Recent evolution of the main banking and monetary indicators - I. Monthly, Analysis Issue No 13, Jul 2003

|

|

|

- Avis Chastity Phillips

- 5 years ago

- Views:

Transcription

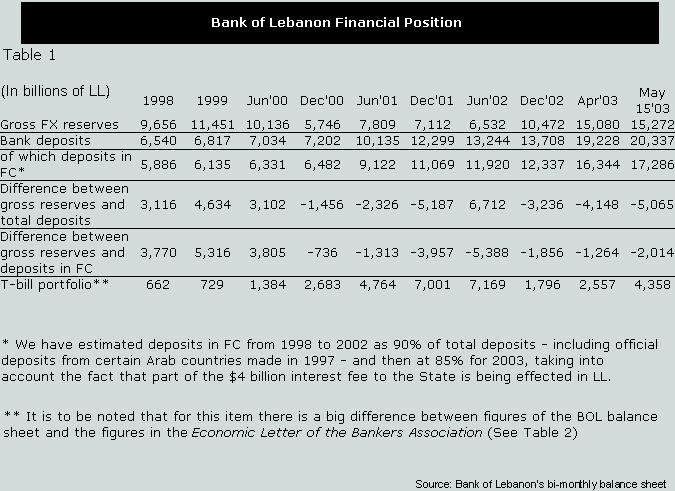

1 Recent evolution of the main banking and monetary indicators - I. Monthly, Analysis Issue No 13, Jul 2003 Discrepancies in figures published by the Central Bank and the Banker s Association The asset/liability structure of the Lebanese banking system has changed substantially in the last two years. Although data are becoming less transparent and appear to contain some contradictions, we will try to assess the evolution that has occurred. Let me begin by pointing to some of these discrepancies. It is regrettable that neither the Bank of Lebanon (BOL) nor the Ministry of Finance (MOF) have explained the technical reasons behind some large changes in published figures that have taken place from time to time. Nor have they explained the important differences in data that we can find between the same figures in the consolidated balance sheet of the banking system and the BOL balance sheet. As an example of the significant discrepancies in the data series, we can point out that, while the BOL balance sheet, as published bimonthly in Lebanese newspapers, indicates that commercial bank deposits with the BOL stood at LL 13, 708 billion in December 2002, the deposits figure shown in the consolidated balance sheet of the banking system, as published in the Monthly Economic Letter of the Association of Banks, was only LL 11, 794 billion at the same date (see Table 2). The LL 2, 000 billion difference is not negligible. It could represent the deposits made by some Arab countries through their national banks to assist Lebanon, but as shown Table 2, this difference is not consistent within the statistical series.

2

3 We find two other important discrepancies in the figures concerning T-bill and Eurobond holdings by Lebanese banks, as follows: As shown in the Economic Newsletter of the Banker s Association, the banks holdings of T-bills denominated in Lebanese pounds stood at 16, 214 billion pounds in December 2002 in the consolidated balance sheet, but are stated at LL 17, 211 billion pounds in the statistics about outstanding public debt by type of holder.

4 In the same source, the amount of outstanding Eurobonds in December 2002 is reported at LL 10, 309 billion in the consolidated balance sheet, while the total outstanding amount of Eurobonds in the statistics by type of holders was LL 19, 759 billion at the same date. This would imply that commercial banks held only 52% of outstanding Eurobonds and that the other 48% were held by non-resident institutions or individual residents or possibly BOL. This is difficult to believe. In the good days, when sovereign Lebanese bonds were selling well, non-residents did not subscribe to more than 15% of any issue. How can one explain the rise in the proportion of non-bank holdings in view of all the pressure on the price of those bonds in One explanation may be that the amounts that were committed by Paris II donors, and paid, are now included in this figure. These discrepancies complicate the task of analyzing the data available. However, some noticeable trend fluctuations in monetary and banking figures could be identified. The pressures on foreign exchange reserves during Owing to the lack of transparency in the data available, as well as the lack of commentary by concerned entities on published figures, a lot of monetary and financial rumors have circulated during the last two years. In fact, between the summer of 2001 and the summer of 2002, we seem to have witnessed a replay of the artificial 1995 crisis, when depositors became very anxious about the fate of their savings, especially those in domestic currency. The specter of a general payment crisis on the Argentinian model loomed heavily on the behavior of depositors and T- bills, or Eurobond holders. The low point in this crisis appears to have occurred at the end of September 2002, when: The price of Lebanese Eurobonds declined under 80% of face value. The ratio of dollar deposits to total deposits increased to 75%, from 62% in The banks refused to roll over their maturing T-bills in domestic currency, obliging the BOL to raise its own holdings to more than LL 8,000 billion. Gross foreign exchange reserves of the BOL declined to LL 5,800 billion in September 2001 and were artificially boosted by imposing a compulsory reserve requirement of 15% on dollar deposits with the banking system. Through one of their brilliant communication campaigns, however, the the Lebanese authorities were able to halt the conversion of domestic currency to US dollars, as well as the large capital outflows that the country was experiencing. The campaign had two main themes: The first focused on the objective of the draft State Budget for the year 2003 to boldly reduce the deficit from the range of 40% 50% in previous years to only 25% of total expenditures. The second spoke loudly about the anticipated success of the planned international gathering to assist Lebanon (what came to be known as Paris II).

5 As in the earlier campaigns to justify the creation of SOLIDERE, or to give glamour to the gathering in Washington in 1996 to finance Lebanon s reconstruction, or the numerous campaigns to destabilize the Hoss government and prevent the implementation of financial reforms, the Prime Minister s media campaign was very successful. BOL also provided an additional boost to expected improvements by inflating its FX reserves through the launch, during the summer of 2001, of a one billion dollar bond issue, to which it subscribed entirely, and apparently included at least part of the future proceeds of such bonds in the reserves. As was known, some bonds were sold subsequently at a very significant discount to some Arab, and possibly, also to some Lebanese institutions.

to the State without interest for a two-year period.")

