPANY NAME] Research & Development Tax Credit Assessment n For tax year ended December 31, 20xx Prepared for ABC Manufacturing, Inc. Estimate for the Tax Year Ended December 31, 2015 Any tax advice

What is a Franchise? International Franchising

WORKSHOP 10: Maximising Intangible Benefits from IPRs Protection to Exploitation of IPRs. Business Strategies based on Franchising and/or Merchandising: IP Issues and Franchising (WIPO, Rome, Italy 10&

WORKSHOP 10: Maximising Intangible Benefits from IPRs Protection to Exploitation of IPRs. Business Strategies based on Franchising and/or Merchandising: IP Issues and Franchising (WIPO, Rome, Italy 10&

Changes proposed for income tax accounting. Revised calculation methodology. Montreal Robert Lefrancois

April 2009 IAS Plus Update. Changes proposed for income tax accounting On 31 March 2009, the International Accounting Standards Board (IASB) issued an exposure draft (ED) ED/2009/2 Income Tax containing

April 2009 IAS Plus Update. Changes proposed for income tax accounting On 31 March 2009, the International Accounting Standards Board (IASB) issued an exposure draft (ED) ED/2009/2 Income Tax containing

Tax Reform (TRAF / Tax Proposal 17) Webcast of 2 October 2018

Webcast of 2 October 2018") (TRAF / Tax Proposal 17) Webcast of 2 October 2018 Today s moderators Dominik Bürgy Partner, Tax Services EY Switzerland Phone: +41 58 286 44 35 dominik.buergy@ch.ey.com Marco Mühlemann Associate Partner,

(TRAF / Tax Proposal 17) Webcast of 2 October 2018 Today s moderators Dominik Bürgy Partner, Tax Services EY Switzerland Phone: +41 58 286 44 35 dominik.buergy@ch.ey.com Marco Mühlemann Associate Partner,

Knowledge Development Box Utilising it for maximum benefit

Knowledge Development Box Utilising it for maximum benefit 10 February 2016 2016 Grant Thornton Ireland. All rights reserved #GTtax GRANT THORNTON WEDNESDAY, 10 TH FEBRUARY 2016 KNOWLEDGE DEVELOPMENT BOX

Knowledge Development Box Utilising it for maximum benefit 10 February 2016 2016 Grant Thornton Ireland. All rights reserved #GTtax GRANT THORNTON WEDNESDAY, 10 TH FEBRUARY 2016 KNOWLEDGE DEVELOPMENT BOX

IFRS 17 for non-life insurers

Ergebnisbericht des Ausschusses Rechnungslegung und Regulierung (Report on findings of the Accounting and Regulation Committee) IFRS 17 for non-life insurers Cologne, 17 August 2018 1 Preamble The Accounting

Ergebnisbericht des Ausschusses Rechnungslegung und Regulierung (Report on findings of the Accounting and Regulation Committee) IFRS 17 for non-life insurers Cologne, 17 August 2018 1 Preamble The Accounting

Exploiting Intellectual Property Rights: Key Attractions of Locating Operations in Ireland

Locating Operations in briefing Many of the leading global corporates in the technology, pharma, medical devices, biotech and other sectors involved in the commercialisation of intellectual property have

Locating Operations in briefing Many of the leading global corporates in the technology, pharma, medical devices, biotech and other sectors involved in the commercialisation of intellectual property have

The Effect of Intellectual Property Boxes on Innovative Activity & Tax Avoidance University of Illinois Tax Doctoral Consortium III

The Effect of Intellectual Property Boxes on Innovative Activity & Tax Avoidance University of Illinois Tax Doctoral Consortium III Tobias Bornemann, Stacie Laplante, Benjamin Osswald 1 Overview What?

The Effect of Intellectual Property Boxes on Innovative Activity & Tax Avoidance University of Illinois Tax Doctoral Consortium III Tobias Bornemann, Stacie Laplante, Benjamin Osswald 1 Overview What?

