2012 Tax guideline for Central and Eastern Europe

|

|

|

- Laura Dickerson

- 5 years ago

- Views:

Transcription

1 2012 Tax guideline for Central and Eastern Europe Overview of legal forms of business, social and health security, labor law and taxation system in CEE countries

2 Contents 01 About us Our locations Czech Republic /01 Legal forms of business /02 Social and health security /03 General comments on labor law /04 General rules on purchasing of real estates /05 Advantages of investing (Investment incentives) /06 Taxation system /06/01 Corporate Income Tax (CIT) /06/02 Personal Income Tax (PIT) /06/03 Value Added Tax (VAT) /06/04 Other taxes /06/05 Tax calendar Hungary Poland Romania Slovakia... 33

3 01 About us Accace is one of the most dynamic outsourcing and consulting companies operating within the region of Central and Eastern Europe (CEE). Accace was founded in September 2006 in order to provide its clients with professional consulting services in financial accounting, tax and payroll advisory, including outsourcing. We develop IT solutions (esolutions) and we are a certified partner of Microsoft for the delivery of Microsoft Dynamics NAV. Portfolio of our services includes: Accounting and reporting Payroll agenda Tax advisory Corporate and trust services esolutions Microsoft Dynamics NAV implementation and outsourcing 02 Our locations We successfully perform our business in ten countries of CEE region. Our permanent subsidiaries are located in: Czech Republic Hungary Romania Poland Slovak Republic Ukraine Moreover, in cooperation with our business partners we also provide services in: Bulgaria Croatia Serbia Slovenia

03/01 Legal forms of business English The form of business Czech The minimum capital The most preferred form of business and reasons Unlimited")

4 03 Czech Republic Capital: Prague Official language: Czech Official currency: CZK Population: 10.5 million Area: 78,864 sqkm GDP growth: 2% (2011) 03/01 Legal forms of business English The form of business Czech The minimum capital The most preferred form of business and reasons Unlimited partnership Veřejná obchodní společnost / v.o.s. 0 Limited partnership Komanditní společnost / k.s. 0 Limited Liability Company Společnost s ručením omezeným / s.r.o. EUR 7,860 Company Limited by Shares Closed Public Akciová společnost, a.s. s veřejnou nabídkou akcií Branch Offices Organizační složka 0 EUR 78,570 EUR 785,660 S.r.o. Low establishment costs Fast establishment and registration Limited liability of the shareholders

5 03/02 Social and health security Payrolls and Contribution Employee Employer Social security (pension insurance) 6.5% 21.5% Social security (sickness insurance) NA 2.3% Social security (unemployment insurance) NA 1.2% Health insurance 4.5% 9.0% TOTAL 11% 34% A maximum assessment base for employers and employees applies. It equals 48 times the monthly average salary for social insurance and 72 times the monthly average salary for health insurance. For 2012, the maximum annual assessment base is EUR 47, for social insurance and EUR 2, for health insurance. 03/03 General comments on labor law Labor law Czech Republic Applicable law on labor Contract type Labor contract (can be for definite or indefinite period of time), agreement to complete a job, agreement to perform work Act No. 262/2006 Coll., the Labor Code Contract must include: Written form, must include: type and place of work, start date If the labor contract does not include remuneration, length of vacation, working hours and terminate period, the employer has to inform the employee in written form within 1 month after beginning of the employment Working time 40 hours per week Holiday entitlement per year 20 days per year

6 03/04 General rules on purchasing of real estates All types of real estate may be acquired by individuals with permanent residence in the territory of the Czech Republic or legal entities with the registered offices in the Czech Republic (resident status) without any restrictions. From the 18 th of July 2011 this regulation has also been modified in relation to foreigners (EU / non EU), so that foreign individuals and legal persons are no more restricted from acquisition of real estate in the Czech Republic. Applicable law: Act No. 219/1995 Coll., The Foreign Exchange Act, as amended. 03/05 Advantages of investing (Investment incentives) One of the most successful CEE countries of attracting foreign direct investment Corporate income tax flat rate 19% Very good geographical position and infrastructure Highly educated and skilled workforce Low labor costs compared to western countries Safe investment environment Transparent system of investment incentives

7 03/06 Taxation system 03/06/01 Corporate Income Tax (CIT) Corporate Income Tax (CIT) Czech Republic Applicable law on CIT CIT 19% Act No. 586/1992 Coll., on Advance payments Quarterly or semi-annually based on amount of tax liability Income Taxes, as amended paid for previous taxable period: Filling the CIT Up to EUR 1,180 corporate income tax liability of previous taxable period no advance payment Up to EUR 5,890 corporate income tax liability of previous taxable period 40% of the tax liability, payable semi-annually More than EUR 5,890 corporate income tax liability of previous taxable period 1/4 of the tax liability, payable quarterly The corporate tax period can be a calendar year, or fiscal year (12 consecutive calendar months) Generally the deadline for filing CIT return is end of third month following the end of the taxable period. If the CIT return is filed by tax advisor or the taxpayer has the obligation of the statutory audit, the deadline for filing CIT return is the end of sixth month following the end of the taxable period.

8 03/06/02 Personal Income Tax (PIT) Personal Income Tax (PIT) Czech Republic Applicable law on PIT Personal income tax Flat rate 15% Advance payment Filling the PIT In case of income from dependent activity (employment) the PIT base equals gross income increased by social security and health insurance paid by employer (generally 34% of the gross income) Quarterly or semi-annually based on amount of tax liability paid for previous calendar year: Up to EUR 1,180 corporate income tax liability of previous calendar year no advance payment, Up to EUR 5,890 corporate income tax liability of previous calendar year 40% of the tax liability, payable semi-annually More than EUR 5,890 corporate income tax liability of previous calendar year 1/4 of the tax liability, payable quarterly The advance payments from dependent activity (employment) is withheld by employer on a monthly basis Generally the deadline for filing PIT return is the end of third month following the end of the taxable period. The PIT period is calendar year. If the PIT return is filed by tax advisor, the deadline for filing PIT return is the end of sixth month following the end of the taxable period. Act No. 586/1992 Coll., on Income Taxes, as amended

9 03/06/03 Value Added Tax (VAT) Value Added Tax (VAT) Czech Republic Applicable law on VAT Basic rate 20% Act No 235/2004 Coll., on Reduced rate 14% Value Added tax, as amended Thresholds registration general EUR 39,280 (for a total period of 12 consecutive calendar months), No VAT registration for taxable person in case of intracommunity acquisition of goods from another EU- Member state if value of those transactions cumulative do not exceeded EUR 12,800 in calendar year The voluntary VAT registration is possible as well VAT group registration VAT return period Monthly if turnover in preceding calendar year reached EUR 393,753, optional if turnover was between EUR 78,752 and EUR 393,753 Quarterly if turnover in the preceding calendar year was less than EUR 393,753 or for foreign tax payers without VAT establishment

10 03/06/04 Other taxes Other taxes Czech Republic Applicable law on other taxes Inheritance tax Tax rates are progressive and range from 0.5% to 20%, depending on the tax base Large exemptions for relatives Gift tax Tax rates are progressive and range from 1 % to 40 %, dependent on the tax base Real estate transfer tax Real estate tax Road tax Excise duties 3% rate Large exemptions for relatives Imposed on lands and buildings Imposed on motor vehicles used for business purposes Imposed on specific products (e.g. fuel, alcohol, tobacco) Act No. 357/1992 Coll., on inheritance, gift and transfer of the real estate tax Act No. 338/1992 Coll., on real estate Act No. 16/1993 Coll., on road tax Act No. 353/2003 Coll., on excise duties