6 Paris II and the interest-free lending by the banks to the State Those adverse trends were reversed following the relative success of the Paris II meeting more specifically, when the BOL, together with the largest Lebanese banks, adopted the spectacular measure of having the commercial banks lend 10% of their deposits (or about $4 billion) to the State without interest for a two-year period. Together with the new amounts effectively committed during the Paris II meeting ($ 2.2 billion, and not $4.4 billion as was announced), this measure amounted to securing more than $6 billion for the Treasury at an average interest rate of 1.75% per annum. Adding bravura, the BOL decided that the interest rate structure could now decline substantially. Previously, it had emphasized that this structure was determined by market forces, rather than by agreement with the banks. This was a total turnaround from previous years, when the BOL and the big banks stubbornly refused to bring about the much-needed decline in interest rates. This was the case even when inflation was subdued, the balance of payments positive and the Treasury flushed with liquidity, which was the picture during the last six months of By the end of 2002, however, the stubborn market suddenly turned extremely positive. (In fact, in 1999 and 2000, the banks refused totally to envisage a three- or five-year bond issue for the Treasury in Lebanese pounds at a floating rate, which the Minister of Finance was asking for so as to reduce the cost of funds to the Treasury and reduce the risk for the banks of interest rate fluctuations. Today, three-year CD issues at 9.5% constitute a very big improvement from the previous rigidity of the BOL and the banks in managing the debt and the liquidity in domestic currency. There are rumors, however, that BOL is now selling those CDs at a discount). The release of funds from Paris II and the interest rate measures agreed upon between BOL and the commercial banks appear to have provided the financial system with some breathing space. The only regret here is that the BOL and the big banks took so much time to understand that the former monopoly game had to

also have expressed their strong feelings about lending at such rates while")

7 stop, at least for the time being, to avoid collapse. Probably the countries that accepted to lend to Lebanon at 5% for 15 years, and the IMF (which did not lend any funds) also have expressed their strong feelings about lending at such rates while Lebanese banks were cashing 18.5% on domestic T-bills and 10% or more when buying sovereign Lebanese Eurobonds at discount. Meanwhile, depositors could be reassured that, for at least the next 12 or 18 months, there would be no liquidity problem for the Treasury, either in Lebanese pounds or in US dollars. Commercial banks have been using the proceeds of their huge portfolio of two-year T-bills yielding 18.5% to continue to pay their depositors high interest rates, in spite of the fact that the BOL has dramatically decreased new T-bill rates. Hefty profits were also made by the banks and institutions that took the risk of buying Lebanese Eurobonds when they were selling at large discounts during most of In addition, and as is well known, lending rates to the private sector did not decline, which should have been the case after the decline in T-bill rates. In fact, banks net interest margins remain quite high and their temporary sacrifice is quite affordable, as interest rates earned on their dollar liquidity placed abroad would not yield more than 1.25%. Apparently, the banks are also continuing to enjoy high interest rates of between 8% and 9% on their dollar deposits with BOL, other than the $4 billion without interest that have not yet been entirely paid. Even if there is no danger under present circumstances of another creeping crisis on the pound, and of renewed outflows of capital out of the banking system, this does not mean that Lebanon will not face the same old problems next year. In fact, the last figures from the BOL balance sheet published on 15 May 2003, as well as data available about the Treasury indebtedness through the February 2003 Economic newsletter of the Association of Banks, continue to show a worrying situation. What the recent data show Analysis of the data presented in Tables 1 and 2 shows the following facts:

8 BOL s net financial position has resumed its deterioration The difference between gross foreign exchange reserves and banks deposits with the BOL stood at plus LL 3,116 billion in 1998, but this figure turned negative in 2001 and 2002, reaching a high of minus LL 6,712 billion in June After an improvement in December 2002 to minus LL 3,236 billion, the figure rose to minus LL 5,065 billion at the most recent date of 15 May (It should be noted that the abbreviated IMF report submitted to the Paris II Conference mentioned the fact that foreign exchange reserves of the BOL were negative to the level of $ 2 billion - this figure did not take into account the one billion dollars of Arab deposits with the BOL). This means that the BOL position, in spite of Paris II, has not improved substantially since December In addition, for unknown reasons and in spite of the $ 6.4 billion that has been put at the disposal of the Treasury, BOL is once again increasing its holdings of T-bills or Eurobonds, which amounted to LL 4,358 billion pounds in May 2003 (as against LL 1,796 billion when BOL cancelled most of the T-bill portfolio on the Treasury, corresponding to the transfer to the Treasury of FX profits on the gold stock of the Bank). The evolution of the commercial banks consolidated balance sheet (Tables 2, 3 and 4) shows a mixed picture In February 2003, banks held LL 13,055 billion in deposits with the BOL, of which at least 80% were in US dollars. If we add to this figure the banks portfolio of Lebanese pound T-bills, amounting to LL 16,591 billion and their Eurobond portfolio of LL 11,315 billion pounds, the amount of exposure of banks to the State and BOL reaches the equivalent of LL 40,961 billion pounds (US$27 billion). This amount represents 52% of total assets of the banking sector. The proportion to the foreign exchange component of this exposure amounted to 35% in 1999, but rose to 43% recently. This could be considered an improvement for the banks, as they have substantially reduced their exposure to T-bills in domestic currency. At the same time, the share of commercial banks in total Treasury and BOL liabilities declined from 73% in 1998 to 62.4% most recently. Table 3 shows that while the State debt in T-bills and Eurobonds held by the banking system at the end of 1998 represented 66.8% of the total, this percentage declined to 57.4% at the end of The domestic currency/foreign currency composition of the banks claims on the Treasury (Table 4) has substantially changed during the last two years. T-bills in Lebanese pounds represented 84% of the portfolio against 16% in Eurobonds in By February 2003, the domestic currency component of banks claims on the Treasury came down to 60%, from 84%, and the foreign currency component shot up to 40%, from 16%. Additional claims on the State due to deposits with BOL are also massively in foreign currency, so that during these last two years the banking system was able to shift from claims held principally in Lebanese pounds to claims in US dollars. Another development that could be considered favorable for the banking sector is that its share in Treasury indebtedness fell from 66.8% to 57.4%, and its share in

9 Treasury and BOL indebtedness decreased from 73% in 1998 to 64% in December The foreign exchange component of this share has gone up, from 35% in 1998/1999 to 54% 55% in 2001/2002. When looking at the total liabilities of the State and BOL, one notices that commercial banks deposits with the BOL represented only 21% of the banks total claims on the State and BOL in 1998, but now amount to 34%. One alarming development is the dramatic increase in the FX content of total indebtedness While the Hoss government, which held office from November 1998 to October 2000, had pledged to Parliament (in the course of presenting the budget for 1999) that it would not raise the ratio of State debt in foreign currencies to total debt to

10 more than 40%, the present government has increased this ratio in just over two years from 25.1% in June 2000 to 46.8% in February 2003 (see Table 5). If we add the gross liabilities of the BOL in FX to the Treasury liabilities, then the FX content in this total indebtedness has increased from 35.5% in June 2000 to 58.4% in February The picture of what happened in the last two years is more alarming when we look at the content of FX in the net total indebtedness of the State and BOL, i.e. the gross indebtedness minus the FX reserves. The share of this component has been multiplied by three, increasing from 12% in June 2000 to 39.4% at the end of 2002 (Table 2). This indicator reflects the huge loss in FX reserves by the BOL since the return of the Hariri government. This is not to raise alarm with depositors. The government does not seem to be under any imminent pressures regarding meeting its maturing obligations. What is of concern, however, is that the government (the one now in office, as well as the former) does not seem to have a credible set of measures to address the structural issues that will surface again by the middle of next year. By that time, the Treasury indebtedness (excluding deposits with BOL) will have reached the equivalent of $35 billion, and total indebtedness of BOL and the State will be well above $45 billion. Even with the recent boost given to GDP figures, the situation will remain alarming. Nor has the government any plan on how to find the dollars needed to service the interest on this part of the debt, except to try to force the re-privatization of the mobile phone sector or the securitization of State receipts (phone or other), which will increase the financial pressures that Lebanon has been going through since 1995.