January - September 2015 Results

January - September 2015 Results 23 rd October 2015 Disclaimer The information and forward-looking statements contained in this presentation have not been verified by an independent entity and the accuracy,

January - September 2015 Results 23 rd October 2015 Disclaimer The information and forward-looking statements contained in this presentation have not been verified by an independent entity and the accuracy,

TAX INCENTIVES FOR GROWING HEALTH SCIENCE COMPANIES

TAX INCENTIVES FOR GROWING HEALTH SCIENCE COMPANIES 0 1 CONTENTS Executive Summary... 1 Introduction... 3 Recommendations : Government of Canada... 5 Recommendations : Government of Ontario... 7 References...

TAX INCENTIVES FOR GROWING HEALTH SCIENCE COMPANIES 0 1 CONTENTS Executive Summary... 1 Introduction... 3 Recommendations : Government of Canada... 5 Recommendations : Government of Ontario... 7 References...

Cross-border Outsourcing

1 st Subject IFA Mumbai October 2014 Cross-border Outsourcing Issues, Strategies & Solutions Natalie Reypens, partner Loyens & Loeff IFA Belgium 15 October 2013 Content 1. Introduction 2. Domestic law

1 st Subject IFA Mumbai October 2014 Cross-border Outsourcing Issues, Strategies & Solutions Natalie Reypens, partner Loyens & Loeff IFA Belgium 15 October 2013 Content 1. Introduction 2. Domestic law

Importance of Intangibles. TP Problems Related to Intangibles. Intangible Issues in Developing Countries

UN-ATAF Workshop on Transfer Pricing Administrative Aspects and Recent Developments Ezulwini, Swaziland 4-8 December 2017 TRANSFER PRICING FOR CASES INVOLVING INTANGIBLES Wednesday, 6 December 2017 2.00pm

UN-ATAF Workshop on Transfer Pricing Administrative Aspects and Recent Developments Ezulwini, Swaziland 4-8 December 2017 TRANSFER PRICING FOR CASES INVOLVING INTANGIBLES Wednesday, 6 December 2017 2.00pm

2 Some Essential Macroeconomic Aggregates

2 Some Essential Macroeconomic Aggregates 2.1 Defining Gross Domestic Product (GDP) 2.2 Deriving GDP in Volume 2.3 Defining Demand: the Role of Investment and Consumption 2.4 Reconciling Global Output

2 Some Essential Macroeconomic Aggregates 2.1 Defining Gross Domestic Product (GDP) 2.2 Deriving GDP in Volume 2.3 Defining Demand: the Role of Investment and Consumption 2.4 Reconciling Global Output

Goldman Sachs Basic Materials Conference. Brad Lich, EVP and Chief Commercial Officer May 15, 2018

Goldman Sachs Basic Materials Conference Brad Lich, EVP and Chief Commercial Officer May 15, 2018 Forward-looking statements During this presentation, we make certain forward-looking statements concerning

Goldman Sachs Basic Materials Conference Brad Lich, EVP and Chief Commercial Officer May 15, 2018 Forward-looking statements During this presentation, we make certain forward-looking statements concerning

New Zealand Equivalent to International Accounting Standard 23 Borrowing Costs (NZ IAS 23)

") New Zealand Equivalent to International Accounting Standard 23 Borrowing Costs (NZ IAS 23) Issued July 2007 and incorporates amendments to 31 December 2015 This Standard was issued by the New Zealand Accounting

New Zealand Equivalent to International Accounting Standard 23 Borrowing Costs (NZ IAS 23) Issued July 2007 and incorporates amendments to 31 December 2015 This Standard was issued by the New Zealand Accounting

Hybrid Approach to Option Valuation

Hybrid Approach to Option Valuation Richard de Neufville Professor of Engineering Systems and of Civil and Environmental Engineering MIT Hybrid Approach to Valuation Slide 1 of 23 Outline R & D creates

Hybrid Approach to Option Valuation Richard de Neufville Professor of Engineering Systems and of Civil and Environmental Engineering MIT Hybrid Approach to Valuation Slide 1 of 23 Outline R & D creates

International Financial Reporting Standards Analyst Briefing March 2005

Aggreko plc International Financial Reporting Standards Analyst Briefing March 2005-1- Briefing Structure IFRS impact summary Time-line for communication with the market IFRS implementation project Key

Aggreko plc International Financial Reporting Standards Analyst Briefing March 2005-1- Briefing Structure IFRS impact summary Time-line for communication with the market IFRS implementation project Key

Worcestershire Mental Health Partnership NHS Trust. Intellectual Property & Property Rights Policy.

