Montenegro a place to invest in

|

|

|

- Lorin Marsh

- 6 years ago

- Views:

Transcription

1

")

2 Montenegro a place to invest in Easy business start up Hub for regional business Strategic geographical position National treatment of foreigners Dynamic economyc growth and development Favourable tax climate (CT 9%, VAT 19%) The positive experience from existing investors Political stability and multi-ethnic harmony Qualified human resources

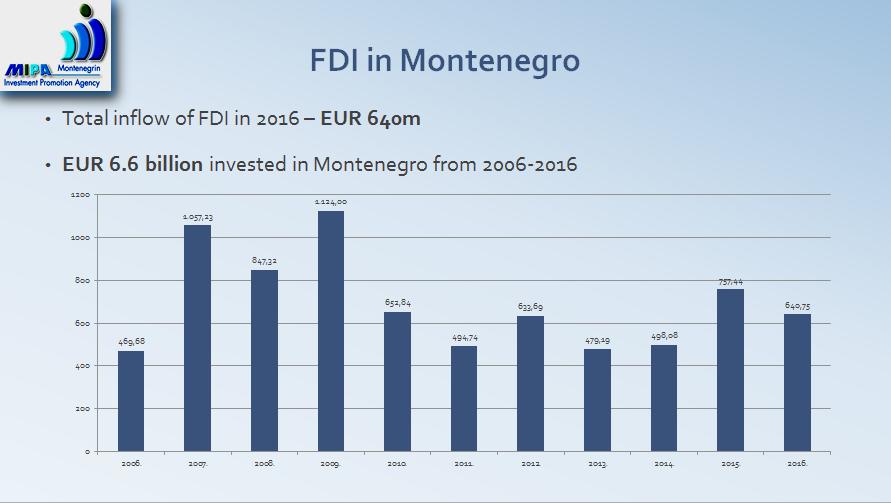

3 Montenegrin economy Montenegro is constantly devoted to the improvement of the business environment. This has been recognised by the World Bank Doing Business Report 2017 and Montenegro has been ranked as the 51 st out of 190 economies in the world, especially improving in the field of dealing with construction permits. Montenegro has been improving on the Doing Business rankings since 2009 when it was ranked the 90 th. INDICATOR GDP at current prices ( million) 3,335 3,458 3,618 2,282 (IIIQ) Real GDP growth (%) (IIIQ) Inflation (%) Unemployment rate (%) Public debt (% of GDP) Net foreign direct investment, current prices ( million) Net foreign direct investment (% of GDP) , ,6 12,2

4 Montenegro memberships: CEFTA

5 Montenegro EU and NATO integration Accession negotiations with the EU opened in 2012, and now, with more than two thirds of the accession chapters opened, the Montenegro enjoys a widespread support among EU members' officials In its 2016 assessment of the accession progress, the European Commission has identified Montenegro as having the highest level of preparation for membership among the negotiating states A formal invitation was issued by the alliance on 2 December 2015, beginning the final accession talks, and 23 countries ratified the Protocol of Accession so far. Government of Montenegro is strongly committed to Montenegro s integration to the EU and NATO

6 Free trade agreements Montenegro joined the Central European Free Trade Agreement CEFTA. Montenegro also signed the FTAs with EFTA (the common market that includes Switzerland, Norway, Iceland and Liechtenstein), Russia, Turkey and Ukraine. Agreements on mutual promotion and protection of investments Since re-gaining its independence, Montenegro has signed 26 agreements on the mutual promotion and protection of investments. Agreements are in place with: Austria, the Slovak Republic, the Republic of Serbia, the Czech Republic, the Republic of Finland, the Kingdom of Denmark, the State of Qatar, the Belgium-Luxemburg Economic Union, the Republic of Macedonia, Malta, France, the Hellenic Republic, the Netherlands, Israel, Cyprus, Romania, Ukraine, Hungary, Germany, Poland, Spain, the Republic of Turkey, the Swiss Confederation, the Republic of Azerbaijan, Moldova, and the United Arab Emirates. Double taxation agreements Montenegro has so far signed 42 double taxation treaties on income and property with: the Republic of Albania, Belarus, Bulgaria, Cyprus, Egypt, Germany, the Republic of Italy, Latvia, Malta, the Kingdom of Norway, the Russian Federation, the Republic of Slovenia, Switzerland, Ukraine, Austria, Belgium, the People s Republic of China, Czech Republic, the Republic of Finland, Hungary, South Korea, the Republic of Macedonia, Moldavia, Poland, the Republic of Serbia, Sri Lanka, the Republic of Turkey, the United Kingdom, the Republic of Azerbaijan, Bosnia and Herzegovina, the Republic of Croatia, the Kingdom of Denmark, France, Ireland, Kuwait, Malaysia, the Netherlands, Romania, the Slovak Republic, Sweden, the United Arab Emirates.