11 The conclusion of this analysis could be summarized in the following key points: The Lebanese economy has to increase its production considerably in order to generate the additional foreign exchange needed to service the large amount of indebtedness in foreign currency that has been accumulated in the last two years. To this effect, a progressive phasing out of our current monetary arrangements should be planned on a two- to three-year time span, as this monetary system has: Ruined the productive capacity of the country and created a complete dependence on borrowing foreign currencies to keep the economy afloat and prevent a financial crash. Transferred wealth and profits away from the productive sectors through the maintenance of very high interest rates on both dollars and Lebanese pounds. Been responsible for this formidable accumulation of private and public sector indebtedness, with the bulk of the debt having been constituted to service outrageously high interest rates. It is time to introduce structural and well-designed measures to deal with the situation and to reactivate our dormant economy, which suffers from a financial overhang totally out of line with the size of our productive capacity. To avoid a destructive future crisis, the productive capacity of the country has to increase dramatically to be in line with the size of the existing unproductive financial wealth. We intend to revisit these issues in the coming months.

12

External Account and Foreign Debt Management

The Lahore Journal of Economics Special Edition External Account and Foreign Debt Management Ashfaque H. Khan * Abstract The paper highlights strong gains in the macro area. The author also shows how total

The Lahore Journal of Economics Special Edition External Account and Foreign Debt Management Ashfaque H. Khan * Abstract The paper highlights strong gains in the macro area. The author also shows how total

EGYPT Affordable Mortgage Finance Program Development Policy Loan (Loan No EG) Release of the Second Tranche Full Compliance

Release of the Second Tranche Full Compliance") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized EGYPT Affordable Mortgage Finance Program Development Policy Loan (Loan No. 7747-EG)

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized EGYPT Affordable Mortgage Finance Program Development Policy Loan (Loan No. 7747-EG)

Ric Battellino: Recent financial developments

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Globalization. International Financial (Chap. 8) and Monetary (Chap. 9) Relations

and Monetary (Chap. 9) Relations") Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Globalization International Financial (Chap. 8) and Monetary (Chap. 9) Relations The Puzzle of Finance n Every year, approximately $5 trillion is invested abroad. Why is so much money invested in foreign

Lecture #8: How Scary is the US Trade Deficit?

Parsons, 2007 Lecture #8: How Scary is the US Trade Deficit? First, the facts: How big IS the US deficit? Well, if we look at the current account, whose largest component is the trade deficit, it was about

Parsons, 2007 Lecture #8: How Scary is the US Trade Deficit? First, the facts: How big IS the US deficit? Well, if we look at the current account, whose largest component is the trade deficit, it was about

QUESTIONS FOR RACHID SEKAK ECONOMIST

QUESTIONS FOR RACHID SEKAK ECONOMIST Question 1 The decline in oil prices for almost three years has resulted in a weakening of Algeria's financial position, both internally and externally: a significant

QUESTIONS FOR RACHID SEKAK ECONOMIST Question 1 The decline in oil prices for almost three years has resulted in a weakening of Algeria's financial position, both internally and externally: a significant

chapter: Savings, Investment Spending, and the Financial System Krugman/Wells 1 of Worth Publishers

chapter: 10 >> Savings, Investment Spending, and the Financial System Krugman/Wells 2009 Worth Publishers 1 of 58 WHAT YOU WILL LEARN IN THIS CHAPTER The relationship between savings and investment spending

chapter: 10 >> Savings, Investment Spending, and the Financial System Krugman/Wells 2009 Worth Publishers 1 of 58 WHAT YOU WILL LEARN IN THIS CHAPTER The relationship between savings and investment spending

Does the Riksbank have to make a profit?

SPEECH DATE: 23 January 2015 SPEAKER: First Deputy Governor Kerstin af Jochnick LOCATION: Swedish House of Finance (SHoF), Stockholm SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8

SPEECH DATE: 23 January 2015 SPEAKER: First Deputy Governor Kerstin af Jochnick LOCATION: Swedish House of Finance (SHoF), Stockholm SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8

External Debt Stock of Private Sector in Turkey

External Debt Stock of Private Sector in Turkey August 2016 Economic Research Division Our reports are available on our website https://research.isbank.com.tr 1 External Debt Stock of Private Sector in

External Debt Stock of Private Sector in Turkey August 2016 Economic Research Division Our reports are available on our website https://research.isbank.com.tr 1 External Debt Stock of Private Sector in

Is Lebanon Ready for CEDAR Conference?

Is Lebanon Ready for CEDAR Conference? On April 6, 2018 while elections will be underway on the ground, Lebanon will be seeking $17 Billion at the Paris IV conference (CEDAR). A National Infrastructure

Is Lebanon Ready for CEDAR Conference? On April 6, 2018 while elections will be underway on the ground, Lebanon will be seeking $17 Billion at the Paris IV conference (CEDAR). A National Infrastructure

Korea s Experience with International Capital Flows

Korea s Experience with International Capital Flows 1. Trends in International Capital Flows Korea s financial liberalization concomitant with its market opening began in the early 1980s, but at that time,

Korea s Experience with International Capital Flows 1. Trends in International Capital Flows Korea s financial liberalization concomitant with its market opening began in the early 1980s, but at that time,

BLOM Bank QI 2018 Earnings Conference Call Hosted by Exotix. 22 May 2018

BLOM Bank QI 2018 Earnings Conference Call Hosted by Exotix 22 May 2018 Hello and welcome to BLOM Bank Q1 2018 results conference call. My name is Amelia and I'll be your coordinator for today's conference.

BLOM Bank QI 2018 Earnings Conference Call Hosted by Exotix 22 May 2018 Hello and welcome to BLOM Bank Q1 2018 results conference call. My name is Amelia and I'll be your coordinator for today's conference.

Regling: Greece has to repay that loan in full. That is our expectation, nothing has changed in that regard.

Handelsblatt, 6 March 2015 Greece needs to repay its loan in full Handelsblatt: Mr. Regling, the euro rescue fund EFSF has lent around 142 billion to Greece and is thus by far Greece s largest creditor.

Handelsblatt, 6 March 2015 Greece needs to repay its loan in full Handelsblatt: Mr. Regling, the euro rescue fund EFSF has lent around 142 billion to Greece and is thus by far Greece s largest creditor.