Worcestershire Mental Health Partnership NHS Trust Intellectual Property & Property Rights Policy. This policy should be read in conjunction with Research Governance Key words Unique identifier: Intellectual

Worcestershire Mental Health Partnership NHS Trust Intellectual Property & Property Rights Policy. This policy should be read in conjunction with Research Governance Key words Unique identifier: Intellectual

City, Town, or Post Office State Zip Code

SRDTC-A REV 12-11 Application for West Virginia Strategic Research and Development Tax Credit for Qualified Expenditures and Qualified Investments Placed in Service On or After January 1, 2003 Name Identification

SRDTC-A REV 12-11 Application for West Virginia Strategic Research and Development Tax Credit for Qualified Expenditures and Qualified Investments Placed in Service On or After January 1, 2003 Name Identification

Belgium. GDP Per Capita, PPS 2001

BELGIUM * 1. REGIONAL DISPARITIES AND PROBLEMS In Belgium, the regional problem is primarily associated with the impact of industrial restructuring and decline. This is especially so in Wallonia where

BELGIUM * 1. REGIONAL DISPARITIES AND PROBLEMS In Belgium, the regional problem is primarily associated with the impact of industrial restructuring and decline. This is especially so in Wallonia where

Worldwide R&D Incentives Reference Guide

Worldwide R&D Incentives Reference Guide 2017 Preface The pace at which countries are reforming their R&D incentives regimes is unprecedented. For some, this means introducing completely new incentives;

Worldwide R&D Incentives Reference Guide 2017 Preface The pace at which countries are reforming their R&D incentives regimes is unprecedented. For some, this means introducing completely new incentives;

Ind AS 16: Property, Plant and Equipment Ind AS 38: Intangible Assets

Ind AS 16: Property, Plant and Equipment Ind AS 38: Intangible Assets WIRC of the ICAI March 2016 Pirooz P Movdawalla piroozpm@alumni.carnegiemellon.edu Agenda 1 Ind AS 16 and Ind AS 38 WIRC of the ICAI

Ind AS 16: Property, Plant and Equipment Ind AS 38: Intangible Assets WIRC of the ICAI March 2016 Pirooz P Movdawalla piroozpm@alumni.carnegiemellon.edu Agenda 1 Ind AS 16 and Ind AS 38 WIRC of the ICAI

Cyprus Tax News Amendments to Cyprus s IP regime

Cyprus Tax & Legal Services 27 October 2016 Issue 14/2016 Cyprus Tax News Amendments to Cyprus s IP regime INTRODUCTION On 14 October 2016, the House of Representatives enacted into law significant amendments

Cyprus Tax & Legal Services 27 October 2016 Issue 14/2016 Cyprus Tax News Amendments to Cyprus s IP regime INTRODUCTION On 14 October 2016, the House of Representatives enacted into law significant amendments

AIRBUS Q1 Results 2018

AIRBUS Q1 Results 2018 27 April 2018 Harald Wilhelm Chief Financial Officer SAFE HARBOUR STATEMENT 2 DISCLAIMER This presentation includes forward-looking statements. Words such as anticipates, believes,

AIRBUS Q1 Results 2018 27 April 2018 Harald Wilhelm Chief Financial Officer SAFE HARBOUR STATEMENT 2 DISCLAIMER This presentation includes forward-looking statements. Words such as anticipates, believes,