7

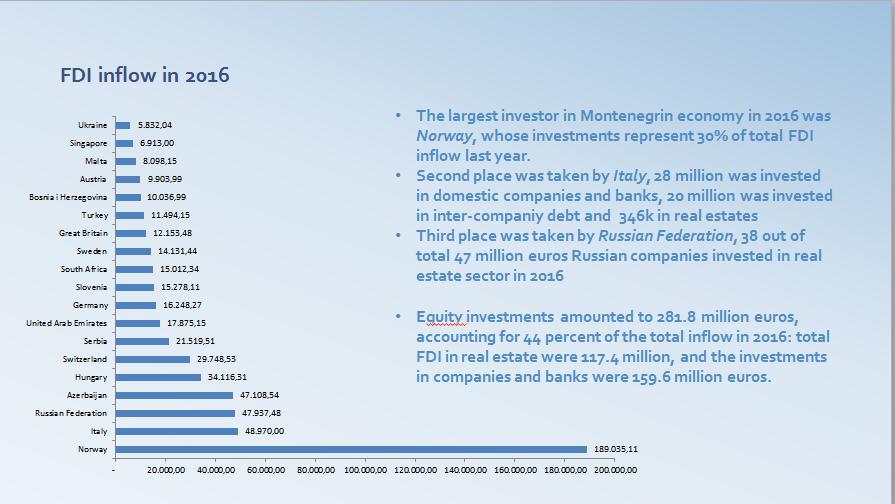

8 FDI inflows by countries ( ) Foreign investors in Montenegro are coming from 107 countries. 16% 9% 8% 5% 5% 6% 6% 7%

9

10 Foreign investors in Montenegro

11 . Opportunities in Montenegro AGRICULTURE - Big potentials in organic production, forestry, fishery, water production etc TOURISM - Projects in process or in initial phase up to 3 billion euro: Porto Montenegro, Porto Novi, Lustica Bay, Aman Sveti Stefan, Qatari Diar, Hilton,Sheraton... RENEWABLE ENERGY. - Enormous potentials in hydropower, wind, biomass and solar energy.

Corporate Income Tax 9% Value Added Tax 19% (reduced to 7% for tourism and 0% for some basic products)")

12 Things that foreign investor should know when starting a business According to Montenegrin law, it is possible to establish six types of companies: Entrepreneur, Limited Liability Company, Joint Stock Company, General partnership, Limited partnership and Part of a foreign company. New business entities can register a company, apply for general tax registration and obtain a VAT, excise and customs code all in one place. This means that it is not necessary to go to several different institutions, since everything can be done with the Central Register of the Commercial Court, which saves time and money. Personal Income Tax 9% (11% for gross personal income above 720) Corporate Income Tax 9% Value Added Tax 19% (reduced to 7% for tourism and 0% for some basic products) Property tax - between 0.08% and 0.80% of the real estate property s market value Withholding Tax 9% on dividends/profit distribution, capital gain, royalties, intellectual property rights, rental income, consulting, marketing.

for the taxable period is lower than the input VAT, deductible for the same period, the difference is either recorded as tax credit for the coming period")

13 Investment incentives and reliefs 1. VAT refund If the tax liability (output tax) for the taxable period is lower than the input VAT, deductible for the same period, the difference is either recorded as tax credit for the coming period or refunded, following the taxpayer s request, within 60 days from the date of submission of the VAT return. To taxpayers who are predominantly involved in export and those who have shown excess input VAT in three consecutive VAT assessments this difference is refunded within 30 days from the date of submission of VAT return. 2. VAT O% - for the delivering products and services for the construction and equipment of four or five stars hotels. 2. The subsidies for employment of certain categories of unemployed persons For the certain categories of the unemployed, the employer does not pay: Contribution for mandatory social insurance on wages and tax on personal income for the period of 12 years Cluster Development Programme in Montenegro. The Programme aims to provide financial support to the entrepreneurs and 100% privately owned MSMEs within clusters through investment in tangible or intangible assets or operational costs The Ministry of Economy will cover up to 65% of the eligible costs of the purchase value of equipment, excluding VAT, for the clusters operating in the less developed municipalities, or up to 50% of the eligible costs for the clusters from other regions; The strategic priority activities eligible for co-financing include the following: - Agricultural production and processing, - Wood processing, - Other manufacturing activities (except those not included in the Programme).