Lebanon s Monetary Overview 2017

BLOMINVEST BANK February 23 rd, 2018 Contact Information Research Analyst: Riwa Daou Head of Research: Marwan Mikhael Confidence: the underlying driver behind every market s boom or bust. Currencies are

BLOMINVEST BANK February 23 rd, 2018 Contact Information Research Analyst: Riwa Daou Head of Research: Marwan Mikhael Confidence: the underlying driver behind every market s boom or bust. Currencies are

Introduction. Learning Objectives. Chapter 15. Money, Banking, and Central Banking

Chapter 15 Money, Banking, and Central Banking Introduction Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley have been big names on Wall Street for years. Known as investment

Chapter 15 Money, Banking, and Central Banking Introduction Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley have been big names on Wall Street for years. Known as investment

Ghana: Implications of the Rising Interest Costs to Government

Fiscal Alert No.4 December 2015 Ghana: Implications of the Rising Interest Costs to Government Introduction One important feature of fiscal management in Ghana in the last few years has been the rapid

Fiscal Alert No.4 December 2015 Ghana: Implications of the Rising Interest Costs to Government Introduction One important feature of fiscal management in Ghana in the last few years has been the rapid

Is China the New France?

Is China the New France? August 6, 2013 by Marianne Brunet Imagine a country that grows its economy by greatly devaluing against the reserve currency to develop a strong export sector. As the country becomes

Is China the New France? August 6, 2013 by Marianne Brunet Imagine a country that grows its economy by greatly devaluing against the reserve currency to develop a strong export sector. As the country becomes

POLICY PAPER. - Nº12 - August 2017 FINANCIAL CRISIS IN LEBANON TOUFIC GASPARD

POLICY PAPER - Nº12 - August 2017 FINANCIAL CRISIS IN LEBANON TOUFIC GASPARD N.B.: The content of this publication does not necessarily reflect the official opinion of the Konrad Adenauer Stiftung or the

POLICY PAPER - Nº12 - August 2017 FINANCIAL CRISIS IN LEBANON TOUFIC GASPARD N.B.: The content of this publication does not necessarily reflect the official opinion of the Konrad Adenauer Stiftung or the

BLOM Bank 2017 Earnings Conference Call Hosted by Exotix. 21 February 2018

BLOM Bank 2017 Earnings Conference Call Hosted by Exotix 21 February 2018 Hello, ladies and gentlemen, and welcome to the BLOM Bank 2017 Results Conference Call. My name is Operator, and I ll be your coordinator

BLOM Bank 2017 Earnings Conference Call Hosted by Exotix 21 February 2018 Hello, ladies and gentlemen, and welcome to the BLOM Bank 2017 Results Conference Call. My name is Operator, and I ll be your coordinator

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

CENTRAL BANK OF EGYPT

CENTRAL BANK OF EGYPT ECONOMIC REVIEW Vol. 46 No. 2 2005/2006 Research, Development and Publishing Sector This Review, issued in Arabic and English by the Research, Development and Publishing Sector, focuses

CENTRAL BANK OF EGYPT ECONOMIC REVIEW Vol. 46 No. 2 2005/2006 Research, Development and Publishing Sector This Review, issued in Arabic and English by the Research, Development and Publishing Sector, focuses

CENTRAL BANK OF EGYPT

CENTRAL BANK OF EGYPT ECONOMIC REVIEW Vol. 46 No. 1 2005/2006 Research, Development and Publishing Sector This Review, issued in Arabic and English by the Research, Development and Publishing Sector, focuses

CENTRAL BANK OF EGYPT ECONOMIC REVIEW Vol. 46 No. 1 2005/2006 Research, Development and Publishing Sector This Review, issued in Arabic and English by the Research, Development and Publishing Sector, focuses

Transcript of interview with ESM Managing Director Klaus Regling. The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016

Transcript of interview with ESM Managing Director Klaus Regling Published in Yomiuri Shimbun (Japan), 1 February 2016 The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016 Yomiuri

Transcript of interview with ESM Managing Director Klaus Regling Published in Yomiuri Shimbun (Japan), 1 February 2016 The interview was conducted by Tomoko Hatakeyama in Tokyo on 26 January 2016 Yomiuri

Money market. Alexander Mukha

Currency Market and Banking System: Pressure of adverse factors Alexander Mukha 219 Summary In 2013, Belarus faced a marked deterioration of external terms of trade, which brought about export cuts, drops

Currency Market and Banking System: Pressure of adverse factors Alexander Mukha 219 Summary In 2013, Belarus faced a marked deterioration of external terms of trade, which brought about export cuts, drops

KAPSAM Economic Briefing Series (2018/1) Exchange Rate Fluctuations and Projections

Exchange Rate Fluctuations and Projections") Exchange Rate Fluctuations and Projections www.kapsam.org.tr In this economic brief, KAPSAM economy unit assess recent exchange rate fluctuations in a wider perspective, makes an analysis on the root-causes

Exchange Rate Fluctuations and Projections www.kapsam.org.tr In this economic brief, KAPSAM economy unit assess recent exchange rate fluctuations in a wider perspective, makes an analysis on the root-causes

In our recent discussion of the Common Market we stated that. economic and political factors often are just as important as military

Draft of January lu, 1963 Speech for Mr. Kimbrel on balance of payments deficits at I t, Gordon In our recent discussion of the Common Market we stated that economic and political factors often are just

Draft of January lu, 1963 Speech for Mr. Kimbrel on balance of payments deficits at I t, Gordon In our recent discussion of the Common Market we stated that economic and political factors often are just

THE LEBANESE ECONOMY IN 2016 BYBLOS BANK ECONOMIC RESEARCH AND ANALYSIS DEPARTMENT

THE LEBANESE ECONOMY IN 2016 BYBLOS BANK ECONOMIC RESEARCH AND ANALYSIS DEPARTMENT ECONOMIC ACTIVITY Economic activity in Lebanon remained below potential in 2016, in line with the previous five years.

THE LEBANESE ECONOMY IN 2016 BYBLOS BANK ECONOMIC RESEARCH AND ANALYSIS DEPARTMENT ECONOMIC ACTIVITY Economic activity in Lebanon remained below potential in 2016, in line with the previous five years.