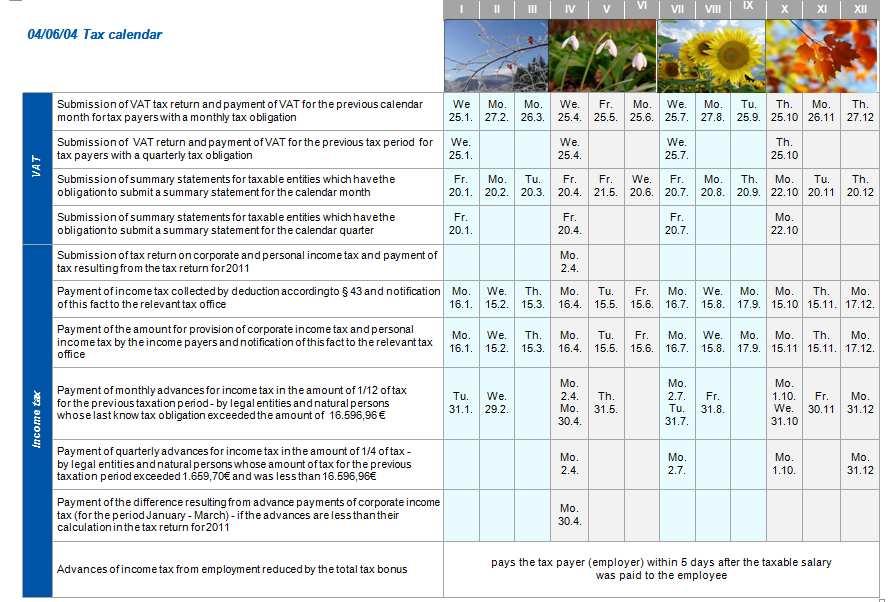

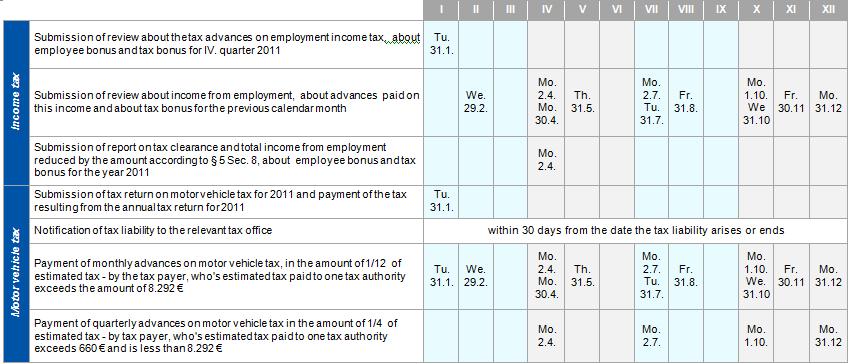

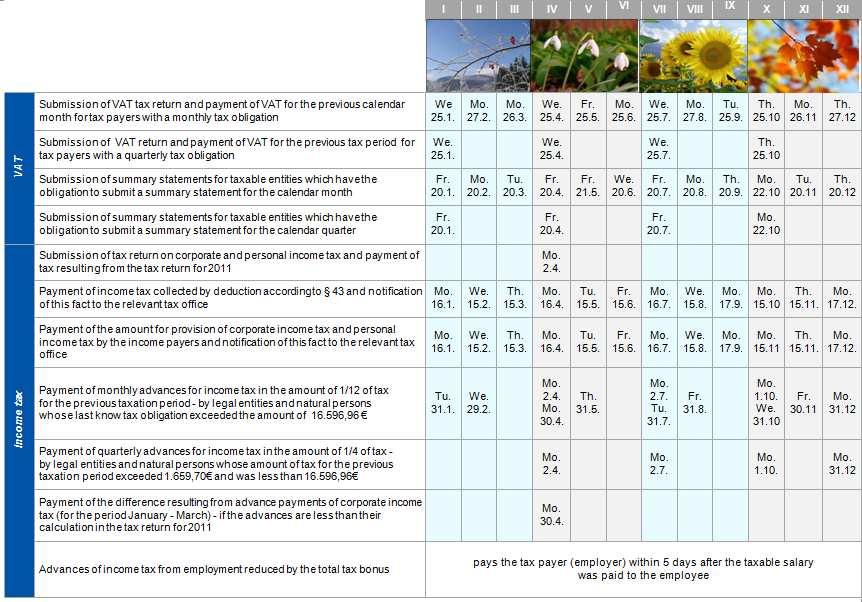

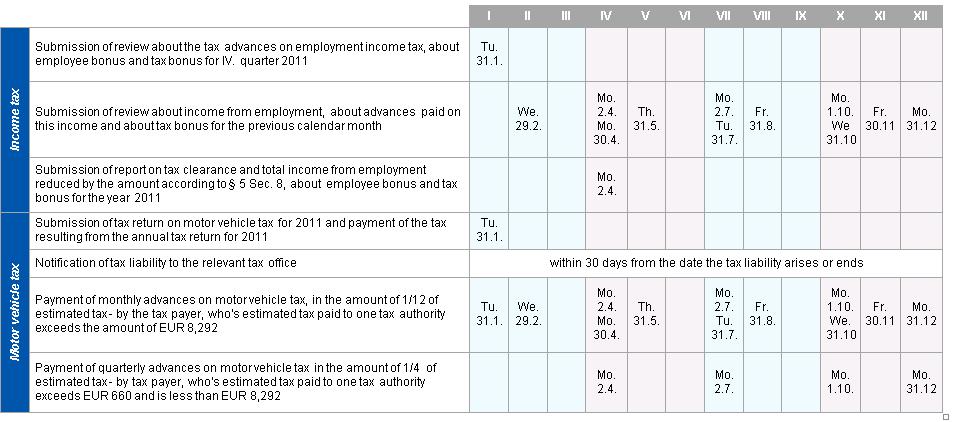

11 I II III IV V VI VII VIII Submission of VAT return and payment of VAT for the previous calendar month for tax payers with a monthly tax obligation Submission of VAT return and payment of VAT for the previous tax period for tax payers with a quarterly tax obligation Submission of EC sales list for taxable entities which have the obligation to submit an EC sales list for the calendar month Submission of EC sales list for taxable entities which have the obligation to submit a EC sales list for the calendar quarter Submission of Intrastat declaration for entities with have the obligation to submit the Intrastat declaration (electronic form) Tu IX X XI XII VAT 03/06/05 Tax calendar Submission of tax return on corporate e and personal income tax and payment of tax resulting from the tax return for 2011 (if taxable period is calendar year) Payment of quarterly advances for corporate and personal income tax Payment of semi-annual advances es for corporate and personal income tax Income tax Tu Tu Tu. Tu Tu Submission ubmission of tax return on corporate and personal income tax filed by tax advisor or if the company hass statutory audit and payment of tax resulting from the tax return for 2011 (if taxable period is calendar year) Payment of monthly advances for income tax from dependent activity (employment) Tu Tu

12 I II III IV V VI VII VIII IX X XI XII Road tax Submission of tax return on road tax for 2011 and payment of the tax resulting from the annual tax return for 2011 Advanced payment on road tax Tu Real estate tax Submission of tax return on real estate tax for 2012 Payment of real estate tax if the tax liability amounts does not exceed EUR 197 Payment of real estate tax if the tax liability amounts does exceed EUR 197 Tu

13 04 Hungary Capital: Budapest Official language: Hungarian Official currency: HUF Population: 9.9 million Area: 93,030 sqkm GDP growth: 1% 04/01 Legal forms of business English The form of business Hungarian The minimum capital The most preferred form of business and reasons Unlimited partnership Közkereseti Társaság / Kkt 0 Limited partnership Betéti Társaság / Bt. 0 Limited Liability Company Korlátolt Felelősségű Társaság / Kft. EUR 1,737 Company Limited by Shares Closed Public Részvénytársaság / Rt.: Zártkörűen működő / Zrt. Nyilvánosan működő / Nyrt. Branch Offices Fióktelep 0 Representative Offices Kereskedelmi Képviselet 0 EUR 17,365 EUR 69,462 Kft. Low establishment costs Fast registration Easier to establish a new standard Kft. than to buy a shell company Limited liability of the shareholders

14 04/02 Social and health security Payrolls and Contribution Employee Employer Social contribution tax / pension contribution 10% 27% Health insurance 7% NA Unemployment insurance 1.5% NA Charges training contribution - 1.5% TOTAL 18.5% 28.5% 04/03 General comments on labor law Contract type Contract must include: Working time Labor law Hungary Applicable law on labor Can be concluded for definite and indefinite term. Act on Labor Law (1992. XXII.) Written form, must include: type and place of work, start New Act on Labor date, remuneration corresponding to type of work, working Law (2012. I.) hours. 40 hours per week Holiday entitlement per year days per year (depending on the age of the employee) Other comments The minimum wage in Hungary is EUR 323

15 04/04 General rules on purchasing of real estates Foreign individuals wishing to purchase real estate in Hungary must obtain a permit from the Government Agency. Hungarian companies with foreign shareholders can purchase real estate without restrictions Concerning citizens and entrepreneurs (including companies) of EEA countries (EU countries + Iceland, Liechtenstein and Norway) and Switzerland do not have to obtain a permit to acquire real estate or shares in companies which are owners of real estate unless the real estate comprises forest or agricultural land 04/05 Advantages of investing (Investment incentives) Preferential corporate income tax rate (corporate income tax rate: 10%) Development benefits (tax and other benefits) for huge investments Research and development benefits for every entity performing research Tax incentives for royalty income Tax benefits for supporting certain organisations (film production companies, sport organisations)

16 04/06 Taxation system 04/06/01 Corporate Income Tax (CIT), local business tax (LBT) Corporate Income Tax (CIT), Local business tax (LBT) Hungary Applicable law on CIT and LBT CIT 19% Act on Corporate Income Tax (Act LXXXI. 1996) Reduced CIT *10% Act on local taxes (Act C. 1990) Local business tax **max. 2% Advance payments Filling the CIT, LBT tax return Tax benefits *Until tax base EUR 1,736,666 ** On the basis of the adjusted net sales revenue Until minimum 90% of income tax and local tax Until / within 150 days Development tax benefit, incentives provided to sport organizations / film production companies 04/06/02 Personal Income Tax (PIT) Personal Income Tax (PIT) Hungary Applicable law on PIT Minimum wage EUR 323 Act on Personal Income Tax (Act Average wage EUR 815 CXVII. 1995) Personal income tax 16% % Tax benefits Child care benefit, sickness benefit

17 04/06/03 Value Added Tax (VAT) Value Added Tax (VAT) Hungary Applicable law on VAT Basic rate 27% Act on Value Added Tax (Act Reduced rate 5% and 18% CXXVII. 2007) Registration Quarterly payer Obligatory Basic registration Monthly payer Obligation / deduction over EUR 3,472 Yearly payer Obligation / deduction up to EUR 868 / year (without EU VAT number) 04/06/04 Other taxes Other taxes Hungary Applicable law on other taxes Property tax Max. 3% of the adjusted value of the property Act on local taxes (Act C. 1990) Inheritance duty 0-40% Gift duty 0-40% Act on duties (Act XCIII. 1991) Innovation contribution *0.3% Real estate transfer duty 4% *On the basis of the adjusted net sales revenue

18 I II III IV V VI VII VIII IX X XI XII Submission of VAT tax return and payment of VAT for the previous calendar month for tax payers with a monthly tax obligation Tu Tu Submission of VAT return and payment of VAT for the pr previous tax period for tax payers with a quarterly tax obligation Tu VAT 04/06/05 Tax calendar Th Income tax Submission of tax return on corporate and locall business for 2011 Payment of the corporate income tax advance payments for 2011, 2012 with monthly obligation Payment of the corporate income tax advance payments for 2011, 2012 with quarterly obligation Tu Th Mo Mo Payment of the local business tax advances Mo Tu Th Submission of the personal income tax return for Payment of the difference resulting from advance payments of corporate income tax and local business tax (for the period January - December) - if the advances are less than the amount in fact Th Submission of VAT tax return on annual basis Paymentt of monthly advances for personal income tax, social security contribution by the employer Th Mo Th