14 Investment incentives and reliefs 1. Programme for Enhancing Regional and Local Competitiveness through Harmonization with International Standards of Business for the period The Programme aims to support entrepreneurs and SMEs, in particular the ones from the less developed municipalities and the northern region, to enhance their competitiveness through harmonization with the international standards related to products, management systems, staff, testing, control and certification and support for conformity assessment accreditation. The program contains two components of support: 1. Support for SMEs in terms of reimbursement of the costs of accreditation of conformity assessment bodies; 2. Support SMEs in terms of reimbursement of the costs of the implementation of standards. Assistance granted by the Ministry of Economy is up to 70% of eligible costs for small companies, or up to 60% of eligible costs for medium-sized companies, in the amount up to EUR 5,000 (excluding VAT) per applicant. 2. Programme to support industry modernization The Programme aims to strengthen competitiveness of companies and upgrade business operation, productivity and profitability by investing in equipment. The Programme includes co-financing of the eligible costs of purchase of equipment up to 20% for small and 10% for medium-sized enterprises, excl. VAT, in line with state aid rules. The remaining funds are provided through the IDF lending scheme. The funds allocated to the Programme are intended to co-finance the costs of purchase of new/used production equipment/machines or new parts and specialized tools, to enable activation of unused machines.

15 Montenegrin state support for business Decree on fostering direct investments Decree defines that financial incentives may be awarded to a foreign and domestic companies, which have the intention to invest at least 500,000 (or 250,000 for the investment project carried out in the territory of local self-government units in the northern and central regions, excluding the Capital City of Podgorica) and will provide jobs for at least 20 new employees (or 10 for the investment project carried out in the territory of local self-government units in the northern and central regions, excluding the Capital City of Podgorica) within a period of three years from the day of concluding the Direct Investment Incentives Agreement. The investment incentives may be used for financing projects in the areas of manufacturing, services, hospitality and hotel industry The amount of investment incentives that can be awarded, based on the award criteria, are in range from to per new employee. Decree also provides reimbursement for infrastructure incurred for purposes of the investment project implementation. The incentive programme is administered by the Secretariat for Development Projects.

16 Montenegrin state support for business Decree on Business Zones Decree categorizes two types of business zones designated and managed by the Government of Montenegro or by the local governments. Investors will be granted national- and local-level incentives. At the national level, the employers who hire staff to work in a Business Zone are exempt from the contribution for compulsory insurance paid to salaries and from personal income tax. Exemptions are applicable for a period of 5 years from the date od employment of employees in the business zone. Local-level reliefs include: Lower utility and other fees; favourable lease/purchase of premises within the business zone; lower or zero surtax to PIT; lower real estate tax rate; opportunity to define a favourable public-private partnership model; access to utilities, where required. Nine local governments have identified Business Zones of Local Importance to date, enabling the investors to invest under favourable terms in Berane, Bijelo Polje, Kolašin, Mojkovac, Cetinje, Nikšić, Podgorica, Ulcinj and Rožaje.

17 MIPA Publications

203-140; 202-910 E-mail: info@mipa.co.me Web site: www.")

18 Thank you for your attention Montenegrin Investment Promotion Agency Jovana Tomasevica 2A Podgorica 81000, MNE Phone: ( ) ; Web site:

Slovenia Country Profile

Slovenia Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Slovenia EU Member State Double Tax Treaties With: Albania Armenia Austria

Slovenia Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Slovenia EU Member State Double Tax Treaties With: Albania Armenia Austria

Spain France. England Netherlands. Wales Ukraine. Republic of Ireland Czech Republic. Romania Albania. Serbia Israel. FYR Macedonia Latvia

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

Serbian Tax Card 2018

Serbian Tax Card 2018 KPMG d.o.o. Beograd kpmg.com/rs CORPORATE INCOME TAX A resident is a legal entity which is incorporated or has a place of effective management and control on the territory of Serbia.

Serbian Tax Card 2018 KPMG d.o.o. Beograd kpmg.com/rs CORPORATE INCOME TAX A resident is a legal entity which is incorporated or has a place of effective management and control on the territory of Serbia.

Double Tax Treaties. Necessity of Declaration on Tax Beneficial Ownership In case of capital gains tax. DTA Country Withholding Tax Rates (%)

") Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Montenegro Country Profile

Montenegro Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Montenegro EU Member State (EU candidate) Double Tax Treaties With: Albania

Montenegro Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Montenegro EU Member State (EU candidate) Double Tax Treaties With: Albania

Slovakia Country Profile

Slovakia Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Slovakia EU Member State Double Tax Treaties Yes With: Australia Austria Belarus

Slovakia Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Slovakia EU Member State Double Tax Treaties Yes With: Australia Austria Belarus

Latvia Country Profile

Latvia Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Latvia EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

Latvia Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Latvia EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

FOREWORD. Estonia. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Serbia Country Profile

Serbia Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Serbia EU Member State Double Tax Treaties With: Albania Austria Azerbaijan Belarus

Serbia Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Serbia EU Member State Double Tax Treaties With: Albania Austria Azerbaijan Belarus

FOREWORD. Montenegro. Services provided by member firms include:

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

BULGARIAN TAX GUIDE 2017

GLOBAL CONSULT EUROPE LTD. Sofia 1504, Bulgaria 23A San Stefano str. Tel : +359 889 85 00 87 info@companyinbg.com www.companyinbg.com BULGARIAN TAX GUIDE 2017 I. CORPORATE INCOME TAX (CIT) Resident companies

GLOBAL CONSULT EUROPE LTD. Sofia 1504, Bulgaria 23A San Stefano str. Tel : +359 889 85 00 87 info@companyinbg.com www.companyinbg.com BULGARIAN TAX GUIDE 2017 I. CORPORATE INCOME TAX (CIT) Resident companies

Croatia Country Profile

Croatia Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Croatia EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

Croatia Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Croatia EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

Table of Contents. 1 created by

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

Withholding Tax Rate under DTAA

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 224 Podgorica, 22 December 2017 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017 The release

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 224 Podgorica, 22 December 2017 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 3 rd quarter 2017 The release

Lithuania Country Profile

Lithuania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Lithuania EU Member State Yes Double Tax Treaties With: Armenia Austria Azerbaijan

Lithuania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Lithuania EU Member State Yes Double Tax Treaties With: Armenia Austria Azerbaijan

DEVELOPMENT AID AT A GLANCE

DEVELOPMENT AID AT A GLANCE STATISTICS BY REGION 5. EUROPE 6 edition 5.. ODA TO EUROPE - SUMMARY 5... Top ODA receipts by recipient USD million, net disbursements in 5... Trends in ODA Turkey % Ukraine

DEVELOPMENT AID AT A GLANCE STATISTICS BY REGION 5. EUROPE 6 edition 5.. ODA TO EUROPE - SUMMARY 5... Top ODA receipts by recipient USD million, net disbursements in 5... Trends in ODA Turkey % Ukraine

(of 19 March 2013) Valid from 1 January A. Taxpayers

Valid from 1 January A. Taxpayers") Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia KPMG Baltics OÜ kpmg.com/ee CORPORATE INCOME TAX In Estonia, corporate income tax is not levied when profit is earned but when it is

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia KPMG Baltics OÜ kpmg.com/ee CORPORATE INCOME TAX In Estonia, corporate income tax is not levied when profit is earned but when it is

Tax Card KPMG in Bulgaria. kpmg.com/bg

Tax Card 2017 KPMG in Bulgaria kpmg.com/bg CORPORATE TAX Corporate income tax (CIT) is due on the accounting profit after adjustments for tax purposes. The applicable tax rate for the year 2017 is 10%.

Tax Card 2017 KPMG in Bulgaria kpmg.com/bg CORPORATE TAX Corporate income tax (CIT) is due on the accounting profit after adjustments for tax purposes. The applicable tax rate for the year 2017 is 10%.

Withholding tax rates 2016 as per Finance Act 2016

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Tax Card KPMG in Macedonia. kpmg.com/mk

Tax Card 2016 KPMG in Macedonia kpmg.com/mk TAXATION OF CORPORATE PROFITS Corporate income tax (CIT) is due from profits realized by resident legal entities as well as by non-residents with a permanent

Tax Card 2016 KPMG in Macedonia kpmg.com/mk TAXATION OF CORPORATE PROFITS Corporate income tax (CIT) is due from profits realized by resident legal entities as well as by non-residents with a permanent

Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%

![Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%](/thumbs/88/116150947.jpg "Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%") Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Tax Card With effect from 1 January 2016 Lithuania. KPMG Baltics, UAB. kpmg.com/lt

Tax Card 2016 With effect from 1 January 2016 Lithuania KPMG Baltics, UAB kpmg.com/lt CORPORATE INCOME TAX Taxable profit of Lithuanian and foreign corporate taxpayers is subject to a standard (flat) rate

Tax Card 2016 With effect from 1 January 2016 Lithuania KPMG Baltics, UAB kpmg.com/lt CORPORATE INCOME TAX Taxable profit of Lithuanian and foreign corporate taxpayers is subject to a standard (flat) rate

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

Enterprise Europe Network SME growth outlook

Enterprise Europe Network SME growth outlook 2018-19 een.ec.europa.eu 2 Enterprise Europe Network SME growth outlook 2018-19 Foreword The European Commission wants to ensure that small and medium-sized

Enterprise Europe Network SME growth outlook 2018-19 een.ec.europa.eu 2 Enterprise Europe Network SME growth outlook 2018-19 Foreword The European Commission wants to ensure that small and medium-sized

Romania Country Profile

Romania Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Austria Country Profile

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile

Romania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

APA & MAP COUNTRY GUIDE 2017 CROATIA

APA & MAP COUNTRY GUIDE 2017 CROATIA Managing uncertainty in the new tax environment CROATIA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