ASSOCIATION OF BANKS IN LEBANON. Indicators of Economic Activity (million USD unless otherwise mentioned)

") Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: September / October 07 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit; BDL=

Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: September / October 07 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit; BDL=

BOARDS OF GOVERNORS 2003 ANNUAL MEETINGS DUBAI, UNITED ARAB EMIRATES

BOARDS OF GOVERNORS 2003 ANNUAL MEETINGS DUBAI, UNITED ARAB EMIRATES WORLD BANK GROUP INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL FINANCE CORPORATION INTERNATIONAL DEVELOPMENT ASSOCIATION

BOARDS OF GOVERNORS 2003 ANNUAL MEETINGS DUBAI, UNITED ARAB EMIRATES WORLD BANK GROUP INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL FINANCE CORPORATION INTERNATIONAL DEVELOPMENT ASSOCIATION

Economic Survey of Latin America and the Caribbean CHILE. 1. General trends. 2. Economic policy

Economic Survey of Latin America and the Caribbean 2017 1 CHILE 1. General trends In 2016 the Chilean economy grew at a slower rate (1.6%) than in 2015 (2.3%), as the drop in investment and exports outweighed

Economic Survey of Latin America and the Caribbean 2017 1 CHILE 1. General trends In 2016 the Chilean economy grew at a slower rate (1.6%) than in 2015 (2.3%), as the drop in investment and exports outweighed

Openness in goods and financial markets. Chapter 18

Openness in goods and financial markets Chapter 18 Illustration: exchange between the US and Ethiopia See videos: Black Gold and Life and Debt US goods market Electronics exports (+); coffee imports from

Openness in goods and financial markets Chapter 18 Illustration: exchange between the US and Ethiopia See videos: Black Gold and Life and Debt US goods market Electronics exports (+); coffee imports from

Monetary Policy in the Wake of the Crisis Olivier Blanchard

Monetary Policy in the Wake of the Crisis Olivier Blanchard Let me start with my bottom line: Before the crisis, mainstream economists and policymakers had converged on a beautiful construction for monetary

Monetary Policy in the Wake of the Crisis Olivier Blanchard Let me start with my bottom line: Before the crisis, mainstream economists and policymakers had converged on a beautiful construction for monetary

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

SUMMARY OF THE DOCTORAL THESIS PUBLIC DEBT AND SOCIAL AND ECONOMIC IMPLICATIONS

SUMMARY OF THE DOCTORAL THESIS PUBLIC DEBT AND SOCIAL AND ECONOMIC IMPLICATIONS The triggering of the global economic and financial crisis generated a sudden increase of sovereign debt in many countries

SUMMARY OF THE DOCTORAL THESIS PUBLIC DEBT AND SOCIAL AND ECONOMIC IMPLICATIONS The triggering of the global economic and financial crisis generated a sudden increase of sovereign debt in many countries

GLOBAL FINANCIAL SYSTEM. Lecturer Oleg Deev

GLOBAL FINANCIAL SYSTEM Lecturer Oleg Deev oleg@mail.muni.cz Contents Concept of the global financial system Evolution of the global financial system International reserve currency Post-Bretton Woods global

GLOBAL FINANCIAL SYSTEM Lecturer Oleg Deev oleg@mail.muni.cz Contents Concept of the global financial system Evolution of the global financial system International reserve currency Post-Bretton Woods global

Monetary and Foreign Exchange Policy of the National Bank of Moldova for 2004

Monetary and Foreign Exchange Policy of the National Bank of Moldova for 2004 The monetary and foreign exchange policy and the main directions of the NBM activity set with the view to fulfilling the basic

Monetary and Foreign Exchange Policy of the National Bank of Moldova for 2004 The monetary and foreign exchange policy and the main directions of the NBM activity set with the view to fulfilling the basic

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 5,

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 5, 2014 http://ijecm.co.uk/ ISSN 2348 0386 Α FINANCIAL ANALYSIS OF PUBLIC FINANCES IN GREECE Markou, Angelos Technological

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 5, 2014 http://ijecm.co.uk/ ISSN 2348 0386 Α FINANCIAL ANALYSIS OF PUBLIC FINANCES IN GREECE Markou, Angelos Technological

Atradius Country Report

Atradius Country Report Hungary March 2012 Budapest Overview General information Most important sectors (% of GDP, 2011) Capital: Budapest Services: 60 % Government type: Parliamentary democracy Industry/mining:

Atradius Country Report Hungary March 2012 Budapest Overview General information Most important sectors (% of GDP, 2011) Capital: Budapest Services: 60 % Government type: Parliamentary democracy Industry/mining:

Suggested Solutions to Problem Set 4

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Rebalancing Toward Sustainable Growth. Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City

Rebalancing Toward Sustainable Growth Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City The Rotary Club of Des Moines and the Greater Des Moines Partnership Des

Rebalancing Toward Sustainable Growth Thomas M. Hoenig President and Chief Executive Officer Federal Reserve Bank of Kansas City The Rotary Club of Des Moines and the Greater Des Moines Partnership Des

Interest and Equity. Chapter What is Interest?

Chapter 6 Interest and Equity This chapter analyzes how money supply is affected by the introduction of interest. It is assumed that bank loans, deposits and discount loans are no longer interest-free,

Chapter 6 Interest and Equity This chapter analyzes how money supply is affected by the introduction of interest. It is assumed that bank loans, deposits and discount loans are no longer interest-free,

Chapter 21 The International Monetary System: Past, Present, and Future

Chapter 21 The International Monetary System: Past, Present, and Future "...for the international economy the existence of a well-functioning financial system assuring efficient exchange is as important

Chapter 21 The International Monetary System: Past, Present, and Future "...for the international economy the existence of a well-functioning financial system assuring efficient exchange is as important

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference Commodities,

Svein Gjedrem: From oil and gas to financial assets Norway s Government Pension Fund Global Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the conference Commodities,

The Future of Thai Fund Management Industry

The Future of Thai Fund Management Industry Speech by Mr. Thirachai Phuvanat naranubala, Secretary-General of Securities and Exchange Commission On The Post / Lipper Thailand Fund Award for 2003 At Dusit

The Future of Thai Fund Management Industry Speech by Mr. Thirachai Phuvanat naranubala, Secretary-General of Securities and Exchange Commission On The Post / Lipper Thailand Fund Award for 2003 At Dusit

Lars Nyberg: Developments in the property market

Lars Nyberg: Developments in the property market Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at Fastighetsvärlden (Swedish newspaper), Stockholm, 30 May 2007. * * * I would like

Lars Nyberg: Developments in the property market Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at Fastighetsvärlden (Swedish newspaper), Stockholm, 30 May 2007. * * * I would like

7. Monetary Trends and Policy

Quarterly Monitor No. 36 January March 214 47 7. Monetary and Policy Inflation has been stable for the past two quarters at about the lower level of the target corridor but the National Bank of Serbia

Quarterly Monitor No. 36 January March 214 47 7. Monetary and Policy Inflation has been stable for the past two quarters at about the lower level of the target corridor but the National Bank of Serbia

ASSOCIATION OF BANKS IN LEBANON. 5- Balance of Trade in Goods = (4) - (3) (16,738) (2,100) (1,591) n.a.