19 05 Poland Capital: Warsaw Official language: Polish Official currency: PLN Population: 38.5 million Area: 312,679 sqkm GDP growth: 3.8% 05/01 Legal forms of business English The form of business Polish The minimum capital The most preferred form of business and reasons Sole proprietorship jednoosobowa działalność gospodarcza 0 Registered partnership Spółka jawna / sp.j. 0 Professional partnership Spółka partnerska / sp.p. 0 Limited partnership Spółka komandytowa / sp.k. 0 Limited joint-stock partnership Spółka komandytowo-akcyjna / S.K.A. 0 Limited liability company Spółka z ograniczoną odpowiedzialnością / sp. z o.o.) EUR 1,160 Joint-stock company Spółka akcyjna / S.A. EUR 23,160 Branch office Oddział przedsiębiorcy zagranicznego 0 Representative office Przedstawicielstwo 0 Sp. z o.o. Low establishment costs Minimum share capital EUR 1,160 Easy establishment Limited lability of the shareholders

20 05/02 Social and health security Payrolls and Contribution Employee Employer Retirement pension contribution 9.76% 9.76% Pension contribution 1.5% 6.5% Sickness contribution 2.45% NA Disability pension NA 0.67% % Health insurance 9% NA Employment Fund NA 2.45% Fund of Guaranteed Employment Benefits NA 0.10% TOTAL 22.71% 19.48% 22.67% 05/03 General comments on labor law Labor law Poland Applicable law on labor Contract type Contract must include: Working time Trial period, definite term, indefinite period, to perform a specific task, fixedterm if replacing an employee during his justified absence from work Parties, type of contract, date of the contract conclusion, work and remuneration conditions which are: the nature of the work, the place of work, the amount of remuneration for work corresponding to the type of the work, including individual components of remuneration, working time, the date of commencement of work 40 hours per week Labor Law Code as of 26 th of June 1974 Holiday entitlement per year 20 or 26 days per year depending on employment period

21 05/04 General rules on purchasing of real estates The agreement has to be concluded in a form of notarial deed. Agreement concluded in another form is invalid Foreigners (individuals and entities) wishing to purchase real estate in Poland must obtain a permit from the Minister of Internal Affairs and Administration Concerning citizens and entrepreneurs (including companies) of EEA countries (EU countries + Iceland, Liechtenstein and Norway) and Switzerland do not have to obtain a permit to acquire real estate or shares in companies which are owners or perpetual usufructuaries of real estate unless the real estate comprises forest or agricultural land this restriction will continue to apply until 2 nd of May 2016 (there are, however, some additional exceptions to this restriction, namely unrestricted acquisition of agricultural or forest land is enjoyed by tenants from the EEA and Switzerland that have used the land under lease agreements (umowa dzierżawy) for a minimum of 3 or 7 years, depending on the location of the land and subject to certain other conditions) 05/05 Advantages of investing (Investment incentives) Stable economic growth Corporate income tax - competitive flat rate 19% Strong consumer market - one of the biggest in Europe The main communication routs intersect in Poland Wide range of investment incentives - 14 Special Economic Zones (SEZ). i.e. special zones where economic activity may be run in favourable conditions Highly educated and experienced employees engineers, IT specialist, scientists and economists Real estate tax incentives provided by municipalities EU subsidies for the companies

22 05/06 Taxation system 05/06/01 Corporate Income Tax (CIT) Corporate Income Tax (CIT) Poland Applicable law on CIT CIT 19% Act of 15 February 1992 on Advance payments Monthly - until 20 th day of each month Corporate Income Tax Filling the CIT 3 months since the end of fiscal year 05/06/02 Personal Income Tax (PIT) Personal Income Tax (PIT) Poland Applicable law on PIT Minimum wage EUR 360 gross Act of 26 July 1991 on Personal Average wage EUR 816 gross Income Tax Personal income tax 18% or 32% 05/06/03 Value Added Tax (VAT) Value Added Tax (VAT) Poland Applicable law on VAT Basic rate 23% Act of 11 March 2004 on Goods Reduced rate 0%, 3%, 5% and 8% and Services Tax Registration Monthly payer Quarterly payer Exemption Obligatory Basic registration The possibility to submit quarterly VAT return depends on the prior written notification to the Head of the Tax Office Exemption if the taxable turnover less than EUR 34,750 in previous fiscal year

23 05/06/04 Other taxes Other taxes Poland Applicable law on other taxes Property tax Determined by proper municipality council Local Taxes and Duties Act as of 12 January 1991 Inheritance and gift tax 0% - 20% depending on tax group and Inheritance and Gift tax Act of 28 gift/inheritance value July 1983 Tax on civil law transactions 0.1% - 2% Act of 9 September 2000 on Tax Agriculture tax Forest tax Tax on transport vehicles Gambling tax 10% - 50% Tonnage tax 19% Fuel duty Environment usage duty Products duty Depending on the market price of rye (price for 2.5 q or 5 q of rye for 1 ha) Depending on the marker price of wood Determined by proper municipality council EUR (PLN 99.19) for 1000 l of fuel EUR (PLN ) for 1000 l of diesel oils EUR (PLN ) for 1000 kg of gas Determined in the attachments to the Announcement of the Minister of Environment Determined by the Regulation of the Minister of Environment on Civil Law Transactions Act of 30 October 2002 on Forest Tax Act of 15 November 1984 on Agricultural Tax Act of 19 November 2009 on Gambling Act of 25 August 2006 on Tonnage Tax Act of 27 October 1994 on paid highways and National Road Fund Announcement of the Minister of Transport of 16 December 2011 on Fuel Duty Announcement of the Minister of Environment of 16 September 2011 on the Environment Usage Duty Act of 11 May 2011 on the Entrepreneurs Duties Regarding the Management of Wastes and Product duty Regulation of the Minister of Environment of 29 December 2010 on the Product Duty Rates

24 I II III IV V VI VII VIII Submission of VAT tax return and payment of VAT for the previous calendar month for tax payers with a monthly tax obligation We Submission of VAT return and payment of VAT for the previous tax period for tax payers with a quarterly tax obligation Submission on of EC Sales List for taxpayers which have the obligation to submit EC Sales List for the calendar month Submission of EC Sales List st for taxpayers which have the obligation to submit EC Sales List for the calendar quarter IX X XI XII Income tax VAT 05/06/05 Tax calendar Submission ubmission of tax return on personal income tax and payment of tax resulting from the tax return for Payment of quarterly advances for income tax by legal entities and natural persones conducting business activity PIT installments paid by employer Tu Submission ubmission of tax return on corporate income tax and payment of tax resulting from the tax return for 2011 Payment of monthly advances for income tax by legal entities and natural persons conducting business activity Tu Tu Tu Tu Tu

06/01 Legal forms of business English The form of business Romanian The minimum capital The most preferred form of business and reasons Subsidiary")

25 06 Romania Capital: Bucharest Official language: Romanian Official currency: RON Population: million Area: 238,391 sqkm GDP growth: 2% (2011) 06/01 Legal forms of business English The form of business Romanian The minimum capital The most preferred form of business and reasons Subsidiary Filiala Same conditions as the parent company General partnership company Limited partnership company Limited joint-stock partnership company Societate in nume colectiv Societate In comandita simpla The law does not specify a minimum limit The law does not specify a minimum limit Societate in comandita pe actiuni The equivalent of EUR 25,000 Limited liability company Societate cu raspundere limitata (SRL) The equivalent of EUR 45 Joint-stock company Societate pe actiuni (SA) The equivalent of EUR 25,000 Branch office Sucursala 0 Representative office Reprezentanta 0 SRL Low establishment costs Low minimum share capital Fast registration Limited liability of shareholders

26 06/02 Social and health security Payrolls and Contribution Employee Employer Health insurance 5.5% 5.2% Social (Pension) contribution 10.5%* 20.8%** Sickness contribution NA 0.85%*** Unemployment fund 0.5% 0.5% Accident Fund NA % Fund of Guaranteed Employment Benefits NA 0.25 TOTAL 16.5% 27.75% 28.45% * Maximum base = 5* average salary ** Maximum base = number employees*5* average salary *** Maximum base = number employees*12* minimum salary Salary Type of salary Amount in EUR Monthly minimum gross salary 160* Average gross salary 481* *applicable for the year 2012

27 06/03 General comments on labor law Labor law Romania Applicable law on labor Contract type Definite term, indefinite period, home work, part time work, temporary agent Labor Law Code Republished Parties, duration of the contract if the contract is a definite type or if is conclude on 18 th of May 2011 Contract must include: by means of temporary agent, date of the contract conclusion, work and remuneration conditions, the place where the work is performed, evaluation criteria of the employee, the occupation, the risks of the job, number of vacation days, number of days applicable for the notice, number of working hours per day and per week, probationary period, the date of commencement of work Working time 40 hours per week Holiday entitlement per year Minimum 20 working days 06/04 General rules on purchasing of real estates The agreement has to be concluded in a form of a public notary. Agreements concluded in another form are null and void All foreigners can acquire buildings in Romania Starting from 1 st of January 2012 EU citizens can also acquire the land beneath the building, if the building is purchased in residential purposes or as secondary premises Limitations imposed by legislation for acquiring agricultural land, forests and forestry land. Such restriction shall be available until 1 st of January 2014 EU farmers who develop independent activities and establish their residence in Romania are not subject to the limitations above regarding agriculture and forestry land and they acquire land starting from 1 st of January 2007 The same situation applies to stateless persons that are domiciled in Romania Non EU members can acquire land in Romania only based on international and bilateral conventions