APA & MAP COUNTRY GUIDE 2017 CROATIA Managing uncertainty in the new tax environment CROATIA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

Finland Country Profile

Finland Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Finland EU Member State Double Tax Treaties With: Argentina Armenia Australia

Finland Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Finland EU Member State Double Tax Treaties With: Argentina Armenia Australia

great place to live and to locate you business Ministry of Economy of the Republic of Moldova

Invest in Moldova great place to live and to locate you business Ministry of Economy of the Republic of Moldova Moldova a strategic location Proximity to key markets European Union Market Commonwealth

Invest in Moldova great place to live and to locate you business Ministry of Economy of the Republic of Moldova Moldova a strategic location Proximity to key markets European Union Market Commonwealth

Malta Country Profile

Malta Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Malta EU Member State Yes. Double Tax Treaties With: Albania Andorra Australia

Malta Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Malta EU Member State Yes. Double Tax Treaties With: Albania Andorra Australia

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Czech Republic Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

INTESA SANPAOLO S.p.A. INTESA SANPAOLO BANK IRELAND p.l.c. 70,000,000,000 Euro Medium Term Note Programme

PROSPECTUS SUPPLEMENT INTESA SANPAOLO S.p.A. (incorporated as a società per azioni in the Republic of Italy) as Issuer and, in respect of Notes issued by Intesa Sanpaolo Bank Ireland p.l.c., as Guarantor

PROSPECTUS SUPPLEMENT INTESA SANPAOLO S.p.A. (incorporated as a società per azioni in the Republic of Italy) as Issuer and, in respect of Notes issued by Intesa Sanpaolo Bank Ireland p.l.c., as Guarantor

Withholding Tax Handbook BELGIUM. Version 1.2 Last Updated: June 20, New York Hong Kong London Madrid Milan Sydney

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

ORD ISIN: DE / CINS CUSIP: D (ADR: / US )

") The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

A. Definitions and sources of data

Poland A. Definitions and sources of data Data on foreign direct investment (FDI) in Poland are reported by the National Bank of Poland (NBP), the Polish Agency for Foreign Investment (PAIZ) and the Central

Poland A. Definitions and sources of data Data on foreign direct investment (FDI) in Poland are reported by the National Bank of Poland (NBP), the Polish Agency for Foreign Investment (PAIZ) and the Central

Paid from Cyprus Divident (1) % Interest (1) %

% Interest (1) %") Tax treaties withholding tax tables The following tables give a summary of the withholding taxes provided by the double tax treaties entered into by Cyprus. Paid from Cyprus Divident Interest Royalties

Tax treaties withholding tax tables The following tables give a summary of the withholding taxes provided by the double tax treaties entered into by Cyprus. Paid from Cyprus Divident Interest Royalties

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Gerry Weber International AG

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

Poland Country Profile

Poland Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Poland EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Poland Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Poland EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Malta Country Profile

Malta Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Malta EU Member State Yes. Double Tax Treaties With: Albania Australia Austria

Malta Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Malta EU Member State Yes. Double Tax Treaties With: Albania Australia Austria

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Czech Rep. EU Member State Yes Double Tax With: Treaties Albania Armenia

Czech Republic Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Czech Rep. EU Member State Yes Double Tax With: Treaties Albania Armenia

Quarterly Gross Domestic Product of Montenegro 2st quarter 2016

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro 2st quarter 2016 The release presents the preliminary data for quarterly gross domestic product

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro 2st quarter 2016 The release presents the preliminary data for quarterly gross domestic product

FOREWORD. Slovak Republic

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Economic and Social Council

United Nations ECE/MP.PP/WG.1/2011/L.7 Economic and Social Council Distr.: Limited 25 November 2010 Original: English Economic Commission for Europe Meeting of the Parties to the Convention on Access to

United Nations ECE/MP.PP/WG.1/2011/L.7 Economic and Social Council Distr.: Limited 25 November 2010 Original: English Economic Commission for Europe Meeting of the Parties to the Convention on Access to

TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA)

") TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA) In the period January - June 2018 the exports of goods from Bulgaria to the EU increased by 10.7% 2017 and amounted

TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA) In the period January - June 2018 the exports of goods from Bulgaria to the EU increased by 10.7% 2017 and amounted

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Gross domestic product of Montenegro in 2016

MONTENEGRO STATISTICAL OFFICE R E L E A S E No:174 Podgorica 29 September 2017 When using the data pleaase name the source Gross domestic product of Montenegro in 2016 Real growth rate of gross domestic

MONTENEGRO STATISTICAL OFFICE R E L E A S E No:174 Podgorica 29 September 2017 When using the data pleaase name the source Gross domestic product of Montenegro in 2016 Real growth rate of gross domestic

Lex Mundi European Union: Accession States Tax Guide. SLOVENIA Vidovic & Partners