- (3) (16,738) (2,100) (1,591) n.a.") Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: August / September 08 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit; BDL=

Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: August / September 08 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit; BDL=

ASSOCIATION OF BANKS IN LEBANON. 5- Balance of Trade in Goods = (4) - (3) (16,738) (1,401) (2,100) (1,591)

- (3) (16,738) (1,401) (2,100) (1,591)") Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: August / September 08 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit; BDL=

Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: August / September 08 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit; BDL=

Middle East - Developments in Restructuring

8 Clifford Street London W1S 2LQ F: +44.20.7851.6000 Middle East - Developments in Restructuring 1. MIDDLE EAST RESTRUCTURINGS AND REFORM OF INSOLVENCY LEGISLATION 2 2. THE FEDERAL LAWS OF THE UNITED ARAB

8 Clifford Street London W1S 2LQ F: +44.20.7851.6000 Middle East - Developments in Restructuring 1. MIDDLE EAST RESTRUCTURINGS AND REFORM OF INSOLVENCY LEGISLATION 2 2. THE FEDERAL LAWS OF THE UNITED ARAB

Total Assets. Bank's Financial Analysis

Bank's Financial Analysis Political crises in Lebanon and the Arab region during the last years had largely affected all financial and economic indicators. Therefore, the bank works on maintaining the

Bank's Financial Analysis Political crises in Lebanon and the Arab region during the last years had largely affected all financial and economic indicators. Therefore, the bank works on maintaining the

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes)

") IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

7/29/2017. Learning Objectives. The International Monetary and Financial Environment. Currencies and Exchange Rates

Learning Objectives The International Monetary and Financial Environment International Business: The New Realities, 4 th Edition by Cavusgil, Knight, and Riesenberger 9.1 Learn about exchange rates and

Learning Objectives The International Monetary and Financial Environment International Business: The New Realities, 4 th Edition by Cavusgil, Knight, and Riesenberger 9.1 Learn about exchange rates and

PART THREE. Answers to End-of-Chapter Questions and Problems

PART THREE Answers to End-of-Chapter Questions and Problems Mishkin Instructor s Manual for The Economics of Money, Banking, and Financial Markets, Eleventh Edition 58 Chapter 1 ANSWERS TO QUESTIONS 1.

PART THREE Answers to End-of-Chapter Questions and Problems Mishkin Instructor s Manual for The Economics of Money, Banking, and Financial Markets, Eleventh Edition 58 Chapter 1 ANSWERS TO QUESTIONS 1.

The Economic Letter December 2010

ASSOCIATION OF BANKS IN LEBANON Research & Statistics Department The Economic Letter December 2010 Summary: Despite the deceleration in the activities of a number of economic sectors in the fourth quarter,

ASSOCIATION OF BANKS IN LEBANON Research & Statistics Department The Economic Letter December 2010 Summary: Despite the deceleration in the activities of a number of economic sectors in the fourth quarter,

China CHINA S RISING DEBT: WHEN DOES A BUBBLE BECOME TROUBLE?

PRICE POINT October 2016 Timely intelligence and analysis for our clients. China CHINA S RISING DEBT: WHEN DOES A BUBBLE BECOME TROUBLE? KEY POINTS Chris Kushlis Fixed Income Sovereign Analyst, Asian Markets

PRICE POINT October 2016 Timely intelligence and analysis for our clients. China CHINA S RISING DEBT: WHEN DOES A BUBBLE BECOME TROUBLE? KEY POINTS Chris Kushlis Fixed Income Sovereign Analyst, Asian Markets

A dollar crisis could be around the corner

Part 1-2014 the year of truth! A US dollar crisis, interest rates spiking and worldwide debt growing out of control and gold and silver through the roof! A dollar crisis could be around the corner The

Part 1-2014 the year of truth! A US dollar crisis, interest rates spiking and worldwide debt growing out of control and gold and silver through the roof! A dollar crisis could be around the corner The

10/30/2018. Chapter 17. The Money Supply Process. Preview. Learning Objectives

Chapter 17 The Money Supply Process Preview This chapter provides an overview of how the banking system create and describes the basic principles of the money supply creation process Learning Objectives

Chapter 17 The Money Supply Process Preview This chapter provides an overview of how the banking system create and describes the basic principles of the money supply creation process Learning Objectives

OPINION ON FISCAL STRATEGY DRAFT FOR 2015 WITH PROJECTIONS FOR 2016 AND Summary

Republic of Serbia FISCAL COUNCIL OPINION ON FISCAL STRATEGY DRAFT FOR 2015 WITH PROJECTIONS FOR 2016 AND 2017 Summary The programme presented in the Fiscal Strategy could bring about a recovery of public

Republic of Serbia FISCAL COUNCIL OPINION ON FISCAL STRATEGY DRAFT FOR 2015 WITH PROJECTIONS FOR 2016 AND 2017 Summary The programme presented in the Fiscal Strategy could bring about a recovery of public

Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015

, 8 November 2015") Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015 Politis: The main goal of the programme is to restore confidence in Cyprus. Is this mission complete?

Interview with Klaus Regling, Managing Director, ESM Published in Politis (Cyprus), 8 November 2015 Politis: The main goal of the programme is to restore confidence in Cyprus. Is this mission complete?

By! O Wog wja.l~j~j~j 9PHXS Y9PY'

isclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized r f-:; 7k71 By! O Wog wja.l~j~j~j 1!!~~ o~~~o= 9PHXS Y9PY' 1!! v-i! Xxt 4x 1!!~~~c m4a WSB My

isclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized r f-:; 7k71 By! O Wog wja.l~j~j~j 1!!~~ o~~~o= 9PHXS Y9PY' 1!! v-i! Xxt 4x 1!!~~~c m4a WSB My

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Notes on Hyman Minsky s Financial Instability Hypothesis

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

SEB MERCHANT BANKING COUNTRY RISK ANALYSIS 28 September 2016

SEB MERCHANT BANKING COUNTRY RISK ANALYSIS 28 September 2016 Higher foreign reserves and lower financing needs following the debt restructuring in 2015 have reduced external vulnerability. In addition,

SEB MERCHANT BANKING COUNTRY RISK ANALYSIS 28 September 2016 Higher foreign reserves and lower financing needs following the debt restructuring in 2015 have reduced external vulnerability. In addition,

Crisis, Threats and Ways Out for the Greek Economy

Cyprus Economic Policy Review, Vol. 4, No. 1, pp. 89-96 (2010) 1450-4561 Crisis, Threats and Ways Out for the Greek Economy Nicos Christodoulakis Athens University of Economics and Business Abstract The

Cyprus Economic Policy Review, Vol. 4, No. 1, pp. 89-96 (2010) 1450-4561 Crisis, Threats and Ways Out for the Greek Economy Nicos Christodoulakis Athens University of Economics and Business Abstract The

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

To fully understand the dramatic turns in the financial markets that

01_chap_murphy.qxd 10/24/03 2:06 PM Page 1 CHAPTER 1 A Review of the 1980s To fully understand the dramatic turns in the financial markets that started in 1980, it s necessary to know something about the

01_chap_murphy.qxd 10/24/03 2:06 PM Page 1 CHAPTER 1 A Review of the 1980s To fully understand the dramatic turns in the financial markets that started in 1980, it s necessary to know something about the