28 06/05 Advantages of investing (investment incentives) Corporate income tax - competitive flat rate 16% Strong consumer market Highly educated and experienced employees engineers, IT specialist and economists 20% supplementary deduction for corporate income tax purposes applicable to eligible R&D activities 5% reduced VAT rate for real estate transactions under certain conditions Subsidies granted by the State for hiring fresh graduates Income tax exemption for IT programmers under certain conditions Tax losses - Generous carry forward period (7 years) Dividend tax exemption for reinvested dividends EU subsidies for the companies 06/06 Taxation system 06/06/01 Corporate Income Tax (CIT) Corporate Income Tax (CIT) Romania Applicable law on CIT and LBT CIT The standard rate for corporate income tax for Romanian companies is 16%. Income derived by companies from night bars, nightclubs, discos and casinos directly or in association is taxable at a rate of 16%, but the amount of tax liability cannot be less than 5% of the gross income derived from such activities. Advance payments Companies are required to pay CIT liabilities quarterly and at year end; at quarterly level CIT liabilities are determined based on the figures within the quarter; at year end a calculation and regularization of annual CIT is made. Banks and financial institutions apply a different system i.e. the quarterly liabilities are not determined based on the figures within the quarter, instead the quarterly liabilities are determined by reference to the previous year annual CIT liability dived by four. This system will be extended starting 2013 to all the companies. Fiscal Code Law 571/2003 and the related methodological Norms Government Decision 44/2004

29 Corporate Income Tax (CIT) Romania Applicable law on CIT and LBT Filling the CIT declarations Under the profits tax law, profits tax payers (companies, branches, permanent establishments, etc) must file tax return quarterly by 25th day of the first month of the following quarter. Tax benefits The annual profits tax return must be filed by 25th of March of the following year. Profits tax. The Fiscal Code allows companies to claim accelerated depreciation in certain circumstances. The Fiscal Code allows sponsorship expenses to be claimed as a credit against profits tax due, subject to certain limitations. The tax credit for sponsorship expenses is limited to the lower of the following: 0.3% of the company s turnover 20% of the profits tax due Research and development costs. Taxpayers can benefit from an additional allowance amounting to 20% of eligible costs for research and development activities (i.e. 120% deduction). Thin-cap rules Interest and FX expenses that are deemed as non-deductible for CIT purposes in one year due to debt-equity ratio higher than 3 or negative can be carried forward indefinitely and deducted at a moment when the debt-equity ratio is restored.

30 06/06/02 Personal Income Tax (PIT) Personal Income Tax (PIT) Romania Applicable law on PIT Minimum gross salary EUR 160 Average gross salary EUR 481 Personal income tax 16% Tax benefits Flat tax rate General tax-free allowance Income tax exemption for the employees performing programming activities under certain conditions. Fiscal Code Law 571/2003 and the related methodological Norms Government Decision 44/ /06/03 Value Added Tax (VAT) Value Added Tax (VAT) Romania Applicable law on VAT Basic rate 24% Reduced rate Registration Tax period 5% and 9% - for certain goods and services Certain enterprises, products and services are exempt, including banks, financial intermediaries and insurance companies The threshold for mandatory VAT registration for taxable entity with registered office, place of business or fix establishment located in Romania is turnover of EUR 35,000 (expected increase of the threshold in the near future EUR 65,000). The taxpayers may require the VAT registration upon their request. Month or quarter Fiscal Code Law 571/2003 and the related methodological Norms Government Decision 44/2004

31

32

07/01 Legal forms of business English The form of business Slovak The minimum capital The most preferred form of business and reasons General commercial partnership Verejná")

33 07 Slovakia Capital: Bratislava Official language: Slovak Official currency: Euro Population: 5.4 million Area: 49,036 sqkm GDP growth: 3.4% (4 th quarter of 2011) 07/01 Legal forms of business English The form of business Slovak The minimum capital The most preferred form of business and reasons General commercial partnership Verejná obchodná spoločnosť (v.o.s.) NA Limited partnership Limited liability Company Komanditná spoločnosť (k.s.) Spoločnosť s ručením obmedzeným (s.r.o.) EUR 250 / minimum deposit of limited partner EUR 5,000 Joint stock company Akciová spoločnosť (a.s.) EUR 25,000 Co(-)operatives Družstvo EUR 1,250 Trade Živnosť NA EUR 750 / minimum deposit of limited partner Ltd. / s.r.o. Low minimum capital Limited liability of shareholders Low operating costs Fast registration procedure

34 07/02 Social and health security Payrolls and Contribution Employee Employer Social security 9.4% 25.2% Health insurance 4% 10% TOTAL 13.4% 35.2% 07/02/01 Minimum wages Type of wage Amount in EUR Monthly minimum wage * Hourly minimum wage 1.880* * applicable for the year 2012

35 07/03 General comments on labor law Contract type Contract must include: Working time Holiday entitlement per year Other comments Labor law Slovakia Applicable law on labor Fixed-term contract, contract for indefinite period of time, contract on reduced working hours, contract on home-work and tele-work, temporary assignation agreement, work performance agreement, agreement on work activity, agreement on student job Job description, place of work, start date, payment conditions, pay day, working hours, holiday duration, length of termination notice period 40 hours per week (maximum of 48 or 56 hours per week in average) 20 days and 25 days in case of employee of 33 years and older Trial period (3, 6 or 9 months), statutory rules in case of employment termination, termination period (1, 2 or 3 months) Labor Code Act on social insurance Act on minimum salary Act regulating travel expenses Act on safety and health protection at work Act on illegal work and illegal employment 07/04 General rules on purchasing of real estates Foreign entities (natural or legal) can purchase almost any real estate in Slovakia with the exception of: Land belonging to the Agricultural or Forest Land Sources located outside district build-up area (some exceptions are allowed) Specific real estate property purchase of which is limited by law (e.g. caves, rivers, cultural heritage and so on)

36 07/05 Taxation system 07/05/01 Corporate Income Tax (CIT) Corporate Income Tax (CIT) Slovakia Applicable law on CIT and LBT CIT 19% Act No. 595/2003 Coll. on Advance payments Quarterly or monthly based on amount of tax paid for previous Income Tax year Filling the CIT return Quarterly tax paid for previous year between EUR 1, EUR 16, Monthly more than EUR 16, The deadline for filing CIT is end of third month following the end of the taxable period. Generally the corporate tax period can be a calendar year, or fiscal year (12 consecutive calendar months) Tax benefits A taxpayer can extend the filing deadline for CIT maximum for another three months (or for six months if part of the taxpayer s source of income is from abroad). This extension is not subject to confirmation of tax office. Deduction of tax losses (five or seven consecutive tax periods). Dividends paid out of profits related to tax periods after 1 January 2004 are not subject to tax in Slovakia No real estate transfer tax No thin capitalization rules Transparent tax system

37 07/05/02 Personal Income Tax (PIT) Personal Income Tax (PIT) Slovakia Applicable law on PIT Minimum wage EUR (since ) Act No. 595/2003 Coll. on Income Average wage EUR 786 Tax Personal income tax 19% Tax benefits Flat tax rate General tax-free allowance, tax bonus

38 07/05/03 Value Added Tax (VAT) Value Added Tax (VAT) Slovakia Applicable law on VAT Basic rate 20% Act No. 222/2004 Reduced rate 10% Coll. on Value Added Tax Registration The threshold for mandatory VAT registration for taxable entity with registered office, place of business or fix establishment located in Slovakia is turnover of EUR 49,790 for a period of 12 previous consecutive calendar months. The voluntary VAT registration is possible as well. A taxable person - not registered as a VAT payer may have to obtain a VAT number and pay output VAT in case of intra-community acquisition of goods from another EU-Member state if value of those transactions cumulative exceeded EUR 13, in calendar year. A taxable person not registered as a VAT payer may have to obtain a VAT number and pay output VAT or report the supply of service in EC Sales list if the place of delivery for that service is: following the Article 44 of the Directive 2006/112/EC, located in another EU-Member state as is the EU-Member state of supplier of that service and person duty to tax will be the recipient of that service. VAT registration is mandatory for foreign taxable persons without registered office or fix establishment in Slovakia before it carries out activity which is subject to VAT in Slovakia and reverse charge mechanism is not applied. A foreign taxable person that makes long-distance sales (mail order business) in Slovakia to any person which is not registered as Slovak VAT payer and where the total value of the goods /supplies reaches EUR 35,000 in a calendar year. Tax period VAT group registration Month or quarter, based on turnover for previous calendar year

39

40

2013 Tax Guideline for Central and Eastern Europe

2013 Tax Guideline for Central and Eastern Europe Overview of Taxation System in CEE Countries, including the Legal Forms of Business, Social Security and Labor Law aspects Contents 01 Who Is Accace?...

2013 Tax Guideline for Central and Eastern Europe Overview of Taxation System in CEE Countries, including the Legal Forms of Business, Social Security and Labor Law aspects Contents 01 Who Is Accace?...