Lex Mundi European Union: Accession States Tax Guide SLOVENIA Vidovic & Partners CONTACT INFORMATION: Natasa Vidovic Vidovic & Partners Tel: 386.1.500.73.20 - Fax: 386.1.500.73.22 E-mail: vp@vidovic-op.si

Lex Mundi European Union: Accession States Tax Guide SLOVENIA Vidovic & Partners CONTACT INFORMATION: Natasa Vidovic Vidovic & Partners Tel: 386.1.500.73.20 - Fax: 386.1.500.73.22 E-mail: vp@vidovic-op.si

ide: FRANCE Appendix A Countries with Double Taxation Agreement with France

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Belgium Country Profile

Belgium Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Belgium Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Quarterly Gross Domestic Product of Montenegro for period 1 st quarter rd quarter 2016

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro for period 1 st quarter 015 - rd quarter 016 The release presents the final results of quarterly

Government of Montenegro Statistical Office of Montenegro Quarterly Gross Domestic Product of Montenegro for period 1 st quarter 015 - rd quarter 016 The release presents the final results of quarterly

Coach Plus Breakdown Insurance

1 Coach Plus Breakdown Insurance Specialist cover for UK and Europe Coach Plus Breakdown Annual Multi-trip Insurance 2018 Underwriting Guide - valid from 1st January 2018 Travel must take place within

1 Coach Plus Breakdown Insurance Specialist cover for UK and Europe Coach Plus Breakdown Annual Multi-trip Insurance 2018 Underwriting Guide - valid from 1st January 2018 Travel must take place within

Cyprus - The gateway to global investments

Cyprus - The gateway to global investments Why Choose Cyprus for International Business Activities? Cyprus has long been established as a reputable international financial centre, the ideal bridge between

Cyprus - The gateway to global investments Why Choose Cyprus for International Business Activities? Cyprus has long been established as a reputable international financial centre, the ideal bridge between

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p)

") MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 46 Podgorica, 22 March 2019 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p) The release

MONTENEGRO STATISTICAL OFFICE R E L E A S E No: 46 Podgorica, 22 March 2019 When using the data, please name the source Quarterly Gross Domestic Product of Montenegro 4 th quarter 2018 (p) The release

Sweden Country Profile

Sweden Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Sweden EU Member State Double Tax Treaties With: Albania Armenia Argentina Azerbaijan

Sweden Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Sweden EU Member State Double Tax Treaties With: Albania Armenia Argentina Azerbaijan

Taxation of Cross-Border Mergers and Acquisitions

KPMG International Taxation of Cross-Border Mergers and Acquisitions Croatia kpmg.com 2 Croatia: Taxation of Cross-Border Mergers and Acquisitions Croatia Introduction the chapter addresses the three fundamental

KPMG International Taxation of Cross-Border Mergers and Acquisitions Croatia kpmg.com 2 Croatia: Taxation of Cross-Border Mergers and Acquisitions Croatia Introduction the chapter addresses the three fundamental

Bosnia and Herzegovina Country Profile

Bosnia and Herzegovina Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Bosnia and Herzegovina EU Member State Double Tax Treaties With:

Bosnia and Herzegovina Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Bosnia and Herzegovina EU Member State Double Tax Treaties With:

InnovFin SME Guarantee

InnovFin SME Guarantee Implementation Update Reporting date: 30/09/2017 Disclaimer This presentation contains general information about the implementation results of InnovFin SME Guarantee, a facility

InnovFin SME Guarantee Implementation Update Reporting date: 30/09/2017 Disclaimer This presentation contains general information about the implementation results of InnovFin SME Guarantee, a facility

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Czech Republic Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

Contents. Andreas Athinodorou Managing Director International Tax Planning

Seize the advantage of our expertise Technical Newsletter This publication should be used as a source of general information only. For the specific applications of the Law, professional advice should be

Seize the advantage of our expertise Technical Newsletter This publication should be used as a source of general information only. For the specific applications of the Law, professional advice should be

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

FOREWORD. Finland. Services provided by member firms include:

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Ireland Country Profile

Ireland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Ireland EU Member State Yes Double Tax Treaties With: Albania Armenia Australia

Ireland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Ireland EU Member State Yes Double Tax Treaties With: Albania Armenia Australia

Valid from 1 January A. Taxpayers

Leaflet. 29/410 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under public law for persons without domicile or in Switzerland (of 19 March 2013) Valid from 1 January 2013

Leaflet. 29/410 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under public law for persons without domicile or in Switzerland (of 19 March 2013) Valid from 1 January 2013

Belgium Country Profile

Belgium Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Belgium Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

APA & MAP COUNTRY GUIDE 2018 UKRAINE. New paths ahead for international tax controversy

APA & MAP COUNTRY GUIDE 2018 UKRAINE New paths ahead for international tax controversy UKRAINE APA PROGRAM KEY FEATURES Competent authority Relevant provisions Types of APAs available Acceptance criteria