ASSOCIATION OF BANKS IN LEBANON. Indicators of Economic Activity (million USD unless otherwise mentioned)

") Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: December 2016 / January 2017 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit;

Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: December 2016 / January 2017 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit;

Outlook for the Chilean Economy

Outlook for the Chilean Economy Jorge Marshall, Vice-President of the Board, Central Bank of Chile. Address to the Fifth Annual Latin American Banking Conference, Salomon Smith Barney, New York, March

Outlook for the Chilean Economy Jorge Marshall, Vice-President of the Board, Central Bank of Chile. Address to the Fifth Annual Latin American Banking Conference, Salomon Smith Barney, New York, March

Monetary Sector: Anchor of the Lebanese Economy

BLOMINVEST BANK December 12, 2015 Contact Information Research Assistant: Lana Saadeh lana.saadeh@blominvestbank.com Head of Research: Marwan Mikhael marwan.mikhael@blominvestbank.com Research Department

BLOMINVEST BANK December 12, 2015 Contact Information Research Assistant: Lana Saadeh lana.saadeh@blominvestbank.com Head of Research: Marwan Mikhael marwan.mikhael@blominvestbank.com Research Department

Economic History of the US

Economic History of the US Depression and the World Wars, 1914-46 Lecture #3 Peter Allen Econ 120 Great Depression, 1929-1941 Largest economic contraction in US history Front-loaded collapse that took

Economic History of the US Depression and the World Wars, 1914-46 Lecture #3 Peter Allen Econ 120 Great Depression, 1929-1941 Largest economic contraction in US history Front-loaded collapse that took

Money, Banking, and the Financial System CHAPTER

Money, Banking, and the Financial System 12 CHAPTER Money: What Is It and How Did It Come to Be? Money: A Definition To the layperson, the words income, credit, and wealth are synonyms for money. In each

Money, Banking, and the Financial System 12 CHAPTER Money: What Is It and How Did It Come to Be? Money: A Definition To the layperson, the words income, credit, and wealth are synonyms for money. In each

Bank of Palestine. October 10, 2012 Recommendation: Buy. Recent Developments and Highlights

Bank of Palestine Recent Developments and Highlights We reiterate our buy recommendation at a price objective of USD 2.89. Bank of Palestine was able to accelerate growth of credit facilities during one

Bank of Palestine Recent Developments and Highlights We reiterate our buy recommendation at a price objective of USD 2.89. Bank of Palestine was able to accelerate growth of credit facilities during one

the Federal Reserve System

CHAPTER 14 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 14.1 What Is Money, and Why Do We Need It? (pages 456 459) Define money and discuss the four functions of

CHAPTER 14 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 14.1 What Is Money, and Why Do We Need It? (pages 456 459) Define money and discuss the four functions of

BOOMS & BUSTS. Supplementary lesson 4. Includes: Student lessons. Teacher notes & answers

BOOMS & BUSTS Supplementary lesson 4 Includes: Student lessons. Teacher notes & answers Teacher Notes: BOOMS & BUSTS History of the Sharemarket: Booms & busts Introduction: The purpose of this unit is

BOOMS & BUSTS Supplementary lesson 4 Includes: Student lessons. Teacher notes & answers Teacher Notes: BOOMS & BUSTS History of the Sharemarket: Booms & busts Introduction: The purpose of this unit is

Iceland s crisis and recovery: are there lessons for the eurozone and its member countries?

Central Bank of Iceland Iceland s crisis and recovery: are there lessons for the eurozone and its member countries? Már Guðmundsson Governor, Central Bank of Iceland Levy Institute conference, Athens,

Central Bank of Iceland Iceland s crisis and recovery: are there lessons for the eurozone and its member countries? Már Guðmundsson Governor, Central Bank of Iceland Levy Institute conference, Athens,

Lebanon: a macro-economic framework

Lebanon: a macro-economic framework This paper is intended to present a synthetic overview of the Lebanese economic situation and to assess the main options of macro-economic policies. Basic economic trends

Lebanon: a macro-economic framework This paper is intended to present a synthetic overview of the Lebanese economic situation and to assess the main options of macro-economic policies. Basic economic trends

A Precondition for Monetary Order

CREATING A STABLE MONETARY ORDER Vaclav Klaus A Precondition for Monetary Order A stable monetary order is for me both a goal and an instrument for achieving other goals. My crucial message is the following:

CREATING A STABLE MONETARY ORDER Vaclav Klaus A Precondition for Monetary Order A stable monetary order is for me both a goal and an instrument for achieving other goals. My crucial message is the following:

ASSOCIATION OF BANKS IN LEBANON Sep-2017 Oct-2017 Nov Building permits (000 m 2 ) 12, ,

12, ,") Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: November / December 07 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit; BDL=

Key Indicators ASSOCIATION OF BANKS IN LEBANON Issue: November / December 07 LBP= Lebanese Pound; USD= US Dollar; FC= Foreign Currency; ( ) indicates a negative number; CD= Certificate of Deposit; BDL=

Global Outlook and Policy Challenges. Olivier Blanchard Economic Counsellor Research Department

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

PRICING OF THE PRODUCT

PRICING OF THE PRODUCT L E A R N I N G O B J E C T I V E S After completing this chapter you should be able to: 1. understand the concept and function of front office. 2. describe the concept and function

PRICING OF THE PRODUCT L E A R N I N G O B J E C T I V E S After completing this chapter you should be able to: 1. understand the concept and function of front office. 2. describe the concept and function

IN THIS ISSUE ECONOMY

IN THIS ISSUE ECONOMY Coincident Indicator Improves by 5.8% Y-O-Y in October 2013 Fiscal Deficit Widened by 32% to USD 3,519 Million in the First Ten Months of 2013 Trade Deficit Goes up on a Yearly Basis

IN THIS ISSUE ECONOMY Coincident Indicator Improves by 5.8% Y-O-Y in October 2013 Fiscal Deficit Widened by 32% to USD 3,519 Million in the First Ten Months of 2013 Trade Deficit Goes up on a Yearly Basis

Market Resiliency: Evidence from Money Market Mutual Fund Reform

Market Resiliency: Evidence from Money Market Mutual Fund Reform Anna Paulson Senior Vice President, Associate Director of Research, and Director of Financial Markets Federal Reserve Bank of Chicago People

Market Resiliency: Evidence from Money Market Mutual Fund Reform Anna Paulson Senior Vice President, Associate Director of Research, and Director of Financial Markets Federal Reserve Bank of Chicago People

Sep 18, 2015 ECONOMY. IIF revises Lebanon s GDP growth rate down to 1.1% in 2015

ECONOMY IIF revises Lebanon s GDP growth rate down to 1.1% in 2015 IIF states that economic activity remains weak, reflecting policy inaction amid a protracted political crisis and rising regional insecurity.