2018 TAX GUIDELINE. Poland.

2018 TAX GUIDELINE Poland poland@accace.com www.accace.com www.accace.pl Contents General information about Poland 4 Legal forms of business 5 General rules on purchasing real estate by foreigners 5 Legal

2018 TAX GUIDELINE Poland poland@accace.com www.accace.com www.accace.pl Contents General information about Poland 4 Legal forms of business 5 General rules on purchasing real estate by foreigners 5 Legal

2018 TAX GUIDELINE. Slovakia.

2018 TAX GUIDELINE Slovakia slovakia@accace.com www.accace.com www.accace.sk Contents General information about Slovakia 3 Legal forms of business 4 General rules on purchasing of real estate 4 Share deal

2018 TAX GUIDELINE Slovakia slovakia@accace.com www.accace.com www.accace.sk Contents General information about Slovakia 3 Legal forms of business 4 General rules on purchasing of real estate 4 Share deal

2017 TAX GUIDELINE. Hungary.

2017 TAX GUIDELINE Hungary hungary@accace.com www.accace.com www.accace.hu Contents General information about Hungary 3 Legal forms of business 4 Personal income tax and social contributions 6 Corporate

2017 TAX GUIDELINE Hungary hungary@accace.com www.accace.com www.accace.hu Contents General information about Hungary 3 Legal forms of business 4 Personal income tax and social contributions 6 Corporate

2019 TAX GUIDELINE. Czech Republic.

2019 TAX GUIDELINE Czech Republic czechrepublic@accace.com www.accace.com www.accace.cz Contents General information about the Czech Republic... 3 Legal forms of business... 4 General rules on purchasing

2019 TAX GUIDELINE Czech Republic czechrepublic@accace.com www.accace.com www.accace.cz Contents General information about the Czech Republic... 3 Legal forms of business... 4 General rules on purchasing

2018 TAX GUIDELINE. Hungary.

2018 TAX GUIDELINE Hungary hungary@accace.com www.accace.com www.accace.hu Contents General information about Hungary 3 Legal forms of business 4 Personal Income tax and Social Contributions 6 corporate

2018 TAX GUIDELINE Hungary hungary@accace.com www.accace.com www.accace.hu Contents General information about Hungary 3 Legal forms of business 4 Personal Income tax and Social Contributions 6 corporate

2018 Company Formation

2018 Company Formation Romania www.accace.com www.accace.ro Contents Legal forms of business, minimum capital, contribution 3 General Partnership (Societate in nume colectiv S.N.C.) 3 Limited Partnership

2018 Company Formation Romania www.accace.com www.accace.ro Contents Legal forms of business, minimum capital, contribution 3 General Partnership (Societate in nume colectiv S.N.C.) 3 Limited Partnership

2019 Company Formation

2019 Company Formation Hungary www.accace.com www.accace.hu Contents Legal forms of business, minimum capital, contribution 3 Limited Liability Company (Korlátolt Felelősségű Társaság Kft.) 3 Company Limited

2019 Company Formation Hungary www.accace.com www.accace.hu Contents Legal forms of business, minimum capital, contribution 3 Limited Liability Company (Korlátolt Felelősségű Társaság Kft.) 3 Company Limited

2018 Company Formation

2018 Company Formation Hungary www.accace.com www.accace.hu Contents Legal forms of business, minimum capital, contribution 3 Limited Liability Company (Korlátolt Felelősségű Társaság Kft.) 3 Company Limited

2018 Company Formation Hungary www.accace.com www.accace.hu Contents Legal forms of business, minimum capital, contribution 3 Limited Liability Company (Korlátolt Felelősségű Társaság Kft.) 3 Company Limited

2018 Company Formation

2018 Company Formation Czech Republic www.accace.com www.accace.cz Contents Legal forms of business, minimum capital, contribution 3 General Partnership (Veřejná obchodní společnost v.o.s.) 3 Limited Partnership

2018 Company Formation Czech Republic www.accace.com www.accace.cz Contents Legal forms of business, minimum capital, contribution 3 General Partnership (Veřejná obchodní společnost v.o.s.) 3 Limited Partnership

Doing Business in the Czech Republic

This document describes some of the key commercial and taxation factors that are relevant on setting up a business in the Czech Republic. Prepared by Peterka and Partners 2 Doing Business in the Czech

This document describes some of the key commercial and taxation factors that are relevant on setting up a business in the Czech Republic. Prepared by Peterka and Partners 2 Doing Business in the Czech

Summary of the most significant changes affecting employment taxation in 2018

Summary of the most significant changes affecting employment taxation in 2018 Czech Republic Hungary Poland Romania Slovakia INTRODUCTION We want to quickly guide you through the most significant changes

Summary of the most significant changes affecting employment taxation in 2018 Czech Republic Hungary Poland Romania Slovakia INTRODUCTION We want to quickly guide you through the most significant changes

Report on Republic of Hungary

Arctic Circle This report provides helpful information on the current business environment in Hungary. It is designed to assist companies in doing business and establishing effective banking arrangements.

Arctic Circle This report provides helpful information on the current business environment in Hungary. It is designed to assist companies in doing business and establishing effective banking arrangements.

Doing Business in Poland

This document describes some of the key commercial and taxation factors that are relevant on setting up a business in Poland. Prepared by Audyt i Doradztwo Pawlik, Modzelewski i Wspólnicy sp. z o.o. and

This document describes some of the key commercial and taxation factors that are relevant on setting up a business in Poland. Prepared by Audyt i Doradztwo Pawlik, Modzelewski i Wspólnicy sp. z o.o. and

TAX CARD 2016 ROMANIA

ROMANIA TAX CARD TAX CARD 2016 ROMANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses/Allowances 1.2 Social

ROMANIA TAX CARD TAX CARD 2016 ROMANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses/Allowances 1.2 Social

Report on the Czech Republic

Arctic Circle This report provides helpful information on the current business environment in the Czech Republic. It is designed to assist companies in doing business and establishing effective banking

Arctic Circle This report provides helpful information on the current business environment in the Czech Republic. It is designed to assist companies in doing business and establishing effective banking

2017 Company Formation

2017 Company Formation Slovakia www.accace.com www.accace.sk Contents Introduction 3 Legal forms of business, minimum capital, contribution 4 General Partnership 4 Limited Partnership 4 Limited Liability

2017 Company Formation Slovakia www.accace.com www.accace.sk Contents Introduction 3 Legal forms of business, minimum capital, contribution 4 General Partnership 4 Limited Partnership 4 Limited Liability

CIT rate development in CEE

CIT rate development in CEE Where do we find the lowest rate? www.accace.com accace@accace.com Corporate income tax (CIT) rate is one of the key elements explored by entrepreneurs when considering operating

CIT rate development in CEE Where do we find the lowest rate? www.accace.com accace@accace.com Corporate income tax (CIT) rate is one of the key elements explored by entrepreneurs when considering operating

Report on the Republic of Poland

Arctic Circle This report provides helpful information on the current business environment in Poland. It is designed to assist companies in doing business and establishing effective banking arrangements.

Arctic Circle This report provides helpful information on the current business environment in Poland. It is designed to assist companies in doing business and establishing effective banking arrangements.

Labour Law and Employment in the Czech Republic Guide

Labour Law and Employment in the Czech Republic - 2019 Guide czechrepublic@accace.com www.accace.com www.accace.cz Contents Entitlement to work in the Czech Republic 3 For residents 3 For non-residents

Labour Law and Employment in the Czech Republic - 2019 Guide czechrepublic@accace.com www.accace.com www.accace.cz Contents Entitlement to work in the Czech Republic 3 For residents 3 For non-residents

Global Banking Service

Arctic Circle This report provides helpful information on the current business environment in Romania. It is designed to assist companies in doing business and establishing effective banking arrangements.

Arctic Circle This report provides helpful information on the current business environment in Romania. It is designed to assist companies in doing business and establishing effective banking arrangements.

European Union: Accession States Tax Guide. LITHUANIA Lawin

A. General information European Union: Accession States Tax Guide LITHUANIA Lawin CONTACT INFORMATION Gintaras Balcius Lawin Jogailos 9/1 Vilnius, LT-01116 Lithuania 370.5.268.18.88 gintaras.balcius@lawin.lt

A. General information European Union: Accession States Tax Guide LITHUANIA Lawin CONTACT INFORMATION Gintaras Balcius Lawin Jogailos 9/1 Vilnius, LT-01116 Lithuania 370.5.268.18.88 gintaras.balcius@lawin.lt

Doing business in Sweden.

Doing business in Sweden www.pwc.se/doingbusinessinsweden 1. What type of presence do we need to undertake our operations? 2. What other registration requirements do we need to be aware of? 3. What are

Doing business in Sweden www.pwc.se/doingbusinessinsweden 1. What type of presence do we need to undertake our operations? 2. What other registration requirements do we need to be aware of? 3. What are

BULGARIAN TAX GUIDE 2017

GLOBAL CONSULT EUROPE LTD. Sofia 1504, Bulgaria 23A San Stefano str. Tel : +359 889 85 00 87 info@companyinbg.com www.companyinbg.com BULGARIAN TAX GUIDE 2017 I. CORPORATE INCOME TAX (CIT) Resident companies

GLOBAL CONSULT EUROPE LTD. Sofia 1504, Bulgaria 23A San Stefano str. Tel : +359 889 85 00 87 info@companyinbg.com www.companyinbg.com BULGARIAN TAX GUIDE 2017 I. CORPORATE INCOME TAX (CIT) Resident companies

SETTING UP BUSINESS IN POLAND

www.antea-int.com SETTING UP BUSINESS IN POLAND 1 General Aspects Poland is situated in the heart of Europe, bordering seven other countries. Its monetary unit is the Polish zloty (PLN). Expected date

www.antea-int.com SETTING UP BUSINESS IN POLAND 1 General Aspects Poland is situated in the heart of Europe, bordering seven other countries. Its monetary unit is the Polish zloty (PLN). Expected date

Tax Card KPMG in Macedonia. kpmg.com/mk

Tax Card 2016 KPMG in Macedonia kpmg.com/mk TAXATION OF CORPORATE PROFITS Corporate income tax (CIT) is due from profits realized by resident legal entities as well as by non-residents with a permanent

Tax Card 2016 KPMG in Macedonia kpmg.com/mk TAXATION OF CORPORATE PROFITS Corporate income tax (CIT) is due from profits realized by resident legal entities as well as by non-residents with a permanent

DOING BUSINESS IN POLAND. Why Poland?