Guide to Going Global Global Equity

Guide to Going Global Global Equity Stock Options 2015 CONTENTS INTRODUCTION 04 05 AUSTRALIA 07 AUSTRIA 09 BELGIUM 11 BRAZIL 13 CANADA 15 17 CHINA 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 MEXICO

Guide to Going Global Global Equity Stock Options 2015 CONTENTS INTRODUCTION 04 05 AUSTRALIA 07 AUSTRIA 09 BELGIUM 11 BRAZIL 13 CANADA 15 17 CHINA 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 MEXICO

MANAGEMENT ACCOUNTING OF HIGHER EDUCATION INSTITUTIONS: IMPLEMENTATION STAGES AND REALIZATION FEATURES

ECONOMICS, ENTREPRENEURSHIP, MANAGEMENT Vol. 2, No. 2, 2015 N. A. Mamontova Doctor of Economics, Professor, A. F. Novak PhD of Economic Sciences, as. prof., The National University of Ostroh Academy MANAGEMENT

ECONOMICS, ENTREPRENEURSHIP, MANAGEMENT Vol. 2, No. 2, 2015 N. A. Mamontova Doctor of Economics, Professor, A. F. Novak PhD of Economic Sciences, as. prof., The National University of Ostroh Academy MANAGEMENT

Restated segment reporting Philips Group 2006

Restated segment reporting Philips Group all amounts unless otherwise stated the data included in this report are unaudited financial reporting according to US GAAP unless otherwise stated restated to

Restated segment reporting Philips Group all amounts unless otherwise stated the data included in this report are unaudited financial reporting according to US GAAP unless otherwise stated restated to

The economics of Pay for Delay cases

The economics of cases Brussels, Dr. Matthew Bennett Vice President, CRA 1 Features of the pharma sector Main players Pharmaceutical companies that are active in research for new compounds (originators)

The economics of cases Brussels, Dr. Matthew Bennett Vice President, CRA 1 Features of the pharma sector Main players Pharmaceutical companies that are active in research for new compounds (originators)

Is it time for your country to consider the "patent box"?

Is it time for your country to consider the "patent box"? By Jim Shanahan PwC's Global R&D Tax Symposium on Designing a Blueprint for Reducing the After-Tax Cost of Global R&D Dublin, Ireland, May 23,

Is it time for your country to consider the "patent box"? By Jim Shanahan PwC's Global R&D Tax Symposium on Designing a Blueprint for Reducing the After-Tax Cost of Global R&D Dublin, Ireland, May 23,

BRITISH HORSERACING GRANT SCHEME STATE AID GUIDANCE

BRITISH HORSERACING GRANT SCHEME STATE AID GUIDANCE BRITISH HORSERACING GRANT SCHEME STATE AID GUIDANCE Part 1 - Introduction 1. EU State aid law is relevant to any distribution of funds from the Tote

BRITISH HORSERACING GRANT SCHEME STATE AID GUIDANCE BRITISH HORSERACING GRANT SCHEME STATE AID GUIDANCE Part 1 - Introduction 1. EU State aid law is relevant to any distribution of funds from the Tote

Evaluation of BBSRC s Follow-on Fund

Evaluation of BBSRC s Follow-on Fund July 2014 This document represents the views and conclusions of a panel of experts. Contents Abbreviations... 4 Key Definitions... 5 Executive Summary... 7 1. Introduction...

Evaluation of BBSRC s Follow-on Fund July 2014 This document represents the views and conclusions of a panel of experts. Contents Abbreviations... 4 Key Definitions... 5 Executive Summary... 7 1. Introduction...