APA & MAP COUNTRY GUIDE 2018 UKRAINE New paths ahead for international tax controversy UKRAINE APA PROGRAM KEY FEATURES Competent authority Relevant provisions Types of APAs available Acceptance criteria

Comparing pay trends in the public services and private sector. Labour Research Department 7 June 2018 Brussels

Comparing pay trends in the public services and private sector Labour Research Department 7 June 2018 Brussels Issued to be covered The trends examined The varying patterns over 14 years and the impact

Comparing pay trends in the public services and private sector Labour Research Department 7 June 2018 Brussels Issued to be covered The trends examined The varying patterns over 14 years and the impact

Turkey Country Profile

Turkey Country Profile EU Tax Centre June 2018 EU Tax Centre June 2018 Turkey Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties No

Turkey Country Profile EU Tax Centre June 2018 EU Tax Centre June 2018 Turkey Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties No

Turkey Country Profile

Turkey Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties With: Albania Algeria Australia Austria

Turkey Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties With: Albania Algeria Australia Austria

Greece Country Profile

Greece Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Greece EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

Greece Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Greece EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

EUREKA Programme A European Research Programme. > Not an EU-Programme (but complementarity and co-operation - ERA)

") EUREKA EUREKA Programme...... Shaping tomorrow s innovations today EUREKA in glance > 2 A European Research Programme > Not an EU-Programme (but complementarity and co-operation - ERA) > Bottom-up project

EUREKA EUREKA Programme...... Shaping tomorrow s innovations today EUREKA in glance > 2 A European Research Programme > Not an EU-Programme (but complementarity and co-operation - ERA) > Bottom-up project

Cyprus Country Profile

Cyprus Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

Cyprus Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

Cyprus New Double Tax Treaties Become Effective

Seize the advantage of our expertise Cyprus New Double Tax Treaties Become Effective Cyprus Double Tax Treaty (DTT) network has been expanded with four new agreements with Lithuania, Norway, Spain and

Seize the advantage of our expertise Cyprus New Double Tax Treaties Become Effective Cyprus Double Tax Treaty (DTT) network has been expanded with four new agreements with Lithuania, Norway, Spain and

International Taxation

International Taxation 2015 www.epwcy.com 1. Tax Planning through Cyprus Cyprus is consistently voted as the most attractive European tax regime by major business organizations and tax professionals across

International Taxation 2015 www.epwcy.com 1. Tax Planning through Cyprus Cyprus is consistently voted as the most attractive European tax regime by major business organizations and tax professionals across

Summary of key findings

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

Malta s Double Tax Treaties

Malta s Double Tax Treaties November 216 In order to encourage the growth of international trade including that of financial services, successive Maltese governments have sought to conclude double tax

Malta s Double Tax Treaties November 216 In order to encourage the growth of international trade including that of financial services, successive Maltese governments have sought to conclude double tax

Lex Mundi European Union: Accession States Tax Guide. BULGARIA Penkov, Markov & Partners

Lex Mundi European Union: Accession States Tax Guide BULGARIA Penkov, Markov & Partners CONTACT INFORMATION: Svetlin Adrianov Penkov, Markov & Partners Tel: 359.2.9713935 - Fax: 359.2.9711191 E-mail: lega@bg400.bg

Lex Mundi European Union: Accession States Tax Guide BULGARIA Penkov, Markov & Partners CONTACT INFORMATION: Svetlin Adrianov Penkov, Markov & Partners Tel: 359.2.9713935 - Fax: 359.2.9711191 E-mail: lega@bg400.bg

Other Tax Rates. Non-Resident Withholding Tax Rates for Treaty Countries 1

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

Malta s Double Tax Treaties

Malta s Double Treaties February 216 In order to encourage the growth of international trade including that of financial services, successive Maltese governments have sought to conclude double tax treaties

Malta s Double Treaties February 216 In order to encourage the growth of international trade including that of financial services, successive Maltese governments have sought to conclude double tax treaties

Following our Announcement A10025, dated 15 February 2010, effective. 1 March 2010

Announcement Tax A10033 Bulgaria: Tax relief procedure for Bulgarian securities Following our Announcement A10025, dated 15 February 2010, effective 1 March 2010 final beneficial owners can use the procedure

Announcement Tax A10033 Bulgaria: Tax relief procedure for Bulgarian securities Following our Announcement A10025, dated 15 February 2010, effective 1 March 2010 final beneficial owners can use the procedure

FY18 Campaign Terms. CAMPAIGN AGREEMENT ( Campaign Agreement ) FOR CEE DYNAMICS 365 CSP CAMPAIGN ( Program )