ECONOMY IIF revises Lebanon s GDP growth rate down to 1.1% in 2015 IIF states that economic activity remains weak, reflecting policy inaction amid a protracted political crisis and rising regional insecurity.

Labour s cost-of-living contract with hardworking Britain 1

Labour s cost-of-living contract with hardworking Britain 1 Foreword Ed Miliband The record of this government is simple: hardworking Britain is worse off month after month, year after year. Since David

Labour s cost-of-living contract with hardworking Britain 1 Foreword Ed Miliband The record of this government is simple: hardworking Britain is worse off month after month, year after year. Since David

Module 19 Equilibrium in the Aggregate Demand Aggregate Supply Model

What you will learn in this Module: The difference between short-run and long-run macroeconomic equilibrium The causes and effects of demand shocks and supply shocks How to determine if an economy is experiencing

What you will learn in this Module: The difference between short-run and long-run macroeconomic equilibrium The causes and effects of demand shocks and supply shocks How to determine if an economy is experiencing

What you should have learnt so far:

What you should have learnt so far: What was the Wall Street Crash? What were the causes of the Wall Street Crash? What you re going to learn this week and next: What was the Great Depression? Why did

What you should have learnt so far: What was the Wall Street Crash? What were the causes of the Wall Street Crash? What you re going to learn this week and next: What was the Great Depression? Why did

Abstract. The political vacuum extending over four months now is weighing down on investors confidence

BLOMINVEST BANK Sept. 21 st 2018 Contact Information Research Analyst: Rouba Chbeir rouba.chbeir@blominvestbank.com Head of Research: Marwan Mikhael marwan.mikhael@blominvestbank.com Research Department

BLOMINVEST BANK Sept. 21 st 2018 Contact Information Research Analyst: Rouba Chbeir rouba.chbeir@blominvestbank.com Head of Research: Marwan Mikhael marwan.mikhael@blominvestbank.com Research Department

5 Domestic and External Debt

flows in billion Rs FY11 FY12 FY13 FY14 FY15 FY16 FY17 percent of GDP 5 Domestic and External Debt 5.1 Overview Gross public debt-to-gdp ratio improved marginally to 67.2 percent by end-june 217 from 67.6

flows in billion Rs FY11 FY12 FY13 FY14 FY15 FY16 FY17 percent of GDP 5 Domestic and External Debt 5.1 Overview Gross public debt-to-gdp ratio improved marginally to 67.2 percent by end-june 217 from 67.6

Has US Debt Reached A Tipping Point?

Has US Debt Reached A Tipping Point? October 28, 2016 by Urban Carmel of The Fat Pitch Summary: Investors have become very concerned about excessive debt in the US. The worry is that current leverage has

Has US Debt Reached A Tipping Point? October 28, 2016 by Urban Carmel of The Fat Pitch Summary: Investors have become very concerned about excessive debt in the US. The worry is that current leverage has

Chapter 14. The Money Supply Process

Chapter 14 The Money Supply Process Three Players in the Money Supply Process Central bank (Federal Reserve System) Banks (depository institutions; financial intermediaries) Depositors (individuals and

Chapter 14 The Money Supply Process Three Players in the Money Supply Process Central bank (Federal Reserve System) Banks (depository institutions; financial intermediaries) Depositors (individuals and

The Problem of Widening Current Account Deficit of India

The Problem of Widening Current Account Deficit of India Article by Subho Mukherjee (2013) Source: http://www.economicsdiscussion.net/india/the-problem-of-widening-current-accountdeficit-of-india/10909

The Problem of Widening Current Account Deficit of India Article by Subho Mukherjee (2013) Source: http://www.economicsdiscussion.net/india/the-problem-of-widening-current-accountdeficit-of-india/10909

LEBANON WEEKLY REPORT

ECONOMY Gross public debt increased by a yearly 10% in April 2014 to reach USD 64.8 billion of which 60% in LBP and 40% in foreign currency. Net public debt reaches USD 54.6 billion at end of April 2014

ECONOMY Gross public debt increased by a yearly 10% in April 2014 to reach USD 64.8 billion of which 60% in LBP and 40% in foreign currency. Net public debt reaches USD 54.6 billion at end of April 2014

Poland: Massive IMF Lending Prevents a Major Banking Crisis, but Longer Term Risks Remain

Poland: Massive IMF Lending Prevents a Major Banking Crisis, but Longer Term Risks Remain Daniel McGovern January 30, 2010 Poland escaped a full-scale banking crisis and severe recession in 2009, thanks

Poland: Massive IMF Lending Prevents a Major Banking Crisis, but Longer Term Risks Remain Daniel McGovern January 30, 2010 Poland escaped a full-scale banking crisis and severe recession in 2009, thanks

Analysis and Action Why is Inflation so Low?

Analysis and Action Why is Inflation so Low? By Tom Slefinger, Senior Vice President, Director of Institutional Fixed Income Sales at Balance Sheet Solutions, LLC. Tom can be reached at tom.slefinger@balancesheetsolutions.org.

Analysis and Action Why is Inflation so Low? By Tom Slefinger, Senior Vice President, Director of Institutional Fixed Income Sales at Balance Sheet Solutions, LLC. Tom can be reached at tom.slefinger@balancesheetsolutions.org.

Overview. I. Monetary Statistics II. Money Creation III. Summary. Jan Gottschalk TAOLAM

Monetary Statistics & Money Supply Overview Jan Gottschalk TAOLAM This training material is the property of the IMF Singapore Regional Training Institute (STI) and is intended for the use in STI courses.

Monetary Statistics & Money Supply Overview Jan Gottschalk TAOLAM This training material is the property of the IMF Singapore Regional Training Institute (STI) and is intended for the use in STI courses.

On your mark. UBS Investor Watch. a b. 100 days into the new administration, investors are poised to act

UBS Investor Watch Analyzing investor sentiment and behavior / 2Q 2017 On your mark 100 days into the new administration, investors are poised to act a b As investors assess the administration s first

UBS Investor Watch Analyzing investor sentiment and behavior / 2Q 2017 On your mark 100 days into the new administration, investors are poised to act a b As investors assess the administration s first

Policy Note 2000/6 Drowning In Debt

Policy Note 2000/6 Drowning In Debt Wynne Godley The U.S. expansion has been driven to an unusual extent by falling personal saving and rising borrowing by the private sector. If this process goes into

Policy Note 2000/6 Drowning In Debt Wynne Godley The U.S. expansion has been driven to an unusual extent by falling personal saving and rising borrowing by the private sector. If this process goes into

The fiscal response to the currency crisis and the challenges ahead - Korea s experience

The fiscal response to the currency crisis and the challenges ahead - Korea s experience Chung Kyu Yung 1 1. Fiscal management and its impact after the currency crisis Fiscal position before the currency

The fiscal response to the currency crisis and the challenges ahead - Korea s experience Chung Kyu Yung 1 1. Fiscal management and its impact after the currency crisis Fiscal position before the currency