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT concept and practical implementation Discussion paper I Introduction The objective of this discussion paper is to explain the concept of managerial accountability

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT concept and practical implementation Discussion paper I Introduction The objective of this discussion paper is to explain the concept of managerial accountability

FB-1048/2013 São Paulo, July 02, Ref.: IASB - Exposure Draft Financial Instruments: Expected Credit Losses - ED/2013/3

Tel.: 55 11 3244 9800 FB-1048/2013 São Paulo, July 02, 2013. International Accounting Standard Board 30 Cannon Street London, EC4M 6XH United Kingdom Ref.: IASB - Exposure Draft Financial Instruments:

Tel.: 55 11 3244 9800 FB-1048/2013 São Paulo, July 02, 2013. International Accounting Standard Board 30 Cannon Street London, EC4M 6XH United Kingdom Ref.: IASB - Exposure Draft Financial Instruments:

IASB Project Update & Agenda Planning

STAFF PAPER Accounting Standards Advisory Forum December 2017 Project Paper topic Accounting Standards Advisory Forum IASB Project Update & Agenda Planning CONTACT(S) Michelle Sansom msansom@ifrs.org +44

STAFF PAPER Accounting Standards Advisory Forum December 2017 Project Paper topic Accounting Standards Advisory Forum IASB Project Update & Agenda Planning CONTACT(S) Michelle Sansom msansom@ifrs.org +44

Recent Developments in Patent Law in Singapore

Recent Developments in Patent Law in Singapore WIPO 27 th SCP Mr Alfred Yip Director, Registries of Patents, Designs and Plant Varieties, IPOS 1 Main Amendments to Singapore Patents Law: 1. Closure of

Recent Developments in Patent Law in Singapore WIPO 27 th SCP Mr Alfred Yip Director, Registries of Patents, Designs and Plant Varieties, IPOS 1 Main Amendments to Singapore Patents Law: 1. Closure of

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606 March 2017 Revenue Recognition Background In May 2014, the FASB 1 and IASB issued their

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 606 March 2017 Revenue Recognition Background In May 2014, the FASB 1 and IASB issued their

What is the Research & Development (R&D) Tax Incentive?

Tax Incentive?") R&D TAX INCENTIVE What is the Research & Development (R&D) Tax Incentive? The R&D Tax Incentive program is the Australian Government s principle measure to enhance and increase the amount of research and

R&D TAX INCENTIVE What is the Research & Development (R&D) Tax Incentive? The R&D Tax Incentive program is the Australian Government s principle measure to enhance and increase the amount of research and

REVISED SWISS CORPORATE TAX REFORM WILL KEEP SWITZERLAND A TOP CORPORATE LOCATION

REVISED SWISS CORPORATE TAX REFORM WILL KEEP SWITZERLAND A TOP CORPORATE LOCATION Authors Danielle Wenger Manuel Vogler Tags Corporate Tax Tax Reform Switzerland INTRODUCTION This article focuses on the

REVISED SWISS CORPORATE TAX REFORM WILL KEEP SWITZERLAND A TOP CORPORATE LOCATION Authors Danielle Wenger Manuel Vogler Tags Corporate Tax Tax Reform Switzerland INTRODUCTION This article focuses on the

A guide to intellectual property and intangible assets

A guide to intellectual property and intangible assets Identifying, protecting and valuing intellectual property within your business Corporate Finance PRECISE. PROVEN. PERFORMANCE. Not surprisingly intellectual

A guide to intellectual property and intangible assets Identifying, protecting and valuing intellectual property within your business Corporate Finance PRECISE. PROVEN. PERFORMANCE. Not surprisingly intellectual

SR&ED and the Plastics Sector Issues and Recommendations

Scientific Research and Experimental Development SR&ED and the Plastics Sector Issues and Recommendations Western Plastics Association Member Meeting September 12, 2017 Wayne Pattern PEng, PMP Senior Manager,

Scientific Research and Experimental Development SR&ED and the Plastics Sector Issues and Recommendations Western Plastics Association Member Meeting September 12, 2017 Wayne Pattern PEng, PMP Senior Manager,

EBF Comment Letter on the IASB Exposure Draft - Financial Instruments: Expected Credit Losses

Chief Executive DM/MT Ref.:EBF_001692 Mr Hans HOOGERVORST Chairman International Accounting Standards Board 30 Cannon Street London, EC4M 6XH United Kingdom Email: hhoogervorst@ifrs.org Brussels, 5 July