DOING BUSINESS IN POLAND Why Poland? Poland is a country in Central East Europe. The total area of Poland is over 120,000 sq mi (9th largest in Europe) with a population of over 38 million people. Poland

DOING BUSINESS IN POLAND Why Poland? Poland is a country in Central East Europe. The total area of Poland is over 120,000 sq mi (9th largest in Europe) with a population of over 38 million people. Poland

International Tax Lithuania Highlights 2017

International Tax Lithuania Highlights 2017 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS and IFRS, or Business Accounting Standards

International Tax Lithuania Highlights 2017 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS and IFRS, or Business Accounting Standards

DOING BUSINESS IN ROMANIA

DOING BUSINESS IN ROMANIA CONTENTS 1 Introduction 3 2 Business environment 4 3 Foreign Investment 6 4 Setting up a Business 7 5 Labour 9 6 Taxation 11 7 Accounting & reporting 16 8 UHY Representation in

DOING BUSINESS IN ROMANIA CONTENTS 1 Introduction 3 2 Business environment 4 3 Foreign Investment 6 4 Setting up a Business 7 5 Labour 9 6 Taxation 11 7 Accounting & reporting 16 8 UHY Representation in

FOREWORD. Slovak Republic

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

BULGARIA TAX CARD 2017

BULGARIA TAX CARD 2017 TAX CARD 2017 BULGARIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Residency 1.1.2 Tax Rates 1.1.3 Taxable Income 1.1.4 Exempt Income 1.1.5 Deductible Expenses

BULGARIA TAX CARD 2017 TAX CARD 2017 BULGARIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Residency 1.1.2 Tax Rates 1.1.3 Taxable Income 1.1.4 Exempt Income 1.1.5 Deductible Expenses

TAXATION OF EXPATRIATES WORKING IN THE SLOVAK REPUBLIC OUR OFFICES:

TAXATION OF EXPATRIATES WORKING IN THE SLOVAK REPUBLIC OUR OFFICES: guide2007.p65 1 Leitner + Leitner No reliance should be placed on nor should decisions be taken on the basis of the contents of this

TAXATION OF EXPATRIATES WORKING IN THE SLOVAK REPUBLIC OUR OFFICES: guide2007.p65 1 Leitner + Leitner No reliance should be placed on nor should decisions be taken on the basis of the contents of this

Everything will stay...new!

Everything will stay...new! On 5 th September 2016 TPA Horwath became 11 Countries. 11 Tax Systems. The year 2014 also brings extensive changes in the areas of taxes, duties and social contributions in

Everything will stay...new! On 5 th September 2016 TPA Horwath became 11 Countries. 11 Tax Systems. The year 2014 also brings extensive changes in the areas of taxes, duties and social contributions in

Corporate income tax. Dear Client, > I. Extended scope of corporate income tax reliefs. > II. Abolished corporate income tax reliefs

Successful together Lithuanian Tax Law Amendments in 2018 Information for investors and entrepreneurs in Lithuania www.roedl.de/litauen www.roedl.com/lithuania Dear Client, As of 1 st January 2018, Lithuania

Successful together Lithuanian Tax Law Amendments in 2018 Information for investors and entrepreneurs in Lithuania www.roedl.de/litauen www.roedl.com/lithuania Dear Client, As of 1 st January 2018, Lithuania

2017 Transfer Pricing Overview Poland

2017 Transfer Pricing Overview Poland poland@accace.com www.accace.com www.accace.pl Contents Applicable Legislation 3 Transactions Subject to Transfer Pricing Documentation 4 Scope of Transfer Pricing

2017 Transfer Pricing Overview Poland poland@accace.com www.accace.com www.accace.pl Contents Applicable Legislation 3 Transactions Subject to Transfer Pricing Documentation 4 Scope of Transfer Pricing

LIST OF ABBREVIATIONS...III LIST OF LEGAL REFERENCES... IV PART I. IMPLEMENTATION OF THE DIRECTIVE... V 1. INTRODUCTION... V

SLOVAK REPUBLIC 428 Page ii OUTLINE LIST OF ABBREVIATIONS...III LIST OF LEGAL REFERENCES... IV PART I. IMPLEMENTATION OF THE DIRECTIVE... V 1. INTRODUCTION... V 1.1. GENERAL INFORMATION ON THE IMPLEMENTATION

SLOVAK REPUBLIC 428 Page ii OUTLINE LIST OF ABBREVIATIONS...III LIST OF LEGAL REFERENCES... IV PART I. IMPLEMENTATION OF THE DIRECTIVE... V 1. INTRODUCTION... V 1.1. GENERAL INFORMATION ON THE IMPLEMENTATION

Romania Country Profile

Romania Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile

Romania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

INTRODUCTION. In the case of any question regarding this new tax, we would be pleased to provide you with our assistance. 2 Tax on non-life insurance

New tax on non-life insurance premium introduced in Slovakia from 1 January 2019 INTRODUCTION As of 1 January 2019, the new law on Insurance Premium Tax, which may concern also your company, will become

New tax on non-life insurance premium introduced in Slovakia from 1 January 2019 INTRODUCTION As of 1 January 2019, the new law on Insurance Premium Tax, which may concern also your company, will become

2018 Transfer Pricing Overview Poland

2018 Transfer Pricing Overview Poland poland@accace.com www.accace.com www.accace.pl Contents Introduction 3 Applicable Legislation 4 Transactions Subject to Transfer Pricing Documentation 5 Scope of Transfer

2018 Transfer Pricing Overview Poland poland@accace.com www.accace.com www.accace.pl Contents Introduction 3 Applicable Legislation 4 Transactions Subject to Transfer Pricing Documentation 5 Scope of Transfer

E-commerce in the Czech Republic. Main Legal and Tax Aspects. 1 E-commerce in the Czech Republic Main Legal and Tax Aspects

E-commerce in the Czech Republic Main Legal and Tax Aspects 1 E-commerce in the Czech Republic Main Legal and Tax Aspects November, 2016 BACKGROUND Over the last years, the e-shop business has been booming

E-commerce in the Czech Republic Main Legal and Tax Aspects 1 E-commerce in the Czech Republic Main Legal and Tax Aspects November, 2016 BACKGROUND Over the last years, the e-shop business has been booming

The most important legislative changes in Slovakia as of 2018 ebook

The most important legislative changes in Slovakia as of 2018 ebook INTRODUCTION Are you wondering about the most significant changes in the Slovak legislation with the arrival of 2018? Our experts have

The most important legislative changes in Slovakia as of 2018 ebook INTRODUCTION Are you wondering about the most significant changes in the Slovak legislation with the arrival of 2018? Our experts have

COUNCIL OF THE EUROPEAN UNION. Brussels, 27 June 2014 (OR. en) 10996/14 Interinstitutional File: 2013/0400 (CNS) FISC 99 ECOFIN 679

10996/14 Interinstitutional File: 2013/0400 (CNS) FISC 99 ECOFIN 679") COUNCIL OF THE EUROPEAN UNION Brussels, 27 June 2014 (OR. en) 10996/14 Interinstitutional File: 2013/0400 (CNS) FISC 99 ECOFIN 679 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: COUNCIL DIRECTIVE amending

COUNCIL OF THE EUROPEAN UNION Brussels, 27 June 2014 (OR. en) 10996/14 Interinstitutional File: 2013/0400 (CNS) FISC 99 ECOFIN 679 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: COUNCIL DIRECTIVE amending

Doing Business in Poland

Doing Business in Poland Peter Nielsen & Partners Law Office Atrium Centrum, Lobby B, 2nd floor Al. Jana Pawła II 27, 00-867 Warszawa POLAND / POLSKA Tel: (+48) 22 59 29 000 Fax: (+48) 22 59 29 030 E-mail:

Doing Business in Poland Peter Nielsen & Partners Law Office Atrium Centrum, Lobby B, 2nd floor Al. Jana Pawła II 27, 00-867 Warszawa POLAND / POLSKA Tel: (+48) 22 59 29 000 Fax: (+48) 22 59 29 030 E-mail:

FOREWORD. Slovak Republic

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

ALBANIA TAX CARD 2017

ALBANIA TAX CARD 2017 TAX CARD 2017 ALBANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses 1.2 Social Security

ALBANIA TAX CARD 2017 TAX CARD 2017 ALBANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses 1.2 Social Security

DOING BUSINESS IN SLOVAKIA

DOING BUSINESS IN SLOVAKIA CONTENTS 1 Introduction 3 2 Business environment 4 3 Foreign Investment 9 4 Setting up a Business 11 5 Labour 19 6 Taxation 25 7 Accounting & reporting 37 8 UHY Representation

DOING BUSINESS IN SLOVAKIA CONTENTS 1 Introduction 3 2 Business environment 4 3 Foreign Investment 9 4 Setting up a Business 11 5 Labour 19 6 Taxation 25 7 Accounting & reporting 37 8 UHY Representation

Romania. Structure and development of tax revenues. Romania. Table RO.1: Revenue (% of GDP)

") Structure and development of tax revenues Table RO.1: Revenue (% of GDP) 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 I. Indirect taxes 11.7 12.8 12.7 12.5 11.8 10.8 11.9 13.0 13.2 12.8 VAT 6.6 8.0

Structure and development of tax revenues Table RO.1: Revenue (% of GDP) 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 I. Indirect taxes 11.7 12.8 12.7 12.5 11.8 10.8 11.9 13.0 13.2 12.8 VAT 6.6 8.0