FOR CEE DYNAMICS 365 CSP CAMPAIGN ( Program )") 1. PROGRAM OVERVIEW CAMPAIGN AGREEMENT ( Campaign Agreement ) FOR CEE DYNAMICS 365 CSP CAMPAIGN ( Program ) OFFERED BY MIOL (MICROSOFT EOC) ( Microsoft ) and/or OFFERED BY MS Subsidiary ( Microsoft ) Microsoft

1. PROGRAM OVERVIEW CAMPAIGN AGREEMENT ( Campaign Agreement ) FOR CEE DYNAMICS 365 CSP CAMPAIGN ( Program ) OFFERED BY MIOL (MICROSOFT EOC) ( Microsoft ) and/or OFFERED BY MS Subsidiary ( Microsoft ) Microsoft

Cyprus Country Profile

Cyprus Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

Cyprus Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

FOREWORD. Serbia. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Katharina Lehmeier San Sebastian > EUREKA. ProFactory2 Brokerage Event. Doing business through technology

Katharina Lehmeier San Sebastian > 07-10-11 EUREKA and its Manufacturing Technology Sector ProFactory2 Brokerage Event EUREKA : 25 Years of R&D support > 2 > EUREKA is a public network supporting R&D-performing

Katharina Lehmeier San Sebastian > 07-10-11 EUREKA and its Manufacturing Technology Sector ProFactory2 Brokerage Event EUREKA : 25 Years of R&D support > 2 > EUREKA is a public network supporting R&D-performing

Financial situation by the end of Table 1. ECPGR Contributions for Phase IX received by 31 December 2016 (in Euro)...3

...3") European Cooperative Programme for Plant Genetic Resources (ECPGR) Phase IX (2014 2018) Financial Report CONTENTS Financial situation by the end of...2 Table 1. ECPGR Contributions for Phase IX received

European Cooperative Programme for Plant Genetic Resources (ECPGR) Phase IX (2014 2018) Financial Report CONTENTS Financial situation by the end of...2 Table 1. ECPGR Contributions for Phase IX received

Double tax considerations on certain personal retirement scheme benefits

www.pwc.com/mt The elimination of double taxation on benefits paid out of certain Maltese personal retirement schemes February 2016 Double tax considerations on certain personal retirement scheme benefits

www.pwc.com/mt The elimination of double taxation on benefits paid out of certain Maltese personal retirement schemes February 2016 Double tax considerations on certain personal retirement scheme benefits

Norway Country Profile

rway Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving rway EU Member State Double Tax Treaties With: Albania Argentina Australia Austria

rway Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving rway EU Member State Double Tax Treaties With: Albania Argentina Australia Austria

INTERNATIONAL JOURNAL OF RESEARCH AND ANALYSIS VOLUME 5 ISSUE 2 ISSN

CRITICAL ANALYSIS ON DOUBLE TAXATION AVOIDANCE AGREEMENT **AASTHA SUMAN & HIMANSHU SHUKLA The DTAA, or Double countries) so that taxpayers can avoid paying double taxes on their income earned from the

CRITICAL ANALYSIS ON DOUBLE TAXATION AVOIDANCE AGREEMENT **AASTHA SUMAN & HIMANSHU SHUKLA The DTAA, or Double countries) so that taxpayers can avoid paying double taxes on their income earned from the

Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

17 July 2017 Global Tax Alert Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

17 July 2017 Global Tax Alert Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

Export and import operations Tax & Legal, April 2017

Export and import operations Tax & Legal, April 2017 Export and import operations Tax & Legal, April 2017 Effective trading operations in Uzbekistan Today Uzbekistan actively develops international trading.

Export and import operations Tax & Legal, April 2017 Export and import operations Tax & Legal, April 2017 Effective trading operations in Uzbekistan Today Uzbekistan actively develops international trading.

European Union: Accession States Tax Guide. LITHUANIA Lawin

A. General information European Union: Accession States Tax Guide LITHUANIA Lawin CONTACT INFORMATION Gintaras Balcius Lawin Jogailos 9/1 Vilnius, LT-01116 Lithuania 370.5.268.18.88 gintaras.balcius@lawin.lt

A. General information European Union: Accession States Tax Guide LITHUANIA Lawin CONTACT INFORMATION Gintaras Balcius Lawin Jogailos 9/1 Vilnius, LT-01116 Lithuania 370.5.268.18.88 gintaras.balcius@lawin.lt

Alter Domus IRELAND WE RE WHERE YOU NEED US.

WE RE WHERE YOU NEED US. Alter Domus is a fully integrated Fund and Corporate services provider, dedicated to international private equity & infrastructure houses, real estate firms, multinationals, private

WE RE WHERE YOU NEED US. Alter Domus is a fully integrated Fund and Corporate services provider, dedicated to international private equity & infrastructure houses, real estate firms, multinationals, private

FOREWORD. Egypt. Services provided by member firms include:

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are