Chief Executive DM/MT Ref.:EBF_001692 Mr Hans HOOGERVORST Chairman International Accounting Standards Board 30 Cannon Street London, EC4M 6XH United Kingdom Email: hhoogervorst@ifrs.org Brussels, 5 July

CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE

RÉPUBLIQUE FRANÇAISE CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE 2008 CENTRAL GOVERNMENT ACCOUNTING STANDARDS CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE 2008 CONTENTS 3/202 CENTRAL GOVERNMENT ACCOUNTING

RÉPUBLIQUE FRANÇAISE CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE 2008 CENTRAL GOVERNMENT ACCOUNTING STANDARDS CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE 2008 CONTENTS 3/202 CENTRAL GOVERNMENT ACCOUNTING

Intangible Assets: Measurement and Accounting Practices

Contents Overview Intangible Assets: Measurement and Accounting Practices Section I Creative Value and Perspectives 1. Intangible Asset: An Introduction 3 Archana Dinesh Mehta and Pankaj M Madhani 2. Management

Contents Overview Intangible Assets: Measurement and Accounting Practices Section I Creative Value and Perspectives 1. Intangible Asset: An Introduction 3 Archana Dinesh Mehta and Pankaj M Madhani 2. Management

History of the Ryan Indexes

Ryan ALM, inc. Asset/Liability Management The Solutions Company History of the Ryan Indexes Ronald Ryan, CEO, CFA When I was the Director of Fixed Income Research at Lehman during the late 1970s and early

Ryan ALM, inc. Asset/Liability Management The Solutions Company History of the Ryan Indexes Ronald Ryan, CEO, CFA When I was the Director of Fixed Income Research at Lehman during the late 1970s and early

The Knowledge Development Box ( KDB ) Public Consultation Paper. We are writing to respond to the above named document issued on 14 January 2015.

Public Consultation Paper. We are writing to respond to the above named document issued on 14 January 2015.") 47 49 Pearse Street, Dublin 2, IRELAND The Knowledge Development Box Public Consultation Tax Policy Division Department of Finance Government Buildings Upper Merrion Street Dublin 2 by email to KDBconsultation@finance.gov.ie

47 49 Pearse Street, Dublin 2, IRELAND The Knowledge Development Box Public Consultation Tax Policy Division Department of Finance Government Buildings Upper Merrion Street Dublin 2 by email to KDBconsultation@finance.gov.ie

Highland Foundry Ltd. v. R. Highland Foundry Ltd. v. Her Majesty The Queen. Tax Court of Canada. McArthur J.T.C.C. Judgment: August 15, 1994

Highland Foundry Ltd. v. R. Highland Foundry Ltd. v. Her Majesty The Queen Tax Court of Canada McArthur J.T.C.C. Judgment: August 15, 1994 Year: 1994 Docket: Court File No. 92-264 Counsel: T.C. Armstrong

Highland Foundry Ltd. v. R. Highland Foundry Ltd. v. Her Majesty The Queen Tax Court of Canada McArthur J.T.C.C. Judgment: August 15, 1994 Year: 1994 Docket: Court File No. 92-264 Counsel: T.C. Armstrong

Chapter 2 - Business Framework: The Theory of the Firm and the Reasons for the Existence of Multinational Enterprises

This is a working draft of a Chapter of the Practical Manual on Transfer Pricing for Developing Countries and should not at this stage be regarded as necessarily reflecting finalised views of the UN Committee

This is a working draft of a Chapter of the Practical Manual on Transfer Pricing for Developing Countries and should not at this stage be regarded as necessarily reflecting finalised views of the UN Committee

Distinguishing Liabilities from Equity Invitation to Comment Private Company Council

Distinguishing Liabilities from Equity Invitation to Comment Private Company Council September 30, 2016 1 Agenda History of liabilities & equity Perceived issues Approaches to improve the guidance - Simple

Distinguishing Liabilities from Equity Invitation to Comment Private Company Council September 30, 2016 1 Agenda History of liabilities & equity Perceived issues Approaches to improve the guidance - Simple