ANNEX VIII RIGHT OF ESTABLISHMENT

1.6.2018 - EEA AGREEMENT - ANNEX VIII p. 1 ANNEX VIII RIGHT OF ESTABLISHMENT List provided for in Article 31 INTRODUCTION When the acts referred to in this Annex contain notions or refer to procedures

1.6.2018 - EEA AGREEMENT - ANNEX VIII p. 1 ANNEX VIII RIGHT OF ESTABLISHMENT List provided for in Article 31 INTRODUCTION When the acts referred to in this Annex contain notions or refer to procedures

ecommerce in Romania Main Legal and Tax Aspects

www.accace.ro romania.office@accace.com ecommerce in Romania Main Legal and Tax Aspects BACKGROUND Over the last years, the eshop business has been booming in Romania. According to reports and estimates

www.accace.ro romania.office@accace.com ecommerce in Romania Main Legal and Tax Aspects BACKGROUND Over the last years, the eshop business has been booming in Romania. According to reports and estimates

TAX PROFILE, ESTONIA. (published in BNAI's Global Tax Guide) KEY FACTS INTRODUCTION RECENT DEVELOPMENTS. Kaido Loor and Elvira Tulvik

KEY FACTS INTRODUCTION RECENT DEVELOPMENTS. Kaido Loor and Elvira Tulvik") TAX PROFILE, ESTONIA (published in BNAI's Global Tax Guide) Kaido Loor and Elvira Tulvik Estonia Pärnu mnt 15, 10141 Tallinn phone +372 6 400 900, estonia@sorainen.com Latvia Kr. Valdemāra iela 21, LV-1010

TAX PROFILE, ESTONIA (published in BNAI's Global Tax Guide) Kaido Loor and Elvira Tulvik Estonia Pärnu mnt 15, 10141 Tallinn phone +372 6 400 900, estonia@sorainen.com Latvia Kr. Valdemāra iela 21, LV-1010

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia KPMG Baltics OÜ kpmg.com/ee CORPORATE INCOME TAX In Estonia, corporate income tax is not levied when profit is earned but when it is

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia KPMG Baltics OÜ kpmg.com/ee CORPORATE INCOME TAX In Estonia, corporate income tax is not levied when profit is earned but when it is

Corporate entities, including subsidiaries of foreign companies incorporated under Macedonian law, are considered Macedonian tax residents.

Taxation Profit Tax Corporate entities, including subsidiaries of foreign companies incorporated under Macedonian law, are considered Macedonian tax residents. Upon registration in Macedonia, these legal

Taxation Profit Tax Corporate entities, including subsidiaries of foreign companies incorporated under Macedonian law, are considered Macedonian tax residents. Upon registration in Macedonia, these legal

Tax Card KPMG in Bulgaria. kpmg.com/bg

Tax Card 2017 KPMG in Bulgaria kpmg.com/bg CORPORATE TAX Corporate income tax (CIT) is due on the accounting profit after adjustments for tax purposes. The applicable tax rate for the year 2017 is 10%.

Tax Card 2017 KPMG in Bulgaria kpmg.com/bg CORPORATE TAX Corporate income tax (CIT) is due on the accounting profit after adjustments for tax purposes. The applicable tax rate for the year 2017 is 10%.

Law regarding the Fiscal Code. Law no. 227/2015 published in the Official Gazette no. 688 of 10 September 2015

21 September 2015 Law regarding the Fiscal Code Law no. 227/2015 published in the Official Gazette no. 688 of 10 September 2015 Starting with 1 January 2016, Law no. 227/2015 regarding the Fiscal Code

21 September 2015 Law regarding the Fiscal Code Law no. 227/2015 published in the Official Gazette no. 688 of 10 September 2015 Starting with 1 January 2016, Law no. 227/2015 regarding the Fiscal Code

International Tax Slovenia Highlights 2018

International Tax Slovenia Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Bank accounts may be held and repatriation payments made in any currency. Accounting principles/financial

International Tax Slovenia Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Bank accounts may be held and repatriation payments made in any currency. Accounting principles/financial

FYR MACEDONIA TAX CARD

FYR MACEDONIA TAX CARD 2017 TAX CARD 2017 FYR MACEDONIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Exemptions 1.1.2 Deductible Expenses 1.2 Capital Gains Tax 1.3 Social Security

FYR MACEDONIA TAX CARD 2017 TAX CARD 2017 FYR MACEDONIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Exemptions 1.1.2 Deductible Expenses 1.2 Capital Gains Tax 1.3 Social Security

Tax Card With effect from 1 January 2016 Lithuania. KPMG Baltics, UAB. kpmg.com/lt

Tax Card 2016 With effect from 1 January 2016 Lithuania KPMG Baltics, UAB kpmg.com/lt CORPORATE INCOME TAX Taxable profit of Lithuanian and foreign corporate taxpayers is subject to a standard (flat) rate

Tax Card 2016 With effect from 1 January 2016 Lithuania KPMG Baltics, UAB kpmg.com/lt CORPORATE INCOME TAX Taxable profit of Lithuanian and foreign corporate taxpayers is subject to a standard (flat) rate

Doing Business in Bulgaria

Doing Business in Bulgaria www.bakertillyinternational.com This guide has been prepared by Baker Tilly, an independent member of Baker Tilly International. It is designed to provide information on a number

Doing Business in Bulgaria www.bakertillyinternational.com This guide has been prepared by Baker Tilly, an independent member of Baker Tilly International. It is designed to provide information on a number

International Tax Slovakia Highlights 2019

International Tax Updated January 2019 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital, and repatriation payments may be made

International Tax Updated January 2019 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital, and repatriation payments may be made

SETTING UP A COMPANY IN POLAND BY NON-EU INVESTORS. How we can help you in achieving success in international investments

SETTING UP A COMPANY IN POLAND BY NON-EU INVESTORS How we can help you in achieving success in international investments The only EU Member State which avoided the financial crisis was Poland. Foreign

SETTING UP A COMPANY IN POLAND BY NON-EU INVESTORS How we can help you in achieving success in international investments The only EU Member State which avoided the financial crisis was Poland. Foreign

Invest in Austria. Legal Aspects of Establishing a Company in Austria. Bucharest I 21 October Markus Piuk / Clemens Leitner

Invest in Austria Legal Aspects of Establishing a Company in Austria Bucharest I 21 October 2014 Markus Piuk / Clemens Leitner Corporate Set Up for doing business in Austria Major legal forms are partnerships

Invest in Austria Legal Aspects of Establishing a Company in Austria Bucharest I 21 October 2014 Markus Piuk / Clemens Leitner Corporate Set Up for doing business in Austria Major legal forms are partnerships

BRIEF STATISTICS 2009

BRIEF STATISTICS 2009 Finnish Tax Administration The Tax Administration is organized under the jurisdiction of the Ministry of Finance. The Tax Administration collects about two-thirds of the taxes and

BRIEF STATISTICS 2009 Finnish Tax Administration The Tax Administration is organized under the jurisdiction of the Ministry of Finance. The Tax Administration collects about two-thirds of the taxes and

VAT in the European Community APPLICATION IN THE MEMBER STATES, INFORMATION FOR USE BY: ADMINISTRATIONS/TRADERS INFORMATION NETWORKS, ETC.

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes Brussels, October 2010 TAXUD/C/1 VAT in the European Community APPLICATION

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes Brussels, October 2010 TAXUD/C/1 VAT in the European Community APPLICATION

PAYROLL CONTRIBUTIONS in force on 1 st January Contribution Employer (rate %) Social security contribution

Social security contribution") page Tax Newsletter No. 12 / 2005 Str. Brezoianu, Nr. 36, Sector 1, Bucuresti Tel: +40 (0)21 313 70 31 Tel: +40 (0)745 20 27 39 Fax:+40 (0)21 313 70 68 Contents: PAYROLL Contributions 2006 NEW software

page Tax Newsletter No. 12 / 2005 Str. Brezoianu, Nr. 36, Sector 1, Bucuresti Tel: +40 (0)21 313 70 31 Tel: +40 (0)745 20 27 39 Fax:+40 (0)21 313 70 68 Contents: PAYROLL Contributions 2006 NEW software

News Flash. October, 2016

News Flash October, 2016 Permanent establishment obligation of foreigners in Hungary in 2016 Do you own a permanent establishment in Hungary? Find out what are your tax obligations! Thanks to the value

News Flash October, 2016 Permanent establishment obligation of foreigners in Hungary in 2016 Do you own a permanent establishment in Hungary? Find out what are your tax obligations! Thanks to the value

Tax Calendar Czech Republic

Tax Calendar Czech Republic 2018 #accacelife www.accace.com www.accace.cz Monthly tasks for you Not necessarily tax related January 2018 January 08 22 25 - Payment of advances on health insurance contributions

Tax Calendar Czech Republic 2018 #accacelife www.accace.com www.accace.cz Monthly tasks for you Not necessarily tax related January 2018 January 08 22 25 - Payment of advances on health insurance contributions

Taxation of cross-border mergers and acquisitions

Taxation of cross-border mergers and acquisitions Slovakia kpmg.com/tax KPMG International Taxation of cross-border mergers and acquisitions a Slovakia Introduction This overview of the Slovak business

Taxation of cross-border mergers and acquisitions Slovakia kpmg.com/tax KPMG International Taxation of cross-border mergers and acquisitions a Slovakia Introduction This overview of the Slovak business

Doing Business in Poland

Doing Business in Poland Content Introduction 5 About Vistra Introduction to Poland 7 Why Do Business in Poland? 8 The Difficulties of Doing Business in Poland Business Environment in Poland 10 Legal

Doing Business in Poland Content Introduction 5 About Vistra Introduction to Poland 7 Why Do Business in Poland? 8 The Difficulties of Doing Business in Poland Business Environment in Poland 10 Legal

Tax System of the Czech Republic

Tax System of the Czech Republic Division of taxes direct indirect Income tax (including inheritance and gift) Road tax Real estate tax Real estate transfer tax Value added tax Excise duties Environmental

Tax System of the Czech Republic Division of taxes direct indirect Income tax (including inheritance and gift) Road tax Real estate tax Real estate transfer tax Value added tax Excise duties Environmental

International Tax Romania Highlights 2018

International Tax Romania Highlights 2018 Investment basics: Currency Romanian New Leu (RON) Foreign exchange control The national currency is fully convertible and residents are allowed to make external

International Tax Romania Highlights 2018 Investment basics: Currency Romanian New Leu (RON) Foreign exchange control The national currency is fully convertible and residents are allowed to make external

FIRST-CLASS PERFORMANCE FOR FULL SERVICE FINANCE & ACCOUNTING SOLUTIONS

3 FIRST-CLASS PERFORMANCE FOR FULL SERVICE FINANCE & ACCOUNTING SOLUTIONS Many companies are confronted with the need to reduce accounting costs and to comply with the required financial reporting standards.

3 FIRST-CLASS PERFORMANCE FOR FULL SERVICE FINANCE & ACCOUNTING SOLUTIONS Many companies are confronted with the need to reduce accounting costs and to comply with the required financial reporting standards.

MANDAT news. Fresh tax, legal and economic information APRIL 2013

Fresh tax, legal and economic information MANDAT news The April issue includes: Income Tax Prepayments Payments to Health Insurance Companies Not to be missed Important Dates MANDAT CONSULTING, k.s., Nám.

Fresh tax, legal and economic information MANDAT news The April issue includes: Income Tax Prepayments Payments to Health Insurance Companies Not to be missed Important Dates MANDAT CONSULTING, k.s., Nám.

Reference Interest Rate published by the National Bank of Romania

May 2015 Reference Interest Rate published by the National Bank of Romania Circular letter of the National Bank of Romania no. 17/2015, published in the Official Gazette no. 316 of 8 May 2015 As of 7 May

May 2015 Reference Interest Rate published by the National Bank of Romania Circular letter of the National Bank of Romania no. 17/2015, published in the Official Gazette no. 316 of 8 May 2015 As of 7 May

Hungary. Structure and development of tax revenues. Hungary. Table HU.1: Revenue (% of GDP)

") Structure and development of tax revenues Table HU.1: Revenue (% of GDP) 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 I. Indirect taxes 16.2 15.6 15.1 16.0 15.8 16.6 17.7 17.5 18.8 18.7 VAT 8.8 8.3

Structure and development of tax revenues Table HU.1: Revenue (% of GDP) 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 I. Indirect taxes 16.2 15.6 15.1 16.0 15.8 16.6 17.7 17.5 18.8 18.7 VAT 8.8 8.3

EXPATRIATE TAX GUIDE. Taxation of income from employment in the EU & EEA

EXPATRIATE TAX GUIDE Taxation of income from employment in the EU & EEA Poland 2016 CONTENTS* 2 Austria 4 Belgium 6 Bulgaria 8 Croatia 10 Cyprus 12 Czech Republic 14 Denmark 16 Estonia 18 Finland 20 France

EXPATRIATE TAX GUIDE Taxation of income from employment in the EU & EEA Poland 2016 CONTENTS* 2 Austria 4 Belgium 6 Bulgaria 8 Croatia 10 Cyprus 12 Czech Republic 14 Denmark 16 Estonia 18 Finland 20 France

FOREWORD. Montenegro. Services provided by member firms include:

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Employee Share Plans Taxation in Croatia

Employee Share Plans Taxation in Croatia Zagreb, December 2017 1 Table of Contents Introduction... 3 Analysis of the current situation in Croatia based on a sample case. 4 Current Croatian tax and social

Employee Share Plans Taxation in Croatia Zagreb, December 2017 1 Table of Contents Introduction... 3 Analysis of the current situation in Croatia based on a sample case. 4 Current Croatian tax and social

Montenegro a place to invest in

Montenegro a place to invest in Easy business start up Hub for regional business Strategic geographical position National treatment of foreigners Dynamic economyc growth and development Favourable tax

Montenegro a place to invest in Easy business start up Hub for regional business Strategic geographical position National treatment of foreigners Dynamic economyc growth and development Favourable tax

Doing Business in Moldova

Doing Business in Moldova www.bakertillyinternational.com Preface This guide has been prepared by Baker Tilly, an independent member of Baker Tilly International. It is designed to provide information

Doing Business in Moldova www.bakertillyinternational.com Preface This guide has been prepared by Baker Tilly, an independent member of Baker Tilly International. It is designed to provide information

INVEST IN HUNGARY DOING BUSINESS IN HUNGARY GUIDE 2017 This brochure has been compiled with the utmost care. In consideration of the general nature of the brochure and the frequent amendments to Hungarian

INVEST IN HUNGARY DOING BUSINESS IN HUNGARY GUIDE 2017 This brochure has been compiled with the utmost care. In consideration of the general nature of the brochure and the frequent amendments to Hungarian

HUNGARY: 10% TAX RATE

HUNGARY: 10% TAX RATE The main intention of the present booklet is to provide a brief guide to foreign individuals, entrepreneurs or corporations considering to establish a company in Hungary. 1- HUNGARY

HUNGARY: 10% TAX RATE The main intention of the present booklet is to provide a brief guide to foreign individuals, entrepreneurs or corporations considering to establish a company in Hungary. 1- HUNGARY

Serbian Tax Card 2018

Serbian Tax Card 2018 KPMG d.o.o. Beograd kpmg.com/rs CORPORATE INCOME TAX A resident is a legal entity which is incorporated or has a place of effective management and control on the territory of Serbia.

Serbian Tax Card 2018 KPMG d.o.o. Beograd kpmg.com/rs CORPORATE INCOME TAX A resident is a legal entity which is incorporated or has a place of effective management and control on the territory of Serbia.

Tax System of the Czech Republic

Tax System of the Czech Republic Division of taxes direct indirect Income tax Road tax Real estate tax Inheritance and gift tax, real estate transfer tax Value added tax Excise duties Environmental protection

Tax System of the Czech Republic Division of taxes direct indirect Income tax Road tax Real estate tax Inheritance and gift tax, real estate transfer tax Value added tax Excise duties Environmental protection

DOING BUSINESS IN SLOVAKIA

DOING BUSINESS IN SLOVAKIA CONTENTS 1 Introduction 3 2 Business environment 4 3 Foreign Investment 8 4 Setting up a Business 11 5 Labour 14 6 Taxation 18 7 Accounting & reporting 26 8 UHY Representation

DOING BUSINESS IN SLOVAKIA CONTENTS 1 Introduction 3 2 Business environment 4 3 Foreign Investment 8 4 Setting up a Business 11 5 Labour 14 6 Taxation 18 7 Accounting & reporting 26 8 UHY Representation

Private Equity Business outlook in the time of change in the CEE Region

Private Equity Business outlook in the time of change in the CEE Region Prepared for Private Equity Forum & Awards Gala 2 Macroeconomic overview Poland and the CEE Region 3 Region of Central and Eastern

Private Equity Business outlook in the time of change in the CEE Region Prepared for Private Equity Forum & Awards Gala 2 Macroeconomic overview Poland and the CEE Region 3 Region of Central and Eastern

Fundamentals Level Skills Module, Paper F6 (CZE)

") Answers Fundamentals Level Skills Module, Paper F6 (CZE) Taxation (Czech) Section B December 207 Answers and Marking Scheme (a) Leboslavia, a.s. (Leboslavia) (i) (b) Jana The shortest time period the tax

Answers Fundamentals Level Skills Module, Paper F6 (CZE) Taxation (Czech) Section B December 207 Answers and Marking Scheme (a) Leboslavia, a.s. (Leboslavia) (i) (b) Jana The shortest time period the tax

International Tax Greece Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Greece, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control Restrictions

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Greece, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control Restrictions

Investing in Romania. An overview of the current tax system 2017

Investing in Romania An overview of the current tax system 2017 Albania Austria Bulgaria Croatia Czech Republic Hungary Poland Romania Serbia Slovakia Slovenia Investing in Romania. An overview of the

Investing in Romania An overview of the current tax system 2017 Albania Austria Bulgaria Croatia Czech Republic Hungary Poland Romania Serbia Slovakia Slovenia Investing in Romania. An overview of the

Romania's New Fiscal Code

FEATURED ARTICLES ISSUE 152 OCTOBER 8, 2015 Romania's New Fiscal Code by Angela Rosca, Taxand Contact: angela.rosca@taxhouse.ro, Tel. +40 21 316 06 45 Law No. 227/2015 was published in the Offi cial Gazette

FEATURED ARTICLES ISSUE 152 OCTOBER 8, 2015 Romania's New Fiscal Code by Angela Rosca, Taxand Contact: angela.rosca@taxhouse.ro, Tel. +40 21 316 06 45 Law No. 227/2015 was published in the Offi cial Gazette

3 We Solve. 2 We Solve

COMPANY & TRUST Formation and operation in Hungary 2018 COMPANY & TRUST Formation and operation in Hungary 2018 5 Forms of companies 12 Structuring & requirements 20 Registration process of companies 22

COMPANY & TRUST Formation and operation in Hungary 2018 COMPANY & TRUST Formation and operation in Hungary 2018 5 Forms of companies 12 Structuring & requirements 20 Registration process of companies 22

International Tax Greece Highlights 2018

International Tax Greece Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Capital controls are in force and certain limitations still apply on bank withdrawals and bank transfers